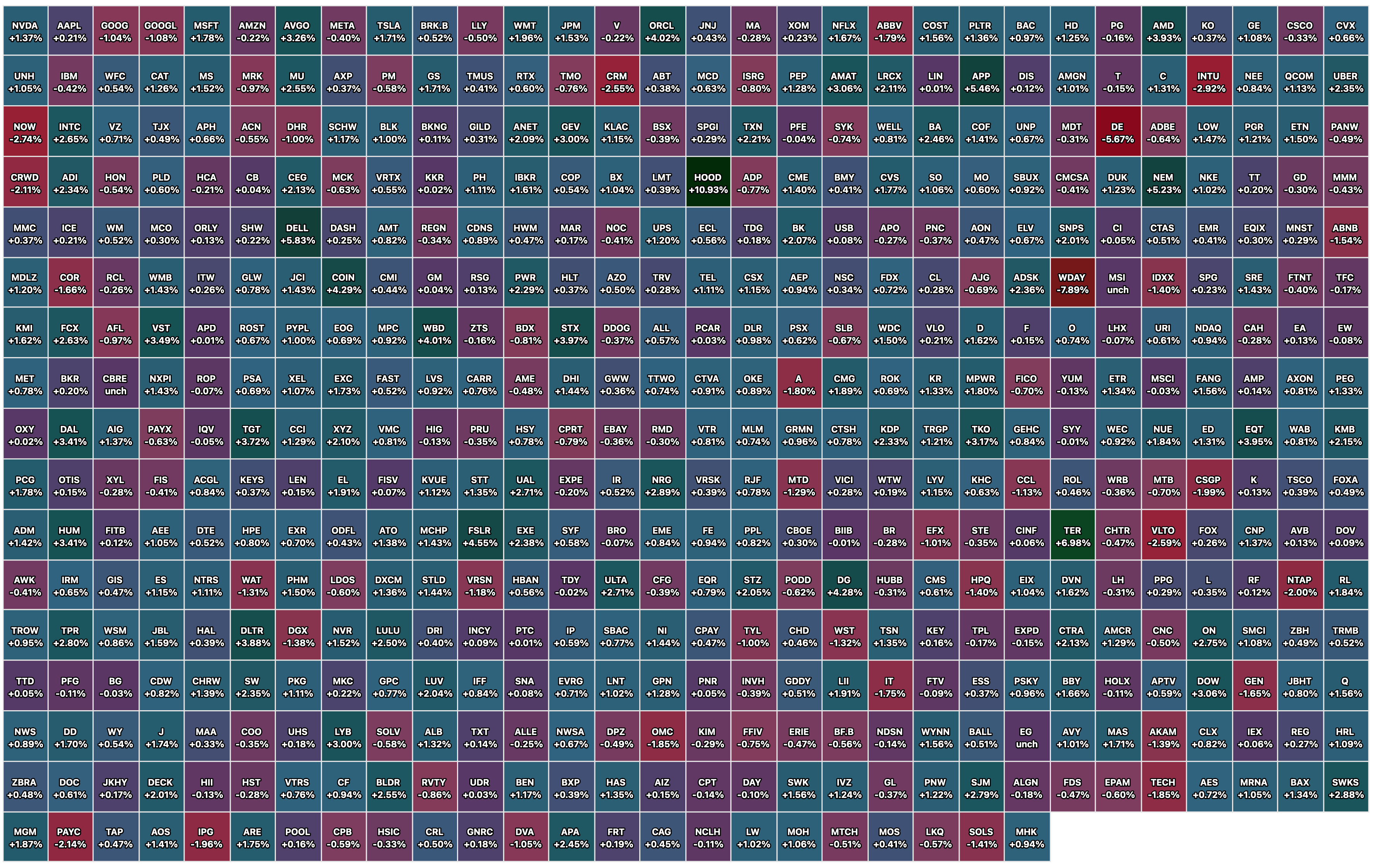

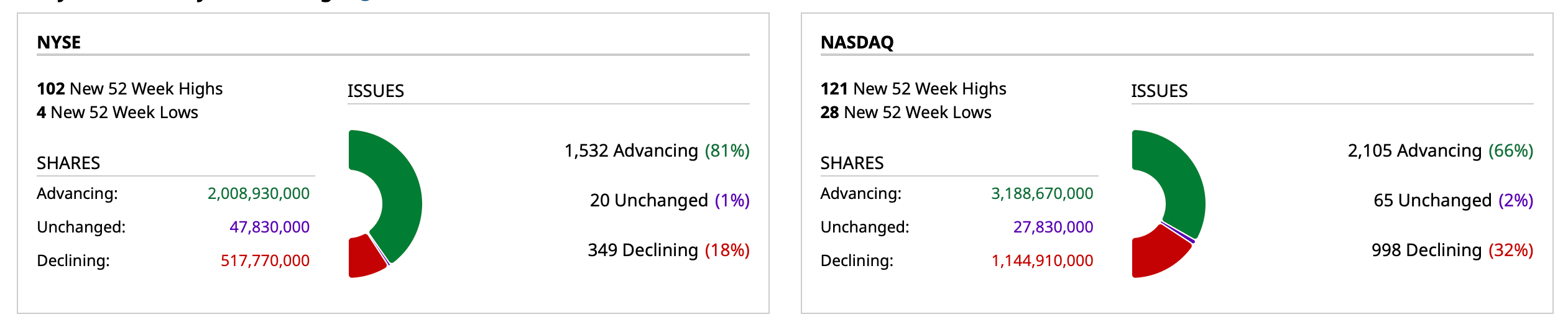

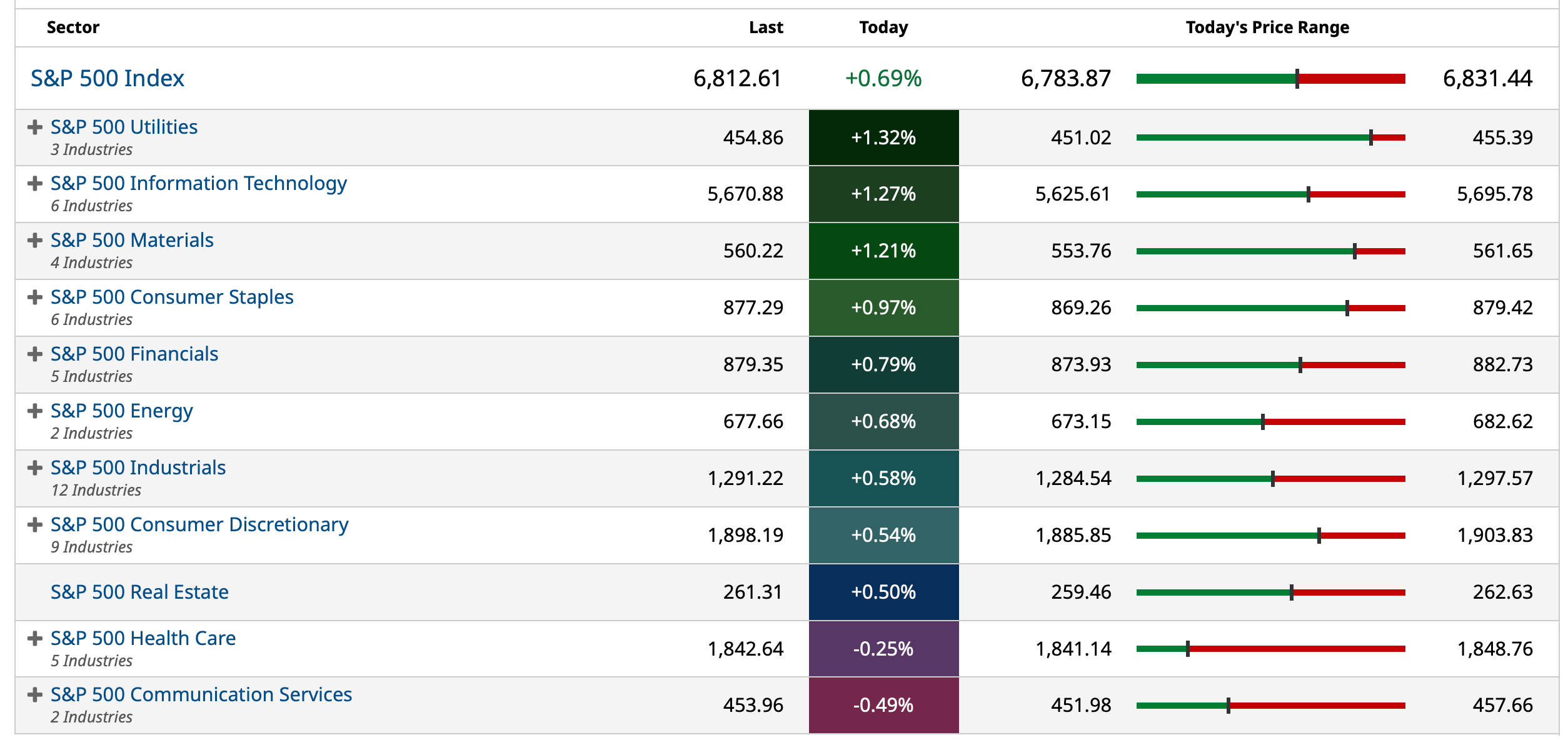

