Wednesday's After-Hours Gainers and Losers

% Gainers

% Losers

BY Doug Kass · Nov 19, 2025, 4:45 PM EST

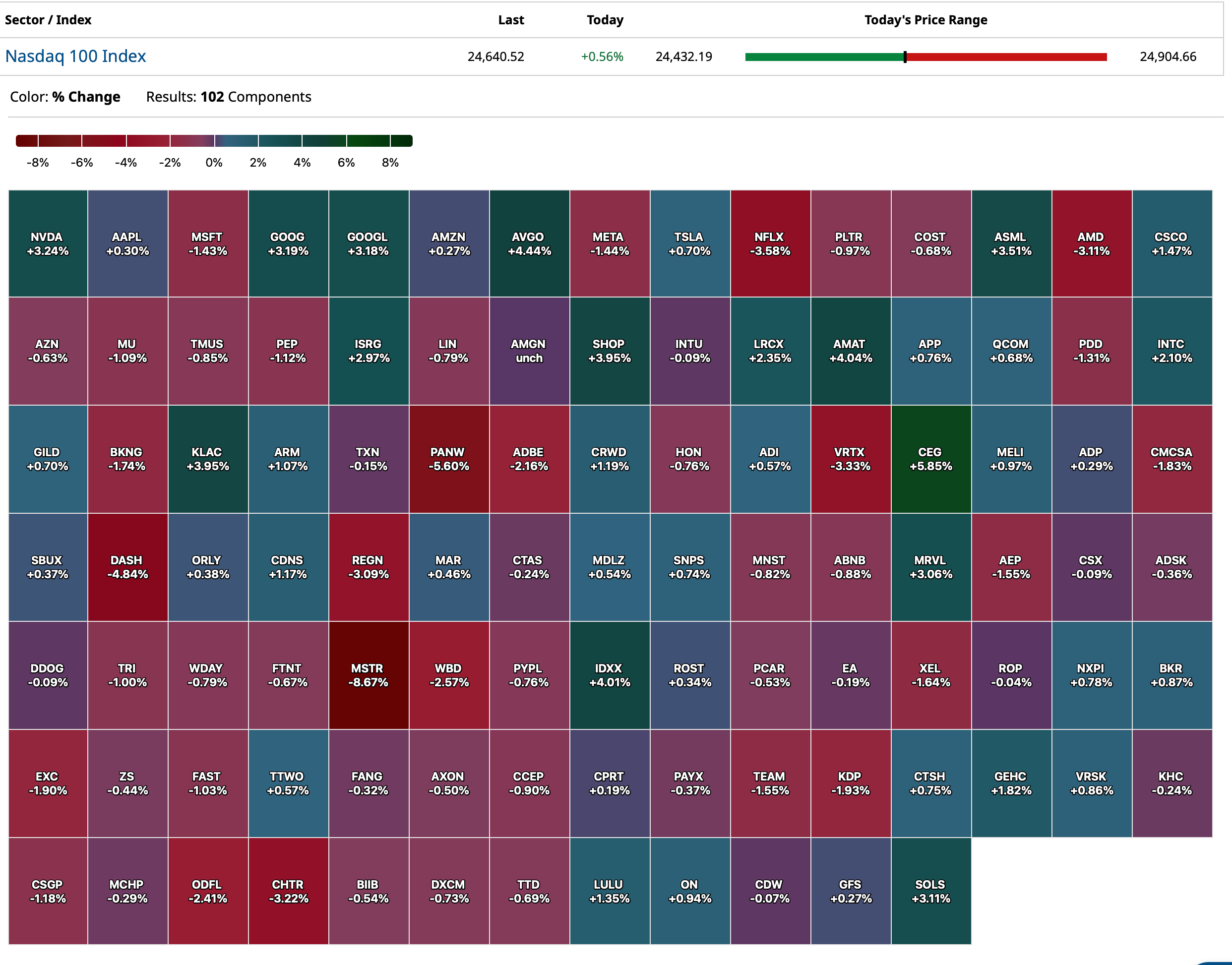

BY Doug Kass · Nov 19, 2025, 4:45 PM EST

BY Doug Kass · Nov 19, 2025, 4:35 PM EST

- NYSE volume 7% below its one-month average

- NASDAQ volume 20% below its one-month average

- VIX index: down 3.81% to 23.75

BY Doug Kass · Nov 19, 2025, 4:24 PM EST

This is also interesting on the Anthropic investment issue, although I think the lead was buried that Google's (GOOGL) newest model is not using Nvidia (NVDA) GPUs:

I excerpted this section below from the end of the article, although the whole thing is worth a read. This I think is the other reason Nvidia dumped all that money into Anthropic, they seem to be paying them to stay on Nvidia architecture. Heck it pretty much says so in the press release:

“For the first time, NVIDIA and Anthropic are establishing a deep technology partnership to support Anthropic’s future growth. Anthropic and NVIDIA will collaborate on design and engineering, with the goal of optimizing Anthropic models for the best possible performance, efficiency, and TCO, and optimizing future NVIDIA architectures for Anthropic workloads. Anthropic’s compute commitment will initially be up to one gigawatt of compute capacity with NVIDIA Grace Blackwell and Vera Rubin systems.”

