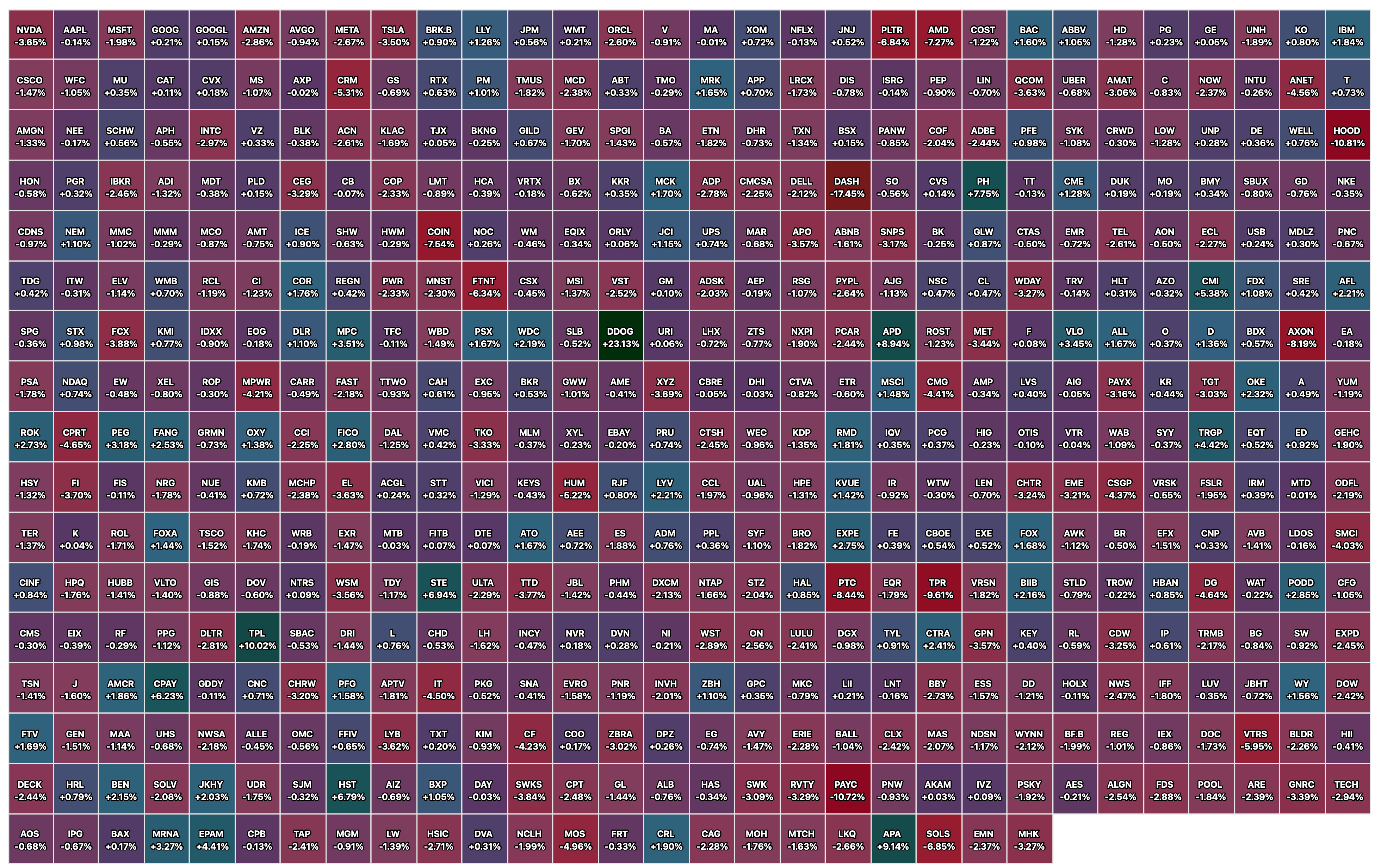

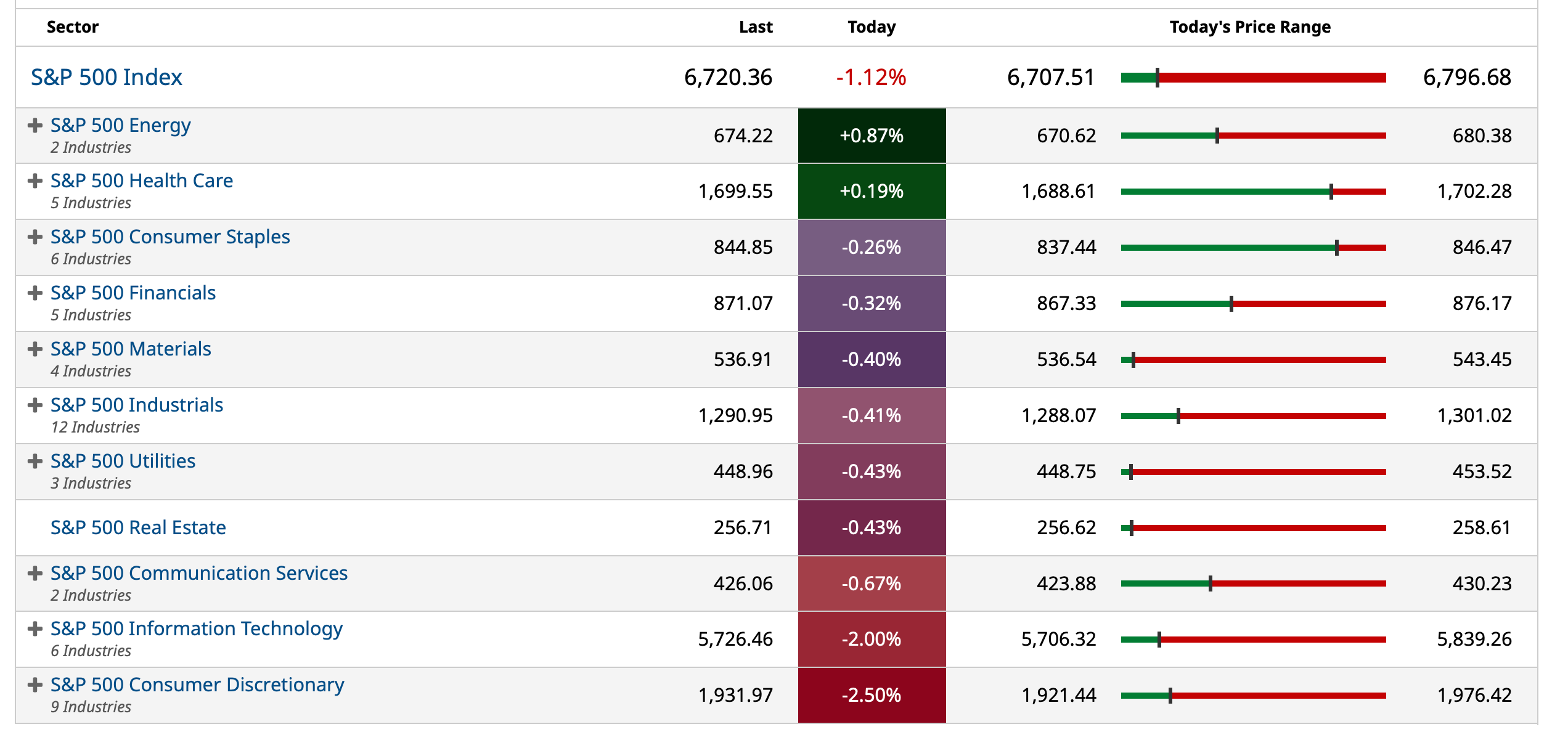

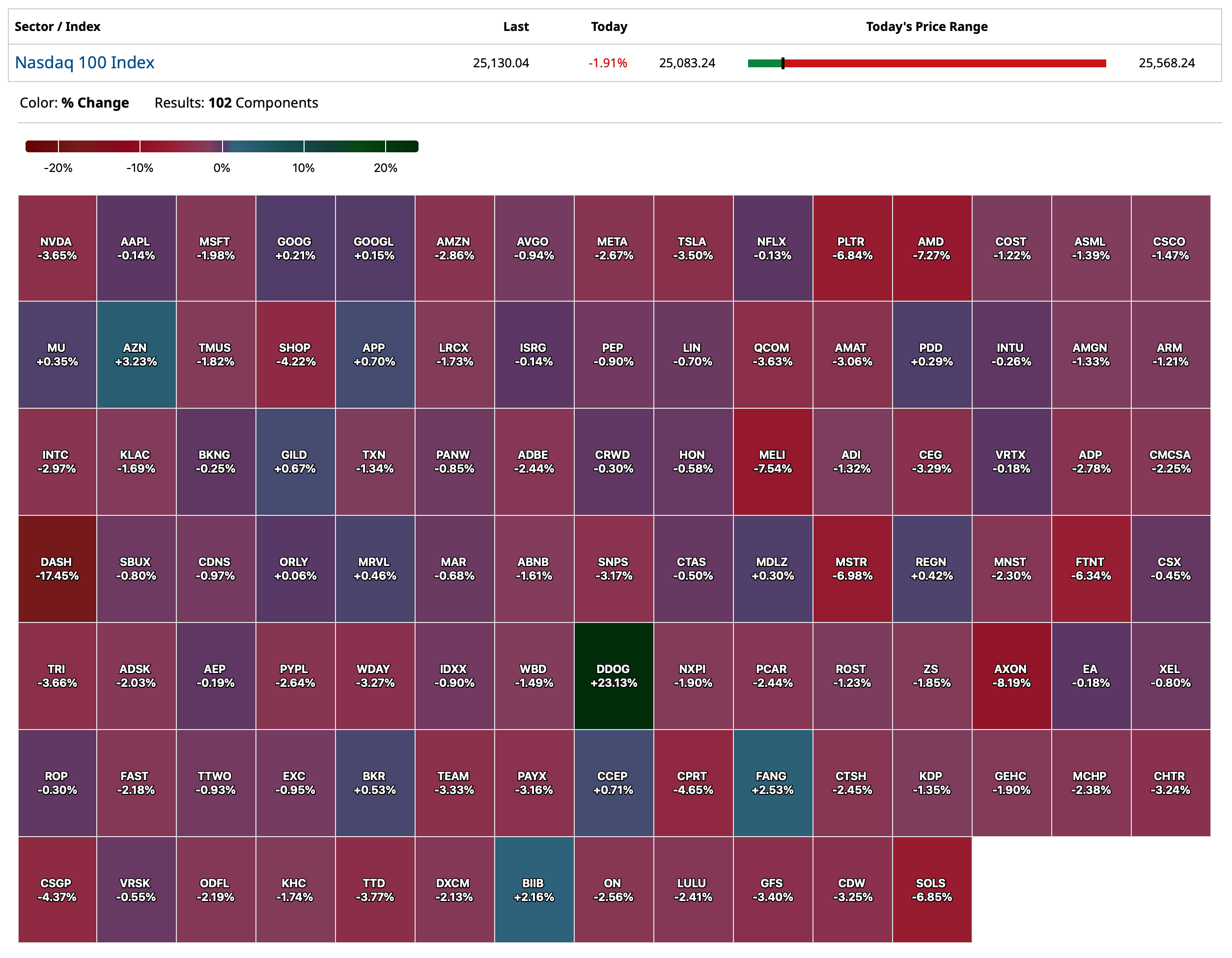

Closing S&P 500 Heat Map

BY Doug Kass · Nov 6, 2025, 5:15 PM EST

BY Doug Kass · Nov 6, 2025, 5:15 PM EST

BY Doug Kass · Nov 6, 2025, 5:08 PM EST

BY Doug Kass · Nov 6, 2025, 3:43 PM EST

Jim F

I think the market isn't focused enough on the Supreme Court ruling on tariff's. The tariffs are effectively a national sales tax. it is expected to generate $350-$400B a year in revenue for the government. So overnight you will get a huge spike in the deficit. Which is already starting at a crazy high level. this lowers our chances of paying down the debt which should in turn lower demand for duration. Which is already weak on its own. Also a $350B tax cut is inflationary which should also hurt demand for duration. maybe I just don't get it but when the government finds itself only able to issue T-Bills to anyone other than banks, Insurance companies (that they force to buy) and the Fed that's a problem.

BY Doug Kass · Nov 6, 2025, 3:20 PM EST

BY Doug Kass · Nov 6, 2025, 3:09 PM EST

BY Doug Kass · Nov 6, 2025, 1:29 PM EST

For the life of me I can't understand why anyone listens to this.

Cathie Wood cuts Bitcoin 2030 bull target by $300K as stablecoins take emerging-market role

BY Doug Kass · Nov 6, 2025, 12:55 PM EST

Dan Greenhaus and I have a strong and long-term professional relationship that is honest and founded on the exchange of differing views. (He is also a dachshund parent, which is a good thing!)

Here Dan responds to my Twitter criticism of FIN TV today:

BY Doug Kass · Nov 6, 2025, 12:41 PM EST

Howard Marks' latest commentary: Cockroaches in the Coal Mine

BY Doug Kass · Nov 6, 2025, 12:26 PM EST

In light of the magnitude of today's drop (-82 S&P handles) and given my expectation that the market could rally a bit into a possible/likely attempt by the Administration to avert a shutdown in the next few days, I have covered my (GRNY) ($25.03) short and I am currently covering my (JOET) ($41.94) short — for a loss.

