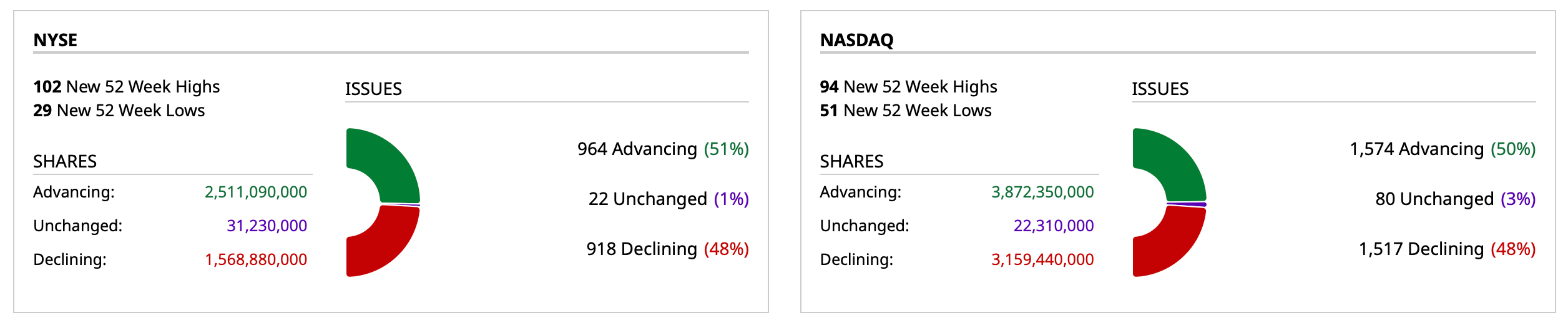

Wednesday's Closing Market Stats

Closing Volume

- NYSE volume 16% above its one-month average

- NASDAQ volume 12% above its one-month average

- VIX index: up 0.06% to 16.29

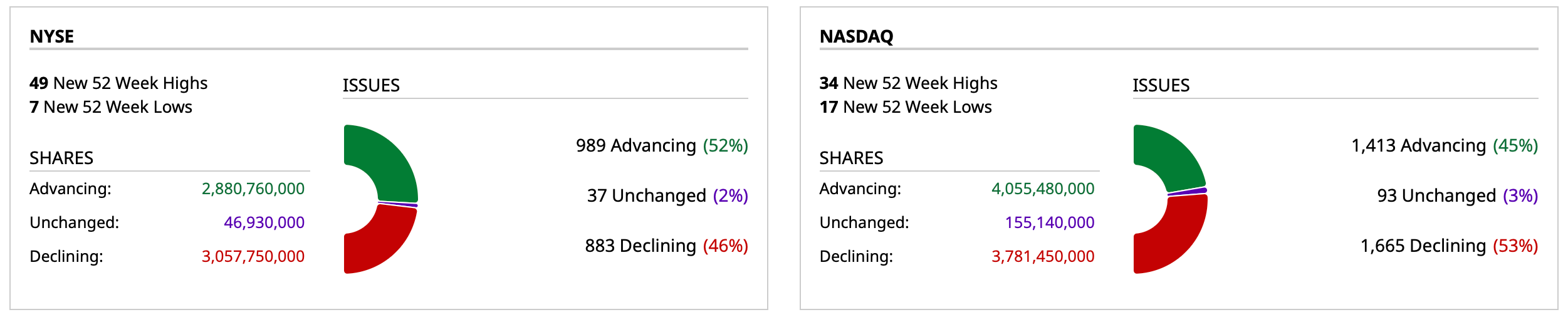

Breadth

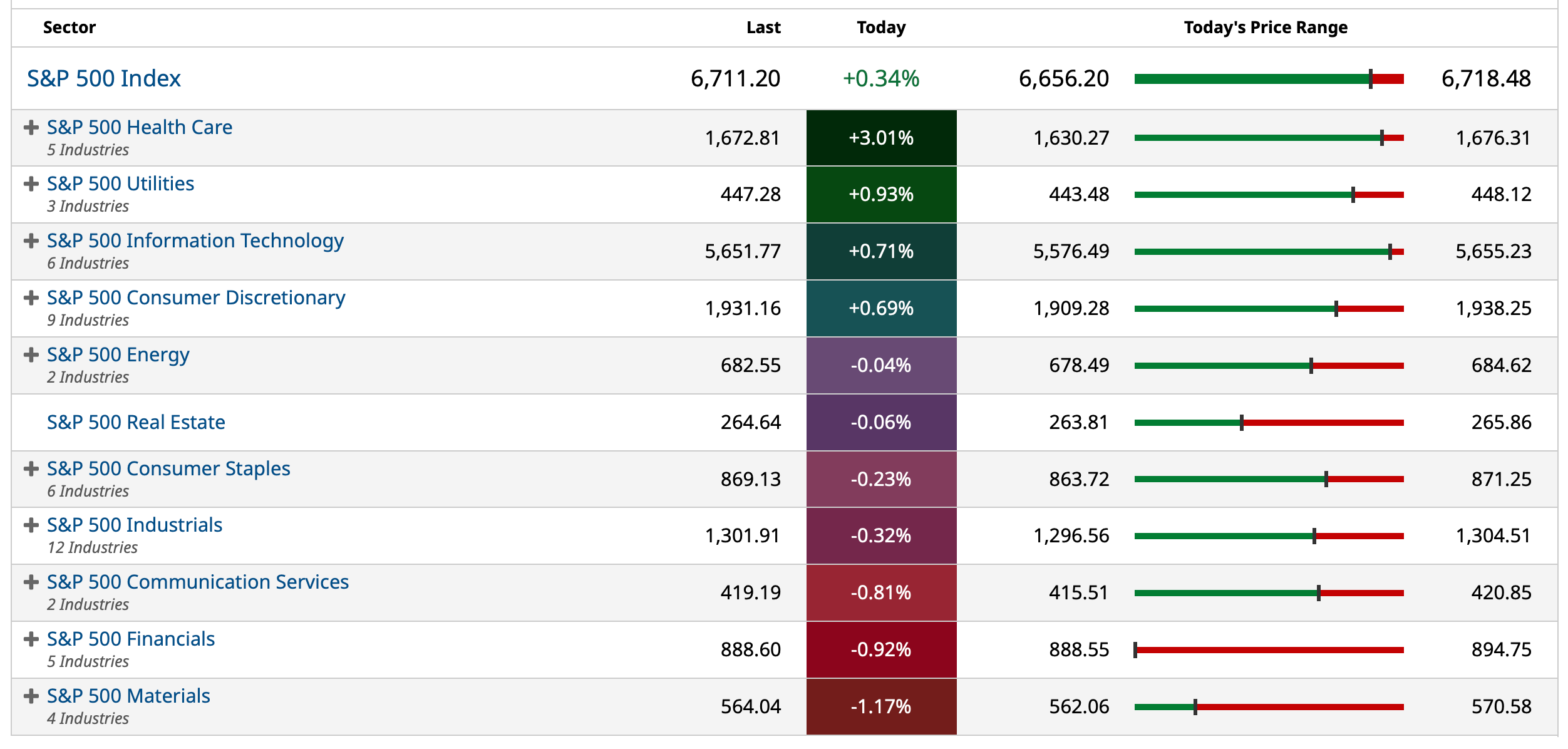

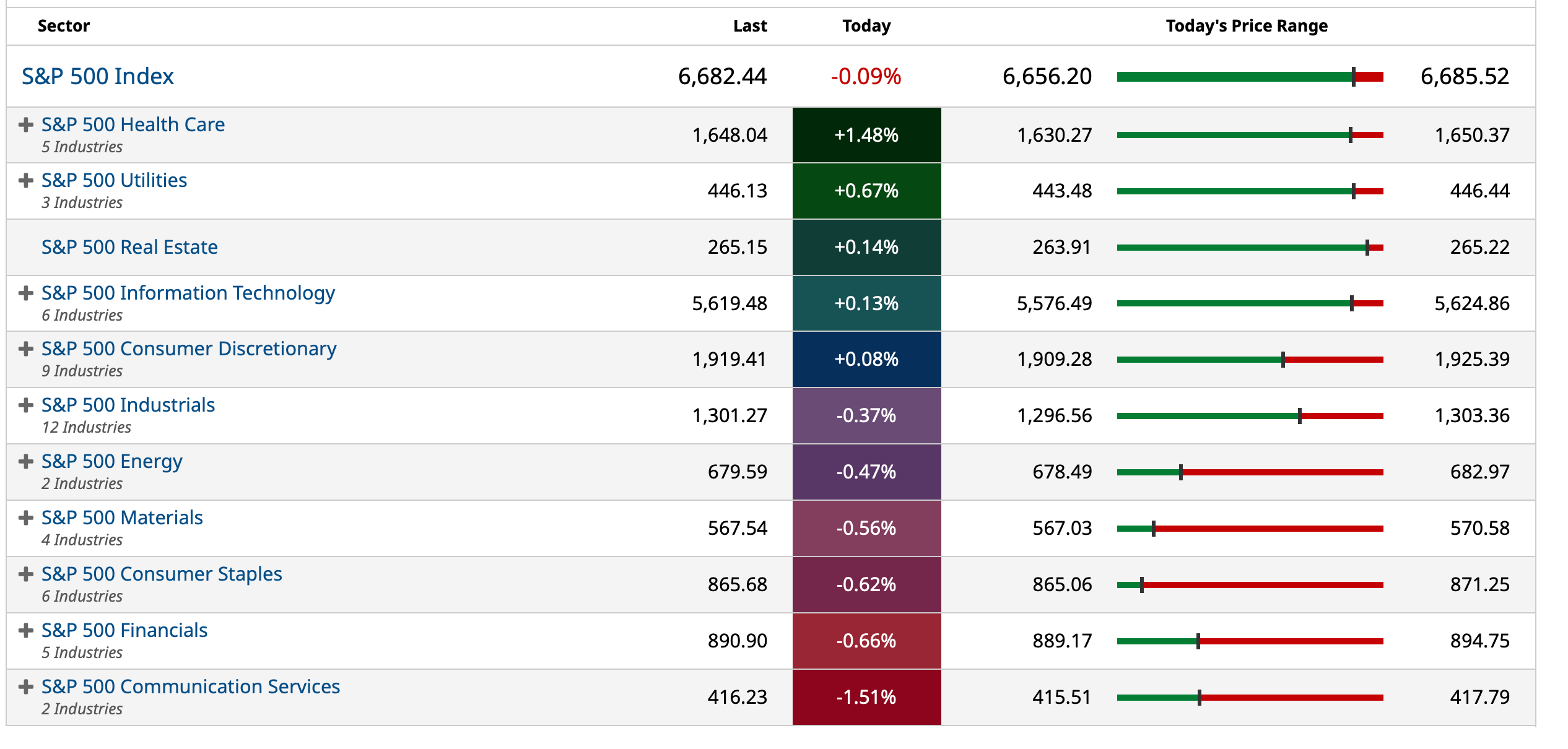

Sectors

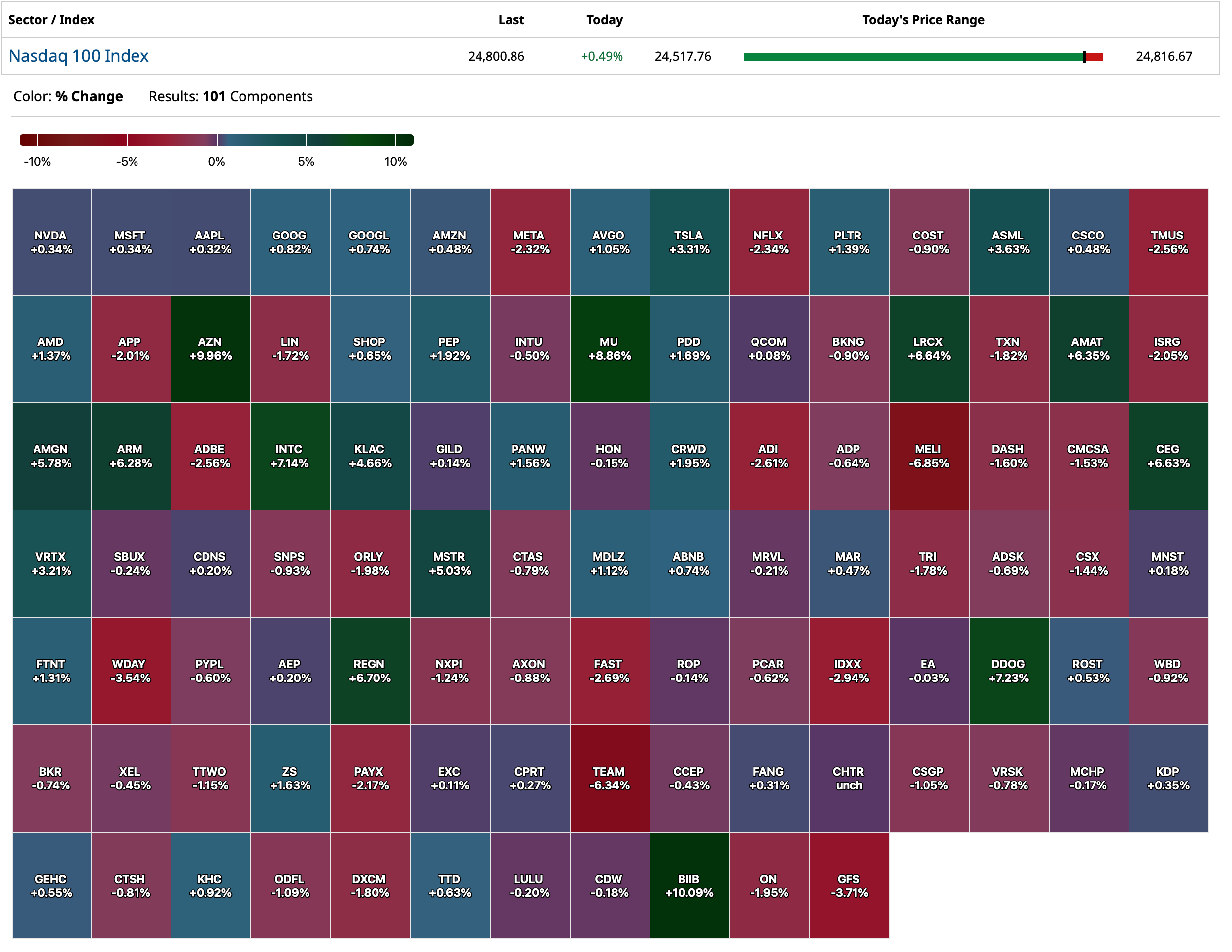

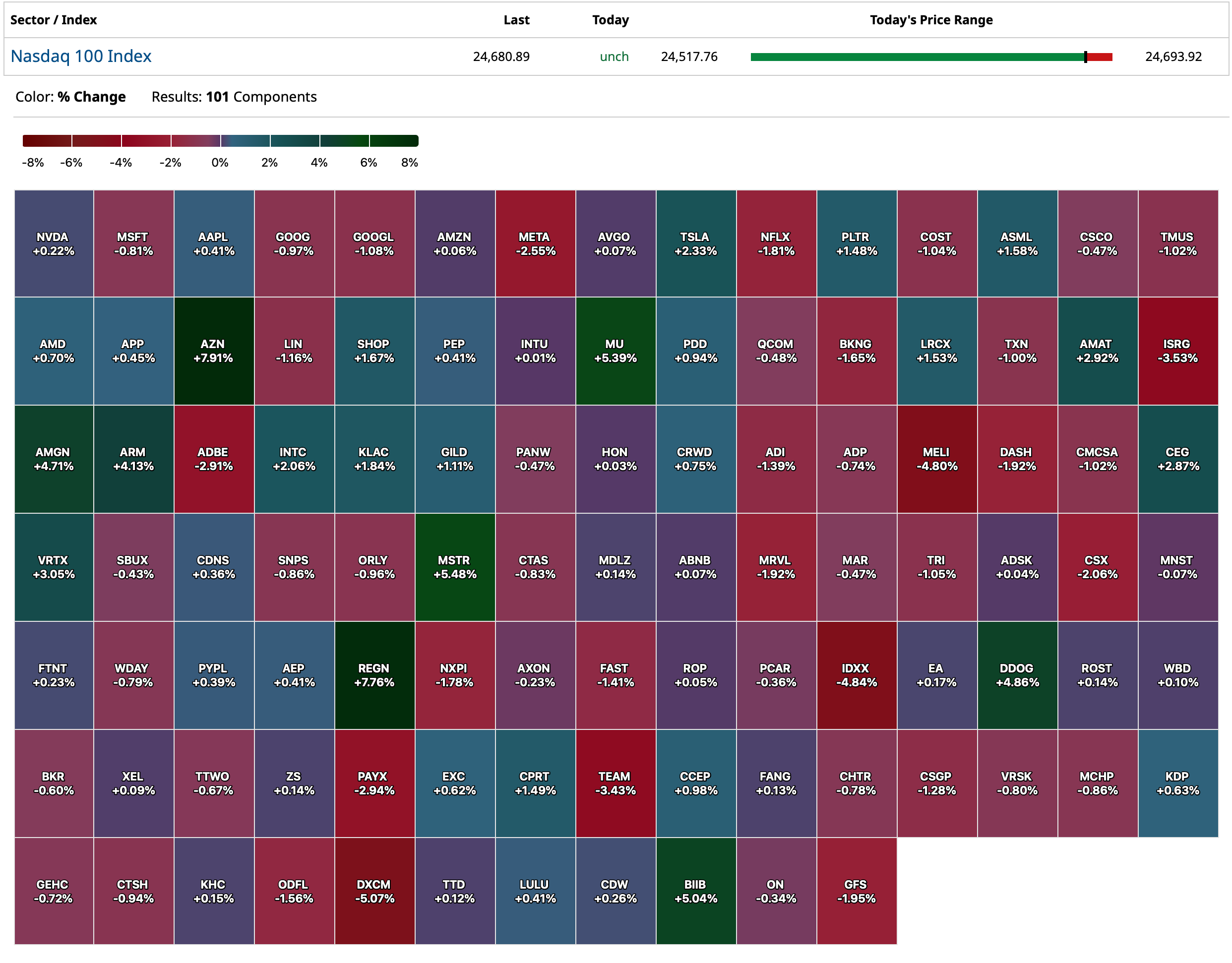

Nasdaq 100 Heat Map

BY Doug Kass · Oct 1, 2025, 4:41 PM EDT

- NYSE volume 16% above its one-month average

- NASDAQ volume 12% above its one-month average

- VIX index: up 0.06% to 16.29

BY Doug Kass · Oct 1, 2025, 4:41 PM EDT

BY Doug Kass · Oct 1, 2025, 2:59 PM EDT

Lost in the noise yesterday was this substantial announcement from CoreWeave (CRWV) about a theoretical $14 billion deal with Meta (META) .

I consider these announcements more than I do deals.

Interestingly, Oracle (ORCL) has already given up about half the gains from the pop they got from displaying a chart, as the markets slowly figure these things out (and insiders tend to sell).

