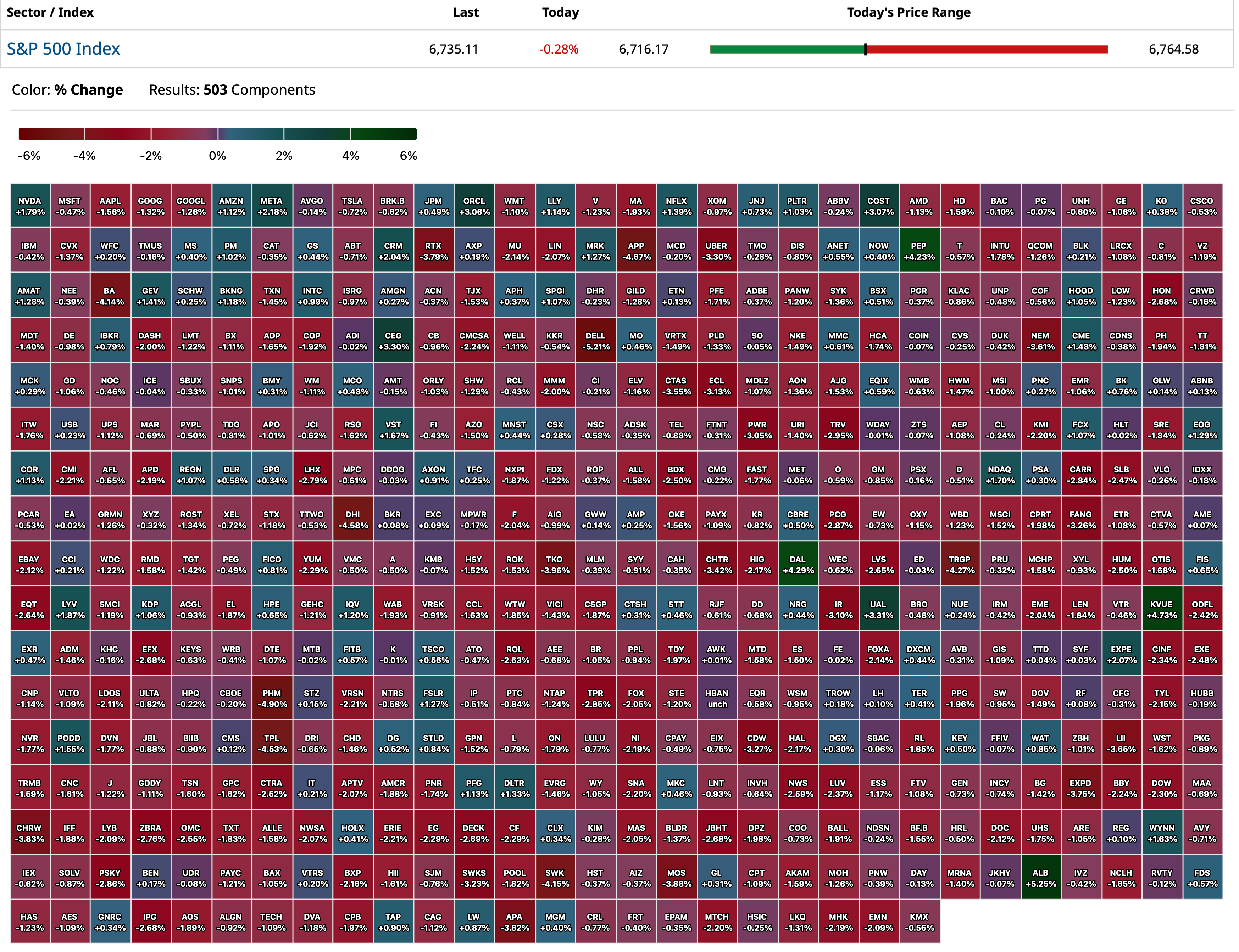

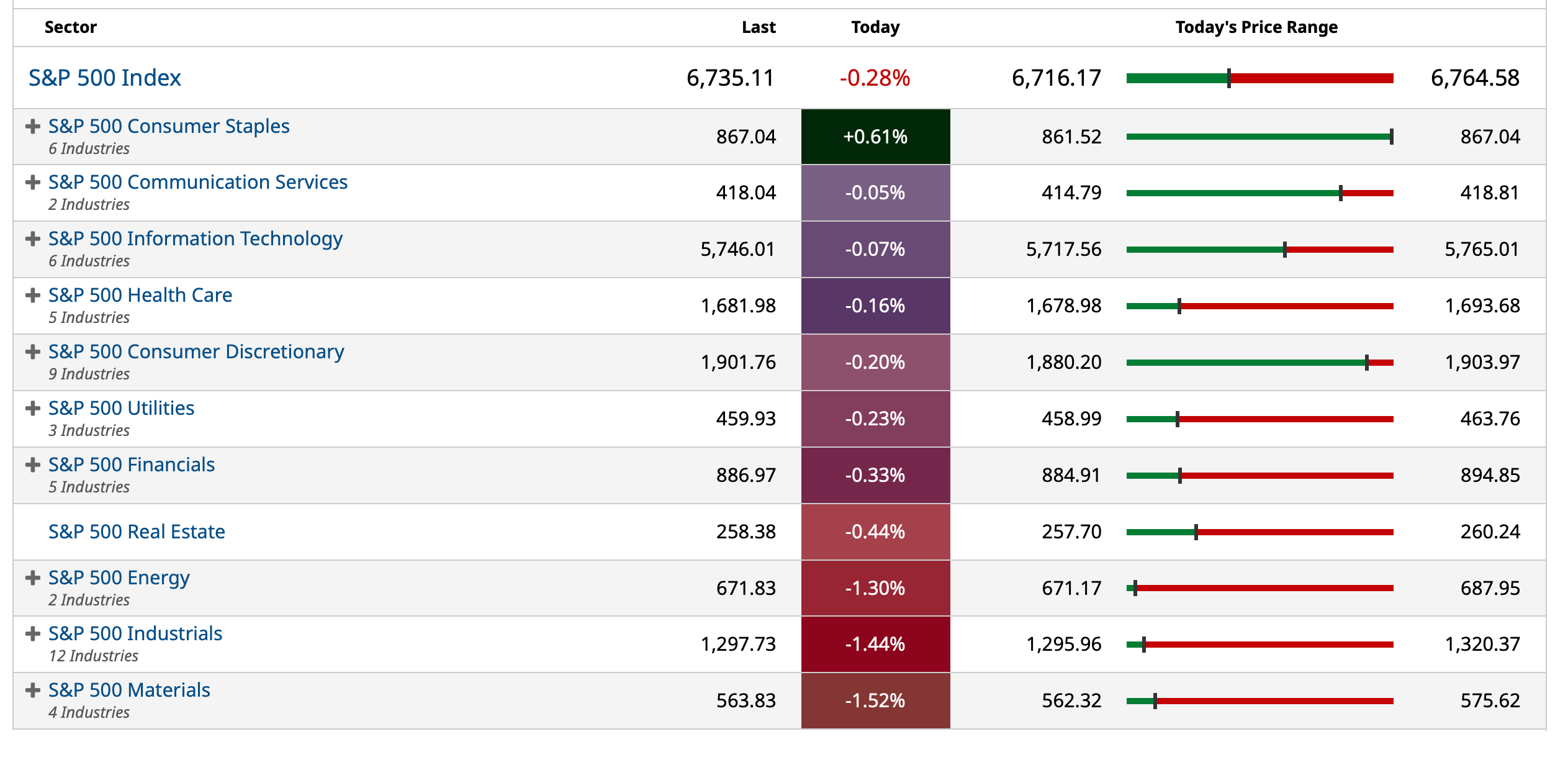

Closing S&P 500 Heat Map

BY Doug Kass · Oct 9, 2025, 4:57 PM EDT

BY Doug Kass · Oct 9, 2025, 4:57 PM EDT

BY Doug Kass · Oct 9, 2025, 4:51 PM EDT

BY Doug Kass · Oct 9, 2025, 3:14 PM EDT

From Peter Boockvar:

30 yr auction results, Takaichi comments on yen & BoJ, Gov Barr a bit more hawkish

As yesterday’s 10 yr note auction was mediocre, so was today’s 30 yr but at least had a positive characteristic. The yield of 4.734% was a hair above the when issued pricing. The bid to cover of 2.38 which just below the one year average of 2.40. The bright spot though was that direct and indirect bidders took down 91% of the auction which is the most since June 2023.

Yields, while at the highs of the day, didn’t move much in response. Something to watch here today with respect to JGB’s and its flow thru to sovereign bonds globally were the comments from the incoming Japanese leader Sanae Takaichi (assuming she gets the parliamentary support at this point) who spoke in response to the sharp drop in the yen over the past week that was triggered by her election. “I have no intention of triggering an excessively weak yen. But, just as a rule of thumb, I would say there are both merits and demerits to a weak yen. For export focused companies, this is a buffer, given the concerns over the Trump tariffs.”

On the comment she made last year that it was ‘stupid’ for the BoJ to hike rates and we were left with the assumption she would push back on Governor Ueda, “Oh, please stop bringing that up. I know I’m not in a position to comment on a rate increase.”

Lastly, Fed Governor Barr isn’t sounding like someone who is convinced that two more rate cuts are necessary this year. He said, “While, in principle, tariffs are a one-time increase in prices and should not sustainably raise inflation, that may not be the case if prices keep rising month after month and affect expectations.”

On the labor market, he believes that it is in “rough balance” but followed with the caveat that there is vulnerability as “the fact that this balance is achieved from simultaneous slowing in labor supply growth and in hiring suggests that the labor market is more vulnerable to negative shocks.”

What to do? He said, “Common sense would indicate that when there is a lot of uncertainty, one should move cautiously.”

BY Doug Kass · Oct 9, 2025, 2:00 PM EDT

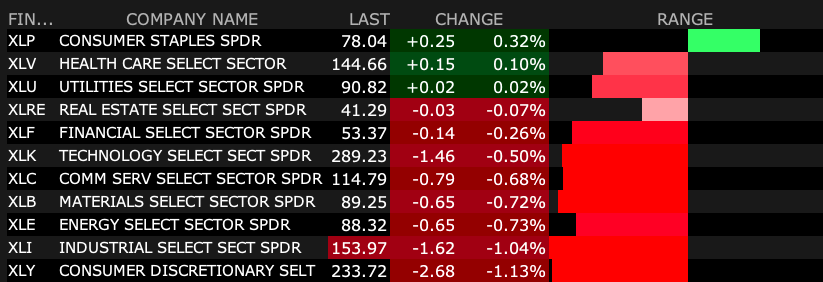

Four hours does not make a definitive market reversal but let's look at a few potentially adverse developments:

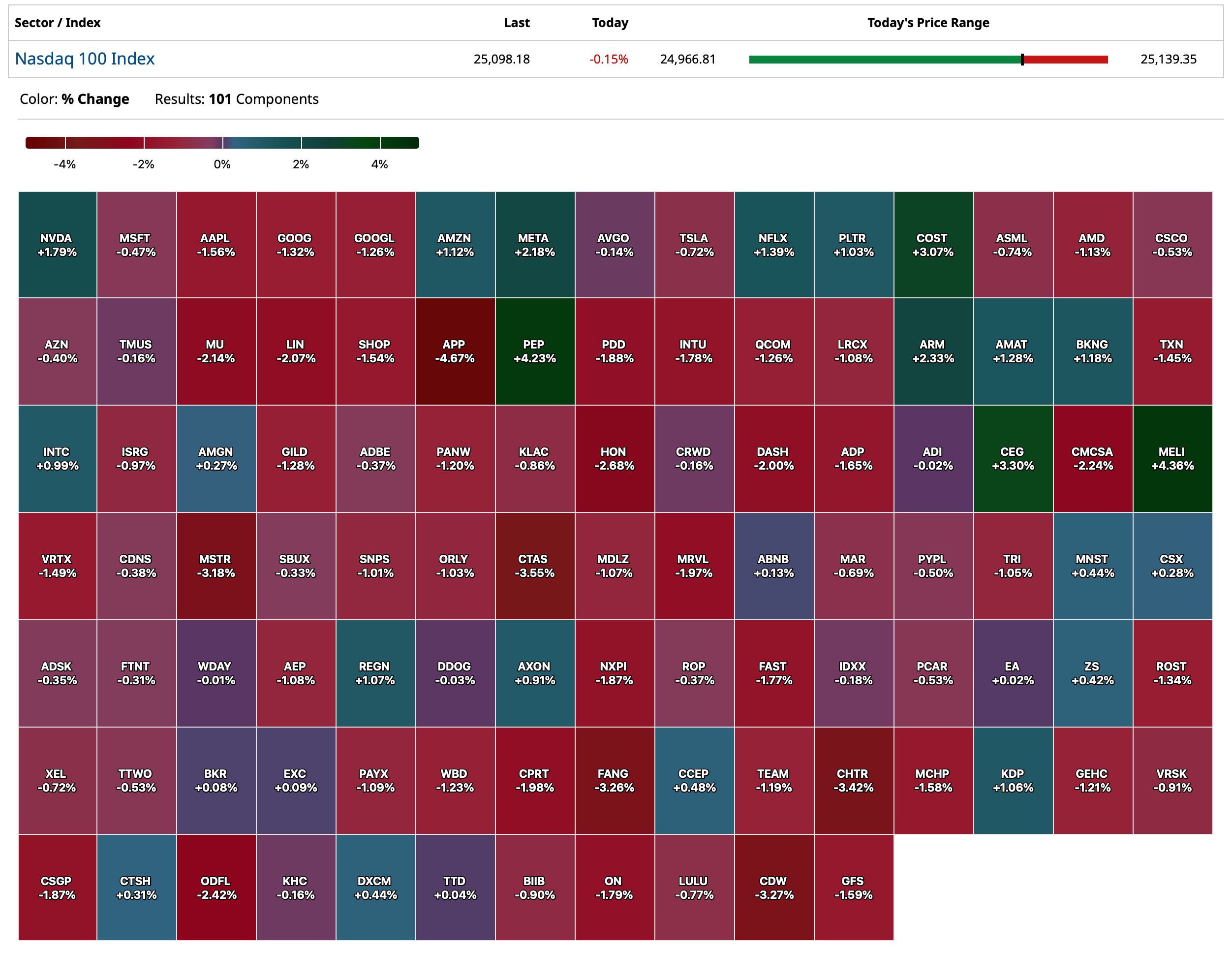

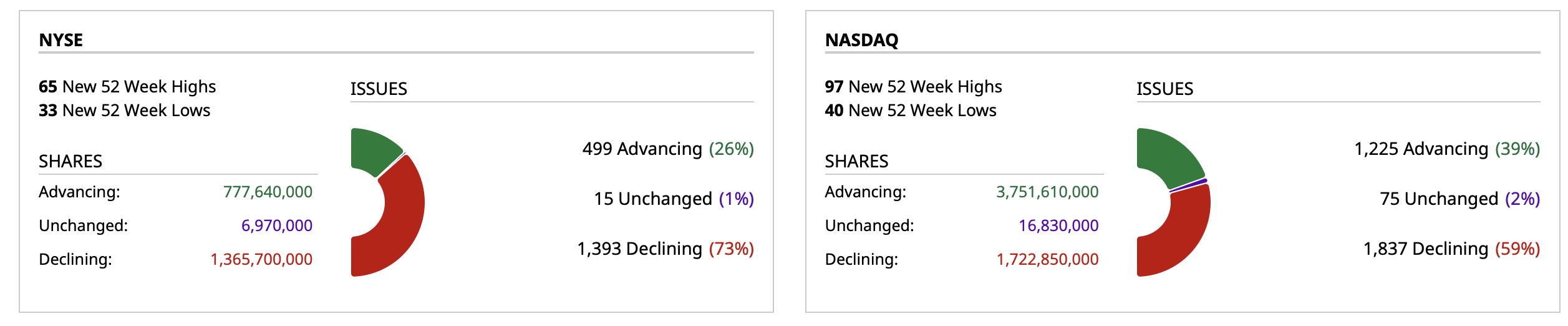

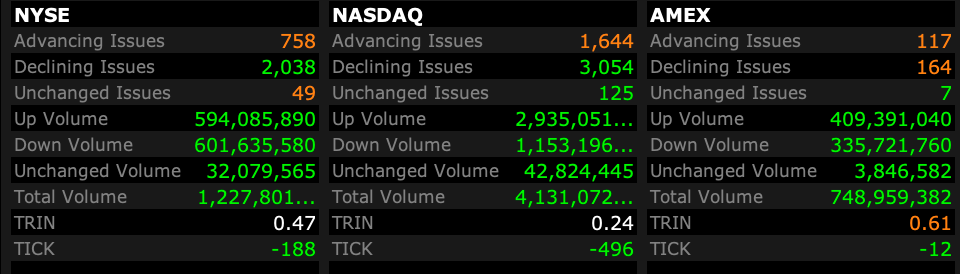

* After a week of narrow leadership and inconsistent market breadth (with AI-related stocks being the "world's fair") — breadth (at 1:08 PM) is noticeably weak:

* Seeing fairly large profit-taking in league-leading stocks like (BABA) .

* Crypto failed to break out after a big run — (ETH) and (BTC) continue lower.

* Financials continue to show absolute and relative weakness. ( (GS) is -$50 from its recent high.)

* Homebuilders are glaring downside leaders — on average, down by five percent on the day.

* The gold market has had an enviable run as gold bugs have gotten very complacent and confident. Big profit-taking today with (GLD) -$9/share.

As I mentioned in my two tweets, the bullish cabal couldn't find a reason to be bearish on the shows today. (That's a tell!)

Anecdotally, save my old boss Lee Cooperman (who I spoke to last night), no one I speak to envisions a meaningful market correction. In fact, over the last few days some of my bearish friends have acquiesced and have loaded up for a "Paul Tudor Jones" melt-up.

BY Doug Kass · Oct 9, 2025, 1:40 PM EDT

With S&P cash -34 handles I have covered half of my index shorts (moving from medium to small sized).

(SPY) $608.24

(QQQ) $669.71

I plan to reshort on strength.

BY Doug Kass · Oct 9, 2025, 1:26 PM EDT

BY Doug Kass · Oct 9, 2025, 12:32 PM EDT

Look at the stock charts of (TOL) , (PHM) , (down another -$7 after being -$10 one day earlier this week), (GRBK) and (KBH) .

My negative thesis from August, 2025:

AUG 27, 2025 7:30 AM EDT

* A more aggressive move to cut interest rates by a politically motivated Fed (lacking independence) will likely backfire and produce higher (not lower) mortgage rates.

* After a spectacular rise in the last four months I am shorting homebuilders.

A 'significantly politicized' Fed is growing risk, warns Wall Street Veteran Rebecca Patterson

Homebuilders' shares have had a big run off of the April lows.

There is a lot of hot (or performance) money in this small-weighted sector based on the perception that the Trump administration (especially after the aggressive legal tact taken towards firing Fed Governor Lisa Cook and the resignation of Adriana Kugler) will easily gain control of the Federal Reserve and cajole Fed members into a path of much easier money.

The consensus belief is that interest rates will then fall and be housing sector stimulative.

As noted by Rebecca Patterson (see above) on CNBC yesterday, this consensus expectation is probably misunderstood and at a material risk.

While I agree that the Trump administration will likely gain majority control of the Fed, I am fearful that Fed rate cuts will stimulate higher yields in the intermediate and longer-term fixed-income markets — triggering higher mortgage rates in the process.

There is historical precedent for this.

