Private Credit Tweet of the Day

BY Doug Kass · Nov 10, 2025, 4:45 PM EST

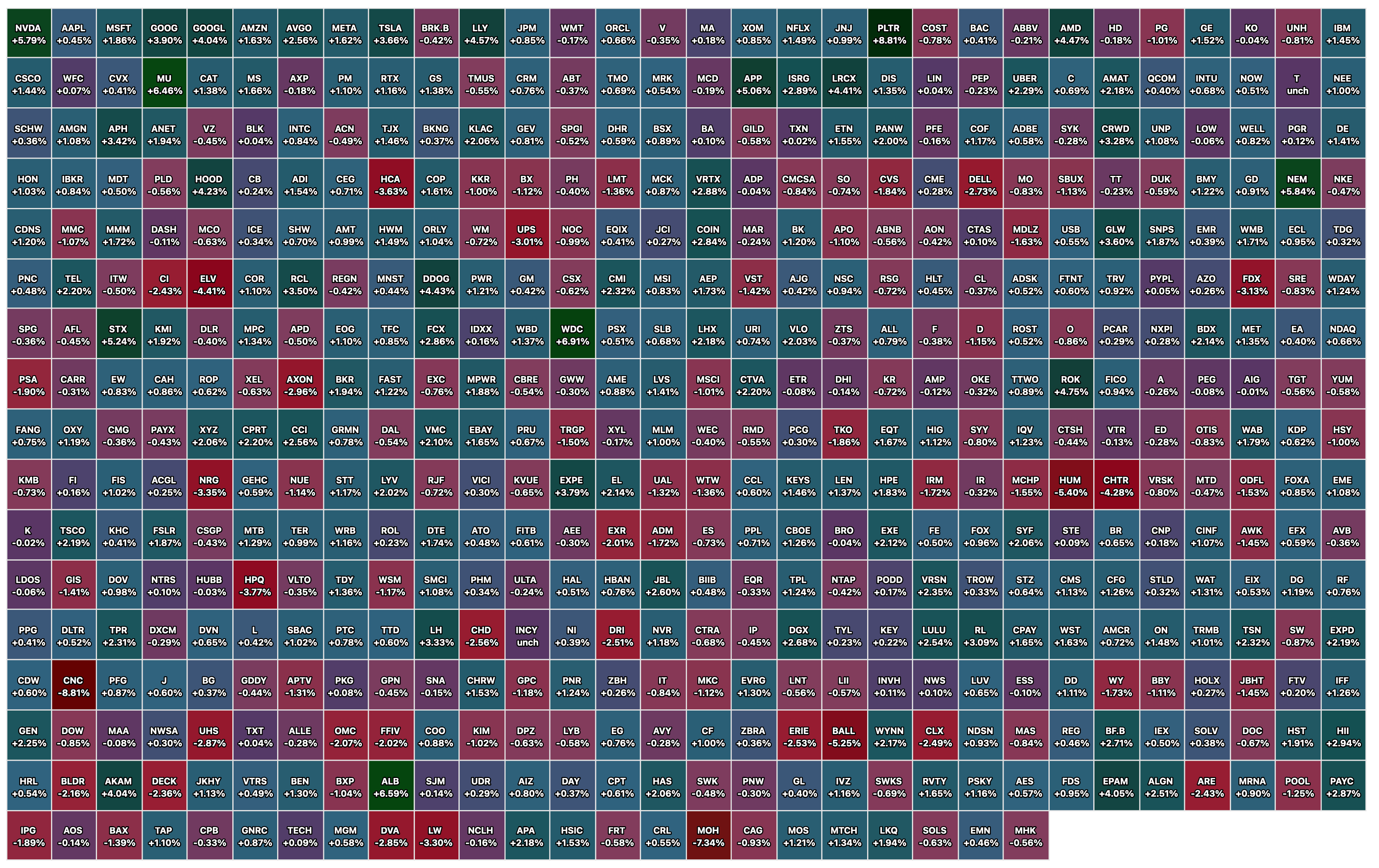

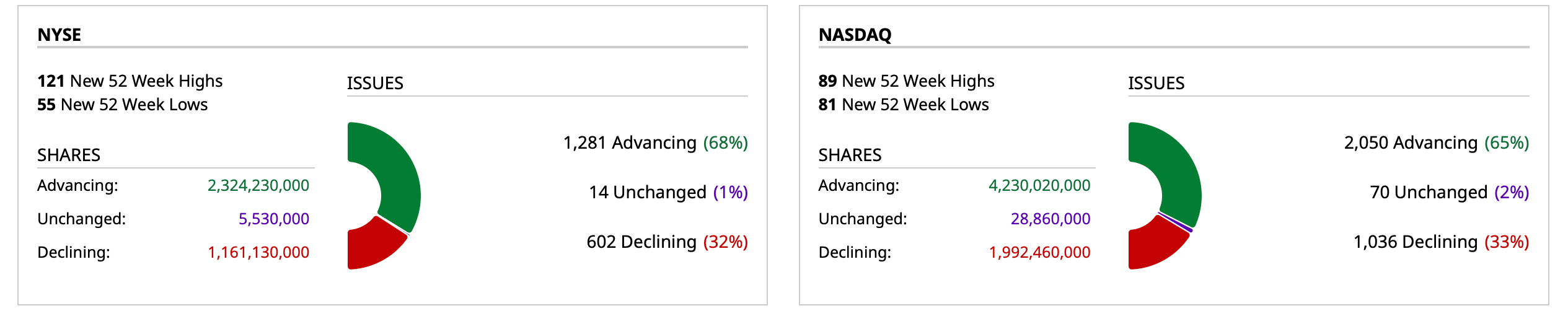

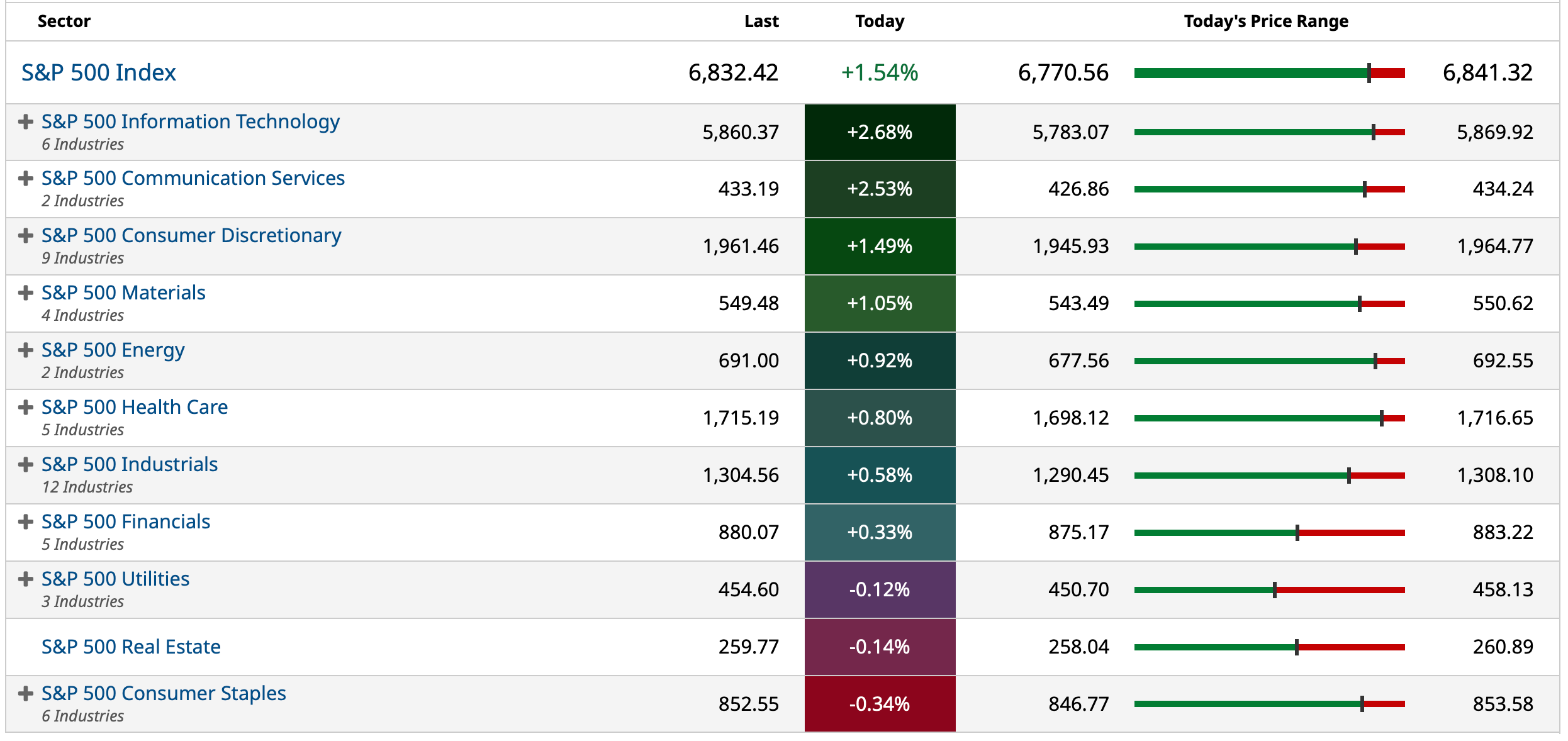

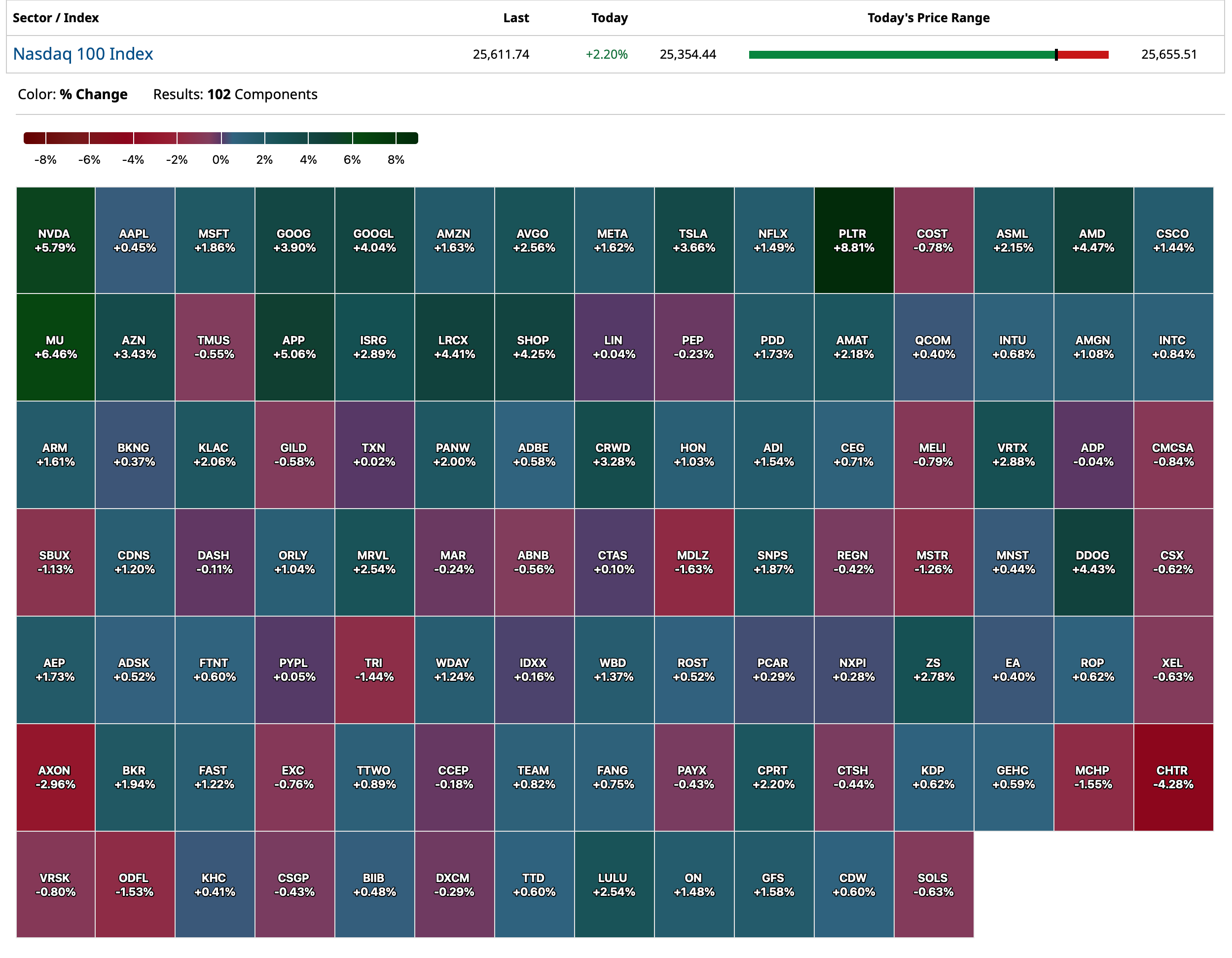

BY Doug Kass · Nov 10, 2025, 4:45 PM EST

BY Doug Kass · Nov 10, 2025, 4:35 PM EST

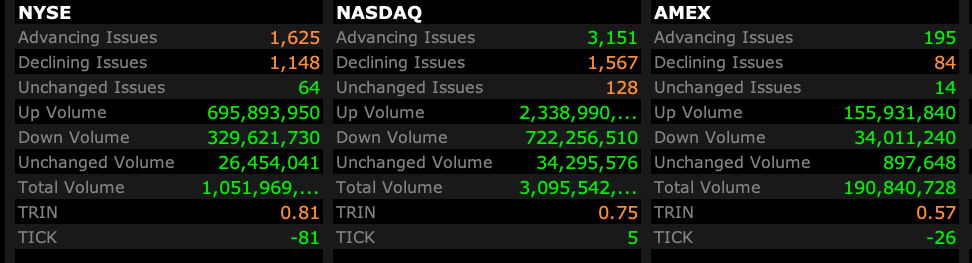

- NYSE volume flat to its one-month average

- NASDAQ volume 14% below its one-month average

- VIX index: down 7.76% to 17.60

BY Doug Kass · Nov 10, 2025, 4:30 PM EST

BY Doug Kass · Nov 10, 2025, 3:52 PM EST

Here are today's things:

* I added to my index short calls.

* Added to longs in PepsiCo (PEP) at $142.06 and Kimberly-Clark (KMB) at $102.39.

BY Doug Kass · Nov 10, 2025, 3:40 PM EST

BY Doug Kass · Nov 10, 2025, 3:35 PM EST

Back from my meetings/stuff to see the S&P index +105 handles.

I am speechless.

BY Doug Kass · Nov 10, 2025, 3:28 PM EST

On Twitter:

MICHAEL BURRY WARNS OF ‘EARNINGS FRAUD’ FROM EXTENDED ASSET LIVES “The Big Short” investor Michael Burry accused major tech firms of inflating profits by extending the useful life of equipment. He said hyperscalers’ Nvidia-driven spending should shorten, not lengthen, depreciation cycles, estimating $176 billion in understated depreciation from 2026–2028. Burry claims Oracle and Meta could overstate earnings by 27% and 21%, respectively, with more details coming Nov. 25.

BY Doug Kass · Nov 10, 2025, 1:33 PM EST

Interesting, even during a risk-on day, the CDSs are still going the other way:

Also I would point out that TSM monthly commentary was pretty interesting too re the current month slowing a fair bit sequentially. Probably a mistake for me to even mention this as I am not on top of the granular details of what could be going on with their business. The stocks are going to do what they are going to do, regardless of what I say anyway.

Taiwan Semiconductor Manufacturing Co. (TSM) just hit a speed bump in its record run. The chipmaking giant posted a 16.9% rise in October sales, its slowest growth since February 2024, raising quiet questions about whether the AI boom is shifting gears.