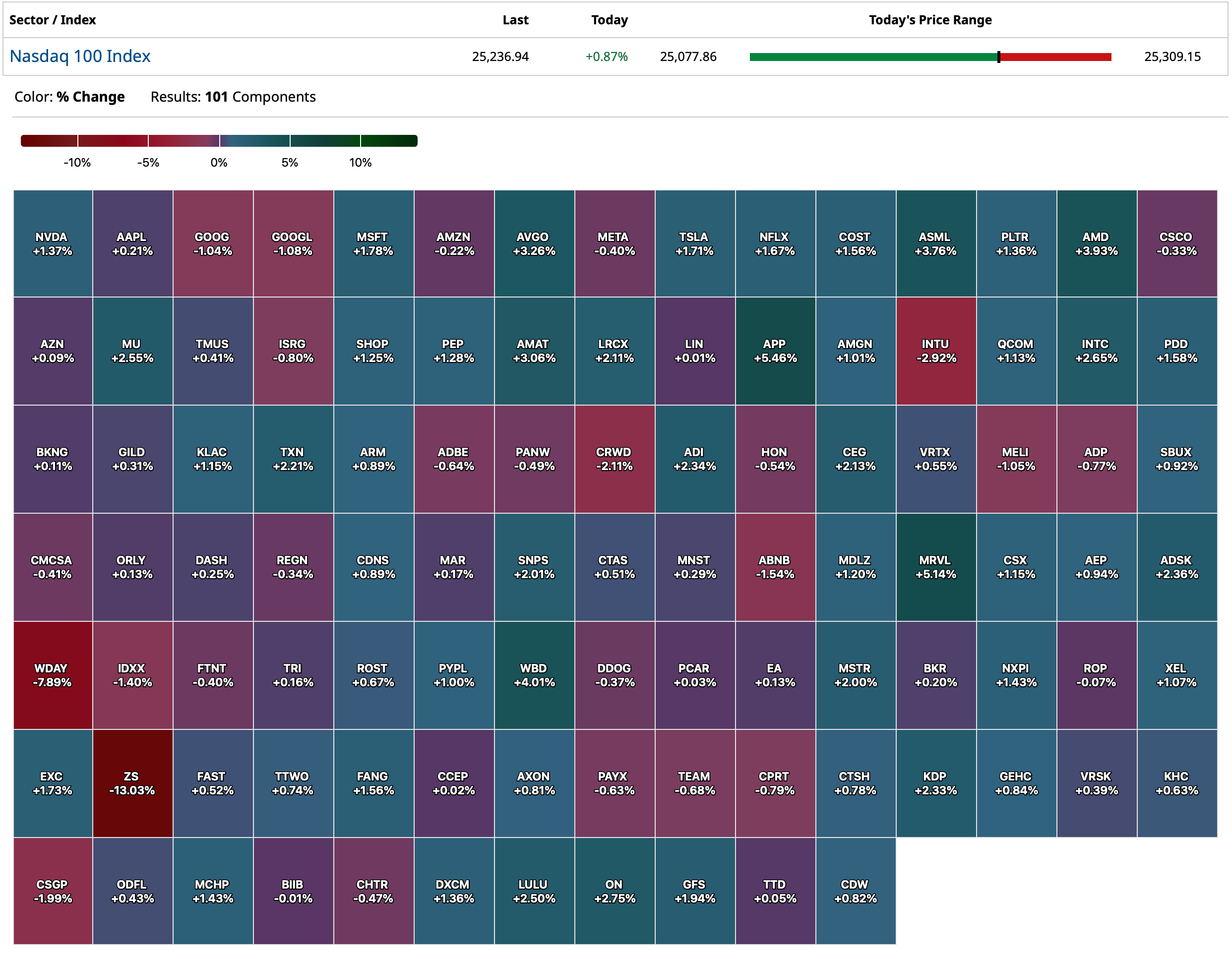

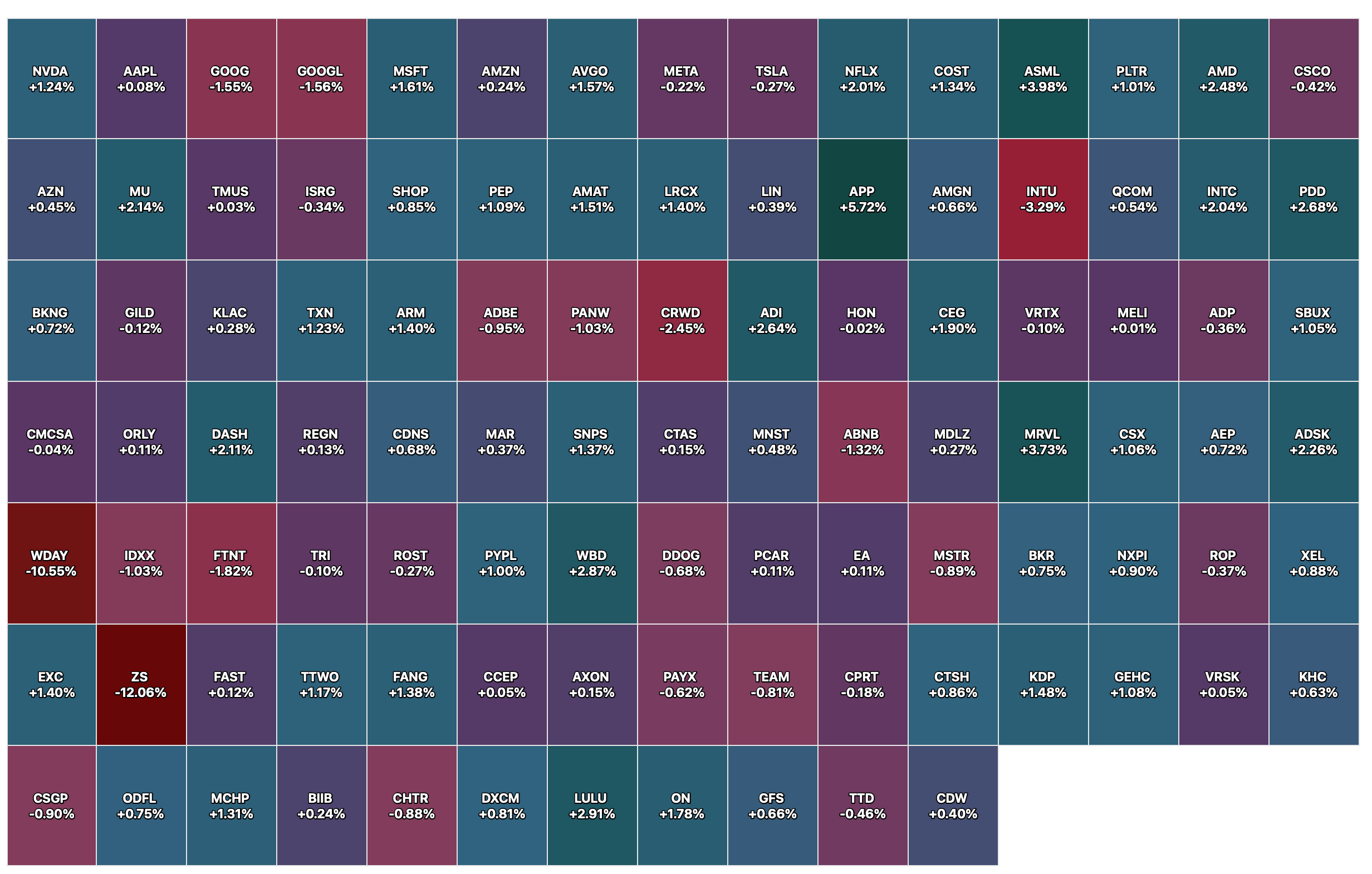

Closing S&P 500 Heat Map

BY Doug Kass · Nov 26, 2025, 4:40 PM EST

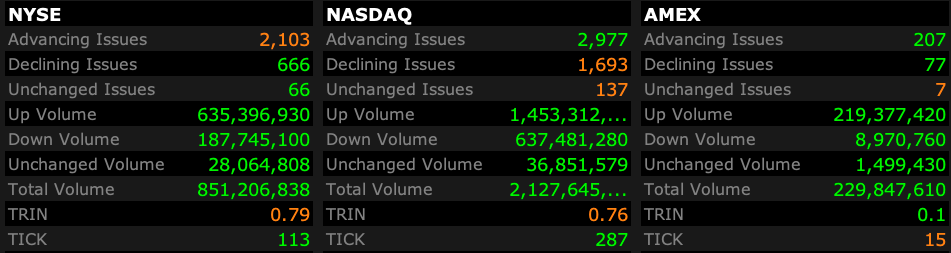

BY Doug Kass · Nov 26, 2025, 4:40 PM EST

BY Doug Kass · Nov 26, 2025, 4:30 PM EST

A very warm and happy Thanksgiving to all of our subs, contributors and editors!

