From Peter Boockvar:

After reading the statement from US Trade Rep Jamieson Greer that “China’s recent retaliatory actions against private companies across the globe is part of a broader pattern of economic coercion to influence American politics and control global supply chains by discouraging foreign companies from investing in America’s shipbuilding and other critical industries,” I felt that he doesn’t get it with respect to the relationship with China in the sense that China is responding to many years of feeling slighted by export controls by the US.

As I do subscribe to the South China Morning Post, nothing reflected better the thinking of China than this essay written by Winston Mok, a private investor and I repeat it here. Getting an understanding of the thinking of the other side makes this a must read I believe and hopefully a deal can be had. I bolded the whole thing:

“China’s export control regime on rare earths isn’t retaliation for recent US restrictions - it’s a response to overall US policy. After a video call last Saturday, US Treasury Secretary Scott Bessent and Chinese Vice-Premier He Lifeng are expected to meet in Malaysia this week to hopefully ease tensions before US President Donald Trump and President Xi Jinping potentially meet on the sidelines of this year’s Apec summit. The meeting was in doubt when Trump threatened to impose an additional 100 per cent tariff on China, despite later relenting that it might not be sustainable. Washington blamed Beijing for the escalation, attributing China’s behaviour to its own economic problems. China in turn held the US responsible for the escalation, citing how the US Commerce Department tightened restrictions on affiliated subsidiaries of Chinese companies on the entity list on September 29.

Bessent called China’s coming export controls on rare earths, announced on October 9, a “substantial unprovoked escalation”. The treasury secretary might be one of the smartest people in the Trump administration, but he missed the big picture. China’s latest controls are a response to 10 years of policy, not 10 days of provocations.

To better understand China’s latest move, Bessent must look inward. He could start by reviewing US legislation against China over the past decade or more. To gain a deeper insight, he should learn Chinese history to see how the country’s leaders responded to past adversity and humiliation with strategic patience. China’s restrictions were not authorised in a vacuum. They were the result of rigorous deliberation.

Regardless of whether the 100 per cent tariff threat was a rational response, Trump had at least an intuitive grasp of the situation. Even though the export control measures announced by China are quite complex, Trump understood the gravity of the situation when he saw the share price corrections of Apple and Taiwan Semiconductor Manufacturing Company in the aftermath.

China’s intricate export control framework is not the product of a 10-day scramble after September 29 but rather the result of patient planning. China was waiting for the opportune moment and the US obligingly provided the perfect pretext. To resolve the stand-off, the US negotiation team must understand this: China was not responding to extra provocative measures unveiled by the US. Beijing has been preparing for a strategic counterstrike against cumulative American hostility for more than a decade.

The litany of Washington’s attempts at containing China is long: from restrictions on Huawei to policing the global semiconductor supply chain to shipbuilding and global shipping. From tariffs to an ever-expanding list of tech restrictions, the US has normalised it all. All the while, China was by no means accepting these suppressive measures. It was biding its time, meticulously preparing for the right time to strike. China is not merely responding to the tariffs and restrictions implemented by the US since “Liberation Day”, but a long history of suppressive measures dating back to the Obama administration, expanded by the first Trump administration, escalated by the Biden administration, and culminating in the comprehensive manoeuvres by the White House in the last few months.

China’s “extraordinarily aggressive” position should not mystify the US. It mirrors America’s own playbook. China is merely doing unto the US what the US has been doing to China. You reap what you sow.

Given the asymmetric trading relationship, China cannot effectively respond likes with likes: tariffs for tariffs or port fees for port fees. In one masterstroke, China is responding to all the blows it has endured from the US for more than a decade. The announced regulatory scheme in relation to the rare earth supply chain is not a blunt instrument like a tariff but rather a surgical tool that can be used with nuance and precision. China does not seek to wreak havoc on the world economy by totally restricting the flow of rare earths and products they help produce. Rather, it wants to signal to the US that it wants a reset of their technology and economic relationships.

