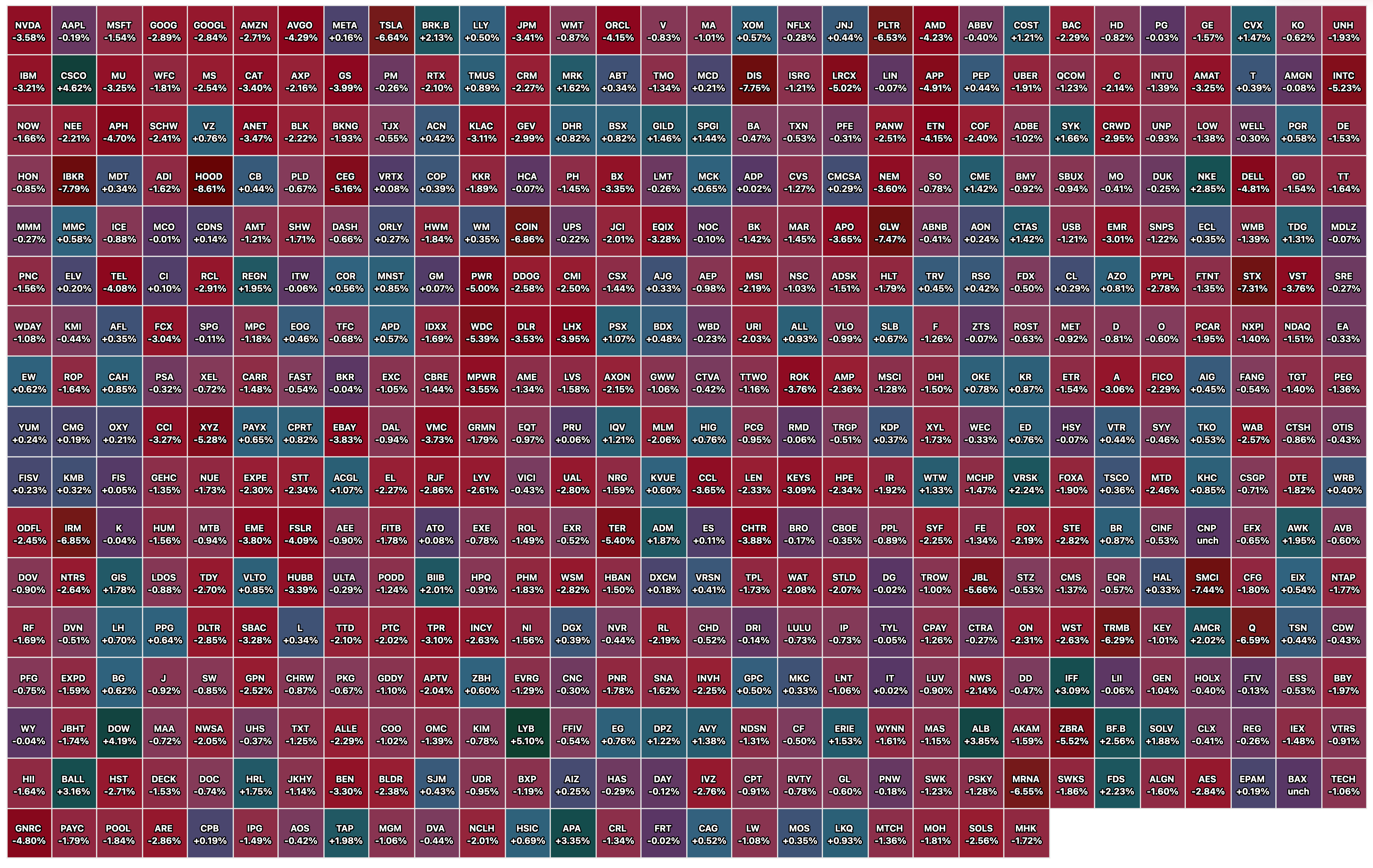

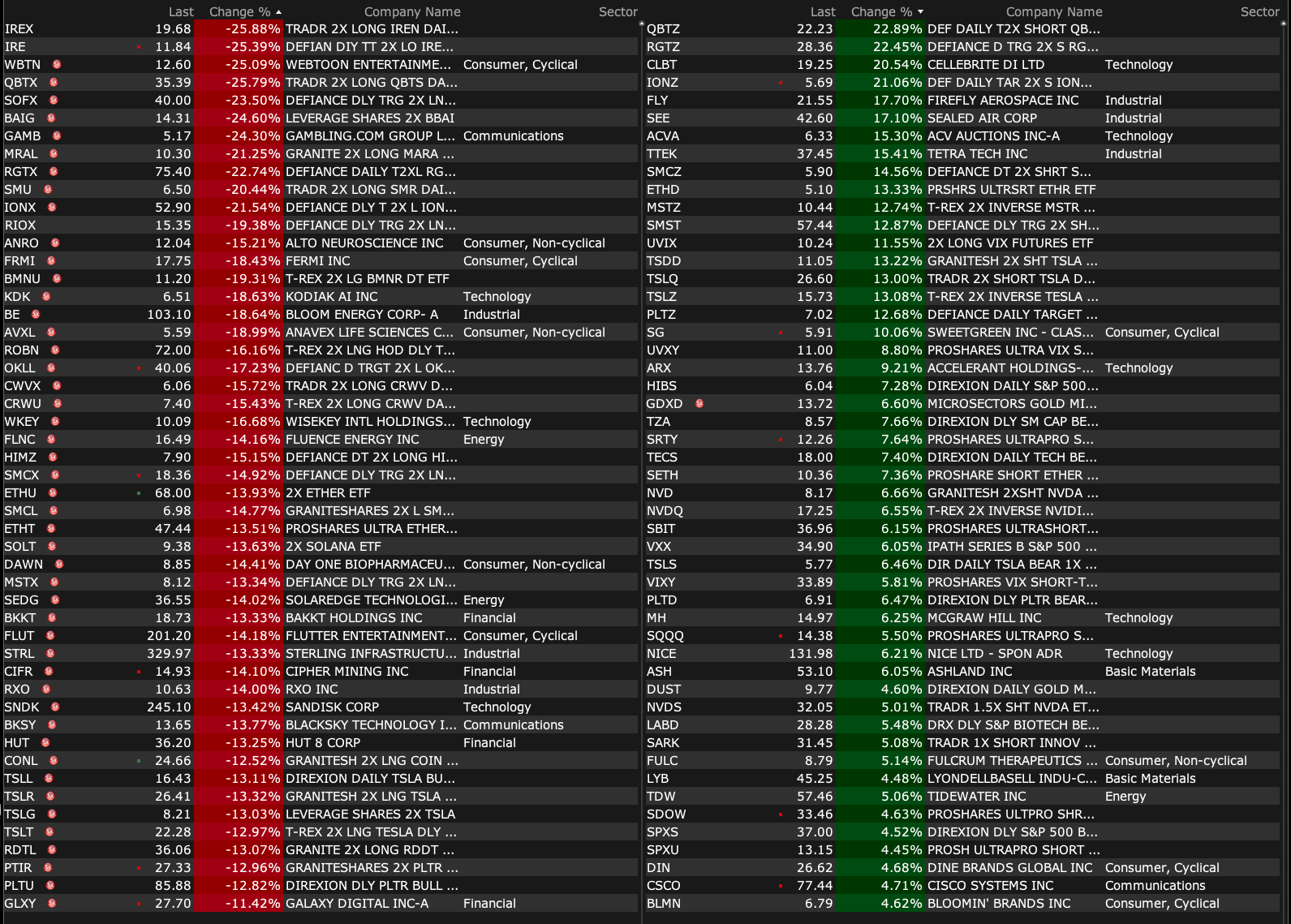

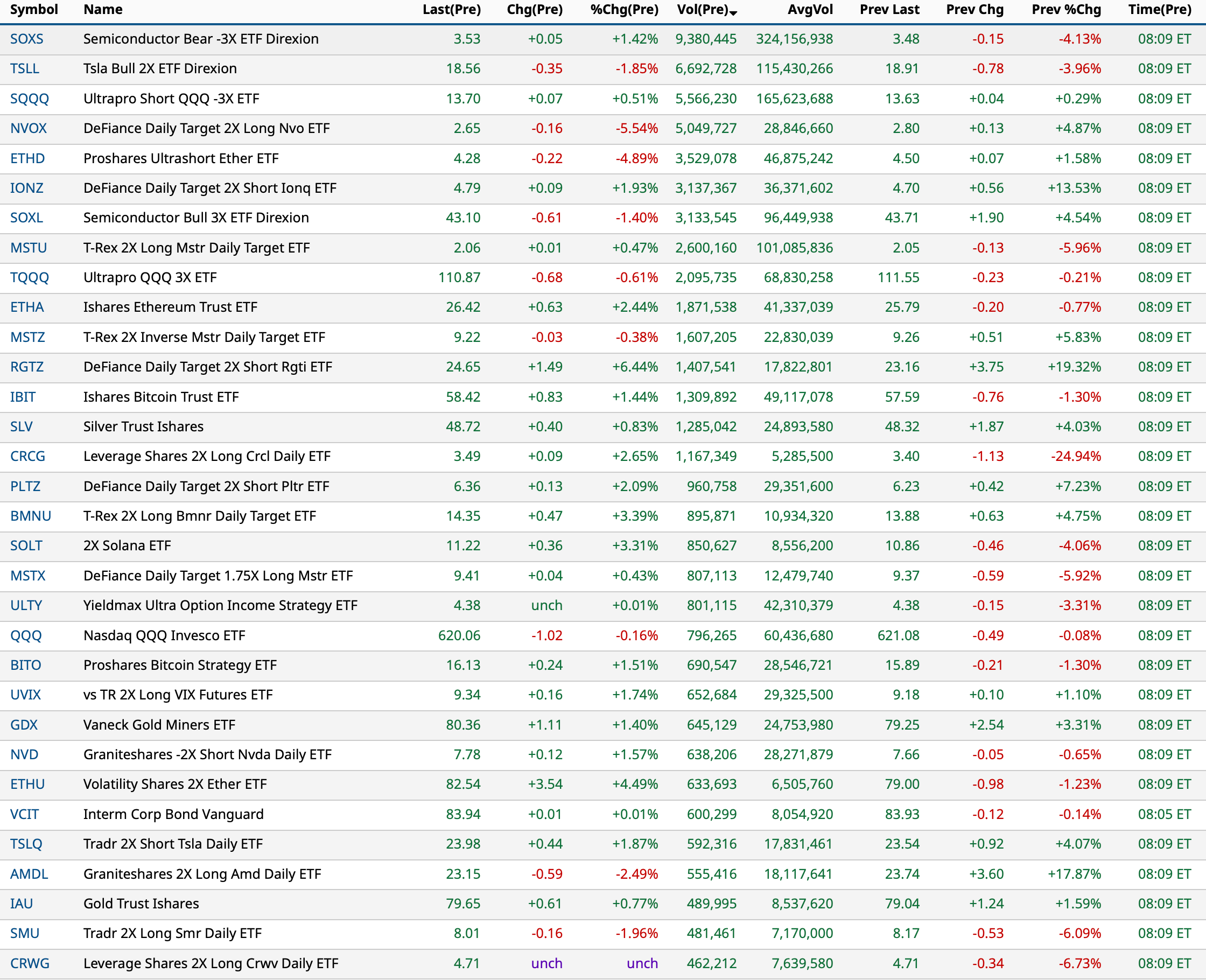

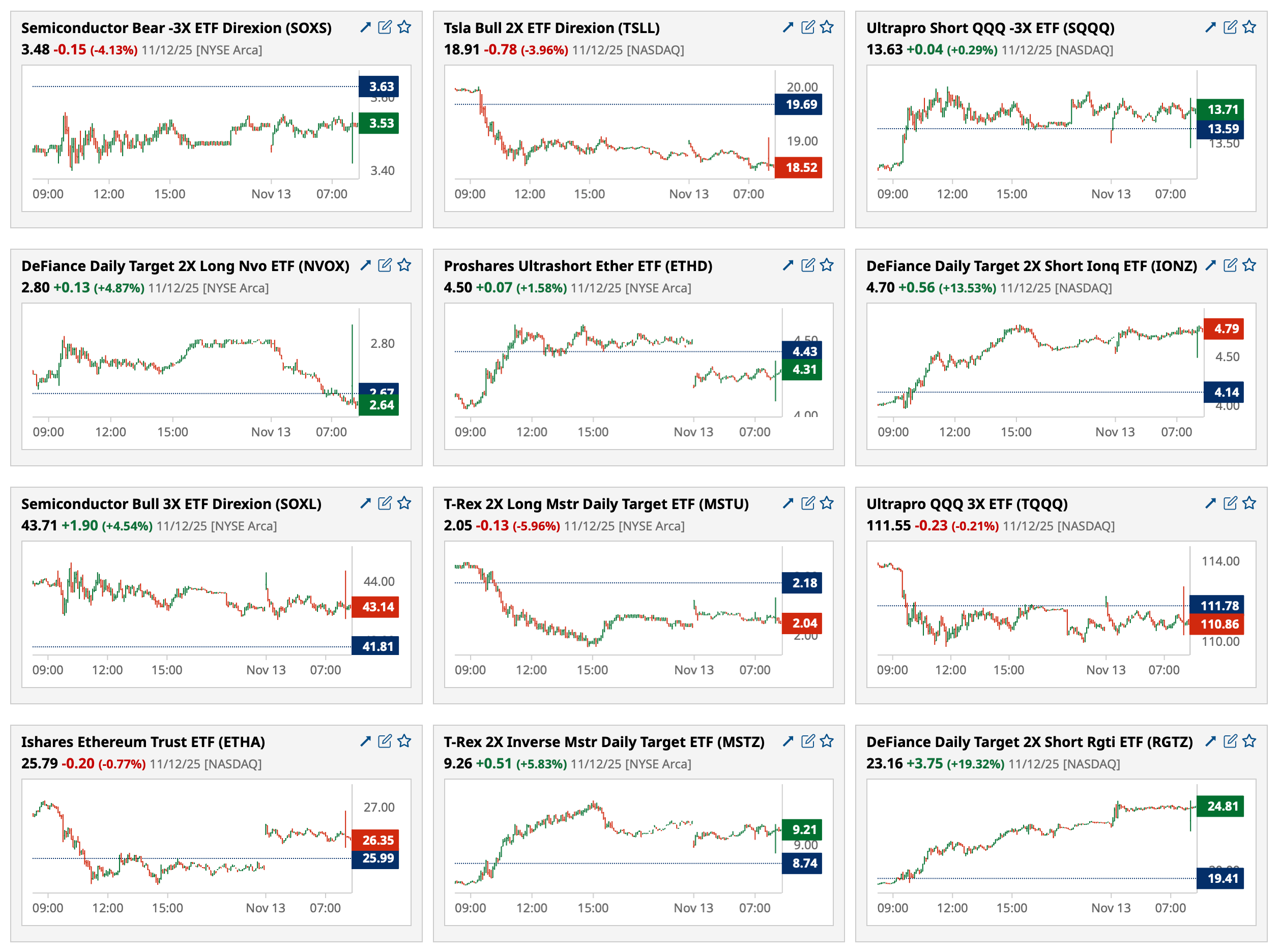

After-Hours Gainers and Losers

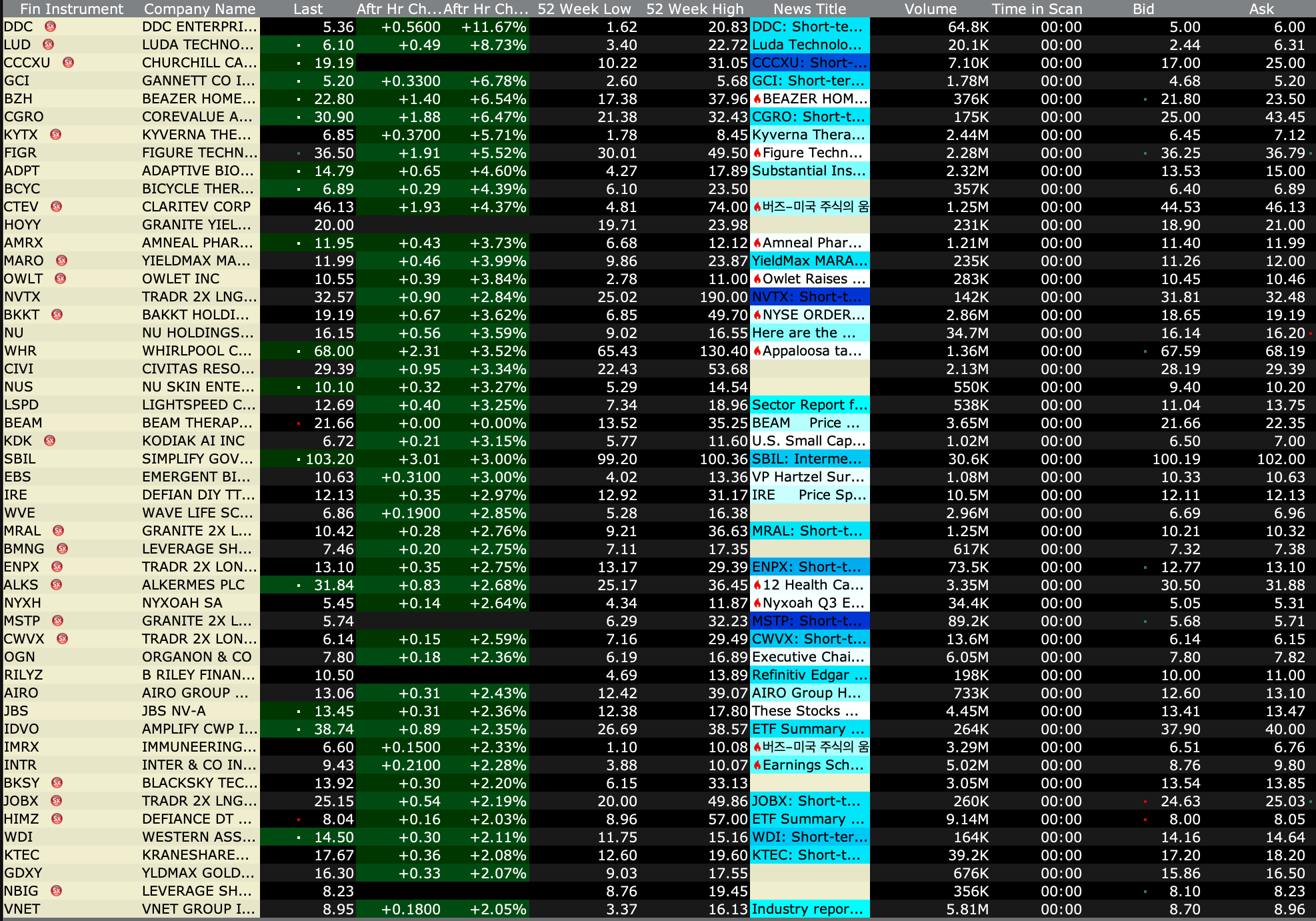

% Gainers

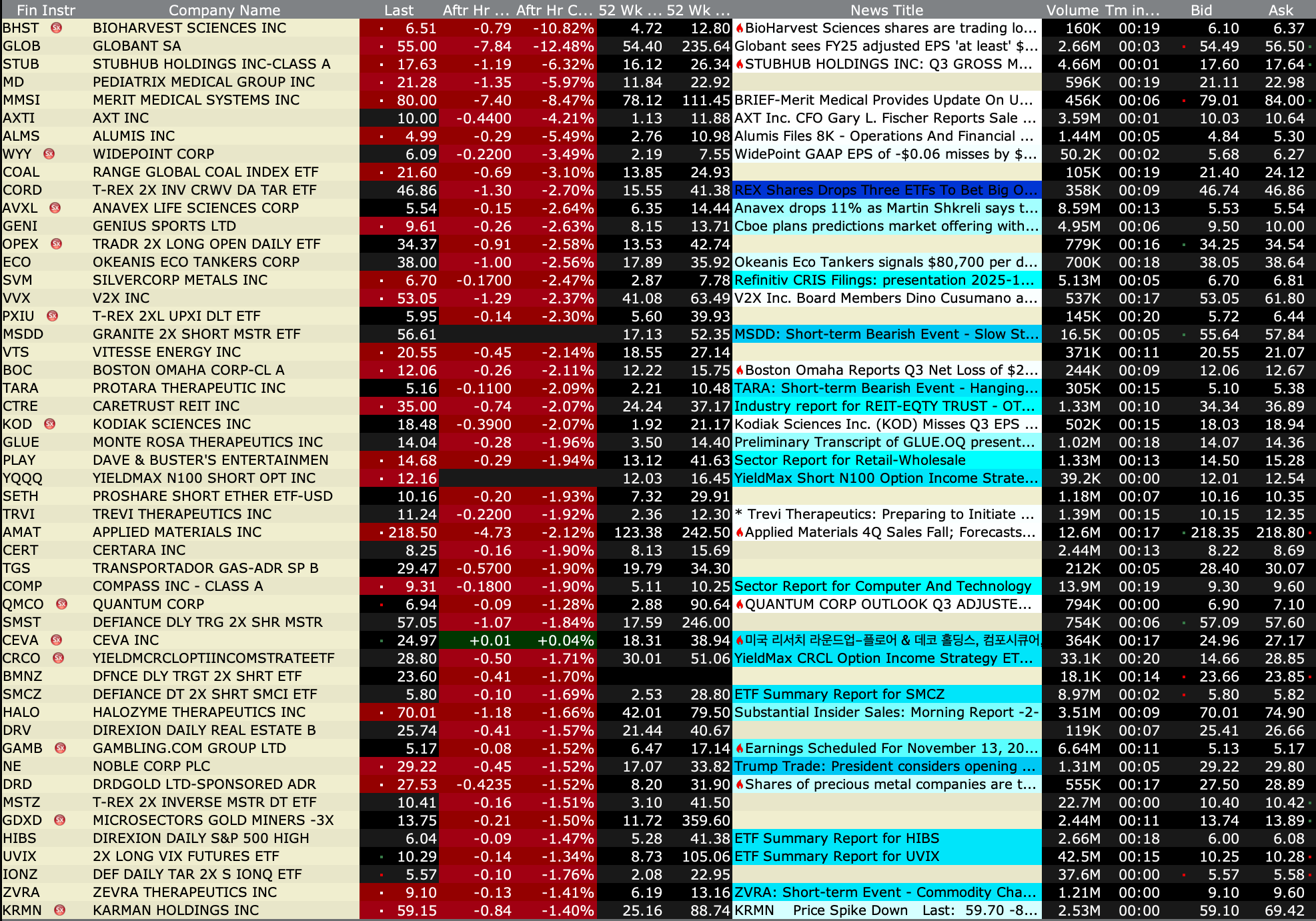

% Losers

BY Doug Kass · Nov 13, 2025, 4:55 PM EST

BY Doug Kass · Nov 13, 2025, 4:55 PM EST

BY Doug Kass · Nov 13, 2025, 4:50 PM EST

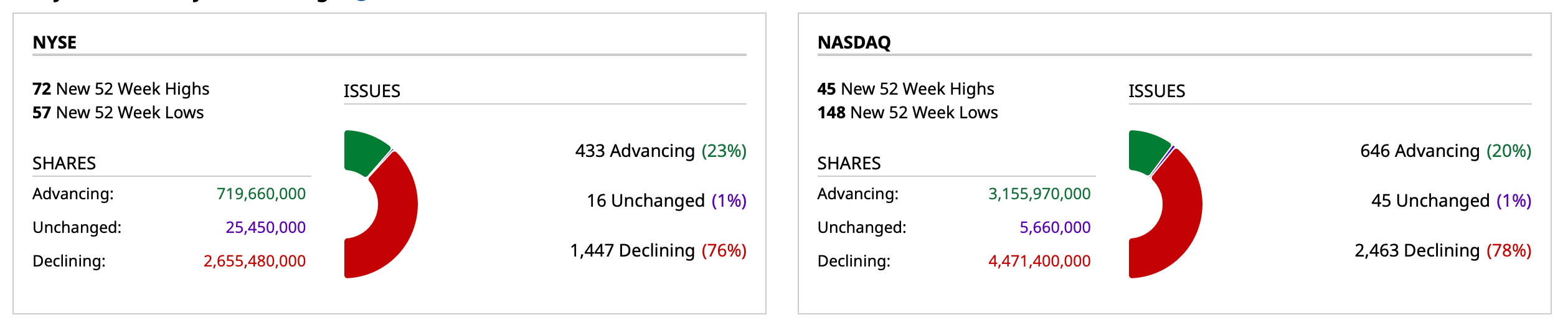

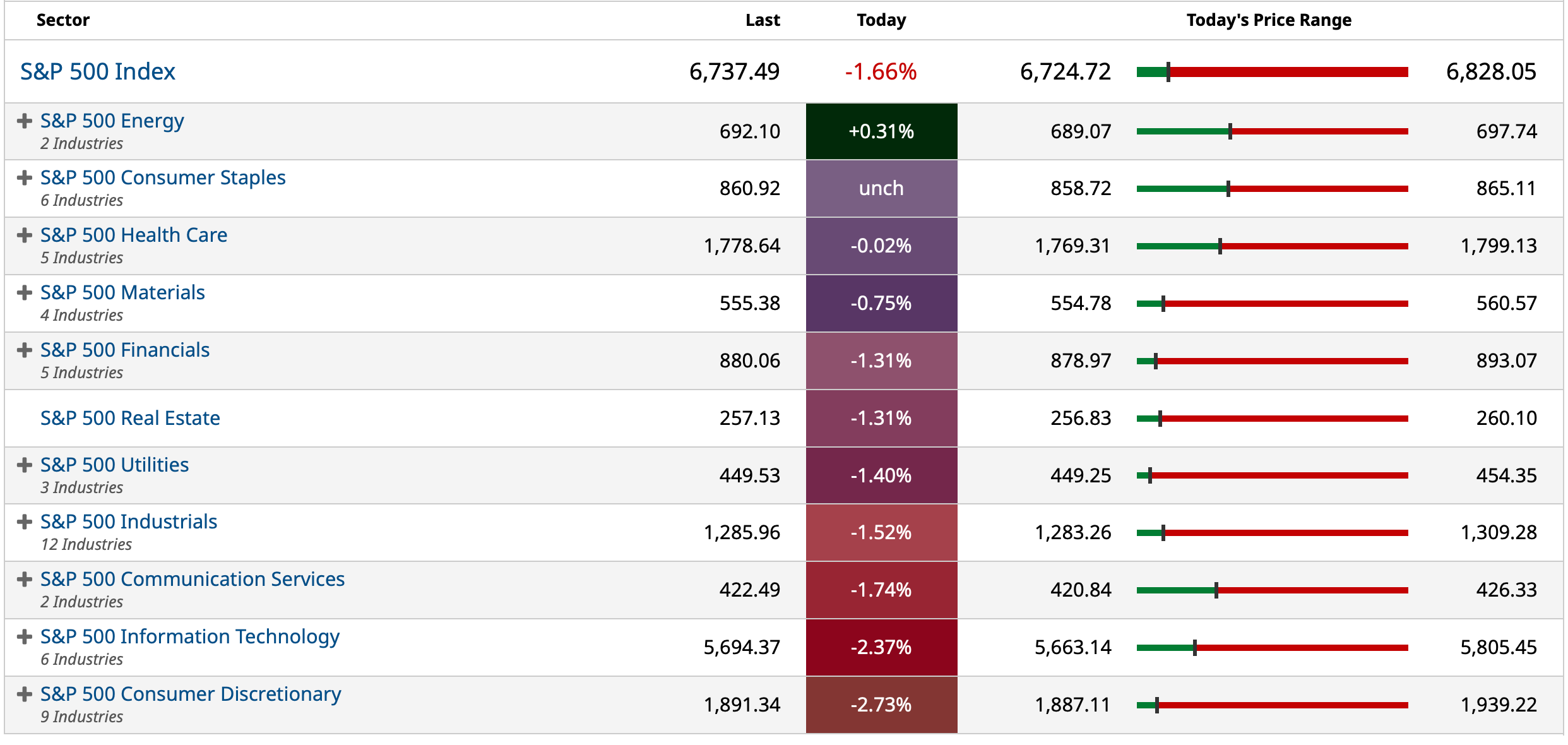

- NYSE volume 4% above its one-month average

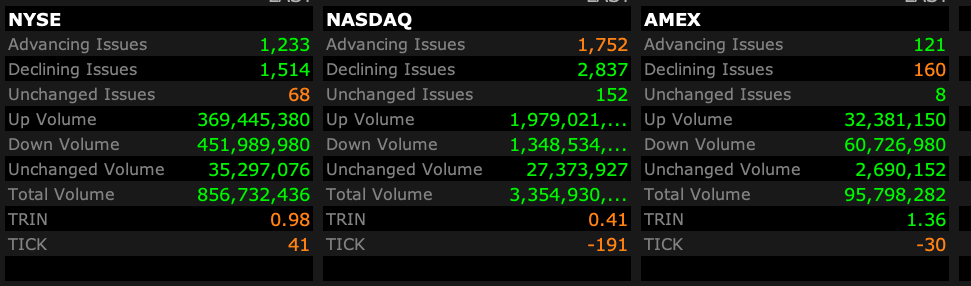

- NASDAQ volume 10% above its one-month average

- VIX index: up 14.96% to 20.13

BY Doug Kass · Nov 13, 2025, 4:42 PM EST

