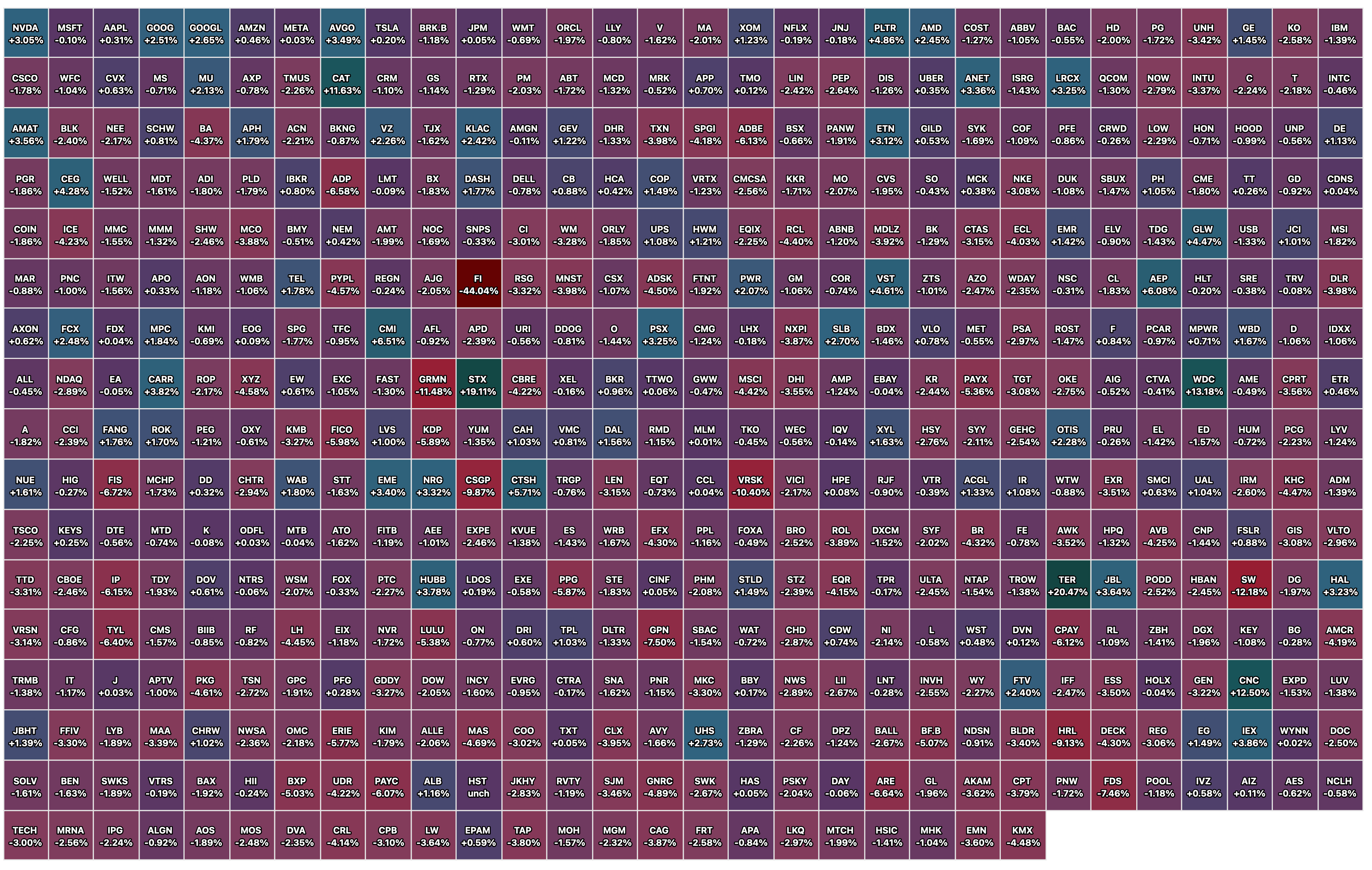

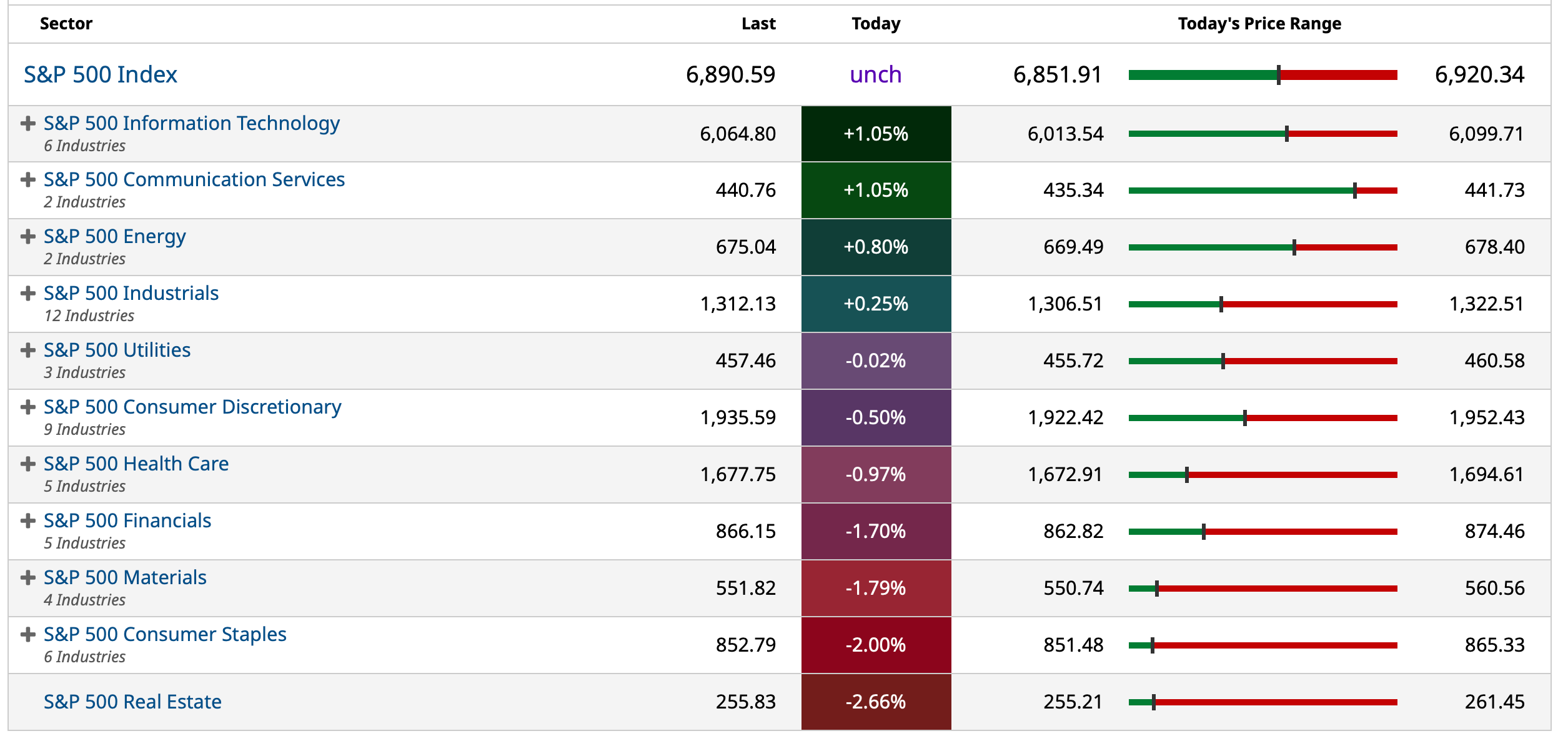

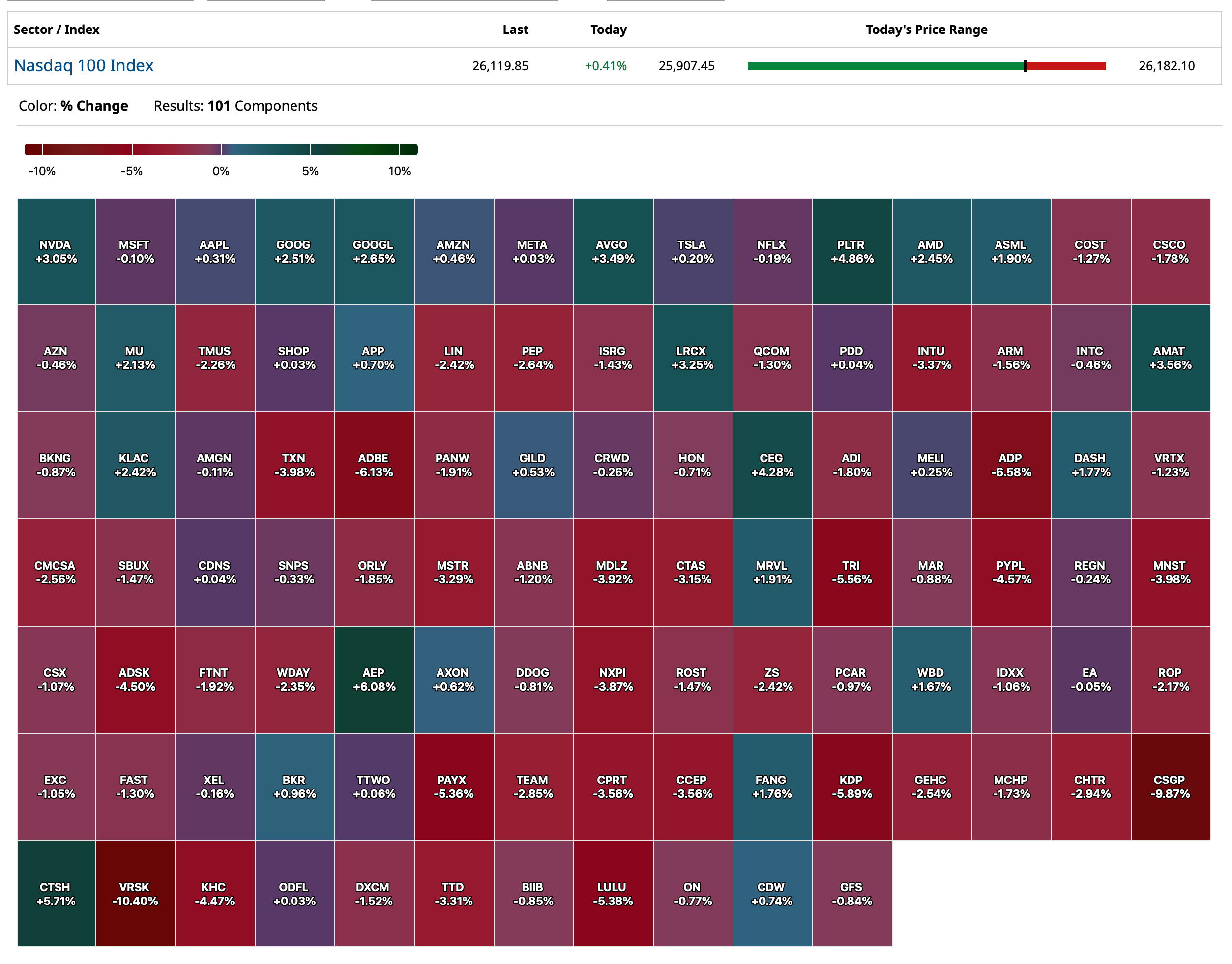

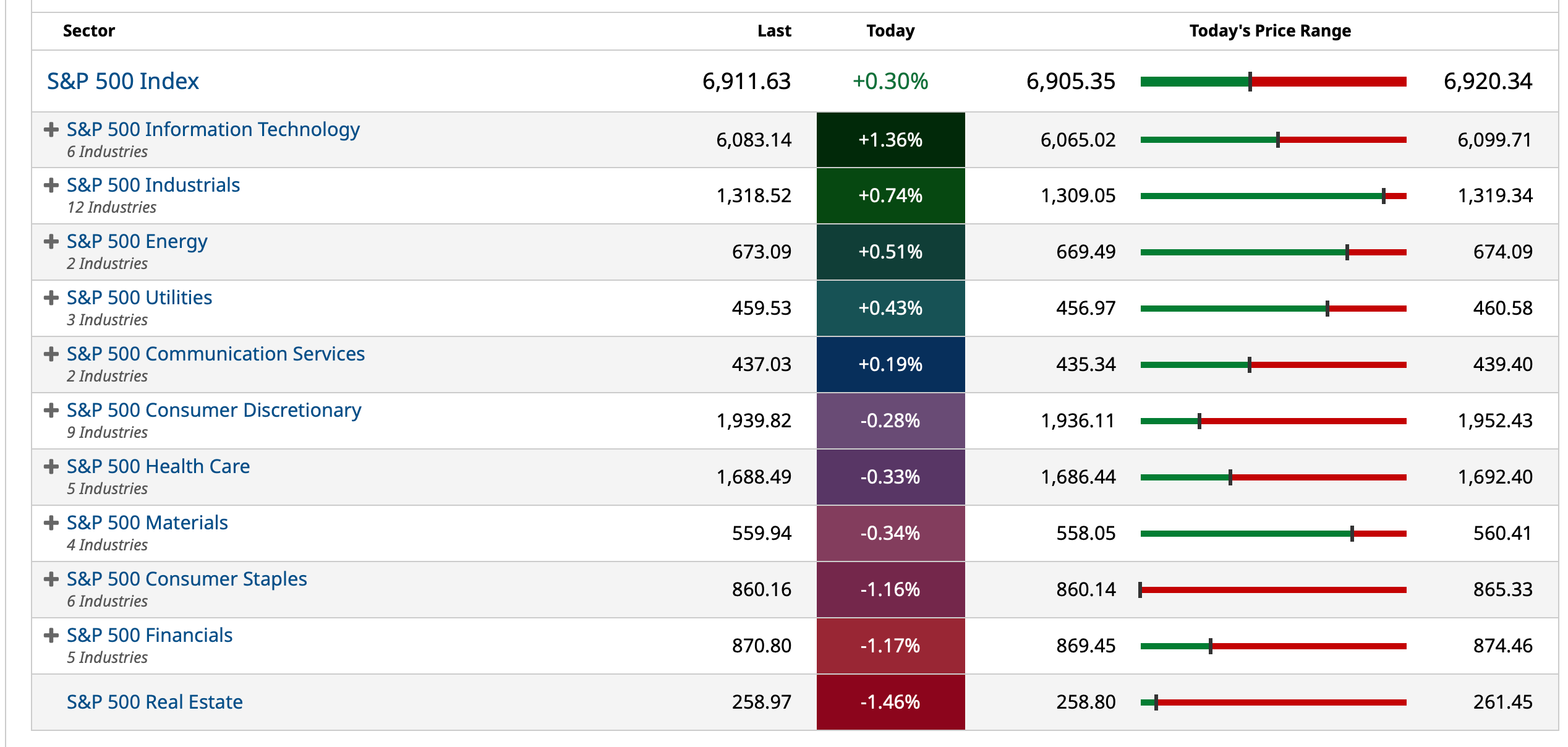

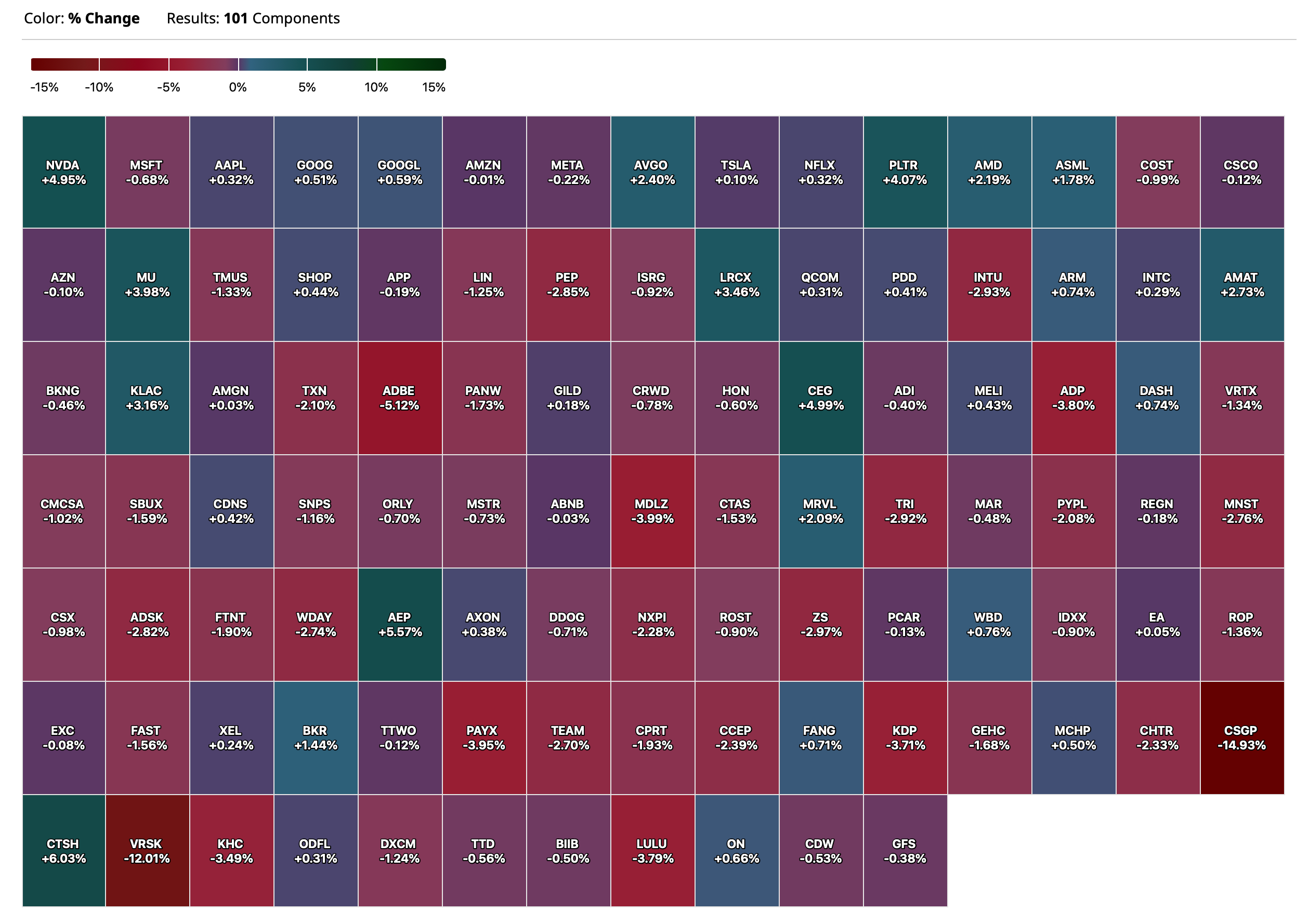

Closing S&P 500 Index Heat Map

BY Doug Kass · Oct 29, 2025, 4:50 PM EDT

BY Doug Kass · Oct 29, 2025, 4:50 PM EDT

- NYSE volume 14% above its one-month average

- NASDAQ volume 5% below its one-month average

- VIX index: up 3.59% to 17.01

BY Doug Kass · Oct 29, 2025, 4:37 PM EDT

I am digesting the multiple earnings reports, but let me deliver you another of my tweets:

BY Doug Kass · Oct 29, 2025, 4:28 PM EDT

With cash only -3 handles I am adding to my short index calls.

BY Doug Kass · Oct 29, 2025, 3:18 PM EDT

The Fed did the expected and trimmed the funds rate again by -25 basis points to a 3.75%-4.0% band and announced an end to QT as of December 1st. There were two dissents, which is very rare — and even rarer, Kansas City Fed President Schmid voted for no move, and Governor Miran predictably pushed for a -50-basis-point cut. Investors may well be disappointed, even with few surprises, by the lack of any support for the market view of five more rate cuts ahead or even in December, which had been nearly fully priced in; and also by the fact that there was a dissent for no rate relief (unlike Schmid’s dissent, Miran’s was totally expected). We will have to await what Powell says at the presser. In the immediate aftermath of the statement, bond yields have ticked up a little more, and the stock market rally has stalled out. Based on the Bank of Canada this morning, benchmarked against what is priced in, the risk is that the Fed Chairman fails to deliver a dovish policy message.

