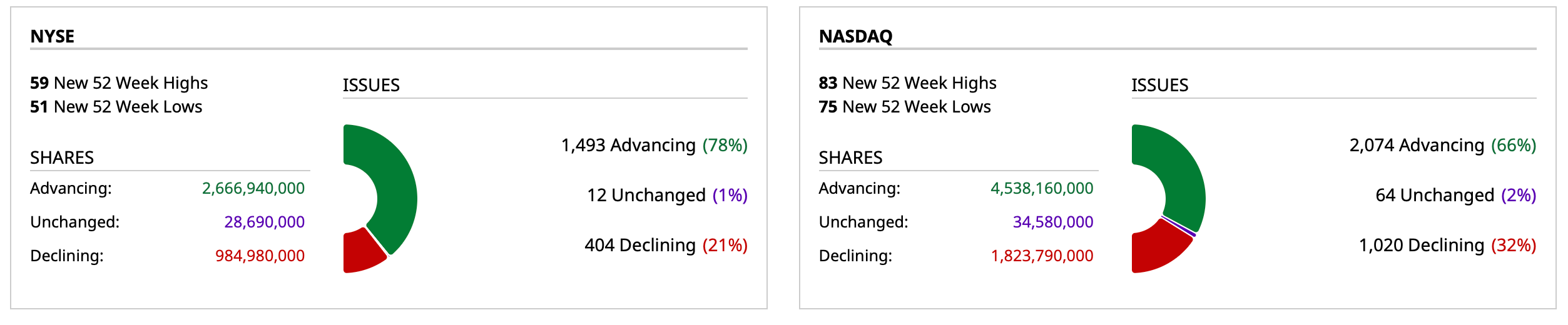

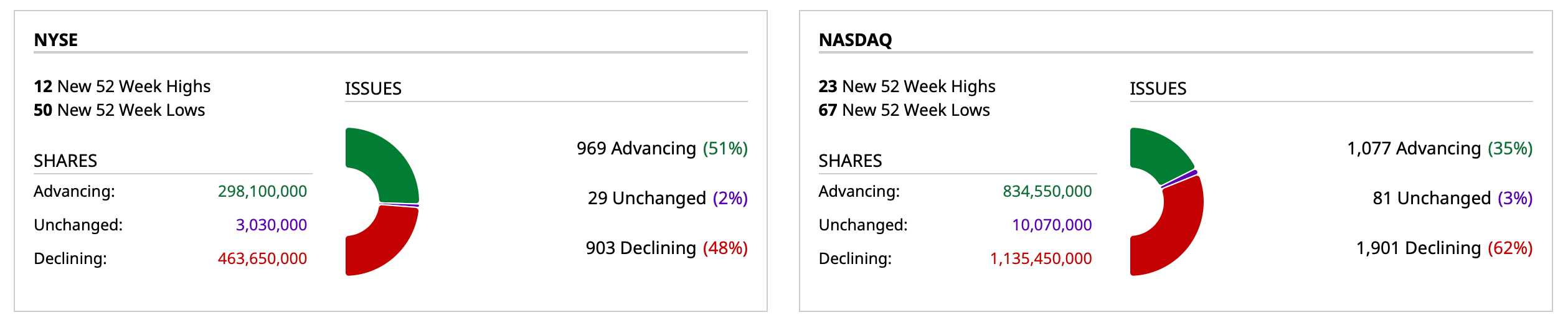

Tuesday's Closing Market Stats

Closing Breadth

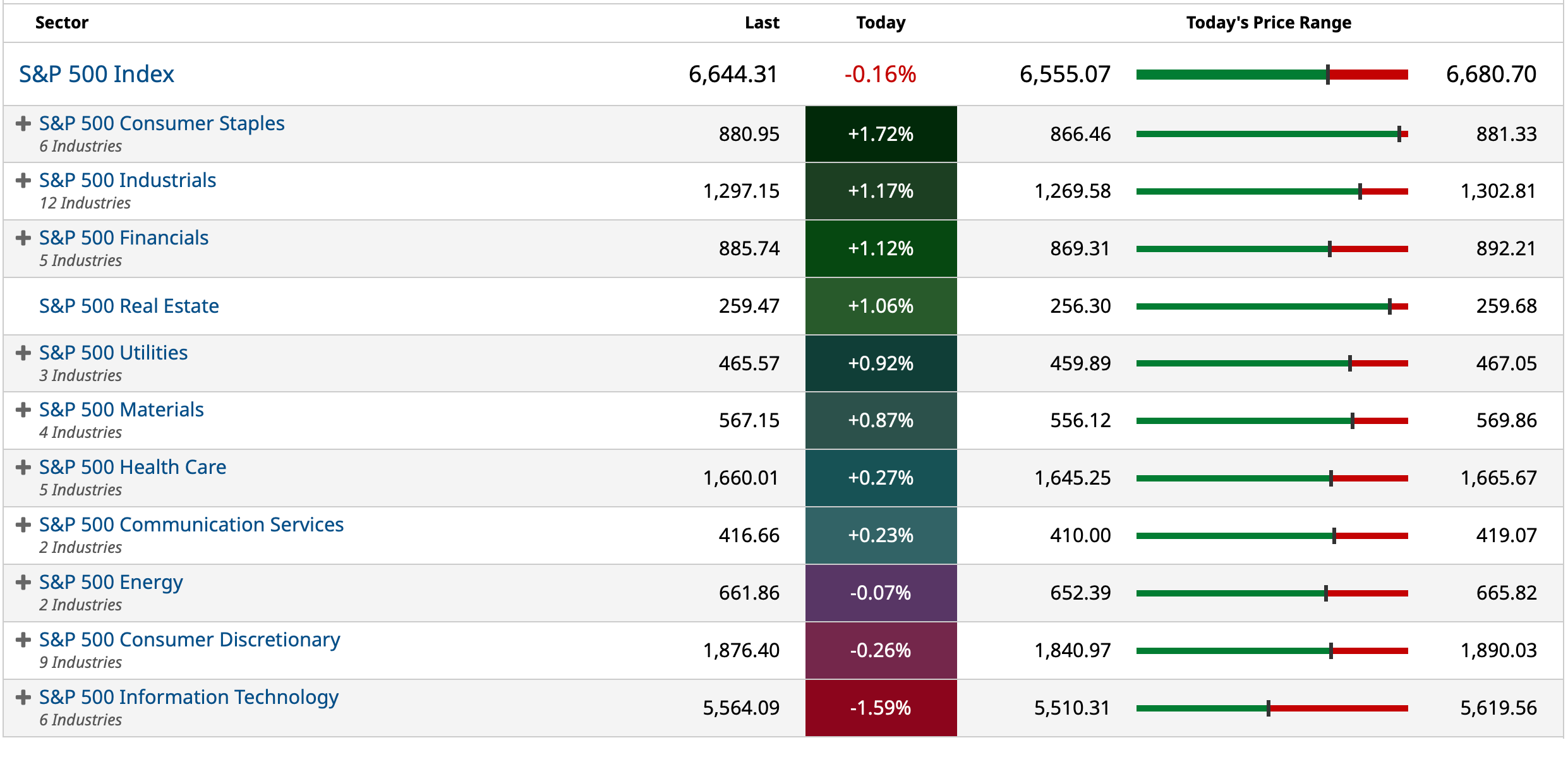

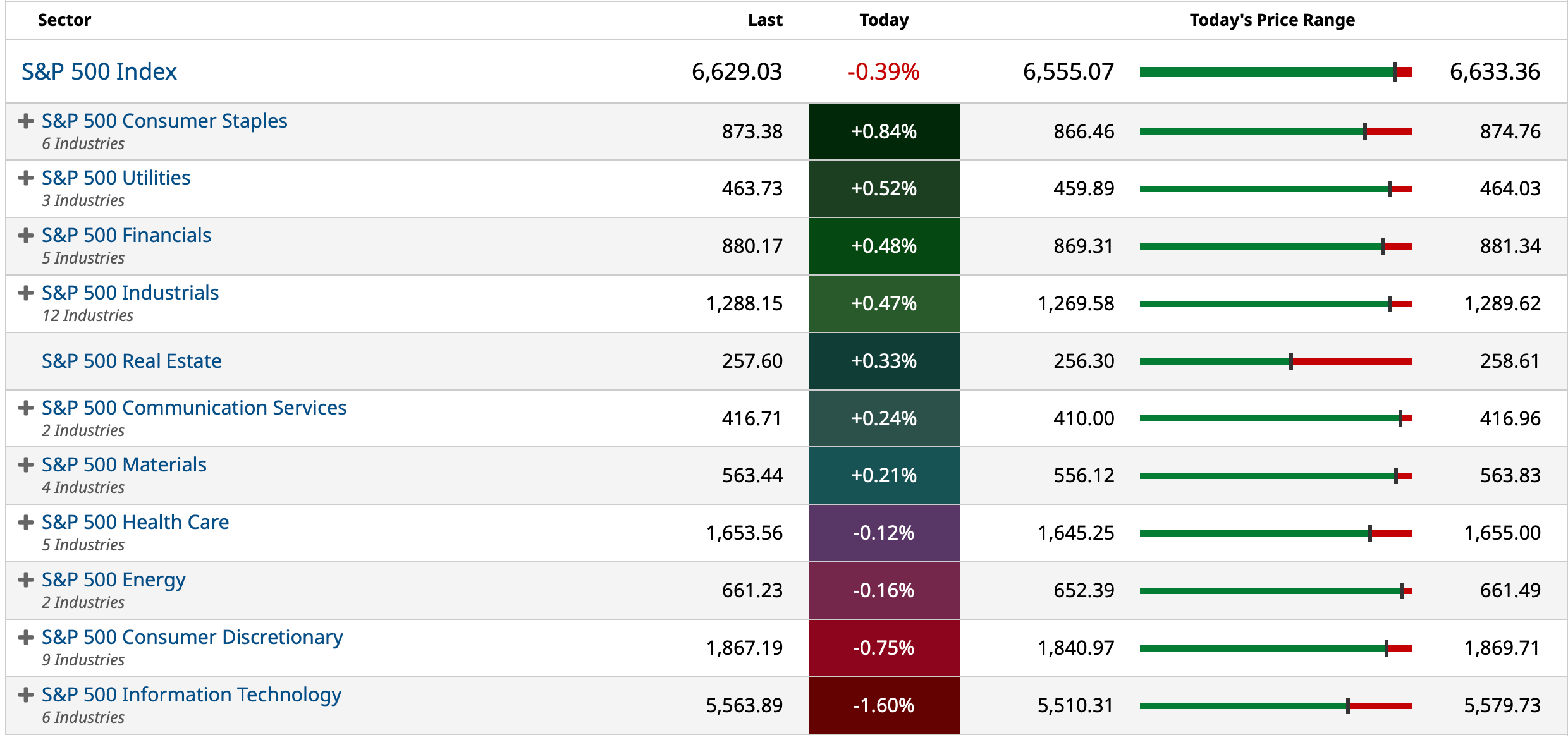

Sectors

