Monday's Closing Market Stats

Volume

- NYSE volume 20% below its one-month average

- NASDAQ volume 20% below its one-month average

- VIX index: up to 5.44% to 17.24

Breadth

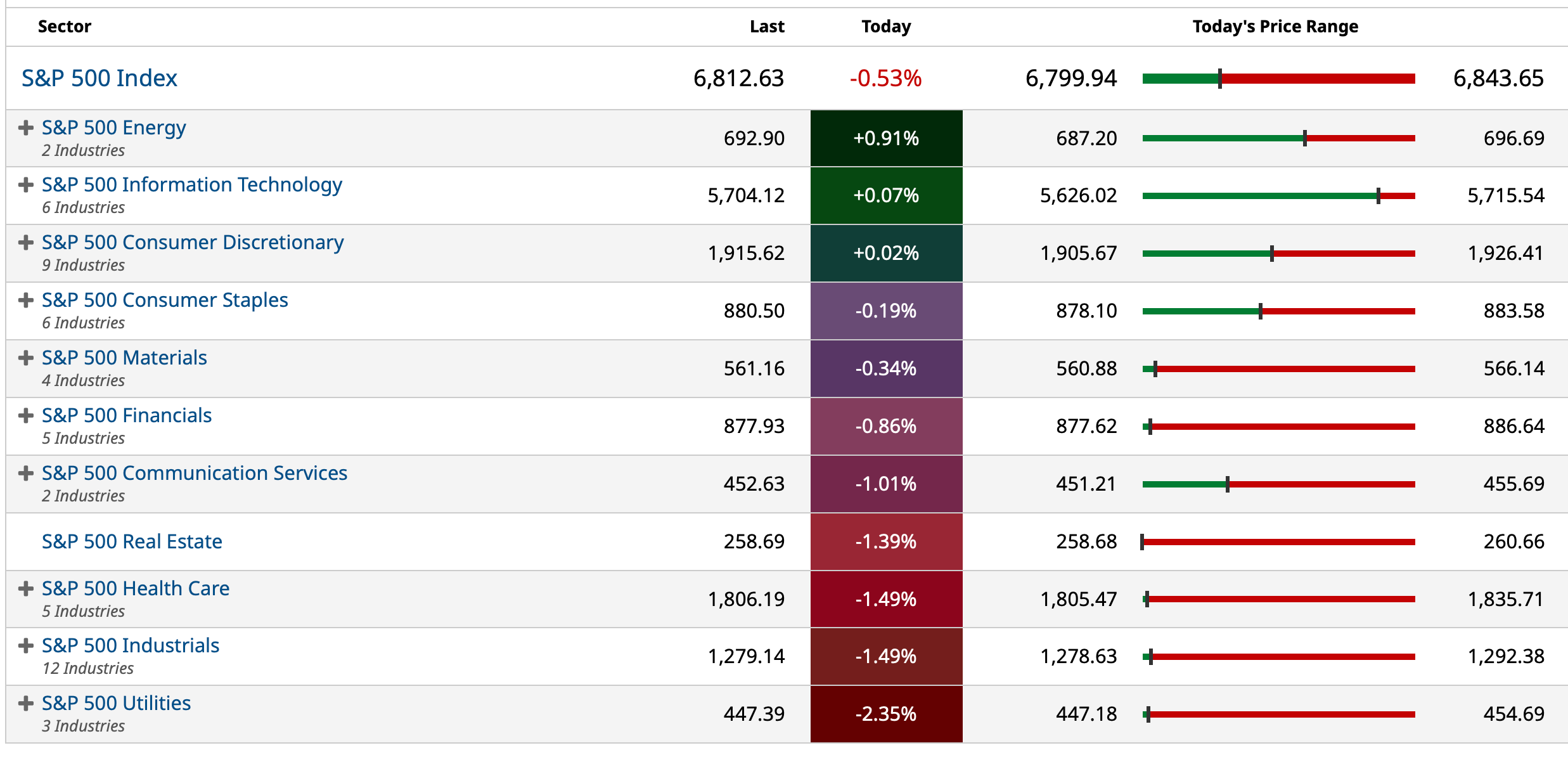

Sectors

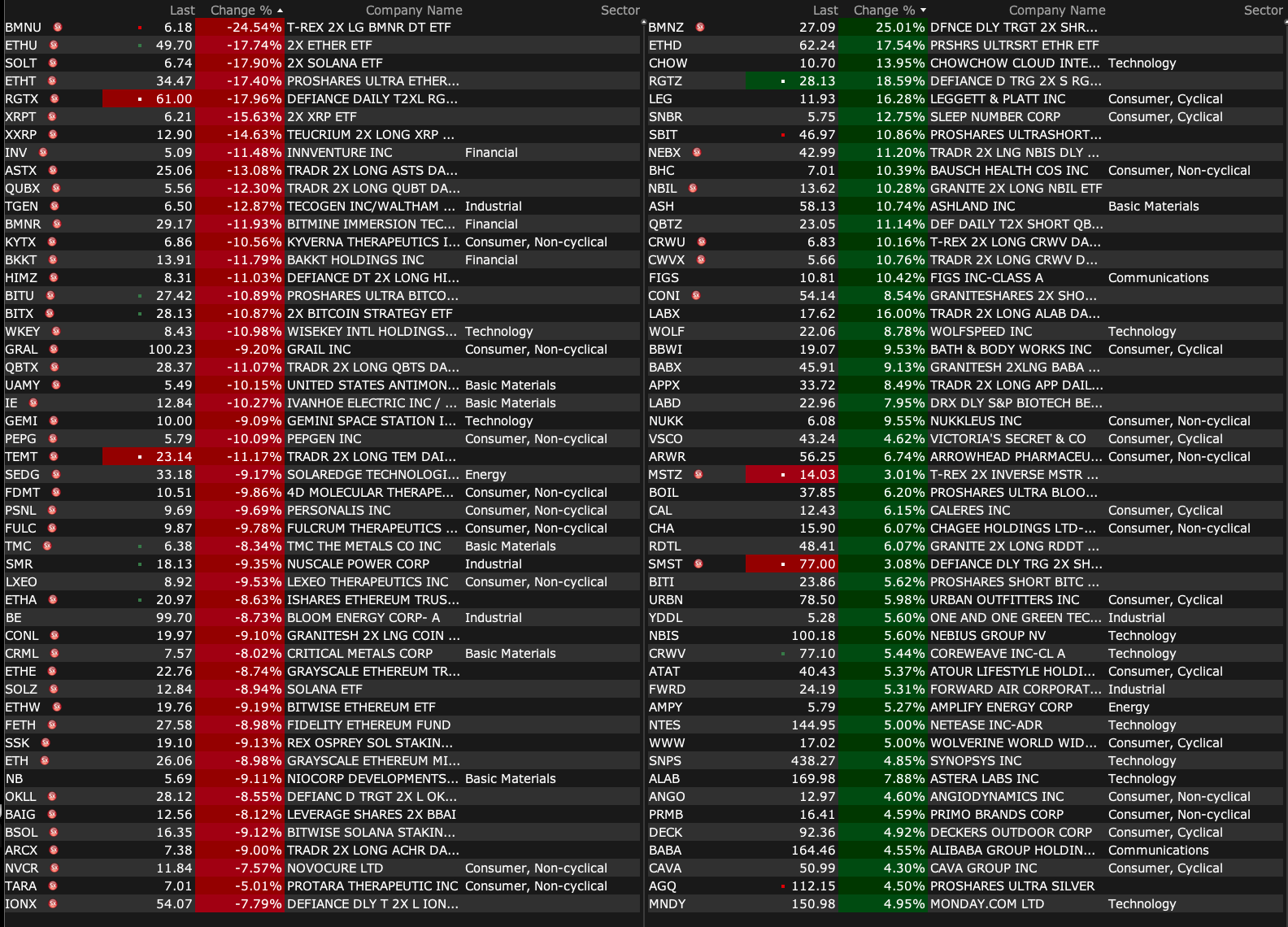

% Movers

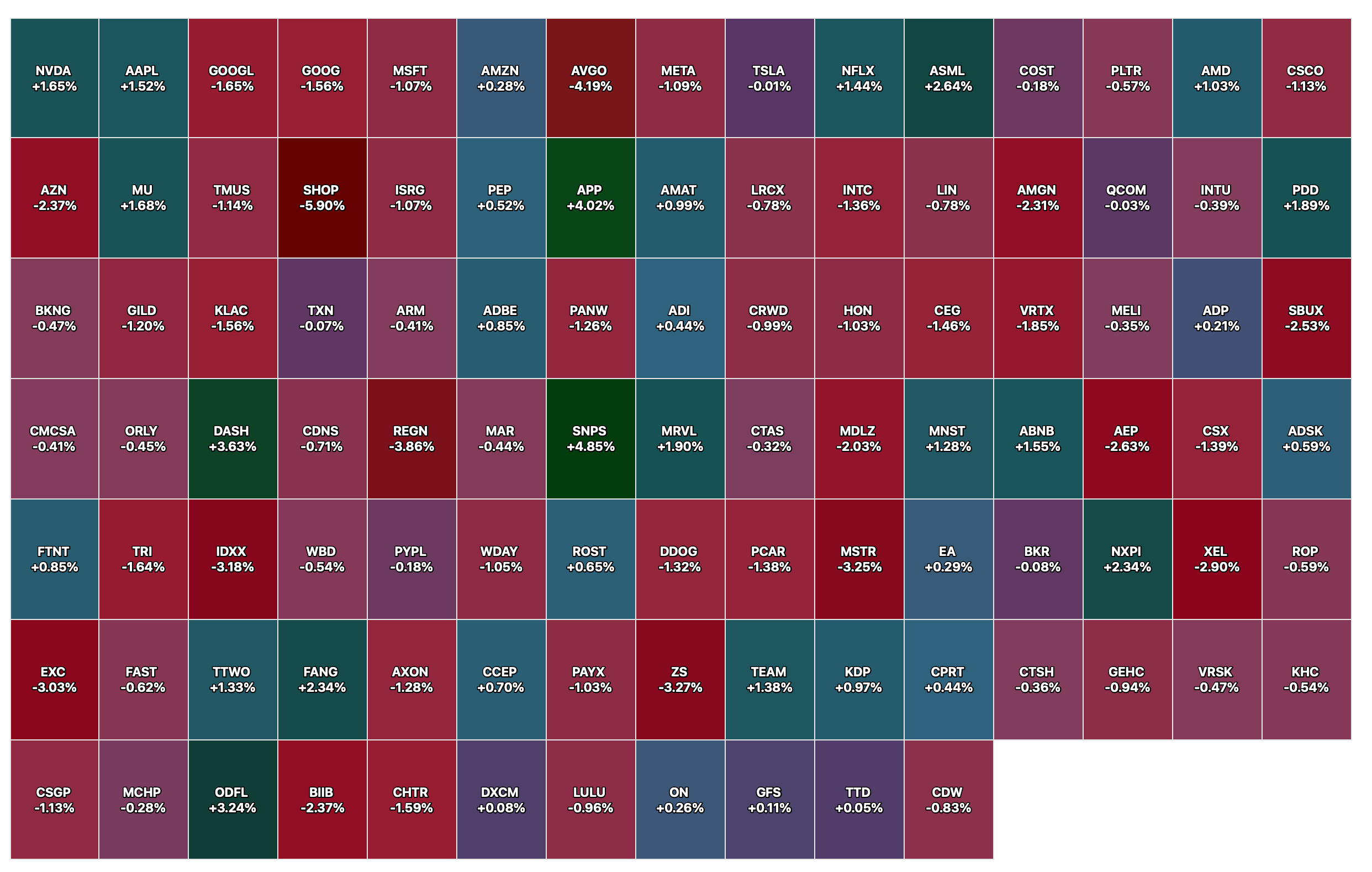

Nasdaq 100 Heat Map

BY Doug Kass · Dec 1, 2025, 4:42 PM EST

- NYSE volume 20% below its one-month average

- NASDAQ volume 20% below its one-month average

- VIX index: up to 5.44% to 17.24

BY Doug Kass · Dec 1, 2025, 4:42 PM EST

BY Doug Kass · Dec 1, 2025, 3:18 PM EST

I added to my Microsoft (MSFT) long at $487.13.

BY Doug Kass · Dec 1, 2025, 3:03 PM EST

With S&P cash -22 handles, I am taking in my index shorts:

* (SPY) $681.30

* (QQQ) $617.63

I plan to reshort strength, but this time I will restrict myself to selling index calls (as given VIX I take in premium).

