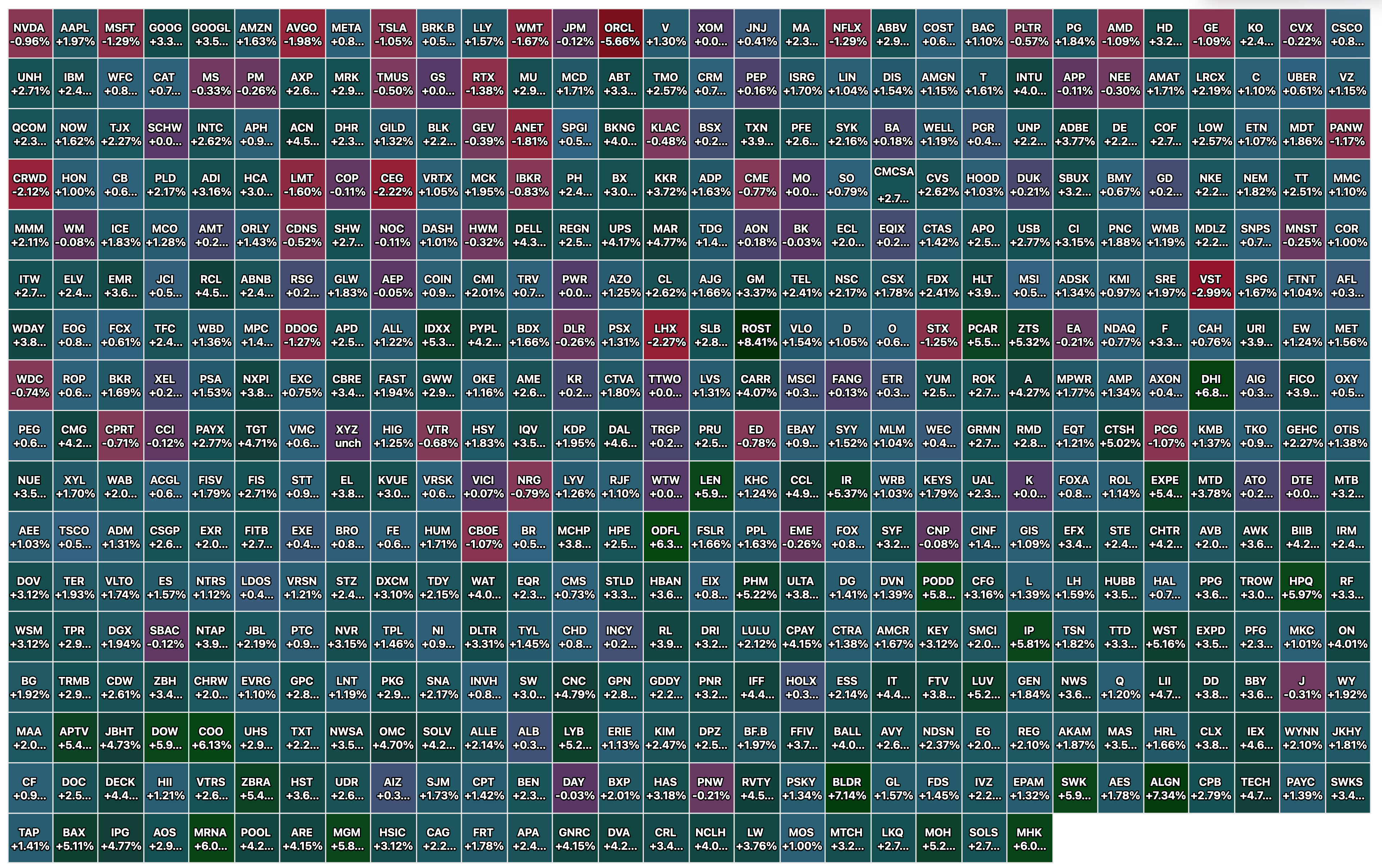

Friday's Closing S&P 500 Heat Map

BY Doug Kass · Nov 21, 2025, 4:40 PM EST

BY Doug Kass · Nov 21, 2025, 4:40 PM EST

- NYSE volume 20% above its one-month average;

- NASDAQ volume 3% below its one-month average;