Why would a cash flow-producing, cash-rich company like Meta want to pay CoreWeave for anything, since in theory they can do this all themselves? Basics of leasing versus buying. It is never economic for a cash-rich, higher credit rating company of scale that can do this on their own to lease capacity from a cash-poor, money-losing, lower credit rating company that already has a lot of debt.

In my view, the only reason Meta should want to do this is if they are paying less to CoreWeave than CoreWeave’s economic cost of the capacity they are providing. Meta’s cost of doing it themselves is lower than what they would have to pay CoreWeave, if Coreweave was charging an economic price.

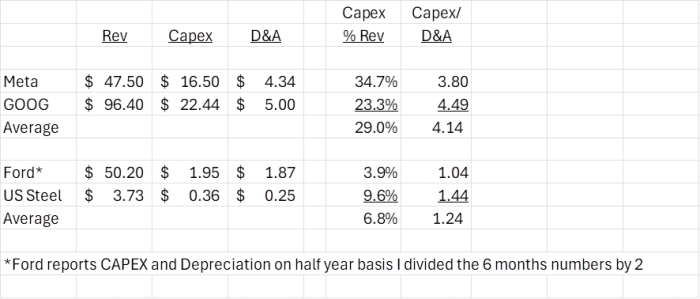

This is also an indicator that the straight CAPEX is at the point where Meta does not even want to bear it on their own anymore (table below from a previous "More Tales"). It is a tacit acknowledgement this is all out of hand.

Yet on this announcement, CRWV stock was up 13% yesterday, which is about $8 billion of market cap. And META’s stock was down about 1% yesterday, which, in their case, was about $25 billion of market cap.

The market got it backwards.

Meta gave their trash to CoreWeave. Meta should have been up and CoreWeave should have been down for selling another giant amount of dis-economic business, otherwise known as buying revenue. Ironically, although not intentionally, the one thing the market did get right was net $17 billion of market cap was lost, which is the consequence of dis-economic investment into generative AI.

P.S.: If this tweet if right, is stunning. OpenAI is planning to use more energy than the U.K. or Germany in five years, and more than India in eight years. That’s just one company. All this power does not exist, nukes cannot be built this quickly, the cost, the water, it all seems impossible:

BY Doug Kass · Oct 1, 2025, 2:40 PM EDT

"As God is my witness."

- Grandma Koufax

On his podcast The Mooch (Anthony Scaramucci) said that the top twenty companies have a combined market cap equal to U.S. GDP.

Today the seven FAANGS’ market cap is $18 trillion.

How is this possibly sustainable?

And more important, how far can prices fall from here when the market corrects?

We could potentially see the biggest loss of paper wealth in history by numbers that will have an enormous macroeconomic effect. These numbers are too large for the Fed or central banks to bail out.

And the decline in stocks, if it occurs, would have a devastating impact on upper-income consumers (who have held up the domestic economy) just as the Fed is trimming their interest income with rate cuts.

The age old question of course remains... when it takes place and when will this matter?