You could make a very good argument these “investments” should actually be treated as cost of sales.

While the easy (free) money may help Anthropic over the short term, in my view, Nvidia architecture will leave them as a high-cost player in a commodity industry. My view too, for a variety of reasons, Google will emerge as the winner (smallest loser) in the space over time. It is already headed in that direction based on the latest market share data I saw. Google also is not the only player who is architecting their own chips and infrastructure.

EXCERPT:

Post Script: I Got The Numbers

I got the numbers.

Prior to putting the $10 billion into Anthropic, NVDA Circular Investment Fund 2 had invested $24 billion in 59 deals since the beginning of 2025. In 2024, NVDA Circular Investment Fund 1 invested $23 billion in 54 deals. Now all of the sudden, $10 billion into one deal, which brings this year’s total to $34 billion. Further they “only” put $6.6 billion into OpenAI, which is a substantially bigger business, as well as “only” $6 billion into xAI. The deals are getting more rapid, and larger, even though the businesses are smaller.

Nvidia’s $24B AI deal blitz has Wall Street asking questions about ‘murky’ circular investments

Interestingly, in the Anthropic deal, on paper, the valuation was marked up from $183 billion in its September fundraise, to the $350 billion now. What happened between September and now? As best as I can tell the only that happened was Anthropic was badly and embarrassingly hacked and used for a cyberattack (

To put the new and improved $350 billion valuation in perspective, an interesting article on Tether. Tether has a dominant market position, actually makes $15 billion a year, which is multiples of Anthropic’s 2025 revenue, and looks to be raising money at a $500 billion valuation. Arguably, if it was not for the crazy world we are in today, that $500 billion valuation should be closer to $150 billion.

BY Doug Kass · Nov 19, 2025, 3:00 PM EST

I'm still short (MSTR) .

BY Doug Kass · Nov 19, 2025, 2:12 PM EST

No trades since last reported!

BY Doug Kass · Nov 19, 2025, 1:17 PM EST

BY Doug Kass · Nov 19, 2025, 11:19 AM EST

* Phew!

* This all adds up...

For the third time today I am taking a small and quick gain in my Index trading.

With S&P cash +25 handles (it was +65 handles at 10:16 a.m.!), I just made the following covers:7

* (SPY) $662.85

* (QQQ) $600.50

From less than an hour ago:

With S&P cash +65 handles I am back shorting the indexes:

* (SPY) $666. 67

* (QQQ) $605.15

Position: Short SPY S QQQ S

By Doug Kass Nov 19, 2025 10:16 AM EST

BY Doug Kass · Nov 19, 2025, 11:03 AM EST

I will be leaving today at around 2:30 p.m. to deal with my friend's recent passing.

BY Doug Kass · Nov 19, 2025, 10:45 AM EST

With S&P cash +65 handles I am back shorting the indexes:

* (SPY) $666. 67

* (QQQ) $605.15

BY Doug Kass · Nov 19, 2025, 10:16 AM EST

... like a kid with emojis ...

BY Doug Kass · Nov 19, 2025, 10:10 AM EST

I added to (KMB) at $102.36.

BY Doug Kass · Nov 19, 2025, 9:49 AM EST

Sold indices for a very quick profit:

* (SPY) $662.20

* (QQQ) $598.57

BY Doug Kass · Nov 19, 2025, 9:46 AM EST

I have again taken a trading long rental in the Indexes:

* (SPY) $660.47

* (QQQ) $596.90

BY Doug Kass · Nov 19, 2025, 9:38 AM EST

From Peter Boockvar

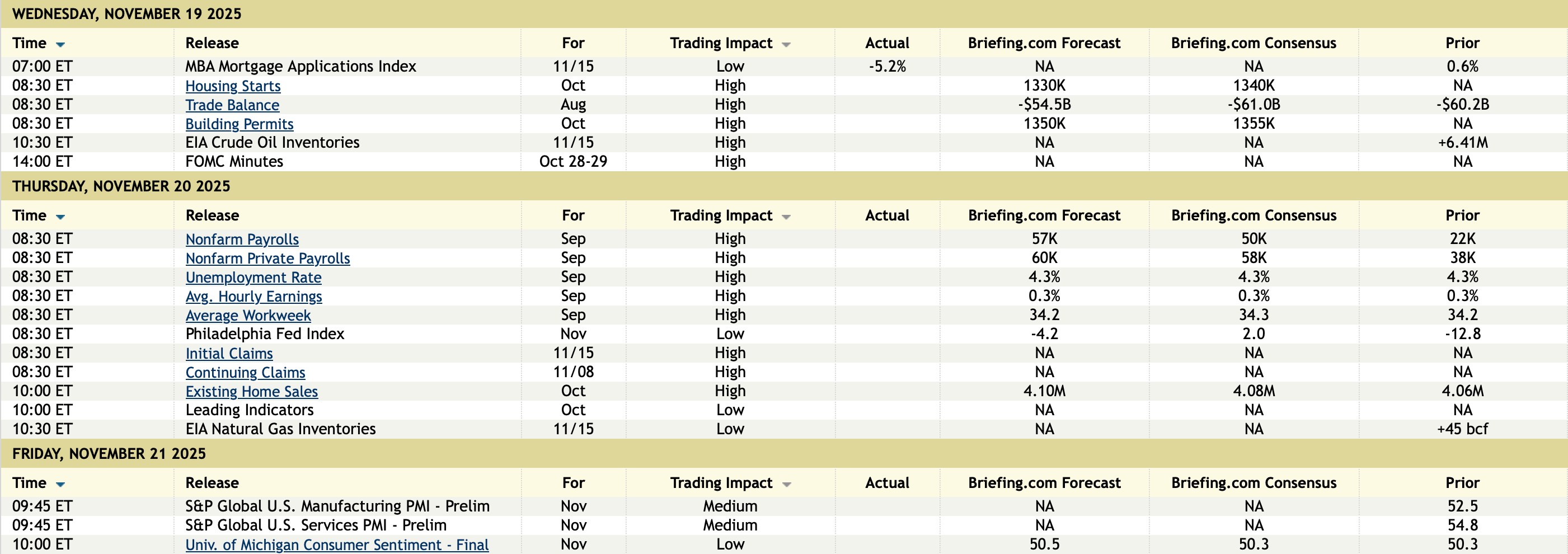

I’m going to start with a reprint of the numbers I put together last month after the big hyperscalers released earnings that show the level of CapEx relative to revenue (not cash flow which would be even higher) to just highlight why investors are asking tougher questions, as they should. These are no longer asset light businesses as we now clearly know.

Oracle expected CapEx $35 billion in fiscal yr 5/26 vs expected revenues of $67 billion and a ratio that equals 52%. It was 10% in 2022.

Microsoft expected CapEx $88 billion in fiscal yr 6/26 vs expected revenues of $323 billion and a ratio that equals 27%. It was 12% in 2022.

Meta expected CapEx $69 billion in fiscal yr 12/25 vs expected revenues of $196 billion and a ratio that equals 35%. It was 16% in 2021 (as they ramped up spend in 2nd half of 2022).

Google/Alphabet expected CapEx $85 billion in fiscal yr 12/25 vs expected revenue of $336 billion and a ratio that equals 25%. It was 10% in 2021 (also ramped up spend in back half of 2022).