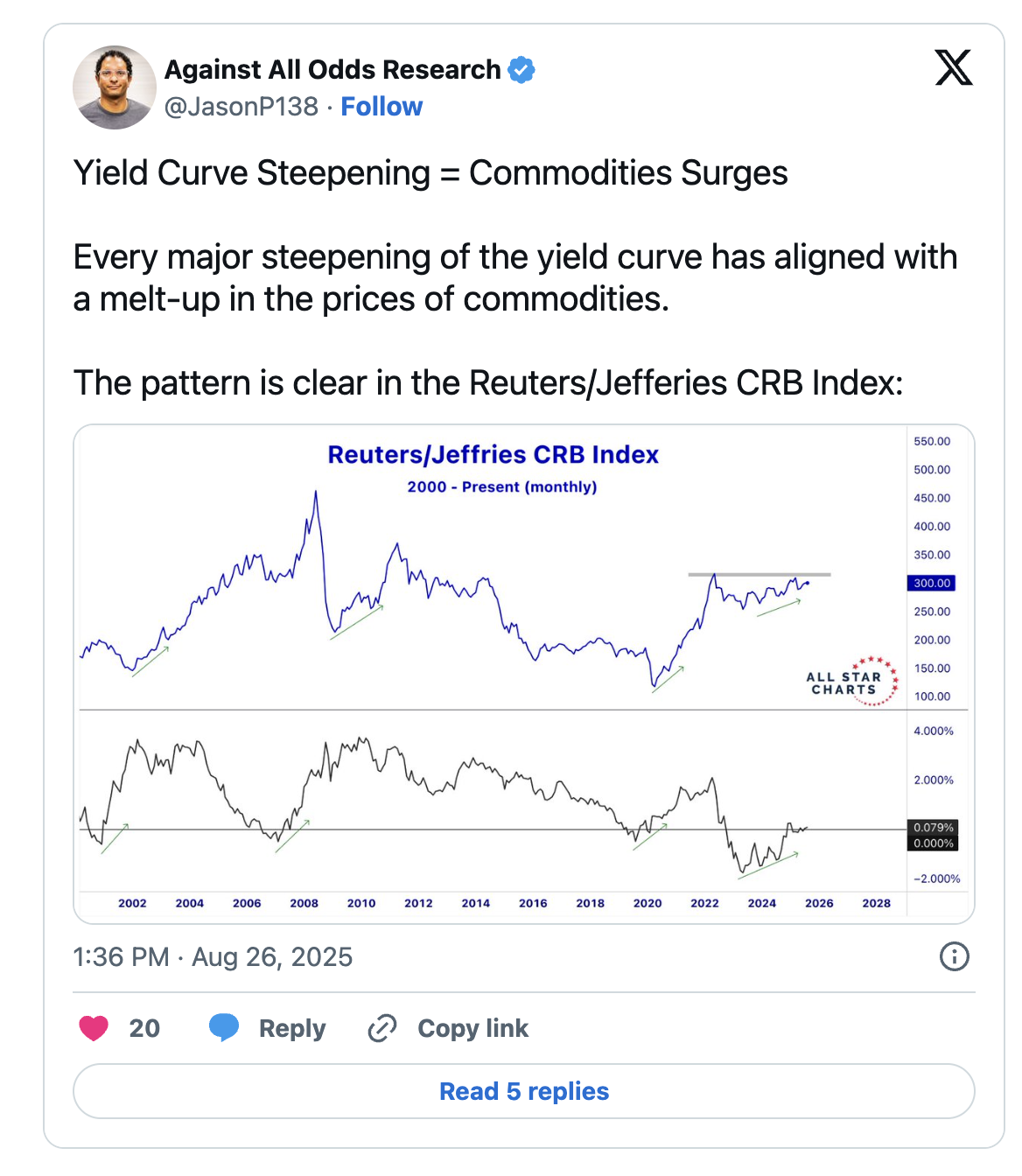

Generally, mortgage rates are tied to the 10-year Treasury note, which I see as moving higher in the months ahead, exacerbated by too-aggressive Fed easing and stubbornly high inflation (which will be boosted by tariff increases going thru the pipeline)

Already the 2/10 yield curve is at the steepest since April 2025:

Besides the likelihood of higher, not lower mortgage rates (byproduct of Fed easing), the inventories of unsold homes are moving higher across the country as home prices begin to sputter:

* Average Age of First-Time Home Buyers and How it Changed over the Past 25 Years | Wolf Street

* Inventory of Homes for Sale Balloons in Texas and its Big Metros: Dallas-Fort Worth, Houston, Austin, San Antonio | Wolf Street et

An additional and non-trivial concern is that the recent rise in the CRB Index and building materials which could dampen profit margins.

With the administration's politically motivated gain of control of the Federal Reserve producing a central bank soon to be hell bent on lowering the Fed Funds rate — another error in monetary policy seems to lie ahead as the interest rates (10-year Treasuries) tied to mortgage rates likely rise.Sticky inflation (causing potential homebuilder profit margin erosion) and a rising glut of unsold homes raise formidable headwinds to homebuilder profitability in the year ahead.

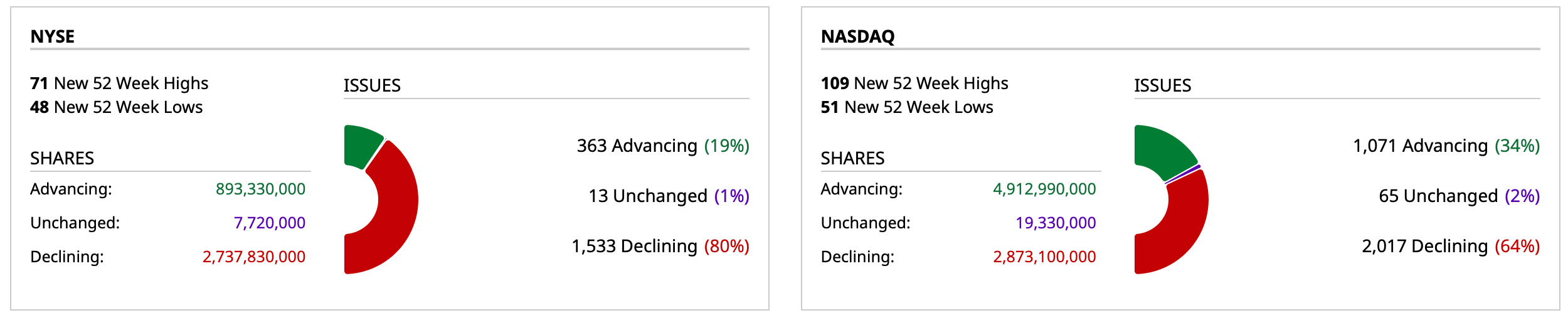

BY Doug Kass · Oct 9, 2025, 11:30 AM EDT

- New York Stock Exchange volume 8% below its one-month average;

- Nasdaq volume 19% above its one-month average;

- VIX index: up 3.87% to 16.93

BY Doug Kass · Oct 9, 2025, 11:18 AM EDT

BY Doug Kass · Oct 9, 2025, 10:55 AM EDT

From Bloomberg:

By Caleb Mutua

(Bloomberg) -- The amount of debt tied to artificial intelligence has ballooned to $1.2 trillion, making it the largest segment in the investment-grade market, according to JPMorgan Chase & Co.

AI companies now make up 14% of the high-grade market from 11.5% in 2020, surpassing US banks, the largest sector on the JPMorgan US Liquid Index (JULI) index at 11.7%, JPMorgan analysts including Nathaniel Rosenbaum and Erica Spear wrote in a note Monday.

The analysts identified 75 companies across tech, utilities and capital goods sectors that are closely tied to AI, including Oracle Corp., Apple Inc. and Duke Energy Corp. Many of these firms are prolific debt issuers and in the case of tech, they are cash rich with very low net debt. The cohort trades at 74 basis points, 10 basis points tighter than the broader JULI index, they said.

See blinks.bloomberg.com for the rest.

BY Doug Kass · Oct 9, 2025, 10:35 AM EDT

My concern, expressed following channel checks and competitor discussion for Pepsico (PEP) was that organic growth would come in weaker than consensus.

This occurred with the quarter's organic growth of only +1.3% v consensus expectations of +2.0% to +2.3%. The pleasant surprise was cost controls, which resulted in a reasonable earnings per share print. Also, a lower U.S. dollar contributed positively to the headline number.

Near term headwinds continue - especially at the ("subdued") lower and middle income consumer cohorts.

I sold the stock, because I now believe it will take a while for Elliott Management, the activist, to impact the beverage company's results.

Meanwhile, organic growth looks locked around 3Q levels and pricing will continue to be pressured in a macroeconomic setting that might grow more volatile (to the downside).

I sold the balance of my stock in premarket (after the positive response to the release) above $141.

With a 4% dividend yield I expect PEP will outperform cash and most stocks in a correction.

My bottom line is that I see the stock trading $135-$145 as far as the eyes can see...

