Six o'clock already, I was just in the middle of a dream I was kissin' Valentino by a crystal blue Italian stream But I can't be late, 'cause then I guess I just won't get paid These are the days when you wish your bed was already made

It's just another manic Monday (Ooh-oh) Wish it were Sunday (Ooh-oh) 'Cause that's my fun day (Ooh-oh) My I-don't-have-to-run day (Ooh) It's just another manic Monday

We ran the gamut of subjects today — from Sam Altman to AI to Grandma Koufax to a Barron's mention to a bullish extreme in investor sentiment to a possible "descending staircase" to strippers.

Strippers Aren't the Only Thing Sliding Down the Pole

We remain short RCI Hospitality Holdings(RICK) (aka Rick's Cabaret International — the chain of "elegant gentlemen clubs"!) — which has hit a 52-week low today.

A feminist, she was a successful business woman and a great investor.

She was even an excellent short-seller (it is in my DNA, I guess!).

I was reminded of something she told me when I wrote Issue #141 of More Tales From Nvidia this morning:

"Dougie, the single most constant and very very relevant truth about frauds and Ponzi Schemes is that the "early" skeptic will definitely make the least and could lose a lot if he backs that skepticism too early and too aggressively."

P.S.: We should carve Grandma's (above) words over the entry to the Federal Reserve!

I was quoted this past weekend on AI in Barron's "Up and Down Wall Street":

Meta Stock Took a Dive. It’s the Poster Child for the Debate Over AI Spending.

All eyes were on the parade of earnings reports from the technology behemoths this past week. But what grabbed the markets’ attention were the implications of their massive capital investments in artificial intelligence on their balance sheets and cash-flow statements.

At the center of this debate was Meta Platforms, which plunged 11% on Thursday after reporting a miss on earnings but, more importantly, said it was pushing full-speed ahead on AI data centers, projecting $71 billion in spending, up from $69 billion previously. Moreover, the company said that capital expenditures “will be notably larger in 2026 than 2025.”

All of which is absorbing increasing amounts of megatechs’ cash flow. As Doug Kass of Seabreeze Partners observes, the so-called hyperscalers have morphed from being “capital light” to capital-intensive operations. In the process, they have had to turn to external financing for their ambitious AI buildouts.

In fact, Meta brought this year’s biggest investment-grade corporate bond deal to market, totaling some $30 billion, the latest in a parade of recent data-center borrowing. Bank of America tallies $75 billion of AI-related public debt offerings in the past two months.

And that doesn’t count other financings, including Meta’s creative off-balance-sheet funding of its Louisiana data center, described by colleague Adam Levine in last week’s Tech Trader column. That includes a $38 billion loan tied to Oracle’s data centers, on top of $18 billion of public bonds issued by the company, led by world’s second-richest person, Larry Ellison.

Putting numbers to Kass’ point, BofA credit strategists Yuri Seliger and Sohyun Marie Lee write in a client note that capital spending by five of the Magnificent Seven megacap tech companies (Amazon.com, Alphabet, and Microsoft, along with Meta and Oracle) has been growing even faster than their prodigious cash flows. “These companies collectively may be reaching a limit to how much AI capex they are willing to fund purely from cash flows,” they write.

With S&P cash +18 handles I am back short index calls for December (monthlies in the money).

Given the rising volatility (a good feature when selling calls short), I will be selling slowly on a scale higher as I give Mr. Market a wider berth in these times of changing price action.

Not surprisingly, US manufacturing remained in contraction in October with an ISM print of 48.7 vs 49.1 in September and .8 pts below the estimate. New orders remained below 50 at 49.4, though up .5 pt m/o/m. Backlogs came in at 47.9 and was last above 50 in September 2022. Inventories too were again below 50 at 45.8 and at the customer level at 43.9.

Employment at 46 was under 50 for the 9th straight month and for the 16th month in the last 17. Supplier deliveries ticked up to match a 5 month high as we approach the holidays (higher # means longer lead time). Prices paid slipped 3.9 pts to 58, though still well above 50 and has come off its early year boil. Export orders remained under pressure at 44.5 with global trade muted.

Specifically on employment, the ISM said “Companies continued to focus on accelerating staff reductions due to uncertain near- to mid-term demand. Layoffs and not filling open positions remain the main head-count management strategies.”

With prices, “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods.”

On still depressed backlogs, “Ongoing contraction in the Backlog of Orders index means that trade issues and other geopolitical tensions are still at play. Significant improvement shouldn’t be expected until those issues begin to recede.”

Industry breadth was similar to last month with 6 sectors seeing growth vs 5 in September. Twelve contracted vs 11 last month.

The industry comments reflect the angst in the industry and the still difficulty in managing the current tariff regime.