BY Doug Kass · Dec 1, 2025, 2:24 PM EST

From Peter Boockvar:

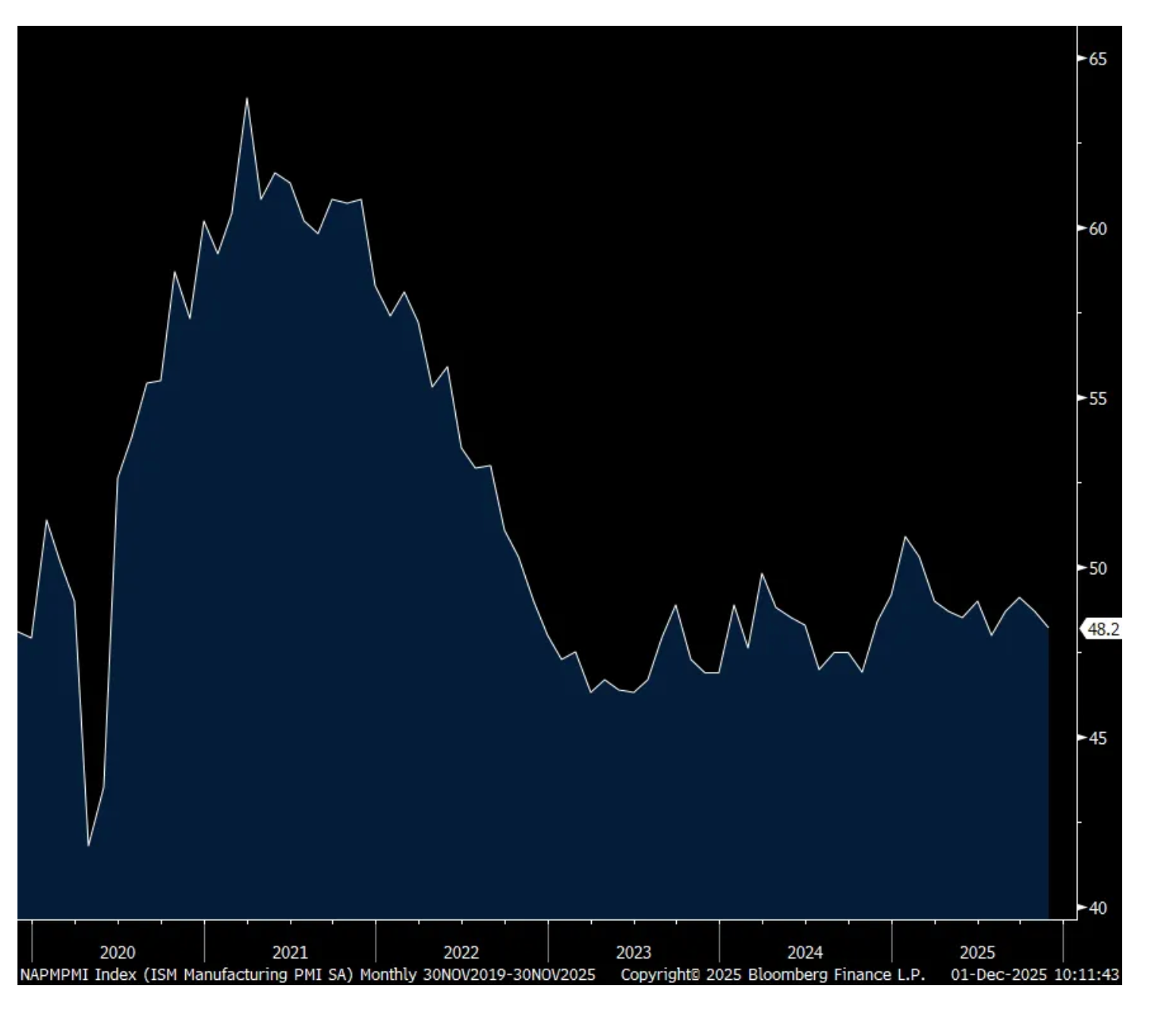

The November ISM manufacturing index remained in recession territory at 48.2 vs 48.7 in October and vs the estimate of 49. This index has been above 50 just twice since the Fall of 2022. New orders fell 2 pts to 47.4 and backlogs were down to 44 from 47.9. Inventories lifted by 3.1 pts but remained below 50 at 48.9. Customer inventories were well below 50 at 44.7, though up .8 pts m/o/m.

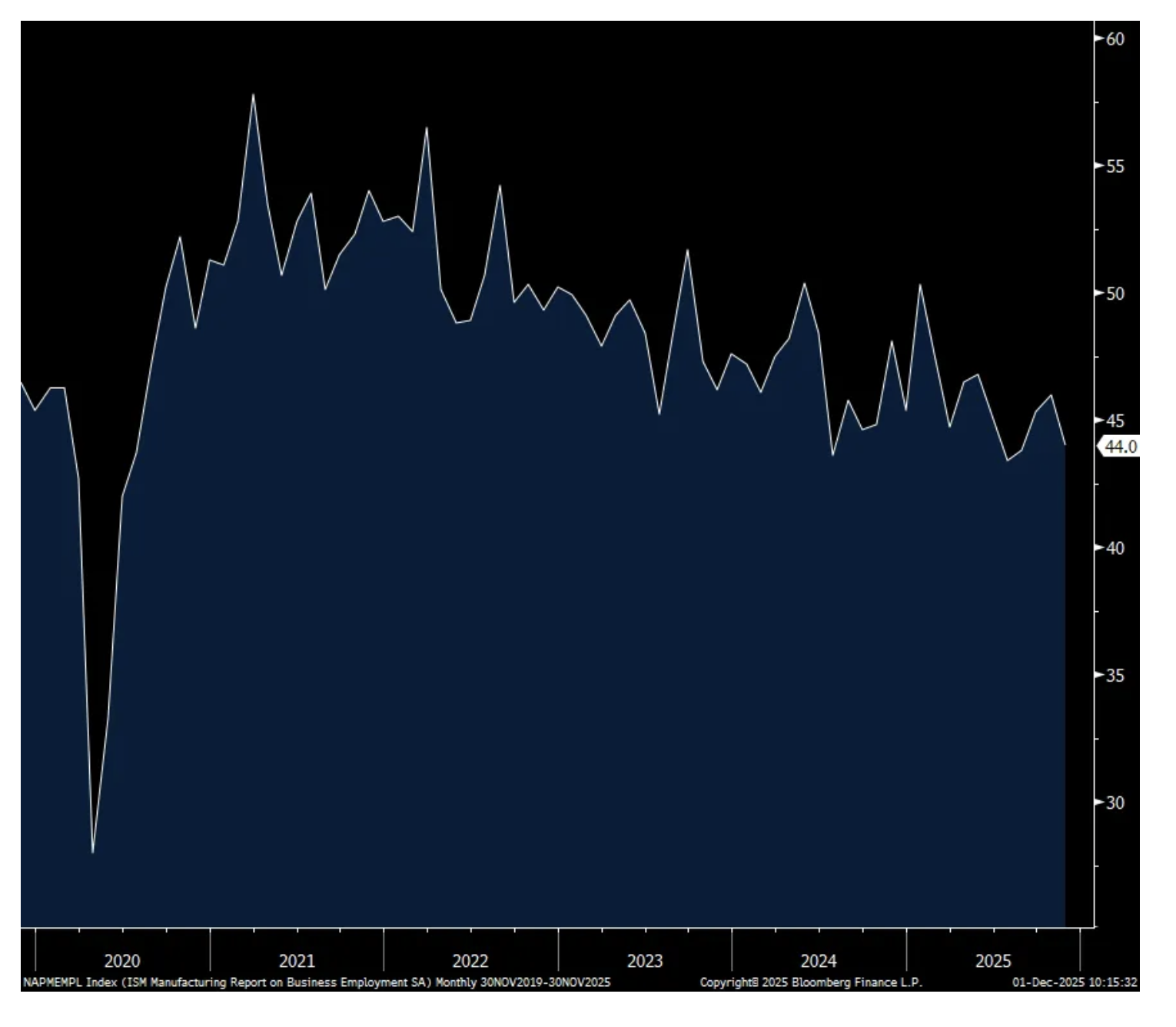

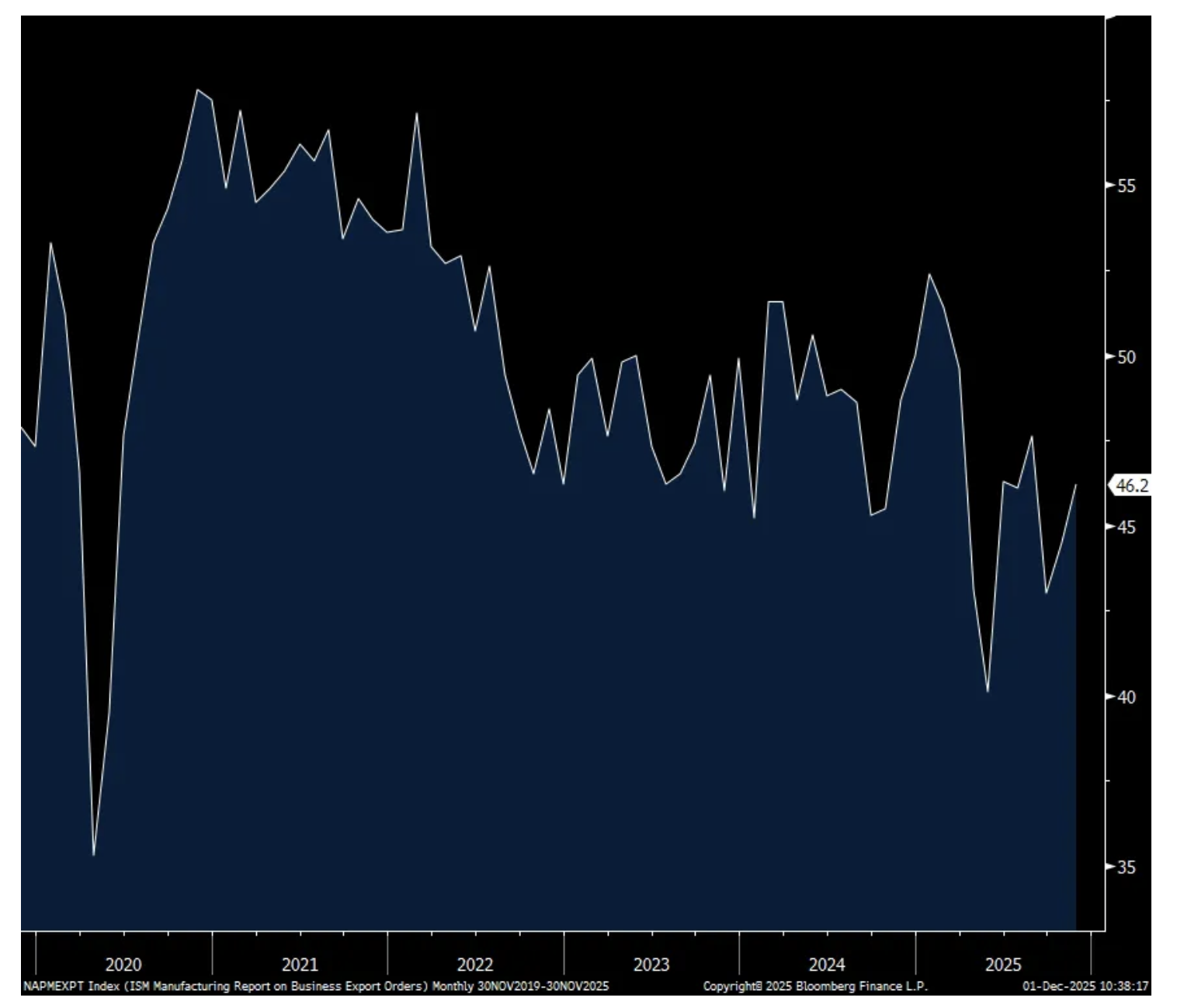

Employment was 44, down 2 pts and under 50 for the 10th straight month. Export orders at 46.2 was less than 50 for a 9th straight month. After three months above 50 (reflecting slower supply chains) supplier deliveries fell 4.9 pts to 49.3. Prices paid rose .5 pt to 58.5 but fell about 4 pts last month.