China is making a statement that the supply chains of the US and China - even at the critical level - are now truly interdependent. The implication is stark: endless escalation is no longer viable, and the US must contemplate dismantling the very tech restrictions it has spent years constructing. As Bessent prepares the ground in Kuala Lumpur, Malaysia, he must transcend the myopic blame narrative and confront an uncomfortable truth: the asymmetric order the US has engineered is collapsing under its own contradictions.

Washington must reckon with its legacy, from Huawei’s suppression to extraterritorial tech controls, and accept that its de-risking strategy has paradoxically amplified global vulnerabilities. The path forward demands that the US shed its self-righteous denial and recognise the fact that containment boomerangs. Trump carries a unique duality as the architect of escalated containment who is pragmatic enough to recognise its failure, hence his recent admission that he doesn’t want to hurt China.

Trump commands the vision, instinct and political capital necessary to forge a historic grand bargain between these intertwined powers. Gyeongju, South Korea - where this year’s Apec summit is due to be held - could witness a Nixon-to-China moment for the ages if Trump and Xi can transcend the containment trap and build a recalibrated framework built on their economies’ inescapable interdependence.”

https://www.scmp.com/opinion/china-opinion/article/3329654/can-scott-bessent-see-chinas-trade-counterstrike-clear-eyes

Now that it is official that Sanae Takaichi is the new Prime Minister of Japan, all eyes are on whether the BoJ will hike rates at the end of October. Two board members already expressed their desire to do so but odds in the Japanese swap market are only about 2% with instead an expected hike in December. We’ll see and we listen to hear what those ‘people familiar with the situation’ leak in the days before the October meeting.

