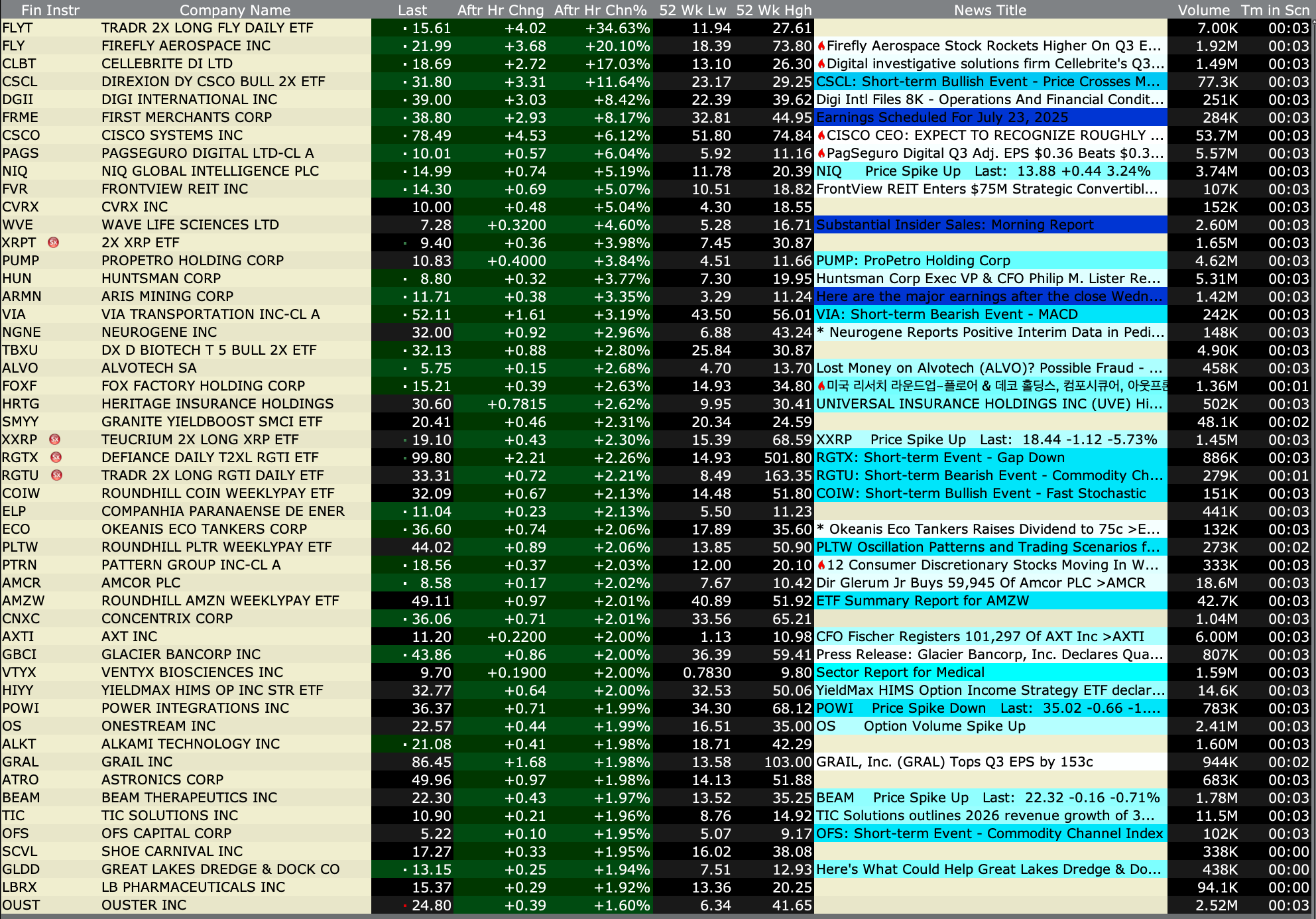

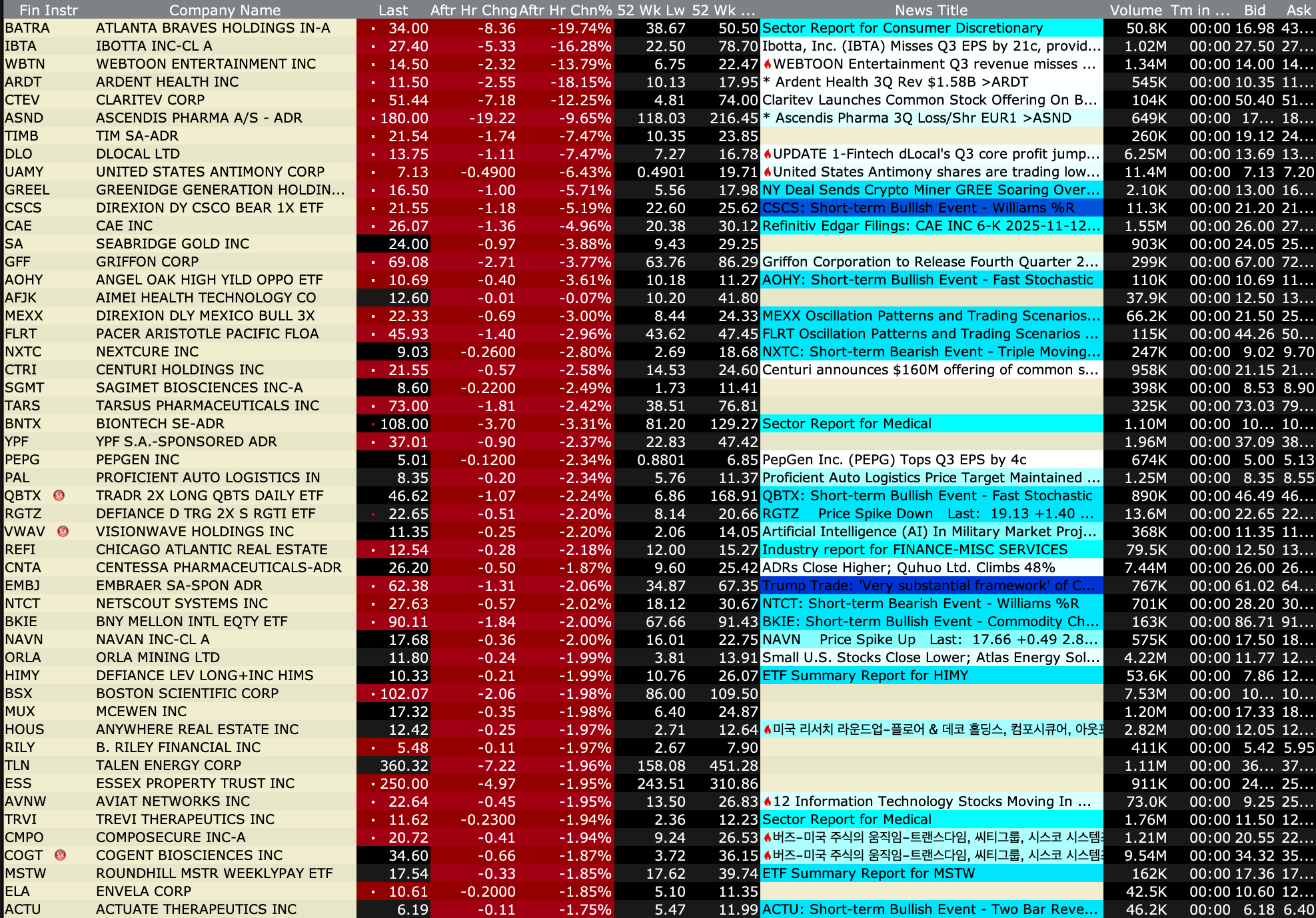

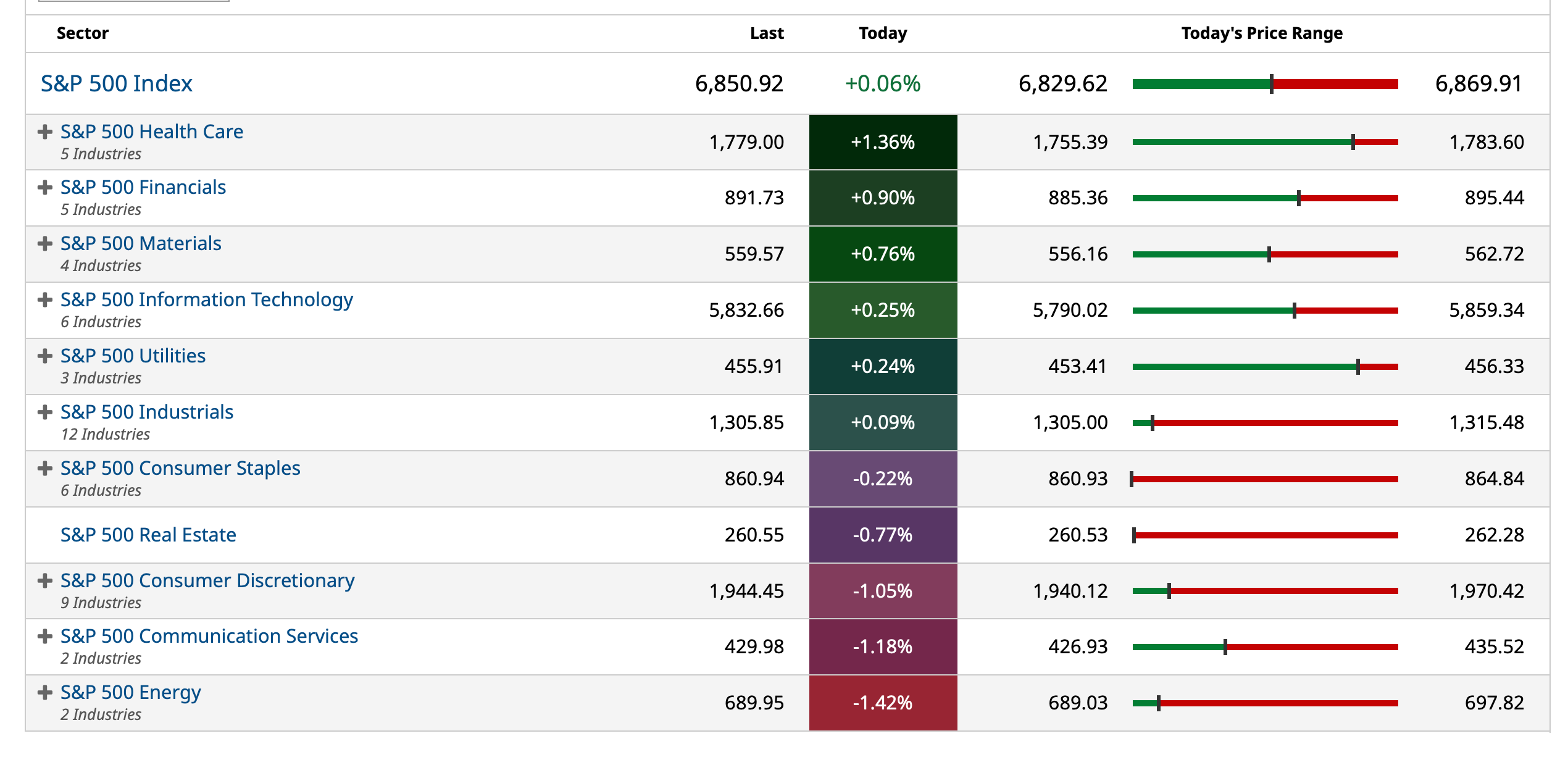

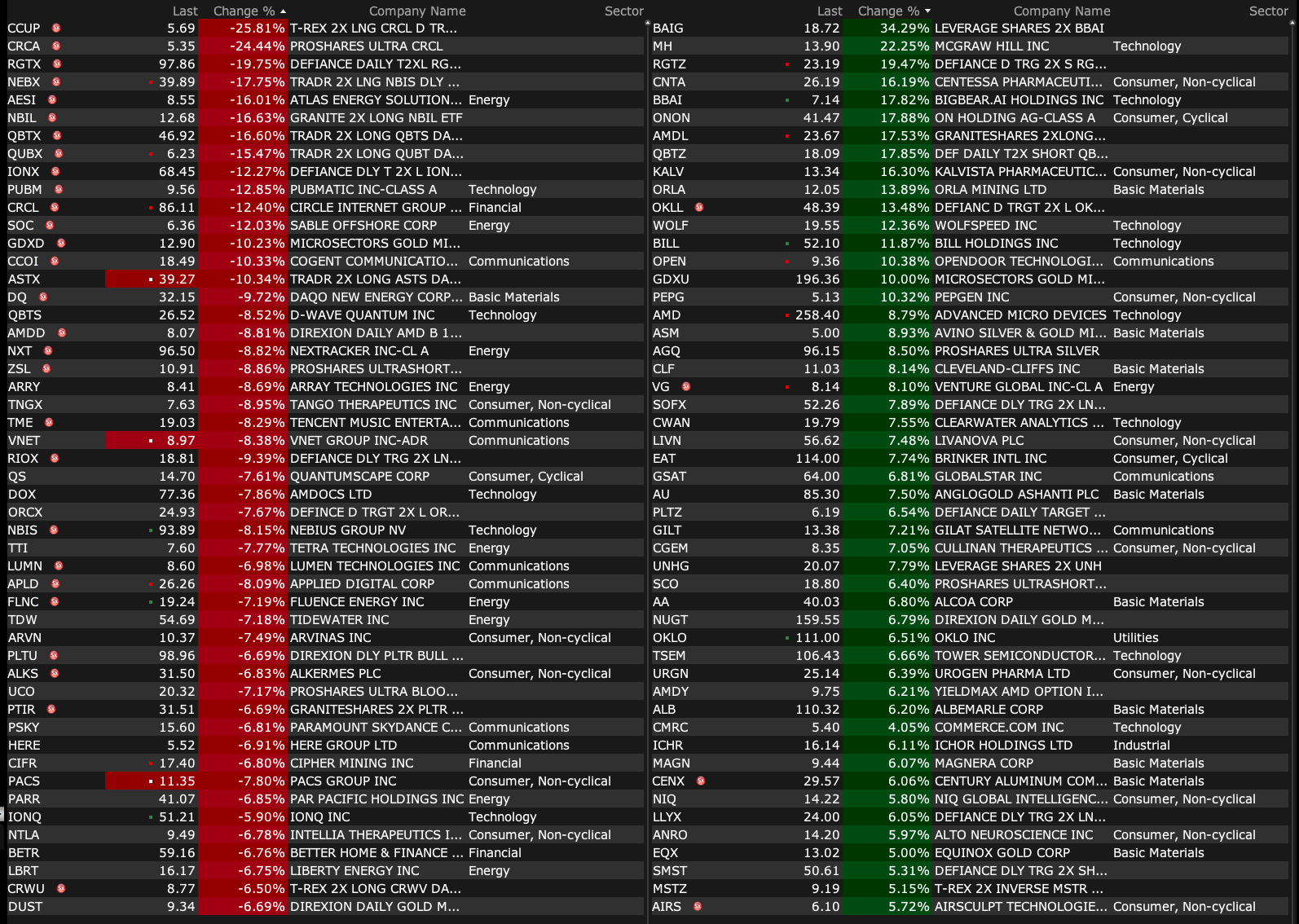

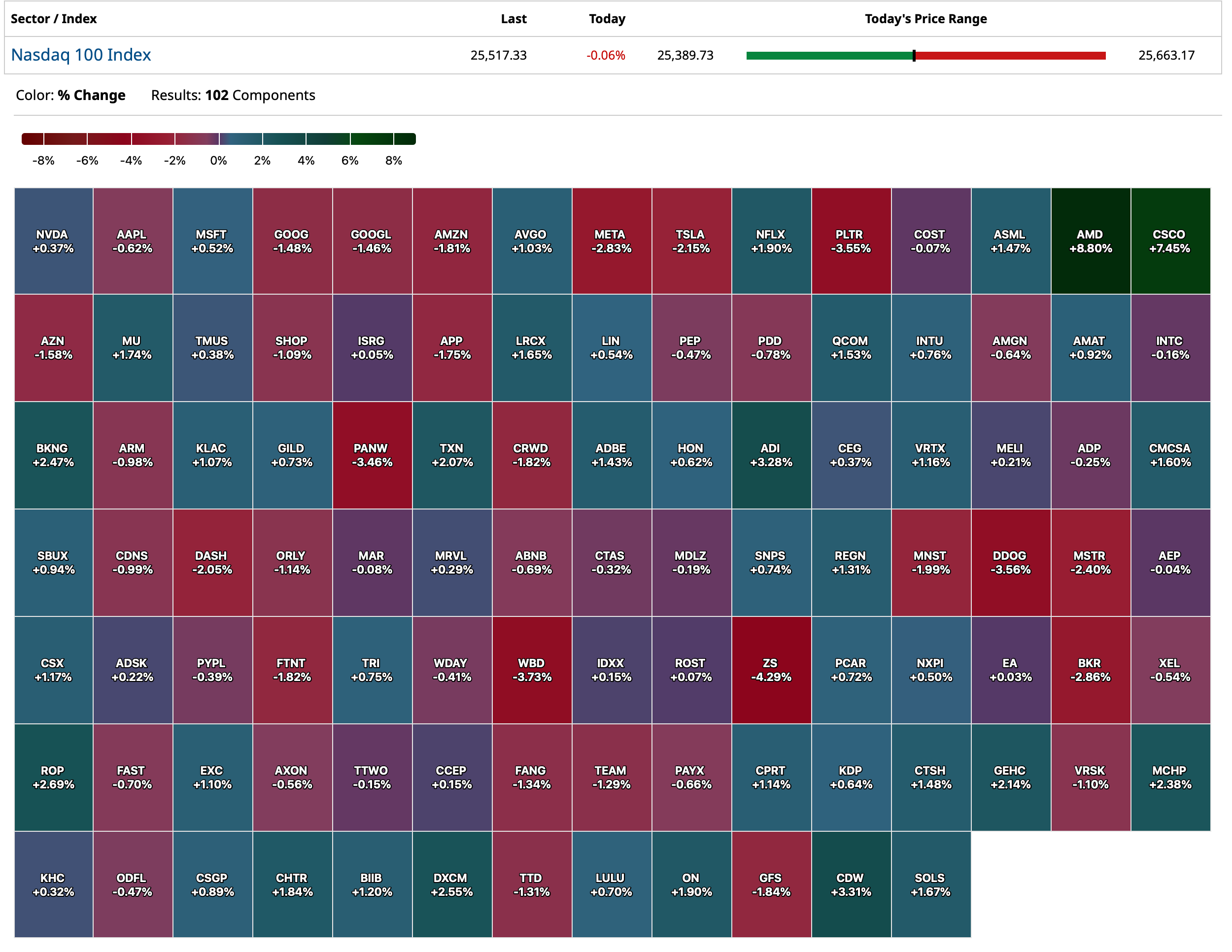

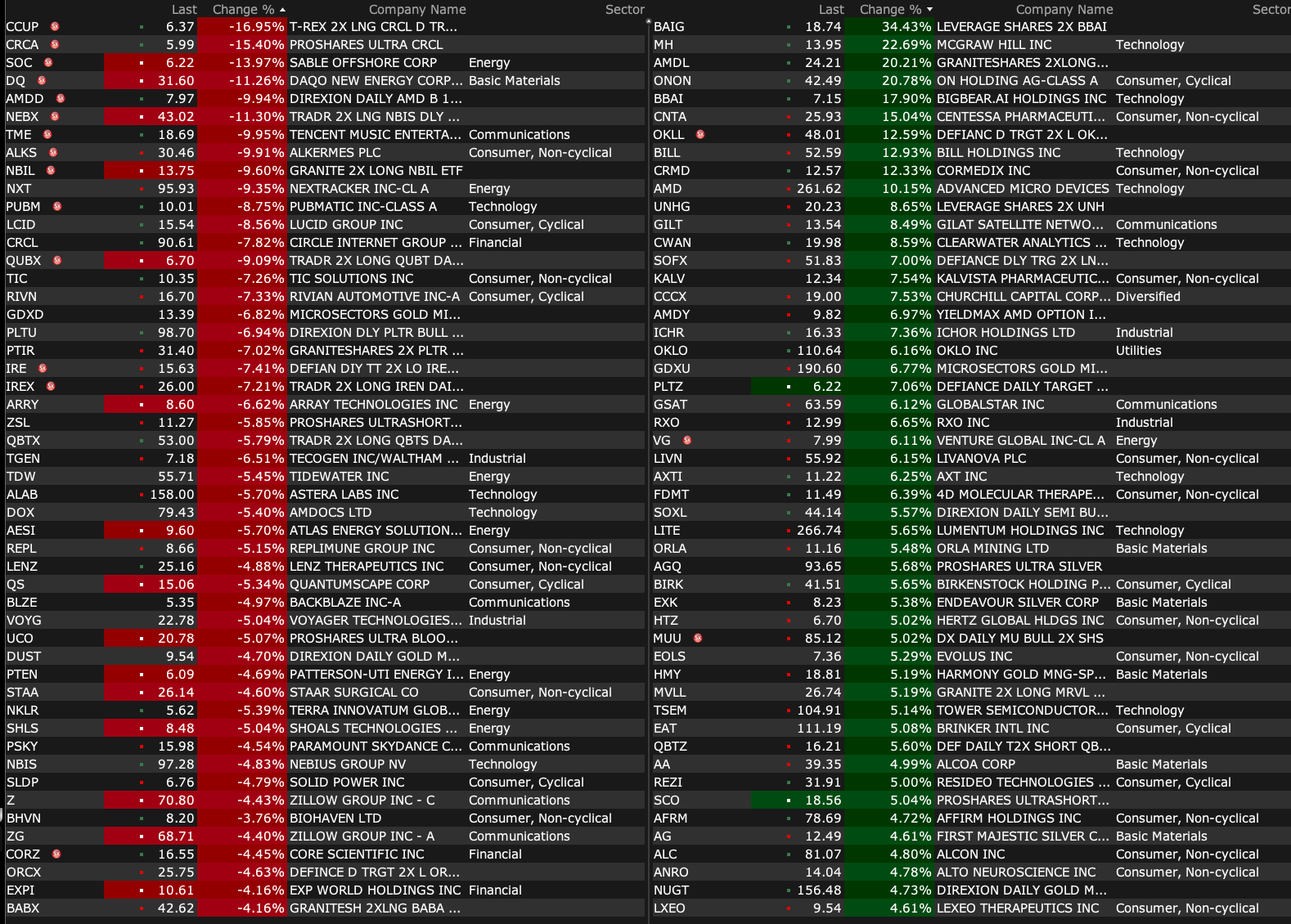

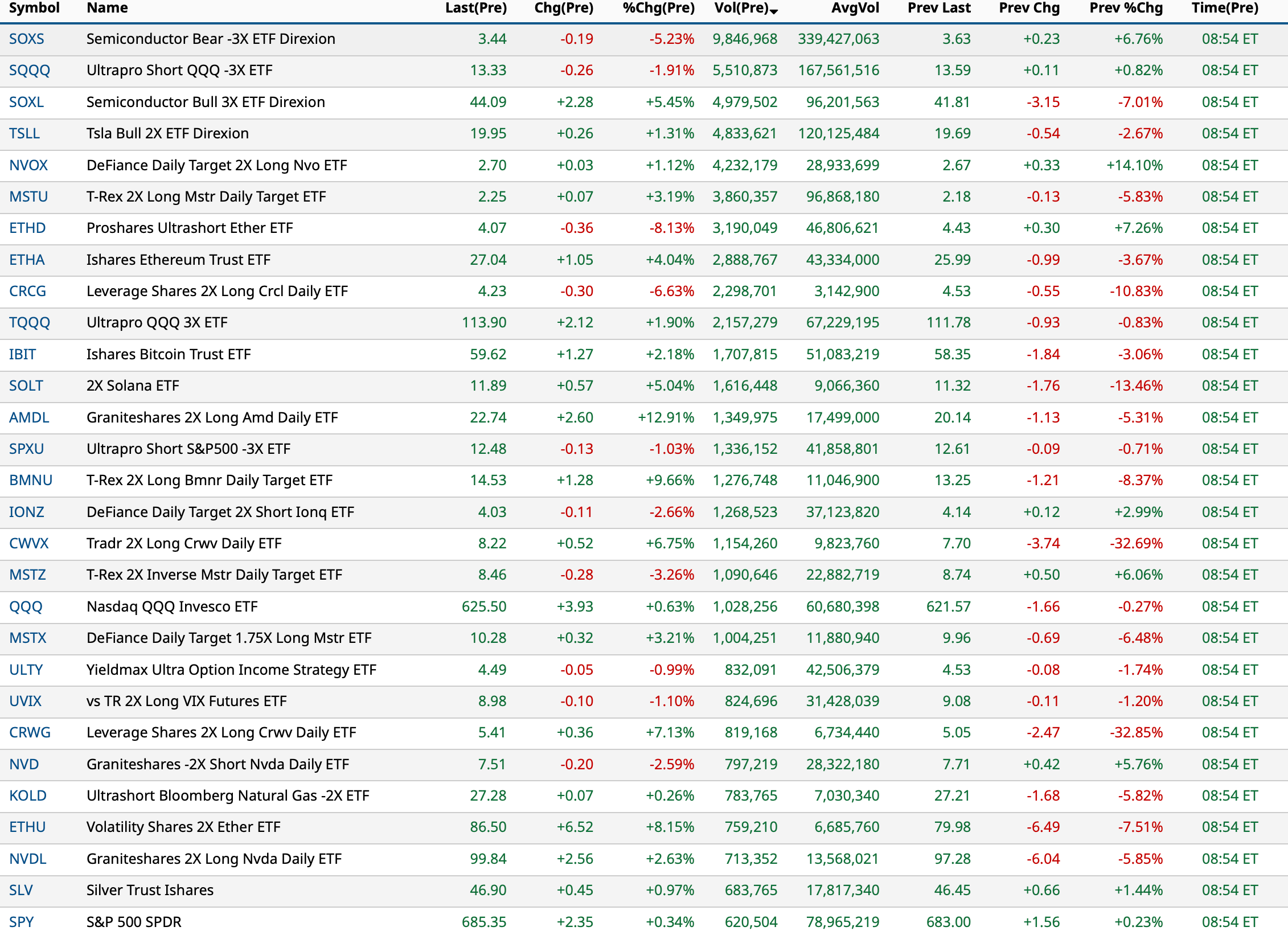

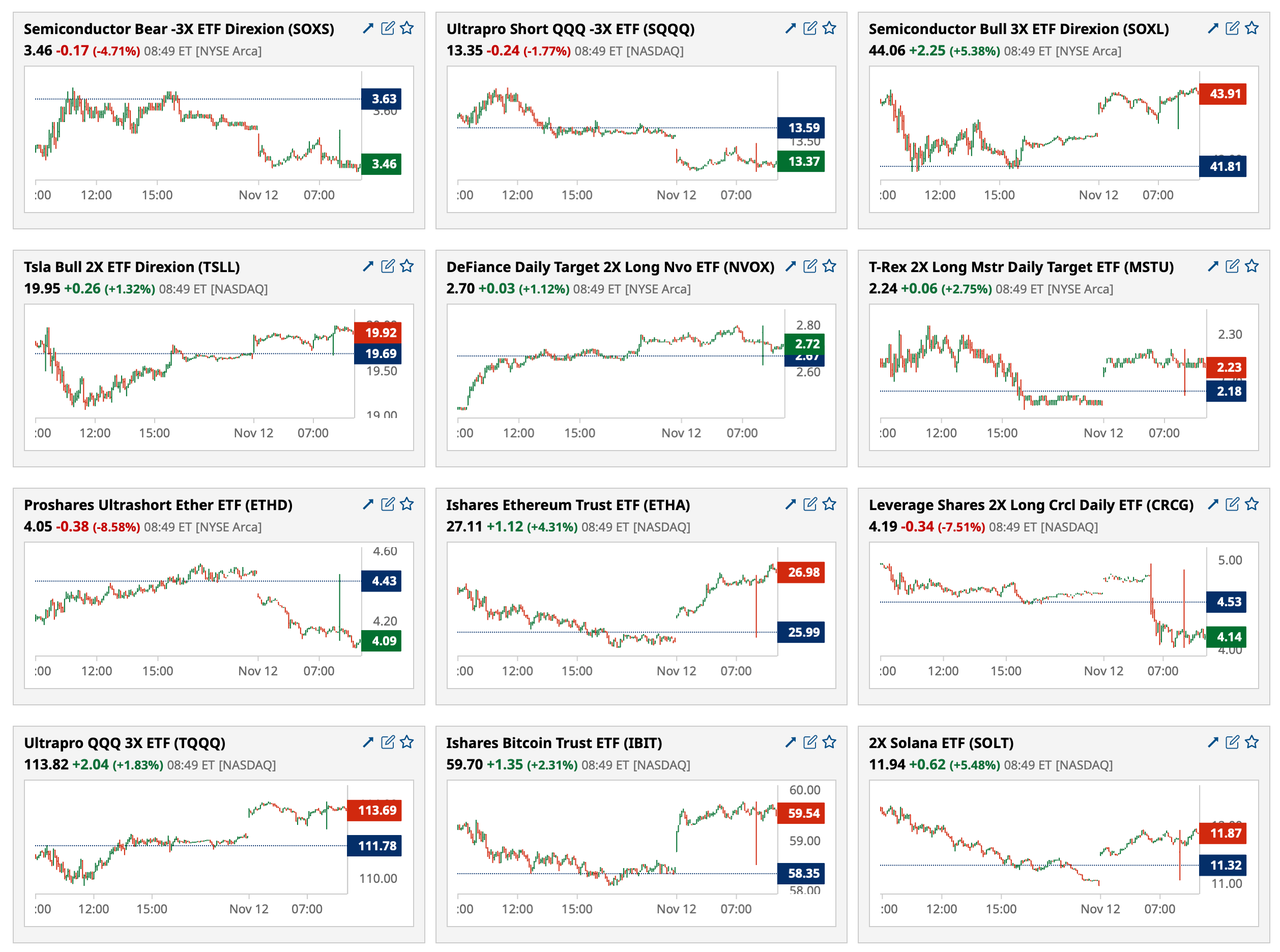

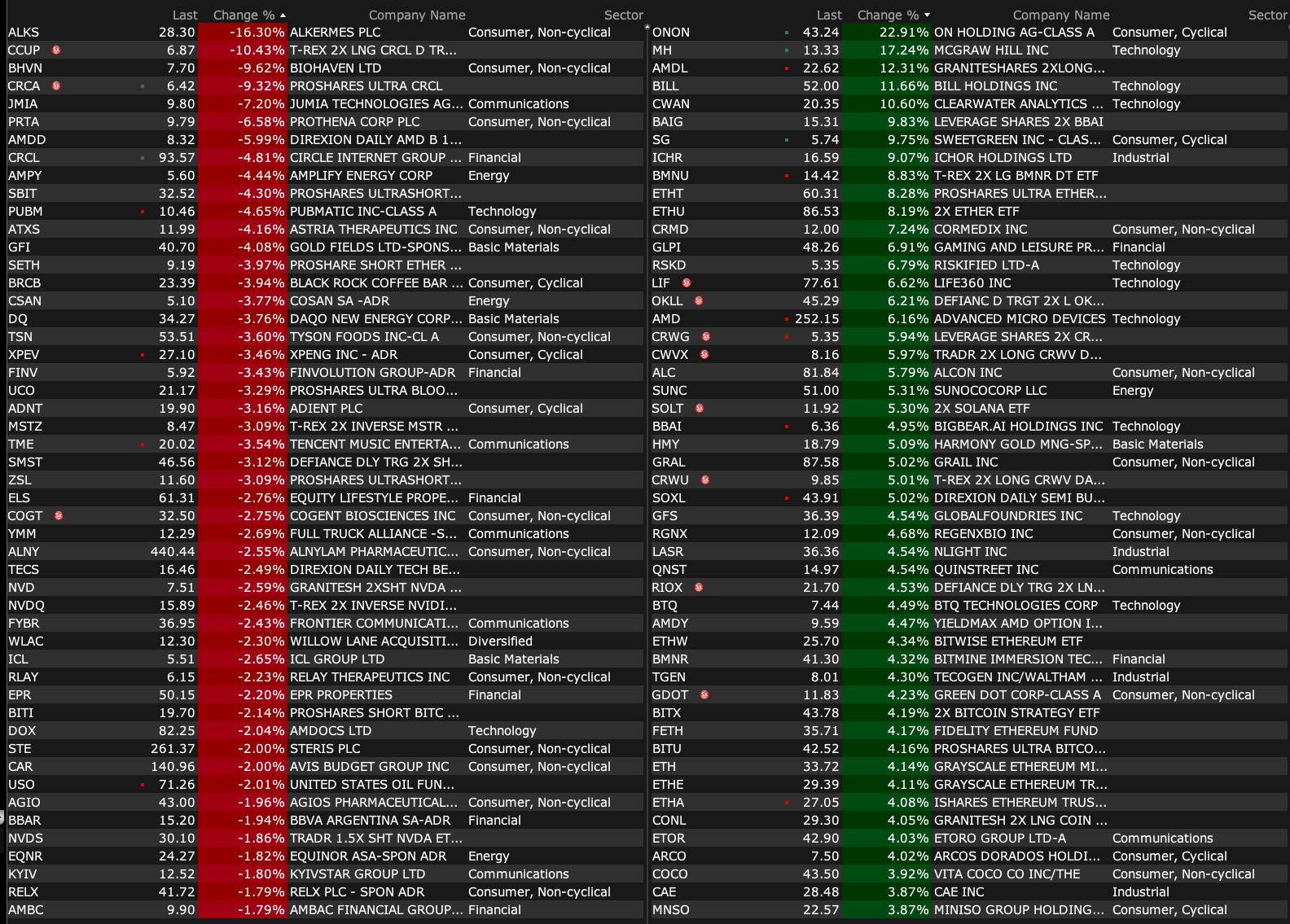

Most Active After Hours

BY Doug Kass · Nov 12, 2025, 4:50 PM EST

BY Doug Kass · Nov 12, 2025, 4:50 PM EST

BY Doug Kass · Nov 12, 2025, 4:45 PM EST

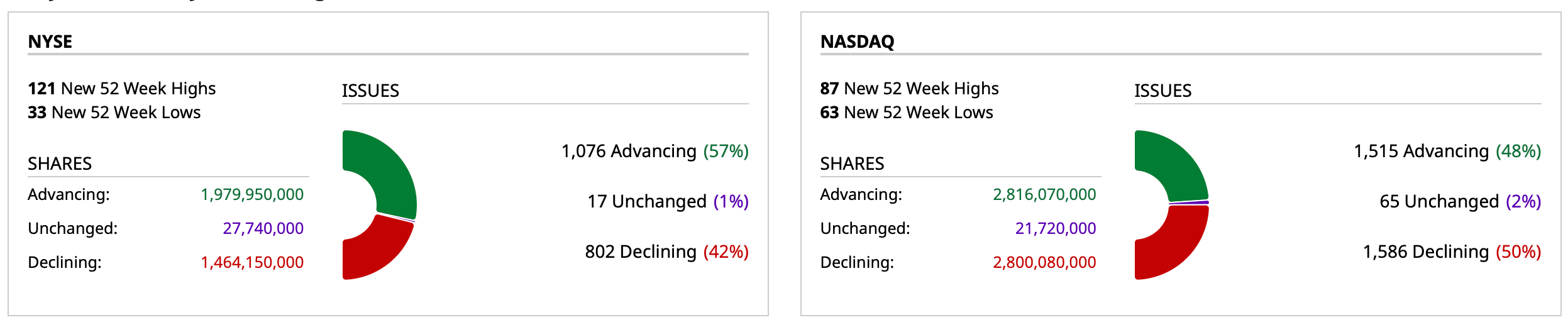

- NYSE volume 3% below its one-month average

- NASDAQ volume 23% below its one-month average

- VIX index: up 1.33% to 17.51

BY Doug Kass · Nov 12, 2025, 4:38 PM EST

With S&P cash +11 handles, I am doing another tranche of shorting index calls.

BY Doug Kass · Nov 12, 2025, 3:40 PM EST

The market has more moves than a shortstop batting .110.

