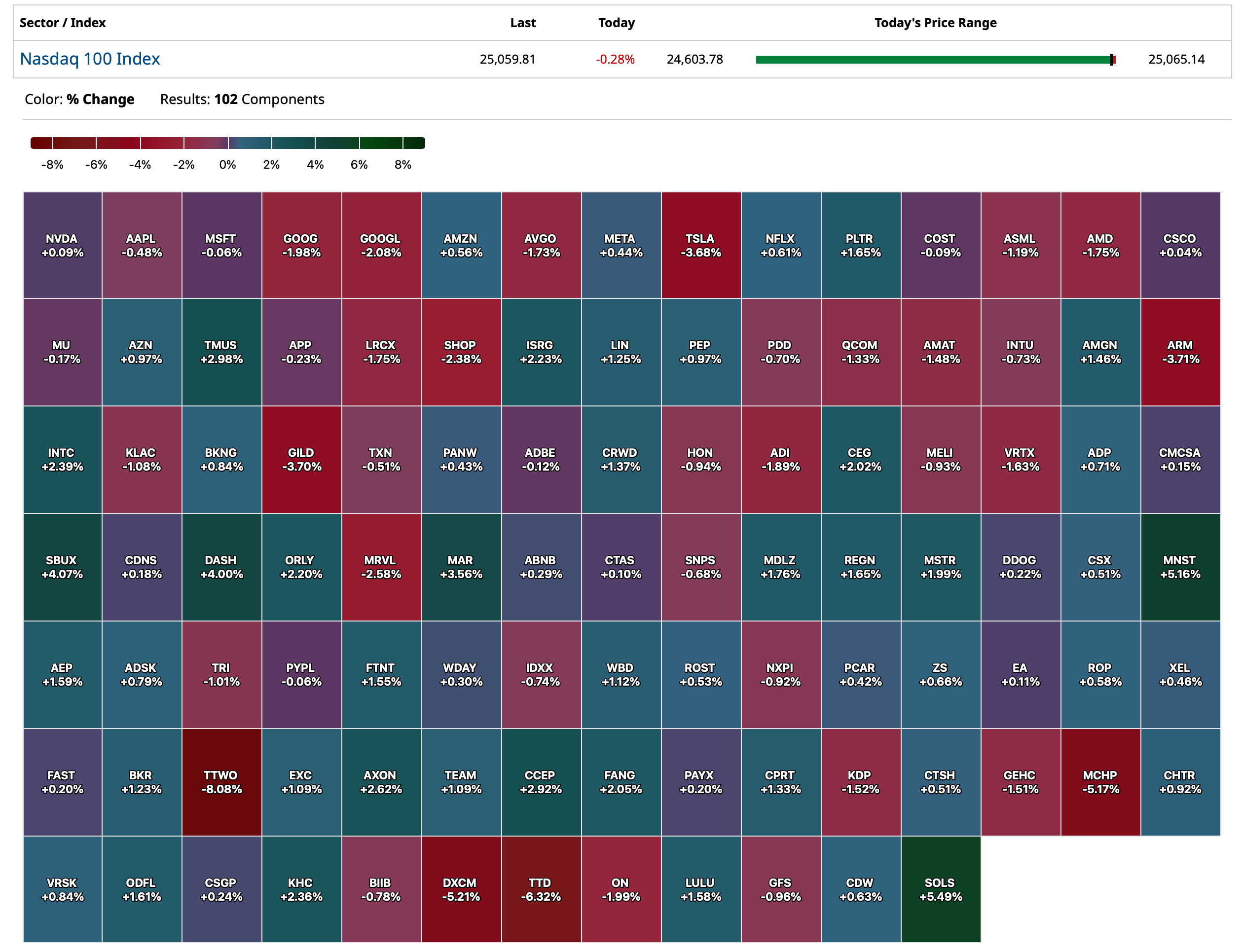

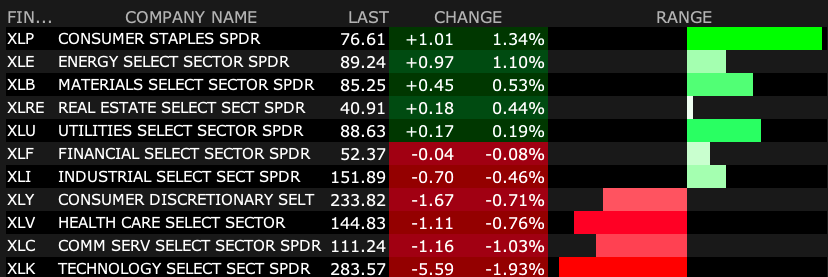

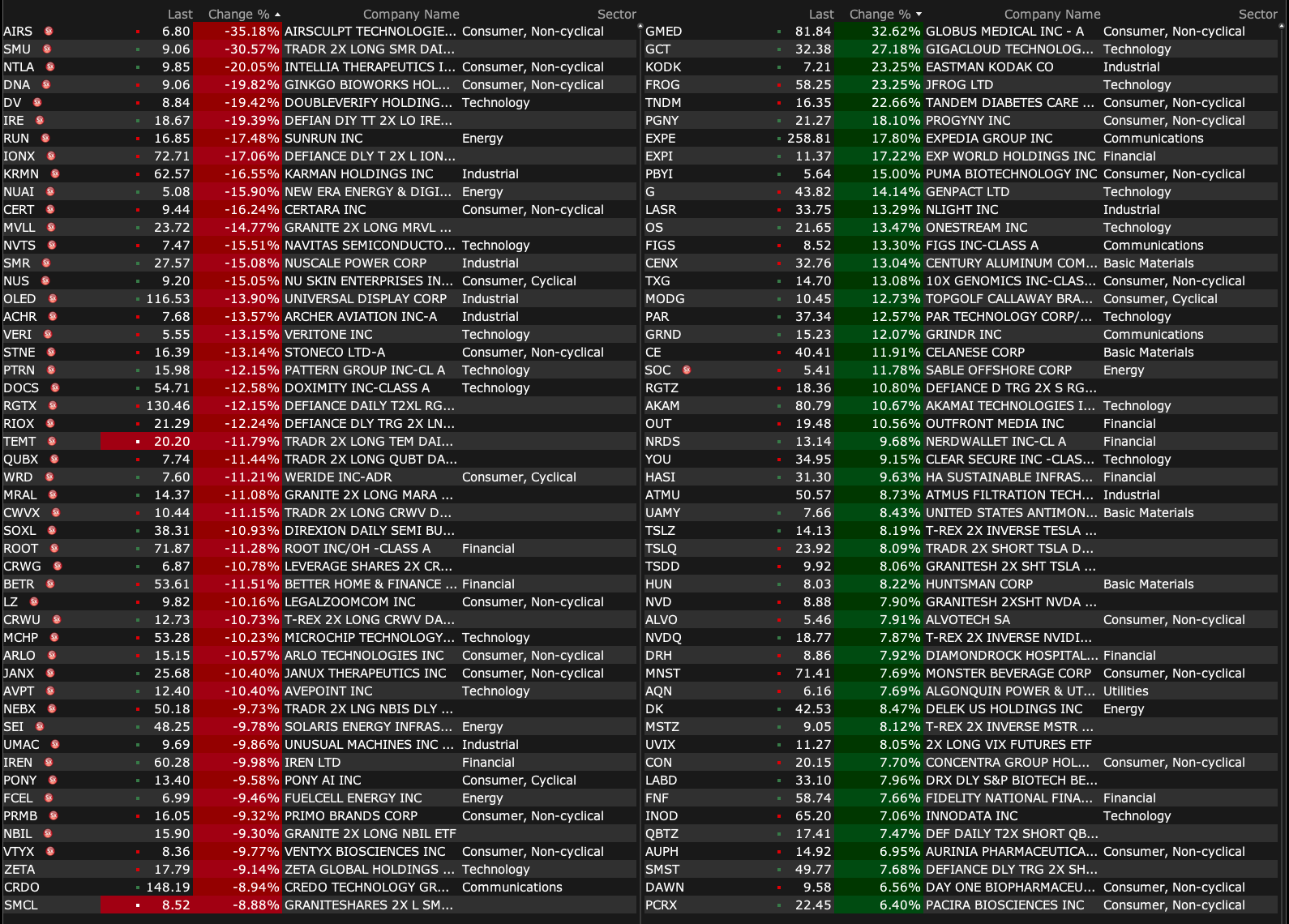

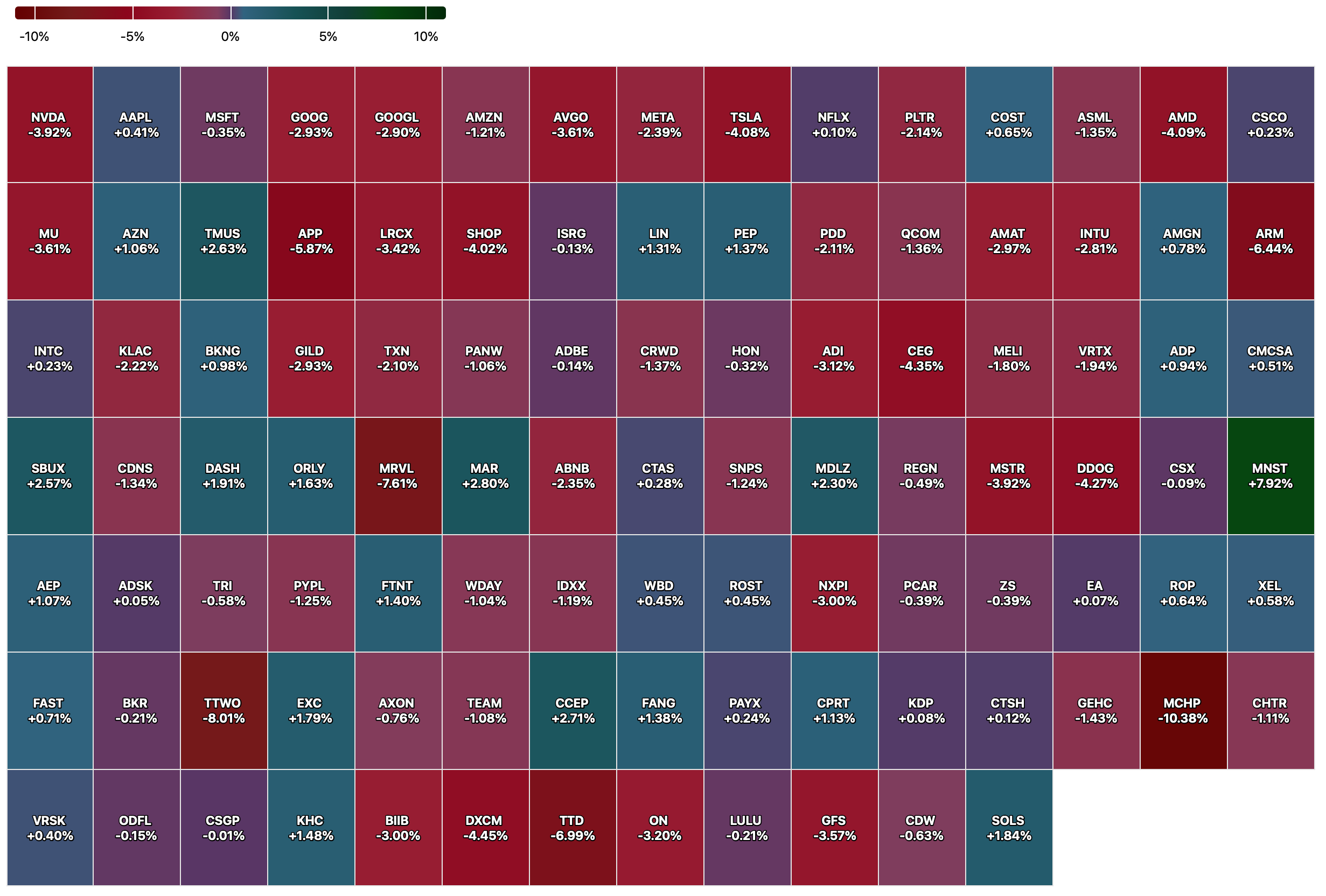

Closing S&P 500 Heat Map

BY Doug Kass · Nov 7, 2025, 4:45 PM EST

BY Doug Kass · Nov 7, 2025, 4:45 PM EST

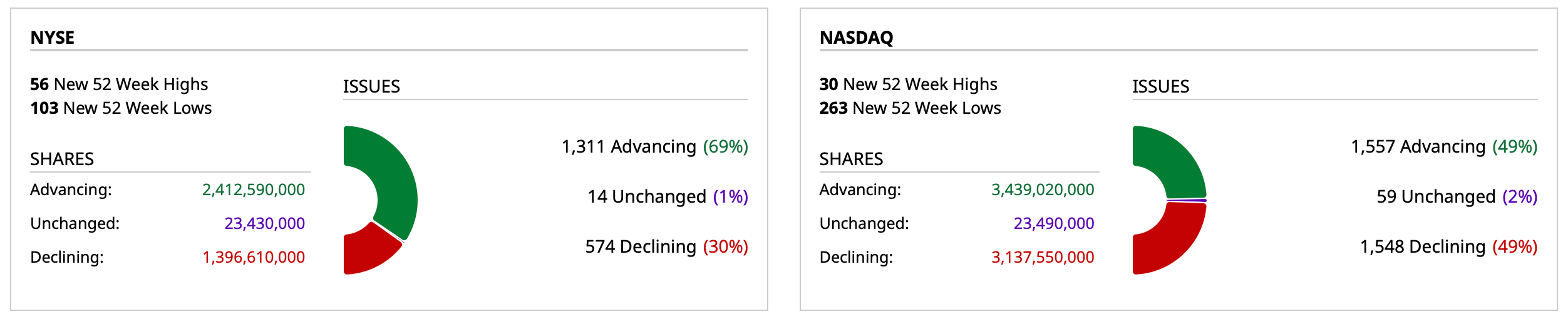

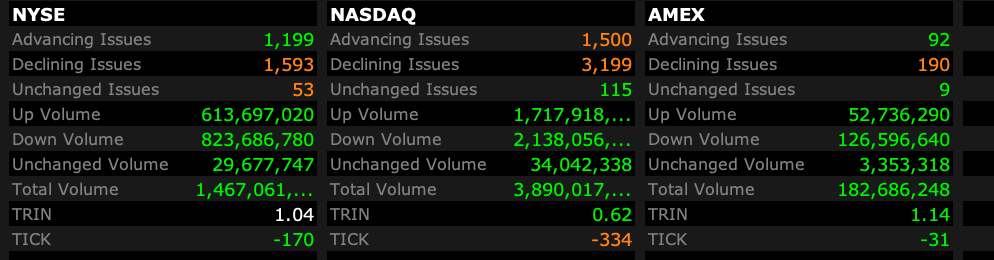

- NYSE volume 14% above its one-month average

- NASDAQ volume 6% below its one-month average

- VIX index: down 2.15% to 19.08

BY Doug Kass · Nov 7, 2025, 4:35 PM EST

I was growing more interested in a trading long over the last few days because I expected resolution of the government shutdown — as I expressed here:

Here is my Ludacris Forecast:

In short order, President Trump okays negotiations in Washington to avert a continued government shutdown.

Stay tuned.

Position: None

By Doug Kass Nov 6, 2025 11:53 AM EST

Now that it is out, I want to resume shorting on strength!

BY Doug Kass · Nov 7, 2025, 3:09 PM EST

