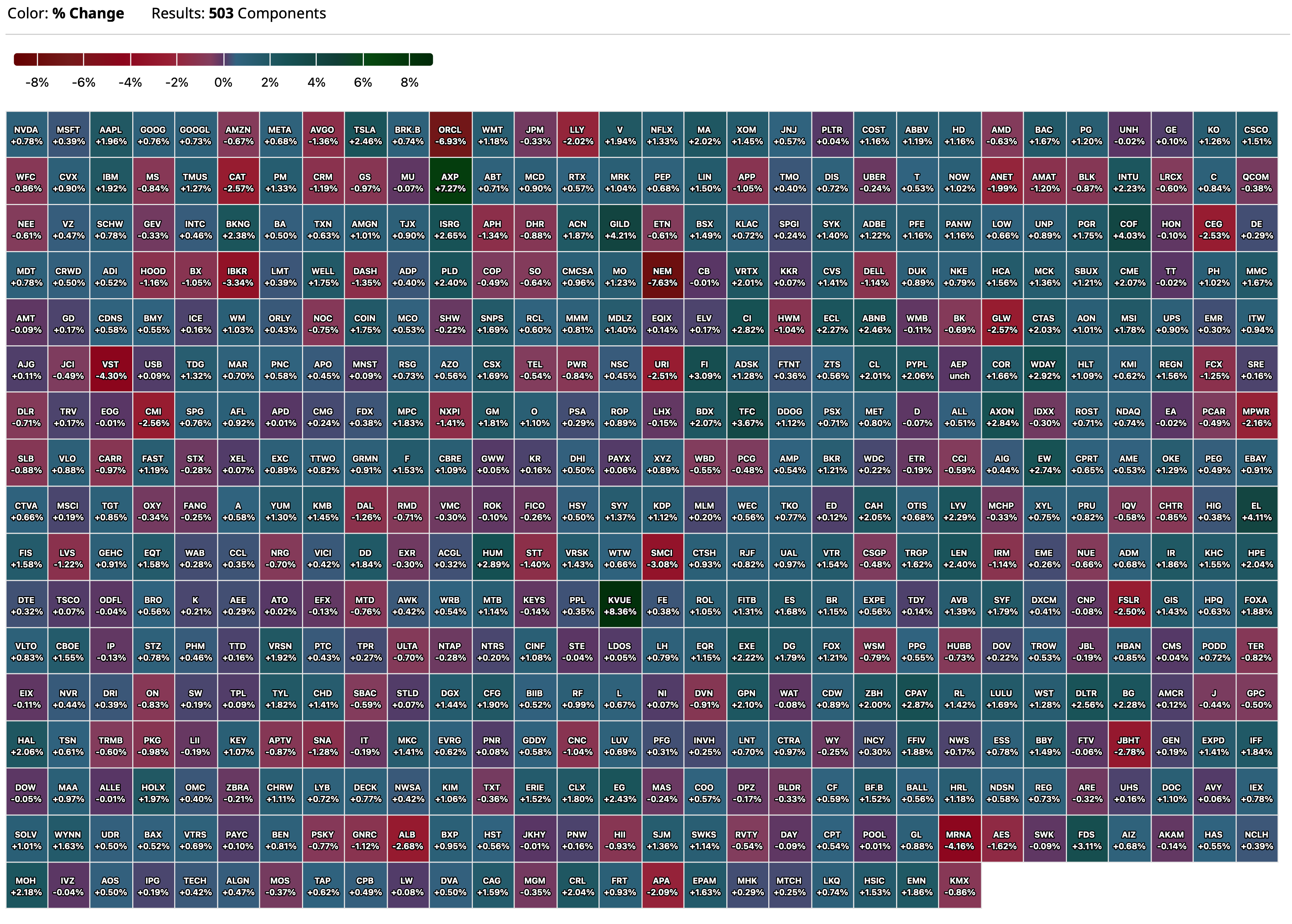

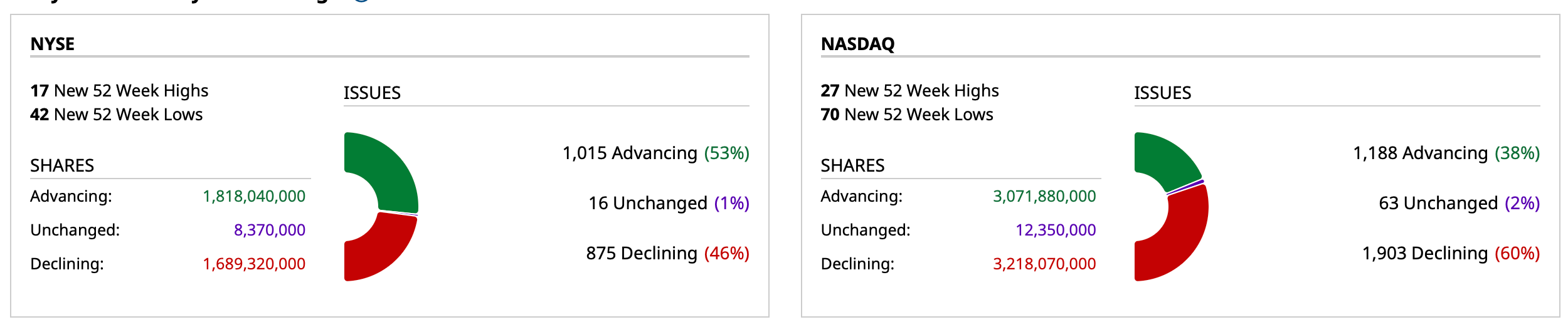

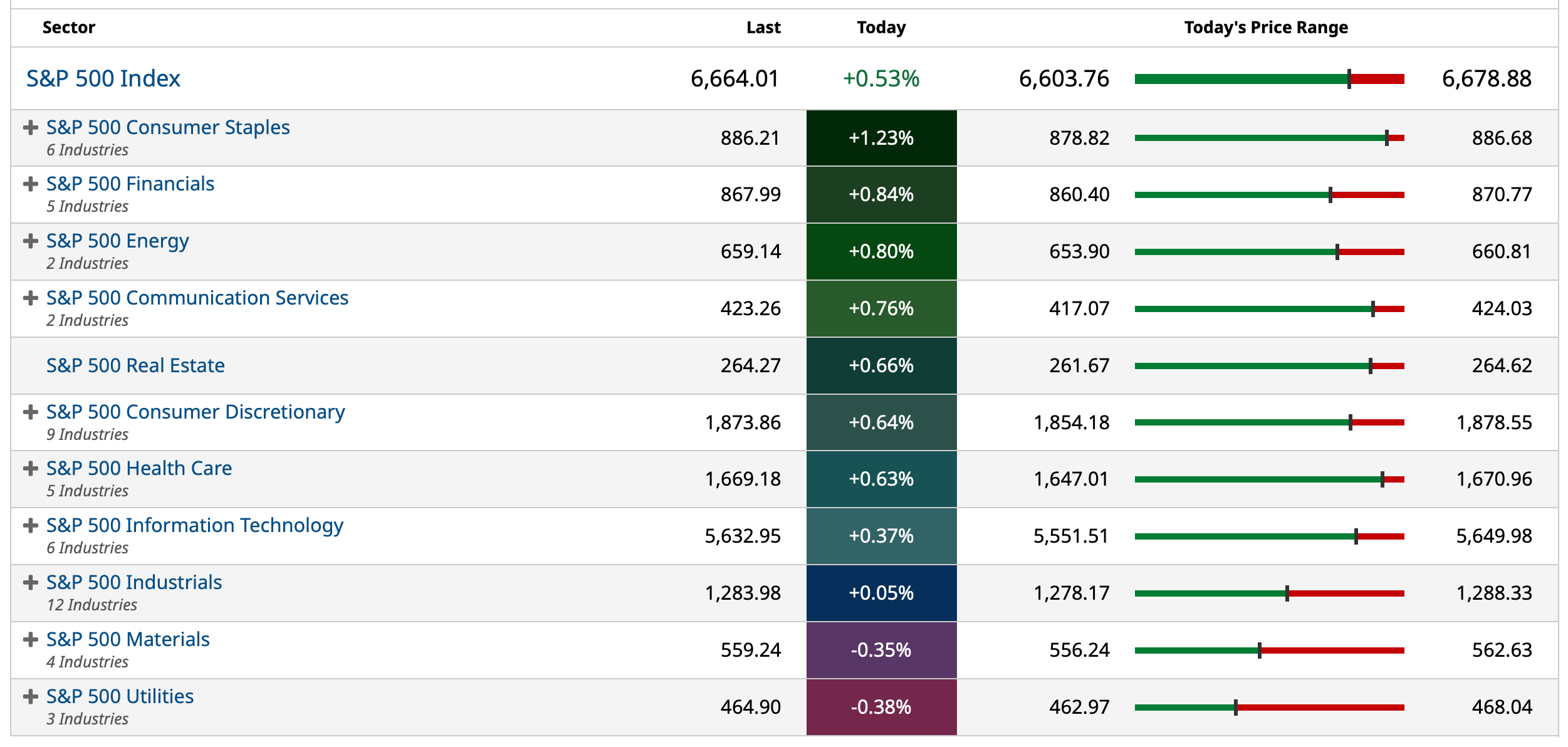

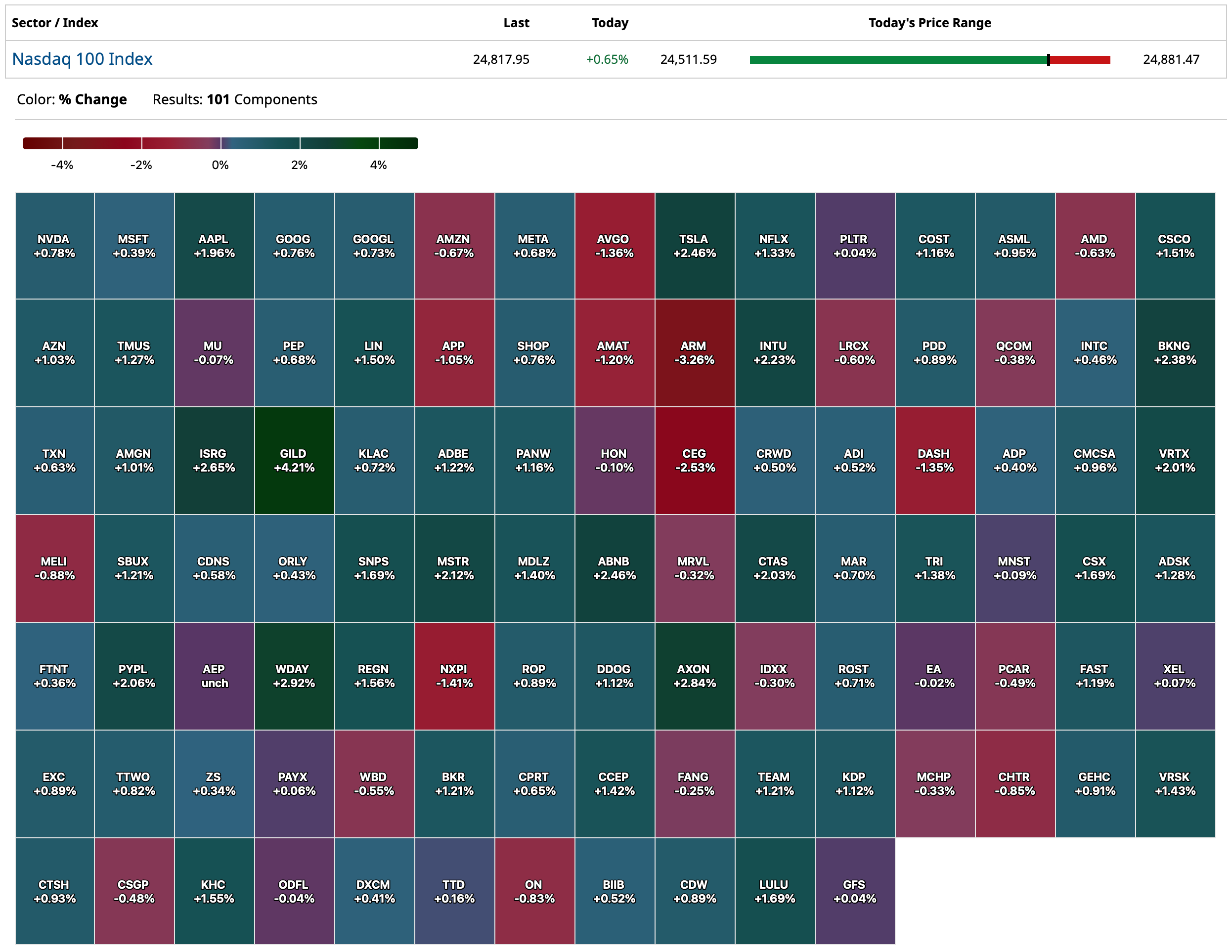

Closing S&P 500 Heat Map

BY Doug Kass · Oct 17, 2025, 4:40 PM EDT

BY Doug Kass · Oct 17, 2025, 4:40 PM EDT

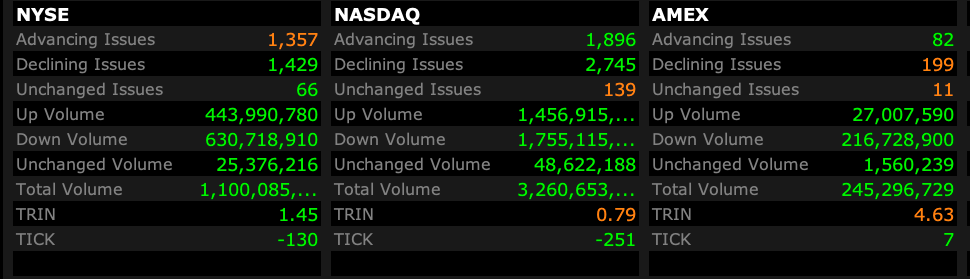

- NYSE volume 2% below its one-month average

- NASDAQ volume 6% below its one-month average

- VIX index -16.87% to 21.04

BY Doug Kass · Oct 17, 2025, 4:30 PM EDT

With about sixty minutes to go in the trading day I am going to take an early exit.

Thanks so much for reading my Diary today — I hope my output was useful.

Enjoy your evening.

Be safe.

BY Doug Kass · Oct 17, 2025, 3:04 PM EDT

Scott Galloway's "No Mercy, No Malice"...

BY Doug Kass · Oct 17, 2025, 2:25 PM EDT

President Trump just stated "it looks like the visit with China will move ahead."

S&P cash vaulted to +25 higher.

I have moved to medium sized:

* (SPY) $663.01

* (QQQ) $603.11

BY Doug Kass · Oct 17, 2025, 2:04 PM EDT

* Today I have been occupied with trading the indices (from the short side)...

With S&P cash +15 handles I am back shorting the Indices:

* (SPY) $662.36

* (QQQ) $601.91

BY Doug Kass · Oct 17, 2025, 1:48 PM EDT

Back from a lunch with friends.

Getting my sea legs back.

BY Doug Kass · Oct 17, 2025, 1:22 PM EDT

I am pretty quick on my feet from a trading perspective.

However, this volatility is tough even for me so I am sizing my Index trading short rentals appropriately.

While I am quite bearish currently, my sizing is much smaller than typical for me.

As the expression goes...

"There are old traders. There are bold traders. But there are few old and bold traders."

BY Doug Kass · Oct 17, 2025, 11:58 AM EDT

BY Doug Kass · Oct 17, 2025, 11:20 AM EDT

With S&P cash -14 handles I am covering my short Index rentals for a swift (in under 30 minutes) and nice profit:

* (SPY) $659.70

* (QQQ) $598.65

From earlier:

With S&P cash +26 handles I am moving to medium-sized short the Indices;

* (SPY) $663.62

* (QQQ) $603.16

Position: Short SPY M QQQ M

By Doug Kass Oct 17, 2025 10:29 AM EDT

BY Doug Kass · Oct 17, 2025, 11:06 AM EDT

From Peter Boockvar:

As I’ve stated my bullish call on gold, silver, and miners many times and for years now, and beginning a year ago on platinum, I do want to express with full disclosure that we did trim a touch of our holdings on gold and the miners into this vertical rise, though not on silver nor platinum yet. While I anticipate a pullback at any moment, possibly beginning today in this complex, I still believe the ultimate highs of this bull run are ahead of us but acknowledge when excitement gets to a very giddy level, it’s time to call a time out and for portfolio management reasons, take some chips off.

BY Doug Kass · Oct 17, 2025, 11:00 AM EDT

This should be good for a trillion dollar valuation on their next raise from NVDA:

BY Doug Kass · Oct 17, 2025, 10:50 AM EDT

With S&P cash +26 handles I am moving to medium-sized short the Indices;

* (SPY) $663.62

* (QQQ) $603.16

BY Doug Kass · Oct 17, 2025, 10:29 AM EDT

With S&P cash +7 handles I am back reshorting the indexes:

* (SPY) $661.45

* (QQQ) $601.07

BY Doug Kass · Oct 17, 2025, 10:12 AM EDT

From Peter Boockvar:

Rising SOFR rates, now about 19 bps above the fed funds rate and increased usage of the Fed’s standing repo facility helps to explain why Jay Powell this week said they are just about done ending QT.

Jamie Dimon was right about cockroaches not because he knows specifically about seeing more but it’s inevitable that when too much money chases too few good lending opportunities, there will be bad loans given. Expect much more loan losses as a result and this will separate the good underwriters from the bad too. I said in the early part of this year that if only I had a dollar for every private credit deal offering I was shown.

And whether this spreads or not, you can be sure that every credit manager, loan officer and investor are scouring all of their loans to see where the next cockroach is and assume too that this will be reflected in credit standards moving forward from here, aka, they should tighten.

Speaking of regional banks, along with what’s been seen with the money center banks, earnings seem to still be pretty good with credit metrics steady, for now but with pockets of rising consumer delinquencies in auto that we’ve seen.

Keycorp said this on their call:

“Asset quality metrics continue to trend in a positive direction with NPAs and criticized loans declining, while net charge-offs were relatively stable. Our net charge-off ratio year-to-date is squarely within our full year target range of 40 bps to 45 bps.”