- VIX index: down 11.05% to 23.50

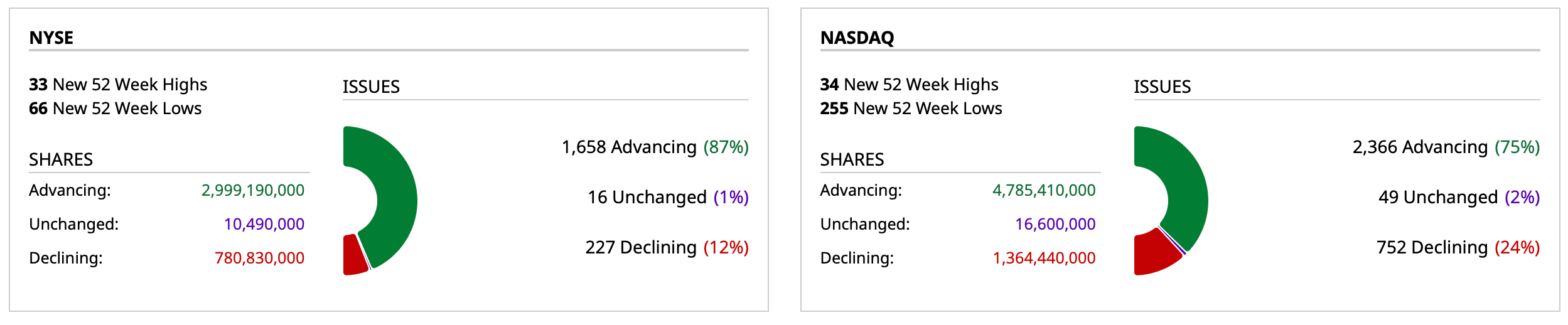

Closing Breadth

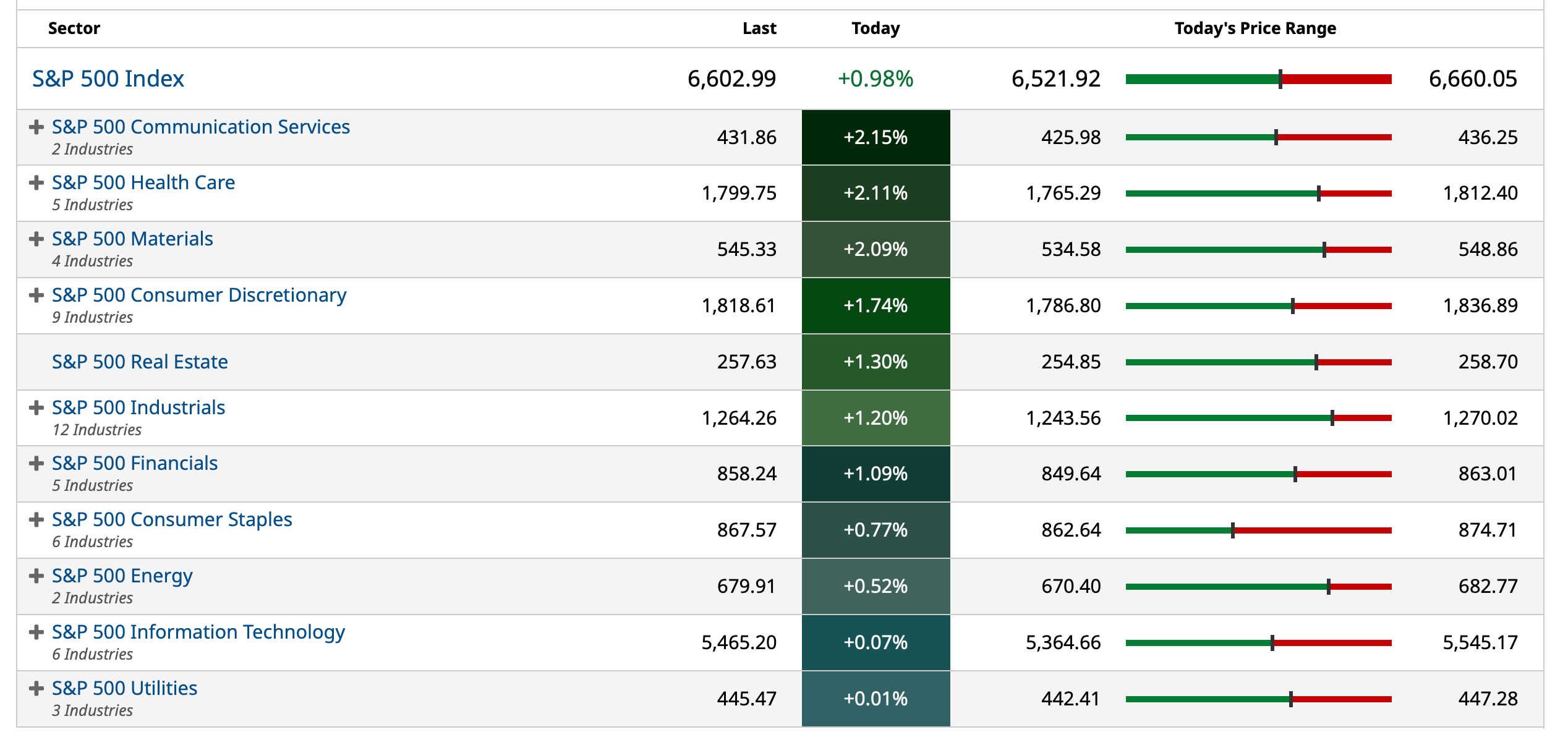

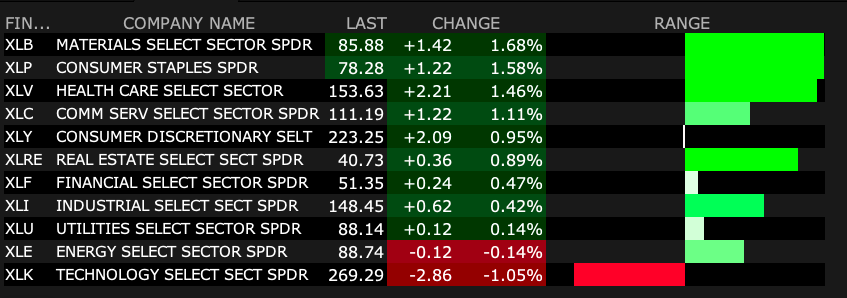

Sectors

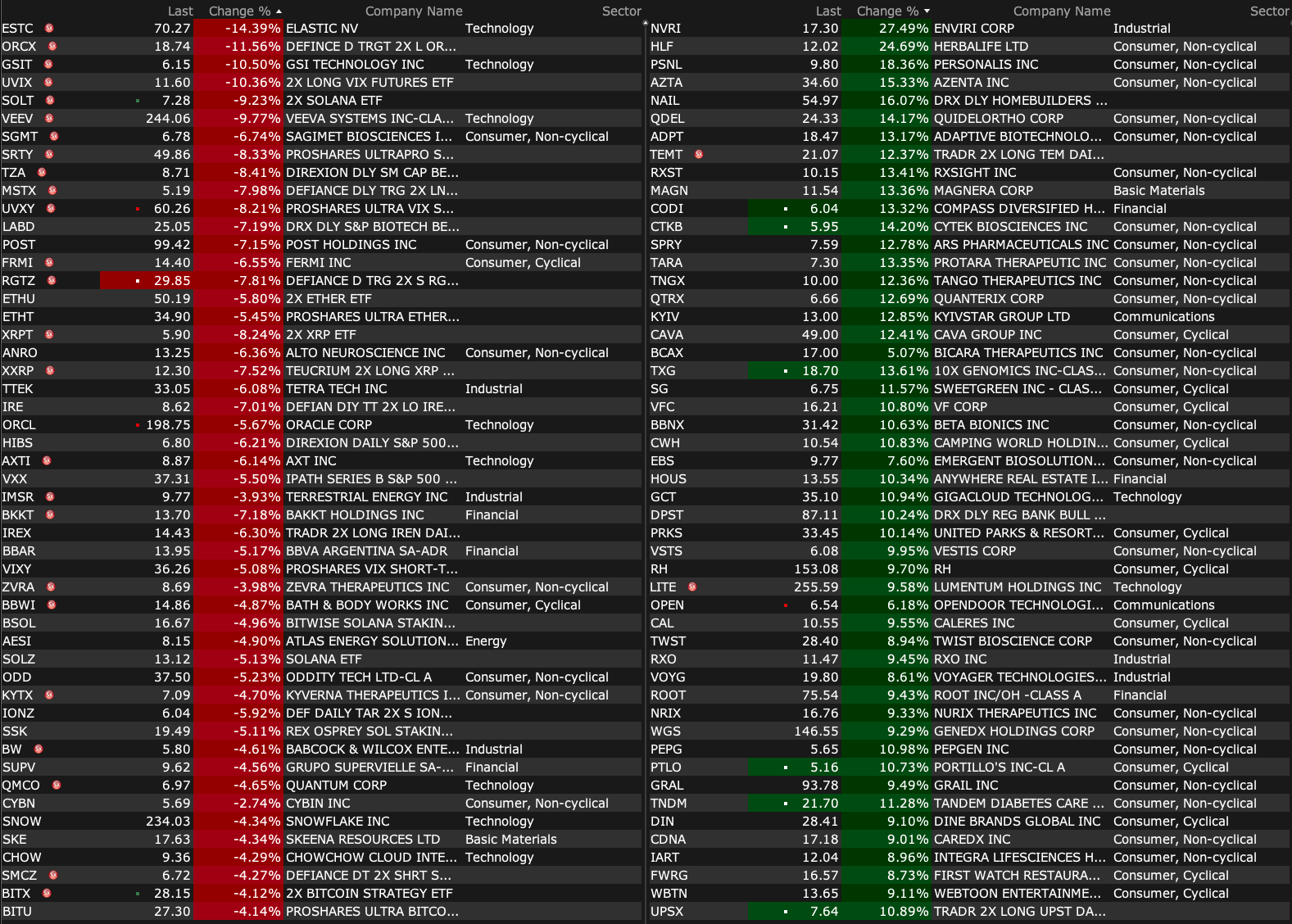

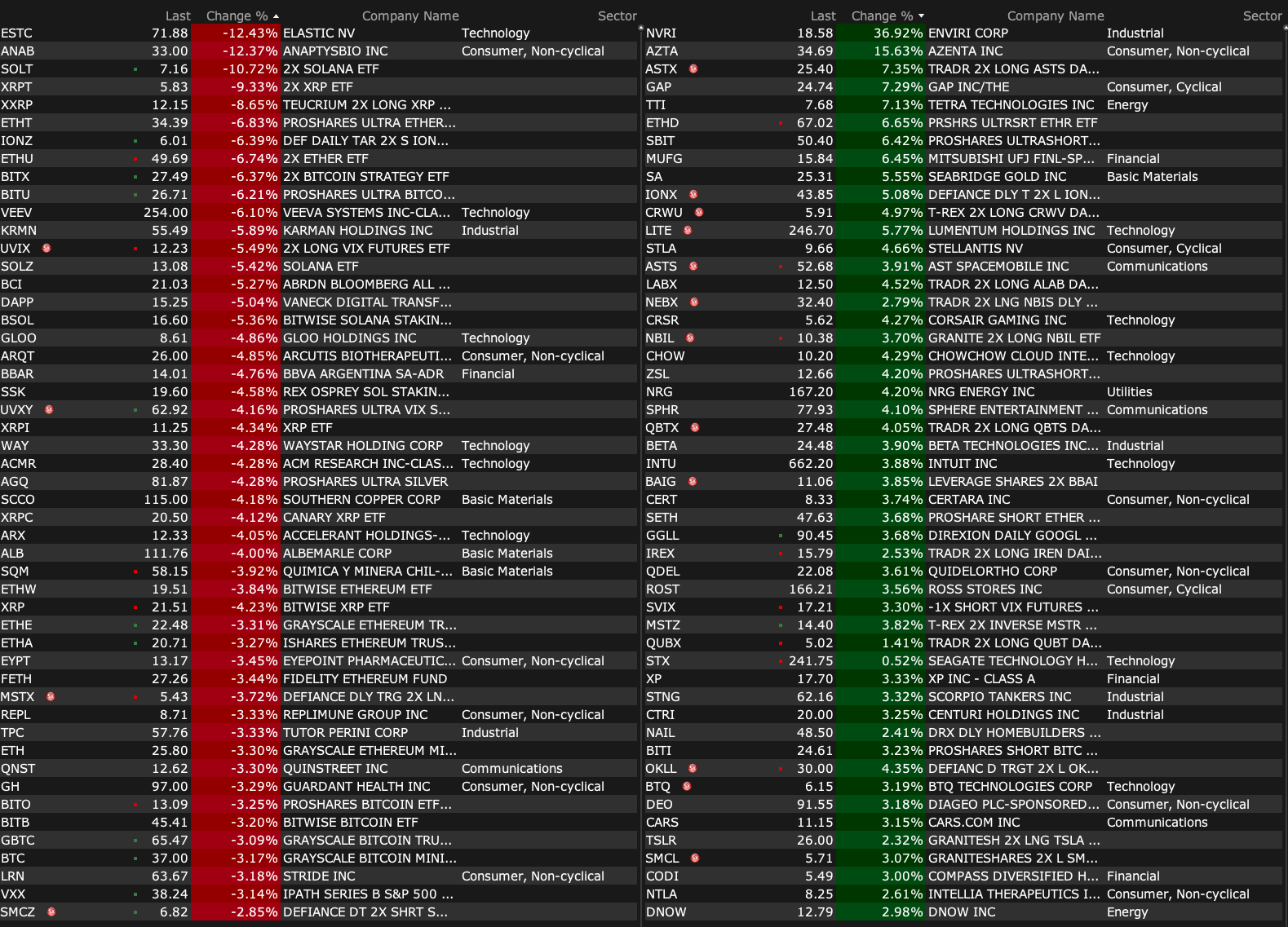

% Movers

Nasdaq 100 Heat Map

BY Doug Kass · Nov 21, 2025, 4:27 PM EST

By Peter Boockvar:

Positives:

1) Old news but the September payroll report showed a net gain of 119k vs the estimate of 53k, partly offset by the downward revision to the two prior months of a combined 33k. Average hourly earnings rose .2%, one tenth less than expected but higher by 3.8% y/o/y as forecasted due to rounding. The participation rate at 62.4% was up from 62.3% in the month before. The key 25-54 age cohort participation rate held at 83.7%. The all in U6 unemployment rate fell to 8% from the multi year high of 8.1% in August.

2) Initial jobless claims for the week ended 11/15 was 220k, 7k below expectations.

3) While missing key parts of the US service sector like retail and wholesale trade and construction, the S&P Global US services PMI was 55 vs 54.8 in the month before. Also, “Optimism hit a five-month high in manufacturing and an 11-month record in services…The brighter mood in part reflected reduced concerns over tariffs and worries over political disruptions more generally and was buoyed by the ending of the government shutdown. However, the survey also saw a broader improvement in sentiment about the economic outlook, in part driven by increased customer enquiries and hopes of greater policy support, including lower interest rates and more government fiscal stimulus.”

4) The volatile November NY manufacturing index picked up the pace to 18.7 from 10.7 and above the estimate of 5.8. It was -8.7 in September. After rising to 30.3 from 14.8 in October, the 6 month business outlook fell to 19.1. Capital spending plans did bounce to +11.5 from -2.9 and I’m guessing the tax expensing incentives in the OBBB helped.

5) Private foreigners have bought $448b of US Treasuries year to date. How much is basis trade related from Cayman and the UK?