BY Doug Kass · Nov 10, 2025, 12:50 PM EST

- NYSE volume 6% above its one-month average;

- Nasdaq volume 13% below its one-month average;

- VIX index: down 5.82% to 17.97

BY Doug Kass · Nov 10, 2025, 11:11 AM EST

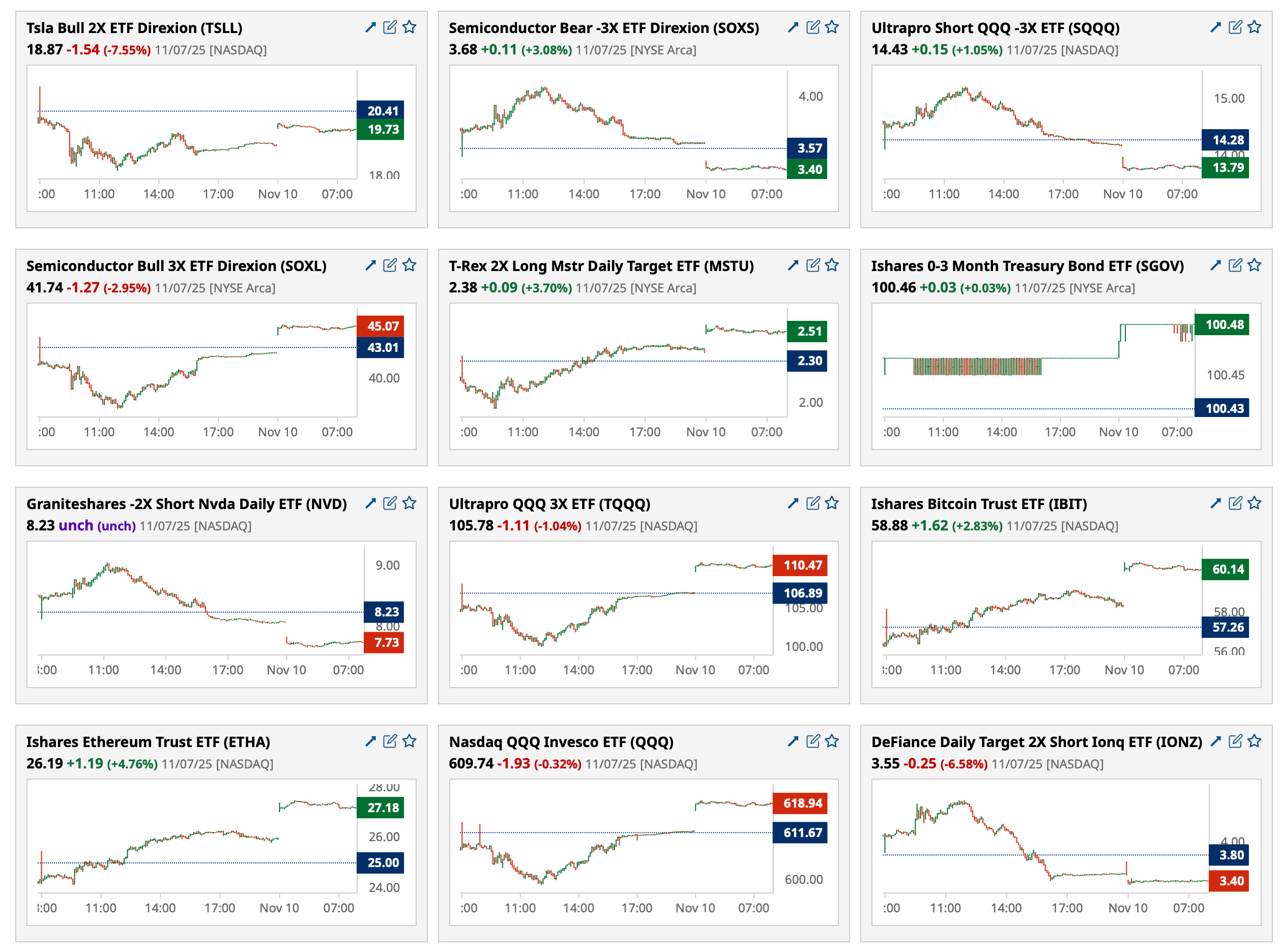

Chart from 10:19 a.m. ET:

BY Doug Kass · Nov 10, 2025, 10:45 AM EST

STAFF

Bret Jensen

3 minutes ago

Miami Madness daily data point dept.

Dezer Development has closed on a $630 million construction loan for Bentley Residences, the world’s first Bentley-branded residential tower under construction in Sunny Isles Beach. The financing, issued by Madison Realty Capital and arranged by Berkadia South Florida, represents the largest construction loan in South Florida so far this year. Designed by Sieger Suarez Architects in collaboration with Bentley Motors, the 61-story oceanfront tower is already more than 50% sold, with remaining units starting at $5.8 million and penthouses priced at $37.5 million each.

BY Doug Kass · Nov 10, 2025, 10:20 AM EST

* Over the weekend...

Sadly, it dawned on me that the next step in our economic doom loop may be some attempt by the Fed to print money once again via QE and with some sort of TARP-like facility that hoovers up AI-related debt in the process, if Scammy (#2) Altman does not get his way in the interim.

This probably won’t happen under Fed Chair Powell so there is no short-term save, but the next guy, who knows. The intent of which will be to prop up the equity markets, the consequence that the pockets of the technocrats are lined at the expense of everyone else will not matter. Why? Because they cannot help themselves with these policy steps that do not work any more well than doing heroin when you have cancer to feel better. It only leads to more problems, which should be obvious by now. Maybe time for different plays in the playbook? If these guys were football coaches, they would have been out of the league long ago.

The economy could not be more K shaped, and they are already easing into a bubble when inflation is running at levels far above targeted rates, which is unprecedented and dangerous. This would only make it worse. Not to mention, populism and AI do not mix one bit. Jobs and cost of living, which includes electricity, is probably this administration’s biggest problem, as are the perceived wealth gaps between the rich and poor. This lesson should have been learned based on what just happened in NYC. They are going after the meat processors, but the AI guys get to drive power bills through the roof and get subsidies and/or their debt bought by the Fed at the same time? I do not think that one is going to fly. Especially when you run for office and represent yourself as a populist and supporter of the American working class. Even conservatives are already rebelling against this, although I may have to rethink my position on this if I am in the same boat as MTG and DeSantis (again):

Meanwhile, this ad from Meta (META) trying to convince the farmers in Iowa that their data centers are good for them is just precious. Nobody is buying this garbage. They would be better off saving the money and paying off the off balance sheet debt and doing something about the scam ads that would seemingly make up a giant hunk of their earnings given they are 10% of revenue and probably drop almost entirely to the bottom line on the margin.

Meta is earning a fortune on a deluge of fraudulent ads, documents show

Isn’t this all getting a bit out of control? Of course, look who is at the vanguard of this one. Am I crazy to think they might be aiming to do what they claim they are not doing? Last thing the world needs is unlimited genetically engineered Scammy babies. In the irony of ironies, they are headquartered in a WeWork building.

Genetically Engineered Babies Are Banned. Tech Titans Are Trying to Make One Anyway.

Then again, I am not sure what the point is, when you can just do this (although I call B.S.). Maybe Ted Williams' frozen head can be turned back into a .400 hitting robot?

Or even better, we could have MMA matches between the uploaded Conor McGregor robot versus the Preventive genetically engineered military fighter baby and ChatGPT can referee, although it may score each round 12 to 3.

It is all starting to feel a bit dystopian. A lot of folks are getting quite carried away with themselves, that is for sure.

What a world...

BY Doug Kass · Nov 10, 2025, 9:45 AM EST

BY Doug Kass · Nov 10, 2025, 9:30 AM EST

From Peter Boockvar:

I view the US government reopening as the end of a negative, not an incremental positive as it should never have closed to begin with, especially with a clean continuing resolution in hand. Also, by closing it is an insult to every single American taxpayer that works hard and has to hand money out of their paycheck to fund basic functions that should never close. My wife yesterday had to deplane after being told the flight was going to be delayed for five hours but finally made it home.

I’ve expressed our positive and long stance on oil and gas, among other commodities. I think a barrel of oil is one of the cheapest assets in the world right now. I’ll add another group we like and are long, consumer staples. These stocks have gotten absolutely obliterated but now have bond like dividend yields, cheap valuations and whose businesses should hang in if the economy slows from here because of the defensive nature of what they sell. To name a few we own Reynolds Consumer Products, Kimberly Clark (bought on this pullback), Kenvue, Pepsi, Nestle and Conagra.

The NY Fed’s Consumer Expectations survey had some good and bad with overall financial conditions softening. One year inflation expectations were 3.2% vs 3.4% in September and vs 3.2% in August and 3.1% in July. Unemployment expectations saw its third month in a row of increases. Spending growth intentions rose one tenth to 4.8% and remaining in the 4.7%-5.2% range most of this year.

Overall, “Perceptions about households’ current financial situations compared to a year ago worsened with a larger share of households reporting a worse financial situation. Year-ahead expectations about households’ financial situations also deteriorated. A larger share of households are expecting a worse financial situation, and a smaller share of households are expecting a better financial situation in one year from now.”

On to some earnings comments with on the ground view points.

From Simon Property:

“we’re still not from a sales point of view hitting on all cylinders...So, we did skew better results in the higher income oriented centers. The value oriented centers were more flat to kind of eking along. So, you didn’t see the entire portfolio.”

“Florida remains very strong. The one area that we’re seeing, and I think everybody has seen is that your Las Vegas from a tourist market is underperforming.”

“you’ve clearly had Canadians that don’t go to Las Vegas and other people that are not going at the frequency that’s happening, but no concern there, but right now it’s kind of in a trough.”

On what they are seeing with tariff management with their tenants, “some of that will be passed on to the supplier. Some of that will be eaten by the retailer, and some of that will be passed on to the consumer. So, there’s just in many cases, the inability for retailers to eat that entire tariff. So, they’re going to have to pass it on or renegotiate better vendor deals. And I still believe we still haven’t see the full impact of it.”

