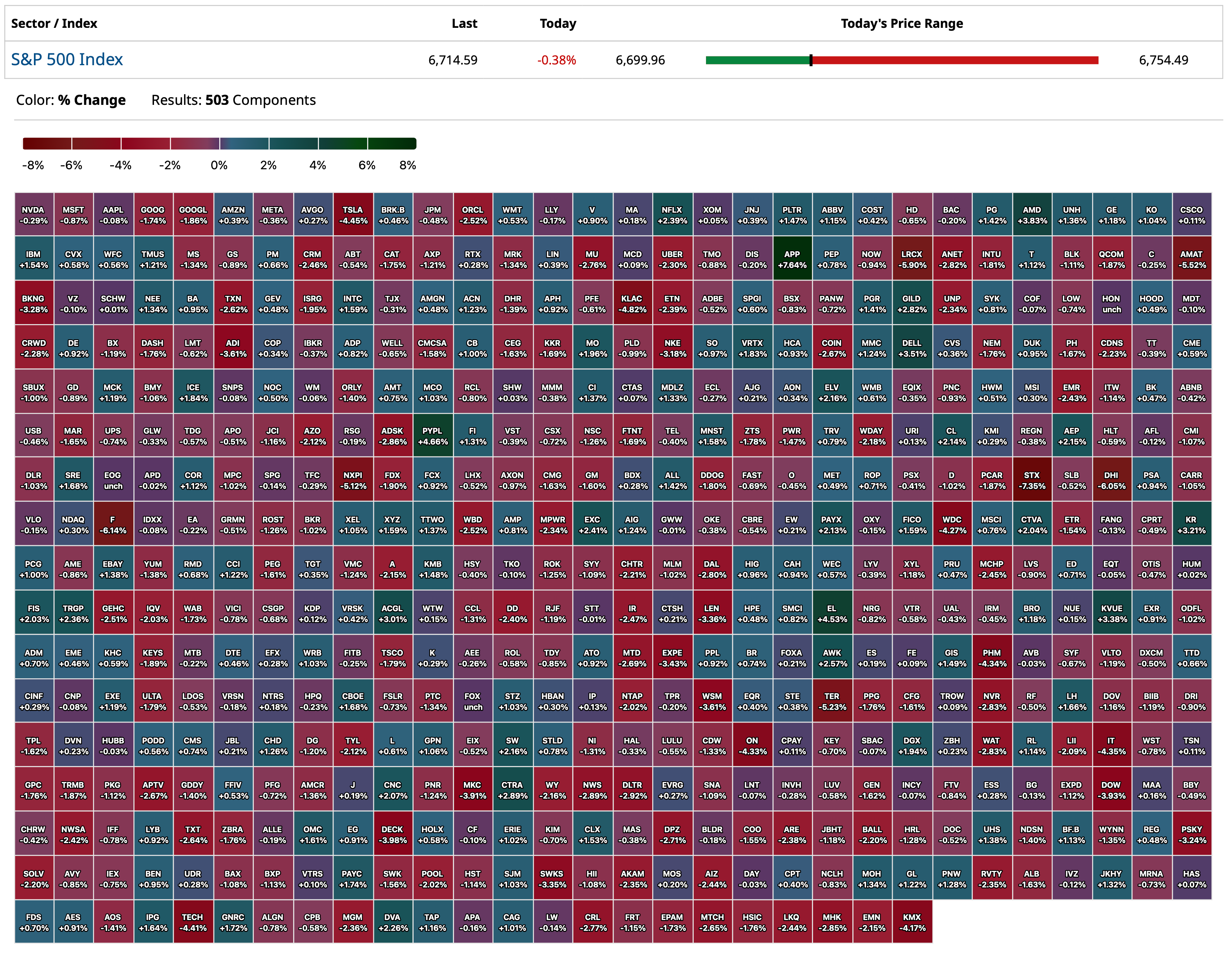

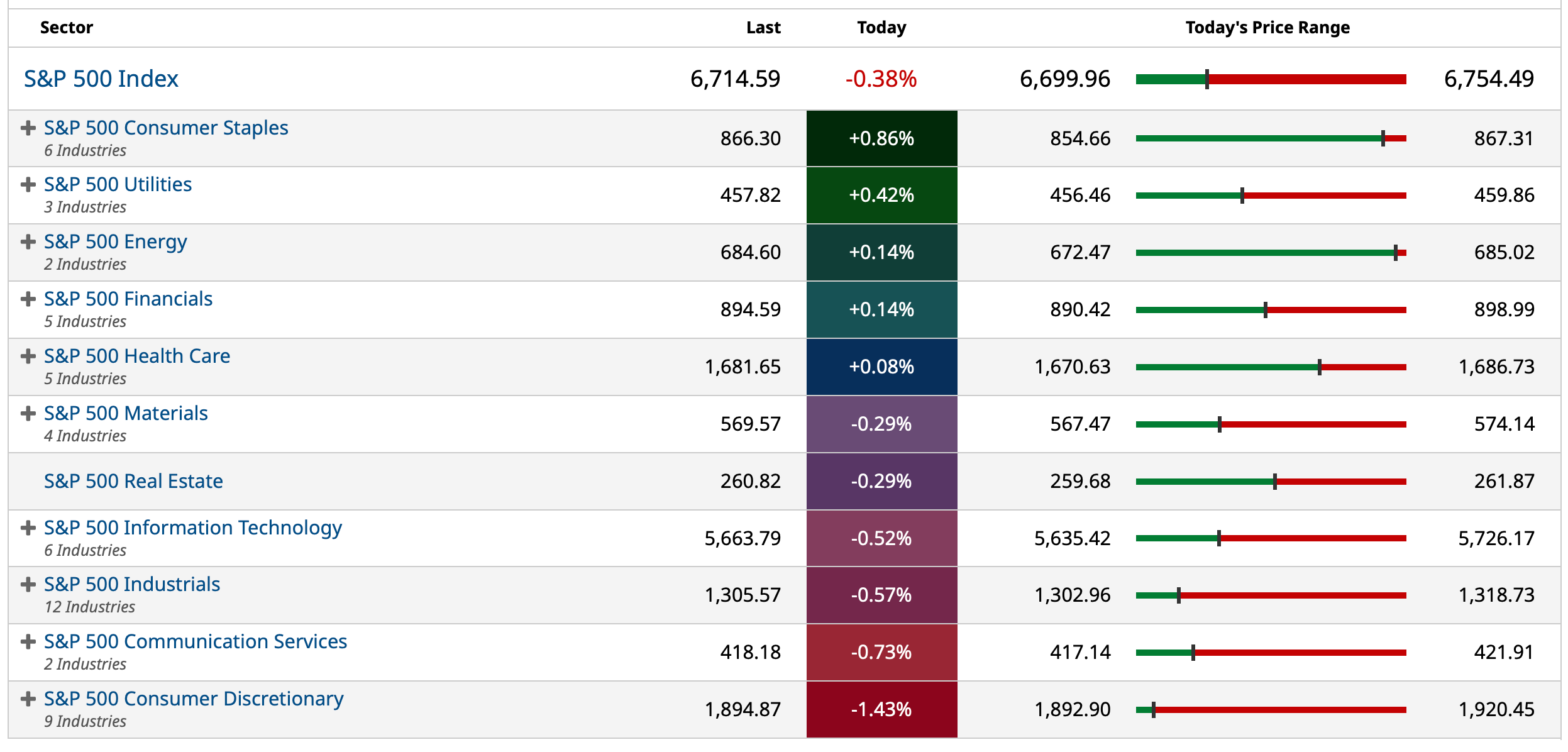

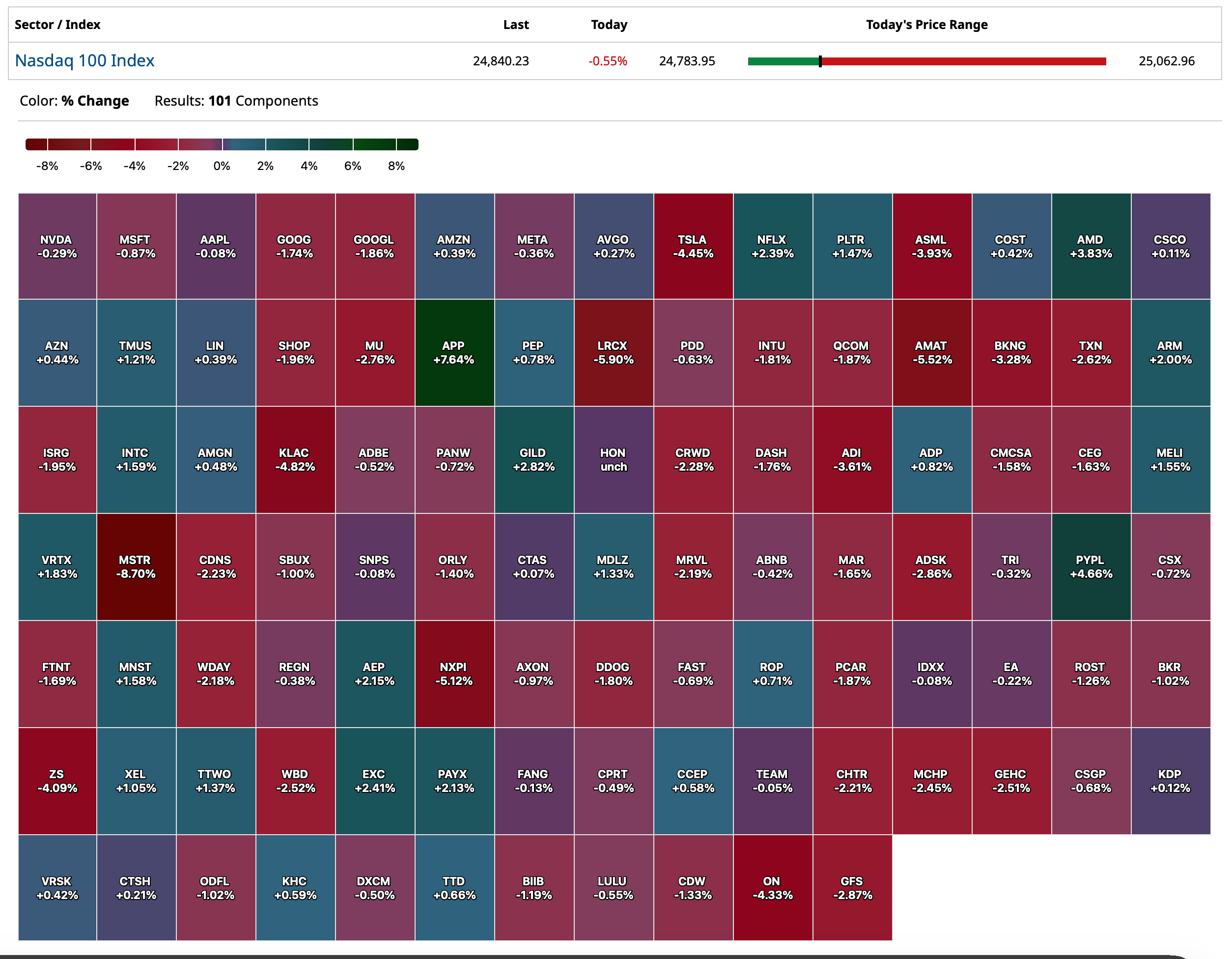

Tuesday Closing S&P 500 Heat Map

BY Doug Kass · Oct 7, 2025, 4:50 PM EDT

BY Doug Kass · Oct 7, 2025, 4:50 PM EDT

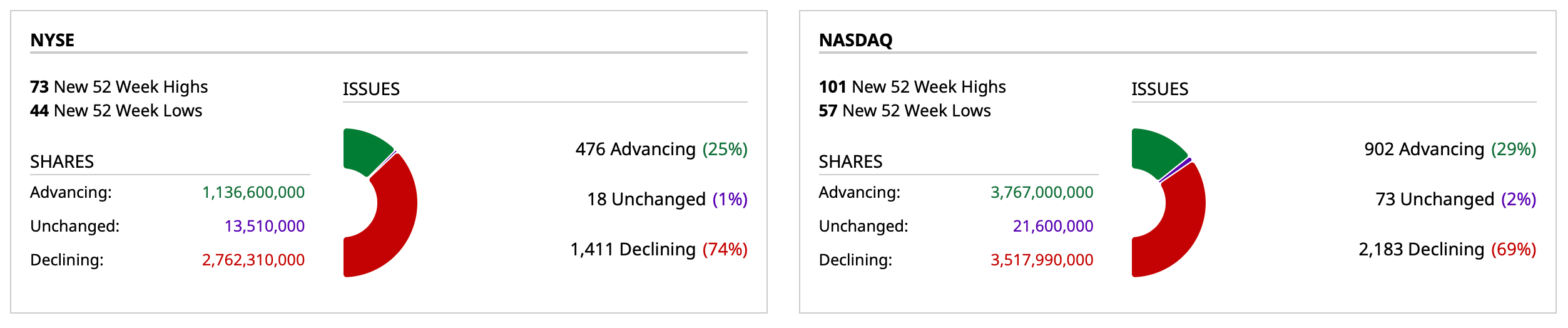

- NYSE volume 4% above its one-month average

- NASDAQ volume 11% above its one-month average

- VIX index: up 5.50% to 17.27

BY Doug Kass · Oct 7, 2025, 4:40 PM EDT

From Charlie:

BY Doug Kass · Oct 7, 2025, 4:10 PM EDT

BY Doug Kass · Oct 7, 2025, 3:58 PM EDT

I have a research call at 3 PM.

It should only take about 30 minutes.

BY Doug Kass · Oct 7, 2025, 3:02 PM EDT

Here are today's things:

* I shorted more indices — (SPY) at $671.29 and (QQQ) at $607.66.

* I then covered some of my Iindex shorts — SPY at $668.33 and QQQ at $603.82.

* I added to my already very large (GRNY) short at $25.55.

* I added to my (AMD) short at $212.30.

BY Doug Kass · Oct 7, 2025, 2:14 PM EDT

Consumer staples ( (KO) , (PEP) and (PG) ) doing what they are supposed to do in today's modest correction.

BY Doug Kass · Oct 7, 2025, 1:11 PM EDT

Here is an explanation of today's reversal lower.

Internal Oracle Data Show Financial Challenge of Renting Out Nvidia Chips — The Information

BY Doug Kass · Oct 7, 2025, 12:15 PM EDT

With S&P cash down by more than 35 handles I have covered some recent index shorts - (SPY) at $668.33 and (QQQ) at $603.82.

I am now small sized from medium sized.

I plan to reshort any strength.

BY Doug Kass · Oct 7, 2025, 11:49 AM EDT

Two sectors that have been conspicuously weak of late are homebuilders and private equity.

Here is my negative take on homebuilders: Doug's Daily Diary - TheStreet Pro

As to private equity - here are the potential headwinds that I see:

* Growing realization that their heady days of returns are over with them now relying on retail to raise money.

* They can’t monetize tens of thousands of companies on their balance sheet.

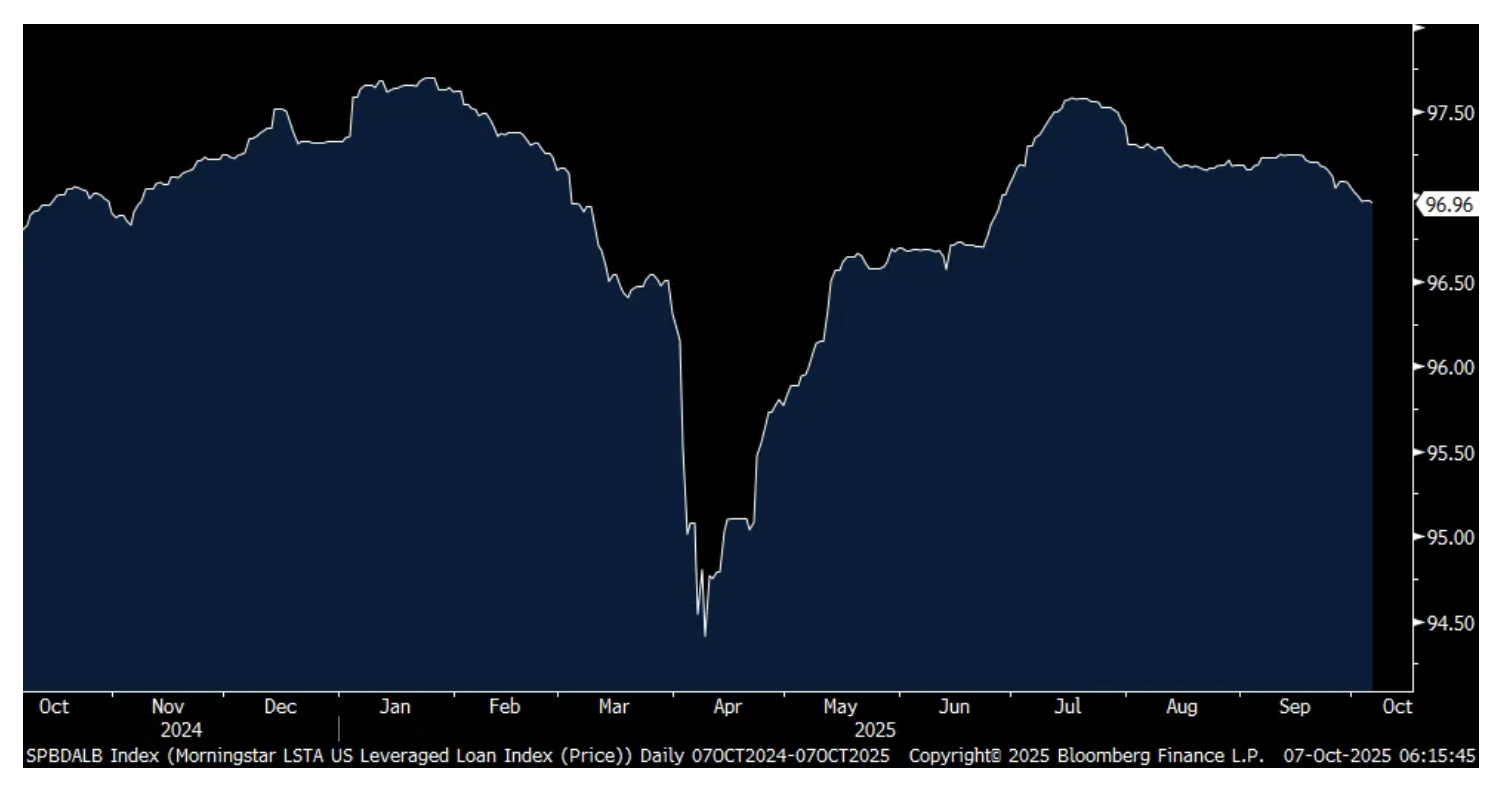

* Yesterday the leveraged loan index closed at the lowest since the end of June.

