It appears my boy has two problems: ate something bad off the ground and early cognitive issues (not surprising considering who is father is and that he is sixteen years old).

As discussed in my "More Tales From Nvidia" (Issues #120-#131 over the last week!) there are already some developing cracks in the foundation of AI growth.

After the recent strength in AI-related stocks, any broader market correction could result in an exaggerated (on a percentage basis) move lower in (NVDA) .

Today, might be the start of something... with inner circle/brethren (ORCL) (-$14.60) and (CRWV) (-$8) all lower on the day.

Even NVDA is only +$0.60 in a sea of green.

A conservative way of taking on a NVDA short would be to buy (short term) out-of-the -money calls to define risk.

Interesting what the markets are looking through today. All the data showing OpenAI growth in the U.S. and Europe flatlining, more bad news on the technology (Karpathy comments, etc), more bad news on the economics of the industry (Information article on (MSFT) ), and now this:

But when this is what is going on, this is what happens.

Also I strongly disagree with El-Erian’s hypothesis. I think it is just retail that doesn’t know, doesn’t care, and then professional investors that just get dragged along. His use of the word “investors” is a euphemism for speculators that chase price, and almost anything with the ticker symbol:

I thought Rosie's commentary, Not So Tiny Bubbles, is a worthwhile read:

It is very clear to us that we are in a classic equity bubble, but as Bob Farrell has always posited, these episodes typically go further than you think, but never correct by going sideways. And, typical of human nature, when greed becomes the primal emotion (clearly the case today), everybody thinks they are nimble enough to time the peak. Shades of Chuck Prince circa July 2007.

There is no doubt that we have experienced an inflection point and a major shift in the innovation curve with the AI boom, but over the centuries, investors have generally over-extrapolated what future growth, productivity, and returns on capital would be down the road. We have reached a point where valuations are so extreme that they are pricing in a 15% average annual EPS growth rate for the next half-decade, double the historical norm. Not impossible, but improbable, and at this point, the risk is one of disappointment based on what is already being discounted.

We assess the not-so-magnificent seven factors depicting the U.S. equity market landscape as being in a classic bubble phase. All seven characteristics have checked the proverbial box: valuations, leverage, market positioning, expectations, sentiment, concentration, and over-ownership. I don’t know why anyone should be surprised.

From the steam engine to the cotton gin to the railway to electricity to the transistor to the mainframe computer to the Internet, investment euphoria and asset price bubbles always follow a major shift in the technology curve. With the generative AI boom, things are playing out, as they always have, with investors overestimating (in their Gordon Gekko lust for greed) what the size of the available market is going to ultimately be. I wouldn’t bother trying to time the peak. Just know that there will be a bubble peak, there always is, and the aftermath is horrible. With reference to another investing legend, Jeremy Grantham — he said on my webcast earlier this year that a bubble is defined by a 2 standard deviation event. Well, of these seven market characteristics, I can safely conclude that the mean, median, and mode are pressing against a 2 standard deviation event versus their historical norms. And anyone who knows me and my investing style knows that I will never participate in, let alone chase, a 2-sigma event. This is when you know that the bull market is in extra innings.

Over 70% of the U.S. household asset mix is now concentrated in the equity market. This is around the peak number that presaged the last three recession bear markets of 2001, 2008, and 2020. This is not the cause of a recession, but such radically high exposure causes the bear market to be severe as everyone moves defensively to rebalance the portfolio into the relative safety of cash and bonds.

Vanguard’s numbers were rather shocking: workers in their late 30s had 88% of their 401(k)s concentrated in stocks last year, while — get this — 401(k) investors in their early 60s had boosted their allocations to stocks of an unheard-of 60%. This is about double the exposure these folks should have in their portfolio. In target-date funds, which move money from stocks to bonds as retirement approaches, the average equity allocation (for workers just beginning their careers) was 92% (at the end of 2024). This speaks to an equity culture in which everybody is loaded up on risk all at the same time. Talk about throwing caution to the wind.

The fact that this strategy is working today is a poor excuse not to diversify or rebalance, but in today’s investing environment, that advice is just met with a yawn and a shrug of the shoulders. Managing risk has been thrown into the wastepaper basket, and while not a problem today, I can guarantee it will become a big problem down the road as everyone attempts to time — and exit — the peak. The CAPE multiple has expanded by almost +5 points since May to 39.5x, which exceeds every prior bubble peak in the past century outside of the unprecedented tech mania in the late 1990s and early 2000s. This compares to the 1929 bubble peak of 33x, the Nifty Fifty peak in the late 1960s of 24x, and the 1987 pre-crash peak of 18x. The average bubble peak in this valuation metric is 26x. It is now pressing against 40x. We are in the stratosphere. Historically, when we have seen the CAPE behave this way, the bubble lasted an average of 17 months (as per Bob Farrell, “going further than you think”). The median lifespan was 11 months. Split the difference and call it 14 months in orbit. The CAPE first emerged as a 2 SD bubble event in June 2024 (it is now approaching a 3 SD event), when it was just a tick below 35x, and so the clock is ticking before the pin pricks the balloon.