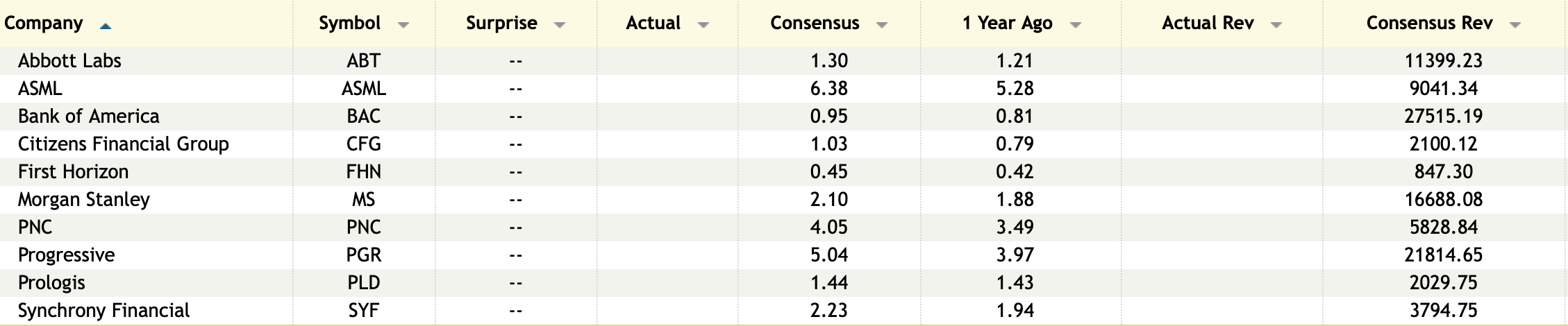

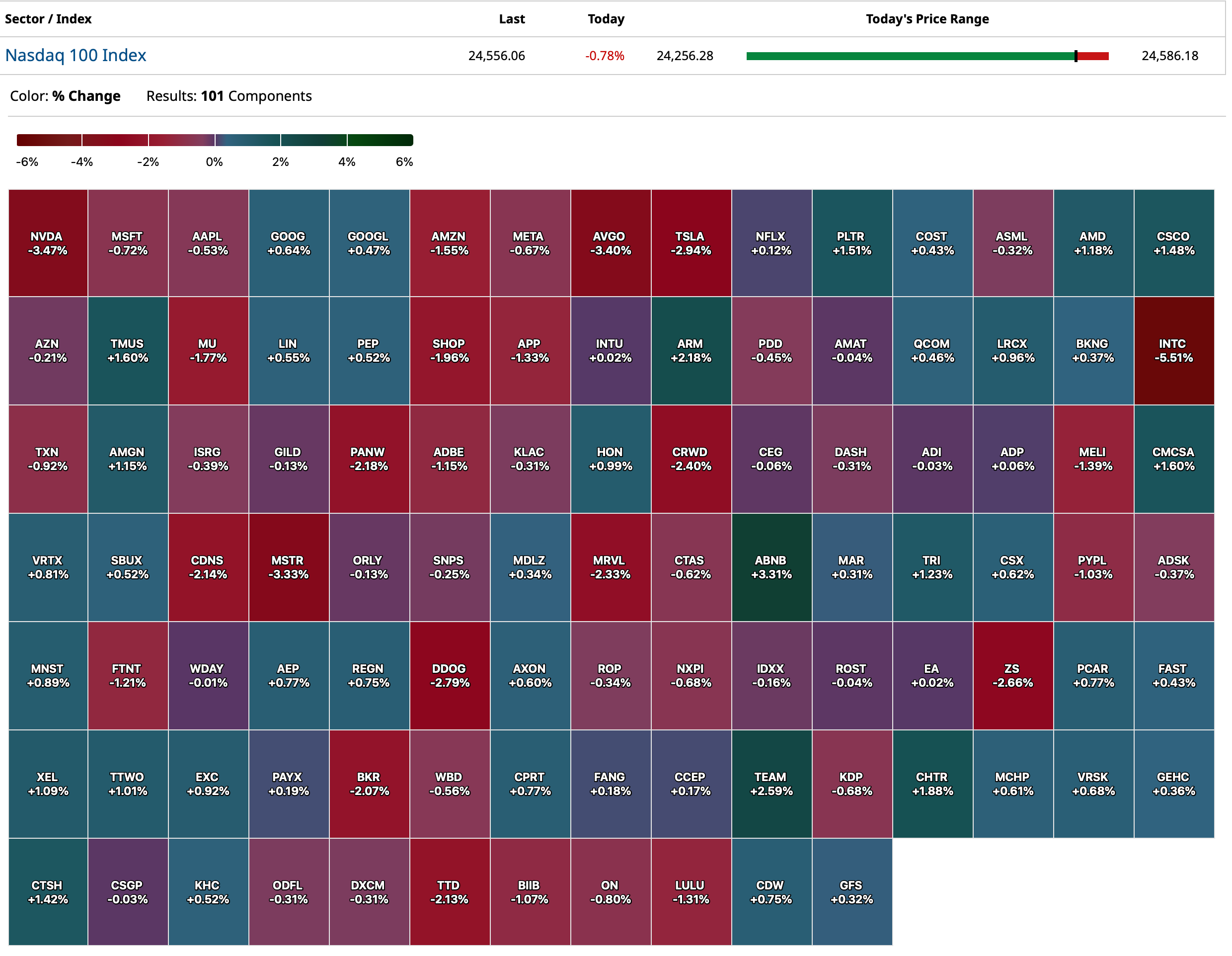

% Movers

BY Doug Kass · Oct 14, 2025, 4:36 PM EDT

BY Doug Kass · Oct 14, 2025, 4:36 PM EDT

With S&P cash -22 handles I am covering my short index positions:

* (SPR) $660.66

* (QQQ) $596.71

BY Doug Kass · Oct 14, 2025, 3:53 PM EDT

More China tariff talk out of President Trump.

I covered my trading short rental in JPMorgan Chase under $102 for a quick profit.