BY Doug Kass · Oct 29, 2025, 3:00 PM EDT

I covered this morning's index shorts:

* (SPY) $683.32

* (QQQ) $631.01

From earlier:

I have added to my index shorts:

* (SPY) $689.13

* (QQQ) $636.38

Position: Short SPY common (M) and calls (VS), QQQ common (M) and calls (VS)

By Doug Kass Oct 29, 2025 5:55 AM EDT

I have added to my index shorts:

* (SPY) $689.28

* (QQQ) $636.16

Position: Short SPY common (M) and calls (VS), QQQ common (M) and calls (VS)

By Doug Kass Oct 29, 2025 8:05 AM EDT

BY Doug Kass · Oct 29, 2025, 2:55 PM EDT

Wolf Street howls about the Fed's move.

BY Doug Kass · Oct 29, 2025, 2:45 PM EDT

From Peter Boockvar:

Fed statement with one that didn't want to cut

With cutting interest rates again by 25 bps to a range of 3.75-4% as we all expected, the commentary on the economy and inflation was little changed from what they said in September. They also announced that on December 1st, QT will officially end with a balance sheet around $6.5 trillion vs $4.2 trillion in February 2020, also as expected.

By the way, on the lack of government issued data, the Fed plugged this line in when talking about the unemployment rate which “has edged up but remained low through August”, “more recent indicators are consistent with these developments.”

Governor Miran wanted a 50 bps cut which is what he voted for in September, as we know. In contrast to Miran and the rest of the voters, KC president Jeff Schmid dissented and wanted no cut.

