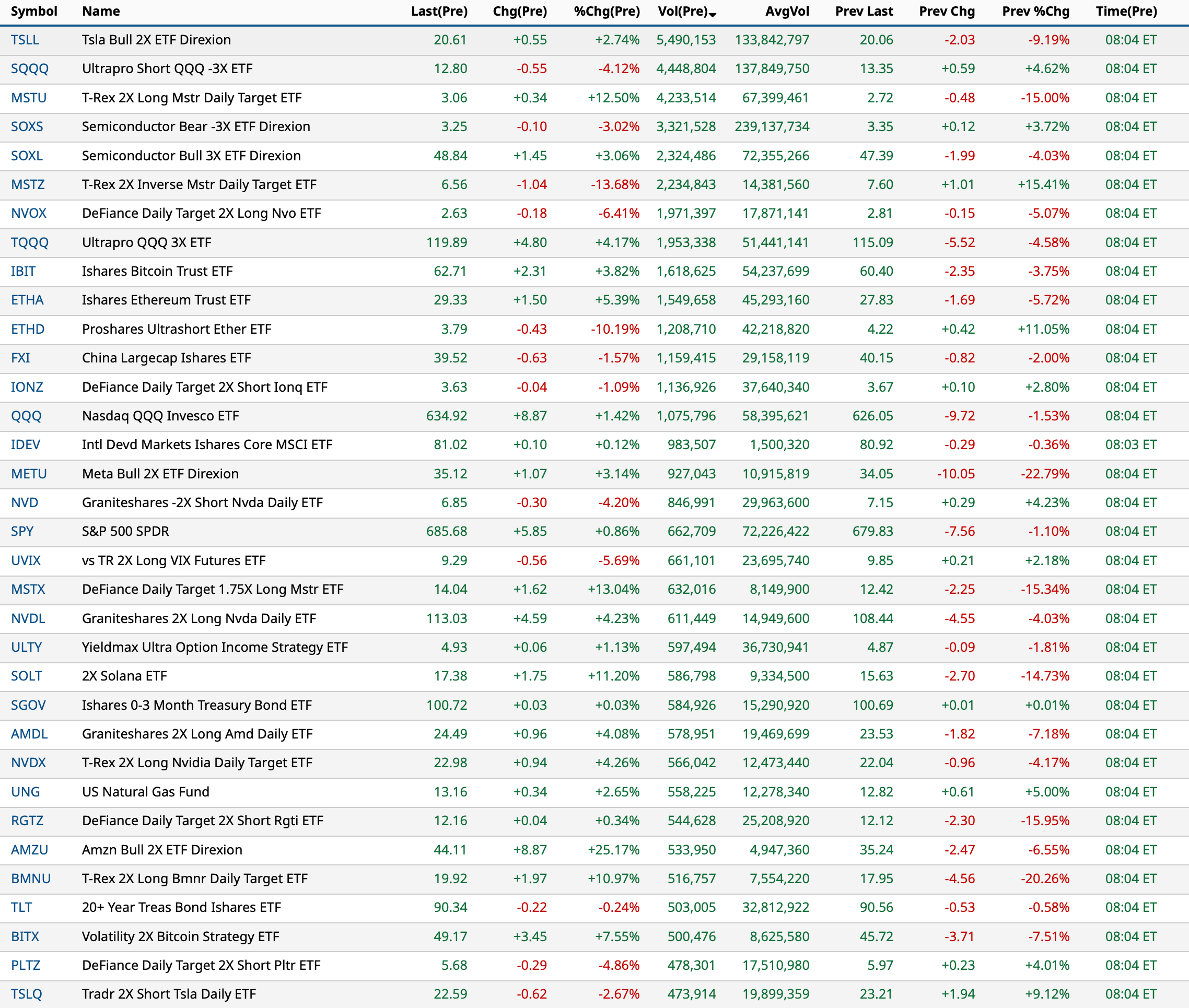

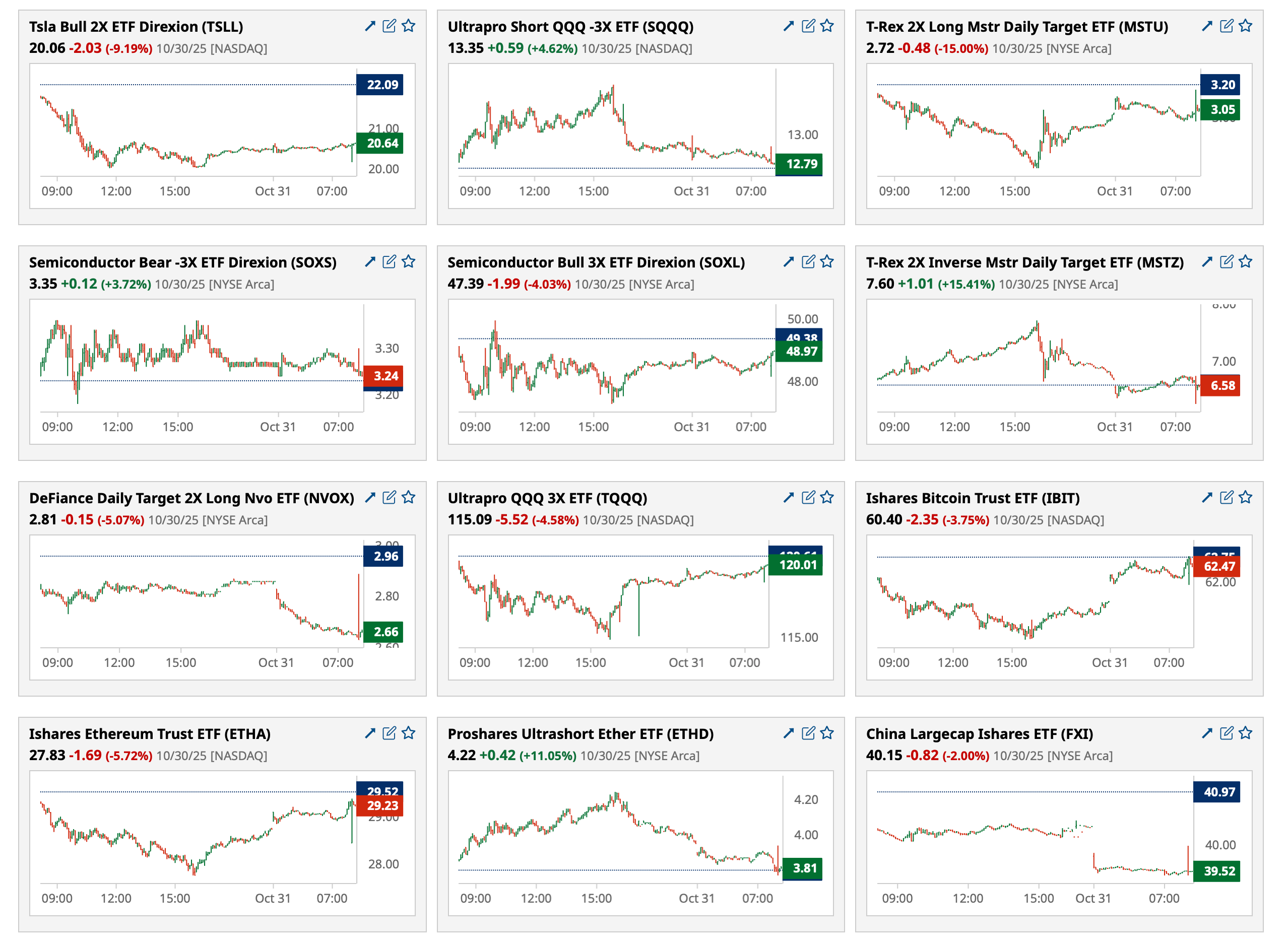

Friday's Closing Market Stats

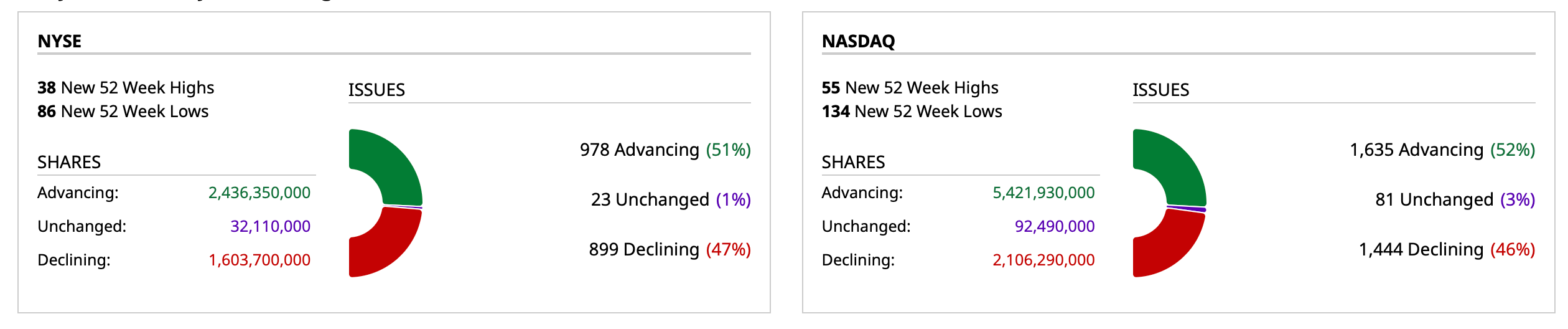

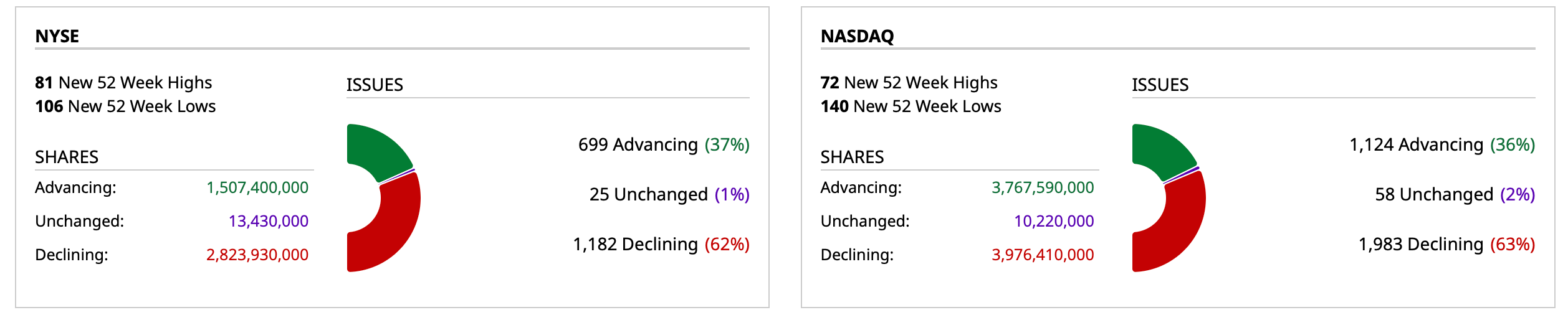

Closing Breadth

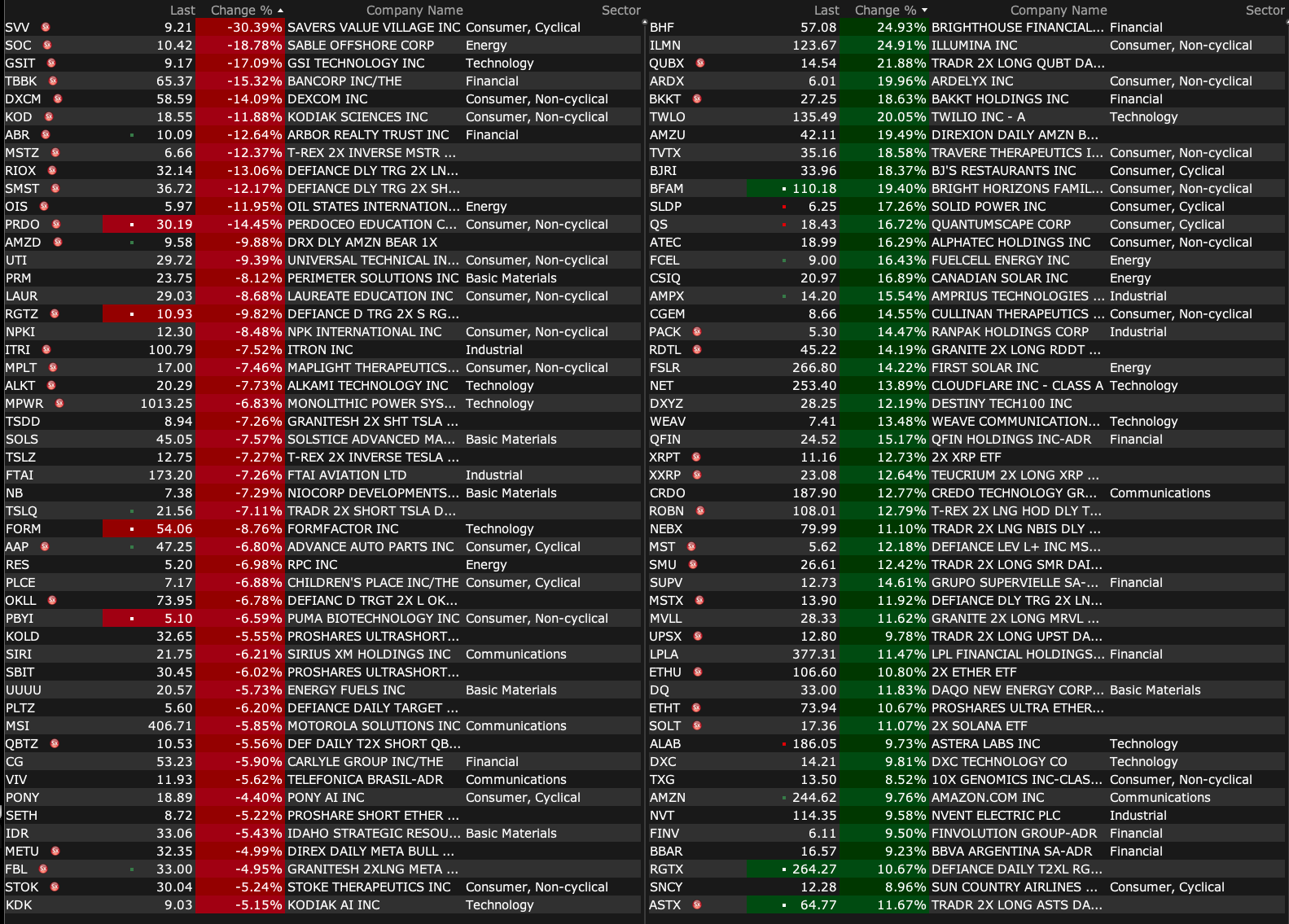

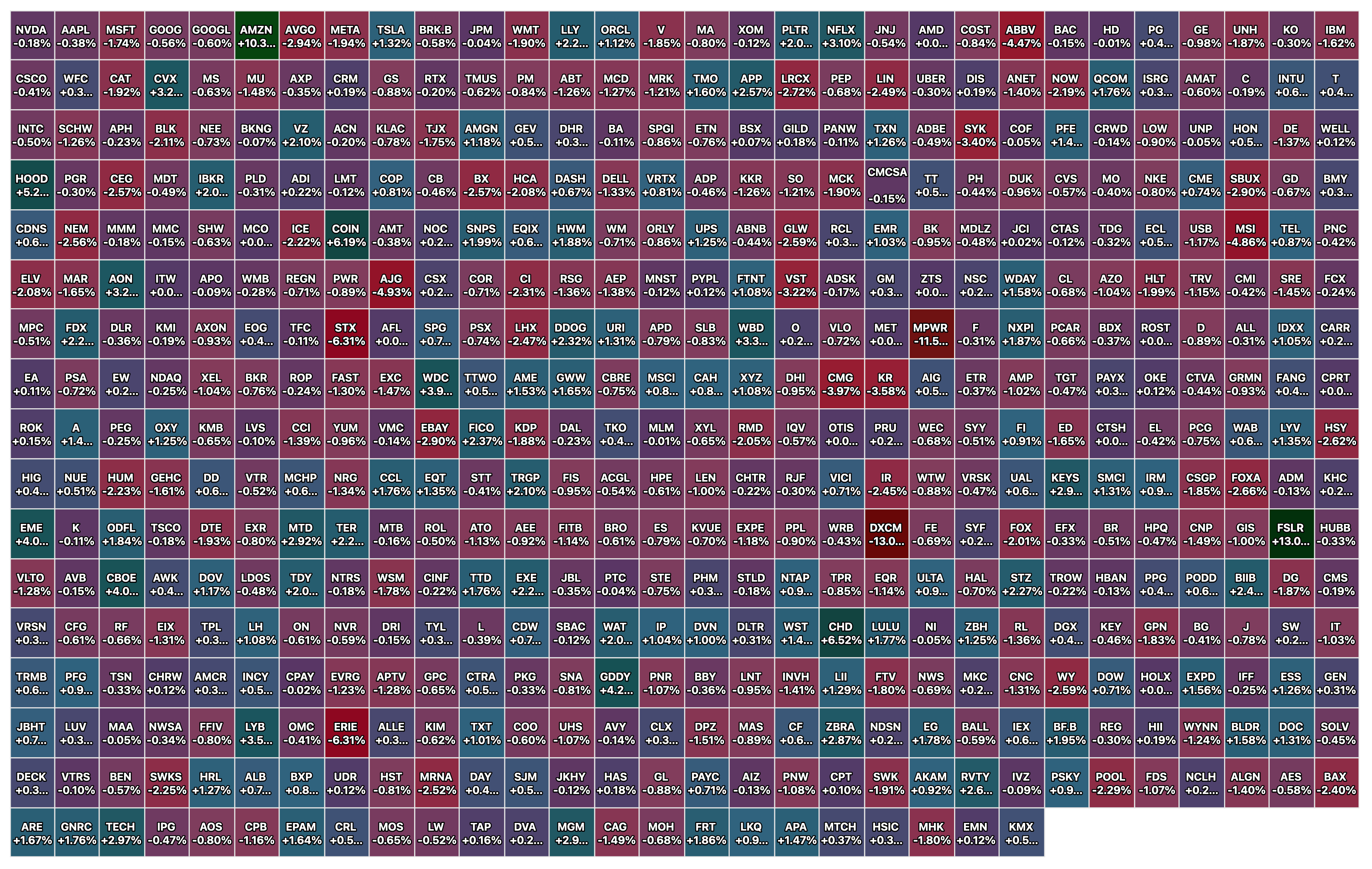

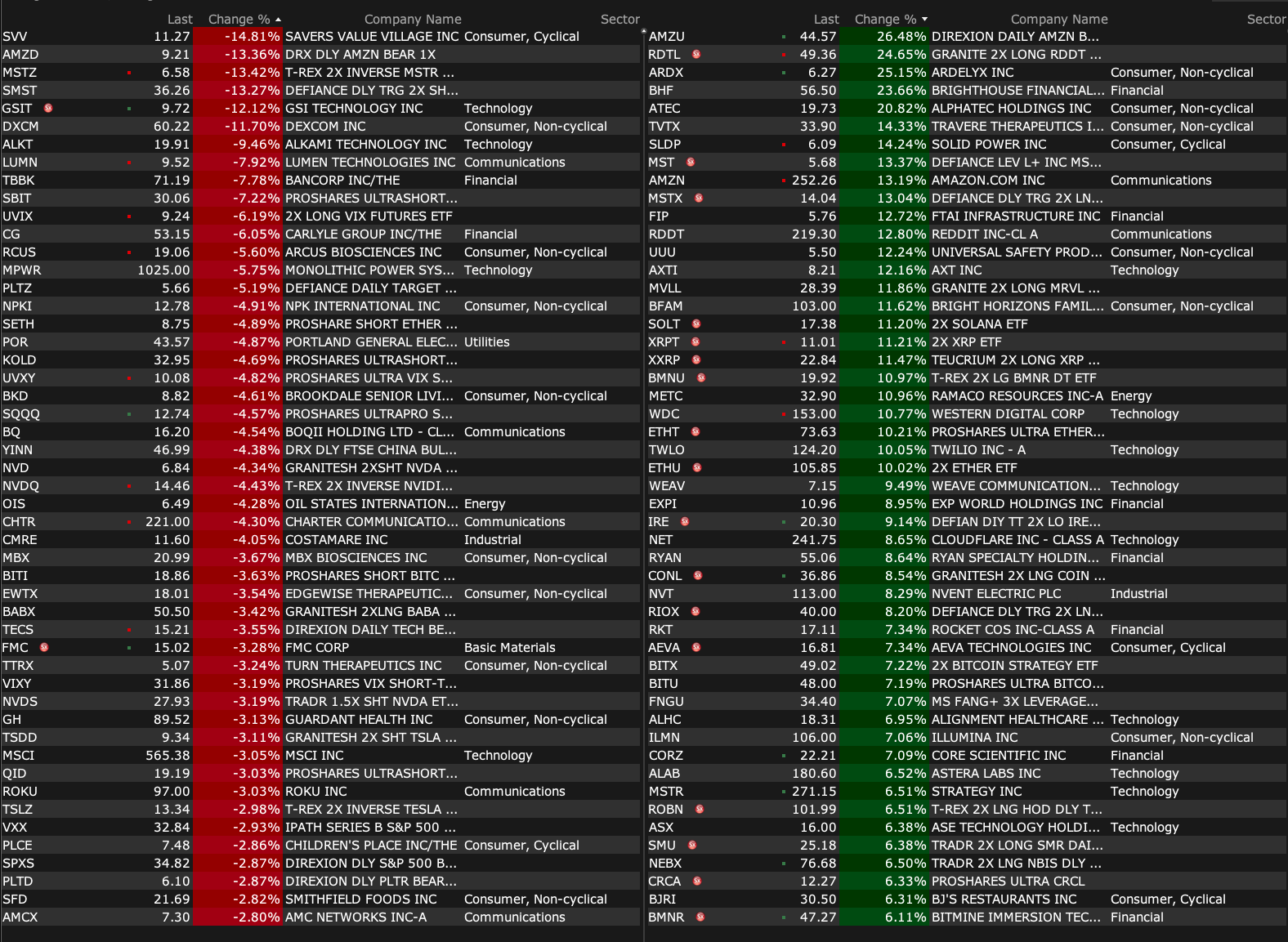

% Movers

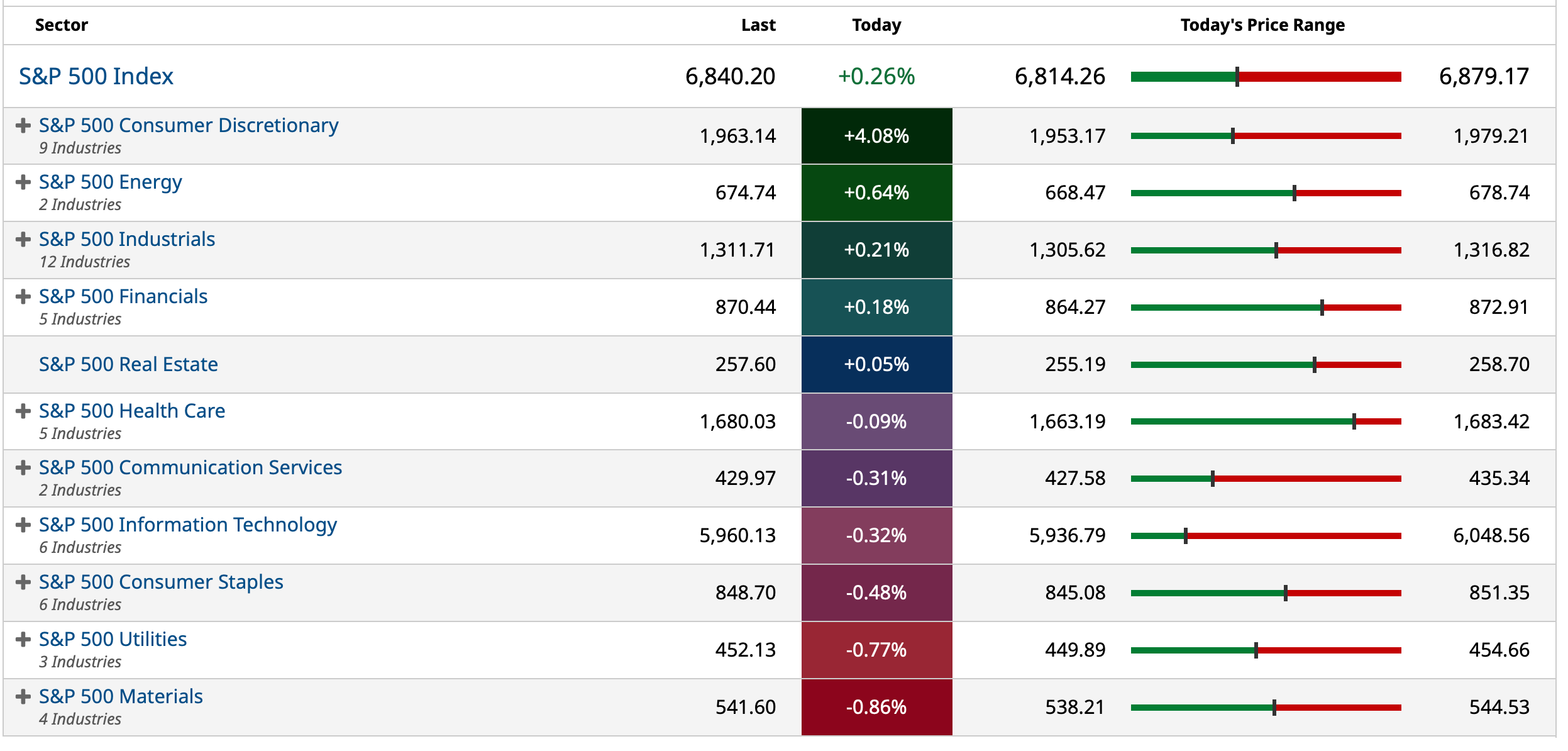

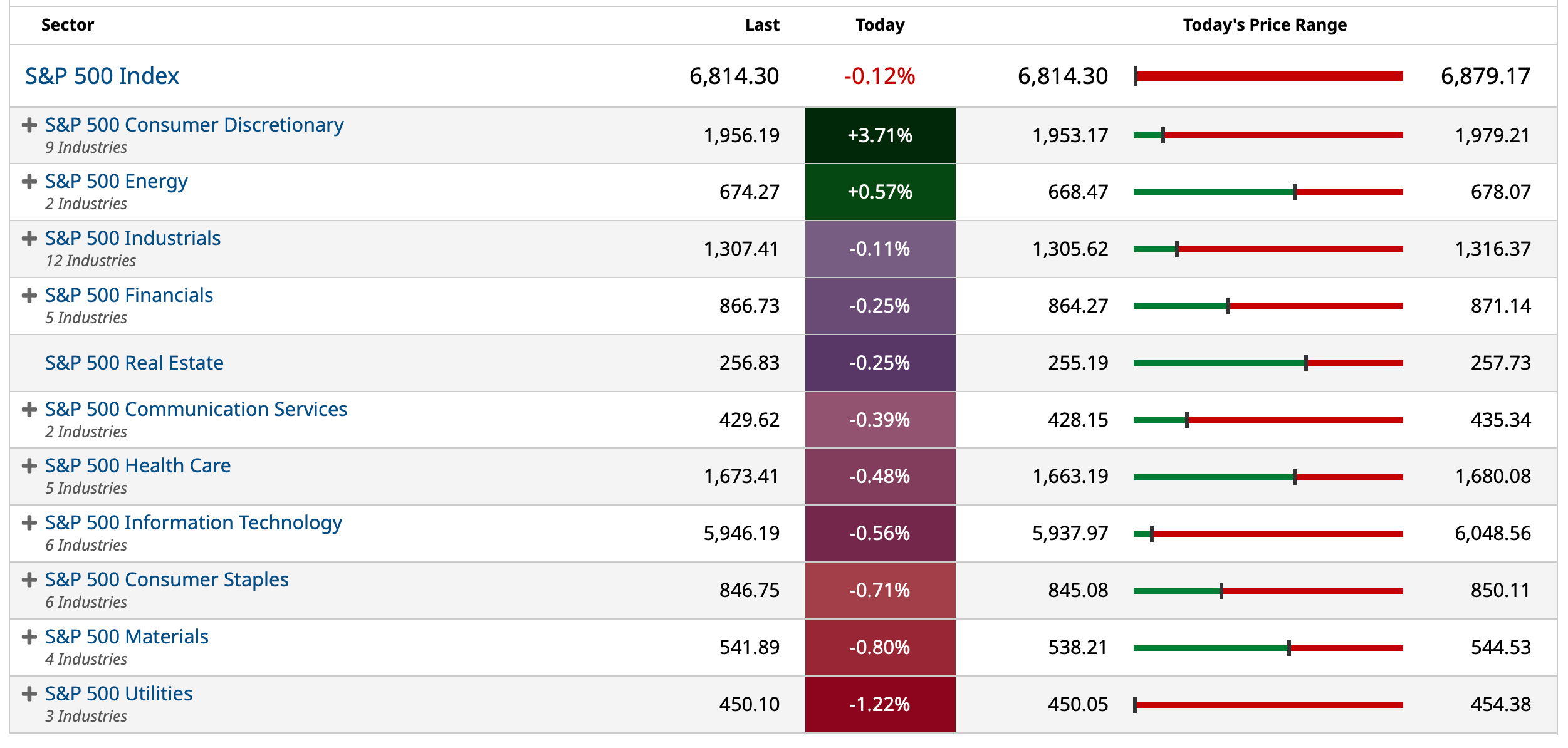

S&P 500 Sectors

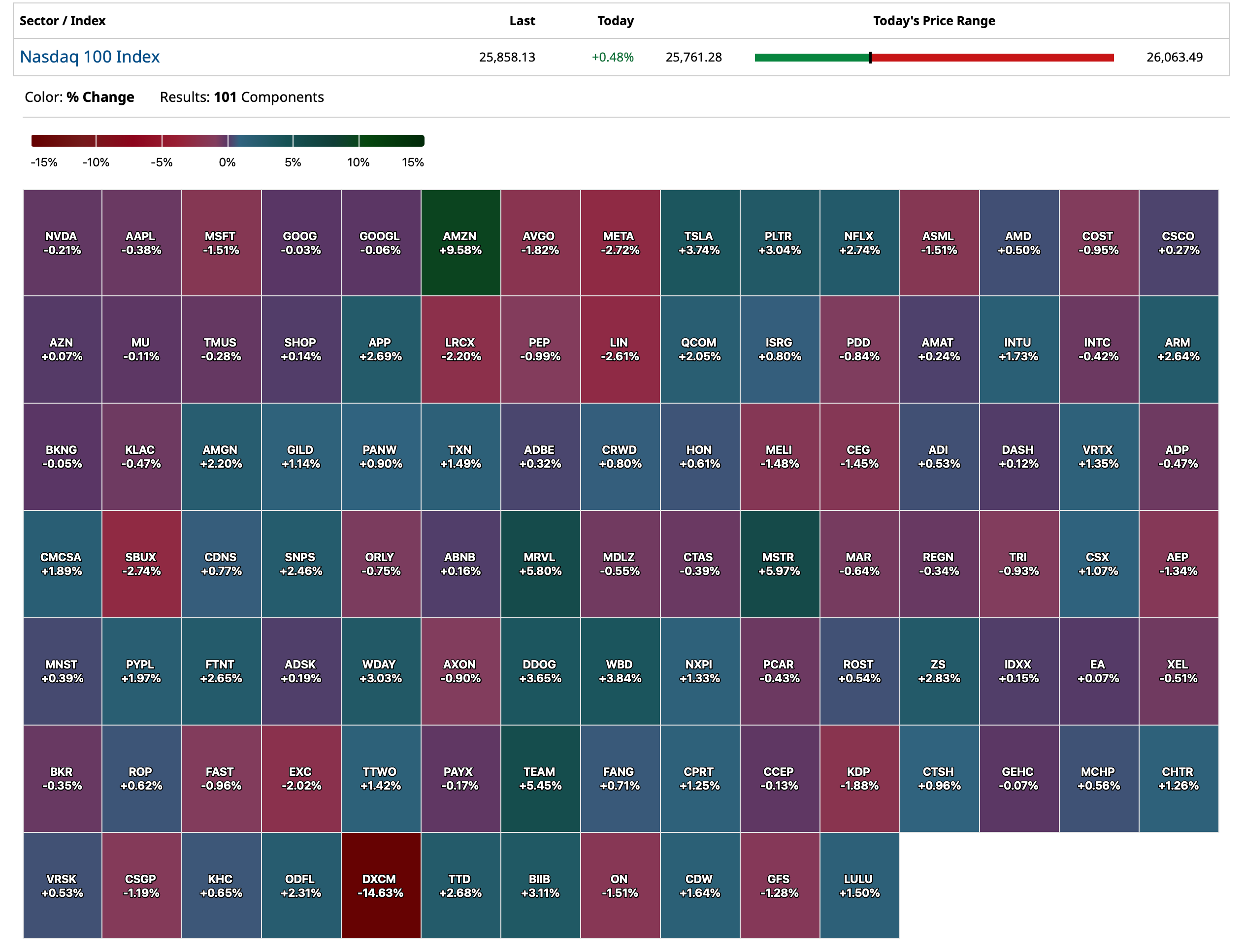

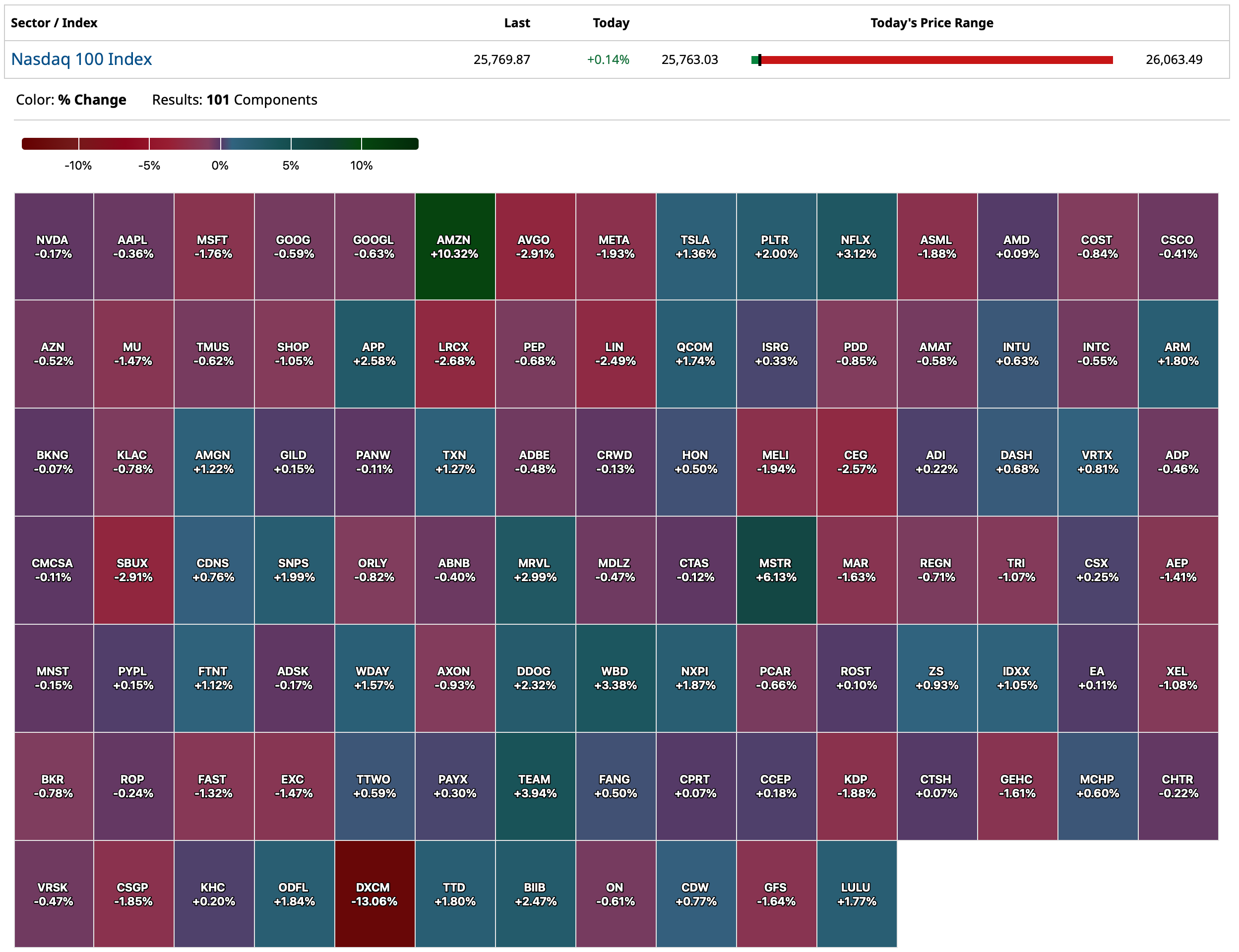

Nasdaq 100 Heat Map

BY Doug Kass · Oct 31, 2025, 4:42 PM EDT

BY Doug Kass · Oct 31, 2025, 4:42 PM EDT

With S&P cash +39 handles I am back shorting index calls (for December).

BY Doug Kass · Oct 31, 2025, 3:52 PM EDT

Breadth continues its week-long deterioration (about 2-1 negative on the NYSE and Nasdaq):

BY Doug Kass · Oct 31, 2025, 2:07 PM EDT

BY Doug Kass · Oct 31, 2025, 1:53 PM EDT

BY Doug Kass · Oct 31, 2025, 1:17 PM EDT

BY Doug Kass · Oct 31, 2025, 12:21 PM EDT

BY Doug Kass · Oct 31, 2025, 11:20 AM EDT