With S&P cash down by only six handles I am adding to my index short calls.

BY Doug Kass · Nov 7, 2025, 2:49 PM EST

With S&P cash now down by only -23 handles (up +60 from the day's nadir), I am closing out my trading long rental.

Sales of index common longs:

* (SPY) $667.51

* (QQQ) $605.71

BY Doug Kass · Nov 7, 2025, 2:40 PM EST

Scott Galloway's No Mercy/No Malice: "Notes on Being a Man"

BY Doug Kass · Nov 7, 2025, 2:00 PM EST

With S&P cash halving the decline (and now down by less than -40 handles) I am selling out half of my trading long rentals on the indices — for a small profit:

* (SPY) $666

* (QQQ) $604.55

BY Doug Kass · Nov 7, 2025, 1:47 PM EST

Top chart is intraday at 1:30 p.m. Daily chart is at the bottom.

BY Doug Kass · Nov 7, 2025, 1:45 PM EST

Here is another tweet exposing Sam Altman:

This is just unreal.

At least Wall Street has the decency to wait to implode before begging for a bailout!!!!

Boy is he full of crap. The answer to his problem is simple. U.S. government buys his massively money-losing and resource-consumptive business for a penny, shuts it down, takes the tax write-off. Voila, problem solved. Granted, not really solved, as it might take the bankruptcy court years to untangle all the financial entanglements contained within this thing — might be worse than figuring out Lehman Brothers.

Post Script: As far as Altman’s contention that they have $20 billion of revenue too, how does anyone know that is true? Why would you believe it? Could be true, could be the run rate of their single best day of revenue, could be what they theoretically plan for at some point, who knows? (I surely don't.)

From Gary Marcus:

BY Doug Kass · Nov 7, 2025, 1:35 PM EST

With S&P futures -72 handles, I have added to my trading LONG rental in the indices.

BY Doug Kass · Nov 7, 2025, 1:03 PM EST

BY Doug Kass · Nov 7, 2025, 11:45 AM EST

BY Doug Kass · Nov 7, 2025, 11:30 AM EST

From Peter Boockvar:

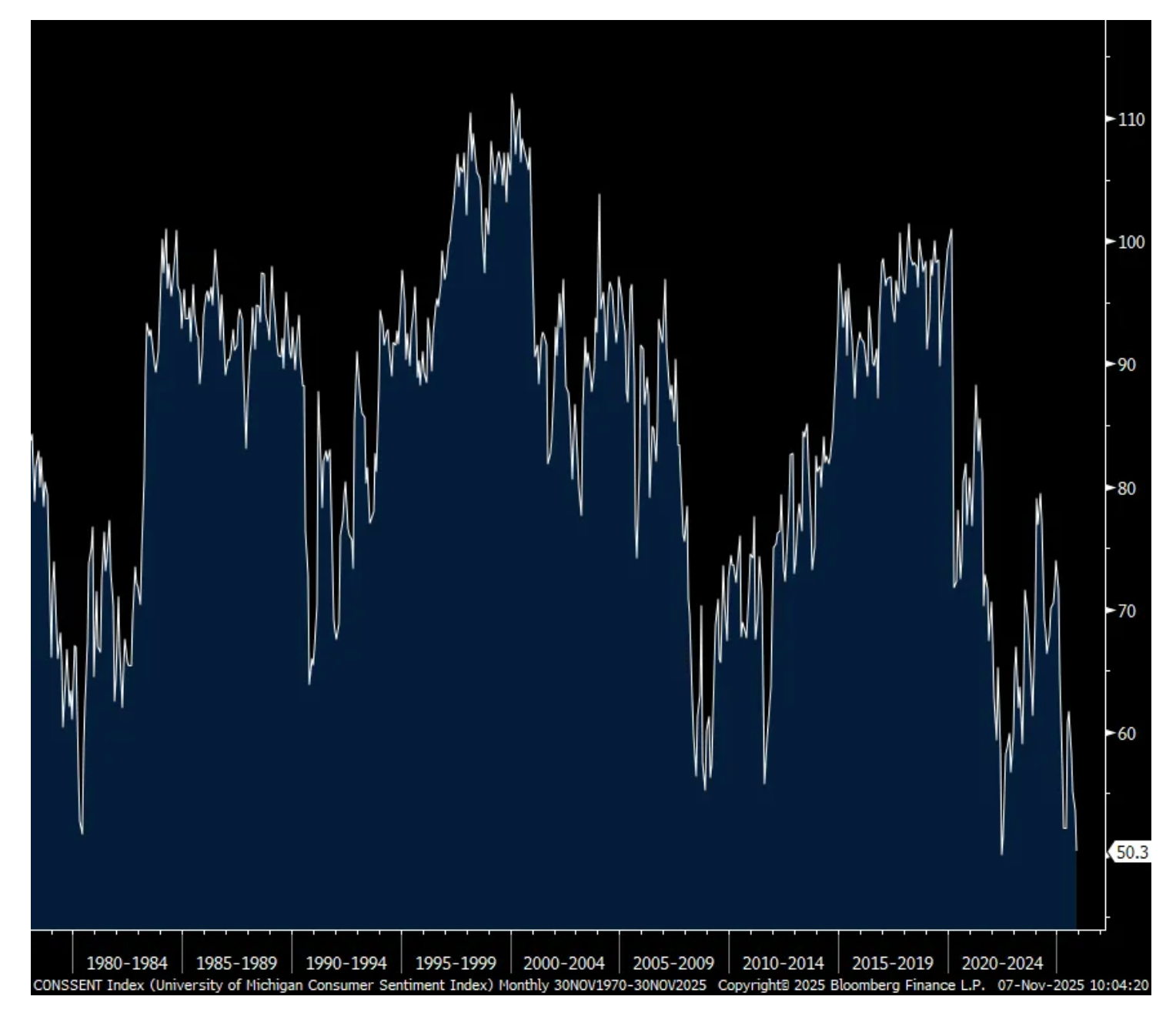

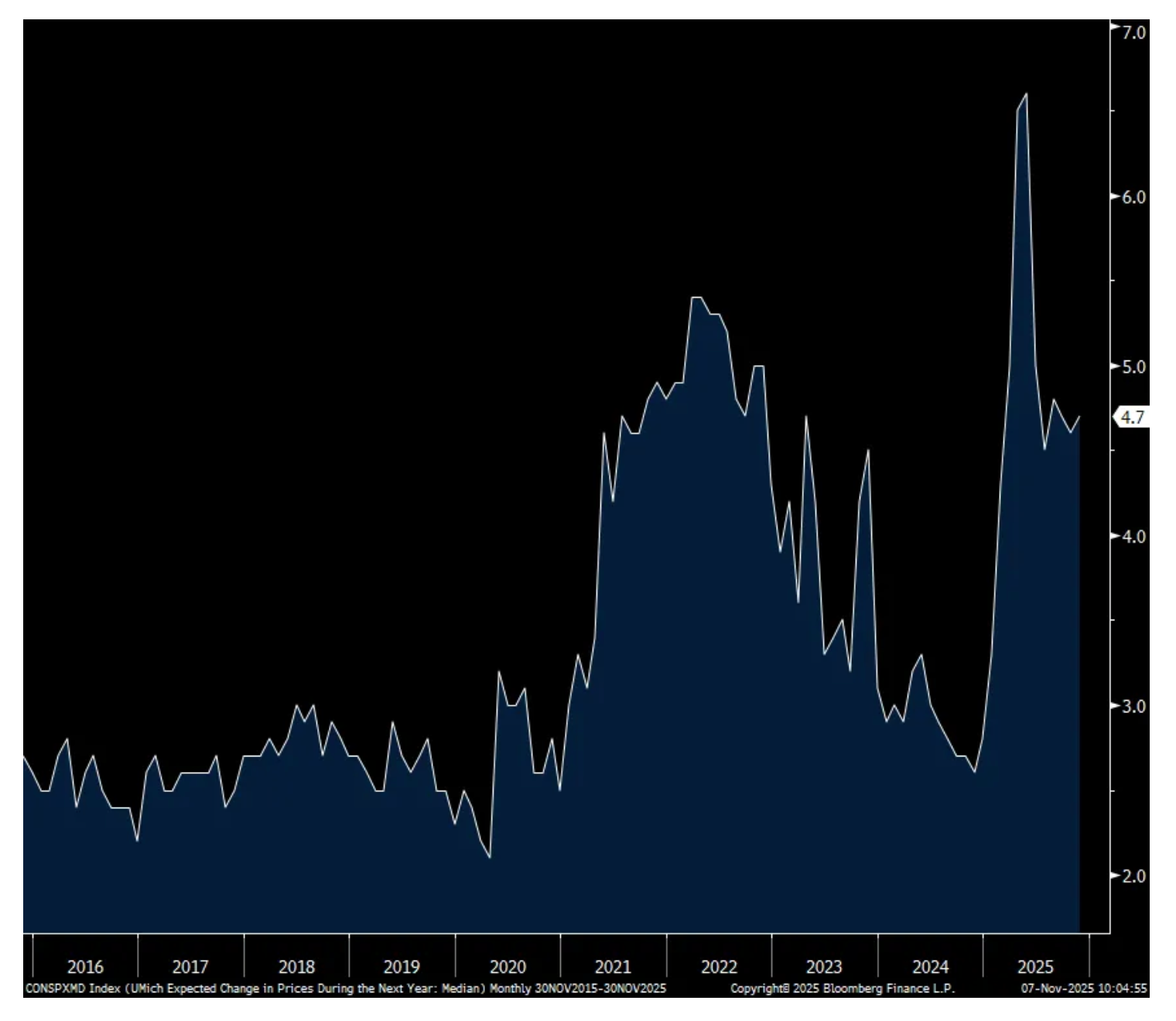

The November UoM consumer confidence index fell to just above a record low in this survey dating back to the 1970s at 50.3 (it was 50 in June 2022). That is down from 53.6 in October. One year inflation expectations ticked up by one tenth to 4.7% but the 5-10 yr guess downshifted to 3.6% from 3.9% in October and vs 3.7% in September.

Most of the decline was in the Current Conditions component which was down 6.3 pts while the Expectations side was lower by 1.3 pts m/o/m.

