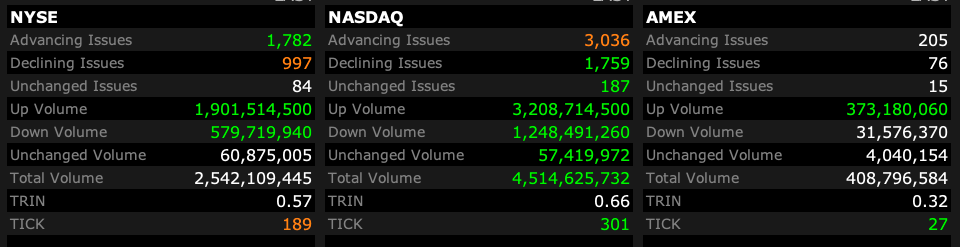

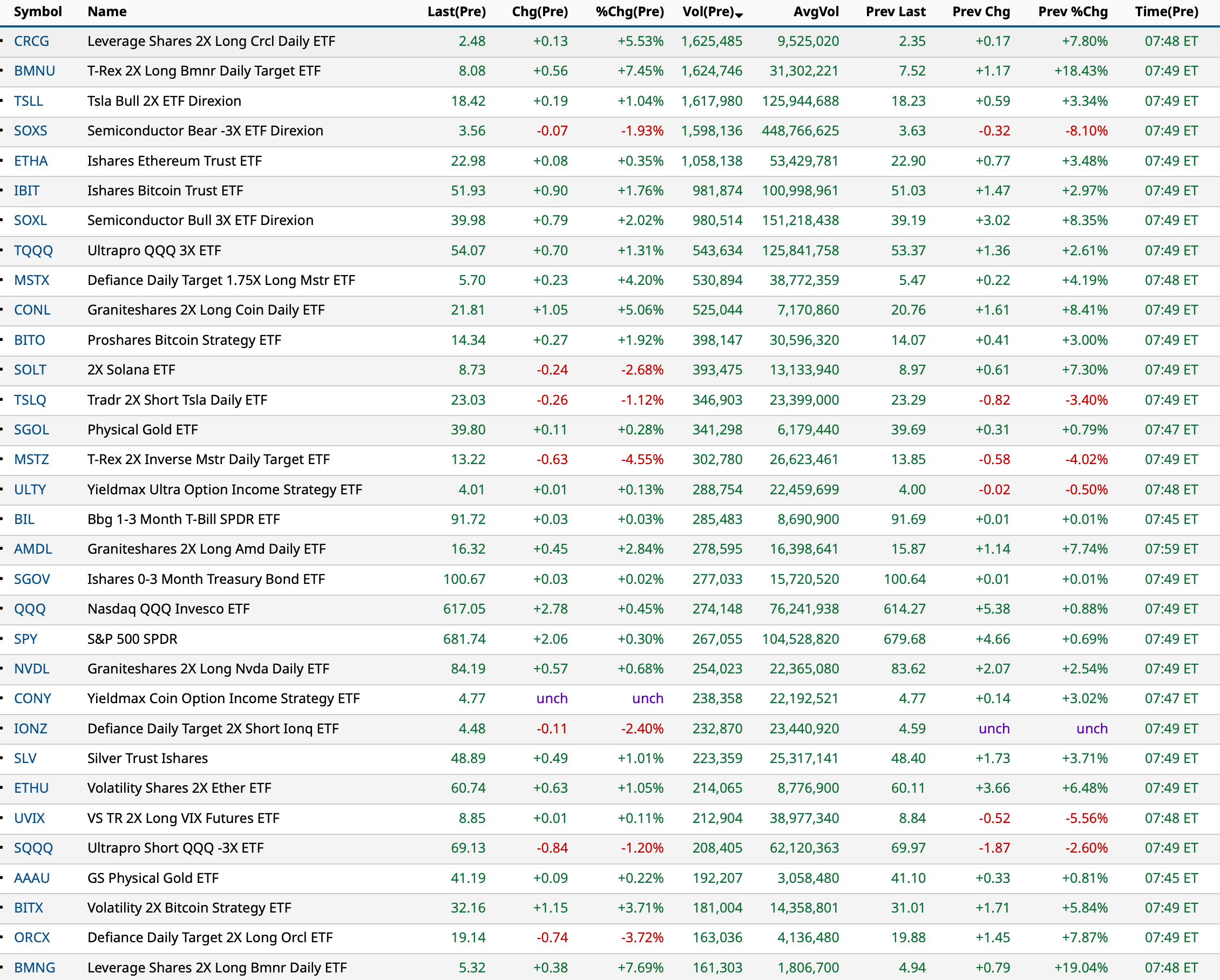

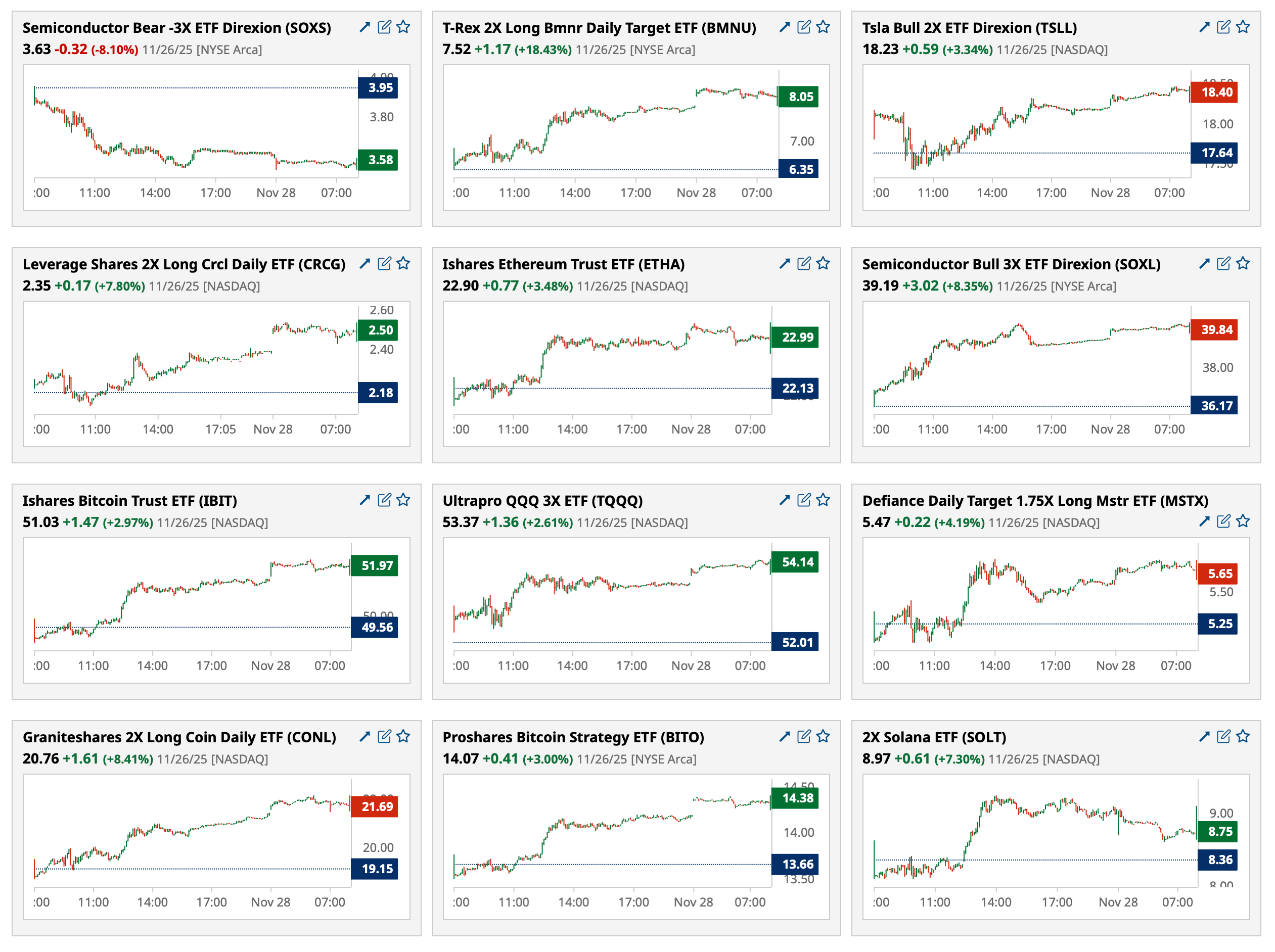