JOE, one of my few longs, had better than expected results yesterday. The St. Joe Company Reports Third Quarter and First Nine Months of 2025 Results and Increases Quarterly Dividend by 14% to $0.16 Per Share | The St. Joe Company

The shares traded up five to six dollars yesterday and is up another two beaners today.

More next week on this name.

BY Doug Kass · Oct 31, 2025, 11:15 AM EDT

With the market rallying smartly off of the lows, I am adding to my speculative basket of high octane, high beta stocks.

Names withheld to protect the innocent traders!

BY Doug Kass · Oct 31, 2025, 11:05 AM EDT

BY Doug Kass · Oct 31, 2025, 10:49 AM EDT

Not specific to Amazon (AMZN) , same story for all of them.

Cash is being lit on fire whether it hits the P&L or not.

This eventually will make its way into the P&L, one way or another.

Watching cash flow now tells you where earnings go in the future.

BY Doug Kass · Oct 31, 2025, 10:40 AM EDT

I have covered my Index shorts on the 30 handle drop from the day's highs ) and with S&P cash up by only +24 handles):

* (SPY) $683.12

* (QQQ) $631.96

From earlier today:

I added to my VS index shorts:

* (SPY) $686.42

* (QQQ) $635.53

Position: Short SPY VS QQQ VS

I plan to reshort strength - if there is any - this afternoon and at the day's close (if there are month-end markups).

BY Doug Kass · Oct 31, 2025, 10:34 AM EDT

BY Doug Kass · Oct 31, 2025, 10:25 AM EDT

Oct 31, 2025∙ Paid

Many of you have probably read about 3I/Atlas, the comet discovered in July after it entered our solar system from another star system. It was given its name because it is the third object known to have entered our solar system and was discovered by the Atlas telescope in Chile. Early in October the comet came within 18 million miles of Mars and in late October was expected to make its closest approach to the sun. In December, it is expected to make its closest approach to the earth – 167 million miles away. Harvard astrophysicist Avi Loeb notes the comet is currently unobservable from earth because it is on the other side of the sun but claims