I expect more of this in the coming months — a seesaw move lower ("downside staircase").

BY Doug Kass · Nov 12, 2025, 3:14 PM EST

BY Doug Kass · Nov 12, 2025, 2:00 PM EST

BY Doug Kass · Nov 12, 2025, 12:55 PM EST

"Do not see several labor market downturn as most likely near-term outcome."

- Fed's Bostic (non voter for 2025-2026)

Bostic say he can't "breezily assume" inflationary pressures will quickly dissipate following one-time tariff-related price increases:

- Urgent risk facing the Fed

- Price pressures look likely to persist until mid-to-late 2026

- Labor market shifting, but not clearly weakening

- Serious trouble awaits if inflation expectations for medium- and longer-term drift upward

- Firms surveyed expect to raise prices well into 2026, and by substantially more than 2%

- Main contributors to inflation are services prices ex-housing and core goods prices

BY Doug Kass · Nov 12, 2025, 12:40 PM EST

* If you are rational, you don't stand a chance in today's market...

The movie, King of Hearts, is a quirky comedic war film which focuses on Scottish soldier Charles Plumpick (Alan Bates), who is sent to a French town on a mission to disarm a bomb left behind by the retreating German army. Plumpick discovers that the area is deserted except for the inmates of the local asylum. The mental patients playfully take over the town and pronounce the soldier their king. While Plumpick is intrigued by the antics of the former inmates, he must stay on task and find the bomb before it detonates.

The movie reminds me of today's market.

My godson wants to sell his Procter & Gamble (PG) and buy more Nvidia (NVDA) .

He has reinvented momentum investing by himself on his own AI-filled desert island.