Closing Breadth, Sectors and Movers

Closing Breadth

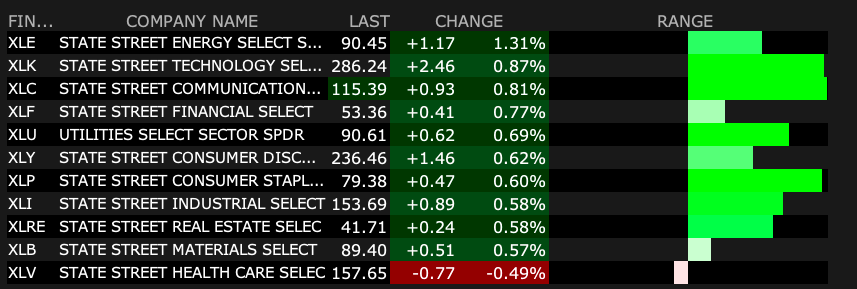

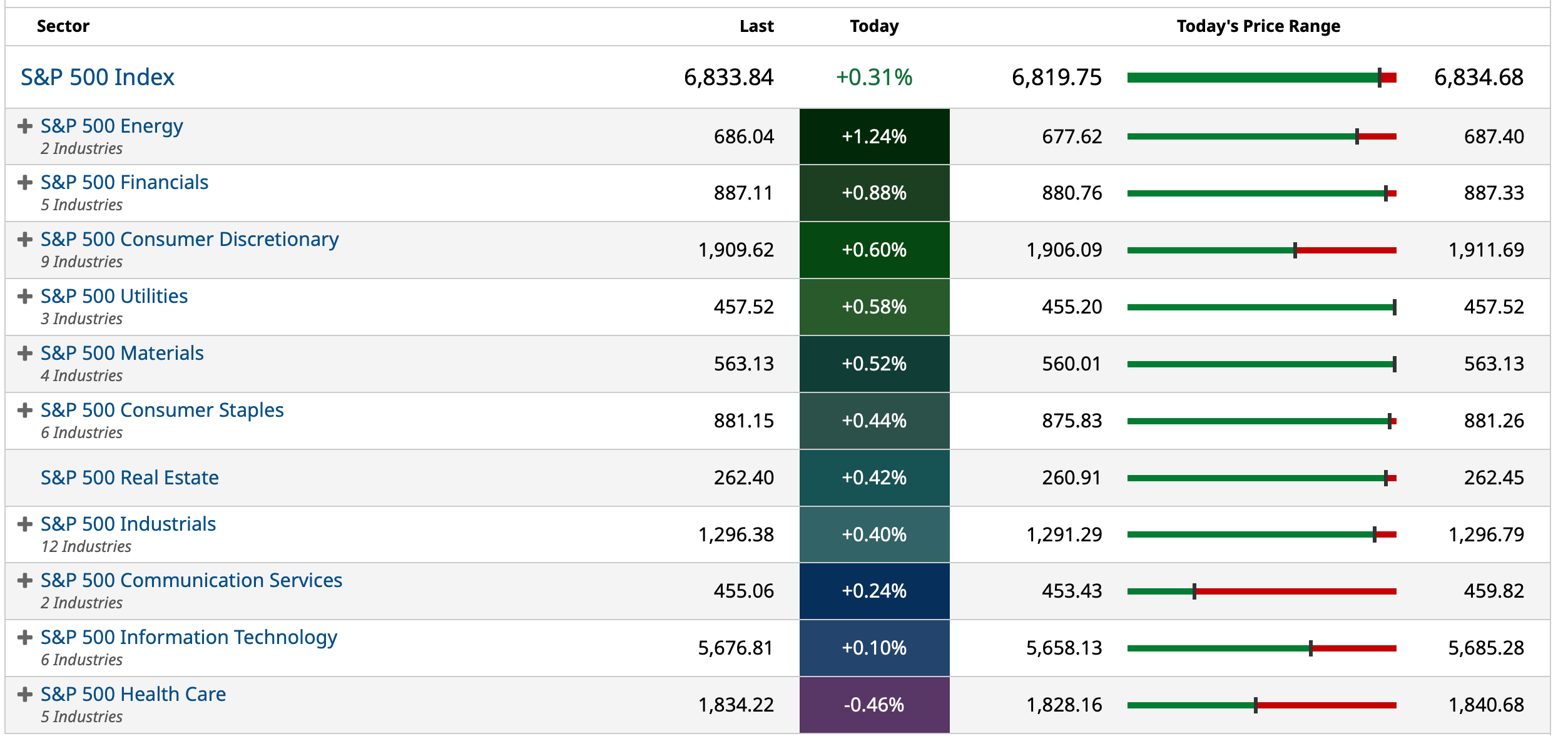

Sector ETFs

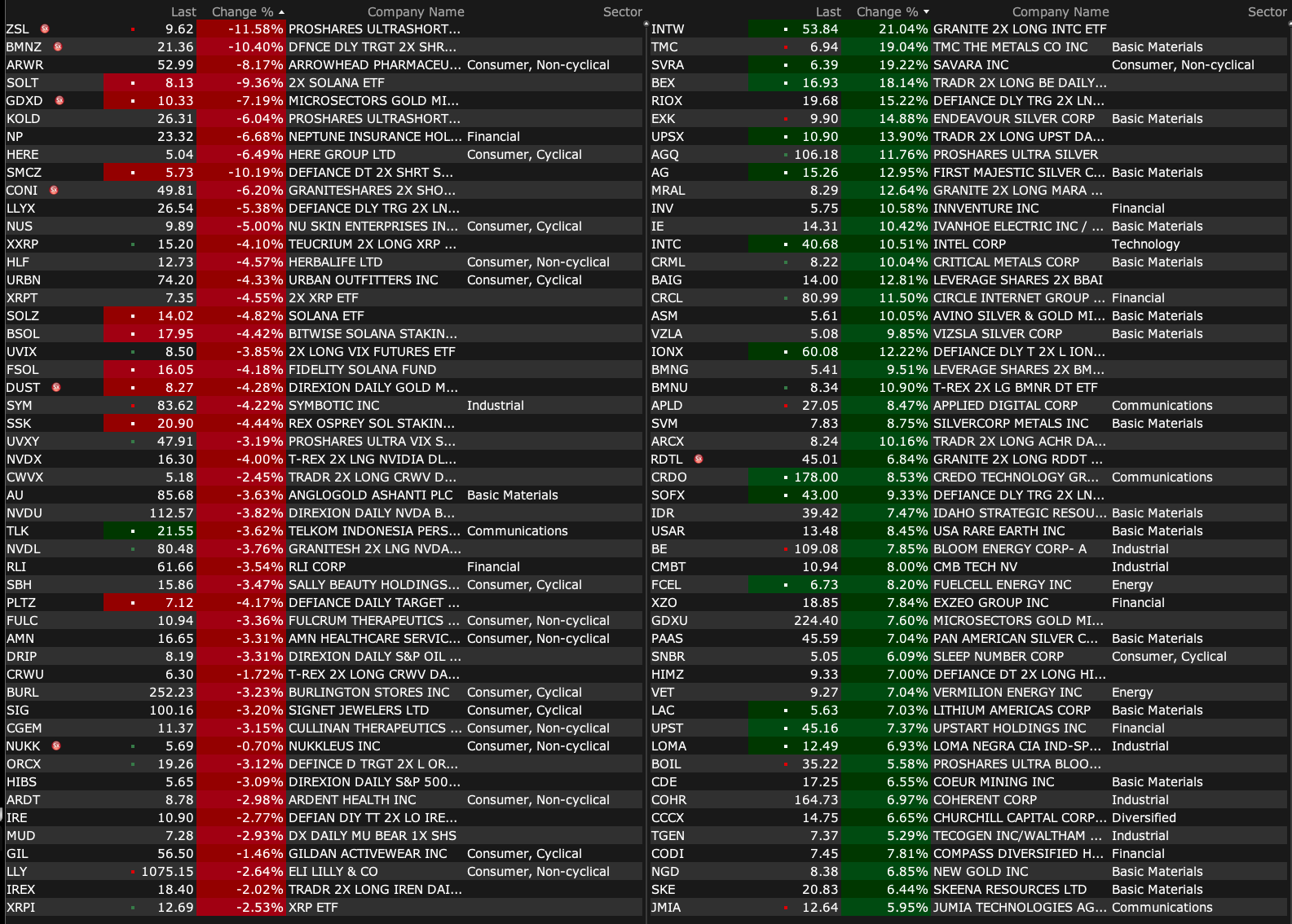

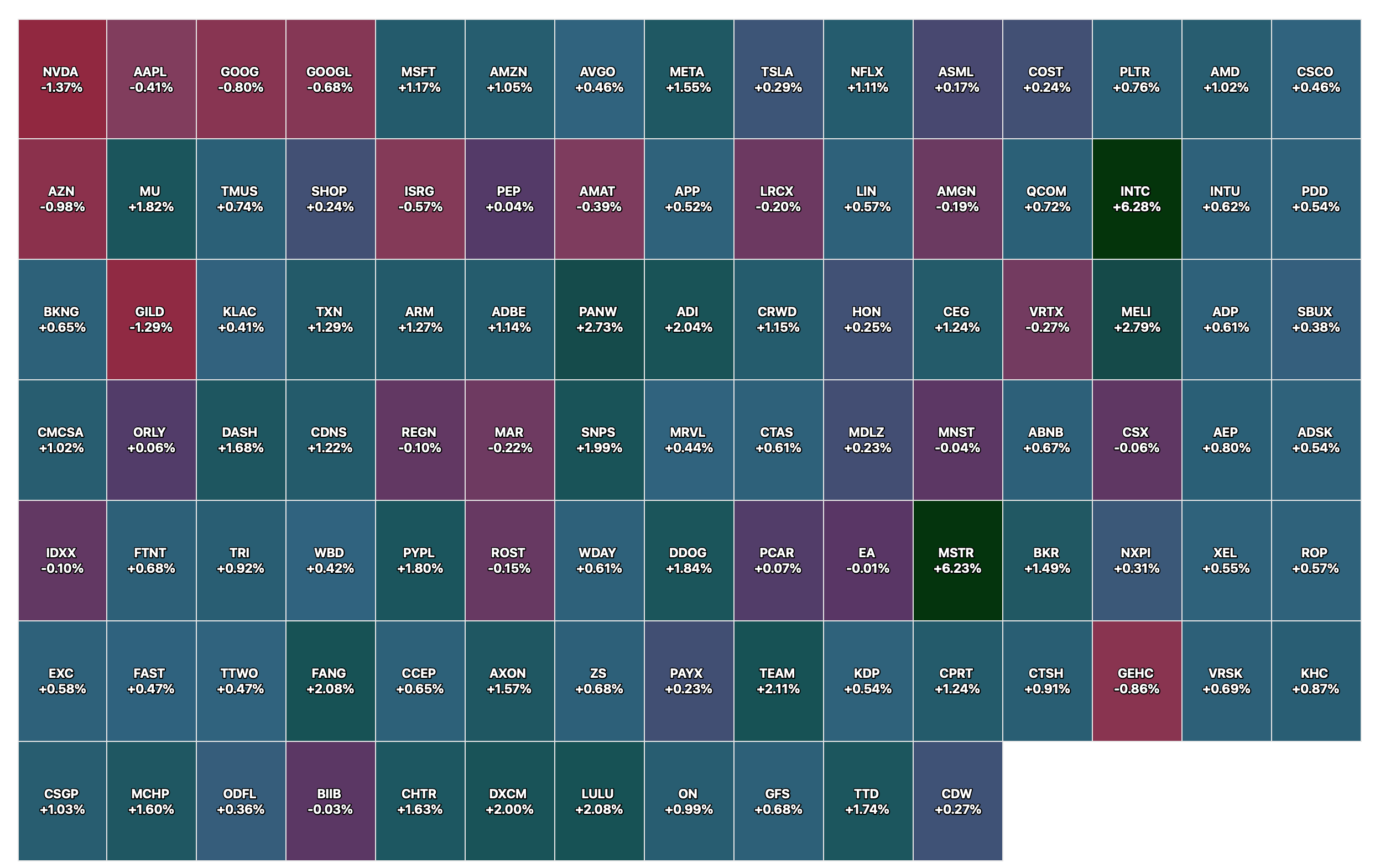