Grandma Koufax, a great investor, always considered upside reward and weighed it against downside risk. She always sought a "margin of safety."

That, you see, is why I am Grandma Koufax's grandson.

BY Doug Kass · Oct 1, 2025, 1:10 PM EDT

- NYSE volume 6% above its one-month average;

- Nasdaq volume 37% above its one-month average;

- VIX index: up 0.43% to 16.35

BY Doug Kass · Oct 1, 2025, 12:00 PM EDT

BY Doug Kass · Oct 1, 2025, 11:51 AM EDT

BY Doug Kass · Oct 1, 2025, 11:45 AM EDT

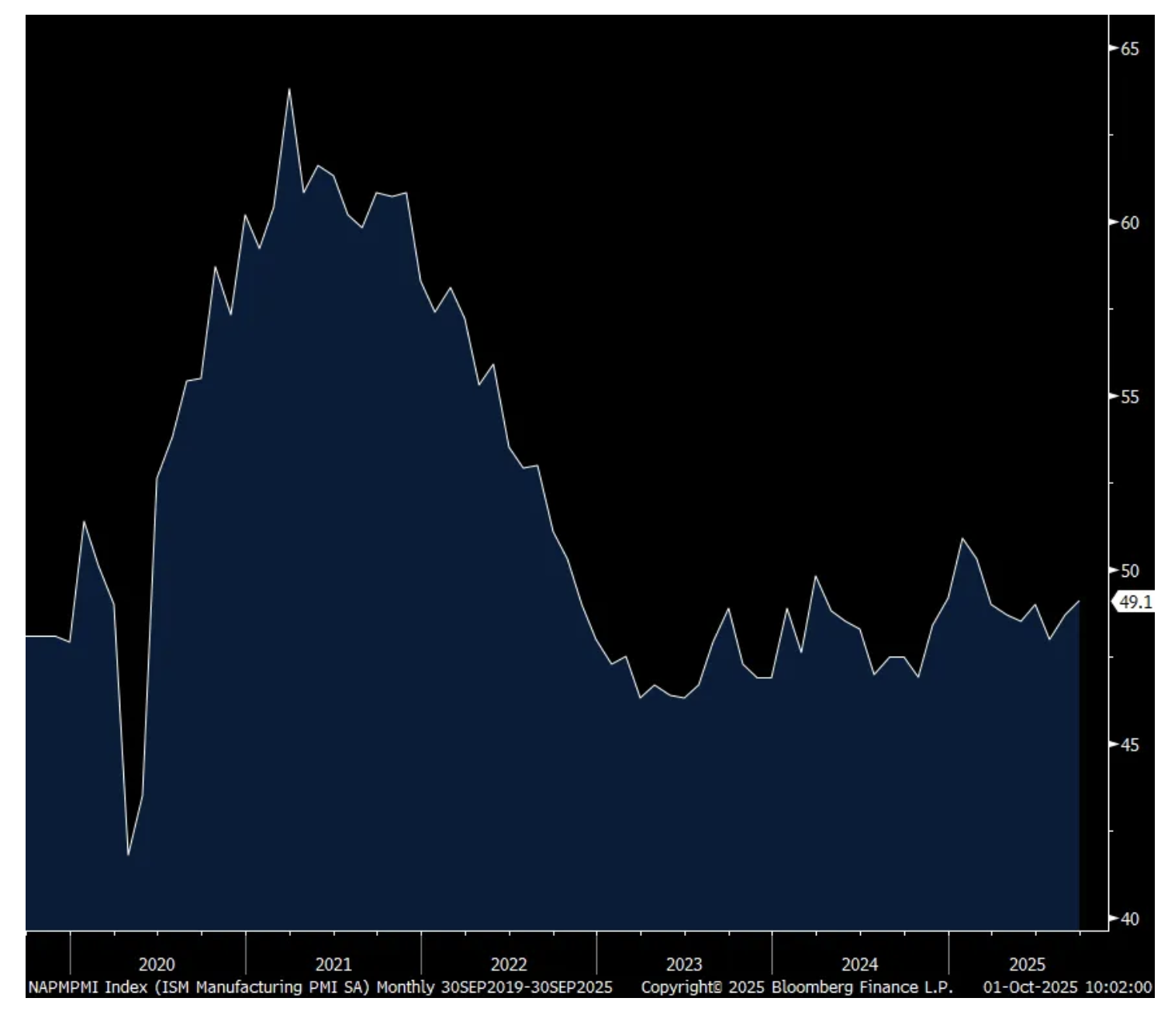

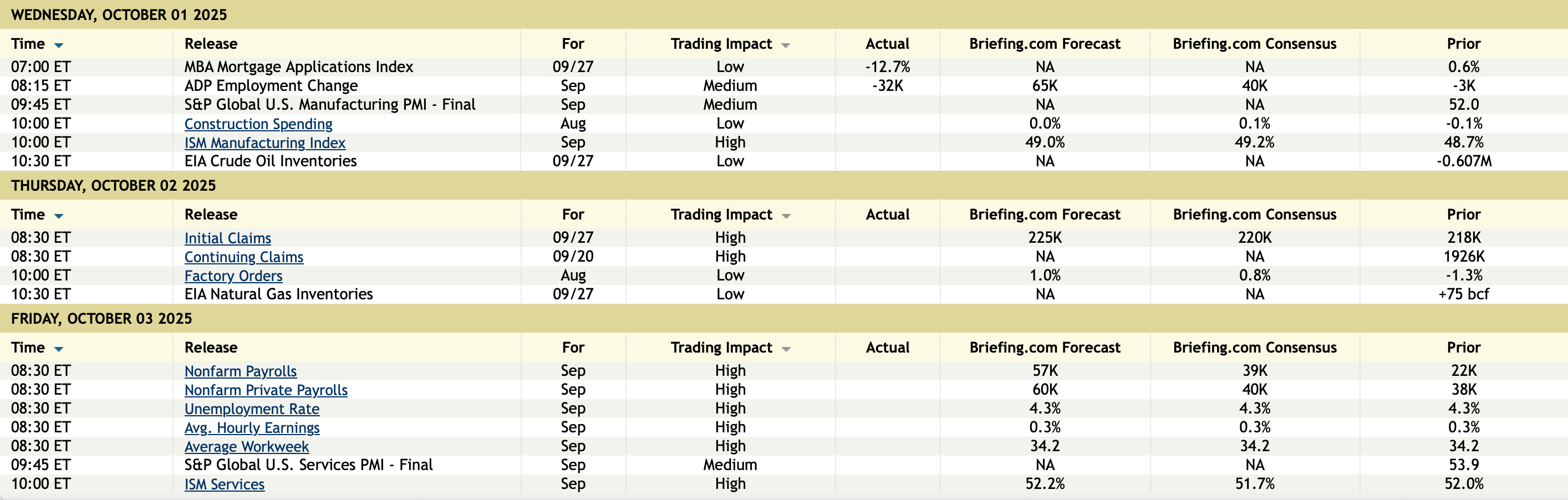

From Peter Boockvar:

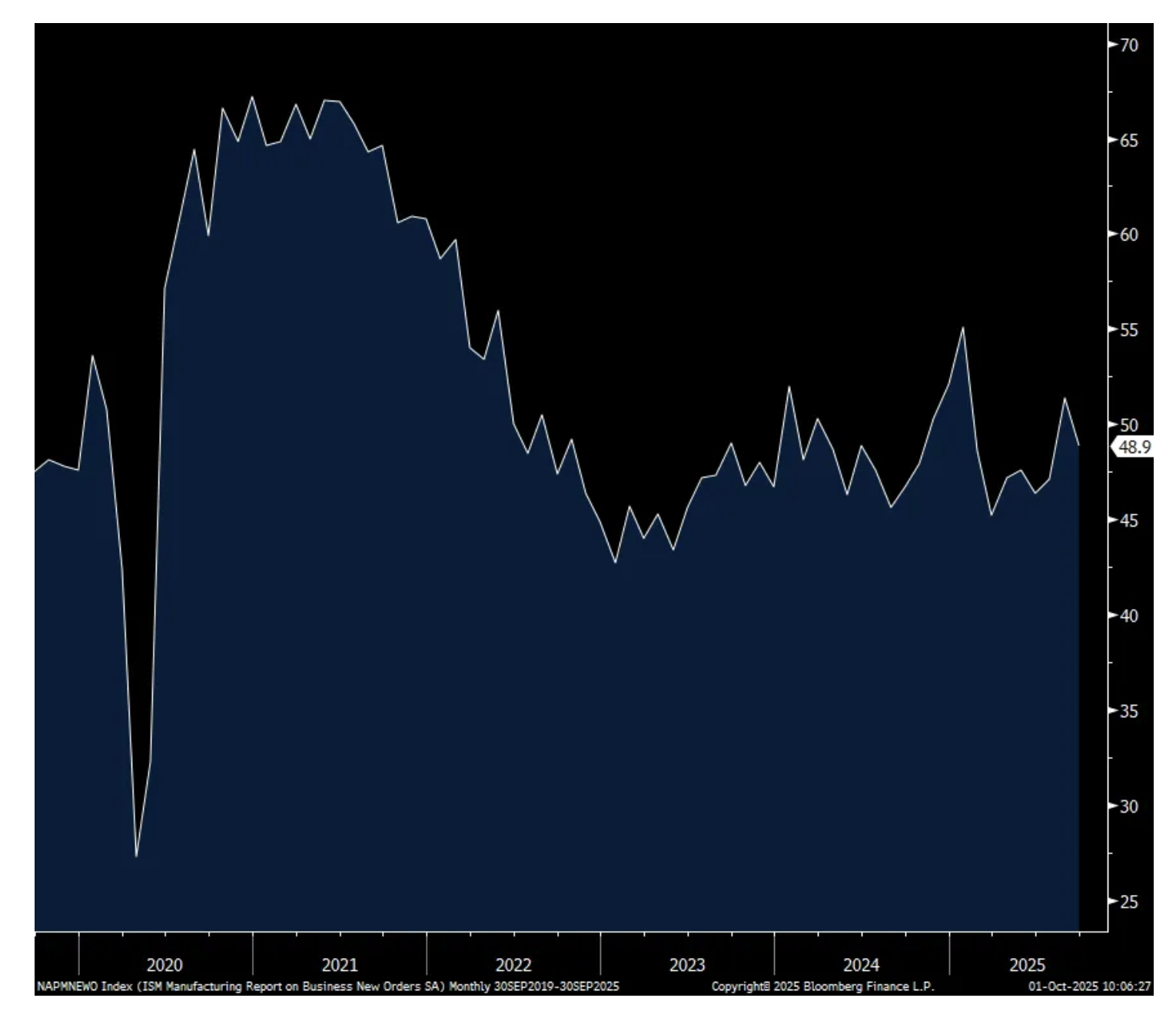

The September ISM manufacturing index was 49.1 as expected and up slightly from the 48.7 print for August. After seeing two figures above 50 in January and February, this is the 7th straight month below 50 and this sector really hasn’t seen any growth since the summer of 2022. Tariffs, as read below by companies themselves, are just kicking the ball in our own net.

New orders fell 2.5 pts to back under 50 at 51.4 after rising by 4.3 pts in August. Backlogs remained well below 50 at 46.2 but up 1.5 pts m/o/m. Inventories were negative too at 47.7 for a 5th month and those at the customer level is at only 43.7. Export orders declined further to 43 from 47.6 while imports were just 44.7. Employment at 45.3 is below 50 for the 8th straight month, though up from 43.8 in August.

Supplier deliveries were up by 1.3 pts to 52.6 but show little sign of supply chain strain. Prices paid fell 1.8 pts but still well above 50 at 61.9.

In terms of industry breadth, just 5 of 18 sectors saw growth vs 7 in August while 11 experienced a contraction vs 10 last month.

With new orders, “Of the six largest manufacturing sectors, none reported increased new orders.”

On employment, “Layoffs and not filling open positions remain the main head-count management strategies.” Of the 18 industries surveyed, 14 saw a decrease in employment.

With inflation, “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods. Higher prices were reported by 32.5 percent of respondents in September, down from 33.5 percent in August.”

Finally with export orders, “Ongoing trade friction is still resulting in dampened demand, as witnessed by the 60 percent of panelists’ comments citing soft demand due to tariffs and uncertain U.S. economic policy.”

The comments from industry are AGAIN littered with the negative implications from tariffs:

“Business continues to be severely depressed. Profits are down and extreme taxes (tariffs) are being shouldered by all companies in our space. We have increased price pressures both to our inputs and customer outputs as companies are starting to pass on tariffs via surcharges, raising prices up to 20 percent. The addition of the derivative steel and aluminum tariffs in the middle of the month — with no announcement — was devastating. Interest-rate lowering or the ‘One Big Beautiful Bill’ will not impact our business, as all capital projects are on hold until there is some level of certainty and customers start to place orders for new equipment again. We believe we are in a stagflation period where prices are up but orders are down due to tariff policy, and again, customers are not willing to pay the higher prices, so they are just not buying. Continuing to find ways to reduce overhead, which means letting go of experienced workers.” (Transportation Equipment)

“The tariffs are still causing issues with imported goods into the U.S. In addition to the cost concerns, product is being held up at borders due to documentation issues. The inflation issues continue; low volumes are a constant concern. The European region is not improving as we had expected, causing further concern for long-term business viability.” (Chemical Products)

“Ongoing macroeconomic conditions highlighted by interest-rate management and tariffs continue to impact customer purchasing decisions, resulting in subdued production rates and growing cost concerns on direct material and operations.” (Machinery)

“Lead times have slightly normalized, but tariffs continue to drive additional spend.” (Petroleum & Coal Products)

“Customer orders are depressed for heavy machinery because tariffs are so impactful to high-end capital equipment. Revenue expectations are flat for the rest of 2025, with no outlook to improve in 2026.” (Electrical Equipment, Appliances & Components)

“Current business conditions remain volatile, with geopolitical tensions, weather disruptions and shifting trade policies driving uncertainty in agricultural commodities. Oils remain sensitive to biofuel demand and global production. Inflation and evolving consumer trends add further complexity. To manage this, we are emphasizing supplier diversification, long-term contracts and formula-based pricing to balance cost stability with flexibility.” (Food, Beverage & Tobacco Products)

“The semiconductor industry is being impacted by high tariff prices on parts from Korea, China and Europe. Our industry is at a low point right now as we race to get new nanotechnology in the U.S.” (Computer & Electronic Products)

“Business is slowing down. Order books are softening as customers push orders out. Seems to be stemming from concerns about the direction of the U.S. economy.” (Plastics & Rubber Products)

“Tariffs still affecting vast amounts of increases in hardware, Al (artificial intelligence) and stainless steel. MRO (maintenance, repair and operating) products have continually increased, and the slowdown in agriculture has had stark impacts on bottom lines for raw materials.” (Fabricated Metal Products)

“Steel tariffs are killing us.” (Miscellaneous Manufacturing)

ISM Mfr’g

New Orders

BY Doug Kass · Oct 1, 2025, 11:35 AM EDT

BY Doug Kass · Oct 1, 2025, 11:19 AM EDT

From my pal "Meet" Bret Jensen on the residential real estate market in Florida (which typically leads the nation) :

Bret Jensen

STAFF

17 minutes ago

Great example of what is happening in the Florida real estate market right now, especially condos with high and rising HOA/taxes/insurance.