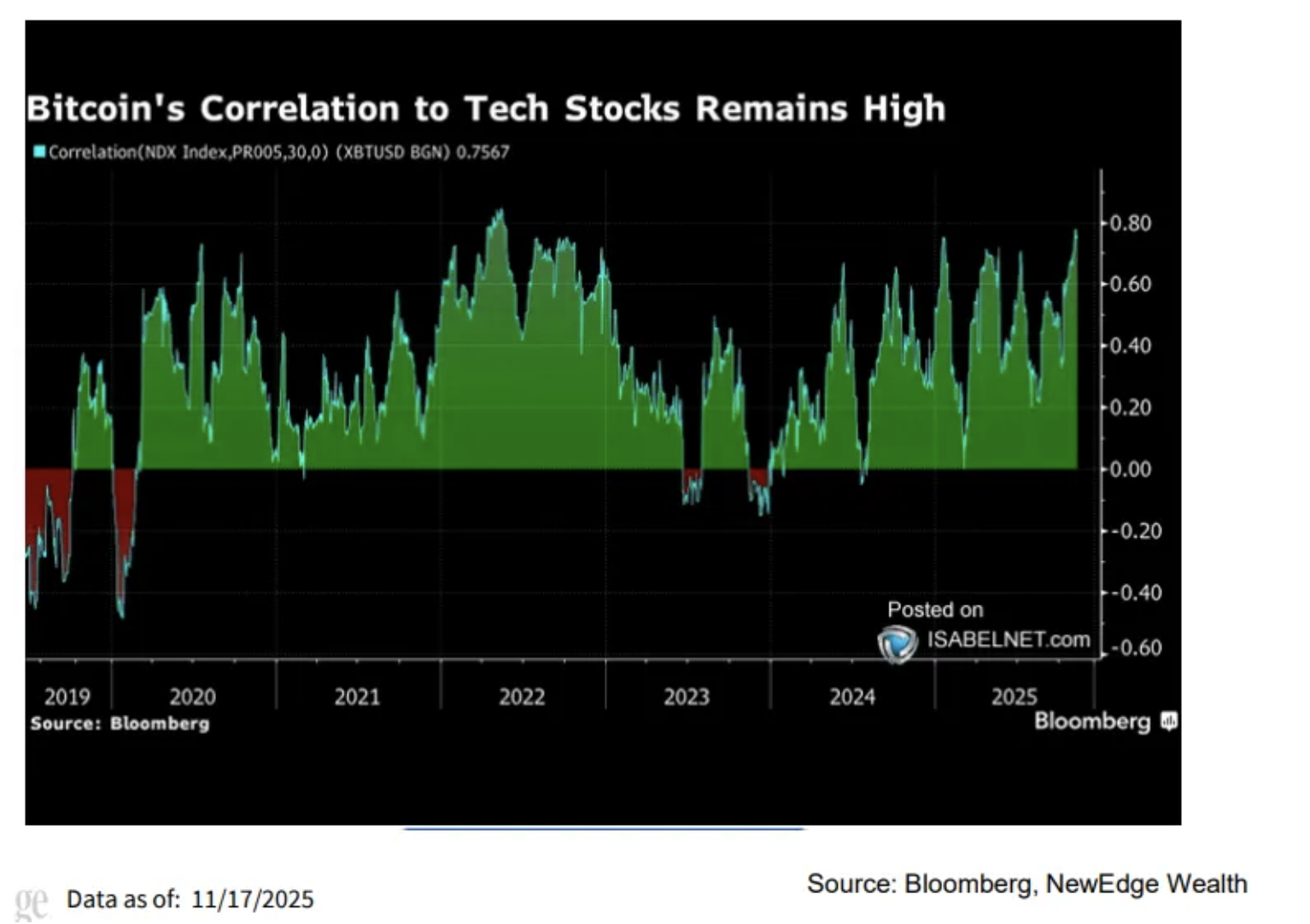

With respect to Bitcoin and the message its action might be sending, this was a great chart from my friend Cameron Dawson in her super helpful weekly chart fest that reflects the real relationship that Bitcoin has and it’s not yet with gold.

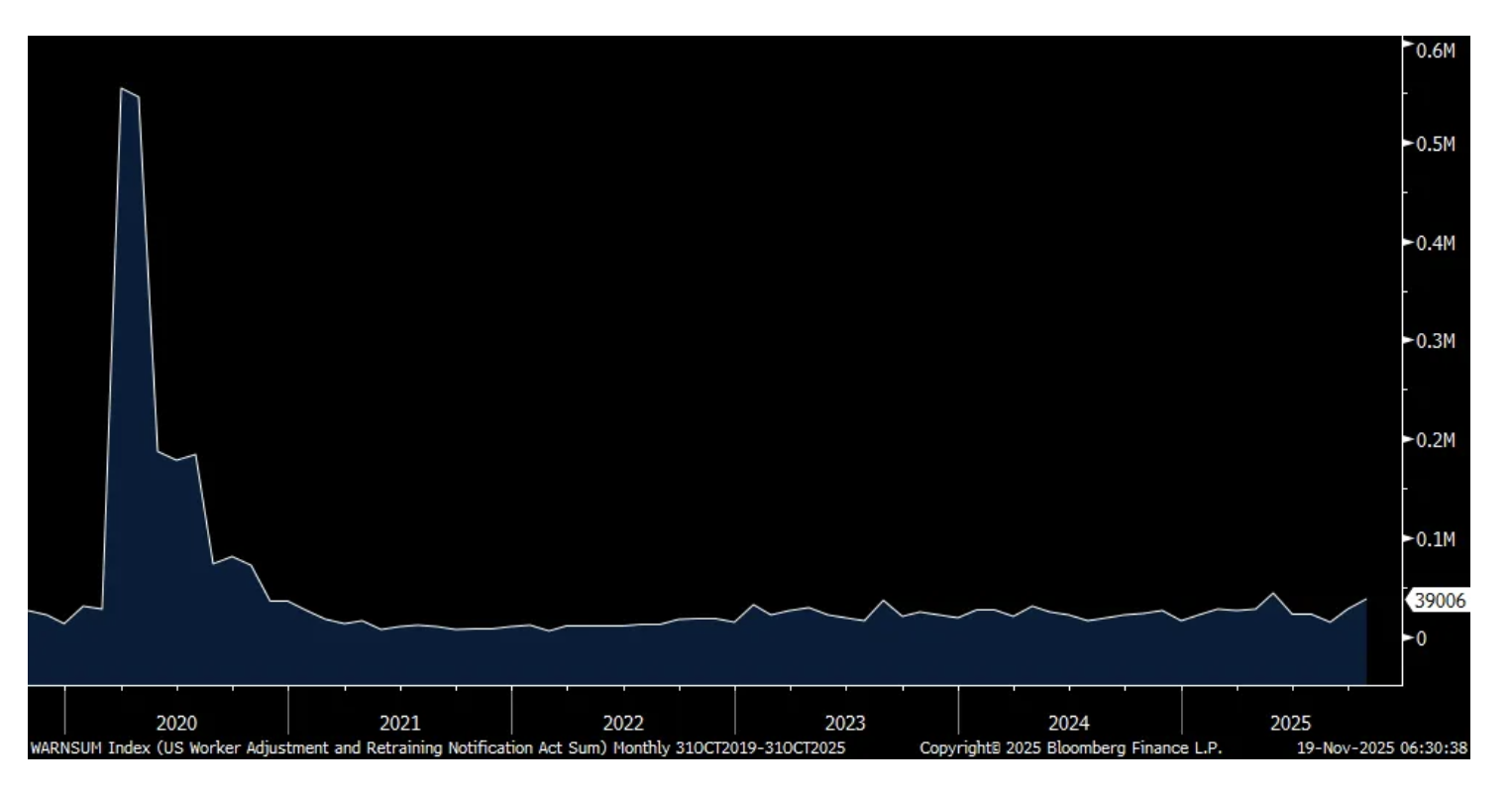

From the Cleveland Fed, WARN (Worker Adjustment and Retraining Notification) notices continue to rise and were up almost 11k in October to 39,000, the highest since May and the 2nd highest since October 2020. Prior to 2020 this level was last seen in 2008 and 2009. This reflects activity in 21 states and where employers need to provide written warnings two months before large layoffs and/or there are closings of plants.