“I think the tariff, if I had to put an inning on it, I’d say 5 or 6, just gut feel, so it’s not scientific.”

Speaking of Vegas and the high end, from Wynn Resorts:

“Demand in the casino was healthy throughout the quarter will solid increases in both drop and handle, leading to casino revenues that were up 10%.”

“More recently, business in the fourth quarter has seen continued momentum with drop and handle both up versus the same prior period last year. We’ve also seen notable growth in RevPAR and strong retail sales.”

F1 is coming next to Vegas and “You can look at our published room rates for the event and see that we are once again pricing at a significant premium to the market. Looking further out, our group and convention business looks strong heading into 2026, on pace to grow both room nights and rate over 2025.”

“demand in Boston has remained healthy in October with both drop and handle above last year.” And, “Macau also delivered very strong results in the quarter, which were further aided by higher than normal VIP holds...The premium segment continues to lead the market in Macau.”

Also on the higher end, from Ralph Lauren:

“Our strong performance through the first half of this fiscal year also gives us confidence to take up our full year guidance once again even as we remain relatively cautious in the second half of the year due to potential consumer headwinds and general volatility.”

Its European and Asian businesses also performed well, particularly in China.

On the macro, “To date, we have not seen any meaningful changes in consumer behavior across our key consumer segments or markets. The brand remains healthy and our core consumer is resilient, especially as we continue to shift our recruiting towards more full priced, less price sensitive, higher basket sized new customers.”

“Now, from a macro perspective, as price increases take root across different sectors, we are watching closely to see how consumers will respond.”

I mentioned Friday that Camden Property Trust, a sunbelt focused multi family REIT and a stock we own, was seeing flattish rents on a blended basis y/o/y (up ,6%) but demand is absorbing the large supply. They said this on their call:

“Strong apartment demand continued through the third quarter, making 2025 one of the best in the last 25 years for apartment absorption, helping to fill up the record number of recent deliveries.”

“the summer peak leasing season was met with continuing new supply, slower job growth, and economic uncertainties that led apartment operators to focus on occupancy instead of rental increases earlier in the season than usual.”

“Apartment affordability improved during the quarter, with 33 months of wage growth exceeding rent growth. And increased affordability improves apartment residents’ ability to absorb higher rents when new apartment deliveries are leased up in 2026 and beyond. Apartments and our shares are on sale, but not for much longer.”

“Resident retention continues to be strong...Renewal offers for December and January were sent out with an average increase of 3.3%. Turnover rates across our portfolio remain 20 bps to 30 bps below last year’s levels, and move-outs attributed to home purchase were at a record low of 9.1% this quarter.”

From Airbnb:

“Nights and seats booked increased 9% y/o/y, representing a 2 point sequential acceleration from Q2, primarily due to the strength in the US.” That was in part due to Reserve Now, Pay Later.

“As we start the fourth quarter, we’re encouraged by the continued momentum. Despite more difficult y/o/y comps, we’re seeing strength in longer lead time bookings, partly driven by our Reserve Now, Pay Later offering in the US. The strength in bookings support our positive outlook for the rest of the year.”

From Affirm, and whose stock popped 12% Friday:

Business remains strong as this type of payment becomes ever more appealing to people. Gross merchandise volume (GMV) rose 42% “with about half of growth coming from direct merchant point-of-sale integrations, a third from the direct-to-consumer business led by Affirm Card, and the remainder from wallet partnerships.”

“GMV from 0% APR monthly installment loans grew 74% as the number of merchants funding 0% APR offers more than tripled to over 40,000 merchants.”

“All categories except sporting goods and outdoors grew during the quarter, with notable strength in services and travel and ticketing. The fashion and beauty category also accelerated to its highest growth rate in three years.”

“30+ day delinquencies excluding Peloton and Pay in X loans declined 4 bps y/o/y and increased 45 bps q/o/q.” As for the later, it was “primarily driven by seasonality and is consistent with prior years.”

As they do, they take great pride in their underwriting standards. “It’s very carefully constructed mathematically.” And, “our consumer is borrowing, paying us back, shopping fairly healthily, etc...I have one fun factoid for you that may serve as a proof point that I probably know what I’m talking about. So we’ve been looking at data from government employees because of the shutdown to understand what it practically means for the ecosystem and us, in particular. And we do not see any loss of repayment. In other words, the delinquencies and defaults in that group are just fine, in line with the rest of the general population, but we see a few basis points of a demand slowdown.” And they were happy with their technological capabilities in parsing out this data.

From Block and whose stock fell 8% Friday because of light margins and no raise in their guidance:

They sounded mostly sanguine about the macro. “Obviously it’s a dynamic environment and we’re paying close attention to the range of potential outcomes here...What we’ve seen so far has been strong, obviously third quarter performance had acceleration across a number of key input metrics or operating KPIs that indicate the health of our underlying ecosystems, whether it’s Square GPV or its inflows per active on the Cash App side, we saw acceleration from 2Q into 3Q.”

“We saw only isolated impacts from tariffs and sort of the de minimis tax exemption changes that appeared in our buy now, pay later business, but even with that, GMV growth remained strong at 17% or 18% on a constant currency basis in the third quarter.”

“Based on what we saw in October was relative consistency across a number of different metrics that we track, whether its average transaction sizes, borrow origination volumes, loss rates. We’re not seeing meaningful changes that indicate a change in the macro environment yet.”

From KKR on the private credit landscape that of course is a growing focus of many of us:

“it is true the industry has grown a lot, in particular direct lending. But let’s put the direct lending market in context, $1.7 trillion compares to the $145 trillion for the global fixed income market. A very small percentage so any suggestion of systemic risk seems ill-informed, and that’s before you get to the duration of capital and lack of deposit funding, low leverage, and senior secured status in the capital structure.”

“Our base view is that credit of all kinds, we’re talking both public and private, has had low default rates for a long time. And we have seen defaults across both markets tick up somewhat. But from everything we are seeing, there’s nothing alarming going on, just the beginning of a return to a more normal default environment.”

“And as in private equity, in credit we expect more dispersion across company, investment, and manager performance. When you step back, our view is that forward credit fundamentals, both liquid and private, will remain attractive. And our clients feel the same way, which is why we are having a record credit fundraising year.” I’ll add this, we know a lot of that now is from retail. Not the natural investor for what should be a long term time horizon as retail isn’t always so long term when they want their money back.

From Expedia, whose stock jumped 18% Friday:

“The market was healthy in the quarter with an acceleration in the US, and continued strength in the rest of the world. We saw longer lengths of stay and longer booking windows, both signs of a stronger consumer.”

“In the US, room nights were up high single digits, our fastest growth in over three years. Nights were up low double digits in EMEA and high teens in the rest of the world, including over 20% in Asia.”

“Overall, as we look at travel, demand for premium travel has performed well, accelerating from Q2, and then was bolstered by resilient demand at the lower end as well.”

“we saw continued momentum in October, but we are monitoring economic indicators within a dynamic macro environment.”

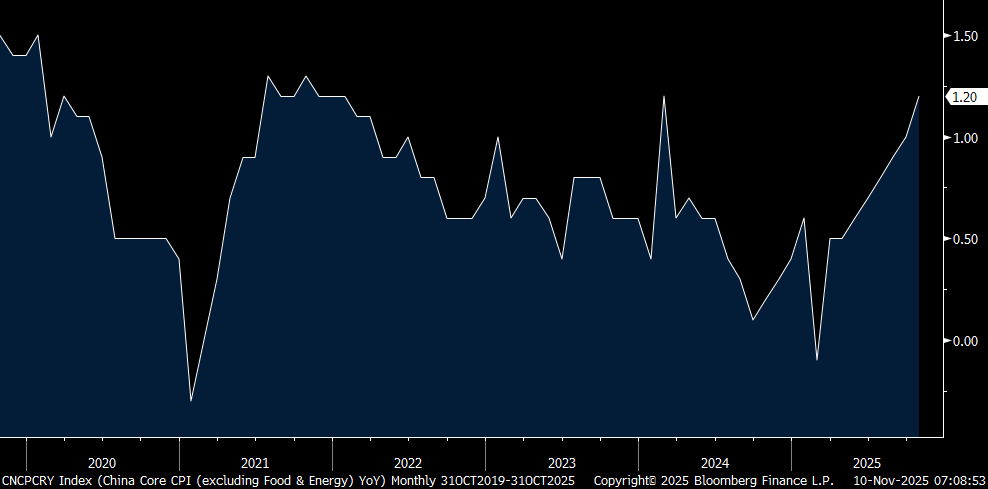

Overseas, core inflation in China in October rose 1.2% y/o/y and which happens to match the quickest since October 2021. PPI continued to fall though, down 2.1% y/o/y vs the estimate of down 2.2% with intense manufacturing competition being a main factor and why anti-involution is a key priority of the government.