I continually argued against him but I started to demur and then I just gave up and gave in — as I don't have the energy to keep crying wolf even as the wolves seem ready to sit down to feast at their Thanksgiving dinners with their families and other members of the herd.

This is a "King of Hearts" market for a "King of Hearts" financial world.

Zero interest rates for 15 years created trillions of dollars, bailed out the bankers and gave rise to a startling cumulative rise in the cost of necessities (that have served to erode the quality of living for the many).

If you are rational, you don't stand a chance in today's market.

BY Doug Kass · Nov 12, 2025, 12:25 PM EST

BY Doug Kass · Nov 12, 2025, 11:55 AM EST

With S&P cash rallying to even, I am selling more SPY calls (short).

BY Doug Kass · Nov 12, 2025, 11:42 AM EST

BY Doug Kass · Nov 12, 2025, 11:35 AM EST

BY Doug Kass · Nov 12, 2025, 11:15 AM EST

BY Doug Kass · Nov 12, 2025, 11:13 AM EST

Run, don't walk to watch MRKT CALL with Guy and Dan at 11 a.m. Why do I spend 45 minutes of every day on their podcast?

Because they are transparent, action oriented and they think outside of the consensus. This non herd-like team (which often includes the lynx-eyed EY from (SOFI) and Carter Worth) take ownership of their losers and don't gloat on their winners - which is refreshing.

Lets go to the tape! MRKT Call - Wednesday, November 12th

BY Doug Kass · Nov 12, 2025, 11:02 AM EST

BY Doug Kass · Nov 12, 2025, 10:50 AM EST

* Some comic relief....

A down day.

BY Doug Kass · Nov 12, 2025, 10:43 AM EST

With S&P cash +10 handles, adding to my short Index call holdings.

BY Doug Kass · Nov 12, 2025, 10:16 AM EST

I have added to my short (SPY) calls.

Note: I have no position in (QQQ) calls - which I mistakenly disclosed earlier this morning.