6) From Walmart: “We drove positive transaction counts and unit volumes and we’re gaining market share in grocery and general merchandise including here in the US, where we saw strength across income cohorts and especially with higher income households…Comps were good across each month of the quarter. On the consumer, “we’d say that overall, the environment feels pretty consistent. There’s certainly some pockets of moderation that we’re keeping an eye on. But if you look at our guidance for 4Q, it would indicate that we have an expectation that it’s going to look pretty similar to the other quarters this year. Holiday is off to a pretty good start. Back-to-school tends to be an early indicator for how that goes, Halloween, likewise for Thanksgiving and everything that we’ve seen so far makes us optimistic and encouraged about customers and members leaning into the seasonal events and holiday shopping period.”

7) From Ross Stores: Comps grew 7% as “Our merchants delivered a compelling assortment of brand name values, which led to broad based growth across all major merchandise categories…We had an excellent back-to-school selling season with strong trends that continued through the balance of the quarter.”

8) From Gap: “We were pleased to see our three largest brands, Old Navy, Gap, and Banana Republic, posting strong positive comps in the third quarter, demonstrating the resilience of our portfolio despite a challenging quarter from Athleta.”

9) From TJX: “Our overall comp sales increase of 5% was driven by strong comp sales growth across each of our divisions. Clearly, our value proposition continues to resonate with consumers in the United States, Canada, Europe, and Australia, and we are confident that we gain market share across each of these geographies.” The comp gain “was driven by a combination of a higher average basket and an increase in customer transactions. Further, we saw strong comp increases in both our apparel and home categories.” Price too helped comps.

10) From Williams Sonoma: “In Q3, our comp came in above expectations at 4%, driven by another quarter of positive comps across all of our brands, and we continue to deliver the bottom line despite the substantial tariff headwinds…And we continue to gain market share and outperform the industry, which declined again in Q3.”

11) From La-Z-Boy: “We were pleased to once again deliver modest sales growth, particularly in our wholesale segment, where we also again delivered margin expansion, continuing to create our own momentum in what remains a choppy market.”

12) From Viking Holdings: “Turning to the overall booking environment, we continue to see strong momentum. As of November 2, 2025, and for our core products, 96% of our 2025 capacity was sold, and 70% of our 2026 capacity was already booked too.”