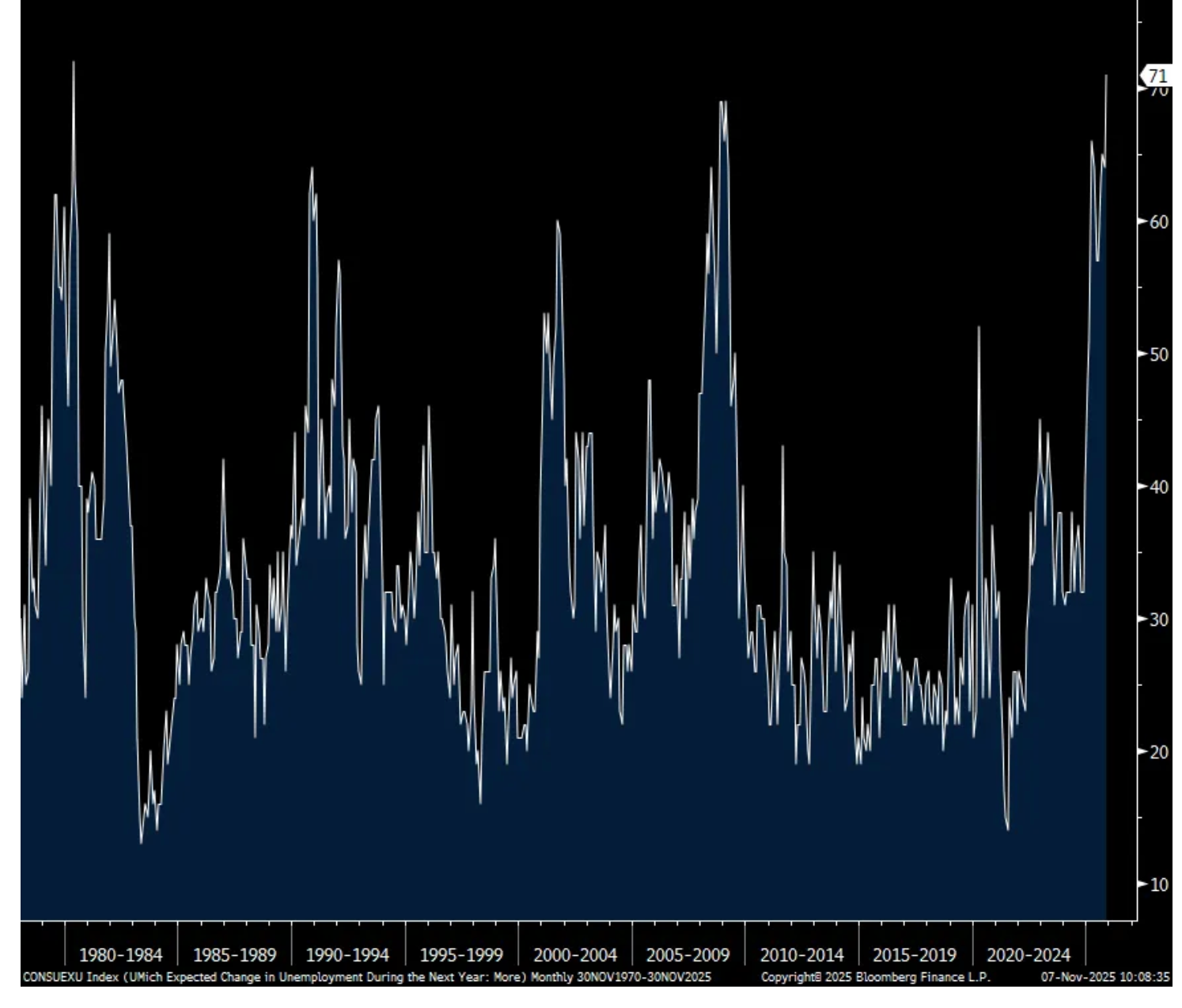

The answers to the labor market questions really weakened. Those that see ‘more' unemployment in the coming 12 months rose 7 pts to 71, the most since May 1980. The income component was down by 14 pts to -16.

Spending intentions weakened across the board. Those saying it’s a good time to buy a vehicle was down 9 pts to the lowest since June 2022, buying a home declined by 5 pts (after rebounding by 8 pts last month with lower mortgage rates) and down by 4 pts for a major appliance.

