100%

Break in!

President Trump to impose additional 100% tariff on China effective November 1.

BY Doug Kass · Oct 10, 2025, 4:59 PM EDT

Break in!

President Trump to impose additional 100% tariff on China effective November 1.

BY Doug Kass · Oct 10, 2025, 4:59 PM EDT

Another housekeeping item.

I covered my (AMD) trading short rental at $215 at the close.

BY Doug Kass · Oct 10, 2025, 4:50 PM EDT

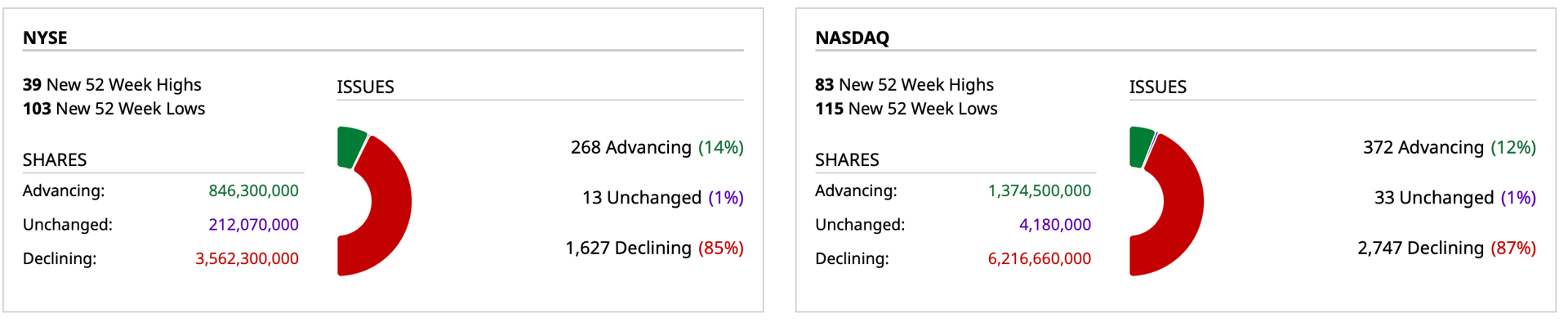

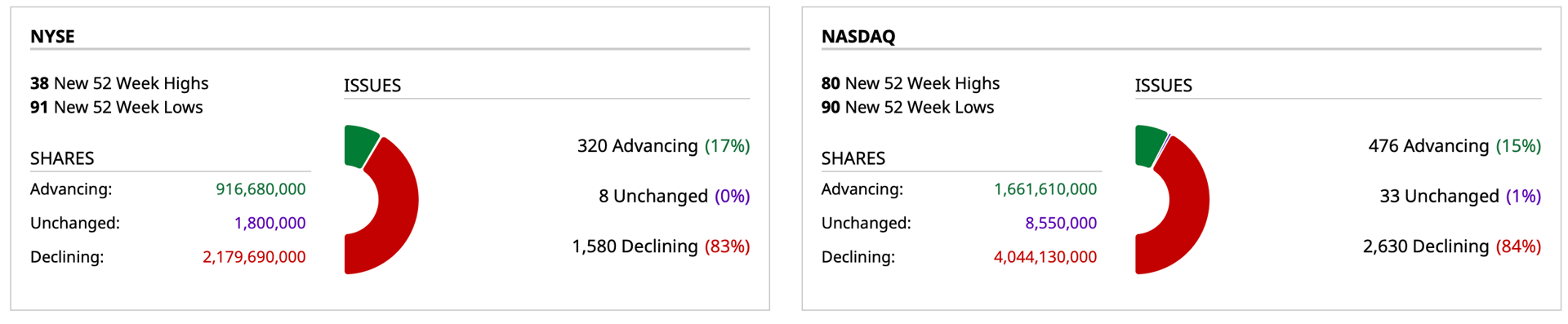

- NYSE volume 26% above its one-month average

- NASDAQ volume 19% above its one-month average

- VIX index: up 32.62% to 21.79

BY Doug Kass · Oct 10, 2025, 4:42 PM EDT

A thought for the weekend.

I think the biggest risk is the circularity.

The whole market is like bowling pins with bitcoin on of the most important pins.

Huge behind-the-line leverage.

Think MicroStrategy (MSTR) .

BY Doug Kass · Oct 10, 2025, 2:45 PM EDT

I am calling it a day early as I tested positive for Covid this morning.

Thanks for reading my Diary.

Enjoy the weekend.

Be safe.

BY Doug Kass · Oct 10, 2025, 2:30 PM EDT

BY Doug Kass · Oct 10, 2025, 2:05 PM EDT

I bought small (MSOS) at $4.95 and some cheap calls.

We are moving ever closer to weed rescheduling and wouldn't it be nice if President Trump called for it at today's 5 PM announcement at the White House?

I actually am hearing that the announcement relates to drug pricing.

That said, sometime during this budget fight with the opposing party one would think the president would love to announce rescheduling of cannabis to throw it in the Democrats faces.

BY Doug Kass · Oct 10, 2025, 1:52 PM EDT

Scott Galloway's No Mercy No Malice ... "Love Algorthmically"

BY Doug Kass · Oct 10, 2025, 1:05 PM EDT

I covered my Starbucks (SBUX) short at $79.40 for a healthy profit today.

BY Doug Kass · Oct 10, 2025, 12:40 PM EDT

From Peter Boockvar:

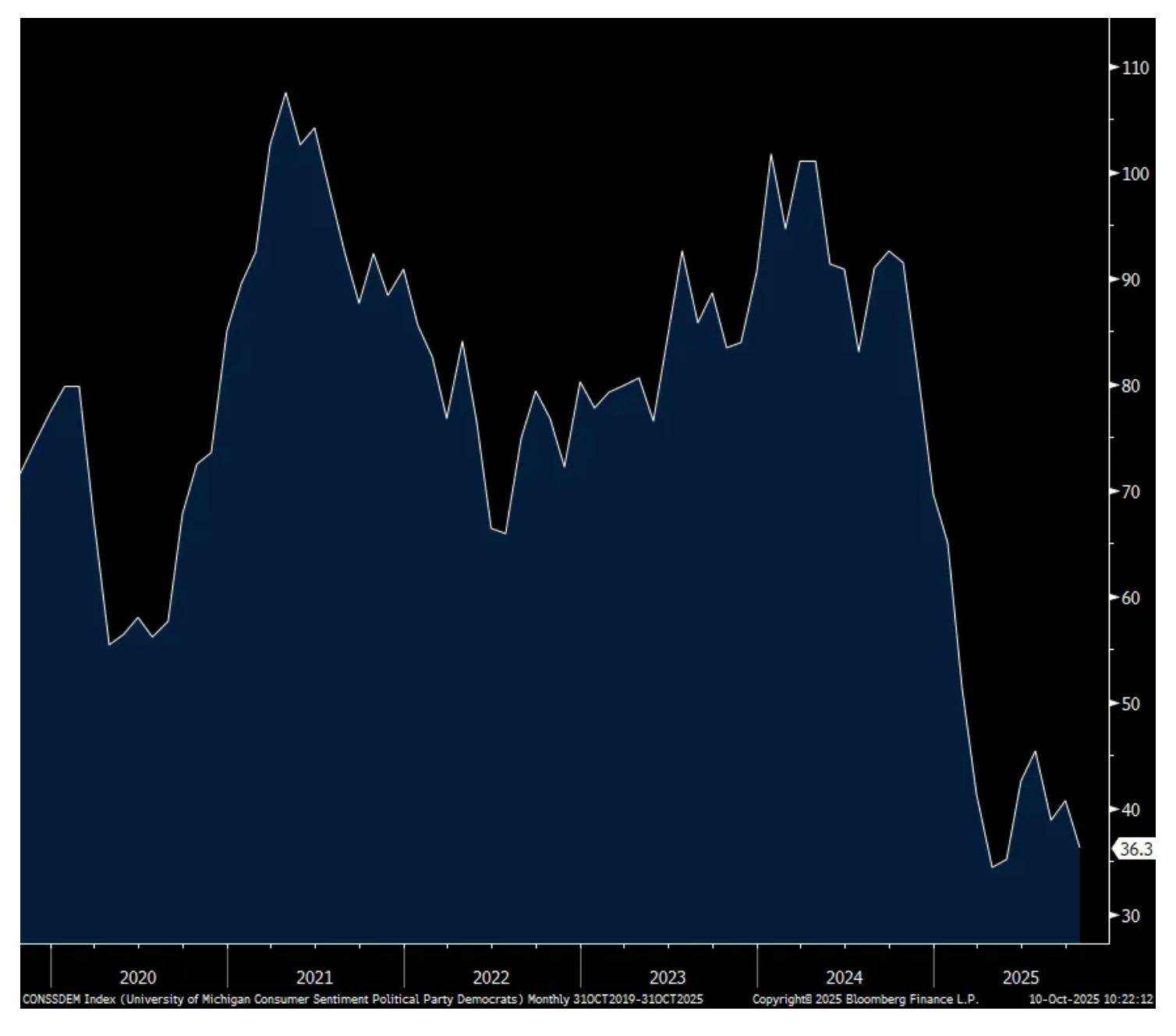

Consumer confidence remains muted in aggregate but quite splintered politically

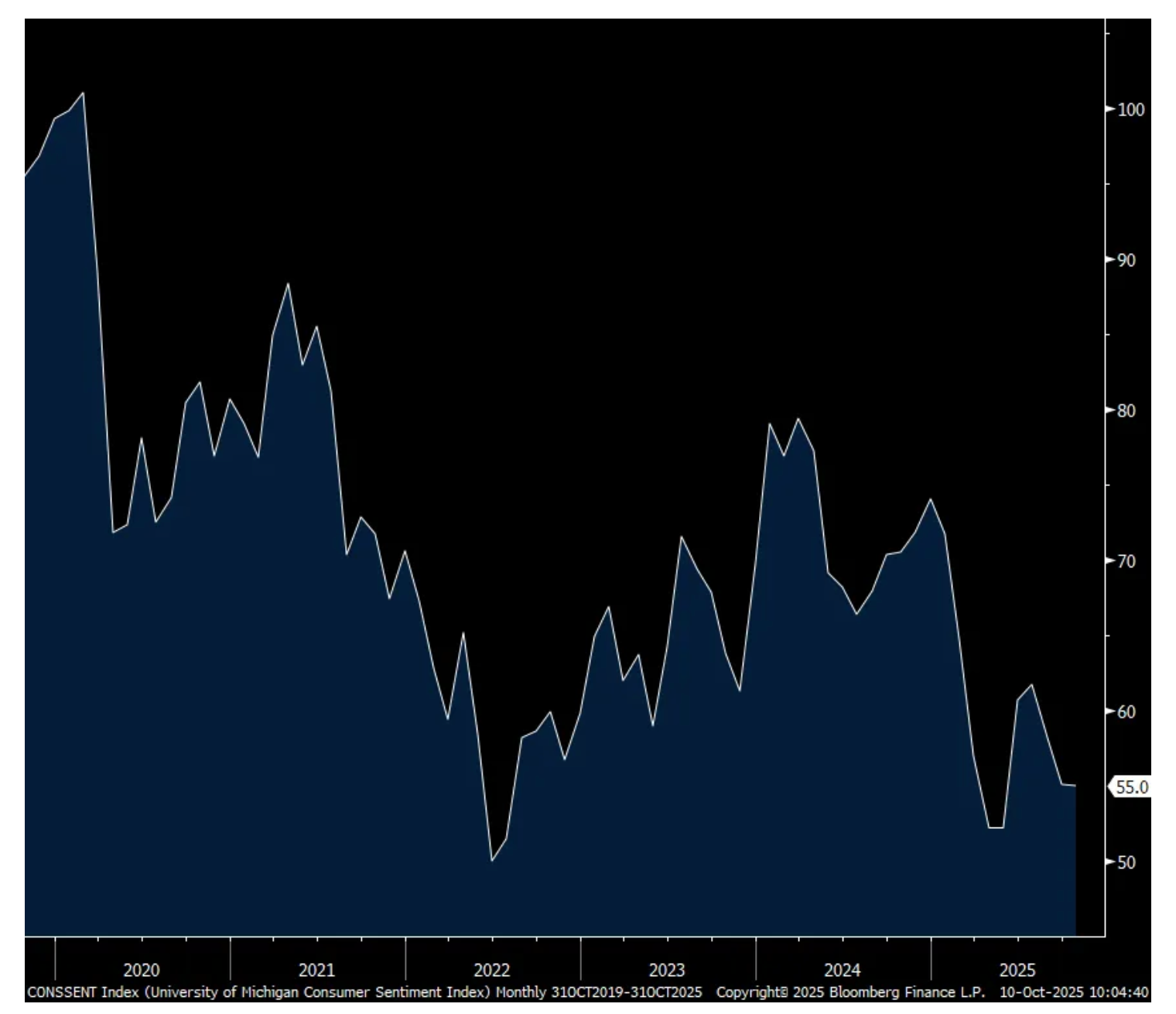

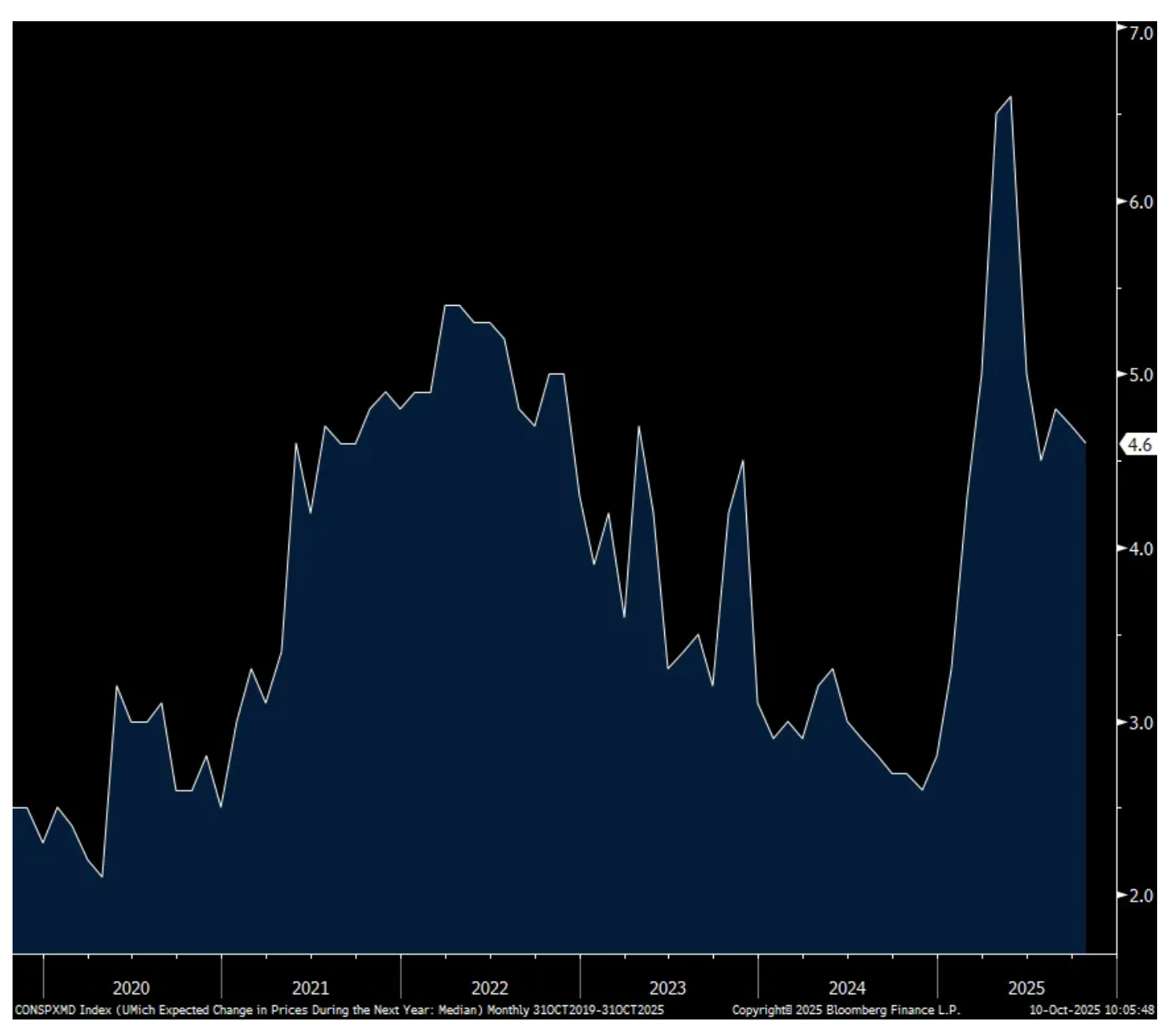

The initial October UoM consumer confidence index was little changed at 55 vs 55.1 in September, still bouncing along the post Covid bottom but was 1 pt above the estimate. For perspective, it’s the softest since May and compares to the 71.7 seen in January. The internals were mixed as there was a modest uptick in Current Conditions, up by .6 while there was a similar drop, by .5 pt, in Expectations. One year inflation expectations fell one tenth m/o/m to 4.6% while the 5-10 yr crystal ball guess held at 3.7%.