I have sold my trading long rental at $673.31 for a small gain.

BY Doug Kass · Nov 13, 2025, 4:11 PM EST

BY Doug Kass · Nov 13, 2025, 3:45 PM EST

I am traveling tomorrow so I won't be writing.

You will be in the very capable hands of Chris Versace.

BY Doug Kass · Nov 13, 2025, 3:10 PM EST

BY Doug Kass · Nov 13, 2025, 2:50 PM EST

With S&P cash -116 handles I am covering my speculative short basket for a profit.

From yesterday and late October:

Adding...

Position: Short Spec Basket

By Doug Kass Nov 12, 2025 11:13 AM EST

With the market rallying smartly off of the lows, I am adding to my speculative basket of high octane, high beta stocks.

Names withheld to protect the innocent traders!

Position: none.

By Doug Kass Oct 31, 2025 11:05 AM EDT

BY Doug Kass · Nov 13, 2025, 2:23 PM EST

From Charlie!

BY Doug Kass · Nov 13, 2025, 2:05 PM EST

I took a small trading long rental in (SPY) at $671.77 with S&P cash -115 handles.

I don't expect to hold this very long and I have a tight stop.

BY Doug Kass · Nov 13, 2025, 1:50 PM EST

BY Doug Kass · Nov 13, 2025, 1:45 PM EST

Recent long buys — PepsiCo (PEP) and Kimberly-Clark (KMB) — are doing yeoman's work.

BY Doug Kass · Nov 13, 2025, 12:55 PM EST

Now the talking heads on Fin TV don’t think we are going to go up into the end of the year!

And the pause in the “AI” space is healthy!

Just priceless, it really is always Groundhog’s Day!

BY Doug Kass · Nov 13, 2025, 12:50 PM EST

Back in the office.