WARN Notices

Foreign central banks continue to sell US Treasuries as seen in the September TIC data last night but private foreign buying is still coming in with still a lot of that taking place via the Cayman Islands. Year to date, ‘official’ aka, central banks, sold a net $21b of US notes and bonds after selling $27b in 2024. What have they been buying more of? Gold, as seen in the stats. Robustly, private foreign buying has bought $448b year to date. Japan remains the largest foreign holder of US Treasuries at $1.19 trillion, followed by the UK at $865b but that can include hedge fund buying and any other foreign purchases via UK banks. Then China at $700b. Canada has $476b, Belgium has $467b but much of that is via Euroclear and thus clouding the actual holders. Then followed by Cayman at $427b where many hedge funds (and in the UK too I’m sure) have placed their basis trades.

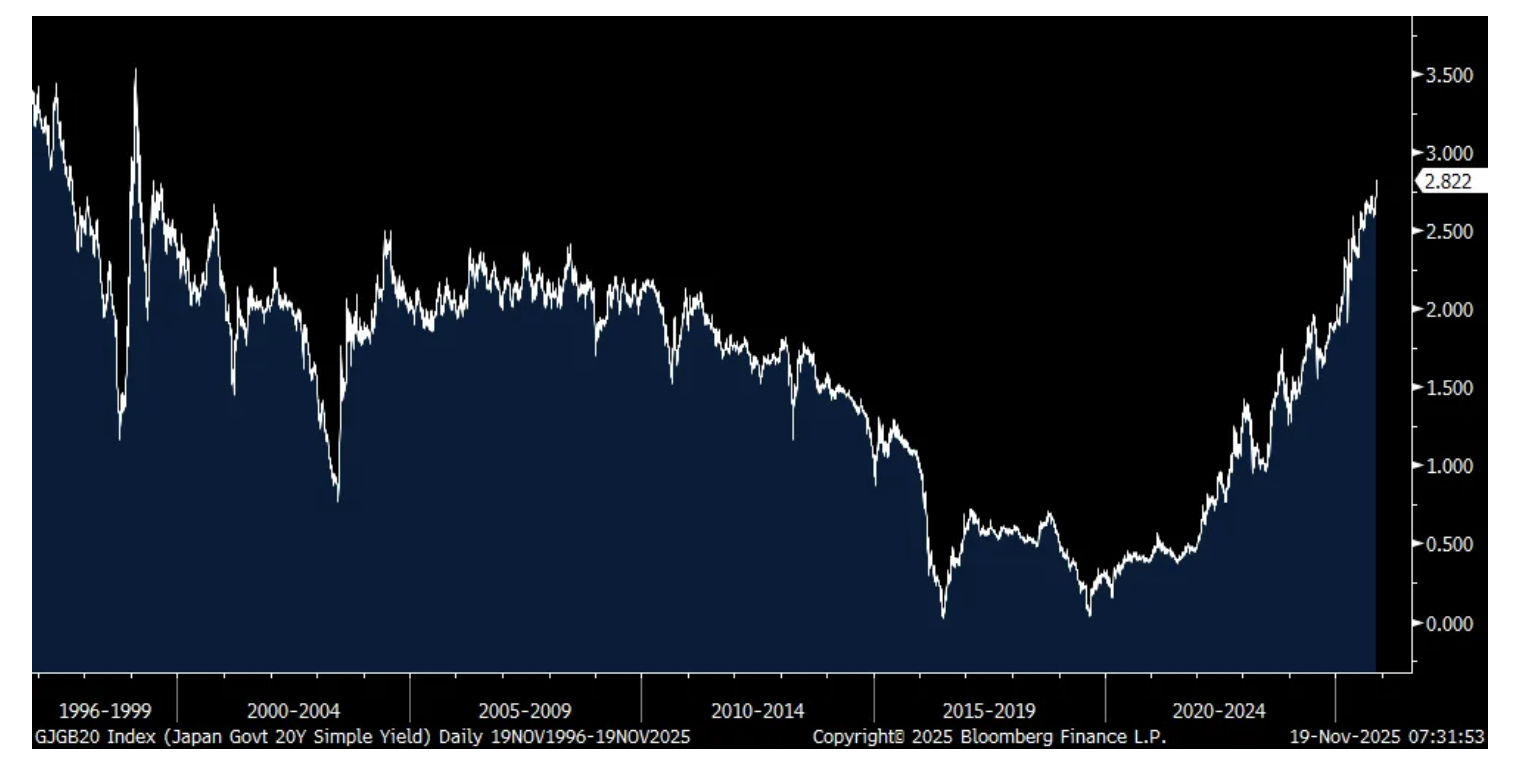

Speaking of the Japanese, JGB yields continue higher and those yields continue to be more and more attractive relative to US yields but the cost of capital is stressful for a highly indebted country that is Japan. The 10 yr JGB yield is up for a 5th straight day, up by almost 3 bps to 1.77%, a fresh 17 yr high. The 20 yr yield is now at the highest since March 1999. The 30 yr and 40 yr yields have also broken out to new highs. Again, something to watch very closely I argue. And it’s not helping the yen which keeps on falling, now at 156, a level last seen in January.