In terms of breadth, just 4 of 18 industries surveyed saw growth in November. That compares with 6 in October and 11 experienced a contraction vs 12 in the month before with the balance seeing no change.

I want to highlight this particular quote from a company in the transportation equipment space as it has been one of my tariff impact fears. There has been this simplistic view that higher US tariffs on the rest of the world will only encourage reshoring to the US without an offsetting consequence. While reshoring will happen to an extent, it didn’t occur to some that it makes US manufacturing less competitive when trying to sell things outside our borders that are made in the US. And instead, a US company that wants to sell things in Europe will make them in Europe. Want to sell into Asia, make it in Asia, etc… Because it’s now much cheaper to make things overseas that will be sold overseas. The bold below is mine.

“We are starting to institute more permanent changes due to the tariff environment. This includes reduction of staff, new guidance to shareholders, and development of additional offshore manufacturing that would have otherwise been for U.S. export.” (Transportation Equipment)

Overall with US exports, ISM said “Many panelists still report softer international orders tied to tariffs and ongoing uncertainty around US economic policy.”

With new orders, “For every positive comment about new orders, there were 1.2 comments expressing concern about near term demand, driven primarily by tariff costs and uncertainty.”

On employment, just 2 industries saw an increase in payrolls as “Companies continued to focus on accelerating staff reductions due to uncertain near to mid-term demand.”

ISM said this on inflation, “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods.”

Bottom line, US manufacturing is now about 3 years into a recession and the tariffs wars helped to extend this out. To remind, US manufacturing went into a recession in 2018 and 2019 due to that experience with tariffs that resulted in the Fed cutting interest rates in 2019 in response.

Below are more respondent comments:

ISM Mfr’g

Employment

Export Orders

BY Doug Kass · Dec 1, 2025, 2:20 PM EST

BY Doug Kass · Dec 1, 2025, 2:15 PM EST

BY Doug Kass · Dec 1, 2025, 2:10 PM EST

BY Doug Kass · Dec 1, 2025, 1:56 PM EST

I love this situation:

BY Doug Kass · Dec 1, 2025, 1:13 PM EST

From Peter Boockvar:

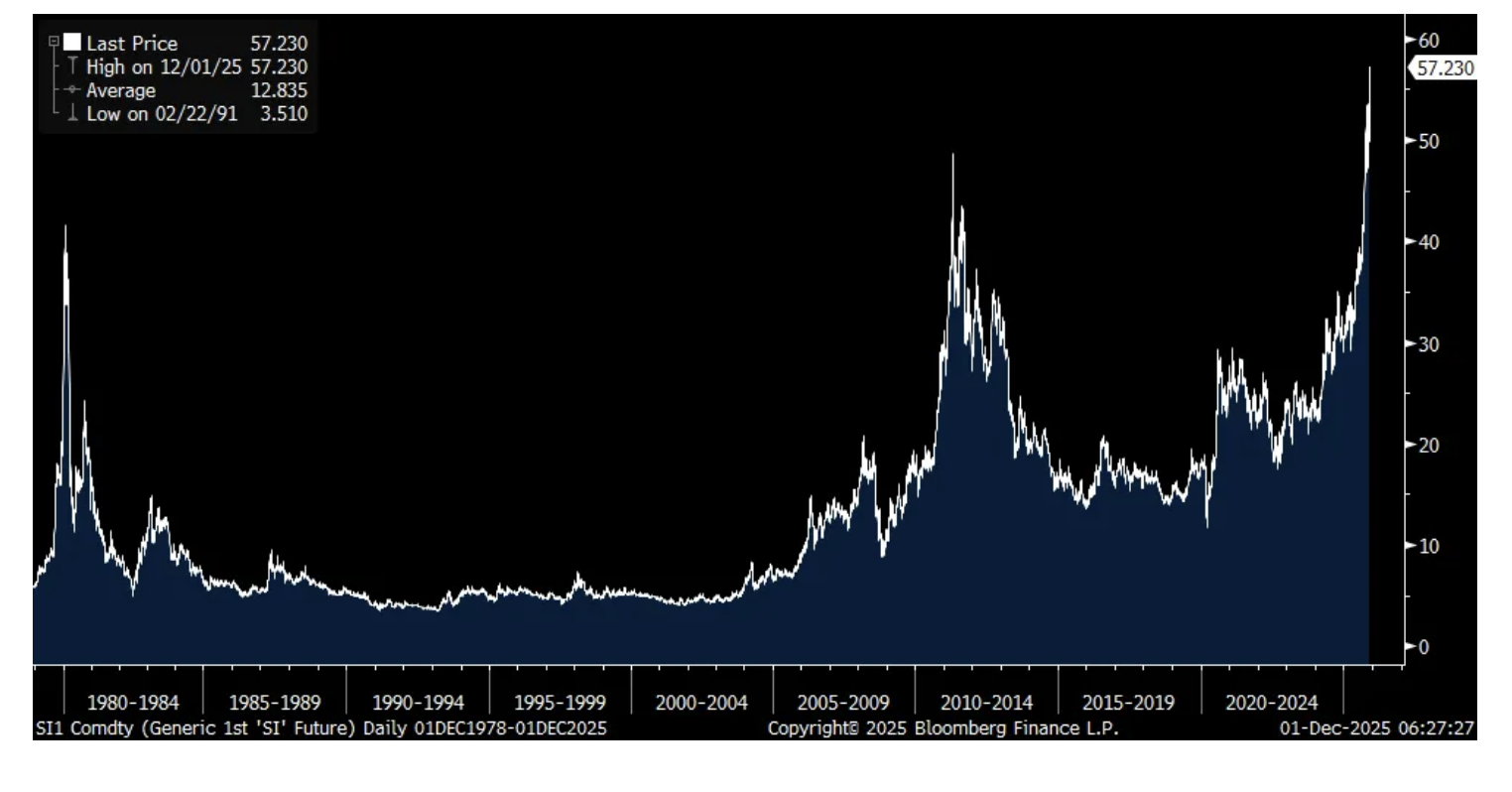

In case you didn’t see on Friday but silver is trading at a record high in nominal terms as more investors notice the multi year supply deficits at the same time industrial demand is benefiting from electrification uses, the metal still plays a monetary role as gold does, though not nearly to the same extent and it has been anointed as a critical mineral by the US Geological Survey. We remain long and positive on silver, along with gold and platinum (as hybrid vehicles win the market share battle vs full EVs and which use more platinum per hybrid than an ICE vehicle). Expectations of an Easy Money Man in the Fed next year is also helping.

The copper price trading on the London Metals Exchange is also trading at a record high, over $11,000 per ton.

This long term silver chart is a generic futures chart so doesn’t capture the around $50 level it touched in 1980

Copper on the LME as of Friday’s close but trading up again today

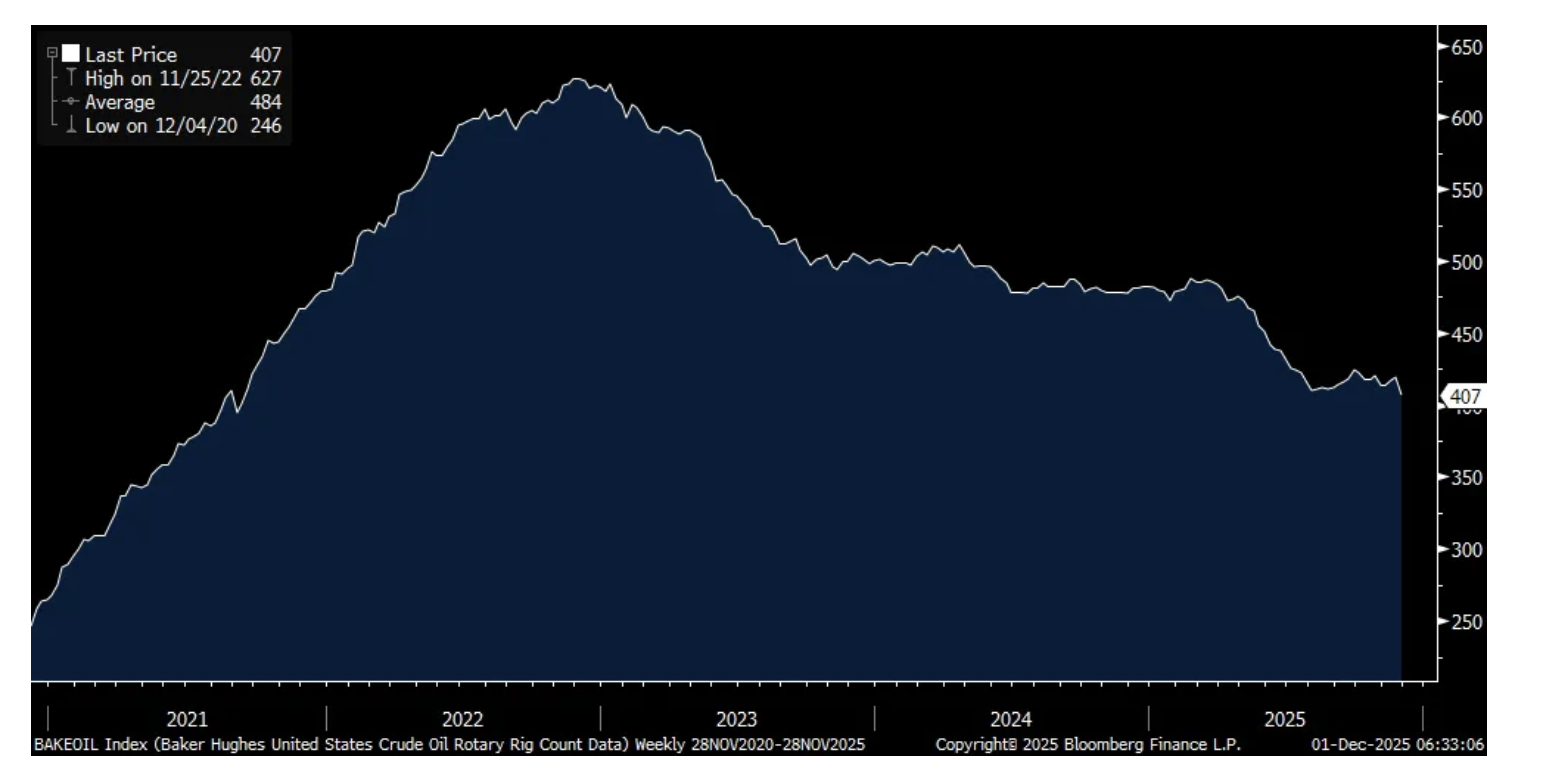

Also of note on the commodity front, the US crude oil rig count as of 11/28 fell by 12 rigs to 407, the least amount since September 2021. I’ll argue again that a barrel of oil is right now one of the cheapest assets in the world and we are long oil and gas stocks.