“Business continues to remain difficult, as customers are cancelling and reducing orders due to uncertainty in the global economic environment and regarding the ever-changing tariff landscape.” (Chemical Products)

“Decrease in domestic demand for finished products has resulted in slower manufacturing and an increase of raw material in inventory.” (Petroleum & Coal Products)

“In general, business is really strained. Money is sitting tighter, and geopolitical changes add to the uncertainty/risk factor. Even medical fields are feeling the pressure.” (Miscellaneous Manufacturing)

“Sales continue to underperform in our automotive OEM and industrial divisions. Our aerospace and automotive aftermarket are the only areas performing slightly above budget. This is the third month of lower-than-expected sales, and the remainder of the year outlook is not looking better. Sales are expected to be slightly less than in 2024.” (Fabricated Metal Products)

“Tariffs continue to be a large impact to our business. The products we import are not readily manufactured in the U.S., so attempts to reshore have been unsuccessful. Overall, prices on all products have gone up, some significantly. We are trying to keep up with the wild fluctuations and pass along what costs we can to our customers.” (Machinery)

“The commercial vehicle (CV) market remains depressed as customers continue to delay vehicle purchases. Uncertainty in price and transportation demand remains the center of attention. U.S. trade policy and reciprocal actions by China in the form of export controls on rare earths and semiconductors, as well as ocean freight carrier restrictions, have once again caused a lot of stress in supply lines. The CV industry is now bracing for the next round of tariffs focused on commercials vehicles, scheduled to begin on November 1.” (Transportation Equipment)

“The tariff trade war has negatively impacted agricultural export markets, driving down demand and price. This negatively impacts farmer revenue and the likelihood of farmers investing in new equipment.” (Machinery)

“The unpredictability of the tariff situation continues to cause havoc and uncertainty on future pricing/cost. But even with the tariffs, the cost to import in many cases is still more attractive than sourcing within the U.S. Challenges with tariffs on production equipment necessary for internal production makes it difficult to justify expansion of capacity.” (Computer & Electronic Products)

“Volatility in some of our highly exposed commodity markets has tempered a bit, thanks to improved weather conditions and overall downward pressure on pricing. Tariffs continue to remain difficult to quantify, manage and deal with in general, since they continue to impact us day-to-day and our bottom line.” (Food, Beverage & Tobacco Products)

“Wonder has turned to concern regarding how the tariff threats are affecting our business. Orders are down across most divisions, and we’ve lowered our financial expectations for 2025.” (Chemical Products)

Bottom line, the manufacturing recession unfortunately continues on.

Sam Bankman-Fried was a messianic con man — seen (for some time) as a savior figure, expected to bring a new age of deliverance via cryptocurrencies.

The J.P. Morgan or the Michael Jordan of Crypto, SBF was the founder of the cryptocurrency exchange FTX and the cryptocurrency trading firm Alameda Research. He misappropriated billions of dollars of customer funds deposited with FTX, defrauded investors in FTX of more than $1.7 billion and defrauded lenders to Alameda of more than $1.3 billion.

FTX turned out to be Bernie Madoff, Theranos, Max Bialystock (The Producers), Baldwin United, Enron, Worldcom, Tyco International, Bre-X Minerals, HealthSouth, ZZZZ Best, the dot-com stocks (that collapsed in the early 2000s), the Covid gewgaws (of 2020-21) and Cathie Wood's 2022 portfolio — all wrapped into one big slice of "Group Stink."

In my Diary I have argued that the business media was complicit in SBF's Ponzi scheme, ignoring his idiosyncracies and lack of transparency by showering him with accolades and participating in softball interviews (who will ever forget CNBC's interview with him one month before his Ponzi was uncovered by the authorities?):

Those same softballs have been tossed at Sam Altman over the last several years.

Like Sam Bankman-Fried, Sam Altman is enormously wealthy. And, as seen by most, as living a life of the boundless mind. Though both somewhat awkward in their presence and delivery — it is reflected in a life freed and unencumbered by petty concerns like clothing and the physical cage of a suit and tie and other conventions.

That said, concerns (about AI and Sam Altman) are rising, and unfortunately this is not being challenged in legacy and in old school business media (who continue to favor seeking access over journalistic objectivity), but from independent critics:

And, most recently, President Trump is getting into the act.

(The president's comments on AI are interesting. I am not sending this as a political point at all as in Dem vs. Republican, or as a comment about Trump. I am sending this as a political point with regard to what often happens. The politicians (from both parties), President Trump (and the whole of government) know nothing.)

Trump appears genuinely shocked by the question. He only knows what he is told by influential donors and CEOs (who all have something to gain; I think Jensen Huang now must have office space in the White House), and what the stock market is suggesting with price action.

