Shorted Apple and More QQQ

I shorted Apple (AAPL) at $283.69.

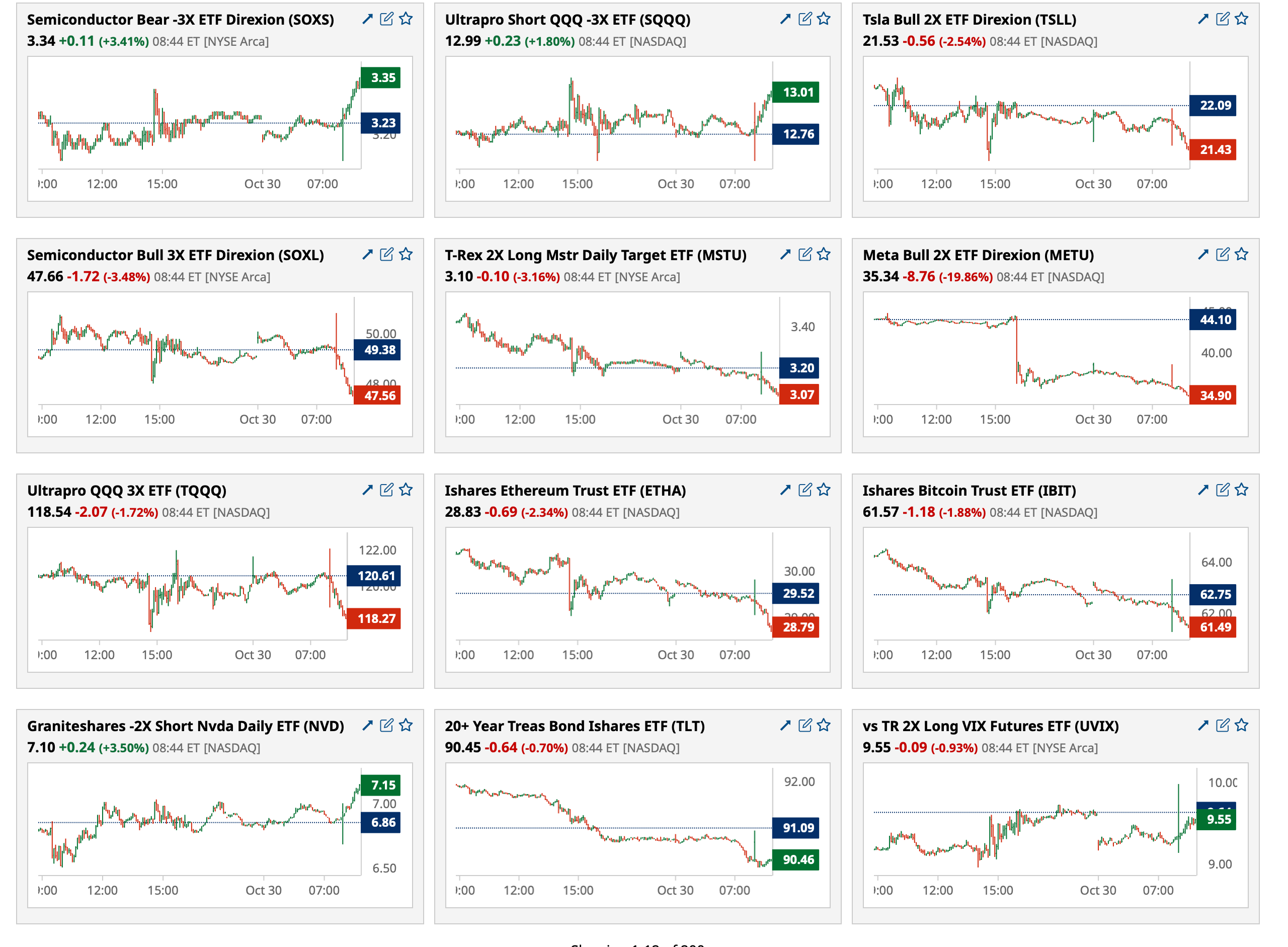

I'm stepping up my (QQQ) short.

BY Doug Kass · Oct 30, 2025, 5:40 PM EDT

I shorted Apple (AAPL) at $283.69.

I'm stepping up my (QQQ) short.

BY Doug Kass · Oct 30, 2025, 5:40 PM EDT

I am back shorting the indices (5:20 PM):

* (SPY) $684.07

* (QQQ) $633.11

BY Doug Kass · Oct 30, 2025, 5:35 PM EDT

BY Doug Kass · Oct 30, 2025, 4:40 PM EDT

- NYSE volume 6% above its one-month average

- NASDAQ volume 2% below its one-month average

- VIX index: up 0.35% to 16.98

BY Doug Kass · Oct 30, 2025, 4:30 PM EDT

BY Doug Kass · Oct 30, 2025, 4:03 PM EDT

JF is right on:

Jim F

"History does not repeat itself but it does rhyme" - Mark Twain

In the housing bubble we had no doc or liar loans. We won't ask for proof of income so just say it's high enough to get approved. We don't care we just need more meat for our MBS sausages.

Now in the private credit market we have no due diligence account receivable loans. We won't check so just make up the account receivable numbers needed to get approved.

Losers do due diligence. Winners make bad loans until it all blows up many large bonuses later!

BY Doug Kass · Oct 30, 2025, 2:25 PM EDT

On cue, Oracle's (ORCL) credit default swaps rise...

Oracle’s credit default swaps rise as AI investments grow By Investing.com

BY Doug Kass · Oct 30, 2025, 2:10 PM EDT

This recent MIT paper is interesting:

MIT just exposed every top AI model and it’s not pretty. They built a new test called WorldTest to see if AI actually understands the world… and the results are brutal….Then they tested 517 humans vs. Claude, Gemini 2.5 Pro, and o3. Humans crushed every model. Even massive compute scaling barely helped. The takeaway is wild.. today’s AIs don’t understand environments; they just pattern-match inside them. They don’t explore strategically, revise beliefs, or run experiments like humans do.

Relatedly, it seems to me that Sam Altman is now talking down the notion of AGI and really moving the goalposts (backwards) in this short clip:

It is stunning to me all the money that keeps being directed at a broken and non-productivity enhancing inflationary brute force resource hog that keeps missing every technology endpoint, no matter how much in the way of $ and electricity is being thrown at the problem. It seems the entirety of the U.S. economy is hell-bent on funding Nvidia (NVDA) and Sam Altman and our entire economy now depends on those two and how this all turns out. Awful bet if you ask me. But this is what the U.S. government seems best at.

If I were running things top down, as opposed to throwing more dollars and resource at a broken technology, it seems like it would make more sense to start pursuing a barbell strategy. I suspect the Chinese may be doing this, and potentially leaving the U.S. economy holding the bag once again (while a select few make out like bandits at the expense of everyone else). Throw dollars at doing the same thing 90-95% as well, but for 10%-20% of the cost and resource, which we know the Chinese are already doing. Then direct another big pie of the investment dollars at an alternative approach (nuerosymbolic AI, etc) that actually might work and do the things Gen AI was hyped as being able to do but clearly cannot. Hopefully, the alternative approach will also be much less resource intensive and therefore actually economic and productivity enhancing.

But for the time being, down the same road we go. We continue to attack a complicated problem with jack-hammers as opposed to brains.

BY Doug Kass · Oct 30, 2025, 2:00 PM EDT

BY Doug Kass · Oct 30, 2025, 11:30 AM EDT

BY Doug Kass · Oct 30, 2025, 11:12 AM EDT

From Peter Boockvar:

So, Jay Powell tempering market expectations for a December rate cut has lowered the odds to 58% from 82% right before the 2pm statement was released. The 2 yr yield is up 10 bps since, the 10 yr by 9 bps and the 30 yr by 8 bps.