BY Doug Kass · Oct 14, 2025, 3:51 PM EDT

BY Doug Kass · Oct 14, 2025, 3:18 PM EDT

I'm back short (JPM) at $304.71.

BY Doug Kass · Oct 14, 2025, 2:38 PM EDT

From Peter Boockvar:

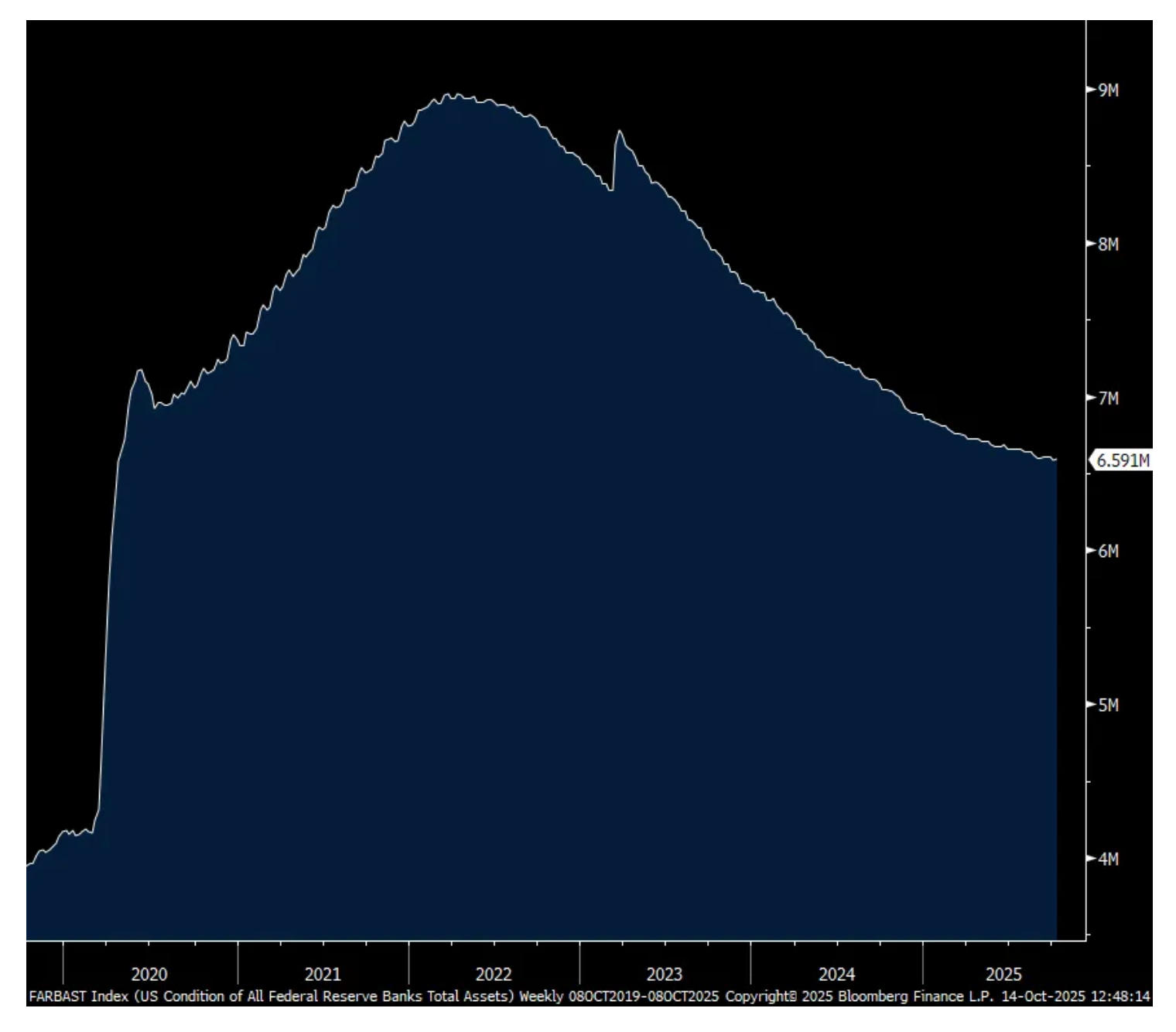

The end of QT is upon us, said Jay Powell

The most noteworthy commentary from Jay Powell’s speech in front of the NABE was on the Fed balance sheet where its Treasury holdings have been shrinking by just $5b per month while its holdings of MBS have been reduced by $35b (at least that is the plan though each month varies).

He said it’s about time to stop reducing its size which stands now at about $6.6 Trillion which is 58% bigger than where it stood at the beginning of 2020. For perspective, nominal GDP has risen by 39%. If the Fed’s balance sheet grew in line with the economy, it would need to shrink by about another $800b. But that is apparently not going to be the case. He also defended the use of QE but it’s clear they went too hog wild with it, especially with MBS purchases that gave us a 50% rise in home prices over 5 years.

He said specifically, “Our long-stated plan is to stop balance sheet runoff when reserves are somewhat above the level we judge consistent with ample reserve conditions. We may approach that point in coming months, and we are closely monitoring a wide range of indicators to inform this decision.”

When asked about when the Fed would stop reducing the size of its balance sheet and where the right level of bank reserves should be, he always said in the past, "We’ll know it when we see it,” I paraphrase. Well, they are now seeing it as “Some signs have begun to emerge that liquidity conditions are gradually tightening, including a general firming of repo rates along with more noticeable but temporary pressures on selected dates.”