There is a reason why the government is the worst allocator of capital in history:

How can OpenAI with $13 billion in revenues make $1.4 trillion of spend commitments? (Source: @BG2Pod)

Sam Altman: “First of all. We’re doing well more revenue than that. Second of all, Brad, if you want to sell your shares, I'll find you a buyer. I just, enough. I think there's a lot of people who would love to buy OpenAI shares. I think people who talk with a lot of breathless concern about our compute stuff or whatever, that would be thrilled to buy shares. So I think we could sell your shares or anybody else's to some of the people who are making the most noise on Twitter about this very quickly. We do plan for revenue to grow steeply. Revenue is growing steeply. We are taking a forward bet that it's going to continue to grow and that not only will ChatGPT keep growing, but we will be able to become one of the important AI clouds, that our consumer device business will be a significant and important thing, that AI that can automate science will create huge value. There are not many times that I want to be a public company, but one of the rare times it's appealing is when those people are writing these ridiculous OpenAI is about to go out of business. I would love to tell them they could just short the stock, and I would love to see them get burned on that. But we carefully plan. We understand where the technology, where the capability is going to grow and how the products we can build around that and the revenue we can generate. We might screw it up. This is the bet that we're making and we're taking a risk along with that. A certain risk is if we don't have the compute, we will not be able to generate the revenue or make the models at this kind of scale.”

All eyes were on the parade of earnings reports from the technology behemoths this past week. But what grabbed the markets’ attention were the implications of their massive capital investments in artificial intelligence on their balance sheets and cash-flow statements.

At the center of this debate was Meta Platforms, which plunged 11% on Thursday after reporting a miss on earnings but, more importantly, said it was pushing full-speed ahead on AI data centers, projecting $71 billion in spending, up from $69 billion previously. Moreover, the company said that capital expenditures “will be notably larger in 2026 than 2025.”

All of which is absorbing increasing amounts of megatechs’ cash flow. As Doug Kass of Seabreeze Partners observes, the so-called hyperscalers have morphed from being “capital light” to capital-intensive operations. In the process, they have had to turn to external financing for their ambitious AI buildouts.

In fact, Meta brought this year’s biggest investment-grade corporate bond deal to market, totaling some $30 billion, the latest in a parade of recent data-center borrowing. Bank of America tallies $75 billion of AI-related public debt offerings in the past two months.

And that doesn’t count other financings, including Meta’s creative off-balance-sheet funding of its Louisiana data center, described by colleague Adam Levine in last week’s Tech Trader column. That includes a $38 billion loan tied to Oracle’s data centers, on top of $18 billion of public bonds issued by the company, led by world’s second-richest person, Larry Ellison.

Putting numbers to Kass’ point, BofA credit strategists Yuri Seliger and Sohyun Marie Lee write in a client note that capital spending by five of the Magnificent Seven megacap tech companies (Amazon.com, Alphabet, and Microsoft, along with Meta and Oracle) has been growing even faster than their prodigious cash flows. “These companies collectively may be reaching a limit to how much AI capex they are willing to fund purely from cash flows,” they write.

Based on some of the above interviews and my own analysis, it is clear that if you ask Sam Altman how his OpenAI, a $13 billion money-losing for profit not-for-profit, can support $1.4 trillion of spending commitments, he gets very defensive and starts to attack non-existent short-sellers. (A basic one of my short-selling tenets is to be wary of managements that blame short-sellers).

One of the exchanges between Sam Altman and Brad Gerstner was particularly revealing to me (and might be something that Sam Bankman-Fried might have said in 2021-2:

Sam Altman: "Brad, if you want to sell your shares, I'll find you a buyer (in OpenA)."

This is what you say when you know you've been caught lying. NOT a way to talk to your investors. Sam Altman's response also reminds me of Bernie Madoff's infamous line which was... "I'm not accepting more money."

As noted in 141 issues of my "More Tales From Nvidia," multipleAIissues abound:

From my perch (and after 141 issues of "More Tales From Nvidia"), the conditions and ingredients for another Sam Bankman-Fried fall are there with Sam Altman and AI.

Like Sam Bankman-Fried, Sam Altman seems to possess a faux, contrived persona in a possible attempt to seem harmless. His seemingly intentionally meek voice and matching body language resembles that of the "other" Sam.

In the movie, The Flim-Flam Man, Rusty says the following line after he and his friends catch up to Mordecai and reveal that they know he is a con artist:

"I know who you are. You are Mordecai Jones, the Flim-Flam Man."

