Tweet of the Day

BY Doug Kass · Oct 22, 2025, 4:11 PM EDT

BY Doug Kass · Oct 22, 2025, 4:11 PM EDT

Here are today's things:

* I shorted more indices in the premarket:

(SPY) $672.06

(QQQ) $611.21

* I covered all of my indices during the whoosh lower (and in several stages):

SPY at $666.78

QQQ at $604.29

* I covered a small amount of my (GRNY) short at $24.82.

* I covered my (NVDA) short at $178.01.

* I covered a portion of several individual shorts. (Names withheld to protect the innocent.)

BY Doug Kass · Oct 22, 2025, 3:55 PM EDT

BY Doug Kass · Oct 22, 2025, 3:50 PM EDT

* The reason I spend so much time on this series is because AI is the lynch pin and foundation to the entire market's advance...

Well, Meta (META) quickly went from hiring people for ungodly amounts of money, to this. I guess they too finally figured out it aint working. DOH!

Meta lays off 600 employees within AI unit

And now this:

Airbnb CEO Chesky says ChatGPT isn’t ‘quite robust enough’ to integrate into travel app

BY Doug Kass · Oct 22, 2025, 2:59 PM EDT

With S&P cash -79 handles, I have moved to market neutral — in exposure terms.

I plan to re-short strength.

BY Doug Kass · Oct 22, 2025, 1:59 PM EDT

I just covered my Trade of the Week (to short (NVDA) at $183.71) for a quick profit.

Done at $178.01.

From Monday:

As discussed in my "More Tales From Nvidia" (Issues #120-#131 over the last week!) there are already some developing cracks in the foundation of AI growth.

After the recent strength in AI-related stocks, any broader market correction could result in an exaggerated (on a percentage basis) move lower in (NVDA) .

Today, might be the start of something... with inner circle/brethren (ORCL) (-$14.60) and (CRWV) (-$8) all lower on the day.

Even NVDA is only +$0.60 in a sea of green.

A conservative way of taking on a NVDA short would be to buy (short term) out-of-the -money calls to define risk.

Position: Short NVDA (VS)

By Doug Kass Oct 20, 2025 2:58 PM EDT

BY Doug Kass · Oct 22, 2025, 12:58 PM EDT

BY Doug Kass · Oct 22, 2025, 12:50 PM EDT

With S&P cash -38 handles I have covered the balance of my index shorts:

* (SPY) 4667.80

* QQQ $605.37

I plan to re-short strength.

BY Doug Kass · Oct 22, 2025, 12:40 PM EDT

Equities make a move lower on a Reuters report that the U.S. will increase export curbs to China.

BY Doug Kass · Oct 22, 2025, 12:36 PM EDT

With S&P cash -38 handles I have reduced my index shorts from medium to small-sized:

* SPY $667.85

* QQQ $604.90

I plan to re-short strength.