JGB 20 yr Yield

Gilt yields are little changed as UK CPI was up 3.6% y/o/y vs the estimate of 3.5% but the core rate of 3.4% was as forecasted. Both compare with 3.8% and 3.5% respectively in the month before and service inflation of 4.5% continues to be their main inflationary challenge. Inflation breakevens are flat with the about as expected figures.

On to the earnings calls.

From Home Depot:

During the third quarter, our comp average ticket increased 1.8% and comp transactions decreased 1.6%. The growth in comp average ticket primarily reflects a greater mix of higher ticket items, customers continuing to trade up for new and innovative products as well as modest price increases.”

“Big ticket comp transactions for those over $1,000 were positive 2.3% compared to the third quarter of last year. We were pleased with the performance we saw in categories such as appliances, portable power, and gypsum. However, we continue to see softer engagement in larger discretionary projects where customers typically use financing to fund renovation projects.”

“the primary driver of that sales pressure was the lack of storm activity in the quarter. We don’t plan for storms per se, but there’s always some weather impact in the baseline. And given last year pretty significant storm activity, and this year truly zero. There was no storm activity this year. So, we saw that most acutely in October.”

Also, “We are expecting interest rates and mortgage rates to come down, which they did, that would have been some assistance to housing, but we really just saw ongoing consumer uncertainty and pressure in housing that are disproportionately impacting home improvement demand.”

“So I mean, it’s certainly a very interesting consumer dynamic out there. On the one hand, you look at certain economic indicators, and you say, geez, things are pretty good. You look at GDP, you look at PCE, those are both strong. But on the other hand, what’s impacting us in home improvement is the ongoing pressure in housing and incremental consumer uncertainty. So take housing, housing has been soft for some time. We all know higher interest rates and affordability concerns. But what we’re seeing now is even less turnover. The housing activity is truly at 40 yr lows as a percentage of housing stock. I think we’re at 2.9% turnover.”

“And then home prices have started to adjust in even more markets over this past quarter. And then when you look at the consumer, what’s going to spark the consumer, we still believe we have one of the healthiest consumer segments in the whole economy. But again, the economic uncertainty continues largely now due to living costs, affordability is the word that’s being used a lot, layoffs, increased job concerns, etc...So that’s why we don’t see an uptick in that underlying storm adjusted demand in the business.”

More on housing, purchase applications in the weekly MBA data fell 2.3% w/o/w and has been really choppy week to week. Refi’s fell for a 3rd straight week, down by 7.3%.

From Klarna and whose stock fell 9.3% because of higher than expected provisions for loan losses as they ramped up activity under its ‘fair financing’ offering:

This was an analyst question of note, “the credit data looks good in Q3, but are you seeing any signals in your data suggesting that you may have to tighten the credit box in any of your major geographies, especially as we head into the holidays and consumers potentially lean in more on BNPL?”

The response from the CEO, “the honest answer is no. We have not seen anything in our data or in our spending that suggests that there should be currently any changes...But I’m keeping a close eye, we’re keeping a close eye on the unemployment numbers.”

From Energizer which sells batteries and auto care brands like STP and Armor All:

“The macro environment continues to evolve. Tariffs have increased our costs, consumer demand softened late in the year, and supply chains required rapid rebalancing. We responded quickly, realigning our manufacturing footprint to minimize tariff exposure, and executing pricing actions to protect margins. These steps weren’t easy, but they were necessary and created a solid foundation for future growth.”

“As we enter fiscal 2026, we know the first quarter will be transitional. It will reflect a challenging sales comparison, transitional tariff related costs and moderating consumer sentiment.”

“I would say the biggest changes we’ve just seen is softening consumer sentiment. You’ve heard it from a lot of our peers, you’ve certainly seen it in some of the macro data that as we progress from August to September and into October, you really did see softening consume sentiment and we’re seeing it in the category data for batteries. We are seeing some improvement in that, but we didn’t feel like it was appropriate to rely on that continuing to ramp up.”

“Consumers are certainly seeking value. They’re cautious. They’re very comfortable shifting channels to be able to find the value of the product that meet their needs.”