13) From Klarna: This was an analyst question of note, “the credit data looks good in Q3, but are you seeing any signals in your data suggesting that you may have to tighten the credit box in any of your major geographies, especially as we head into the holidays and consumers potentially lean in more on BNPL?” The response from the CEO, “the honest answer is no. We have not seen anything in our data or in our spending that suggests that there should be currently any changes...But I’m keeping a close eye, we’re keeping a close eye on the unemployment numbers.”

14) From Amer Sports: “Amer Sports’ strong momentum continued in the third quarter, as our unique portfolio of premium technical brands continues to create white space and take share in sports and outdoor markets around the world. All three segments performed extremely well led by exceptional Saloman footwear growth, an Arc’teryx omni-comp reacceleration, and solid growth from Wilson Tennis 360 and our Winter Sports Equipment franchises.”

15) Japan’s composite PMI was 52 vs 51.5 with an improvement in manufacturing that is still below 50 at 48.8. Services were unchanged at 53.1. Australia’s index rose .5 pt m/o/m to 52.6 with manufacturing back above 50 at 51.6 from 49.7 while services rose a touch to 52.7. India’s remained strong at 59.9 vs 60.4 with a dip in manufacturing and a lift in services.

16) The November Eurozone PMI was little changed at 52.4 vs 52.5 in October with manufacturing back under 50 at 49.7 while services led the growth at 53.1. S&P Global said, “For months the manufacturing sector of the Eurozone has been marooned in a no-man’s land of directionlessness. Production has picked up slightly since March of this year, but the overall situation has not improved during this period. Companies continue to face weak demand, which is reflected in a slight decline in new orders.” Also, “The service sector in the Eurozone is a ray of hope. Although business activity growth in Germany has slowed significantly, French service providers have returned to growth.”

Negatives:

1) Old news but the September unemployment rate rose one tenth m/o/m to 4.4% as the 470k person increase in the labor force was not fully met by the 251k increase in the household jobs survey. Average hours worked remained at just 34.2.

2) Continuing claims for the week ended 11/8 remained high at 1.974mm.

3) The November US manufacturing index slipped to 51.9 from 52.5. S&P Global said, “manufacturers reported a worrying combination of slower new orders growth and a record rise in finished goods stock. This accumulation of unsold inventory hints at slower factory production expansion in the coming months unless demand revives, which could in turn feed through to lower growth in many service industries.” The bottom line from the UoM, “consumers remain frustrated about the persistence of high prices and weakening incomes.” Encapsulating the two lane consumer highway, “Interviews continue to reveal considerable differences in economic views across the wealth distribution. This month, a majority of consumers without stock holdings as well as consumers in the bottom two terciles of portfolio values spontaneously mentioned high prices as a drag on their personal finances. In contrast, only about one-third of consumers with the largest tercile of stock holdings did so. This gap reflects differences in the degree of pain that inflation and high prices exert for various types of households.”

4) The November Philly manufacturing index stayed below zero at -1.7 vs estimate of +1 and again not correlating with the NY index. The positive though was the 6 month business outlook which rose to 49.6 from 36.2 and that is the best since November 2024.

5) The final November UoM Consumer Confidence index was 51, up from the initial read a few weeks ago of 50.3 but down from 53.6 in October and the weakest level since June 2022 which is one of the lowest prints on record. All of the m/o/m decline was seen in the Current Situation which fell 7.5 pts from October. Expectations lifted a touch to 51 from 50.3. One year inflation expectations were 4.5% vs 4.6% last month. The longer term view fell to 3.4% from 3.9%.

6) From the Cleveland Fed, WARN (Worker Adjustment and Retraining Notification) notices continue to rise and were up almost 11k in October to 39,000, the highest since May and the 2nd highest since October 2020. Prior to 2020 this level was last seen in 2008 and 2009.

7) Foreign central banks continue to sell US Treasuries according to the September TIC data. Year to date, ‘official’ aka, central banks, sold a net $21b of US notes and bonds after selling $27b in 2024.

8) The November NAHB home builder sentiment index rose 1 pt m/o/m to 38. The consensus was for an unchanged print but it still remains well below 50. After popping by 9 pts in October, the Future outlook slipped by 3 pts to 51 with hopes that lower mortgage rates will drive activity. The Present Situation though while up 2 pts to 41 and the best since April, is still 9 pts below 50. The Prospective Buyers Traffic remains depressed at 26, though up 1 pt m/o/m. Lower mortgage rates of course didn’t help much and the NAHB said “Market uncertainty exacerbated by the government shutdown along with economic uncertainty stemming from tariffs and rising construction costs kept builder confidence firmly in negative territory in November.” Some more, “While lower mortgage rates are a positive development for affordability conditions, many buyers remain hesitant because of the recent record-long government shutdown and concerns over job security and inflation,” said NAHB Chairman Buddy Hughes, a home builder and developer from Lexington, N.C. “More builders are using incentives to get deals closed, including lowering prices, but many potential buyers still remain on the fence.”

9) Purchase applications in the weekly MBA data fell 2.3% w/o/w and has been really choppy week to week. Refi’s fell for a 3rd straight week, down by 7.3%.

10) From Home Depot: “Big ticket comp transactions for those over $1,000 were positive 2.3% compared to the third quarter of last year. We were pleased with the performance we saw in categories such as appliances, portable power, and gypsum. However, we continue to see softer engagement in larger discretionary projects where customers typically use financing to fund renovation projects…the primary driver of that sales pressure was the lack of storm activity in the quarter. We don’t plan for storms per se, but there’s always some weather impact in the baseline. And given last year pretty significant storm activity, and this year truly zero. There was no storm activity this year. So, we saw that most acutely in October.” Also, “We are expecting interest rates and mortgage rates to come down, which they did, that would have been some assistance to housing, but we really just saw ongoing consumer uncertainty and pressure in housing that are disproportionately impacting home improvement demand.”

11) From Target: “Q3 comp sales were down 2.7%, reflecting continued softness in discretionary categories like home and apparel, partially offset by growth in food and beverage and Fun 101” which includes toys, video games, music and sporting goods. “Turning to the consumer, many of the themes remain largely consistent with what we shared in prior quarters. Guests are choiceful, stretching budgets, and prioritizing value. They’re spending where it matter most, especially in food, essentials, and beauty, while looking for trend right deals in discretionary categories. They want quality and price to coexist.”

12) From Bath & Body Works: “While the consumer environment is tougher, this is no excuse as we continue to underperform the sector.”

13) From Williams Sonoma: This is a lot to manage, “Our updated guidance reflects all the tariffs in place as of this call. This includes the new Section 232 tariffs on furniture, the revised 20% additional China tariffs, the 50% India tariff, the 20% Vietnam tariff, and an average 18% tariff on the rest of the world, as well as the 50% steel and aluminum tariffs and the 50% copper tariff. In fact, our incremental tariff rate has more than doubled from 14% earlier this year to 29% today, inclusive of all the tariffs I just mentioned.”

14) From La-Z-Boy: “While consumer trends remain challenging for our industry, we continue to be agile and hone our execution. We saw our strongest results of the second quarter in October, where we achieved positive written same store sales. However, results in early November remain mixed.”

15) From Energizer: “As we enter fiscal 2026, we know the first quarter will be transitional. It will reflect a challenging sales comparison, transitional tariff related costs and moderating consumer sentiment…Consumers are certainly seeking value. They’re cautious. They’re very comfortable shifting channels to be able to find the value of the product that meet their needs.”