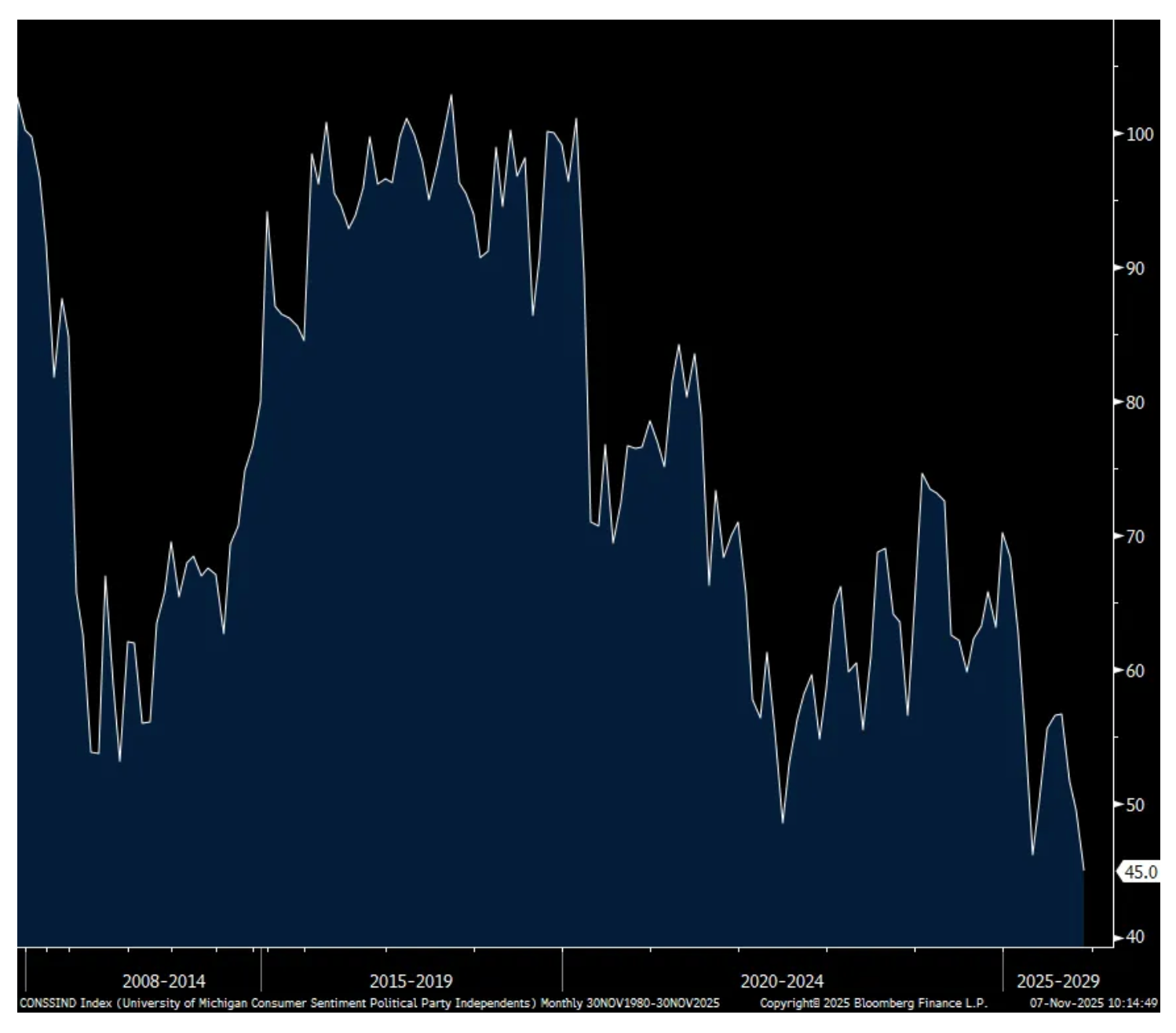

Politics of course filters in but we saw a drop for both Dems and Republicans as well as for Independents. Specifically for Independents to separate the two parties and their partisan feelings, confidence here fell 4.5 pts to 45, the lowest since the question was first asked in 1984.

The UoM said this, “With the federal government shutdown dragging on for over a month, consumers are now expressing worries about potential negative consequences for the economy. This month’s decline in sentiment was widespread throughout the population, seen across age, income, and political affiliation.”

And this, “One key exception: consumers with the largest tercile of stock holdings posted a notable 11% increase in sentiment, supported by continued strength in stock markets.”

More, “Some consumers also blamed the shutdown for recent job losses among family members or reductions in incomes. While these concerns were mentioned by a relatively small group of consumers, they are likely to escalate until the federal government re-opens.”

The biggest issue remains though, that of the high cost of living at the same time wage growth slows. “The share of consumers spontaneously mentioning the negative effects of high prices on their personal finances rose for the fifth consecutive month to 48%, up from 34% in January 2025. In addition, 29% of consumers spontaneously referenced weak incomes, surging from 20% last month and the highest seen since 2020. Taken together, consumers perceive pressure on their personal finances from multiple directions.”

Bottom line, we have a lower case ‘i’ economy (I can’t take credit for that as I heard it somewhere else) with the upper income/stock holding consumer being the dot and the lower part being the rest of the consumers that have a pretty downbeat view of their financial state.

UoM

One yr Inflation Expectations

Those that see ‘More’ Unemployment in the coming 12 months

Confidence of Political Independents

BY Doug Kass · Nov 7, 2025, 11:15 AM EST

From Charlie!

BY Doug Kass · Nov 7, 2025, 11:00 AM EST

BY Doug Kass · Nov 7, 2025, 10:45 AM EST

With SPY -52 handles I have taken a trading long rental in (SPY) and (QQQ) :

* (SPY) $664.41

* (QQQ) $603.02

BY Doug Kass · Nov 7, 2025, 10:19 AM EST

* That an AI bailout has been discussed at all, blows my mind

* The very existence of such a discussion may justify my one year criticism regarding "roundtripping," the industry's growth prospects and valuations

* Sam "Scammy" Altman is so full of it that his eyes are brown...

The federal government says there will be no bailout/backstop for OpenAI. Specifically, President Trump's AI advisor David Sacks said that "there will be no federal bailout for AI. The U.S. has at least 5 major frontier model companies. If one fails, others will take its place."

Open AI is now backpedaling, saying it was just a theoretical comment, which is baloney. This is the video, the comments were very specific and very clear:

OpenAI CFO Would Support Federal Backstop for Chip Investments

The government should not be involved in any of this. They have already been too involved with Project Stargate and other ancillary activities.

The most they should do is regulatory action designed to lower the cost of power, and allow it to be more accessible more quickly, BUT not at the general consumer’s expense. Any incremental grid and generation expense should be solely borne by the incremental customer, which is the data center. That is their cost, not mine. I do not get a share of their equity, so I should not get the expense shared into my bill.

What should happen is what I mentioned before. A barbell approach. Try to do the same thing that works 90% as well, for 10%-20% of the cost and resource consumption, like the Chinese are already doing. The companies that already exist here should be doing this too. One of them can try to be the disruptor, or private enterprise should start another business that disintermediates these guys because they are being too pigheaded with regard to their brute force kluge approach, that still does not seem to be scaling and therefore is going from bad to worse on an ROIC basis. If nobody here does it the Chinese will keep doing it.

Then, more $s should flow into a new approach that may actually have a chance of working and also be much less resource intensive. If the government wants to get involved, fund a few scientists in academic labs to do this, which does not take trillions, billions, or even hundreds of millions. I hesitate to even suggest this, but it is the lesser of two evils. Private enterprise should be throwing the dollars at trying to figure this out, as opposed to doing what they are doing just because it gooses their stock prices for the short term.

Late in the week Sam "Scammy" Altman responded to the controversy of a government bailout.

He is so full of it his eyes are brown. This tweet is lengthy, even by Bill Ackman’s standards. I am wondering if ChatGPT can summarize it for me without doubling my power bill?

This tweet from Governor DeSantis and subtweet are good too. Not sure why the sub-tweeter puts the onus on Republicans, the statement should be simply be NOBODY should support this. He also correctly describes the game they are playing to continue to try and get the support of the government “So those supporting this vile cronyism will try to use the China card, and they’ll make ridiculous analogies to the Manhattan Project, or the space race, or whatever other historically illiterate false binary they can get away with.”

The second to last paragraph of the sub-tweet is not terribly relevant or necessary, could be re-phrased to simply state there is a larger information and thinking issue with regard to all of this. Social media is engineered to provide people with dopamine hits, probably to everyone’s detriment, especially children. The technocrats know this, and don’t care. How AI is being used carries risks as well with regard to how people think, or do not think. Again, the technocrats do not care, nor do they care about their reckless financial behavior, which they are now trying to put to the public at large.

I can’t believe I missed this one from yesterday. Open AI CFO also tells us “I don’t think there’s enough exuberance about AI.” Wow.

These are also interesting:

Meta in $27 billion financing deal with Blue Owl Capital for Louisiana data center

The above company has a $150 million market capitalization, announces it will build what probably is a $100 billion AI data center. The shares are only +12% on the news, should have quadrupled:

Here is a decent summary of the whole thing:

Good luck to us all!