BY Doug Kass · Oct 22, 2025, 11:39 AM EDT

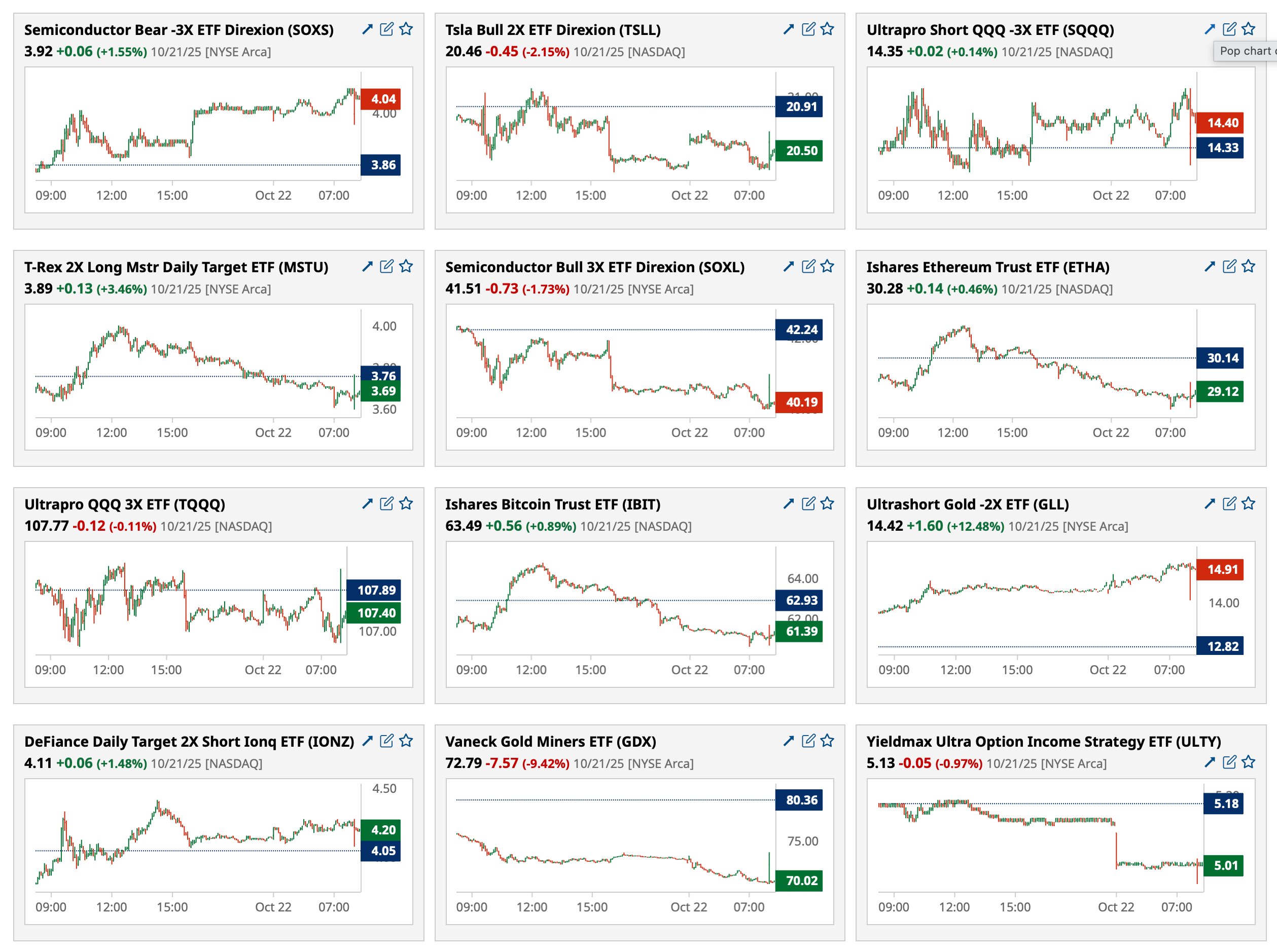

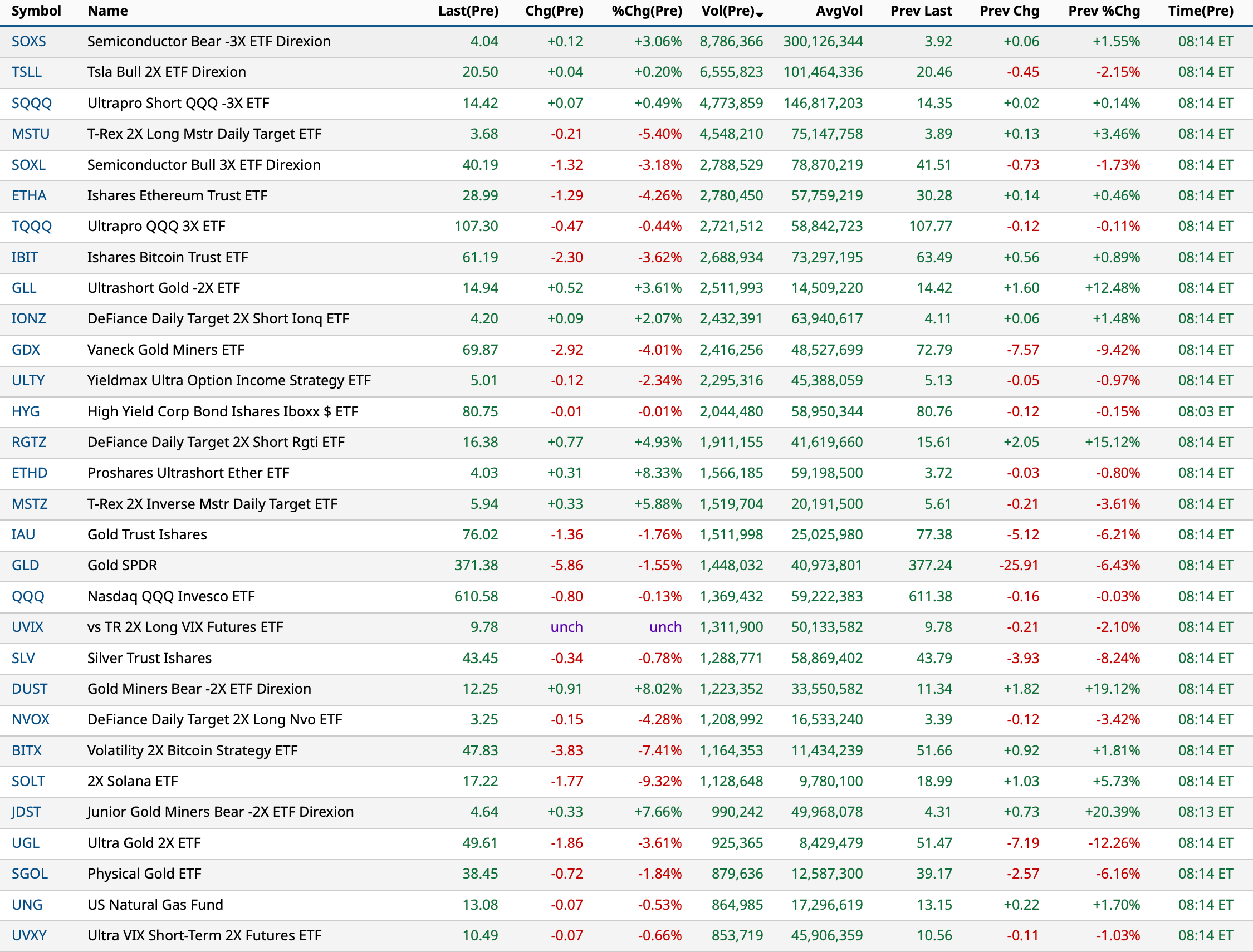

* Charts from 10:48 a.m. ET

BY Doug Kass · Oct 22, 2025, 11:20 AM EDT

BY Doug Kass · Oct 22, 2025, 11:00 AM EDT

With S&P cash -30 handles I am taking in yesterday's and this morning's Index shorts for a good and swift profit:

* (SPY) $668.52

* (QQQ) $606.51

Back down to medium-sized.

From this morning:

* Raising short exposure...

More Index shorts:

* (SPY) $672.12

* (QQQ) $611.03

Position: Short SPY m/l QQQ m/l

Short SPY M QQQ M

Oct 22, 2025 9:37 AM EDT

Short SPY M QQQ M

Oct 22, 2025 9:37 AM EDT

BY Doug Kass · Oct 22, 2025, 10:51 AM EDT

From Randorama:

7 minutes ago

CFRA, an independent research provider, Lowers Rating On Shares Of Netflix, Inc. To Buy From Strong Buy

We lower our target price by $185 to $1,300, applying a forward TEV/EBITDA of 32.9x compared to three-year historic average at 30.0x. Our EBITDA estimates are $14.0B in 2025 and $17.3B in 2026. We lower our 2025 EPS estimate by $1.05 to $25.15 and 2026's by $0.50 to $32.50, compared to consensus at $25.46 and $32.27, respectively. Our revenue projections are $45.1B and $50.6B, which supports mid-teen revenue growth. Revenue in Q3 2025 grew 17.2% Y/Y, and the same on an FX neutral basis. NFLX reported an earnings miss in Q3 2025 at $5.87 versus $6.95 consensus, mostly due to cumulative accounting charge of $619M for its operations in Brazil since 2022. The company emphasized that absent this expense, NFLX would have exceeded its Q3 operating margin forecast. Operating margin for the first nine months of 2025 was 31.3% compared to 27.4% for full-year 2024. Q4 2025 has the highest quarterly spend on production and programming costs, which will likely narrow operating margins as its does every year.