BY Doug Kass · Oct 9, 2025, 10:05 AM EDT

Here are today's things:

* I added to Index shorts - (SPY) $673.43 and QQQ $611.54.

* I added to my (GRNY) short at $25.62

* I sold the balance of my (PEP) at $141.26.

* I added to my (HOOD) short at $150.01.

BY Doug Kass · Oct 9, 2025, 9:57 AM EDT

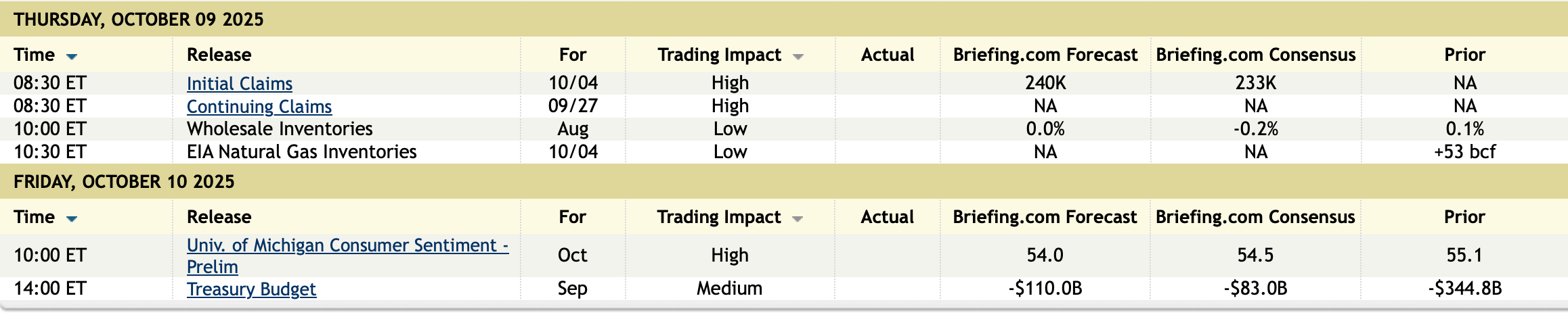

11:00 a.m.: Treasury announces a 3 and 6 month bill auction;

11:30 a.m.; Treasury hosts a $110B 4 and $95B 8 Week Bill Auction;

1:00 p.m.: Treasury hosts a $22B 30-Year Bond Auction

8:30 a.m.: (PRE-RECORDED) Fed Chair Powell gives welcome remarks before the Community Bank Conference hosted by the Federal Reserve Board, that "will bring together bankers, industry experts, and other stakeholders to discuss and identify issues facing community banks," Washington, DC (Livestream at federalreserve.gov and youtube.com/federalreserve);

8:35 a.m.: Fed Vice Chair for Supervision Bowman (Voter) gives opening remarks and participates in fireside chat before the Community Bank Conference hosted by the Federal Reserve Board, that "will bring together bankers, industry experts, and other stakeholders to discuss and identify issues facing community banks," Washington, DC (Livestream at federalreserve.gov and https://www.youtube.com/federalreserve); at

8:45 a.m.: Vice Chair Bowman "Future of Community Banking: Challenges and Opportunities" discussion before the Community Bank Conference hosted by the Federal Reserve Board (Livestream at federalreserve.gov and here. No text. Vice Chair Bowman will moderate Q&A)

9:00 a.m.: Fed Bank of Chicago President Goolsbee (Voter) Podcast Appearance -- Let's Appreciate w/ Kyla Scanlon;

12:45 a.m.: Fed Board Governor Barr (Voter) speaks on the economic outlook before an Economic Club of Minnesota luncheon; Fed Bank of Minneapolis President Kashkari (Non-Voter) is moderator. Golden Valley, MN (Livestream at minneapolisfed.org/live. Barr text available. No Kashkari text. Q&A from moderator and audience);

3:45 p.m.: Fed Vice Chair for Supervision Bowman (Voter) gives closing remarks before the Community Bank Conference hosted by the Federal Reserve Board, that "will bring together bankers, industry experts, and other stakeholders to discuss and identify issues facing community banks," Washington, DC (Livestream at federalreserve.gov and youtube.com/federalre-serve;

9:40 p.m.: Federal Reserve Bank of San Francisco President Mary Daly (Non-Voter) participates in moderated conversation before the Silicon Valley Directors

Exchange, San Jose, CA (Livestream here. No prepared remarks. No group media interview)

BY Doug Kass · Oct 9, 2025, 9:45 AM EDT

From Peter Boockvar:

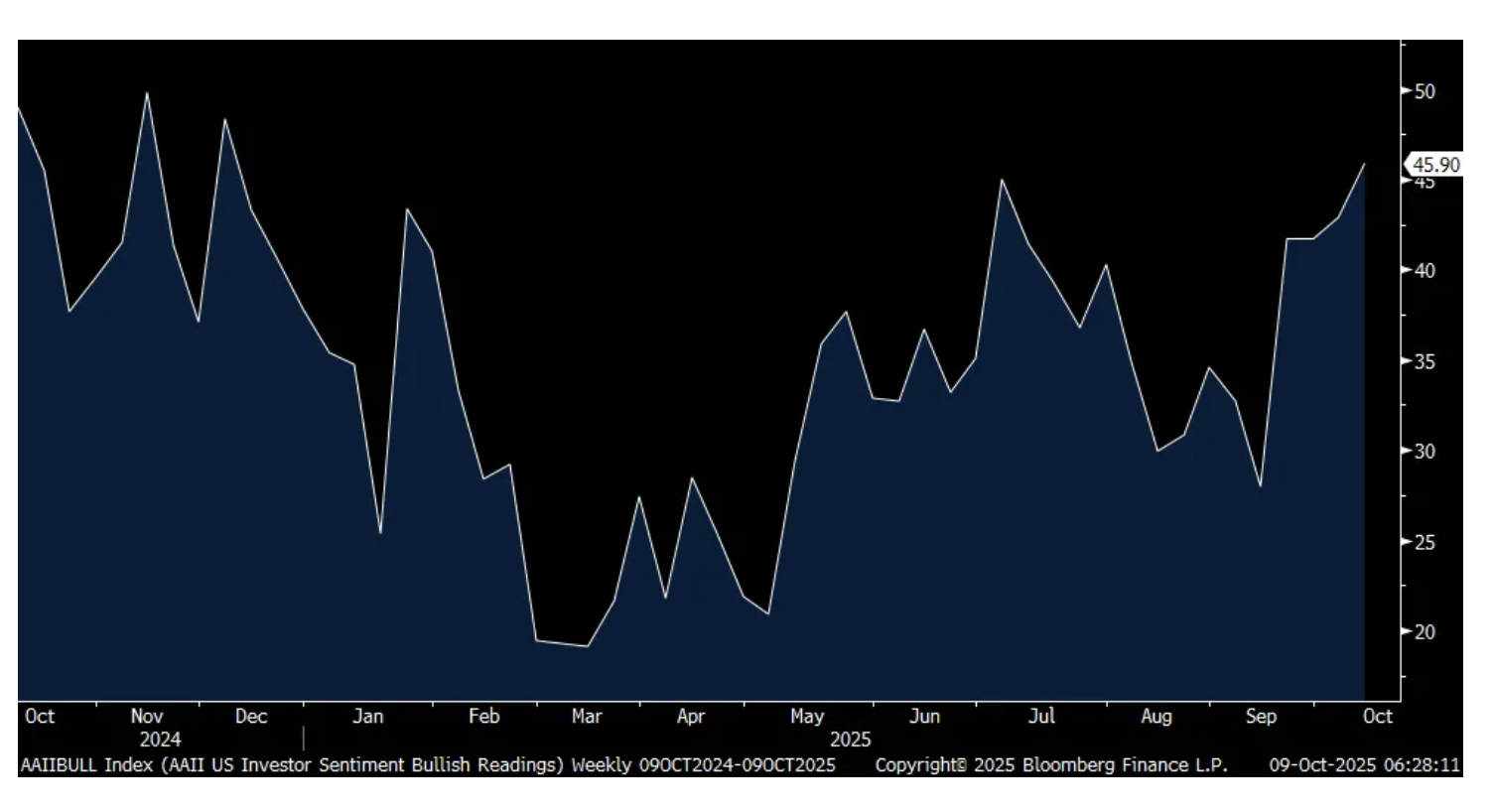

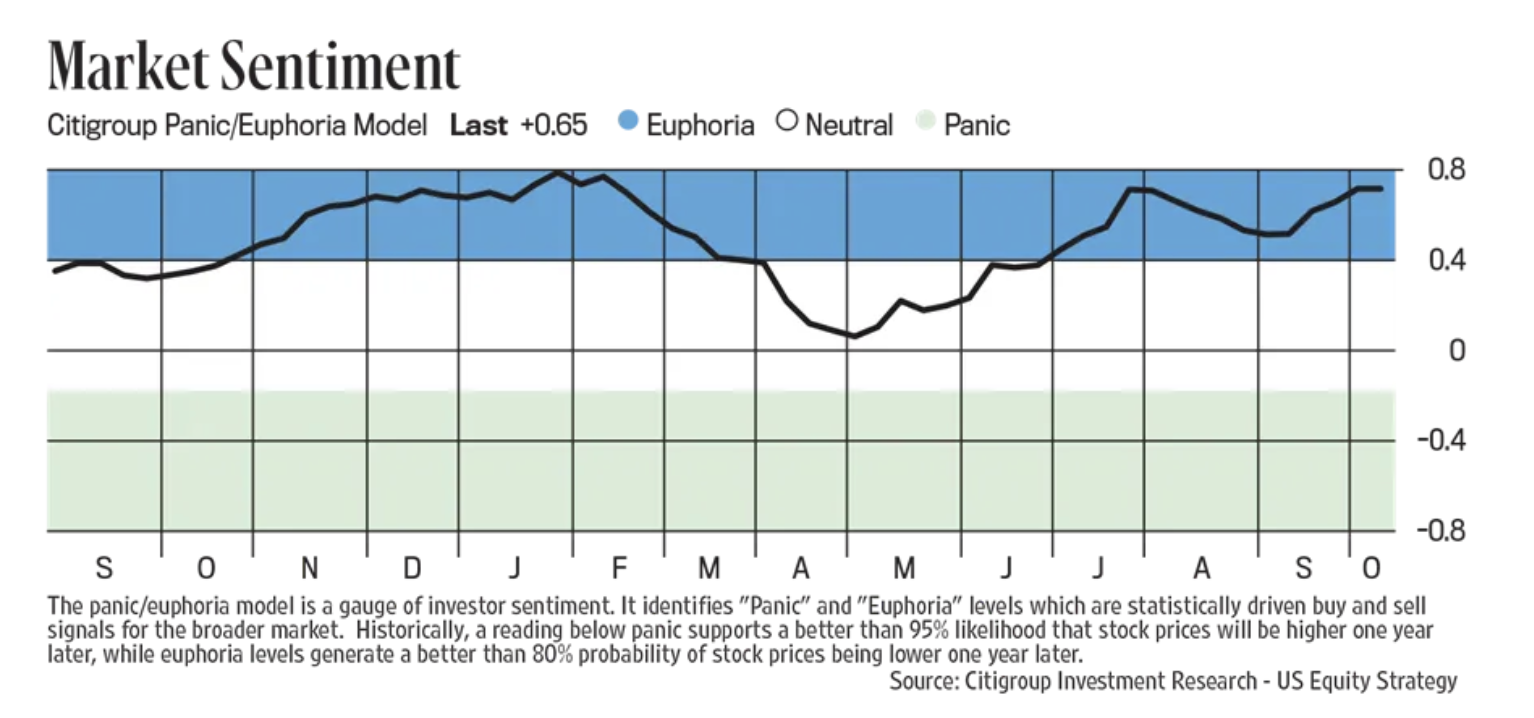

With respect to stock market sentiment, I have to throw out the red flag today after seeing the Investors Intelligence survey with Bulls rising to 57.7 from 53.7 while Bears fell to just 15.4 from 16.7. That’s the least amount of Bears since the summer of 2024 and the spread of 42.3 exceeds my extreme threshold of 40. In today’s AAII, Bulls rose by another 3 pts to 45.9, the most since December 2024. The Bear read of 35.6 is down 3.6 pts w/o/w and the lowest since late July. This follows the Citi Panic/Euphoria index which rose to the most euphoric since February.

Bottom line, the sentiment is now ebullient and from a contrarian standpoint we should take note.

AAII Bulls

With respect to the oncoming onslaught of Q3 corporate earnings, I again ‘guarantee’ that about 75% of those companies reporting will exceed earnings expectations.

Delta beat both top and bottom line forecasts and said this:

The 4.1% y/o/y sales gain reflected “the strength of our diverse, high margin revenue streams and improving Domestic fundamentals. Over the last 6 weeks, sales trends have accelerated across all geographies and in every advance purchase window, positioning Delta to finish the year with momentum.”

“Premium revenue grew 9% compared to the September quarter of 2024, with improvement across all products.”

“Domestic passenger revenue grew 5% y/o/y, supported by an acceleration in corporate sales, continue strength in premium cabins and an inflection in main cabin unit revenue growth.”

“Corporate sales were up 8% over prior year in the third quarter. Recent corporate survey results indicate that roughly 90% of companies expect their travel volume to increase or remain steady in 2026, 5 points higher than last year’s survey at this time.”

From Pepsi, a stock we own:

They saw 3% top line y/o/y revenue growth due to “An acceleration in organic revenue growth within our North America beverage business with Trademark Pepsi continuing to deliver volume and net revenue growth; A resilient international business which delivered its 18th consecutive quarter of at least mid single digit organic revenue growth - despite poor weather impacting some of our beverage markets; An improvement in global convenient foods organic volume trends.”

“we expect to mitigate the impact of higher supply chain costs (primarily related to the sourcing of certain global inputs and ingredients and related tariff impacts) moving forward. These higher costs represented a 3 percentage point headwind to our core EPS during the third quarter.”

From Costco’s monthly comp report:

“Food and sundries were positive mid-single digits. Better performing departments include candy, cooler, and deli. Fresh foods were up mid single digits. Better performing departments included meat and bakery.”

“Non-foods were positive high single digits. Better performing departments included jewelry, majors (like tv’s), and health and beauty. Ancillary business sales were up mid-single digits. Pharmacy, hearing aid, and optical were the top performers. Gas was up low single digits driven by volume increases y/o/y.”