BY Doug Kass · Nov 7, 2025, 9:46 AM EST

From Peter Boockvar:

When I said a few times last month that OpenAI has become too big to fail I was referring to its huge presence, influence and spender and at the center of this data center ecosystem buildout. I was certainly not referring to an entity that should be getting back stopped by the US government which the CFO essentially asked for a few days ago if you did not see. Either way, it seems that the reality of the massive amount of spending that is going on and the obligations being created is settling in.

So many earnings calls to go through but chock full of information and still confirming the very split US economy to an extent I’ve never seen.

From Sweetgreen, down sharply pre-market:

Comps fell 9.5%. “Performance was impacted by softer sales trends in our Northeast and Los Angeles markets, which together represent about 60% of our comp base. This was coupled with lighter spending among younger guests, particularly the 25 to 35 year old age group, where we over indexed.”

We heard the exact same thing from Chipotle.

From Bloomin’ Brands, the owner of more upscale casual dining brands such as Fleming’s, Outback Steakhouse, Carrabba’s, and Bonefish Grill that get older crowds than Gen Z:

“Our Q3 sales comp was up 120 bps, which was 130 bps better than Q2. And US traffic was negative 10 bps, which was 190 bps better than Q2. While our focus has been primarily on Outback over the last year, all brands achieved positive comp sales growth this quarter for the first time since Q1, 2023.”

“All casual dining brands execute value offers to meet the guests where they are economically.”

“Traffic improvements and growth, they were consistent in all the brands and that was across income groups and ages. Our check averages were also up low to mid single digits across income groups and age groups, and we did see larger party sizes offset by slightly lower PPA (per person average). Maybe where we saw a little bit of slight check management was in the cohorts over 65 years old and that was predominantly in beer, wine and liquor. But importantly, what we liked is they chose to dine out based on the visitation results, which were positive. So, to me, what this tells me is it’s just another validation that dine out remains a very affordable luxury.”

From Dine Brands, the owner of IHOP and Applebee’s:

“In Q3, we sustained the sales and traffic momentum from Q2, driven by new menu innovation and targeted marketing campaigns. While we continue to operate in a competitive environment, Applebee’s and IHOP held their ground, underscoring the strength and relevance of our brands as guests continue to seek value, variety, and an exceptional dining experience.”

“While spending patterns remained relatively consistent, we’re observing slightly higher macroeconomic anxiety, leading to more intentional decision making, where every dollar spent must feel justified across the entire dining experience. Guests continue to manage their check by trading down to lower priced or value items on our menus. IHOP’s value mix remained at 19%, while Applebee’s value mix slightly increased to about 30% in Q3.”

Papa John’s missed numbers and said this:

“we are navigating weaker consumer sentiment and a more promotional QSR marketplace, particularly in North America, resulting in mixed third quarter performance.”

“As we moved through the third quarter, we saw the greatest order decline within small ticket web customers in North America. Small ticket web orders tend to over index with lower income customers corresponding with the disproportionate sales pressure we’ve seen with this cohort.”

“The majority of North America sales pressure was driven by declines in product outside of our core pizza offering, including wings, bread sides, Papadias, and Papa Bites. As consumers are pressured, they tend to control their spend by focusing on center of plate rather than adding sides and desserts.”

Live entertainment, I’ll argue again, remains a consumer priority and Madison Square Garden Entertainment, the owner of MSG, Radio City, the Beacon Theater, and the Chicago Theater, a stock we own, said this:

“We continue to see broad based strength across our business, most notably for bookings and this season of the Christmas Spectacular. And in light of the demand we’re seeing, we are increasingly confident in our ability to drive solid growth in revenue and adjusted operating income this fiscal year.”

“During the quarter, our venues welcomed over 900,000 guests across 140 events. That includes a new record for the number of concerts in any quarter at The Garden, as we hosted a number of sold out multi night runs and welcomed new headlining acts to the arena this past quarter.”

“From a consumer demand standpoint, the majority of concerts across our portfolio of venues were again sold out during the first quarter. In addition, food and beverage per caps at concerts at The Garden were up while per caps at our theaters were down compared to the prior year quarter, which we primarily attribute to the mix of events.”

With respect to the Knicks and Rangers, “the cash component of the arena license fees will be $45 million and will continue to grow at 3% each year through fiscal 2055. And while still early, we are seeing positive momentum across our share of food, beverage, and merchandise sales at Knicks and Rangers home games.”

From Tapestry, the owner of Coach and Kate Spade and whose stock fell 10% yesterday:

Coach seemed to have a strong quarter with North American growth in particular up 21% in sales. Kate Spade, not so much with sales down 9%.

“So, we’re seeing a customer who is resilient, they are being choiceful and cautious as we’ve talked about before, but they’re active around the world and where we’re delivering innovation and emotion, we are winning. And again, that’s success attracting more young consumers to the brand...Our retention rates are higher among Gen Z, but they’re also higher and growing in non-Gen Z cohorts.”

Going through the Camden Property Trust, a stock we own, earnings release and ahead of their call this morning, these are their apartment rental figures and that skews heavy in sunbelt states where most of the excess supply lives:

Q3 ‘25 Effective New Lease Rates -2.5% vs -2.1% in Q2

Q3 ‘25 Effective Renewal Rates +3.5% vs +4% in Q2

Q3 ‘25 Effective Blended Least Rates +.6% vs 1% in Q2

And occupancy was 95.5% vs 95.6% in Q2

Hyatt was up 6% yesterday because of strength in their luxury hotels:

“Our luxury brands continue to generate the highest RevPAR growth, consistent with trends that we’ve seen since the beginning of the year.”

“Business transient RevPAR was flat in the quarter, but we saw improved performance in the United States...Group RevPAR declined 4.9% in line with our expectations” and in part due to tougher comps and holiday timing.

“Corporate negotiated rate discussions are ongoing, and we expect average rates to increase in the low to mid-single digit range in 2026 compared to 2025.”

From Maersk, the giant shipping company:

They saw “strong volumes and high asset utilization as well as asset turns” but “As expected, rates softened during the period as new capacity continued to be inflated ahead of demand.”

More on volumes and this was interesting, “Despite talk of deglobalization, nearshoring, trade wars, container demand has shown a remarkable resilience over the past few years that has confounded many observers and models. During this period, China’s export growth into all regions of the world, except for North America, has not only been resilient, it has gathered pace. China’s share of global export has increased significantly and never as fast as it has over the past two years. Specifically, its global export share has increased steadily from 33% only two years ago to about 37% this year.”

“Given the widely available production capacity in China and the very competitive products that are being exported, we do not expect this trend of accelerated export growth from China to stop. The momentum is strong. The consequences for us are not only the resilience of demand growth, which will contribute to absorbing some of the new capacity coming online, but also the increased trade imbalance that it is causing, which over time will lead to higher production costs and lower asset intensity for the industry.”

