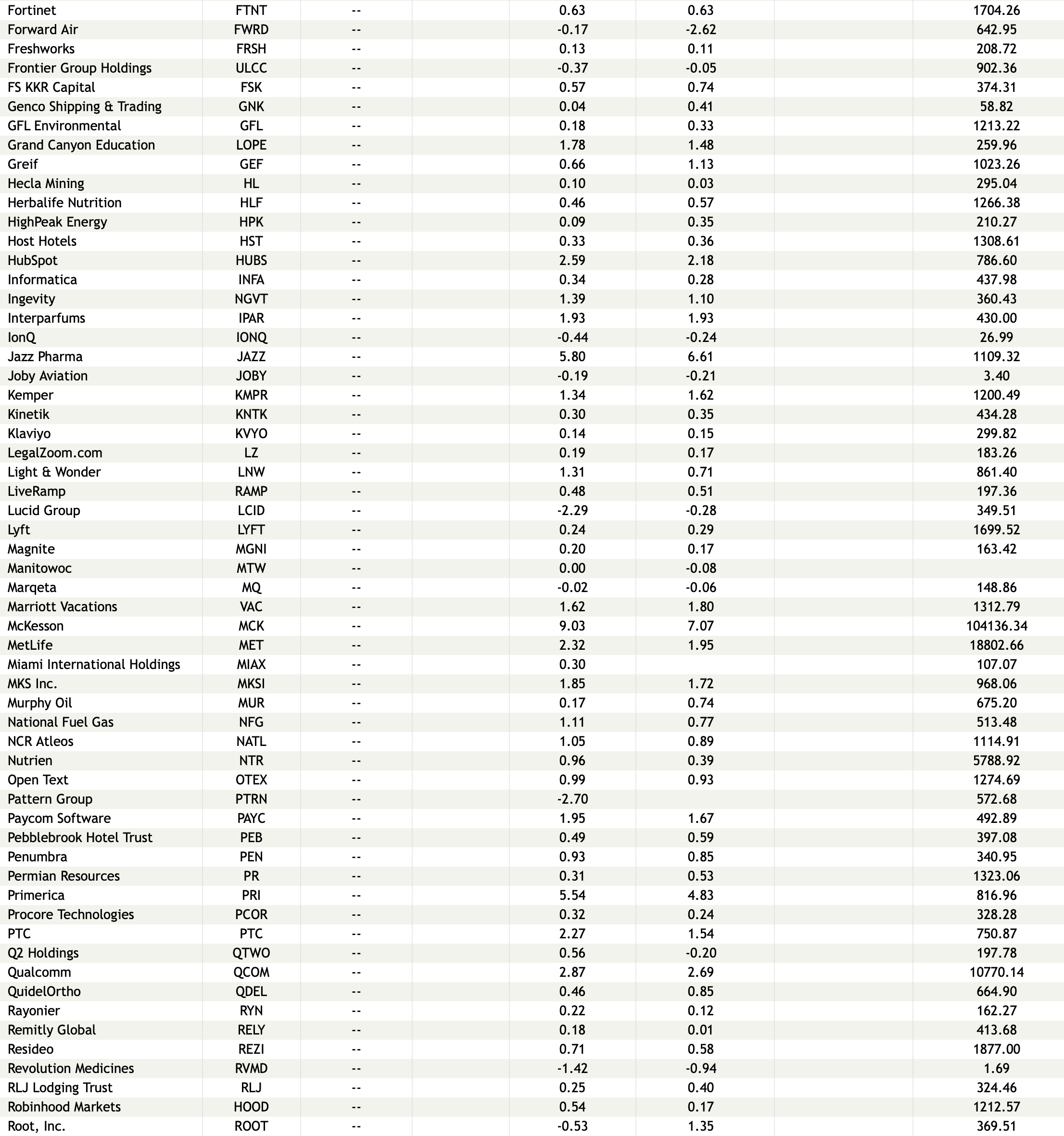

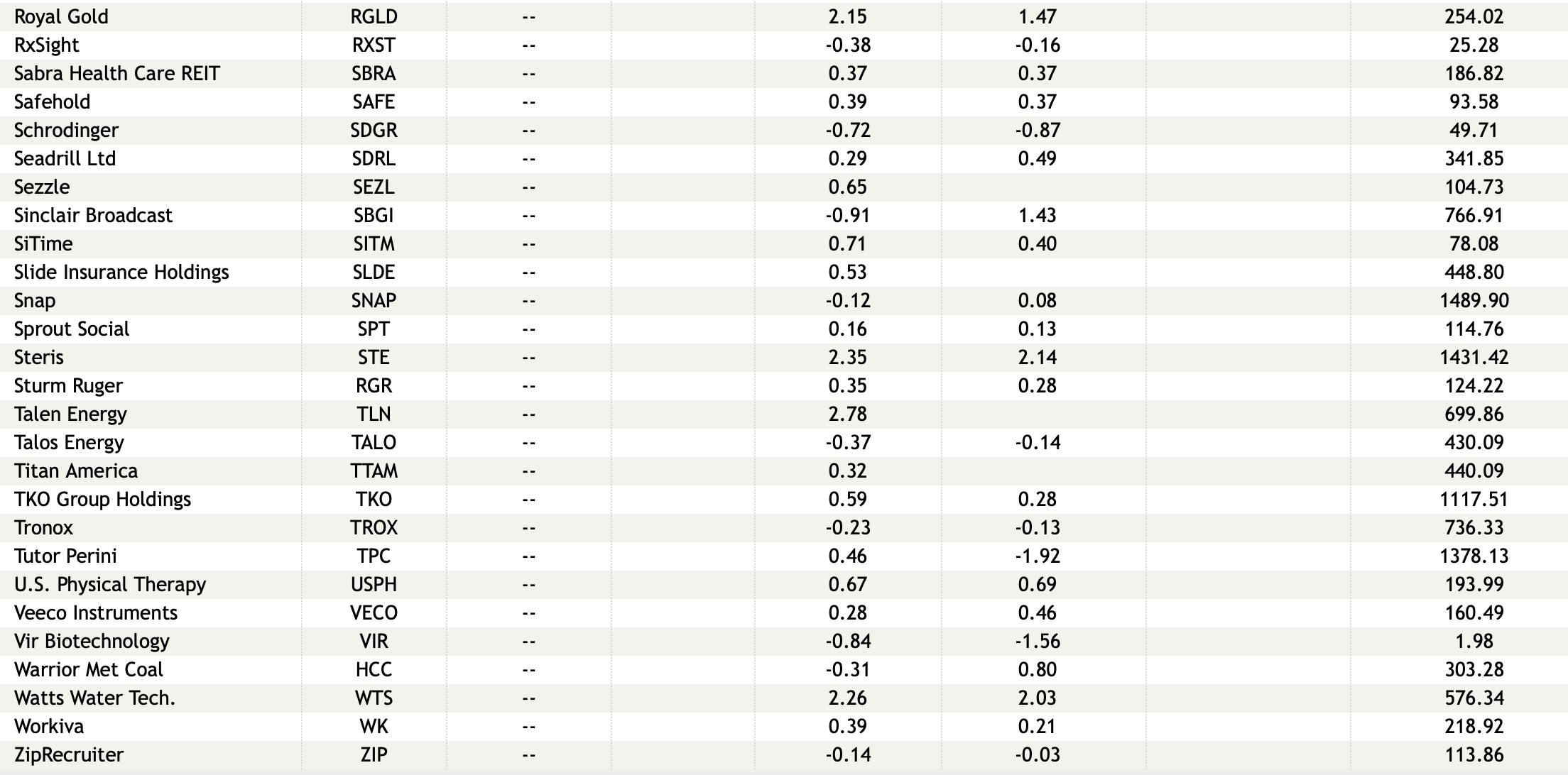

Wednesday's Closing Market Stats

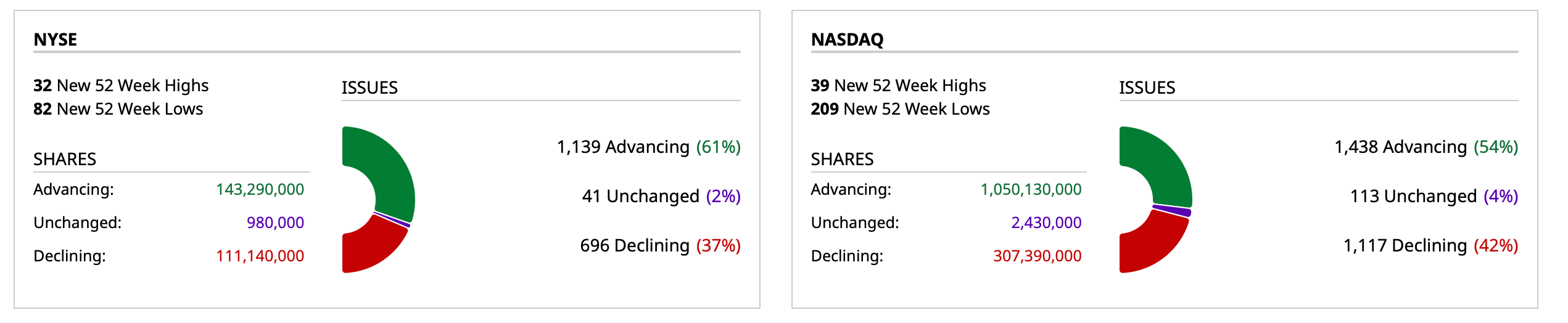

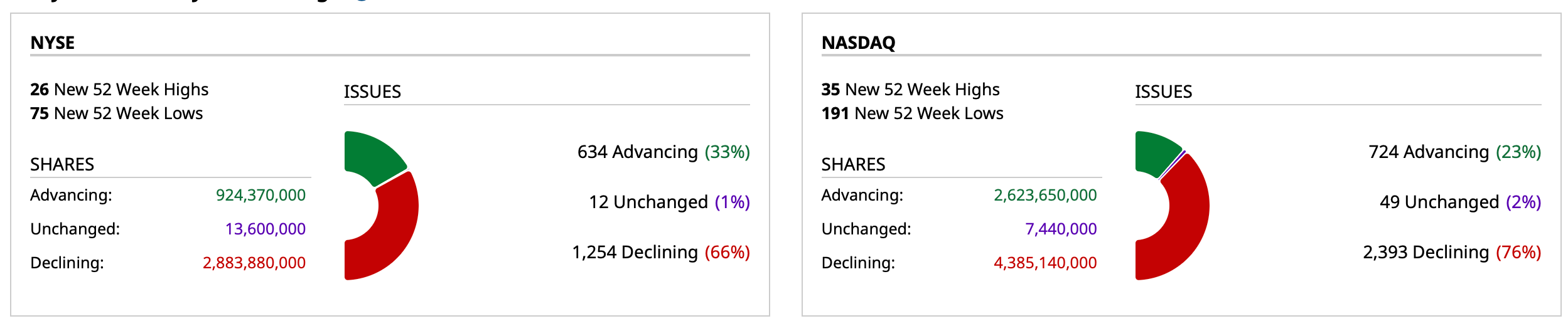

Closing Breadth

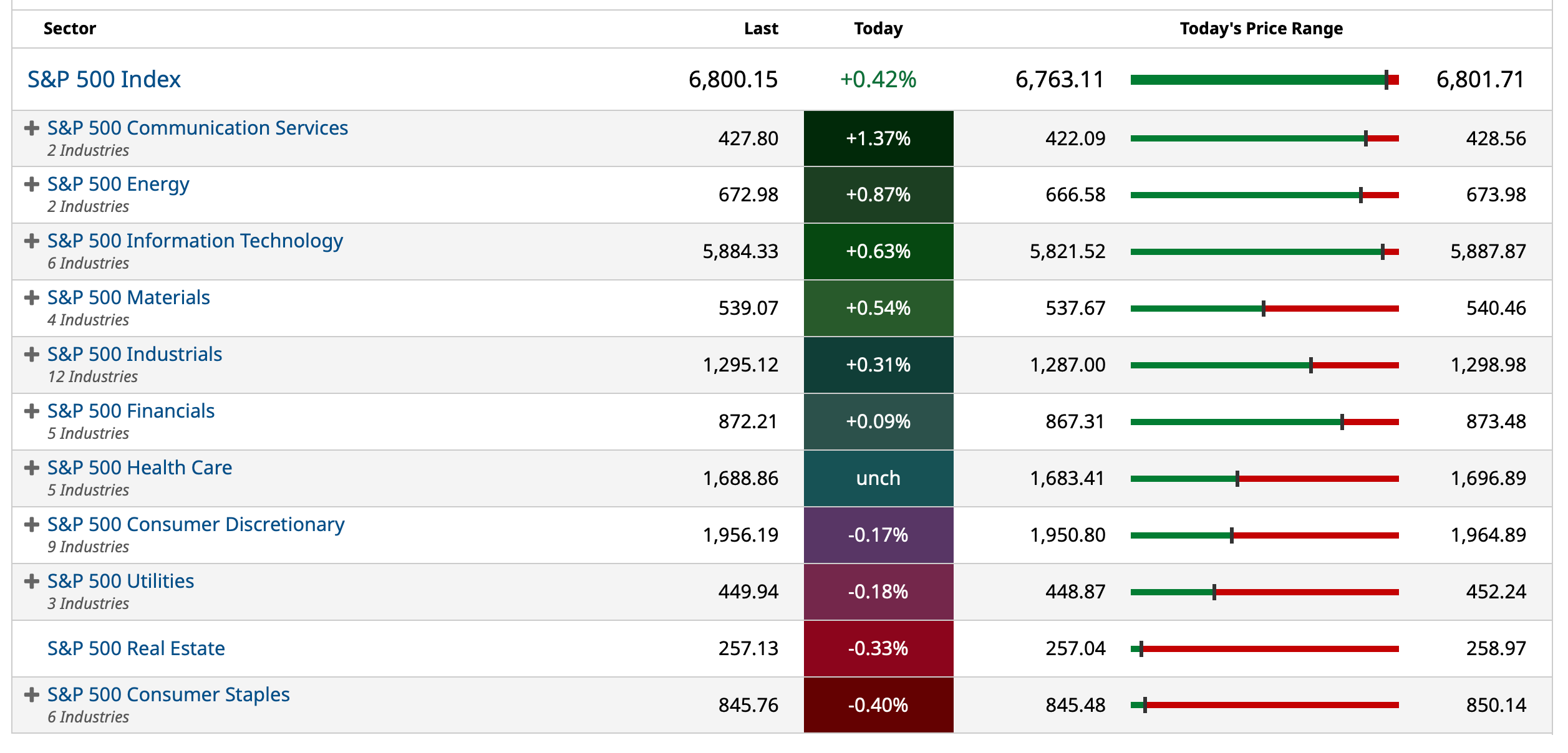

Sectors

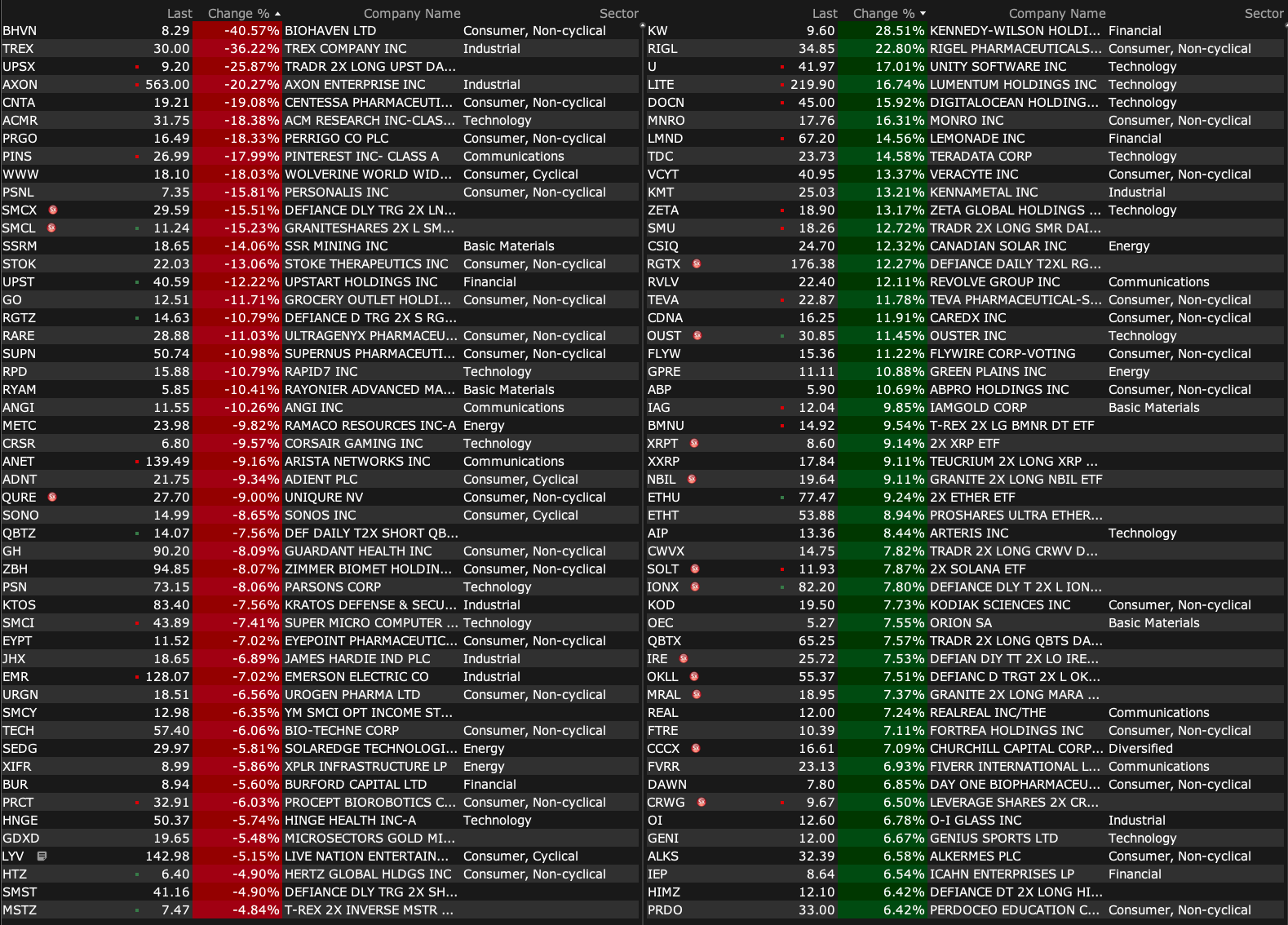

% Movers

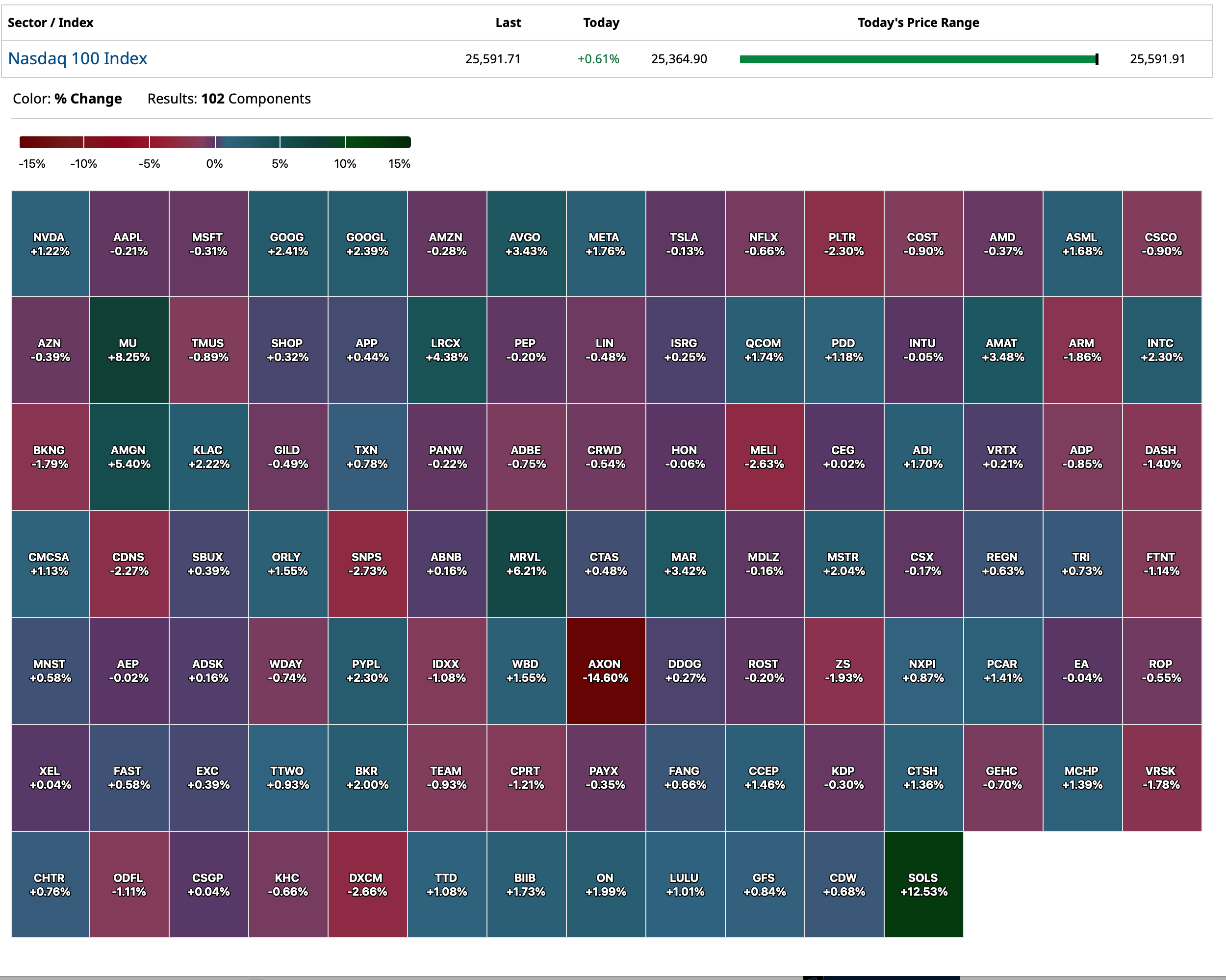

Nasdaq 100 Heat Map

BY Doug Kass · Nov 5, 2025, 4:30 PM EST

BY Doug Kass · Nov 5, 2025, 4:30 PM EST

BY Doug Kass · Nov 5, 2025, 3:57 PM EST

Thanks for reading my Diary today.

I hope my output was helpful.

I have a 3:30 PM research call.

Enjoy your evening.

Be safe.

BY Doug Kass · Nov 5, 2025, 3:35 PM EST

I have moved to large long (KMB) and (PEP) .

I will have writeups in the next few days.