* If private credit blows up, they are holding the bag, along with retail.

Also:

* If Private Equity can’t sell their portfolio, performance fees are lower and those they can sell won’t generate big gains so again lowered performance fees

* Concerns about credit markets especially private credit given the possibility that large industry inflows reduced underwriting standards

* Private equity shares were (historically) very expensive heading into 2025

* Market doesn’t think Fed will cut rates that much or that cuts will have that much of effect on overleveraged companies

* I see the potential for lots of problems in their portfolios - private credit and private equity - especially if economy's growth moderates and equities mean revert

BY Doug Kass · Oct 7, 2025, 10:45 AM EDT

Unclear who is dumber:

-The AI

-The people that used AI for this, they should know by now

-The Aussie government, for spending money to do this stuff to begin with, probably wasting money on one more silly project as governments tend to do

Net/net, no matter what happens, soup to nuts, Gen AI seems to always lose money!

Read the story: www.theguardian.com

BY Doug Kass · Oct 7, 2025, 10:25 AM EDT

DarrylCGreen

1 hour ago

Some of my thoughts on AI.

In addition to the market trading I do. I invest in smallish private companies (5-25% stakes) that already have product market fit. I then work with the exec teams, sometimes joining them for a bit to help them scale or grow internationally (my experience). Since I´m operationally involved I can only do 2-4 at any given time.

I bring this up because right now 3 for 3, they are all economically successfully deploying AI-powered solutions. One is a pure-play AI solution. Returns on investment for clients with the pure-play solution are a measurable 2000%. It´s an easy sell and growing fast. So I can attest to the fact that there are some great efficiencies to be had with AI in it´s current incarnation.

It´s not without concerns though -

1) How do you maintain a competitive advantage when others have access to all the same tools as you? and

2) Based on the commentary I read here and elsewhere, I am quite certain that that the AI service providers are not charging us market rates for their services (i.e. what would be expected to cover costs and give investors return on capital if profit/cash flow were a consideration). The current economics of the solutions could go down significantly (or dissappear) if that were ever attempted.

So while i think the commentary here is sometimes too negative on what will be the ultimately value of AI tech, it feels alot like 1999 again for me. Indeed there will be huge opportunities and changes (big winners and big losers). Right now, the public market participants seem by-and-large FOMO´d. The time to invest in the infrastructure plays will be after prices normalize to what they can charge for their services not against what they are investing in providing the services.

So my conclusion on all this is that you can't buy the hype at the moment and you can't short the momentum (for anything but short-term trades). I will wait and continue to get experience on the implementation side of the market. And i hope that in the next year of so, there will be a good time to invest in NVIDIA shares etc. (traded long enough to know that will be when it really feels like it´s the wrong thing to do).

BY Doug Kass · Oct 7, 2025, 10:10 AM EDT

From Peter Boockvar:

I said a few weeks ago that we’ve reached a point that OpenAI is too big to fail with respect to its economic impact. ‘Too big to fail’ in terms of them being a major support to this whole AI data center buildout and tech stock market trade with financial tentacles reaching everywhere. Broadly speaking, the US economy and markets are essentially all in on this GenAI ecosystem construct to the point where there was about no US economic growth in the first half of 2025 without this buildout and the CapEx that took place. And we know the upper end consumer is highly dependent on the wealth created via its stock market holdings which is of course heavily dependent on this trade too.