BY Doug Kass · Oct 22, 2025, 10:35 AM EDT

From The Street of Dreams:

From JPMorgan:

US: Futs are flat with NDX / RTY lagging as the yield curve shift lower by 1bp and the USD continues its recent move higher. USD is +2.5% since making a 52-wk low on Sep 16. Pre-mkt, Mag7 names are mostly weaker ex-GOOG on its cloud deal. Large-cap Tech earnings missed expectations (NFLX / TXN) with both stocks being punished, -6.8%, -8.5% pre-mkt. Mining stocks are weaker pre-mkt, though gold and silver are bouncing off their overnight lows; both are underperforming platinum / palladium. The balance of the cmdty complex is bid with WTI +1.7% the standout. US / India are said to be close to a trade deal, which could see US cut tariffs to 15% from 50%. US / China situation still has aides talking behind closed doors as Trump / Xi remain likely to meet next week.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, SPX finished flat. We saw a mixed of positive earnings (GM and KO) and momentum unwind in AI themes (GOOG/L, AVGO, Quantum Computing) and precious metals. There were not much incremental on trade updates, but Trump’s remarks today was largely in line with his remarks yesterday. There was a BBG headline saying that Trump may not meet with Xi, which led to an intraday swoon. However, this may be taken out of context as the full quote is, “Maybe it won’t happen. Things can happen where, for instance, maybe somebody will say, ‘I don’t want to meet, it’s too nasty.’ But it’s really not nasty. It’s just business.” On geopolitics, EU / Ukraine are said to have constructed a 12-point plan to end the war even as the US has been said to be delay its support for using Russian assets to fund the Ukrainian effort. A ceasefire would likely pressure oil at a time when the US is said to begin refilling the SPR.

On regional banks, the concerns seem to be eased given Zions earnings and commentary from WFC. CEO from Wells Fargo today said that credit quality at Wells Fargo has been “exceptionally good” with no significant causes for concern (“I think ‘worry’ is a strong word”). In addition, ZION earnings yesterday reiterated that the $50mn charge-off was an isolated incident; similar comments were made by WAL.

AI: ARE STOCKS IN A BUBBLE? Harlan’s Rev / GW “Sanity Check” Suggests Nowhere Near … full note is here. Summary from Josh Meyers

· Following the recent flurry of AI compute capacity deals, Harlan Sur tackles the question of revenue/GW for GPU & XPU rack systems, to assess what expectations are actually priced in to AMD, AVGO & NVDA.

· He walks away from the exercise confident that there is still conservatism baked into estimates

· Maybe it is concerns on infra funding, or competitive dynamics, or execution… regardless, there’s ample room for upside to spending in coming years, supporting his expected 40~50% AI accelerator market TAM – and with it continued positive revisions (with XPU’s slice of the pie growing as a %).

· For NVDA, Harlan models mid-to-high-$20b/GW for Blackwell/Ultra platform silicon, growing to $30b for Rubin/Ultra; based on that estimate, Street consensus seems to bake in ~7 GW of AI DC deployments in CY25, growing to ~9 GW in CY26 (+35%) and ~10 GW in CY27 (+10%)… numbers he thinks undershoot likely growth in GW deployments.

· Ditto AMD, where $20b/GW for Helios and $25b for subsequent platforms gets us a run-rate of $30~35b annual revenue just for OpenAI (market prices in only $31b for DC GPU revenue for AMD in 2027).

· And AVGO ~$27b/GW gets us a run-rate of $70~90b/year for OpenAI alone from F27~29, versus market pricing in only ~$60b for all AVGO AI revenue in C27; laying in just GOOGL TPU gets that AI revenue to nearly $100b in C27, from only $21b this year.

· BOTTOM-LINE: the market remains too conservative in pricing in upside from AI chip demand. Click through to the note to see Harlan’s math, and of course appreciate your feedback!

BY Doug Kass · Oct 22, 2025, 10:15 AM EDT

* Raising short exposure...