Bottom line, no real surprise except the Schmid dissent makes me more confident that Jay Powell is going to push back on a December cut being the lay up the markets think it is. Bond yields across the curve are up a slight 1 bp from 1:59pm est. At the presser, I expect some more market action.

BY Doug Kass · Oct 29, 2025, 2:40 PM EDT

BY Doug Kass · Oct 29, 2025, 2:32 PM EDT

BY Doug Kass · Oct 29, 2025, 2:15 PM EDT

"Meshuganah is trump." (Craziness is three-fold in Yiddish)

- Grandma Koufax

Japan's GDP is $4.05 trillion.

The total stock market capitalization of all Japanese equities is $6.35 trillion.

Nvidia's (NVDA) market capitalization is $5.03 trillion or 16% of estimated 2025 U.S. GDP.

Nvidia's expected 2025 sales are less than 1% of estimated 2025 U.S. GDP.

BY Doug Kass · Oct 29, 2025, 1:50 PM EDT

Wolf Street howls about home sales not responding to lower mortgage rates.

And as I mentioned earlier in my Diary, Fed cuts could produce the opposite interest rate effect.

BY Doug Kass · Oct 29, 2025, 1:26 PM EDT

BY Doug Kass · Oct 29, 2025, 12:40 PM EDT

BY Doug Kass · Oct 29, 2025, 12:26 PM EDT

BY Doug Kass · Oct 29, 2025, 12:12 PM EDT

BY Doug Kass · Oct 29, 2025, 11:57 AM EDT

Housekeeping item.

I covered the balance of my Microsoft (MSFT) short at $538.03. (Originally shorted at $555.48 two days ago.)

From earlier this week:

I have covered one half of my remaining half of my Microsoft (MSFT) short at $542.

From earlier:

I have covered half of my (MSFT) trading short rental at $544.

Last post:

I have taken a trading short rental in (MSFT) (at $555.48) after this announcement with OpenAI. Microsoft agrees new terms with OpenAI worth $135 billion stake

No one should follow me into this trade!

Position: Short MSFT S

By Doug Kass Oct 28, 2025 12:31 PM EDT

BY Doug Kass · Oct 29, 2025, 11:40 AM EDT

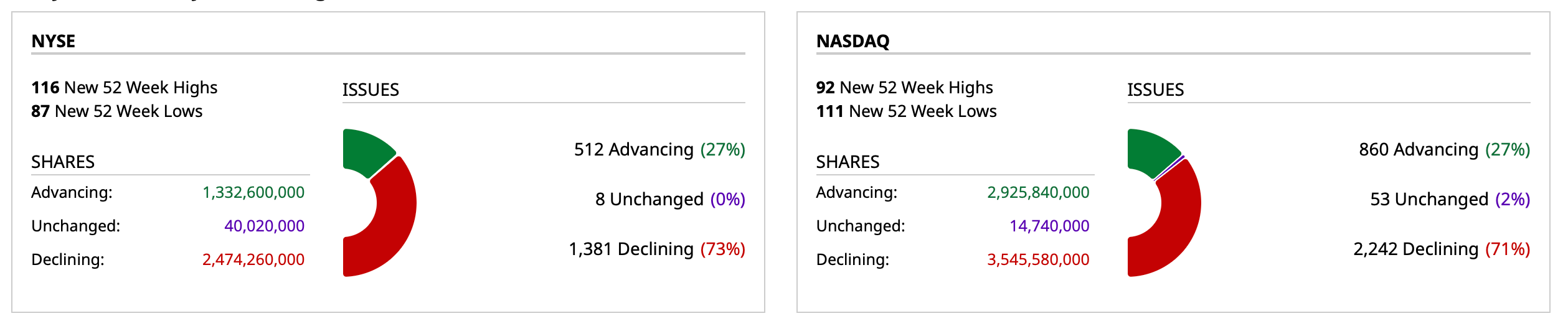

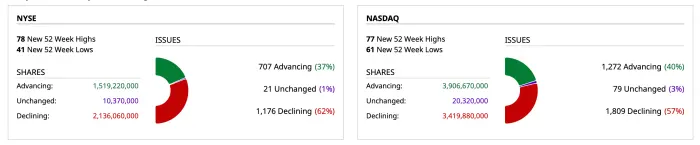

- NYSE volume , 2% above its one-month average; Decliners lead advancers by 1.3:1

- Nasdaq volume 6% below its one-month average; Decliners lead advancers by 1.5:1

- VIX index: up 3.23% to 16.95

BY Doug Kass · Oct 29, 2025, 11:30 AM EDT

From Charlie!

BY Doug Kass · Oct 29, 2025, 11:12 AM EDT

* The market's top-heavy condition is nearly unprecedented

* The S&P Index should be renamed 'The Nvidia and Friends Index'

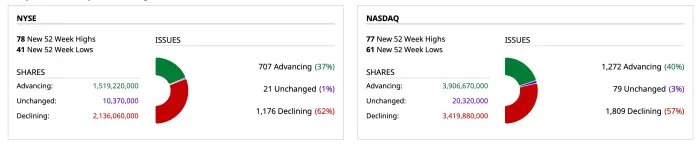

* In yesterday's session, 80% of the S&P Index closed lower (398 issues ended red, only 102 issues ended green), yet the S&P and Nasdaq surged to all-time highs

Two AI investors are walking in a forest when they come across a pile of sh@t.

The first AI investor says to the other, "I'll pay you $100 to eat that pile of sh#t."

The second AI investor takes the $100 and eats the pile of sh#t.

They continue walking until they come across a second pile of sh#t.

The second AI investor turns to the first and says "I'll pay you $100 to eat that pile of sh#t."

The first AI investor takes the $100 and eats the pile of sh#t.

Walking a little more, the first AI investor looks at the second and says, "You know, I gave you $100 to eat sh#t, then you gave me back the same $100 to eat sh#t, I can't help but feel like we both just ate sh#t for nothing."

"That's not true" responded the second AI investor. "We increased our stock price's value by $20 billion."

- Heard in Silicon Valley last weekend

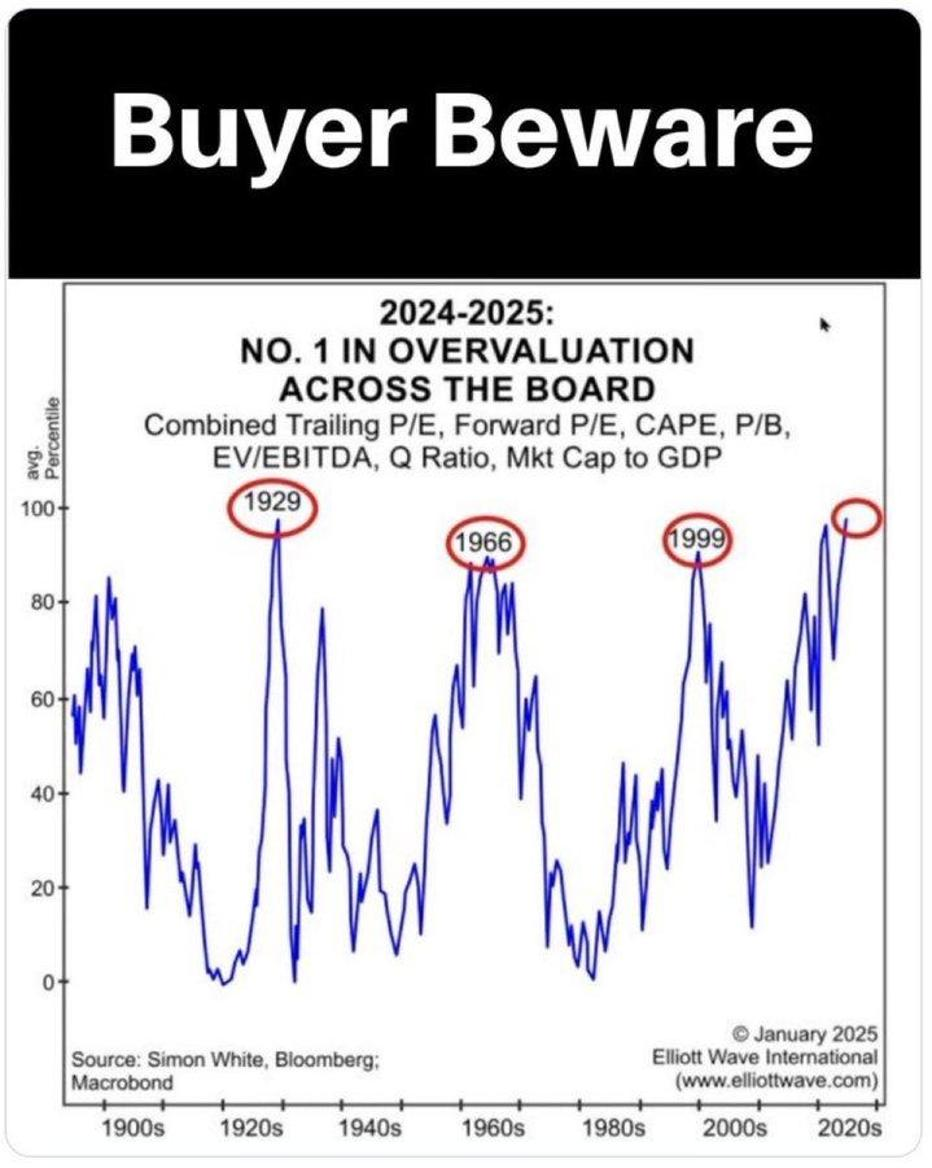

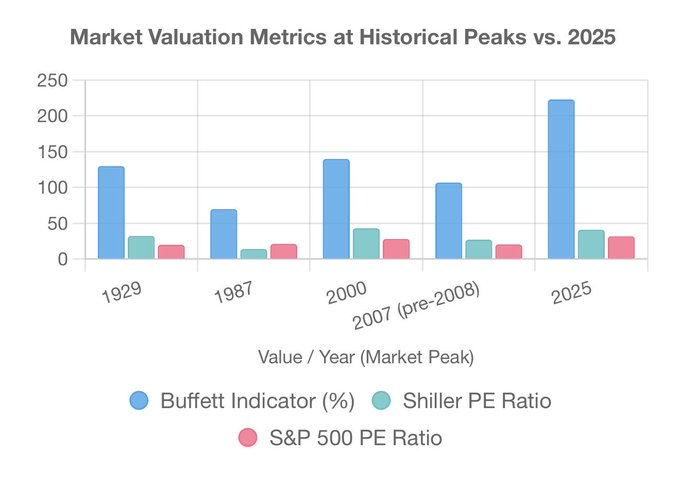

By most metrics, equities today are pornagraphically overvalued:

Equities, based on traditional valuation metrics, are now in the 98%-tile:

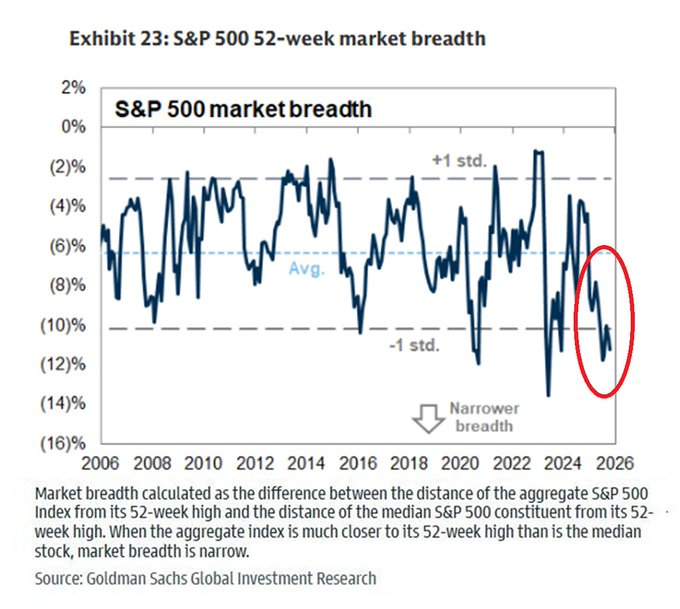

Students of market history have been taught that improving market breadth is integral to a healthy Bull Market.