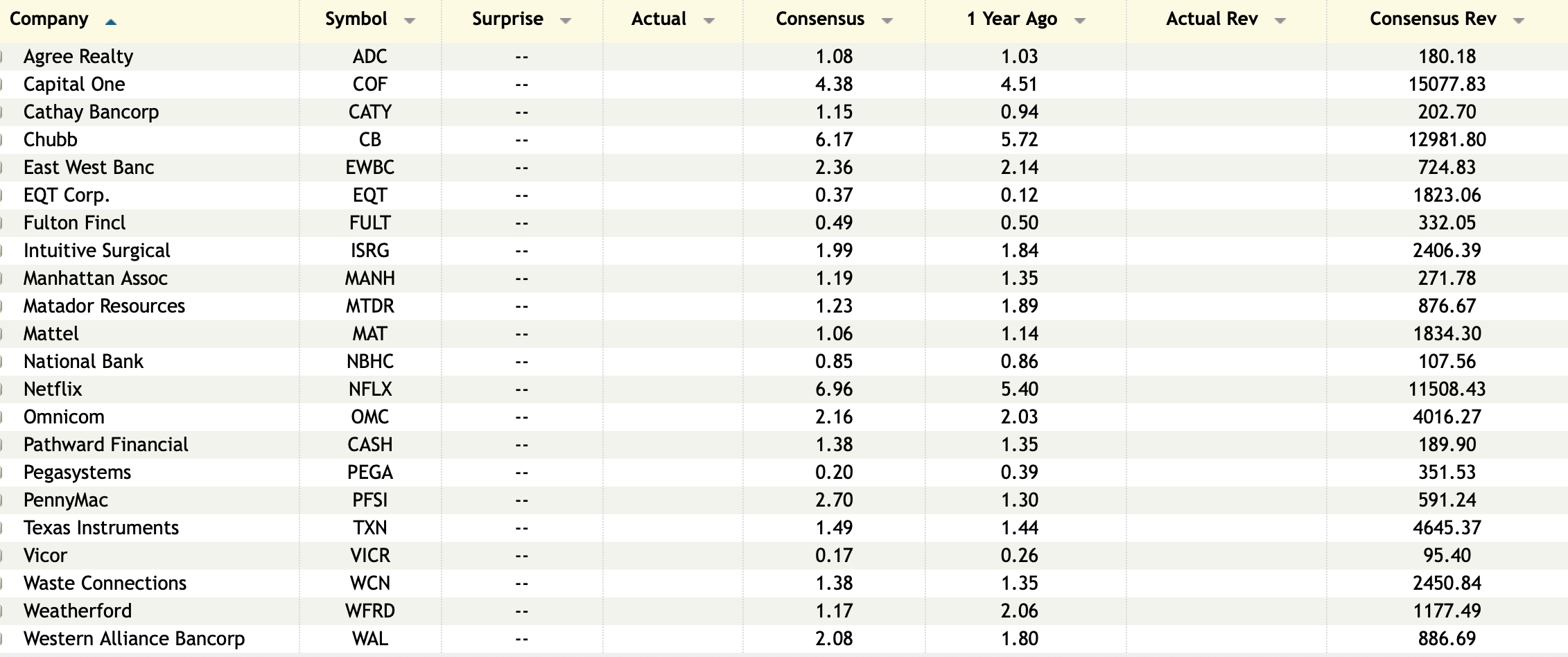

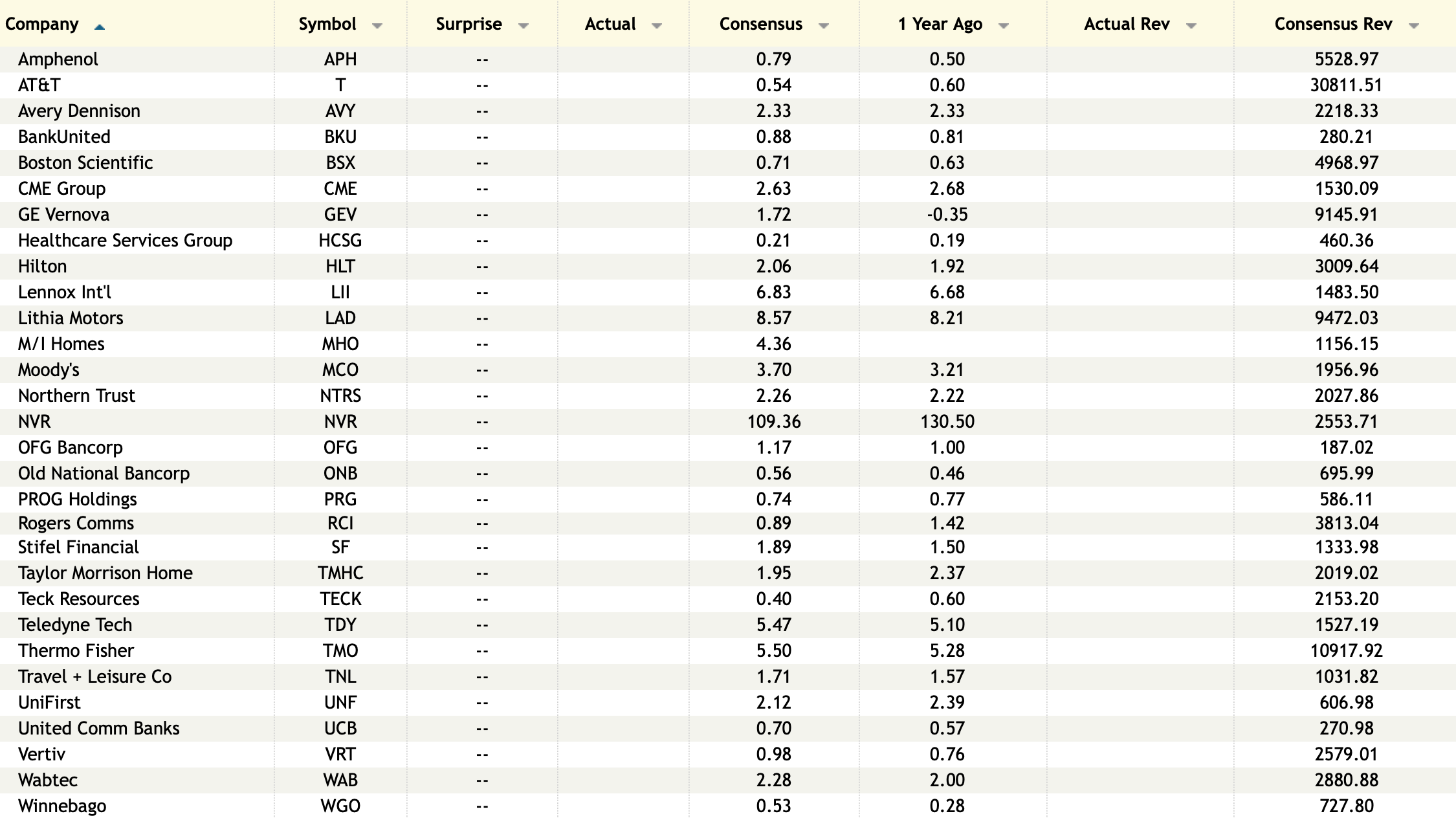

With little economic data out there to analyze, we will dive right into the earnings calls of note.

From Zions Bancorp whose stock is trading up pre-market as they try to quell last week’s credit concerns:

On the credit hit they announced last week, “We view this as an isolated situation resulting from a particular couple of borrowers. We have no further exposure related to these borrowers or guarantors. I would note that excluding the impact of this matter, net charge-offs were minimal at 4 bps annualized on average loans and credit quality generally improved for the quarter as well.”

More on this, “This was a case where we had some unusual things going on that really are not kind of commonplace. And as we noted, we’re going to continue reviewing with an external party to make sure that we’re learning from the experience and seeing what we can continue to improve upon, but I think that our care in extending credit speaks for itself.”

NDFI loans make up just 3% of their total loan book. It seems that the ones with the biggest NDFI loan exposure are the money center banks, not the regionals based on the earnings I’ve gone through.

From Steel Dynamics press release where they slightly beat top and bottom line estimates:

After going thru some highlights of the quarter, “We also achieved record quarterly steel shipments, as imports declined from the elevated levels seen earlier in the year...However, we continue to observe some customer inventory overhang of value-added flat rolled products that were imported earlier this year. We have seen some order hesitancy from flat rolled steel customers due to domestic trade actions, despite numerous encouraging demand drivers - such as manufacturing onshoring, infrastructure program funding, lower interest rates, and the increasing regionalization of supply chains in the US. As it relates to long product steel demand and pricing, structural steel and railroad rail have remained very strong.”

