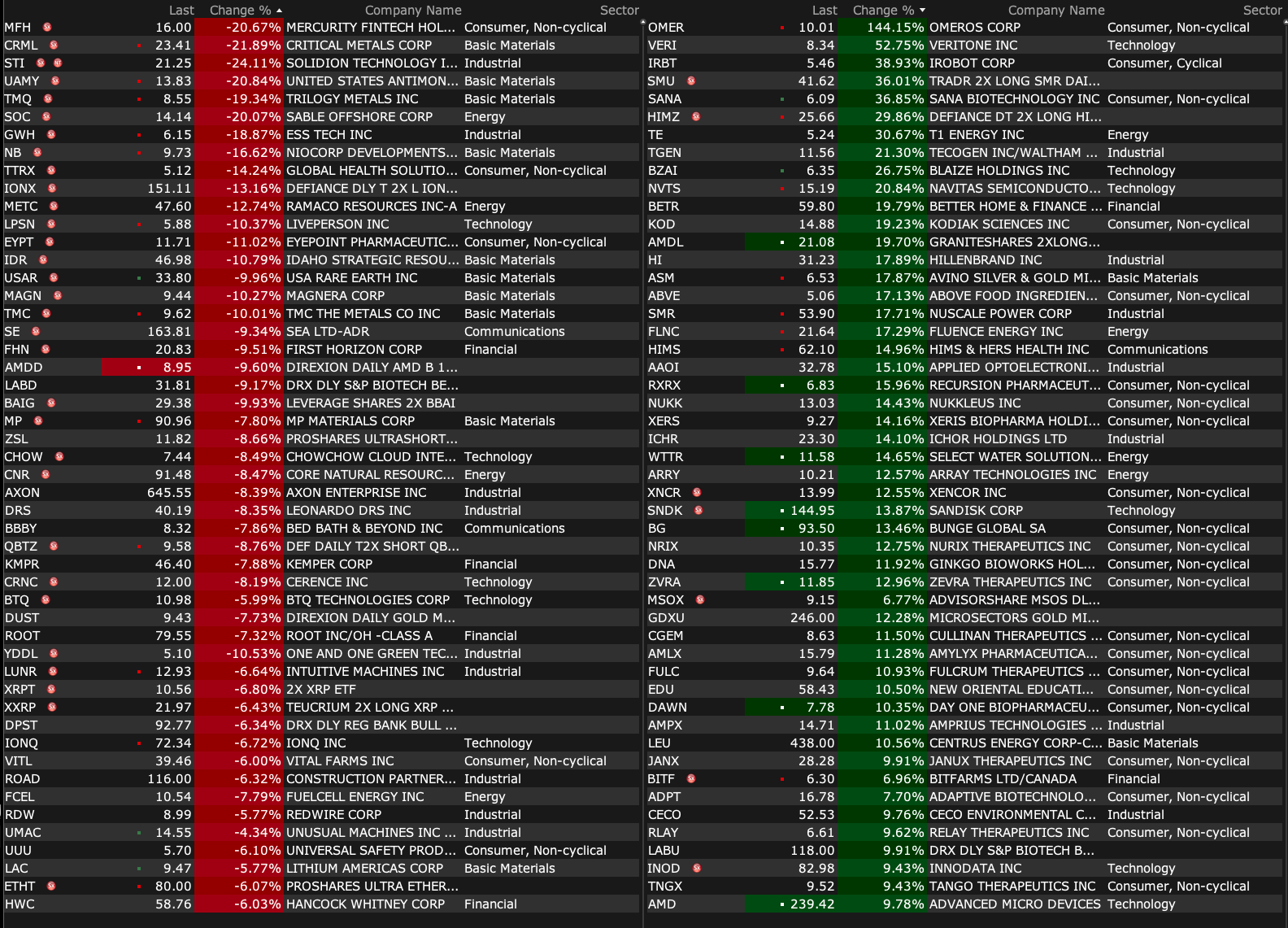

Upside:

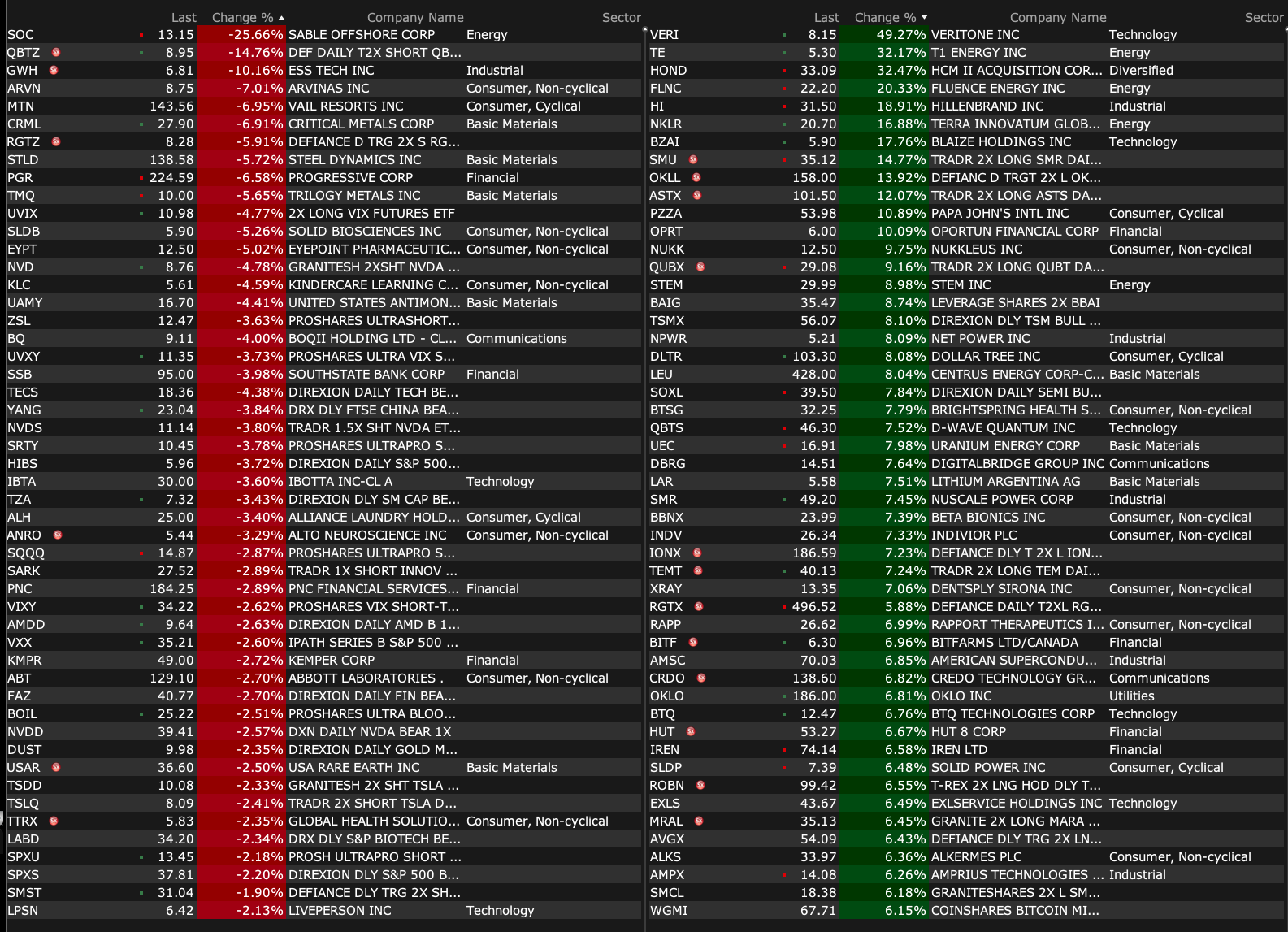

-OMER +72% (Novo Nordisk and Omeros announce asset purchase and license agreement for Omeros’ clinical-stage MASP-3 inhibitor zaltenibart (OMS906))

-VERI +47% (reports prelim Q3; announces VDR contracts)

-TE +27% (Nextracker and T1 Energy partner on US-made steel solar frames; Deal valued over $75M)

-BTDR +21% (reports Sept BTC Produced 452 v 375 m/m)

-HI +19% (to be acquired by Lone Star for $32.00/shr cash at EV ~$3.8B)

-FLNC +18% (hearing BMO raises price target)

-PZZA +11% (renewed talk of $64/share bid from Apollo)

-SPRC +9.6% (to acquire Miza III Ventures at EV $3.3M to which it will transfer its Advanced Clinical Stage Pharmaceutical Portfolio)

-DLTR +7.8% (guidance from Investor Day)

-CRDO +6.6% (planning to develop custom silicon for AI data centers)

-BG +5.4% (adjusts guidance)

-UUUU +5.2% (nuclear, uranium stock strength off escalating US/China trade tensions)