I will revisit these ETF shorts on a rally — should my expectations above be met.

BY Doug Kass · Nov 6, 2025, 12:15 PM EST

Here is my Ludacris Forecast:

In short order, President Trump okays negotiations in Washington to avert a continued government shutdown.

Stay tuned.

BY Doug Kass · Nov 6, 2025, 11:53 AM EST

Last week, reflecting my acute bearishness, I shorted a package of speculative stocks. (See below).

With S&P cash -71 handles and unsteady throughout the last several trading sessions, I have just covered the package for a profit.

From last week:

Given my view of the potentially large market downside, I have shorted a package of high-octane, high-beta and speculative market leaders in the premarket this morning.

Names not divulged in order to protect the innocent (most retail investors should not short)!

Position: Short Spec

By Doug Kass Oct 30, 2025 7:20 AM EDT

BY Doug Kass · Nov 6, 2025, 11:25 AM EST

BY Doug Kass · Nov 6, 2025, 11:10 AM EST

From Peter Boockvar:

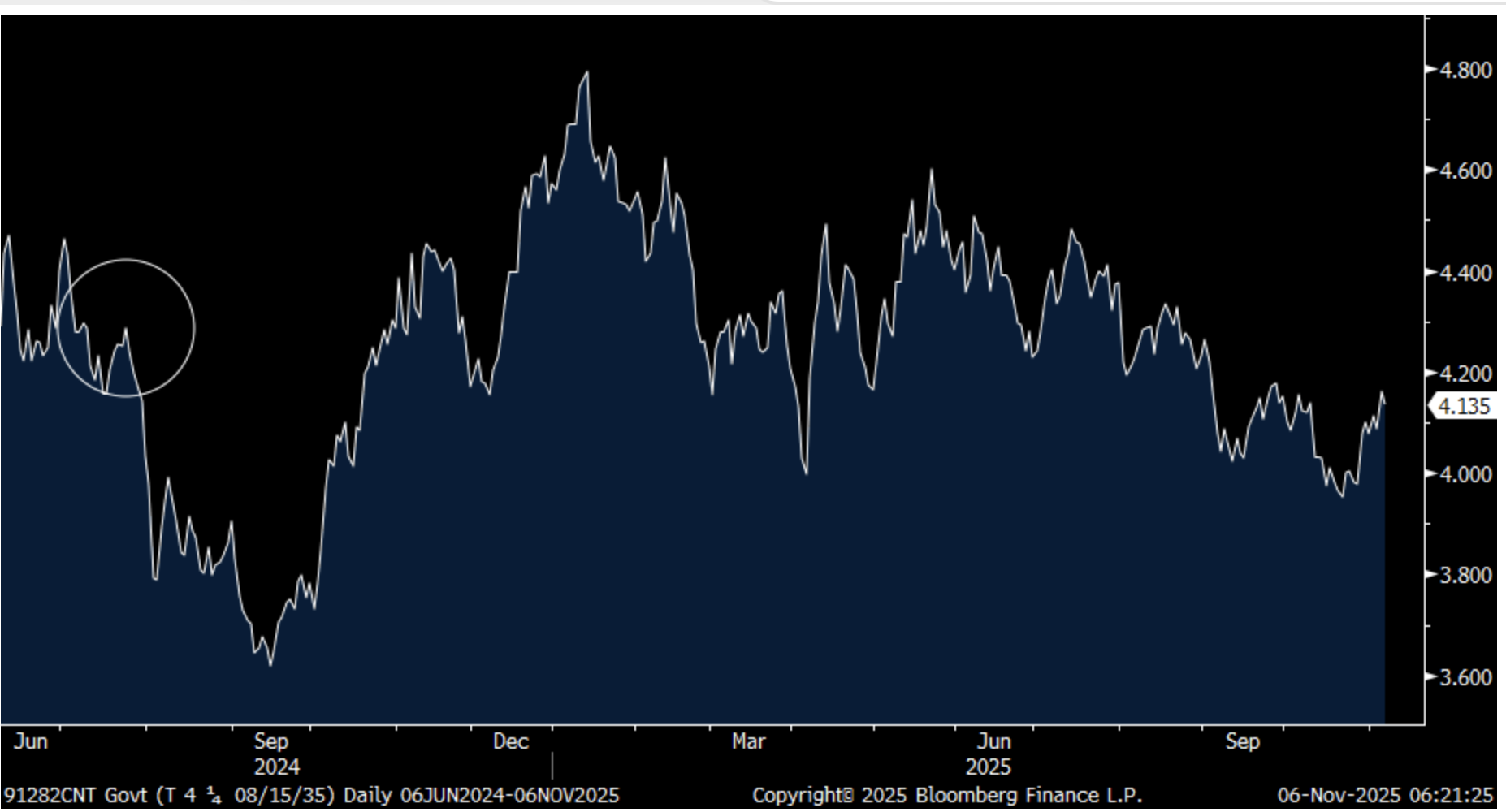

So the Federal Reserve cuts rates by 150 bps over the past 14 months and all we got was a stinking 15 bps drop in the 10 yr Treasury yield? Of course I can pick any starting point but I’ll pick July 24th 2024, because it was right before the 10 yr yield took a big leg lower into the September 2024 lows at 3.6%, see spot circled below. On that date in July the 10 yr yield was 4.29% vs today’s level of 4.14%. I still believe we’re in a bond duration bear market and long term rates are going to stay higher for a while. The Fed cuts and the calls for more are just not having the intended impact on the long end of the curve where the long end doesn’t want an easy Fed because of its distaste for inflation.

10 yr Treasury Yield

Strictly from a stock market sentiment standpoint I believe the stage is now set for a pullback because the two figures I believe have statistical significance now show extreme bullishness. I reflected Monday the off the chart Euphoric read in the weekly Citi index. Seen yesterday was the Investors Intelligence survey which already had a Bull/Bear spread above 40 but now you have the level of Bulls kissing 60 at 59.3, up from 57.7 last week. Off the lowest level since January 2018, Bears ticked up to 14.8 from 13.5. That spread of 44.5 from 44.2 last week is dangerously wide. I want to emphasize that any stock market digestion that this leads to would just be a short term reset as that is only what sentiment indicators are relevant for.

Without jobless claims today and payrolls tomorrow but after getting ADP yesterday, Challenger today said employers cut 153,074 jobs in October, up 175% y/o/y and higher by 183% from September. They said, “October’s pace of job cutting was much higher than average for the month. Some industries are correcting after the hiring boom of the pandemic, but this comes as AI adoption, softening consumer and corporate spending, and rising costs drive belt-tightening and hiring freezes. Those laid off now are finding it harder to quickly secure new roles, which could further loosen the labor market.”