More Index shorts:

* (SPY) $672.12

* (QQQ) $611.03

BY Doug Kass · Oct 22, 2025, 9:37 AM EDT

-BYND +80% (expands distribution with Walmart)

-VICR +27% (earnings)

-DNUT +23% (momentum)

-FLWS +23% (momentum)

-ISRG +18% (earnings, guidance)

-NRIX +14% (initiates DAYBreak Pivotal Study of Bexobrutideg in Relapsed or Refractory Chronic Lymphocytic Leukemia; files to sell $250M Registered Offering of 24.5M Shares at $10.21/shr)

-WGO +13% (earnings, guidance)

-PEGA +12% (earnings)

-APH +9.1% (earnings, guidance)

-HCSG +8.6% (earnings)

-VRT +7.6% (earnings, guidance)

-BIOA +6.6% (CitiGroup Raised BIOA to Buy from Neutral, price target: $10)

-APLD +6.4% (signs $5B, 15-year lease agreement with a U.S. Based Investment Grade Hyperscaler at its state-of-the-art, purpose-built Polaris Forge 2 Campus currently under construction near Harwood, North Dakota)

-PMT +4.6% (earnings)

-GEV +4.4% (earnings, guidance)

-BDSX +4.0% (signed an expanded agreement with Bio-Rad to develop, clinically validate, and submit IVD assays using Bio-Rad’s ddPCR technology on the QX600 platform)

-AVDL +3.5% (Alkermes to Acquire Avadel Pharmaceuticals for $18.50/shr cash with CVR for an additional $1.50/shr cash for total consideration of up to $20.00/shr at valutation up to $2.1B)

-DKNG +3.2% (acquires Railbird to Advance Future Growth in Prediction Markets)

-WBD +2.9% (acquisition speculation)

-SMMT +2.7% (raises $500M via private placement of 26.7M shares at $18.74/shr)

-TMO +2.4% (earnings)

-GOOGL +2.2% (reportedly Antrophic in talks for Google cloud deal)

-BSX +2.0% (earnings, guidance)

-ARCT -60% (reports ARCT-032 Interim Phase 2 Data for Cystic Fibrosis (CF) Program)

-ALEC -51% (cuts workforce by ~49%, following discontinuation of dementia program)

-ASTS -9.0% (prices Private Offering of $1.0B of Convertible Senior Notes Due 2036)

-TXN -7.7% (earnings, guidance)

-NFLX -7.6% (earnings, guidance)

-MAT -5.7% (earnings, guidance)

-TDY -3.3% (earnings, guidance)

-HPQ -2.8% (JPMorgan Chase and Co Cuts HPQ to Neutral from Overweight, price target: $30)

BY Doug Kass · Oct 22, 2025, 9:20 AM EDT

BY Doug Kass · Oct 22, 2025, 9:05 AM EDT

BY Doug Kass · Oct 22, 2025, 8:55 AM EDT

From Peter Boockvar:

Lower interest rates has yet to really help the residential real estate market as seen with mortgage applications and it hasn’t lifted the commercial side either. The September US Architecture Billings Index fell to 43.3 from 47.2 and thus further below 50. Three of the four categories (commercial/industrial, institutional, mixed practice and multi family) weakened m/o/m. They said “Unfortunately, business conditions remain relatively weak at architecture firms. There was some erosion in project backlogs this past quarter, with the greatest slippage coming from firms with an institutional specialization.”

Speaking of mortgage applications, the MBA just said that purchase applications fell by 5.2% w/o/w, down for a 4th straight week and clear that home buyers are just not yet enticed by lower mortgage rates and that is likely due to the still expensive price of a home and still high rates.

And this is what Pulte Group said yesterday:

“Specifically in today’s market, weaker consumer confidence and stretched affordability are limiting opportunities with first time buyers, while demand has been more resilient within the active adult segment, where we through our Del Webb brand are a recognized leader.”