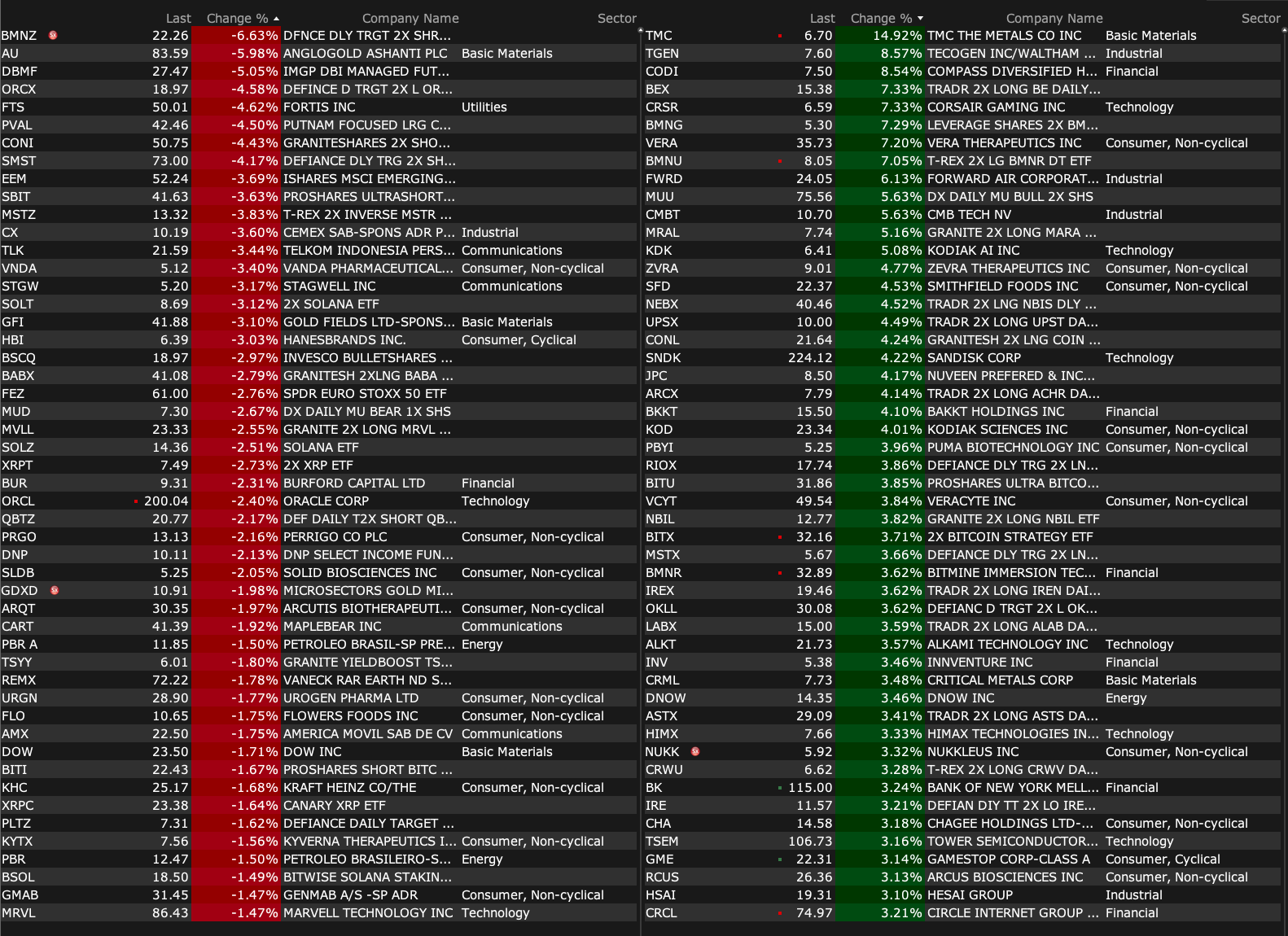

% Movers

BY Doug Kass · Nov 28, 2025, 1:30 PM EST

BY Doug Kass · Nov 28, 2025, 1:30 PM EST

Warm holiday wishes to our subs, contributors, editors and management.