With respect to hiring, Challenger said that US employers have reduced the pace by 35% y/o/y and we’re on track for the lowest year-to-date pace since 2011.

We also heard from Ian Siegel, the CEO of ZipRecruiter, last night and he said this on the labor market:

“Well, I think, as we talked about, coming into 2025 post-election, there seemed to be a really significant spike in optimism from businesses of all sizes in regards to their hiring plans. And then, as we’ve gotten into 2025 for a variety of reasons, I think the overall picture is one of more of a continued modest decline in hiring is what we have observed. There have been brief periods of stability, but the overall bend has still been one of modest decline. The projections that we gave you are based on an expectation of a continuation of the market that we are in.”

From McDonald’s whose stock traded up but slightly missed estimates and they confirm what we keep hearing:

“In the US, we continue to see a bifurcated consumer base with QSR traffic from lower income consumers declining nearly double digits in the third quarter, a trend that’s persisted for nearly two years. In contrast, QSR traffic growth among higher income consumers remains strong, increasing nearly double digits in the quarter.”

“We continue to remain cautious about the health of the consumer in the US and our top international markets and believe the pressures will continue well into 2026.”

On the cadence, “I think we saw that in the US, kind of got a little bit worse through Q3 and into the start of Q4. I’m talking about from an external perspective.”

On inflation, “we’re expecting to see there’s going to be above average inflation next year. You’ve heard others referencing what’s going on with beef prices. Certainly we’re seeing very high inflation around beef prices versus what we’re used to historically. And so I think all of that just keeps putting pressure on the industry.”

Toast has been an amazing growth story with great technology and has been taking market share, particularly from Clover who is owned by Fiserv. They have exposure to both lower and upper end restaurants with many independents and not much exposure to QSR. They said this on the consumer:

“Look, the summer was strong, Q3 was strong y/o/y. We saw in October the consumer has normalized a little bit, but really within a narrow band and in line with kind of what our expectations were. And so our customers and our restaurants are performing well.”

Elf Beauty is down 24% pre market as guidance was terrible and said this;

“Pricing and product mix added approximately 21 points to net sales growth, partially offset by a 6 percentage point impact from lower unit volumes.”

“So, from a consumption standpoint...we had about a 7% consumption rate in Q2. As we’ve gotten into Q3, we have seen that be a bit stronger, so feeling great again from a consumption standpoint.”

“I think everyone’s still worried about the American consumer. There’s so much uncertainty on inflation, on tariffs, but what I would tell you is consumers are being choosy, but they’re choosing Elf.”

As 75% of their global production comes from China, they are challenged with a 45% tariff, though down from the highs. “For context, we estimate every 10 percentage points of incremental tariffs results in a $17 million gross impact to our cost of goods sold on an annualized basis before any mitigating actions.”

From Trex which fell a whopping 31%:

“We anticipated 2025 would include some recovery in R&R (repair and remodel) spend based on historical trends. While there were indications of recovery in the second quarter and into July, consumer demand eased during the rest of the third quarter, resulting in third quarter revenues coming in 5% below the midpoint of our guidance range.”

Higher costs too did them in, “you’ve got higher labor costs, just general inflation that comes in…And then from a mix perspective, this is related to tariffs on many of the new products that we have coming in. Whether it’s aluminum or steel that’s being sourced here in the US, the prices of those products have gone up because of tariffs, or whether we’re bringing it in from overseas. So we’re not able to capture all of the revenue to offset those tariffs and the general market conditions at this point.”

Sticking to a business focused on residential real estate and commercial too, Owens Corning fell 10% yesterday. They said:

“Our financial results continue to reflect our ability to perform at a high level in challenging market conditions, as we see weakening residential trends in the US, impacting our volumes in both repaid and remodel, and new construction product lines.”

“In roofing, market demand in the quarter was impacted by a uniquely quiet storm season, with no named storms making landfall in the US in the third quarter for the first time in a decade.”

“In our doors business, volumes continue to be impacted by both slower discretionary spending in repair and remodel and weaker new construction activity, resulting in lower than expected earnings.”

With rents of course a big part of CPI and PCE, last week Avalon Bay and Equity Residential, two coastal focused apartment REITS reported.

From Avalon Bay:

“Apartment demand has been softer than anticipated this year, which we attribute mainly to the reduced job growth backdrop with related factors including higher macroeconomic uncertainty, lower consumer confidence, and a reduction in government hiring and funding.”

“softness in rental rates in August continued in September, along with a slight occupancy dip. With the further softness continuing into October, trends that are now incorporated into our updated outlook for the remainder of the year.”

They expect for the full year 2025 same store revenue growth of 2.5% with particular softness in LA and Denver, with the movie business hurting the former in terms of hiring. Blended lease rates were up .7% in October.

For Equity Residential, new leases were down 1% in Q3 while renewal rates were up 4.5%. They were more upbeat than Avalon. “Despite what is generally a mixed macroeconomic picture, we continue to see good demand and excellent resident retention across most of our markets, with results strongest in San Francisco and New York, where continuing high demand has met modest supply. We see our existing residents as having a generally stable employment situation and good wage growth.”

Their main resident is college educated with an unemployment rate of 2.7%, “considerably below the national average…We have also seen incomes rise for our new residents by 6.2% y/o/y, a healthy rate of growth. Finally, we continue to see residents react to the uncertainty in the economy and the quality of our properties and people by renewing with us at record rates.” Hence the 4.5% renewal rate.

Why new leases are down slightly, “On the new customer acquisition side, we began to see weakness in traffic during the back half of September. This was most pronounced in Washington, DC, but did manifest itself in other markets as well.”

The NY Fed’s Q3 Debt Report came out yesterday and the absolute debt levels are less relevant than what we’re seeing with delinquencies, and this is what they reflected with student loans sticking out like a sore thumb:

Category Q3 2024 Q3 2025

Mortgage Debt 1.08% 1.28%

Home Equity Line of Credit .43% 1.27%

Student Loan Debt .77% 14.26%

Auto Loan Debt 2.90% 2.99%

Credit Card Debt 7.10% 7.05%

Other 5.50% 5.35%

ALL 1.68% 3.03%

Overseas of note, the Bank of England left its base rate unchanged at 4% as expected but it was a tight vote of 5-4 with the 4 members wanting to cut by 25 bps. In the statement they state they believe that inflation has peaked and “Progress on underlying disinflation continues, supported by the still restrictive stance of monetary policy.”

Also, “The risk from greater inflation persistence has become less pronounced recently, and the risk to medium term inflation from weaker demand more apparent, such that overall the risks are now more balance.” So why didn’t they cut rates in light of this? “But more evidence is needed on both.”

With 4 members now wanting to cut, the 2 yr gilt yield is down by 2.5 bps while the pound is still up but off its morning highs vs the dollar.