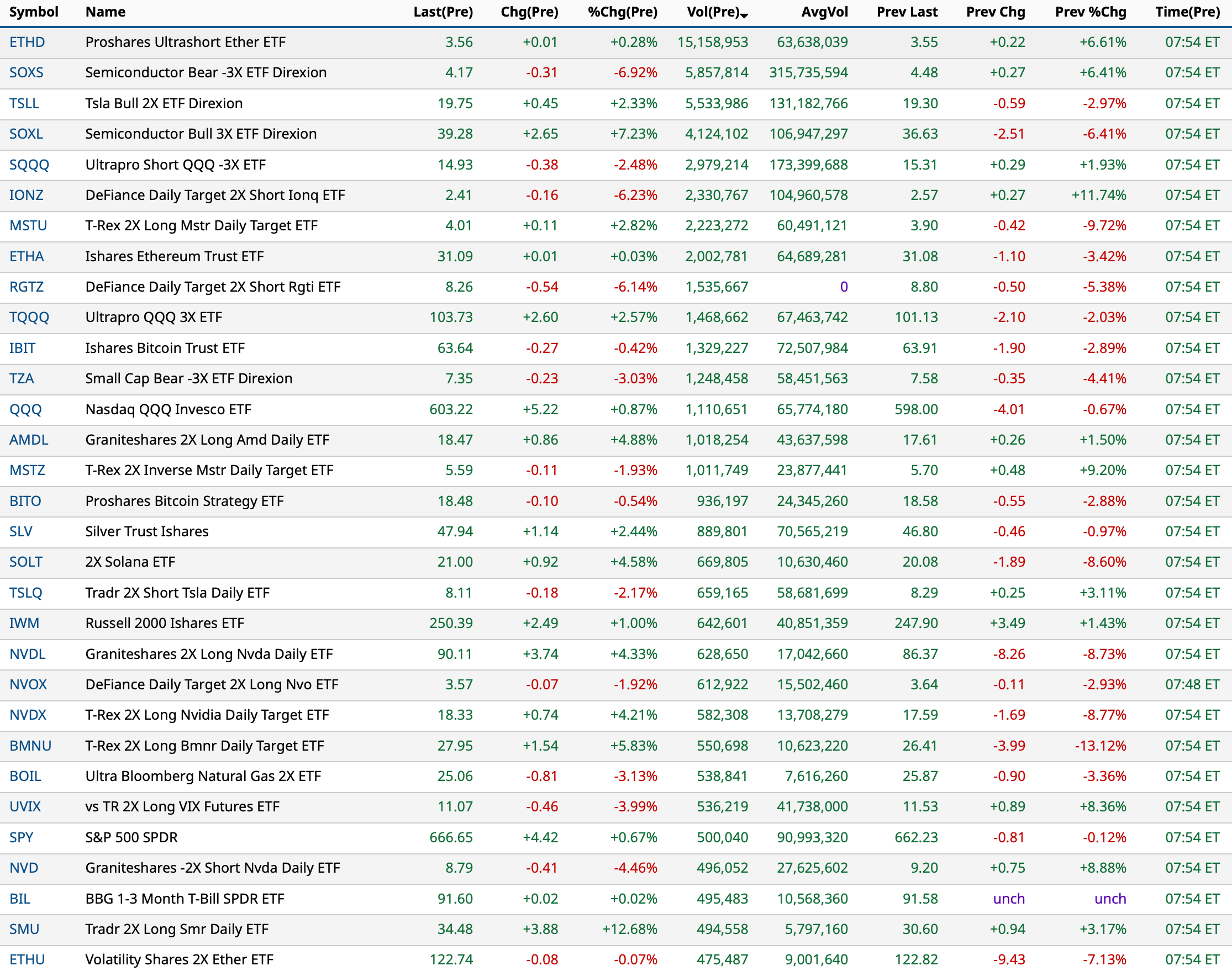

-APLD +4.7% (strength following Blackrock, Nvidia led group $40B data center agreement)