Enjoy the long weekend with your family and friends.

Be safe.

I will see you back early Monday morning.

I will be delivering a lengthy and multi-part tome on my market outlook upon my return in three days.

It is good food for thought — for bulls and bears, alike.

That said... I am often wrong and always in doubt!

BY Doug Kass · Nov 28, 2025, 1:00 PM EST

From Peter Boockvar:

Positives,

1) The GenAI tech trade is no longer a one way ride and investors need to start differentiating.

2) While possibly distorted by the holidays, jobless claims which for the week ended 11/22 totaled 216k, 9k below expectations and vs 222k in the week before.

3) In the weekly MBA data and right ahead of the holidays, purchase applications jumped 7.6% w/o/w but refi’s fell for a 4th straight week by 5.7%. While the data is seasonally adjusted, it’s still noisy around the holidays.

4) Pending home sales in October rose 1.9% m/o/m after a flat read in September and that was above the forecast of a slight .2% rise.

5) While the durable goods figure was for September and is old news, the non defense capital goods ex aircraft rise of .9% m/o/m was 6 tenths above expectations and August was revised to a .9% increase from the first print of .4%. Are we seeing the beginnings of the non-AI CapEx lift in response to the OBBB? Hopefully.

6) While headline September PPI was as expected up by .3% m/o/m, the core rate gain of .1% was one tenth below the forecast.

7) For the sake of the first time home buyer, home prices in September rose just 1.3% y/o/y according to S&P Cotality’s national home price index.

8) From Best Buy: “For the most part, customer shopping behavior in Q3 did not change materially from the commentary we have shared for the past several quarters. Customers remain resilient, but deal focused, and attracted to more predictable sales moments, including our back-to-school sales events and our Techtober sales held in close proximity to the October Prime Day event.”

9) From DICK’s Sporting Goods: “Q3 comps increased 5.7% with growth in average ticket and transactions…We also saw broad based strength across our three primary categories of footwear, apparel, and hardlines...The consumer is focused on sport, and we are right sitting at the middle of the intersection of sport and culture.”

10) From Burlington Stores: “Traffic to our stores fell off significantly after the back-to-school period driven by unseasonably warm temperatures in our major markets. Our comp trend then picked up to mid-single-digits in mid-October once the weather cooled, and that strong trend has continued through the first three weeks of November.”

11) From Dell Technologies: “AI server demand remained exceptionally strong.” In their Client Solutions Group which includes PCs, laptops, desktops, etc…, “Demand from small and medium business remained strong…Consumer revenue declined 7%, although the demand environment turned to growth as we refocused on expanding where we play in the market. Commercial profitability was stable, while consumer and education were competitive. The PC refresh cycle remains durable, supported by an aging installed base and a significant portion of systems not yet upgraded to Windows 11.”

12) From HP: “We drove worldwide PC market share gains, particularly in high value categories, including commercial and consumer premium and workstations. With 40% of installed base still on Windows 10 at the end of Q4, the Windows 11 refresh will remain a tailwind for the PC market into 2026. And demand for AI PCs continues to accelerate, now representing more than 30% of our shipments this quarter.”

13) From Workday: “the headcount of our customer base is up y/o/y. So while there are some layoffs out there, we’re still growing headcount across our customer base. And what we’re doing…we are selling back into our base, and we’re focused not on just seats, but actually revenue per seat.”

14) The Reserve Bank of New Zealand cut rates but that could be it through next year. They said, “We have published a central projection that would be consistent with the official cash rate being on hold through the course of 2026 and one where we feel the risks are balanced. If the OCR was to change over the next three to six months, it might be more likely to go down than up.”

15) The Bank of Korea held rates at 2.5% as expected.

16) The November Economic Confidence index in the Eurozone rose a touch to 97 from 96.8 with services, retail and construction gains offsetting a drop in manufacturing.

17) French November CPI rose .8% y/o/y, better than the estimate of up 1%.

18) Italian CPI was up 1.2% in November as expected.

19) German unemployment rose by 1k in November, less than the estimate of up 4.3k though the unemployment rate held at 6.3%, a 5 yr high.

Negatives,

1) The GenAI tech trade is no longer a one way ride and investors need to start differentiating.

2) The ADP weekly jobs report (reflects four week average) saw a job decline of 13,500.

3) The conclusions from the Fed’s Beige Book still point to a still highly mixed and uneven US economy. “Economic activity was little changed since the previous report, according to most of the twelve Federal Reserve Districts, though two Districts noted a modest decline and one reported modest growth.”