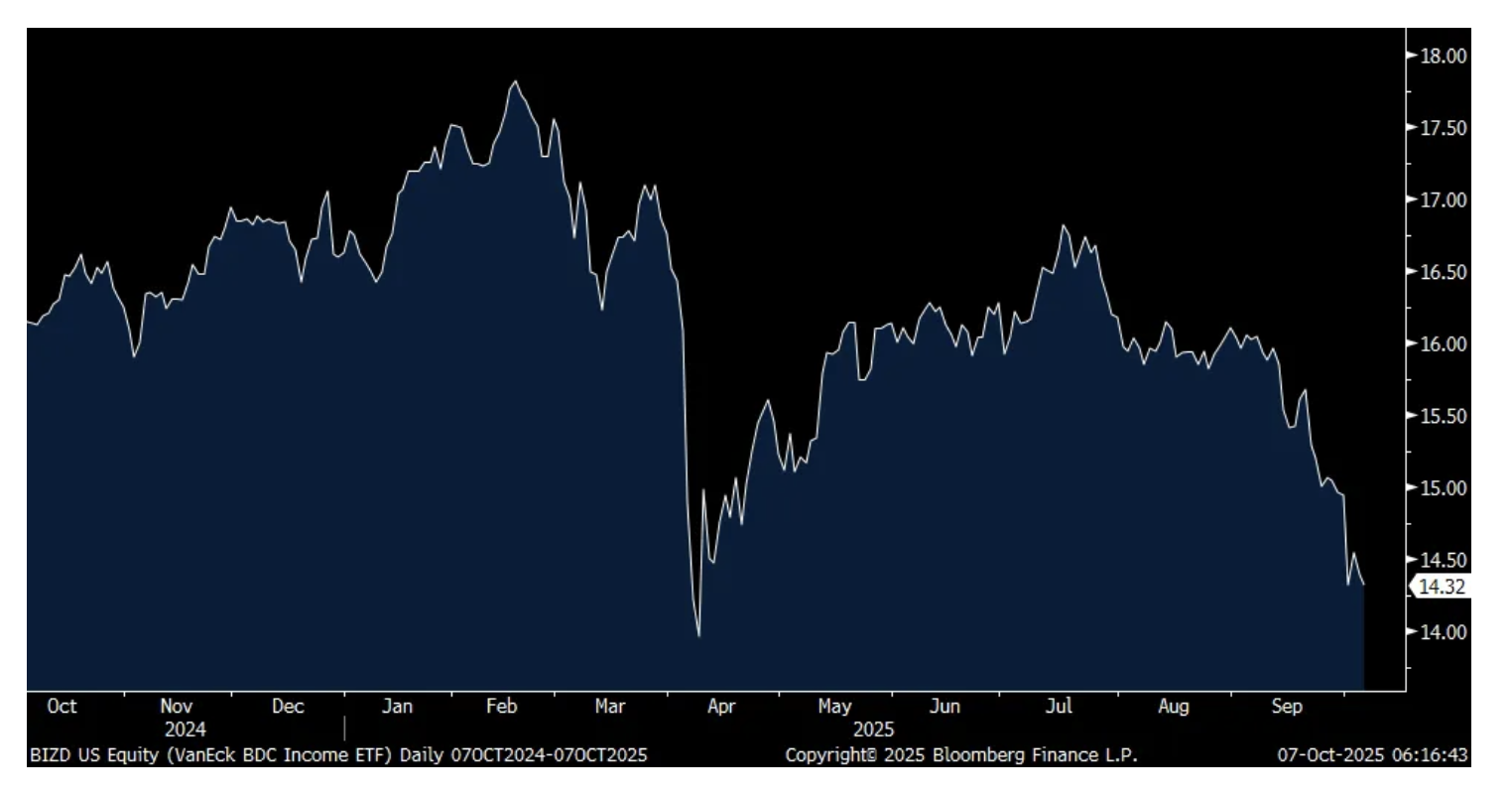

If you’re watching, like me, to see whether the private credit canaries are beginning to whistle in light of the things we’ve seen play out over the past month, the LSTA leveraged loan index yesterday closed at the lowest level since last June. The BIZD BDC etf closed at the lowest level since the April tariff panic. Something to watch indeed.

LSTA Leveraged Loan Index

BIZD

So maybe we have to wait until December to get that next BoJ rate hike. In an interview yesterday on Bloomberg, an economic advisor to the incoming PM Sanae Takaichi, named Etsuro Honda said “A rate hike in October is probably difficult in my view. It depends on the macroeconomic environment, but I don’t see a problem if it’s raised by 25 bps in December.”

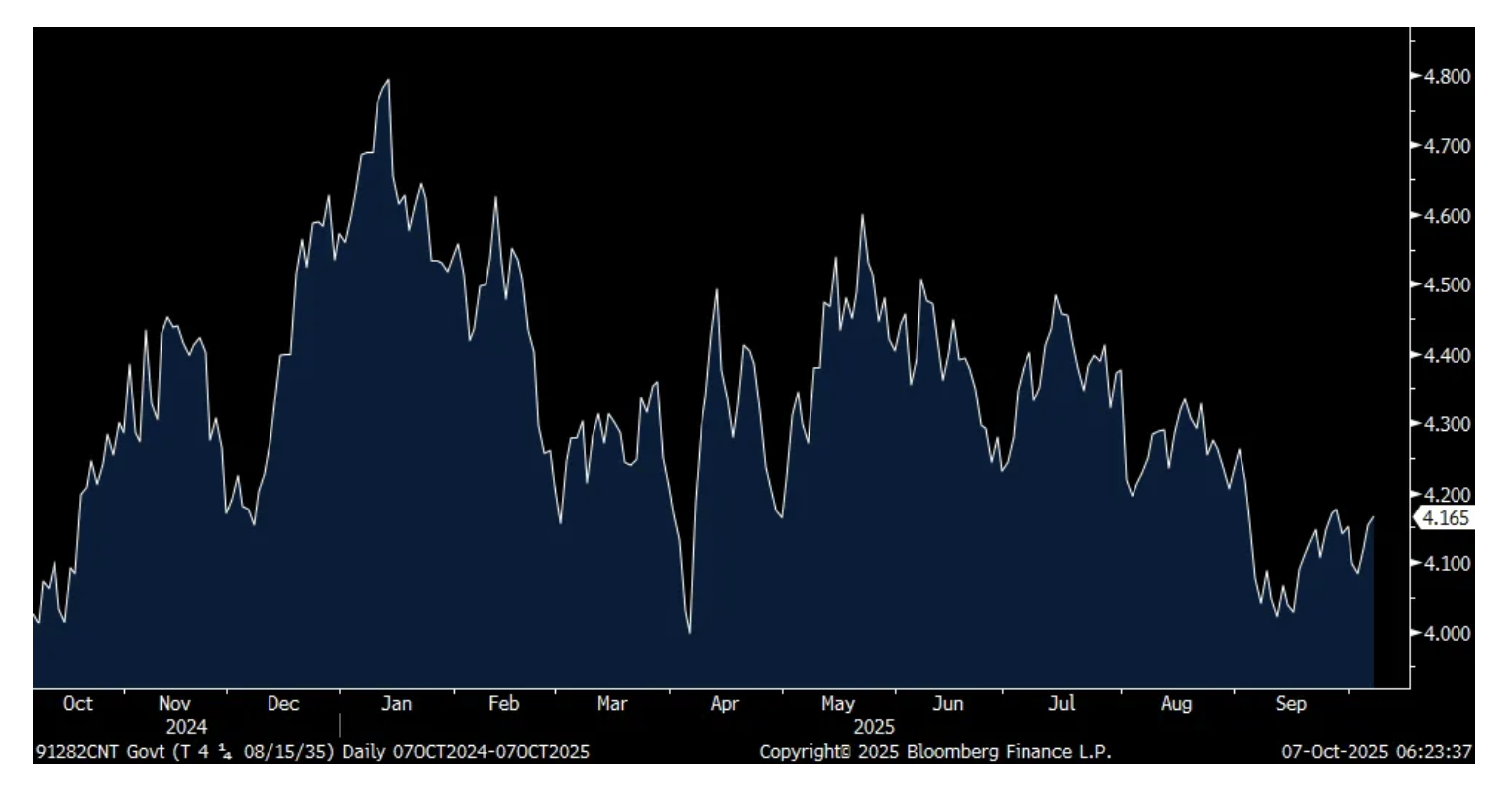

Regardless, as we saw yesterday the long end of the JGB yield curve is conducting policy on its own and they are raising rates. A decent 30 yr JGB auction today kept rates little changed overnight. Keep your eye on the US 10 yr yield of 4.18% (vs 4.16-.17% right now) and 4.76% on the 30 yr (vs 4.76% right now) as these are the high yields post the September Fed rate cut. There is a 10 yr note auction tomorrow and a 30 yr bond auction on Thursday. Yields in Europe are up between 1-2 bps today.