On the debate on the state of the labor market and questions to Powell on why hiring is soft, why isn’t anyone talking about the possibility that tariffs are negatively impacting hiring? I’ve gone through countless earnings calls, and you’ll see a bunch more below, but as part of the mitigation process of reducing the impact on tariffs for those companies impacted, cutting costs is part of that. While most don’t specifically mention that a slowdown in hiring is a cost cutting response, I have to assume it is for some.

I think it’s a good thing that there is a trade detente between the two largest economies that need each other with commercial trade. I applaud Trump’s desire, to the likely dismay of some of the China hawks, to have a good relationship with China. But, substantively, it seems all we got was China buying US soybeans again, pushing out rare earth approval rules and in return they got a lowering of the fentanyl tariff to 10% from 20% (obviously a great thing if we can stop these chemicals from coming to the US) and a one year break on shipping fees. No talk about Nvidia’s Blackwell (and why stock is down a touch pre-market) and no discussions on Taiwan.

Back to the Fed and the direction of inflation, NEW lease rental growth continues to moderate according to Apartment List as they released this morning its October report. In the seasonally slow period ahead of the holidays, rents fell .8% m/o/m and they said “It’s likely that we’ll continue to see further modest rent declines to close out the year.” Rent growth seasonally then picks up again in the early Spring. Rents are down .9% y/o/y.

The vacancy rate ticked up by one tenth to 7.2%, a new high since they started calculating it in 2017. “We’re past the peak of a multifamily construction surge, but a healthy supply of new units are still hitting the market and colliding with sluggish demand, causing vacancies to continue trending up.” Austin again was the weakest market because of the excess supply with rents down 6.5% y/o/y while Providence, RI was the best with a y/o/y increase of 5.3%.

Again, these are new leases and we’ll get an update in coming weeks from the publicly traded multi family REITS on the pace of renewals that last quarter were running between 2-4%. As for overall inflation, housing should continue to slow but with still sticky non-shelter inflation and a rise in goods prices.

While the Bank of Canada cut rates by 25 bps to 2.25% as expected, Governor Macklem seems like he now wants to take a pause and the market responded in kind with a 9 bps rise in the 2 yr yesterday. The Canadian dollar though didn’t respond much. Macklem said “If the economy evolves roughly in line with the outlook, the governing council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.” He also said, “The range of possible outcomes is wider than usual, we need to be humble about our forecast.” Macklem also admitted his limited ability via monetary policy to impact their economy. “The structural damage caused by the trade conflict reduces the capacity of the economy and adds costs. This limits the role that monetary policy can play to boost demand while maintaining low inflation.”

The Bank of Japan did not surprise the market as they left rates unchanged but it’s still confounding why they think .50% is the right rate with inflation running above 3% and the populace obviously upset.

Some quotes from Ueda:

“We would like to spend a bit more time scrutinizing wages and price moves. We will have more data on how companies, hit by 15% tariffs, would respond and set wages including for next year...We would like to confirm whether wage and prices will gradually rise in tandem.”

“Food inflation is moderating, while underlying inflation is rising moderately. The economy is moving in line with baseline scenario, so we don’t see ourselves as being behind the curve.”

“As for the timing and viability of rate hikes, we don’t have any preset idea.”

“Uncertainty surrounding trade policy, and their impact on overseas and US economies may have diminished somewhat. But it’s still there. For the time being, we would like to scrutinize a bit more data to gauge how next year’s wage negotiations could unfold.”

On this continued foot dragging on rates, the yen is weaker though JGB yields are little changed as was the Nikkei after a great run.

Yes, I’m swamped going thru earnings calls.

From Old Dominion Freight:

“Old Dominion’s third quarter financial results reflect continued softness in the domestic economy.” Revenue fell 4.3% y/o/y “due primarily to a 9% decrease in our LTL tons per variable cost as a result.”

From Caterpillar and whose stock jumped by more than 10%:

“Higher sales volume was driven by higher sales of equipment and users across our three primary segments…Despite the tariff headwind, adjusted operating profit margin was slightly above our expectation, primarily due to better than expected sales volume in energy and transportation.”

In the ‘energy and transportation’ group, “The largest growth came from power generation with a 33% increase, primarily due to demand for reciprocating engines for data center applications.” Also, “Turbines and turbine related services also contributed to power generation growth.”

From Masco, down 5% yesterday:

“We continue to navigate a dynamic geopolitical and macroeconomic environment during this quarter. While the near term market conditions remained a headwind to our business, our teams continue to focus on execution to grow market share and drive long term shareholder value.”

Particularly in their paint business, “overall paint sales decreased low single digits. DIY paint sales decreased mid single digits as demand for DIY paint remained soft across the industry, impacted by low existing home turnover. In PRO Paint, sales increased low single digits.”

Plumbing sales rose 1%, “driven by favorable pricing.”

“The market environment remains volatile and tariff uncertainty persists…we now estimate that the total annualized cost impact of all incremental tariffs enacted this year to be approximately $270 million before mitigation, up from $210 million as of our second quarter earnings call.” They hope to mitigate all of this via “cost reductions, continued efforts to change our sourcing footprint, and pricing where necessary.”

From PPG Industries which fell 6%:

Sales grew 2% “which included both volume growth and price growth…despite a challenging macro environment.”

“From a regional perspective, the macro environment was choppy.” Sales grew in the US, Canada, Latin America and Asia Pacific but were “flat in Europe.”

From ADP which was down 7%:

“Employer services pays per control growth continued to moderate and rounded to 0% for the first quarter with clients remaining cautious around adding head count in the current environment.” Their other business lines seemed to have been stronger like HR outsourcing and retirement services.

From Brinker’s, down 7% and home to Chili’s which has been killing it with their Smashburger meal:

Chili’s comps jumped 21.4%, “outperforming the casual dining industry by 1,650 basis points.” Traffic rose 14%.

On their customer, “Chili’s continues to grow sales across all households of all income levels. And while others in the restaurant industry are seeing households with lower income pull back, we are seeing just the opposite. Our customer base is very representative of the US consumer across all income cohorts, but our cohort growing at the fastest is actually now households with income under $60,000. It’s clear that the ‘better than fast food’ campaign we’ve been hammering over the past two years, has positioned Chilli’s as an important value leader in the industry. And we are gaining market share with low income households, with others are reporting softness with that group.”

Why was the stock down so much? Their Maggiano’s chain was soft. “I think we lost a little bit of what the North Star of Maggiano’s is.”

From Etsy, whose stock fell 13% in part because of a management change, though beat eps and sales expectations:

“On the tariff and trade line front, we experienced some pressure on our US import trade route during the quarter. However, sequential improvement in our US domestic trade route helped offset the impact. The expiration of the de minimis exemption at the end of August weighed on performance immediately thereafter, and our business stabilized as we moved through the quarter, resulting in only a modest headwind to quarterly results.”

On their customer, “we saw a favorable y/o/y inflection across all income levels in Q3 with the strongest performance among our highest income buyers, which is consistent with the US consumer spending trends we are all reading about.”

“We saw particular strength in vintage home and living, jewelry above $100 and wedding and engagement rings.”

From Kraft Heinz:

“Overall, the operating environment remains challenging – with worsening consumer sentiment and inflation shaping consumer behavior globally.”

“The consumer continues to navigate a tough environment – with sentiment worsening, costs continuing to rise, and SNAP related headwinds expected to intensify. We see these pressures as persisting beyond the fourth quarter, leading to a longer path to consumer recovery.”