4) Continuing claims for the less holiday influenced week of 11/15 totaled 1.96mm, remaining around levels seen in November 2021.

5) The November consumer confidence index from the Conference Board fell to 88.7 from 95.5, below the estimate of 93.3 and the 2nd weakest print since January 2021. Both main components were down m/o/m. One yr inflation expectations held at 5.7% on average with a median read of 4.8% vs 4.6% in October. The answers to the labor market questions were mixed. Spending intentions fell for autos, homes and major appliances. Not surprisingly, this is what continues to be the wet blanket on consumer confidence, “Consumers’ write in responses pertaining to factors affecting the economy continued to be led by references to prices and inflation, tariffs and trade, and politics, with increased mentions of the federal government shutdown. Mentions of the labor market eased somewhat but still stood out among all other frequent themes not already cited.” Finally of note, “Assessments of current financial situations collapsed to the lowest level since August 2024, when a confluence of negative events stoked a brief financial market selloff and US recession concerns.”

6) The Richmond November manufacturing survey fell to -15 from -4.

7) The November Dallas manufacturing index remained in contraction at -10.4 vs -5 in October and vs the estimate of -2.0.

8) The Dallas November services index stayed negative at -2.3 vs -9.4 in the month before.

9) The November Philly non-manufacturing index was -16.3 vs -22.2.

10) September core retail sales fell one tenth vs the estimate of up .3% but off a .6% gain in August (revised down by one tenth) .

11) From BJ’s Wholesale: “Looking at the behavior of our membership base this quarter, we continued to see members across all income levels remain cautious, which tracks with what we broadly see in the consumer confidence data. We saw members exhibiting value seeking behavior, including higher sensitivity to promotions, increasing purchasing of private label items, and some trade down. For example, given the high price of beef, we saw higher purchasing of ground beef versus more expensive cuts. Despite this type of behavior, member trends exhibited stability q/o/q across all cohorts when adjusting for the noise from the port strike.”

12) From Kohl’s: “we continue to operate in an environment where our customers are becoming increasingly choiceful, as their discretionary income remains pressured. This is especially notable in our low to middle income consumers, as well as in our younger customers. These customers are becoming increasingly savvy and are seeking more value. We expect this customer behavior to continue into the fourth quarter, as we believe the macroeconomic environment will remain uncertain.”

13) From Central Garden & Pet: With overall guidance, “We think ‘26 is going to be extremely challenging...we’ve got a little bit of a headwind with tariffs. Consumer confidence is at a low point right now. So, we really need to see how the consumer is going to react to pricing and really their behavior, and the whole notion of the bifurcation of income right now is very real. We’re seeing it in both of our categories.”

14) From JM Smucker: “Consumers continue to seek value and prioritize their spending, which our portfolio is well positioned for, as it features offerings across the value spectrum, in the attractive categories of coffee, snacking and pet.”

15) From HP: “In print, revenue declined 4%, reflecting market softness and delayed purchasing decisions across all regions.”

16) From American Woodmark: “Demand trends remain challenged in both the new construction and remodel markets.” They are also getting hit hard by tariffs. “We estimate the unmitigated tariff impact at the current rates, in effect as of today’s date, to represent approximately 4-4.5% of the Company’s annualized net sales with the impact varying by product category. This impact does not include the potential increase on Section 232 tariffs to 50%.”

17) In Australia, October CPI rose 3.8% y/o/y, above the estimate of up 3.6% and the trimmed mean rate of 3.3% was 3 tenths higher than anticipated.

18) Inflation in Japan remained high in November as Tokyo CPI rose 2.8% y/o/y ex food and fuel, but as expected.

19) The November German IFO business confidence index slipped to 88.1 from 88.4 and that was under the estimate of 88.5. The 1 pt drop in Expectations was partly offset by a slight gain in the Current Assessment. The IFO said simply on German business, “They have little faith that a recovery is coming anytime soon.”

20) German consumer confidence from GFK remained deeply negative at -23.2 but a touch less so vs -24.1 in the month before.

21) German retail sales fell .3% m/o/m in October vs the estimate of up .2%.

22) Spanish CPI in November rose 3.1% y/o/y, one tenth more than forecasted.

23) German CPI was up 2.6% y/o/y in November, above expectations of 2.4%.

BY Doug Kass · Nov 28, 2025, 12:45 PM EST

BY Doug Kass · Nov 28, 2025, 12:30 PM EST

Kimberly-Clark (KMB) trading higher (again) as it takes the cue from an improving Kenvue (KVUE) .

BY Doug Kass · Nov 28, 2025, 12:26 PM EST

BY Doug Kass · Nov 28, 2025, 12:24 PM EST

BY Doug Kass · Nov 28, 2025, 11:56 AM EST

Long (MSFT) , (META) , (AMZN)

Short (AAPL) , (NVDA)

BY Doug Kass · Nov 28, 2025, 11:33 AM EST

BY Doug Kass · Nov 28, 2025, 11:29 AM EST

I am adding to my small index shorts on a scale.