BY Doug Kass · Nov 12, 2025, 10:10 AM EST

BY Doug Kass · Nov 12, 2025, 10:00 AM EST

From Peter Boockvar:

In trying to square up the monthly ADP jobs report seen last week of +42k and the number yesterday from ADP saying that 11,250 jobs were lost in the four weeks ended Oct 25th needs more explanation from ADP. But my back of the envelope is this as the monthly figure captured job growth from mid September to October 12th. At a gain of +42k, that assumes about +10k per week on average. So, the first two weeks of October would imply +20k and in order to get a full month of -11k means that the last two weeks of October saw a job loss of 64k. If about right, I’m assuming a factor in the notable drop had to do with the government shutdown. Not with respect to government jobs, as that is not included here, but maybe government contractors that were not paid (though eventually will) and temporarily didn’t pay workers. Just a guess here.

Stress on the consumer we know has been seen particularly in the subprime auto sector. I didn’t see the actual Fitch report but Bloomberg News is reporting today on it that “The share of subprime borrowers at least 60 days past due on their auto loans rose to 6.65% in October, the highest in data going back to 1994, according to Fitch ratings.”

With the average 30 yr mortgage rate at 6.34% for the week ended 11/7, purchase applications rose 5.8% w/o/w after a slight drop last week. Refi’s though fell 3.4% but are still up 147% y/o/y. We know we’ve seen a muted response so far to the drop in mortgage rates and that’s because of still high home prices. I think we need a bigger drop in home prices in order to stimulate demand that would join lower mortgage rates. People who own homes won’t like that but it would be some lubricant, along with lower rates, to jump start more transactions.

We have a two lane economy overall for sure but also one within tech, as we’ve seen. You’re either selling into the AI data center buildout or you’re not. From Infineon Technologies, the German chipmaker and whose stock is jumping by 9%:

“Global investment in AI infrastructure is continuing to rise rapidly and we expect considerable growth. Growth momentum in the automotive, industrial and consumer markets remains modest. Many customers are proceeding cautiously and placing short-term orders.”

No real other earnings of note to cover but Baird had its Global Industrial Conference and some tidbits were picked up there.

From FedEx who rallied 5.6% yesterday:

When asked about the peak season which we are in the midst of, “we expect modest demand for peak, as we said before. And there is one extra operating day between Thanksgiving and Christmas...So the demand from our customers are consistent with what they have been telling us historically. So that’s what we are planning for...So we’re more or less in line with what we expected.”

“what we said in September was we expected a modestly improved peak y/o/y by way of specific update. Also in September, we said there would be sequential improvement from Q1 to Q2. I can update that not only do we expect that sequential improvement from Q1 to Q2, but also a y/o/y improvement.” That’s what lifted the stock.

From JB Hunt who was more cautious, still:

“Well I think this is the longest downturn of my career of 31 years. I think maybe the longest downturn in our company’s history for the duration.”

“We’re in a freight market that is no good...And so you’re in a depressed freight market.” But they are beginning to see some tightness in capacity in part due to changes in regulations with drivers.

The Japanese yen is weakening back to the key 155 level with expectations of looser fiscal policy at the same time the BoJ keeps dragging its feet with rate hikes. But will they even hike in December? The new PM said today “The conduct of appropriate monetary policy is very important to achieving both a strong economy and stable inflation at the same time. We will continue to work together for the development of the economy.” Does that mean her administration will press the BoJ not to hike?

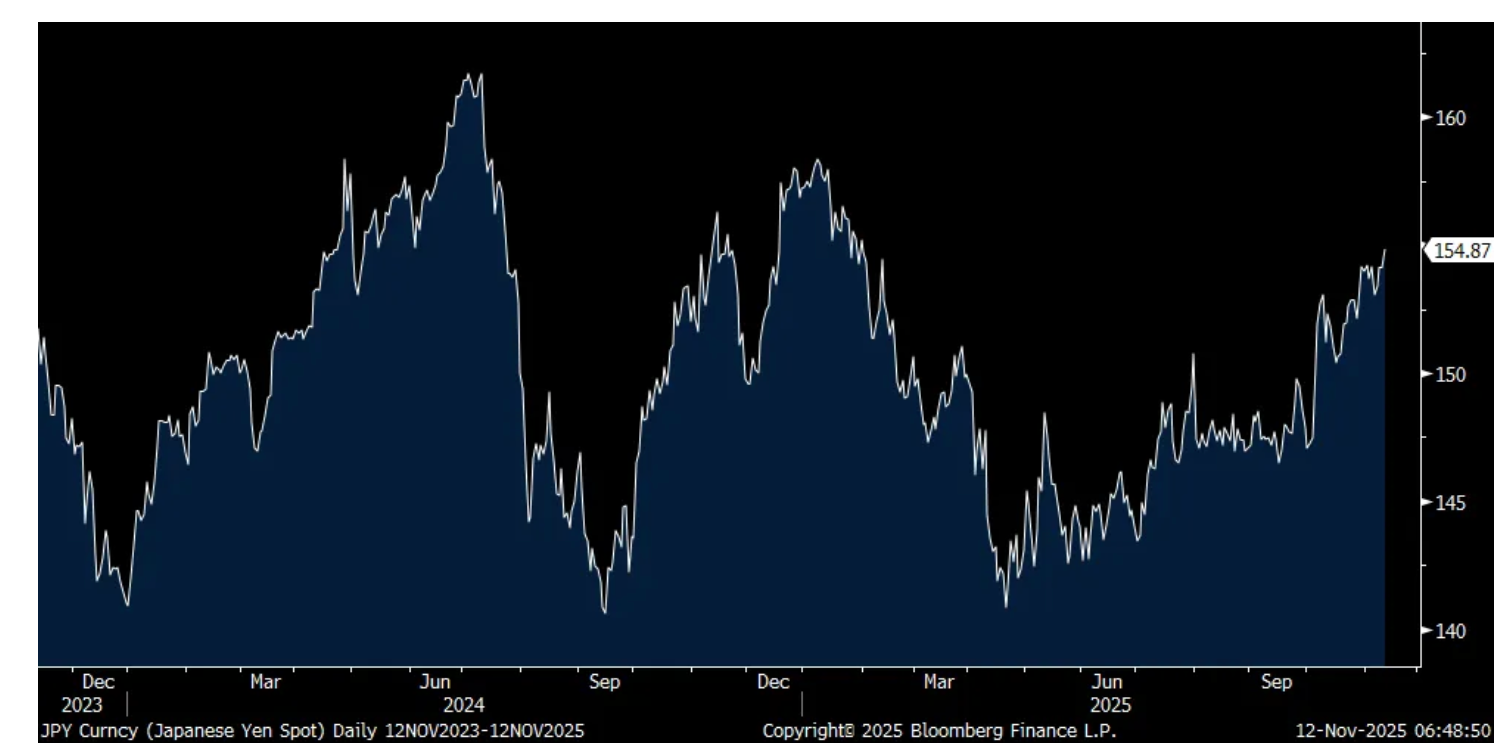

On the other hand, a weak yen is not good for inflation, nor consumer spending. The Finance Minister doesn’t like the yen weakness and said “Recently, we have been seeing one-sided and rapid movements in the foreign exchange market...Exchange rate movements have both positive and negative effects on the economy, and I do not deny that the negative aspects have become more pronounced in some respects.”

And the jawboning part to stem the yen weakness, “The government is watching for any excessive and disorderly moves with a high sense of urgency.” We watch as well.