Crude Oil Rig Count

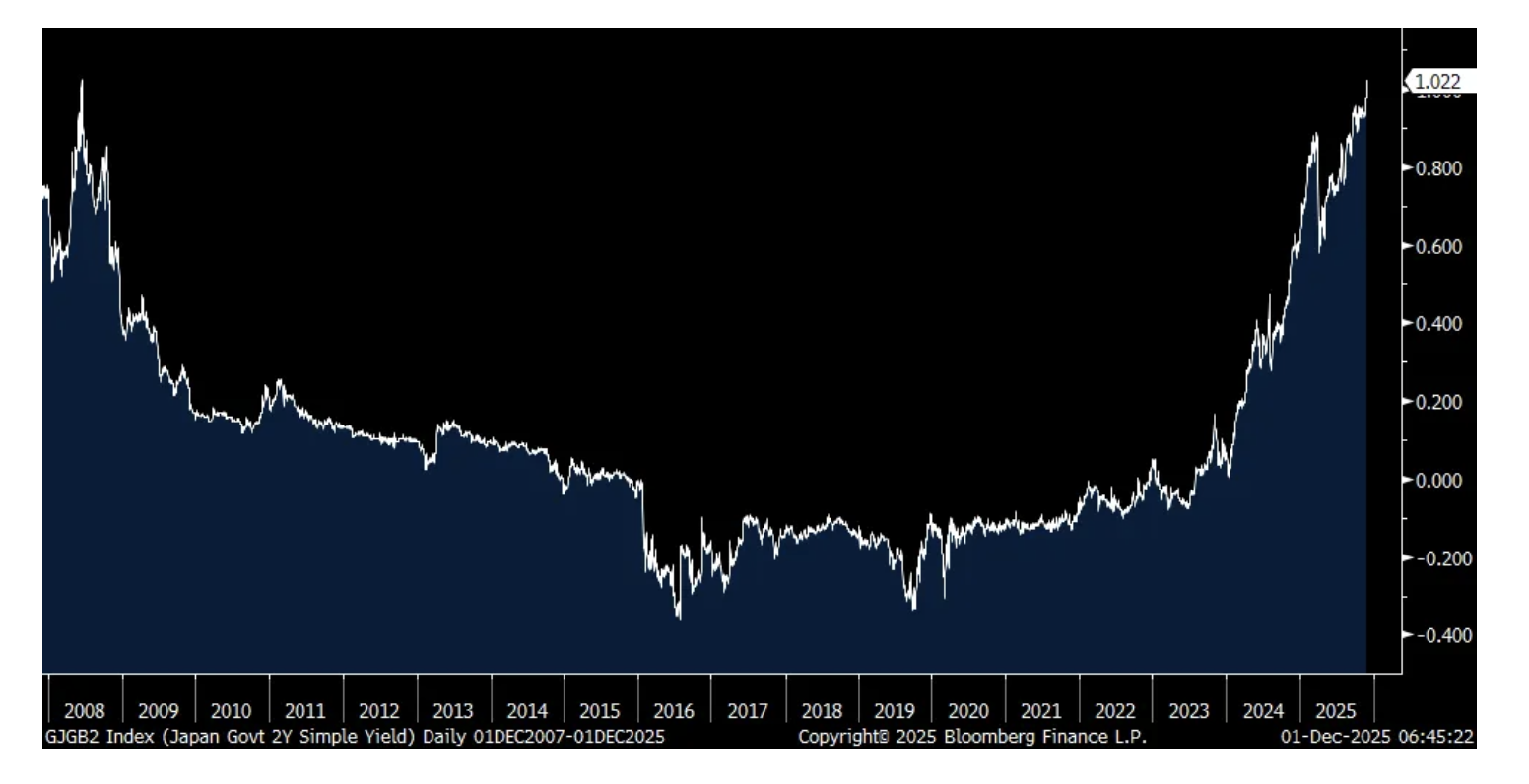

Interest rate hike odds for the Bank of Japan on December 19th is now up to 82% vs 30% just two weeks ago. Governor Ueda himself today in a speech is setting us up for a rate rise. He said, “Raising the policy interest rate under accommodative financial conditions is about the process of easing off the accelerator as appropriate toward achieving stable economic growth and price developments, not about applying the brakes on economic activity.” And they will “examine and discuss economic and price developments at home and abroad, as well as market moves...and consider the pros and cons of raising interest rates.” Finally in what seems like a clinching of the hike, “Being too late in adjusting the degree of monetary support could cause very high inflation and force us to respond rapidly, which would cause turmoil.”

The market reaction was instant with the 2 yr yield rising 4.3 bps to above 1% for the first time since 2008 at 1.02%. The 10 yr yield was higher by 6 bps to 1.87%, also a 17 yr high. Yields further out on their curve rose too and the yen is rallying to a two week high. I point my finger here as to also why European and US Treasury yields are higher. AGAIN, this is a really big deal for global bond yields I continue to believe. The Nikkei closed down 1.9%.

2 yr JGB Yield

Ahead of the US ISM manufacturing index today we got flooded with PMI’s from overseas with an overall mixed picture. Here was the breakdown:

China 49.2 vs 49 in manufacturing and 49.5 vs 50.1 in their non manufacturing PMI for their state sector weighted indices

China’s private sector manufacturing PMI 49.9 vs 50.6

Japan 48.7 vs 48.2

Australia 51.6 vs 49.7

South Korea 49.4 vs 49.4

Taiwan 48.7 vs 47.7

Vietnam 53.8 vs 54.5

Indonesia 53.3 vs 51.2

Malaysia 50.1 vs 49.5

Thailand 56.8 vs 56.6

Philippines 47.4 vs 50.1

India 56.6 vs 59.2

The final Eurozone manufacturing PMI was 49.6 vs 50 and the UK index was 50.2 vs 49.7.

Specifically with China, “On a sub-index basis, the expansion of both production and demand slowed in November to levels that were close to or at stagnation. On the demand side, although new export orders picked up in November, this trend failed to reverse the sluggish state of the manufacturing sector, with new orders remaining almost stagnant.”

With the Eurozone, “In terms of the number of countries in which industry is growing again, the outlook for the eurozone looks quite reasonable. Of the eight countries in which Manufacturing PMIs are recorded, a clear majority of six countries are showing a positive economic picture. However, when the sizes of these economies are taken into account, the situation looks completely different, as it is the two largest economies whose industries slipped even deeper into recession in November. In France, this is probably due to the continuing political uncertainty, which is causing many companies to hold back on investment decisions. In Germany, a large part of the economy appears to be disappointed with the federal government’s course of action to date, and a dangerous sense of resignation regarding the country’s ability to reform may be taking hold. However, we believe that visible investments in infrastructure could soon revive the mood. The current picture of the Eurozone is sobering, as the manufacturing sector is unable to break out of stagnation and is even tending towards contraction.”

To a few earnings calls.

From Petco Health & Wellness last week from their earnings call and a stock we own:

“Look, overall, the competitive set really hasn’t changed much from the last quarter. I would say what’s changed is the consumer’s been probably a little bit more cautious. I mean, obviously tariffs and political tensions and interest rates still high that’s really been bogging down their outlook on the economy a little bit. But as far as the pet industry goes, it’s been pretty stable, flattish in terms of growth.”

From Analog Devices:

“All of our end markets increased by double digits, reflecting both cyclical and company specific drivers” and despite “persistent macro and geopolitical headwinds.”

“The stronger than seasonal results underpins the cyclical momentum we see across industrial as well as the secular growth unfolding in AI infrastructure.”

BY Doug Kass · Dec 1, 2025, 12:59 PM EST

With S&P cash -9 handles, I am shorting index calls.

BY Doug Kass · Dec 1, 2025, 12:55 PM EST

BY Doug Kass · Dec 1, 2025, 12:45 PM EST

What follows is the third part of a compilation of my correspondences with Seabreeze Partners' investors and recent articles I have written on TheStreet Pro.

In terms of negative near term catalysts, we have long held onto the belief that a meaningful fall in equity prices would likely be associated with two factors. First, is the deleveraging of a highly leveraged financial system (quantitative hedge funds, cryptocurrencies and non-bank financial institutions). Second is the increased skepticism associated with more limited productivity benefits and lower-than-consensus returns on invested capital of the enormous outlays in AI capital spending.

In recent days, concerns about systemic leverage in the crypto currency markets (and elsewhere) and skepticism regarding AI orders and future profitability are beginning to be felt. With price earnings multiples (and other historic valuation metrics) in the 97% tile -- the market decline could be swift.

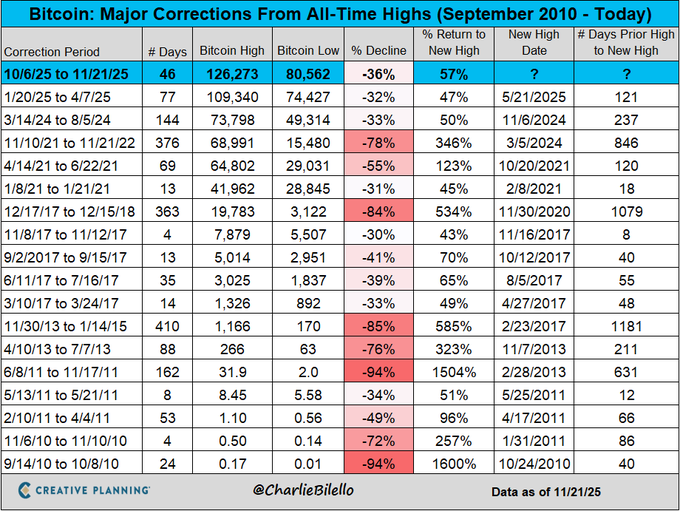

* At $80,600 bitcoin is now down around -36% from its all-time high of $126,300. That is the biggest correction off an all-time high since 2022.

Despite the broadening adoption, we would argue that most cryptocurrencies have no fundamental value:

In the extreme, quantum computers could destroy bitcoin and other crypto currencies. Regardless, the crypto currency market is characterized by enormous leverage and any further drop in value could cause cross asset contamination:

* As to AI, over the last 12 months I have written over 150 columns on the risks of AI on TheStreet Pro.

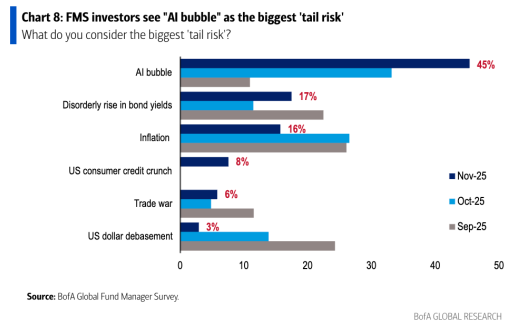

Forty five percent of fund managers surveyed by Bank of America said an "AI Bubble" was the biggest tail risk for markets, spiking from just 11% in September:

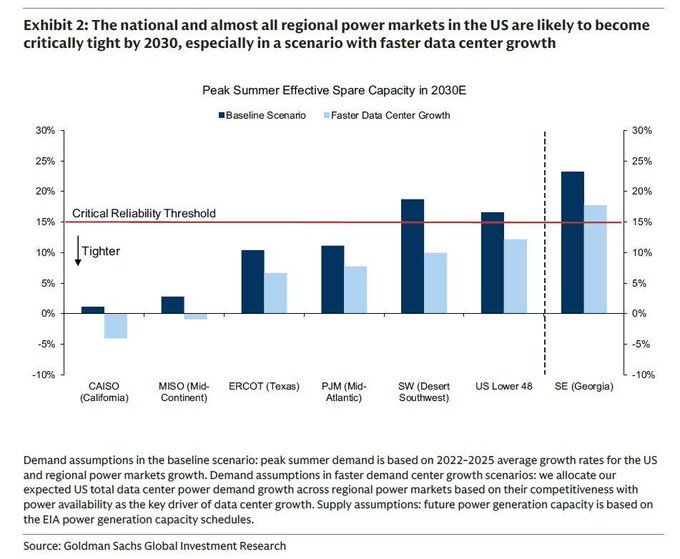

Among the many other issues, we are skeptical about the cost and availability of the power markets' ability to fund data center expansion. Already eight of the thirteen U.S. regional markets are at or below critical spare capacity levels:

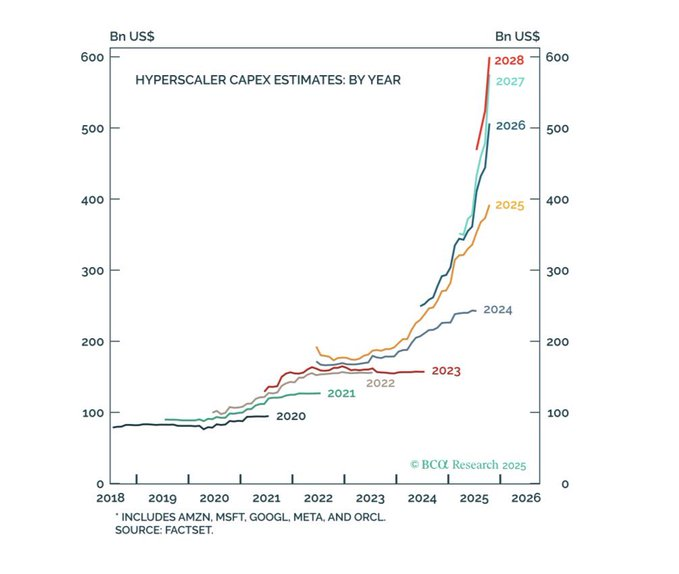

We are also skeptical that the enormous capital outlays will generate sufficient AI profits.

Here is one example: If you take the numbers in this chart, the hyperscalers will hold at least $2.5 trillion in AI assets by the end of this decade. Assuming a depreciation rate of 20%, that would mean $500 billion in annual depreciation expenses which is more than their combined profits in 2025:

The Magnificent Seven hyperscalers are rapidly moving from being capital-light to capital intensive.