10 yr US yield

Gold is rising for a variety of reasons but the main one is that it’s become a wanted reserve asset around the world and no better a highlight than what we’ve seen with China’s holdings. In today’s September reserve asset data from China, it’s gold holdings have almost tripled over the past three years as seen in the chart below to $283b. And as seen, the holdings really took off in Q4 2022, soon after the US and EU decided to freeze half of Russia’s central bank reserves. Imagine the look on Xi Jinping’s face when that happened as they owned at the time about $1t of US Treasuries. Those holdings are now down to $731b. The difference is about what the increase in their gold holdings have been. No coincidence.

China’s Gold Holdings

China holdings of US Treasuries

Germany’s August factory orders unexpectedly fell by .8% m/o/m vs the estimate of up 1.2% and follows a 2.7% drop in July. The weakness in orders was seen in both the rest of the Eurozone and also non-Eurozone countries, mostly offset by a rise in domestic demand. Autos/parts was the main area of weakness, not surprisingly.

BY Doug Kass · Oct 7, 2025, 9:45 AM EDT

From The Guardian:

Deloitte will provide a partial refund to the [Australian] government over a $440,000 report that contained several errors, after admitting it used generative artificial intelligence to help produce it.

The Department of Employment and Workplace Relations confirmed Deloitte would repay the final installment under its contract, which will be made public after the transaction is finalized. It comes as one Labor senator accused the consultancy firm of having a “human intelligence problem.” . . .

University of Sydney academic, Dr Christopher Rudge, who first highlighted the errors, said the report contained “hallucinations” where AI models may fill in gaps, misinterpret data, or try to guess answers.

BY Doug Kass · Oct 7, 2025, 9:35 AM EDT

-TMQ +242% (US will take 10% stake and get warrants to purchase an additional 7.5% of Trilogy Metals)

-SPRB +56% (momentum following after receiving U.S. FDA Breakthrough Therapy Designation for Tralesinidase Alfa Enzyme Replacement Therapy (TA-ERT) in Sanfilippo Syndrome Type B (MPS IIIB))

-LXEO +31% (U.S. FDA open to pooling data from ongoing Phase I/II studies of LX2006 with pivotal data to support a BLA for Accelerated Approval)

-TELO +22% (announces New Findings in a Prostate Cancer Model Demonstrating Telomir-1 Also Resets DNA Methylation of Tumor Suppressor Genes Implicated in Two of the Most Persistent Challenges in Oncology-Metastasis and Treatment Resistance)

-LIDR +21% (has begun shipments of Apollo to a global defense contractor for use in manned and unmanned aerial vehicles)

-AMKR +13% (breaks ground on new Semiconductor Advanced Packaging and Test Campus in Arizona; Expands investment 3.5x to $7B)

-CLIR +9.4% (secures 32-Burner Engineering Order)

-AMTX +6.8% (Aemetis California Ethanol Plant Drives Substantial Carbon Intensity Reduction using Praj Low-Carbon MVR System)

-DELL +5.4% (guidance from Investor Day event)

-YRD +4.6% (announces significant update to its Magicube Agent Platform, a proprietary multi-agent AI system)

-IBM +4.4% (IBM and Anthropic partner to advance enterprise software development with proven security and governance)

-KAPA +4.1% (to Present Positive Safety and Efficacy Data from Phase 2 Prostate Cancer Trial at ESMO 2025)

-AMD +3.9% (Jefferies Raised AMD to Buy from Hold, price target: $300)

-PROF +3.8% (reports prelim Q3 revenue)

-ICE +3.6% (to invest up to $2B in Polymarket)

-PYPL +3.6% (unveils PayPal Ads Manager)

-STZ +3.2% (earnings, guidance)

-EAT +2.2% (JPMorgan Chase and Co Raised EAT to Overweight from Neutral, price target: $175)

-CRWV +2.1% (to acquire Monolith, expanding AI Cloud platform into industrial innovation)

-BMEA -23% (files to sell common stock of an indeterminate size)

-AEHR -20% (earnings)

-CPSH -16% (prices 3.0M shares are $3.00/shr in $9.0M offering)

-BTM -10% (files to sell $15M Registered Direct Offering of Class A Common Stock at $3.50/shr)

-ASTS -7.9% (files to sell $800M in stock)

-SEI -4.8% (prices upsized offering of $650M of 0.25% convertible senior notes due 2031)

-DLTR -3.2% (hearing Jefferies Cuts DLTR to Underperform from Hold, price target: $70)

-GTLB -2.8% (Mizuho Securities Cuts GTLB to Neutral from Outperform, price target: $52)

-JNJ -2.5% (release ACUVUE OASYS MAX 1-Day and Icotrokinra data in ulcerative colitis drug data)

-MKC -2.3% (earnings, guidance)

BY Doug Kass · Oct 7, 2025, 9:28 AM EDT

BY Doug Kass · Oct 7, 2025, 9:00 AM EDT

BY Doug Kass · Oct 7, 2025, 8:35 AM EDT

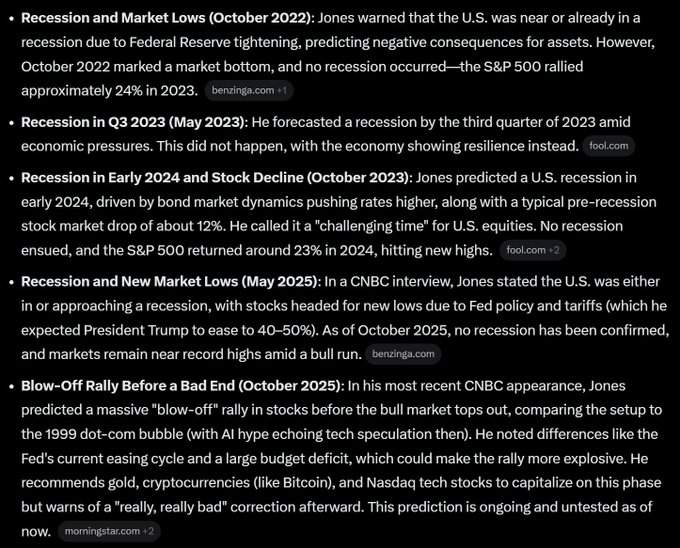

Paul Tudor Jones' Confident Market View Was Greeted Uncritically By Fin TV

* But, what is his record (for free advice)?

