Monday Night Shorts (Of an Index-Kind - 6:30PM)

- SPY $671.75

- QQQ $607.89

BY Doug Kass · Oct 6, 2025, 6:55 PM EDT

BY Doug Kass · Oct 6, 2025, 6:55 PM EDT

BY Doug Kass · Oct 6, 2025, 4:40 PM EDT

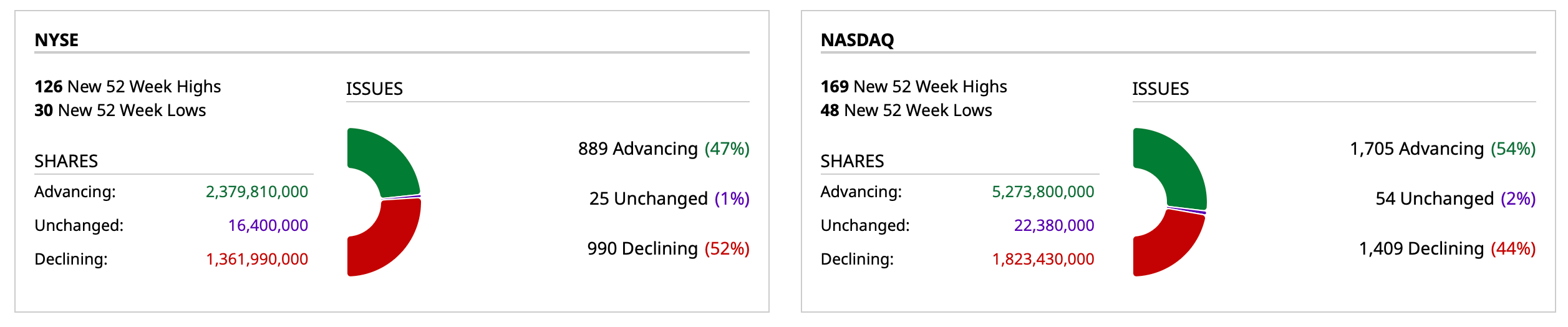

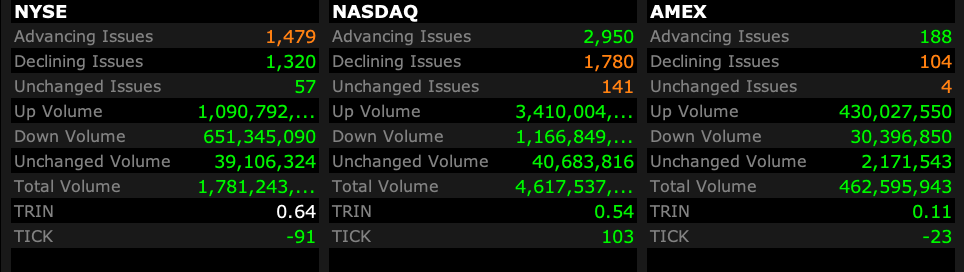

- NYSE volume 9% above its one-month average

- NASDAQ volume 13% above its one-month average

- VIX index: down 1.68% to 16.37

BY Doug Kass · Oct 6, 2025, 4:28 PM EDT

BY Doug Kass · Oct 6, 2025, 3:30 PM EDT

BY Doug Kass · Oct 6, 2025, 2:54 PM EDT

BY Doug Kass · Oct 6, 2025, 2:30 PM EDT

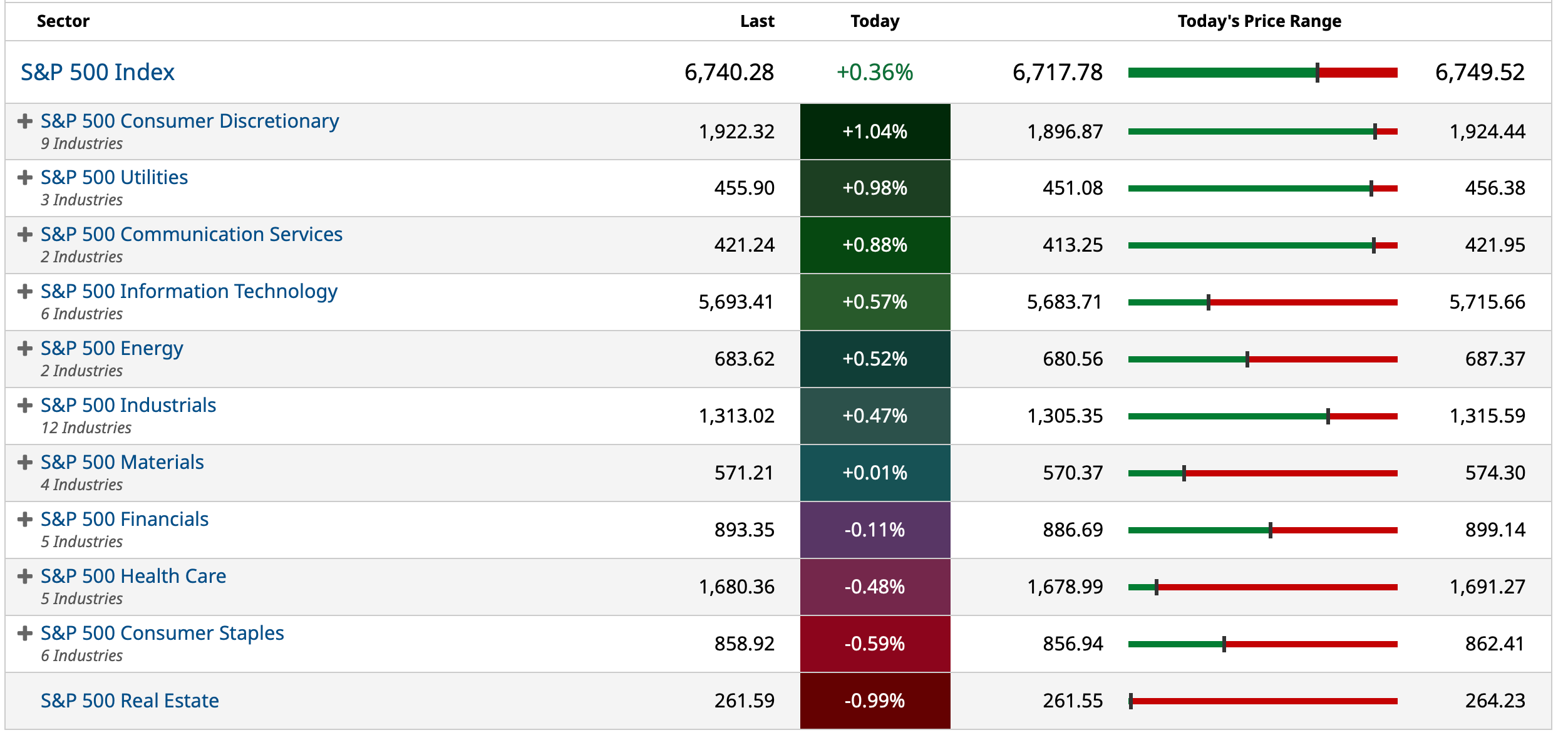

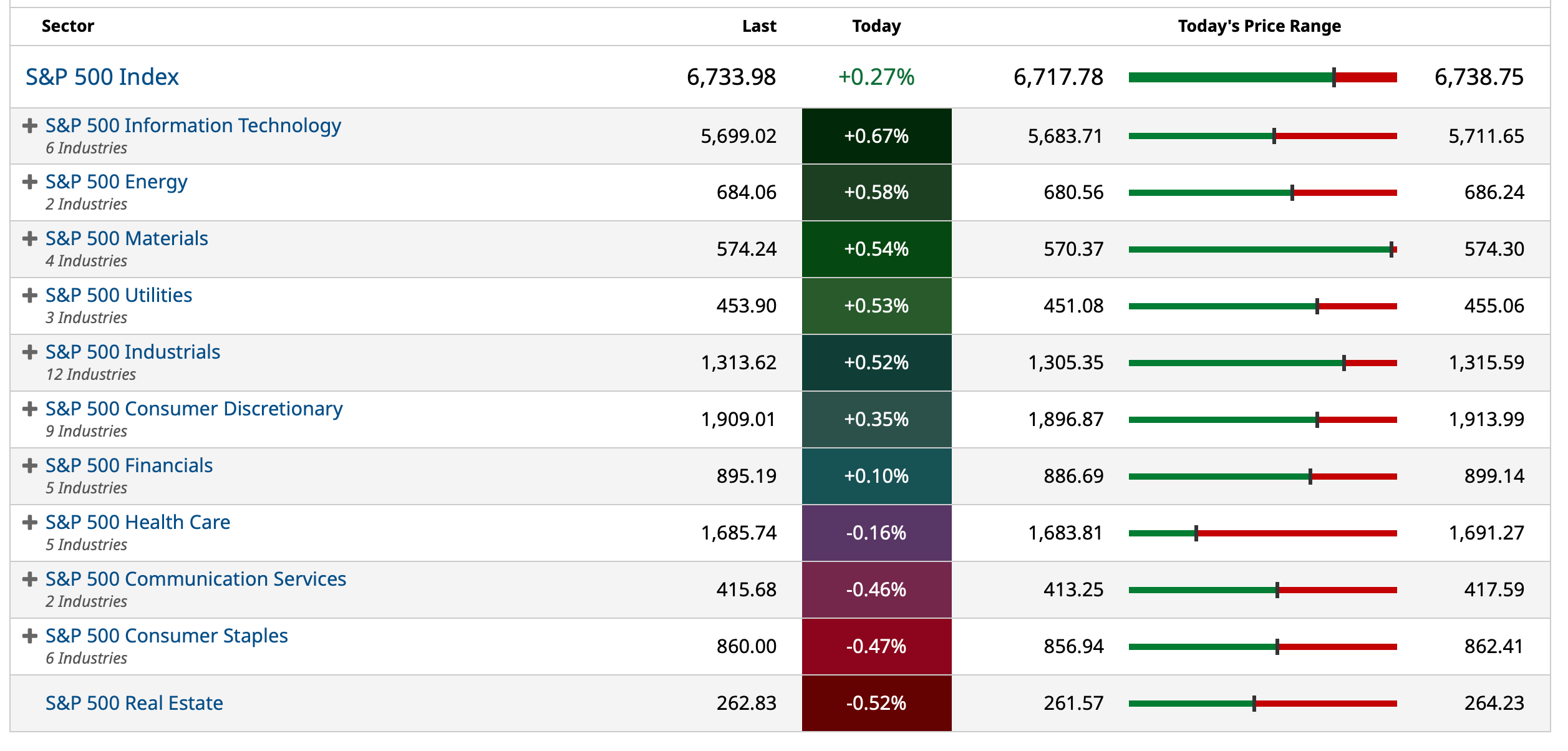

* Market structure changes (to passive investing) have put value investors out of business...

I wasn't being facetious about this tweet:

The long side is all about AI all the time — now in the extreme.

Value stocks are getting no or limited play whatsover (consistent with David Einhorn's comments two years ago and, again, four months ago.

Meanwhile individual short ideas — bottom up ideas, away from technology — are actually thriving.

Some examples of this today include (in our portfolio) Winnebago (WGO) (-$2 or -4.5%), RCI Hospitality Holdings (RICK) (-$3 or -8%), Starbucks (SBUX) (-$4 or -4%).

No doubt Ben Graham is rolling over in his grave today.

BY Doug Kass · Oct 6, 2025, 1:41 PM EDT

BY Doug Kass · Oct 6, 2025, 12:58 PM EDT

BY Doug Kass · Oct 6, 2025, 12:05 PM EDT

Take it from the Ginger Baker of investing, Sven Henrich:

BY Doug Kass · Oct 6, 2025, 11:18 AM EDT

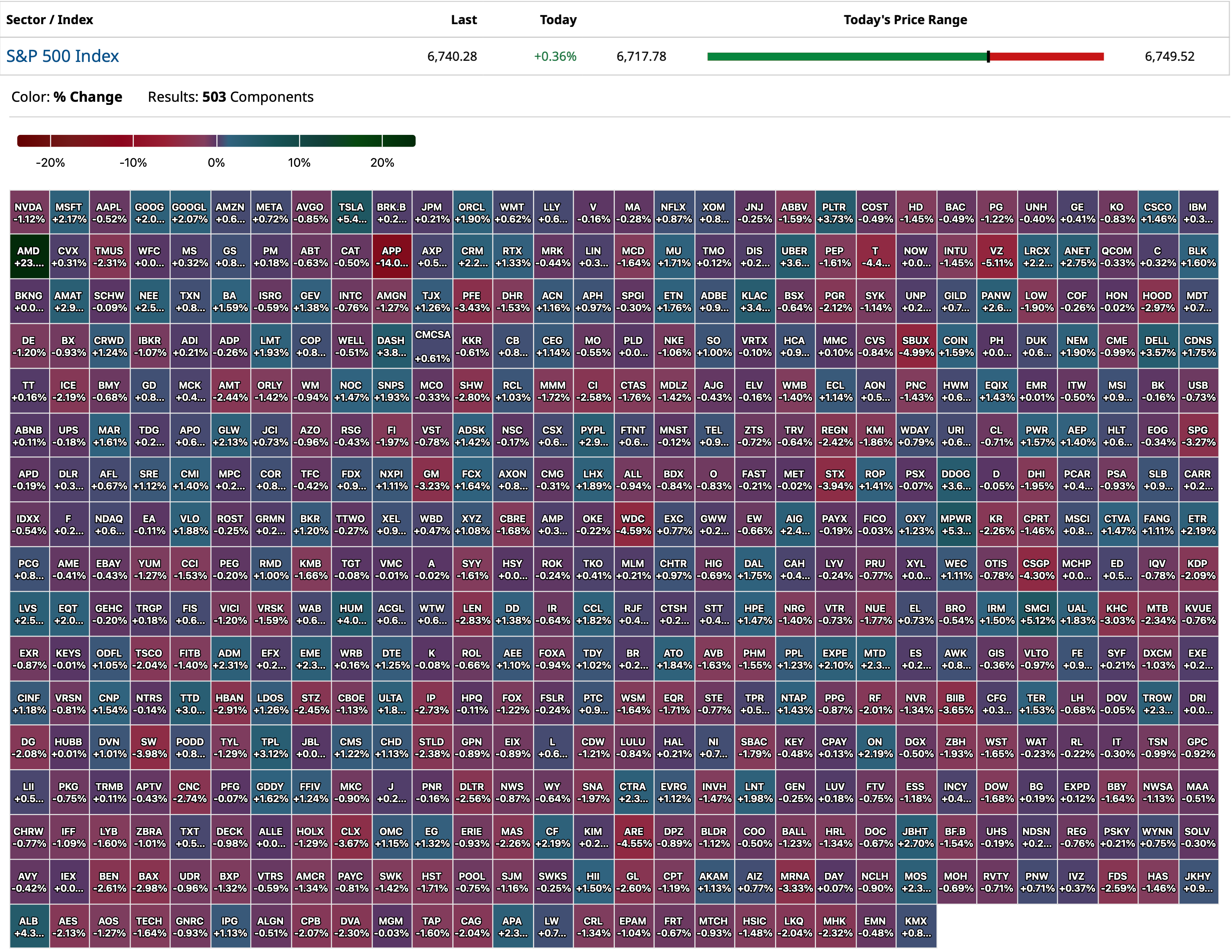

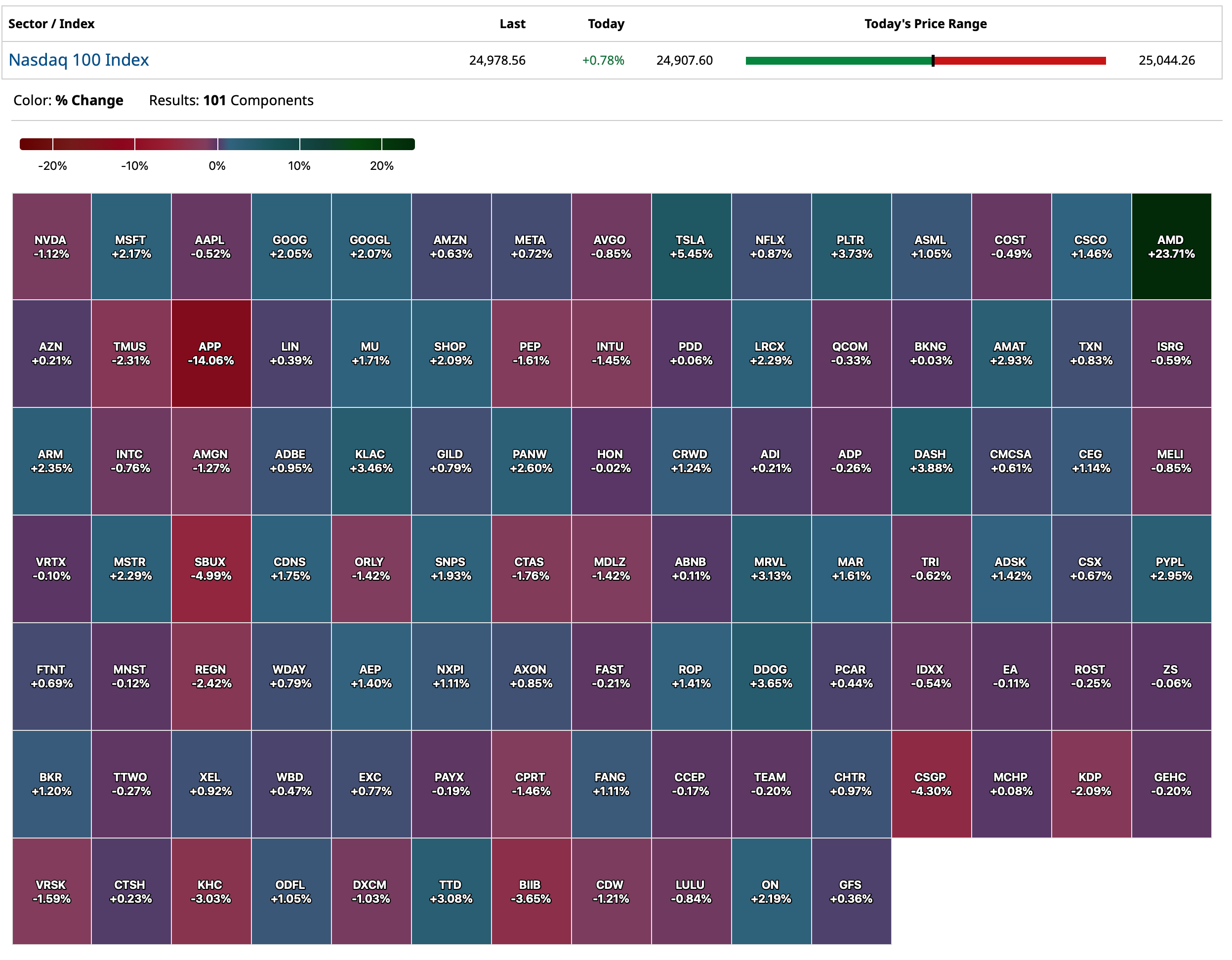

Here are today's things:

* I added to my Index shorts - (SPY) $671.32 and (QQQ) $606.46.

* I added to my already very large (GRNY) short at $25.58.

* I added to my small (NVDA) short at $185.44.

* I initiated a trading short rental in (AMD) at $224 (just covered 1/2 at $208.23) - see Comments Section