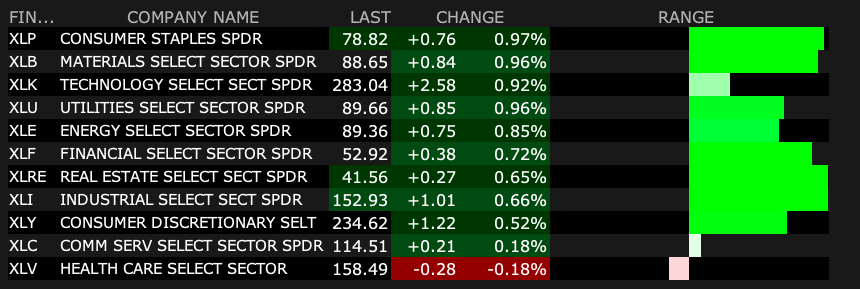

BY Doug Kass · Nov 26, 2025, 3:50 PM EST

BY Doug Kass · Nov 26, 2025, 3:31 PM EST

BY Doug Kass · Nov 26, 2025, 3:20 PM EST

From Peter Boockvar:

The key points from the Fed's Beige Book

Here were the notable comments from the just released Fed Beige Book and while not hard data, it is a compilation of a broad reach of business contacts and still sounds like a highly uneven economy with growth in some places and contraction in others.

“Economic activity was little changed since the previous report, according to most of the twelve Federal Reserve Districts, though two Districts noted a modest decline and one reported modest growth.”

“Overall consumer spending declined further, while higher-end retail spending remained resilient. Some retailers noted a negative impact on consumer purchases from the government shutdown, and auto dealers saw declines in EV sales following the expiration of the federal tax credit. Reports of travel and tourism activity reflected little change in recent weeks, with some contacts noting cautious discretionary spending among consumers.”

“Manufacturing activity increased somewhat, according to most Districts, though tariffs and tariff uncertainty remained a headwind.”

“Revenues in the nonfinancial services sector were mostly flat to down, and reports of loan demand were mixed.”

“Some Districts reported declines in residential construction, while others said it was unchanged, and home sales activity varied. A few Districts noted ongoing recovery in the office real estate market.”

“Outlooks were largely unchanged overall. Some contacts noted an increased risk of slower activity in coming months, while some optimism was noted among manufacturers.”

On the labor market, “Employment declined slightly over the current period with around half of Districts noting weaker labor demand. Despite an uptick in layoff announcements, more Districts reported contacts limiting headcounts using hiring freezes, replacement-only hiring, and attrition than through layoffs. In addition, several employers adjusted hours worked to accommodate higher or lower than expected business volume instead of adjusting the number of employees.”

“A few firms noted that artificial intelligence replaced entry-level positions or made existing workers productive enough to curb new hiring. Across most Districts, employers had an easier time finding workers, but there were still pockets of difficulty related to certain skilled positions and fewer immigrant workers.”

This is what was said on inflation, “Prices rose moderately during the reporting period. Input cost pressures were widespread in manufacturing and retail, largely reflecting tariff-induced increases. Some Districts noted rising costs for insurance, utilities, technology, and health care. The extent of passthrough of higher input costs to customers varied, and depended upon demand, competitive pressures, price sensitivity of consumers, and pushback from clients. There were multiple reports of margin compression or firms facing financial strain stemming from tariffs. Prices declined for certain materials, which firms attributed to sluggish demand, deferred tariff implementation, or reduced tariff rates. Looking ahead, contacts largely anticipate upward cost pressures to persist but plans to raise prices in the near term were mixed.”

BY Doug Kass · Nov 26, 2025, 2:30 PM EST

No trades since last recorded!

BY Doug Kass · Nov 26, 2025, 2:19 PM EST

BY Doug Kass · Nov 26, 2025, 12:45 PM EST

BY Doug Kass · Nov 26, 2025, 12:28 PM EST

I have a business lunch and later on in the afternoon a research call from 3PM to 4PM.

BY Doug Kass · Nov 26, 2025, 11:55 AM EST

- NYSE volume 23% below its one-month average;

- Nasdaq volume 43% below its one-month average;

- VIX index: down 4.42% to 17.74

BY Doug Kass · Nov 26, 2025, 11:35 AM EST

Speaking of defensives, (PEP) is picking up a bid again today.

BY Doug Kass · Nov 26, 2025, 11:15 AM EST

BY Doug Kass · Nov 26, 2025, 11:11 AM EST

I am adding to my (JOET) short. (42.06)

BY Doug Kass · Nov 26, 2025, 10:56 AM EST

* How does this end well?

The discussion over the last few days -- and for that matter, months -- has been focused more on AI than anything else. Other, more fundamental and enduring concerns have been put on the back burner.

One of those core concerns is the absence of any fiscal discipline from either political party in Washington, D.C. (I will be discussing this at more length on Monday morning).

This is sheer madness.

Government spending was up 18% year over year last month. The deficit is exploding. The U.S. government has borrowed $2.2 trillion already this year with over a month left, or 6% of gross domestic product, and this is while the economy is OK.

DOGE is effectively dead and this is with Republicans controlling the government and Congress and Democrats caving in on the government shutdown. Inflation is running well above targeted levels, and they are telling us to expect 3%-4% GDP growth next year, thanks to tax cuts and other things. Pres. Trump wants to appoint Kevin Hassett as the head of the Fed to aggressively cut rates? How is this supposed to end well?