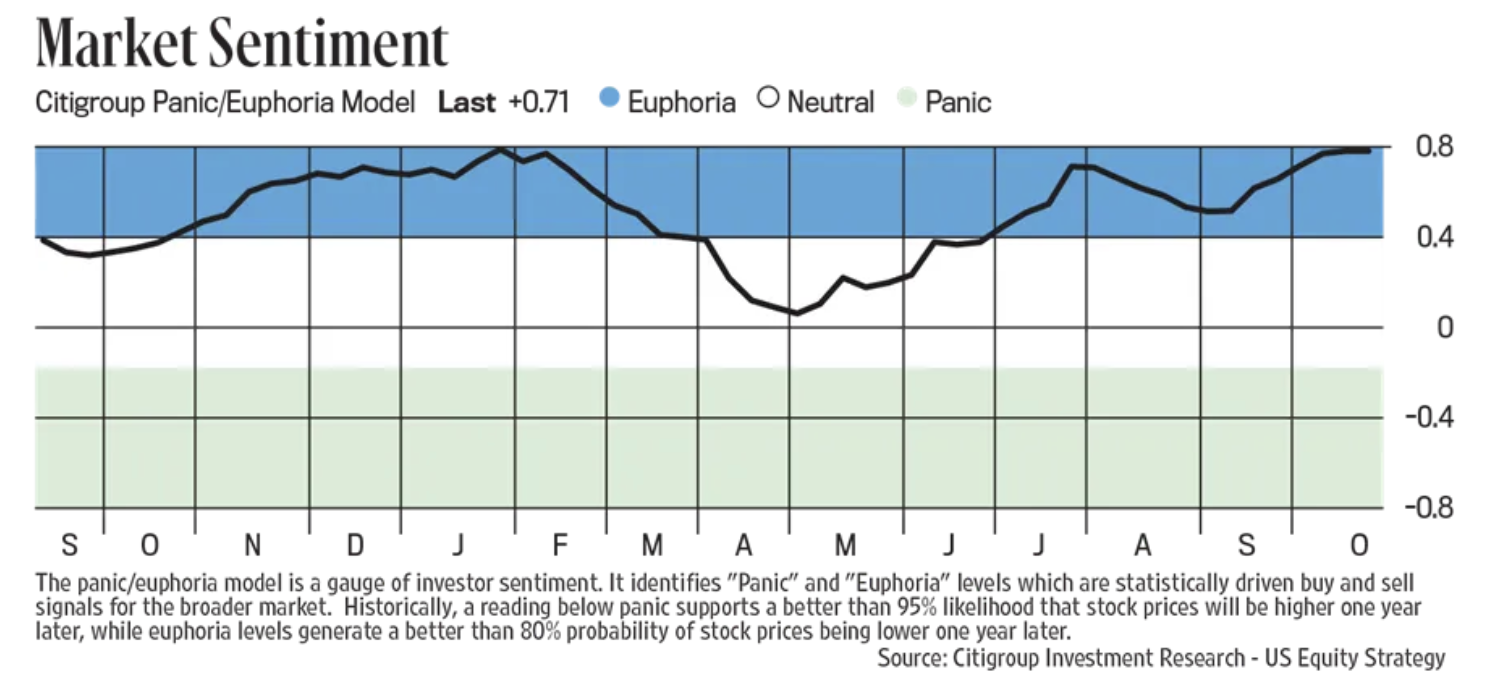

The surge in valuations has coincided with investor sentiment indices soaring off the charts, which happens to be a contrary negative. Herd mentality. The madness of crowds. An overwhelming consensus. A red flag. The Investors Intelligence survey that came out recently showed the bull share at almost four times the bear camp, and the spread is in the danger zone. As we saw in early 2022, this is a harbinger of trouble ahead. The Citi Panic/Euphoria index had also recently risen to the most euphoric level since February, and this presaged the springtime correction. When you are priced for perfection, and are expecting perfection, disappointment always follows because the world is not perfect. The major point here is how extreme things have become.

I have been changing the composition of my cannabis position.

Given my expectation of a mid-November to mid-December rescheduling announcement, I have been exchanging my common position with out-of-the-money call options.

I expect to be entirely out of (MSOS) common and entirely into MSOS calls sometime soon.

They are finally listening to me/Another BoJ member wants a hike/FITB customer 'nauseously optimistic'

I’ve been ranting for six months now that it was nonsensical to tariff items that we can’t or would never make in the US as we’re just taxing ourselves with no production shifts in response. Well, the administration is finally listening to me as the WSJ reported over the weekend that “President Trump in recent weeks has exempted dozens of products from his so-called reciprocal tariffs and offered to carve out hundreds more goods from farm products to airplane parts when countries strike deals with the US.”

“The offer to exempt more products from tariffs reflects a growing sentiment among administration officials that the US should lower levies on goods it doesn’t domestically produce, people familiar with administration planning said. That notion ‘has been emerging over time’ within the administration, said Everett Eisenstat, deputy director of the National Economic Council in Trump’s first term. ‘There is definitely that recognition.’ “

Now we’re finally getting somewhere though this now opens up a whole new can of worms over who can lobby for exemptions and who can’t but we’ll take what we can get right now for those goods we’re just not going to produce here, ever.

De increases are still coming. In case you didn’t see the WSJ article last week, “IKEA’s Yearslong Price-Cutting Bonanza is Coming to an End.” The article said, “IKEA’s low-cost furniture has won it legions of fans around the world. Now President Trump’s tariffs are forcing the company to do something it hates: raise prices.” They quote Tolga Oncu, a retail manager at Ingka, “the company that operates most IKEA stores around the world” who said “Our ambition is to continue lowering prices. But of course in the world we live in sometimes...that becomes very difficult or even impossible at some point. We have to adapt and pass on parts of the cost increase to the customers.” The extent of the company’s exposure, “Only about 15% of what it sells in the US is sourced regionally, mostly from factories in North America.”

