Upside:

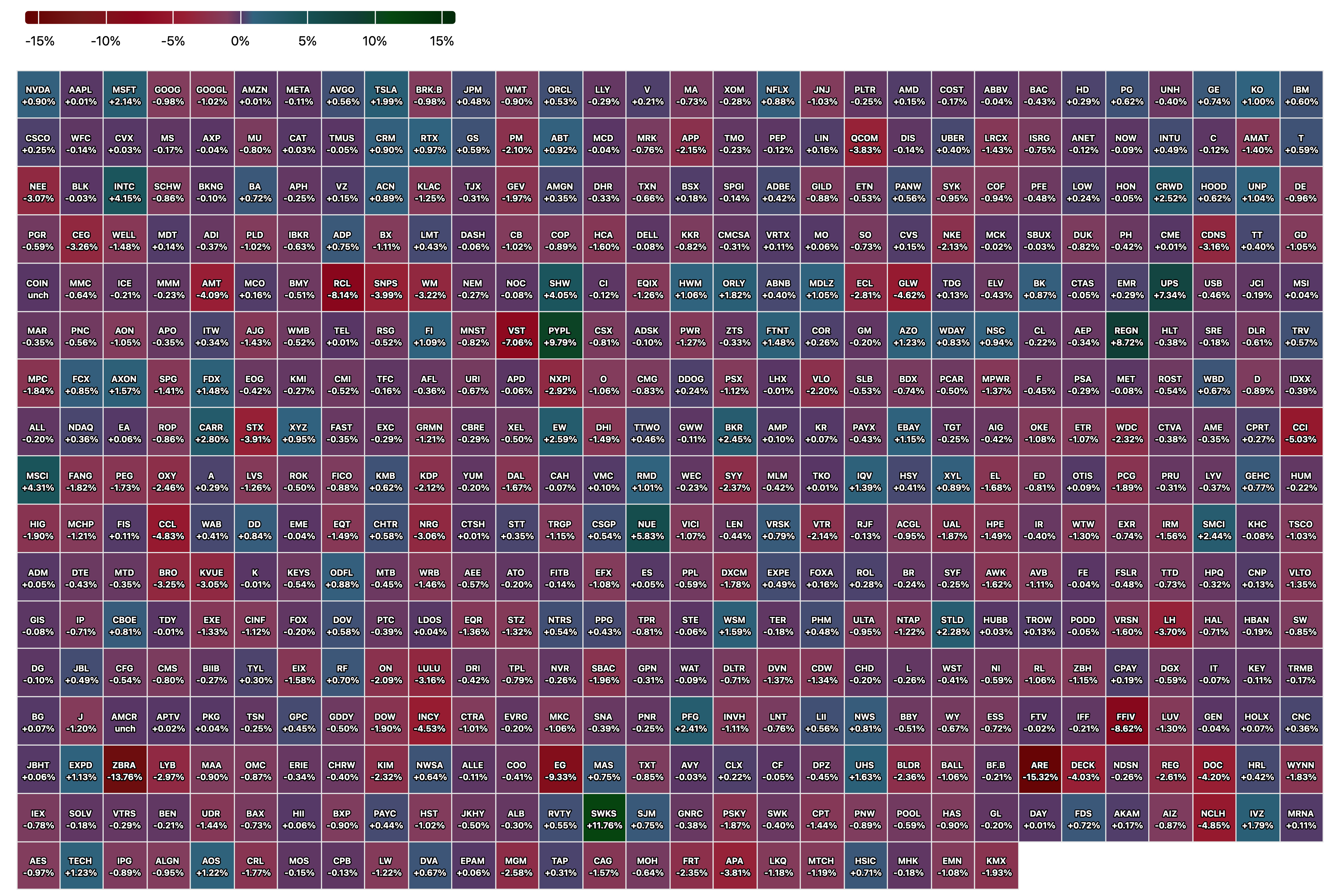

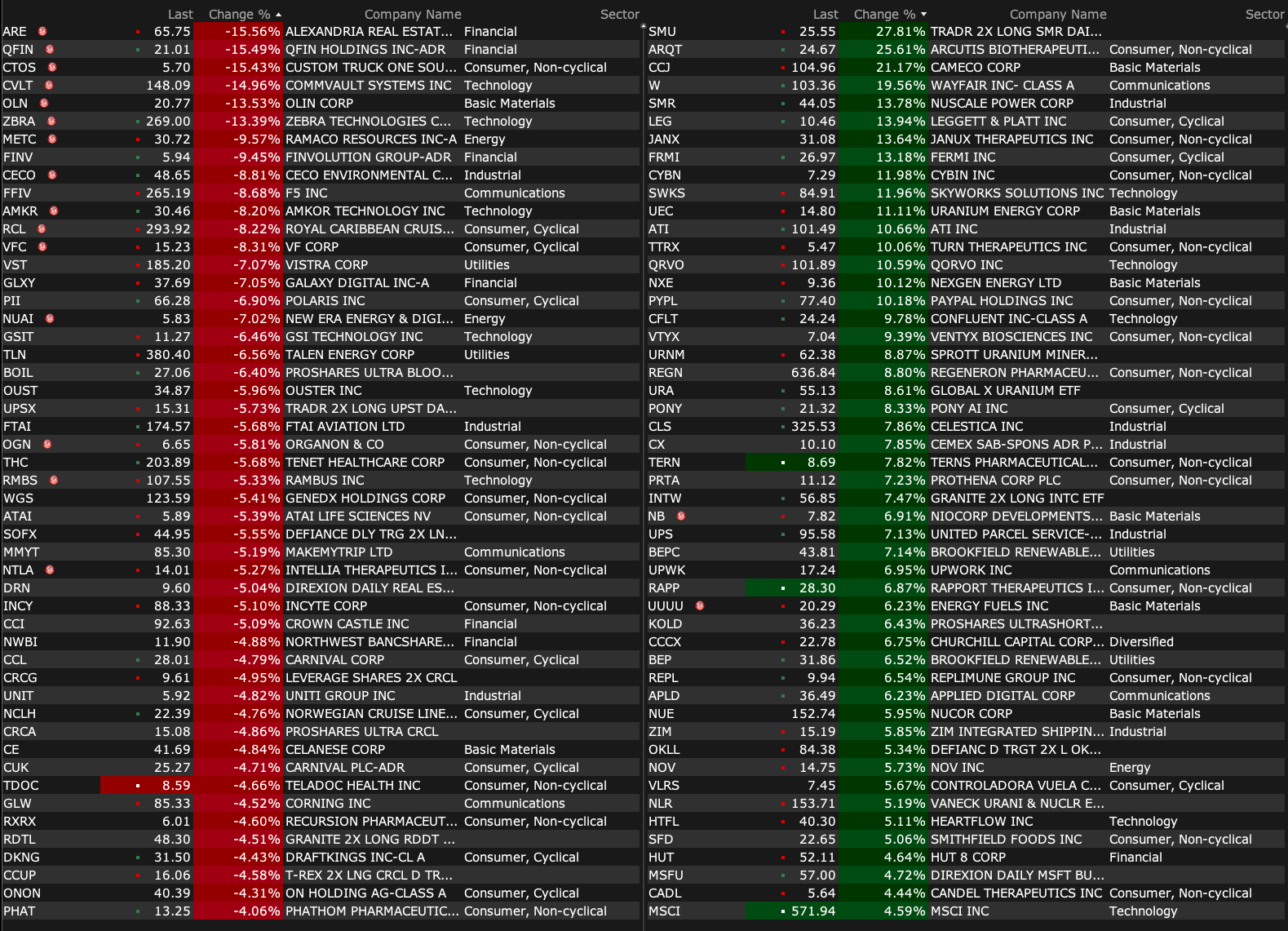

-CCJ +16% (US govt, Westinghouse, Cameco and Brookfield enter a strategic partnership that will see at least $80B of new nuclear reactors constructed in the US)