it changed appearance in earlier photographs and may have the characteristics of a technological rather than a naturally-formed object. His speculations have set conspiracy theorists on fire pondering a close encounter from another solar system. Loeb himself notes (with a smile) that such an event could set off a stock market crash or other cataclysmic possibilities. At this point, aliens visiting earth might be the only thing that could derail this stock market rally (and no doubt Jensen Huang, Sam Altman, Elon Musk and Donald Trump would greet the space craft with open arms). I place the odds of 3I/Atlas visiting earth as roughly the same as our government returning to sanity; let’s just hope those odds are much lower than mankind achieving AGI before the technology industry bankrupts itself.

Back here on planet earth, the Fed cut interest rates as expected by another 25 basis points on October 29th. The only news that emerged from the October Fed meeting was that another December cut was not a certainty which sent stocks down slightly because it contradicted market expectations. With the government closed and limited data to work with, the Fed is flying blind with respect to setting policy. But given the data that is available, it seems set on an easing cycle that has little to do with its dual mandate. Instead, its actions support the argument that we are in a period of “fiscal dominance” where monetary policy is driven by fiscal policy needs which in this case means lowering rates to reduce the cost of servicing the deficit.

Click here for the rest...

BY Doug Kass · Oct 31, 2025, 10:15 AM EDT

I am short Carvana.

CARVANA FRAUD: THE SMOKING GUN - JustDario

This is a wild and volatile stock.

90% of retail investors should never short.

99.9% of retail investors should not short the stock.

BY Doug Kass · Oct 31, 2025, 10:00 AM EDT

I just covered last night Apple (AAPL) short at $269.85 (shorted last night at $283.69!) - for a gain of $14/share in less than 18 hours.

From last night:

I shorted Apple (AAPL) at $283.69.

I'm stepping up my (QQQ) short at $633.15.