Yen

BY Doug Kass · Nov 12, 2025, 9:45 AM EST

BY Doug Kass · Nov 12, 2025, 9:27 AM EST

BY Doug Kass · Nov 12, 2025, 9:20 AM EST

BY Doug Kass · Nov 12, 2025, 8:50 AM EST

Treasury Auctions:

11:30 a.m.: Treasury hosts a $69 billion 17-week Bill Auction;

1 p.m.: Treasury hosts a $42 billion 10-Year Note Auction; 2:00 p.m.: Treasury buyback (liq support)

Fed Speakers:

9:20 a.m.: Fed Bank of New York President Williams (Voter) speaks before the 2025 U.S. Treasury Market Conference co-hosted by the Federal Reserve System and the Treasury Department, NYC (Text and livestream available. No Q&A);

10 a.m.: Fed Bank of Philadelphia President Paulson (Voter in 2026) speaks on Fintech before hybrid Ninth Annual Fintech Conference hosted by the Federal Reserve Bank of Philadelphia, Philadelphia, PA (Text available. No Q&A);

10:20 a.m.: Fed Board Governor Waller (Voter) participates in "Payments" discussion before hybrid Ninth Annual Fintech Conference hosted by the Federal Reserve Bank of Philadelphia (No text. Q&A from moderator);

12:15 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter) speaks on the economic outlook before the Atlanta Economics Club November luncheon, Atlanta, GA (Livestream at https://www.youtube.com/watch?v=ZJFFdS5T8gM. Audience Q&A expected. No media. Q&A. Embargoed text available);

12:30 p.m.: Fed Board Governor Miran (Voter, Dovish Dissenter) participates in conversation before event hosted by the University of Cambridge Judge Business School, Cambridge (No text. Q&A from moderator. Webcast available, link forthcoming);

2:35 p.m.: New York Fed Bank Director of Research Athreya speaks at 62nd Annual Arizona State University (ASU)/PNC Bank Economic Forecast Luncheon;

3:50 p.m.: NY Fed Bank SOMA Manager Roberto Poli speaks at 2025 US Treasury Market Conference, NYC;

4:00 p.m.: Fed Bank of Boston President Collins (Voter) speaks on "Perspectives on the Economy and the Financial Landscape" and participates in a moderated discussion before the 24th Annual Regional and Community Bankers Conference at the Federal Reserve Bank of Boston (Livestream available, link forthcoming. Embargoed text available. No audience Q&A. No media Q&A)

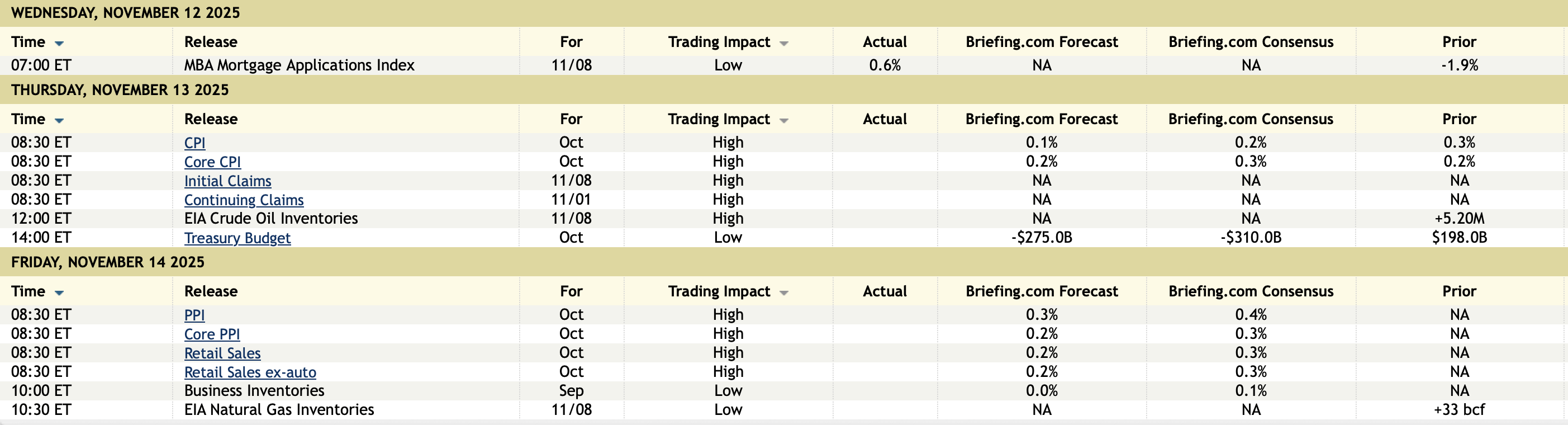

Economic Calendar:

BY Doug Kass · Nov 12, 2025, 8:25 AM EST

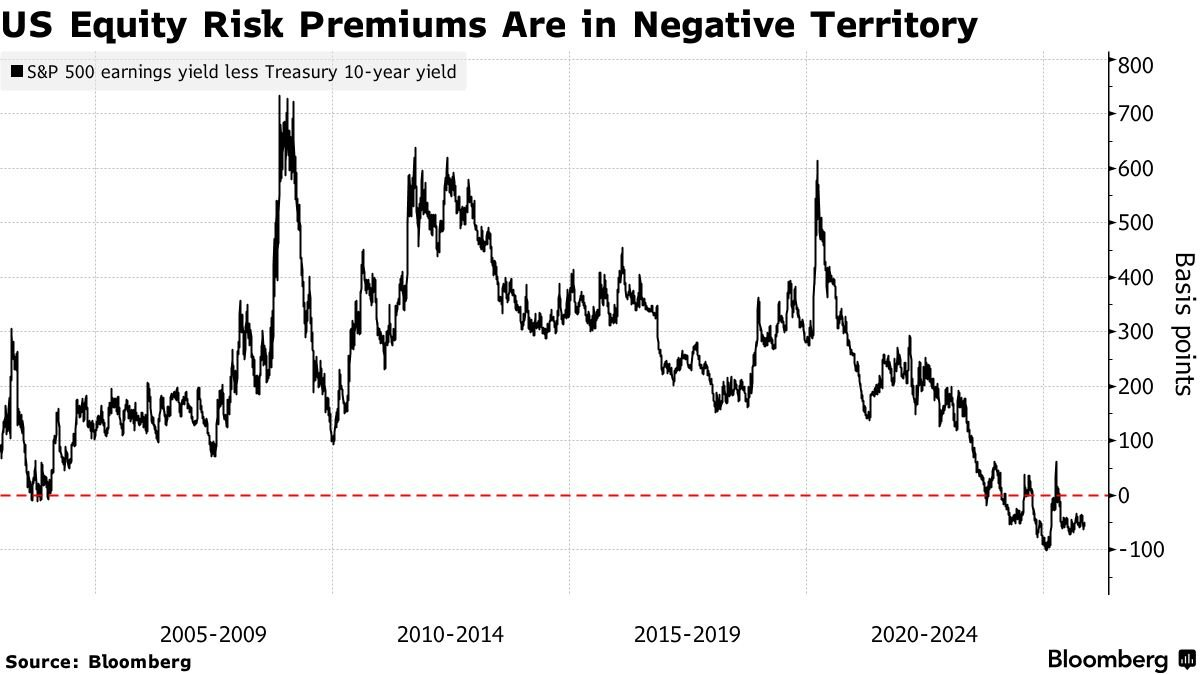

"The equity risk premium (ERP) is the excess return that investors expect to receive from holding stocks compared to a risk-free asset, like government bonds. It serves as compensation for the additional risk of investing in the stock market, which is generally more volatile than bonds. A higher ERP suggests investors demand more return for the risk they take, while a lower or negative ERP can signal that stocks may not be offering sufficient compensation for their risk. "

- Equity Risk Premium, WIKI

The Equity Risk Premium represents the additional return stocks offer over risk-free investments like Treasury notes, compensating investors for higher risks.

In an earlier column this morning, The Equity Risk Premium Is in Negative Territory, I declared that, to me:

this is the most important chart regarding stock valuations and prices being overvalued.

From a historical standpoint, the Equity Risk Premium Equity Risk Premium (ERP) | Formula + Calculator was last in negative territory from 1997-2000. The dot.com bubble soon burst dramatically. To put the Equity Risk Premium into context, the long term average (when applying the 10 year Treasury note's yield) is +2.50% - compared to only 20 basis points this morning.

Since mid-2024 I have been using the paper thin Equity Risk Premium argument as why valuations are a poor launching pad for future investment returns.

This has proven incorrect, as a very slim Equity Risk Premium has not constrained the equity market.

That said, I remain focused and lean on the miniscule Equity Risk Premium as an important factor in my ursine market outlook.