From Bob Farrell's Ten Lessons On Investing:

Lesson #7. Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names.

Translation: Breadth is important. A rally on narrow breadth indicates limited participation and the chances of failure are above average. The market cannot continue to rally with just a few large-caps (generals) leading the way. Small- and mid-caps (troops) must also be on board to give the rally credibility. A rally that lifts all boats indicates far-reaching strength and increases the chances of further gains.

But, this is not our father's market - and exceptions to the rule are plentiful and divergences are being ignored. Ergo, I have been wrong and in a slump:

Childhood days, lemonade, romance.

Many portfolios are wrapped into Nvidia

Met her at the World's Fair in 1900...

Ah, Nvidia, she was the most glorious stock under the Sun!

Amazon, Alphabet, Apple... rolled into one!

In other words... and please sing along with Groucho and me:

Lydia the Tattooed Lady

Oh Lydia, oh, Lydia, say have you met Lydia

Oh, Nvidia, the tattooed lady

She has sales that folks adore so

And GAAP earnings even more so

Nvidia, oh, Nvidia, that encyclopedia

Oh, Nvidia, the queen of tattoo

On her back is the Battle of Waterloo

Beside it (short sellers') Wreck of the Hesperus too

And proudly above waves

The Red, White and Blue

You can learn a lot from NVDA

La la la la la la

La la la la la la

When a robe is unfurled Huang will show you the world

If you stand up and tell him where

For a dime you can see Kankakee or Paree

Or Washington crossing the Delaware

La la la la la la

La la la la la la

Oh, Lydia, oh, Lydia, say have you met Lydia

Oh, Nvidia, the tattooed lady

When her muscles start relaxin'

Up the hill comes that cool cat Jensen

Nvidia, oh, Nvidia, that encyclopedia

Oh, NVDA, the champ of them all

For two bits she will do a Mazurka in Jazz

With a view of Santa Clara that no company has

And on a clear day you can see Alcatraz

You can learn a lot from Nvidia

La la la la la la

La la la la la la

Come along and see Buffalo Bill with his lasso

Just a little classic by Mendel Picasso

Here is Captain Bezos exploring the Amazon

And Apple's Tim Cook, but with his pajamas on

La la la la la la

La la la la la la

Announced NVIDIA HGX™ H200 with the new NVIDIA H200 Tensor Core GPU, the first GPU with HBM3e memory, Over on the west coast investors have Treasure Island

Here is Sifei Liu doing the rumba

And the company's $4.93 fully diluted earnings number.

Oh Lydia, oh, Lydia, say have you met Lydia

Oh, Nvidia, the tattooed lady

Lydia, oh, Lydia, that encyclopedia

Oh, Lydia, the queen of them all

She once swept an Admiral clear off his feet

The ships on her hips make portfolios skip a beat

And now the old boy NVDA is in command of the fleet

For he went and married Lydia

Groucho said Lydia (I said Nvidia)

Groucho said Lydia (Investors are buying Nvidia)

La la!

- Lydia (Nvidia) The Tattooed Lady, Kass Column on TheStreetPro Doug's Daily Diary - TheStreet Pro

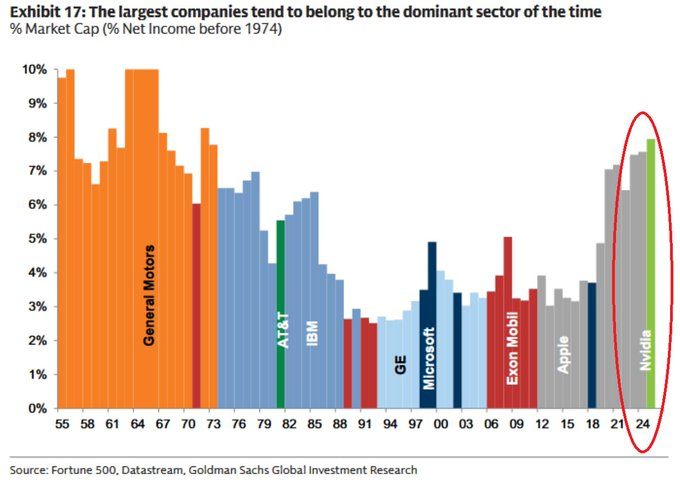

Nvidia now represents a record 8% of the S&P Index - its been 50 years since one company so dominated the Senior Index (that was General Motors in the early 1970s):

Nvidia's market cap exceeds the economies of Japan or India and is closing in on Germany's GDP.

This morning you will be showered about the "top heavy" large cap tech dominance:

I continue to view this narrowness as unhealthy - but my view hasn't translated into lower stock prices as the strong equities get stronger, carrying the Indices to multiple new highs.

My observations and warnings about weak breadth have populated my Diary this week:

I thought the chart I presented in my Diary of yesterday's performance of (XLK) (technology) vs. (XLF) (financials) was conspicuous and ominous... yet the averages flourished and closed near their daily highs:

OCT 28, 2025 3:54 PM EDT

On the shows we hear cheerleading. Here is something you will not even hear being discussed on the shows — a conspicuous divergence (and a measure of the narrowing of market breadth I expressed over the last 24 hours):

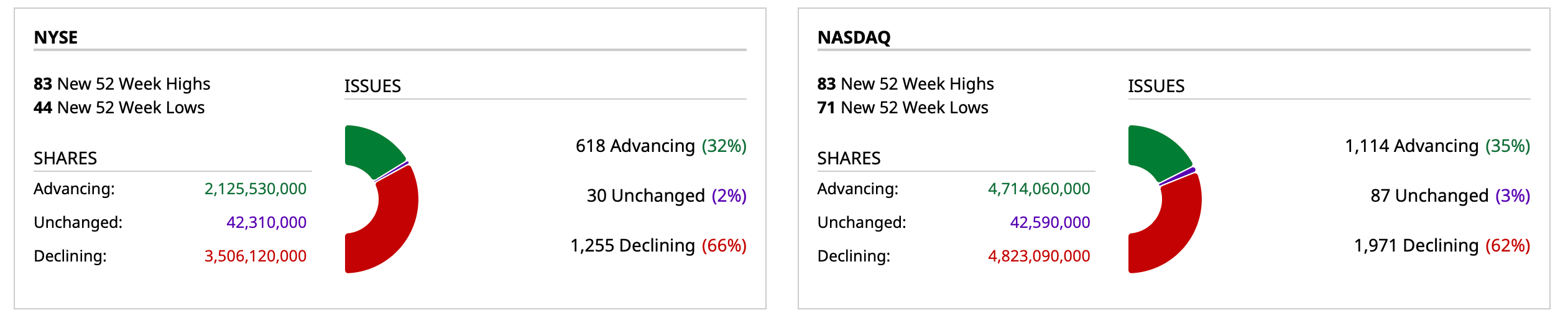

More broadly, aggregate breadth has had a bad odor of late:

Breadth yesterday:

Breadth Monday:

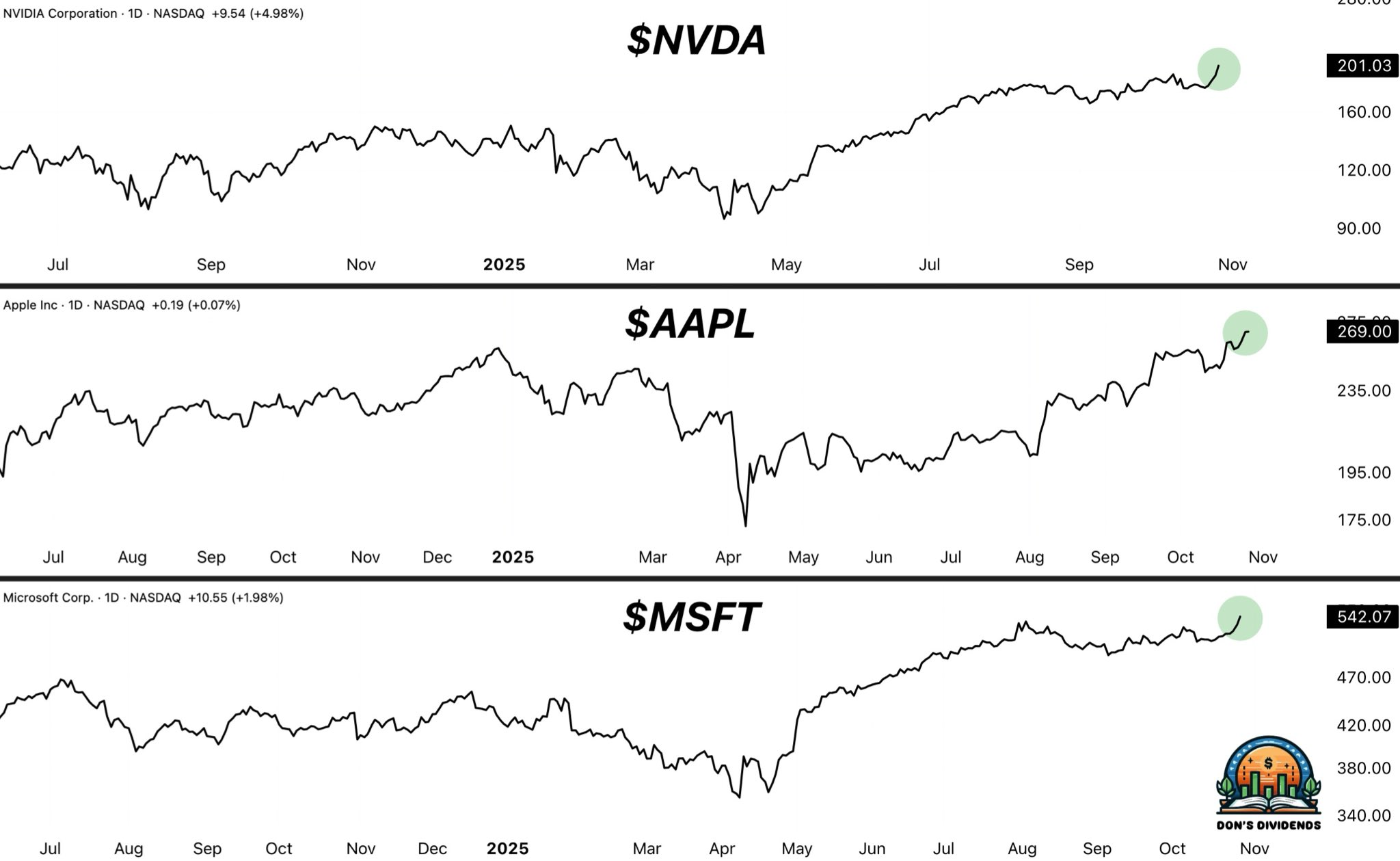

The three largest companies in the world (Nvidia (NVDA) , Apple (AAPL) and Microsoft (MSFT) ) all hit new all-time highs yesterday