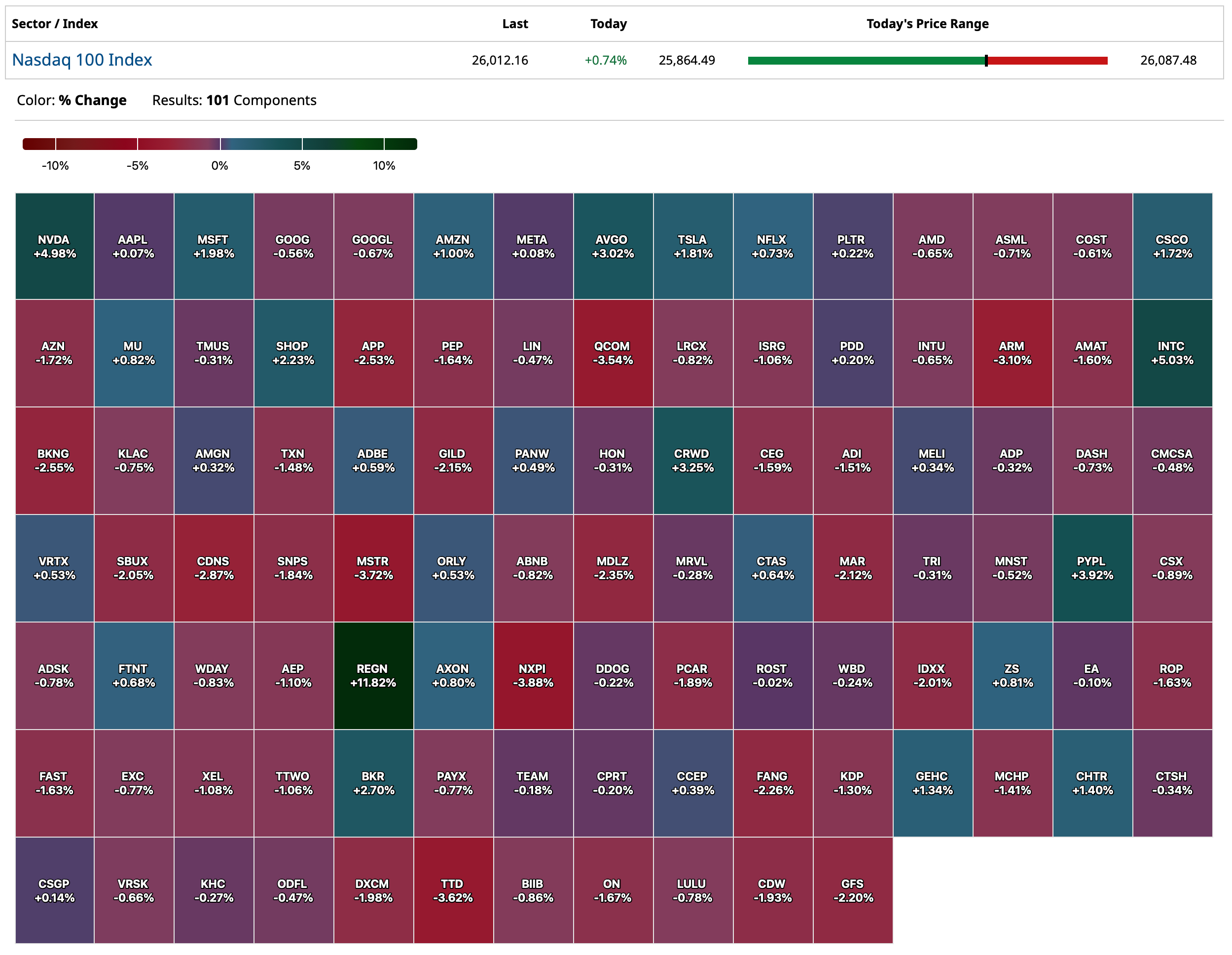

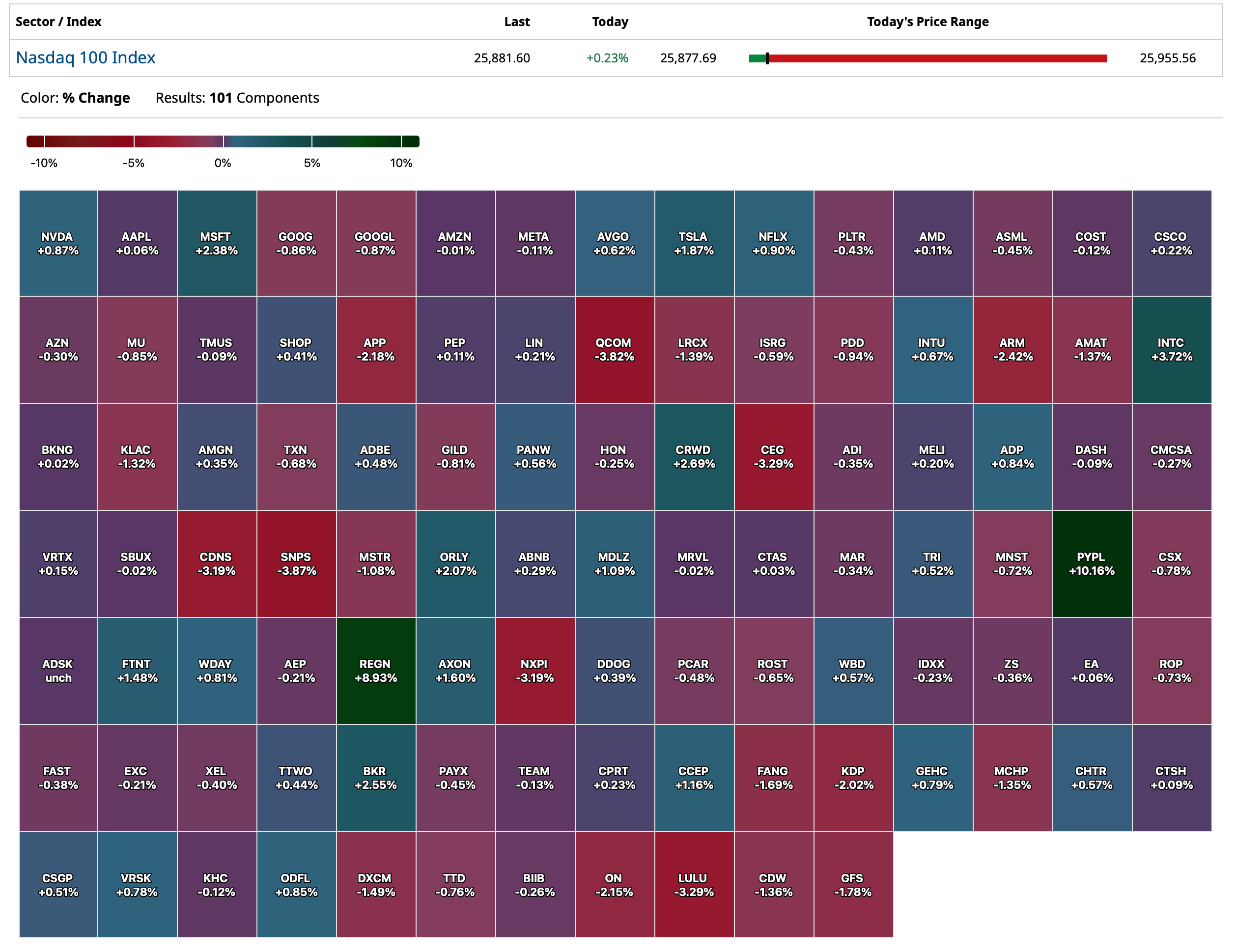

-PYPL +15% (earnings, guidance; OpenAI partnership regarding ChatGPT Wallet deal)

-SWKS +14% (earnings, guidance)

-ATI +13% (earnings, guidance)

-QRVO +12% (Skyworks and Qorvo to merge in $22B deal to create US RF semiconductor leader; earnings)

-UPS +12% (earnings, guidance)

-W +11% (earnings, color)

-CHKP +9.8% (earnings, guidance)

-DJT +9.3% (confirms Truth Social to become World’s First Social Media Platform offering prediction markets via Exclusive Partnership with Crypto.com)

-ALKS +8.5% (earnings, guidance)

-WULF +7.8% (reports prelim Q3 revenue; TeraWulf and Fluidstack form 25-year HPC joint venture for 168 MW critical IT load at Abernathy, TX, expected H2 2026)

-SFD +6.7% (earnings, guidance)

-PONY +6.1% (UBER said to be planning to invest in Pony AI and WeRide Hong Kong listings)

-NEO +5.8% (earnings, guidance)

-WGS +5.6% (earnings, guidance)

-SHW +5.2% (earnings, guidance)

-UNH +4.8% (earnings, guidance)

-IVZ +4.3% (earnings)

-REGN +4.0% (earnings, guidance)

-VFC +4.0% (earnings, guidance)

-CAR +3.8% (earnings)

-AXTA +3.2% (earnings, guidance)

-WRD +3.1% (UBER said to be planning to invest in Pony AI and WeRide Hong Kong listings)

Downside:

-RMBS -15% (earnings, guidance)

-CVLT -9.6% (earnings, guidance)

-RCL -8.5% (earnings, guidance)

-CECO -7.2% (earnings, guidance)

-AMKR -6.0% (earnings, guidance)

-GLW -5.8% (earnings, guidance)

-DHI -5.3% (earnings, guidance)

-SYY -4.5% (earnings, guidance)

-WM -4.1% (earnings, guidance)

-NCLH -3.5% (lower in sympathy with RCL)

-AOS -2.4% (earnings, guidance)

-FLUT -2.0% (Truth Social to become World’s First Social Media Platform offering prediction markets via Exclusive Partnership with Crypto.com)