“As it pertains to the two recent bankruptcies making headlines in the auto industry, we have no direct exposure.”

“Average loans increased by $.5 billion sequentially, reflecting a 2% increase in C&I loans and a modest increase in CRE loans, partially offset by planned runoff of about $600 million of low yielding consumer loans.” On the C&I loan growth, “Most of the growth came from the power and utility sector and in middle market broadly across sectors and regions.”

From US Bancorp:

“As expected, nearly all key credit quality metrics, including non-performing assets and net charge-offs improved both sequentially and on a y/o/y basis.”

As to their exposure to the non-depository financial institution space, aka private credit, it totals 12% of their loan book and “this is a highly diversified portfolio with a balanced and broad composition of borrowers that is underpinned by our proven underwriting capabilities and strong collateral and structural protections.”

American Express just reported and said this:

They said the 11% revenue growth y/o/y “was primarily driven by increased Card Member spending, higher net interest income supported by growth in revolving loan balances, and continued strong card fee growth.” Card member spend specifically rose 8% y/o/y.

“Consolidated provisions for credit losses were $1.3 billion, compared with $1.4 billion a year ago. The decrease reflected a lower reserve build compared to prior year, partially offset by higher net write-offs. The third quarter net write-off rate was 1.9%, flat y/o/y.”

With banks again dominating the conversation and market action yesterday, lost was the 6.5% drop in Manpower, the staffing company, and this is what they said on their earnings call on the labor market:

“When we last reported earnings in July, we characterized the environment as one of continued uncertainty yet growing resilience, with employers hiring very cautiously and labor markets holding steady against the backdrop of geopolitical complexity and economic softening. Since then, these dynamics have largely persisted, and geopolitical tensions remain elevated, the race to invest in AI continues at pace, and employers are adapting to the fluctuating environment and cautious consumer sentiment in Europe and North America.”

“Globally, conditions remain mixed, strong momentum across Latin America and APME (Asia Pac and Middle East) offset by softer trends in Europe and North America, where activity levels remain well below historical peaks yet stable over recent quarters. While hiring remains cautious, we continue to see gradual, broad based signs of stabilization.”

This all gets to the theme we’ve seen of little hiring, little firing. The CEO said more on this, “it is a bit of a strange time in many labor markets in Europe and North America. As you heard me characterize in our call, it’s like a frozen labor market. There’s very little hiring going on, and there’s very little workforce reductions going on.”

From United Airlines and whose stock fell 5.5% on worries about the sustainability of the premium strength:

“Premium cabins outperformed the main cabin once again.”

“Leisure demand is also healthy as we head into Q4. Not unlike 2024, capacity and demand are simply better balanced in the last quarter of this year, particularly for global long haul flying.”

“We saw bookings inflect positive in early July, and industry revenues are expected to be positive y/o/y for all remaining months of 2025.”

“International RASM (revenue per available seat mile) in Q4 will outperform domestic based on the current outlook.”

“General inflation in this industry is running about 3% to 4% annually, and we expect that to continue, inclusive of labor.”

From Commercial Metal, the steel maker:

“Shipments of finished steel increased y/o/y and were unchanged from the prior quarter’s strong level. Downstream bid volumes, our best gauge of the construction pipeline, remained healthy and were consistent with recent quarters as we continue to see strength across a number of key market segments, including public works, highway and bridge, institutional buildings, and data centers.”

“our customers are increasingly bullish as they experience a large inflow of projects into the pipeline related to energy generation, reshoring, advanced manufacturing, and LNG infrastructure.”

Separately, I’m happy to see the US automakers get some tariff relief on imported car parts for an additional five years, past the current two year time frame. But, it points to the cronyism of this where those with big time lobbyists can get help with exemptions from tariffs while those small and medium sized businesses that don’t, get no help.:

BY Doug Kass · Oct 17, 2025, 10:00 AM EDT

Covered trading short rental in the indexes right after the opening - for a quick profit:

* (SPY) $658.77

* (QQQ) $597.52

BY Doug Kass · Oct 17, 2025, 9:40 AM EDT

Risk happens fast.

An important repost from four days ago:

OCT 13, 2025 1:45 PM EDT

* Stocks remain pornographically overvalued.

* Look out below — investors are meaningfully underpricing risk.

* "Slugflation" remains our base case — accompanied by a revaluation (lower) in price earnings multiples.

* The Fed may be between a rock and a hard place.

* More aggressive money printing (encouraged by President Trump) could cushion the market downside over the short term but could contribute to more downside "down the road."

* We think the downside risk is approximately 4x the upside reward...

Driving that train

High on cocaine

Casey Jones you better

Watch your speed

Trouble ahead

Trouble behind

And you know that notion

Just crossed my mind

Trouble ahead

A lady in red

Take my advice

You'd be better off dead

Switchman sleeping

Train hundred and two is

On the wrong track

And headed for you

- The Grateful Dead, Casey Jones

In my view investors are continuing to underprice risk — perhaps significantly so.

I started out a recent podcast/interview with David Rosenberg by stating equities were potentially pornographically overvalued. This continues to be my base case:

That said, for the moment, I clearly continue to underestimate the markets' strength and my ursine market view (which is in the distinct minority) has been wrong-footed. (As Grandma Koufax used to tell me, "Dougie, If you want to be trusted, be honest!)

I invest unemotionally, refusing to compromise our dual mandate of assessing of reward v. risk and "margin of safety" even as many market participants seem to be losing their heads.

Investors continue to disregard the worsening fundamentals (slowing economic growth and sticky inflation), threatening geopolitics (China is building their own axis of power with Russia and India at a time in which the U.S. technology complex remains highly dependent on inputs from China), the most polarized and uncooperative Democratic/Republican parties in history, an unbalanced domestic economy (of haves and have nots), reckless fiscal policy that has contributed to a never ending expansion of the U.S. debt load and historically elevated valuations.

As I have expressed over the last few months, I feel strongly that stocks represent little value today. I am increasingly confident that equities will likely decline from current levels.

I am equally confident that I will be willing to expand my long exposure at the appropriate time when equities, again, represent a better value proposition.

In the business media, comparisons today are being increasingly made with prior bubbles. I wanted to offer my views of this subject.

There have arguably been three well-defined speculative cycles in equities over the last six decades — The Nifty Fifty Era (the 1960s to the early 1970s), the Dot-Com Boom (mid-to-late 1990s to early 2000) and the recent Mag 7 and AI Boom.

All three of these eras have fueled a bull market in equities. The end of the Nifty Fifty Era and the Dot-Com Boom marked the end of the respective bull markets and were followed by market crashes.

* The Nifty Fifty Era was marked by fifty large cap stocks that were considered blue chips and buy and hold (one decision) growth stocks. The common characteristic of the stocks in this basket was that the companies achieved consistently superior profits growth. They were assigned extraordinarily high price/earnings ratios of 50x or higher — well above the long-term market average of between 15x and 20x. Representative stocks included American Express, Avon Products, Bristol-Myers, Coca-Cola, Eastman Kodak, General Electric, Polaroid, Procter & Gamble, Sears, Roebuck and Xerox. Most of the companies on this list were well established, where investors perceived deep moats (preventing competitors from making market share inroads) and with a clear expectation that the companies would sustain high returns on invested capital. The reality was that there was far less innovation taking place in those anointed companies. At the time of The Nifty Fifty, bank trust departments (Citigroup, JPMorgan, etc.) were the dominant investors and materially overweighted these anointed stocks.

* The Dot-Com Boom existed in the late 1990s and peaked in the first quarter of 2000, coincident with the widespread adoption and use of the internet. This technology-inspired boom was seen as similar to others in the past (railroads in the 1840s, automobiles in the early 1900s, radio in the 1920s, television in the 1940s and computer time-sharing in the 1960s and home computers in the 1980s). Webvan, Boo.com and Pets.com were the standard-bearers of that period. In large measure the companies were not real in the sense that they had no plausible business models and they were run by dreamers and not serious businessmen. Essentially, they were one giant promotion. But in size (market capitalizations), the promotions (like Pets.com) were not consequential in market capitalization.

However, several large tech companies (like Cisco and Sun Microsystems) were swept up to ridiculously high valuations along with the worthless dot-com promotions.

Sun Microsystems' market capitalization peaked at over $200 billion — representing a price-to-revenue of (a lofty) 10x (which pales when compared to today's tech leaders). Sun Microsystems actually had a suite of revolutionary products from Java programming language to SPARC processors, StarOffice, My SQL, Solaris OS and VirtualBox. The company was ultimately sold for only $7 billion to Oracle a decade after the Dot-Com Boom deflated.

Years after the Dot-Com bust Sun Microsystem's Chairman Scott McNealy famously reflected on the absurdity of Sun's peak valuation with this iconic quote:

"At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate. Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?"