Meanwhile, tariff induced price increases are still coming. In case you didn’t see the WSJ article last week, “IKEA’s Yearslong Price-Cutting Bonanza is Coming to an End.” The article said, “IKEA’s low-cost furniture has won it legions of fans around the world. Now President Trump’s tariffs are forcing the company to do something it hates: raise prices.” They quote Tolga Oncu, a retail manager at Ingka, “the company that operates most IKEA stores around the world” who said “Our ambition is to continue lowering prices. But of course in the world we live in sometimes...that becomes very difficult or even impossible at some point. We have to adapt and pass on parts of the cost increase to the customers.” The extent of the company’s exposure, “Only about 15% of what it sells in the US is sourced regionally, mostly from factories in North America.” https://www.wsj.com

I often cite the Citi Panic/Euphoria index as part of my stock market sentiment mosaic and view it each Saturday within Barron’s. This past weekend saw its read at .71 which is well above the Euphoria threshold of .41 and is almost as Euphoric as it got in 2021. Take heed as it says “Historically, a reading below panic supports a better than 95% likelihood that stock prices will be higher one year later, while euphoria levels generate a better than 80% probability of stock prices being lower one year later.”

Citi Panic/Euphoria index

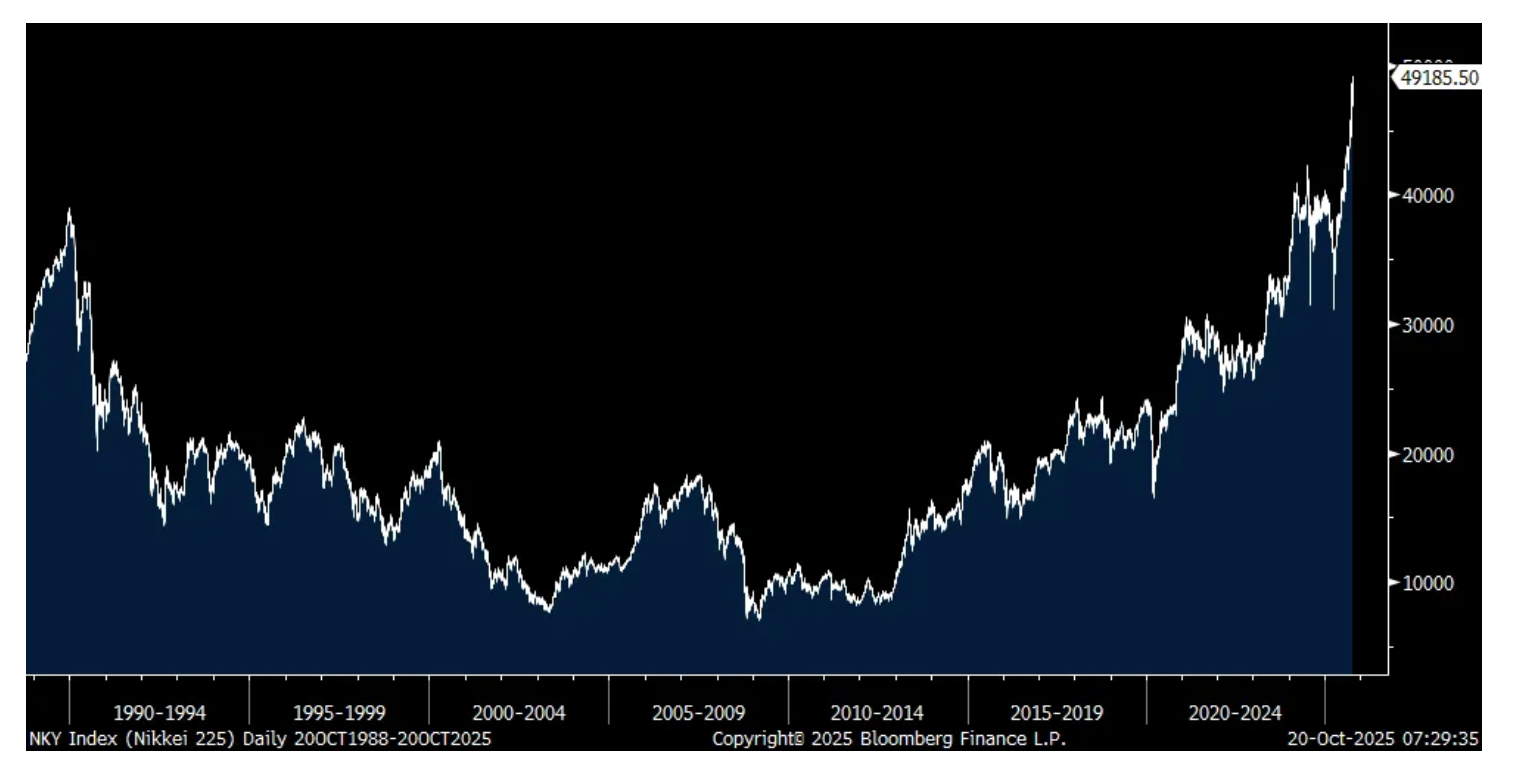

So finally Sanae Takaichi will be the first Japanese female Prime Minister after all after the LDP signed a coalition deal with the Japan Innovation Party. Combine this with another BoJ member who said it’s time to raise rates again and Japanese yields jumped across most of its curve and rose as well throughout Asia. That BoJ member Hajime Takata said “I believe that now is a prime opportunity to raise the policy interest rate. The once deeply entrenched norm has waned in Japan, that the price stability target has been almost achieved.” This follows Naoki Tamura who echoed a similar line of thinking last week.