16) Japan’s October CPI rose 3.1% y/o/y as expected but up from 3% in September.

17) JGB yields continue higher.

18) The UK PMI fell to 50.5 from 52.2 with a lift in manufacturing to 50.2 from 49.7 while services fell to 50.5 from 52.3. S&P Global said, “Economic growth has stalled, job losses have accelerated, and business confidence has deteriorated. The PMI is broadly consistent with no change in GDP in November and a meager .1% quarterly pace of growth so far in the fourth quarter.”

19) UK October retail sales fell 1% m/o/m ex auto fuel, twice the estimate of a .5% drop.

20) The November UK CBI industrial orders index was weak at -37 vs -38 in October. CBI said “Manufacturers face a challenging end to the year. What’s striking in this month’s survey is how consistently firms link the slowdown to uncertainty ahead of the Budget, with customers delaying purchases and investment until they know what’s coming.”

21) UK CPI was up 3.6% y/o/y vs the estimate of 3.5% but the core rate of 3.4% was as forecasted. Both compare with 3.8% and 3.5% respectively in the month before and service inflation of 4.5% continues to be their main inflationary challenge.

BY Doug Kass · Nov 21, 2025, 3:44 PM EST

Words can't describe how exhausted I am!

So I am leaving early for the weekend.

Enjoy the next few days.

I will be traveling to Los Angeles on Monday so I will see you all back on Tuesday morning.

You will be in the very capable hands of TheStreet Pro Portfolio manager Chris Versace.

Be safe.

BY Doug Kass · Nov 21, 2025, 3:10 PM EST

With S&P cash +115 handles, I added to my (SPY) $663.69 and (QQQ) $595.83 shorts.

BY Doug Kass · Nov 21, 2025, 2:17 PM EST

Defensive consumer staples are the world's fair today: (PG) (+$3), (KO) (+$1.75), (PEP) (+$1.05), (KMB) ($1.40).

BY Doug Kass · Nov 21, 2025, 2:05 PM EST

On the NVDA news I am back shorting the indices:

* (SPY) $663.55

* (QQQ) $595.71

BY Doug Kass · Nov 21, 2025, 1:58 PM EST

Trump considering selling (NVDA) chips to China.

BY Doug Kass · Nov 21, 2025, 1:55 PM EST

Scott Galloway's No Mercy/No Malice:

BY Doug Kass · Nov 21, 2025, 1:45 PM EST

The action is terrible.

BY Doug Kass · Nov 21, 2025, 1:25 PM EST

Here are today's things:

* Traded the indices actively:

(SPY) bought at $653.74 and sold at $655.76.

(QQQ) bought at $584.51 and sold at $586.65.

* (HOOD) bought $105.30 and sold at $106.75.

* (PLTR) bought $152.84 and sold $153.92.

* Initiated investment longs in (AMZN) at $217.48, (META) at $585.27 and (MSFT) at $469.87.

BY Doug Kass · Nov 21, 2025, 12:50 PM EST

BY Doug Kass · Nov 21, 2025, 12:27 PM EST

I have sold out of my trading long rentals in (HOOD) $107.29 and (PLTR) $153.37 on the robust rally in the indices (+75 S&P handles from the lows).

BY Doug Kass · Nov 21, 2025, 11:58 AM EST

As promised, I have sold out my trading long index positions.

I am out of index long with S&P cash +36 handles:

* (SPY) $656.01

* (QQQ) $587.01

BY Doug Kass · Nov 21, 2025, 11:45 AM EST

I have purchased very small long positions in (MSFT) at $469.87, (AMZN) at $216.75 and (META) at $585.27.

BY Doug Kass · Nov 21, 2025, 11:40 AM EST

From Peter Boockvar:

As the US PMI from S&P Global doesn’t include the key service areas like wholesale and retail trade in addition to construction, I prefer to rely on the ISM services report. Thus, here I will mostly focus on what they said about US manufacturing in the month of November. Its index slipped to 51.9 from 52.5. For those looking at the services component, it was 55 vs 54.8 in the month before.

They said this of note, which does include some commentary on services too:

“manufacturers reported a worrying combination of slower new orders growth and a record rise in finished goods stock. This accumulation of unsold inventory hints at slower factory production expansion in the coming months unless demand revives, which could in turn feed through to lower growth in many service industries.”

They also said “Manufacturers took on more staff at the fastest rate for three months.” And, “Companies took on more staff to meet improved demand, though a sustained reluctance to take on additional staff due to cost related budget cuts and the need to focus on efficiency improvements was again evident, dampening jobs growth. Some companies also reported difficulties finding staff, often struggling to fill vacancies caused by voluntary leavers.” Particularly with services, “service sector job creation was only modest and slower than in October.”

On prices, “Input cost inflation accelerated sharply in November, hitting the fastest rate for three years barring the jump in costs seen in May. Tariffs were again the predominant reason cited by companies for increased costs, alongside reports of higher wage rates.” Specifically with manufacturing though, “input price inflation cooled to the lowest since February but remained well above the average seen over the past three years” and “selling price inflation slowed in manufacturing but reaccelerated in services.”

Finally, “Optimism hit a five-month high in manufacturing and an 11-month record in services…The brighter mood in part reflected reduced concerns over tariffs and worries over political disruptions more generally and was buoyed by the ending of the government shutdown. However, the survey also saw a broader improvement in sentiment about the economic outlook, in part driven by increased customer enquiries and hopes of greater policy support, including lower interest rates and more government fiscal stimulus.”

Bottom line, still a mixed economy but with hopes for improvement due to tariff relief, the end of the shutdown and Fed rate cuts.

The final November UoM Consumer Confidence index was 51, up from the initial read a few weeks ago of 50.3 but down from 53.6 in October and the weakest level since June 2022 which is one of the lowest prints on record. All of the m/o/m decline was seen in the Current Situation which fell 7.5 pts from October. Expectations lifted a touch to 51 from 50.3. One year inflation expectations were 4.5% vs 4.6% last month. The longer term view fell to 3.4% from 3.9%.

The bottom line from the UoM, and I would say the same thing, “consumers remain frustrated about the persistence of high prices and weakening incomes.”

Also of note, “By the end of the month, sentiment for consumers with the largest stock holdings lost the gains seen at the preliminary reading. This group’s sentiment dropped about 2 index points from October, likely a consequence of the stock market declines seen in the final two weeks of the interview period.”

Encapsulating the two lane consumer highway, “Interviews continue to reveal considerable differences in economic views across the wealth distribution. This month, a majority of consumers without stock holdings as well as consumers in the bottom two terciles of portfolio values spontaneously mentioned high prices as a drag on their personal finances. In contrast, only about one-third of consumers with the largest tercile of stock holdings did so. This gap reflects differences in the degree of pain that inflation and high prices exert for various types of households.”

Lastly and disconcertedly, “Meanwhile, the overall probability of personal job loss increased this month to the highest reading since July 2020…generally speaking, younger consumers report higher probabilities of job loss than older consumers, consistent with national unemployment trends by age.

UoM Consumer Confidence

One year inflation expectations

BY Doug Kass · Nov 21, 2025, 11:30 AM EST

I moved to S/M in size in indexes on the move lower to -15 on S&P cash.

I will be reducing on a rally.