BY Doug Kass · Nov 5, 2025, 2:19 PM EST

BY Doug Kass · Nov 5, 2025, 1:51 PM EST

With S&P cash +59 handles (and +102 handles from last night's low!) I have added to my short index calls — moving to medium-sized short in the indices.

BY Doug Kass · Nov 5, 2025, 1:44 PM EST

BY Doug Kass · Nov 5, 2025, 1:30 PM EST

BY Doug Kass · Nov 5, 2025, 1:23 PM EST

From Bramo:

BY Doug Kass · Nov 5, 2025, 12:40 PM EST

The following three conditions exist:

* The labor data not as bad as thought.

* Inflation remains sticky.

* The Fed is under pressure by the President.

Shouldn't the 10-year and long bond yields now rise?

Isn't that a poor influence for stock prices and market unfriendly for valuations?

BY Doug Kass · Nov 5, 2025, 12:25 PM EST

cjsolus

So it seems the labor situation is not in the dire straits as the FED thought...at least as it looks now....inflation is still here even though some say its not... beg to differ....so the FED cutting isn't really needed... and the bond market is off which reinforces that thought ...so once again why are equities rallying off of the only news that doesn't seem bullish??

BY Doug Kass · Nov 5, 2025, 11:45 AM EST

I pressed my short index calls on the rally —close to medium sized.

BY Doug Kass · Nov 5, 2025, 11:25 AM EST

- NYSE volume 7% above its one-month average;

- Nasdaq volume 6% below its one-month average;

- VIX index: down 6.79% to 17.71

BY Doug Kass · Nov 5, 2025, 11:20 AM EST

From Peter Boockvar:

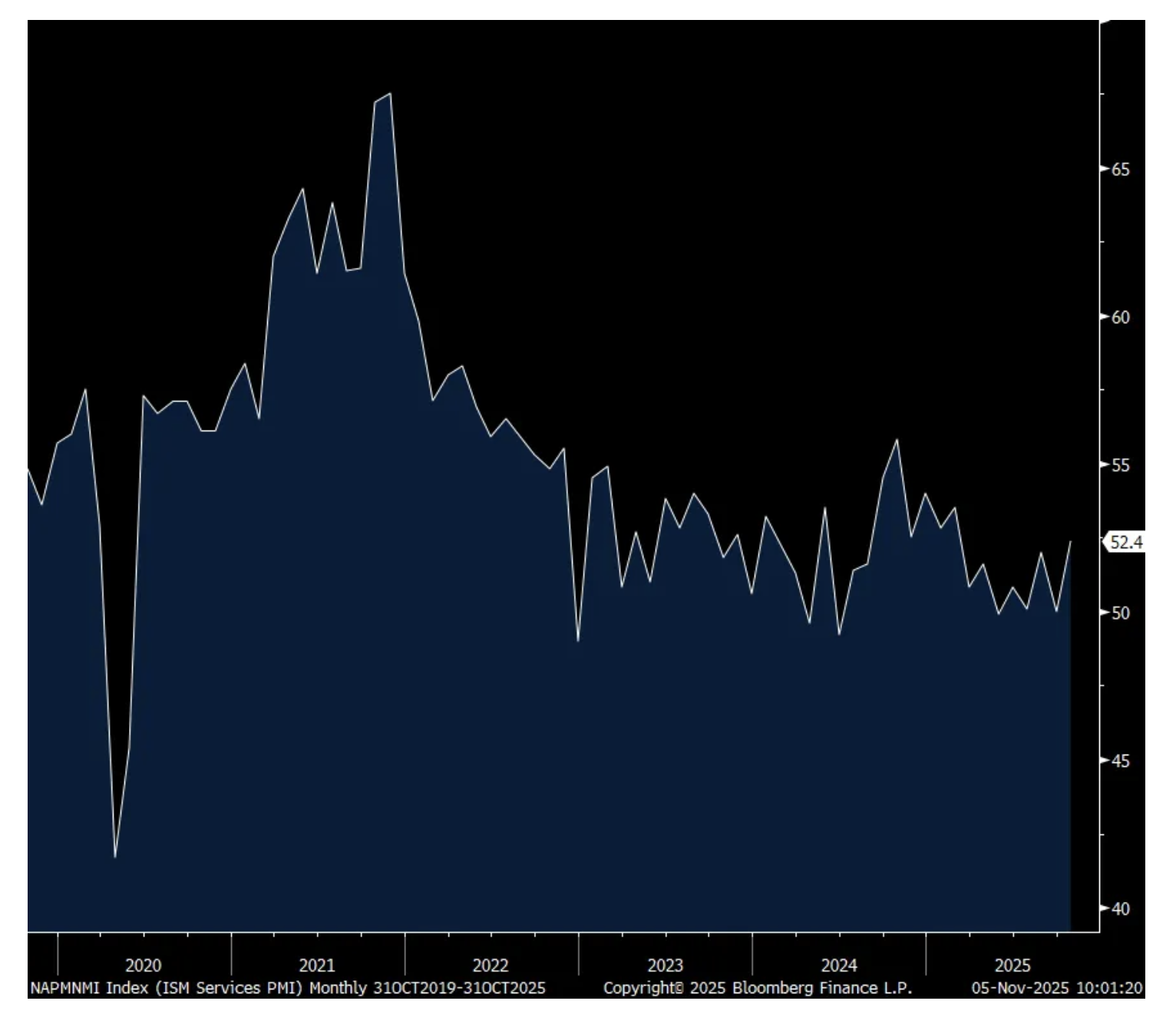

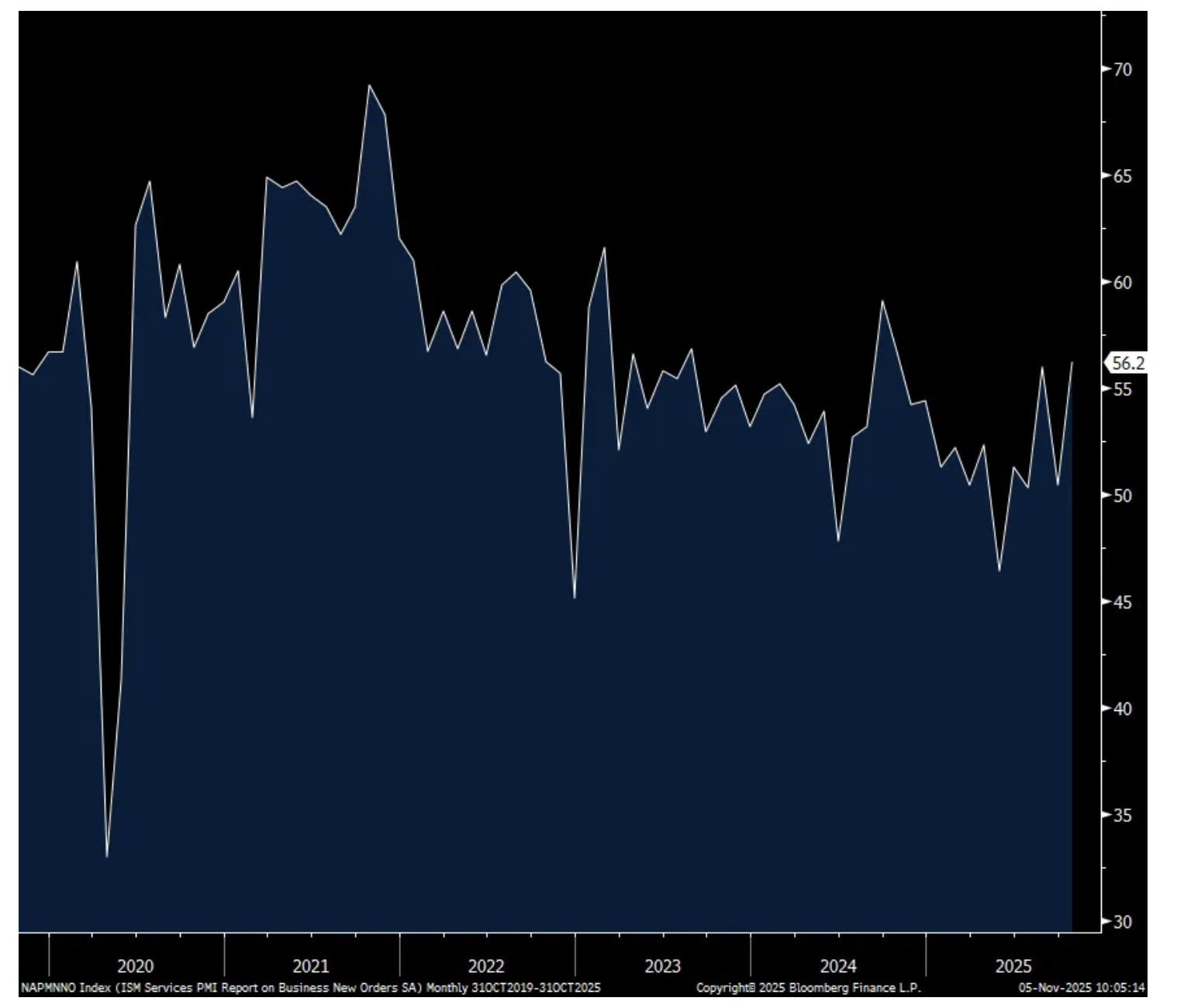

The October ISM services index rose to 52.4 from exactly 50 in September and 52 in August and that was above the estimate of 50.8. New orders rose 5.8 pts to 56.2 but after falling by 5.6 pts last month. Backlogs rose 6.9 pts in September and fell 6.5 pts in October. Inventories remained below 50 at 49.5, though up 1.7 pts m/o/m.