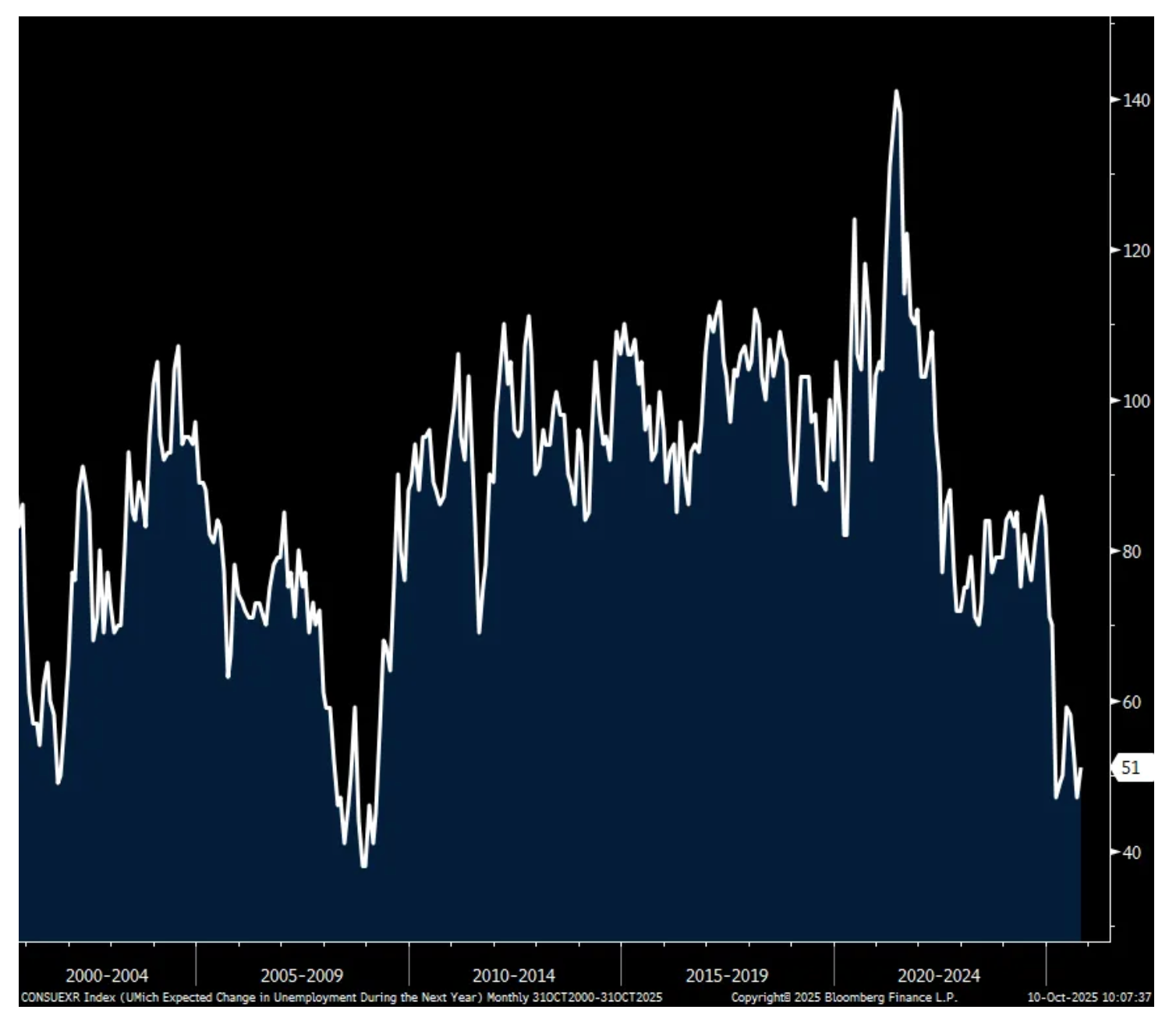

After falling by 5 pts last month to match the weakest since 2009, the employment component improved by 4 pts. After two months of below zero prints at -3, the income component rose 4 pts to +1.

With respect to buying intentions, they rose 5 pts to 35 for ‘Good Time to Buy a House’ with likely the help of lower mortgage rates. It was though at 40 in July. The desire to buy a car/truck rose 2 pts to 52 after falling by 1 pt in September. It was 56 in July. Interest in buying a major household item dropped 4 pts to 74, the lowest since November 2022.

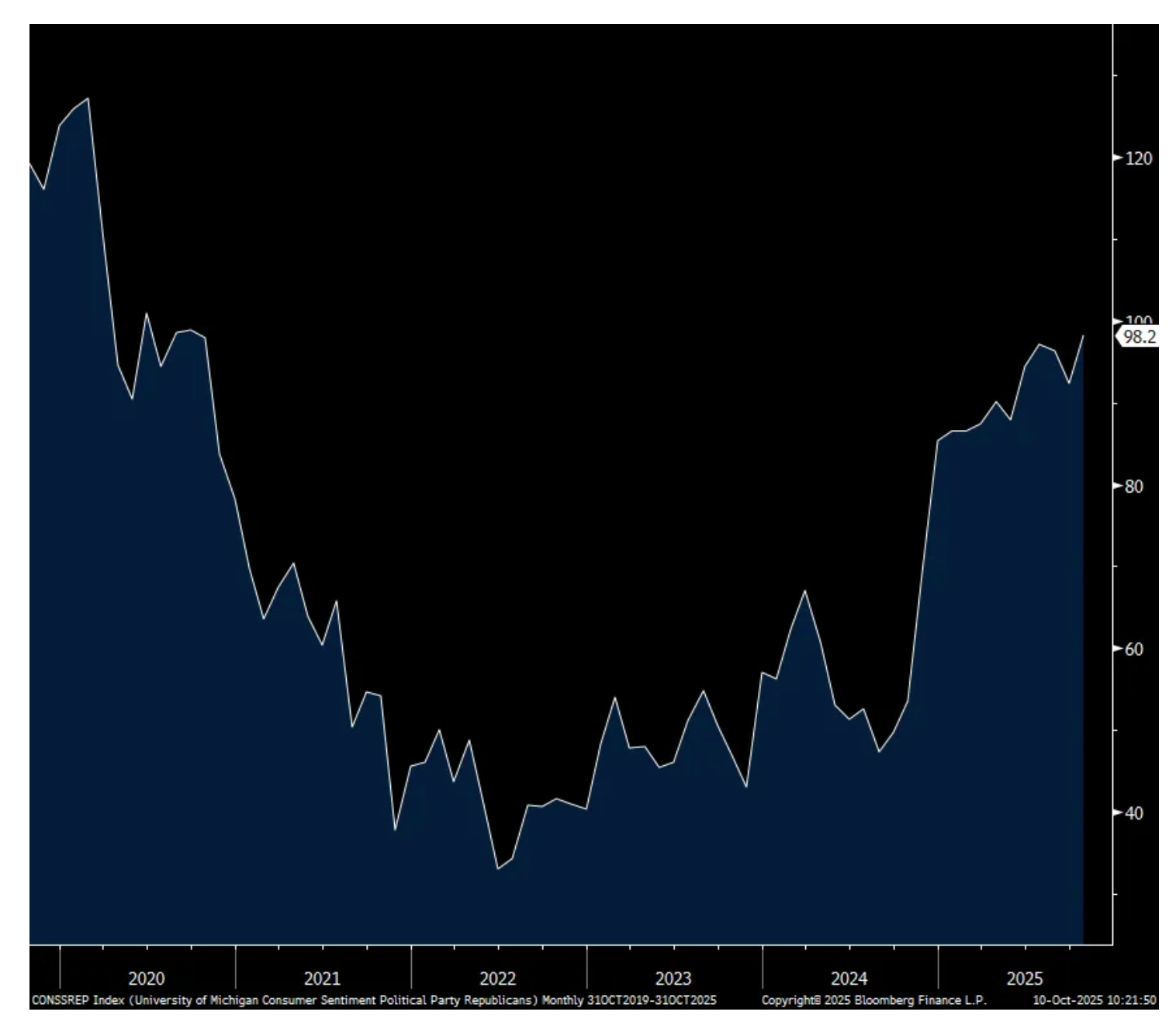

The political flow thru in this data point was obvious again as the confidence of Republicans rose to the highest level since September 2020 at 98.2 while for Democrats, they fell to just 36.3, near the lowest since party affiliations were asked about in 2006. Talk about a splintered populace and we thus must take this into account when reading through this data.