BY Doug Kass · Nov 19, 2025, 9:20 AM EST

BY Doug Kass · Nov 19, 2025, 9:12 AM EST

BY Doug Kass · Nov 19, 2025, 9:00 AM EST

BY Doug Kass · Nov 19, 2025, 8:45 AM EST

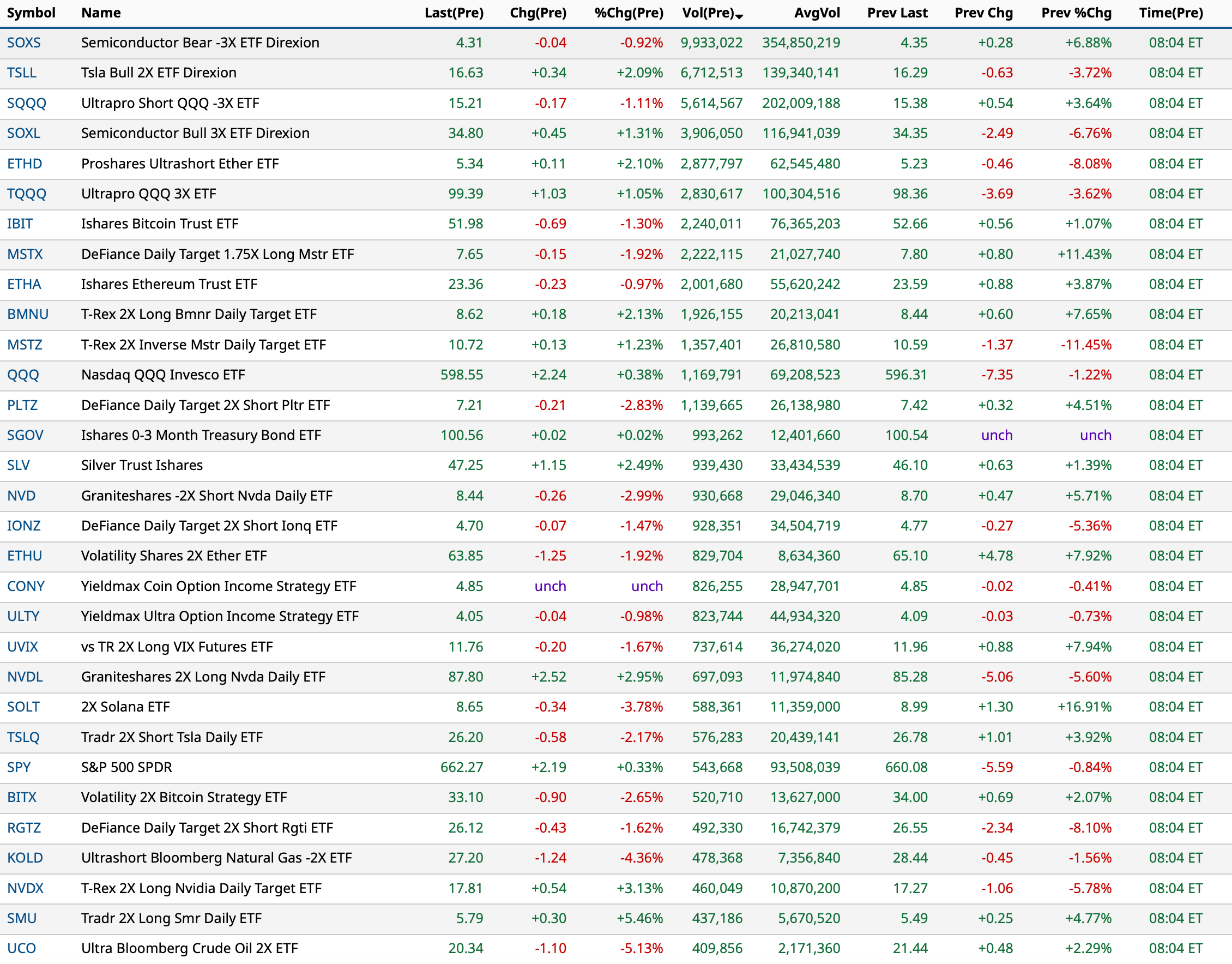

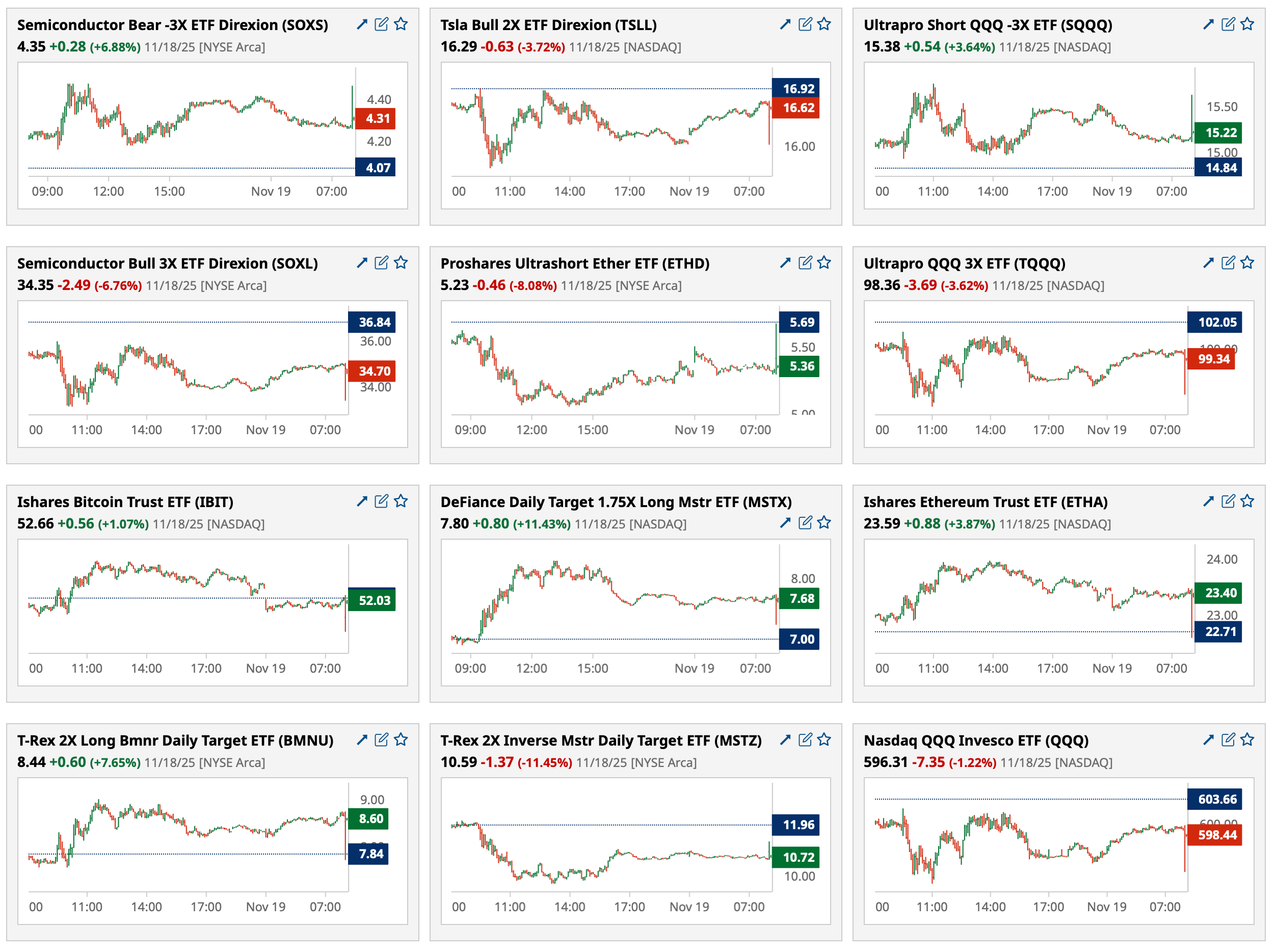

- KZIA +50% trial update

- LZB +6% earnings

- ELDN +5% trial data

- CHPT +4% balance sheet update

- ON +3% buyback announcement

- RILY +3% earnings

- CEG +3% US gov loan backing Crane Clean Energy Center

- LOW +5% earnings

- DASH +2% Jefferies upgrade

- DY +7% earnings

- VIK +2% earnings

- TJX +3% earnings

- VIK +2% earnings

- SEMR +70% Adobe purchase

- PLUG -20% convertible offering

- KULR -9% earnings

- IPAR -5% earnings/guidance

- ECO -4% offering

- OLMA offering

- TGT -3% earnings

- NOK -7% guidance

BY Doug Kass · Nov 19, 2025, 8:32 AM EST

The step up in valuation Anthropic got in this deal is stunning. Now $350 billion. And that makes the point.

The Nvidia (NVDA) /Microsoft (MSFT) investment, in my view, was not about earning a return on the investment, it was about buying business.

Notice, absent from this round were all the traditional sources of capital, because it seems they don’t want to touch it here. The traditional sources of capital have turned into tulip pickers, and they still didn’t participate.

Nvidia/Microsoft seemingly allowed for the step up in valuation, because they do not care about earning a return on their investment. It appears they just care about the business they bought and were unconcerned about price.