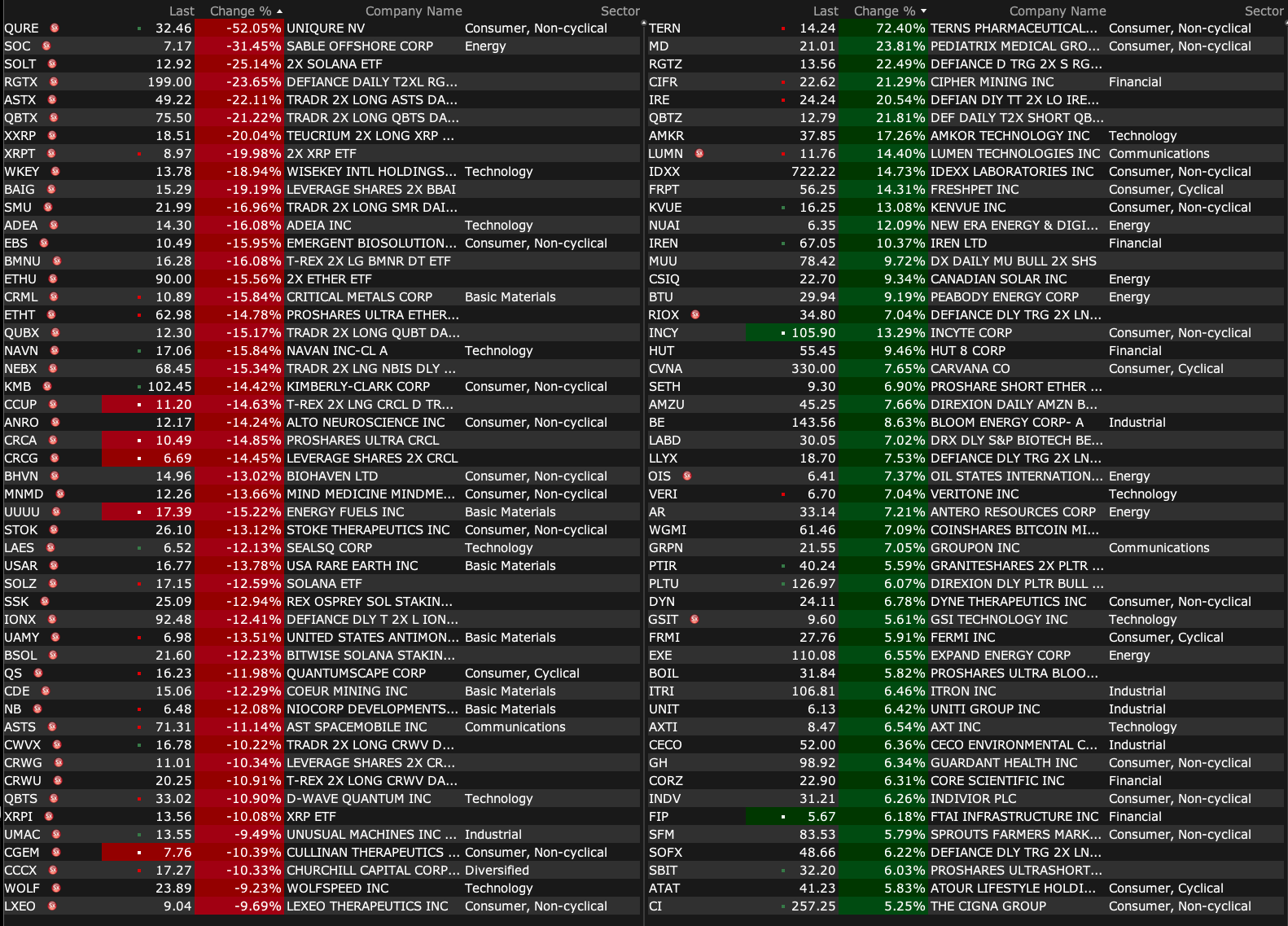

-CRBU +47% (announces Positive Data from ANTLER Phase 1 Trial Demonstrating Efficacy and Durability of Vispa-cel (CB-010), an Allogeneic CAR-T Cell Therapy, on Par with Autologous CAR-T Cell Therapies; announces Positive Data from CaMMouflage Phase 1 Trial of CB-011 in Multiple Myeloma)

-IREN +22% (secures $9.7B AI cloud contract with Microsoft; IREN has also entered into an agreement with Dell Technologies to purchase the GPUs and ancillary equipment for $5.8B)

-IOVA +19% (reports interim data from its registrational Phase 2 IOV-LUN-202 trial of lifileucel monotherapy in patients with previously treated advanced nonsquamous NSCLC without actionable genetic mutations)

-CURR +18% (Animoca Brands merger proposal)

-KVUE +18% (to be acquired by Kimberly-Clark in mostly stock deal with cash part based on EV of $48.7B; Kenvue shareholders will receive $3.50 per share in cash as well as 0.14625 Kimberly-Clark shares for each Kenvue share held at closing)

-CIFR +17% (earnings)

-CMPO +13% (confirms combining with Husky Technologies Limited, manufacturer of engineered equipment and aftermarket service)

-LQDA +9.0% (earnings)

-FRPT +7.7% (earnings, guidance)

-NGD +6.6% (Coeur to acquire New Gold; NGD shareholders will receive 0.4959 shares of Coeur per NGS share, equivalent to $8.51 per New Gold, for total valuation ~$7.0B)

-SNDK +5.2% (strength in memory names)

-MU +3.6% (strength in memory names)

-ON +3.5% (earnings, guidance)

-TGTX +3.5% (earnings, guidance)

-DELL +3.4% (higher in sympathy with IREN)

-CIVI +3.0% (to combine with SM Energy in $12.8B, all-stock combination; under the terms of the Transaction, each common share of Civitas will be exchanged for 1.45 shares of SM Energy common stock)

-MDB +2.8% (guides Q3 above high-end of guidance ranges driven by strength in Atlas; Chirantan Desai appointed President and CEO)

-TOST +2.3% (Toast and Uber announce multi-year strategic global partnership)

-FUBO +2.0% (earnings)

