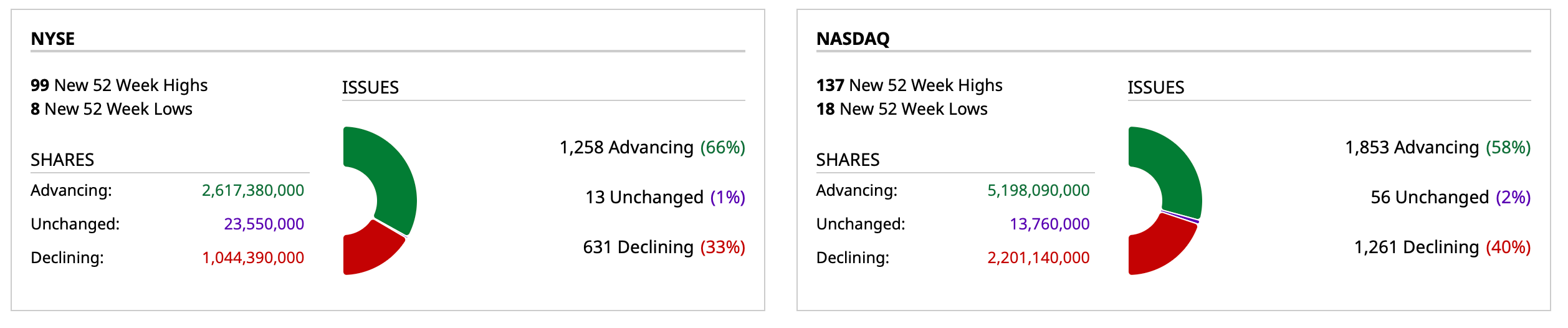

Friday's Closing Market Stats

Closing Breadth

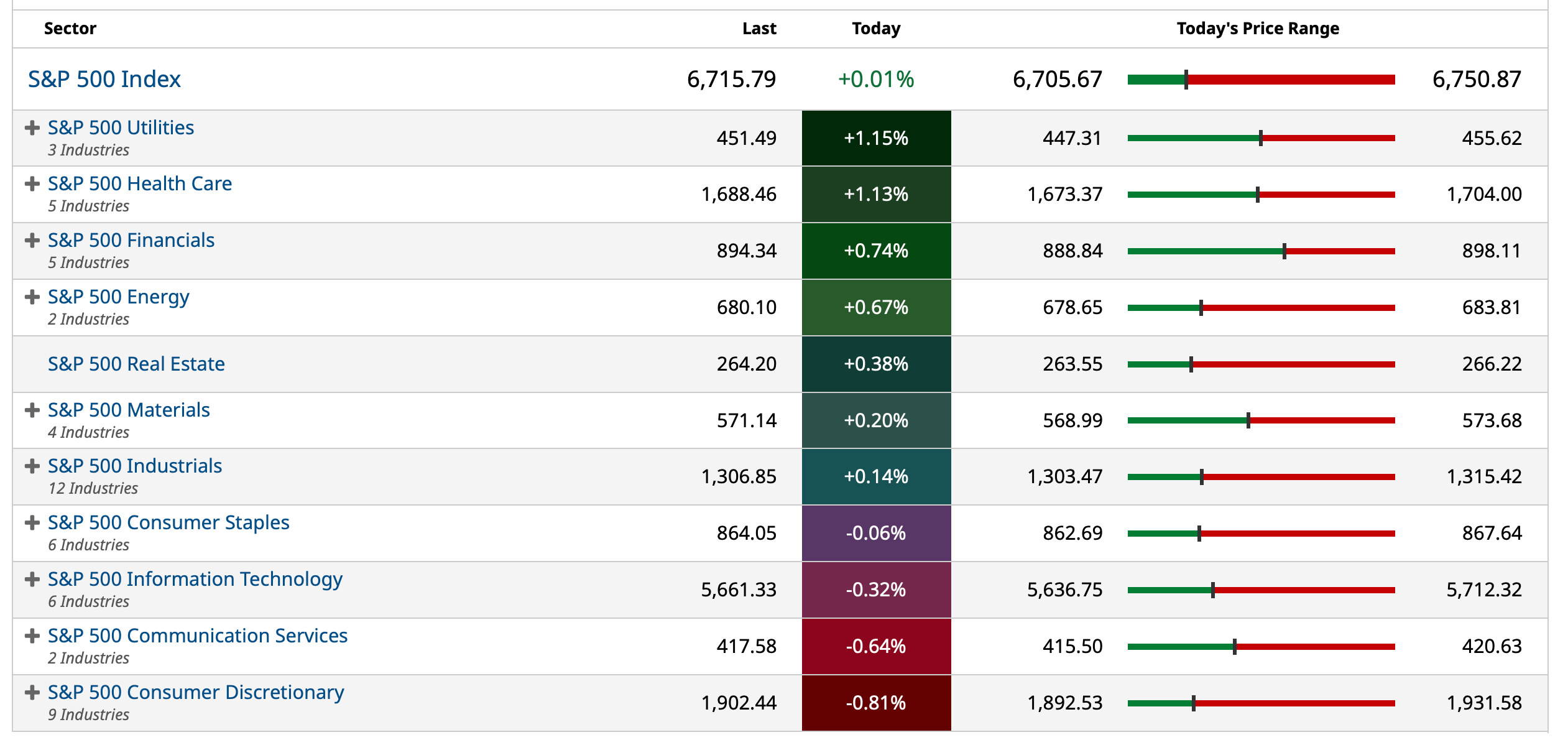