Getting my sea legs back.

BY Doug Kass · Nov 13, 2025, 12:42 PM EST

BY Doug Kass · Nov 13, 2025, 11:45 AM EST

With S&P cash -77 handles, I have taken in my index shorts (common and calls):

* SPY $675.41

BY Doug Kass · Nov 13, 2025, 11:36 AM EST

From Peter Boockvar:

I don’t know when we’ll start getting government economic data again but I think we’ve all done a pretty good job of putting our fingers on the pulse of the economy, the good and the not so good whether from private data sources and/or from company earnings results and comments.

I was happy to hear yesterday that the White House is finally listening to me, not literally, where Scott Bessent said this week that there will be a reduction of tariffs on things we will never make in the US in scale, like coffee and bananas. Coffee prices fell 5.7% yesterday and are down another 1.3% today in response.

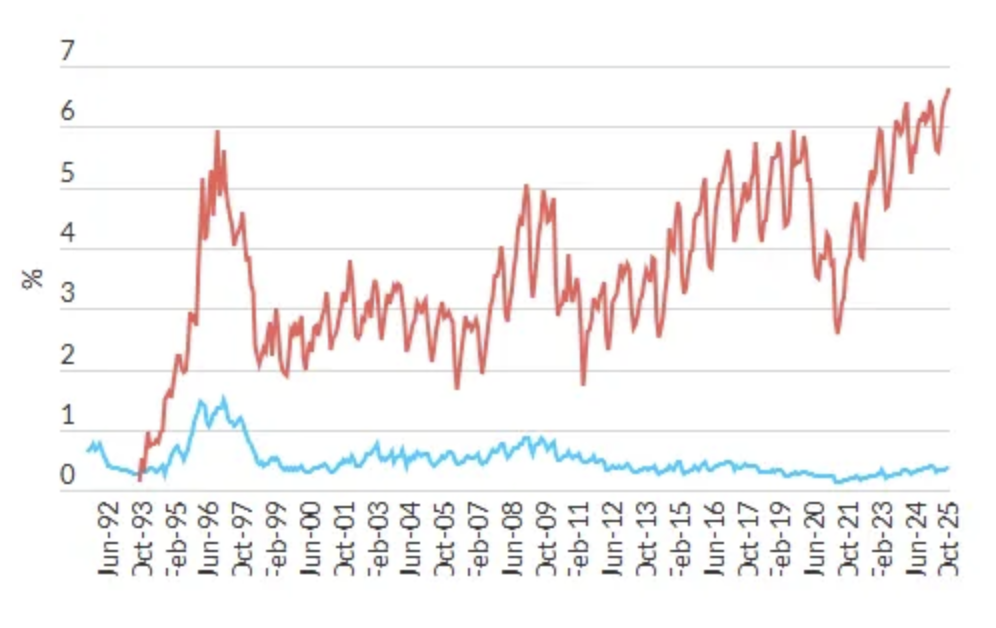

I mentioned yesterday the updated Fitch subprime delinquency number rising to the highest on record dating back to 1994. Here is the chart in red that also includes prime in blue which still remains very low, below .5%.

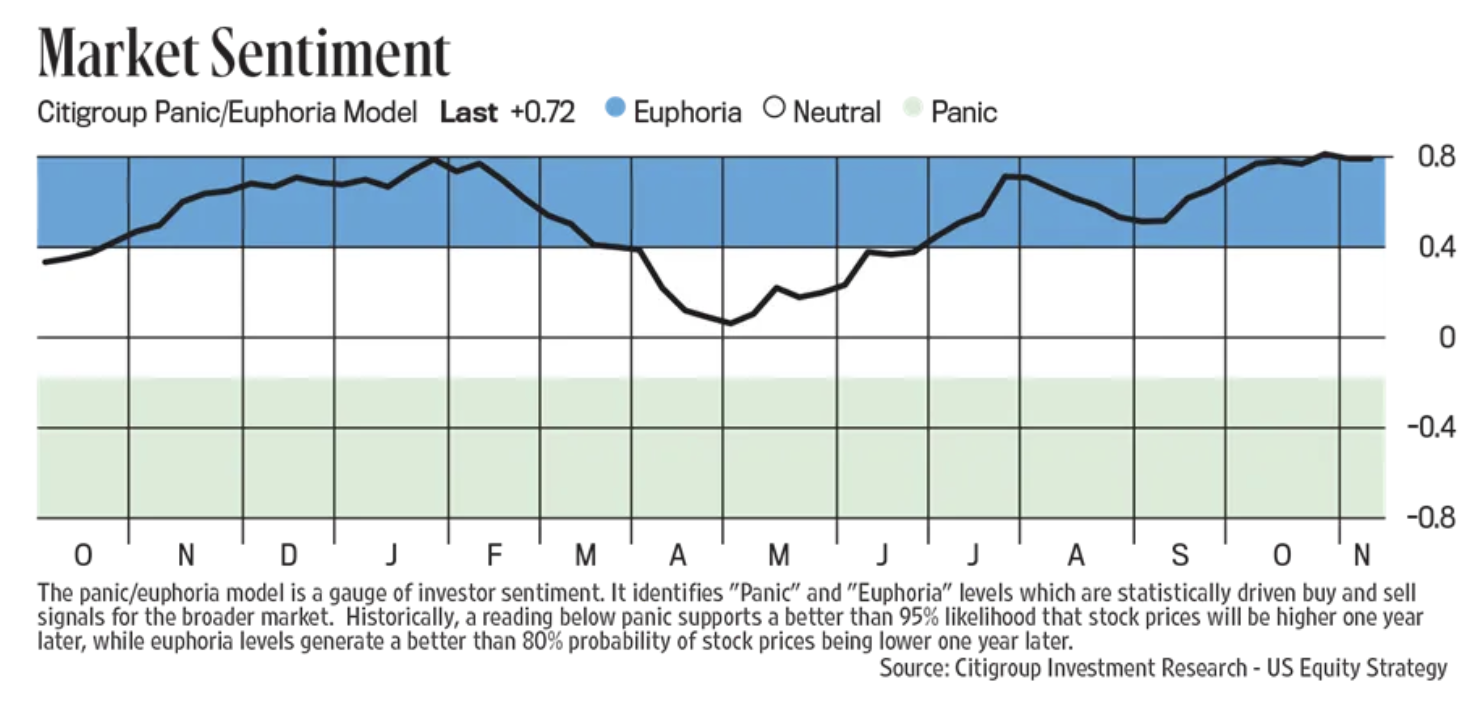

Updating stock market sentiment has the Bulls slipping to 56.6 from 59.3 in the weekly Investors Intelligence figure but which is still more than 40 pts above where the Bears are at just 15.1 vs 14.8 in the week before. The Citi Panic/Euphoria index is still very much in Euphoria land. The much more volatile read from AAII on the other hand saw Bulls fall by 6.4 pts to 31.6, the lowest in two months while Bears jumped by 12.8 pts to 49.1, the most in two months. It will get updated today but last week’s NAAIM Exposure Index at 90 was just off the upper end of the range around 100. The bottom line is that there is a certain level of ebullience out there, and has been, but with the retail investor instead showing more weekly bipolar behavior.

On Holding continues to crush it with their sneakers/apparel and the stock popped by 18%. Sales rose 25% y/o/y and 35% in constant currency and they said this, “This success is exceptional broad based, with significant growth contributions from across our portfolio in performance and lifestyle, footwear, and apparel, proving the global appeal of our brand.”

And who is their customer target? The upper income which we of course know is spending without concern. “What sets us apart is our premium position. Our vision is and will remain to be the most premium global sportswear brand.”

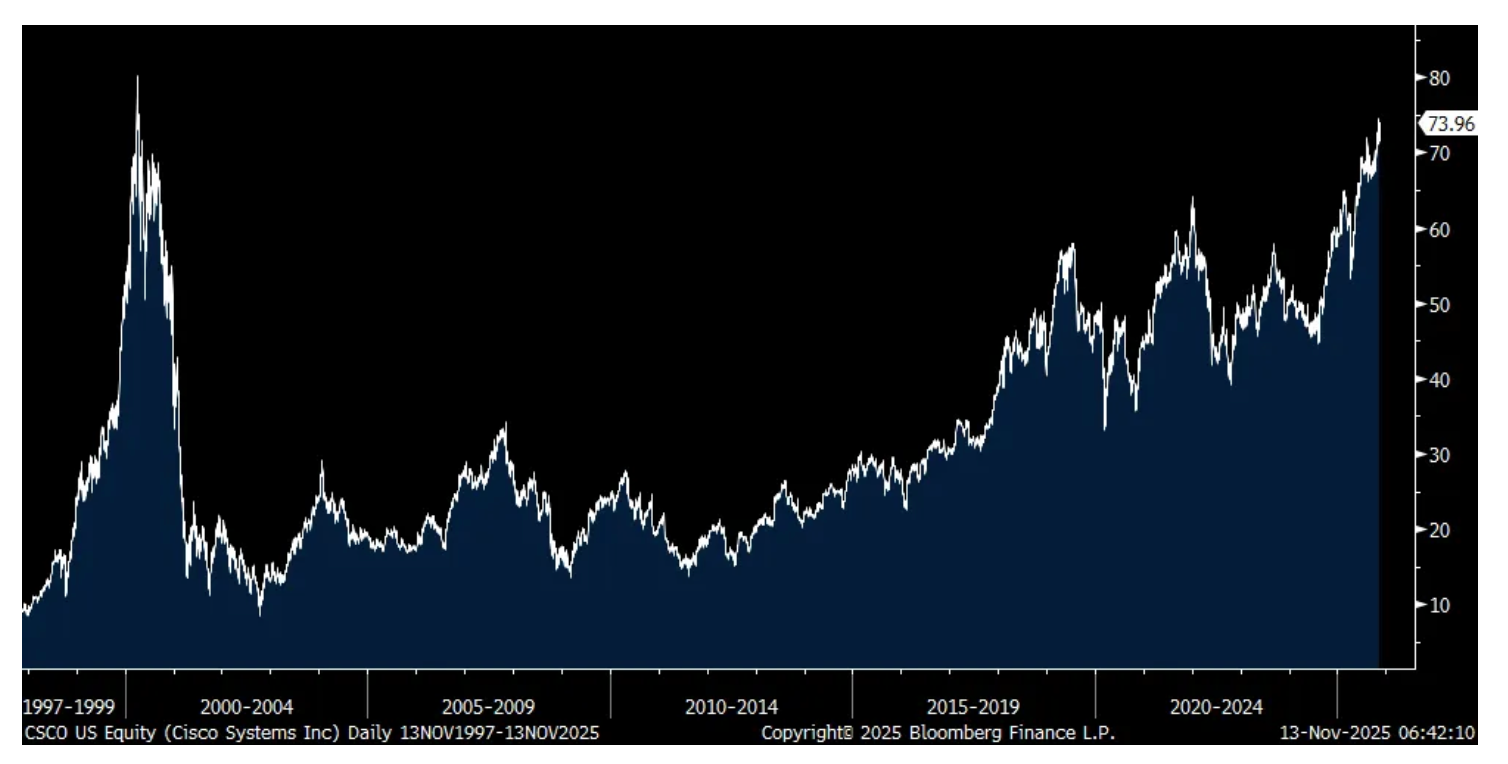

Cisco pre market is higher by 7% and FINALLY almost back to where it was 25 years ago at the peak ($80.06 close at the March 2000 top) in nominal terms as the backbone builder of the internet is still digesting that valuation bubble. They are now benefiting from its products selling into the GenAI data center buildout.