Energy prices are about as low as can go, too. How do we not have a big inflation problem, again? Will rate markets figure this out? Can gold go to $50,000?

Also, now the administration wants to send out the $2,000 checks on top of it all.

Didn’t they learn last time under Pres. Biden what this does? It blows out the deficit more, more money into the economy, more inflation. This is when “affordability” is the biggest issue being faced from a political perspective, too. Handing out money has the opposite of its theoretical intended consequences. This is all so absurd.

BY Doug Kass · Nov 26, 2025, 10:15 AM EST

(KMB) up by an additional +$2 - the world's fair this week.

BY Doug Kass · Nov 26, 2025, 10:00 AM EST

With S&P cash up 37 handles, I have moved from very small- to small-sized short the indexes:

* (SPY) $679.02

* (QQQ) $613.32

BY Doug Kass · Nov 26, 2025, 9:58 AM EST

From Peter Boockvar:

On the eve of Thanksgiving, I am thankful each day for you who takes the time out to read what I write.

He hasn’t even been appointed yet but Kevin Hassett has already been anointed by Wall Street ‘The Easy Money Man.’ If it were so easy but if there is one thing we’ve learned over the past 25 years plus with easy money and the Fed put, booms and busts and lackluster growth (7 yrs of zero rates came with a lame GFC recovery) come as part of that and as seen also in Japan and Europe, cheap money doesn’t necessarily lead to quicker economic growth. And I will say too, everyone needs to read the economic room. That room is filled with people that are angry about 5 years of much higher inflation, the challenging cost of living and cost pressure issues for small and medium sized businesses. If easier money ends up restoking inflation, not only will that be bad for the economy, the long end of the US yield curve will have its say as well and same with the value of the US dollar by weakening.

I argue that inflation (not necessarily the rate of change right now but the cumulative damage of it) is the disease and a softening labor market is the symptom. We need stable, low prices as the foundation for a healthier economy that eventually leads to more hiring. I’ll give the Fed another rate cut but as it will take the effective rate to about 3.63%, it would be barely above the rate of inflation, under 1% give or take. There is no good economic history when that REAL rate gets to zero or negative.

Speaking of Japan, it looks like we just might get another rate hike in December. Reuters today is reporting that “The Bank of Japan is preparing markets for a possible interest rate hike as soon as next month, sources say, reviving hawkish language as worries about sharp yen declines return and political pressure for the bank to keep rates low fades. A change in BoJ messaging over the past week has shifted focus back to inflationary risks of a weak yen from earlier worries about the US economy, comments aimed at reminding markets a December rate hike was still a prospect, two people familiar with the bank’s thinking told Reuters.” JGB yields were only slightly higher in response and the yen is weaker too as it’s still a ‘believe it when you see it’ type situation with the feet dragging BoJ when it comes to rate moves.