2/2 condo right on the intracoastal with a just over $1,400/month HOA. Listed for $675K in August of last year. A price they easily would have got during the boom years following the pandemic. Finally, sold it last week for $425K. I remember when there were bidding wars for these types of properties in 2021 and 2022. AKA, it is getting downright ugly in some real estate markets here.

555 SE 6th Ave Unit 6h, Delray Beach, FL 33483 - 2 beds/2 bathsredfin.com

BY Doug Kass · Oct 1, 2025, 11:00 AM EDT

BY Doug Kass · Oct 1, 2025, 10:45 AM EDT

More Index shorts:

* (SPY) $665.17

* (QQQ) $599.52

BY Doug Kass · Oct 1, 2025, 10:30 AM EDT

BY Doug Kass · Oct 1, 2025, 10:25 AM EDT

From Peter Boockvar:

Not only did the September ADP private sector jobs figure decline by 32k vs the estimate of a gain of 51k, the August number was revised down by 57k to a drop of 3k. Small and medium sized businesses led the job trims with the former seeing a fall of 40k and the latter by 20k. Large businesses, those with 500+ employees, added a net 33k.

The service sector shed 28k with job declines broad and seen in leisure/hospitality, professional/business services, financial services, trade/transportation/utilities and ‘other’. Education/health services and information were the only two sectors adding jobs, with the latter I’m sure boosted by the GenAI hunt for talent.

On the goods producing side, manufacturing lost 2k jobs and construction was trimmed by 5k, partly offset by a 4k person rise in natural resources/mining.

With respect to wages, for ‘job stayers’ pay rose by 4.5% y/o/y vs 4.4% in August. For those changing jobs, they saw a 6.6% y/o/y pay raise versus 7.1% in August.

ADP said succinctly, “this month’s release further validates what we’ve been seeing in the labor market, that US employers have been cautious with hiring.”

My bottom line, the 3 month job gain average is down to 23k that includes the two months of declines and this compares with the 6 month average also at 23k and the 12 month average at 96k. You’ve heard me many times be critical of tariffs and I have to point my finger at them as the main culprit for the labor market weakness, particularly with small and medium sized businesses. The scattershot approach to using tariffs rather than something strategic and selective has battered many small businesses that just do not have the financial flexibility and sourcing capabilities that larger companies do. And it remains a mystery to me why we are putting tariffs on things that we will NEVER produce in the US as it’s just a tax on ourselves.

Interest rates are falling in response but longer end yields remain above where they were right before the Fed cut rates again a few weeks ago.

BY Doug Kass · Oct 1, 2025, 10:10 AM EDT

I added to (HOOD) short at $141.12.

BY Doug Kass · Oct 1, 2025, 10:02 AM EDT

Financials taken to the woodshed again.

We are short across-the-board.

BY Doug Kass · Oct 1, 2025, 9:55 AM EDT

With S&P cash -8 handles I am back to medium-sized short (SPY) $665.10 and (QQQ) $598.57.

BY Doug Kass · Oct 1, 2025, 9:51 AM EDT

From Peter Boockvar:

I will not be publishing tomorrow.

So, with the government partially closed we now watch the polls as I guess the party being blamed the most will be the first one to cave.

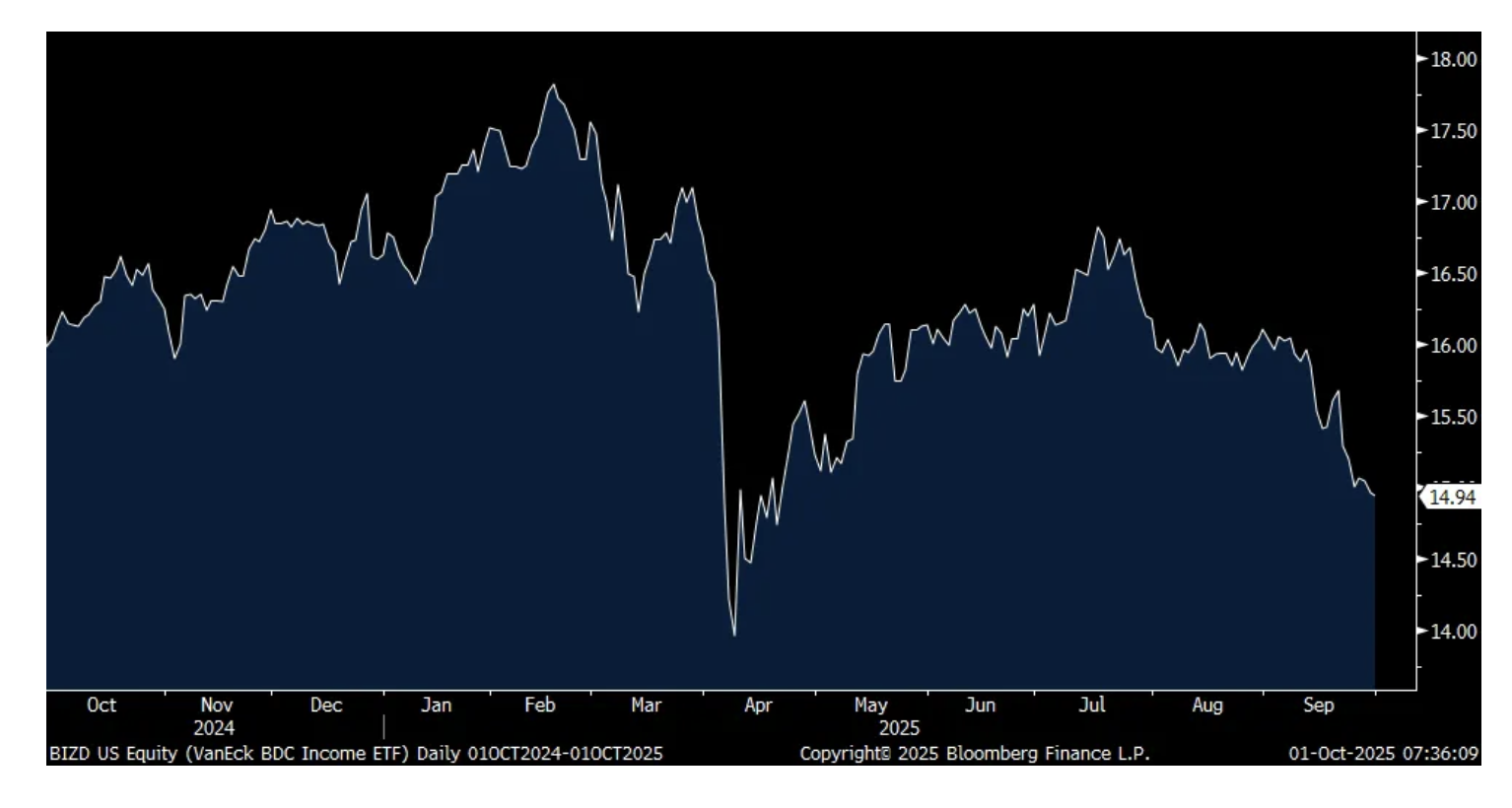

First it was the Tricolor subprime auto news followed by CarMax last week raising its loan loss provisions followed by a Wall Street sell side piece talking about rising delinquencies at Upstart. And throw in the bankruptcy of First Brands and many all of a sudden noticed yesterday this progression of events. The LSTA leveraged loan index closed yesterday within a penny of its lowest since last June. Upstart is down 25% over the past two weeks and Affirm is lower by 26%. Capital One closed Tuesday down 5%, Synchrony Financial lower by 3.1%, SoFi fell 4.1%, American Express weaker by 3%, and the wider BKX index sold off by 1%. Also, BIZD, the business development company ETF, closed at the lowest level since April as dividend cuts are a worry too as a lower fed funds rate clips the interest income of the floating rate loans that are held by these companies.