“the reality is that we are seeing some inventory pullback from customers. I think that’s a response to what they’re seeing in terms of the consumer sentiment. So the fact that we have now, in one of the worst consumer sentiments we have seen in decades. As we go into even a holiday season, we already see how customers are pulling back on inventory, and that’s reflected in our guidance as well too.”

From Chipotle, down sharply pre-market:

“Our third quarter performance fell short of our expectations due to persistent macroeconomic pressures.”

Comps grew just .3% y/o/y. “Earlier this year, as consumer sentiment declined sharply, we saw a broad based pullback in frequency across all income cohorts. Since then, the gap has widened, with low to middle income guests further reducing frequency. We believe that this guest with household income below $100,000 represents about 40% of our total sales, and based on our data is dining out less often due to concerns about the economy and inflation.”

“A particularly challenged cohort is the 25 to 35 year old age group. We believe that this trend is not unique to Chipotle and is occurring across all restaurants as well as many discretionary categories. This group is facing several headwinds, including unemployment, increased student loan repayment, and slower real wage growth. We tend to skew younger and slightly over index to this group relative to the broader restaurant industry.”

“Finally, the promotional environment has intensified with value as a price point and menu innovation escalating throughout the year.”

From Starbucks, lower pre-market:

US comps were flat y/o/y but that was an improvement and they rose in Canada “and in both markets, transaction comps continued to improve sequentially from the third quarter.”

“Across our US company operated portfolio, we more than tripled the percentage of coffeehouses with positive transaction comps from a year ago, with y/o/y transactions improving across all regions and dayparts.”

International comps grew 3%, “led by strength across our top markets, including Japan, which bounced back into positive comp territory in the quarter, as well as China, the UK and Mexico.”

From MGM Resorts who talked about the Vegas visitation challenges and differential between their higher end properties and lower end:

“Bellagio, Aria and Cosmopolitan have continued to maintain rates, continued to maintain ADRs, generally speaking in a tough environment.” On the other hand, Excalibur and Luxor have been softer. They got hurt by the airline troubles of Spirit, the value airline that flies to Vegas. Also, “When you think about what’s going on in the country and you think about Southern California market heavily Hispanic, I think our drive traffic was down in the summer. And so that had presented and continues to present somewhat of a challenge.”

“You think about international visitation in Canada, and while we’re all trying to do things to make that better, I don’t think that’s going to go away anytime soon.”

Alphabet had an amazing quarter and I’ll just mention here their still huge amount of spend:

CapEx in the quarter was $24 billion with “The vast majority of our CapEx invested in technical infrastructure, with approximately 60% of that investment in servers and 40% in data centers and networking equipment.”

With CapEx guidance, “we now expect CapEx to be in the range of $91 billion to $93 billion in 2025, up from our previous estimate of $85 billion...Looking out to 2026, we expect a significant increase in CapEx, and we’ll provide more detail on our fourth quarter earnings call.”

For perspective, CapEx is expected to be 27% of revenue this year vs 9.5% in 2021.

From Microsoft, who also had a great quarter but I’ll pick out what they said on hiring within LinkedIn and their level of CapEx:

Within LinkedIn, “The Talent Solutions business was impacted by continued weakness in the hiring market.”

“Capital expenditures were $34.9 billion, driven by growing demand for our cloud and AI offerings. This quarter, roughly half of our spend was on short lived assets, primarily GPUs and CPUs to support increasing Azure platform demand, growing first party apps and AI solutions, accelerating R&D by our product teams as well as continued replacement for end-of-life server and networking equipment.”

For their fiscal 6/30/26 yr, CapEx is expected to be 27.5% of revenue vs 12% in 6/30/22 fiscal yr.

From Meta, still putting up stellar revenue numbers but spending gobs of money too:

“Capital expenditures, including principal payments on finance leases, were $19.4 billion, driven by investments in servers, data centers and network infrastructure.”

“We currently expect 2025 capital expenditures, including principal payments on finance leases, to be in the range of $70 billion to $72 billion, increased from our prior outlook of $66 billion to $72 billion.”

That will be 35% of 2025 expected revenue vs 16% in 2021.

These are all astonishing levels of spend.

BY Doug Kass · Oct 30, 2025, 10:20 AM EDT

With S&P cash -56 handles I have taken off all of my short Index common and calls.

* (SPY) $681.44

* (QQQ) $627.91

BY Doug Kass · Oct 30, 2025, 9:55 AM EDT

Today's Fed speakers:

9:55 a.m.: (VIA PRE-RECORDED VIDEO) Fed Vice Chair for Supervision Bowman (Voter) speaks before virtual Economic Growth and Regulatory Paperwork Reduction Act Outreach Meeting (Topic TBA. Text available. No Q&A. Livestream link will be available);

1:15 p.m.: Fed Bank of Dallas President Logan (Non-Voter) gives welcome remarks before "The Evolving Landscape of Bank Funding" research conference hosted by the Federal Reserve Banks of Dallas, Atlanta and Cleveland, Dallas, TX (Livestream.)

Treasury auctions today:

11:00 a.m.: Treasury announces a 6-Week and a 3 and 6 Month Bill Auction;

11:30: Treasury hosts a $110B 4 and $95B 8 Week Bill Auction

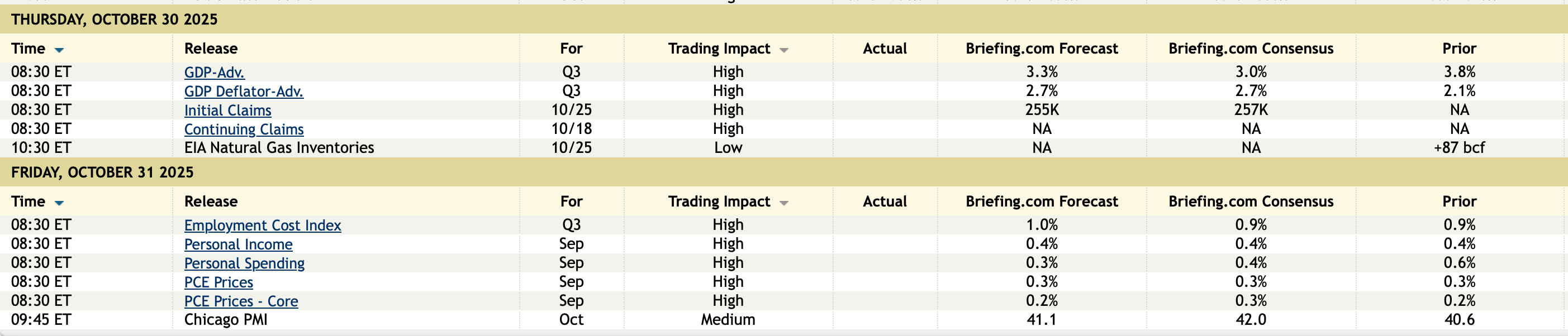

Economic calendar for the week:

BY Doug Kass · Oct 30, 2025, 9:35 AM EDT

BY Doug Kass · Oct 30, 2025, 9:23 AM EDT

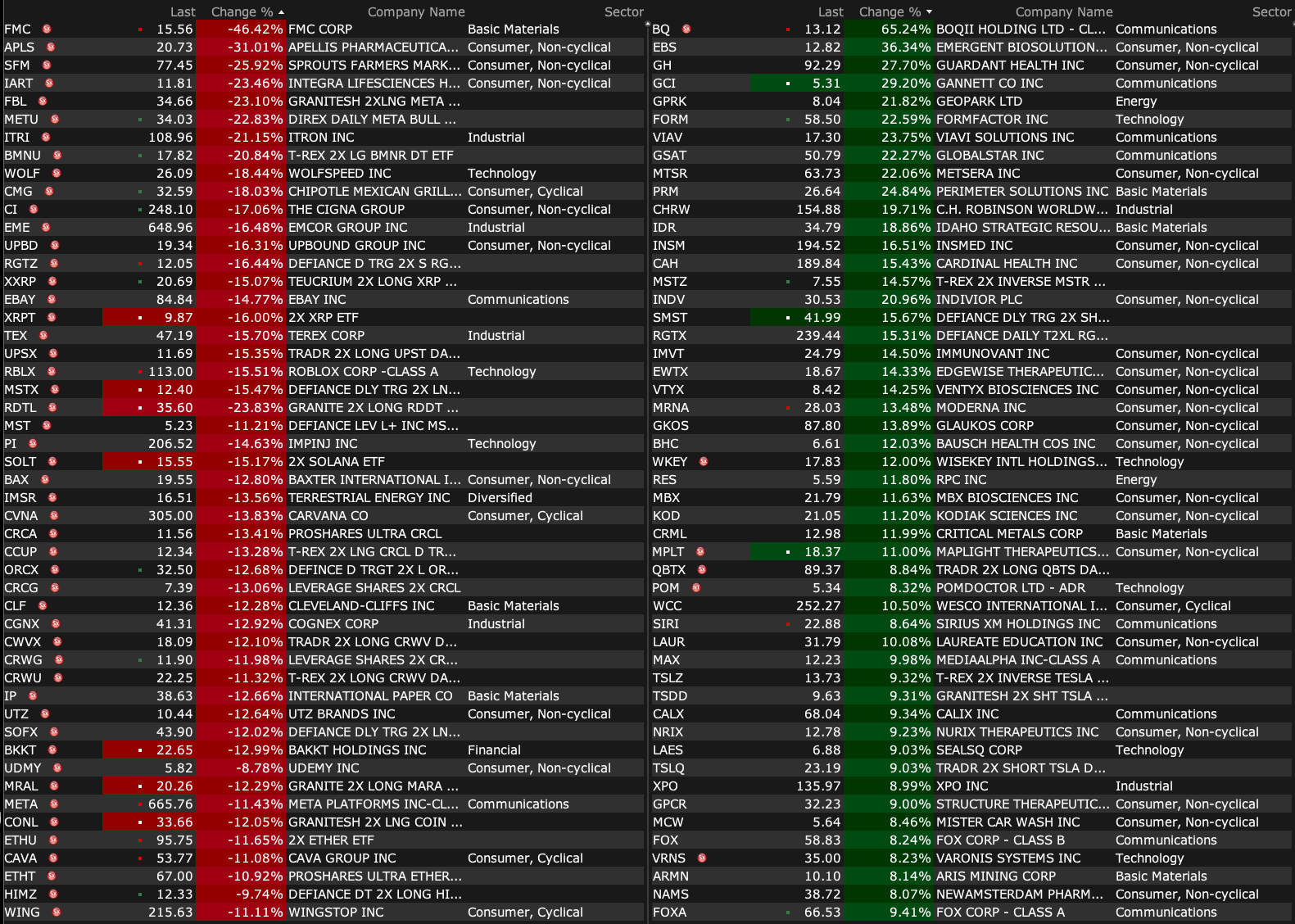

-MTSR +20% (Novo Nordisk confirms proposal to acquire Metsera, Inc. at $56.50/shr)

-CHRW +15% (earnings, guidance)

-INSM +11% (earnings, guidance)

-CAH +10% (earnings, guidance)

-GOOGL +8.2% (earnings, guidance)

-EL +7.8% (earnings, guidance)

-AME +6.4% (earnings, guidance)

-ITRI +6.3% (earnings, guidance)

-HII +5.9% (earnings, guidance)

-SHAK +4.6% (earnings, guidance)

-DTE +3.6% (earnings, guidance)

-KMB +3.5% (earnings, guidance)

-LLY +3.5% (earnings, guidance)

-AAP +3.4% (earnings, guidance)

-CVI +2.5% (earnings; raises dividend)

-CMCSA +2.0% (earnings)

-FMC -29% (earnings, guidance)

-WOLF -22% (earnings, guidance)

-CMG -18% (earnings, guidance)

-EME -13% (earnings, guidance)

-BAX -12% (earnings, guidance)

-IP -10% (earnings, guidance)

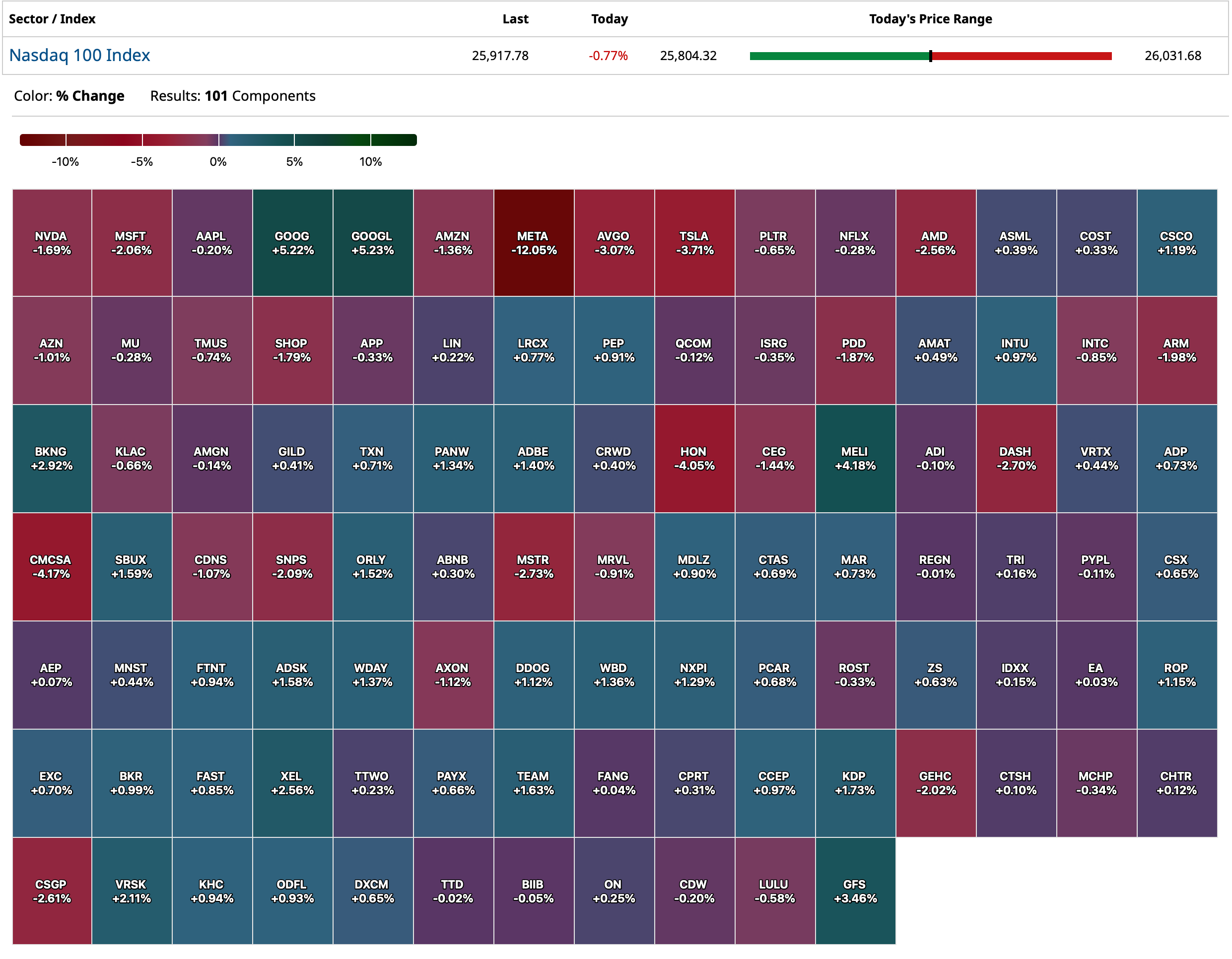

-META -9.4% (earnings, guidance)