Sales rose 8% y/o/y “driven by robust demand for our AI infrastructure and campus networking solutions.”

“According to our 2025 Global AI Readiness Index, only one-third of organizations feel their IT infrastructure can accommodate the needs of their planned AI projects, which creates a massive opportunity for Cisco.”

“Networking product orders accelerated to high teens growth in Q1, marking the fifth consecutive quarter of double digit growth, driven by hyperscale infrastructure, enterprise routing, campus switching, wireless, industrial IoT, and servers.”

“To summarize, we are seeing strong demand across all customer markets and geographies, as well as expanded opportunities as our customers power their AI use cases from the data center to the edge.”

Cisco

I’ll go through the Disney earnings call soon (a stock we own) but they specifically said this on their ‘Experiences’ business which includes parks and cruises, with all eyes on what their consumers are spending:

“Operating income at our domestic parks and experiences increased compared to the prior year quarter due to growth at Disney Cruise Line attributable to an increase in passenger cruise days, partially offset by higher fleet expansion costs, both reflecting the launch of the Disney Treasure in the first quarter of the current year.”

I notice they didn’t mention growth in the domestic parks.

Also, “International parks and experiences’ operating results increased compared to the prior year quarter, primarily due to growth at Disneyland Paris. The increase at international parks and experiences was attributable to volume growth due to an increase in attendance, an increase in guest spending, and higher costs attributable to new guest offerings.”

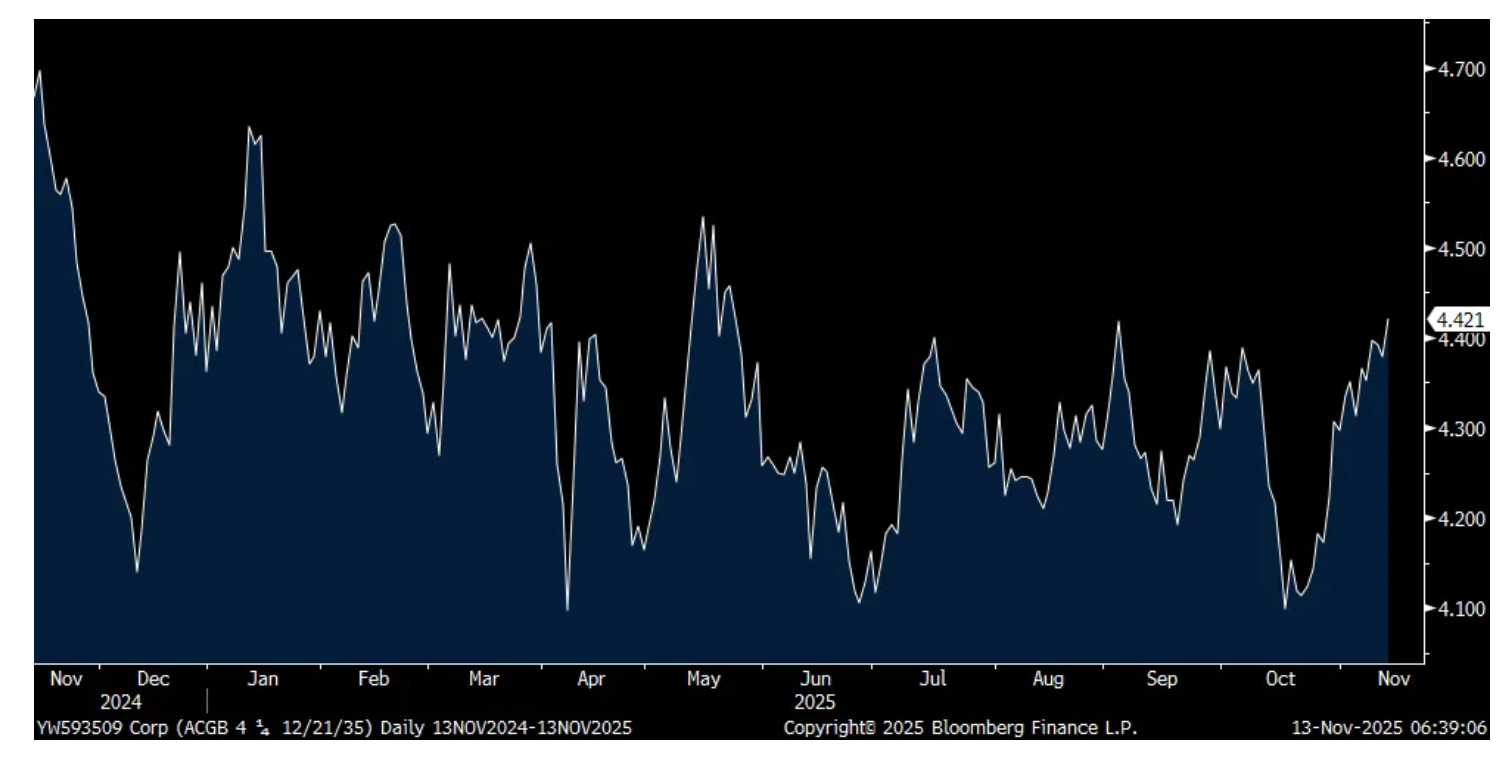

Overseas, the Australian 10 yr yield is rising to the highest level since late May at 4.42% after they saw a better than expected job gain in October and a drop in their unemployment rate to 4.3%. Reducing the odds of another rate cut has the 2 yr yield higher by 9 bps. Bond yields were higher too across Asia and we’re seeing a slight uptick in European yields and in US Treasuries.

Aussie 10 yr yield

BY Doug Kass · Nov 13, 2025, 11:35 AM EST

In Hebrew, the word "emes" means truth (emunah).

As most are now aware I try to be transparent and honest in my Diary.

You've got to ac-cent-tchu-ate the positive

E-lim-i-nate the negative

Latch on to the affirmative

Don't mess with Mr. In-Between

You've got to spread joy up to the maximum

Bring gloom down to the minimum

Have faith, or pandemonium

Liable to walk upon the scene

To illustrate his last remark

Jonah in the whale, Noah in the ark

What did they do

Just when everything looked so dark?

- Harold Arlen and Johnny Mercer, Ac-Cent-Tchu-Ate the Positive ACCENTUATE THE POSITIVE ~ Johnny Mercer & The Pied Pipers (1945)

Like many in the business media who "spread joy up to the maximum and bring gloom down to the minimum," I am not trying to accentuate the positives of my ideas and sweep the investment boners under the rug. I take full ownership for my losers and mistakes.

Here is a vivid example of the repeated B.S. on Fin TV that occurred yesterday - in which panelists use networks as platforms to improve their brands, sell a service and gather assets:

Rather, I am trying to explain (analysis) why, when and at what price I conduct my business of trading and investing. I attempt to provide a thoughtful and, at times, an outside of consensus view on companies, sectors and markets. (And I try to write in a readable and fun matter (often quoting musical lyrics or pop culture events)).

I have been terribly off-sided in my market view over the last 18 months. And I have admitted this, frequently.

That wrong view has resulted in my inability to take advantage of investment opportunity sets on the long side.

But, almost as important (perhaps!) is that despite such a problematic and ursine market outlook - reflected in mostly a net short exposure since early 2024 - my hedge fund has recorded profitable monthly returns in 21 of the last 22 months (with the only drawdown a modest -22 basis points in a four week period!). And, in November (month to date), my Partnership has been profitable - so that's 22/23 months of generating positive investment performance.

Am I pleased how wrong-sided I have been in view? Absolutely not. I take my mistakes in view (and this has been a whopper) seriously... perhaps, at times, too seriously.

But I press forward, awaiting the day when I capture the grand opportunity set on the short side.

So, how do I generate possible returns while being so stupid?

In a nutshell, I trade opportunistically and dispassionately. You see this daily in my (sometimes) frenetic trading activity (which I provide in real time - 24/7- to all subscribers).

Think of a cash register.

As Friedrich Nietzsche wrote, and Kelly Clarkson sang, "What Doesn’t Kill Us Makes Us Stronger."

BY Doug Kass · Nov 13, 2025, 10:45 AM EST

* More reasons why OpenAI's Sam Altman and Nvidia's Jensen Huang are positioning AI as an existential crisis and a battle between the U.S. and China...

* ...If they do not get the government’s help, the Chinese will eat all of our babies, frogs will drop from the sky and there will be a plague of locusts

* Meanwhile, down on the AI campus, it seems so circular (again, that word!) when Softbank has to sell their Nvidia stock to come up with cash to fund their investment in Open AI, who will then buy NVDA chips.

* It just never ends in this space!

Coincidentally per yesterday's "More Tales from Nvidia - More Coreweave Double Speak (Issue #146!) Doug's Daily Diary - TheStreet Pro = the nuclear plant shortfall is discussed in a Morgan Stanley report. The data point I came up with was we would need to come up with 325,000–580,000 gigawatt-hours per year and therefore 40-70 new nuclear reactors to power the data centers that have been announced in these circular deals.

Morgan Stanley is coming up with 44 nukes for the 2025-2028 period alone. To put that in perspective, the U.S. has only added two new reactors in the last 30 years. Building even one new reactor takes 10 + years. Using other forms of power is feasible to some degree, but is even less efficient (ergo more expensive to run and therefore even more dis-economic), and there are still all sorts of other issues at the grid level and we probably are short capacity to build this stuff, too. In third grade language, not happening. A lot of these deals are vaporware. This is one more reason why OpenAI's Sammy Altman and Jensen Huang and the Nvidia (NVDA) team are positioning AI as an existential crisis and a battle between the U.S. and China, where if they do not get the government’s help, the Chinese will eat all of our babies, frogs will drop from the sky and there will be a plague of locusts. These guys need the bubble to persist. This whole thing is an elegant and sophisticated game of tulips. The math does not scribble out, not even close.