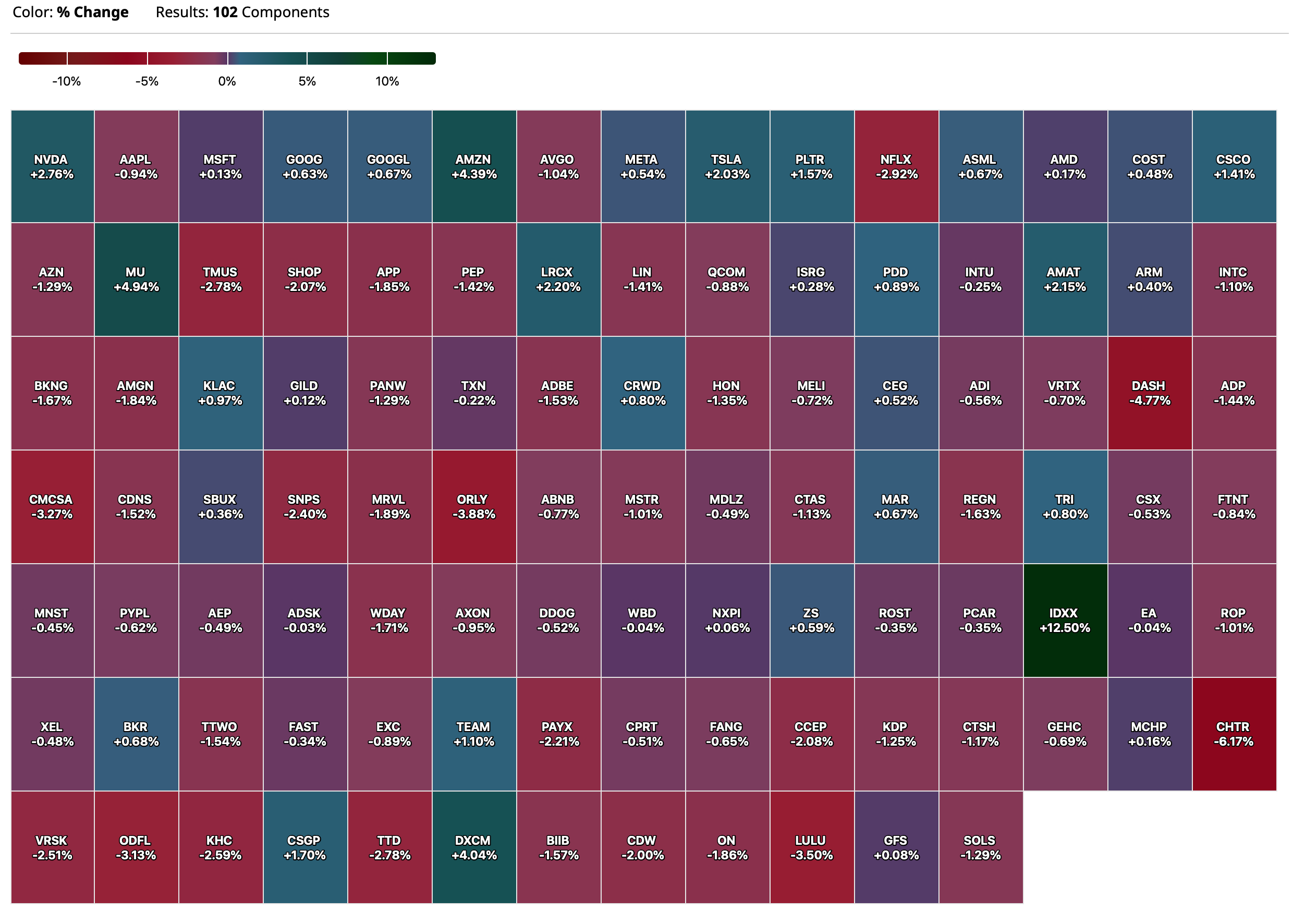

-NVDA +2.0% (reportedly US allows Microsoft to ship Nvidia AI chips to use in UAE for the first time; Microsoft secured export licenses to export advanced NVIDIA A100, H100, and G200 GPUs into UAE)

Downside:

-QURE -60% (believes FDA currently no longer agrees that data from Phase I/II studies of AMT-130 in comparison to an external control, is adequate to provide the primary evidence in support of a BLA submission; Expects to receive final minutes within 30 days of the pre-Biologics License Application (BLA) meeting and plans to urgently interact with the FDA to discuss AMT-130, an investigational gene therapy for Huntington’s disease (HD))

-ALVO -24% (FDA rejects Biologics Application for a biosimilar candidate to JNJ’s Simponi; cuts 2025 outlook)

-BHVN -24% (weakness related to QURE news)

-ADEA -18% (earnings, guidance)

-KMB -14% (acquiring KVUE in mostly stock deal with cash part based on EV of $48.7B; Kenvue shareholders will receive $3.50 per share in cash as well as 0.14625 Kimberly-Clark shares for each Kenvue share held at closing)

-BYND -8.2% (delays Q3 earnings)