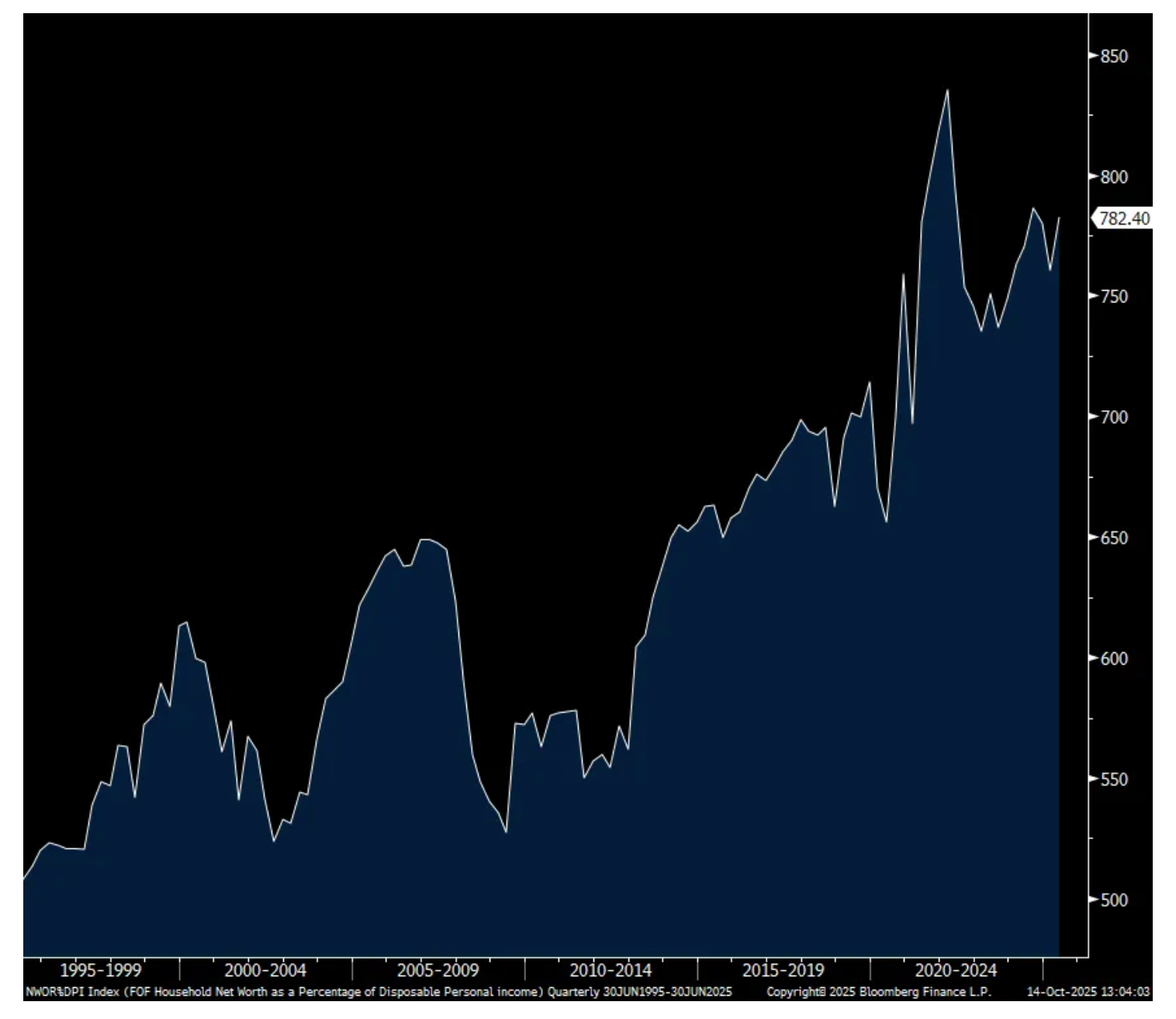

Bottom line, QT is about to end, and has essentially already ended for Treasuries and why there was no response today in the market to what he said. We’ll see if spreads between Treasuries and MBS tighten from here. I think QE (and saying nothing new from me), outside of the 2008-2009 experience with its use, has been a very dangerous use of monetary policy that has resulted in the unaffordability of housing for many (which followed the experiment of a 1% fed funds rate in the early to mid 2000’s that resulted in the obvious) and bubbles in various asset prices that has brought the net worth as a percent of disposable income to 782% as of Q2 2025. That compares with 614% in Q1 2000 and 649% in Q1 2007. Steve Eisman years ago poetically referred to QE as ‘monetary policy for rich people.’ What an incredible ride for asset and home owners but what a tough road it’s been for everyone else.

Fed’s Balance Sheet

Net Worth as a % of Disposable Income

BY Doug Kass · Oct 14, 2025, 1:56 PM EDT

I'm now back to medium sized short the indices:

* (SPY) $664.84

* (QQQ) $601.91

BY Doug Kass · Oct 14, 2025, 1:05 PM EDT

I'm adding to my index shorts — now small sized (up from very small):

* (SPY) $662.10

* (QQQ) $599.23

Short SPY S QQQ S

BY Doug Kass · Oct 14, 2025, 12:00 PM EDT

With S&P cash - 23 handles, I am reshorting the indices:

* (SPY) $660.88

* (QQQ) $597.79

BY Doug Kass · Oct 14, 2025, 11:50 AM EDT

- NYSE volume 12% below its one-month average

- NASDAQ volume 2% below its one-month average

- VIX index: up 9.09% to 20.76

BY Doug Kass · Oct 14, 2025, 11:45 AM EDT

Wolf Street howls about the blowing off of the debasement trade.

BY Doug Kass · Oct 14, 2025, 11:35 AM EDT

Howard Marks' commentary over the years.

BY Doug Kass · Oct 14, 2025, 10:52 AM EDT

From Peter Boockvar:

Political challenges for the LDP President Takaichi in stepping into the Prime Minister role resulted in a rally in JGB’s and a selloff in Japanese stocks, though the yen is slightly higher. And in response to the port fees the US is about to start charging Chinese shipping companies, China is sanctioning five US divisions of the South Korean shipbuilder Hanwha Ocean. Fun times.