-EBAY -9.0% (earnings, guidance)

-RBLX -5.4% (earnings, guidance)

-MO -4.8% (earnings, guidance)

-MGM -4.7% (earnings)

-BTU -3.8% (earnings, guidance)

-BIIB -3.6% (earnings, guidance)

-SBUX -3.2% (earnings, color)

-CP -3.1% (earnings)

-PPC -2.6% (earnings)

-MRK -2.2% (earnings, guidance)

-MSFT -2.1% (earnings, guidance)

BY Doug Kass · Oct 30, 2025, 9:16 AM EDT

BY Doug Kass · Oct 30, 2025, 8:42 AM EDT

Article below:

Bill Gates says we're in an AI bubble similar to the dot-com bubble

Well, at least Bill Gates said it is not tulips!

As far as Gates other comparisons with regard to the dot-com era, I think he makes three mistakes that people often make:

* The dot-com stuff worked.

* It was economic, and productivity enhancing on an economic basis — ergo the food chain was making money while providing the product they supplied, and while paying an economic price, it was still productivity enhancing for the end customers and therefore the economy.

* It did not screw up everyone’s electricity bill and was not socially untenable for that and other reasons.

As an aside, the related party transactions then were far less significant and far less to the benefit of one business, than they are now. Now it all leads back to one place who is effectively funding the entire circular relationship. Then it was more broadly distributed, and much less significant. It was a sidebar. Now it is not.

BY Doug Kass · Oct 30, 2025, 8:15 AM EDT

A good and candid tweet — not ad hominem:

BY Doug Kass · Oct 30, 2025, 7:53 AM EDT

* My pal Bob Farrell would, no doubt, become more concerned with the market's conspicuously weak internals...