-SER -6.2% (U.S. FDA placed a clinical hold on Investigational New Drug (IND) application for SER-252 for advanced Parkinson’s disease)

-CDE -4.6% (Coeur to acquire New Gold; NGD shareholders will receive 0.4959 shares of Coeur per NGS share, equivalent to $8.51 per New Gold, for total valuation ~$7.0B)

Even more Euphoric/No gov't data still but plenty of info out there and I have a lot of it here

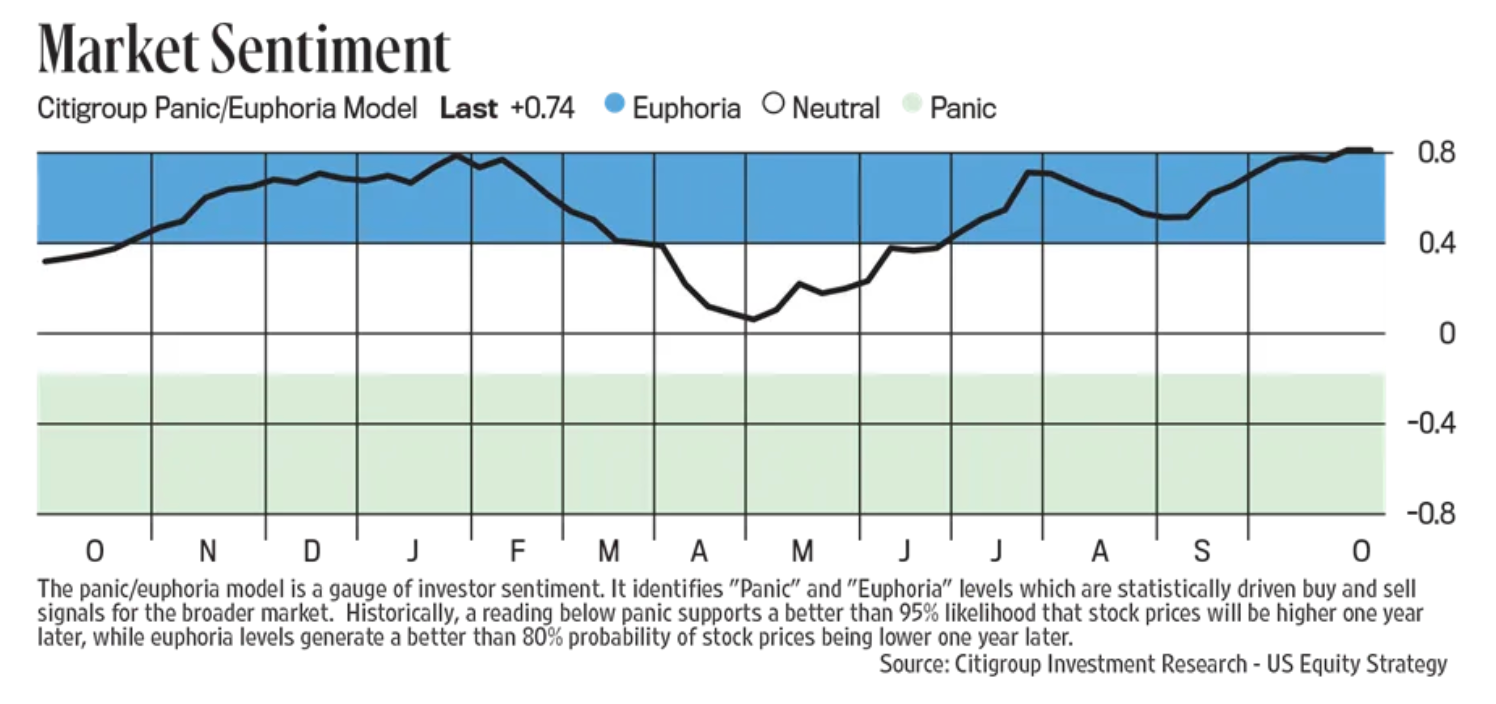

After seeing the number of Bears in the weekly Investors Intelligence survey fall to just 13.5 last week, the lowest since January 2018, the updated Citi Panic/Euphoria index at .74 is now almost double the .41 Euphoria threshold and literally off the chart seen below. In the short term, it’s always good to be aware of one’s investing surroundings and can be currently defined as euphoric, exuberant, giddy, etc…

Not that we needed another reminder of how split in two the US economy is between the AI data center build and upper income spending vs everything else, FreightWaves basically told us what we heard from a bunch of trucking companies over the past few weeks and something that has truly been going on for the past few years.

From them in a new piece, “As someone who’s spent decades immersed in the freight and logistics industry, I’ve learned that freight data often tells the story of the broader economy long before traditional indicators catch up. Right now, that data is painting a stark picture: The US economy is entrenched in a goods recession. While consumer spending on services might be holding steady, the movement of physical goods - the lifeblood of manufacturing, retail, and industrial sectors - has ground to a halt. This isn’t speculation; it’s evident in the high frequency data we track at FreightWaves through our SONAR platform.”