The bottom line from the UoM, “Overall, consumers perceive very few changes in the outlook for the economy from last month. Pocketbook issues like high prices and weakening job prospects remain at the forefront of consumers’ minds. At this time, consumers do not expect meaningful improvement in these factors. Meanwhile, interviews reveal little evidence that the ongoing federal government shutdown has moved consumers’ views of the economy thus far.”

On inflation, “About 45% of consumers spontaneously mentioned that high prices are eroding their personal finances, little changed since August and comparable to last October’s 43%. A solid 26% of consumers spontaneously referenced food or groceries, primarily in terms of cost considerations, up from 18% last month and above last October’s 23%.”

I have nothing more to add and wish the data wasn’t so polluted by one’s political beliefs.

UoM

One yr Inflation Expectations

Employment

Republicans Confidence

Democrats Confidence

BY Doug Kass · Oct 10, 2025, 12:15 PM EDT

With S&P cash -105 handles I have covered the following financial trading short rentals for profits:

(BAC) $49.17

(BX) $155.52

(C) $94.99

(GS) $766.26

(JPM) $303.78

(KKR) $118.84

(MS) $153.31

(WFC) $78.91

BY Doug Kass · Oct 10, 2025, 11:49 AM EDT

- NYSE volume 8% below its one-month average;

- Nasdaq volume 5% below its one-month average;

- VIX index: down 1.03% to 16.26

BY Doug Kass · Oct 10, 2025, 11:31 AM EDT

I have covered all of my Index shorts on the -60 handle whoosh lower in the S&P futures based on the Trump Truth Social post.

https://truthsocial.com/@realDonaldTrump/posts/115350455734003647

* (SPY) $665.55

* (QQQ) $$604.01

I have also covered (NVDA) $191.79 and (HOOD) $146.01 trading rental shorts.

BY Doug Kass · Oct 10, 2025, 11:17 AM EDT

Donald J. Trump

@realDonaldTrump

Some very strange things are happening in China! They are becoming very hostile, and sending letters to Countries throughout the World, that they want to impose Export Controls on each and every element of production having to do with Rare Earths, and virtually anything else they can think of, even if it’s not manufactured in China. Nobody has ever seen anything like this but, essentially, it would “clog” the Markets, and make life difficult for virtually every Country in the World, especially for China. We have been contacted by other Countries who are extremely angry at this great Trade hostility, which came out of nowhere. Our relationship with China over the past six months has been a very good one, thereby making this move on Trade an even more surprising one. I have always felt that they’ve been lying in wait, and now, as usual, I have been proven right! There is no way that China should be allowed to hold the World “captive,” but that seems to have been their plan for quite some time, starting with the “Magnets” and, other Elements that they have quietly amassed into somewhat of a Monopoly position, a rather sinister and hostile move, to say the least. But the U.S. has Monopoly positions also, much stronger and more far reaching than China’s. I have just not chosen to use them, there was never a reason for me to do so — UNTIL NOW! The letter they sent is many pages long, and details, with great specificity, each and every Element that they want to withhold from other Nations. Things that were routine are no longer routine at all. I have not spoken to President Xi because there was no reason to do so. This was a real surprise, not only to me, but to all the Leaders of the Free World. I was to meet President Xi in two weeks, at APEC, in South Korea, but now there seems to be no reason to do so. The Chinese letters were especially inappropriate in that this was the Day that, after three thousand years of bedlam and fighting, there is PEACE IN THE MIDDLE EAST. I wonder if that timing was coincidental? Dependent on what China says about the hostile “order” that they have just put out, I will be forced, as President of the United States of America, to financially counter their move. For every Element that they have been able to monopolize, we have two. I never thought it would come to this but perhaps, as with all things, the time has come. Ultimately, though potentially painful, it will be a very good thing, in the end, for the U.S.A. One of the Policies that we are calculating at this moment is a massive increase of Tariffs on Chinese products coming into the United States of America. There are many other countermeasures that are, likewise, under serious consideration. Thank you for your attention to this matter!

DONALD J. TRUMP, PRESIDENT OF THE UNITED STATES OF AMERICA

BY Doug Kass · Oct 10, 2025, 11:11 AM EDT

This is why all the press releases and circular deals keep coming. It goes up.

It is amazing the amount of time Jensen and others spend on stock PR these days. Would think he has a business to run? Instead, the appearances on CNBC, road show with investors yesterday when the Investor Relations department should really be doing this stuff, etc.

It is interesting that the CRWV 10b5-1 was tied to stock price targets. Feels to me like a crafty way of arranging for an early unlock. If I read this correctly, Jensen put a new 10b5-1 in place in March, to sell his 6 million shares by the end of this year, not sure exactly what makes that a 10b5-1, but anyway.

The whole industry is quite crafty. The accounting (and depreciation schedules), the circular deals, reporting earnings before expenses, the slides, the promotion, the stock selling, all of it. It is a giant stock promotion operation, around and around we go……

This Bloomberg story addresses the massive insider selling in some of the major technology companies - something that FIN TV never discusses:

By Biz Carson

(Bloomberg) -- Leaders at AI computing company CoreWeave Inc. sold shares worth more than $1 billion after a lockup on the stock lifted in mid-August, putting them among the top 10 individual insider sellers of the third quarter.

It was insiders’ first chance to cash out since CoreWeave’s March initial public offering minted four new billionaires.