By Doug Kass Oct 30, 2025 5:40 PM EDT

Position: Short AAPL (S), QQQ (VS)

Short QQQ VS

Oct 31, 2025 6:29 AM EDT

BY Doug Kass · Oct 31, 2025, 9:47 AM EDT

From Peter Boockvar:

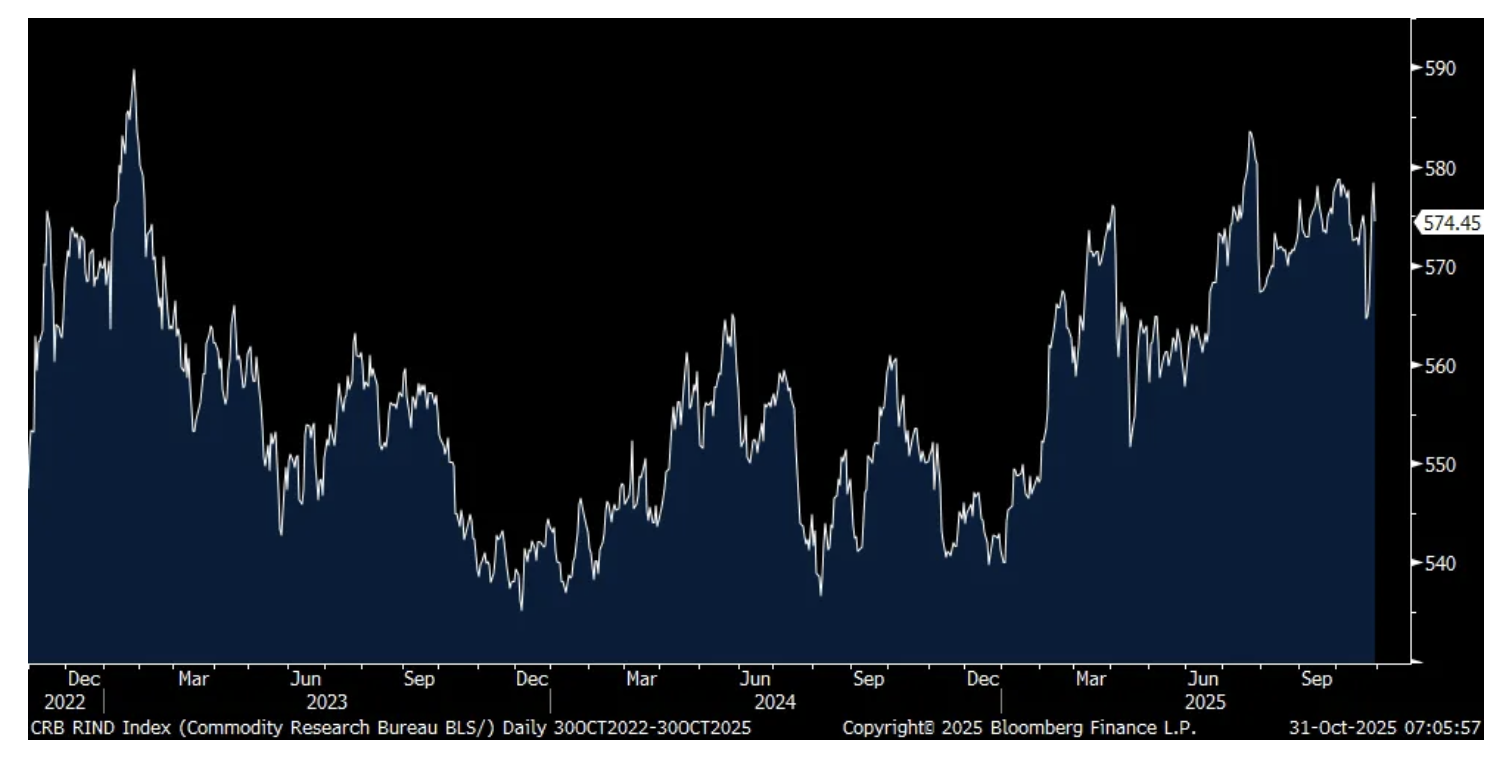

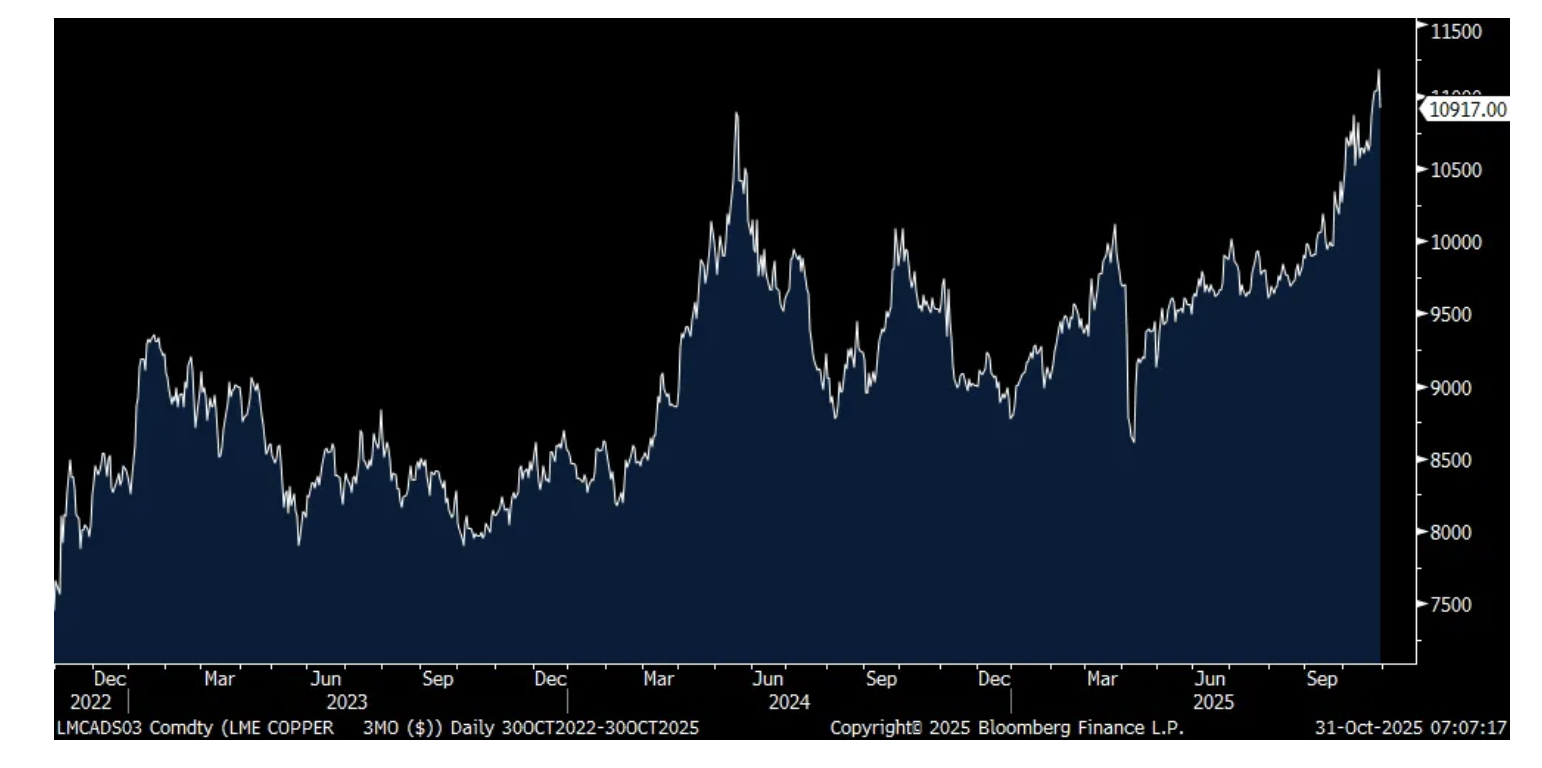

The record high price in copper has helped to lift the CRB raw industrials index to just below the highest level since January 2023. Specifically copper scrap is in this index.CRB Raw Industrials index