After going through the last five years of traffic volume and with ‘green shoots’ appearing at the end of 2024, “2025 has delivered a gut punch...freight demand has nosedived again, dropping to levels not seen since the depths of the pandemic.”

Some more, “Of the segments that drive freight, retail is holding up far better than other sectors. We know this because freight volumes dispatched out of local distribution centers (within 100 miles) are doing okay. Those volumes are flat y/o/y, but not down. The long haul trucking segment (800+ miles), however, has fallen off a cliff. Y/o/y volumes are down a shocking 30%, a sign that the broader economy is in trouble. Long-haul trucking is more exposed to the energy, manufacturing, auto, and housing segments.”

The glass half full that they talked about is more trucking capacity is leaving the industry and will eventually be good for those that survive.

Here is what one trucking company said on Friday, Werner Enterprises:

“Demand in Q3 was below normal seasonality for most of the quarter. However, we did see improvement in One-Way trucking demand through September and so far in October. While concerns about consumer health persist, consumers remain resilient with rising retail sales and moderate inflation relief. These are supportive signs for retail. However, beneath the surface, there are other concerns. Consumer confidence is lower, real growth is modest, and many cosnumers are in preservation mode rather than expansion mode. And as a result, we like our mix of retail being more concentrated in discount and value retailers.”

As for the holidays, “Customers have provided additional insights into their peak season volume estimates. Shipment forecasts vary by customer, but in total, peak volume and pricing are estimated to be similar to last year, with more balance across the network.”

Similar to what FreightWaves said, “Capacity continues to exit, and recent supply/demand tightening would suggest the pace is increasing, given developments surrounding non-domiciled CDLs (commercial driver’s license), B1 visas and English language proficiency. As challening operating conditions continue, we are also seeing an uptick in bankruptcies as a further limiter.”

What WW Grainger said on tariffs and the pricing actions they have taken and will again was noteworthy:

“In the third quarter, we remain engaged in active dialogue with our supplier partners and used our September price increases to help offset continued cost pressure. While our initial pricing actions back in May only applied to a small portion of our products, largely those where Grainger imported the product directly, the September increase was much broader and included initial pricing actions on supplier imported products, where we have finalized negotiations.”

And, “As we move into the fourth quarter, we’re seeing inflationary pressure continuing to build, including impacts from the recent Section 232 expansion. As a result, we are taking some incremental pricing actions to better align price cost timing as the tariff landscape unfolds. These actions are only modest in nature, but are in addition to the price passed earlier in the year.”

With the big focus on credit and the private equity firms, Carlyle Group, whose stock is down in 8 out of the last 9 days, said this:

“Turning to credit markets, there’s clearly been a lot of focus here over the past several weeks. To date, our own market and portfolio data are not signaling any broad deterioration in overall credit quality or systemic risk...fundamentals remain pretty solid and credit events have been idiosyncratic. Of course, the credit cycle is evolving as it should, repricing where necessary, but again, not flashing broad stress.”

Also, “Capital markets activity has meaningfully accelerated, announced M&A volume was up more than 40% y/o/y in the third quarter, IPO volumes are up 60% year-to-date with increased activity during the quarter.” I’ll add, these are all coincident, not leading, with higher stock prices and tight credit spreads.

From Colgate Palmolive, the maker of pretty stable necessities like toothpaste, deodorant and shampoo:

“consumer uncertainty, tariffs, and geopolitics, high cost inflation, and other factors are all pressuring sales and profit growth across the consumer sector.”

“Consumer still remains relatively weak across North America...We’re seeing higher levels of couponing. Hispanic traffic is still down. And as you’ve heard from others, category takeaway in the US, particularly in September, was a little softer than most of us anticipated and a little softer than preceding months,”

“So clearly a lot of volatility in the market. Particularly in the quarter we’re seeing month-to-month swings that are quite frankly pretty surprising through the quarter. August was very difficult, but September shipments did get better, but just not enough to make up for the August softness we saw.”

From Ethan Allen, obviously impacted by the lower pace of home transactions:

Their DC business was negatively impacted by the government shutdown. Overall, “What we saw was much lower traffic, interestingly, but more qualified people and the ones who came in were buying. And what we saw was that mostly, most of the quarter, we maintained more or less the similar increases. We did not see any major highs or lows during the quarter. What we saw was people coming in, working with our designers, and buying.”

From Camping World:

“consumers are focused on value and affordability across every single segment in the RV industry. Consumers build their monthly financial models around monthly payments, period. We anticipate entering 2026 with consumer sentiment and labor markets uneven and OEM new pricing rising on like-for-like models.”

“While we see signs of resistance on the new side of the business, with our proven track record to address affordability and on used, I believe we can have another record year of combined new and used unit volume growth.”

“we are purposely modeling a conservative outlook on the new RV market, given the OEM prices passed along to dealers.”

From Cheesecake Factory:

“While we, along with the broader restaurant industry, are navigating a softer macro and consumer environment, our overall performance remained stable in line with our expectations.”

