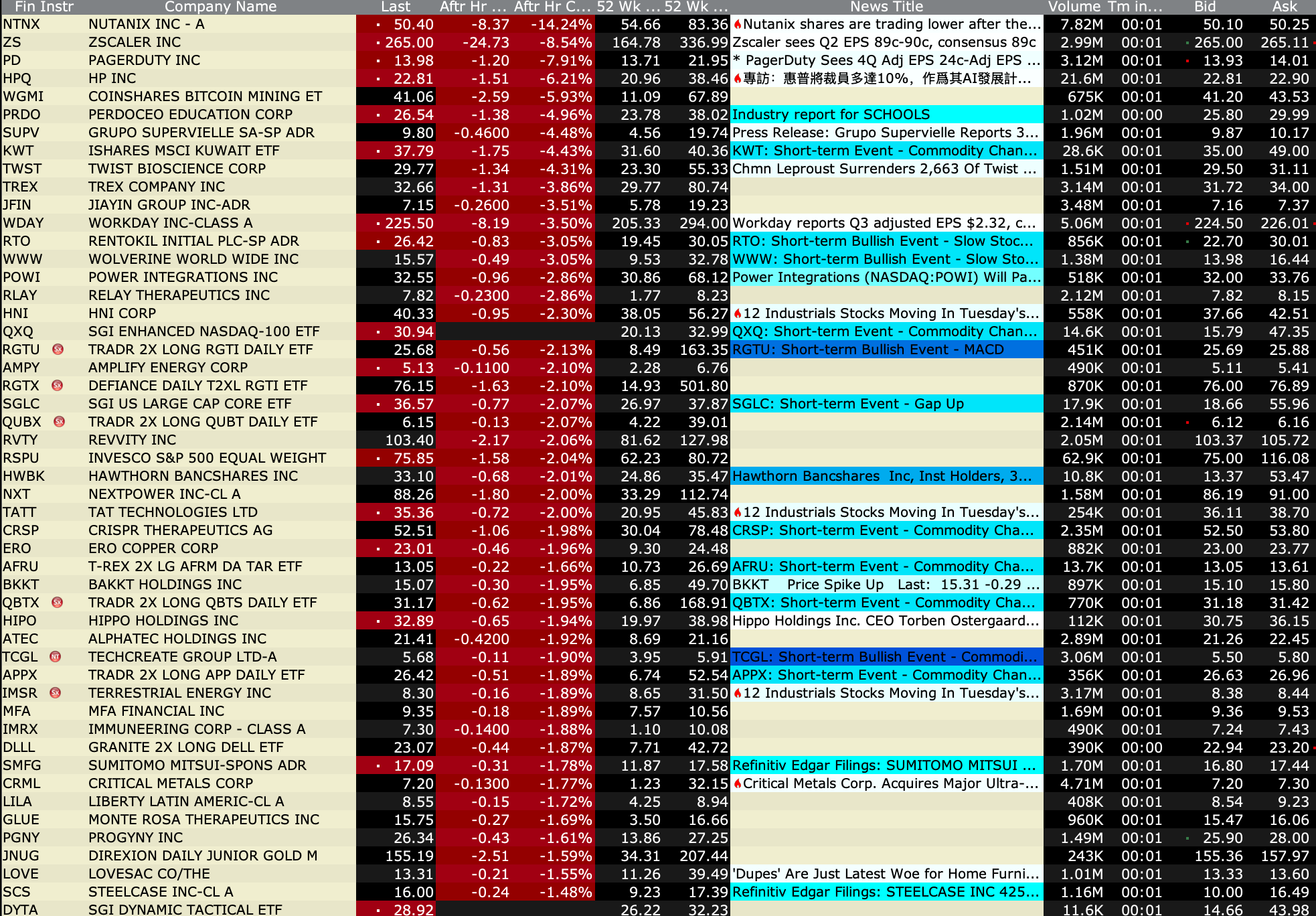

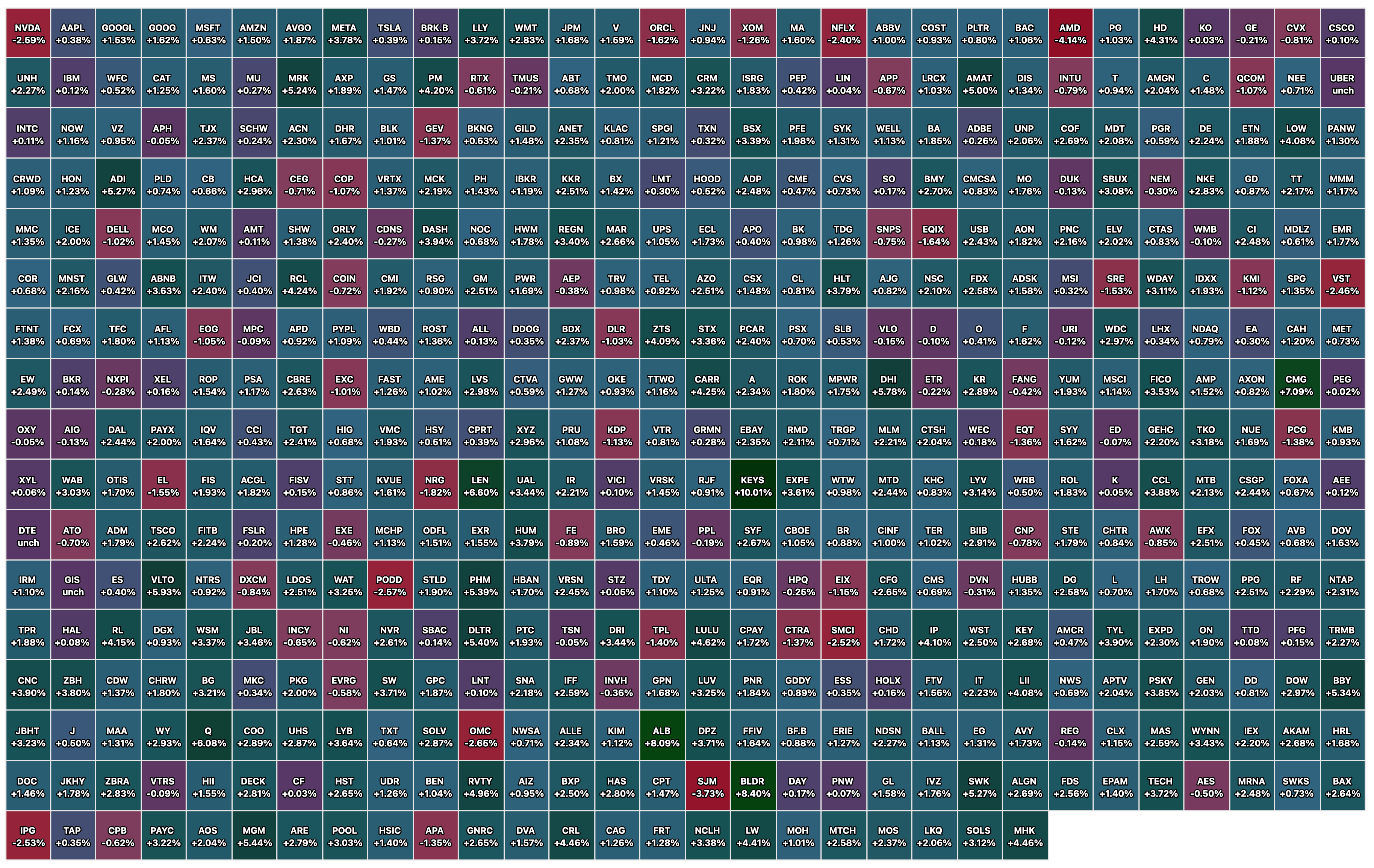

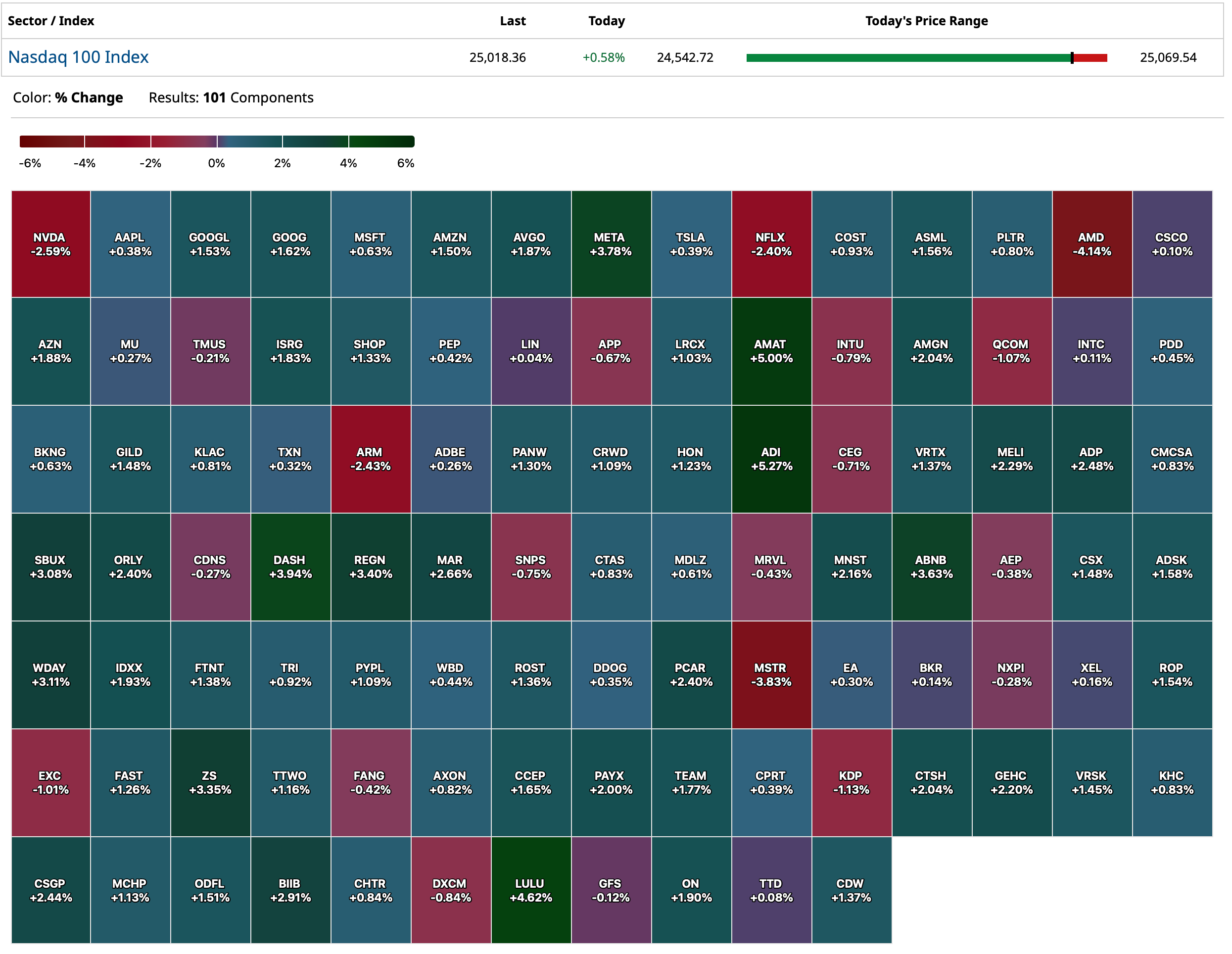

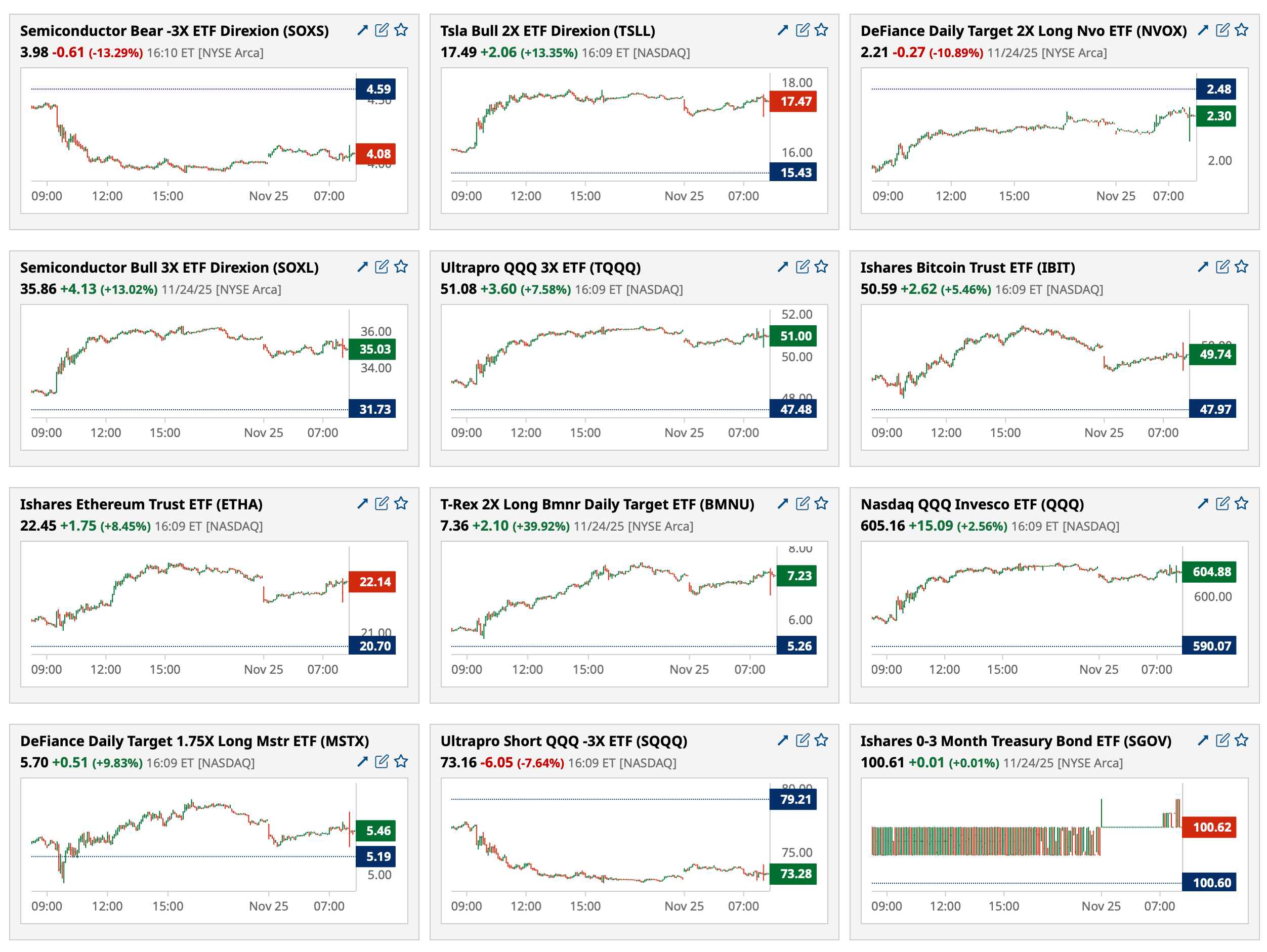

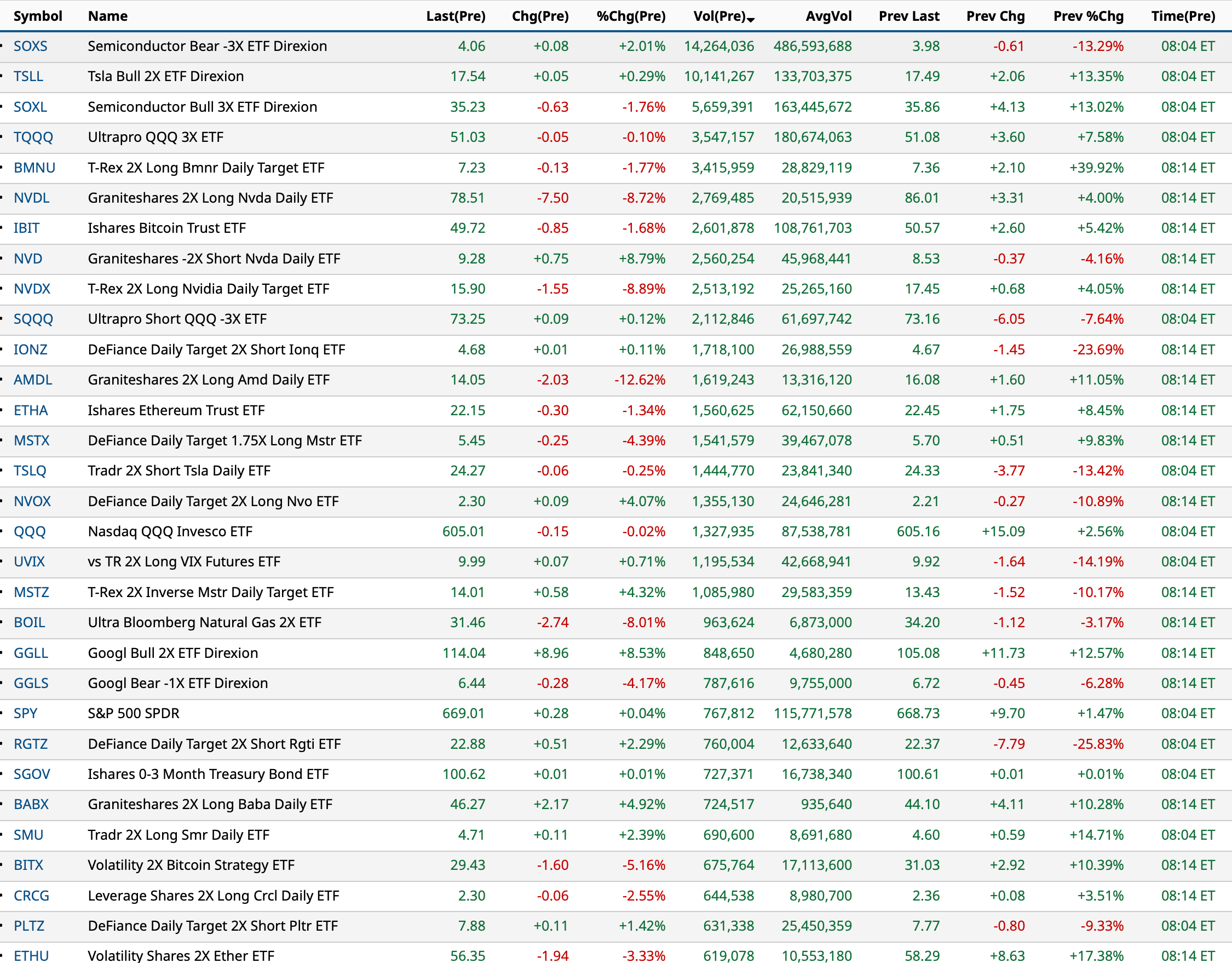

Tuesday's After-Hours Gainers and Losers

% Gainers

% Losers

BY Doug Kass · Nov 25, 2025, 4:55 PM EST

BY Doug Kass · Nov 25, 2025, 4:55 PM EST

BY Doug Kass · Nov 25, 2025, 4:40 PM EST

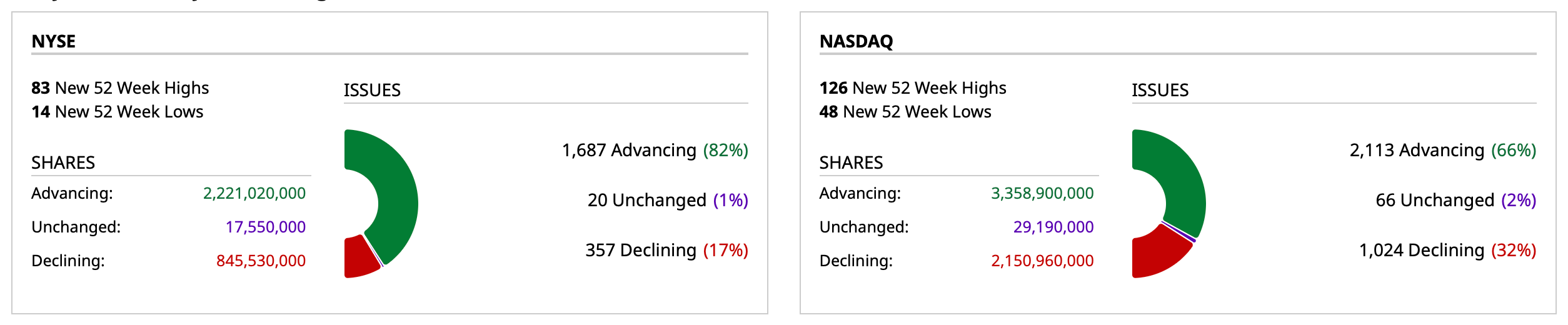

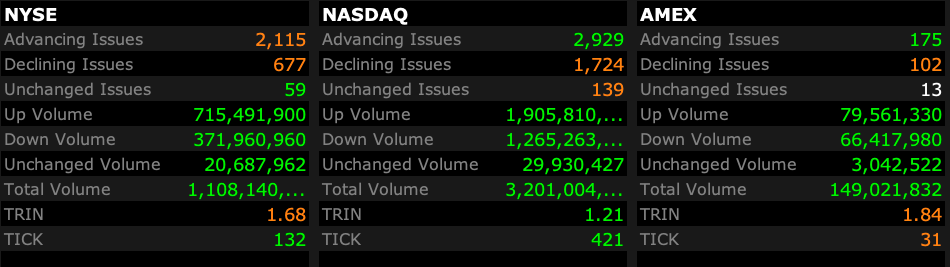

- NYSE volume 13% below its one-month average;

- NASDAQ volume 16% below its one-month average;

- VIX index: down 9.55% to 18.56

BY Doug Kass · Nov 25, 2025, 4:34 PM EST

I have covered my (SPY) short trading rental at $675.03 for a loss.

I will revisit tomorrow.

I now have no index positions on.