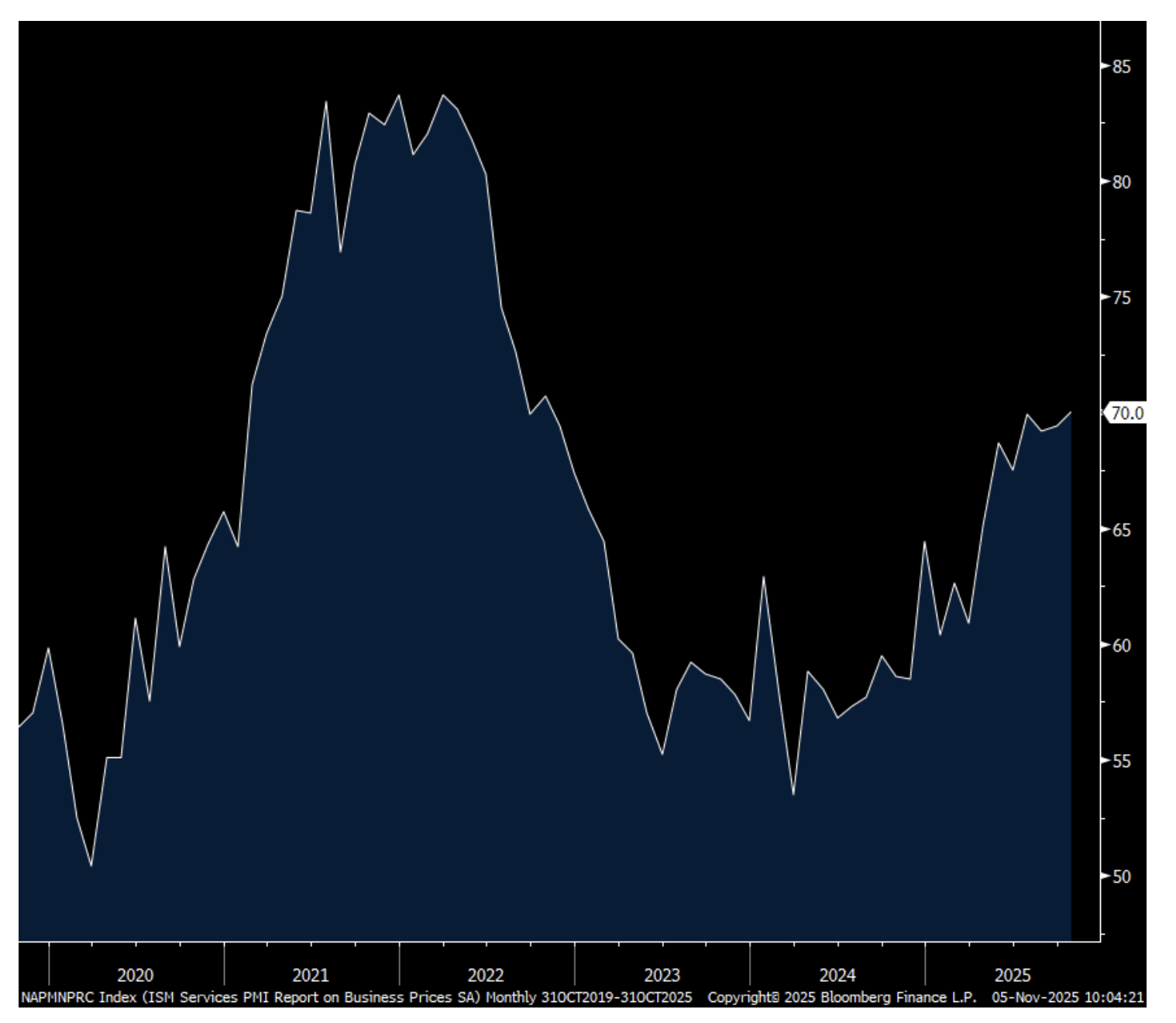

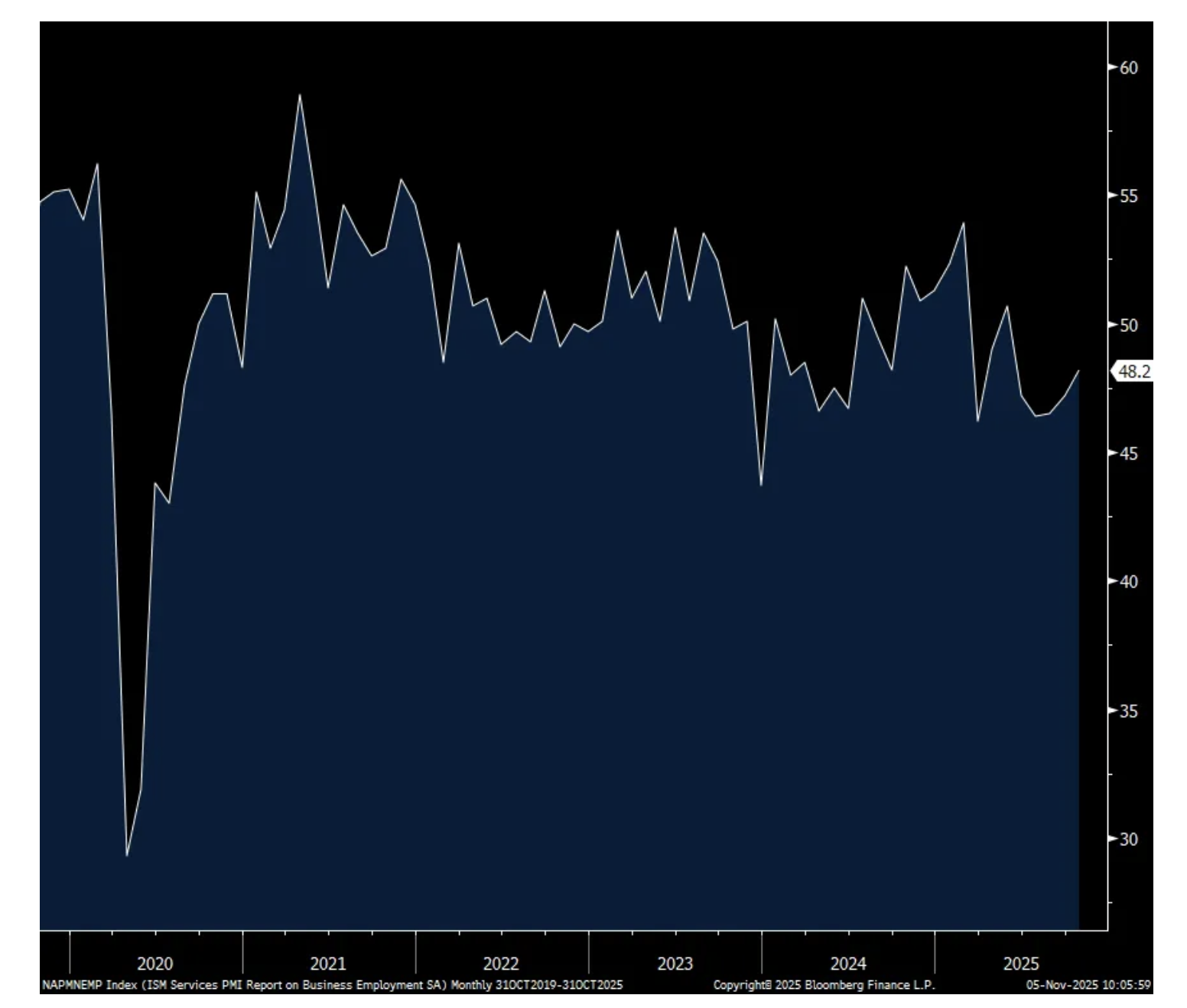

Employment rose 1 pt but stayed below 50 at 48.2 with just 4 industries adding workers. The ISM said, “There was no indication of widespread layoffs or reductions in force, but the federal government shutdown was mentioned several times as impacting business activity and generating concerns for future layoffs.” Supplier deliveries fell 1.8 pts but remained above 50 at 50.8. Prices paid touched 70, up .6 pts m/o/m and that is the highest since October 2022 with 16 of 18 industries paying higher prices. The ISM said “Respondents continued to mention the impact of tariffs on prices paid.” In other words, you don’t have to be in manufacturing to be feeling the impact of tariffs as inputs/raw materials/sourced products flow into the service sector via retail, restaurants, construction, etc…

Breadth improved a touch with 11 industries of 18 seeing growth vs 10 in September. Those in a contraction totaled 6 vs 7 last month.

Here were the notable comments:

“Activity is generally flat month-over-month; we are closely monitoring effects of the new tariff announcement.” [Finance & Insurance]

“Uncertainty due to the federal government shutdown has shuttered many non-essential functions. This will lead to project delays and likely hurt our overall fiscal year 2026 expectations. Our sites are funded through the next couple of months, but if the shutdown continues beyond that time, we will expect mass furloughs of our employees.” [Management of Companies & Support Services]

“Relatively flat activity levels for oil and gas.” [Mining]

“Client demand for advisory and compliance services remains solid, particularly as businesses navigate evolving tax legislation and increased regulatory scrutiny. However, we are seeing extended approval cycles on discretionary projects and tighter controls on consulting spend, which is putting pressure on procurement to be more agile and cost-efficient.” [Professional, Scientific & Technical Services]

“Heightened business activity due to new fiscal year budget. Items made with or utilizing precious metals are up, basic labor is down — though maintaining employees has been more difficult since a return-to-office order was implemented.” [Public Administration]

“The overall economy continues to provide mixed signals, which makes it difficult to determine how to move forward as a business given the uncertainty.” [Real Estate, Rental & Leasing]

“Business very strong, no supply chain or logistical issues.” [Retail Trade]

“General business has been steady, with minimum fluctuation.” [Transportation & Warehousing]

“Tariffs continue to cause disruption in contracts and contracting, driving up pricing on goods, particularly engineered and manufactured equipment. The backlog of existing orders with delays continues to persist for equipment and manufactured equipment.” [Utilities]

“Business seems to be picking up. Multifamily is a big driver. I think most projects that have been postponed are finally coming to fruition as lumber prices have found a bottom. The outlook is better with the Fed’s plan to continue with rate cuts. Home prices coupled with elevated interest rates continue to keep a lid on sales. Home affordability is still a bit out of reach for a large portion of potential buyers. [Wholesale Trade]

Bottom line, the service sector continues to carry the weight of the economy as we know but even within services we know how divergent the differing sectors are in terms of strength.

Treasury yields are at the highs of the day in response to the data.

ISM Services

Prices paid

New Orders

Employment

BY Doug Kass · Nov 5, 2025, 11:00 AM EST

Chart from 9:42 a.m. ET:

BY Doug Kass · Nov 5, 2025, 10:36 AM EST

St. Joe Company's (JOE) shares are +$10 since its good EPS report last week.

I am reducing my holdings at $58.84.

BY Doug Kass · Nov 5, 2025, 10:16 AM EST

With S&P cash +25 handles I have sold out all of the Index common - remain short Index calls:

* (SPY) $677.50

* (QQQ) $621.80

BY Doug Kass · Nov 5, 2025, 10:01 AM EST

From Peter Boockvar:

I’ve made clear here over the past 6 months my disagreement with the protectionist use of tariffs in such a scattershot way as opposed to the use of them in a narrow, strategically focused approach. I thus anxiously await the Supreme Court’s decision as we all do. I much preferred another cut in the corporate income tax rate to say 15% and combined with a deregulatory path would have been a more effective way of making the US a more competitive place to make things and do business. If there is one thing we’ve learned over the past 5 years is the disgust the American people have with inflation, as all people around the world have too, and layering on more costs and inflation, whether one time or not via tariffs, is why I believe consumer confidence is still very low. The higher cost of living unfortunately just got a socialist elected mayor even though those policies will only make things much worse as the history of the world provides plenty of evidence for that. It’s truly shocking the financial illiteracy that is out there in the voting pool.