BY Doug Kass · Oct 6, 2025, 10:20 AM EDT

From Peter Boockvar

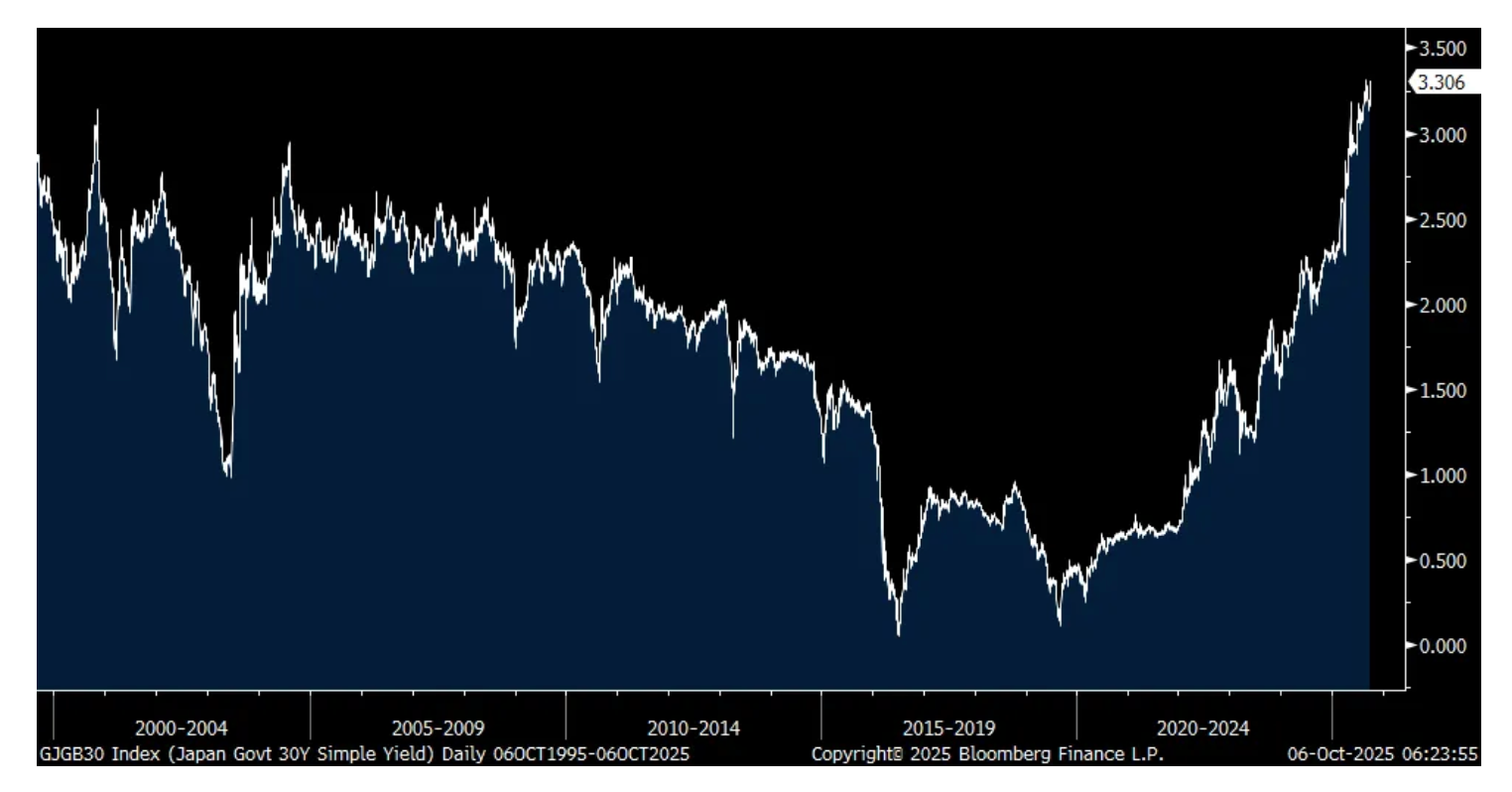

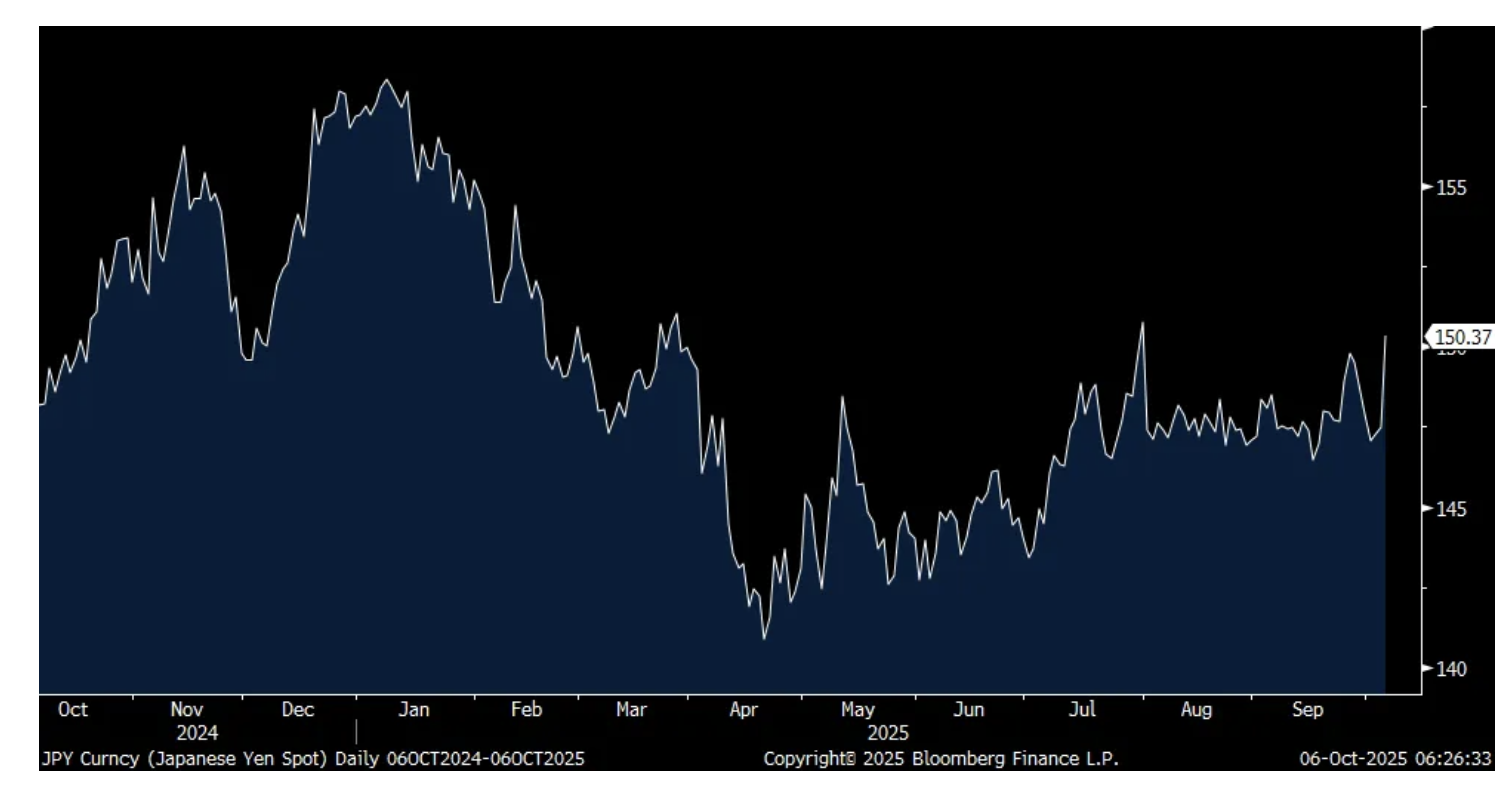

Congrats to Sanae Takaichi, elected the first woman PM of Japan and who Margaret Thatcher was always a hero of hers. We’ll now see how similar or not their policies are. The first market reaction and based on Takaichi comments in the past is that she supports more fiscal and monetary stimulus, with the latter punching up against the BoJ’s desire to continue to raise interest rates, albeit slowly, and the elevated inflation in the country. The yen selloff of 2% highlights what the market believes Takaichi will support, as did the rally in Japanese stocks with the Nikkei up almost 5%. But the JGB market had a really interesting reaction. The 2 yr yield fell almost 4 bps to a 3 week low to .905% but the 10 yr yield was up by 2 bps to 1.69%, the highest since June 2008, the 30 yr yield spiked by 14 bps to 3.31%, the highest since this issue was first released in 1999 and the 40 yr yield jumped by 15 bps to 3.54%, just below its highest since it was first issued in 2008. The 10 yr inflation breakeven in Japan rose 4 bps to 1.65%, the highest since May.

This JGB selloff flowed over to Europe and joined with the French PM unexpectedly resigning and French oat yields are up the most in Europe, with the 10 yr rising by 8 bps to 3.59%, within 1 bp from a level last seen 14 years ago. US Treasuries are selling off in kind. Gold continues to power higher as it is the growing alternative to sovereign bond holdings. The French CAC is down 1.5%.

Bottom line, the sovereign bond bear market I believe is intact and the response in Japan and France today is reflective of the belief that excessive debts and deficits now matter and the demand for long duration is shrinking as a result.

JGB 30 yr Yield

yen

Crude oil is bouncing after OPEC+ announced a production quota increase of 137,000 which was the same amount as their previous hike but below the whisper from last week that it could be as much as 500,000 barrels per day. There is also the belief and has been seen in the numbers that the group continues to pump less than the announced quota increases. We remain bullish on oil stocks believing the price of crude is dirt cheap at current levels.

After a lift of 12 rigs over 5 weeks, the US rig count slipped by 2 to 422.

Crude Oil Rig Count

Vietnam’s economy grew by 8.2% y/o/y in spite of the US tariffs slapped on them with exports rising by 25%. That exceeded the estimate of 7.2%. Tourism, consumer spending and manufacturing also helped to lift economic activity. We remain bullish on Vietnam and are long some stocks there. I’m sure some of the export and manufacturing activity was a rush to front run certain tariffs as the outline of a deal was announced.