I most recently, shorted:

(SPY) $682.54

(QQQ) $617.51

BY Doug Kass · Nov 28, 2025, 11:07 AM EST

- NYSE volume 33% below its one-month average

- NASDAQ volume 41% below its one-month average

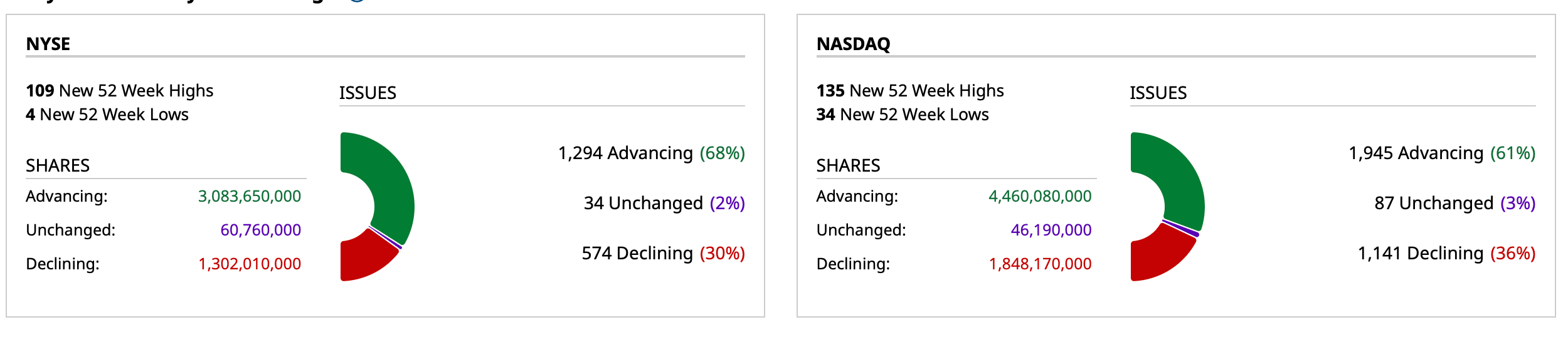

- VIX index: down 2.38% to 16.80 Breadth

BY Doug Kass · Nov 28, 2025, 11:04 AM EST

I'm shorting (AAPL) at $277.37 and (NVDA) at $178.98.

BY Doug Kass · Nov 28, 2025, 9:56 AM EST

With S&P cash +14 handles I am adding to my index shorts:

* (SPY) $681.51

* (QQQ) $616.87

BY Doug Kass · Nov 28, 2025, 9:44 AM EST

We recently (last Friday) initiated new buys in (META) , (AMZN) and (MSFT) during the November whoosh lower:

I have purchased very small long positions in (MSFT) at $469.87, (AMZN) at $216.75 and (META) at $585.27.

Position: Long MSFT (VS), AMZN (VS), META (VS)

By Doug Kass Nov 21, 2025 11:40 AM EST

On further strength I plan to short (NVDA) and (AAPL) .

I have no current plans to reduce my other Mag 7 longs.

BY Doug Kass · Nov 28, 2025, 9:25 AM EST

Upside:

-BEAT +36% (provides update on Regulatory Path Following FDA Decision on 12-Lead ECG Synthesis Software Application)

-VUZI +6.7% (received and fulfilled a series of follow-on volume orders in Q4 of 2025 for custom M400 smart glasses kits totaling nearly $1M)

-WLDS +4.8% (announces a Warrant Inducement Transaction at $1.71/shr for $5.68M in Gross Proceeds)

-SNDK +4.1% (memory sector strength; replaces IPG in the S&P 500 Index)

-CRCL +3.2% (S&P cuts Stablecoin issuer, rival Tether to ‘weak’)

-GME +3.2% (momentum)

-MU +2.9% (memory sector strength)

Downside:

-TLRY -14% (earnings, guidance)

-ORCL -2.4% (reportedly group of banks are in discussions to lend another $38B for ORCL and data centre builder Vantage to fund additional sites for OpenAI)

BY Doug Kass · Nov 28, 2025, 9:15 AM EST

BY Doug Kass · Nov 28, 2025, 9:00 AM EST

Bonus — Here are some good links:

When the S&P Is Up Big Before Thanksgiving

BY Doug Kass · Nov 28, 2025, 8:47 AM EST

I am wondering if (SPY) and (QQQ) moves are exaggerated given the futures showdown — insofar as the only way to hedge a short is to buy index ETFs.

Just talking out loud...

BY Doug Kass · Nov 28, 2025, 8:31 AM EST

Shorting more indices (820 AM):

* (SPY) $681.80

* QQQ $617.07

BY Doug Kass · Nov 28, 2025, 8:29 AM EST

BY Doug Kass · Nov 28, 2025, 8:26 AM EST

Late start.

On Los Angeles time.

Back in a few.

BY Doug Kass · Nov 28, 2025, 7:58 AM EST