Manheim on Tuesday released its September wholesale used vehicle data and said prices fell .2% m/o/m seasonally adjusted but were up 2% y/o/y. They said “As we close the books on Q3, we’ve continued to see wholesale values remain elevated against normal depreciation trends, even with the declines in September and right as tax incentives on EVs come to an end. Both new and used retail sales were fairly elevated over most of Q3, but we started to see some declines in the last few weeks of September. Simultaneously, we observed that weekly wholesale valuations declined a bit more than earlier in the month, as the relationship between supply on dealer lots and wholesale values remains strongly intertwined.”

If imports into the US are challenged because of tariffs and manufacturing is still in contraction it means we transport less stuff. On Tuesday the September Logistics Manager’s Index fell 1.9 pts m/o/m to 57.4, the lowest since March. In particular, the Transportation Utilization component fell 4.7 pts to 50 “which indicates no movement. This is the first time we have seen a reading this low for Transportation Utilization in September, which is generally a busy season in the freight market” said LMI.

Also of note, “Upstream respondents at the manufacturing and wholesale level have been relatively stagnant in terms of new inventories because so many of them front-loaded goods early in the year.”

Moving overseas, Taiwan’s exports in September rose 34% y/o/y, robust but below the estimate of 39%. Thanks to our tariffs on Taiwan, exports to the US slowed to the least since April though still remained strong.

Finally, it’s an interesting dynamic with the Japanese yen as it’s down for a 6th straight day, albeit very modestly today. Its weakness is certainly in response to the likelihood of Sanae Takaichi becoming the new PM who won’t want an October BoJ rate hike but that currency weakness in turn further stokes inflationary pressures. It is those inflationary pressures that cost Ishiba his job that Takaichi now can’t ignore.