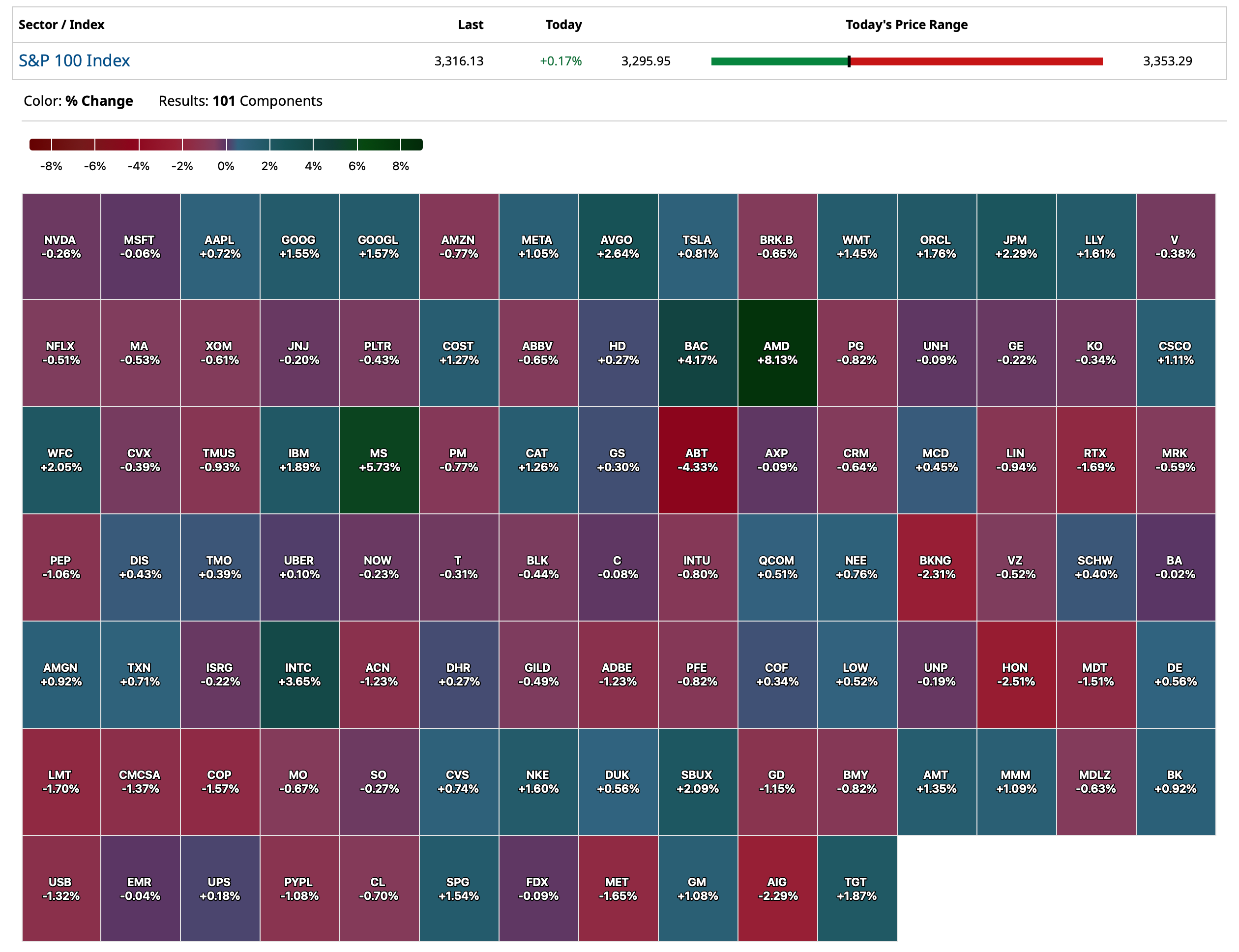

-ASML +4.6% (earnings, guidance)

-MS +4.6% (earnings, color)

-BAC +4.5% (earnings, guidance)

-RUN +4.4% (BMO Capital Markets Raised RUN to Market Perform from Underperform, price target: $19)

-SARO +3.8% (lands maintenance deal with Mauritania Airlines)

-CFG +3.1% (earnings, guidance)

-FHN +2.5% (earnings, guidance)

-NVDA +2.5% (reportedly investment consortium that includes BlackRock, Nvidia, xAI and Microsoft to acquire Texas-based Aligned Data Centers from Macquarie Asset Management for $40B)

Downside:

-SOC -23% (issues statement on California Coastal Commission Litigation; Court ruled it would deny Sable's claims; Sable vigorously disagrees with the court’s tentative ruling)

-ASPI -9.7% (prices 17.2M shares in $210M underwritten public offering)

-KARO -6.5% (earnings, guidance)

-EQBK -3.7% (earnings, guidance)

-PNC -3.0% (earnings, guidance)

-ABT -2.6% (earnings, guidance)

-FFIV -2.3% (discloses unauthorized access by a nation-state threat actor)