Here is a stock chart of Sun Microsystems (1996-2007):

* The (Current) Climb in Mag 7 and AI has fueled almost the entirety of the market advance over the last few years. Unlike the Nifty Fifty or the Dot-Com promotions, Mag 7 consists of companies that historically have had consistently sizeable cash flows, unleveraged and liquid balance sheets and limited (physical plant) capital needs owing to deep competitive moats (and near monopoly status in phones, operating systems, search, etc.). Whereas the industrial Nifty Fifty companies needed to build new factory production lines and new factories to maintain their competitive status and growth, the Mag 7 are able to innovate rapidly and relatively inexpensively by simply sending product upgrades online (with no manufacturing or shipping required).

Until recently the Mag 7 business models were capital light but that has changed with the monumental AI capital spend. Most of the Mag 7 constituents are now becoming capital intensive, which is a big change (and incorporates sizeable risks). This capital outlay is being accompanied by an uncertain timing and level of return on massive and unprecedented amounts of invested capital.

There are some substantial differences between the Dot-Com days and what is going on now with the AI infrastructure build. Capacity put in place in the late 1990s was a very long-lived asset. Take fiber optic cable for example — much of the stuff (and constituent components) put into place then is still in use now. This is one of the reasons why the Dot-Com buildout quickly went into overcapacity. The assets were sticky.

AI infrastructure is the polar opposite. It obsoletes incredibly quickly — much more quickly than depreciation schedules imply. Oddly, this is part of the bull case, ergo everything will keep having to be rapidly replaced, so the spending will not stop. The bull case treats investment capital as infinite and the laws of economics as irrelevant. It assumes the circular financing and money losing will go on forever. Of course, professional investors know that is not true and they do not really believe the grossly dis-economic behavior can continue forever. They just believe it is in place for the quarter we are in (with upbeat guidance) and it is just one more way to rationalize the game of musical chairs they are playing. Most recognize that they are playing the same game and are just being dragged along by the whims of over-levered retail as well. They all think they will be the first to get out when the music stops. Many just don’t care because they manage against a benchmark.

Here are two tweets that demonstrate how dis-economic the AI spend might be:

One other big difference between the Dot-Com days and now, is the Dot-Com stuff actually worked like it was supposed to — it was not a capital black hole. Actually it did increase net productivity, did not consume so much in the way of energy and other resources that it was in fact inflationary. And it was not being subsidized by the public at large (power cost) and actual human content creators.

And just for fun:

Bottom Line: I would conclude that the Nifty Fifty Era consisted of a bunch of entrenched companies that were materially overvalued in a period when bank trust departments were the dominant investors. The Dot-Com Boom consisted of a number of promotions and large-cap tech stocks that became significantly overvalued (with day traders becoming the dominant investors). Both could be described as bubbles.

By contrast, the Mag 7/AI period consists of near monopolies (that are arguably fully priced to overpriced) as they morph from capital-light to capital-intensive business models — with the risks associated with circular vendor financing, accessing adequate sources of energy (at a reasonable cost), the availability of capable workers and other potential problems inherent with the construction of large-scale data centers.

While bank trust departments no longer roam the investing planet, passive investing products and strategies (ETFs and quantitative investors) now dominate. Passive investors are unemotional and no nothing about value but everything about price as they all worship at the altar of price momentum — serving to exaggerate the market's returns and that of the leading technology companies.

I conclude that today we are not in a bubble (as we were with the Nifty Fifty and The Dot-Com Boom), though some similarities exist. Rather we are simply in an extremely and historically overvalued market (within a much different market structure backdrop dominated by passive investors).

Finally, here are some examples of comparing valuations in these three eras.

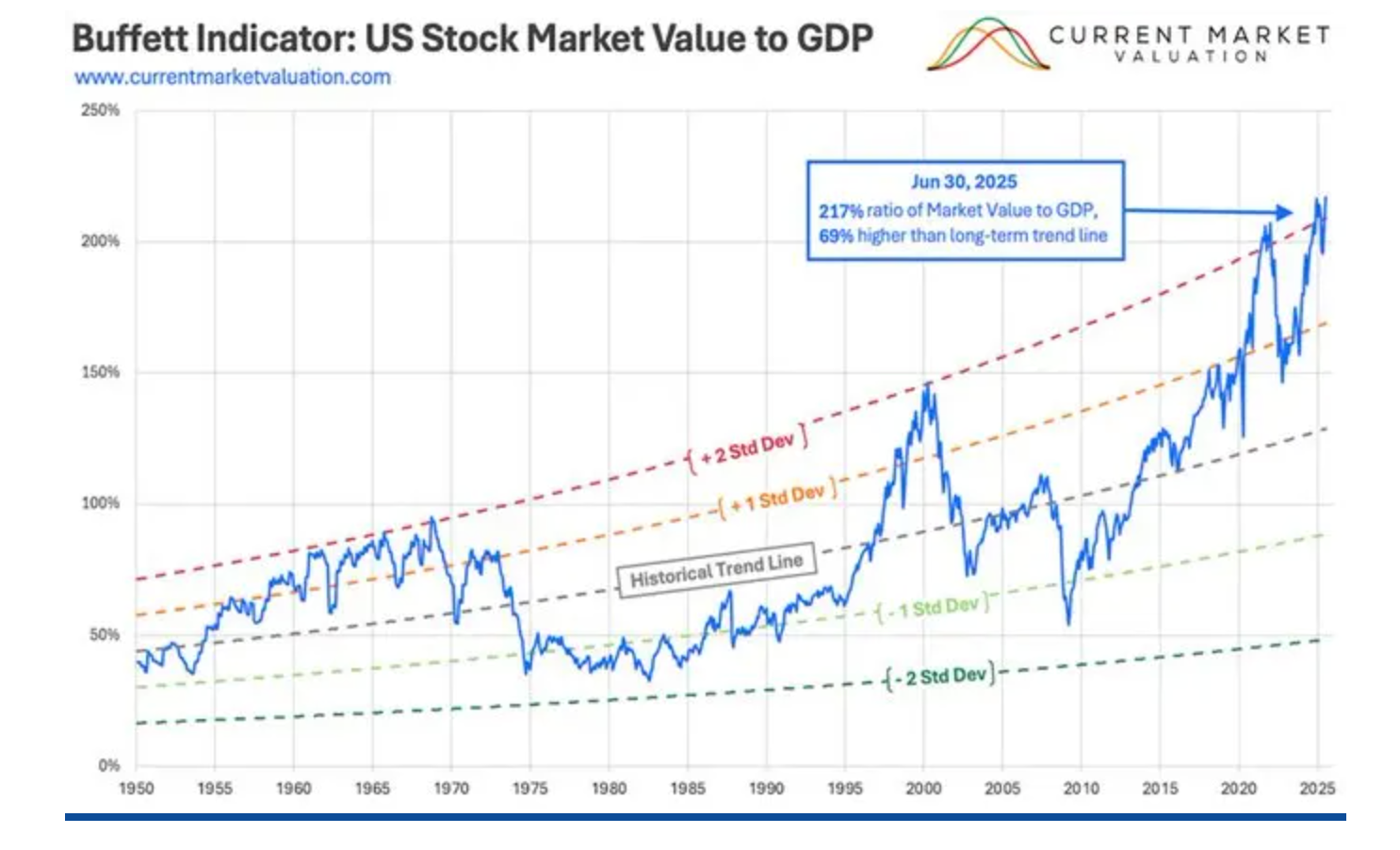

The Buffett Indicator stands at two standard deviations above its long-term trendline and at a record high of 217% (well above the Dot-Com era):