BY Doug Kass · Nov 25, 2025, 4:11 PM EST

Bitcoin taking another leg lower.

(MSTR) follows...

BY Doug Kass · Nov 25, 2025, 2:50 PM EST

An issue I will discuss in my market update on Monday:

BY Doug Kass · Nov 25, 2025, 2:35 PM EST

BY Doug Kass · Nov 25, 2025, 2:20 PM EST

BY Doug Kass · Nov 25, 2025, 1:45 PM EST

Following the Thanksgiving holiday, I will be delivering a multi-part market view on Monday morning.

Working on it now. It's going to be a good read (whether one agrees or not).

BY Doug Kass · Nov 25, 2025, 1:30 PM EST

I am inclined to take some Meta (META) long off my books as its trading up to $630 (+$18 today) and far from my 11/21 (only four days ago) buy at $585.27.

But for now I will let the profit run — though I am looking into selling some upside calls short against long common.

Stay tuned.

I have purchased very small long positions in (MSFT) at $469.87, (AMZN) at $216.75 and (META) at $585.27.

Position: Long MSFT (VS), AMZN (VS), META (VS)

Nov 21, 2025 11:40 AM EST

BY Doug Kass · Nov 25, 2025, 1:15 PM EST

At $674.08, I have moved closer to medium-sized short (SPY) .

BY Doug Kass · Nov 25, 2025, 12:55 PM EST

Earlier I referenced some MAG7 longs into the teeth of last week's weakness.

I typed the wrong prices (damn laptop!), here are the correct buys/costs:

I have purchased very small long positions in (MSFT) at $469.87, (AMZN) at $216.75 and (META) at $585.27.

Position: Long MSFT (VS), AMZN (VS), META (VS)

Nov 21, 2025 11:40 AM EST

BY Doug Kass · Nov 25, 2025, 12:21 PM EST

From Peter Boockvar:

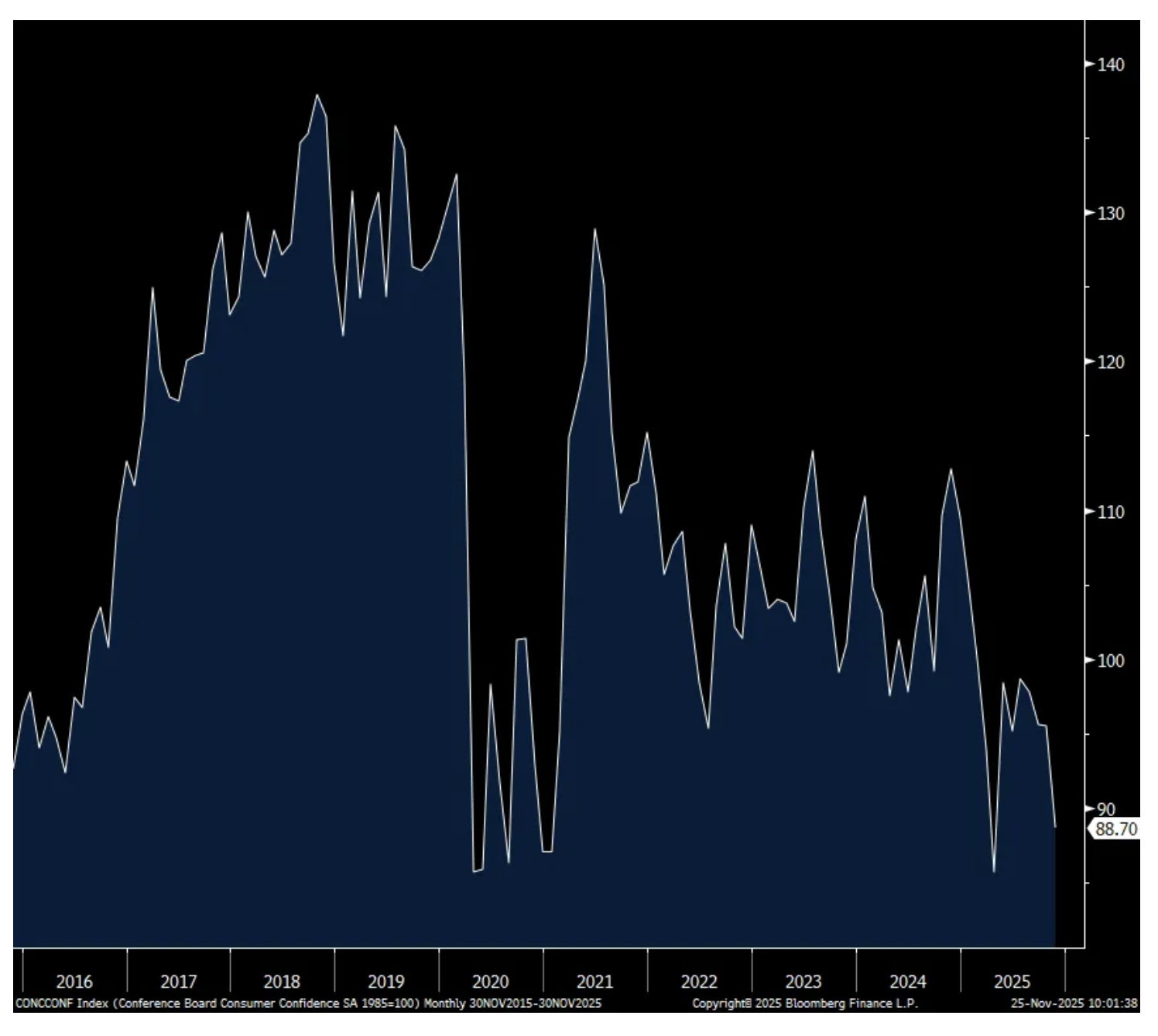

The November consumer confidence index from the Conference Board fell to 88.7 from 95.5, below the estimate of 93.3 and the 2nd weakest print since January 2021. Both main components were down m/o/m. One yr inflation expectations held at 5.7% on average with a median read of 4.8% vs 4.6% in October.

