From JPMorgan:

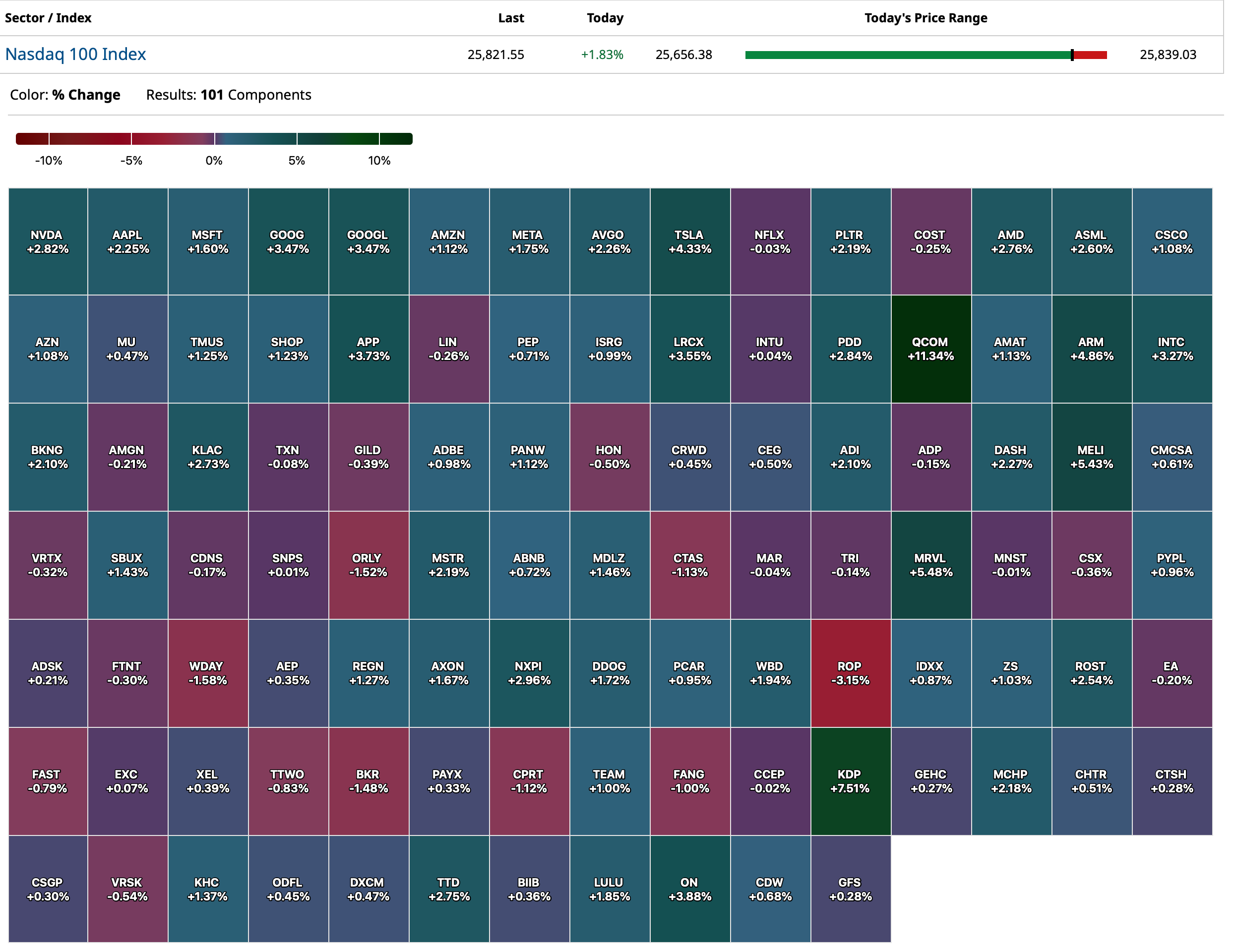

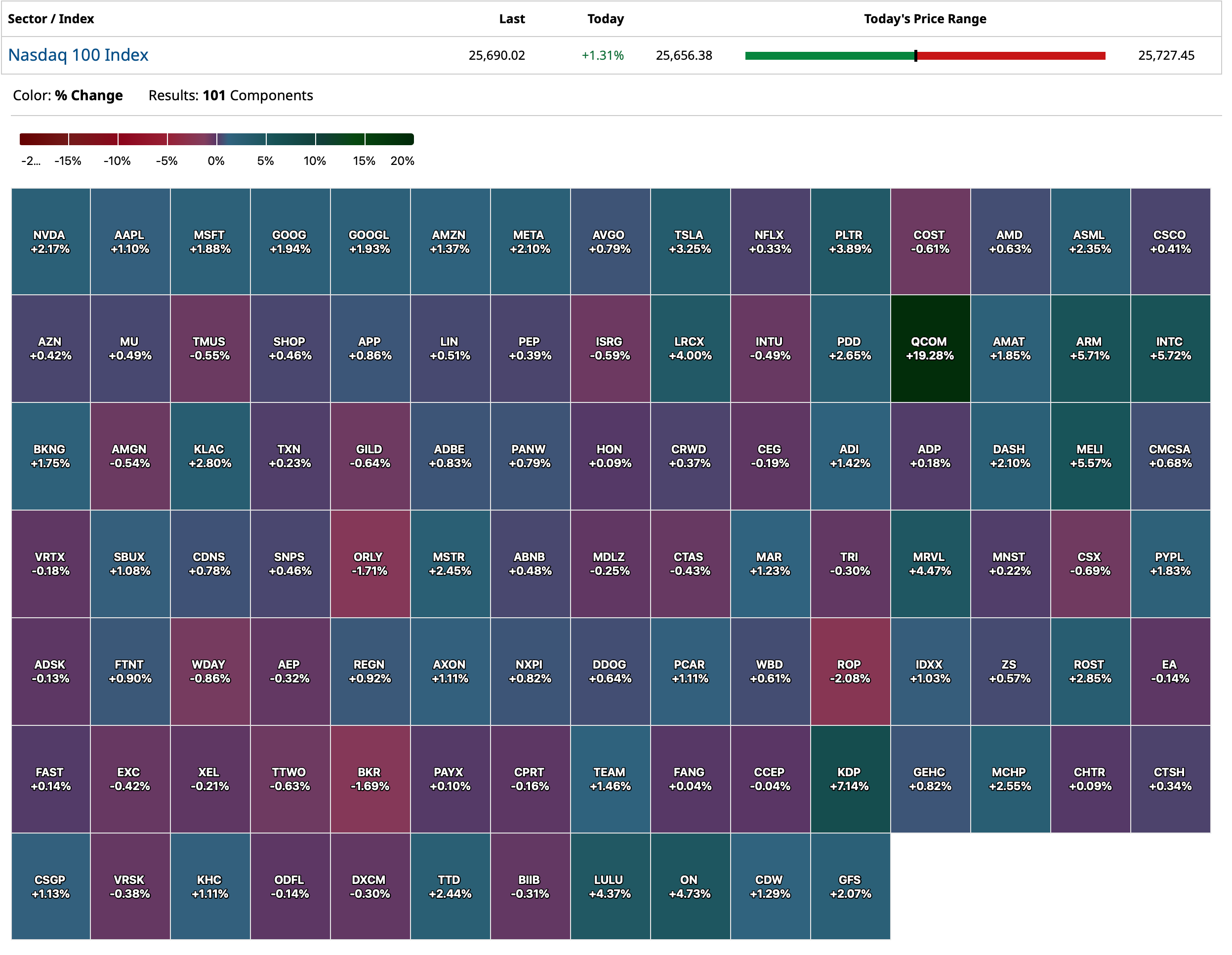

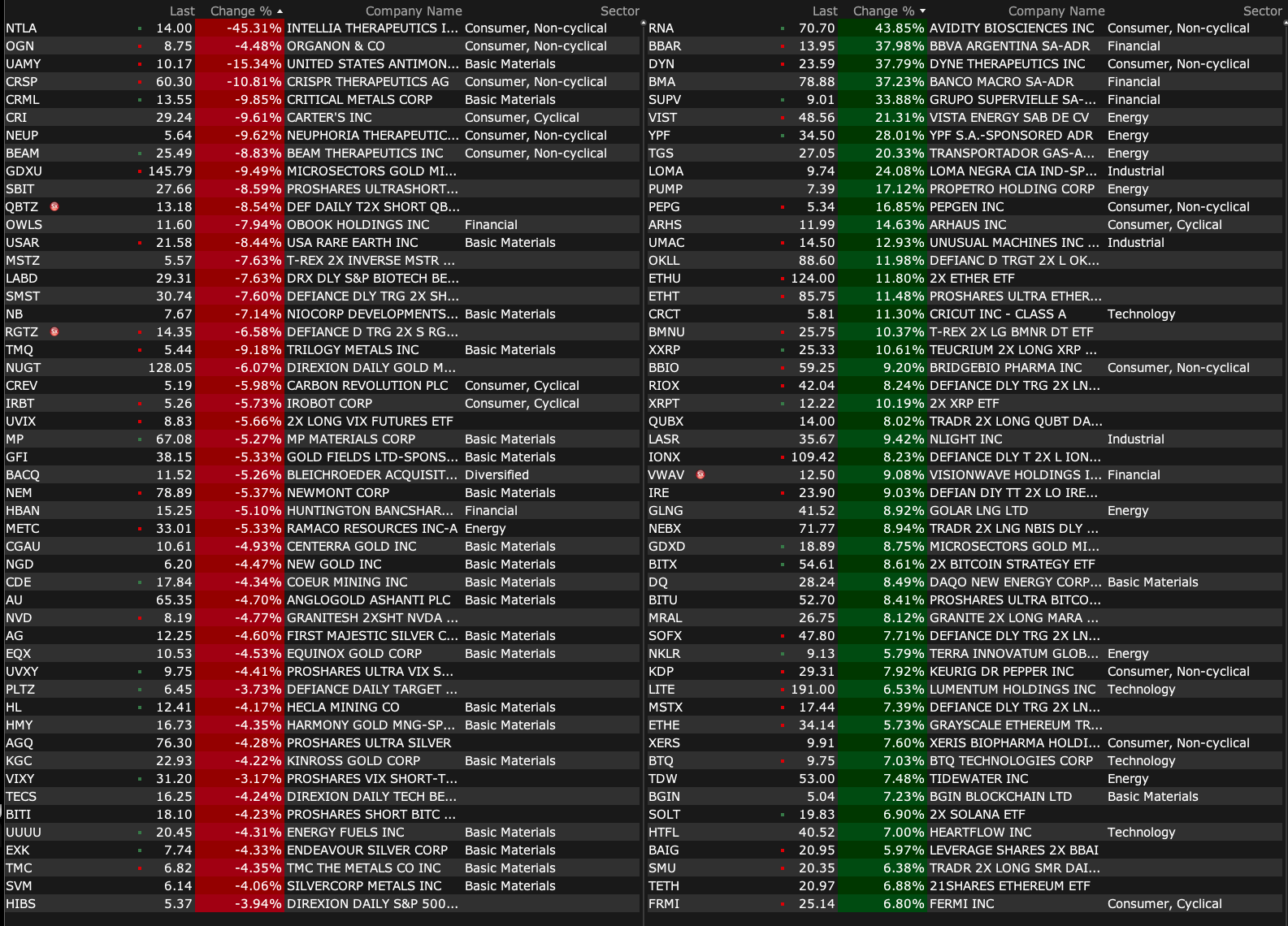

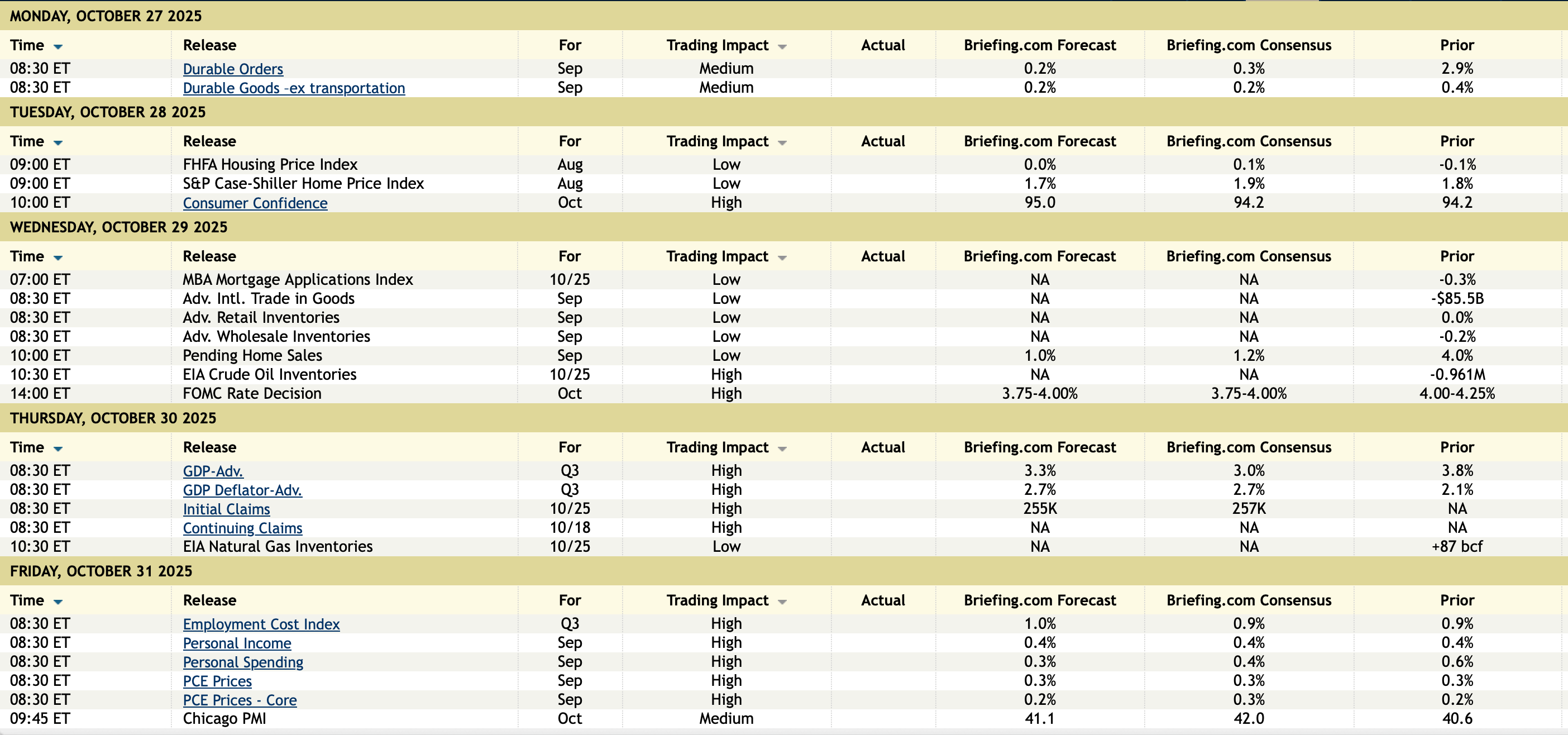

US: Futs are higher as US / China establish a framework of a deal ahead of the Trump / Xi meeting this week. Pre-mkt, NDX and RTY are outperforming as the framework deal is boosting Semis / Mag7 while rare earth plays are under pressure. AMD, AVGO, and NVDA are +2%+ with all Mag7 higher by 86bp to 236bp. Cyclicals are outpacing Defensives with parts of Staples in the red. Bond yields are up 2bp across the