Copper

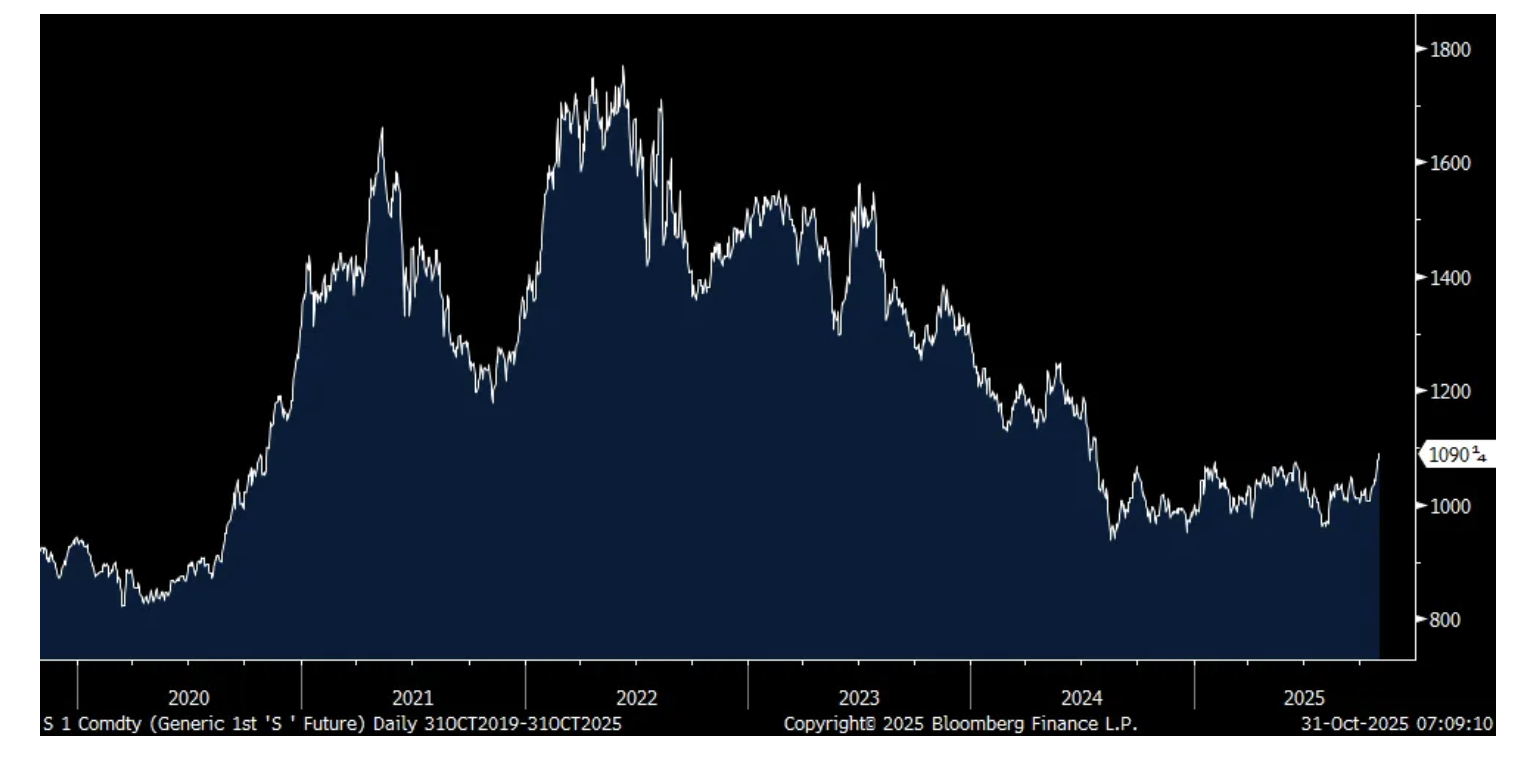

With China buying US soybeans again, the price has risen to the highest since July 2024 but still well off its multi year highs seen a few years ago. Corn and wheat prices both remain depressed and we still own fertilizer stocks believing that crop prices are cheap.

Soybeans

The 10 yr JGB yield is again knocking on multi year highs, up 1.3 bps overnight to 1.67% after Tokyo October CPI exceeded expectations. Ex food and energy it was up 2.8% y/o/y, 2 tenths more than estimated and up from 2.5% in September. The headline gain was also 2.8%, above the forecast by 4 tenths. The end of subsidies for water was a main reason. What the BoJ is waiting for to hike rates again is a mystery to me as those subsidies were put in to protect people from inflation that the BoJ doesn’t seem intent on wanting to fight back against. Also out, the Japanese jobs data was as expected thru September.

China’s manufacturing PMI remained in contraction at 49 in October, down from 49.8 last month. The non-manufacturing PMI was flattish at around the flatline coming in at 50.1 vs 50 in September. Overall, about at the flatline for this state sector weighted measure of their economy. The private sector figures come out in a few days and most of the Chinese economy is actually private with more than 80% of employment working for private industry.

In Europe, a day after the ECB held rates unchanged as expected and seems to be set there for now, the October Eurozone CPI rose 2.1% y/o/y as expected and vs 2.2% in the month before. The core rate at 2.4% was one tenth above the forecast and unchanged with September. So, with a deposit rate of 2%, the ECB believes the neutral rate in Europe is slightly negative. European yields are up a hair in response and the euro is up a touch. Stocks there are down. The 5 yr 5 yr euro inflation swap is little changed at 2.06% which is where the ECB wants it to be.

Now to the earnings calls which in the aggregate, reads like the Fed’s Beige Book and sounds like an economy that is barely growing outside of the obvious pockets of strength.

From SAIA, the trucking company whose stock traded up on good execution, particularly cost control:

They said “the economic backdrop continued to exhibit the trends seen throughout 2025, with customers awaiting a more certain environment.”

“If we look at October so far, we’ve seen trends be a little bit, depending on the day, up and down a little bit. I think there’s maybe a few things that could be attributable to, but the first couple of weeks were a little bit lighter than we anticipated.”

From Eagle Materials, down 6%:

“In line with our expectations, our cement and aggregates volume increased for the 2nd consecutive quarter and were up for the first half of the year. The backdrop for cement and aggregates volumes remains favorable for the remains of our fiscal year for several factors. About 60% of the investment in the Infrastructure and Jobs Act or IIJA funds have yet to be spent and all signs point to those IIJA dollars flowing into construction projects.”

“We also continue to believe private non-residential construction dynamics should support cement construction. Against the improving volume outlook for cement and aggregates, we have announced price increases across most of our markets effective January 1, 2026.”

“Our views regarding residential construction activity, the primary driver for wallboard consumption, remains more reserved in the near term. Volumes this quarter are affected by reduced demand due to high interest rates and affordability challenges. As the builders pulled back over the summer, our wallboard volumes were impacted.”

From Hershey whose stock was down but seemed to have had a good quarter though much had to do with price increases:

Its Candy, Mint and Gum (CMG) category saw sales rise 5.4% y/o/y. “This strong performance was balanced across core brands and innovation as well as across instant consumables and take home items.” In particular, Reese’s, Hershey, Cadbury and Jolly Rancher did well.

Overall, sales rose 6.2% in constant currency and “was driven by net price realization of approximately 6 points along with slight volume growth in the third quarter. Net price realization reflects the combination of pricing announced in 2024 and 2025, and only partially mitigates commodity cost inflation absorbed over the last two years.”

Maybe this is why the stock fell, “Although the Halloween season began slower than anticipated, it was likely influenced by factors such as warmer weather conditions, and a concentration of seasonal purchases in the final week due to Halloween occurring on a Friday. While Hershey’s Halloween performance has been disappointing, the softness is not broad based across our business. We are using this opportunity to analyze the trends and will adjust our product lineup and marketing strategies for future seasons.”

Their salty snack business had a good quarter led by Pirate Booty and Skinny Pop.

From Kimberly Clark, a stock we own and up about 2% yesterday:

They referred to the macro as “dynamic and consumers remain under pressure” but luckily for them, they sell products like tissues and toilet paper that everyone needs, as well as diapers, for both babies and adults.

From Reynolds Consumer Products, another staples stock we own that is cheap with a good dividend:

They also mentioned the “challenging environment” but when selling tin foil and garbage bags which benefit from more people eating at home, business is not bad. They also gained market share in the quarter.

“Turning to the environment. The operating environment remains challenging with low and middle income consumers under continued pressure and retailers facing cost inflation, especially from overseas suppliers subject to tariffs.”

On the consumer, “I think when we initiated the 2025 guide, we talked about a consumer that was challenged and under pressure, that remains to be the case…And as we think about elements of the economy, we still see inflation in that sort of 3% zone, above the Fed’s target of 2%, so generally not helpful or ideal. Number two, we also see the labor market cooling a bit, unemployment levels in the low 4s. But I think the most important one as we see it would be consumer sentiment. Yet again to move 3, 4 points down in terms of confidence in the month of September. October came out last night, down again a point, but the takeaway there to me is we’re double digits down year-to-date heading into the holidays. So we remain of the view that consumer is under pressure.”

From International Paper that plunged by 13% yesterday:

“macro conditions in North America and EMEA continue to be challenging.”

“As we move to demand, as we came into the year we anticipated US box industry shipments would be up 1% to 1.5%. However, we now expect industry shipments to be down approximately 1% to 1.5% for the full year due to factors like trade uncertainty, soft consumer sentiment, and weak housing market.”

“Similarly, in EMEA, our expectation coming into the year was for box volume to be in the 2% to 3% range. We’re now seeing that closer to 1%.”