Read the rest here: www.bloomberg.com

BY Doug Kass · Oct 10, 2025, 11:05 AM EDT

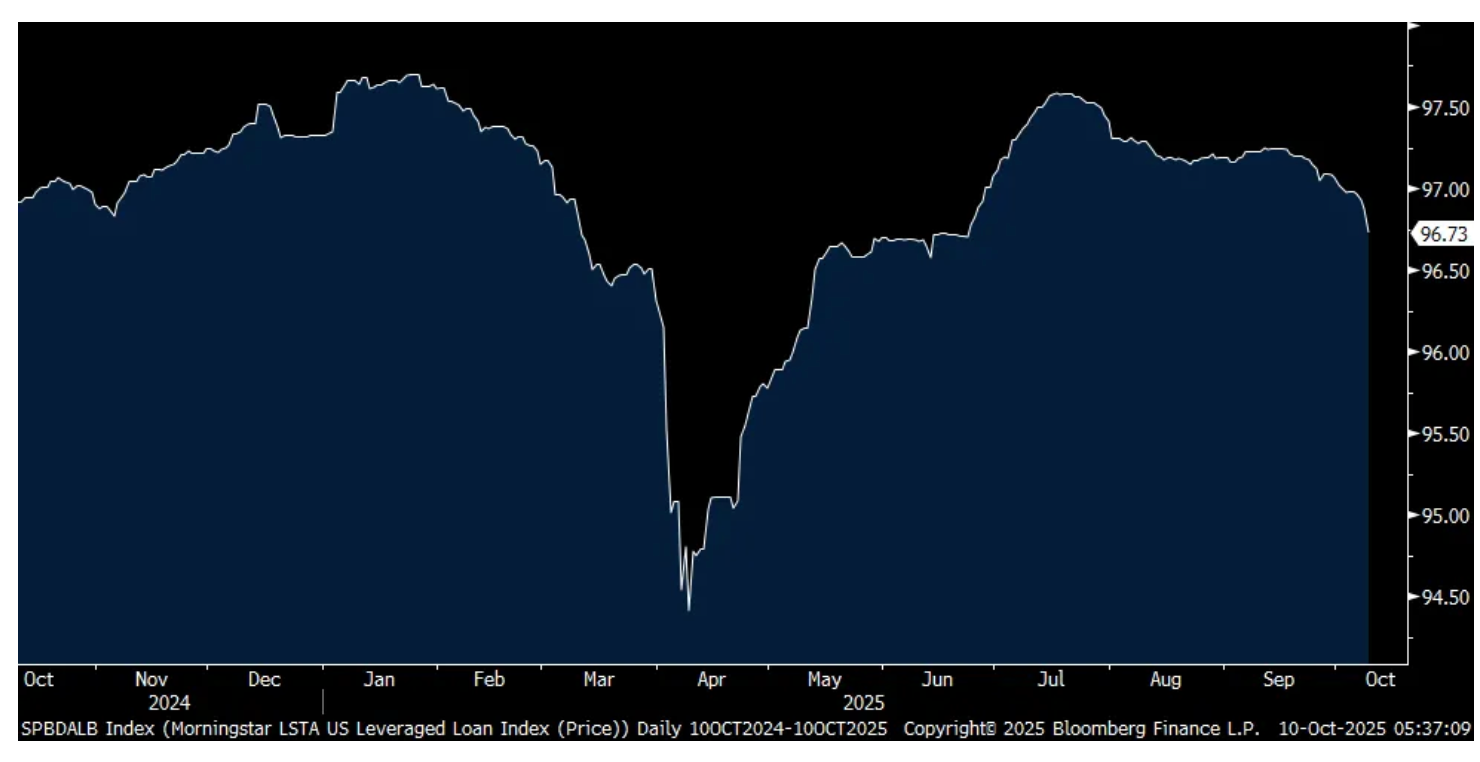

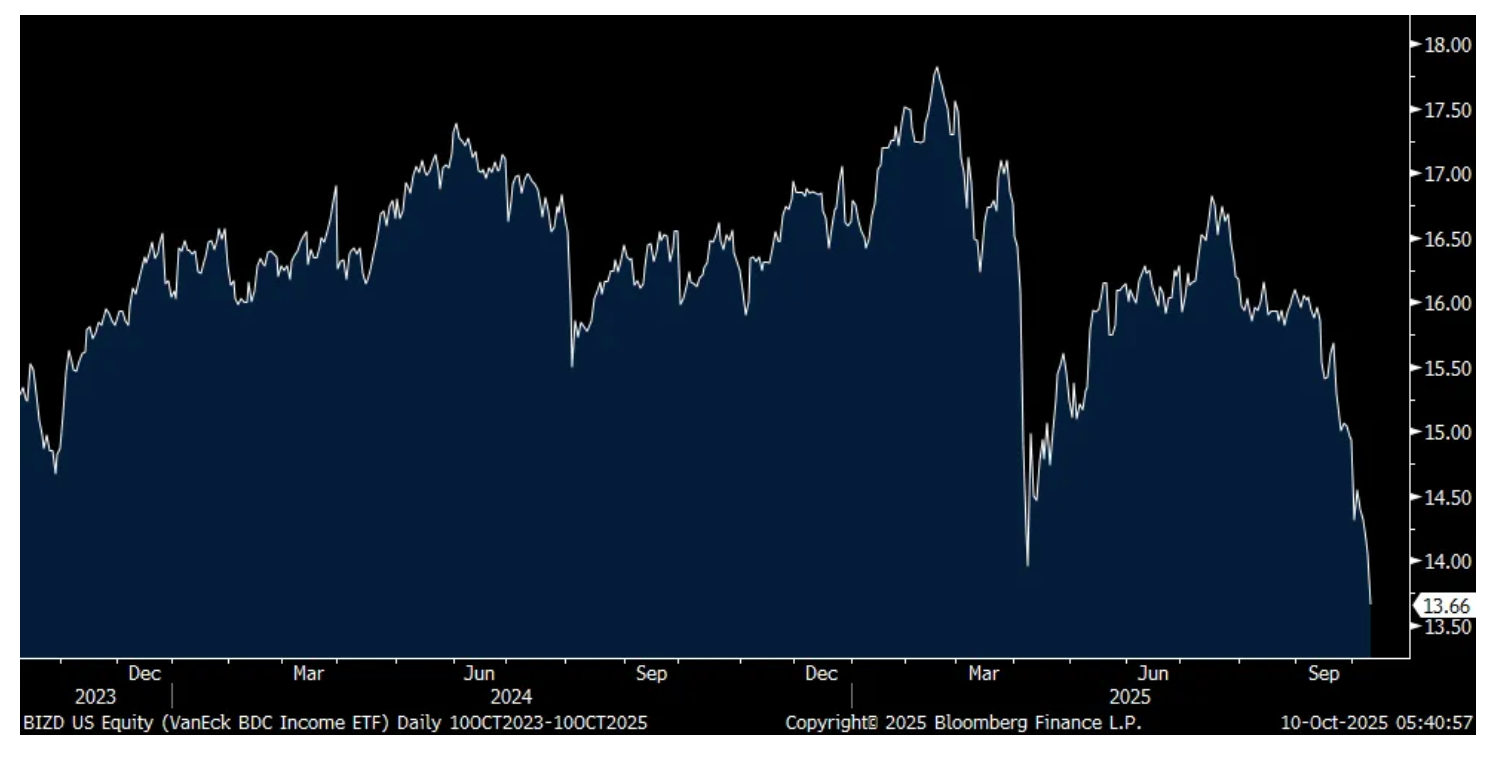

This morning my pal Peter Boockvar observed the continued weakness in LSTA (Leveraged Loan Index) and BIZD (Business Development Companies):

"I’m going to highlight again the LSTA Leveraged Loan Index which had its worst day yesterday since April in percentage terms, down .14%. It’s had two green days over the past month. Coincident with this is the continued weakness in Business Development Company stocks where BIZD is back at the April lows (below it also because of ex dividends). Specifically with the BDC’s, dividends are getting cut because of less interest income due to the Fed rate cuts. On the private side, the private credit monster BCRED from Blackstone cut its dividend last month. Also, there is heightened focus on credit quality in this entire space with the growing use of PIK (payment in kind) interest payments and tight cash flows. Again, something to watch."LSTA Leveraged Loan index

BIZD

In the last few weeks (perhaps owing to the bankruptcies of Tricolor After Tricolor and First Brands’ Collapse, U.S. Banks Face New Scrutiny $1.7 Trillion Worth of Opaque Loans - Barron's and First Brands First Brands: why a maker of spark plugs and wiper blades has Wall Street worried | Business | The Guardian ) the Leveraged Loan Index had its worst day since April, 2025 and BDC equities are down by about 15% in the last month.

In the later case, lower short term rates hurt BDCs but the offset is that lower rates lower the cost of leverage and lower rates should stimulate loan demand. As most BDCs have double digit yields and single digit price/earnings ratios - it seems we are likely getting some systemic (quant selling). At the same time there have been a few dividend cuts, which may continue.

If the macro backdrop is as good as the S&P Index indicates, it is hard to understand the recent BDC weakness.

However, if the macro backdrop is as bad as BDC share prices suggest, the S&P Index could be quite vulnerable.

BY Doug Kass · Oct 10, 2025, 10:20 AM EDT

Back shorting the indexes with S&P cash +23 handles:

* (SPY) $673.45

* (QQQ) $612.71

BY Doug Kass · Oct 10, 2025, 9:49 AM EDT

-APLD +28% (earnings)

-SWKH +17% (Runway Growth Finance Corp. to acquire SWK Holdings Corporation for $145M cash)

-CRML +15% (critical metal strength)

-ESTC +13% (earnings, guidance)

-USAR +9.2% (critical metal strength)

-IREN +6.3% (crypto strength)

-RKLB +6.1% (secures multiple launches with Japan Aerospace Exploration Agency)

-ODC +5.7% (earnings)

-AMCR +3.1% (names new CFO)

-VKTX +3.1% (momentum)

-CIEN +2.2% (Morgan Stanley Raised CIEN to Equal Weight from Underweight, price target: $140)

-ORCL +2.1% (reportedly among Nvidia customers approved for shipments to UAE)

-ANVS -31% (announces $6M Registered Direct Offering of 4M Shares of common stock at $1.50/shr)

-VG -18% (reportedly handed defeat in BP LNG arbitration over LNG cargoes)

-KIDS -12% (earnings, guidance)

-SEPN -12% (downside momentum; appoints new Board member)

-SERV -8.9% (announces $100M Registered Direct Offering of 6.3M Shares Common Stock)

-MOS -8.5% (reports Q3 volumes; Scotia Howard Weil Cuts MOS to Sector Perform from Sector Outperform, price target: $34)

-LEVI -7.4% (earnings, guidance)

-EDUC -6.1% (earnings)

-TLRY -2.9% (files for mixed shelf of indeterminate amount)

-VIK -2.9% (Mizuho Securities Initiates VIK with Underperform, price target: $54)

BY Doug Kass · Oct 10, 2025, 9:43 AM EDT

I added to my trading short rentals in (HOOD) $153.11 and (NVDA) $193.47.