Sectors

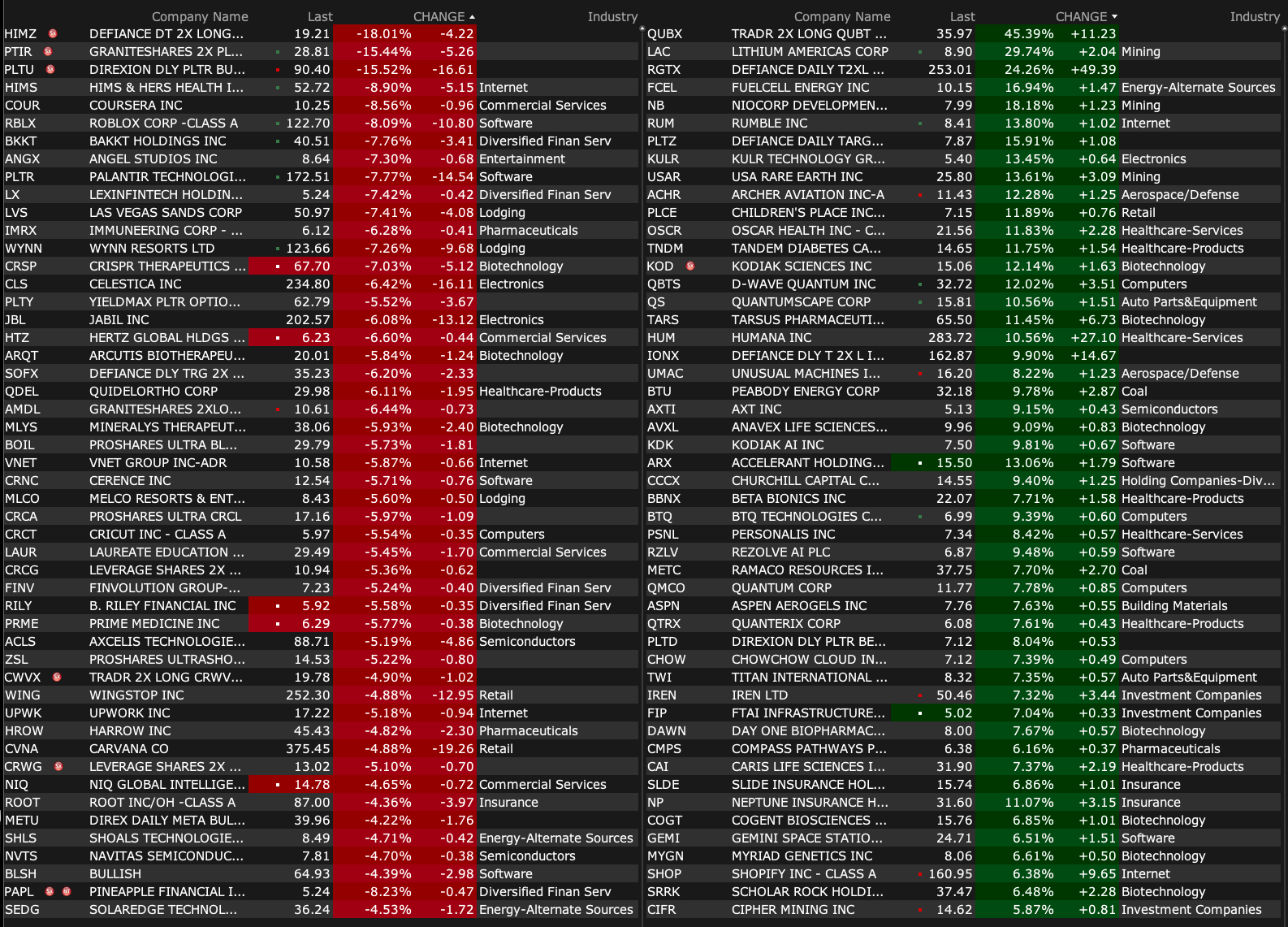

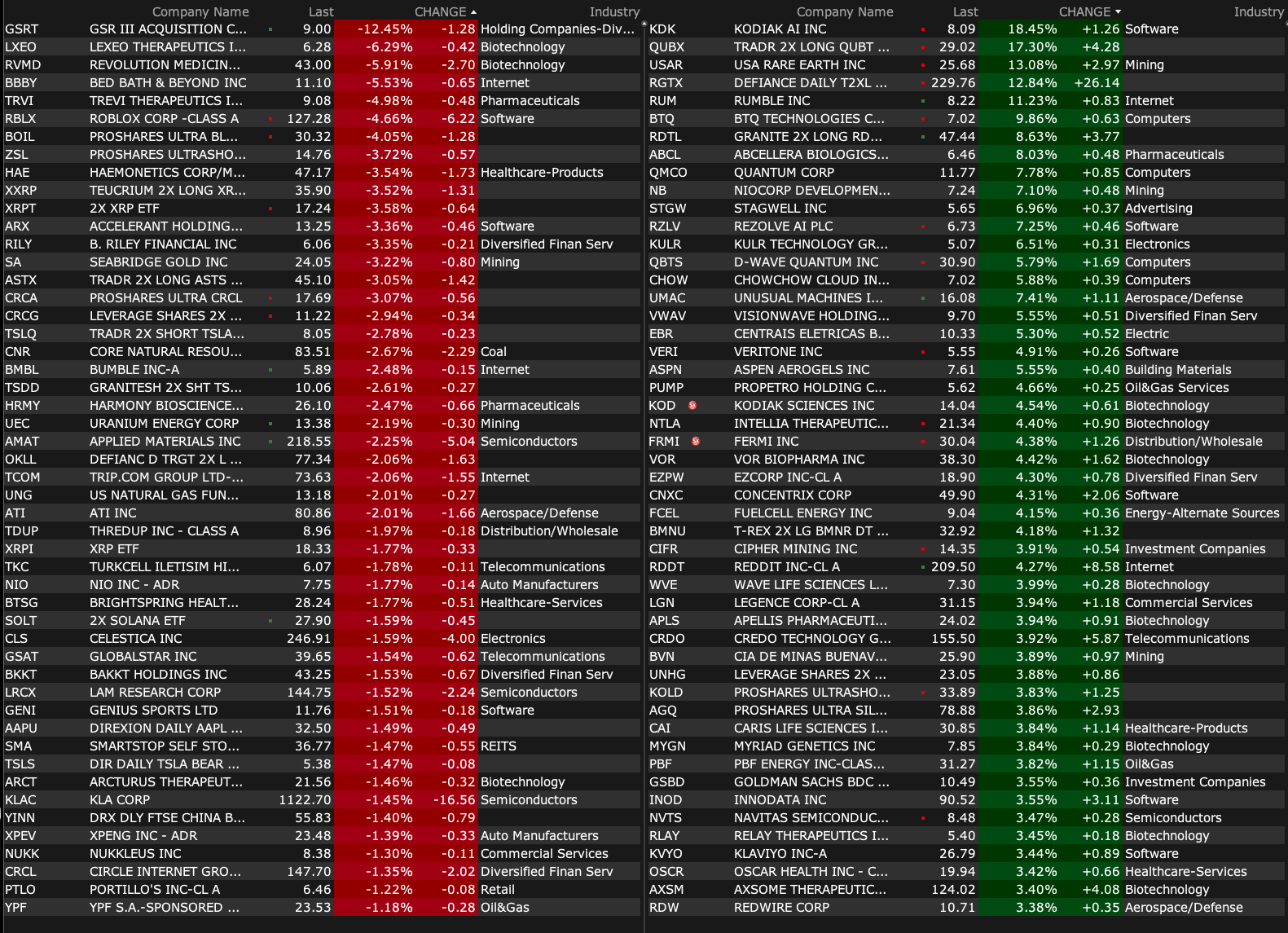

% Movers

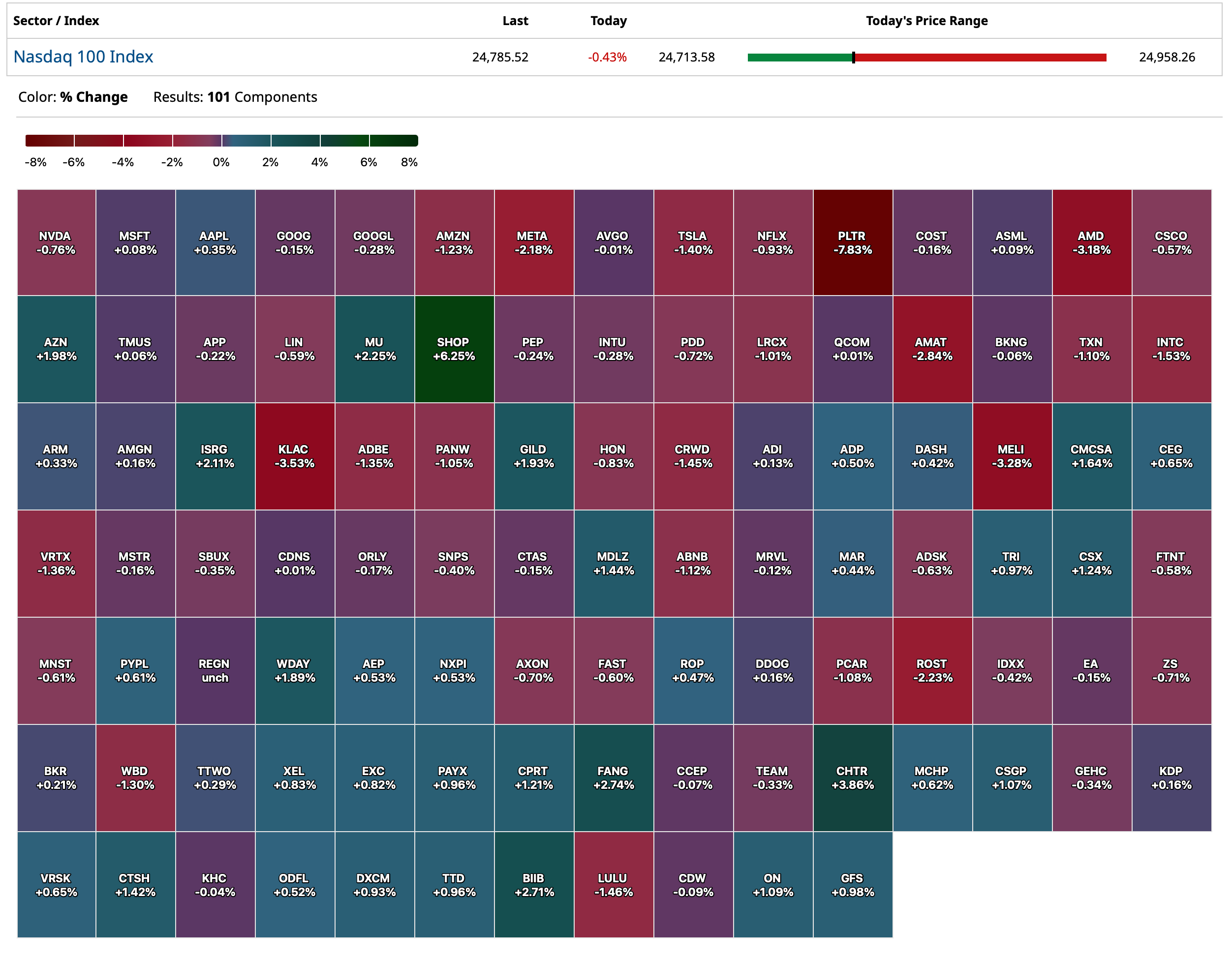

Nasdaq 100 Heat Map

BY Doug Kass · Oct 3, 2025, 4:40 PM EDT

BY Doug Kass · Oct 3, 2025, 4:40 PM EDT

From Peter Boockvar:

Stall speed in services while prices paid remains high and a look on employment

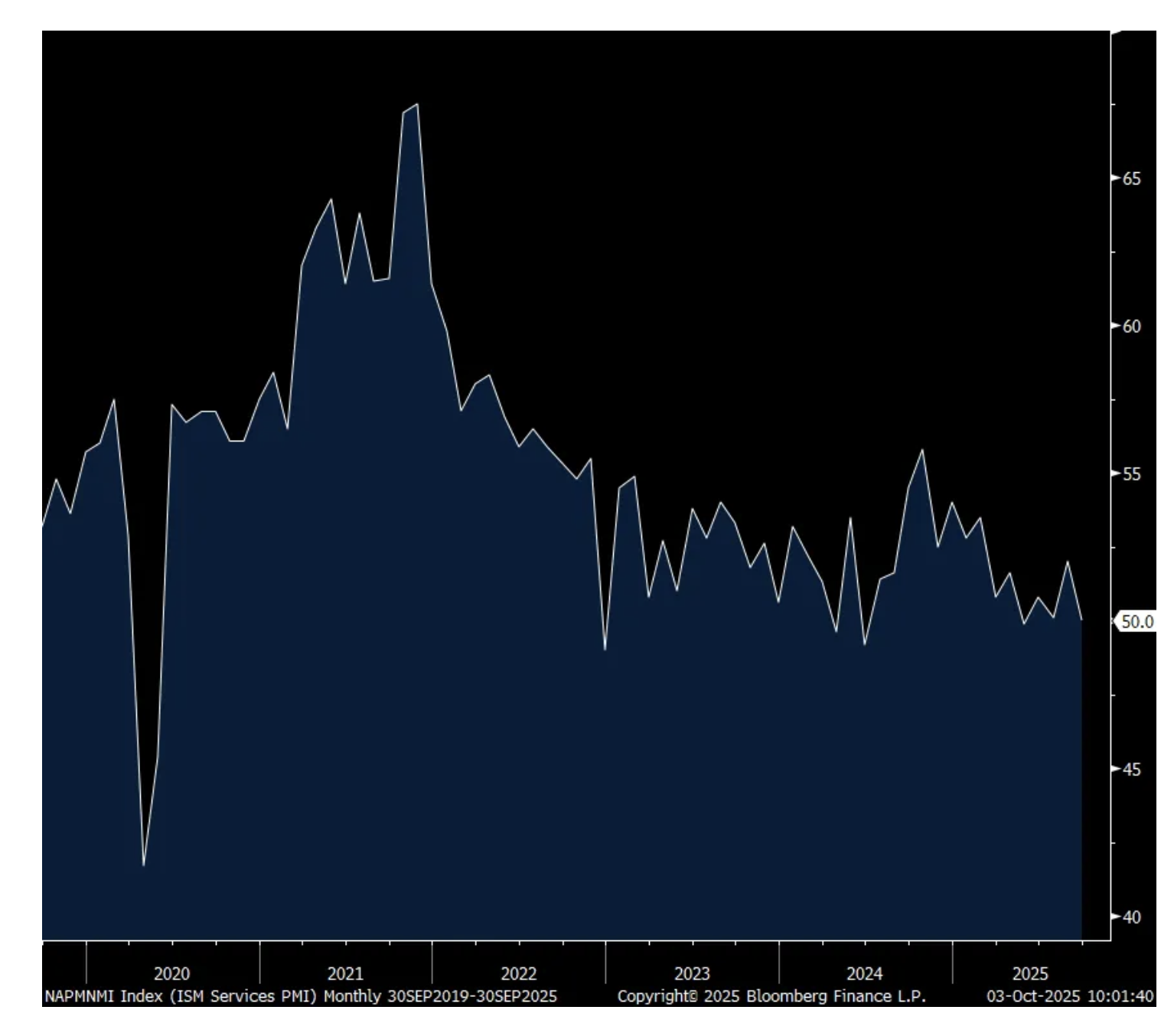

The September ISM services index fell to exactly 50 from 52 in August and compares with the estimate of 51.7. That’s also the 2nd lowest print since June 2024. The Business Activity component fell 5.1 pts to 49.9.