By the way, two of my favorite Thomas Sowell quotes was this, “Socialism in general has a record of failure so blatant that only an intellectual could ignore or evade it.” And, “Socialism is a wonderful idea. It is only as a reality that it has been disastrous.”

As to the argument that ‘we’re taking in all this money’ from tariffs, well it is mostly coming right out of the pockets of US businesses and households which then leads to lower economic growth, less profits and a slowing rate of hiring which results in less tax collection from companies and workers which then offsets the tariff take. A tariff regime focused on key strategic sectors? Ok. Spraying them on everything like stuff we’ll never make here? Not ok. And at the end of the day, the US government has a major spending problem, not a tax collection one.

While it would finally be nice to get some economic data from the government, Corporate America is telling us all we need to know and it continues to reflect this hugely split economy. But, I want to emphasize that this is not new, companies have been talking about this mixed and uneven economy for the past few years that people are finally waking up to.

When describing the US consumer, the word ‘choiceful’ used by company executives started in late 2023 and it should be no surprise as an almost 25% rise in the cost of living over the past five years has resulted in a downbeat consumer both in how they feel as seen in the soft consumer confidence figures and how they are spending.

I cannot emphasize enough how much economic information I glean from going through probably 150 earnings calls every single quarter to hear exactly what is going on at the ground level so we just don’t get our information 30,000 feet up from the government and other diffusion indexes.

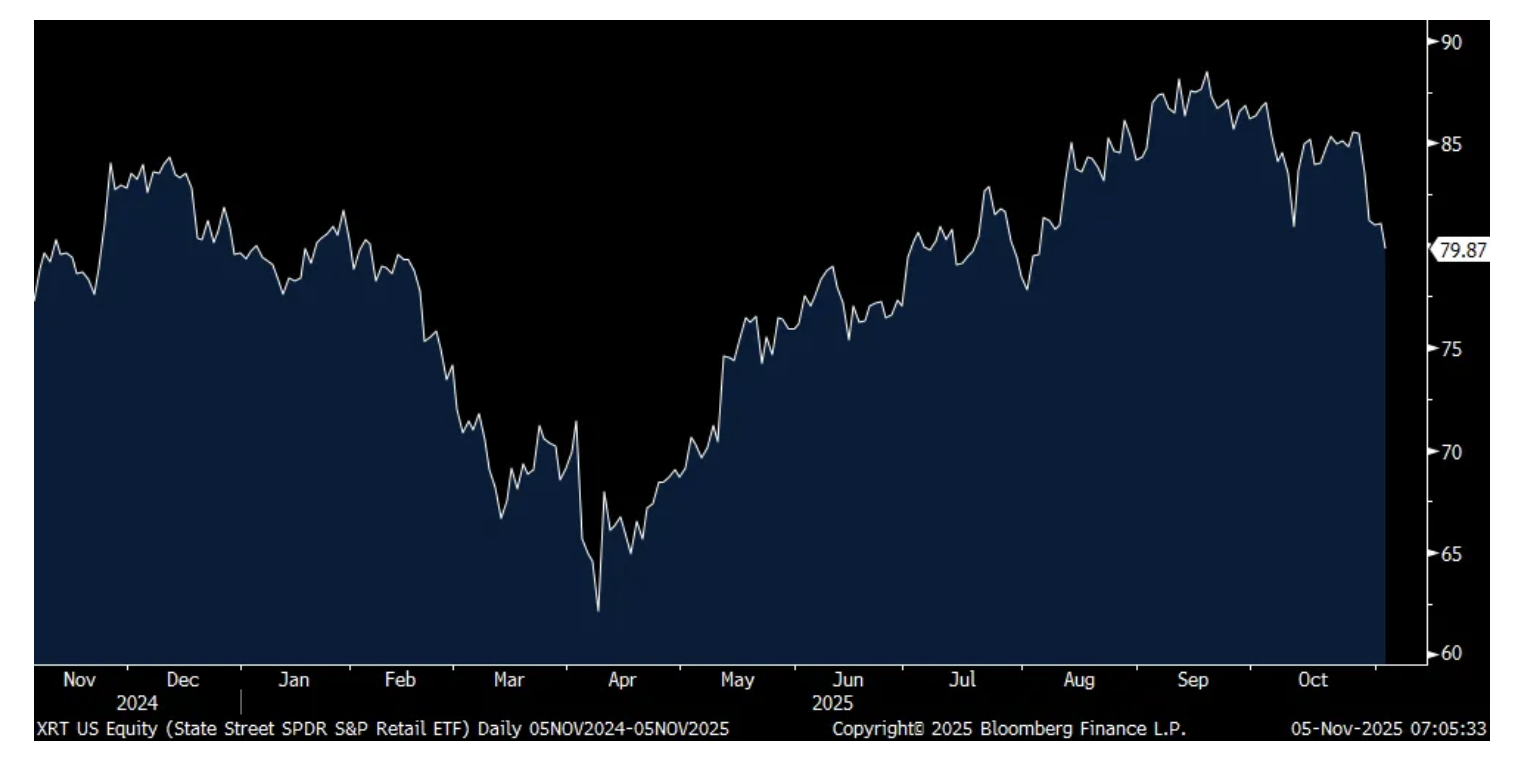

By the way on the US consumer, XRT, the equal weighted retail ETF closed yesterday at the lowest level in 3 months.

XRT

Here is what Wingstop said, a stock that rallied 11% but missed numbers and that rally was off a near 52 week low:

“We shared earlier this year that certain regional pockets, which over index to Hispanic and low income consumers, were experiencing some softness in sales as we lap two consecutive years of industry leading same store sales growth. During the third quarter, we saw this dynamic broaden across the industry and within our business to more geographies as well as to the middle income consumer in some areas, resulting in a 5.6% decline in same stores sales in Q3 that was below our expectations.”

From Cava and whose stock is down pre-market as they missed numbers:

“we recognize that today’s environment is creating real pressures for consumers, especially younger guests who are making more deliberate choices about where they spend. It’s incumbent upon restaurants to deliver exceptional experiences and differentiated value to guests.”

As to the cadence of their business, “As we exited the second quarter, we saw same restaurant sales reaccelerate, and we’re encouraged by the sequential improvement. However, as the third quarter progressed, we experienced some moderation in trends, reflecting broader macroeconomic pressures. Entering the fourth quarter, we’re seeing further moderation as we continue to lap stronger same restaurant sales from the prior year.”

Norwegian Cruise saw its stock plunge by 15% due to slowing yield growth (revenue per passenger):

Business was still pretty good though, as we saw with Royal, as “We met or exceeded the guidance we provided in July and delivered the highest quarterly revenue in our company’s history.”

“Turning now to recent demand, bookings in the third quarter marked the strongest third quarter bookings in company history, with bookings up over 20% from last year. With this trend continuing into October, all collectively driven by strong demand, not only for our short Caribbean sailings this winter, but also for our luxury brands.”

This is what spooked investors, “As we attract more families, we are seeing more third and fourth guests in a cabin and naturally those guests come in at a lower price point, which has a modest impact on overall pricing. As a result of this dynamic, in the fourth quarter we expect net yield to grow approximately 3.5% to 4%, reflecting our deliberate decision to welcome more families while taking a slight trade off on price, which remains healthy at nearly 3% growth. As a result, full year net yield growth expectations have been adjusted slightly to 2.4% to 2.5% for the year.”

Live entertainment continues to where consumes are prioritizing and Sphere Entertainment rallied almost 5% yesterday. Their showing of Wizard of Oz is doing about $2mm per day in revenue and “we also saw revenue growth from concert residencies.”

More on this sector of the economy, from Live Nation, a stock we still own but is down pre market after missing both top and bottom line estimates, though business is still very good:

“Strong fan demand drove another record quarter, as we continue to attract more fans to more shows globally. With these tailwinds, 2026 is off to a strong start with a double digit increase in our large venue show pipeline and increased sell through levels for these shows.”

“Growth continues to be led by our international markets, where fan count is on track to surpass the US for the first time.”

As they look to next year, “Ticket sales for Live Nation concerts in 2026 have reached 26 million, up double digits overall and for each of stadiums, arenas, and festivals, reflecting broad based demand.”

“Fan spending up 8%, with an 8% increase in average order size.”

To a question on whether the high end consumer is spending more but observing pressure on the low end, the CEO said this, “No. We have not seen any of that. Our business is very diverse. It’s powered from clubs to arenas to festivals, stadiums, small town to big on a global basis. So we see it all. And we need all levels of consumers consuming to make the show sell out. And we’re already on sale for next year for many shows and festivals of certain sizes, and they are selling as fast as ever. So the appetite, the consumption going to that show still seems to be number one priority for them, and we saw no pullback anywhere yet.”