curve as USD kicks off the week lower. Cmdtys are mixed as both energy and precious metals are for sale, though base metals are higher and Ags are mostly higher. Earnings and the Fed are the focus this week with ~44% of SPX market cap reporting this week and the Fed likely to cut by 25bps and potentially to halt QT.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Last week, SPX added 1.9%, NDX 2.2%, and RTY 1.2% with SPX and NDX closing the week at all-time highs and RTY closing ~25bp below its all-time high. Over the last two weeks we had a more cautious stance on markets given risks from positioning, technicals, and valuation. While we did see a vol spike and some churn, markets ultimately moved higher. Now, as we enter the bulk of Mag7 earnings with a series of trade deals expected to be formally announced this week, the setup is much cleaner. We are tactically bullish as we think Mag7 earnings will beat expectations; we are removing our cautious tone which ultimately proved to be the wrong call. Speaking with John Schlegel, he tells me that while positioning in the group is high, higher than the last two earnings periods, positioning is similar to early 2024 when the group traded well in 24Q2 ahead of setting a near-term peak in July taking until November to set a new high. Mag7 (proxied using JP1BMAG7 Index) added 17.3% in 24Q1, 17.1% in 24Q2, 3.3% in 24Q3, and 13.4% in 24Q4. More generally, our bullish framework of (i) resilient macro data; (ii) positive EPS growth; and (iii) thawing trade war remains intact receiving a boost from the US / China deal, among others, and expectations for Mag7 names to beat a low earnings bar. As buybacks resume, this may be the strongest quarter on record for buybacks which is the single largest source of Equity demand.