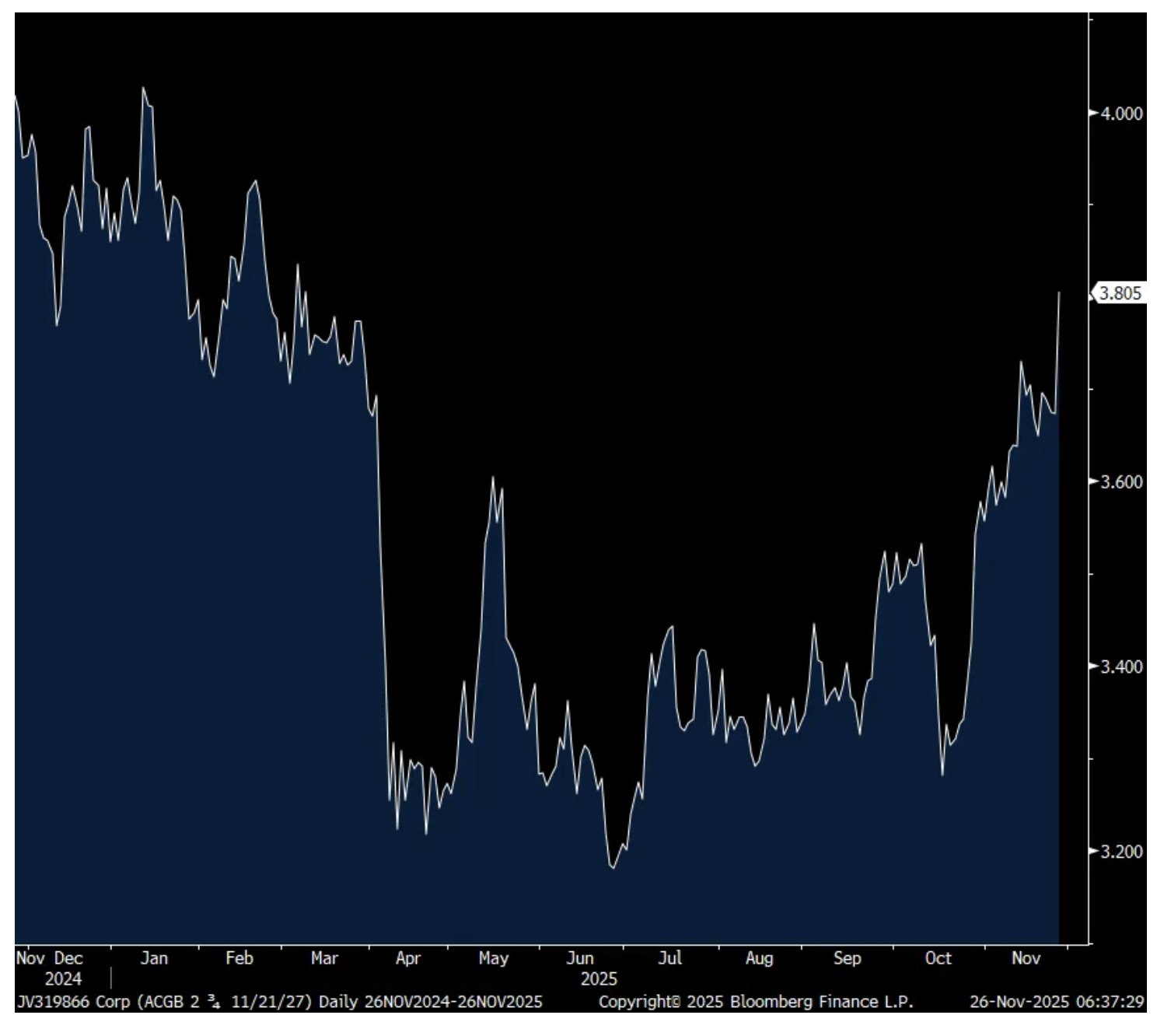

Aussie yields jumped overnight after October CPI rose 3.8% y/o/y, above the estimate of up 3.6% and the trimmed mean rate of 3.3% was 3 tenths higher than anticipated. The 2 yr Aussie yield jumped by 13 bps to 3.81% in response and the 10 yr yield was higher by 10 bps. The Aussie$ is higher for a 4th straight day vs the USD.

The Reserve Bank of New Zealand cut rates but that could be it through next year. They said, “We have published a central projection that would be consistent with the official cash rate being on hold through the course of 2026 and one where we feel the risks are balanced. If the OCR was to change over the next three to six months, it might be more likely to go down than up.” On the hawkish cut, the 2 yr yield jumped 8 bps.

Aussie 2 yr yield

To some earnings calls.

From Best Buy:

“We continue to drive strong sales performance across computing, gaming, and mobile phones. We also saw growth in other categories, including wearables and headphones. This growth was partially offset by declines in the home theater, appliance, and drone categories.”

“For the most part, customer shopping behavior in Q3 did not change materially from the commentary we have shared for the past several quarters. Customers remain resilient, but deal focused, and attracted to more predictable sales moments, including our back-to-school sales events and our Techtober sales held in close proximity to the October Prime Day event.”

“September, which was relatively quiet outside of the Labor Day sales event, had the slowest growth of the quarter. Importantly, while customers continue to be thoughtful about big ticket purchases in the current environment, they are willing to spend on high price point products when they need to or when there is technology innovation.”

From DICK’S Sporting Goods:

“Q3 comps increased 5.7% with growth in average ticket and transactions…We also saw broad based strength across our three primary categories of footwear, apparel, and hardlines.”

And what helped the business? “Everything from newness from our strategic partners to emerging brands, our vertical brands, consumers, athletes are really resonating with the products that we are providing. And at the same time, our entire team is fully focused on delivering an engaging athlete experience. So, that’s in our stores, that’s our digital environment.”

“The consumer is focused on sport, and we are right sitting at the middle of the intersection of sport and culture.”

From Kohl’s:

“we continue to operate in an environment where our customers are becoming increasingly choiceful, as their discretionary income remains pressured. This is especially notable in our low to middle income consumers, as well as in our younger customers. These customers are becoming increasingly savvy and are seeking more value. We expect this customer behavior to continue into the fourth quarter, as we believe the macroeconomic environment will remain uncertain.”

From Dell Technologies:

“AI server demand remained exceptionally strong.”

In their Client Solutions Group which includes PCs, laptops, desktops, etc…, “Demand from small and medium business remained strong…Consumer revenue declined 7%, although the demand environment turned to growth as we refocused on expanding where we play in the market. Commercial profitability was stable, while consumer and education were competitive. The PC refresh cycle remains durable, supported by an aging installed base and a significant portion of systems not yet upgraded to Windows 11.”