In early November, I was quoted on AI in Barron's "Up and Down Wall Street" column, Meta Stock Took a Dive. It’s the Poster Child for the Debate Over AI Spending:

All eyes were on the parade of earnings reports from the technology behemoths this past week. But what grabbed the markets’ attention were the implications of their massive capital investments in artificial intelligence on their balance sheets and cash-flow statements.

At the center of this debate was Meta Platforms, which plunged 11% on Thursday after reporting a miss on earnings but, more importantly, said it was pushing full speed ahead on AI data centers, projecting $71 billion in spending, up from $69 billion previously. Moreover, the company said that capital expenditures “will be notably larger in 2026 than 2025.”

All of which is absorbing increasing amounts of megatechs’ cash flow. As Doug Kass of Seabreeze Partners observes, the so-called hyperscalers have morphed from being “capital light” to capital-intensive operations. In the process, they have had to turn to external financing for their ambitious AI buildouts.

In fact, Meta brought this year’s biggest investment-grade corporate bond deal to market, totaling some $30 billion, the latest in a parade of recent data-center borrowing. Bank of America tallies $75 billion of AI-related public debt offerings in the past two months.

And that doesn’t count other financings, including Meta’s creative off-balance-sheet funding of its Louisiana data center, described by colleague Adam Levine in last week’s Tech Trader column. That includes a $38 billion loan tied to Oracle’s data centers, on top of $18 billion of public bonds issued by the company, led by world’s second-richest person, Larry Ellison.

Putting numbers to Kass’ point, BofA credit strategists Yuri Seliger and Sohyun Marie Lee write in a client note that capital spending by five of the Magnificent Seven megacap tech companies (Amazon.com, Alphabet, and Microsoft, along with Meta and Oracle) has been growing even faster than their prodigious cash flows. “These companies collectively may be reaching a limit to how much AI capex they are willing to fund purely from cash flows,” they write.

Read the rest of the Barron's column here: (Barrons’ Meta Stock Took a Dive. It’s the Poster Child for the Debate Over AI Spending.)

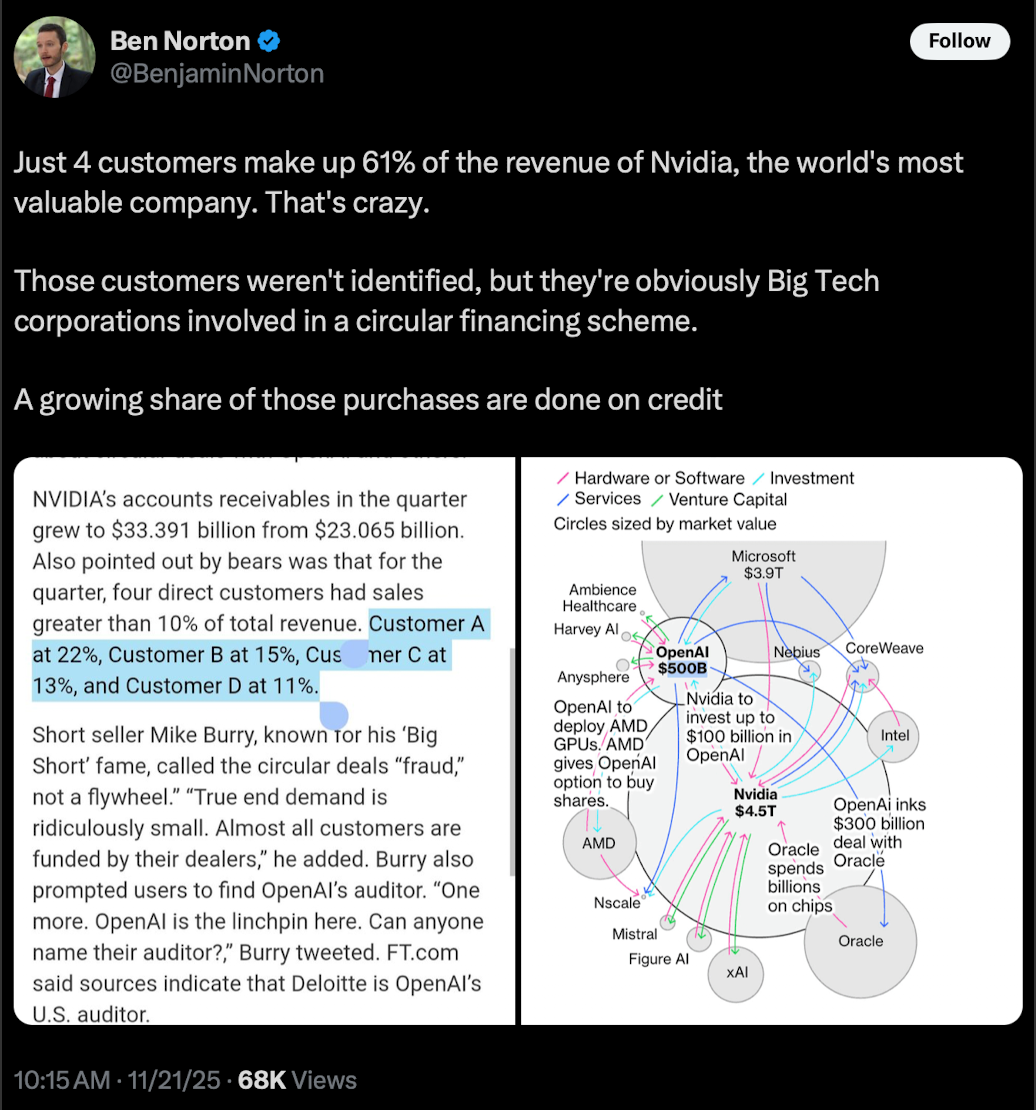

As noted in our previous monthly commentaries, we are skeptical of the circular funding (and "roundtripping") of the unprecedented and large AI capital expenditures that have been announced:

The "crack" and order fragility may be deeper than most realize. When a small group (of Nvidia (NVDA) and "friends") acts as a customer, partner, investor and infrastructure provider -- and a growing share is financed -- it starts to look less like organic demand and more like a tightly coupled system.

Last week I began to read my friend Andrew Ross Sorkin's new book 1929: Inside the Greatest Crash in Wall Street History-and How It Shattered a Nation. I couldn't help but see the similarities between then and now.

The 1920s did not end well as our society lost sight of the value of regulations:

* Wise rules are a source of abundance.

* Well-regulated markets/systems attract users and investors.

* Removing the constables patrolling our financial markets is potentially dangerous.

* U.S. capital markets became the world's largest not despite regulation, but because of it.

In late 2025, like 1929, we find our markets racing to new highs. Arguably, speculation, too, remains a mainstay with massive amounts of capital being employed into cryptocurrencies and artificial intelligence. And, despite a century of hard-won lessons, governmental policy/ authorities are embracing dissolute policies to keep the punch bowl filled as regulatory oversight slips:

The current Administration has been ordering the chaperones removed. Since January, his administration has been firing regulators and vigorously tearing down the guardrails that have kept our markets thriving for nine decades.

For the first time in a century, the S.E.C. is seriously exploring how to allow firms and funds to sell investments to masses of Americans without registration or disclosure. The administration is even encouraging individual retirees to vouchsafe their life savings to exotic financial offerings like private equity. Private equity is, as the name suggests, notoriously opaque, which means retirees would know little about what they’re investing in. The White House and the private fund lobby argue that this policy will “democratize” access to alternative assets and promote “better returns.” But such a plan, which comes with neither the information nor the protections needed to defend investors from serious economic risks, is as compelling as a plan to “democratize” brain surgery. The Administration is also allowing financial regulators to atrophy: The five-person Commodity Futures Trading Commission, tasked by this administration to oversee significant portions of the crypto and prediction markets, has dwindled to a single member. Only two of five statutorily mandated S.E.C. commissioners are serving in their normal terms; the lone remaining Democratic appointee, Caroline Crenshaw, is in her post-expiration grace period, and warning that the agency’s policies are “a reckless game of regulatory Jenga.”

The agency’s chair has declared “a new day at the S.E.C.” But the lamps are going out all over the agency: Staff has been cut by 16 percent (substantially more than the 10 percent of a literal decimation), quarterly reports are on the chopping block and forms that provide intelligence about dark corners of the market are being repeatedly deferred.

Meanwhile, the Administration is relentlessly browbeating the Federal Reserve to lower interest rates. That could also, as it did in the 1920s, overstimulate an already-lofty stock market. And all that money chasing too few goods is what leads to inflation — a problem that takes longer to develop and is devastating when it arrives. Mr. Trump may no longer be president when that bill comes due. For now, his administration is stamping on the gas while turning off the headlights. And as Fitzgerald warned us in the climactic scene of “The Great Gatsby,” terrible consequences come from automobile accidents in the gathering darkness".

- William Birdthistle (former director of the Division of Investment Management at the Securities and Exchange Commission - 2021-2024), New York Times essay It Could Be 1929 All Over Again

The lesson of 1929 was that when sentinels sleep, fraudsters flourish: Their confident, ebullient and frenzied celebration of unreal profits pumps froth into the market.

The mantra, embodied by Citigroup's CEO (Charles Prince) quote in the Financial Times (July, 2007) only a few months before The Great Financial Crisis began, has been embraced by the majority of investors today:

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We are still dancing."

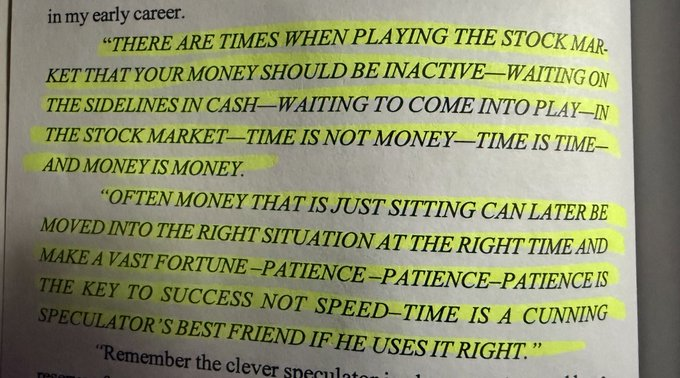

We at Seabreeze Partners prefer Jesse Livermore over Charles Prince. Here is a quote from Livermore's book How To Trade Stocks - published in 1940 and available on eBay for $4,950 1940 ~ How to Trade in Stocks Jesse Livermore 1st Ed. ~ Wall Street Stock Market | eBay:

As I noted in a recent monthly commentary to Seabreeze's limited partners - Warren Buffett warned about such a mindset in November 1999, only four months before the dot.com bubble burst:

“Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.”

Voltaire also put it well when he wrote:

"History never repeats itself. Man always does."

Delusions swing between extremes, like pendulums. Delusions of grandeur and unending wealth give place to delusions of unending gloom. One is as unreal as the other. Today we seem to be close to an extreme in speculative activity and valuations. Unfortunately, history teaches us that the unsustainable cannot be sustained as, ultimately, with panic and pain, bubbles burst.

BY Doug Kass · Dec 1, 2025, 12:20 PM EST

What follows is the continuation of a compilation of my correspondences with Seabreeze Partners' investors and recent articles I have written on TheStreet Pro.