The 2 yr yield rose 4 bps to .953% and the 10 yr by a like amount. The 30s and 40s were little changed as they want rate hikes to cool inflation. The Nikkei jumped 3.4% to a fresh record high on the coalition news but the yen is down slightly. We remain bullish and long Japanese stocks.

Nikkei

Yields in France are 2 bps higher after S&P downgraded their credit rating to A+ from AA-. They said, “Despite this week’s submission of the 2026 draft budget to the parliament, uncertainty on France’s government finances remains elevated. While, in our view, the 2025 general government budget deficit target of 5.4% of GDP will be met, we believe that, in the absence of significant additional budget deficit reducing measures, the budgetary consolidation over our forecast horizon will be slower than previously expected.”

To some earnings calls where credit quality for the upper end remains solid and regional banks are still seeing pretty good trends right now notwithstanding the growing set of worries.

From AmEx:

“Card member spending in the quarter accelerated to 9% or 8% on an FX adjusted basis, with particularly strong retail spending and a bounce back in travel, and our credit performance continues to be excellent...with both US consumer and small business delinquency rates still below 2019 levels.”

“This performance is supported by our focus on premium products, which tend to attract high income, highly credit worthy customers.”

“Airline spending picked up this quarter. In restaurant, our largest T&E category continued to be very strong, up 9%. Premium T&E bookings saw good momentum with spending on front of cabin airline tickets up 14%.”

“The momentum we’ve seen from younger customers also continued. Millennials and Gen-Z now account for 36% of total spend, making up the same share as Gen-X.” I’ll add, this cohort really only knows cashless payments.

“International had another strong quarter.”

Overall on its customer base, “we’re still in a relatively stable environment. I would also point out, as I always point out, our card base is not representative of what’s going on across the United States. It truly is a bifurcated economy. We have a small percentage of the cards, but our card holders are much more premium and we’re lucky to have a much more premium card base. So we’re seeing a little bit of a pickup in spend. We hope that continues into the fourth quarter. I think what was encouraging for us is also the pick up in small business. We saw 4% growth, the pick up in large and global as well, which was up at about 6%.”

From Fifth Third Bank:

“We once again saw growth in nearly every major consumer lending category, led by continued strength in auto and home equity lending.”

Notwithstanding the credit hit they took due to Tricolor, “Broad-based credit trends remain stable across industries and geographies.”

“The broad consumer portfolio remains healthy, with non-accrual and over 90 day delinquency rates stable and improving across loan categories.”

As to their NDFI exposure, it’s “8% of the total portfolio” and they did go through a more detailed analysis of this portfolio. “Our disciplined underwriting framework is designed to safeguard portfolio quality by avoiding aggressive advance rates, which we see in the marketplace sometimes, overly concentrated collateral pools, inexperienced management teams and structures that do not meet our overall risk appetite.” On this point, you can be sure others are not as disciplined.

On the state of their business customers, “So I got to visit about three dozen of our commercial clients. And the quote of the quarter went to the client who referred to the outlook as ‘nauseously optimistic.’ The tariff uncertainty absolutely continues to weigh on any clients that are exposed. That said, I would tell you, in general, people are more optimistic than they were in the second quarter. In part, because when you add up all of the different tariffs, there is some uniformity across most of the countries that provide significant sources of the supply chains for folks in materials and manufacturing and construction and the other sectors that are big in our footprint.”

“The question mark really has been who would bear the brunt of the tariffs? And I would say now, on balance, is a sort of a shared pain approach here where the supplier, the intermediary, and the customer are each absorbing about 1/3 of the increased cost, but the supplier and the intermediaries have also been clear whenever we talk to them that their intent is ultimately to get back to prior margins, which would mean over time you would see continued price increases as a mechanism to move cost through.”

And where is their customer base seeing the most strength? “The folks that are having the most robust demand obviously are the people who are either attached to the big government infrastructure investments, things like bridges and roads that are moving forward, or the folks that are attached to AI, and there’s so much demand there because with one of our clients that’s in the concrete business, they not only have a strong order book, but the suppliers are driving the pricing as opposed to the buyers driving the pricing.”

From Ally Financial:

“credit trends across our portfolios remain encouraging. The consolidated net charge-off rate was 118 bps, a decline of 32 bps to the prior year.”

Their 30 day plus all in delinquency of 4.9% is “down 30 bps from the prior year and marks the second consecutive quarter of improvement y/o/y. This continued improvement further reinforces our constructive view of the near term loss trajectory within our portfolio, but we continue to assess the dynamic macro environment.”

With their auto finance business specifically, “Prime credit remained the majority of our originations in the quarter, with average FICO of 708. FICO scores below 620 represented roughly 10% of volume, while sub 540 volume was only 2%, both consistent with historical trends.”