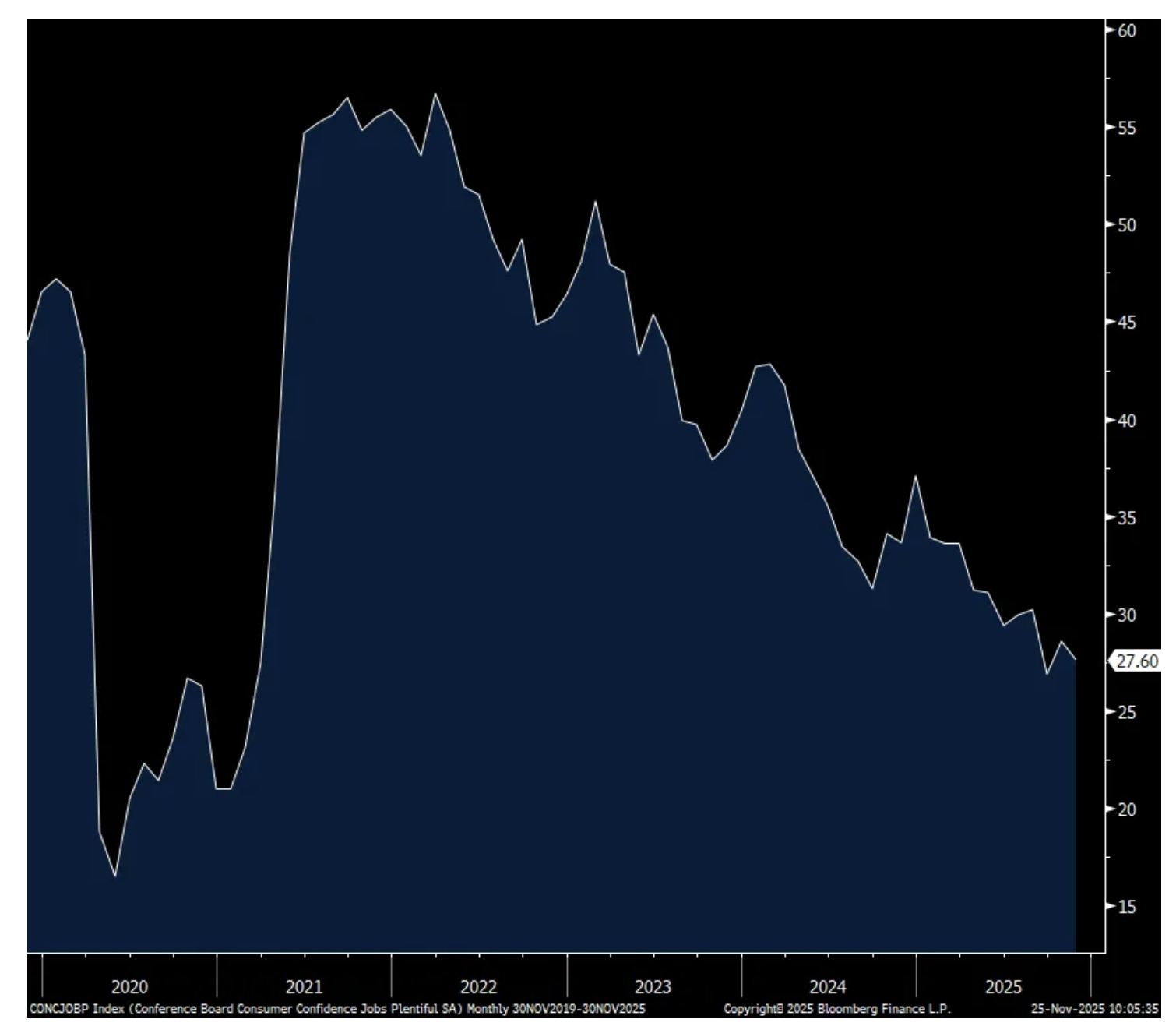

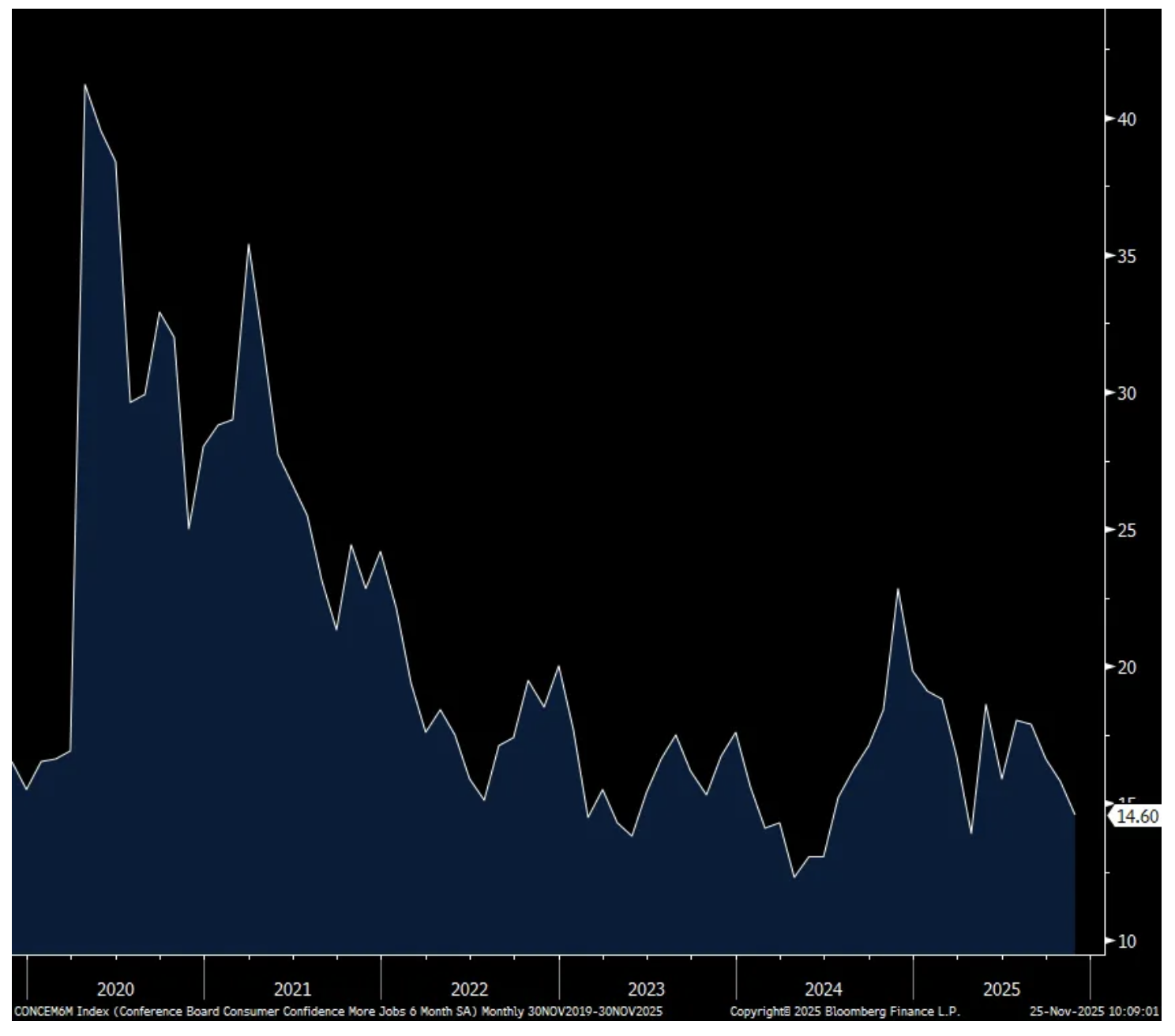

The answers to the labor market questions were mixed. Jobs Plentiful fell 1 pt to 27.6 and that is the 2nd lowest since March 2021. Hard To Get though fell .4 pts. Expectations for the labor market looking out 6 months deteriorated as those that see ‘more jobs’ fell 1.2 pts to the lowest since April. Income expectations weakened as well.

Spending intentions fell for autos, homes and major appliances. The ‘home’ category was particularly noteworthy because it fell to the lowest since April notwithstanding the drop in mortgage rates.

Politically, the Conference Board said “Confidence fell among consumers of all political stripes, with the sharpest retreat among independent voters.”

Not surprisingly, this is what continues to be the wet blanket on consumer confidence, “Consumers’ write in responses pertaining to factors affecting the economy continued to be led by references to prices and inflation, tariffs and trade, and politics, with increased mentions of the federal government shutdown. Mentions of the labor market eased somewhat but still stood out among all other frequent themes not already cited.”

Finally of note, “Assessments of current financial situations collapsed to the lowest level since August 2024, when a confluence of negative events stoked a brief financial market selloff and US recession concerns.”

My bottom line, inflation and the ever rising cost of living continues to be the main consumer pain point. This VERY MUCH complicates the job of the Federal Reserve. I know it’s easy to think that the Fed should cut rates in response to an economy that seems more fragile and with a softening labor market but if that is the case because many consumers are stressed with inflation, shouldn’t inflation then be the main focus of the Fed? In other words, don’t we need low and stable prices first before we can be confident of a stronger economy and labor market? No easy answers here for them.

Consumer Confidence

Jobs plentiful

Expectations for more jobs

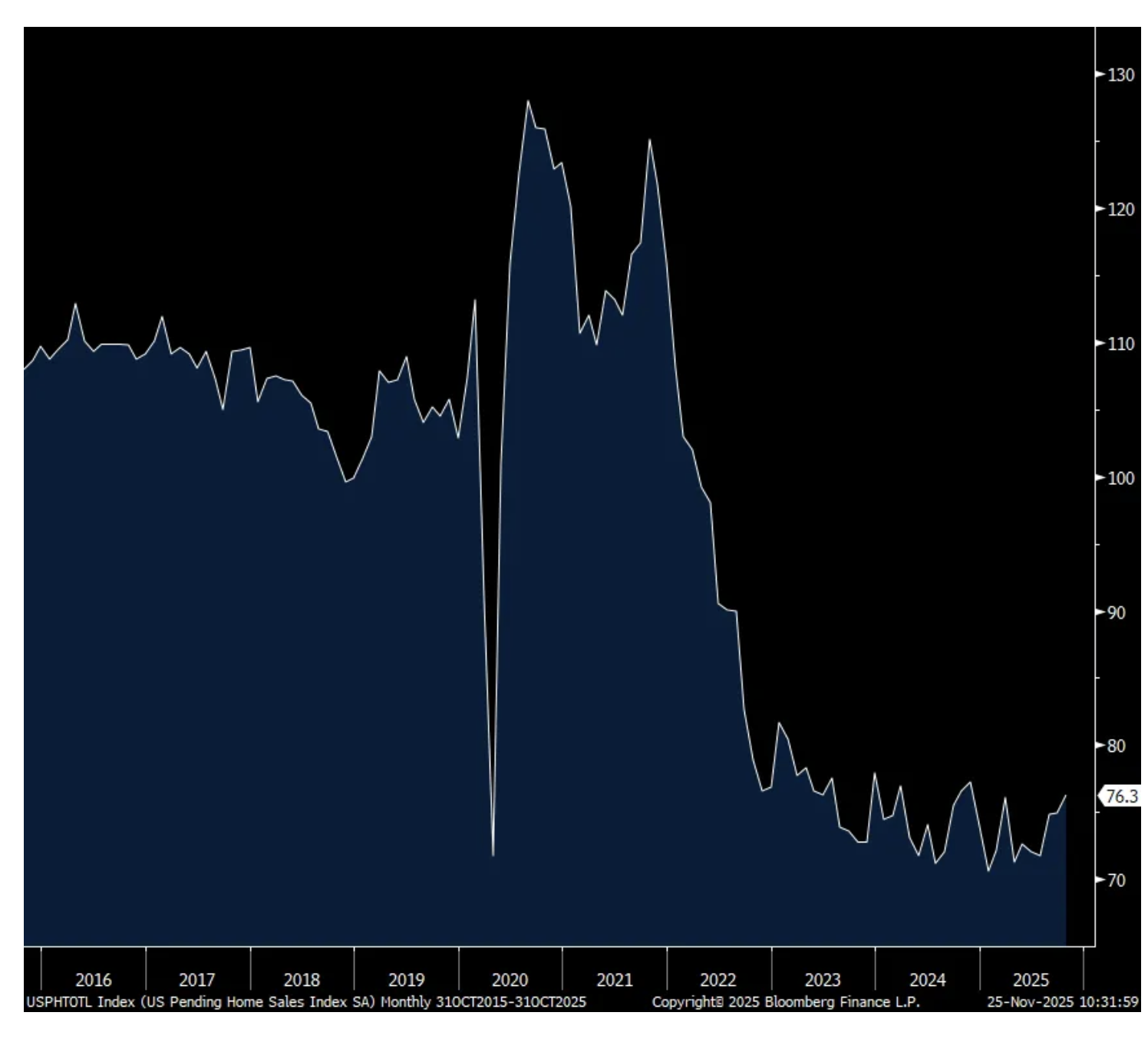

Pending home sales in October rose 1.9% m/o/m after a flat read in September and that was above the forecast of a slight .2% rise.

The NAR said “The Midwest shined above other regions due to better affordability, while contract signings retreated in the more expensive West region.” Sales in the Northeast were up by 2.3% m/o/m and by 1.4% in the South vs a 5.3% increase in the Midwest and a 1.5% decline in the West.

Bottom line, we know the housing market is trying to unfreeze here with the drop in mortgage rates and more supply seemingly coming to market but pricing still remains particularly tough for the first time buyer because of the cumulative 50% rise in prices over the past 5 years.

Pending Home Sales

Following negative prints seen in the Philly and Dallas manufacturing indices and the positive one for NY, the Richmond survey fell to -15 from -4.