“In the third quarter, traffic to our communities was higher than last year, although conversion rates fluctuated from week to week. Based on feedback from our sales associates, consumers remain engaged in the home buying process, but they are proceeding with caution given concerns, which I think range from economic weakness and job stability to stretched affordability. I think that is why buyer response to the decrease in interest rates was more muted than we experienced in other periods of recent rate declines”

“We have always said that interest rates are a positive - lower interest rates are a positive for housing demand, but rates don’t operate in a vacuum. There is a clear offset if rates are coming down because the economy is slowing and people are worried about their jobs, I believe that is the scenario we are experiencing right now.“ I bolded for emphasis.

From Texas Instruments and whose stock is down sharply pre market:

“The overall semiconductor market recovery is continuing, though at a slower pace than prior upturns, likely related to the broader macroeconomic dynamics and overall uncertainty. That said, customer inventories remain at low levels, and their inventory depletion appears to be behind us.”

More on the moderate recovery, “I think you have to go back many years to see similar behavior...And if you think about investing, building new factories, putting more CapEx, there is a bit of a wait and see mode with our customers. They’re just hesitant to have clarity on what exactly are the final rules. Should I put my factory in this country or another one? Even in our domain, think about it. The rules are still not finalized in terms of the rates of tariffs, for example. Will they be or not? So I do see this hesitancy at the customer base, and I think mainly on the industrial side.”

On auto in particular, “automotive was kind of sequentially up and down and up and down, but all in a very similar level. The recovery in automotive, at least for TI, the trough was shallow, and now it’s kind of back to where it used to be, so I would not read too much into it. It came in more or less as expected...It grew sequentially across all regions.”

“And the outlier is data center. Data center, again, not a large part of our revenue, but growing more than 50% for TI year-to-date. That’s where we see a strong investment. That’s the only place where we see strong growth, where customers are investing and moving fast.”

From MMM:

The organic sales growth of 3.2% was “the fourth consecutive quarter of positive organic growth across all three business groups against a macro backdrop that is largely unchanged and generally soft.“ I highlight because the rally of 8% yesterday in the stock was focused more on execution.

China was their best market with sales up high single digits “with strength in industrial adhesives, films, and electronic bonding solutions.” The US saw “strength in general industrial, safety, and demand for filters, partially offset by market driven weakness in auto aftermarket and roofing granules.” Europe saw a bounce in “personal safety communication solutions, which more than offset the weakness in auto.”

From Mattel, whose sales fell 7% y/o/y in constant currency and gears up for the holidays:

“This quarter, our US business was again challenged by industry wide shifts in retailer ordering patterns. That said, consumer demand for our products grew in every region, including in the US and gross billings increased in our international business.”

“Retailers are restocking to meet the expected consumer demand ahead of the holiday season. So all of these bodes well for the strong holiday season and also for a good ending of the year.”

From GM and to some of their comments on their supply chains:

“We are also monitoring the supply of certain chips from China. This is an industry issue I know you’re all aware of. While this has the potential to impact production, we have teams working around the clock with our supply chain partners to minimize possible disruptions. The situation is very fluid and we will provide updates throughout the quarter as appropriate.”

They are still committed to their EV business but acknowledge it won’t develop as fast as originally hoped, “we are not surprised to see EV demand soften signficantly and we expect this trend to continue into early 2026, before we see what the natural demand is for EVs.” Elsewhere, “I’m equally confident in our ICE strategy. It is clear that ICE volumes will remain higher for longer.” I’ll add, it is why we are long platinum.

On their overall business, “We continue to demonstrate disciplined incentives, pricing and inventory management, while attaining a 17% US share in the quarter, up 50 bps y/o/y. Our US incentives remain below the industry average for the 10th consecutive quarter.”

On tariffs by the way, it’s still going to cost them about $3.5-$4 billion, though down from their previous estimate of $4-$5 billion. And, “We expect to offset around 35% of this lower gross tariff impact through go-to-market, cost and footprint initiatives.”

On pricing, “Pricing was up modestly y/o/y with model year 2026 incremental pricing being partially offset by a small fleet headwind.”

On the credit quality of their customer within the GM Financial division and in light of the heightened focus on auto lending, “What we’ve seen so far in our portfolio performance is a consumer that’s been pretty resilient. We’ve seen credit performance kind of as we would expect to see given the credit mix on our portfolio, which is predominantly prime.”