The bigger picture trends of markets and economies using more and more leverage are quite clear:

* Leverage in increasingly crowded passive investing products and strategies (markets are not elastic enough to take in the rising inflows - this serves to lower the point in which quants may become a destabilizing market influence)

* Nearly 70% of daily option trading has an expiration of one day

* Leverage in structured products

* Leverage in non-deposit financial institutions, private equity and crypto currencies

* Leverage underlying the AI cap spending cycle

* Leverage at the municipal and Federal government levels (with annual federal debt service payments now topping annual U.S. defense outlays)

Some lack concern regarding a worrisome credit cycle and/or a systemic trend -- like my pal, the lynx-eyed Dan Greenhaus. Dan writes that "the recent credit market flare-ups are best viewed as a series of one-offs rather than evidence of a broader systemic issue:

A Cause for Concern: The Unexpected and Leveraged Corners of Speculation

* The entirety of the recent four-week market advance has been based on an expansion in price earnings multiples.

* As narratives multiply and fear/doubt disappear, guards and disciplines are dropped with many asset classes at all-time highs.

* But as asset prices rise, diligence and the assessment of reward vs. risk should take on greater irrelevance - unfortunately just the opposite is occurring.

* And so should the concept of "a margin of safety" be evermore embraced - as it is an essential and integral ingredient to investing over a "market cycle."

* As the late but great Sir Arthur Cashin would often write - in the current euphoria - one should pay strict heed to Bob Farrell's "Lessons of Investing."

* Expect the unexpected...in the corners of leverage and those that are endorsing the narrative of a "new paradigm" (of higher valuations).

"What the wise man does in the beginning, the fool does in the end."

- Warren Buffett

"A bull market is like sex, it feels best just before it ends."

- Barton Biggs

Over history, market inflection points and economic dislocations often come from places not anticipated. Indeed, the most important turning points in markets (and in life) often come at the most unexpected times and in the most unexpected ways. In particular, leverage, as proven by history, is often uncovered in unexpected places. Think about the collapse of a generally unknown currency, the Thai Bhat that gripped Asia in 1997 and then spread to other countries (with a ripple effect), raising fears of a financial contagion and a worldwide economic meltdown. Or the failure of the highly leveraged (and formerly successful) Long Term Capital hedge fund (managed by several Nobel Prize winners in economics) in the following year -- which was, in part precipitated by the Russian Debt crisis in 1998 and required a multi billion dollar bailout by 14 banks (orchestrated by The New York Federal Reserve). But the best example of hidden leverage (where no one was looking) was seen in The Great Financial Crisis of 2007-09 when one overleveraged segment, real estate, proved to be the Achilles Heel for the global economy.

Indeed, what started out as what many believed to be only a few California mortgages under water, multiplied geometrically and almost bankrupted our worldwide financial system -- as the layers of leverage were swiftly uncovered and spread rapidly. This morning's market commentary will highlight several significant market (and economic) risks that are not regularly discussed.

The "failure" or combustion of any of these factors could have a most adverse impact on equities and on the domestic economy.

* The U.S. economy has never been more levered to the U.S. stock market. Indeed, one can argue that -- with household ownership of equities at an all-time high, with a chorus of "its different this time" and with dreams of a new investing paradigm (of higher valuations) dominating the narrative. As discussed below, it is almost as if the domestic economy is being collateralized by a foundation asset, equities.

From Tom Dyson:

The US stock market is such a foundational asset. You could say, the US stock market has become the collateral that backs the world economy, and all its debt. As long as the stock market keeps rising, everything’ll be okay. But as soon as it turns down, things will start breaking. Employment, real estate values, consumption, trade… and even the government’s finances. It’s the wealth effect, when the stock market is such an important store of wealth. They all rely on a strong stock market to function. The fact that the world’s prosperity has one single point of failure – even as it rises day after day – should terrify you. The market’s function should be to allocate scarce capital efficiently… not collateralise the entire system. In effect, it’s become too big to fail, which is an acute fragility for our capitalist system. As allocators of capital ourselves, how should we approach our investment discipline in a market where expectations (and stock market values) are literally “off the charts”? The bears say "every other time this has happened, there's been a big wreck." The bulls say "this time is different, and besides, the trend is your friend and getting the timing wrong is the same as being wrong."What do you do? Neither position is falsifiable. Which means there is no way to figure out the correct answer with logic… or research… or data. So it comes down to philosophy. Are you a contrarian? Or are you a trend-follower?... The global debt stock surged by over $12 trillion in the first three quarters of 2024 to a record high of nearly $323 trillion. It’s a huge wealth bubble and when it pops, $400 trillion or $500 trillion of (mostly) paper claims ($323 trillion in debt plus whatever owners’ equity the system has) will rush for the exits and seek safety. And policy makers won’t be able to stop it.

* Elon Musk's health and business/innovative successes are critical to a continuation of economic growth and stock market gains. Musk's broad reach -- on the road, under ground, in space, over the internet, in defense, in artificial intelligence -- has now advanced into Washington, and in the formulation and implementation of policy. To have one person so immersed and involved in all these critical areas could pose broad risks -- in many ways.

* An extremely leveraged cryptocurrency market represents potential systemic risks. It is my view that cryptocurrency is "the mother of all bubbles" perpetuated by a number of factors (including the rejection of fiat money) and developing digital narratives -- many of which have a weak foundation of logic. The absurd notion that the limiting of supply of bitcoin is as stupid as it is damning -- as there is no limit to the supply of other cryptocurrencies. To this observer, the sheet market size of bitcoin and other cryptocurrencies is a manifestation of the risks.

And, as I have written, MicroStratetgy (MSTR) (with its "math" in expressing the case of buying $1 bills for $3 and MSTR's multiple derivative plays), is the standard bearer of the digital speculation today. See: TheStreet Pro

When the cryptocurrency markets implodes, which is my baseline expectation, the contagion effect will likely be pronounced on all of the capital markets.