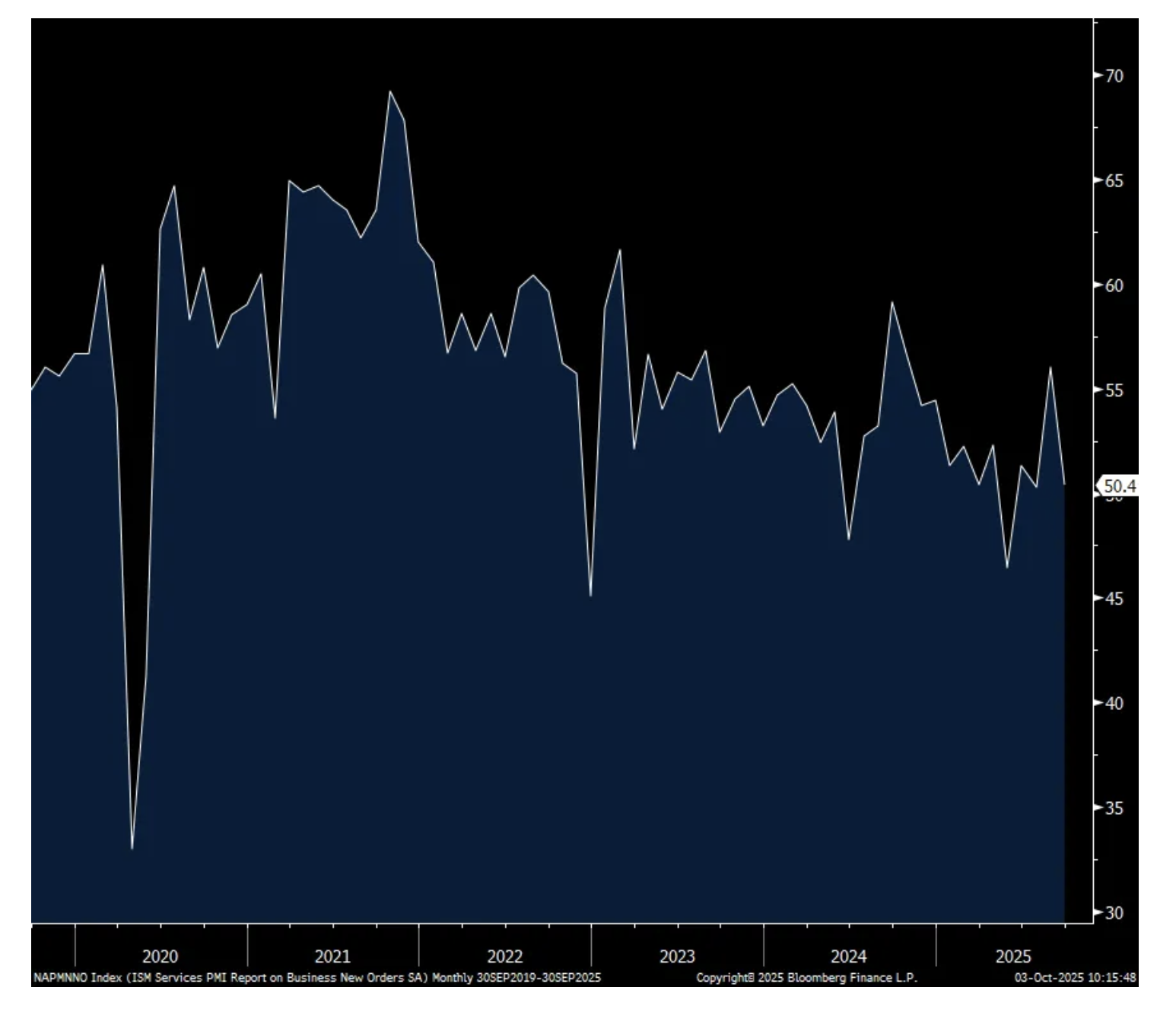

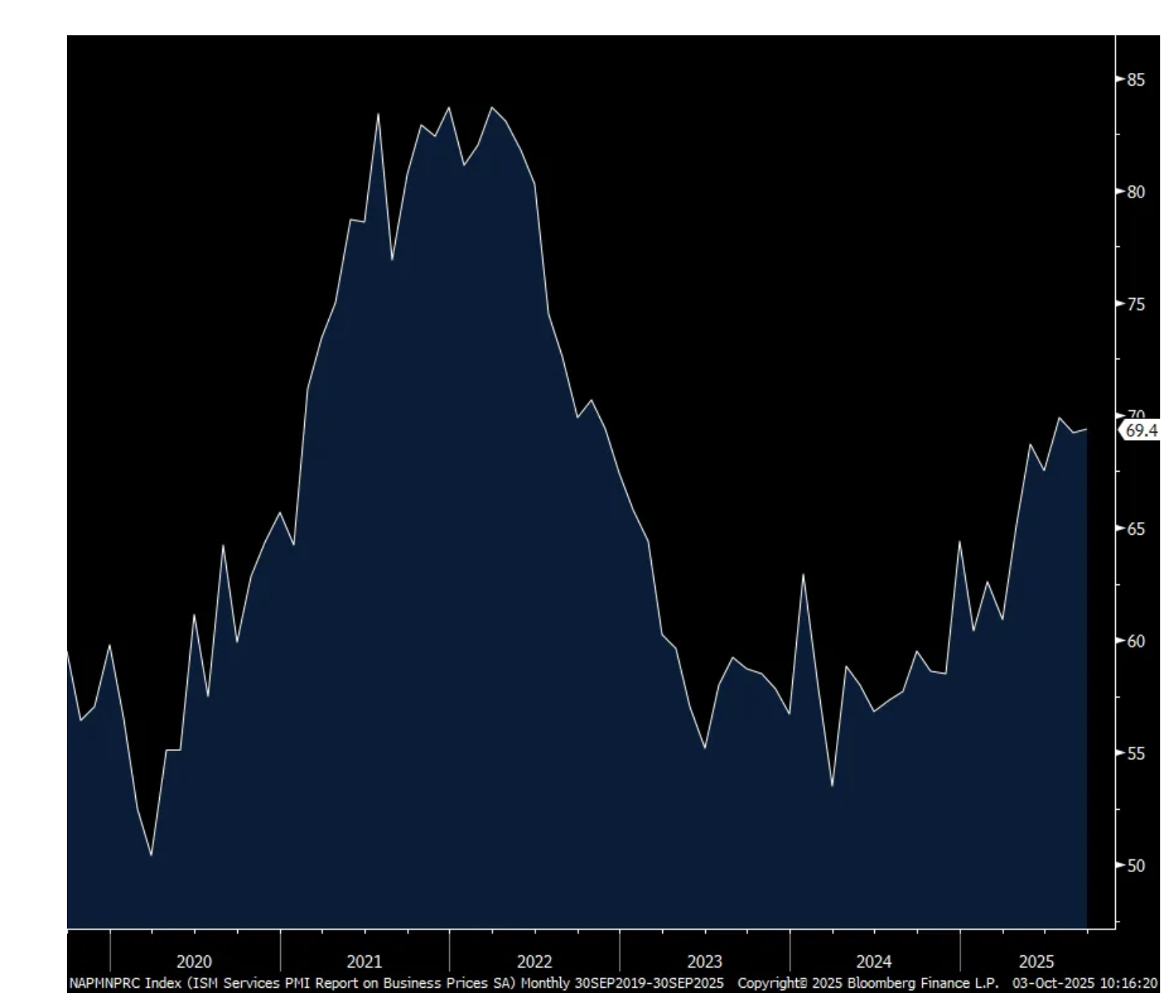

New orders were down 5.6 pts to 50.4, giving back the August 5.7 pt rise. Backlogs bounced by 6.9 pts but remains below 50 at 47.3. After three months above 50, inventories fell 5.4 pts to 47.8. Employment at 47.2 is under 50 for the 4th straight month, and below that threshold for the 6th month in the past 7, though up .7 pts m/o/m with 6 industries adding workers out of 18 vs 2 in August and 7 in July. Prices paid remained elevated and well above 50 at 69.4 vs 69.2 in August and 69.9 in July. Within prices paid, 15 of 18 industries said they paid higher prices in the month vs 16 in August and 15 in July.

This was an interesting comment on the housing sector within the ‘new orders’ component, “Buyers are sitting on the sidelines waiting for mortgage rates to drop; some buyers are having difficulty selling their home and are not able to purchase a new one unless they do.”

In the backlogs section, this stood out: “Major capital projects with the exception of data centers are being delayed.”

The industry breadth weakened as 10 of 18 industries saw growth vs 12 in August and 7 reported a contraction vs 4 last month.