“As we’ve said, even in the less than prime space, in the sub-prime space, which is a very, very small part of the portfolio, that performance too has been pretty consistent. Yes, there is some stress for those borrowers, but they continue to be employed. And so performance again, really as expected.”

From Genuine Parts, mainly an auto parts supplier:

“Our end markets remain muted, most notably in Europe...Globally, customers remain cautious and looking for the best value as they make purchasing decisions. Tariffs, trade uncertainties, elevated interest rates, a cautious consumer, and muted industrial spending are familiar challenges.”

From Capital One and whose stock is popping pre market:

They released $753 million of credit allowance in their domestic card business and “The primary drivers of this quarter’s release were continued observed credit favorability in both losses and recoveries, as well as a slight improvement in the forecasted unemployment rate. These factors were partially offset by greater consideration of potential economic downside.”

On the commercial side they released $37 million and “was largely driven by recent favorable credit performance.”

On their consumer, “The US consumer and the overall macroeconomy have been quite resilient so far in 2025. The unemployment rate has ticked up a bit recently but remains quite low by historical standards. Layoffs and new unemployment claims are low and stable. Wages are growing in real terms and debt servicing burdens remain stable and close to pre-pandemic levels. But I do think we’re in a period of elevated economic uncertainty.”

“We’ve seen inflation tick back up. There’s uncertainty related to tariffs. We’ve seen job creation be strikingly slow. Some consumers are feeling pressure from the accumulated effects of price inflation and higher interest rates which have increased the cost of new borrowing in most asset classes. We’re waiting closely as student loan repayments and collections resume. And, of course now we’re in a government shutdown.”

That all said, charge offs fell in the quarter and “Now as we look ahead, our delinquencies remain our best leading indicator of near term credit performance. In Q3, delinquencies moved in line with normal seasonality...So, now in auto our credit has been very strong. And auto losses were 25% lower y/o/y in the third quarter. And those losses are in line with pre-pandemic levels. And auto delinquencies continue to improve. When we compare the auto results with industry numbers, there is a really pretty striking gap there. And I think it is probably more indicative of the choices that we’ve made and some of the technology behind those choices in our auto business.”

On subprime auto, “There’s been a lot of noise in the subprime auto space pointing to rising delinquency rates. Our own performance in subprime auto has remained stable through this time. And again, I think this is a product of choices that we made. We anticipated inflated credit scores, normalizing credit, and declining vehicle values. So, that led us to pull back pretty significantly back in 2022 and 2023. As a result, our front book vintages have remained stable and in line with pre-pandemic levels.”

So bottom line for them on auto, “our stable performance is largely the result of our own adaptive underwriting. So, it’s not really a comment on the performance of subprime across the industry.”

From Coca Cola, a stock we own:

“During the quarter, the operating landscape remained complex. While many consumers remain in overall good shape, certain segments of the population are under pressure due to varying factors. Some factors are transitory, like unseasonable weather. Others may be long lasting, like the cumulative impact of inflationary pressures, uncertain trade dynamics, and an ever changing geopolitical environment. Despite this backdrop, we’ve delivered volume growth. July and August were slow to start, but September ended on a stronger note.”

I’ll wrap up with the September UK inflation stats. Headline CPI rose 3.8% y/o/y, the same pace seen in August but was 2 tenths under the estimate. The core rate gain of 3.5% was also 2 tenths below the forecast. Services inflation remains the main problem, rising by 4.7% y/o/y and why the BoE is under internal dissent on whether to cut rates again.

While still elevated, the lower than expected inflation print drove an 11 bps drop in the 2 yr gilt yield while the 10 yr yield is down by 10 bps. The pound is lower too as a result and helping to lift the FTSE 100 up by .9%. I continue to find the UK stock market one of the cheapest in the world with plenty of opportunities that we own.

BY Doug Kass · Oct 22, 2025, 8:35 AM EDT

From Gary Marcus:

Amateurs might not be replacing teams of coders, after all

Oct 22, 2025

Remember how in October and in March I told you that vibe coding — in the sense of amateurs using large language models to write code to “build products that would have previously required teams of engineers” — would never be remotely reliable? And that such tools were fine for demos but not for complex apps in the real world? And that the code they wrote would be hard to maintain?