The October Eurozone Sentix Investor Confidence index rose to -5.4 from -9.2 and better than the estimate of -7.7 and compares with -3.7 in August and +4.5 in July. Sentix said this, “Is this the hoped-for economic turnaround for the better? At first glance, it might seem so, because it is not only the Eurozone Index that is improving. The sub-indices for Germany, Austria and Switzerland also show some strong improvements in the situation and expectations. However, if we take a closer look at the figures, the Eurozone figures for all the countries mentioned and for the Eurozone as a whole are mostly below the August figures. In other words, the September data was negatively exaggerated from the investors’ point of view, especially with regard to expectations. Let us remember that it was concerns about the US economy, combined with recessionary trends in the Eurozone, that fueled pessimism among investors. The US is now in a ‘shutdown’, but this is causing investors little concern – at least so far. The data reflects hopes for a quick end to the shutdown.” Nothing market moving from this though.

Sentix Index

BY Doug Kass · Oct 6, 2025, 10:05 AM EDT

- Mel Brooks, Spaceballs (1987) Opening Title

I think the most telling thing right now is that the gen AI people desperately try to prevent any output of gen AI from getting into their training datasets. They literally call it poison. In other words, the output of what they produce is of lower quality than what goes in. Which is the opposite of human intelligence; everything we learn goes to building higher quality output, which is reused by ourselves or others to produce higher quality output, ad infinitum. So much for the agentic systems, which rely on Gen AI for their input.

About this article about Bezos data centers in space, good luck if you need to do this. Wonderful example of how out over their ski’s people are with this stuff now. If need to go to space to do it, good luck. It shows the resources are just not here, which also implicitly means the whole proposition is dis-economic. Even if feasible, which I highly doubt, the expense of doing this makes it even more dis-economic. Then the fact that it still doesn’t even work right and is the world’s most expensive homework cheating, slop generating machine. Have fun getting generated heat out of the space-based data center without fluid convection. Space is cold, but it’s empty. Most heat transfer on earth is by interacting atoms that bump each other and pass off heat. There are no atoms in space to bump against. So you have to radiate. Radiation is great at very high temperatures but terrible at low temperatures. Even I, a finance major at Wharton know this.

Clearly too much money was created by central banks around the world, and it has led to all of this. It is now working its way into the economy via AI related investment. We would probably be in a recession without it. All this cockamamie investment will most likely lead to an enormous amount of capital destruction. Capital destruction is normally an awful thing, but in this case, it just may be nature’s way of correcting for all the excess money that was un-necessarily and erroneously put into the economy to begin with.

This is interesting too:

Finally, a tidbit from Kuppy:

An AI Addendum - Praetorian Capital

- Space Balls

BY Doug Kass · Oct 6, 2025, 9:50 AM EDT

I am still medium-sized short the indexes on the early strength (added by one third with S&P cash +23 handles) - but will move to large sized on a further rally .

BY Doug Kass · Oct 6, 2025, 9:49 AM EDT

Last week I warned about our PepsiCo (PEP) channel checks (and the 3Q EPS might be at risk).

This morning JPMorgan maintained PEP with a neutral but lowered its price target from $157 to $151.