BY Doug Kass · Nov 12, 2025, 8:10 AM EST

BY Doug Kass · Nov 12, 2025, 7:30 AM EST

Back to the "irrelevant" economic data:

BY Doug Kass · Nov 12, 2025, 7:20 AM EST

* For a quick gain... (which adds up!)

In the last 50 minutes, the gain in S&P futures has more than halved — now +12 handles.

I have covered my earlier index shorts this morning at:

* (SPY) $684.11

* (QQQ) $623.67

I plan to re-short strength.

With S&P futures +28 handles, I am back shorting index common:

* (SPY) $685.57

* (QQQ) $625.83

Position: Short SPY common (VS) and calls (VS), QQQ common (VS) and calls (VS)

By Doug Kass Nov 12, 2025 6:05 AM EST

BY Doug Kass · Nov 12, 2025, 7:10 AM EST

From JPMorgan:

US: Futs are higher as the US takes another step to reopen with a House vote (expected to pass_ later today with Trump’s approval. Watch the AI theme with bullish signals from AMD analyst day (+4.9%) and Foxconn earnings. Pre-mkt, Mag7 names are all higher and NVDA (+1.5%) and AVGO (+1.4%) boosting Semis. Cyclicals (ex-Energy) poised to outperform as the yield curve bull steepens with traders buying bonds to match yesterday’s rally in Treasury Futs follower weaker than expected jobs data. USD is bid up pre-mkt; cmdtys are mixed with Energy and Ags weaker with Base higher, gold flat, and silver +1.2%. The macro focus today is on the House vote and mtge applications; XHB has outperformed the SPX by ~1% MTD; IYR and XLRE have outperformed by almost 2% MTD. Also, Trump is hosting Wall Street execs for dinner tonight.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

The biggest news from yesterday was the weaker labor market data which should fuel a rally in bonds as the market prices back in higher probabilities of rate cuts in Dec and Jan fueling hopes that this bull rally continues into late 2026 or beyond. More color is provided below as the AI theme finds additional support into next week’s NVDA earnings report.

· MACRO DATA – Yesterday, we received both the NFIB Small Business Survey, with its Hiring Plans sub-index, and ADP’s weekly jobs print. In both cases, it points to a potentially softening labor market with both prints seeing deterioration MoM. In the case of ADP, it has not been a reliable indicator of NFP in the post-COVID era. Also, with the gov’t poised to reopen, Feroli created a time line for when macro data will be release.

· FED VIEW – Feroli never wavered on his forecast for 25bp cuts for each of the next two meetings, though the market reduced the probability of cuts following Powell’s hawkish press conference following the Oct Fed meeting. Given the weak labor market data yesterday we think bonds will quickly move back to pricing in those cuts. Yesterday, Treasury Futures rallied after the labor market prints, implying the 10Y yield declining by 5bp.

· STILL BULLISH? Yes, we are still bullish. On a day where AI fatigue was evident (AMD analyst day, CRWV miss, NVDA negative holder headlines) given the SPX an excuse to decline 1%+ on a low liquidity day, we saw the market rotate to a combination of Defensives (HC, Staples, and RE) and commodity-related sectors to post another gain. The gain came with ~68% of the index in the green and SPW outperforming SPX by 37bp.

· SEASONALITY – I think most clients are aware of the strong, positive seasonality in Q4 for Equity indices, but we thought it worthwhile to look at it by the major factors.

BY Doug Kass · Nov 12, 2025, 7:00 AM EST

Bonus — Here are some great charts:

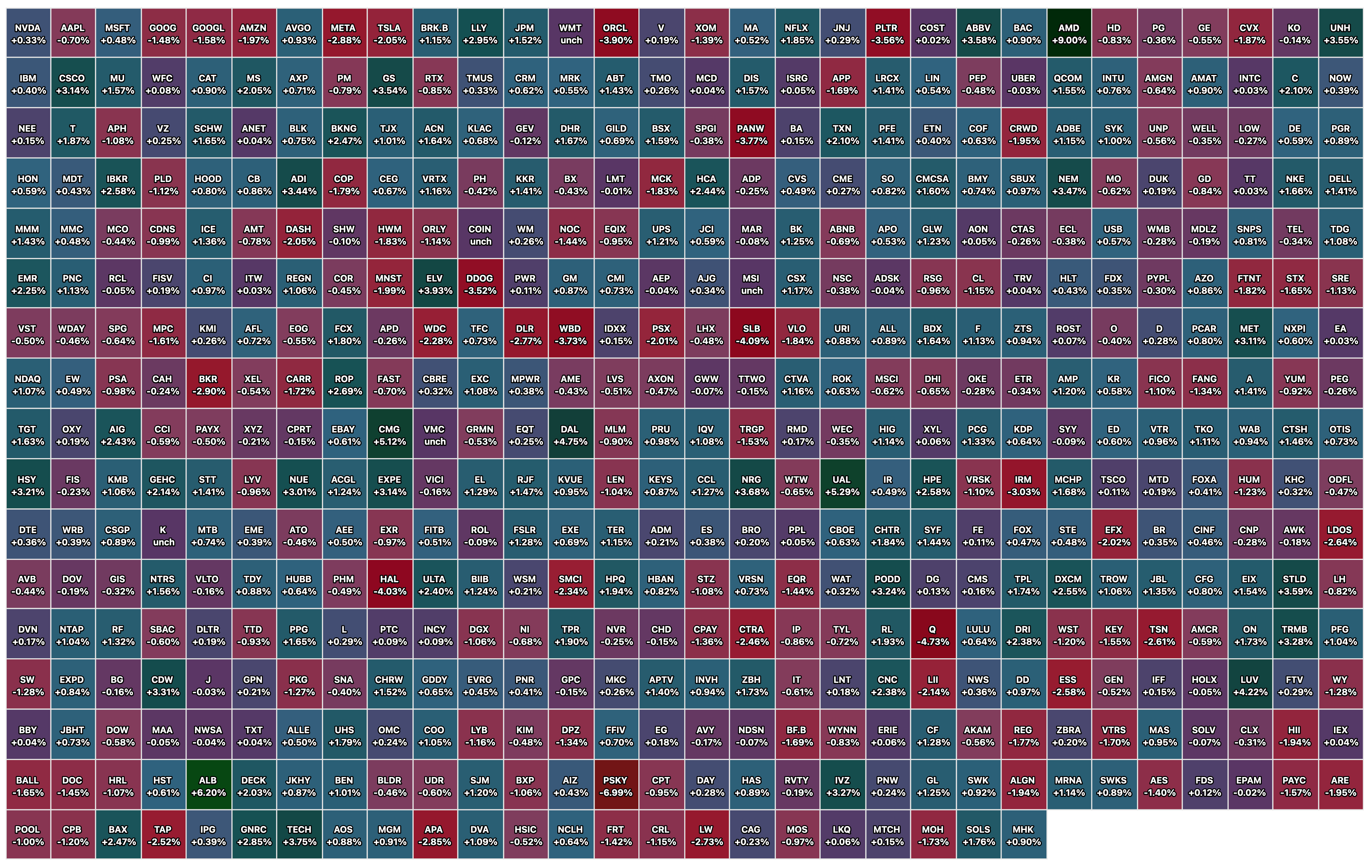

It Can’t Be 7 Stocks if It’s 150

BY Doug Kass · Nov 12, 2025, 6:45 AM EST

BY Doug Kass · Nov 12, 2025, 6:35 AM EST

BY Doug Kass · Nov 12, 2025, 6:25 AM EST

Wolf Street on stupid fifty-year mortgages.

BY Doug Kass · Nov 12, 2025, 6:15 AM EST

With S&P futures +28 handles, I am back shorting index common:

* (SPY) $685.57

* (QQQ) $625.83

BY Doug Kass · Nov 12, 2025, 6:05 AM EST

The S&P Short Range Oscillator is at 0.16% vs. -1.34%.

It is no longer oversold.

BY Doug Kass · Nov 12, 2025, 5:55 AM EST

To me, this is the most important chart regarding stock valuations:

BY Doug Kass · Nov 12, 2025, 5:45 AM EST