BY Doug Kass · Oct 7, 2025, 8:25 AM EDT

* More on the AI 'deals'

From Bloomberg's Matt Levine:

The basic situation is that if OpenAI announces a big partnership with a public company, that company’s stock will go up. Today OpenAI announced a deal to buy tens of billions of dollars of chips from Advanced Micro Devices Inc., and AMD’s stock went up. As of noon today, AMD’s stock was at $213 per share, up about 29% from Friday’s close; it had added about $78 billion of market capitalization.

How do those negotiations go? Like, schematically:

Read the rest here.

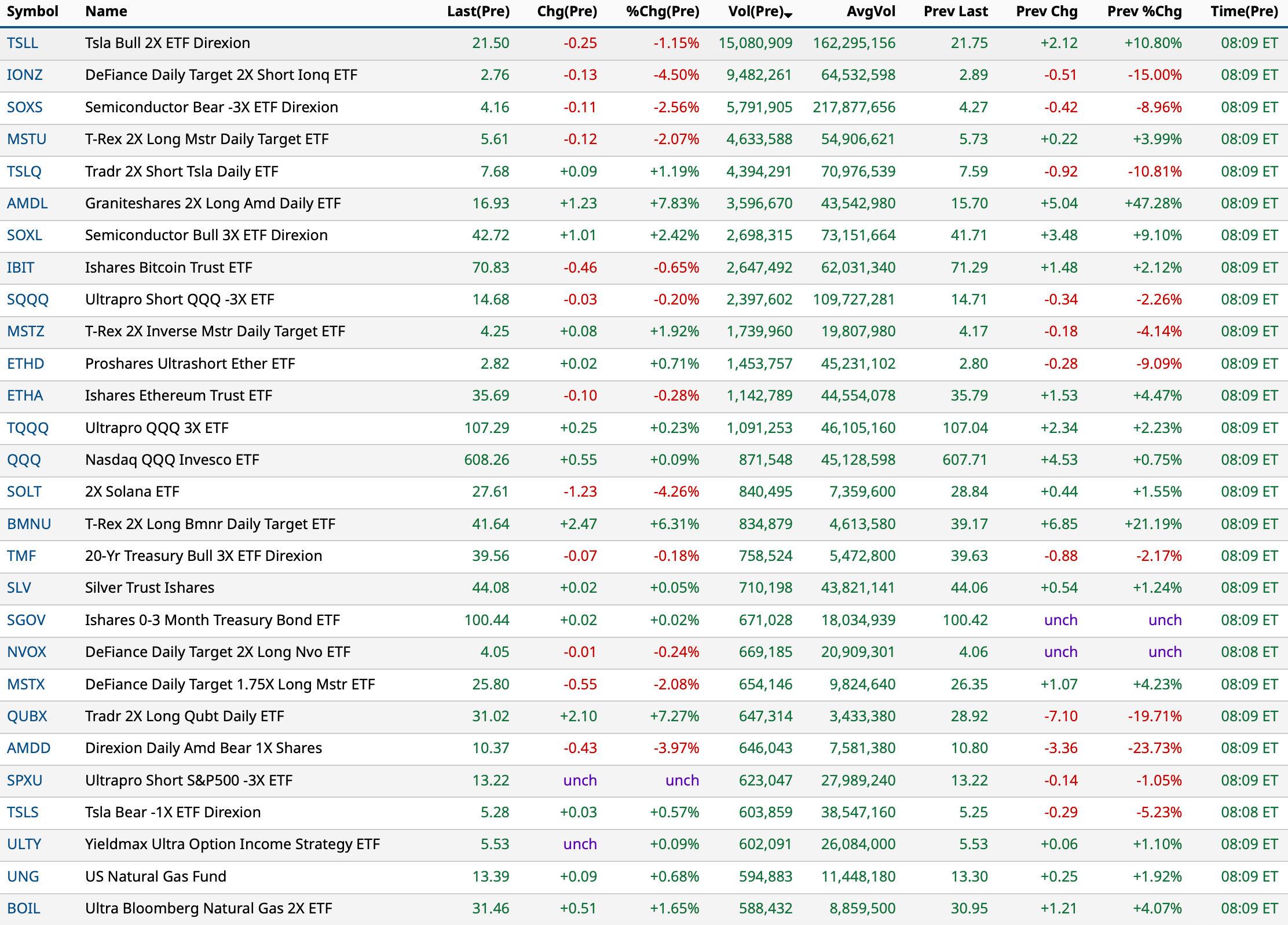

BY Doug Kass · Oct 7, 2025, 8:09 AM EDT

I was quoted several times in this Washington Post column by Bethany McLean:

AI Will Trigger Financial Calamity. It'll Also Remake The World

Here's an excerpt:

“AI could eventually cure cancer, end poverty, and even bring world peace,” wrote Dario Amodei, the founder of Anthropic, in a 14,000-word piece entitled “Machines of Loving Grace.”

“The house of cards is going to start crumbling,” Sasha Luccioni, a researcher at the artificial intelligence start-up Hugging Face, told the New York Times recently. “The amount of money being spent is not proportionate to the money that’s coming in.”

The conflicting perspectives are head-spinning in their extremes. On Sept. 22, OpenAI and chipmaker Nvidia announced yet another deal involving sums of money that are vast beyond comprehension. Nvidia agreed to invest up to $100 billion — about the size of New York City’s entire 2024 budget — in OpenAI and in turn provide it with hard-to-get chips.

For believers in Amodei’s forecast, the deal added weight to the idea that when it comes to investing in AI, too much is not enough. The announcement added nearly $160 billion to Nvidia’s market value, which itself has increased by some $4 trillion over the last three years. But for skeptics, it’s another dangerous sign of excess, because such deals, in which players in the AI ecosystem are exchanging money, are simply financial tricks that are camouflaging the evidence of a bubble that is about to burst.

“The AI industry is now buying its own revenue in circular fashion,” wrote skeptic Doug Kass, who runs hedge fund Seabreeze Partners, in a recent piece. It’s precisely what happened in the dot-com boom — except then we called it “roundtripping.” Or at least, we called it that after the crash.