That Asian bond rally by the way spilled over to European bonds and a reason why the US 10 yr yield is down at 4-4.01%. Helping too with the bond rise in Europe was a 4 yr high seen in the UK unemployment rate at 4.8% thru August and where gilt yields are down the most in the region. Also, jobless claims in the UK rose in September. The pound is weaker.

The September Cass Freight shipments index rose 1.5% m/o/m seasonally adjusted after it fell by 1.5% in August. Versus last year shipments were down by 5.4%. Cass said “For the second straight month, truckload volumes rose slightly within the data, but LTL volumes declined. We think the LTL declines reflect ongoing available TL capacity—where low rates lead shippers to consolidate LTL loads into truckloads—and private fleet insourcing. The positivity in TL volumes may be temporary, as pre-tariff shipping may lead to more air pockets in demand.”

And, “Just as we correctly expected tariff reprieves to support a recovery in September volumes, we also expect tariffs to result in volume declines and additional softness as price increases reduce affordability and impact spending.”

Speaking of the stuff that Cass customers transport, this is what Fastenal had to say about the state of the industrial and manufacturing sector that they sell into:

“I think the big takeaway is our underlying growth remained strong and steady...And when we’re looking at where the growth came from, the broader market wasn’t much help. Now, the industrial economy remained sluggish, essentially flat. I think the PMI averaged about 48.6 in the quarter, which indicates contraction, but I think I’d characterize our growth as mostly self-help and market share gains rather than any particular macro lift.”

“Pricing did contribute roughly 2.5 percentage points to growth.” And from here, “Additional pricing actions will be necessary in the fourth quarter of 2025, with the potential to increase the impact of pricing on like-for-like parts to be in a range of 3.5% to 5.5%, depending on where the tariff litigation ultimately settles and the pace and execution of our actions.”

Here was more commentary on tariffs. “Year-to-date, significant tariffs have been applied to products from China, as well as steel, including steel-derived products likes fasteners on a global basis. We continue our long term trend on diversifying our supply chain where possible to the size and timing of our suppliers’ pricing actions, and we added some inventory to our own balance sheet. That said, supply chains have gotten more expensive and a part of our response over time has been incremental pricing. We have been proactively engaging with our customers for several months.”

From Jamie Dimon and his quick take on the macro in the JP Morgan press release:

“While there have been some signs of a softening, particularly in job growth, the US economy generally remained resilient. However, there continues to be a heightened degree of uncertainty stemming from complex geopolitical conditions, tariffs and trade uncertainty, elevated asset prices and the risk of sticky inflation. As always, we hope for the best, but these complex forces reinforce why we prepare the Firm for a wide range of scenarios.”

The stock trades at an amazingly expensive 3x tangible book value but there is no one better than Dimon in running a bank, as we know.

We’ll hear more in the call but they did raise their provision for credit losses and net-charge offs “predominantly driven by Wholesale and Card services.”

From Charlie Scharf at Wells Fargo who said something similar to Dimon:

“While some economic uncertainty remains, the US economy has been resilient and the financial health of our clients and customers remains strong. Spending on debit and credit cards continued to increase, auto loan originations had strong growth from a year ago, and total client assets in our Wealth and Investment Management business continued to grow. We grew fees from investment banking and trading and our commercial loan balances continued to grow.”

Their provision for loan losses came in well below expectations and “included a decrease in the allowance reflecting improved credit performance and lower commercial real estate loan balances, partially offset by higher commercial and industrial, auto, and credit loan balances.”

With now a big focus on the auto lending business, on the heels of Tricolor, what CarMax said a few weeks ago and the blow up of First Brands, Wells said they saw “higher auto net loan charge-offs.”

Domino’s Pizza slightly beat both top and bottom line estimates and said this in their release:

“In the US, we drove positive order counts behind our Best Deal Ever promotion and stuffed crust pizza product innovation for the third quarter. This resulted in another quarter of strong growth in both our delivery and carryout businesses.”

Volume helped but so did “an increase in the Company’s food basket pricing to stores, which increased 3.3% during the third quarter of 2025” y/o/y.

The industrial policy of trying to force feed EVs into all of our garages continues to unravel with a $1.6b charge that GM is announcing relating to its EV business and in reducing production.