BY Doug Kass · Oct 9, 2025, 9:20 AM EDT

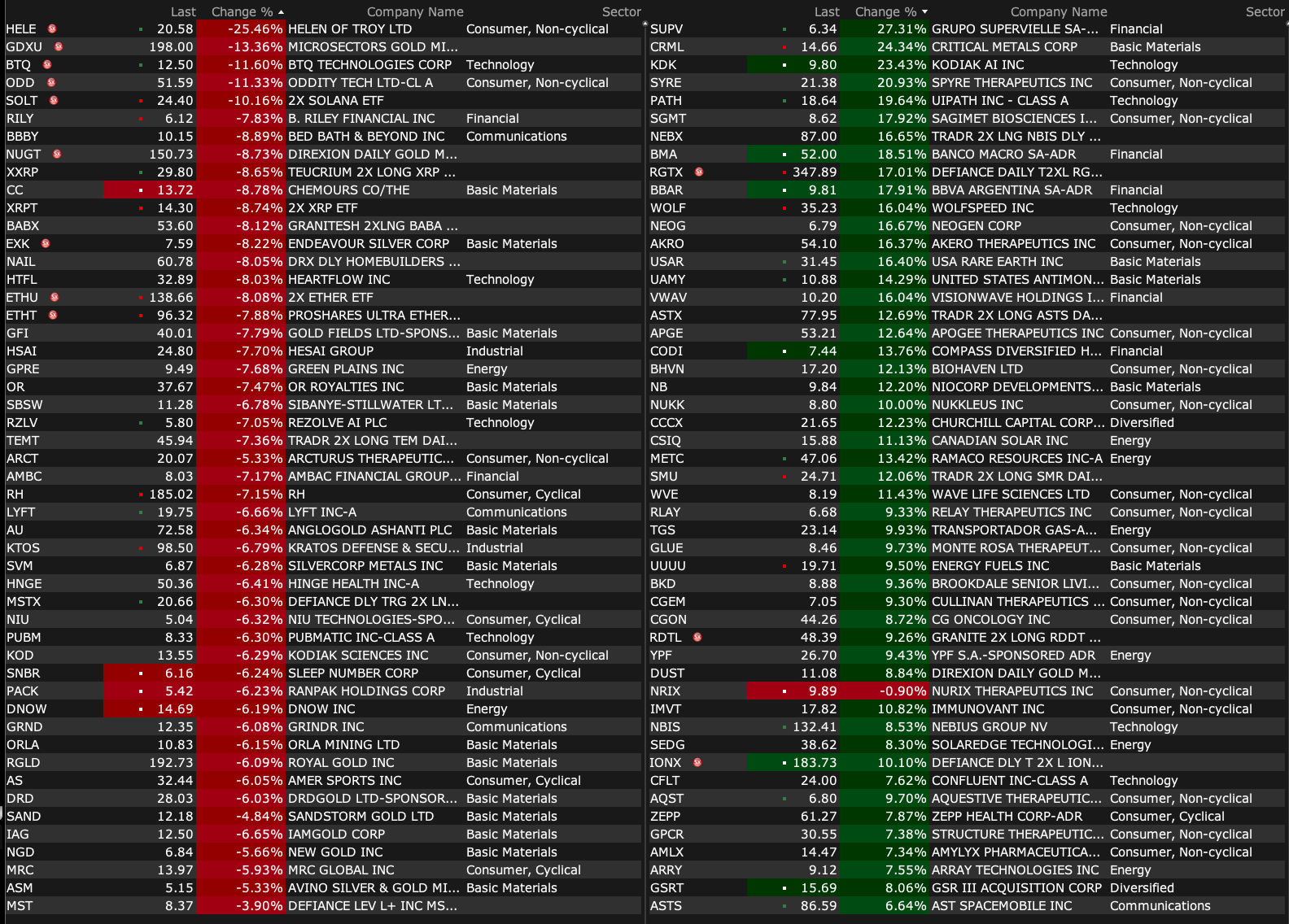

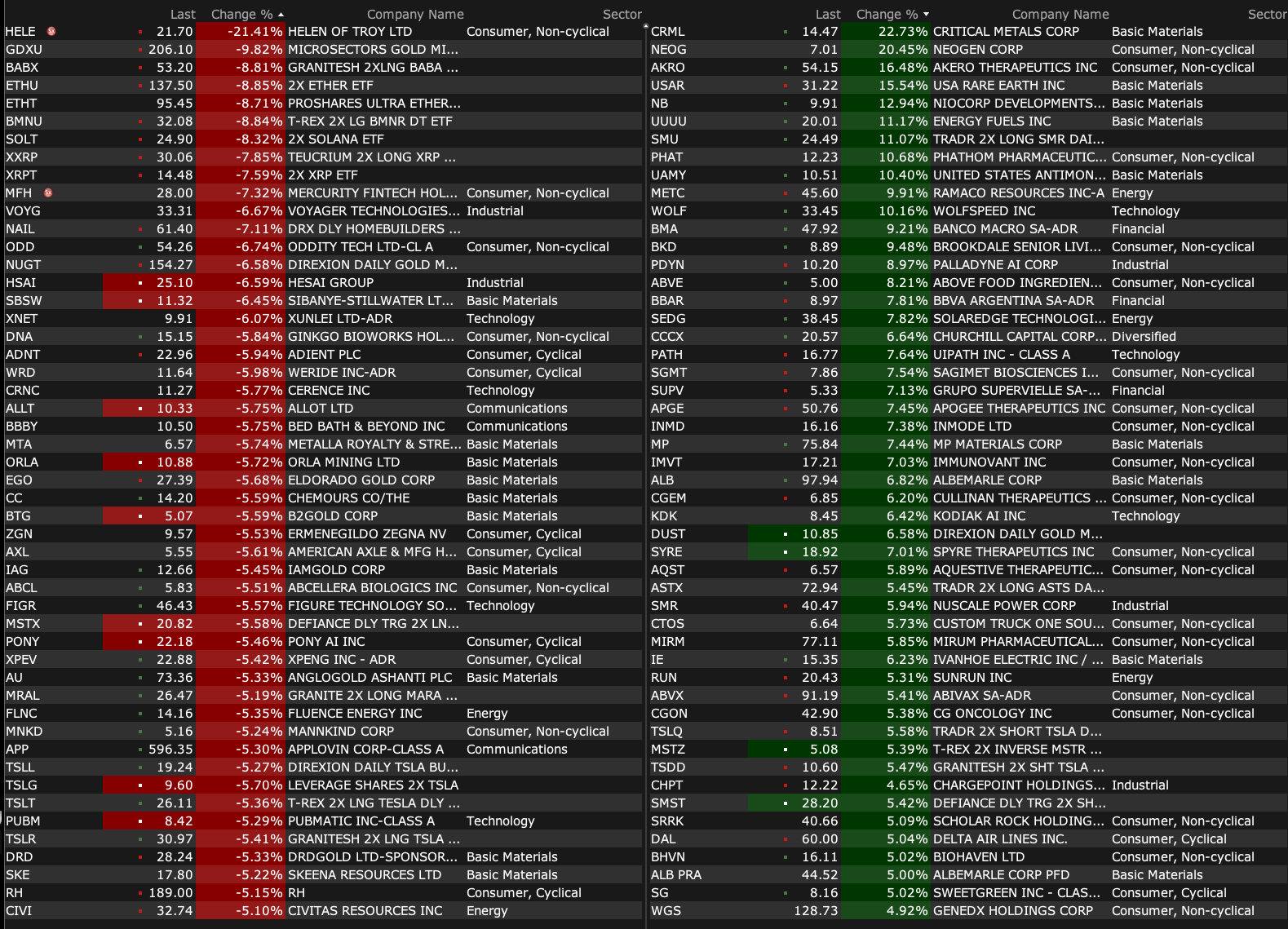

-RELL +20% (earnings)

-AKRO +18% (to be acquired by Novo Nordisk at $54.00/shr in cash in up to $5.2B deal)

-TLRY +14% (earnings, guidance)

-SERV +12% (DoorDash and Serve to bring Serve robots to DoorDash platform for autonomous deliveries across the US, starting in Los Angeles)

-BYRN +9.7% (earnings)

-NEOG +8.6% (earnings, guidance)

-USAR +7.3% (China tightens rare earth export curbs)

-DAL +6.4% (earnings, guidance)

-AAL +4.8% (higher in sympathy with DAL)

-IMMP +3.9% (announces Update for TACTI-004 (KEYNOTE-F91) Phase III Trial in First Line Non-Small Cell Lung Cancer)

-RGP +3.4% (earnings)

-HELE -18% (earnings, guidance)

-RACE -12% (guidance, provides long-term financial targets)

-AZZ -9.2% (earnings, guidance)

-BSET -4.8% (earnings)

-APGE -3.5% (prices 6.95M shares at $41/share; gross proceeds ~$300M)

-AISP -2.3% (announces exercise of warrants for $9.7M in gross proceeds at $4.50/shr

BY Doug Kass · Oct 9, 2025, 9:04 AM EDT

BY Doug Kass · Oct 9, 2025, 8:56 AM EDT

BY Doug Kass · Oct 9, 2025, 8:40 AM EDT

* What, us worry?

From Rolfy:

rolf thrane

16 minutes ago

BY Doug Kass · Oct 9, 2025, 8:05 AM EDT

Pepsico (PEP) had a slight beat on the top line and reported and in line bottom line.

The shares are gapping higher (+$2.50) on signs of more aggressive actions by management discussed in the press release.

I have sold my holdings in the name at $141.26.

As best as I can see, PEP is dead money for now (not an AI play!). That said, I don't see much downside and I view the stock as attractive longer term as Elliott Management catalyzes some actions.

I will discuss the EPS later.

BY Doug Kass · Oct 9, 2025, 7:35 AM EDT

BY Doug Kass · Oct 9, 2025, 7:20 AM EDT

Bonus — Here are some great links:

BY Doug Kass · Oct 9, 2025, 7:05 AM EDT

* Retail investors have purchased over $100 billion of equities in the last month...

* Retail's participation has doubled from the dot-com bubble!

The retail investing cohort cares little about fundamentals and more about FOMO (fear of missing out).

Join this group with systematic traders — algos and CTAs (who are also momentum investors) and other quant strategies (like risk parity) — and you have a market that violates many metrics of valuation (that I have observed in my Diary this year).

BY Doug Kass · Oct 9, 2025, 6:55 AM EDT

BY Doug Kass · Oct 9, 2025, 6:45 AM EDT

This is not a synchronized worldwide expansion, by any stretch of the imagination:

BY Doug Kass · Oct 9, 2025, 6:35 AM EDT

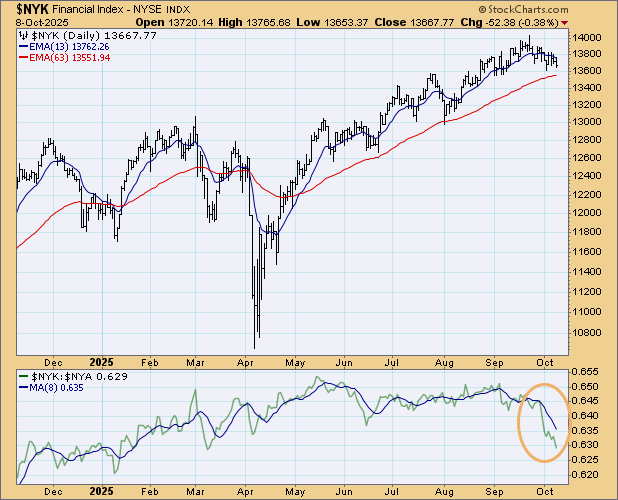

* Historically, a rollover in selected financials is a precursor to broader market weakness...

Over the last couple of days I have observed the conspicuous rollover in financials, which grew ever more obvious yesterday afternoon.

We remain short a wide swath of private equity, money center banks and brokerages.

Thus far, the semi-led market has ignored this.

From Wally:

This is not my father's market.

BY Doug Kass · Oct 9, 2025, 6:25 AM EDT

I added to trading short rental (HOOD) at about $150 (around 4:05 AM).

BY Doug Kass · Oct 9, 2025, 6:15 AM EDT

The S&P Short Range Oscillator is at 0.83% vs. -0.38%. That is back into overbought territory.

BY Doug Kass · Oct 9, 2025, 6:05 AM EDT

BY Doug Kass · Oct 9, 2025, 5:55 AM EDT

BY Doug Kass · Oct 9, 2025, 5:45 AM EDT