Bottom line, the manufacturing recession unfortunately continues on in November.

BY Doug Kass · Nov 25, 2025, 12:16 PM EST

- NYSE volume 9% below its one-month average;

- Nasdaq volume 12% below its one-month average;

- VIX index: down 3.56% to 19.79

BY Doug Kass · Nov 25, 2025, 11:55 AM EST

* In a more hostile market setting...

I have added small to (KMB) at $105.38.

I am planning to add to other (defensive) consumer nondurables in the belief that a market rotation could move in their direction.

BY Doug Kass · Nov 25, 2025, 11:44 AM EST

Dougie Kass

STAFF

1 minute ago

The haters always come out of the woodwork when the Indices (and certain AI related equities) rip higher.

(They remind me of some of the kids in my High School, the "I told you so kids" who rarely had an original thought.

It's become predictable.

I have even used their hating as a contrary market signal.

For that, I give thanks!

BY Doug Kass · Nov 25, 2025, 11:35 AM EST

My favorite podcast of the day with Guy and Dan.

The appeal? They are straight shooting, are accountable for their trading and investment boners, provide excellent option strategy and thoughtful market observations.

Run, don't walk....

Let's go to the tape! MRKT Call - Tuesday, November 25th

BY Doug Kass · Nov 25, 2025, 11:25 AM EST

I am back shorting (JOET) at $41.59.

BY Doug Kass · Nov 25, 2025, 11:17 AM EST

BY Doug Kass · Nov 25, 2025, 11:01 AM EST

Added to (SPY) $671.02

BY Doug Kass · Nov 25, 2025, 10:49 AM EST

Back shorting (SPY) at $669.38 - I am a scale seller now.

BY Doug Kass · Nov 25, 2025, 10:45 AM EST

I stand by my 155 columns about the threats to AI and NVDA.

Today's market, especially the divergences within technology, is unprecedented.

BY Doug Kass · Nov 25, 2025, 10:25 AM EST

Here's is JustDario's opinion on (NVDA) :

BY Doug Kass · Nov 25, 2025, 10:00 AM EST

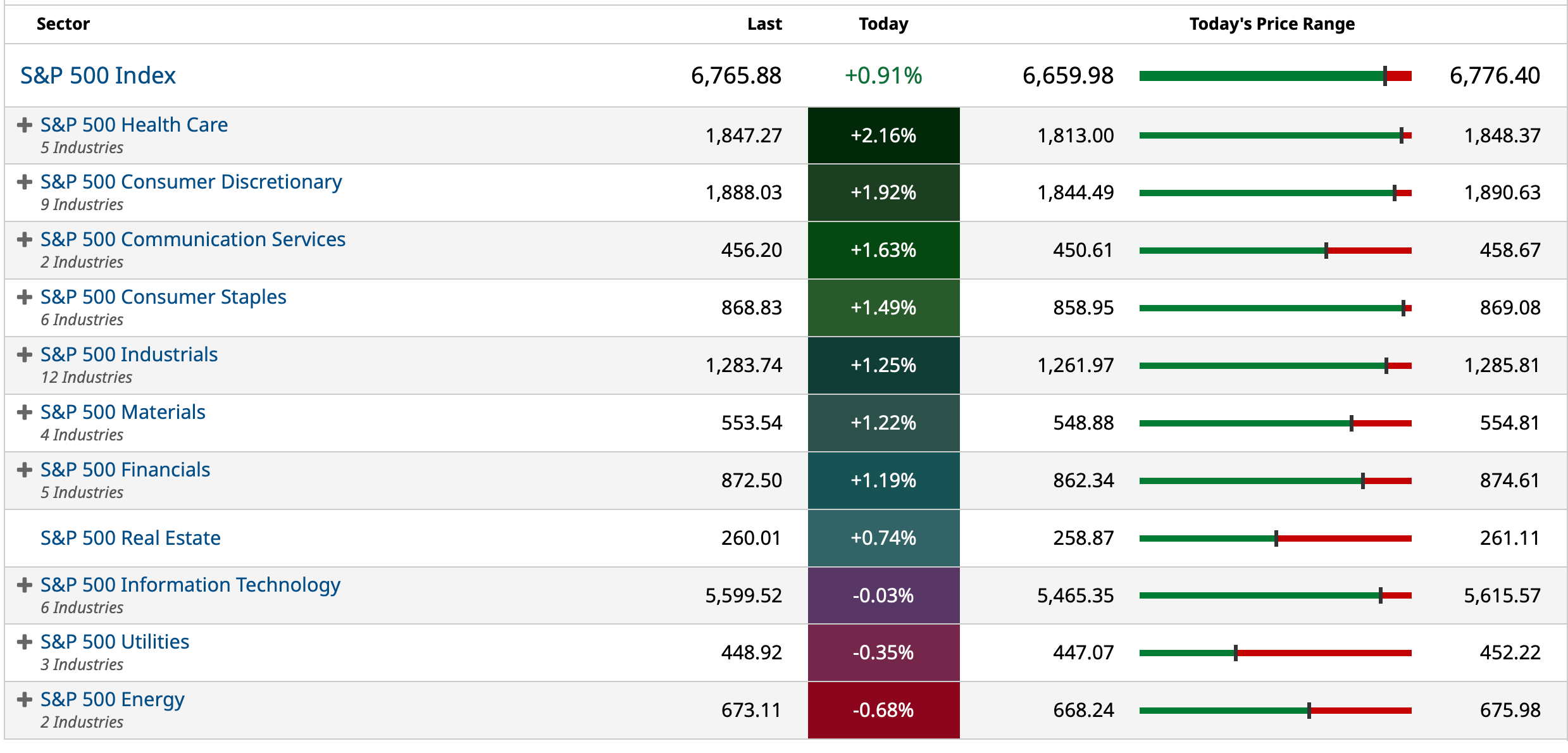

With S&P cash -35 handles and the Nasdaq futures down by more than -300 handles I am taking in all of my Index shorts:

* (SPY) $664.59 (-$3.35)

* (QQQ) $598.39 (-$6.60)

BY Doug Kass · Nov 25, 2025, 9:54 AM EST

From Peter Boockvar:

Not that I know the difference between a TPU (Tensor Processing Unit) and a GPU (Graphic Processing Unit) nor one GenAI model from another but we are being reminded again as to how competitive and quickly changing technology is. Up until a few years ago, Google and Meta were essentially advertising companies. Amazon was a retailer. Business of course evolved where it started with cloud, but now with GenAI and semiconductors, and they are all now swimming in the same technological waters along with the pure play tech companies, particularly Nvidia. Such fascinating times that we also benefit from as a user of this technology. That said, with the Google ecosystem that they are creating, vertically, it opens up a whole new competitive dynamic with the ‘too big to fail’ OpenAI world that so many companies are now so dependent on, especially Oracle. Investors are clearly in the process of shifting from GenAI being one big trade, to now trying to figure out who will win and who will not.

With the September economic data now being released I’m not going to bother writing about as we’re just about two months past it.

Yesterday, the November Dallas manufacturing index remained in contraction at -10.4 vs -5 in October and vs the estimate of -2.0.

Here were the notable comments from companies in a variety of industries:

Beverage and tobacco product manufacturing· Concerns about the economy, the independence of the Fed and tariffs continue to cause uncertainty. We are not certain that [uncertainty] has actually increased as much as it has remained at an uncomfortably elevated level.

Computer and electronic product manufacturing· We don’t know if it’s the shutdown or just that demand has dropped, but our orders have dropped in half.

Fabricated metal product manufacturing· There is a continued weakness in the retail consumer market. Interest rates and inflation are certainly factors, but there is a general level of uncertainty in the consumer market that is tied to both political and economic uncertainty.· Have not been able to initiate work due to a slowdown with our contractor and owner base. We now are hearing that work has been delayed until 2026.

Food manufacturing· We are shifting volume to higher-priced products that reflect demand for our organic products. This is a consumer shift that we are seeing due to increased demand for minimally processed foods. This is a positive shift for our company.· We’re currently facing challenging business conditions on several fronts, including rising raw material costs from national suppliers; supply disruptions and higher prices from international vendors; the loss of a few key distributors that have gone out of business; difficulties in collecting outstanding payments; increased labor costs; and a shortage of qualified candidates.

Machinery manufacturing· Looking forward to a tax rebate for the month of government shutdown.· November was our most profitable month this year. We are seeing increased business activity and many new projects.· It seems even the modest decrease in interest rates has assuaged fears of inflation and provided comfort that we are indeed headed in the right direction. Tariff revenue has not dramatically impacted opportunity to grow in our industry, and it has seemingly improved our overall economy. We remain hopeful of continued progress through 2026.