The bottom line from ISM, “Commentary in general indicated moderate or weak growth, with more isolated observations of supplier delivery challenges (which rose in the month). Employment continues to be in contraction territory, thanks to a combination of delayed hiring efforts and difficulty finding qualified staff.”

My bottom line, a stagflation lite type print with prices paid remaining high at the same time service growth stalls. Yields are up slightly in response to the former.

Here were the comments from companies in a variety of industries and outside of those selling into the data center buildout, there seems to be very little economic growth.

“We are beginning to see the impact of the tariffs impact our business, particularly for food products from India, China, and Southeast Asia, coffee from South America, and apparel and electronics from Asia. Our year-over-year cost increases are getting progressively greater.” [Accommodation & Food Services]

“New residential construction continues to struggle in a tough market. Housing values remain high, and tariffs are beginning to be passed through on materials that are metal based. The pace of housing starts has been stagnant to slightly declining, as we head out of the summer building season.” [Construction]

“Pharmacy costs continue to rise, and medical devices are being held at bay mainly due to contracts and continued negotiations where we have two to three sources for a given product.” [Health Care & Social Assistance]

“Demand for artificial intelligence (AI) and cloud infrastructure remains very strong. Our primary focus this month was on increasing production throughput to begin clearing the significant order backlog built up over the summer. While new order intake has stabilized at a high level, the overall business outlook remains positive. We are still facing significant supply chain challenges, especially for advanced semiconductors and power components, with lead times remaining extended. Price pressures are still present but have not worsened compared to the previous month.” [Information]

“Client demand in professional services remains steady, though decision-making timelines are lengthening due to continued economic uncertainty and interest-rate concerns. We are also seeing modest upward pressure on labor costs, which impacts both our internal resourcing and supplier pricing.” [Professional, Scientific & Technical Services]

“Growing apprehension regarding state efforts to reduce or eliminate property taxes that are a major revenue source for local governments. And continuing concern about future economic conditions, inflation, tariffs and their impact on increased prices.” [Public Administration]

“The overall housing market remains stagnant, which has forced our company to be hyper-vigilant about costs. However, we are growing and increasing our market share despite the headwinds. Tariffs continue to inject an unnecessary level of uncertainty across the broader economy, and costs are now beginning to increase with the full effect of the tariffs now coming into play.” [Real Estate, Rental & Leasing]

“Costs overall have stabilized, and we’ve not seen any interruptions in sourcing or shipments.” [Retail Trade]

“We’ve had more tariff charges last month than in previous months.” [Utilities]

“Business conditions continue to soften, even in markets that have historically been more resilient. Demand is simply weak.” [Wholesale Trade]

ISM Services

New Orders

Prices Paid

BY Doug Kass · Oct 3, 2025, 4:00 PM EDT

Thanks for reading my Diary today and all week.

Enjoy your weekend.

Be safe.

And... Go Yankees!

BY Doug Kass · Oct 3, 2025, 3:35 PM EDT

BY Doug Kass · Oct 3, 2025, 2:14 PM EDT

In his characteristically witty style, Warren Buffett wrote in his 1992 letter to Berkshire Hathaway (BRK.A) (BRK.B) shareholders:

"We’ve long felt that the only value of stock forecasters is to make fortune tellers look good. Even now, Charlie [Munger] and I continue to believe short-term market forecasts are poison and should be kept locked up in a safe place, away from children and also from grown-ups who behave in the market like children.”

At the risk of being Warren's target (and the target of the bullish cabal) I am making the Ludacris Forecast that the S&P index has or is about to make a top for the year.

There... I have written it.

BY Doug Kass · Oct 3, 2025, 1:55 PM EDT

Scott Galloway's "No Mercy No Malice": Strike

BY Doug Kass · Oct 3, 2025, 1:45 PM EDT

As mentioned in my Bloomberg TV interview this morning, I am at my highest net short exposure since November 2021.

BY Doug Kass · Oct 3, 2025, 1:20 PM EDT

I have a research meeting at noon — out for about one hour.

Radio silence.

BY Doug Kass · Oct 3, 2025, 12:18 PM EDT

I am battening down the hatches in preparation for a market fall (which has, thus far, failed to materialize).

As a consequence I am selling out a portion of some longs, including PepsiCo (PEP) ($143.09 this morning). In the process I am taking a small loss as I have averaged down.

In the case of PEP I am getting some negative channel checks, possibly portending a slightly weaker-than-expected Q3 2025 EPS release and forward guidance.

I fully recognize that a modestly reduced outlook may have already been discounted in the current share price — as the shares have been an underperformer for some time.

That said, I wlll likely buy back what I sold in a move below $140, but that depends on the context of the third-quarter announcement.

Remember, Elliott Management is involved as an activist.

As a result of this move I have gone from very large to medium sized.

BY Doug Kass · Oct 3, 2025, 12:00 PM EDT

With S&P cash +26 handles (buoyed by healthcare strength) I am adding to (SPY) at $671.66 and (QQQ) at $606.45 shorts.