From Dupont:

“Third quarter saw organic growth across all businesses with continued strong volume growth in Healthcare & Water, coupled with strength in Electronics, driven by AI technology demand in both Interconnect Solutions and Semi.”

They saw low single digit growth in Diversified Industrials and “ongoing weakness in construction end markets.”

Cummins is no longer just a stodgy truck maker, they now sell products feeding into the now insatiable demand for power.

Sales fell 2% as “Lower sales were primarily driven by weaker North America heavy and medium duty truck demand with unit volumes declining 40% from a year ago, which was largely offset by continued strength in our global power generation markets, higher light-duty truck volumes and favorable pricing.”

RXO, the freight forwarding company saw its stock plunge by 23%:

“Capacity began exiting in certain regions, driven primarily by regulatory changes in enforcement. About two thirds of RXO’s freight in the quarter came from regions where buy rates increased, and this impacted our results. Buy rates increased faster than our contractual sale rates with no meaningful corresponding increase in accretive spot opportunities.”

“While we posted another quarter of impressive double digit stock growth in the third quarter, since Labor Day, we’ve seen a weakening in demand for big and bulky goods.”

With data overseas, we saw a big jump in Chinese exports in September of 8.3% y/o/y but it slowed to a 1.1% drop in October, worse than the estimate of up 2.9%. Exports to the US continue to fall, down 25% y/o/y while rising .9% y/o/y to the EU and by 11% to Southeast Asia.

Of note too, there has been plenty of evidence that China has been stock piling crude oil and that was seen in the numbers with oil imports up 8.2% y/o/y vs 2.3% growth in September.

Thanks to semis, Taiwan’s exports in October skyrocketed by 50% y/o/y, well above the estimate of 31.5% growth. Exports to the US ballooned to 144%.

BY Doug Kass · Nov 7, 2025, 9:30 AM EST

-GIFI +50% (IES Holdings to acquire Gulf Island for $12.00/shr cash or $192M)

-GMED +30% (earnings, guidance)

-FROG +23% (earnings, guidance)

-CGC +17% (earnings)

-TNDM +15% (earnings, guidance)

-LASR +14% (earnings, guidance)

-EXPE +13% (earnings, guidance)

-TXG +13% (earnings, guidance)

-HLLY +11% (earnings, guidance)

-FLGT +8.7% (earnings, guidance)

-WEN +8.4% (earnings, guidance)

-GRND +7.9% (earnings, guidance)

-INOD +7.1% (earnings)

-AFRM +6.1% (earnings, guidance)

-PAR +6.1% (earnings)

-ABNB +5.8% (earnings, guidance)

-TASK +5.7% (earnings, guidance)

-MNST +5.5% (earnings)

-PTON +5.5% (earnings, guidance)

-AKAM +4.8% (earnings, guidance)

-ASIX +4.2% (earnings, guidance)

-FLR +3.9% (earnings, guidance)

-KKR +3.2% (earnings)

-ELDN -51% (presents Phase 2 BESTOW Trial Results for Tegoprubart for the Prevention of Rejection in Kidney Transplantation at the American Society of Nephrology’s Kidney Week 2025 Annual Meeting)

-NTLA -28% (earnings)

-FOXF -24% (earnings, guidance)

-PSIX -24% (earnings, guidance)

-AIRS -23% (earnings, guidance)

-OPEN -23% (earnings, guidance; files to offer indeterminate amount of stock)

-SG -19% (earnings, guidance)

-KRMN -17% (earnings, guidance)

-AAOI -14% (earnings, guidance)

-ACHR -14% (earnings)

-XYZ -14% (earnings, guidance)

-RUN -12% (earnings, guidance)

-CNH -11% (earnings, guidance)

-OLED -11% (earnings, guidance)

-USAR -8.9% (earnings)

-DOCS -6.8% (earnings, guidance)

-SMR -6.8% (earnings)

-DKNG -6.7% (earnings, guidance)

-MP -6.7% (earnings)

-CEG -6.1% (earnings, guidance)

-LION -5.3% (earnings)

-TTWO -4.5% (earnings, guidance)

-DV -4.2% (earnings, guidance)

-SOUN -4.0% (earnings, guidance)

BY Doug Kass · Nov 7, 2025, 9:20 AM EST

BY Doug Kass · Nov 7, 2025, 9:05 AM EST

BY Doug Kass · Nov 7, 2025, 8:50 AM EST

Fed speakers:

3 a.m.: Federal Reserve Bank of New York John Williams (Voter) gives the keynote speech before the ECB Conference on Money Markets 2025 organized by the European Central Bank, Frankfurt, Germany (Text and moderated Q&A expected. Livestream available);

7 a.m.: Fed Vice Chair Jefferson (Voter) speaks on "AI and the Economy" and participates in a moderated discussion before an Euro20+ event, Frankfurt, Germany (Text available. Q&A from moderator and audience. Webcast at https://www.euro20plus.de);

3 p.m.: Fed Board Governor Miran speaks on "Stablecoins and Monetary Policy" before the BCVC Summit 2025, Harvard, Club, NYC (Text available. Q&A from moderator.

Economic Calendar:

BY Doug Kass · Nov 7, 2025, 8:27 AM EST

BY Doug Kass · Nov 7, 2025, 6:50 AM EST

Bonus — Here are some great links:

Stocks Will Keep Making Records

BY Doug Kass · Nov 7, 2025, 6:35 AM EST

Carvana (CVNA) was one of the stocks in my speculative short package (and the only one that I had commented on in my Diary.

The shares fell by -$20 yesterday. It was the only one that I did not cover yesterday.

From last week:

I am short Carvana.

CARVANA FRAUD: THE SMOKING GUN - JustDario

This is a wild and volatile stock.

90% of retail investors should never short.

99.9% of retail investors should not short the stock.

Position: Short CVNA VS

By Doug Kass Oct 31, 2025 10:00 AM EDT

BY Doug Kass · Nov 7, 2025, 6:25 AM EST

BY Doug Kass · Nov 7, 2025, 6:15 AM EST

BY Doug Kass · Nov 7, 2025, 6:05 AM EST

Wolf Street howls about the Fed's balance sheet.

BY Doug Kass · Nov 7, 2025, 6:05 AM EST

I will be out of the office from 8 AM to 10 AM as I have to take a family member to the doctor (routine visit!).

BY Doug Kass · Nov 7, 2025, 5:55 AM EST

The S&P Short Range Indicator stands at -1.61% vs. 0.01% — that's an oversold reading.

BY Doug Kass · Nov 7, 2025, 5:45 AM EST