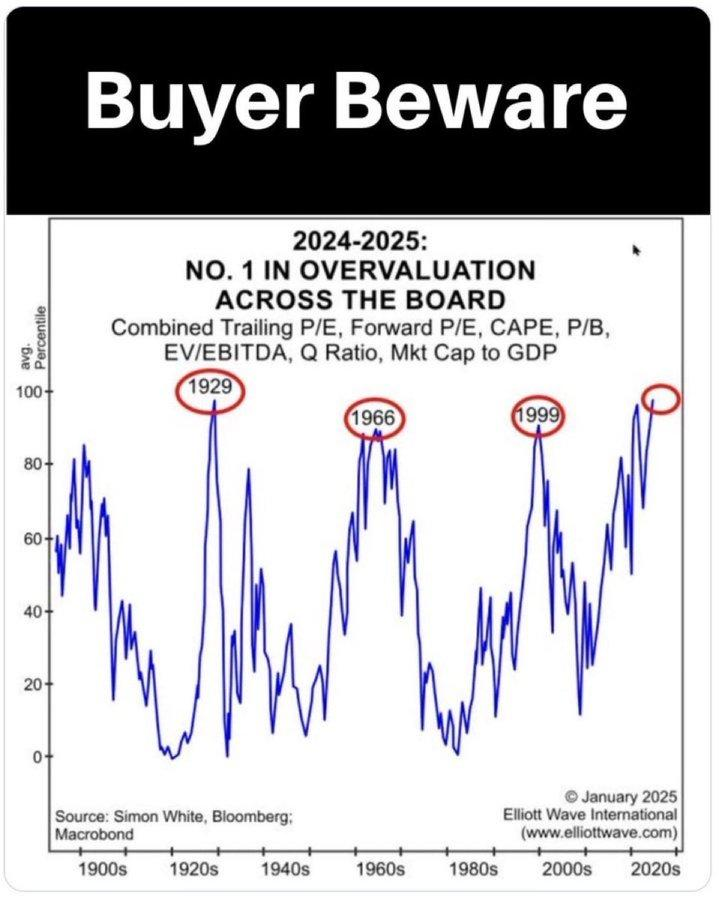

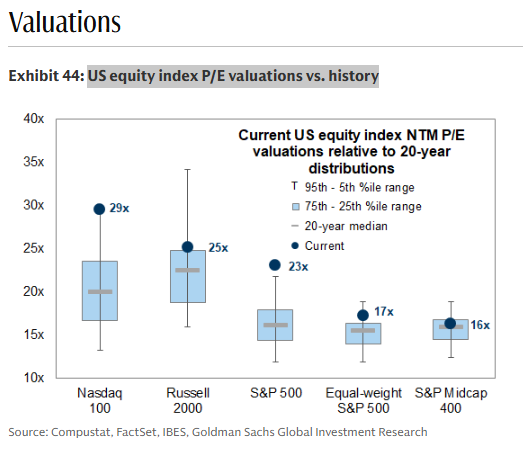

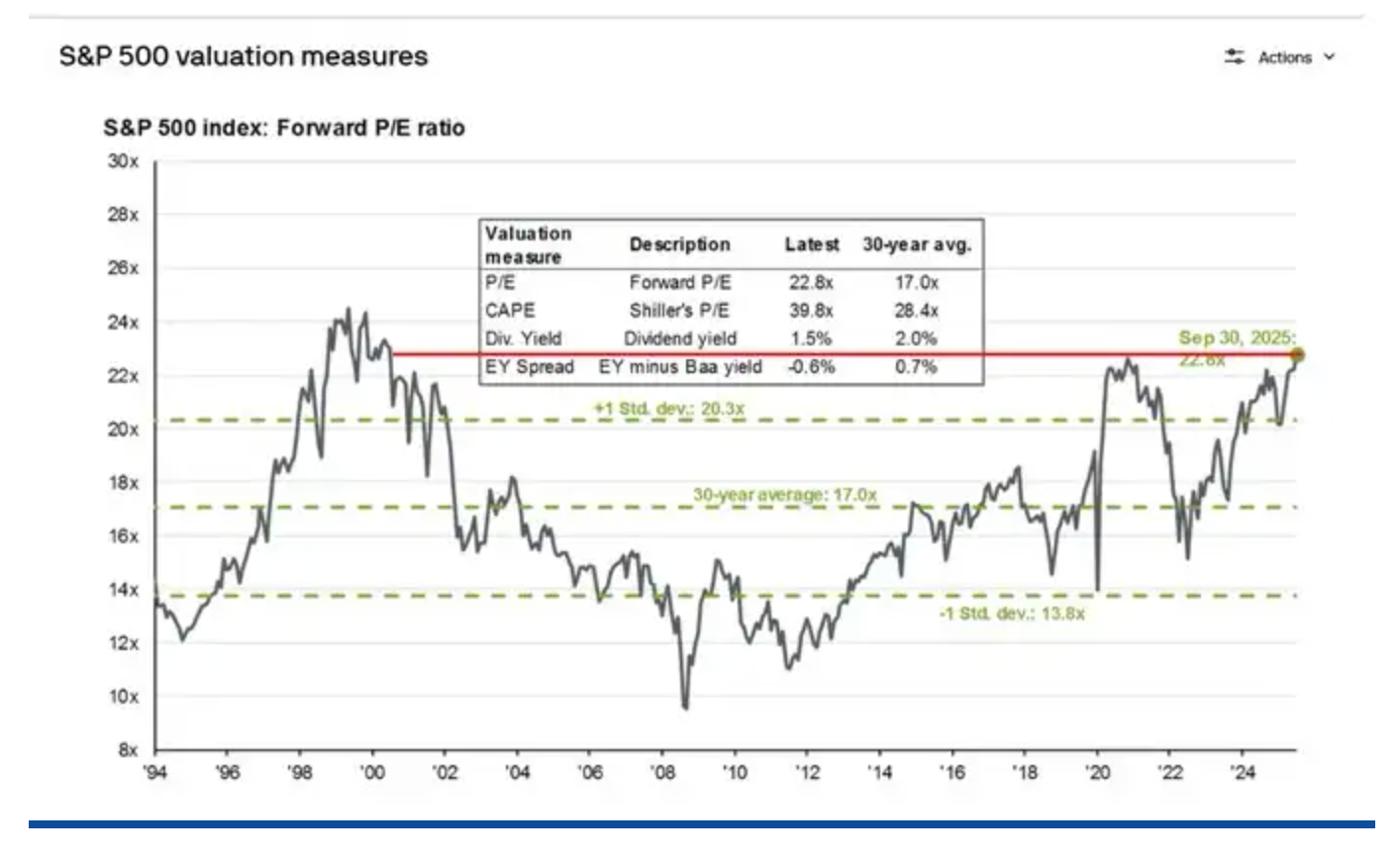

Most traditional valuation metrics approach the 98%-tile. Today's price-earnings multiple on the S&P Index is 23x — the highest in 26 years (back to the peak in the Dot-Com period) and compared to the 30-year long-term average of only 17x:

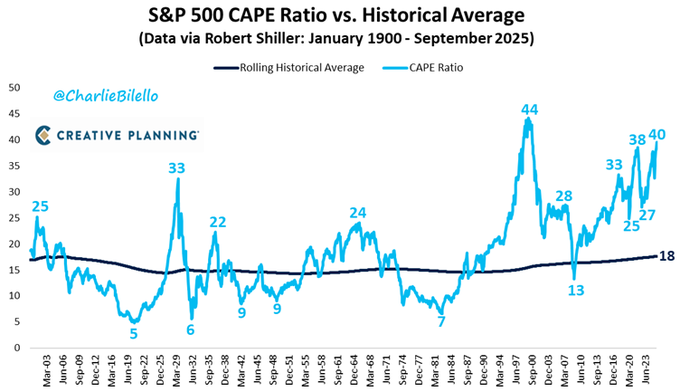

Dr. Robert Shiller's CAPE Ratio today is 40x vs 44x at the peak of Dot-Com and only 24x at the height of the Nifty Fifty Era. However, if we adjust profits for the low tax rates today compared to the peak in 2000 the Schillers CAPE is above 46x:

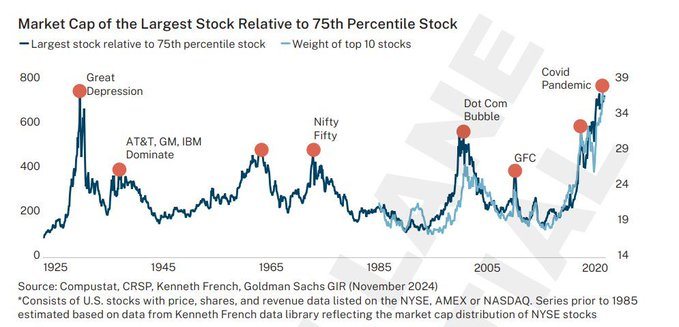

Today's unparalleled S&P concentration into a handful of large-cap tech stocks is similar (and more extreme) than in the prior bubbles. Such concentration when coupled with elevated valuations almost always is a poor launching pad for future investment returns and often presages substantive bear markets or extended periods of substandard returns (our base case):