High end spend we know too is still doing well, though North America sales were down at this company. From Capri Holdings, the owner of Michael Kors and Jimmy Choo:

“In our retail channel, we continue to see signs of momentum with a sequential improvement in trends in our full price channel across all regions. In fact, comps in our full price channel turned positive in the second quarter, demonstrating that our strategies are beginning to take hold. Consumers are responding to our modern jet set lifestyle marketing, standout styles, and updated pricing architecture.”

Marriott reflected the two lane consumer highway:

“The slight RevPAR decrease in the US and Canada was driven by declines in select service brands, which offset nice gains in luxury.”

The government shutdown didn’t help them, “Business transient was further impacted by government RevPAR declining 14%.”

Uber fell 5% off a 52 week high but had a good quarter:

“Trips grew 22%, marking our fastest growth since 2023. Both lines of business accelerated with mobility trips scoring 21%, significantly exceeding our expectations.”

“We’re expecting more of the same strong performance in Q4, with another quarter of high teens gross bookings growth and low to mid 30s EBITDA growth.”

Shopify sold off on a slight miss on margins but still was a big growth quarter. They had this interesting tidbit on tariffs and pricing:

“We still see that our merchants have in the aggregate raised their prices some since the April tariff announcements in the US, but the level of pricing increases is, in fact, slightly lower than the trends that we were seeing last quarter.”

On the consumer, “shoppers keep buying, they keep returning, and demand remains really resilient across channels and categories. So, I can only comment on what we saw at Shopify, whether it’s the GMV (gross merchandise volume), but consumers are more selective right now, and they’re buying from brands they love, and those brands are on Shopify.”

My go to tech earnings call is always CDW because their tech distribution tentacles reach everywhere. The stock fell 8.5% after missing top line estimates and they said this:

“During the quarter, customer priorities remained focused on must do’s such as security enhancements and client device upgrades that are foundational to enabling modern work.”

“And once again, major capital investments were heavily scrutinized. Corporate and small business customers also prioritized pre-production AI trials to prove out use cases to validate concepts and ROIs. These priorities led to strength in cloud, software and services.”

“Small business delivered double digit growth in top line and gross profit as customers continue to lean more into technology in this dynamic environment.”

“Corporate delivered mid single digit top line growth with low single digit gross profit.”

Government sales rose 8% led by state and local spend that offset declines in federal. “Growth in higher education was offset by an expected decline in K-12.”

“Given our year-to-date performance in current market conditions, we are maintaining our prudent full year outlook, which calls for US IT market growth to be in the low single digits on a customer spend basis with CDW growth premium of 200 bps to 300 bps.”

Finally on how they describe the broad macro, “I would say volatility. Uncertainty might be the word most people would use.”

Interesting comments from Marc Rowan, CEO of Apollo Global:

“We are at a really interesting juncture of time in asset management and one that we frame really simply for our clients. We have them ask three questions. Are things cheap? Resoundingly no. Do we think rates that matter, long rates, are going to plummet? We do not. We think most of what we’re doing in the world is actually inflationary rather than contributing to lower rates. And finally, do we see enhanced sources of geopolitical risk? We do.”

“The answer to those three questions is yes. The logical thing to do is to take risk down. That is what we are doing as a firm. That is what we are doing for our clients. And we have been able to do this without reducing our need for return.”

At the same time, they certainly talked their book on the call, particularly with private credit. Said Jim Zelter, “Having navigated credit cycles for more than four decades, I can tell you we’ve seen this one way before. Isolated incidents are nothing new, and they’re rarely a signal of broader stress. As we remain vigilant in our underwriting and risk management efforts, what we’re seeing is idiosyncratic, not systemic.”

And for the market as a whole from Rowan, “There are good banks, there are bad banks, there are good asset managers, there are bad asset managers, there are good insurance companies, there are bad insurance companies. I don’t think we’re talking about systemic risk. I think we’re talking about late cycle behavior and bad actors, I believe, are going to get called out.”

I want to add this from my buddy David Rosenberg in his piece yesterday and who I will be speaking with next Wednesday on his podcast:

“Roughly $42 billion of corporate bonds have been downgraded this year (Barclays data) from the IG tranche to HY (’fallen angels’). The share of the IG market now possessing a ‘negative outlook’ by the rating agencies just hit a ten-year high; ditto for the BBB/BBB- tranche. Jamie Dimon was right - the number of cockroaches is on the rise.” That $42b figure by the way is up from $6b in 2024.

Eaton has been a key beneficiary of the data center buildout. “Organic growth for the quarter was 7%, driven by strength in aerospace, electrical Americas and electrical Global, partially offset by weakness in short-cycle markets, including vehicle and eMobility.”

With the electrical Americas division, “Organic sales growth of 9% was driven primarily by strength in data centers, up about 40%.”

Overseas, Singapore’s October PMI rose to 57.4 from 56.4 and continues to be a place of strong economic growth. We remain bullish and long stocks there. The private sector RatingDog China services PMI slipped a touch to 52.6 from 52.9 while Hong Kong’s PMI rose to 51.2 from 50.4.

With China’s print, “Specifically, affected by increased instability in the global trade environment, new export business fell noticeably into contractionary territory. The domestic market saw some improvement in demand, and total new orders remained in expansion, with the pace of growth quickening.”

The services PMI for the Eurozone and the UK were revised up slightly from their initial print a few weeks ago.

Also in Europe, the Swedish Riksbank left interest rates unchanged at 1.75% as expected.

BY Doug Kass · Nov 5, 2025, 9:55 AM EST

From Peter Boockvar:

ADP said that a net 42k private sector jobs were created in October, 12k more than estimated and follows a 29k job loss seen in September (revised a touch from -32k). Small and median sized businesses continue to be where the labor market has softened the most. Those with 1-19 employees shed 15k people while hiring 6k for those sized 20-49 employees. For those with 50-249 employees, 25k jobs were lost. About all of the job gain was seen for companies with more than 500 employees, adding 73k.

The breakdown among sectors was VERY mixed. Overall, services added 33k led by a 47k person rise in trade/transportation/utilities and I have to wonder if the data center buildout is showing up there in utilities along with construction (which added 5k). Financial services added 11k and education/health services contributed 26k. Job losses were seen in information, professional/business services, leisure/hospitality and ‘other services.’On the goods side, in addition to the 5k hired in construction as mentioned, natural resources/mining hiring rose by 7k. Manufacturing, still under stress, shed 3k.

Wage gains were still pretty good with the supply of labor shrinking but no acceleration being seen. For ‘job stayers’ pay rose 4.5% y/o/y unchanged with September. For ‘job changers’, wages rose by 6.7% y/o/y vs 6.6% in the month before.Bottom line from ADP “Private employers added jobs in October for the first time since July, but hiring was modest relative to what we reported earlier this year. Meanwhile, pay growth has been largely flat for more than a year, indicating that shifts in supply and demand are balanced.”I’ll add, whatever economic stresses there are out there, we know small and medium sized businesses are more sensitive to them and in the current ‘challenging macro environment’ we are in (that I’ve heard from so many), it should be no surprise that this is where most of the labor market slowing is taking place. That said, it seems now every week that we are hearing about a large company shedding workers and cutting costs. Now, as to the slowing supply of labor impacting the number of jobs needed to be added to hold the unemployment rate steady? I’ve heard numbers all over the place but assume it’s not less than 100k, maybe even below 50k?

BY Doug Kass · Nov 5, 2025, 9:35 AM EST

I am adding to (PEP) and (KMB) in the premarket.

BY Doug Kass · Nov 5, 2025, 9:30 AM EST

BY Doug Kass · Nov 5, 2025, 9:20 AM EST

-EVC +29% (earnings, guidance)

-KW +28% (gets buyout proposal at $10.25/shr from consortium led by Fairfax Financial)

-MNRO +18% (IEP said to have position in Echostar and also owns big stake in Monro)

-NPCE +18% (earnings, guidance)

-U +17% (earnings, guidance)

-LITE +16% (earnings, guidance)

-KMT +15% (earnings, guidance)

-LMND +15% (earnings, guidance)

-DOCN +14% (earnings, guidance)

-TDC +14% (earnings, guidance)

-TPB +13% (earnings, guidance)

-CDNA +12% (earnings, guidance)

-TEVA +12% (earnings, guidance)

-OUST +11% (earnings, guidance)

-IEP +7.9% (earnings)

-MOS +6.8% (earnings, guidance)

-TOST +5.2% (earnings, guidance)

-JCI +4.6% (earnings, guidance)

-JOBY +4.6% (begins Power-On Testing of First Conforming Aircraft, Enters Final Stage of Type Certification Process)

-BHVN -40% (US FDA Issues Complete Response Letter for VYGLXIA (troriluzole) NDA for Spinocerebellar Ataxia)

-TREX -36% (earnings, guidance)

-SNBR -22% (earnings, guidance)

-AXON -20% (earnings, guidance)

-CLOV -20% (earnings, guidance)

-CNTA -20% (earnings)

-PINS -18% (earnings, guidance)

-PRGO -18% (earnings, guidance; initiating strategic review of infant formula business)

-SSRM -13% (earnings, guidance)

-GO -12% (earnings, guidance)

-BUR -11% (earnings)

-METC -11% (prices public offering of $300M aggregate principal amount of 0% convertible senior notes due 2031)

-RPD -9.6% (earnings, guidance)

-ZBH -8.0% (earnings, guidance)

-CRSR -7.7% (earnings, guidance)

-EMR -7.4% (earnings, guidance)

-SEDG -7.0% (earnings, guidance)

-CAVA -5.5% (earnings, guidance)

-HUM -4.6% (earnings, guidance)

-OC -3.7% (earnings, guidance)

-CRVS -2.9% (earnings)

-AMD -2.7% (earnings, guidance; AMZN exits AMD stake)

BY Doug Kass · Nov 5, 2025, 9:10 AM EST

With S&P futures +5 handles I am selling out my long leg of the Indices (and keeping my short calls) - to expand my short exposure.