BY Doug Kass · Nov 21, 2025, 11:21 AM EST

BY Doug Kass · Nov 21, 2025, 11:20 AM EST

Moved (HOOD) $102.95 and (PLTR) $148.16 longs to medium-sized.

BY Doug Kass · Nov 21, 2025, 11:18 AM EST

With S&P cash about unchanged, I have moved back into a small net long exposure for the first time in many months

BY Doug Kass · Nov 21, 2025, 10:39 AM EST

BY Doug Kass · Nov 21, 2025, 10:35 AM EST

(PEP) and (KMB) doing yeoman's work.

BY Doug Kass · Nov 21, 2025, 10:30 AM EST

From Peter Boockvar:

Nothing is by accident and NY Fed President John Williams is telling us in a prepared speech that he wants a December rate cut, in so many words. “I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions. Therefore, I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals.”And, “My assessment is that the downside risks to employment have increased as the labor market has cooled, while the upside risks to inflation have lessened somewhat. Underlying inflation continues to trend downward, absent any evidence of second round effects emanating from tariffs.”Of course there is no real definition of ‘neutral’ and why trying to predict what Fed members will do has gotten tougher. According to the last dot plot, a 1% REAL rate is considered neutral and with CPI/PCE around 3%, they are already at neutral. Please somewhat ask Williams what his definition of ‘neutral’ is. Either way, he’s telling us he wants to cut next month.