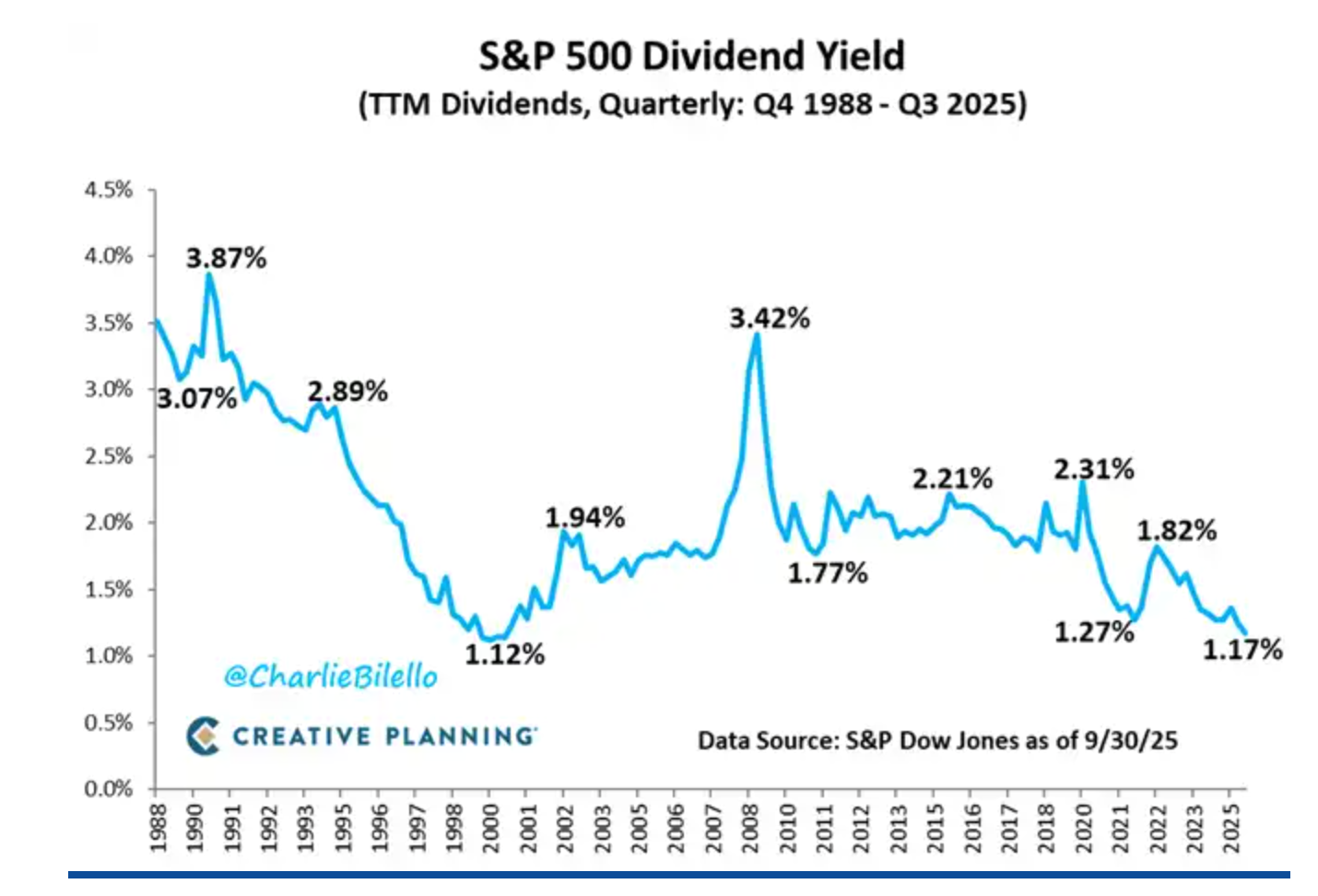

Let’s look at the similarity of the S&P dividend yield today compared to the peak of the Dot-Com Boom:

Over time dividends have contributed to about one-third of the total return for stocks — with the rest coming from capital appreciation. Today, the S&P Dividend Yield is only 1.17% — the lowest read in 2 1/2 decades (since the Dot-Com Boom). This means if S&P dividends maintain their 1/3 historical contribution to the total annual return for stocks, a 1.17% dividend yield translates into a lowly +3.5% total return for equities. With the S&P earnings yield of about 4.0% (the inverse of the P/E) and the 10-year Treasury yielding 4.15% — the equity risk premium is negative! The difference between the S&P dividend yield (1.17%) and the risk-free rate of return (4.15%) is also at a multiple-decade wide.

A low expected total return for equities coupled with a higher risk-free rate of return is fundamental to my bearish market case.

While I don't think the next few years will resemble the brutal declines of The Nifty Fifty (that began in 1973-74) of the Dot-Com bust (that commenced in early 2000), the downside to equities remains meaningful.

One of the most important factors that could insulate the S&P Index from the magnitude of the drawdown that I expect is if the current Administration is successful in persuading the Federal Reserve to adopt a very aggressive path to easing monetary policy. Events of the last few months suggest that President Trump will try his best to encourage the Fed to cut rates dramatically over the next six to 12 months.

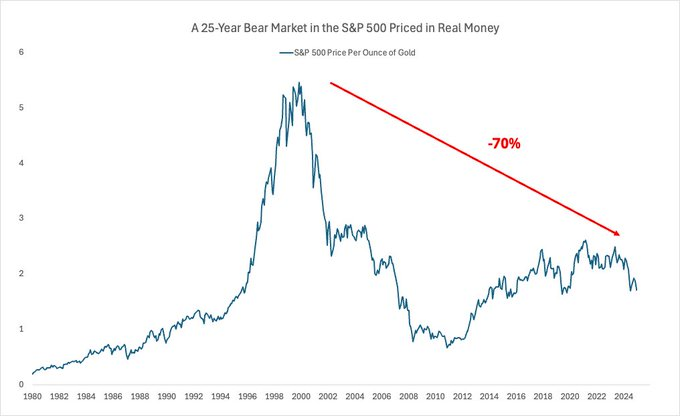

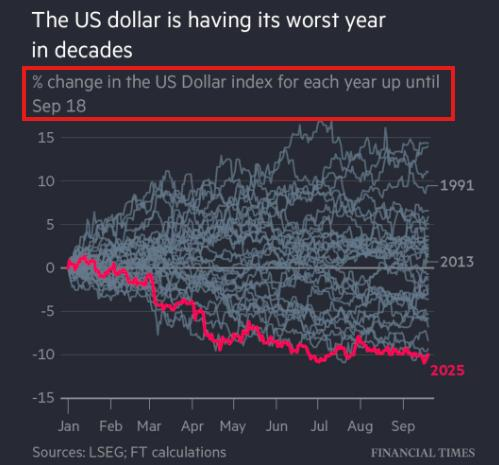

The excessive global easing of the past 15 years has been a money illusion that has created the mirage of wealth through excessive monetary ease and rampant currency devaluation. In real money terms, the S&P Index has lost 70% of its value in the last twenty-five years:

Our currency just saw its biggest six-month drop in 50 years. The U.S. dollar in now on track for its worst year since 1973 (-10% year to date) as the Federal Reserve cuts rates into relatively strong U.S. GDP and core inflation remains stubbornly high.

The U.S. isn't falling apart — we are still a leader in innovation, education, etc. But with our government debt out of control and inflation not in control, the rest of the world is adjusting their perception of us.

Confidence in our currency is changing as global investors are beginning to question the safety of holding U.S. assets. Non-U.S. investors are no longer willing to go all-in on the U.S. dollar as they are keeping one foot in growth (in U.S.-based equities) and the other in the safety (of non-U.S. currencies).

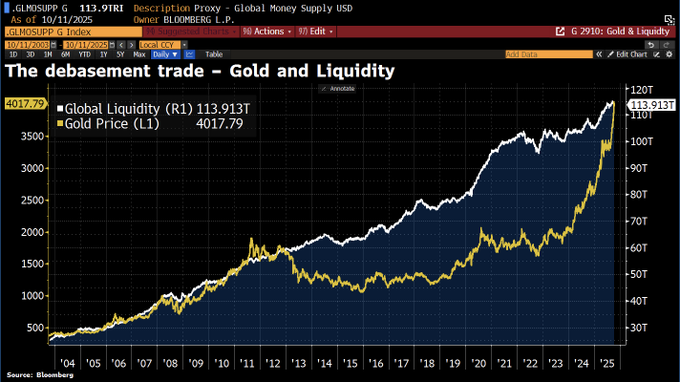

Gold is setting records daily as money is slowly leaving assets that depend on trust and moving into things that may be able to stand on their own like precious metals and cryptocurrencies.

The debasement trade is in overdrive. To wit, gold, in particular, has recently climbed much faster than global liquidity, a clear sign of growing mistrust in the monetary system:

Even foreign investors who want exposure to U.S. companies have begun to hedge their returns into local currencies because they are losing confidence in U.S. policy and even in the generation of our economic data.

In summary, a more aggressive-than-expected monetary easing in the U.S. could contribute to the appearance of a better-than-forecast stock market going forward. (This expectation may explain the surprising strength in global equities this year.)