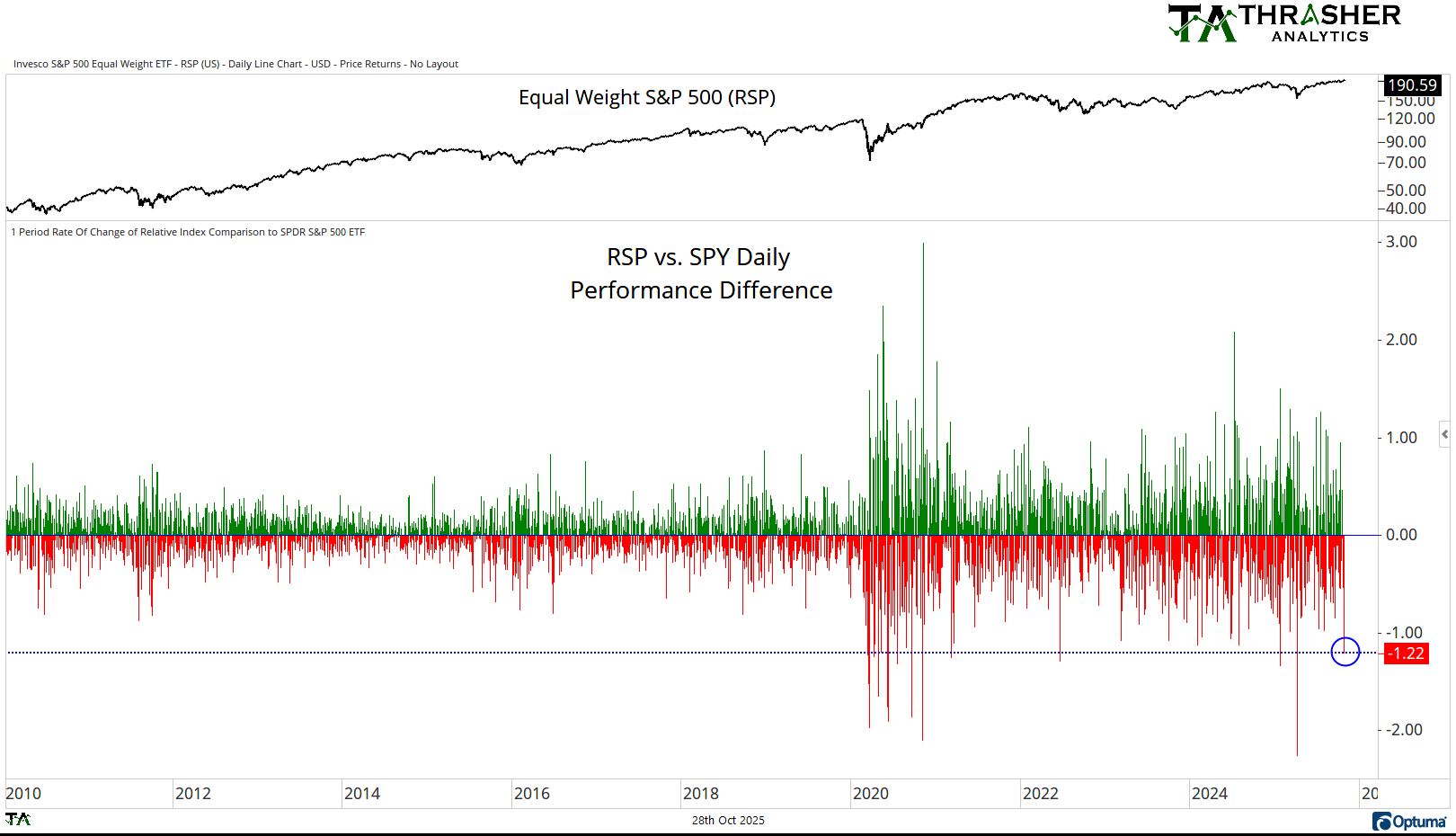

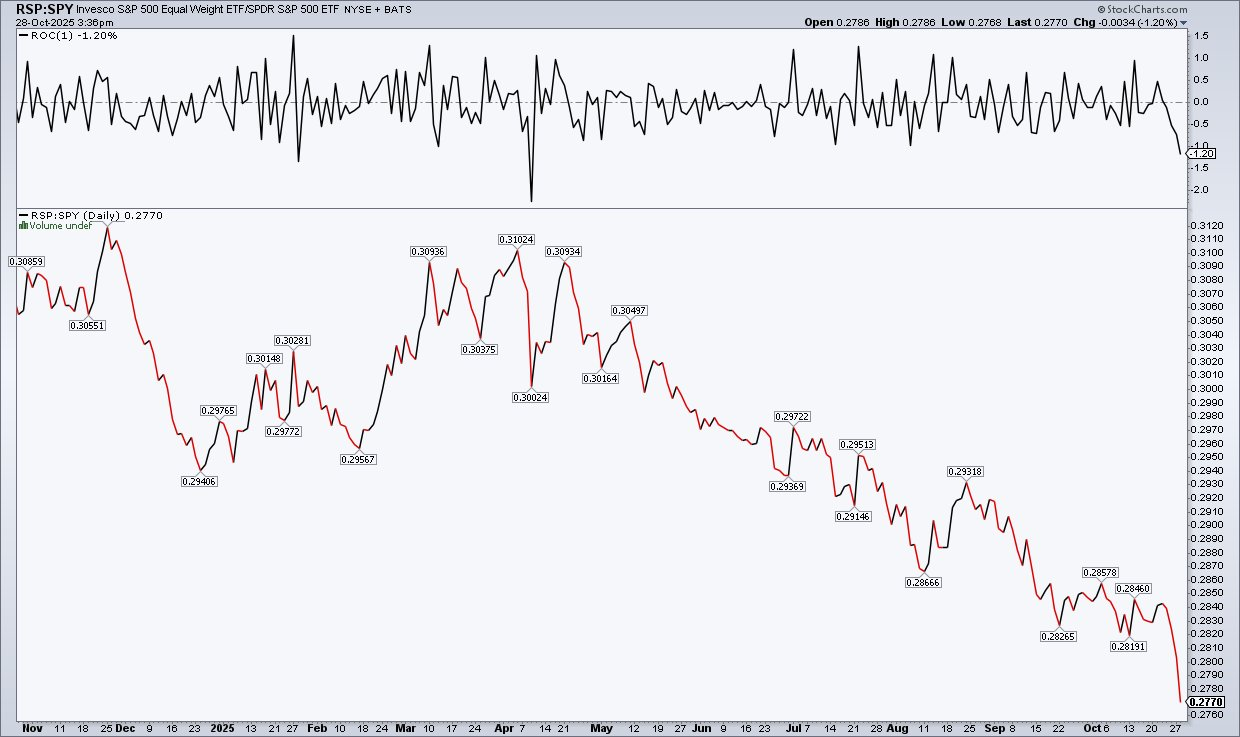

The disparity between the cap-weighted and equal-weighted S&P index have rarely been greater:

And the difference between (RSP) and (SPY) was the greatest since early April, 2025:

Finally, Bespoke's tweet will be distributed widely this morning:

Warren Buffett reminds us that over the short run the market is a voting machine but in the long run it is a weighing machine.

The Oracle's observation, however, can be questioned in a market that is dominated by passive investing (quants and exchange-traded funds), which prize momentum and worship at its altar and by options traders who are not really traders at all -- who operate more like gamblers (considering nearly 70% of daily volume represented by zero day to expiration options):

I am convinced that the market's top-heavy status and casino-like trading/gambling will be resolved by lower prices - but given how wrong I have been regarding the market's direction, it would be arrogant of me to say I know when the timing of the downturn may be.

It could be today, it could be tomorrow, it could be next week or it could be in the next few months.

At this point I have no freakin' clue.

This week I heard from two of the most knowledgeable market observers extant:

* The first investing icon - who has been as bearish as I have - wrote (from a calendar sense) that it is hard to fight the markets at this time of the year.

* The second investing icon - who has been a cautious (but almost fully invested) Bull - is convinced the market is making an important top this week.

In times like this, actually all the time, I try to remain unemotional - assessing reward vs. risk with a calculator in hand.

I remain skeptical of many of the aspects of AI (financing, usability, user sets, energy challenges, expected low return on invested capital, etc.) as represented by nearly 140 "More Tales From Nvidia" columns. (See "Heard in Silicon Valley quote at the beginning of today's missive!):

I also remain net short in exposure - as according to my analysis, risk dwarfs reward by numerous multiples.

That said (stated simply), I have sh#t on my face...