Like many previous bubbles, everyone investing in the space -- including the private investors (ergo those funding Open AI) -- are just betting that the next in line will pay a higher price. There is no set of underlying economics or assets to hang their hat on at these valuations. Open AI needs the bubble to stay inflated because that is the only reason people will keep funding their tulips with giant sums of money. NVDA needs the bubble to stay inflated for the same reason, because money flowing into the space and the mania keeps people throwing caution to the wind and buying more chips for dis-economic data centers, which are funded by the tulip buyers as well. It has psychological ramifications for our government with regard to how they view the sector too and what policy actions they will take. The survivability of the space is predicated on a mania and tulip flipping, not economics. P.S. it also seems circular when Softbank has to sell their NVDA stock to come up with cash to fund their investment in Open AI, who will then buy NVDA chips. It never ends in this space!

The Morgan Stanley report is further discussed in "A Giant Problem Emerges For The AI Trade: A Power Shortfall Of 44 Nuclear Power Plants By 2028."

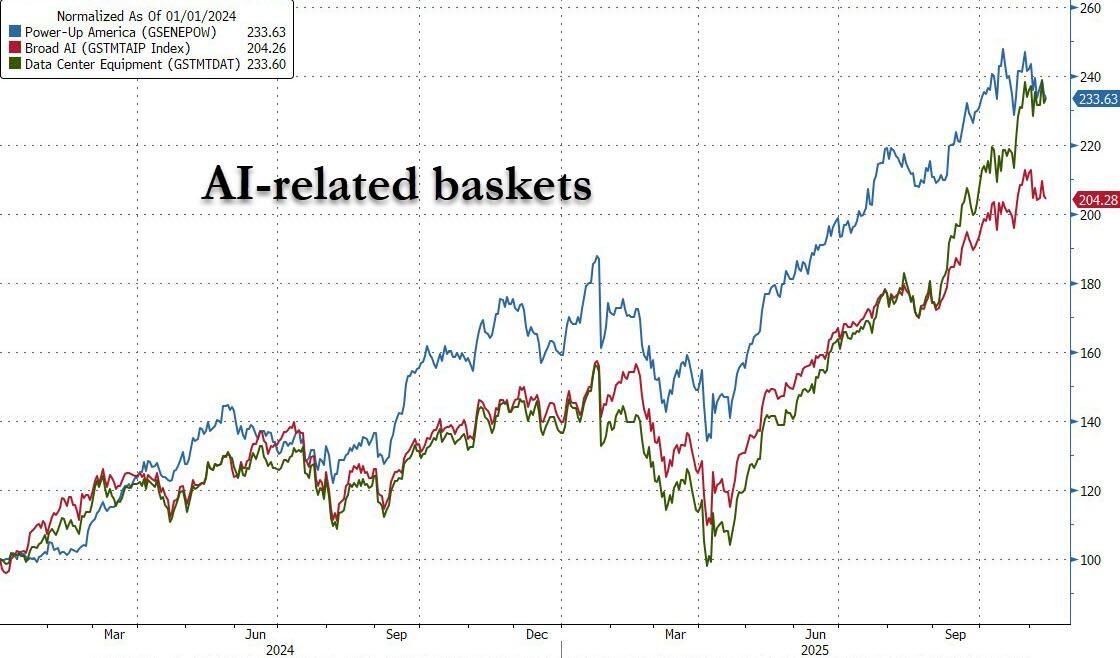

For much of the past 18 months we have been banging the table on what we said would be the Next AI Trade (which we first discussed in April 2024) pitching the "picks and shovels" angle of the AI revolution, namely going long the "Power-Up America" basket - i.e., companies that produce and support the massive energy backbone that will be needed to energize the hundreds of new data centers popping up across the country (and which in some cases are now dark because they don't have access to energy) predicting that energy would materially outperform the pure AI/data center trade. That's precisely what has happened as the following chart breaking down the AI trade into its three core components - broad AI, data center equipment, and our preferred trade, Power Up America (or energize the grid) - shows. The blue line has doubled since we first discussed its merits in April '24.

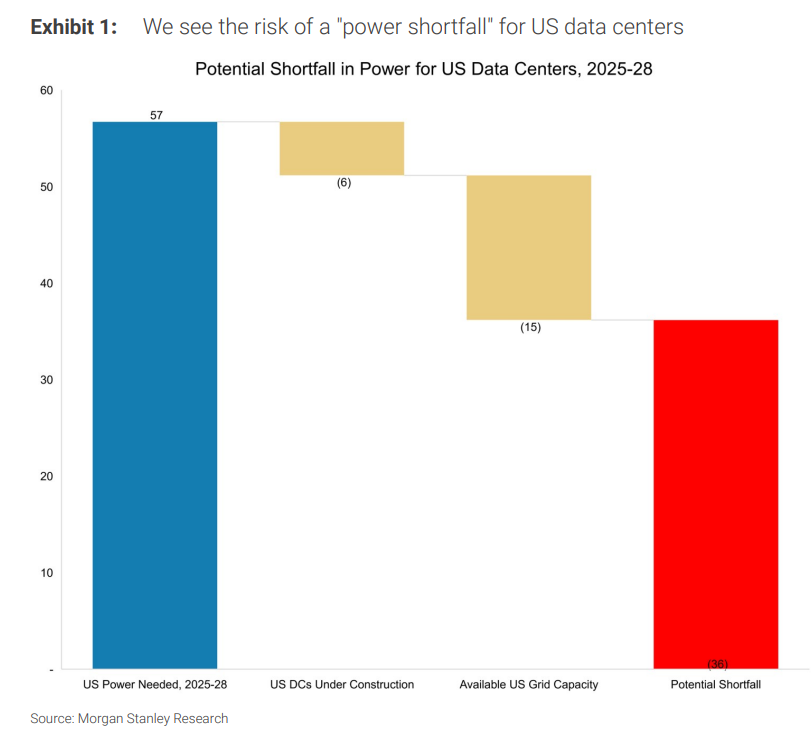

Our conviction in this trade was only reinforced by an analysis from Morgan Stanley last December, which found that for the 2025-28 period, "we project ~57 gigawatts (GW) of U.S. data center power demand, and we quantify available power capacity to serve this demand as: near-term grid access of ~12-15 GW, plus ~6 GW of data centers under construction, resulting in a ~36 GW shortfall of US power access for data centers in 2025-28." Indicatively 36GW is sufficient to power ~27 million homes. Instead it will be going to power chatbots.

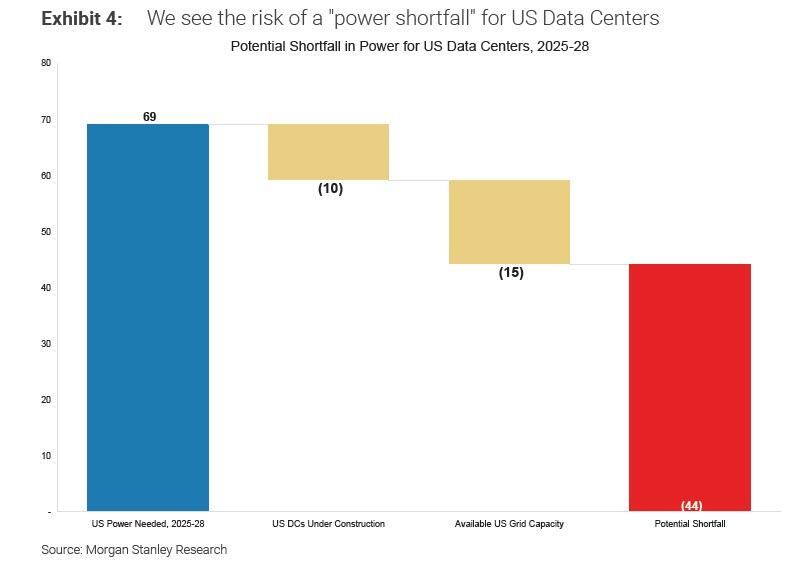

Fast forward one year since Morgan Stanley published its original estimate when this morning Morgan Stanley's strategist Stephen Byrd published his follow up report, "Powering AI: Bitcoin Conversion: Business Models, a US Power Shortage, and the Big Picture" (available to pro subs), in which he reassessed US power needs through 2028.

It will probably not come as a surprise to anyone, that his latest estimate is materially higher, rising to a staggering 44GW...

... or roughly the output equivalent of 44 nuclear power plants!

No wonder the Trump admin recently announced that it was prepared to lend hundreds of billions from the Energy Department's Loan Programs Office almost exclusively to nuclear power plants to kick start this process.

While the full Morgan Stanley note is a must read for those who have an interest in the AI trade, and certainly in the details of the "Next AI trade," and includes a detailed analysis on Bitcoin-to-Data center conversions, the non-linear rate of AI improvement and the continued upward growth in compute demand (we urge all pro subscribers to read it), what we focus on in this post is the bank's revised estimate of power shortfall facing U.S. data center developers (we will discuss the financial implications in a subsequent post, suffice to note that 1GW in data center capacity costs roughly $50 billion - 60 billion in total capex spend).

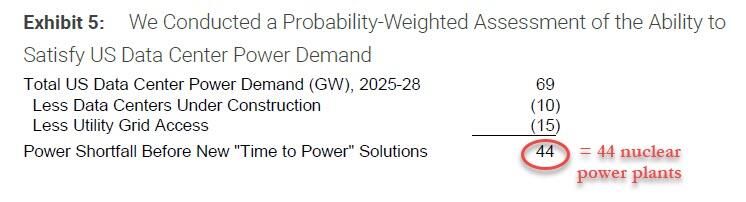

For its revised projection, Morgan Stanley conducted a probability-weighted assessment of the ability to satisfy U.S. data center power demand, and found that with 69GW in total data center power demand from today until 2028, some 10GW will be satisfied with Data Centers under construction, and another 15GW through Utility Grid Access.

That leaves a 44GW power shortfall, or a number so staggering any hopes of the AI revolution growing into Wall Street's optimistic projections implodes instantly... unless of course the government steps in to foot the bill (we will have more to say on that in a subsequent post).