BY Doug Kass · Oct 6, 2025, 9:40 AM EDT

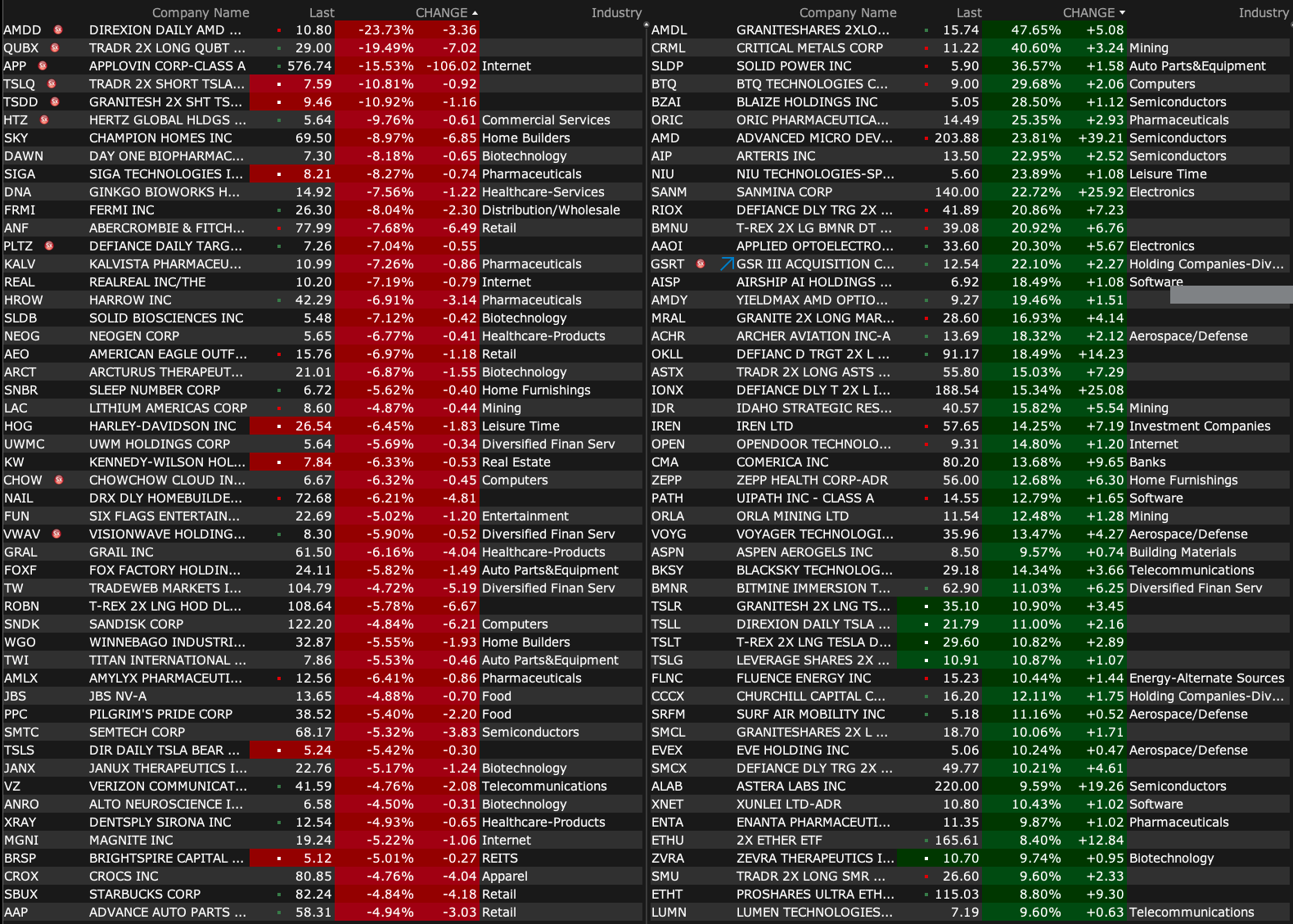

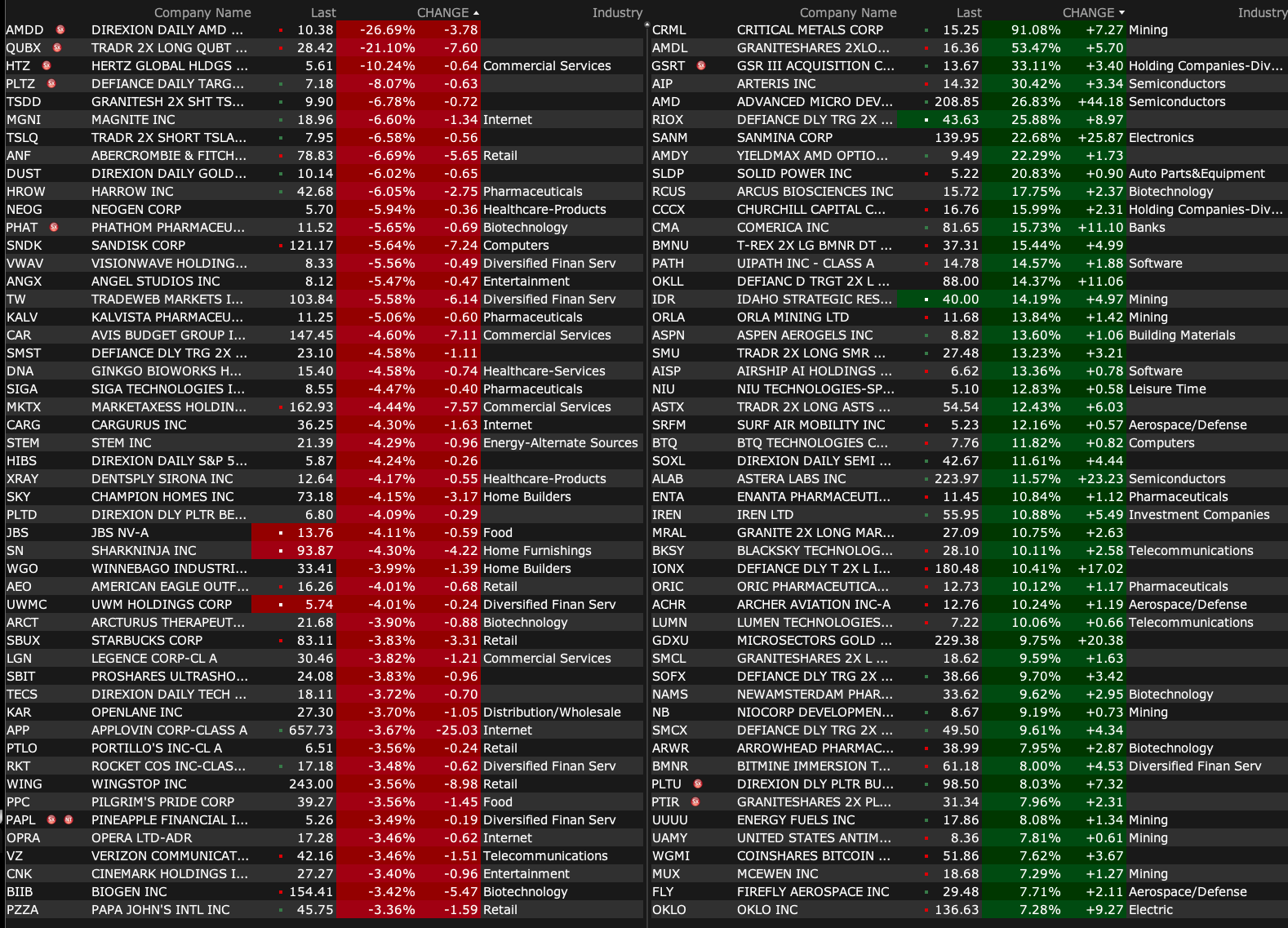

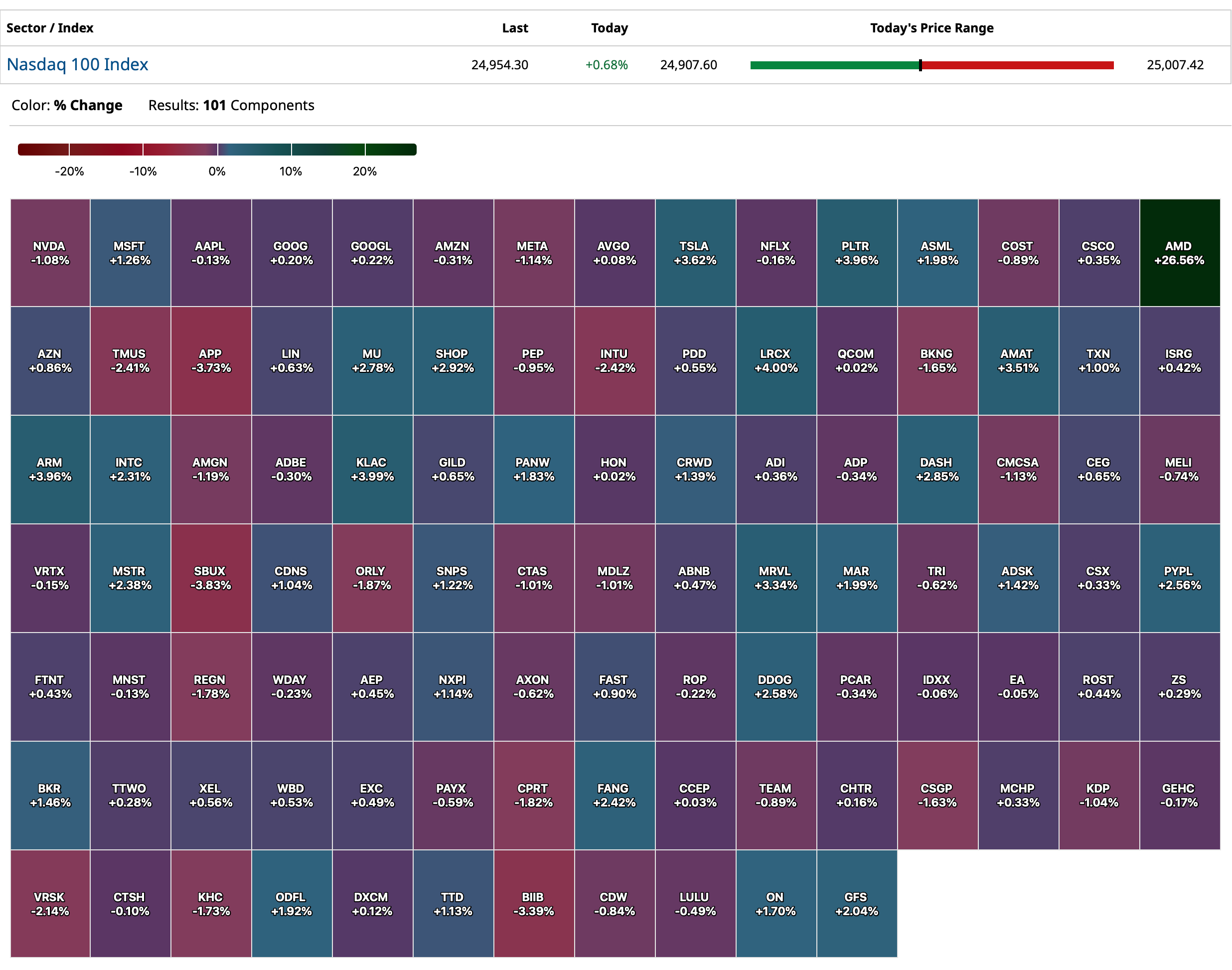