* Both fiscal and monetary policy - which is needed to secure the foundation of growth -- are travesties. Neither political party has been fiscally responsible -- the profligate spending over the last few decades continues apace. (I do not, in any way, buy Elon Musk's objective of cutting $2 trillion from the U.S. budget, as when you go over the numbers only about $1.5 trillion can be cut (and that is if one cut all that was "available" to be cut in total). As well, the Federal Reserve has been guilty of reckless, feckless and fatuous policy in its delayed response to inflation and, then, in effecting a rapid rise in interest rates. I have little confidence in Powell's Fed steering clear of debris in his remaining time at that institution. Nor am I confident in any Fed chairman that might replace him.

* Changing market structure poses a significant market risk. Passive investing has engulfed the stock market landscape. We are all traders now, on the same side of the boat and worshipping at the altar of price momentum. (See the first bullet point!) Massive inflows into passive strategies and products have been the straw that has stirred the market's drink:

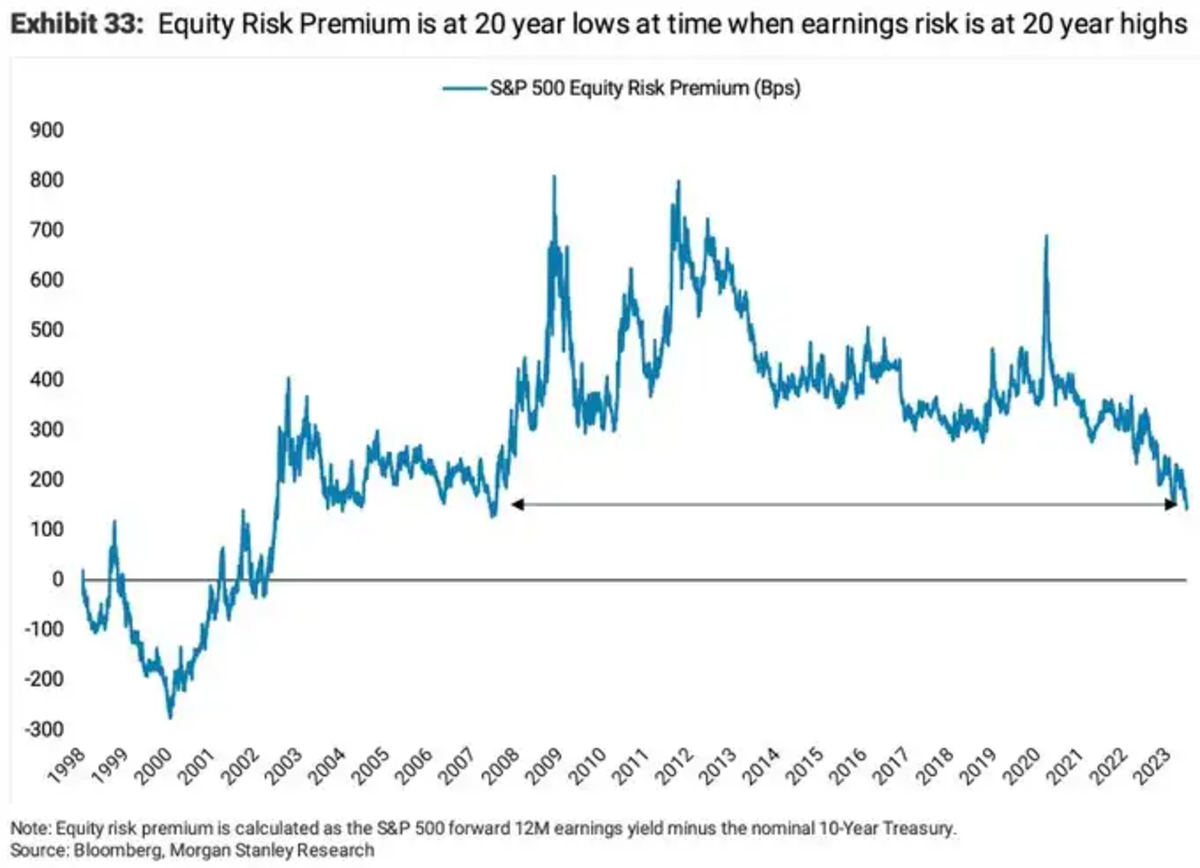

In part, those inflows, have contributed to a near unprecedented narrowing in the equity risk premium (to 20-year lows) while the risk to earnings growth are at 20-year highs:

I can guarantee you (and history has proven) that these inflows - as well as FOMO and the animal spirits - will not be permanent conditions.

Bottom Line

"We must stop regarding unpleasant or unexpected things as interruptions of real life. The truth is that interruptions are real life."- C.S. Lewis

The history of speculation is that it resides in areas that are rationalized (with broadening acceptance of a new paradigm).

It is also the condition of history that it is fueled by leverage and lasts longer than most expect. But excesses are never permanent. They become ever more dangerous when markets are consumed with optimism, are no longer fearful and are levered up.

11 a.m.: Federal Reserve Board of Governors Closed Board meeting. Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks.