If memory serves, this is now Nvidia's biggest investment, by a fair bit. It is into a subscale player that is far from the industry leader, at a massive valuation. In my view, the fact that Nvidia's investments in its own customers are becoming bigger and of lower quality at ridiculous valuations, speaks volumes about what is really going on here.

BY Doug Kass · Nov 19, 2025, 7:30 AM EST

BY Doug Kass · Nov 19, 2025, 6:30 AM EST

BY Doug Kass · Nov 19, 2025, 6:20 AM EST

The S&P Short Range Oscillator is at -0.8% vs. -1.42%.

BY Doug Kass · Nov 19, 2025, 6:10 AM EST

BY Doug Kass · Nov 19, 2025, 5:55 AM EST

I was a little too tall, could've used a few pounds

Tight pants, points, hardly renowned

She was a black haired beauty with big dark eyes

And points all her own, sitting way up high

Way up firm and high

Out past the cornfields where the woods got heavy

Out in the back seat of my '60 Chevy

Workin' on mysteries without any clues

Workin' on our night moves

Tryin' to make some front page drive-in news

Workin' on our night moves

In the summertime, mmm

In the sweet summertime

- Bob Seger, Night Moves

Dougie Kass

At around 6PM I took a trading LONG rental in the Indices:

Dougie Kass

Adding:

SPY $659.40

QQQ $594.97

Dougie Kass

Sold Indices for a small profit (315AM)

SPY $661.35

QQQ $597.38

BY Doug Kass · Nov 19, 2025, 5:45 AM EST

World's first AI attack just happened 🚨 And who's behind it? Chinese state-backed hackers. Anthropic says they hijacked Claude Code to run AI cyber espionage. They used autonomous agents to infiltrate ~30 global companies, banks, manufacturers and government networks. So, Show more

Join us on spaces at 11am ET to talk charts and more! x.com/i/spaces/1LyxB…