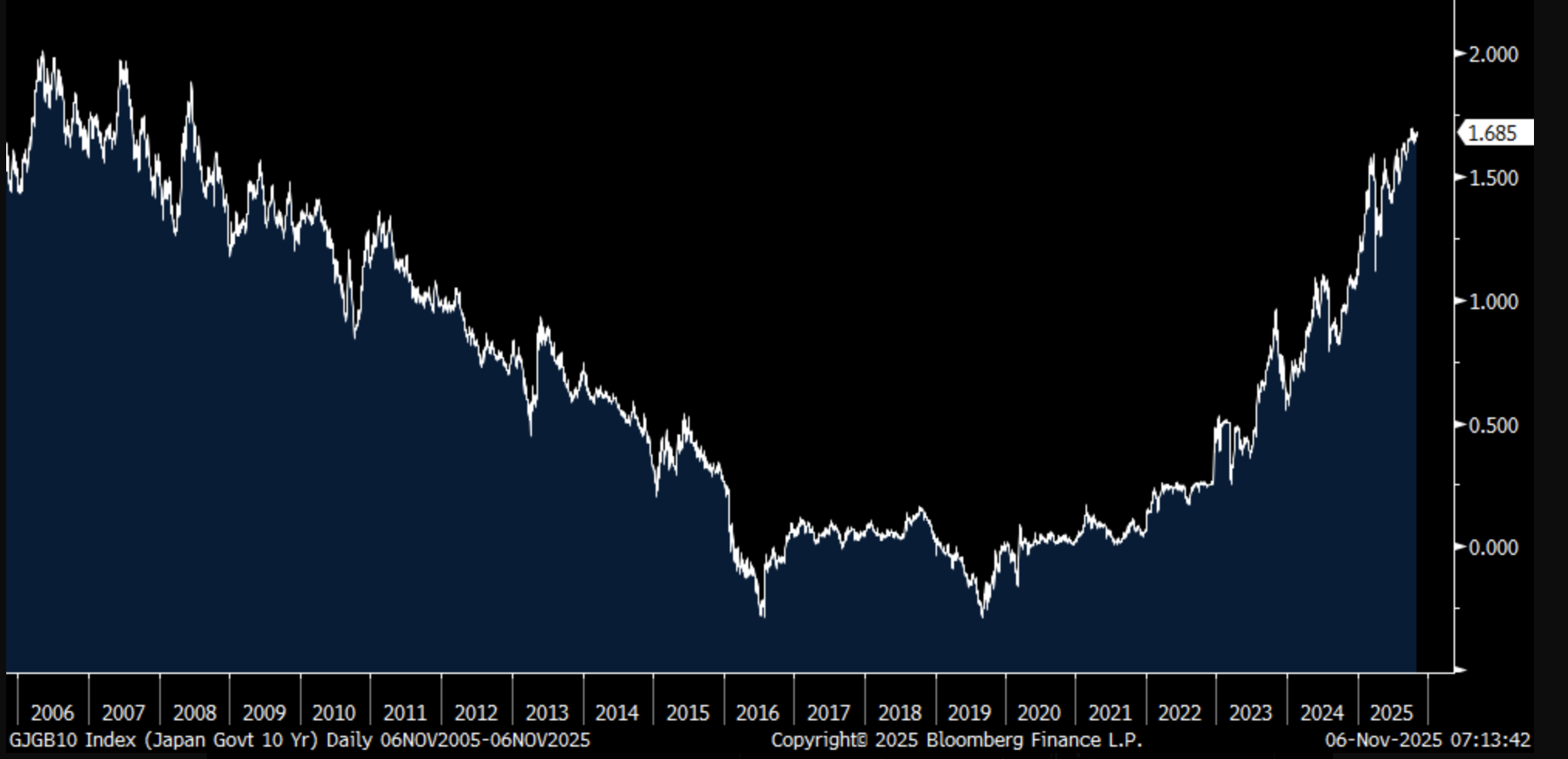

Base pay in Japan in September rose 1.9% y/o/y holding at a pretty solid level for them but still trending below the rate of inflation. The 10 yr JGB yield is just 1 bp from the highest level since July 2008 and should continue to be a focus.

JGB 10 yr Yield

BY Doug Kass · Nov 6, 2025, 10:30 AM EST

* For a small profit...

With S&P futures -1 handle (and consistent with my short-term strategy post a few minutes ago), I am calling an audible and I have covered my early morning index shorts. I am also going long the indexes against my short Index calls (and I have moved to delta adjusted neutral position):

* (SPY) $676.37

* (QQQ) $621.59

From this morning:

When I awoke at about 3:15 AM — at that time the S&P futures were -17 handles.They are now +5 handles.I am adding to my short exposure by shorting the indices:* (SPY) $678.31* (QQQ) $624.00Position: Short SPY common (VS) and calls (S), QQQ common (VS) and calls (S)

BY Doug Kass · Nov 6, 2025, 9:53 AM EST

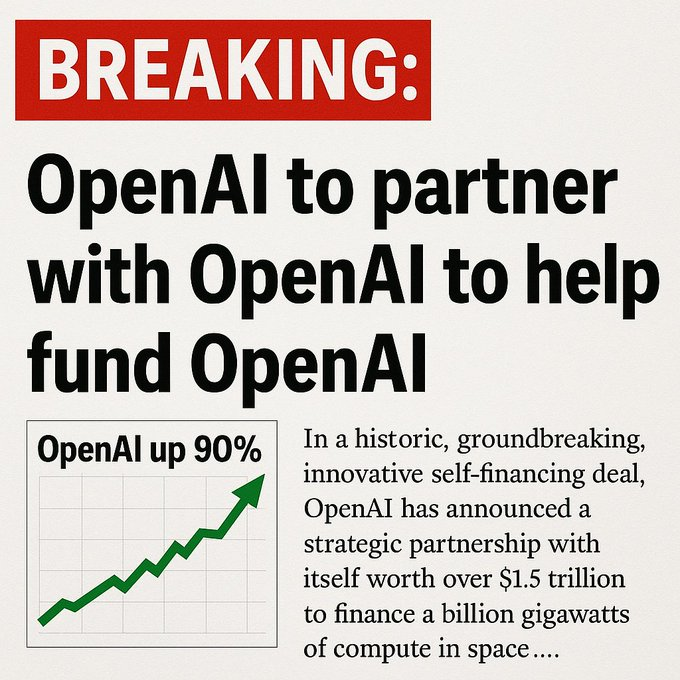

* You literally can't make this up — too big to fail has become an AI strategy.

* The worst allocator of capital in the world is the U.S. government.

* The U.S. economy is terribly dependent on the AI "bet."

* Privatizing profits but socializing losses.