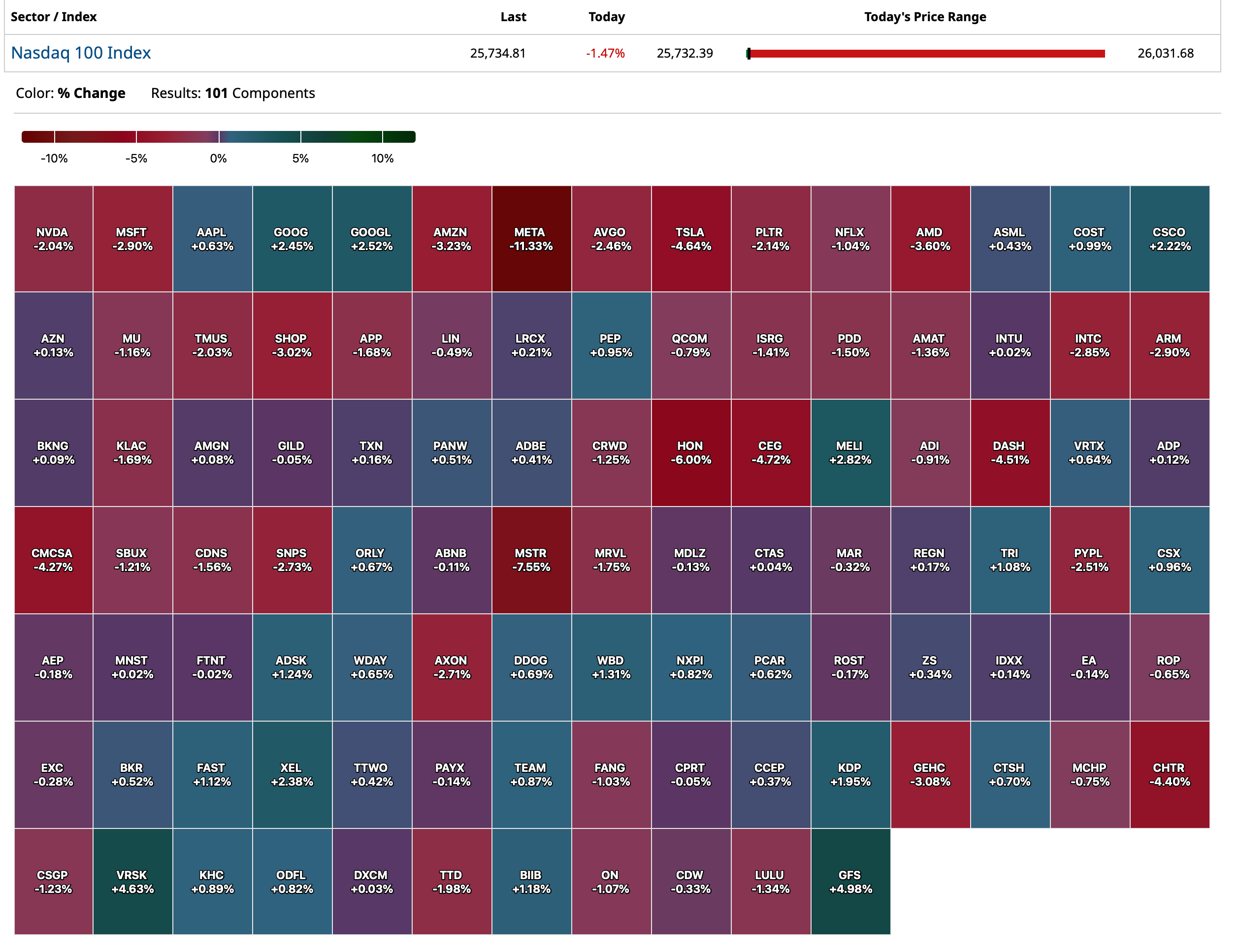

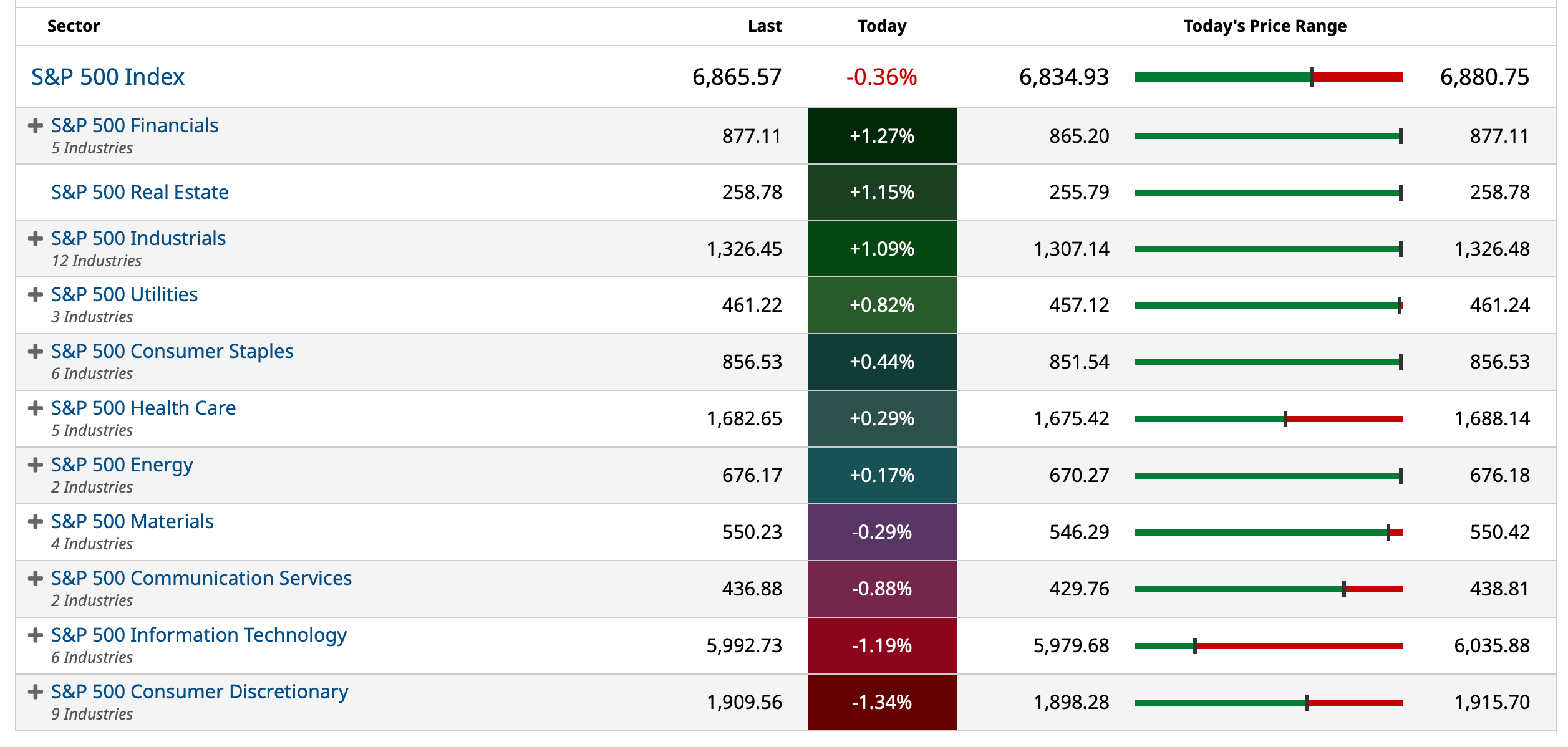

In yesterday's opening missive, Nvidia, She Was the Most Glorious Stock Under the Sun! I made several key summary points:

* The market's top-heavy condition is nearly unprecedented

* The S&P Index should be renamed "The Nvidia and Friends Index"