BY Doug Kass · Oct 10, 2025, 9:40 AM EDT

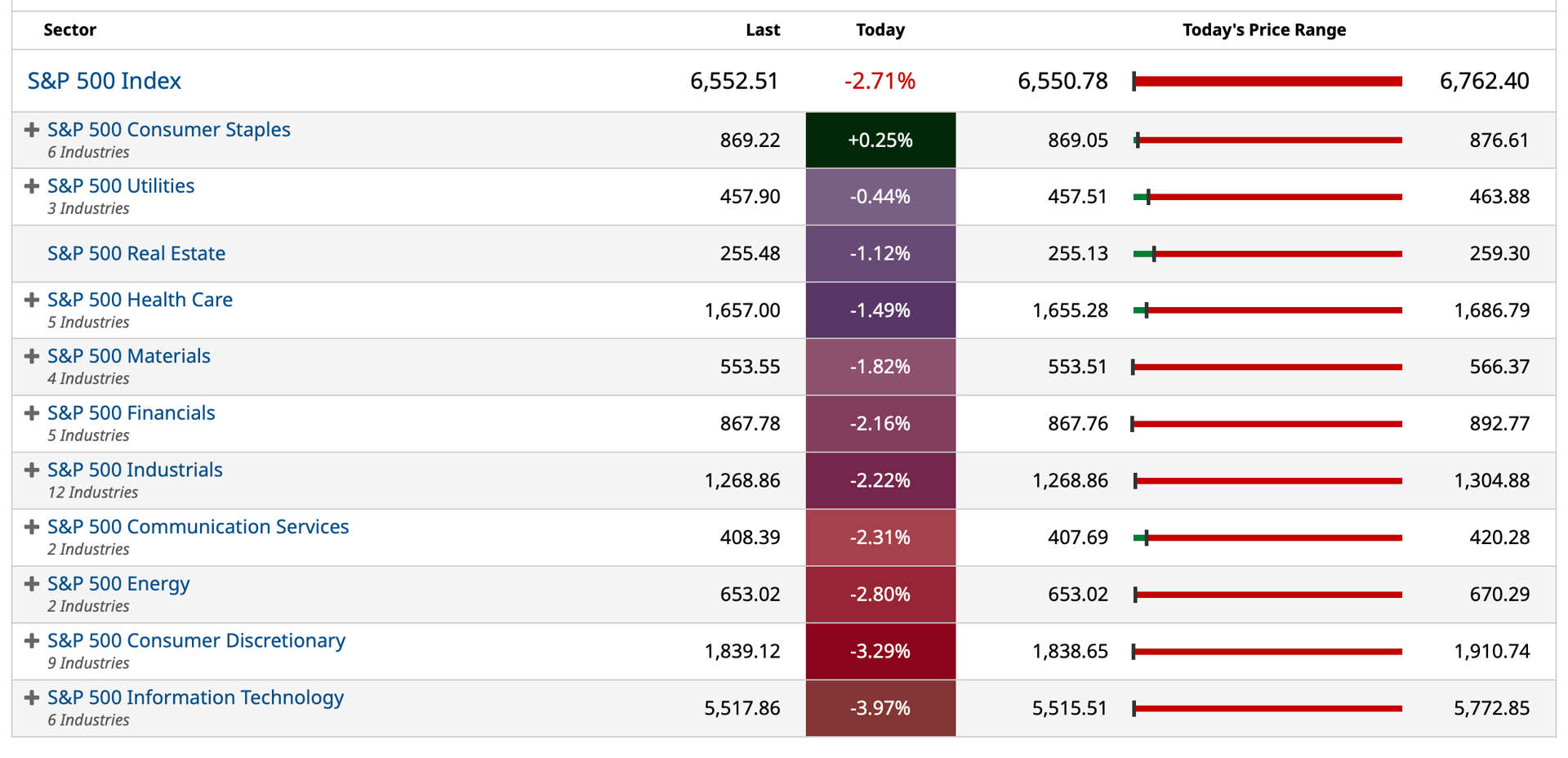

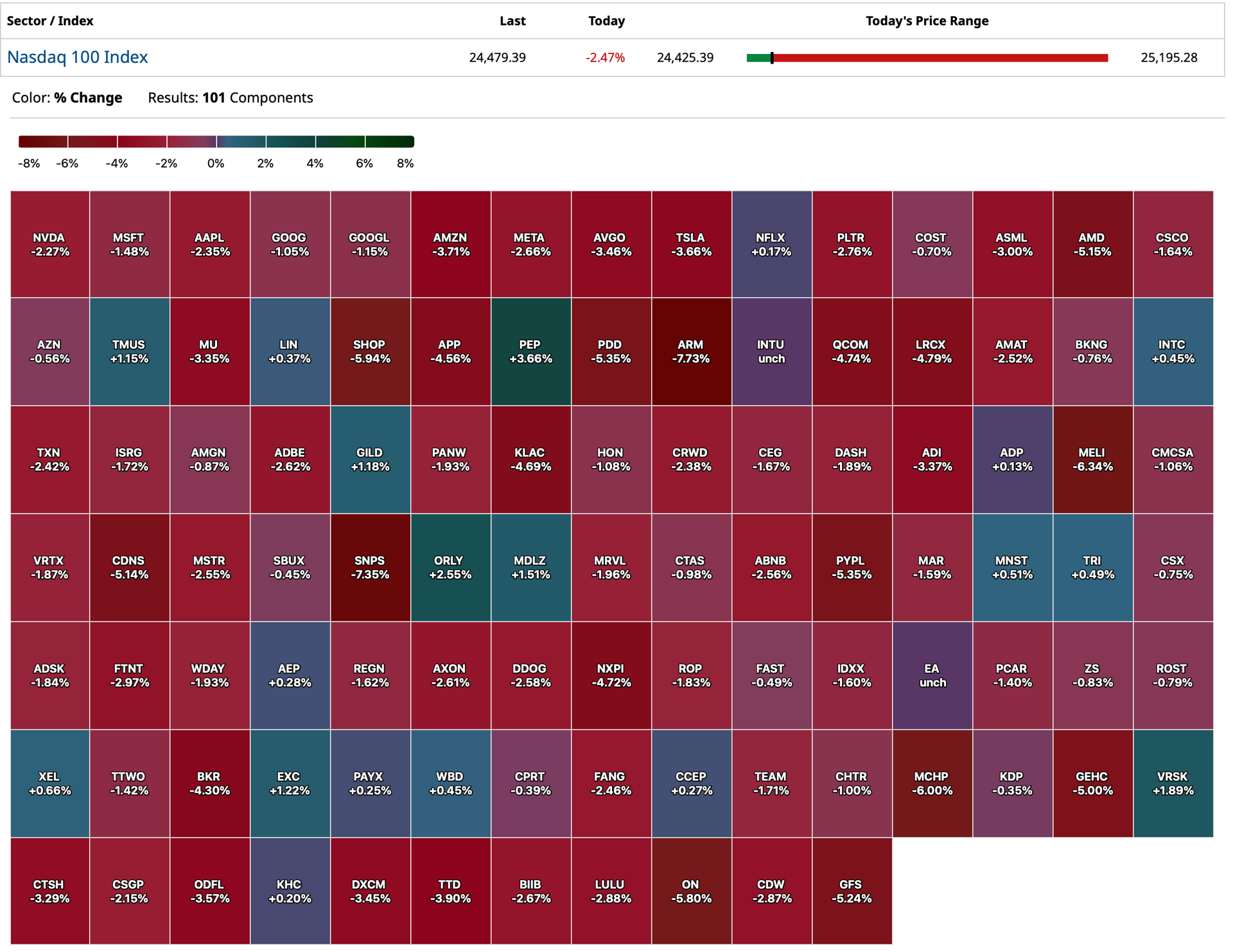

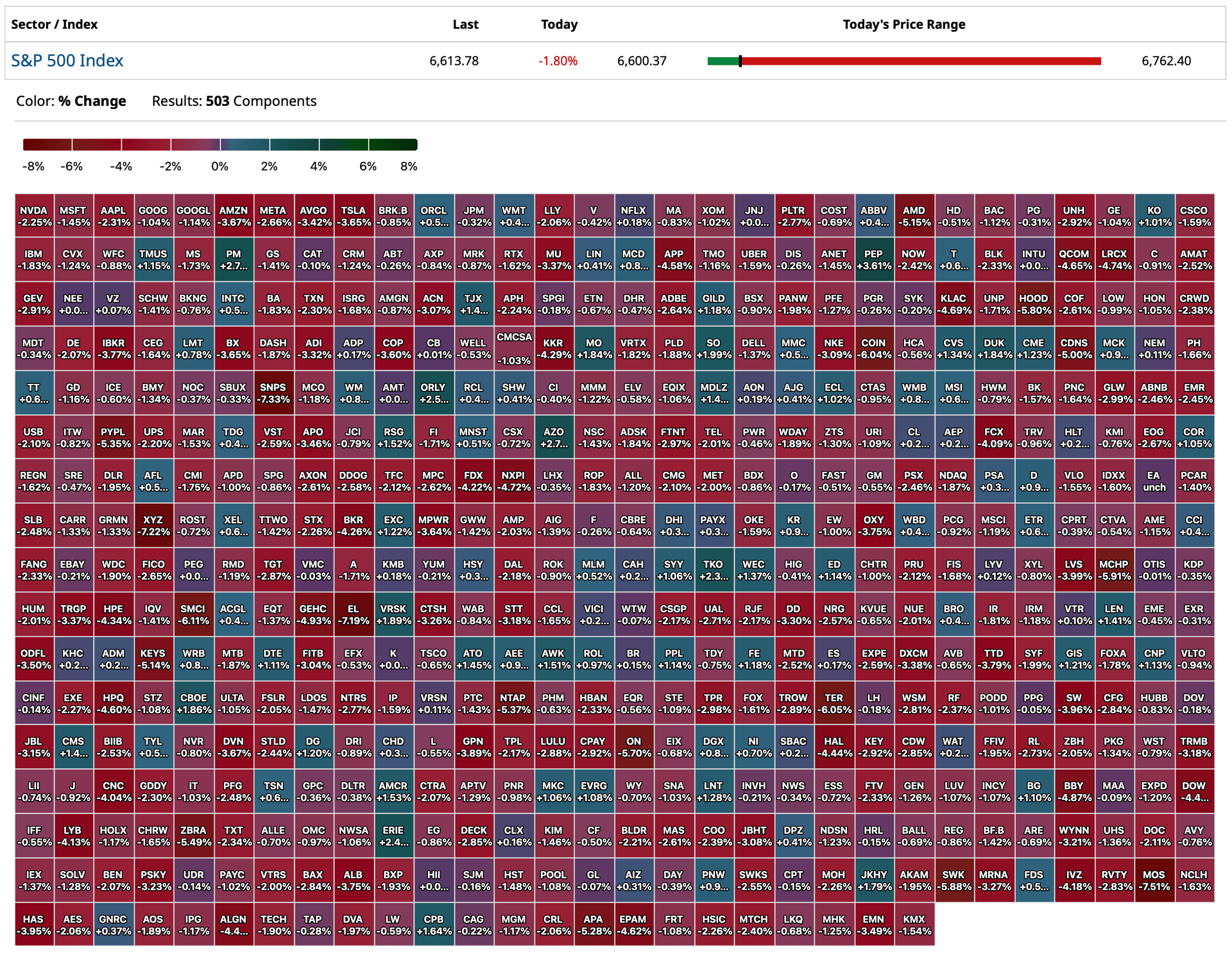

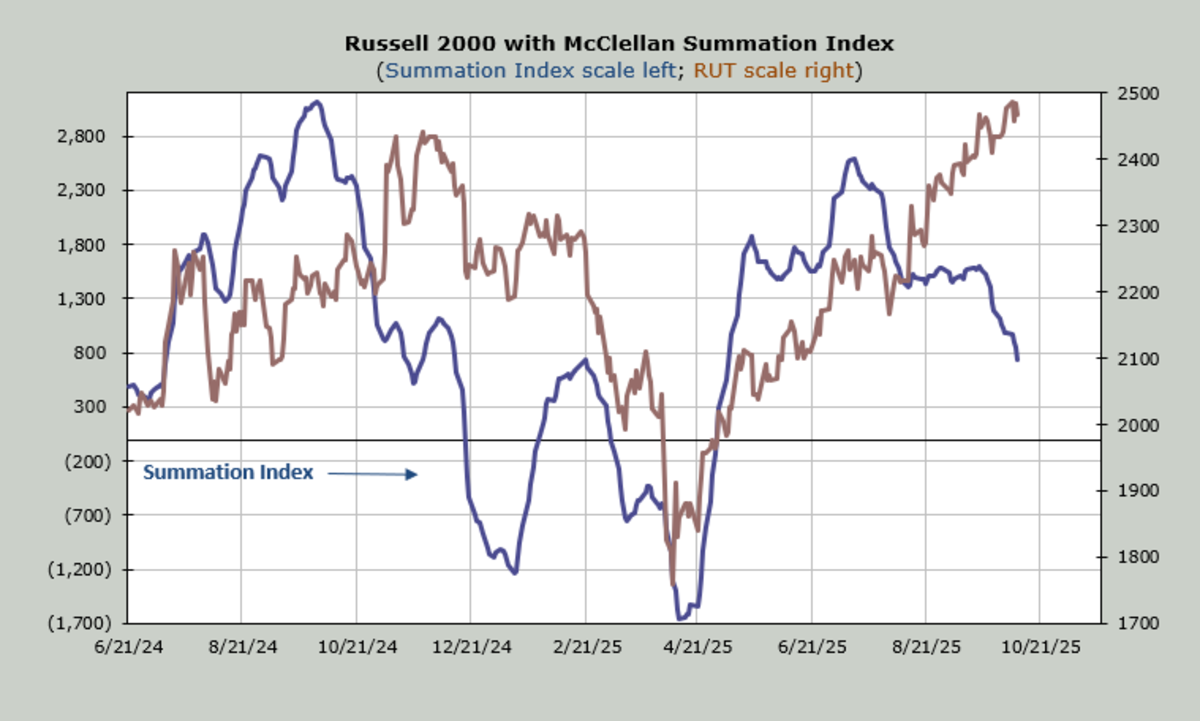

* The markets are not broadening (the new highs are declining and market breadth is mixed), low quality (and meme) stocks are flying

I thought Divine's (Helene Meisler) observations today were important. Is This Ratio Signaling a Correction Is in the Offing? - TheStreet Pro

* Indicators (like the McClellan Summation Index which represents the majority of the stocks) have not kept pace with the market's climb and continues to trend lower:

* The number of stocks making new highs has not increased and market breadth is inconsistent. So, despite the consensus view that the markets are broadening - it is not, its getting narrower.

From Ms Meisler:

About 3,000 stocks trade on the NYSE. In the past 10 trading days we have had only two quadruple-digit readings, which is unusual for a market that has seen the S&P relentlessly rise. One of those readings was Thursday. And of those 10 trading days, breadth has been up five days and down five days.

We have seen the majority of the market leaders falter. I’ve gone on about Amazon and Meta, but when the S&P made a new high a few days ago, not one of the 10 largest (by market cap) stocks made a new high. And now the banks/financials are struggling.

* As Divine and I both have mentioned in quoting Liz Ann Sonders, there is a quality issue in the market - meme stocks are the thing again and non profitable equities are flying:

Back to Divine:

"Most of what we’ve seen in the recent rally is low quality. Here is a chart of the S&P Quality ETF relative to the S&P. That plunge in the past month or so tells you how far away from the quality stocks folks have gone — so much further out on the risk curve".