As I mentioned in Monday's Is Another Sam the Next Flim-Flam Man, Florida Governor Ron DeSantis hits the nail on the head:

I guess when DeSantis tweeted this a few days ago, he probably had a sense they were all looking to get bailed out.

He is well positioned to know, and is doing his best to stop the anti-capitalistic behavior:

At the same time Scammy #2 (Sam Altman, Scammy #1 was Sam Bankman-Fried) a few days ago went bonkers when asked how OpenAI could pay for $1.4 trillion in obligations with their $13 billion in revenue and doth protested way too much. He knows the numbers and technology are not even close to working, and so does Nvidia's Jensen Huang, which is why they are begging for handouts, so they can keep the stock prices up and keep selling is my guess:

And of course, at almost the same time, as I also pointed out in Flim-Flam Man, President Donald Trump’s comments on AI were interesting. The politicians — Trump (and the whole of government) know nothing. They only know what they are told by influential donors and CEOs (who all have something to gain, I think Nvidia's Huang now must have office space in the White House), and what the stock market is suggesting with price action. Trump seemed genuinely stunned by the mere suggestion that something wasn’t right with all the AI hype, because he has not heard anything differently from anyone in his circle and he sees what the stonks are doing:

I repeat this is why the government is the worst allocator of capital in the entire world. China is probably laughing at us over this. We are mortgaging our entire economy on a technology that is grossly overhyped, and does not work, and is terribly dis-economic and resource intensive. China indirectly burned us badly during Covid, and the damage is now permanent due to the monetary and fiscal excess that has become ingrained in our economy to everyone’s detriment. The existential threat of a technology race with China is now being used with respect to AI by the technocrats that personally benefit from it, when Gen AI is in fact nothing but an economic and productivity black hole. Putting more money into generative AI, the way we are doing it, is probably exactly what China wants us to do, because the U.S. destroying capital benefits them.

Dunno how it has come to the point where Jensen Huang and Sam Altman's office, as well as a few other greedy influential donors and corporations dictate all of this. If the technology worked, and was economic, the investment side would solve for itself, without all the shenanigans. That is capitalism. What is going on now is the worst form of central planning, capital destruction, and self-serving greed. As Governor DeSantis pointed out, the profits are privatized and the losses are socialized.

These guys are all greedy sociopathic idiots in my view. Silicon Valley has become multiples worse than Wall Street. It should be renamed Exploitation Valley. At least Wall Street waits to implode before asking to be bailed out, these guys are so bad they ask to be bailed out, and their stock prices (or private valuations) propped up before they implode!

This short two minute video worth a watch.

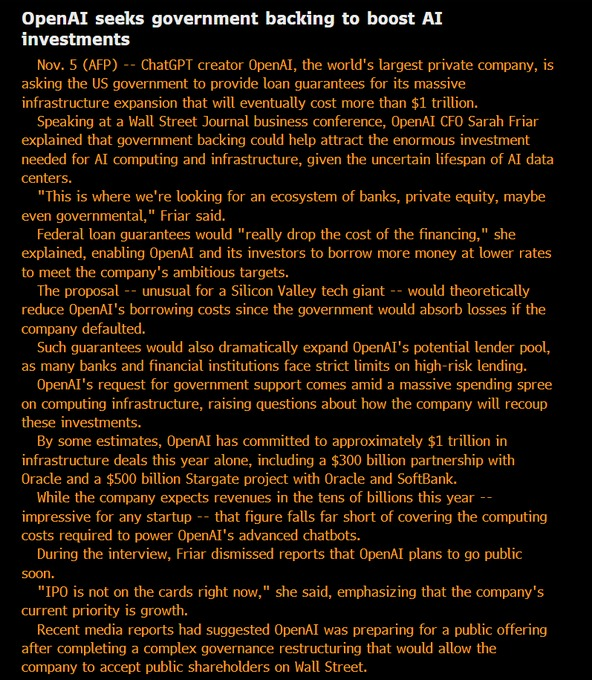

OpenAI Wants Federal Backstop for New Investments

Well, we have officially jumped the shark, and we are going to need a bigger boat. Here is the OpenAI CFO discussing a federal backstop for their new investments. While doing so, she makes the bear case for the industry:

* If they are on their way to massive amounts of profits, why would a federal backstop be necessary? Normal capital market activity should be sufficient to finance them. But I guess Open AI now wants the general public to pay their power bills, and bear the risk of their business too. Let me get this straight, they need Nvidia to finance them to buy Nvidia chips, and the federal government (ergo the taxpayer) to finance them as well? The whole thing does not work.

* And they should then personally reap all the rewards from their equity sales?

* Notice how she talks about how quickly the chips obsolete. Exactly! There is not one single depreciation schedule that is realistic. The industry is much worse than it looks. CoreWeave (CRWV) (a short) is going to be besides themselves.