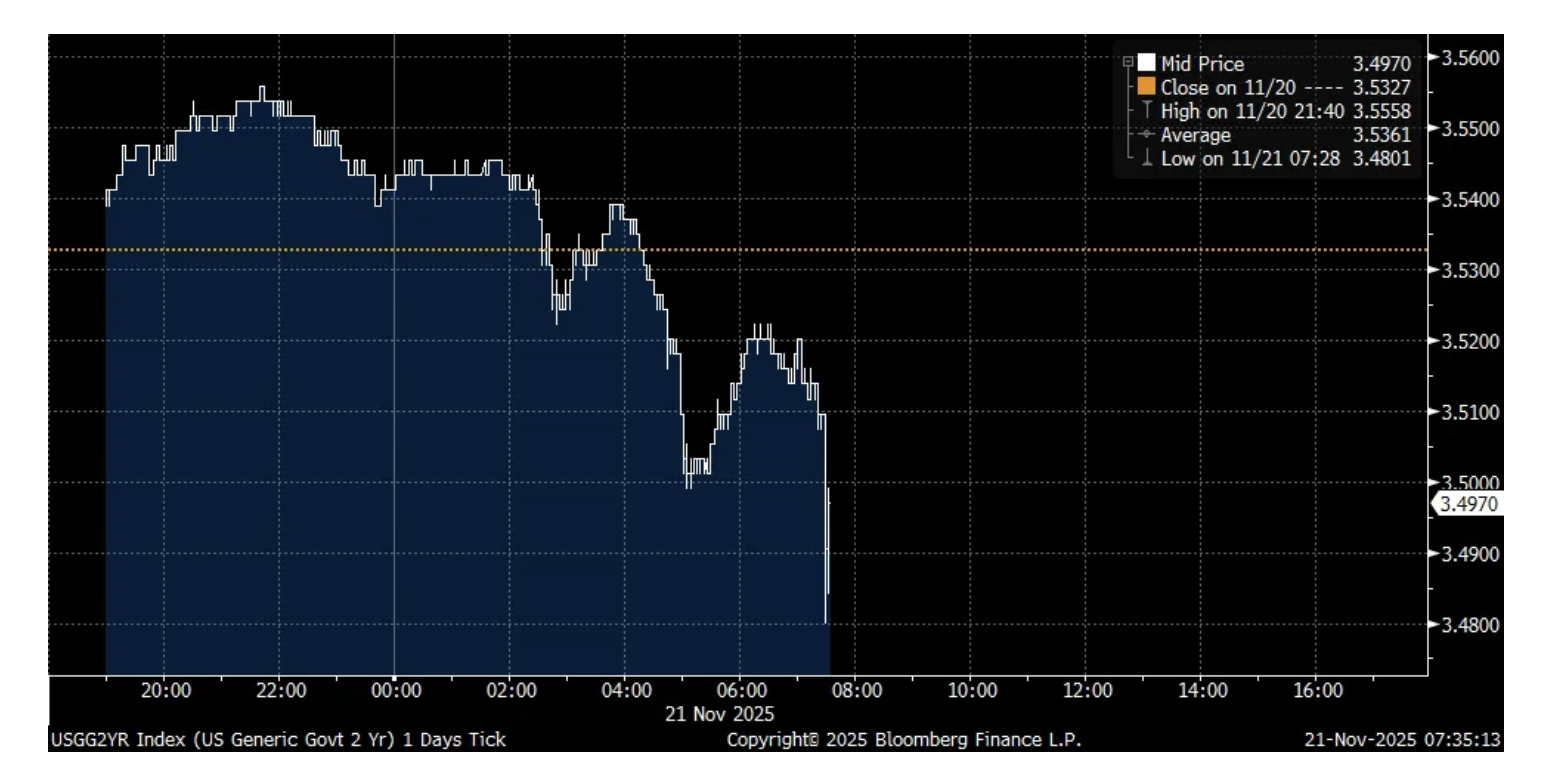

2 yr yields fell in response

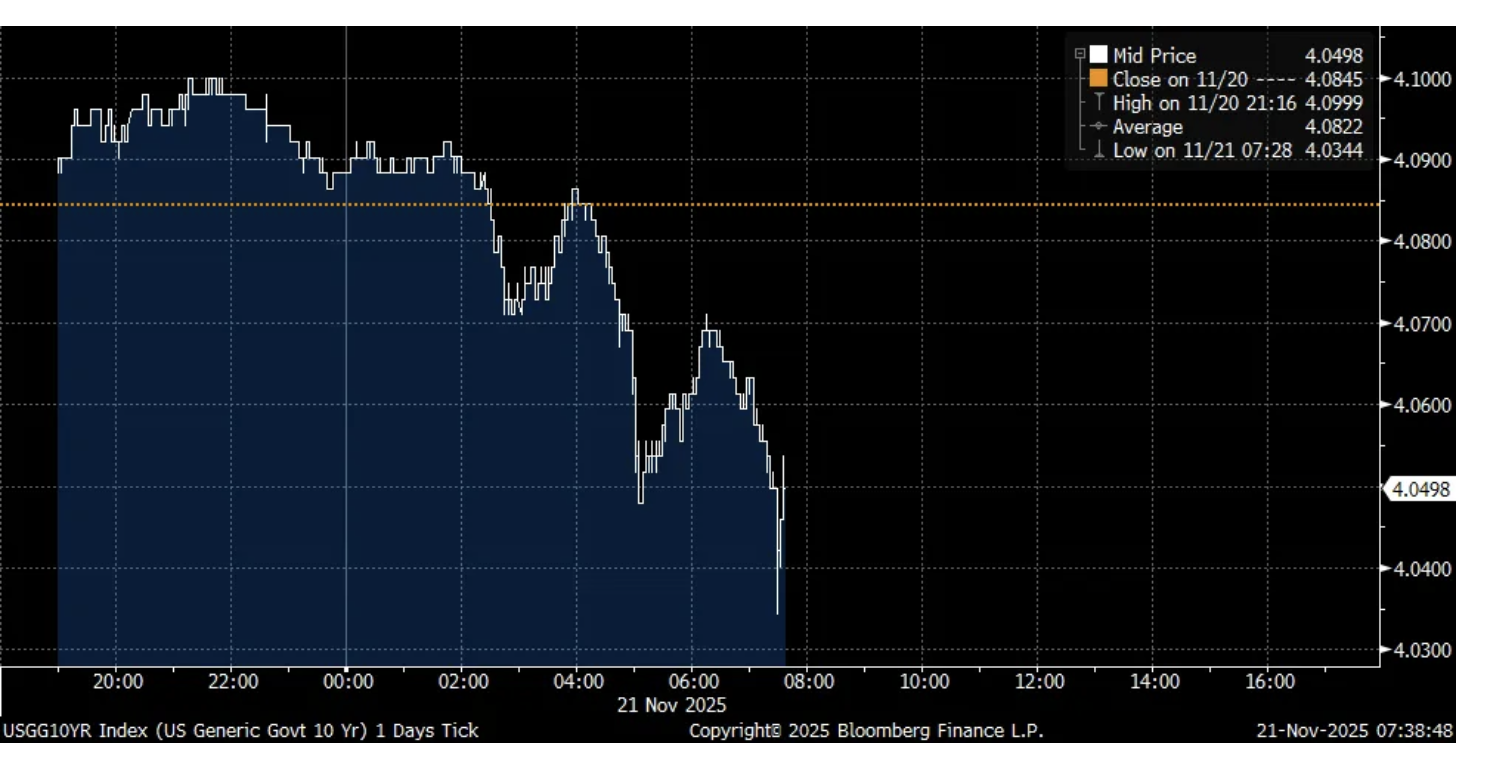

But 10 yr yield is where it was just before after initial dip

BY Doug Kass · Nov 21, 2025, 10:10 AM EST

I am back long the indexes:

* (SPY) $653.89

* (QQQ) $585.75.

BY Doug Kass · Nov 21, 2025, 10:09 AM EST

This morning I literally can't post fast enough given the volatility - as my posts (and cost) become so quickly "outdated."

Suffice to say I am gingerly buying all whooshes lower.

BY Doug Kass · Nov 21, 2025, 9:55 AM EST

From Peter Boockvar:

I wrote this yesterday and we clearly know that the question was answered rather quickly.

“With respect to Nvidia’s earnings, I do not think there is a debate on how solid the quarter was nor the good guidance. It is more on the sustainability of it, subject to the ongoing levels of hyperscaler spend, including OpenAI. What will be a test though starting today is what has been priced in already. As of this writing, the stock is trading pre-market at around $196 which compares with the intraday high on October 29th of $212 and a closing high of $207 on that same day. Business is great right now and Huang addressed the depreciation debate on their chips, but does the current market cap already reflect all of this? We’ll soon see.”

From Walmart:

“We drove positive transaction counts and unit volumes and we’re gaining market share in grocery and general merchandise including here in the US, where we saw strength across income cohorts and especially with higher income households.”

“Comps were good across each month of the quarter.”

“At a category level, sales in general merchandise were positive with fashion, home, and automotive leading the way. Grocery performed well with good unit growth, and health and wellness was up low double digits.”

With Sam’s Club, “As we look at our customers and members here in the US, they’re still spending with upper and middle income households driving our growth. We continue to benefit from higher income families choosing to shop with us more often.”

“Middle income households have been steady, and while lower income families have been under additional pressure of late, we’re encouraged by how our teams are meeting them with greater value across necessities and doing what we can to help them stretch their dollars further.”

“For the quarter, like-for-like inflation in Walmart US was 1.3% with food and general merchandise up low single digits. We continue working to resist the upward pressure on our cost of goods and to manage our mix. We have about 7,400 active rollbacks in Walmart US right now, with more than half of those in the grocery category. Often, our 90 day rollbacks lead to a permanent price reduction.”

“Everyone wants value.”

On the consumer, “we’d say that overall, the environment feels pretty consistent. There’s certainly some pockets of moderation that we’re keeping an eye on. But if you look at our guidance for 4Q, it would indicate that we have an expectation that it’s going to look pretty similar to the other quarters this year. Holiday is off to a pretty good start. Back-to-school tends to be an early indicator for how that goes, Halloween, likewise for Thanksgiving and everything that we’ve seen so far makes us optimistic and encouraged about customers and members leaning into the seasonal events and holiday shopping period.”

From Ross Stores, the discount retailer and which is trading up pre market with solid execution and market share gains:

Comps grew 7% as “Our merchants delivered a compelling assortment of brand name values, which led to broad based growth across all major merchandise categories.”

“We had an excellent back-to-school selling season with strong trends that continued through the balance of the quarter.”

“For the third quarter at Ross, cosmetics, shoes and ladies were the strongest merchandise areas. By geography, we saw broad based strength with the Southeast and the Midwest performing the best.” They also said “Home was slightly below the chain average.”

“From a pricing perspective, it is clear the consumer is prioritizing value, and our updated assortment is driving stronger customer engagement. While pricing has increased across the retail environment, our commitment to delivering value remains unchanged.”

“In terms of household income, not only was the sales very broad based across geographies and merchandise categories, they’re also very broad based across trade area income levels.”

The Gap is trading up pre market too and they said this:

“We were pleased to see our three largest brands, Old Navy, Gap, and Banana Republic, posting strong positive comps in the third quarter, demonstrating the resilience of our portfolio despite a challenging quarter from Athleta.”

With Old Navy in particular, “Customers responded to the compelling value proposition, resulting in healthy growth in average unit retail and notably across all income cohorts, which is encouraging despite widely reported macroeconomic pressure on the low income consumer.”

Gap is seeing more business from Gen Z customers and Banana continues to turn around. “We have seen more high income consumers choosing Gap, and we really do believe that with the strong competitive position that we’ve taken between premium and value and the fact that we’re bridging the generation gap.”

Bath & Body Works plunged by 25% yesterday. They said this:

“While the consumer environment is tougher, this is no excuse as we continue to underperform the sector.” Their execution issues were glaring.

Moving on.

As eyes should be on the Japanese JGB market where yields were lower overnight for the first time in a week with details of their fiscal package now out, October CPI rose 3.1% y/o/y as expected but up from 3% in September. The yen is finally rallying too as the rhetoric from the Finance Minister heated up on its weakness. “We are concerned the current movement is extremely one-sided and abrupt...Regarding excessive volatility and disorderly movements, including speculative trends, we will take appropriate measures as necessary based on the Japan-US Finance Ministers’ Joint Statement” and said it’s “certainly a possibility” they can intervene.

I’ll add, the BoJ can easily stem the weakness by hiking rates next month.

To some November PMI’s ahead of the US one today. Japan’s composite index was 52 vs 51.5 with an improvement in manufacturing that is still below 50 at 48.8. Services was unchanged at 53.1. Australia’s index rose .5 pt m/o/m to 52.6 with manufacturing back above 50 at 51.6 from 49.7 while services rose a touch to 52.7. India’s remained strong at 59.9 vs 60.4 with a dip in manufacturing and a lift in services.

The November Eurozone PMI was little changed at 52.4 vs 52.5 in October with manufacturing back under 50 at 49.7 while services led the growth at 53.1. S&P Global said, “For months the manufacturing sector of the Eurozone has been marooned in a no-man’s land of directionlessness. Production has picked up slightly since March of this year, but the overall situation has not improved during this period. Companies continue to face weak demand, which is reflected in a slight decline in new orders.”