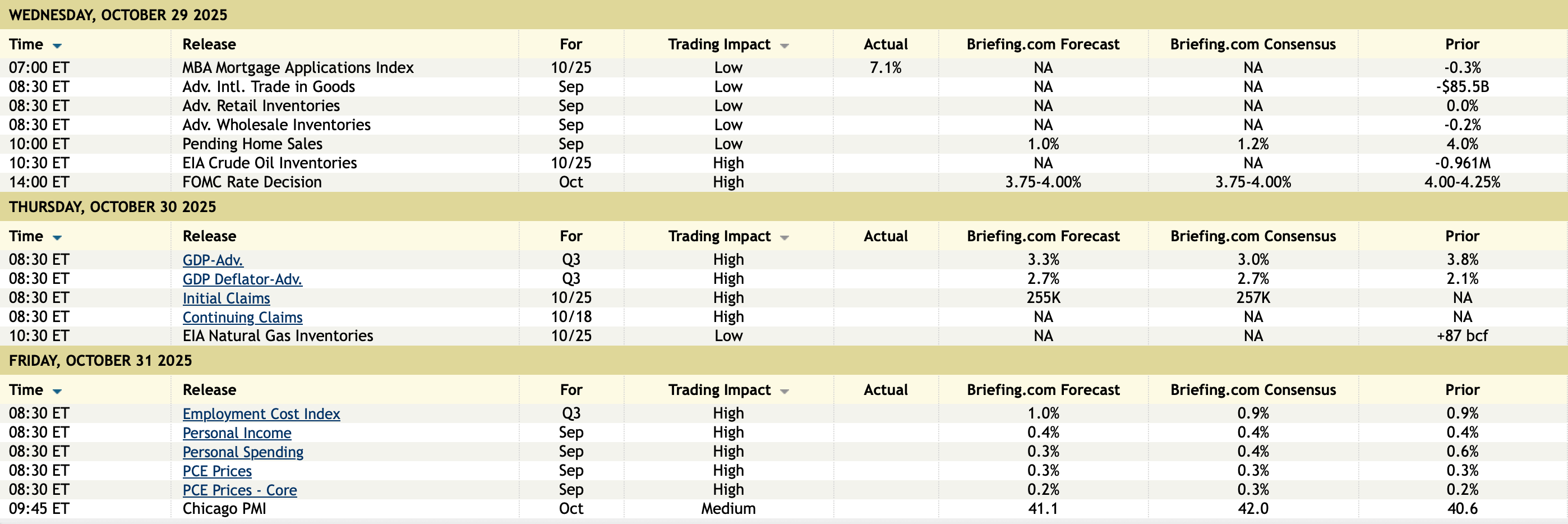

BY Doug Kass · Oct 29, 2025, 10:00 AM EDT

From Peter Boockvar:

One more thing, on stock market sentiment I mentioned in my earlier note that in the weekly Investors Intelligence survey that Bears fell to just 13.5 and a level I can’t even remember seeing this low. Thanks to my friend Helene Meisler, she mentioned that it’s the lowest since January 2018 when it touched 12.2. The spread between Bulls and Bears is now the widest since late July 2024.

BY Doug Kass · Oct 29, 2025, 9:50 AM EDT

From Peter Boockvar:

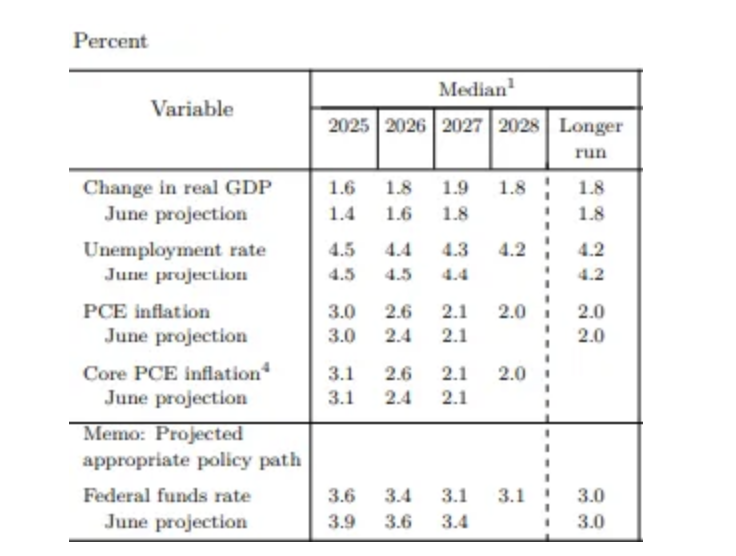

Remember the matrix below? It was the dot plot from the September meeting and as you can see, under the current make up of the Fed under Jay Powell, the ‘longer run’ median REAL rate is 1%. So, after the 25 bps rate cut today the effective fed funds rate will be 3.87% and comparing that to the 3% core CPI figure seen last week and figure about a 2.7-2.8% core PCE (assuming the usual differential), the REAL rate by days end will be around 1%. With the fed funds futures currently pricing in an 82% chance of another cut in December, I think there is a high likelihood that Jay Powell today could be much more neutral about that meeting than the markets anticipate and thus those odds could fall. Not that they won’t cut but if they are going to stick to that ‘longer run’ REAL rate, it could take further deceleration in the inflation rate and/or a further rise in the unemployment rate.

My bottom line, I think Powell is going to be more hawkish than the markets anticipate today. Outside of this, expect an end to QT as there are clear signs of liquidity tightness in short term money markets evidenced by a variety of signals. One in particular, after the Fed cut in September, the effective fed funds rate was 4.08% vs 4.12% today.

If I’m right, expect a selloff in Treasuries and if the BoJ surprises us with a rate hike tomorrow, expect it to continue.

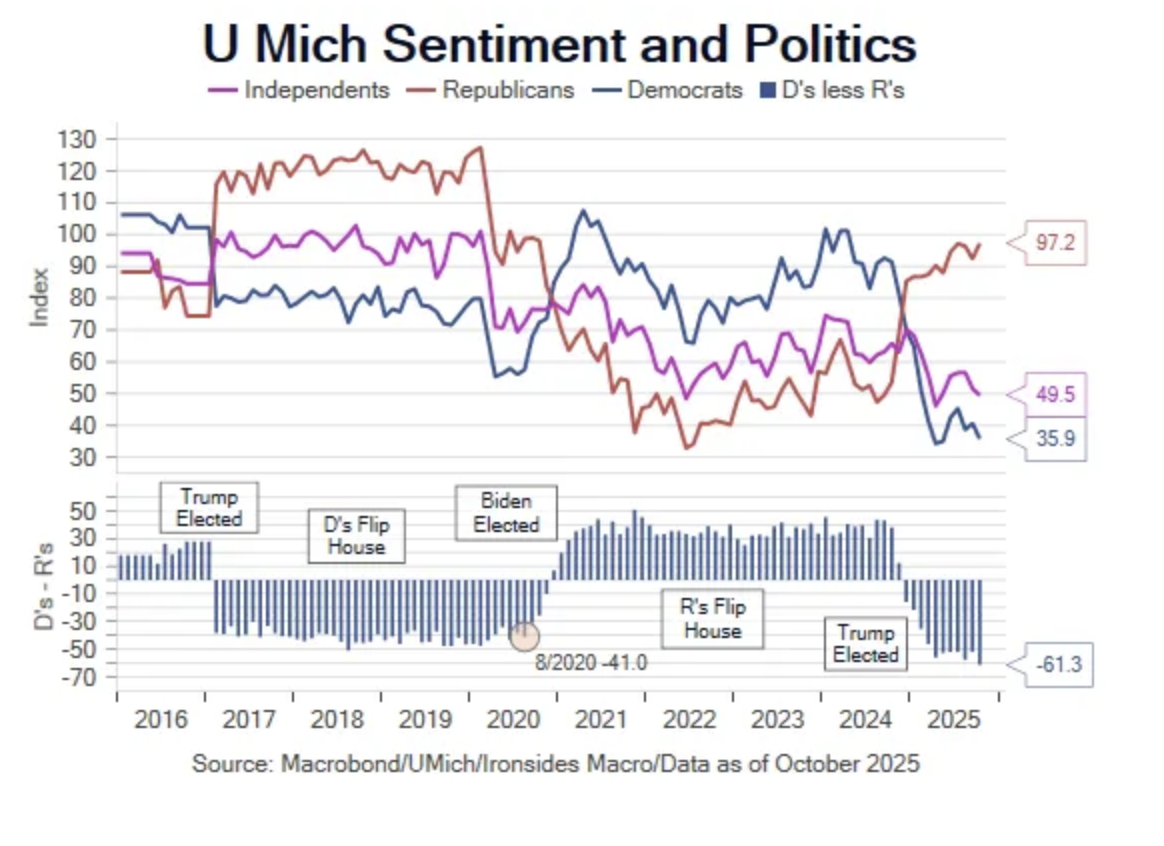

As a follow up to my chart yesterday of the consumer confidence of Independents, my friend Barry Knapp of Ironsides Macro sent me this great chart of the political breakdown of consumer confidence over different administrations and following midterm elections.

For those paying closer attention to the private credit world, I highly recommend this read from yesterday’s WSJ, https://www.wsj.com/

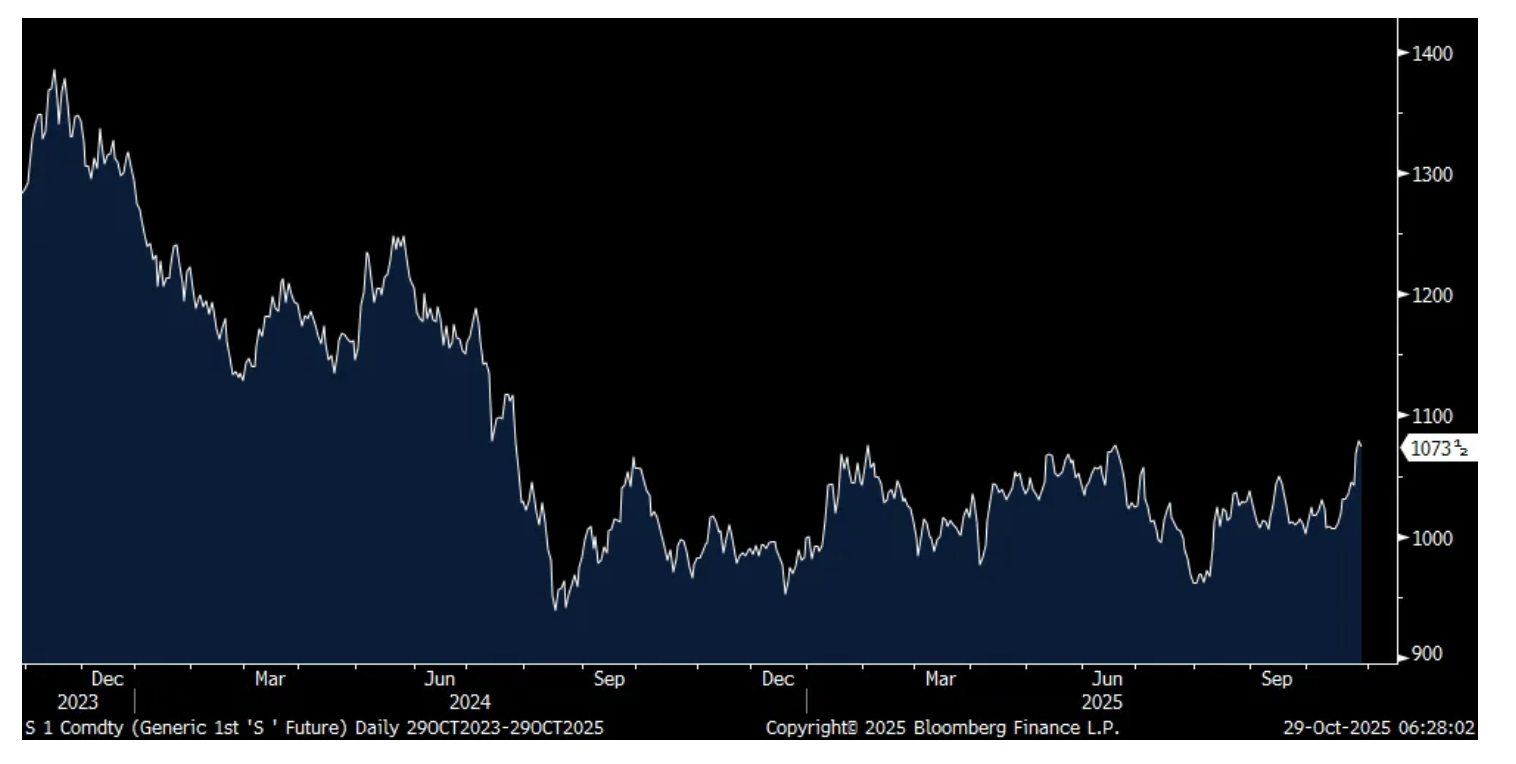

Ahead of the Trump/Xi meeting tomorrow, soybeans closed at the highest level since July 2024 yesterday, though down a touch today. China did buy a few shipments of US soybeans this week for the first time this harvest and ahead of the meeting and are we going to give them Nvidia Blackwell chips in return?