Core CPI in China y/o/y

In Europe, the November Sentix investor confidence index weakened to -7.4 from -5.4 and they said “The Eurozone economy remained in a growth crisis in November...Germany also slipped back into recession...The bright spot is in Asia, Japan in particular scored with its third consecutive increase.” I’ll add, likely helped by the election. Nothing market moving here but Europe is still seeing little growth though with pockets of strength in Spain and Greece.

Finally, and of huge importance I continue to believe. The 10 yr JGB yield closed up 3 bps to 1.71%, the highest level since June 2008 as the BoJ minutes from their last meeting is opening up the possibility of a December rate increase. The 2 yr yield closed less than 1 bp from a level last seen also in June 2008. Strangely though, the yen is trading down but maybe that’s just a US government reopening unwind?

10 yr JGB Yield

I view the US government reopening as the end of a negative, not an incremental positive as it should never have closed to begin with, especially with a clean continuing resolution in hand. Also, by closing it is an insult to every single American taxpayer that works hard and has to hand money out of their paycheck to fund basic functions that should never close. My wife yesterday had to deplane after being told the flight was going to be delayed for five hours but finally made it home.

I’ve expressed our positive and long stance on oil and gas, among other commodities. I think a barrel of oil is one of the cheapest assets in the world right now. I’ll add another group we like and are long, consumer staples. These stocks have gotten absolutely obliterated but now have bond like dividend yields, cheap valuations and whose businesses should hang in if the economy slows from here because of the defensive nature of what they sell. To name a few we own Reynolds Consumer Products, Kimberly Clark (bought on this pullback), Kenvue, Pepsi, Nestle and Conagra.

The NY Fed’s Consumer Expectations survey had some good and bad with overall financial conditions softening. One year inflation expectations were 3.2% vs 3.4% in September and vs 3.2% in August and 3.1% in July. Unemployment expectations saw its third month in a row of increases. Spending growth intentions rose one tenth to 4.8% and remaining in the 4.7%-5.2% range most of this year.

Overall, “Perceptions about households’ current financial situations compared to a year ago worsened with a larger share of households reporting a worse financial situation. Year-ahead expectations about households’ financial situations also deteriorated. A larger share of households are expecting a worse financial situation, and a smaller share of households are expecting a better financial situation in one year from now.”

On to some earnings comments with on the ground view points.

From Simon Property:

“we’re still not from a sales point of view hitting on all cylinders...So, we did skew better results in the higher income oriented centers. The value oriented centers were more flat to kind of eking along. So, you didn’t see the entire portfolio.”

“Florida remains very strong. The one area that we’re seeing, and I think everybody has seen is that your Las Vegas from a tourist market is underperforming.”

“you’ve clearly had Canadians that don’t go to Las Vegas and other people that are not going at the frequency that’s happening, but no concern there, but right now it’s kind of in a trough.”

On what they are seeing with tariff management with their tenants, “some of that will be passed on to the supplier. Some of that will be eaten by the retailer, and some of that will be passed on to the consumer. So, there’s just in many cases, the inability for retailers to eat that entire tariff. So, they’re going to have to pass it on or renegotiate better vendor deals. And I still believe we still haven’t see the full impact of it.”

“I think the tariff, if I had to put an inning on it, I’d say 5 or 6, just gut feel, so it’s not scientific.”

Speaking of Vegas and the high end, from Wynn Resorts:

“Demand in the casino was healthy throughout the quarter will solid increases in both drop and handle, leading to casino revenues that were up 10%.”

“More recently, business in the fourth quarter has seen continued momentum with drop and handle both up versus the same prior period last year. We’ve also seen notable growth in RevPAR and strong retail sales.”

F1 is coming next to Vegas and “You can look at our published room rates for the event and see that we are once again pricing at a significant premium to the market. Looking further out, our group and convention business looks strong heading into 2026, on pace to grow both room nights and rate over 2025.”

“demand in Boston has remained healthy in October with both drop and handle above last year.” And, “Macau also delivered very strong results in the quarter, which were further aided by higher than normal VIP holds...The premium segment continues to lead the market in Macau.”

Also on the higher end, from Ralph Lauren:

“Our strong performance through the first half of this fiscal year also gives us confidence to take up our full year guidance once again even as we remain relatively cautious in the second half of the year due to potential consumer headwinds and general volatility.”

Its European and Asian businesses also performed well, particularly in China.

On the macro, “To date, we have not seen any meaningful changes in consumer behavior across our key consumer segments or markets. The brand remains healthy and our core consumer is resilient, especially as we continue to shift our recruiting towards more full priced, less price sensitive, higher basket sized new customers.”

“Now, from a macro perspective, as price increases take root across different sectors, we are watching closely to see how consumers will respond.”

I mentioned Friday that Camden Property Trust, a sunbelt focused multi family REIT and a stock we own, was seeing flattish rents on a blended basis y/o/y (up ,6%) but demand is absorbing the large supply. They said this on their call:

“Strong apartment demand continued through the third quarter, making 2025 one of the best in the last 25 years for apartment absorption, helping to fill up the record number of recent deliveries.”

“the summer peak leasing season was met with continuing new supply, slower job growth, and economic uncertainties that led apartment operators to focus on occupancy instead of rental increases earlier in the season than usual.”

“Apartment affordability improved during the quarter, with 33 months of wage growth exceeding rent growth. And increased affordability improves apartment residents’ ability to absorb higher rents when new apartment deliveries are leased up in 2026 and beyond. Apartments and our shares are on sale, but not for much longer.”

“Resident retention continues to be strong...Renewal offers for December and January were sent out with an average increase of 3.3%. Turnover rates across our portfolio remain 20 bps to 30 bps below last year’s levels, and move-outs attributed to home purchase were at a record low of 9.1% this quarter.”

From Airbnb:

“Nights and seats booked increased 9% y/o/y, representing a 2 point sequential acceleration from Q2, primarily due to the strength in the US.” That was in part due to Reserve Now, Pay Later.

“As we start the fourth quarter, we’re encouraged by the continued momentum. Despite more difficult y/o/y comps, we’re seeing strength in longer lead time bookings, partly driven by our Reserve Now, Pay Later offering in the US. The strength in bookings support our positive outlook for the rest of the year.”

From Affirm, and whose stock popped 12% Friday:

Business remains strong as this type of payment becomes ever more appealing to people. Gross merchandise volume (GMV) rose 42% “with about half of growth coming from direct merchant point-of-sale integrations, a third from the direct-to-consumer business led by Affirm Card, and the remainder from wallet partnerships.”

“GMV from 0% APR monthly installment loans grew 74% as the number of merchants funding 0% APR offers more than tripled to over 40,000 merchants.”

“All categories except sporting goods and outdoors grew during the quarter, with notable strength in services and travel and ticketing. The fashion and beauty category also accelerated to its highest growth rate in three years.”

“30+ day delinquencies excluding Peloton and Pay in X loans declined 4 bps y/o/y and increased 45 bps q/o/q.” As for the later, it was “primarily driven by seasonality and is consistent with prior years.”

As they do, they take great pride in their underwriting standards. “It’s very carefully constructed mathematically.” And, “our consumer is borrowing, paying us back, shopping fairly healthily, etc...I have one fun factoid for you that may serve as a proof point that I probably know what I’m talking about. So we’ve been looking at data from government employees because of the shutdown to understand what it practically means for the ecosystem and us, in particular. And we do not see any loss of repayment. In other words, the delinquencies and defaults in that group are just fine, in line with the rest of the general population, but we see a few basis points of a demand slowdown.” And they were happy with their technological capabilities in parsing out this data.

From Block and whose stock fell 8% Friday because of light margins and no raise in their guidance:

They sounded mostly sanguine about the macro. “Obviously it’s a dynamic environment and we’re paying close attention to the range of potential outcomes here...What we’ve seen so far has been strong, obviously third quarter performance had acceleration across a number of key input metrics or operating KPIs that indicate the health of our underlying ecosystems, whether it’s Square GPV or its inflows per active on the Cash App side, we saw acceleration from 2Q into 3Q.”

“We saw only isolated impacts from tariffs and sort of the de minimis tax exemption changes that appeared in our buy now, pay later business, but even with that, GMV growth remained strong at 17% or 18% on a constant currency basis in the third quarter.”

“Based on what we saw in October was relative consistency across a number of different metrics that we track, whether its average transaction sizes, borrow origination volumes, loss rates. We’re not seeing meaningful changes that indicate a change in the macro environment yet.”