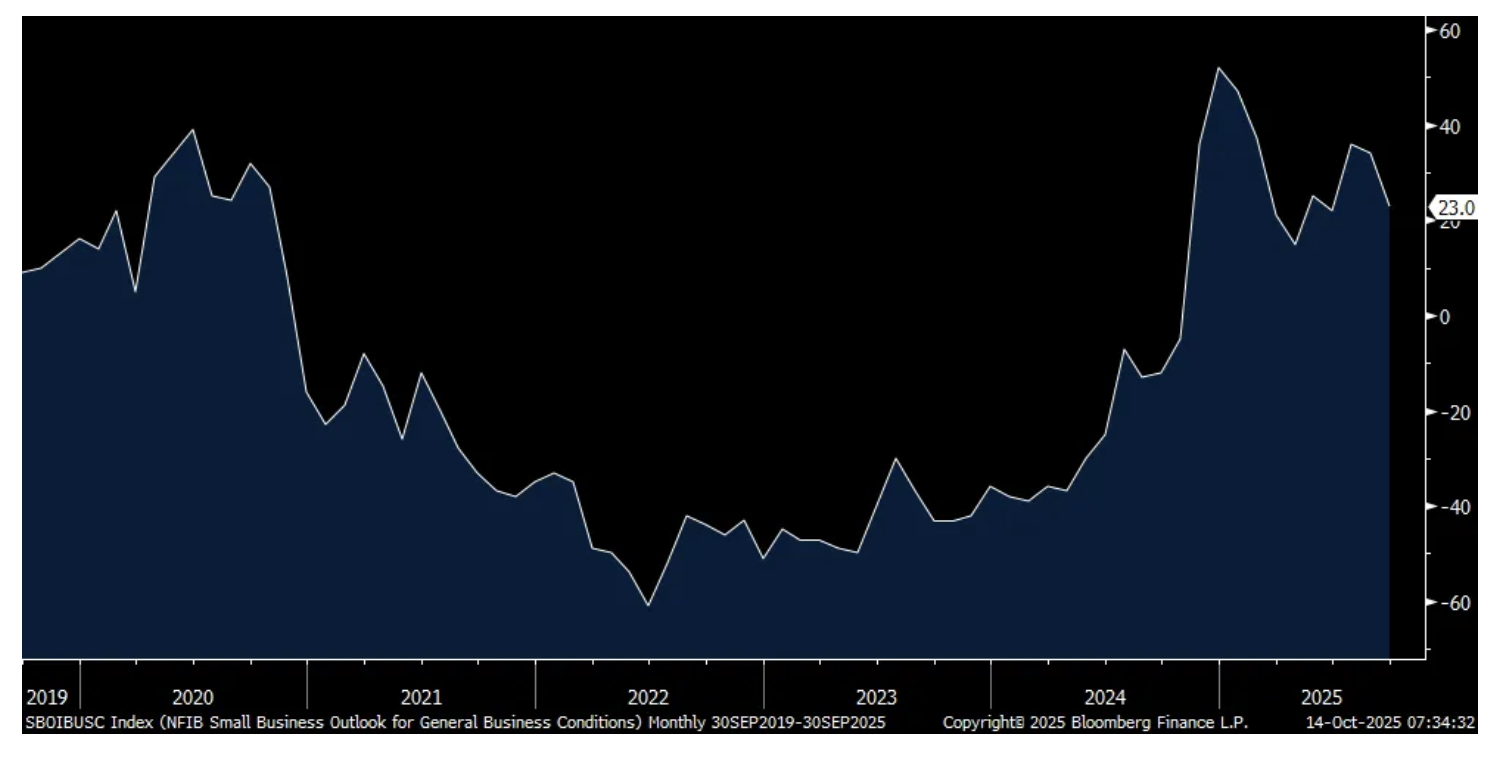

I’ll finish up with the September NFIB Small Business Optimism index which fell 2 pts m/o/m to 98.8. The internals were mixed. Interestingly as the Fed is worried about the labor market, Plan to Hire rose 1 pt to 16%, the highest since January. Current compensation plans were up by 2 pts to a 3 month high but slipped 1 pt for future comp plans though after rising by 3 pts last month.

The expectation components were all weak. Those that Expect a Better Economy fell 11 pts and Expect Higher Sales were down by 4. Those that said it’s a Good Time to Expand was lower by 3 pts.

Those who increased Capital Spending was unchanged at 21% and there was no change either for Plan to Increase Inventory. Expected earnings remained negative at -16 but 3 pts better than August.

Higher selling prices rose 3 pts after falling by 3 pts last month. And “A net 31% plan to increase prices over the next three months, up 5 points from August.” There was also a 3 point rise from August to 14% of owners reporting that “inflation was their single most important problem in operating their business (higher input costs).”

Of note too, “64% of small business owners reported that supply chain disruptions were affecting their business to some degree, up 10 points from August.”

Tariffs are a real challenge for small businesses and taxes now equal labor quality as their biggest challenge, though labor was down 3 pts.

The NFIB’s bottom line was this, “Optimism among small business owners decreased in September. While most owners evaluate their own business as currently healthy, they are having to manage rising inflationary pressures, slower sales expectations, and ongoing labor market challenges. Although uncertainty is high, small business owners remain resilient as they seek to better understand how policy changes will impact their operations.”

NFIB

Plans to Hire

Expect a Better Economy

Pricing Plans in Coming Three Months

BY Doug Kass · Oct 14, 2025, 10:25 AM EDT

11 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasury hosts a $86B 3 and $77B 6-Month Bill Auction;

1 p.m.: Treasury hosts a $95B 6-Week Bill Auction

Early Morning: Fed Bank of Chicago Goolsbee (Voter) Podcast Appearance -- You Might Be Right;

8:45 a.m.: Fed Vice Chair for Supervision Bowman (Voter, Dove) participates in discussion before the 2025 Institute of International Finance Annual Membership Meeting, Washington, DC (Topic TBA. No text. Q&A from moderator);

10 a.m.: Federal Reserve Board of Governors Meeting: Periodic Briefing and Discussion on Financial Markets, Institutions, and Infrastructure;

12:20 p.m.: US Fed Chair Powell speaks on the economic outlook and monetary policy before the National Association for Business Economics Annual Meeting, Philadelphia, PA (Text available. Q&A from moderator);

3:25 p.m.: Fed Board Governor Waller (Voter) participates in "Payments" discussion before the 2025 Institute of International Finance Annual Membership Meeting, Washington, DC (No text. Q&A from moderator)

3:30 p.m.: Fed Bank of Boston President Collins (Voter) speaks and participates in a moderated question-and-answer session before the Greater Boston Chamber of Commerce, Boston, MA (Livestream at bostonfed.org. Advance text available. No audience Q&A. No media Q&A)

BY Doug Kass · Oct 14, 2025, 10:03 AM EDT

BY Doug Kass · Oct 14, 2025, 9:25 AM EDT

-ELAB +109% (momentum)

-AQMS +90% (momentum)