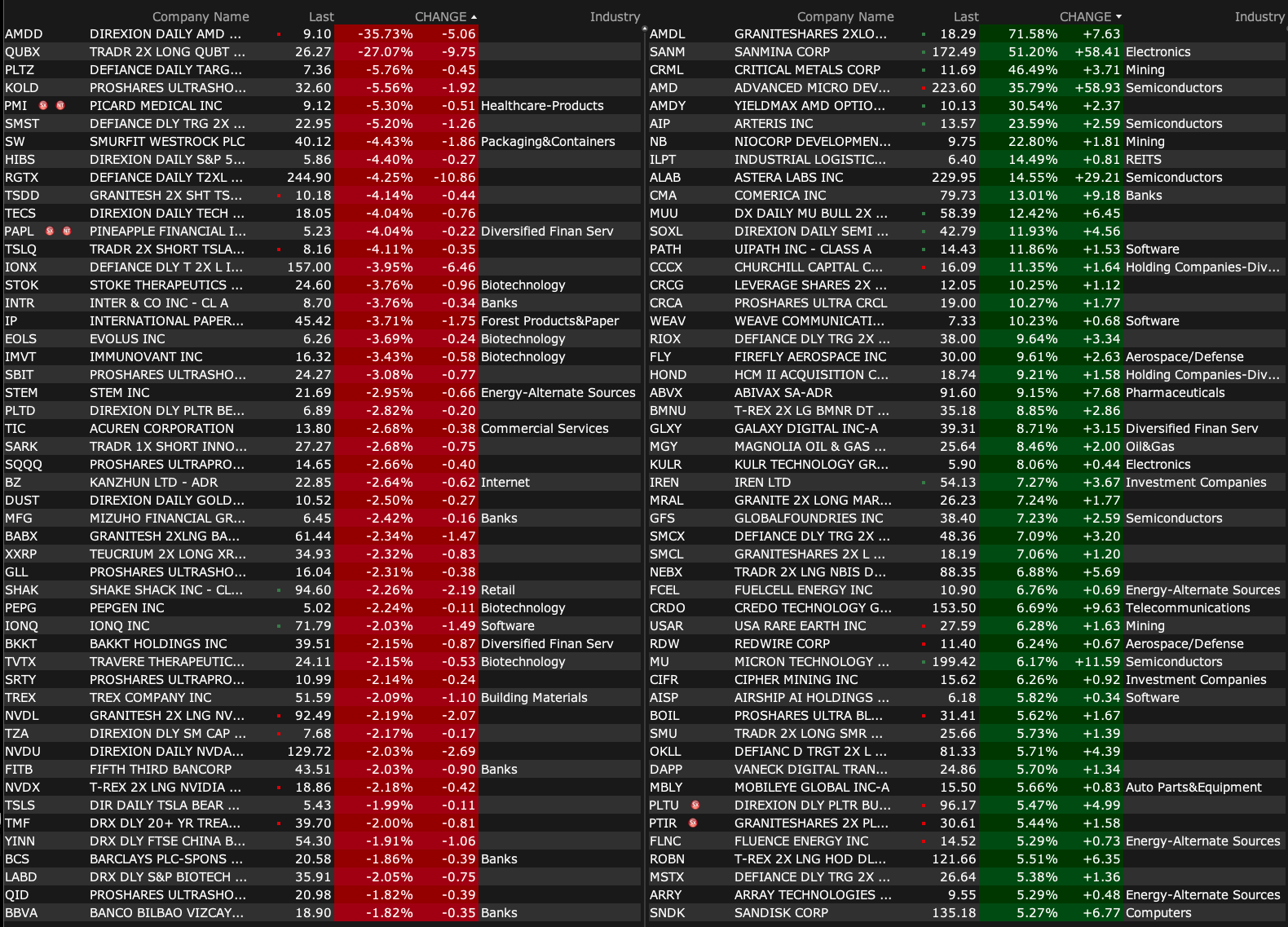

-SPRB +129% (receives U.S. FDA Breakthrough Therapy Designation for Tralesinidase Alfa Enzyme Replacement Therapy (TA-ERT) in Sanfilippo Syndrome Type B (MPS IIIB))