Soybeans

A follow up to yesterday’s comment on the extent to which the NDX is above its 200 day moving average. With today’s opening it will reach 19% and we can now add from a sentiment standpoint, the Investor Intelligence survey out today saw Bears down to just 13.5 vs 15.1 in the week before and I can’t remember the last time it was this low. Bulls rose to 57.2 from 52.8 and thus puts the spread to 43.7 and above the 40 danger zone that we’ve seen in the past.

After four weeks of declines, purchase applications rebounded by 4.5% while refi’s were up by 9.3%. This comes as the average 30 yr mortgage rate fell to 6.3% from 6.37%. It’s good to see the rise but it’s clear that buyer demand has only modestly been stimulated by the drop in rates and that’s because it’s not enough considering how expensive the average home now is.

To the flood of earnings.

From UPS, whose stock jumped on good execution and with a cheap valuation:

“Looking at ADV (average daily volume), it increased 5.9%, marking the fifth quarter in a row of growth. But due to the changes in trade policy, export volume fell in our higher margin lanes and grew in our lower margin lanes. This volume mix change pressured our international operating margin and also pressured our forwarding business.”

“SMB (small/medium sized businesses) average daily volume was down 2.2% vs last year. However, we continue to see bright spots in SMB healthcare and automotive, as well as growth from DAP, our digital access program.”

On these SMBs, “some are doing just fine and managing through the changes in trade policy, and some of them candidly are challenged. So we’ve got a close attention to these customers.”

Their biggest 100 customers which make up 80% of their holiday peak surge “expect a good peak...So they’ve got the inventory, they’re ready for peak. On the SMB side, they’re a little short of where they were a year ago.”

Don’t think the impact of tariffs is over for these SMBs, “it’s still something I think to watch out for, particularly as we head into next year, because next year is when you’re going to feel the full brunt of some of these tariffs hitting some of these SMBs.”

From Visa, which continues to benefit from the secular shift to digital payments and away from cash use:

“US payments volume was up 8%, slightly above Q3, with e-commerce growing faster than face-to-face spend. Credit and debit were both up 8%, reflecting resilience in consumer spending.”

“When we look at quarterly spend category data in the US, we saw broad based strength, including improvements in retail services and goods, travel and fuel. Both discretionary and non-discretionary spend were up from Q3. And growth across consumer spend bands remained relatively consistent with Q3 with the highest spend band continuing to grow the fastest.”

International growth of 10% was led by Asia Pacific, “driven by timing effects and a modest improvement in Mainland China.”

From Whirlpool whose stock rallied 5% yesterday:

“our Q3 results demonstrate organic growth while our margins are still impacted by tariff pre-loading in the industry.” They grew organic growth via their KitchenAid small domestic appliance business and market share gains in the major appliance business.

With 80% of their sales in produced in the US vs their competitors that are mostly importers, they like the tariffs but it did cost them 250 bps in added costs in Q3, totaling $100 million.

And why they will benefit ultimately from the tariffs, “we expect to face approximately 3% cost increase on an annual basis. Our foreign competitors on the other hand are estimated to experience approximately 5% to 15% cost increase, depending on their production footprint, as they are largely importers in the US.”

From Sherwin Williams whose stock also bounced by 5%:

They “delivered solid third quarter results as we continued to execute our strategy in a demand environment that remains softer for longer, as we have previously described.”

“we continue to navigate a very choppy demand environment across every one of our end markets.”

From DR Horton:

“New home demand remains impacted by affordability constraints and cautious consumer sentiment.”

“Our cancellation rate for the quarter was 20%, up from 17% sequentially and down from 21% in the prior year quarter. Our cancellation rate is in line with our historical average.”

On incentives, they’ve bought down mortgage rates for some down to 3.99%.

On the cadence of business, “I think we did see decent demand throughout the quarter. It was choppy as rates were a little bit volatile, and that will push people off the couch and back onto the couch, it seems like with the headlines, but we did lean into the incentives pretty hard in the quarter as we talked about and we expected to.”

From Booking Holdings and whose stock is popping pre market:

Q3 room nights rose 8% y/o/y. “This exceeded the high end of our prior expectations, driven by healthy demand across all of our major regions. Of particular note was the US, where growth accelerated to high single digits, supported primarily by stronger outbound travel and momentum in our B2B business.”

“Our globally diversified portfolio proved its value once again as we continue to see robust growth in certain travel corridors, including Canada to Mexico and Europe to Asia, which effectively offset softer demand in certain inbound corridors to the US. Notably, our US booker room night growth accelerated meaningfully from the second quarter, driven by solid improvements in domestic and outbound growth, and we believe our growth once again outpaced the broader US accommodations industry in a meaningful way.”

That said, in the US we continue to see slightly lower ADRs and a shorter length of stay versus the prior year, which may indicate that some US consumers are continuing to be thoughtful on their discretionary spending.”

Again, that bifurcated consumer.

From Mondelez and whose stock is down $3 pre market:

“Lingering softness in European chocolate consumption following the summer heat wave, combined with record high cocoa input costs, impacted our results for the quarter.”

“In North America, consumer confidence remains weak due to broad economic uncertainty and cost of living concerns, exacerbated by the ongoing US government shutdown. The US biscuits category has softened over the last three months, with value seeking consumers increasingly turning to discounters and club stores, while higher income consumers increasingly are choosing premium and better-for-you products.”

Again, that bifurcated consumer.

Overseas, Australian bond yields are rising after Q3 CPI rose 3.2% y/o/y, above the estimate of 3% and the trimmed rate was higher by 3%, 3 tenth more than expected.