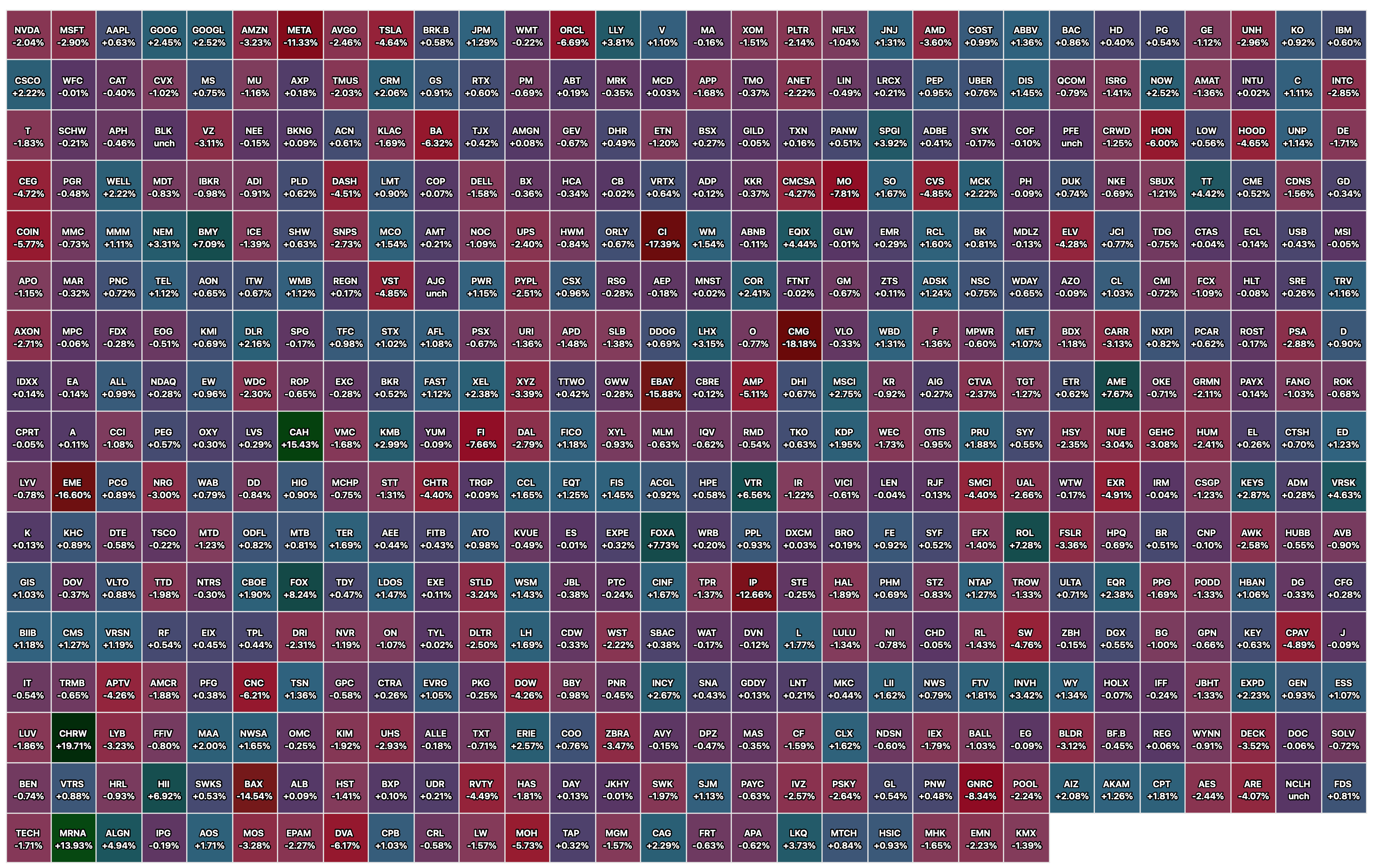

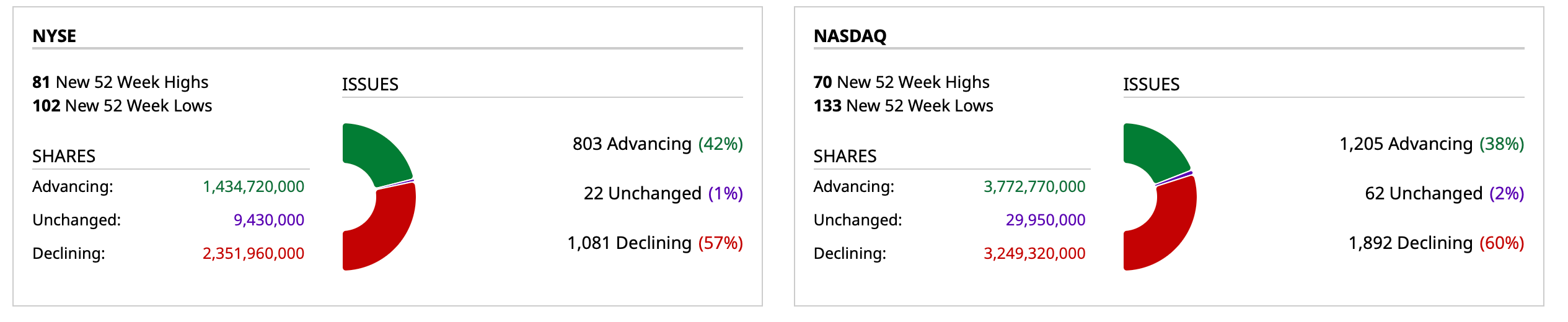

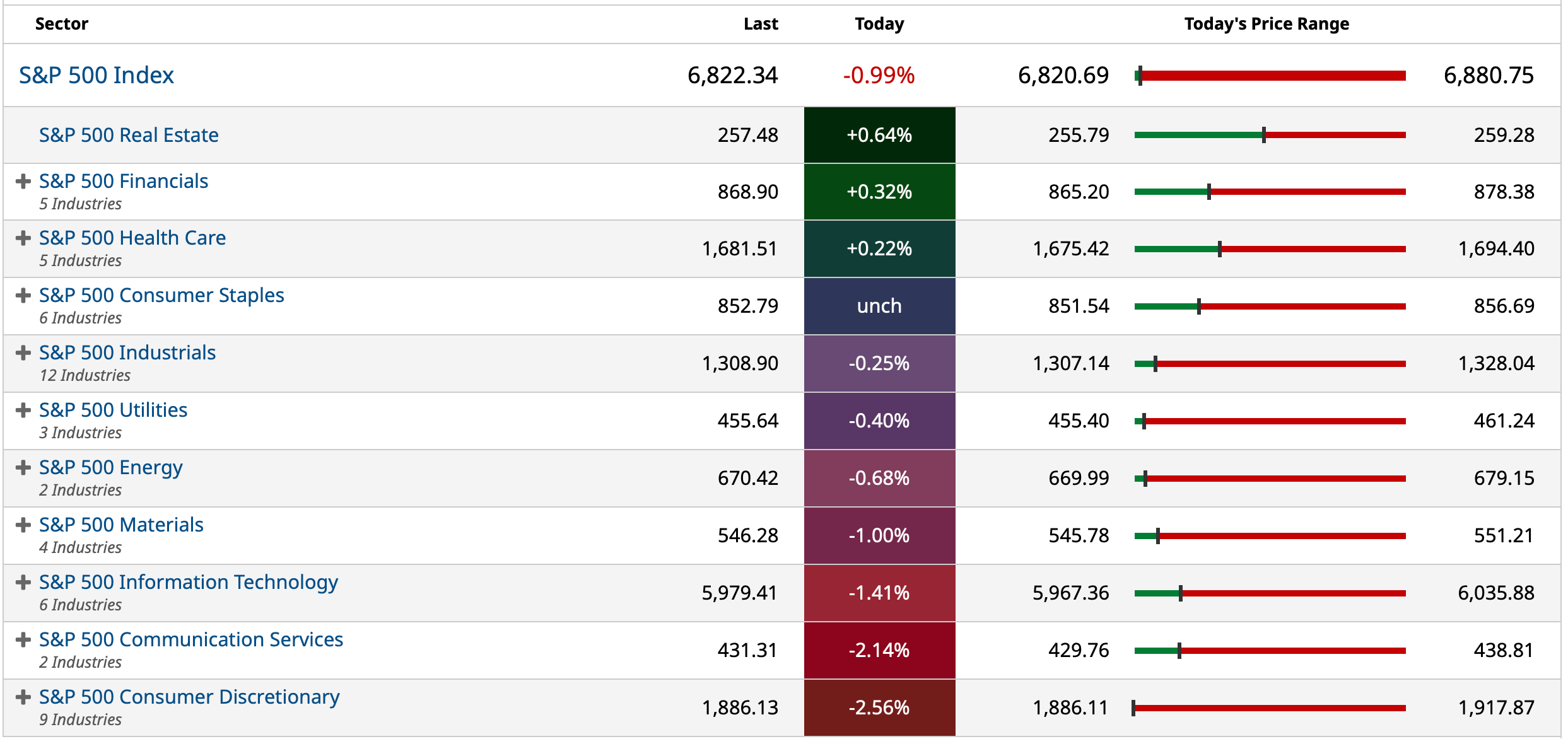

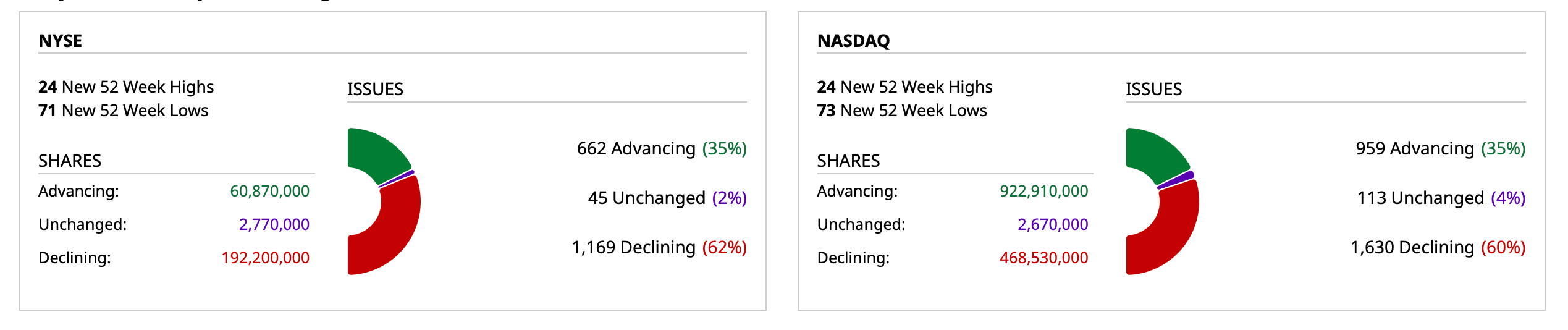

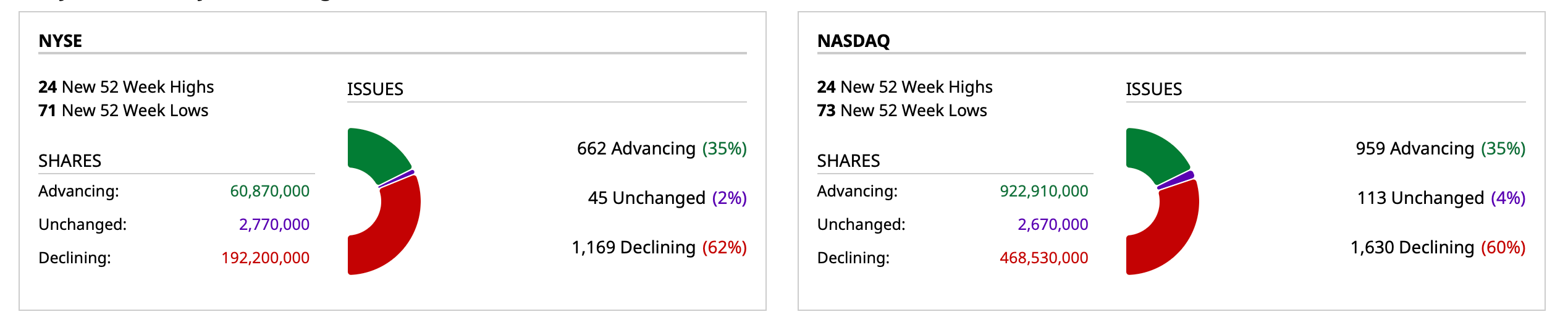

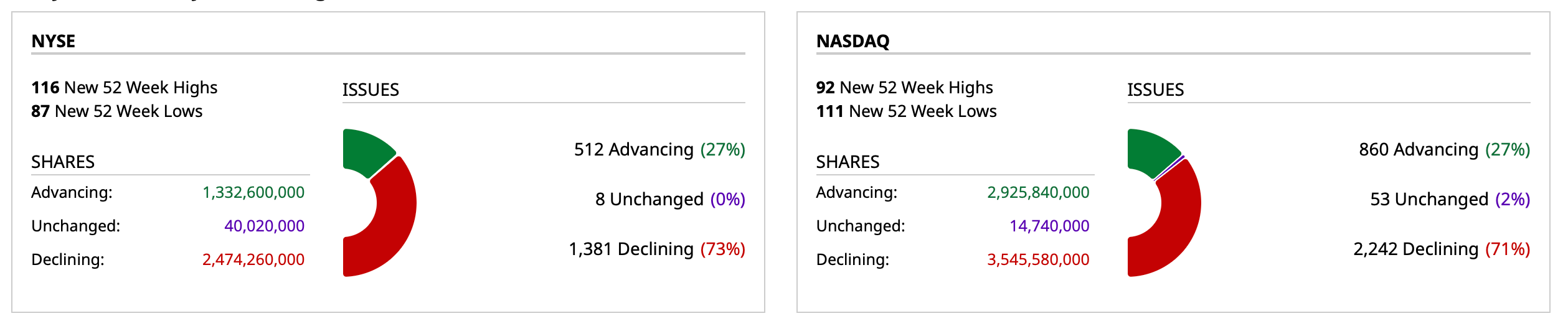

* In yesterday's session, 80% of the S&P Index closed lower (398 issues ended red, only 102 issues ended green), yet the S&P and Nasdaq surged to all-time highs

Yesterday's market breadth continued to stink up the joint — with decliners leading advancers (on both the NYSE and Nasdaq) at nearly 3-1:

If Bob magically appeared on Fin TV this morning (trust me, he won't!), he would likely make several observations about the market's current state:

1. Markets tend to return to the mean over time.

2. Excess moves in one direction will lead to an excess move in the opposite direction.

3. Exponential rapidly rising stocks usually go further than you think, but they do not correct by going sideways.

4. The public buys the most at the top and the least at the bottom.

5. And, most importantly, markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Thank you, Uncle Bob.

BY Doug Kass · Oct 30, 2025, 7:30 AM EDT

Given my view of the potentially large market downside, I have shorted a package of high-octane, high-beta and speculative market leaders in the premarket this morning.

Names not divulged in order to protect the innocent (most retail investors should not short)!

BY Doug Kass · Oct 30, 2025, 7:20 AM EDT