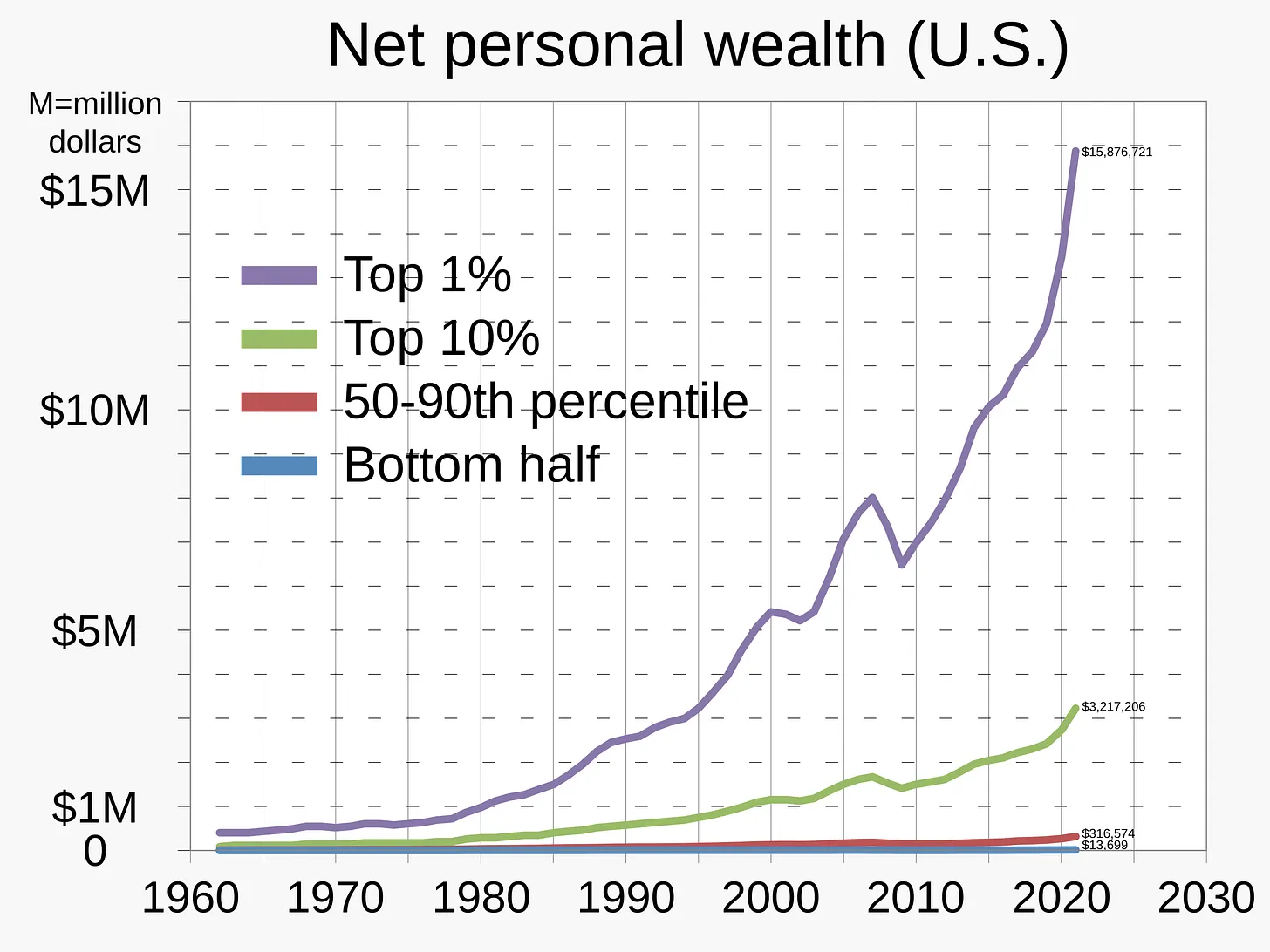

The problem is that this policy, if it continues, may serve to further widen the inequality gap — disproportionately affecting the middle and lower classes (who don't hold large balance sheets consisting of real estate and equities):

Under this circumstance, with inflation likely accelerating (as bond vigilantes come out of hibernation, causing intermediate-to longer-term interest rates to rise) in response to the Fed's interest rate cuts and with the likely continuation of irresponsible fiscal policies in Washington, D.C., the notion of American Exceptionalism might be seriously challenged.

Thus, higher equity prices, in nominal terms, may really be more of an illusion when coupled with a continued denigration in the U.S. dollar.

From Christopher Irons who writes under the pseudonym Quoth The Raven:

"There will come a point one day where, psychologically, the Fed intervenes and stock prices may go up again, but the average investor is living out depressionary hardships. And I mean this for people who are lucky enough to even own financial assets. Many lower- and middle-class families don’t even have significant amounts of financial assets but, rather, have negative net worth. The wreckage to these classes will be unlike anything we’ve ever seen before.

Make no mistake about it — we appear to be stuck between a rock and a hard place where the only exit door seems to be stagflation. This is something we haven’t combated since the 1970s, and the monetary policy and fiscal layout of the country right now is so distorted that people from the 1970s wouldn’t even recognize it.

The Fed has no option to raise rates into a stagflationary environment because of the ungodly amount of debt we have outstanding. Even with rates where they are now, I believe the Fed is out over its skis and has already sealed the fate of guaranteed defeat for the economy and markets.

So what happens then? We’re stuck between welcoming a deflationary depression by raising rates to try to combat inflation, or we’re going to have to let inflation run wild. We’ve never been in this situation before in modern history. And even more frightening than that is the fact that market participants and the average American citizen are the most coddled and the least equipped to handle bad news related to the economy than they’ve ever been."

BY Doug Kass · Oct 17, 2025, 9:35 AM EDT

BY Doug Kass · Oct 17, 2025, 9:15 AM EDT

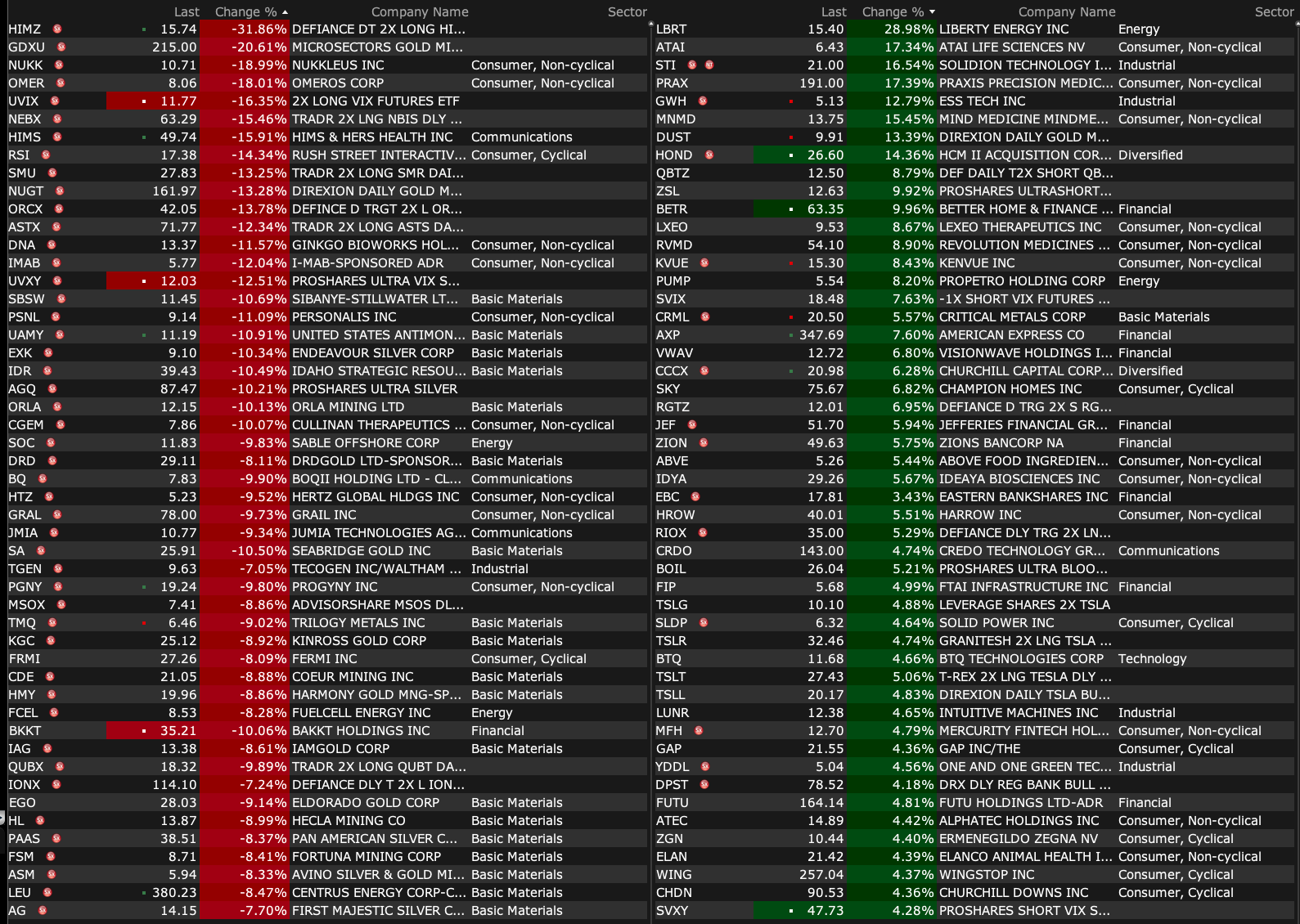

-RANI +152% (signs $1B+ collaboration with Chugai; secures $60.3M financing to extend cash runway to 2028)

-ARTV +107% (announces Refractory Rheumatoid Arthritis as Lead Indication, Upcoming Data Releases, and Corporate Update; FDA feedback expected in 1H26)

-AKAN +26% (awarded 20 tower expansion agreement in $7B Mexican telecom project)

-ACHV +19% (receives FDA Commissioner's National Priority Voucher for Cytisinicline for Treatment of Nicotine Dependence for E-cigarette or Vaping Cessation)

-ALLY +6.6% (earnings, guidance)

-LUNR +5.2% (Deutsche Bank Raised LUNR to Buy from Hold, price target: $18)

-ZION +4.3% (Baird Raised ZION to Outperform from Neutral, price target: $65)

-FNB +3.4% (earnings, guidance)

-GBCI +3.3% (earnings)

-WAL +3.1% (momentum)

-JEF +3.0% (hearing Oppenheimer Raised JEF to Outperform from Perform, price target: $81)

-CSX +2.9% (earnings, color)

-RF +2.9% (earnings, guidance)

-HBAN +2.7% (earnings, guidance)

-SLI -19% (prices upsized $130M offering of ~29.9M shares at $4.35/shr (prior $120M))

-JMIA -7.4% (hearing Boutique Firm Cuts JMIA to Sell from Buy, price target: $7.50)

-CIFR -4.8% (major shareholder sells shares)

-LXEO -4.0% (prices 15.6M shares at $8.00/shr for gross proceeds ~$135M)

-NVO -4.0% (President Trump targets lowering weight loss med prices)

-LLY -3.7% (President Trump targets lowering weight loss med prices)

-ASTS -3.5% (Barclays Cuts ASTS to Underweight from Overweight, price target: $60)

-STT -2.6% (earnings, color)

-ORCL -2.1% (Investor Day guidance)

BY Doug Kass · Oct 17, 2025, 9:05 AM EDT

With S &P futures now +1 after being -95 handles four hours ago I am back shorting the Indexes:

* (SPY) $660.99

* (QQQ) $599.22

BY Doug Kass · Oct 17, 2025, 8:50 AM EDT

BY Doug Kass · Oct 17, 2025, 8:45 AM EDT

12:15 p.m.: Fed Bank of St. Louis President Musalem (Voter) discusses the U.S. economy and monetary policy before the Institute for International Finance Annual Membership Meeting, Washington, DC (No text. No media availability. In person event with virtual option)

BY Doug Kass · Oct 17, 2025, 8:33 AM EDT

BY Doug Kass · Oct 17, 2025, 8:00 AM EDT

Rule 1. Markets are risky.