Miscellaneous manufacturing· Tariff uncertainty is the largest impact on our purchasing strategy, along with a rise in employee benefits and costs.

Paper manufacturing· Currently steady at a low demand and production rate. If no uptick in business in the next 1-2 months, will need some further reduction in workforce to right-size operations.

Primary metal manufacturing· In addition to the double-invoicing issue we reported last month—still ongoing, with importers paying tariffs only on the raw material cost rather than the full value of the finished product—auto, truck and aircraft parts have now been temporarily excluded from Section 232 aluminum and steel tariffs. This has led to a surge in imported components and is contributing to job losses across U.S. aluminum manufacturing.· Expecting 3 percent wage increases going into year 2026. New product line is bolstering business outlook.

Printing and related support activities· We continue to see soft incoming orders, with poor general activity in our industry. It’s as if all the chaos in Washington is creating a lot of wait-and-see attitude among our customers’ customers. We are very hopeful that things will improve in the next 6 months.

Transportation equipment manufacturing· Signs indicate business activity is improving, i.e. lowering of interest rate, improving economy and consumer confidence for major purchases.· We are seeing commercial vehicle production continue to decline. Many of our original equipment manufacturer (OEM) customers have open production slots in November and December.· Business is as delicate today as it was under the previous administration. Small, established businesses have nowhere to turn for help when suddenly paying new tariffs. We purchase raw materials from [Asian nations] and manufacture in the U.S., only to see [those nations’] governments subsidize manufacturing.

To some specific publicly traded company commentary.

From Central Garden and Pet, the maker of, you guessed it, garden and pet products:“We expect consumers to remain focused on value and performance with a promotionally active but stable retail environment and continued channel shifts from pet specialty to e-commerce.”In their pet business, “While demand for durables remained soft, consumables performance continued to be relatively stable.”With garden, “We benefited from an extended selling season driven by favorable fourth quarter weather following a cool and wet third quarter” among other factors.With overall guidance, “We think ‘26 is going to be extremely challenging...we’ve got a little bit of a headwind with tariffs. Consumer confidence is at a low point right now. So, we really need to see how the consumer is going to react to pricing and really their behavior, and the whole notion of the bifurcation of income right now is very real. We’re seeing it in both of our categories.”

Burlington Stores, the discount retailer, missed the comp estimate but is citing weather in their earnings press release:“Traffic to our stores fell off significantly after the back-to-school period driven by unseasonably warm temperatures in our major markets. Our comp trend then picked up to mid-single-digits in mid-October once the weather cooled, and that strong trend has continued through the first three weeks of November.”

Best Buy beat both top and bottom line estimates and said this in their earnings release:“Our comparable sales grew 2.7% as we continued to drive strong results across computing, gaming and mobile phones. We delivered sales growth across both online and stores, saw continued improvements in customer experience ratings and launched our Best Buy Marketplace.” They saw declines in “home theater and appliances.”

From the DICK’S Sporting Goods release:“In the third quarter, the DICK’S business comps grew 5.7% driven by increases in both average ticket and transactions, and we were pleased to deliver gross margin expansion.”

From JM Smucker prepared remarks:“Consumers continue to seek value and prioritize their spending, which our portfolio is well positioned for, as it features offerings across the value spectrum, in the attractive categories of coffee, snacking and pet.”Their Uncrustables brand is doing particularly well and I contributed to that in the quarter.

From American Woodmark, the maker of kitchen cabinets and vanities:“Demand trends remain challenged in both the new construction and remodel markets.”They are also getting hit hard by tariffs. “We estimate the unmitigated tariff impact at the current rates, in effect as of today’s date, to represent approximately 4-4.5% of the Company’s annualized net sales with the impact varying by product category. This impact does not include the potential increase on Section 232 tariffs to 50%.”

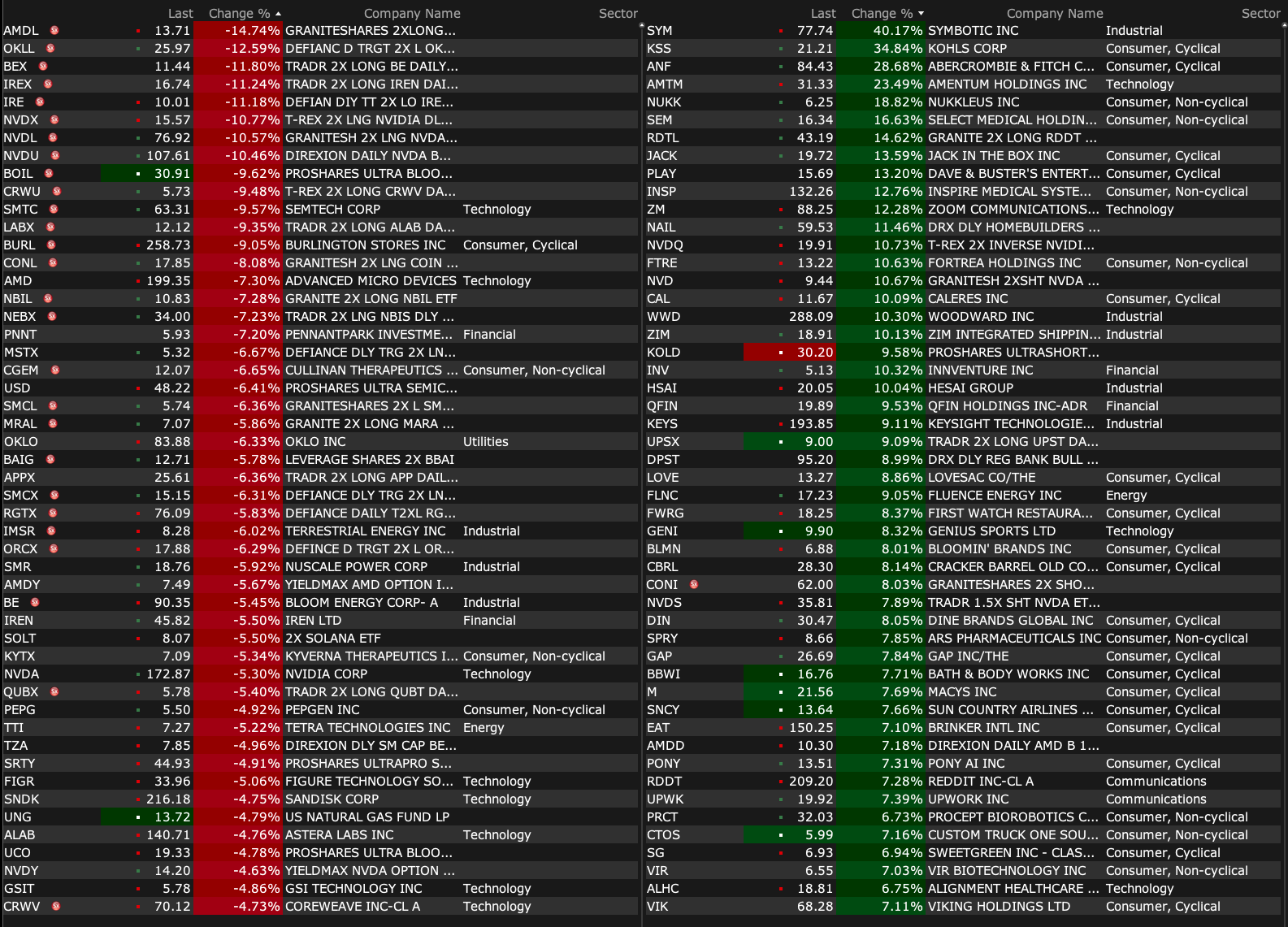

BY Doug Kass · Nov 25, 2025, 9:45 AM EST

-SYM +28% (earnings, guidance)

-KSS +27% (earnings, guidance)

-ANF +18% (earnings, guidance)

-KEYS +13% (earnings, guidance)

-SEM +13% (acknowledges Executive Chairman's Take-Private Proposal for consideration of $16.00-16.20/shr)

-ZIM +13% (explores strategic alternatives; reviewing potential sale and capital allocation)

-BNED +12% (earnings)

-AMTM +11% (earnings, guidance)

-KYIV +6.6% (launches Starlink Direct to cell satellite connectivity by SpaceX in Ukraine)

-ZM +5.5% (earnings, guidance)