-ATXS +44% (BioCryst to acquire Astria Therapeutics at $13.00/shr at EV $920M)

-CRML +36% (rare earth and minerals broadbased strength amid US/China trade tensions)

-NVTS +32% (supports 800 VDC Power Architecture for NVIDIA’s Next-Generation AI Factory Computing Platforms)

-REKR +12% (reports prelim Q3 revenue)

-RCKT +11% (US FDA accepts BLA Resubmission of KRESLADI for Treatment of Severe Leukocyte Adhesion Deficiency-I (LAD-I))

-USAR +11% (rare earth and minerals broadbased strength amid US/China trade tensions))

-ACI +7.2% (earnings, guidance; announces $750M accelerated share repurchase agreement)

-CALC +7.0% (announce collaboration with Telperian to Integrate Innovative Artificial Intelligence Engine to Analysis of Clinical Trials of Auxora)

-PII +6.8% (reports prelim Q3; to separate Indian Motorcycle into a Standalone Company, will sell majority stake to Carolwood LP)

-MP +6.7% (rare earth and minerals broadbased strength amid US/China trade tensions)

-BNZI +6.1% (announces Institutional Investor Increases Direct Equity Stake to 18.7% following Exercise of Warrants for 1.2M shares)

-PCH +5.7% (reportedly Rayonier and PotlatchDeltic plan to combine in an all-stock deal)

-DPZ +4.1% (earnings)

-VOR +3.8% (Telitacicept Demonstrates Clinically Meaningful and Statistically Significant Impact on ESSDAI Compared to Placebo in Late-Breaking China Phase 3 Results in Primary Sjögren’s Disease at ACR 2025)

-RNAZ +3.6% (preliminary data from completed Phase 1a study with TTX-MC138 in metastatic disease achieved Safety primary endpoint)

-AMD +3.2% (Oracle and AMD expand partnership)

-WFC +2.7% (earnings, guidance)

-BCRX -7.5% (BioCryst to acquire Astria Therapeutics at $13.00/shr at EV $920M)

-MBOT -4.7% (files for 14.7M common share offering)

-SOTK -3.8% (earnings, guidance)

-RIO -2.4% (reports Q3 production)

-GS -2.2% (earnings)

-GM -2.1% (records $1.6B EV realignment charges; Strategic shift slows EV expansion; See's EV adoption rate to slow)

BY Doug Kass · Oct 14, 2025, 9:10 AM EDT

BY Doug Kass · Oct 14, 2025, 8:59 AM EDT

BY Doug Kass · Oct 14, 2025, 8:40 AM EDT

* The interconnected AI deal making biz continues....

Break in!

Taylor Swift and Open AI have announced a strategic partnership to deploy at least 10 gigawatts of Nvidia systems for OpenAI's next generation AI infrastructure. Taylor plans to invest up to $10 billion in OpenAI (over the next 20 years) and the project aims to create AI factories capable of supporting OpenAI's large-scale AI models and, of course, to facilitate the release of all new Taylor Swift albums going forward.

In response, Taylor Swift has sold the rights to all of her music to Coreweave for an astounding $7.5 billion. In turn, Coreweave is selling Nvidia a convertible bond (0.25% interest rate, with a conversion premium of 55%) exchangeable into Taylor Swift's music rights.

Taylor Swift and OpenAI's Sam Altman will appear on CNBC's Squawk Box this morning at 8 to further discuss the transaction and to announce that Taylor Swift will perform at the 2027 Nvidia Super Bowl Halftime Show. (In celebration, Andrew Sorkin, Joe Kernen and Becky Quick all plan to be dressed in red on Squawk Box)

BY Doug Kass · Oct 14, 2025, 8:20 AM EDT

Leverage allows the use of a small, initial "investment" to produce a magnified output.

Stated simply, leverage amplifies gains AND losses.

Why anyone would think the rank speculation (and excessive leverage) is confined to just crypto is beyond me.

"Leverage: don't make deals without it. Enhance."

- Donald Trump (Trump: The Art of the Deal)

It is in all asset classes to varying degrees.

From Bloomberg:

A $131 Billion Crypto Crash Has Traders Fearing Lasting Damage

By Olga Kharif

Read more: Crypto’s Biggest Crash Reveals a Market Littered With Pitfalls

Here is the column I wrote at the end of last week in which I issued a warning about the systemic risks associated with a levered crypto currency market:

A thought for the weekend.

I think the biggest risk is the circularity.

The whole market is like bowling pins with bitcoin on of the most important pins.

Huge behind-the-line leverage.

Think MicroStrategy (MSTR) .

Position: Short MSTR (VS)

By Doug Kass Oct 10, 2025 2:45 PM EDT

BY Doug Kass · Oct 14, 2025, 7:00 AM EDT

BY Doug Kass · Oct 14, 2025, 6:32 AM EDT

The S&P Short Range Oscillator is at -1.07% vs. -2.39% — that is moving back towards neutral.

BY Doug Kass · Oct 14, 2025, 5:55 AM EDT

* Out of index shorts on early morning (4:50 AM) weakness...

With S&P futures -59 handles I am hitting the cash register.

I have covered all of yesterday's index shorts for a quick and nice gain:

* (SPY) $657.46

* (QQQ) $595.41

From Monday:

* Thus far...

These are today's things:

* Re-established index shorts — (SPY) at $662.26 and (QQQ) at $600.63.

* Added to (GRNY) short at $25.27.

* Day traded (AVGO) (short then cover on opening gap) for a quick profit. (Didn't report because he happened too fast!)

* Added to (MSOS) long at $4.98.

Position: Short SPY (VS), QQQ (VS), GRNY (VL)

By Doug Kass Oct 13, 2025 10:53 AM EDT

BY Doug Kass · Oct 14, 2025, 5:45 AM EDT