The only near-term solution for Chipotle (CMG) would be for the company to announce a deal with OpenAI(!):

BY Doug Kass · Oct 30, 2025, 7:10 AM EDT

I made about +$20 on my recent (MSFT) short (in less than three days), but I should never have covered my short:

BY Doug Kass · Oct 30, 2025, 7:00 AM EDT

1. Worst Day For Bonds Since June:

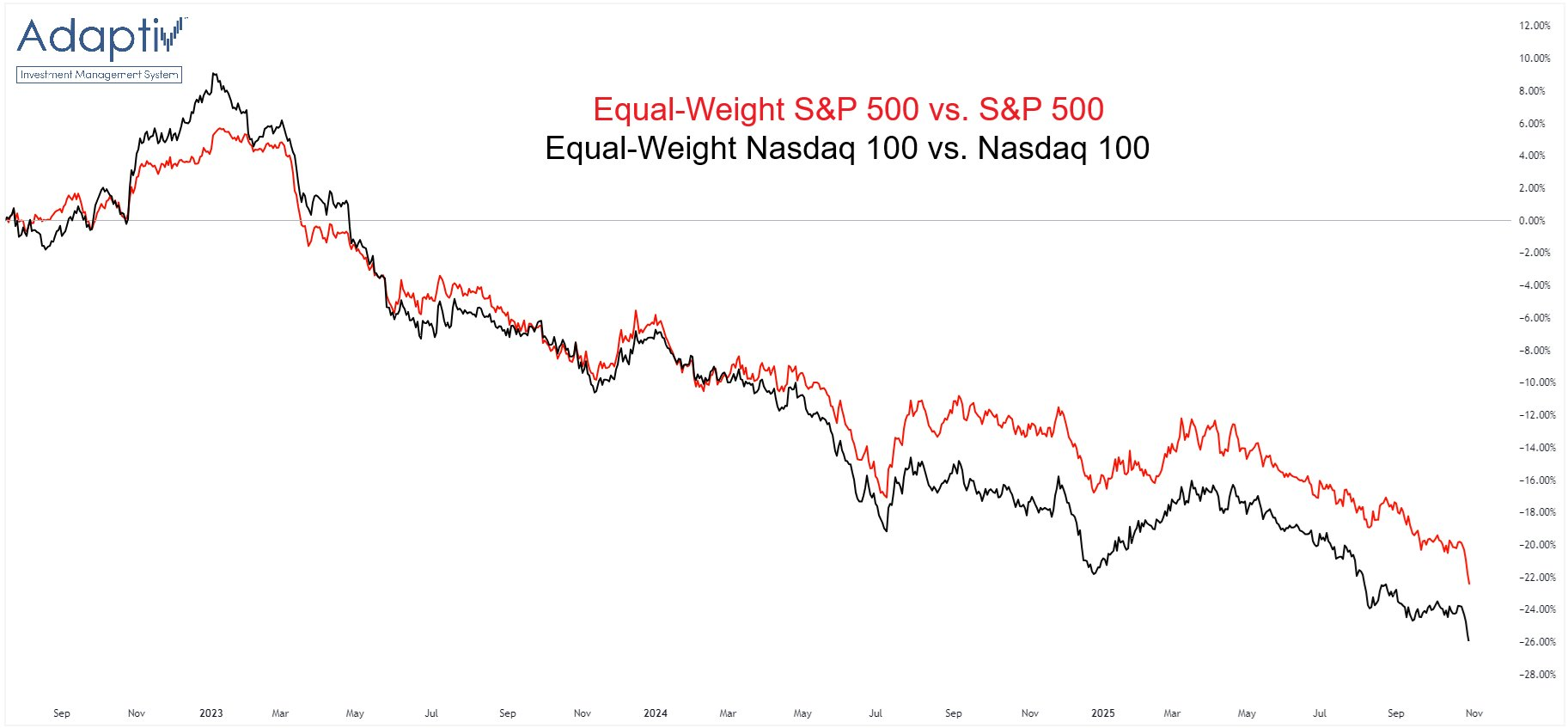

2. Cap Weight or Die

BY Doug Kass · Oct 30, 2025, 6:50 AM EDT

BY Doug Kass · Oct 30, 2025, 6:35 AM EDT

Meta (META) is the subject of numerous price target reductions this morning as investors grow fearful of rising costs relative to the growth in revenues (reverse operating leverage).

We sold our META long last week at $740:

I am continuing to eliminate longs in a market that I view as materially overvalued.

I have sold the balance of my Meta (META) at $740.09 just now.

Position: None

By Doug Kass Oct 23, 2025 12:23 PM EDT

BY Doug Kass · Oct 30, 2025, 6:25 AM EDT

BY Doug Kass · Oct 30, 2025, 6:15 AM EDT

BY Doug Kass · Oct 30, 2025, 6:05 AM EDT

The S&P Short Range Oscillator is moving back toward neutral, standing at 1.34% vs. 2.71%.

BY Doug Kass · Oct 30, 2025, 5:55 AM EDT

Workin' on our night moves

Tryin' to lose the awkward teenage blues

Workin' on our night moves

Mmm, and it was summertime

Mmm, sweet, summertime, summertime

- Bob Seger, Night Moves Bob Seger & The Silver Bullet Band - Night Moves (Official Video)

BY Doug Kass · Oct 30, 2025, 5:45 AM EDT