From KKR on the private credit landscape that of course is a growing focus of many of us:

“it is true the industry has grown a lot, in particular direct lending. But let’s put the direct lending market in context, $1.7 trillion compares to the $145 trillion for the global fixed income market. A very small percentage so any suggestion of systemic risk seems ill-informed, and that’s before you get to the duration of capital and lack of deposit funding, low leverage, and senior secured status in the capital structure.”

“Our base view is that credit of all kinds, we’re talking both public and private, has had low default rates for a long time. And we have seen defaults across both markets tick up somewhat. But from everything we are seeing, there’s nothing alarming going on, just the beginning of a return to a more normal default environment.”

“And as in private equity, in credit we expect more dispersion across company, investment, and manager performance. When you step back, our view is that forward credit fundamentals, both liquid and private, will remain attractive. And our clients feel the same way, which is why we are having a record credit fundraising year.” I’ll add this, we know a lot of that now is from retail. Not the natural investor for what should be a long term time horizon as retail isn’t always so long term when they want their money back.

From Expedia, whose stock jumped 18% Friday:

“The market was healthy in the quarter with an acceleration in the US, and continued strength in the rest of the world. We saw longer lengths of stay and longer booking windows, both signs of a stronger consumer.”

“In the US, room nights were up high single digits, our fastest growth in over three years. Nights were up low double digits in EMEA and high teens in the rest of the world, including over 20% in Asia.”

“Overall, as we look at travel, demand for premium travel has performed well, accelerating from Q2, and then was bolstered by resilient demand at the lower end as well.”

“we saw continued momentum in October, but we are monitoring economic indicators within a dynamic macro environment.”

Overseas, core inflation in China in October rose 1.2% y/o/y and which happens to match the quickest since October 2021. PPI continued to fall though, down 2.1% y/o/y vs the estimate of down 2.2% with intense manufacturing competition being a main factor and why anti-involution is a key priority of the government.

aCore CPI in China y/o/y

In Europe, the November Sentix investor confidence index weakened to -7.4 from -5.4 and they said “The Eurozone economy remained in a growth crisis in November...Germany also slipped back into recession...The bright spot is in Asia, Japan in particular scored with its third consecutive increase.” I’ll add, likely helped by the election. Nothing market moving here but Europe is still seeing little growth though with pockets of strength in Spain and Greece.

Finally, and of huge importance I continue to believe. The 10 yr JGB yield closed up 3 bps to 1.71%, the highest level since June 2008 as the BoJ minutes from their last meeting is opening up the possibility of a December rate increase. The 2 yr yield closed less than 1 bp from a level last seen also in June 2008. Strangely though, the yen is trading down but maybe that’s just a US government reopening unwind?

10 yr JGB Yield

BY Doug Kass · Nov 10, 2025, 9:20 AM EST

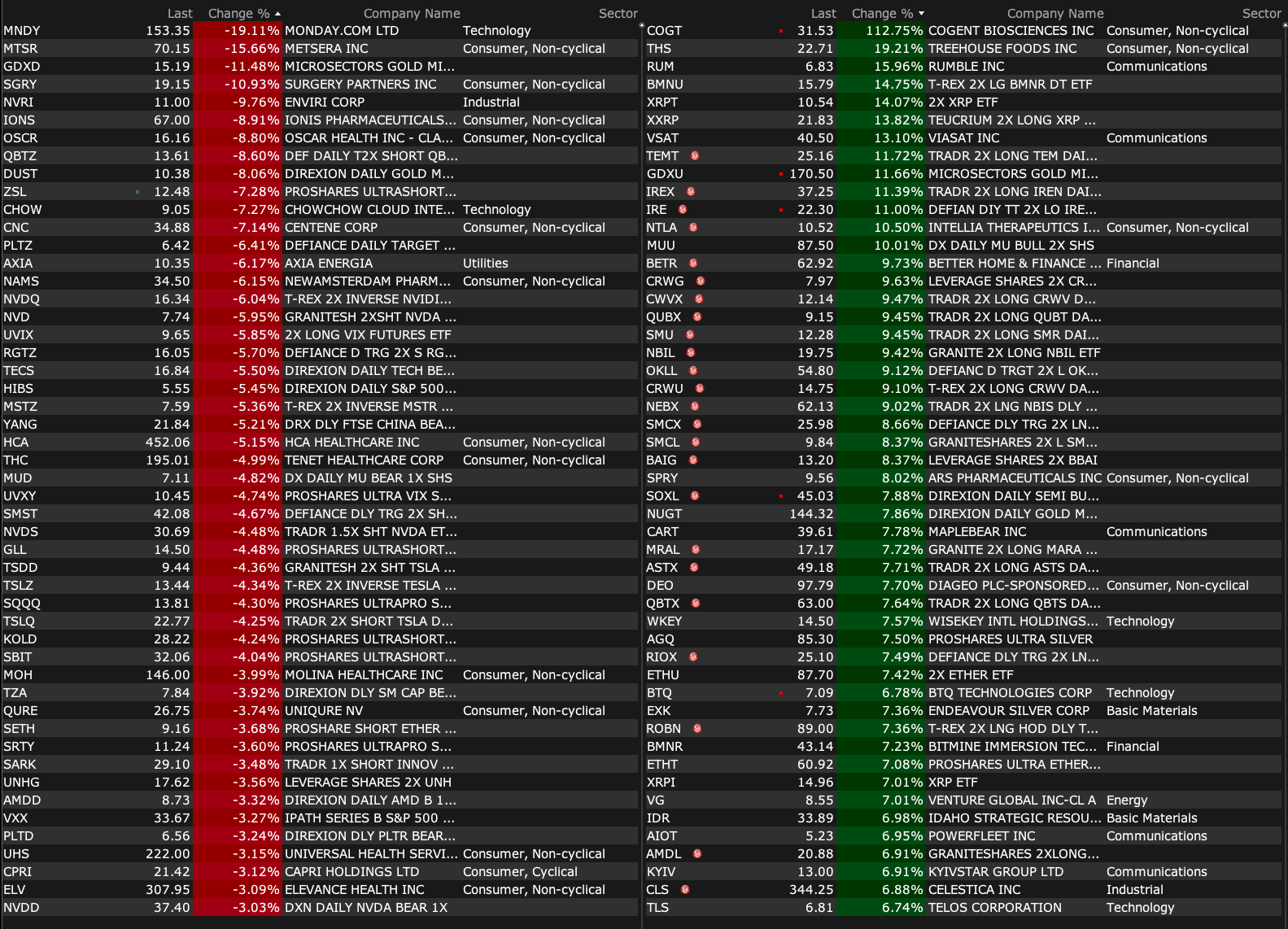

-GLTO +308% (acquires privately-held Damora Therapeutics)

-COGT +109% (reports Positive Results from Bezuclastinib PEAK Phase 3 Trial in Gastrointestinal Stromal Tumors)

-IFRX +70% (earnings)

-IRWD +27% (earnings, guidance)

-PGY +21% (earnings, guidance)

-SRFM +18% (guidance; raises $100M to advance SurfOS software and strengthen balance sheet; Equity raise includes $20M via direct offering/private placement and $6M issued to Palantir for software access and AI integration)

-VFF +18% (earnings)

-VSAT +16% (earnings, guidance)

-RUM +15% (earnings; confirms to acquire AI Infrastructure Company Northern Data; Tether puts in Initial Commitment of up to $150M of GPU Services to Fuel AI Plans)

-MGTX +14% (signs broad strategic collaboration in the area of ophthalmology with Eli Lilly and Company)

-NTLA +13% (expects topline readout from Phase 3 HAELO clinical trial by mid-2026; Presents Positive Pooled Phase 1/2 Data of Lonvoguran Ziclumeran (lonvo-z) in Patients with Hereditary Angioedema)

-PRTH +13% (Board Confirms Receipt of Preliminary, Non-Binding Take Private Proposal at $6.00-6.15/shr Cash)

-VEON +11% (earnings, guidance)

-PLUG +10% (to generate >$275M Through Monetization of Electricity Rights and Operational Efficiencies)

-EVGO +8.2% (earnings, guidance)

-CART +8.0% (earnings, guidance; announces $1.5B expansion of share repurchase program and $250M Accelerated Buyback Plan)

-BMNR +7.7% (crypto and cash holdings reach $13.2B)

-CRSP +5.2% (earnings)

-MP +5.1% (Deutsche Bank Raised MP to Buy from Hold, price target: $71)

-B +4.8% (earnings, guidance; increases share buyback program by $500M and raises dividend)

-TSN +4.8% (earnings, guidance)

-COIN +4.4% (to roll out new token offerings platform)

-GFS +4.2% (licenses GaN Technology from TSMC to Accelerate U.S.-Manufactured Power Portfolio for Datacenter, Industrial and Automotive Customers)

-TREE +4.2% (momentum)

-BCDA +3.8% (Henry Ford Health Enrolls Their First Patient in Phase 3 CardiAMP HF II Cell Therapy Pivotal Trial)

-BYND +3.6% (momentum)

-HHH +3.4% (earnings, guidance)

-PLTR +3.4% (SFRM equity raise includes $20M via direct offering/private placement and $6M issued to Palantir for software access and AI integration)

-BHVN +3.0% (earnings)

-TSEM +2.6% (earnings, guidance)

-DAL +2.0% (government shutdown progress)

-MNDY -19% (earnings, guidance)

-MTSR -15% (Novo Nordisk will not increase its $86.20/shr proposal to acquire Metsera, Inc.)