A canary whistling or nothing more? We watch of course but know full well the financial stress lower to middle income consumers are living through. We also know about the absolute flood of money that has piled into private credit over the past few years. A literal flood of money. I’m sure the experienced underwriters will be fine but when so much money flows into a market, we also assume that many of these loans will not work out. Will credit standards and the cost of capital/credit spreads start to respond?

LSTA Leveraged Loan Index

BIZD etf

As we await the September ADP jobs report as we won’t be seeing the Friday BLS figure, this is what Paychex said in their earnings call yesterday where the stock fell 1.4%:

The glass is half and likely reflecting still a muted pace of firing’s, “Turning to the macro environment, small business remains resilient. Our Small Business Employment Watch shows stable employment and moderating wage inflation and has over the past year, with no signs of recession. Since our last call, we’ve seen greater clarity on key issues such as tariffs, taxes and inflation. With the tax bill in place and Fed rate cuts done, we believe this will support renewed business confidence. This clarity should encourage business owners, particularly those previously adopting a wait-and-see approach, to make more informed strategic decisions, potentially boosting investment and hiring.”

From Nike:

The CEO said, “I spent a lot of time reflecting on the last several months. What keeps me grounded is every time I return from a major sporting event, meeting with athletes or being in the marketplace, I’m even more convinced that the Win Now actions are absolutely the right focus for our teams. With that said, we’re also realistic that we are turning our business around in the face of a cautious consumer, tariff uncertainty, and teams that are still settling into the Sport Offense. We know we have a lot left to prove.”

Revenues rose 1% y/o/y, which was better than expected. A 5% increase in wholesale offset weakness in Nike Direct and their stores. With North America in particular, it “is building momentum through sustained brand activity across sports, leveraging our leading portfolio of sports marketing assts. North America is furthest ahead in taking steps to elevate and transform the marketplace for future growth. Running, training and basketball each delivered double digit growth. Sportswear grew in the quarter, but there is still work to do.” Their ‘classic footwear’ category was weak.

In Europe, the Middle East and Asia, “traffic and demand remained soft” in Nike digital while stores and wholesale grew.

“Greater China, as I mentioned on the last call, is facing structural challenges in the marketplace. Our business was down 10% for the quarter. Seasonal sell-through continues to underperform our plans, requiring larger investments to keep the marketplace clean.”

How much are tariffs costing them now? “And so with the new rates in effect today, we now estimate the gross incremental cost to Nike on an annualized basis to be approximately $1.5 billion, up from the $1 billion we shared 90 days ago. Given the magnitude and timing of the most recent rate increases, we now expect the net headwind in fiscal ‘26 to increase from approximately 75 bps to 120 bps to gross margin.”

And they are likely to never make in the US the things they are sourcing from abroad so these costs are completely unnecessary I will add.

Finally, they expect Q2 revenues “to be down low single digits, including 1 point of benefit from FX.” And they referred to the backdrop as “a dynamic environment.”

From Lamb Weston, the french fry maker:

Something I did not know, “Fries are the most ordered item at US restaurants. They appeal to a broad range of consumers in our America’s favorite order across every generation. The fry attachment rate or how often someone orders fries with their meal remains approximately 2 percentage points higher than before the pandemic. What that means is that when people go out to eat, they are ordering fries more often than in 2019. And we see positive trends around the globe.”

“Turning to the industry, restaurant traffic at several customer channels was flat in the quarter, including overall QSR traffic, while some are growing, including QSR chicken, QSR hamburger, however, was down low single digits and declined another percent in August. Restaurant traffic outside the US has been mixed. Traffic in certain markets, including the UK, our largest international market, declined 4%.”

“Our customers continue to lean into value and menu innovation, including limited time offerings to drive traffic and meet consumer needs.”

As they import palm oil and other ingredients from overseas, tariffs are going to cost them $25 million as they bring this stuff in from Indonesia and Malaysia.

To some data. With the 12 bps w/o/w uptick in mortgage rates, refi’s fell by 21% w/o/w and purchases were down by 1%. Amazing how the slightest changes in rates flow thru applications.

The RBA left rates unchanged as expected at 3.60%. They said “Recent data, while partial and volatile, suggest that inflation in the September quarter may be higher than expected at the time of the August Statement on Monetary Policy.” And, “The decline in underlying inflation has slowed.” These more hawkish comments resulted in a jump in Australian bond yields.

Here were the manufacturing PMI’s for September in Asia that came out today and they seem mixed:

Japan 48.5 vs 49.7

South Korea 50.7 vs 48.3

Taiwan 46.8 vs 47.4

Vietnam 50.4 vs 50.4

Indonesia 50.4 vs 51.5

Thailand 54.6 vs 52.7

Malaysia 49.8 vs 49.9

Philippines 49.9 vs 50.8

India 57.7 vs 59.3

The Eurozone manufacturing PMI was revised up a touch to 49.8 from 49.5 but down from 50.7 in August which happened to be the first time this index was above 50 since 2022. The UK index was 46.2 vs 47 in August.

Also out of Europe was the September CPI which rose 2.2% y/o/y as expected with a core rate gain of 2.3%, also in line and both compare with the ECB deposit rate of 2%. They are on hold, for now. With the data in line, European yields are little changed.