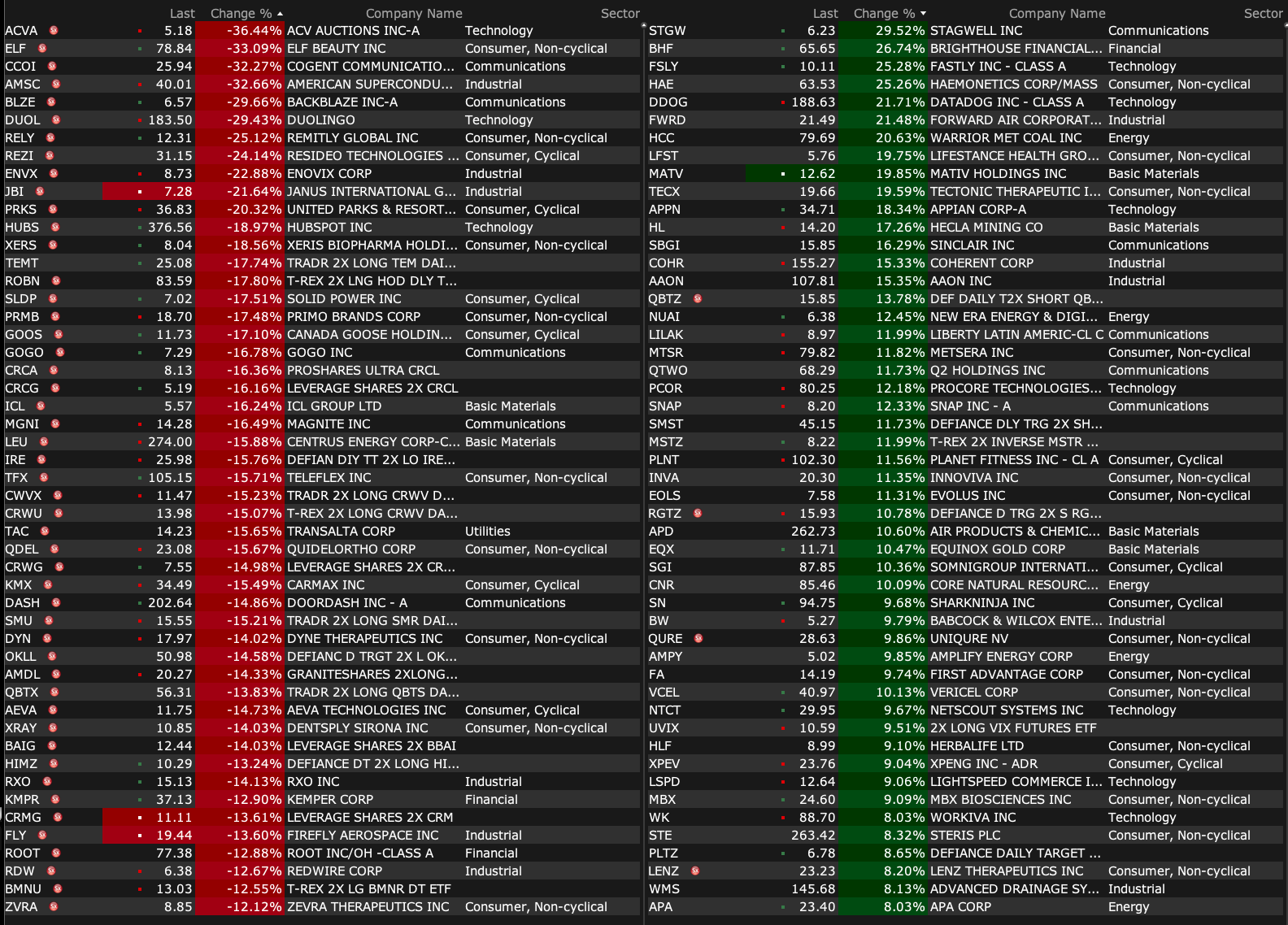

BY Doug Kass · Nov 6, 2025, 9:30 AM EST

-FRGE +67% (Charles Schwab confirms to acquire Forge Global at $45/shr)

-STGW +55% (earnings, guidance)

-GDEN +40% (earnings)

-BHF +26% (confirms to be acquired by Aquarian Capital at $70.00/shr all-cash $4.1B deal)

-ALTO +25% (earnings)

-LZ +24% (earnings, guidance)

-SKYT +24% (earnings, guidance)

-DDOG +23% (earnings, guidance)

-FSLY +21% (earnings, guidance)

-SNAP +19% (earnings, guidance; Snap and Perplexity sign partnership to integrate Perplexity’s AI-powered answer engine directly into Snapchat)

-RXST +17% (earnings, guidance)

-PLNT +16% (earnings, guidance)

-SES +15% (earnings, guidance)

-COHR +14% (earnings, guidance)

-LFST +13% (earnings, guidance)

-EOLS +11% (earnings, guidance)

-SN +11% (earnings, guidance)

-YOU +11% (earnings, guidance)

-HAE +9.8% (earnings, guidance)

-MRNA +9.7% (earnings, guidance)

-ROK +9.0% (earnings, guidance)

-OSCR +8.5% (earnings, guidance)

-CMI +7.0% (earnings)

-MRVL +6.9% (SoftBank Group said to have considered merging Marvell with ARM)

-APP +6.8% (earnings, guidance)

-DNUT +6.4% (earnings, color)

-FOUR +6.4% (earnings, guidance)

-EPAM +5.0% (earnings, guidance)

-DKNG +4.8% (ESPN names DK as new sports-betting partner)

-ACAD +4.3% (earnings, guidance)

-H +4.3% (earnings, guidance)

-AZN +4.0% (earnings, guidance)

-SONO +3.9% (Morgan Stanley Raised SONO to Equal Weight from Underweight, price target: $17 from $11)

-SATS +3.3% (earnings; discloses to Sell Full Unpaired AWS-3 Spectrum License Portfolio to SpaceX for $2.6B)

-GEO +3.0% (earnings, guidance)

-ARM +2.5% (earnings, guidance)

-ASPN -31% (earnings, guidance)

-DUOL -25% (earnings, guidance)

-AOSL -22% (earnings, guidance)

-ELF -21% (earnings, guidance)

-PRCH -19% (earnings, guidance)

-GOOS -16% (earnings)

-PRKS -16% (earnings)

-RELY -16% (earnings, guidance)

-CELH -14% (earnings)

-HUBS -13% (earnings, guidance)

-XRAY -12% (earnings, guidance)

-BMBL -11% (earnings, guidance)

-KMX -11% (CEO resigns; provides prelim Q3 metrics)

-DASH -10% (earnings, guidance)

-TPR -9.4% (earnings, guidance)

-LEU -8.1% (earnings; enters $1B ATM equity sales agreement)

-WRBY -7.5% (earnings, guidance)

-PAYC -7.4% (earnings, guidance)

-PZZA -5.2% (earnings, guidance)

-VST -3.9% (earnings, guidance)

BY Doug Kass · Nov 6, 2025, 9:24 AM EST

Valuations are elevated (96%-tile), investor sentiment is at dangerously optimistic levels, interest rates are climbing, inflation is sticky, economic growth is decelerating, the K-shaped U.S. economy holds social/economic risks and neither political party gives a damn about our deficit and debt load.

I remain bearish in market view.

I expect a resolution to the government shutdown in the next few days.

I am holding off on more shorts until that expected agreement - at which time I will aggressively short equities (likely on a bump higher).

There you have it.

BY Doug Kass · Nov 6, 2025, 9:05 AM EST

BY Doug Kass · Nov 6, 2025, 8:55 AM EST

BY Doug Kass · Nov 6, 2025, 8:45 AM EST

From Peter Boockvar:

Strictly from a stock market sentiment standpoint I believe the stage is now set for a pullback because the two figures I believe have statistical significance now show extreme bullishness. I reflected Monday the off the chart Euphoric read in the weekly Citi index. Seen yesterday was the Investors Intelligence survey which already had a Bull/Bear spread above 40 but now you have the level of Bulls kissing 60 at 59.3, up from 57.7 last week. Off the lowest level since January 2018, Bears ticked up to 14.8 from 13.5. That spread of 44.5 from 44.2 last week is dangerously wide. I want to emphasize that any stock market digestion that this leads to would just be a short term reset as that is only what sentiment indicators are relevant for.