-CAMT -9.1% (earnings, guidance)

-OSCR -8.2% (earnings, guidance)

-CNC -7.7% (weakness following Trump funding proposal)

-MNKD -5.7% (to discontinue ICoN-1 Phase 3 clinical trial evaluating nebulized clofazimine inhalation suspension for nontuberculous mycobacterial (NTM) lung disease, following a futility determination based on medical monitoring data)

-IONS -3.5% (presents data from Phase 3 studies of Tryngolza in sHTG at the AHA meeting)

-TNYA -3.1% (US FDA placed a clinical hold on MyPEAK-1, Phase 1b/2a clinical trial evaluating TN-201 in MYBPC3-associated hypertrophic cardiomyopathy)

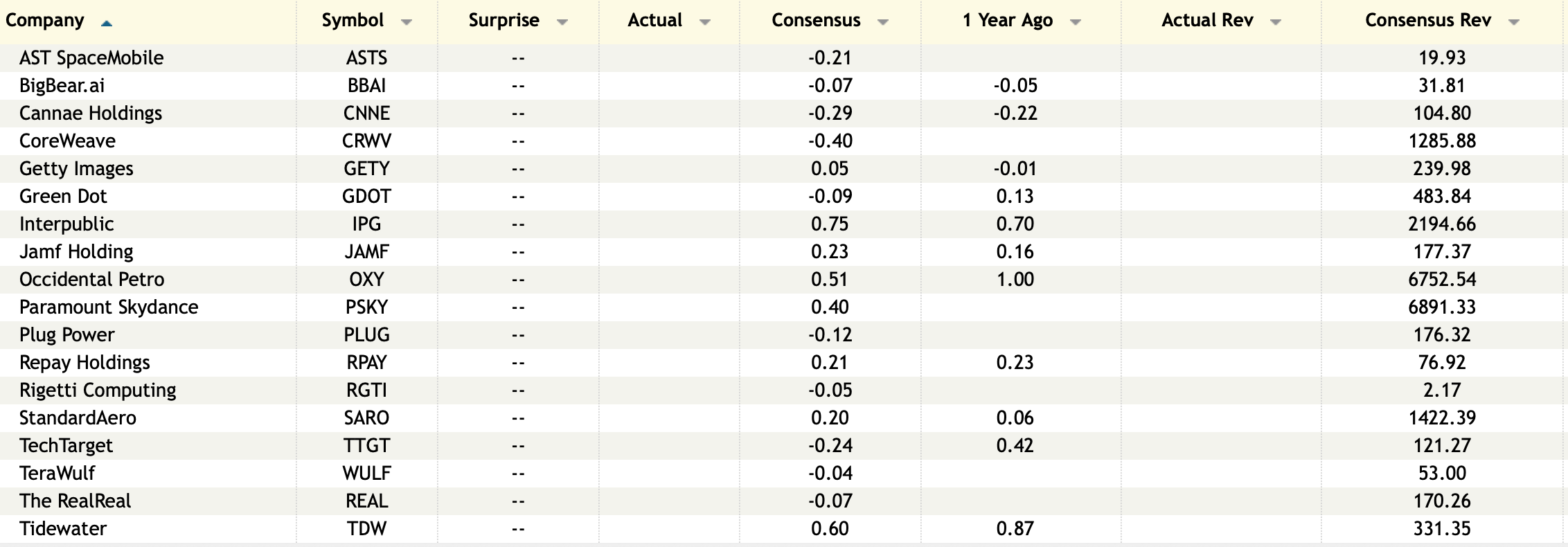

BY Doug Kass · Nov 10, 2025, 9:10 AM EST

I have been writing about AI's fallibility for one year - with over 141 issues of "More Tales From Nvidia":

BY Doug Kass · Nov 10, 2025, 8:55 AM EST

BY Doug Kass · Nov 10, 2025, 8:40 AM EST

Fed Speakers:

10:15 p.m.: FOMC Member Michael Barr (Voter) participates in a panel discussion titled "The Global Policy Dialogue: Towards the Next Decade of Transformation and New Financial Corridors" at the Singapore Fintech Festival (Audience questions expected)

Treasury Auctions

11 a.m.: Treasury Announces a 4, 8 and 17-Week Bill Auction;

11: Treasury buyback announcement (liq support);

11:30: Treasury hosts an $86B 3 and a $77B 6-Month Bill Auction;

11:30: Treasury hosts a $95B 6-Week Bill Auction;

1 p.m.: Treasury hosts a $58B 3-Year Note Auction;

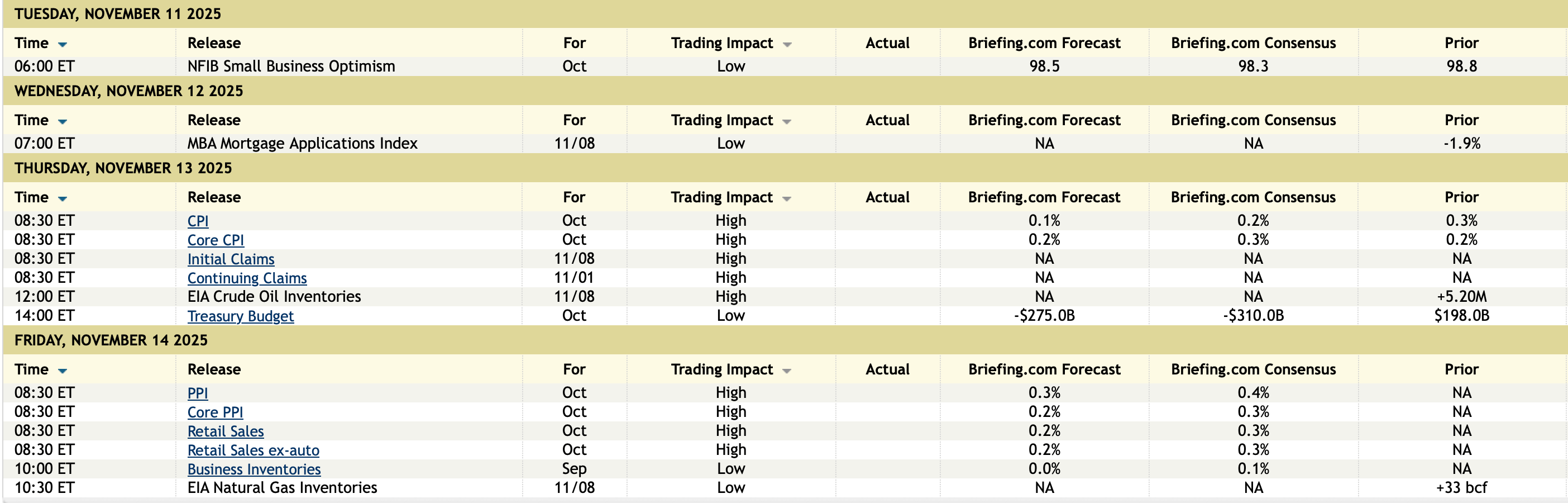

Economic Calendar:

BY Doug Kass · Nov 10, 2025, 8:25 AM EST

I have to take a family member to a doctor at 9 a.m. so I will be out of the office a bit more than I thought today.