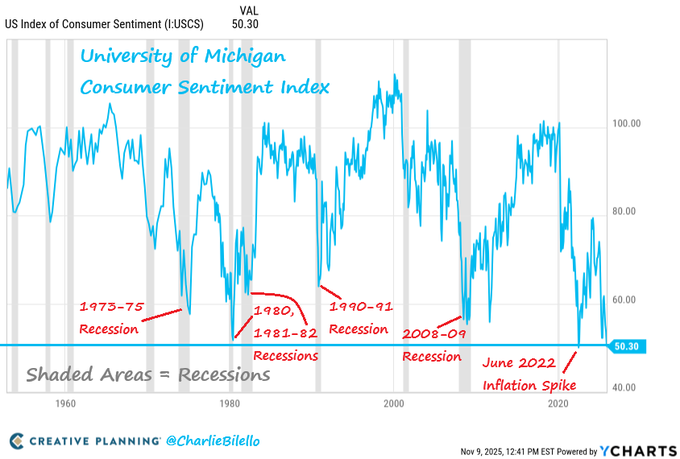

Consumers represent 2/3rds of the domestic economy. Their confidence has deteriorated and sentiment is making new lows:

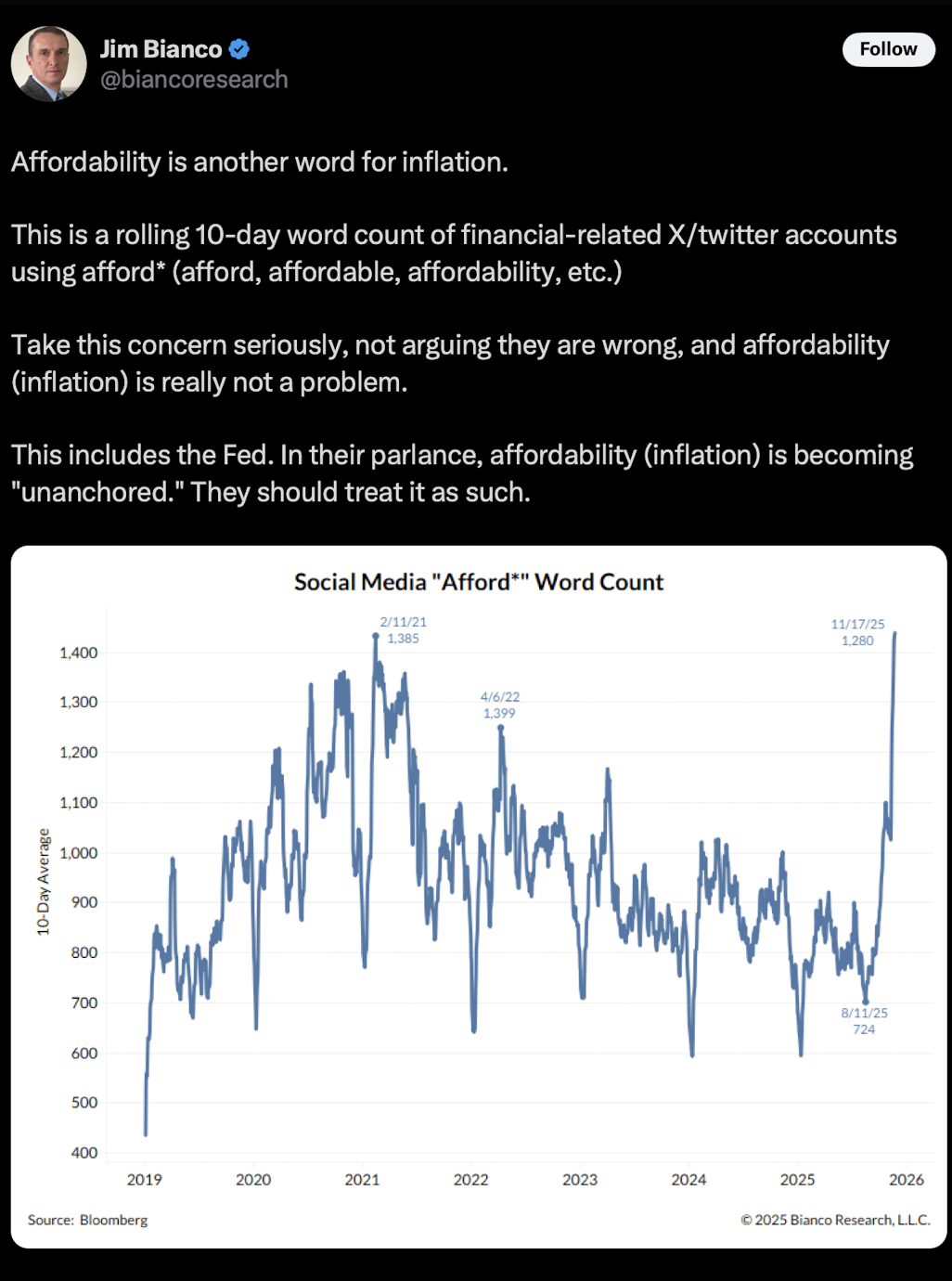

Affordability is another word for inflation:

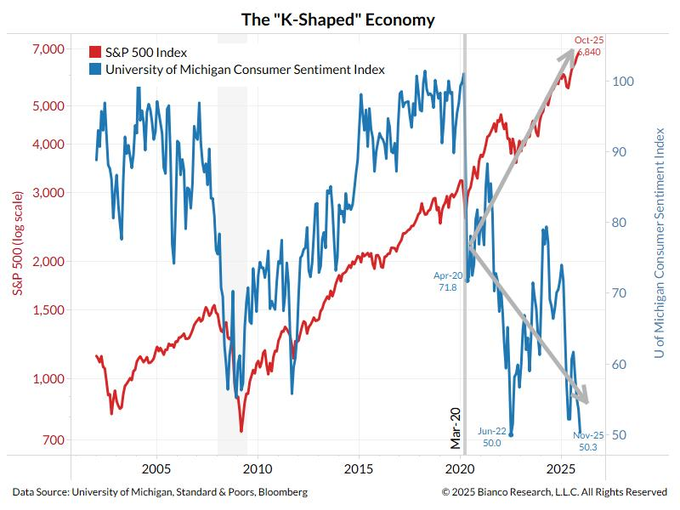

The U.S.' K-shaped economy (What is a 'K-shaped' economy, and what’s causing the divide?) is embellishing the health of the average U.S. consumer who is weighed down by the cumulative or stacked inflation since Covid, five years ago -- something that interest rate cuts by the Federal Reserve will not fix:

In October, U.S. wage growth (+2.5%). Excluding the 2020 pandemic this is the lowest rate of growth in seven years - for perspective, wage growth rose by +9% at the January, 2022 peak) and is now tracking less than inflation. According to Indeed.com, inflation is growing faster than wages by 2.5% vs. 3.1%

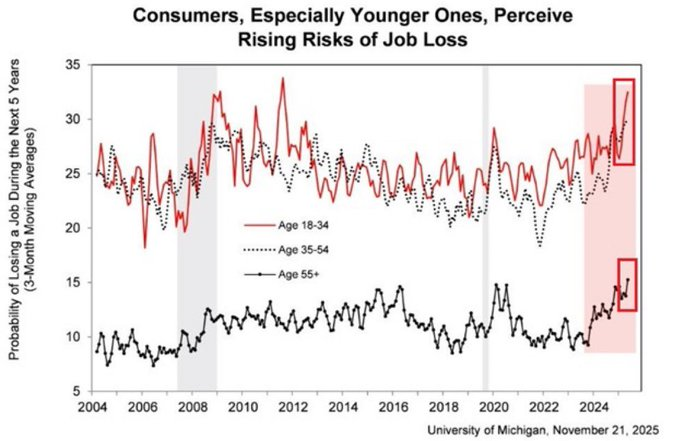

U.S. consumers are losing confidence in their job security. Younger workers are the most worried in years, middle-aged workers just hit a record level of fear and even older Americans are the most pessimistic ever. The majority of people now expect unemployment to rise:

Moreover, the enormous growth in AI capital expenditures has also likely masked a weaker non-AI U.S. (consumer dominated) economy.

In the next post, we'll look at negative short-term market catalysts that are emerging.

BY Doug Kass · Dec 1, 2025, 11:35 AM EST

That's not right. How can the price be going down?

Something's wrong. Where's Wilson?

What are they doing here?

They are selling Mortimer

That's ridiculous. Unless that crop report?

God help us. I told you we shouldn't have committed everything you a**hole.

You gotta get Wilson and tell him to sell

Wilson, where are you going? You idiot, get back there at once and sell, sell...

- Randolph and Mortimer Duke, Trading Places: Sell!

What follows is an combination of my correspondences with Seabreeze Partners' investors and recent articles I have written on TheStreet Pro:

Given the plethora of existing and potential headwinds, the climb in equities over the last few months has been anathema to me.

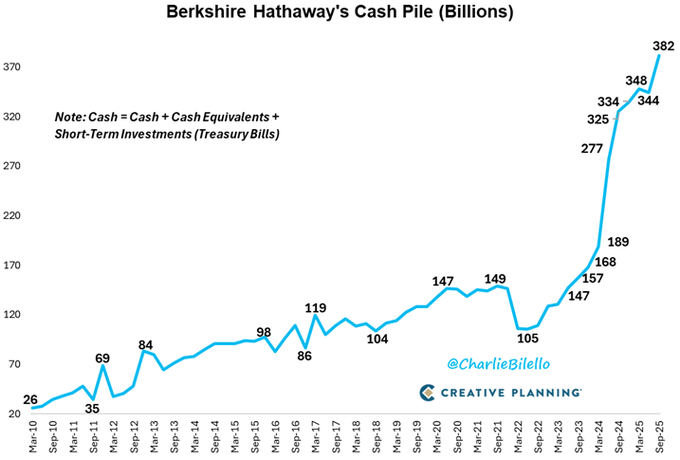

I continue to be cautious in my hedge fund’s investment positioning, and like Warren Buffett's Berkshire Hathaway, I have plenty of cash reserves:

For the first time since April, 2025, investors are beginning to open up their eyes to our concerns as reflected in the recent market weakness. At its deepest, the S&P Index was down by 5.8% from the Oct. 29, 2025 peak. It was the 31st pullback of greater than 5% in the averages since the March, 2009 low.

Despite the rally back to within a percentage or so from the all-time high in the S&P Index -- with the recent break in price momentum, I am growing more optimistic that stocks will decline to levels that will provide more reasonable long opportunities.

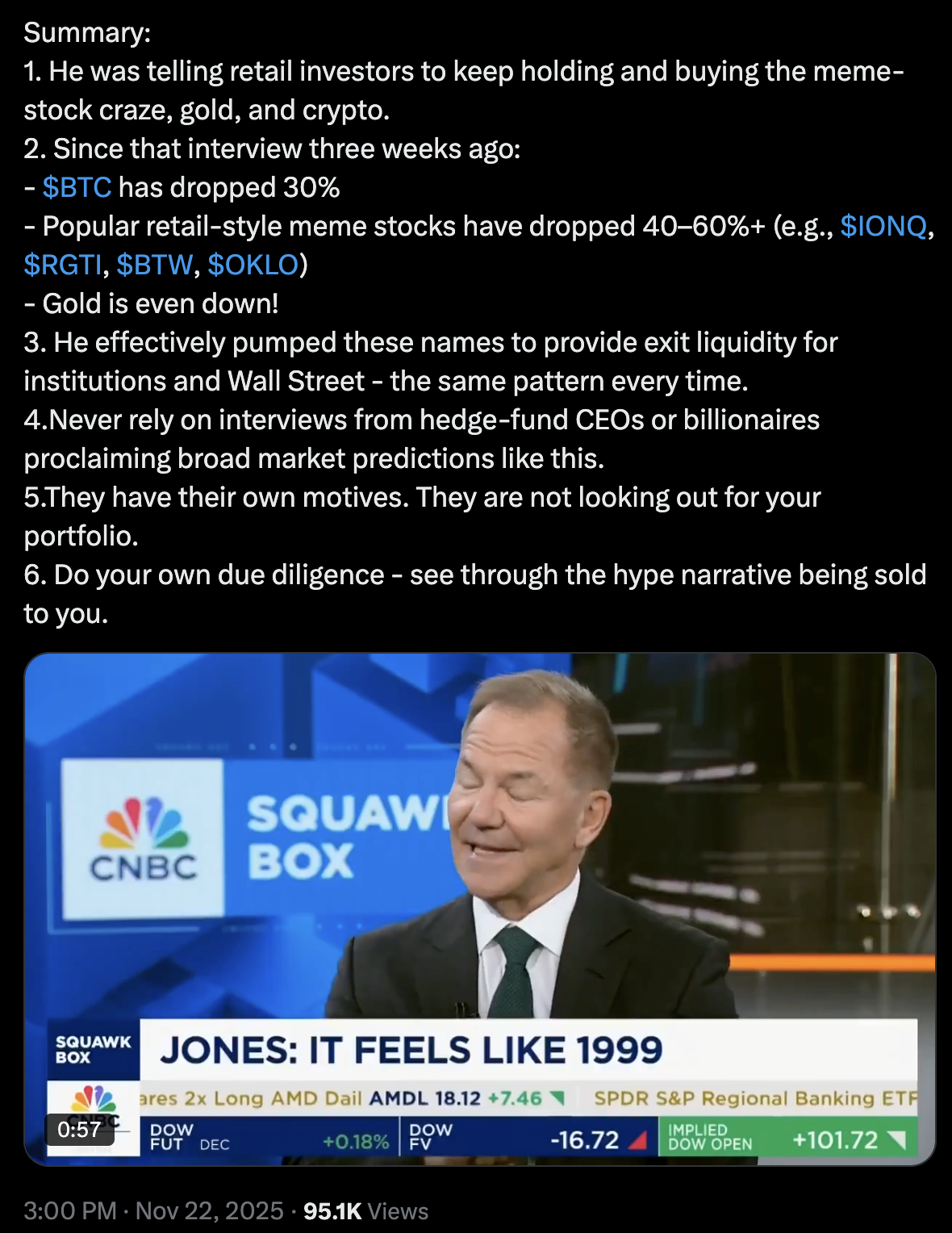

With calculator in hand we gauge risk, never getting emotional and chasing equity prices higher. Unlike many, I will not abandon my growing and multiple fundamental concerns even in the face of higher stock prices, which result in a further deterioration in reward compared to risk... even in the face of many who have been looking for a melt up in equities and other asset classes like bitcoin into year-end (like Paul Tudor Jones and Fundstrat's Tom Lee):

Tom Lee, meanwhie, points out a mechanical "glitch" that may be fueling crypto’s rollover.