From Cleveland Cliffs whose CEO is very colorful and pro tariffs:

“Our third quarter results were a clear indication there was a significant rebound in domestic steel demand has started and the automotive sector is leading the way. It’s now widely accepted and understood that tariffs are here to stay. Particularly the Section 232 tariffs on steel, autos and derivative products. These tariffs are not a negotiating tool and the only effective way to avoid tariffs is manufacturing in the United States.”

“With all that, third quarter was our best auto steel shipment quarter since the first quarter of 2024...Over the past quarter, Cleveland Cliffs was able to lock in two or three year agreements with all major automotive OEMs, covering higher sales volumes in favorable pricing through 2027 or 2028. These are not small renewals, these agreements represent strategic commitments to domestic steel sourcing by the most relevant auto OEMs. Many of these customers have told us directly that they want to reduce their exposure to tariffs and to foreign volatility. They want stability and resilient supply chains.” I’ll add, yes, agree but it’s going to cost them.

He then panned the use of aluminum in auto manufacturing over the years and in light of the fire at Novelis a few weeks ago that is hampering supply. “The silver lining is that switching back to steel is now under serious consideration by the most affected OEMs.”

I’ll go through the GM call later. MMM is another important one because of its depth of products, customers and geographies. They grew organic sales by 2.6% y/o/y in the quarter and adjusted organic sales by 3.2%.

From Coca Cola, a stock we own:

Going thru the earnings release, it looks like all of their revenue growth was price and mix and not volume. Particularly in North America, price/mix grew 6% “primarily driven by pricing actions in the marketplace and favorable mix.” This while “unit case volume was even, as growth in water, sports, coffee and tea was offset by declines in Trademark Coca-Cola and juice, value added dairy and plant based beverages.”