From Malibu Boats that also fell by 13%:

“As expected, retail activities remained soft, and inventories entering the quarter were slightly elevated.”

“Looking ahead, we will continue to remain realistic about the broader marine environment. While we have yet to see a clear inflection signaling a broader market recovery, our focus remains unchanged.”

Carvana fell 14% yesterday because of light guidance and said this on credit quality and the subprime auto concerns that are widening:

“So the very simple answer on loan performance is our 2024 and 2025 loan originations are performing extremely well, both in an absolute sense and relative to industry comparables. I think some of the chatter out there about loan performance more broadly, we think has a lot to do with the 2022 and 2023 industry wide cohorts, which did underperform initial expectations.”

“I think most of the industry, ourselves included, tightened credit in late 2023. We certainly did, and we’ve maintained that tightness here through where we are today in 2025. As a result, our loans are performing strongly.”

Broadly, they remain optimistic on the macro, “things feel relatively stable. I think we’re always paying close attention. And I think while we don’t see signs of macro weakness today, I think that we’re very well positioned if I guess when that does come to pass. At some point there will be cycles.”

From Mastercard:

Similar to what Visa said, “We continue to see healthy consumer and business spending in the quarter, with the macroeconomic environment still generally supportive. Inflation levels have remained fairly steady, and labor markets remain well balanced. Financial markets were near record highs, further contributing to the wealth effect, which helps to stimulate spend.”

I’ll add, it all depends on who your customer is because the overall macro is hugely mixed and they benefit from inflation directly and the secular trend of using digital payments over cash.

From Shake Shack:

“Now going to October, our sales trends, although positive, were not consistent with what we saw in the third quarter. Macro headwinds to the industry did intensify, and we are lapping one of the most iconic LTOs (limited time offer) in our history, Black Truffle. We continued to invest in advertising and media to support the business. However, our French Onion Burger LTO, while loved by the media, has not been as accretive to traffic or check as was the case for our LTOs in Q3.”

“We had positive comps in traffic in nearly all of our regions. However, we continue to see macro pressures in New York Metro and Washington, DC, that are weighing on our overall results. New York Metro and DC represent over a quarter of our sales, and we have been experiencing a higher degree of macro pressure in these regions than many industry peers, given our footprint today. So, a challenging macro backdrop here continues to have an outsized impact on our overall performance.”

From Amazon, obviously up big pre-market:

Overall revenue growth was 12% y/o/y with AWS accelerating to 20.2%, “our largest growth rate in 11 quarters.”

With AWS, “Backlog grew to $200 billion by Q3 quarter end and doesn’t include several unannounced new deals in October, which together are more than our total debt volume for all of Q3. AWS is gaining momentum.” I’ll add, as long as this GenAI data center buildout continues, but hopefully they’ll benefit from the inference side on the other end.

North America saw sales up 11% and international by 10% y/o/y. Unless I missed it, I did not see one question from analysts on what Amazon is seeing on the consumer which is strange considering we’re talking about one of the biggest retailers.

On CapEx, it was $34.2b in Q3 and have spent $89.9b year to date. “This primarily relates to AWS as we invest to support demand for AI and core services and in custom silicon, like Trainium, as well as tech infrastructure to support our North America and International segments...Looking ahead, we expect our full year cash CapEx to be approximately $125 billion in 2025, and we expect that amount will increase in 2026.”

That is 17.6% of expected 2025 revenue which compares with 13% in 2021. Not as much of a difference between the years when compared to the skyrocketing rates of CapEx growth seen with Oracle, Microsoft, Meta and Google.

From Apple:

On the December quarter, “We expect iPhone revenue to grow double digits y/o/y, which would be our best iPhone quarter ever.”

BY Doug Kass · Oct 31, 2025, 9:45 AM EDT

BY Doug Kass · Oct 31, 2025, 9:20 AM EDT

-GETY +51% (Getty Images and Perplexity announce multi-year global licensing partnership, granting Perplexity access to Getty’s creative and editorial imagery through its API)

-ARDX +25% (earnings, guidance)

-BHF +24% (Aquarian said to near $4.0B deal to take Brighthouse private)

-ATEC +21% (earnings, guidance)

-AMZN +13% (earnings, guidance)

-RDDT +13% (earnings, guidance)

-SSTK +12% (Getty Images and Perplexity announce multi-year global licensing partnership)

-WDC +11% (earnings, guidance)

-METC +10% (executes Far-Reaching Strategic Agreement on Rare Earths and Critical Minerals with U. S. Department of Energy's (DOE) National Energy Technology Laboratory; t aps Goldman Sachs as structuring agent for Strategic Critical Minerals Terminal)

-TWLO +10% (earnings, guidance)

-NVT +8.3% (earnings, guidance)

-NET +7.8% (earnings, guidance)

-RKT +7.4% (earnings, guidance)

-ILMN +6.6% (earnings, guidance)

-MRVL +5.5% (strength off AMZN Trainium commentary)

-FSLR +5.3% (earnings, guidance)

-CHD +5.2% (earnings, guidance)

-LYB +5.2% (earnings)

-COIN +4.4% (earnings, guidance)

-SXT +4.3% (earnings, guidance)

-AGCO +3.8% (earnings, guidance)

-RIOT +3.0% (earnings)

-WBD +3.0% (reportedly Netflix is actively exploring bid and has hired Moelis & Co as financial advisor)

-TEAM +2.7% (earnings, guidance)

-AAPL +2.5% (earnings, guidance)

-SPSC -32% (earnings, guidance)

-CRBP -21% (prices underwritten public offering of 4.74M shares of its common stock at a public offering price of $13.00/shr)

-NWL -20% (earnings, guidance)

-DXCM -12% (earnings, guidance)

-LUMN -8.8% (earnings, guidance)

-ATR -6.3% (earnings, guidance)

-CHTR -4.9% (earnings, guidance)

-CG -4.2% (earnings)

-ROKU -4.1% (earnings, guidance)

-POR -3.0% (earnings, guidance)

BY Doug Kass · Oct 31, 2025, 9:11 AM EDT

BY Doug Kass · Oct 31, 2025, 9:01 AM EDT

Fed speakers:

10 a.m.: Fed Bank of Dallas President Logan (Non-Voter) gives opening remarks before "The Evolving Landscape of Bank

Funding" research conference hosted by the Federal Reserve Banks of Dallas, Atlanta and Cleveland, Dallas, TX ( Livestream here. Text available. No audience Q&A);

12 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter)

and Fed Bank of Cleveland President Hammack (Non-Voter)

participate in discussion before "The Evolving Landscape of Bank Funding"

research conference hosted by the Federal Reserve Banks of Dallas, Atlanta and Cleveland, Dallas, TX (No Hammack text. No Bostic text. Audience Q&A expected. No Bostic media Q&A. Livestream here. )

Economic calendar:

BY Doug Kass · Oct 31, 2025, 8:56 AM EDT

I added to my VS index shorts:

* (SPY) $686.42

* (QQQ) $635.53

BY Doug Kass · Oct 31, 2025, 8:41 AM EDT

BY Doug Kass · Oct 31, 2025, 8:30 AM EDT

BY Doug Kass · Oct 31, 2025, 8:10 AM EDT

From Shake Shack (SHAK) (a popular investment recommendation on Fin TV):

“Now going to October, our sales trends, although positive, were not consistent with what we saw in the third quarter. Macro headwinds to the industry did intensify, and we are lapping one of the most iconic LTOs (limited time offer) in our history, Black Truffle. We continued to invest in advertising and media to support the business. However, our French Onion Burger LTO, while loved by the media, has not been as accretive to traffic or check as was the case for our LTOs in Q3.”

“We had positive comps in traffic in nearly all of our regions. However, we continue to see macro pressures in New York Metro and Washington, DC, that are weighing on our overall results. New York Metro and DC represent over a quarter of our sales, and we have been experiencing a higher degree of macro pressure in these regions than many industry peers, given our footprint today. So, a challenging macro backdrop here continues to have an outsized impact on our overall performance.”

BY Doug Kass · Oct 31, 2025, 7:59 AM EDT

Bonus — Here are some great links:

November Best Month of the Year for DJIA & S&P 500

BY Doug Kass · Oct 31, 2025, 7:25 AM EDT

I shorted Apple (AAPL) at $283.69.

I'm stepping up my (QQQ) short at $633.15.

By Doug Kass Oct 30, 2025 5:40 PM EDT

BY Doug Kass · Oct 31, 2025, 6:29 AM EDT

* The Hindenburg Omen is triggered...

BY Doug Kass · Oct 31, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at 1.83% vs. 1.34%.

BY Doug Kass · Oct 31, 2025, 5:45 AM EDT