Customers are finally figuring that out.

So is the often-enthusiastic investor Chamath Palihapitiya, not known for his skepticism. Yesterday he posted some fascinating data on X, including this chart which shows that vibe coding usage has been declining for months, after an initial steep rise:

For more, click here.

BY Doug Kass · Oct 22, 2025, 8:11 AM EDT

First of all, I am quite curious how both of these things are being ignored. Heck, the subscriber growth at OpenAI might be worse than Netflix (NFLX) ! Also, what is an 82% decline in GPU use amongst friends? Guess none of this matters, because people expect Nvidia's (NVDA) quarter and guidance to be quite good.

1. Alibaba Cloud claiming to cut Nvidia GPU use by 82% via a new pooling system (link)

2. ChatGPT’s mobile app showing slowing download growth and daily engagement. (link)

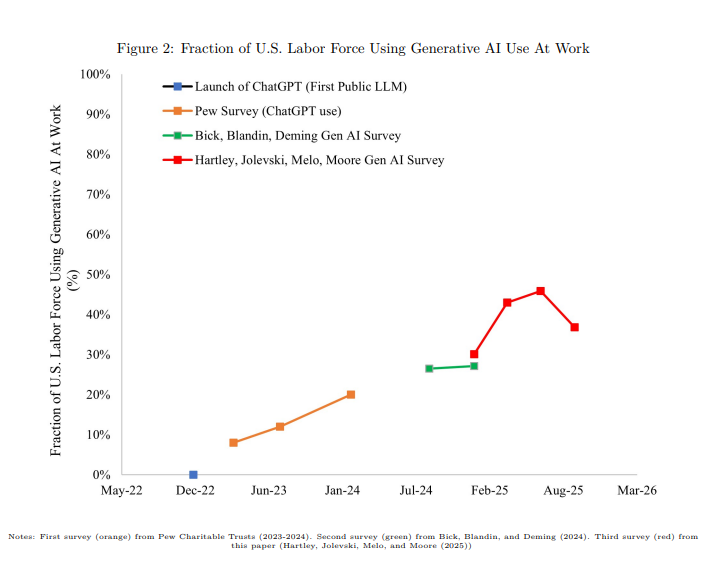

From Torsten Slok at Apollo, I guess one more way AI has been inflationary in addition to the power bills! It probably has something to do with all the AI slop the humans are forced to clean up. I would note, the wage increases in the bolded section are on top of paying for the AI, and the price paid for said AI still results in massive losses for the ecosystem sitting below it. This all defies belief:

The Labor Market Effects of Generative Artificial Intelligence

We find that Generative AI tools like large language models (LLMs) are most commonly used in the labor force by younger individuals, more highly educated individuals, higher income individuals, and those in particular industries such as customer service, marketing and information technology.

We find that LLM adoption among U.S. workers has increased rapidly from 30.1% as of December 2024 to 36.7% as of September 2025, and adoption in the U.S. remains the highest among advanced economies.

We also estimate the effects of Generative AI exposure on several labor market outcomes, finding that more exposed occupations have experienced larger wage increases since the November 2022 public release of ChatGPT while finding no significant effects in job openings or total jobs.

Link: The Labor Market Effects of Generative Artificial Intelligence

BY Doug Kass · Oct 22, 2025, 7:16 AM EDT

* As previously noted, there was universal optimism on gold last week (following the same in bitcoin a month ago)... sic transit gloria

Bonus — Here are some great links:

BY Doug Kass · Oct 22, 2025, 6:35 AM EDT

* Beyond Meat is +$4 or +110% in premarket trading...

BY Doug Kass · Oct 22, 2025, 6:25 AM EDT

BY Doug Kass · Oct 22, 2025, 6:15 AM EDT

BY Doug Kass · Oct 22, 2025, 6:05 AM EDT

Added to Index shorts:

* (SPY) $672.26

* (QQQ) $611.58

BY Doug Kass · Oct 22, 2025, 5:55 AM EDT

The S&P Short Range Oscillator stands at 1.16% vs. -0.15% — that's modestly overbought.

BY Doug Kass · Oct 22, 2025, 5:45 AM EDT