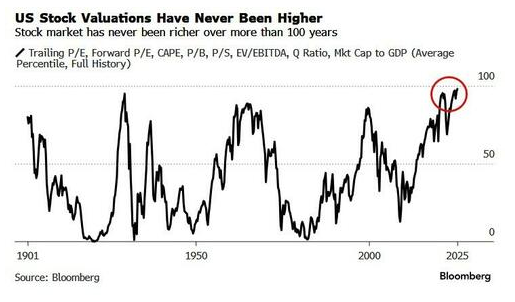

By every traditional valuation metric equities are richly priced:

Few equities meet our standards for selection on the long side, there is little "margin of safety" and most stocks still present a poor reward/risk proposition:

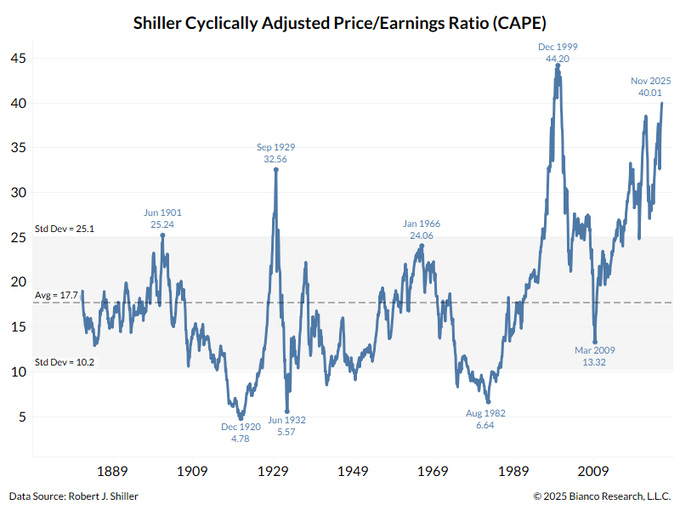

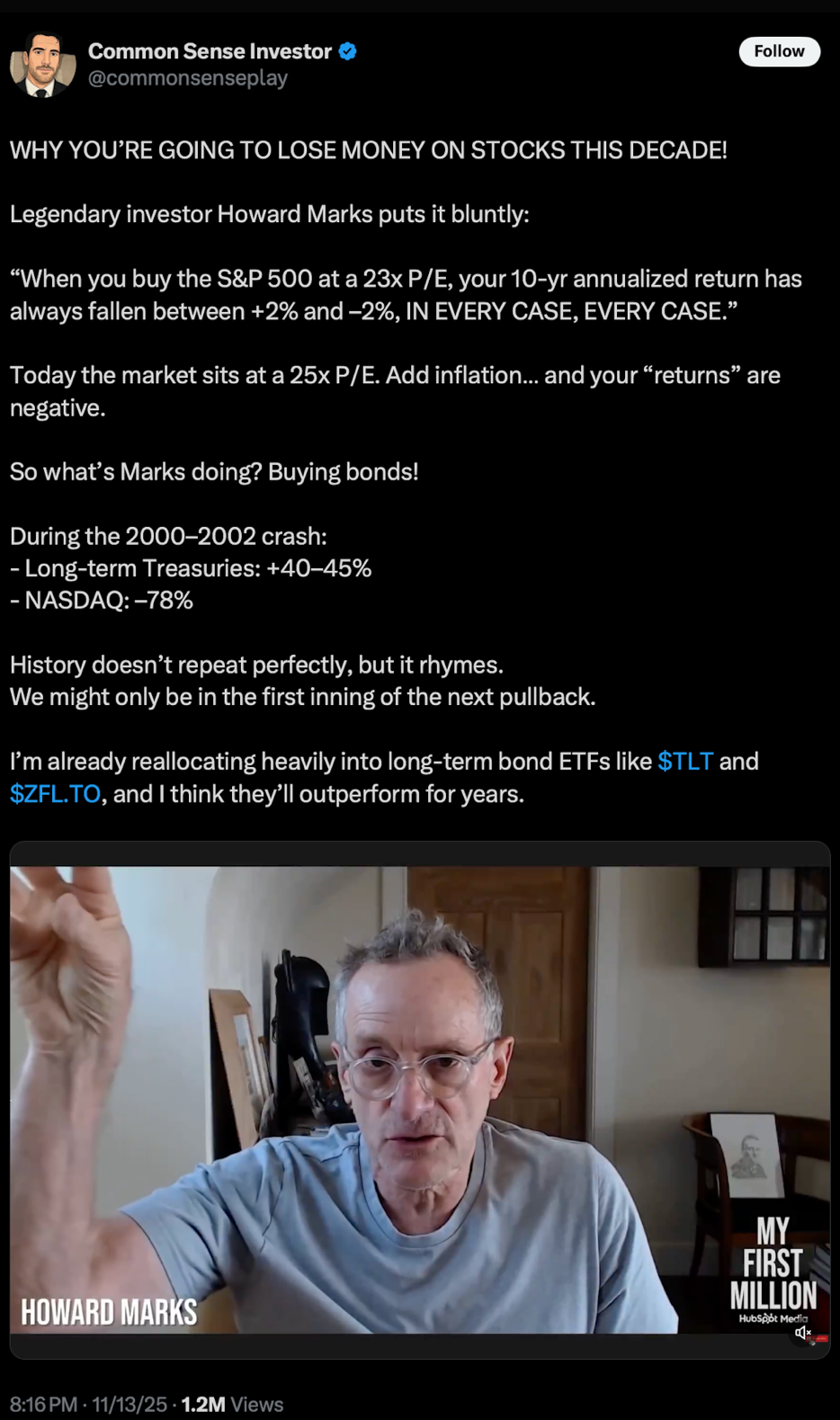

Today's lofty valuations are a poor launching pad for future investment returns:

"When you buy the S&P 500 Index at a 23x PE, your ten year annualized return has always fallen between +2% and -2% IN EVERY CASE."

- Howard Marks

As noted below, speculative activity is beginning to leak as the highest beta stocks have begun to retreat in recent weeks:

The foundation of our ursine market view resides in our expectation of slowing global economic growth, elevated interest rates, high valuations and sticky inflation.

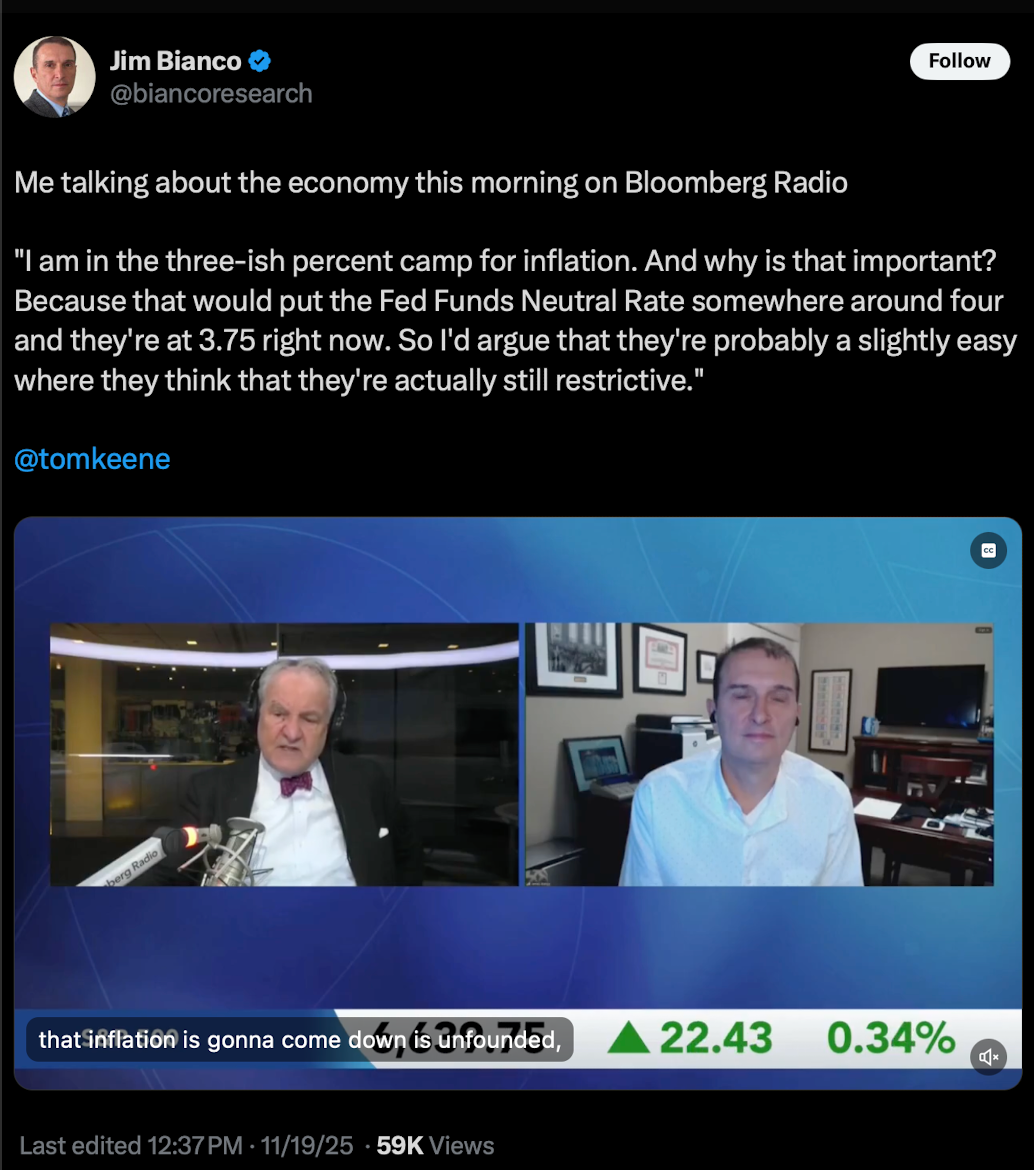

Inflation rates are now trending back toward the 3% level. So, even though (an easy money) Kevin Hassett looks likely to replace Jay Powell as the Chairman of the Federal Reserve - the Fed finds itself between a rock and a hard place.

Here Jim Bianco talks about the consequences of inflation being above the Fed's target:

The equity risk premium (the S&P earnings yield minus the risk-free rate of return) has moved to a discount - something that has not happened in nearly three decades.

Meanwhile, market structure (the massive shift from active management to passive management) presents a grave risk to equities. With everyone on the same side of the leveraged boat (of equities and other asset classes), the probability of a market dislocation has risen dramatically.