Rule 2. Trouble runs in streaks.

Rule 3. Markets have a personality.

Rule 4. Markets mislead.

Rule 5. Market time is relative

― Benoît B. Mandelbrot, The (Mis)Behavior of Markets

BY Doug Kass · Oct 17, 2025, 7:50 AM EDT

BY Doug Kass · Oct 17, 2025, 7:40 AM EDT

BY Doug Kass · Oct 17, 2025, 7:30 AM EDT

BY Doug Kass · Oct 17, 2025, 7:20 AM EDT

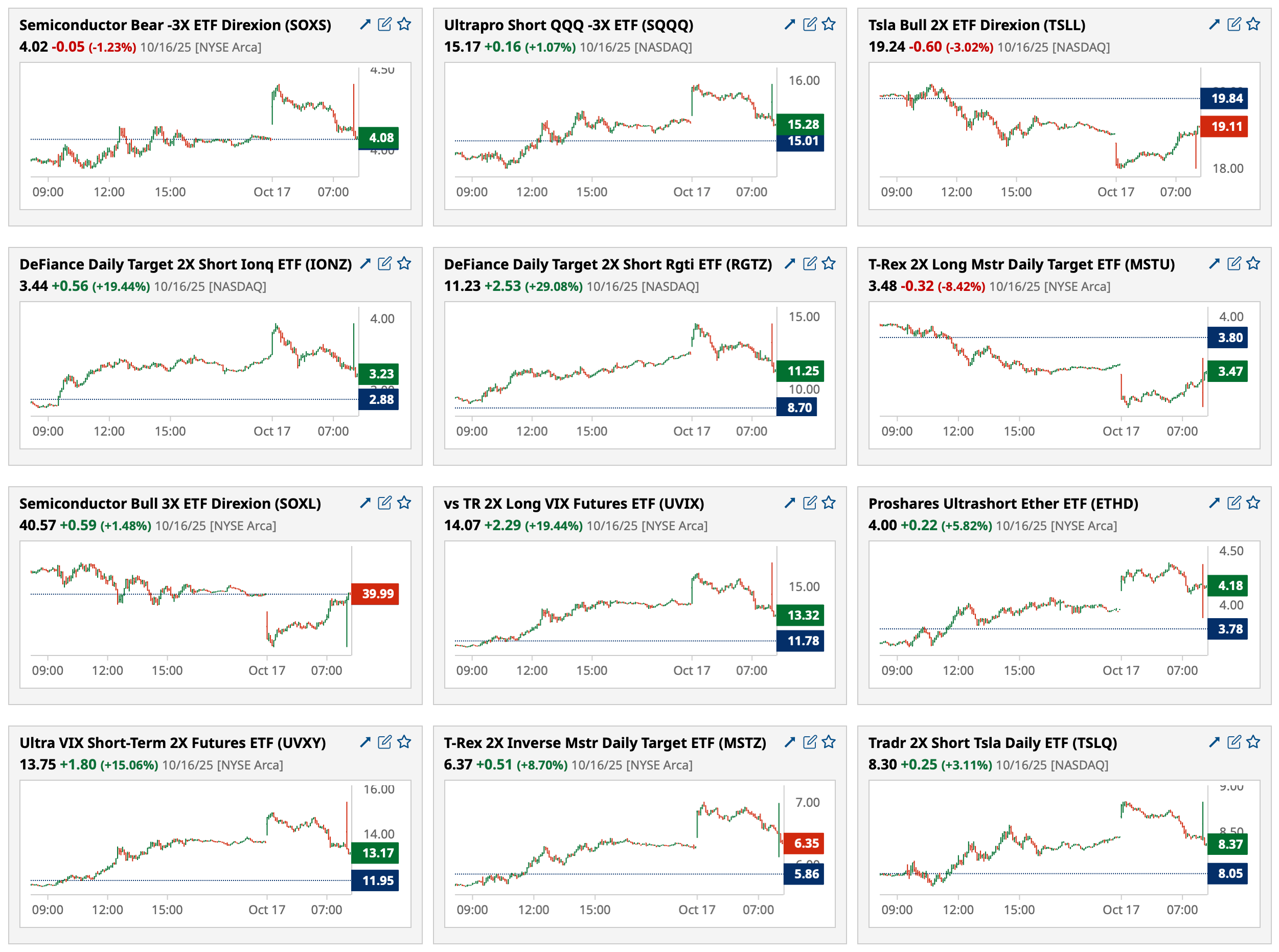

* Some of the best charts lie at the bottom of the ocean (remember bitcoin, financials and) ...

Bonus — Here are some great links:

Market's Best Three Months Starts Now ("Jazzy" Jeff Hirsch)

10-Year Below 4% Is a Positive

BY Doug Kass · Oct 17, 2025, 7:05 AM EDT

BY Doug Kass · Oct 17, 2025, 6:55 AM EDT

BY Doug Kass · Oct 17, 2025, 6:45 AM EDT

BY Doug Kass · Oct 17, 2025, 6:35 AM EDT

* The most recent example, financials...

They'll be ga ga at the go go

When they see me in my toga

My toga made of blond

Brilliantined

Biblical hair

- Hair Hair (1979) - song Hair

Less than one week ago, technical analysts were "gaga at the gogo" over financials:

Much like they were for bitcoin three weeks ago.

Sic transit gloria.

Another lesson learned: Be independent of thought and analysis.

BY Doug Kass · Oct 17, 2025, 6:25 AM EDT

BY Doug Kass · Oct 17, 2025, 6:15 AM EDT

Remember, I told you all to bookmark this post from October 7:

OCT 7, 2025 8:25 AM EDT

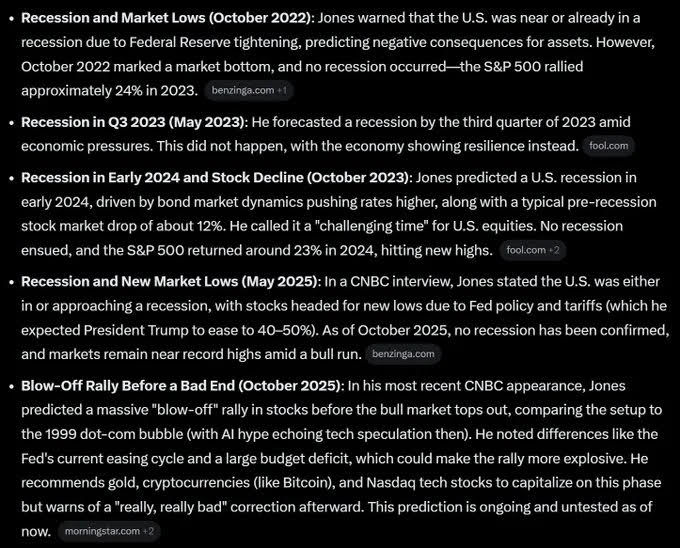

The Gospel According to Paul Tudor Jones

Paul Tudor Jones' Confident Market View Was Greeted Uncritically By Fin TV

* But, what is his record (for free advice)?

BY Doug Kass · Oct 17, 2025, 6:05 AM EDT

Gentlemen:

Maybe it's because I just finished re-reading "Too Big To Fail", but the cracks in WAL and ZION today on the heels of the unpleasantness in JEF grabbed my attention.

Back in 2007, Markit's ABX and CMBX indexes were giving the clearest warnings of the trouble ahead:

https://deemermarketmemos.com/archive/2000s/11-11-2007.pdf

Markit's data is now entrenched behind a very strong and very expensive paywall, but since there have now been at least three sightings of sick canaries I'm wondering if similar indexes exist that might be worth watching here. Closely. Very Closely.

Walter

BY Doug Kass · Oct 17, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at -1.63% vs. -0.49% — that's back into an oversold.

BY Doug Kass · Oct 17, 2025, 5:45 AM EDT