BY Doug Kass · Nov 10, 2025, 8:05 AM EST

At 7:47 AM:

BY Doug Kass · Nov 10, 2025, 7:55 AM EST

From "El Capitan":

BY Doug Kass · Nov 10, 2025, 7:40 AM EST

From JPMorgan:

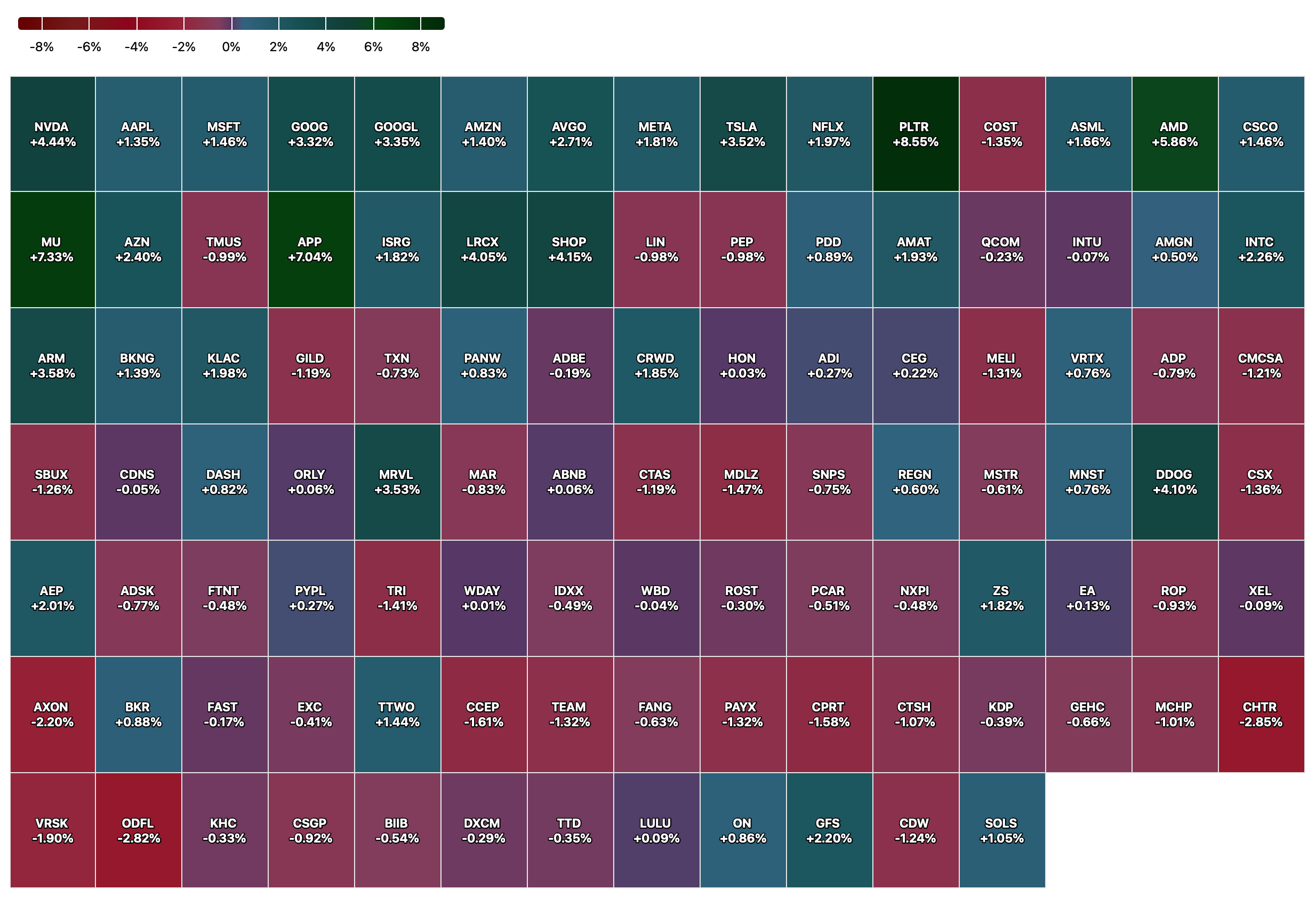

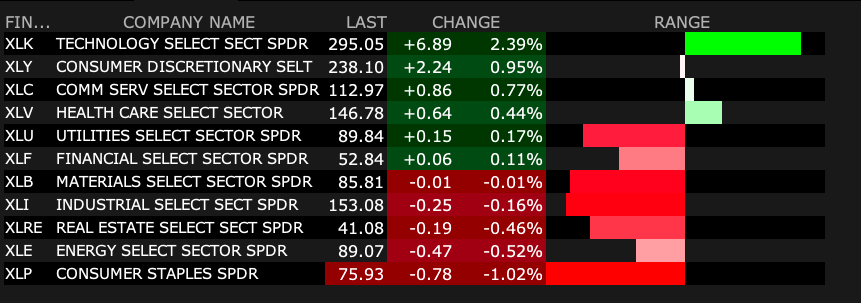

US: Futs are seeing a significant bid as the Senate advanced a bill to end the shutdown. Pre-mkt, Mag7 and Semis are the notable outperformers with AMD, AVGO, GOOG, META, MU, NVDA all up at 2% - 3.5% pre-mkt. Cyclicals are also seeing a pre-mkt bid while parts of Defensives are in the red. Bond yields are +3-4bp with USD flat. In cmdty space, the story is the strength in Ags and Precious Metals with the former seeing +1% move across much of the Ag complex and gold and silver up 2% and 3.3%, respectively, outpacing Base Metals which are also bid up. With the gov’t reopening, the market appear to be shifting its view back to fundamentals which remain strong for earnings and macro, but likely not enough for the Fed to pause/skip in December, which should benefit risk-assets.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

The SPX fell 1.6% last week, breaking a string of 3 consecutive winning weeks. Despite a strong earnings season, beats are not being rewarded (avg. beat delivers +0.3% up-day vs. ~+1.0% on average). This earnings season is coming as investors have increasing concern around valuation, cracks in the macro picture made further opaque by the government shutdown, the Fed’s reaction function given hawkish Fedspeak, and the specter of contagion emanating the biggest ‘known unknown’, the private credit market.

We are buyers of this dip and maintain our tactical bullish call. The biggest near-term catalyst would be a reopening of the government which would buttress current quarter GDP forecasts but also may release more liquidity into the market, which typically is supportive of stocks. Next, NVDA earnings can assuage concerns on the AI theme as well as supporting revenue / EPS growth outperformance this quarter. Lastly, it seems most likely that the Fed delivers another 25bps cut in Dec unless we see the labor market see an unlikely surge in hiring. Combine this with elevated buyback activity and the biggest risks come from positioning / lack of retail investor participation.

Risks: We would move away from our bullish call if we saw a combination of the following (i) NVDA earnings miss; (ii) gov’t shutdown appears to last into year-end; (iii) uncertainty leads to lower than expected buyback execution; and / or (iv) a spike to bond vol / bond yields.

· MONETIZATION MENU – we have no changes WoW but would flag Financials and Transports parts of the Cyclical trade especially if we get a stronger than expected NFIB and ADP reports.

· OLD MONETIZATION MENU (Nov 3) – We like MegaCap Tech and Cyclicals plays but think it makes sense to have a bias towards large-cap plays irrespective of sector. We may see a rise in rates, especially if the market consensus on macro / labor markets is one of increased growth / hiring albeit with inflation remaining sticky. Further, this would reduce the probability of a December rate cut, further pressuring yields higher. If so, this would tend to favor large-caps over small-caps.

· OLDER MONETIZATION MENU (Oct 27) – We return to our Monetization Menu from earlier this month (Oct 6). Mag7 earnings set the stage for another leg higher with the Fed rate cut expectations also aiding small-caps and higher beta plays. As USD continues to strengthen, this may allow US markets to close the performance gap to RoW, if so, it seems likely that MegaCap Tech is what leads the indices.

BY Doug Kass · Nov 10, 2025, 7:30 AM EST

This post was originally made in the late morning on Friday:

I was growing more interested in a trading long over the last few days because I expected resolution of the government shutdown — as I expressed here:

Here is my Ludacris Forecast:

In short order, President Trump okays negotiations in Washington to avert a continued government shutdown.

Stay tuned.

Position: None

By Doug Kass Nov 6, 2025 11:53 AM EST

The post above was brilliant, but my execution was horrible:

Now that it is out, I want to resume shorting on strength!

Position: None

By Doug Kass Nov 7, 2025 3:09 PM EST

BY Doug Kass · Nov 10, 2025, 7:05 AM EST

BY Doug Kass · Nov 10, 2025, 6:36 AM EST

BY Doug Kass · Nov 10, 2025, 6:26 AM EST

BY Doug Kass · Nov 10, 2025, 6:16 AM EST

I have a Board meeting between 11 AM and 1 PM.

I also have a research meeting out of the office between 2 PM and 3 PM.

BY Doug Kass · Nov 10, 2025, 6:06 AM EST

* Getting shorter...

I am selling a portion of my long indices (I hold short calls against this):

* (SPY) $677.63

* (QQQ) $619.27

BY Doug Kass · Nov 10, 2025, 5:56 AM EST

The S&P Short Range Oscillator moved to a slightly larger oversold at -1.87% vs. -1.61%.

BY Doug Kass · Nov 10, 2025, 5:45 AM EST