But the consequences this time are much, much bigger. As Neil Dutta, the head of economic research at Renaissance Macro, first pointed out in a tweet, the capital expenditures made by a small number of companies are now contributing more to GDP than the spending of all of America’s consumers. “Wonder if the black holes ultimately consume each other as well as our economy and power grid in the process?” Kass asked.

BY Doug Kass · Oct 7, 2025, 8:00 AM EDT

kdog

these shorts are getting painful

Dougie Kass

In the aggregate I make money on my shorts, but it is difficult. Most don't have the patience or the analytical skills to do bottoms up, individual stock shorting. They tend to short the most popular and best performing stocks.

As I write repeatedly, most retail investors should not short:

BY Doug Kass · Oct 7, 2025, 7:45 AM EDT

Melanie Mitchell:

BY Doug Kass · Oct 7, 2025, 7:25 AM EDT

BY Doug Kass · Oct 7, 2025, 7:10 AM EDT

Dark Helmet: "I am your father's brother's nephew's cousin's former roommate."

Lone Starr: "What's that make us?"

Dark Helmet: "Absolutely nothing."

- Spaceballs Spaceballs [1987]: I Am Your Father's Brother's Nephew's Cousin's Former Roommate

The AMD/OpenAI deal is interesting. Here we go again. I thought the way a capitalistic economy works is company A makes something and company B buys it. In theory that is the case, except when it comes to AI, where the whole thing once again seems to be a circular relationship of press releases, self-dealing, business buying and entirely dis-economic business relationships. This short video (which I published yesterday afternoon) is a good summary of how the economics of AI work.

Key line from the (AMD) press release:

“As part of the agreement, to further align strategic interests, AMD has issued OpenAI a warrant for up to 160 million shares of AMD common stock, structured to vest as specific milestones are achieved. The first tranche vests with the initial 1 gigawatt deployment, with additional tranches vesting as purchases scale up to 6 gigawatts. Vesting is further tied to AMD achieving certain share-price targets and to OpenAI achieving the technical and commercial milestones required to enable AMD deployments at scale.”

Beyond the fact that this sounds about as firm as gelatin (as many of these announcements do) it is also a bit curious. OpenAI loses money hand over fist. In theory, after accounting for the equity give-away by AMD as part of the deal, I suspect AMD will have given more away in equity than the profit they will make from whatever theoretical chip sales they will ultimately make to OpenAI.

Once again, everyone loses money in the whole AI lack of value chain.

Yet, AMD's stock price is up 25% on this press release. This is the biggest move the stock has had in a decade, and last time it had its big move, it had not much market cap. This move is about $80 billion in market cap. I guess the markets reward equity dilution and buying business these days.

Profits shmofits.

Not long ago, Nvidia (NVDA) announced a theoretical $100 billion investment in OpenAI. I wonder if NVDA is happy their theoretical money is going towards buying theoretical chips from their competitor at their own expense? NVDA stock incidentally is down a whopping 1% on this news and a 1% move is probably an average day for that stock, at best. Oracle (ORCL) should make sure to add all of this to their slide deck when they report their quarter that misses revenue and EPS.

One last point...

When you are at the point when even Elon Musk is questioning these deals (ergo he of Tesla (TSLA) /Solar City fame and numerous other shenanigans), you know there are issues.

I would also say, Elon, you are a smart guy, I wonder why you would not ask the same terms as well of both NVDA and AMD re xAI? And why wouldn’t all of your competitors?

Hopefully, you guys are all smart enough to not use AI to do the Black Scholes calculation and price the value of the warrants!

It is all quite the slippery slope for everyone.

As previously mentioned, I thought the Fermi (FRMI) IPO took the cake ($19 billion for a business plan with no revenue), but I keep being surprised.

Tweet subtweet and the tweet that follows:

BY Doug Kass · Oct 7, 2025, 6:50 AM EDT

BY Doug Kass · Oct 7, 2025, 6:36 AM EDT

BY Doug Kass · Oct 7, 2025, 6:25 AM EDT

From JPMorgan:

US: Stocks closed higher led by NDX. Catalysts in the US remain muted as the government shutdown delays the data release. The OpenAI/AMD deal triggered another rally in AI/Tech theme; AMD added 25% today. Outside tech, Rare Earth, Crypto Exposure and Meme Stocks were among the top performing baskets. Retail and Housing were the main laggards. Outside the US, political development in Japan and France were the focus over the weekend.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Stocks closed higher led by Tech given the limited macro data and OpenAI/AMD deal; AMD added 25%, representing ~30% of the SPX total gains today. The rally today was relatively narrow: 52% of the SPX stocks actually finished lower on the day. Investors conversations have been reflecting some concerns over AI/Tech valuation into the earnings season. Below is a repost today’s morning note:

· AI / TECH INTO EARNINGS SEASON (a repost from today’s morning note) – Recent client conversations reflect the concerns over Mag 7 earnings season specifically positioning and valuation. Positioning Intel tells us that the recent rally in AI / Tech put positioning back to highs (L/S ratio ~98th %-tile and net exp >2z). On valuation, we have seen earnings growth estimates for Tech increased to 20.9% from 15.9% as of June 30, per FactSet. Specifically, 81% of the stocks in the Tech sector has seen increases to their EPS estimates, led by NVDA (from $1.17 to $1.24) and Apple (from $1.65 to $1.76). The growing positive revisions within the Tech sector could potentially create a higher bar for this upcoming earnings season. Tech and Comm Srvcs have added 22.7% and 22.4% YTD vs. SPX’s 14.2% total return.

o US MKT INTEL – While we maintain the view that resilience of US economy and consumers should continue to support Equities, leading to a continued broadening of the rally which could come at the expense of TMT. To play a broadening, and excluding TMT, we continue to prefer cyclicals sectors such as Financials, especially given the positive comments on consumers from major banks during a September industry conference.

BY Doug Kass · Oct 7, 2025, 6:15 AM EDT

The S&P Short Range Oscillator is now at 0.41% v 0.56% — that's slightly overbought.

BY Doug Kass · Oct 7, 2025, 6:05 AM EDT

Position: Short SPY M QQQ M

By Doug Kass Oct 6, 2025 6:55 PM EDT

BY Doug Kass · Oct 7, 2025, 5:55 AM EDT

* At 4:55 AM

Adding to Index shorts:

* SPY $671.16

* (QQQ) $607.49

BY Doug Kass · Oct 7, 2025, 5:45 AM EDT