Here are my long sale prices:

* (SPY) $675.75

* (QQQ) $619.66

BY Doug Kass · Nov 5, 2025, 8:58 AM EST

BY Doug Kass · Nov 5, 2025, 8:56 AM EST

With S&P futures flat now (after being -53 handles at the nadir last night) - I am moving into a larger net short exposure in the indexes.

I made the following sales:

* (SPY) $675.30

* (QQQ) $619.10

BY Doug Kass · Nov 5, 2025, 8:39 AM EST

BY Doug Kass · Nov 5, 2025, 8:11 AM EST

Knowledge@Wharton on the U.S. housing crisis.

What Will It Take to Solve America’s Housing Crisis? - Knowledge at Wharton

BY Doug Kass · Nov 5, 2025, 8:00 AM EST

* Now the technicians are giving up on Bitcoin...

Bonus — Here are some great links:

Every Year Has Bad News and Volatility

BY Doug Kass · Nov 5, 2025, 7:30 AM EST

* I have consistently voiced concerns about this technical development.

Over the last four weeks Mag 7 is +5.4% as compared to the equal-weighted S&P index being down by -2.1%:

BY Doug Kass · Nov 5, 2025, 7:00 AM EST

BY Doug Kass · Nov 5, 2025, 6:45 AM EST

BY Doug Kass · Nov 5, 2025, 6:45 AM EST

"They are in the business of being skeptical and wrong, we are in the business of giving an unfair advantage to American workers, American war fighters and our investors."

- Alex Karp, Palantir CEO (on short sellers)

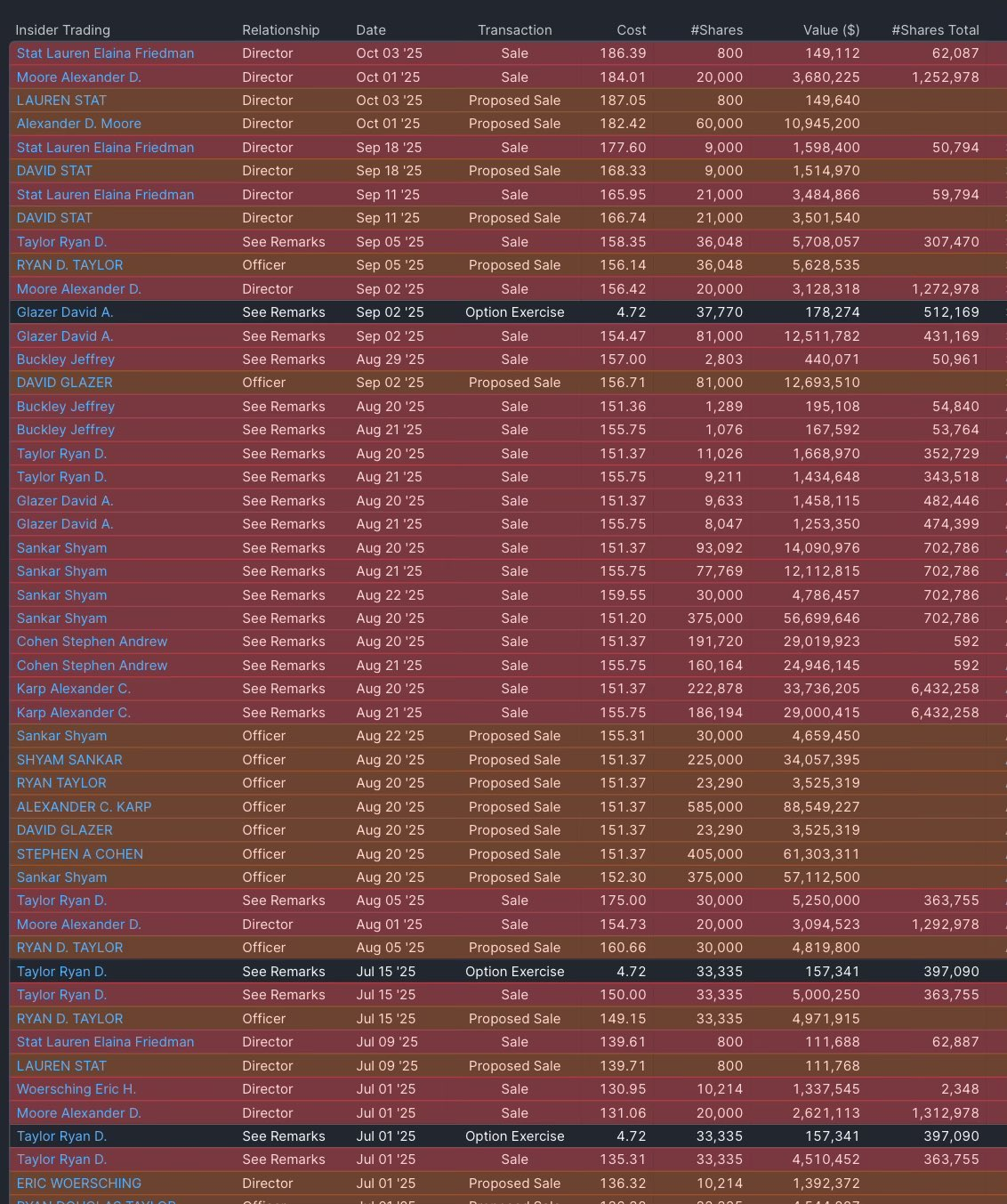

Here are the recent insider sales at Palantir (PLTR) :

We covered our PLTR short at about $187 yesterday — for a profit:

I have covered my trading short rental in Palantir (PLTR) at $187.12 (-$20 today) for a profit.

Position: none.

By Doug Kass Nov 4, 2025 9:40 AM EST

BY Doug Kass · Nov 5, 2025, 6:35 AM EST

The S&P Short Range Oscillator is at -1.20% vs. 0.23%. That is back into oversold.

BY Doug Kass · Nov 5, 2025, 6:25 AM EST

“Beware of the false prophets, who come to you in sheep’s clothing, but inwardly are ravenous wolves. You will know them by their fruits. Grapes are not gathered from thorn bushes nor figs from thistles, are they?"

- Matthew 7:15-6

BY Doug Kass · Nov 5, 2025, 6:15 AM EST

* S&P futures were volatile last night — with a 50-handle range (to the downside) in S&P futures and a 255-handle range in Nasdaq futures.

* I opportunistically traded that unexpected volatility.

I was a little too tall, could've used a few pounds

Tight pants, points, hardly renowned

She was a black haired beauty with big dark eyes

And points all her own, sitting way up high

Way up firm and high

Out past the cornfields where the woods got heavy

Out in the back seat of my '60 Chevy

Workin' on mysteries without any clues

Workin' on our night moves

Tryin' to make some front page drive-in news

Workin' on our night moves

In the summertime, mmm

In the sweet summertime

- Bob Seger, Night Moves

There was perplexing market volatility (at first to the downside and then back to near even) last night.

Some possible downside influences:

1. An extension of Tuesday's weakness in the regular session — in which market breadth smelled up the joint (something I have been warning about for two weeks):

2. Tokyo was -4%.

3. The drop occurred coincident with the NYC mayoral win by Democratic Socialist candidate Zohran Mamdani.

I was busy last night as the futures demonstrated loads of volatility — with S&P futures in a range of about 50 handles.

I am not sure why, but S&P futures were -53 and Nasdaq futures were -295 at one point (around 8:15 PM) in the evening — where I added to my index longs — moving off a delta-neutral position against short index calls and to a net long position.

Bought:

* (SPY) $671.32

* (QQQ) $613.79

When I awoke to take Ollie for a walk at about 1:30 AM S&P futures were down by only -3 handles and Nasdaq futures were down by only -34 handles. I sold what I had purchased... and then some — moving back to a very small delta-equivalent net short exposure (again).

Sold:

* SPY $674.87

* QQQ $618.33

BY Doug Kass · Nov 5, 2025, 5:59 AM EST