BY Doug Kass · Nov 6, 2025, 8:35 AM EST

Fed speakers:

8:30 a.m.: Fed Bank of Chicago President Goolsbee (Voter) Television Appearance -- CNBC; and at 4:20PM: Television Appearance -- Newsmax;

11 a.m.: Fed Bank of New York Williams President (Voter) gives lecture on "The Natural Rate of Interest" before event organized by the Goethe University Institute for Monetary and Financial Stability (IMFS), Frankfurt, Germany (No text. Moderated Q&A expected. Livestream available); (in-person attendance): Live stream. Event information;

11 a.m.: Fed Board Governor Barr participates in virtual "Community Development" discussion hosted by Fed Communities, Washington, DC ( No text. Q&A from moderator); 12 p.m.: Fed Bank of Cleveland Beth M. Hammack (Non-Voter) speaks at the Economic Club of New York;

3:30 p.m.: New York Federal Reserve Bank Director of Research Kartik Athreya speaks at National Economic Outlook in Long Island University Post Honors College;

3:30 p.m.: Fed Board Governor Waller (Voter) participates in "Central Banking and the Future of Payments" panel before the Bank of Canada 2025 Annual Economic Conference, Ottawa, Canada ( No text. Q&A from moderator. Livestream link available);

4:30 p.m.: Fed Bank of Philadelphia President Paulson (Non-Voter till 2026) speaks on "The Federal Reserve Bank of Philadelphia's Consumer Finance Institute" before the "New Perspectives on Consumer Behavior in Credit and Payments Markets Conference – 2025" hosted by the Federal Reserve Bank of Philadelphia, Philadelphia, PA (In-person event. Text available. No Q&A);

5:30 p.m.: Fed Bank of St. Louis President Musalem (Voter) speaks on the U.S. economy and monetary policy before the Fixed Income Analysts Society, Inc., Penn Club of NY, NYC (Audience Q&A expected. No text. No media availability. In person with virtual option)

Treasury auctions:

11 a.m.: Treasury announces a 3 and 6 month bill auction;

11:30 a.m.: Treasury hosts a $110 billion 4 and $95 billion 8 Week Bill Auction

Economic Calendar:

BY Doug Kass · Nov 6, 2025, 8:14 AM EST

BY Doug Kass · Nov 6, 2025, 7:40 AM EST

BY Doug Kass · Nov 6, 2025, 7:30 AM EST

BY Doug Kass · Nov 6, 2025, 7:20 AM EST

BY Doug Kass · Nov 6, 2025, 7:10 AM EST

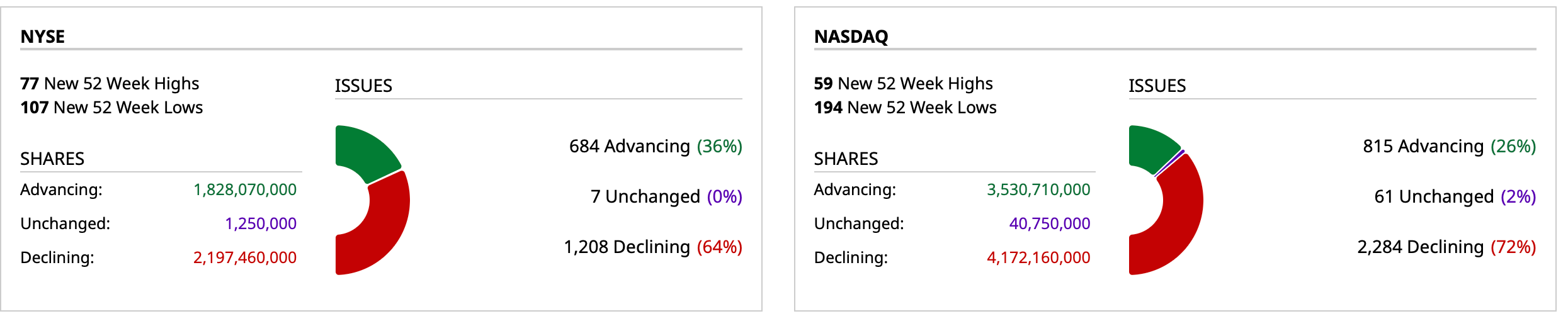

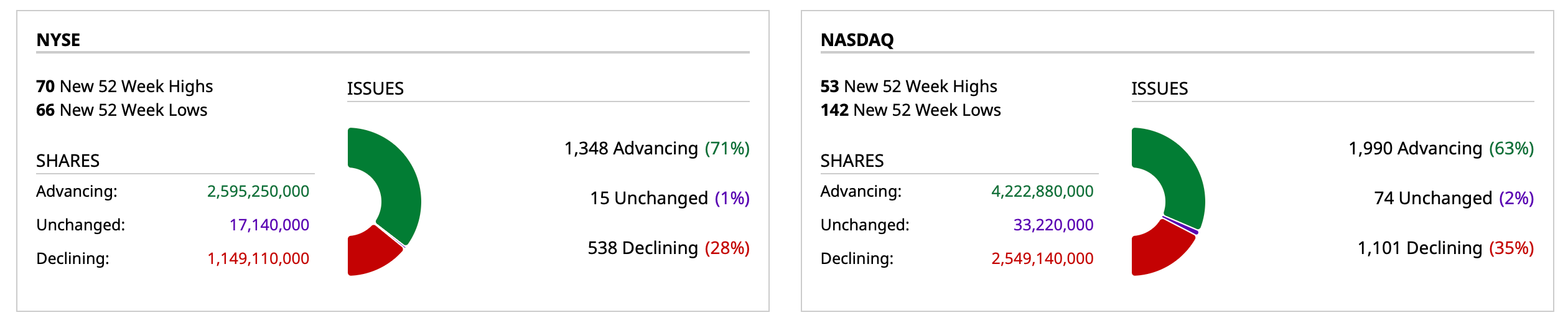

Yesterday marked a change in breadth — it improved:

Stay tuned.

BY Doug Kass · Nov 6, 2025, 7:00 AM EST

* Another late day swoon...

He also wrote:

"History never repeats itself. Man always does."

Bonus — Here are some great links:

The Good, The Bad and The Ugly

BY Doug Kass · Nov 6, 2025, 6:45 AM EST

BY Doug Kass · Nov 6, 2025, 6:35 AM EST

BY Doug Kass · Nov 6, 2025, 6:25 AM EST

* This is not market friendly

* The equity risk premium grows ever more thin...

Little discussion on Fin TV of the breakdown in bonds, which suffered the worst six-day drawdown in six months:

BY Doug Kass · Nov 6, 2025, 6:15 AM EST

Another MACD breakdown (?):

BY Doug Kass · Nov 6, 2025, 6:05 AM EST

When I awoke at about 3:15 AM — at that time the S&P futures were -17 handles.

They are now +5 handles.

I am adding to my short exposure by shorting the indices:

* (SPY) $678.31

* (QQQ) $624.00

BY Doug Kass · Nov 6, 2025, 5:55 AM EST

The S&P Short Range Oscillator is at 0.01% vs. -1.20%.

That's right in the middle of readings — solidly neutral.

BY Doug Kass · Nov 6, 2025, 5:47 AM EST