BY Doug Kass · Oct 10, 2025, 9:30 AM EDT

BY Doug Kass · Oct 10, 2025, 9:05 AM EDT

BY Doug Kass · Oct 10, 2025, 8:55 AM EDT

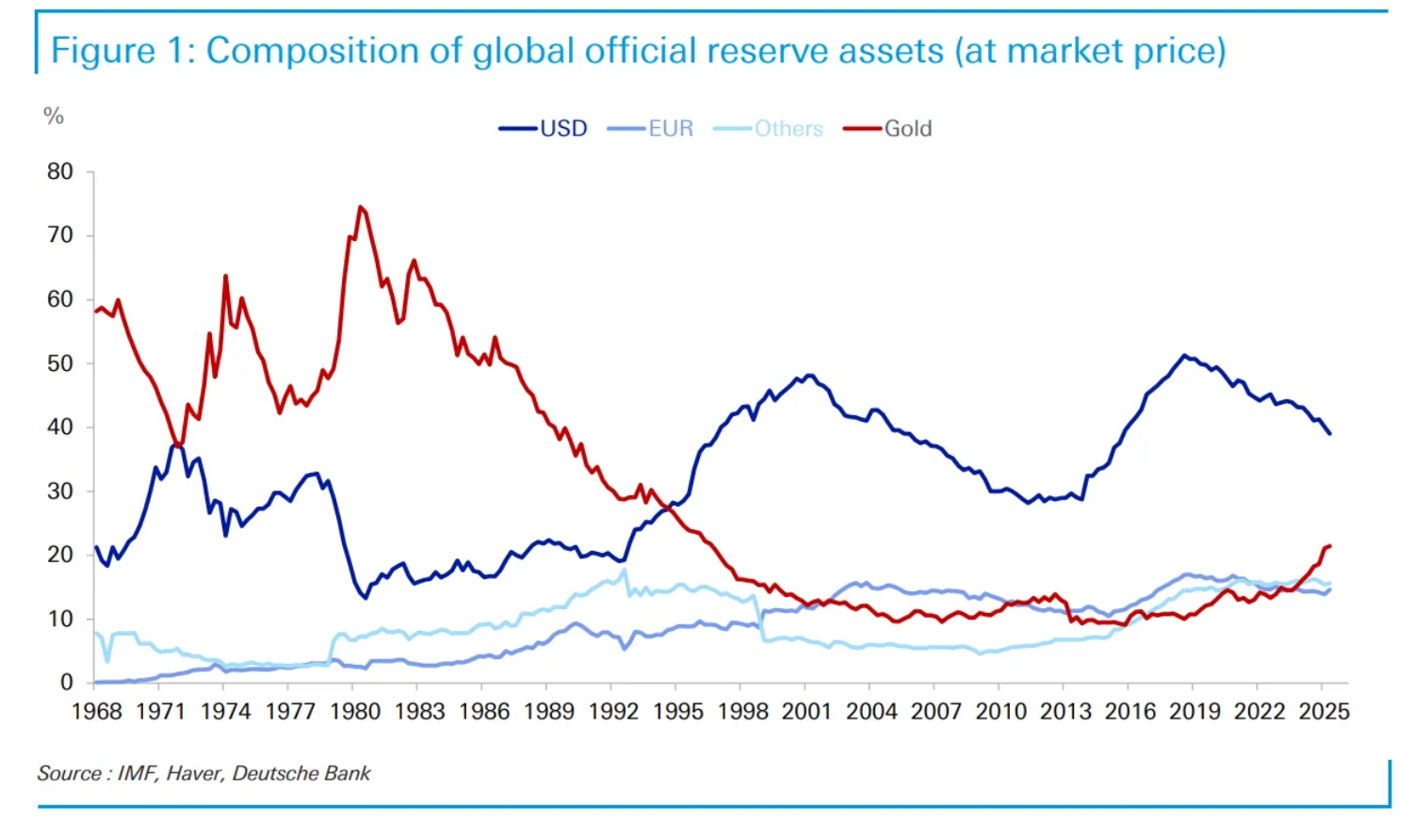

From Peter Boockvar:

Chart of the day from Jim Reid at Deutsche Bank yesterday reflecting the rising market share of gold in the basket of global reserve assets. As of Q2 2025 it stood at 24% (and now higher with the rising price since then) vs a bottom of 9% in Q4 2015. The high was 74.5% in the early 1980’s. As seen below, getting back to around 40% would put it half way between the upper end and the lower end and I believe where it is headed in the coming years.

Maybe Sanae Takaichi doesn’t become Japan’s Prime Minister after all as the LDP main’s coalition party, Komeito, overnight said they will not support her over disputes over how to regulate political donations. Hopefully this is something they can figure out but something to watch in coming days. The yen is higher for the first day in 7.

From Pepsi on the consumer:

“Now overall, the consumer is, I would say, stressed all over the world. We see the consumer making very choiceful decisions in many parts of the world, in China for sure, and China is a big market for us. Not so much in India...We’re seeing good growth in the Middle East...Eastern Europe better than Western Europe, I would say. And then, yes, Mexico is somehow connected to the US and however the US goes, that impacts Mexico quite a lot. Clearly, the Hispanic cohort in the US is being impacted by all these decisions and we see remittances impacting Mexico in a way and that will continue probably for the next few quarters. Brazil continues to be strong for us...I would say we see the consumer in different parts of the world, different realities.”

Also, “And then affordability is also a reality. I think when you look at low income households or middle income households, they’re very stretched. Fixed cost of living is going up around the world and that will create the need for affordability and value and price points and cost consciousness also for the foreseeable future.”

From Helen of Troy, whose stock plunged 25% yesterday:

They have gotten hit particularly hard by the tariffs as “we have experienced significant increases in tariff rates, which have created immediate and ongoing revenue, earnings, cash flow and balance sheet impacts.” They have taken mitigation steps like supplier diversification, inventory management, SKU prioritization, supplier cost reductions and customer price increases.”

On the pricing, “We notified retail customers of targeted price increases with the original goal of having them in place near the end of the summer. Working collaboratively with our key retailers and in careful consideration of market and category dynamics, we have now implemented the majority of our planned price increases as of the end of September. However, there are some isolated price increases that are still pending and we are holding shipments in some instances as we work toward consistent adoption across our retail customer base.”

On the top line impact from tariffs, “Approximately 30% of the organic revenue decline was attributed to tariff related revenue disruptions As expected, this primarily stems from two key factors, the pause or cancellation of direct import orders from China in response to higher tariffs and trade policy uncertainty and changing dynamics within the China market.”

Also, “The remaining decline is indicative of softness in certain categories and overall point of sale decline, even if several of our brands gained or maintained market share and saw point of sale unit improvements. Category softness can be attributed to changing consumer behaviors, particularly the prioritization of essential categories amid concerns regarding future pricing pressures and overall economic uncertainty. As these trends influence purchasing volumes, retailers also continue to modify their inventory levels.”

From Levi Strauss:

“our consumer continues to be resilient and we’re seeing that around the globe...And we saw broad based strength across geographies, across categories, that’s both men’s and women’s, tops and bottoms, and both DTC and wholesale. So, consumers are responding, our strategies are working.” Denim in particular was strong for them, and that of course is what they are known for.

The research report of interest yesterday came from the Dallas Fed who argued “Break-even employment declined after immigration changes.” In the piece they claim, “A new, high frequency estimate of break-even employment shows a dramatic reversal in immigration flows, combined with cyclical shifts in labor force participation, has caused the monthly break-even requirement to collapse from a peak of approximately 250,000 in 2023 to about 30,000 in mid-2025.”

“This recalibration suggests that today’s more modest payroll gains don’t signal weakness but are consistent with a balanced labor market.”

This likely explains why Dallas Fed president Lorie Logan is more hawkish than many of her peers, https://www.dallasfed.org/research/economics/2025/1009.

I’m going to highlight again the LSTA Leveraged Loan Index which had its worst day yesterday since April in percentage terms, down .14%. It’s had two green days over the past month. Coincident with this is the continued weakness in Business Development Company stocks where BIZD is back at the April lows (below it also because of ex dividends). Specifically with the BDC’s, dividends are getting cut because of less interest income due to the Fed rate cuts. On the private side, the private credit monster BCRED from Blackstone cut its dividend last month. Also, there is heightened focus on credit quality in this entire space with the growing use of PIK (payment in kind) interest payments and tight cash flows. Again, something to watch.

LSTA Leveraged Loan index

BIZD

I went to Vietnam last December and came back bullish on the country and we bought stocks there. If you didn’t see a few days ago, FTSE Russell has reclassified Vietnam as a secondary emerging market from a frontier market. They said “The reclassification of Vietnam reflects the implementation of key market infrastructure enhancements, and we look forward to continued collaboration to ensure sustained progress ahead of the target reclassification date in September 2026.”

The Ho Chi Minh index is up 38% year to date and 34% in dollar terms and we remain long.

BY Doug Kass · Oct 10, 2025, 8:45 AM EDT

9:45 a.m.: Fed Bank of Chicago President Goolsbee (Voter) gives opening remarks and moderates a discussion before the 19th annual Community Bankers Symposium, "Community Banking: Charting the Course" hosted by the Federal Reserve Bank of Chicago, Chicago, IL (Livestream TBD);

1:00 p.m.: Fed Bank of St. Louis President Musalem (Voter) speaks on the U.S. economy and monetary policy in fireside chat before the Springfield Area Chamber of Commerce Public Policy Speaker's Series, Springfield, MO (In-person and virtual option. No text. Audience Q&A expected. No media availability)

BY Doug Kass · Oct 10, 2025, 8:19 AM EDT

- Young Frankenstein Young Frankenstein Abby Normal - YouTube

More...

BY Doug Kass · Oct 10, 2025, 8:05 AM EDT

Bonus — Here are some great links:

BY Doug Kass · Oct 10, 2025, 6:37 AM EDT

* Is First Brands the "tip of the iceberg?"

BY Doug Kass · Oct 10, 2025, 6:05 AM EDT

BY Doug Kass · Oct 10, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at 0.62% vs. 0.83%.

BY Doug Kass · Oct 10, 2025, 5:45 AM EDT