Cheesecake comps rose .3% y/o/y. North Italia comps fell 3%, “reflecting sales trends in the broader industry, which softened in the quarter” and they mentioned a few other factors, including “the lingering impact of the Los Angeles fires.”

Flower Child continues to be the fastest growing concept with comps up 7%.

Shifting overseas and ahead of the US ISM manufacturing index for October, we saw a bunch from overseas and the mixed bag situation in this sector continues. South Korea 49.4 vs 50.7, Taiwan 47.7 vs 46.8, Japan 48.3 vs 48.5, Vietnam 54.5 vs 50.4, Indonesia 51.2 vs 50.4, Thailand 56.6 vs 54.6, Malaysia 49.5 vs 50.7, the Philippines 50.1 vs 49.9, and Australia 49.7 vs 51.4. The standout performer remains India at 59.2 vs 57.7 while China’s private sector focused index remained around 50 at 50.6 vs 51.2 in the month before.

With China specifically, RatingDog said “On the demand side, heightened trade uncertainty in October caused new export orders to fall sharply into contraction territory, dragging down the new orders reading. Market concerns about weakening exports persisted.”

On pricing, “the divergence of rising raw material prices and falling finished goods prices continued, keeping corporate profit margins under pressure. Due to concerns about the external demand environment, goods producers reduced their export charges for the first time since April this year.”

The final Eurozone read was exactly 50 vs 49.8 in September and vs 50.7 in August. The UK index at 49.7 was up from 46.2 but hasn’t been above 50 since September 2024.

More Tales From Nvidia: Riddle Me This, AI (Issue #141!)

Apple (AAPL) is getting rewarded for not burning cash on AI. Can people make up their minds? And yes, there is massive overlap between the owners of Apple and all of these other things. The answer I guess continues to be it goes up.

Alphabet said it expects to spend about $92 billion on capital expenditures this year. Microsoft said it spent about $34.9 billion on capex during the September quarter and will spend more in capex for its fiscal 2026 than it did the year prior. Meta stock got whacked after CEO Mark Zuckerberg defended the company’s plan to spend about $71 billion on AI chips and other expenses in 2025. On Thursday, Amazon raised its 2025 spending forecast 6% to $125 billion. Compared to them, Apple’s barely spending at all. In its fiscal 2025, which ended in September, Apple spent $12.72 billion on capital expenditures.

"After seeing the number of Bears in the weekly Investors Intelligence survey fall to just 13.5 last week, the lowest since January 2018, the updated Citi Panic/Euphoria index at .74 is now almost double the .41 Euphoria threshold and literally off the chart seen below. In the short term, it’s always good to be aware of one’s investing surroundings and can be currently defined as euphoric, exuberant, giddy, etc..."

US: Futs are higher led by Tech with RTY flat. Pre-mkt, bond yields are up 1bp across the curve with the USD seeing a slight bid. In stocks, Mag7 are all higher with Semis also bid; Cyclicals poised to lead Defensives with both higher. Cmdtys are mixed with Ags leading, Metals weaker, and Energy mostly lower ex-natgas. China suspends curbs on rare earths and suspends chips investigation. OPEC+ looks to pause its supply expansion next qtr ahead of expected demand declines / supply glut. SCOTUS to hear IEEPA tariff challenges with the market expecting those tariffs to be struck down and later replaced by sectoral tariffs and could trigger a near-term squeeze/broadening subject to moves in the bond market.

and...

PM MARKET INTEL EQUITY & MACRO NARRATIVE

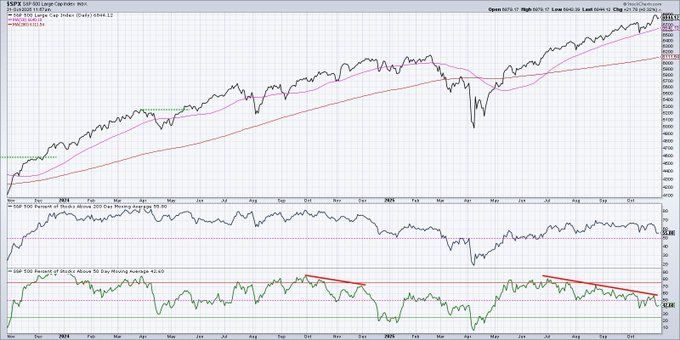

The SPX closed October with a 2.3% gain, its sixth consecutive monthly gain, with the index now up 37.3% since the April 8 low. This compares to NDX +51.3%, RTY +40.8%, Mag7 (JP1BMAG7 Index) +71.1%, and SWP (equal-weighted SPX) +22.8%. With the major indices all within 170bp of their all-time highs, the question is whether there is another leg higher into year-end. We think yes and maintain our Tactical Bullish call as (i) we see the macro picture improving in the near-term, (ii) earnings printing materially above expectations, and (iii) Trump’s Asia trip leading to lower net effective tariff rates and unlocking the rare earth supply chain. We see the key risks coming from (i) AI exhaustion and (ii) higher bond yields / spike in bond volatility. In the remaining sections we provide more color on our thinking plus an update from our colleagues in Positioning Intelligence.