Treasury Auction:

11:30 a.m.: Treasury hosts a $86B 3 and $77B 6-Month Bill Auction

Economic Calendar originally scheduled for the Week:

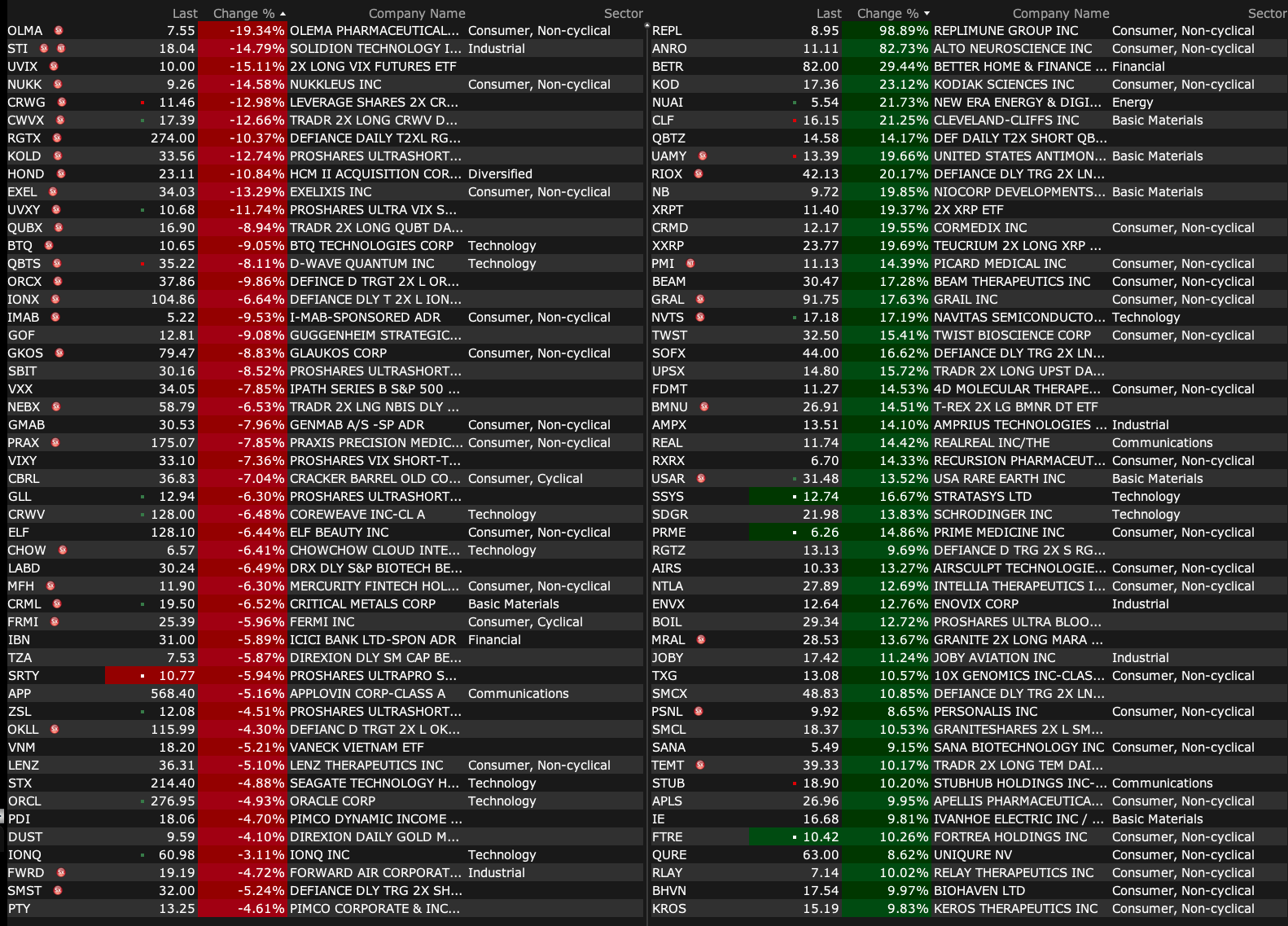

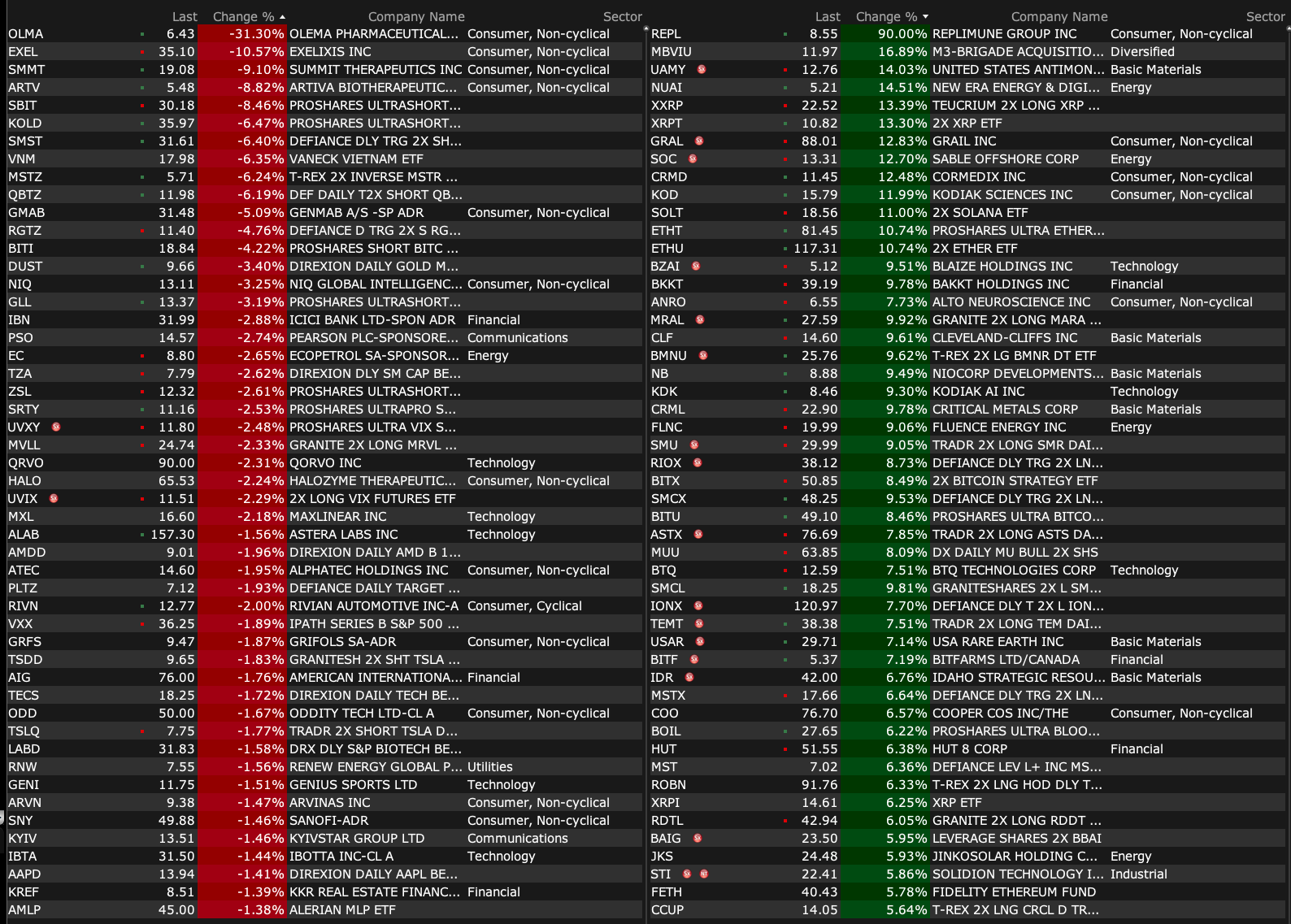

-REPL +90% (US FDA accepts BLA Resubmission of RP1 for Treatment of Advanced Melanoma)

-BYND +56% (sets date for Special Meeting for proposals related to Exchange Offer)

-RAPT +52% (announces with Shanghai Jeyou Pharmaceutical Positive Topline Data from Phase 2 Trial of RPT904 (JYB1904) in Chronic Spontaneous Urticaria)

-CELC +51% (detailed Results from PIK3CA Wild-Type Cohort of Phase 3 VIKTORIA-1 Trial Presented at 2025 ESMO Congress Demonstrate Potential for Gedatolisib Regimens to be Practice Changing for Patients with HR+/HER2- Advanced Breast Cancer)

-DVLT +17% (partners with Max International to launch Swiss Digital RWA Exchange)

-COGT +13% (US FDA grants Breakthrough Therapy Designation for Bezuclastinib)

-SOC +13% (Holder Pilgrim Global ICAV discloses purchase of 980K shares, raising stake to 10.9M shares)

-CRMD +12% (earnings, guidance)

-WW +8.9% (collaborates with Amazon Pharmacy)

-CLF +8.5% (earnings, guidance)

-ODYS +8.0% (announces successful technology demonstration on AW139 Leonardo helicopter operated by Italian Air Force flight test unit)

-USAR +7.1% (William Blair Initiates USAR with Outperform)