-SOPA +123% (reports Q2 revenue)

-SANM +62% (earnings, guidance)

-CRML +39% (earnings, guidance)

-AMD +35% (confirms AMD and OpenAI Announce Strategic Partnership to Deploy 6 Gigawatts of AMD GPUs)

-AIP +26% (momentum following AMD and OpenAI Announce Strategic Partnership to Deploy 6 Gigawatts of AMD GPUs)

-PALI +18% (momentum)

-ALAB +14% (Realta Investment Advisors acquires shares)

-PLUG +14% (momentum)

-CMA +13% (to be acquired by Fifth Third in all-stock $10.9B deal with implied price of $82.88/shr)

-IVVD +11% (US FDA cleared IND for VYD2311, a monoclonal antibody COVID prophylactic)

-FLY +9.6% (entered into a definitive agreement to acquire SciTec, Inc.)

-CCCX +8.4% (Citron mention)

-DVLT +8.2% (guidance; launches four data exchanges)

-ABVX +7.1% (announces Late-Breaking Presentation of 8-Week ABTECT Trial Results with Updated Safety Data)

-MU +5.5% (Morgan Stanley Raised MU to Overweight from Equal Weight, price target: $220; momentum following AMD and OpenAI Announce Strategic Partnership to Deploy 6 Gigawatts of AMD GPUs)

-WRAP +5.4% (launches Data Partnership with Le Sueur Police Department to Study Non-Lethal Force and Pre-Escalation Tactics)

-KLAR +2.6% (broker initiations)

-PLTR +2.6% (OneMedNet selects Palantir to advance healthcare AI and data analytics)

-TSLA +2.2% (teases Tue, October 7th event)

-AFRM +2.1% (PYPL reportedly introduces 5% cash back on BNPL purchases through year-end)

-HSII - Halted (PE consortium led by Advent to acquire Heidrick & Struggles at $59.00/shr in $1.3B deal)

-SKYE -60% (reports Topline CBeyond Phase 2a Data from Nimacimab Monotherapy and Combination Clinical Trial)

-DFLI -28% (prices 20M share offering at $1.25/shr)

-QUBT -15% (announces $750M Oversubscribed Private Placement of Common Stock Priced at the Market Under Nasdaq Rules)

-ANF -2.2% (JPMorgan Chase and Co Cuts ANF to Neutral from Overweight, price target: $103)

-FITB -2.0% (acquiring CMA in all-stock $10.9B deal with implied price of $82.88/shr)

-SHAK -2.0% (Tier1 firm Cuts SHAK to Underperform from Neutral, price target: $86 from $148)

BY Doug Kass · Oct 6, 2025, 9:28 AM EDT

11:30 a.m.: Federal Reserve Board of Governors Closed Board meeting: Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks;

5:00 p.m.: Fed Bank of Kansas City President Schmid (Voter) speaks on monetary policy and the economic outlook before the CFA Society Kansas City, Kansas City, MO (Embargoed text and livestream available. Audience Q&A expected)

BY Doug Kass · Oct 6, 2025, 9:20 AM EDT

BY Doug Kass · Oct 6, 2025, 9:05 AM EDT

BY Doug Kass · Oct 6, 2025, 8:50 AM EDT

BY Doug Kass · Oct 6, 2025, 8:41 AM EDT

BY Doug Kass · Oct 6, 2025, 8:22 AM EDT

BY Doug Kass · Oct 6, 2025, 7:50 AM EDT

BY Doug Kass · Oct 6, 2025, 7:40 AM EDT

From JPMorgan:

US: Futs are higher, led by Tech as the markets continue to look through the gov’t shutdown though federal unions are heading to court to prevent the furloughs from being converted into RIFs. USD poised for its strongest day since late Aug as USD / JPY and is +2% and EUR / USD -65bp on election news. The yield curve is twisting steeper around the 2Y. Pre-mkt, Mag7 and Semis are seeing a bid; Cyclicals are standing out but there is a broad-based bid pre-mkt. In cmdtys, all 3 complexes are higher with WTI, natgas, and precious metals outperforming.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

With the government shutdown, a dearth of macro earnings, and the calendar about one week from earnings season kicking off the information vacuum could see markets chop sideways. We remain tactically bullish but acknowledge risk forming / increasing. Our framework of (i) resilient macro data + (ii) positive EPS growth + (iii) improving trade war dynamics = bull market remains intact. A few thoughts on some of the risks, stemming from recent client conversations. Our monetization menu follows before exploring some risks.

BY Doug Kass · Oct 6, 2025, 7:30 AM EDT

BY Doug Kass · Oct 6, 2025, 7:10 AM EDT

I expect Broadcom (AVGO) and Nvidia (NVDA) to suffer from the just-announced OpenAI/AMD deal.

OpenAI looks to take 10% stake in AMD through AI chip deal

I added to my (NVDA) short in premarket trading.

BY Doug Kass · Oct 6, 2025, 7:08 AM EDT

BY Doug Kass · Oct 6, 2025, 7:00 AM EDT

Bonus — Here are some great links:

Bull Market Keeps on Printing Records

BY Doug Kass · Oct 6, 2025, 6:45 AM EDT

Will the developing non-U.S. political events (in Japan and France) adversely impact our equity and bond markets?

This is the key question that will be asked by investors this morning.

While the initial reaction is a +4% advance in Japan's equity market and a +0.50% rise in S&P futures, the climb in worldwide yields must, at some point, be an (unexpected) headwind.

My shorting of SPY (early this morning) is a signal of how I interpret the news.

BY Doug Kass · Oct 6, 2025, 6:35 AM EDT

BY Doug Kass · Oct 6, 2025, 6:25 AM EDT

BY Doug Kass · Oct 6, 2025, 6:15 AM EDT

The S&P Short Range Oscillator stands at 0.56% vs. -0.78%. That is slightly overbought, from slightly oversold.

BY Doug Kass · Oct 6, 2025, 6:05 AM EDT

In response to:

BY Doug Kass · Oct 6, 2025, 5:55 AM EDT

Shorted more indices:

* (SPY) $671.14

* (QQQ) $605.72

BY Doug Kass · Oct 6, 2025, 5:48 AM EDT