From HP:

“We drove worldwide PC market share gains, particularly in high value categories, including commercial and consumer premium and workstations. With 40% of installed base still on Windows 10 at the end of Q4, the Windows 11 refresh will remain a tailwind for the PC market into 2026. And demand for AI PCs continues to accelerate, now representing more than 30% of our shipments this quarter.”

“In print, revenue declined 4%, reflecting market softness and delayed purchasing decisions across all regions.”

From Workday:

“the headcount of our customer base is up y/o/y. So while there are some layoffs out there, we’re still growing headcount across our customer base. And what we’re doing…we are selling back into our base, and we’re focused not on just seats, but actually revenue per seat.”

BY Doug Kass · Nov 26, 2025, 9:50 AM EST

BY Doug Kass · Nov 26, 2025, 9:23 AM EST

Microsoft (MSFT) is enjoying a substantial run in premarket trading - now up by almost $9.

I suspect the reason for the strength is some catch-up from recent weakness and the expectation that the Google AI narrative went a bit too far. (See (ORCL) and (NVDA) "ketchup" in premarket trading).

We initiated a new long in the name late last week:

I have purchased very small long positions in (MSFT) at $469.87, (AMZN) at $216.75 and (META) at $585.27.

Position: Long MSFT (VS), AMZN (VS), META (VS)

By Doug KassNov 21, 2025 11:40 AM EST

BY Doug Kass · Nov 26, 2025, 9:10 AM EST

BY Doug Kass · Nov 26, 2025, 9:08 AM EST

Treasury Auctions:

11:00 a.m.: Treasury announces a 3 and 6 month bill auction;

11:30 a.m.:Treasury hosts a $100B 4 and $85B 8 Week Bill Auction;

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

11:30 a.m.: Treasury hosts a $44B 7-YearNote Auction*

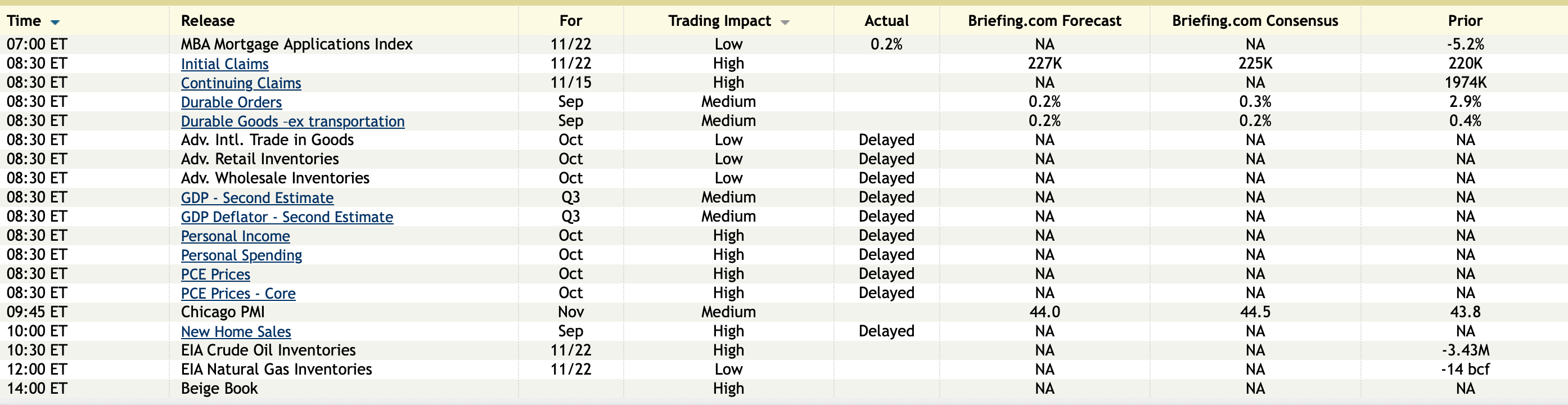

Today’s Economic Calendar

BY Doug Kass · Nov 26, 2025, 9:00 AM EST

Bonus - Here are some great links:

BY Doug Kass · Nov 26, 2025, 8:40 AM EST

With S&P futures +18 handles, I am back shorting the indexes:

* (SPY) $677.07

* (QQQ) $611.75

BY Doug Kass · Nov 26, 2025, 8:26 AM EST

The S&P Short Range Oscillator is at -2.22% vs. -3.23%.

That is less oversold.

Remember this indicator uses a multi-day moving average, so the oversold will continue to drop in the days ahead.

BY Doug Kass · Nov 26, 2025, 7:51 AM EST

Wolf Street howls about a spending consumer.

BY Doug Kass · Nov 26, 2025, 7:45 AM EST