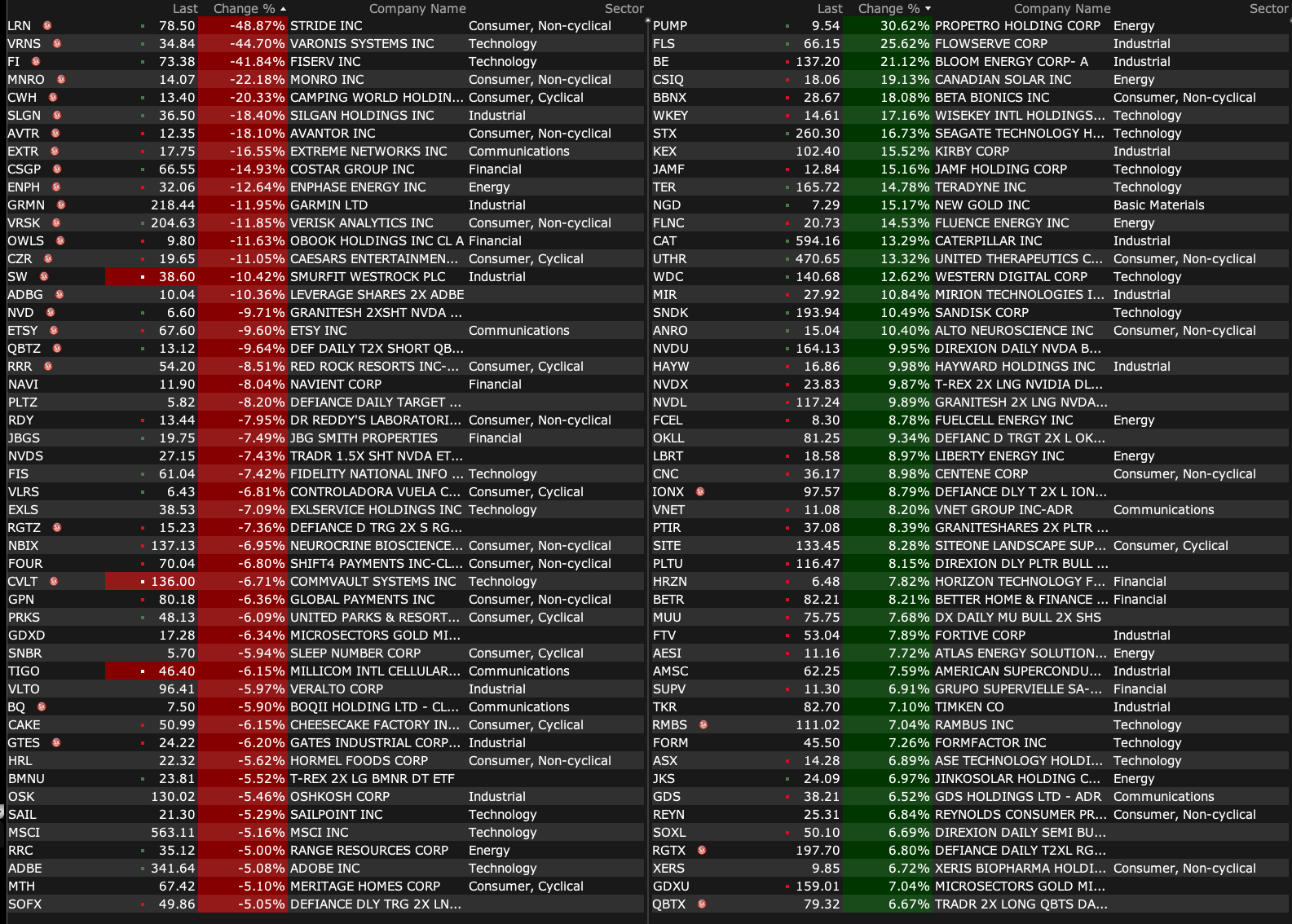

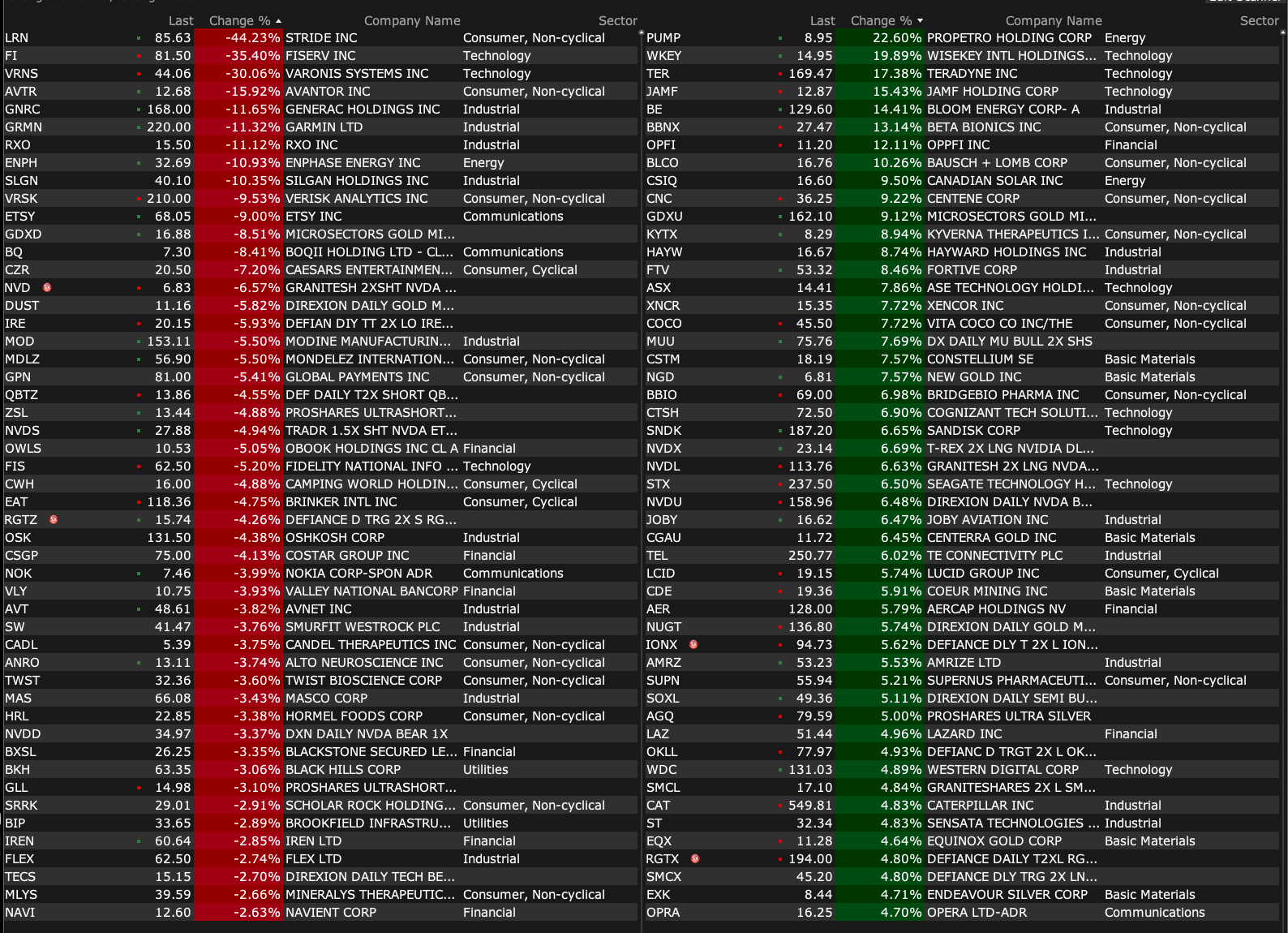

BY Doug Kass · Oct 29, 2025, 9:35 AM EDT

-PUMP +27% (earnings, guidance)

-TER +16% (earnings, guidance; appoints new CFO)

-ZEUS +16% (to be acquired by Ryerson Holding in an all stock deal)

-JAMF +15% (confirms to be acquired by Francisco Partners at $13.05/shr all-cash)

-BE +14% (earnings, guidance)

-CRTO +11% (earnings, guidance)

-CNC +9.3% (earnings, guidance)

-FTV +9.3% (earnings, guidance)

-BBIO +7.8% (Encaleret Phase 3 Topline results in patients with Autosomal Dominant Hypocalcemia Type 1 met primary and secondary endpoints)

-COCO +7.7% (earnings, guidance)

-FUBO +7.7% (completes Business Combination with Disney’s Hulu + Live TV)

-LCID +6.3% (Uber to use Lucid vehicles; Uber plans to offer driverless rides in San Francisco next year)

-STX +6.3% (earnings, guidance)

-CTSH +6.2% (earnings, guidance)

-CAT +5.8% (earnings, guidance)

-ODFL +5.1% (earnings, guidance)

-NESR +4.4% (Saudi Aramco Awards Multi-Billion Dollar Unconventional Contract to NESR)

-AER +4.1% (earnings, guidance)

-VZ +4.1% (earnings, guidance)

-CVS +3.5% (earnings, guidance)

-NVDA +3.4% (momentum)

-OTIS +3.0% (earnings, guidance)

-LRN -44% (earnings, guidance)

-FI -37% (earnings, guidance; names new CFO)

-VRNS -31% (earnings, guidance)

-AVTR -18% (earnings, guidance)

-ENPH -11% (earnings, guidance)

-GRMN -11% (earnings, guidance)

-VRSK -9.7% (earnings, guidance)

-ETSY -8.8% (earnings, guidance; names new CEO)

-CZR -8.3% (earnings, guidance)

-RYI -6.7% (earnings, guidance)

-EAT -5.9% (earnings, guidance)

-MDLZ -5.5% (earnings, guidance)

-TYGO -5.5% (earnings, guidance)

-WULF -4.0% (announces Proposed Private Offering of $500M of Convertible Notes)

-HRL -3.4% (guidance)

-IREN -3.1% (H.C. Wainwright Cuts IREN to Sell from Buy, price target: $45)

-SW -2.8% (earnings, guidance)

-FLEX -2.5% (earnings, guidance)

-ADP -2.0% (earnings, guidance)

BY Doug Kass · Oct 29, 2025, 9:07 AM EDT

BY Doug Kass · Oct 29, 2025, 9:05 AM EDT

11:30 AM: Treasury hosts a $69B 17-Week Bill Auction

11:30 AM: Treasury hosts a $30B 2-Year FRN Auction

BY Doug Kass · Oct 29, 2025, 8:53 AM EDT

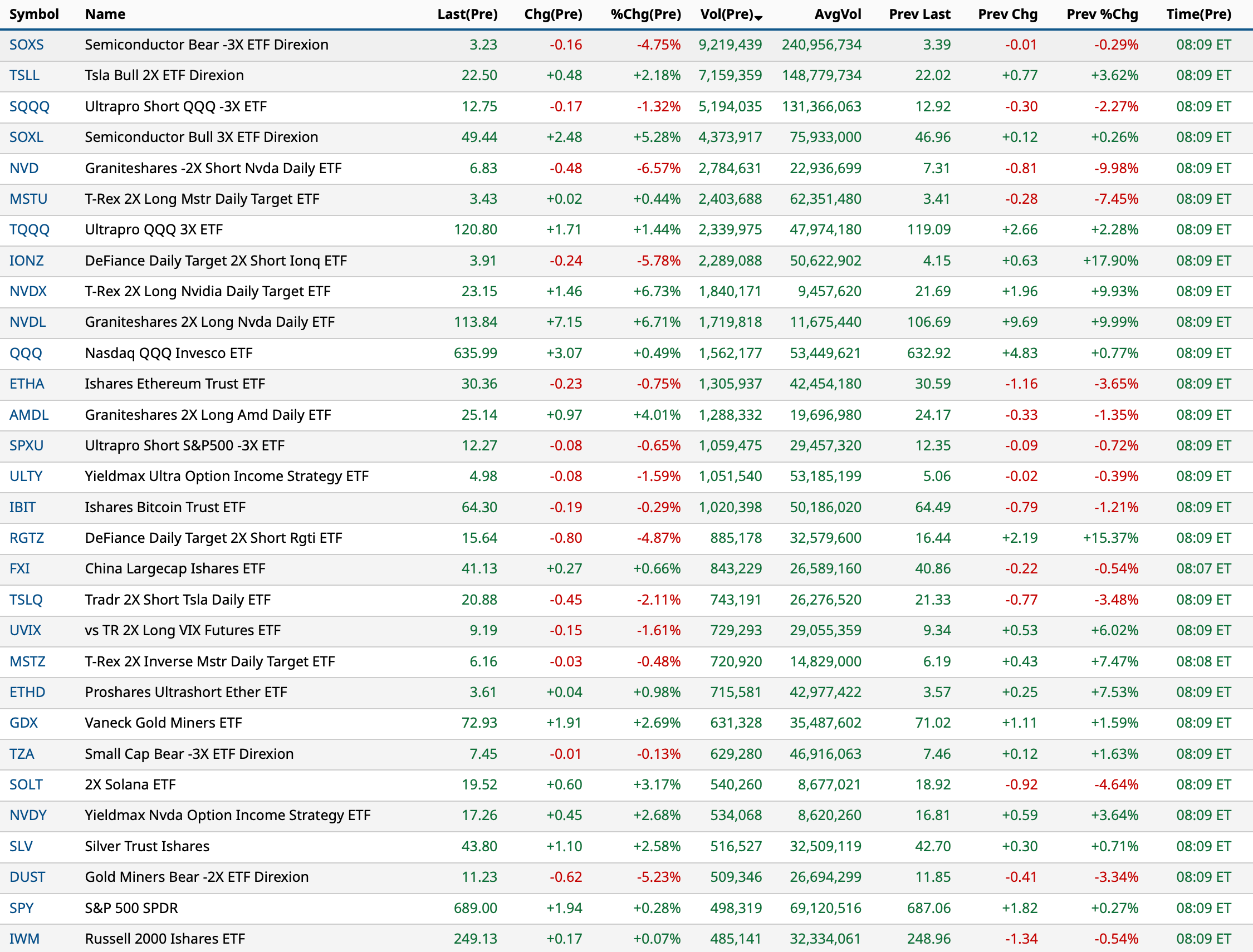

BY Doug Kass · Oct 29, 2025, 8:52 AM EDT

BY Doug Kass · Oct 29, 2025, 8:36 AM EDT

I have added to my index shorts:

* (SPY) $689.28

* (QQQ) $636.16

Short SPY common M calls VS QQQ common M calls VS

BY Doug Kass · Oct 29, 2025, 8:05 AM EDT

BY Doug Kass · Oct 29, 2025, 7:50 AM EDT

BY Doug Kass · Oct 29, 2025, 6:50 AM EDT

BY Doug Kass · Oct 29, 2025, 6:40 AM EDT

BY Doug Kass · Oct 29, 2025, 6:30 AM EDT

BY Doug Kass · Oct 29, 2025, 6:15 AM EDT

BY Doug Kass · Oct 29, 2025, 6:05 AM EDT

I have added to my index shorts:

* (SPY) $689.13

* (QQQ) $636.38

BY Doug Kass · Oct 29, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at 2.74% vs. 4.01%.

BY Doug Kass · Oct 29, 2025, 5:47 AM EDT