BY Doug Kass · Oct 3, 2025, 11:35 AM EDT

BY Doug Kass · Oct 3, 2025, 11:21 AM EDT

BY Doug Kass · Oct 3, 2025, 10:15 AM EDT

Short people got no reason

Short people got no reason

Short people got no reason

To live

They got little hands

And little eyes

And they walk around

Tellin' great big lies

They got little noses

And tiny little teeth

They wear platform shoes

On their nasty little feet

Well, I don't want no short people

Don't want no short people

Don't want no short people

'Round here

- Randy Newman - Short People (Official Video)

Spruce Point Capital issues a sell recommendation on Draft Kings. DraftKings Inc. - Spruce Point Capital Management LLC

BY Doug Kass · Oct 3, 2025, 10:00 AM EDT

On this rally I added to (GRNY) $25.33, (SPY) $671.17 and (QQQ) $607.09 shorts.

BY Doug Kass · Oct 3, 2025, 9:50 AM EDT

-OVID +18% (next-generation GABA-aminotransferase inhibitor, OV329, demonstrate strong inhibitory activity and a potential best-in-category safety profile; files to sell $175M private placement)

-PLUG +14% (Wainwright raises price target; Pres Trump ready to cancel Western hydrogen hubs amid shutdown fight)

-USAR +13% (reportedly CEO Humpton told CNBC it is “in close communication” with the White House)

-RUM +11% (Rumble and Perplexity enter into a strategic partnership; collaboration to drive improved video discovery on Rumble by leveraging Perplexity AI tools)

-ANRO +8.3% (receives FDA Fast Track Designation for ALTO-101 for treatment of cognitive impairment associated with schizophrenia)

-UMAC +7.1% (secures $800K order for high-performance drone components from Red Cat)

-WTM +5.0% (agrees to Sell Bamboo to CVC for $1.75B)

-Z +2.8% (hearing Gordon Haskett Raised Z to Buy from Hold, price target: $90)

-ICE +2.0% (reports Q3 total open interest +15% y/y)

-GME -4.6% (files to sell mixed shelf of indeterminate amount)

-RBLX -4.6% (weakness attributed to cautious comments at M Science citing decelerating US bookings growth)

-VANI -3.9% (withdraws record date for Cortigent Neuromodulation Subsidiary Spin-Off; Vivani expects to reestablish and announce a new record date as soon as possible)

-TROX -2.6% (JPMorgan Chase and Co Cuts TROX to Neutral from Overweight)

-AMAT -2.3% (US Commerce Dept expands export restrictions; Expects BIS affiliates rule to further export restrictions to China; Expects impact will reduce revenue in Q4 by ~$110M, and ~$600M in FY26)

BY Doug Kass · Oct 3, 2025, 9:20 AM EDT

I will be appearing on Bloomberg at 9:25 a.m. this morning.

BY Doug Kass · Oct 3, 2025, 9:10 AM EDT

BY Doug Kass · Oct 3, 2025, 8:55 AM EDT

BY Doug Kass · Oct 3, 2025, 8:43 AM EDT

"Now we will show her who is in charge of the Galaxy...

Prepare ship for light speed. No, light speed is too slow. Prepare the ship for ludacris speed.

Sir, we have never gone that fast,

What's the matter Colonel Sandurz, chicken...

Prepare ship for Ludacris speed, Cancel the three ring circus.

Ludacris speed, go!

What have I done? My brains are going into my feet!

What the hell was that? Spaceball I - we've gone to plaid."

- Space Balls Spaceballs (1987) | They've Gone to Plaid! | MGM Studios

This one might take the cake.

An AI business plan went public yesterday. Yes, Fermi (FRMI). It looks to be a nine-month old company, with no revenue. I thought CoreWeave (CRWV) took the cake, when it went public on an Earnings Before Expenses basis, and then skyrocketed. This thing appears to be a business plan for an Earnings Before Expenses business, that in the nine months since the business plan was written, is worth $19 billion, after the IPO yesterday also ripped.

Why not take every available piece of dirt in the middle of the country public?

Take all the federal land, make it one giant IPO, and turn the federal deficit into a surplus.

We are all rich, nobody has to work anymore. I guess AI actually did it, just in a different way than everyone thought it would!

Smoke 'em if you got 'em.

BY Doug Kass · Oct 3, 2025, 7:30 AM EDT

BY Doug Kass · Oct 3, 2025, 7:15 AM EDT

BY Doug Kass · Oct 3, 2025, 7:05 AM EDT

* Approaching large-sized...

More index shorts:

* (SPY) $671.20

* (QQQ) $607.71

BY Doug Kass · Oct 3, 2025, 6:55 AM EDT

BY Doug Kass · Oct 3, 2025, 6:45 AM EDT

BY Doug Kass · Oct 3, 2025, 6:29 AM EDT

BY Doug Kass · Oct 3, 2025, 6:19 AM EDT

BY Doug Kass · Oct 3, 2025, 6:09 AM EDT

The S&P Oscillator stands at -0.78% vs. -0.04%. That is modestly oversold.

BY Doug Kass · Oct 3, 2025, 5:59 AM EDT

BY Doug Kass · Oct 3, 2025, 5:47 AM EDT