“Germany and France are moving in the same direction - unfortunately, it is the wrong one, with the index falling markedly in both.”

“The service sector in the Eurozone is a ray of hope. Although business activity growth in Germany has slowed significantly, French service providers have returned to growth.”

Profit margins are getting squeezed as “The two price indices from the survey signaled differing trends midway through the final quarter of the year. Input costs increased sharply, and at the fastest pace since March.”

But, “On the other hand, the pace of output price inflation eased in November, slowing to the weakest in just over a year and pointing to only a modest monthly rise in charges across the Eurozone private sector.”

The UK PMI fell to 50.5 from 52.2 with a lift in manufacturing to 50.2 from 49.7 while services fell to 50.5 from 52.3. S&P Global said, “Economic growth has stalled, job losses have accelerated, and business confidence has deteriorated. The PMI is broadly consistent with no change in GDP in November and a meager .1% quarterly pace of growth so far in the fourth quarter.”

Also out was UK October retail sales which fell 1% m/o/m ex auto fuel, twice the estimate of a .5% drop.

The fall in JGB yields spilled over to a fall in European and US Treasury yields but as stated here many times, cuts in short term interest rates by the respective central bankers in the US and Europe has not led to a drop in long rates and in Europe, they are higher.

BY Doug Kass · Nov 21, 2025, 9:45 AM EST

-NVRI +39% (Divests Clean Earth to Veolia for $3.04B and Taxable Spin-Off of Harsco Environmental and Rail Businesses to Shareholders)

-AZTA +15% (earnings, guidance)

-GAP +7.6% (earnings, guidance)

-TELO +7.2% (Telomir-1 Kills Aggressive Human Leukemia Cells)

-ASTS +4.9% (announces BlueBird 6 launch date of Dec 6th)

-INTU +3.7% (earnings, guidance)

-DOCS +2.6% (Raymond James Raised DOCS to Strong Buy from Outperform, price target: $65 from $75)

-MOG.A +2.6% (earnings, guidance)

-ROST +2.6% (earnings, guidance)

-ANAB -12% (TESARO, a GSK subsidiary, initiates litigation against AnaptysBio, Inc.)

-ESTC -12% (earnings, guidance)

-VEEV -6.2% (earnings, guidance)

-GEOS -4.6% (earnings)

-NGVC -4.3% (earnings, guidance)

-ALB -4.2% (weakness in lithium mining names; reportedly China exchange's move to curtail lithium market speculation causes lithium prices to crash)

-CPRT -3.0% (earnings)

-POST -2.9% (earnings, guidance)

-AHR -2.6% (prices 8.1M secondary sale of shares)

BY Doug Kass · Nov 21, 2025, 9:20 AM EST

BY Doug Kass · Nov 21, 2025, 9:10 AM EST

BY Doug Kass · Nov 21, 2025, 9:00 AM EST

Fed Speakers:

7:30 a.m.: Fed Bank of New York President Williams (Voter) gives keynote before the Annual Conference of the Central Bank of Chile, Santiago (Text and audience Q&A expected. Event information: bcentral.cl);

8 a.m.: Fed Bank of Boston President Collins (Voter) is interviewed on CNBC; 8:30AM: Fed Board Governor Barr (Voter) delivers opening remarks at the College Fed Challenge Finals Washington, DC (No Q&A. No livestream);

8:45 a.m.: Fed Vice Chair Jefferson (Voter) speaks at the Federal Reserve Bank of Cleveland Financial Stability Conference (Text available. Audience Q&A expected);

9 a.m.: Fed Bank of Boston President Collins (Voter) gives opening remarks before the "U.S. Economy in a Changing Landscape" conference at the Federal Reserve Bank of Boston, Boston, MA (Advance text expected. No Q&A. Livestream link );

9 a.m.: Fed Bank of Dallas President Logan (Non-Voter) participates in moderated panel before the "SNB and its Watchers 2025" event, Zurich, Switzerland (Text available. Audience Q&A expected. No livestream);

Saturday: 11:55 a.m.: Federal Reserve Bank of Boston President Susan Collins (Voter) gives brief, informal closing remarks before the "U.S. Economy in a Changing Landscape" conference at the Federal Reserve Bank of Boston, Boston, MA (No Q&A. Livestream link)

BY Doug Kass · Nov 21, 2025, 8:45 AM EST

* And talking strategy when wrong footed...

phogan

1 hour ago

While I have no interest in trying to trade like you do, I've got great respect for how you do it as well as for your stamina!

Jaw4860

1 hour ago

True .What are your results using his investment style in general ?Mine are sub optimal .My style is better

Dougie Kass

STAFF

Just Now

Replying to Jaw4860

I have implemented a trading strategy (in the Indices) to offset the fact that my big picture outlook (a bear in a bull market) has been sorely wrong footed.

That my negative market outlook has been very poorly timed and that I have not taken advantage of the opportunit set, I have written continuously.To offset this poor timing I have utilized trading the indices to generate positive returns.

Buying and holding, with the benefit of hindsight, would have been the right thing to do.I can not go back in time and change my view - I can churn out profits (cash register) effect to produce positive returns.

Since early 2024 (with some exceptions like April 2025) I have had negative net exposure to equities.Despite the market's climb I have generated positive returns in 21 of the last 22 months (with the only negative return a drawdown of only -22 basis points).

And in the 23rd month, November, I have had a positive return month to date.I try my best, I try to be objective (and challenge my negative points) and I take ownership for being wrong.

BY Doug Kass · Nov 21, 2025, 8:24 AM EST

BY Doug Kass · Nov 21, 2025, 7:35 AM EST

BY Doug Kass · Nov 21, 2025, 7:15 AM EST

BY Doug Kass · Nov 21, 2025, 7:00 AM EST

* First the technicians got on Mag 7, then the cryptocurrency trade and then the market was supposedly broadening out (and the Russell index was the favorite ice cream flavor)... what now?

Bonus — Here are some great links:

BY Doug Kass · Nov 21, 2025, 6:45 AM EST

BY Doug Kass · Nov 21, 2025, 6:35 AM EST

BY Doug Kass · Nov 21, 2025, 6:25 AM EST

BY Doug Kass · Nov 21, 2025, 6:15 AM EST

At 510 AM I added to indices:

* (SPY) $650.22

* (QQQ) $581.22

I am now out of long trading rentals for a quick profit:

I have no index positions on now, but I want to buy weakness.

BY Doug Kass · Nov 21, 2025, 6:06 AM EST

I added to (HOOD) at $103.75 and (PLTR) at $153.29.

BY Doug Kass · Nov 21, 2025, 6:00 AM EST

With S&P futures -8 handles (they were +22 handles about an hour ago), I have taken a LONG trading rental in the indices (at around 445 AM):

* (SPY) $652.20

* (QQQ) $583.85

BY Doug Kass · Nov 21, 2025, 5:55 AM EST

At around 745 PM, I sold my trading long rentals for a nice gain:

* (SPY) $654.55

* (QQQ) $587.26

BY Doug Kass · Nov 21, 2025, 5:50 AM EST

The S&P Short Range Oscillator has moved further into an oversold — now at -3.73% v -2.77%.

As I mentioned yesterday, I expect a far deeper oversold over the next couple of days.

BY Doug Kass · Nov 21, 2025, 5:45 AM EST