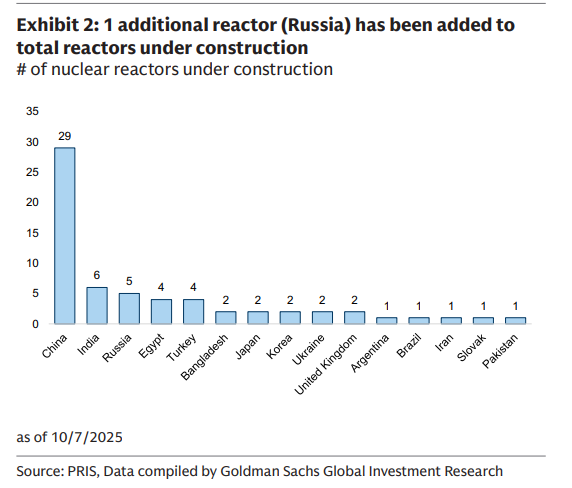

Clearly, with precisely 0 nuclear reactors being built in the U.S. (vs. 29 for China)...

... and even if they were, the construction would take a decade if not longer - this is a massive problem, as it means that absent some miracles, the U.S. simply can not grow its grid to support the massive data center power drain that is looming... and that generously assumes the trillions of dollars needed to build said data centers were readily available. They are not, which is why Sam Altman has been begging U.S. taxpayers to bail him out (again, we will have more to say on this shortly).

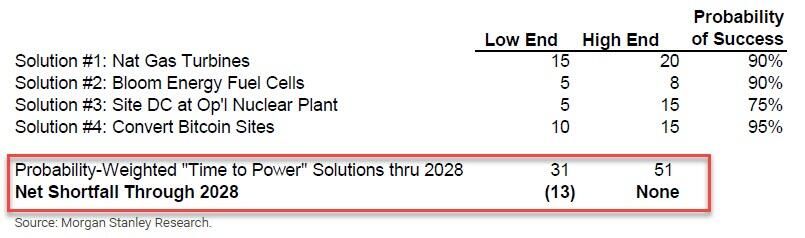

So what then? To provide some possible solutions, Morgan Stanley has focused on so called "time to power" solutions which do not rely on the typical grid interconnection process, that have the potential to eliminate the shortfall.

Assuming these Time to Power solutions are implemented, Morgan Stanley concludes that through 2028, we could experience a power shortfall totaling as much as 20%, which equates to a ~13 gigawatt (GW) shortfall, better than the 44GW base case above but still a huge gap of roughly 13 nuclear power plant. That said, an even more rapid increase in "time to power" solutions have the potential to eliminate this shortfall (and would certainly cost an arm and a leg).

Stephen Byrd details his proposed solutions as follows:

Of the above, Morgan Stanley believes that Bitcoin miners/sites offer AI players the fastest time to power with the lowest execution risk, and believe this will increasingly be valued/ recognized. The bank also continues to believe Bloom Energy (BE) can be a highly reliable, "time to power" solution that drives rapid volume growth. Beyond these two categories of solutions (fuel cells and Bitcoin conversions), we would expect to see "all of the above" in terms of "time to power" transactions — involving merchant power companies, turbine manufacturers, energy companies and others.

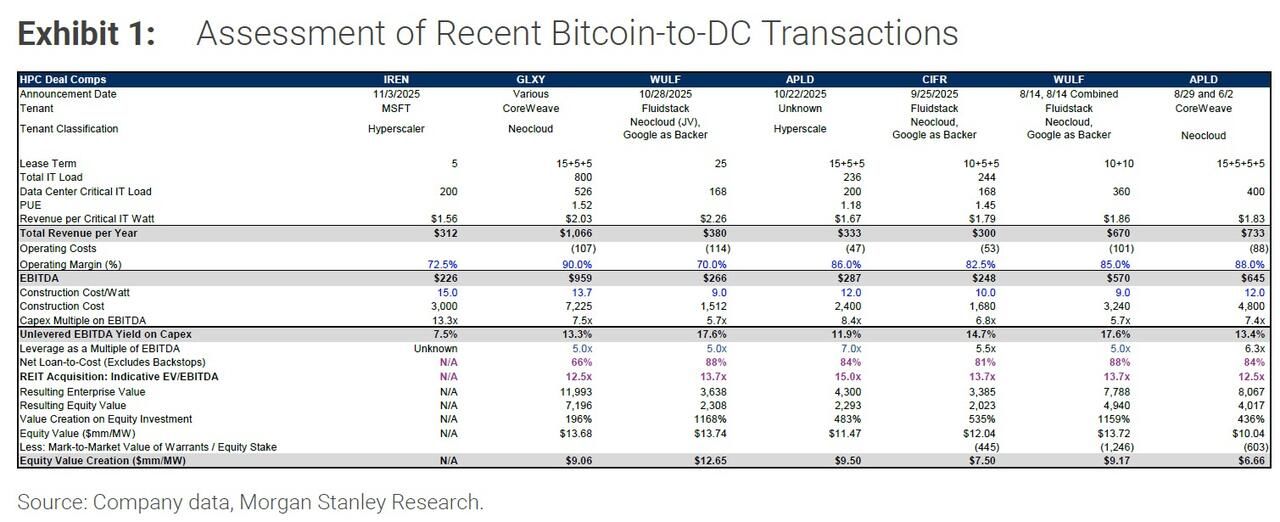

For those eager to jump down the rabbit hole with Morgan Stanley and contemplate - or trade - the conversion of bitcoin miners into data centers, the bank has an extended discussion of this particular opportunity, from which we excerpt below:

Continued trend of repurposing Bitcoin mining centers to host HPC data centers, with 2 different business models: (A) the "new neocloud" and (B) the "REIT endgame."

Under the "new neocloud" model, most notably exhibited by IREN, the Bitcoin miner purchases GPUs/TPUs, builds the entire data center and leases the facility to hyperscalers and other customers - potentially under leases with relatively short durations (such as the 5-year lease signed by IREN with Microsoft (MSFT) ). Under the "REIT endgame" model, the Bitcoin miner builds the "powered shell" (typically, everything but the chips + servers) and signs a lease with a neocloud and/ or hyperscaler, typically under fairly long-term leases (such as the APLD 15-year lease with an unnamed hyperscaler). We see value creation potential with respect to both approaches. The following chart provides an overview of the Bitcoin-to-DC conversion transactions, including the "colocation" portion of the "new neocloud" transaction recently entered into between IREN and Microsoft:

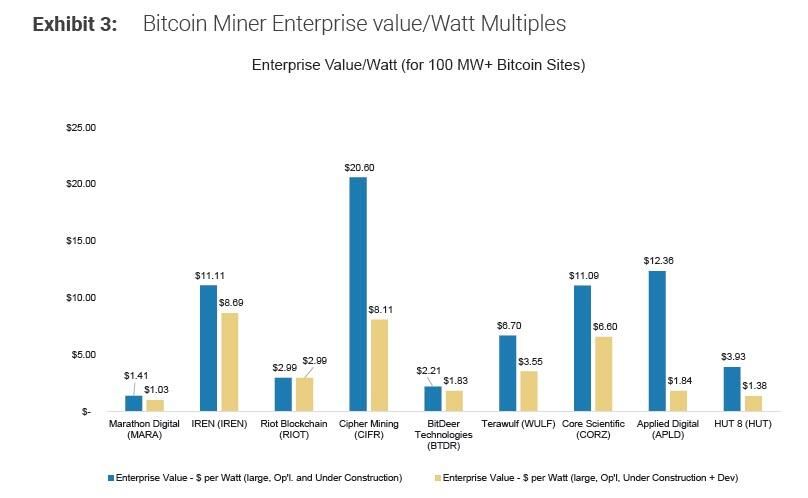

Finally, for those seeking relative Bitcoin to DC conversion metrics, the following table shows the latest Enterprise Value/ watt multiples for Bitcoin stocks - it includes all large sites (>100 MW) with firm grid access. Needless to say, the lower the column, the cheaper the potential conversion opportunity.