-ACHR +6.8% (Korean Air Selects Archer as its Exclusive Partner to Introduce eVTOL Aircraft in Korea; Includes the potential for Korean Air to purchase up to 100 Midnight aircraft, to be deployed across multiple use cases)

-COO +6.7% (Jana Partners acquires stake)

-SNDK +5.2% (momentum)

-HOLX +4.8% (reportedly Blackstone and TPG are in late stage talks to acquire Hologic; Price talks said to be over $75/shr, a more than $17B enterprise value)

-NCNO +4.4% (Raymond James Raised NCNO to Strong Buy from Outperform, price target: $36)

-MU +4.0% (Barclays raises price target)

-ADGM +3.4% (closes financing of $19M upfront)

-LBRT +3.1% (hearing Piper raises price target)

-MP +3.1% (higher in sympathy with CLF)

Downside:

-OLMA -30% (announces New Data from the Phase 1b/2 Trial of Palazestrant Plus Ribociclib in ER+/HER2- Metastatic Breast Cancer at ESMO 2025)

-HSDT -18% (files prospectus registering shares for resale)

-EXEL -10% (reports data from STELLAR-303 trial)

-SMMT -9.5% (earnings)

-SWKS -2.6% (Mizuho Securities Cuts SWKS to Underperform from Neutral, price target: $60 from $70)

-QRVO -2.3% (Mizuho Securities Cuts QRVO to Underperform from Neutral, price target: $75 from $87)

-RIVN -2.0% (Mizuho Securities Cuts RIVN to Underperform from Neutral, price target: $10 from $14)

Per above from a U.S.-based enterprise IT demand tracking service:

Latest survey points to major slowdown in AI demand growth from corporate buyers (and tech spending intentions the lowest in almost 3 years). Still positive but rate slowed quite a bit.