-AVGO +4.4% (higher in sympathy with GOOGL)

-GOOGL +4.4% (reportedly Meta considers spending billions of dollars on Google Cloud Tensor Processing Units (TPUs), incl for Meta data centers)

-TLSA +4.1% (Nasal Foralumab Phase 2 Clinical Trial Accepted into Healey ALS MyMatch Program)

-BABA +3.2% (earnings, color)

-SNDK +2.9% (to replace IPG in the S&P 500 Index, effective Nov 28th)

-SPOT +2.9% (reportedly to raise US subscription prices in Q1 of 2026)

-XENE +2.2% (to present New Azetukalner OLE Study Data in Epilepsy at AES 2025)

-EAT +2.1% (CitiGroup Raised EAT to Buy from Neutral, price target: $176 from $144)

-NVO +2.1% (receives US FDA NDA Supplemental 23 approval for Wegovy)

-EMBC -8.1% (earnings, guidance)

-BURL -4.7% (earnings, guidance)

-NVDA -4.1% (downside momentum)

-DKS -3.8% (earnings, guidance)

-COHR -3.7% (Bain Capital reportedly seeks up to $1.14B in block sale of Coherent stock)

BY Doug Kass · Nov 25, 2025, 9:17 AM EST

BY Doug Kass · Nov 25, 2025, 9:05 AM EST

BY Doug Kass · Nov 25, 2025, 8:55 AM EST

* (SPY) $669.60

* (QQQ) $605.66

BY Doug Kass · Nov 25, 2025, 8:53 AM EST

11 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasury hosts a $50B 52-Week Bill Auction;

11:30 a.m.: Treasury hosts an $85B 6-Week Bill Auctuin;

1 p.m.: Treasury hosts a $28B 2-Year FRN Auction;

1 p.m.: Treasury hosts a $70B 5-Year Note Auction;

2 p.m.: Treasury Buyback (Liquidity Support)

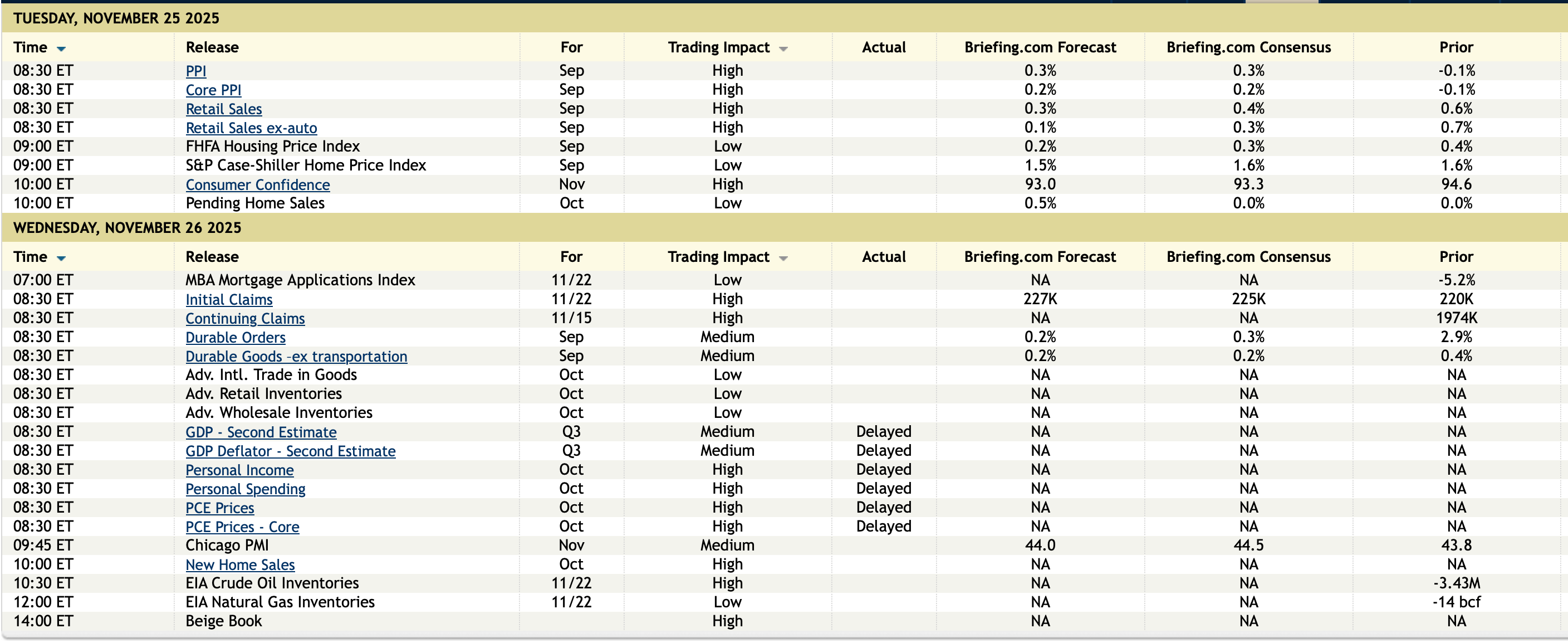

Economic Calendar of the Week

BY Doug Kass · Nov 25, 2025, 8:40 AM EST

BY Doug Kass · Nov 25, 2025, 8:25 AM EST

* My skepticism regarding NVDA/AI/Crypto continues to grow

* The biggest beneficiary of Gen AI might be gold

* And some pearls of wisdom from Peter Boockvar

This is a good write-up on some of the original propaganda that got the U.S. government all geeked up about the AI thing:

BREAKING: The AI 2027 doomsday scenario has officially been postponed

Oops they did it again.

This is what you get when you have governance by the All-In podcast.

Same garbage with crypto. Maybe those guys will turn the whole country into a SPAC and have Sam Altman run the thing. At any rate, sounds like one of the senior policy advisors at the White House is on to it, hopefully Scott Bessent too!

And (NVDA) 's Jensen Huang with this garbage, woe is me.

First of all this is a load of baloney. The guy cannot sell stock fast enough. Same with his Palantir (PLTR) buddy, who complains about the short sellers, but my guess is he sells more stock per quarter than any single investor is actually short in total. If there is a small hint of truth to the notion that Jensen Huang feels a fair bit of pressure now, well whose fault is that for hyping up the space so much? Who is investing in his own customers who turn around and buy product back? And on and on and on… :

P.S. Per my point about the All In (self-interested) podcast running the U.S. economy, here you go. He even has the All In logo in his banner. Maybe we shouldn’t be going All In on a broken technology that is overly resource consumptive and dis-economic, this country has found enough ways to light money on fire already. His point seems to be that spending money to dig holes and then fill them back up is somehow good for the economy because that adds to GDP. The biggest beneficiary from Gen AI might be the price of gold.

Finally, some good stuff from fellow stooge, Peter Boockvar:

Not that I know the difference between a TPU (Tensor Processing Unit) and a GPU (Graphic Processing Unit) nor one GenAI model from another but we are being reminded again as to how competitive and quickly changing technology is. Up until a few years ago, Google and Meta were essentially advertising companies. Amazon was a retailer. Business of course evolved where it started with cloud, but now with GenAI and semiconductors, and they are all now swimming in the same technological waters along with the pure play tech companies, particularly Nvidia. Such fascinating times that we also benefit from as a user of this technology. That said, with the Google ecosystem that they are creating, vertically, it opens up a whole new competitive dynamic with the ‘too big to fail’ OpenAI world that so many companies are now so dependent on, especially Oracle. Investors are clearly in the process of shifting from GenAI being one big trade, to now trying to figure out who will win and who will not.

BY Doug Kass · Nov 25, 2025, 8:10 AM EST

Moved up to small sized on index shorts with following shorts:

* (SPY) $669.00

* (QQQ) $605.03

BY Doug Kass · Nov 25, 2025, 7:30 AM EST

* I covered my long-standing short last week at $174...

The Terminal Equilibrium: A Forensic Analysis of Strategy Inc.’s Impossible Capital Structure

BY Doug Kass · Nov 25, 2025, 7:25 AM EST

* From yesterday and last week...

Yesterday I sold indexes (common) short (VVS) with S&P cash +45 handles and then after the close +103 handles (plus another +5 in futures).

A reminder of several recent long purchases (KMB) and (PEP) and, later in the week (on Nov. 21) , (META) $469.87 (AMZN) $216.75 and (MSFT) $585.27.

BY Doug Kass · Nov 25, 2025, 7:12 AM EST