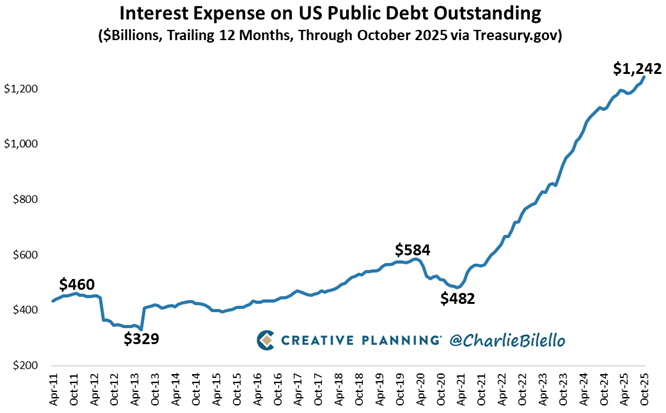

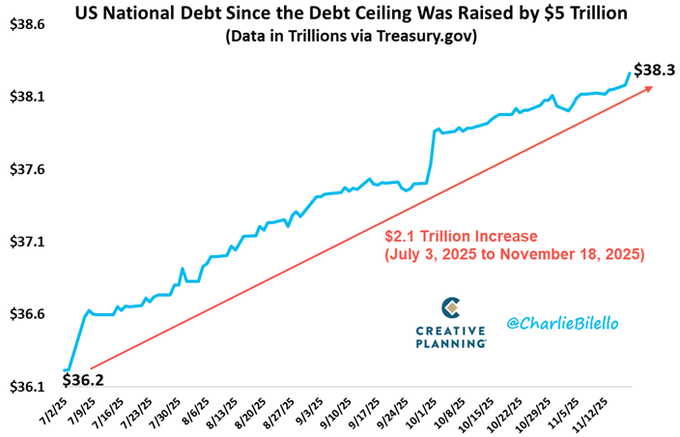

The absence of fiscal discipline by our leaders of both parties in Washington, is a profoundly deep threat. Interest expense on the national debt rose to a record $1.24 trillion over the last 12 months, more than doubling over the last four years. The U.S. now spends more money on interest that it does on national defense:

The U.S. National Debt has now increased by over $2 trillion since the Debt Ceiling was raised back in July. The Federal Government continues to borrow from our future to spend money like drunken sailors today. The absence of fiscal discipline is nonpartisan - representing an expanding and non-trivial economic and market risk:

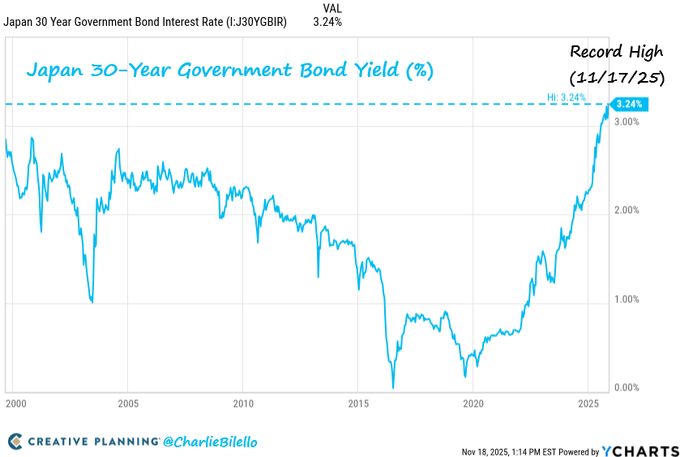

Japan's 30-year bond yield has spiked to 3.24% - the highest on record. This could be a preview of what is coming to the U.S. if we don't get our deficit/debt spiral under control. The chicken eventually will come home to roost:

My dear friend John Mauldin writes a weekly commentary, Thoughts From the Frontline Thoughts from the Frontline - Mauldin Economics, which is free and that I encourage everyone to subscribe to. These recent issues from last month discuss at length the enormity of our country's debt problem:

2. Big Debt Cycles Part II Big Debt Cycles, Part 2 | Mauldin Economics

When I continue this post, we'll look at where the health of the U.S. economy and the outlook for corporate profits Is being overstated....

BY Doug Kass · Dec 1, 2025, 11:00 AM EST

I added to my (AAPL) short at $278.

BY Doug Kass · Dec 1, 2025, 10:37 AM EST

I added to my (NVDA) short at $178.26

BY Doug Kass · Dec 1, 2025, 10:22 AM EST

Reshorted indexes with the rally off the lows and cash -15 handles (from -45 handles):

* (SPY) $681.71

* (QQQ) $616.53

BY Doug Kass · Dec 1, 2025, 10:07 AM EST

(KMB) and (PEP) have gone from defensives to offensives!

BY Doug Kass · Dec 1, 2025, 9:41 AM EST

-QTTB +97% (divests ADX-097 to Akebia; $12M upfront extends runway into 2H27; SIGNAL-AA Part B topline bempikibart data for alopecia areata due mid-2026)

-KALA +30% (receives $6M investment; David Lazar becomes CEO and chair)

-WBUY +29% (momentum)

-NFE +28% (said to receive tentative approval of deal to supply LNG to Puerto Rico for ~$3B)

-CSIQ +13% (to resume direct oversight of U.S. manufacturing and operations)

-LEG +13% (offered to be acquired by Somnigroup at $12.00/shr in all-stock deal worth ~$1.62B)

-NMRA +7.6% (RBC Raised NMRA to Outperform from Sector Perform, price target: $7)

-SNPS +7.5% (NVIDIA invested $2B in Synopsys stock at $414.79/shr and expanded its strategic partnership to revolutionize design and engineering across industries)

-WOLF +6.4% (receives $698.6M in Section 48D cash tax refunds from IRS)

-B +3.7% (announces evaluation of an IPO of its North American gold assets)

-SVRN +3.1% (announces up to $10M Share Repurchase Program)

-ACN +2.9% (partners with OpenAI to accelerate enterprise reinvention with advanced AI)

-WYNN +2.0% (Macau Nov casino revenue)

-EMPD -6.7% (announces update on Share Repurchase Program)

-CPNG -5.2% (confirmed that personal information related to 33.7M customers had been 'compromised')

-JOBY -4.8% (Goldman Sachs Initiates JOBY with Sell, price target: $10)

-MSTR -4.7% (discloses acquired 130 BTCs; has established a US dollar reserve of $1.44B to support the payment of dividends on its preferred stock and interest on its outstanding indebtedness)

-COIN -4.4% (downside momentum)

-DARE -3.8% (announces return of rights to Ovaprene)

-MRNA -3.8% (reportedly internal memo says FDA attributes deaths of 10 children to Covid vaccinations, citing myocarditis as a possible cause)

-PTCT -3.2% (RBC Cuts PTCT to Sector Perform from Outperform, price target: $91)

-IONQ -2.4% (partners with CCRM, quantum-biotech investment to drive advanced therapy development)

BY Doug Kass · Dec 1, 2025, 9:25 AM EST

BY Doug Kass · Dec 1, 2025, 9:15 AM EST

BY Doug Kass · Dec 1, 2025, 9:09 AM EST

8:00PM: Fed Chair Powell gives brief remarks and participates in "George Schultz and his Economic Policy Contributions" panel before the Hoover Institution George P. Shultz Memorial Lecture Series: George Shultz and Economic Policy, Stanford, CA (Text available. Q&A from moderator. Webcast at

https://www.hoover.org/events/george-p-shultz-memorial-lecture-series-shultz-and-economic-policy)

BY Doug Kass · Dec 1, 2025, 9:05 AM EST

BY Doug Kass · Dec 1, 2025, 8:57 AM EST

I should have gone back to first principles. Gen AI does not think. It re-assembles content that was already produced by humans (which it often has taken without permission or compensation). This is why it needs to be “trained.” Without the humans, Gen AI is useless.

Hypothesis creep is one of the worst mistakes one can make when investing. It is a sure-fire way to lose money. There were two key hypotheses with Generative AI:

* Scaling The notion that the more processing power that was thrown at the models, they would become exponentially better. That has turned out not to be the case. In fact, the opposite. The additional processing power has been oodles more expensive (capital and power) and resulted in negligible gain. All the same problems, like hallucinations, remain. Therefore, the marginal return on capital is terrible and getting worse.

* AGI Somewhat related to the last point. The notion was Gen AI would eventually get there. Now it is pretty clear Generative AI has no path to AGI. Why anyone ever thought that Generative AI was a path to AGI to begin with, is completely beyond me. I said this from Day 1 (More Tales Issue #1), it cannot get there. Maybe a new approach can, but not LLMs/Generative AI. Generative AI needs the humans, because at best it just rapidly re-assembles previously produced human content. Show it 1,000 videos of apples falling from a tree, it could never come up with a theory of gravity on its own.

In conclusion, the entire economy (including the government) is now being bet on hypothesis creep. Hypothesis creep rarely, if ever, works. When it does work, it is usually after your investment goes from 100, down to 10, and then back to 15, so you are still well short of where you started.

And what do you know. You wonder why the entire economy and power grid are being bet on hypothesis creep? Similar issue with regard to crypto:

Silicon Valley’s Man in the White House Is Benefiting Himself and His Friends

This one is good too:

Three years on, ChatGPT still isn't what it was cracked up to be – and it probably never will be

What he leaves out is it is all so terribly dis-economic on top of it all. If every entity in the value chain charged enough such that they were earning real economics (not fake earnings before expenses like CoreWeave (CRWV) ), the price to the final end customer would be so high, there would be negligible demand. Alternatively, one could say end demand is already flattening when the product is provided at a discount to its cost. When the brand-new product goes to the closeout rack at TJ Maxx, and it still does not sell, there is a problem.

The other big problem with Generative AI is it is massively compute intensive. Every single query causes a massive cascade of compute and power consumption. That is the reason for the massive volume of business for Nvidia (NVDA) and the other infrastructure providers over the short term. But that is also the reason it is so dis-economic, and this is endemic to the technology.

Then on top of it all, the end-product has rapidly commodified. Ex the capital investment, the underlying technology is easy to do, as evidenced by the numerous un-differentiated suppliers that are now doing it. This is the problem OpenAI and others will have. OpenAI tried the typical Silicon Valley thing to giga scale — to become the biggest by far the fastest, so nobody could compete. It blew up in their face. They scaled as a non-monetizable homework-cheating machine and internet search engine. Then, because there was so much hype in the space, too many other players also got massively funded. And along came the low-cost Chinese too. The product quickly turned into a non-differentiated commodity. OpenAI quickly turned into a high-cost player in a commodity space.

Wall Street and the venture community always piles into these things, and sells them as the next great miracle, and often draws the government along in the process. The results are most often a disaster.

MRNA vaccines were supposed to cure cancer by now. All they seem to do is continually fail clinical trials, because they don’t work and have bad side effects. Read about Pfizer’s (PFE) last effort with their failed MRNA vaccine for the flu, where they seemingly buried the results of the clinical trial (https://alexberenson.substack.com/p/very-urgent-pfizers-mrna-flu-shot).

At any rate, look at the stock price history of Pfizer and Moderna (MRNA) , which makes the point. Same for the biotech index. All the damage done to the U.S. economy and social structure in the process, because it was so poorly handled, probably in part because of “science” pushed on the government by the public companies and other parties that got a tremendous financial benefit from the policies the government put in place.

Windmills? Solar? Electric vehicles? On and on. How much in the way of $ did the government throw at green energy projects, like Solyndra, that went belly up? Europe is practically bankrupting their economies with this stuff. None of this ever turns out to be the miracle we were told it would be.

BY Doug Kass · Dec 1, 2025, 8:00 AM EST

BY Doug Kass · Dec 1, 2025, 7:50 AM EST

BY Doug Kass · Dec 1, 2025, 7:37 AM EST

* A must read and nowhere discussed on Fin TV....

BY Doug Kass · Dec 1, 2025, 7:25 AM EST

Following the opening I will be delivering my lengthy market update.

It's long, so it will be in multiple parts.

I hope you find the output value-added.

BY Doug Kass · Dec 1, 2025, 7:15 AM EST

BY Doug Kass · Dec 1, 2025, 7:05 AM EST

BY Doug Kass · Dec 1, 2025, 6:55 AM EST

BY Doug Kass · Dec 1, 2025, 6:45 AM EST

As noted recently, the rise in Japanese bond yields are worrisome:

BY Doug Kass · Dec 1, 2025, 6:35 AM EST

BY Doug Kass · Dec 1, 2025, 6:25 AM EST

BY Doug Kass · Dec 1, 2025, 6:15 AM EST

BY Doug Kass · Dec 1, 2025, 6:05 AM EST

I covered my trading short rental in the indices last night — on the whoosh lower:

Dougie Kass

805PM Sunday Night

Covered 1/2 of my Index shorts with SPOOS -32 handles (moved back to small sized):

I plan to reshort on any strength...

Nite.

Dougie Kass

With SPOOs -38 handles I covered the balance of my Index shorts - will reshort on strength

BY Doug Kass · Dec 1, 2025, 5:55 AM EST

The S&P Short Range Oscillator is at 1.64% vs. -0.92%.

BY Doug Kass · Dec 1, 2025, 5:45 AM EST