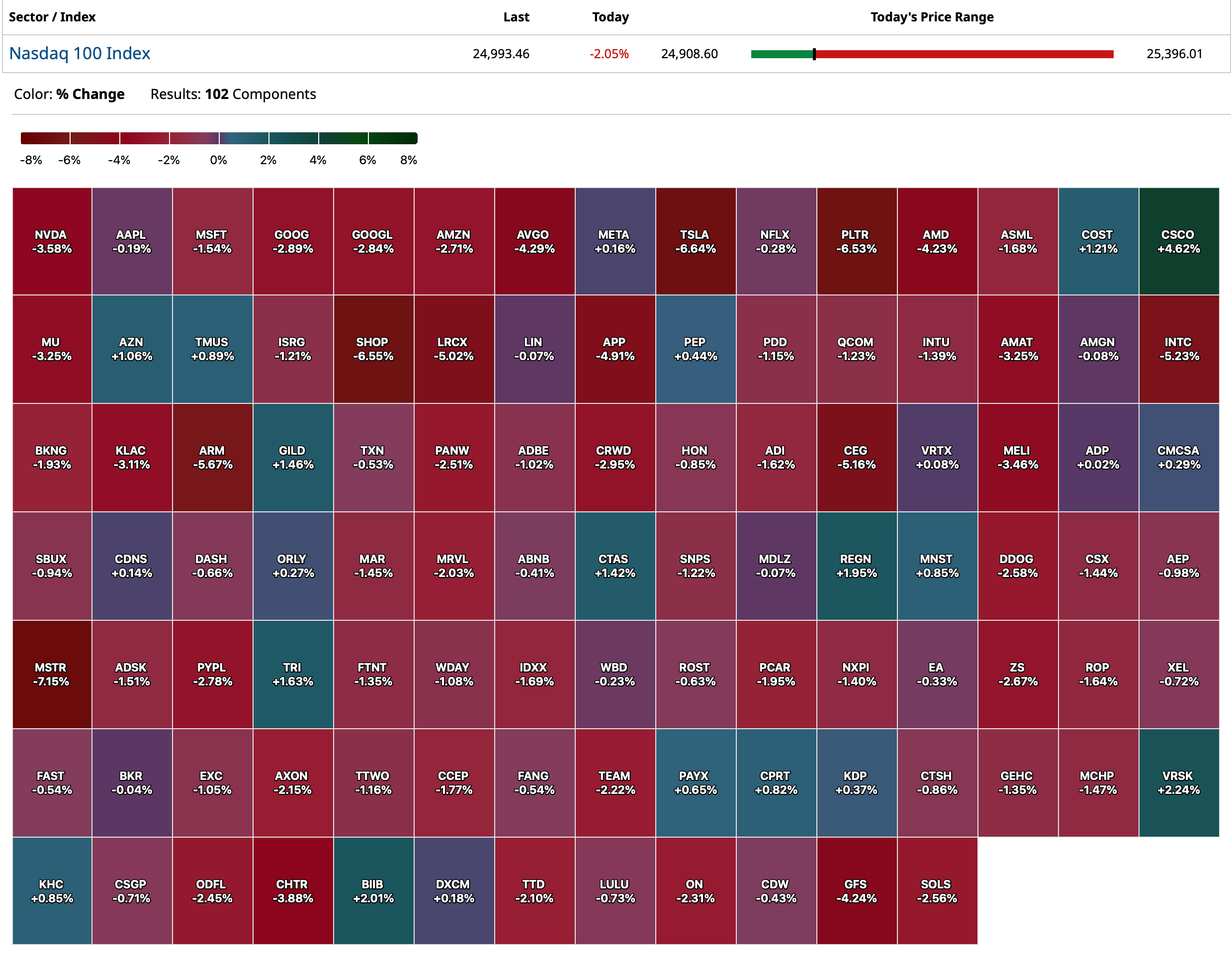

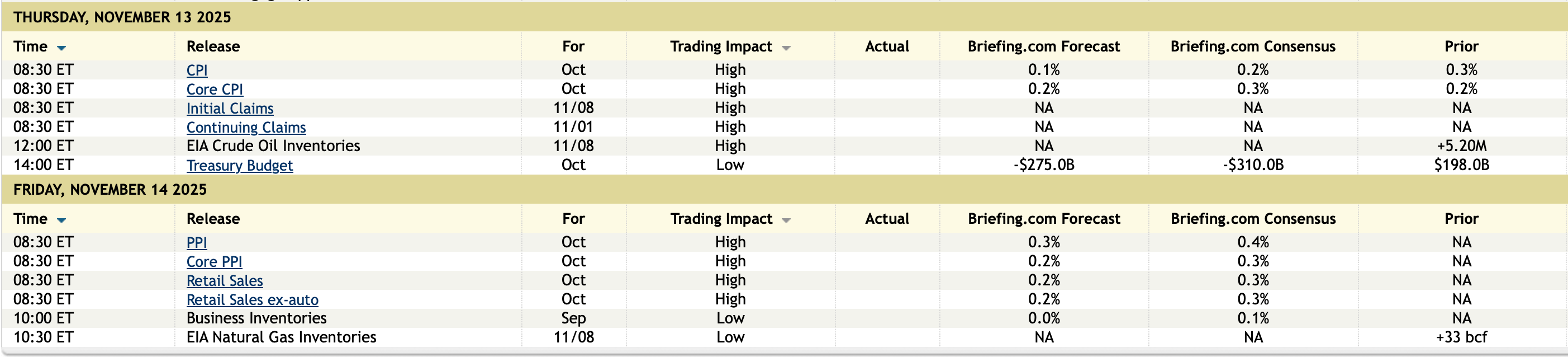

BY Doug Kass · Nov 13, 2025, 10:00 AM EST

BY Doug Kass · Nov 13, 2025, 9:30 AM EST

-MRSN +209% (to be acquired by Day One for $25.00/shr in upfront cash plus up to $30.25/shr in CVRs)

-MGRX +23% (partners with Eli Lilly and Novo Nordisk to Deliver Affordable Access to Zepbound and Wegovy for Obesity Management for Medicare patients with obesity, effective mid-0)

-FLY +22% (announces Acceptance of Biologics License Application by U.S. FDA for ONS-5010 as a Treatment for Wet AMD)

-OTLK +22% (announces Acceptance of Biologics License Application by U.S. FDA for ONS-5010 as a Treatment for Wet AMD)

-ONDS +16% (earnings, guidance)

-DDS +10% (earnings)

-DGII +8.7% (earnings, guidance)

-CSIQ +7.2% (earnings, guidance)

-CSCO +6.2% (earnings, guidance)

-NKE +2.6% (Wells Fargo Raised NKE to Overweight from Equal Weight, price target: $75)

-TKO +2.2% (confirms First-of-Its-Kind Sports Partnership with Polymarket; Platform will become the Official and Exclusive Prediction Market Partner of UFC and Zuffa Boxing)

-KRRO -78% (earnings; KRRO-110 did not reach projected levels of functional protein following a single administration; Pivoting to GalNAc delivery for patients with AATD; development candidate nomination expected in the first half of 2026; Cuts staff and takes Q4 impairment charge)

-ARDT -32% (earnings, guidance)

-IBTA -20% (earnings, guidance)

-BTDR -19% (files to sell registered direct offering of Class A Ordinary Shares of indeterminate amount)

-DAWN -19% (acquiring MRSN for $25.00/shr in upfront cash plus up to $30.25/shr in CVRs)

-PSFE -16% (earnings, guidance)

-CTEV -11% (prices stock for selling holders of 1.5M shares at $51.50/shr)

-BETR -6.5% (earnings, guidance)

-KDK -6.4% (earnings)

-DIS -5.6% (earnings, guidance)

-NFE -5.2% (delays quarterly report)

-SNDK -5.0% (sector weakness)

-FLUT -4.0% (earnings, guidance)

-BOF -3.5% (announces $2.5M Institutional Investment Pricing of 1M Shares to be purchased by Bard Associates)

-GMRE -2.5% (announces Proposed Public Offering of Series B Preferred Stock of indeterminate amount)

-WDC -2.1% (sector weakness)

BY Doug Kass · Nov 13, 2025, 9:26 AM EST

BY Doug Kass · Nov 13, 2025, 9:05 AM EST

BY Doug Kass · Nov 13, 2025, 8:52 AM EST

11:00AM: Treasury announces a 6-week and a 3 and 6 month Bill Auction

11:00AM: TIPS and bond announcement

11:30AM: Treasury hosts a $110B 4 and a $95B 8 Week Bill Auction

1:00PM: Treasury hosts a $25B 30-Year Bond Auction; TBD: Quarterly Mortgage Delinquencies (Q3) (tentative)

8:00AM: Federal Bank of San Francisco President Mary Daly (Non-voter) addresses Irish think tank on 'central banking, policy implementation and balance sheets', Dublin

12:15PM: Fed Bank of St. Louis President Musalem (Voter) speaks on the U.S. economy and monetary policy before the Evansville Regional Economic Partnership 2025 Economic Impact and Policy Forum, Evansville, IN (In-person and virtual options. No text. No media availability; Event information

12:20PM: Fed Bank of Cleveland President Hammack (Non-Voter) participates in fireside chat before the Economic Club of Pittsburgh, Pittsburgh, PA (No text. Q&A expected. Livestream TBD)

BY Doug Kass · Nov 13, 2025, 8:41 AM EST

BY Doug Kass · Nov 13, 2025, 7:45 AM EST

BY Doug Kass · Nov 13, 2025, 7:30 AM EST

For the reasons previously mentioned (and despite last night's positive response) I would continue to avoid the shares of Disney (DIS) .

Disney’s Q4 FY25 Earnings Results Webcast - The Walt Disney Company

From late September, 2025:

* A boycott of Disney+ and Hulu streaming is now joining the bonafide threats of AI and absurdly high theme park admission prices

* Look for reduced EPS expectations at Disney...and a likely lower share price

Besides ridiculously high theme park admission and lodging costs etc. — which hits the increasingly vulnerable middle class (a deteriorating jobs market nationally and sticky inflation relative to incomes) — Disney (DIS) now faces another challenge.

Regardless of one's political views, those that argue against the Jimmy Kimmel cancellation have mounted an effort to cancel Disney+ and Hulu streaming memberships and, even, to cancel Disney theme park vacations.

I expect further pressure on Disney's shares in the time ahead and I would not be surprised (in a market correction) that the company's share price tumbles and creates an excellent entry point on the buy side.

But, the time to buy is not yet likely at hand. I would be patient on price with this popular and heavily institutionalized name.

I wrote this column about three weeks ago:

It's a world of laughter,

a world of tears

It's a world of hopes

and a world of fears

There's so much that we share

that it's time we're aware

It's a small world after all

It's a small world after all

It's a small world after all

It's a small world after all

It's a small, small world

- It's A Small World It's A Small World

This New York Times article on Disney underscores my concern about this popular but disappointing company and stock: Opinion | Disney World Is the Happiest Place on Earth, if You Can Afford It.

For some time I have viewed too steady and rapid escalation of theme park admission prices as a threat to consensus earnings per share expectations.

I have found that demand elasticity (read: weakening demand) would follow those admission price hikes over the fullness of time.

I still do.

This keeps me from buying this seemingly cheap stock.

By Doug Kass Sep 2, 2025 10:20 AM EDT

I wrote this article in August:

I recently purchased a very small starter position in Disney (DIS).

In a different era, I would be more aggressive.

But we live in the new (altered) world of artificial intelligence and I am increasingly concerned that AI could disintermediate both Disney's movie and its theme park business. (The latter — admission prices — being priced sky high into a likely consumer slowdown. Come to think of it, the same can be said of Disney's movie admission prices!)

I don't think many are thinking in these terms.

By Doug Kass Aug 11, 2025 1:45 PM EDT

Position: None

By Doug KassSep 22, 2025 7:00 AM EDT

BY Doug Kass · Nov 13, 2025, 7:12 AM EST

BY Doug Kass · Nov 13, 2025, 7:00 AM EST

* Read below how technicians get all excited about an all-time high in a meaningless index (DJIA)

Bonus — Here are some great links:

Greatest Bit of Annual Highs Is in December

BY Doug Kass · Nov 13, 2025, 6:45 AM EST

BY Doug Kass · Nov 13, 2025, 6:35 AM EST

BY Doug Kass · Nov 13, 2025, 6:25 AM EST

BY Doug Kass · Nov 13, 2025, 6:15 AM EST

The S&P Short Range Oscillator is back into overbought — at 1.33% vs. 0.16%.

BY Doug Kass · Nov 13, 2025, 6:05 AM EST

I have a business breakfast and then a board meeting this morning.

I will be out from 9:30 AM to about noon.

BY Doug Kass · Nov 13, 2025, 5:55 AM EST

Up early again this morning, 'cause of Ollie (the doxie)....

I shorted more indices last night ( (SPY) common $684.21), with futures +8 handles (around 830 PM) — now S&P futures are -12 (425 AM).

Randy

Any news after hours causing the drop (besides usual thinner after hours trading)?

Dougie Kass

back higher, +8 handles and i am shorting spy

BY Doug Kass · Nov 13, 2025, 5:45 AM EST