BY Doug Kass · Oct 1, 2025, 9:45 AM EDT

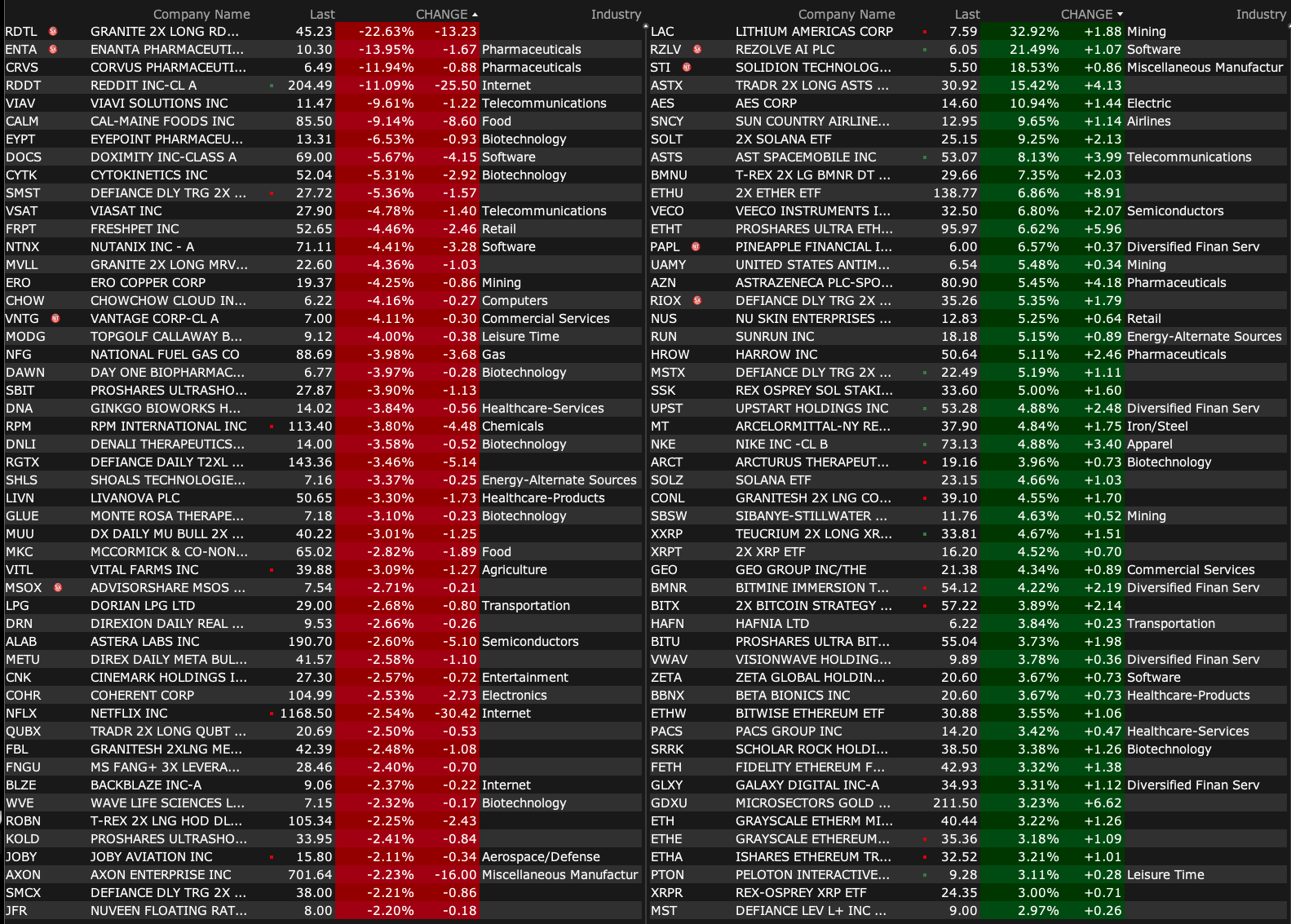

-LAC +37% (US Energy Sec Wright: US to take a 5% stake in Lithium Americas, and 5% stake in Nevada mine project; reaches agreement with GM and U.S. DOE regarding First Draw on DOE Loan)

-RZLV +21% (earnings, guidance)

-VECO +7.3% (Axcelis Technologies and Veeco Instruments to combine in ~$4.4B merger)

-ENTO +6.6% (acquires GRID AI to expand Into High-Growth AI Energy Infrastructure Market)

-RUN +5.1% (Jefferies Raised RUN to Buy from Hold, price target: $21)

-NKE +4.5% (earnings, guidance)

-PLUG +3.9% (delivers First Electrolyzer for 100MW Green Hydrogen Project at Galp’s Sines Refinery)

-AVTX +3.4% (names new Chief Business Officer)

-PTON +3.1% (introduces new commercial equipment line)

-GO +2.8% (hearing upgrade from Telsey)

-HALO +2.3% (to acquire Elektrofi; guidance)

-IOT +2.3% (hearing Evercore ISI Institutional Equities Raised IOT to Outperform from In Line, price target: $50)

-CAG +2.2% (earnings, guidance)

-RDDT -12% (traders circulating unverified stats that OpenAI was barely using Reddit as a source during month of Sept which may have decreased Reddit DAUs)

-CALM -8.0% (earnings)

-AIR -7.0% (prices 3M shares at $83/share)

-VSAT -5.0% (Barclays Cuts VSAT to Underweight from Equal Weight, price target: $23)

-ACLS -3.9% (Axcelis Technologies and Veeco Instruments to combine in ~$4.4B merger)

-RPM -3.6% (earnings, guidance)

-ALAB -2.5% (TD Cowen initiates coverage with Hold rating)

-MRVL -2.1% (TD Cowen Cuts MRVL to Hold from Buy, price target: $85)

-DKNG -2.0% (price target lowered at Oppenheimer)

-GEV -2.0% (RBC Cuts GEV to Sector Perform from Outperform, price target: $605)

BY Doug Kass · Oct 1, 2025, 9:20 AM EDT

BY Doug Kass · Oct 1, 2025, 9:15 AM EDT

BY Doug Kass · Oct 1, 2025, 9:05 AM EDT

Netflix (NFLX) a new short (Monday), traded lower yesterday (-$8).

This morning, in premarket trading, NFLX is -$30/share following Elon Musk's support of the Cancel Netflix Movement. Elon Musk backs 'Cancel Netflix' trend on X: Here's all you need to know | Company News - Business Standard

BY Doug Kass · Oct 1, 2025, 9:00 AM EDT

12:15 p.m.: Fed Bank of Richmond President Barkin (Non-Voter) speaks at the University of North Carolina, Wilmington, NC (Repeat of Sept. 26 speech. Q&A with other speakers follows. No livestream);

5 p.m.: Fed Bank of Chicago President Goolsbee (Voter) Radio Appearance

11:30 a.m.: Treasury hosts a $67B 17-Week Bill Auction

BY Doug Kass · Oct 1, 2025, 8:44 AM EDT

* As 'promised', shorting the rally off the lows of four hours ago...

I am back shorting the indexes:

* (SPY) $663.62

* (QQQ) $597.71

From very early this morning:

* At 4:02 a.m....

Dougie Kass

4:02 AM Wednesday morning

Covered SPY $660.96 and QQQ $594.85 shorts with S and P futures -52 handles - for a profit.

I will recover on a rally.

From yesterday:

With S&P cash +3 handles I am adding to my index shorts:

* (SPY) $663.90

* (QQQ) $598.62

Position: Short SPY (M), QQQ (M)

By Doug Kass Sep 30, 2025 2:40 PM EDT

Position: None

By Doug KassOct 1, 2025 5:45 AM EDT

BY Doug Kass · Oct 1, 2025, 8:15 AM EDT

From JPMorgan:

US: Futs are weaker to start the quarter but have cut overnight losses by more than a third, as the US gov’t shutdown begins. The first shutdown during Trump 1.0 lasted 3 days and the second shutdown 35 days. Pre-mkt, we are seeing a risk-off tone in US assets, including USD weakness, helping buttress int’l mkts where Eurostoxx 50 set a new intraday ATH. The yield curve is twisting steeper. Mag7 names are lower with Semis also pressured; NKE +3% post-EPS. Cmdtys are weaker ex-Precious Metals with silver o/p gold. With the potential for the NFP release to be delayed, ADP takes on heightened importance today and we also receive ISM-Mfg, construction spending, vehicle sales, and mtge applications.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Below we outline what we are looking for in today’s data release as markets weigh Oct and Dec rate cuts, economic trajectory, and the read-through to earnings. Our view is that Oct is a certainty, in terms of a rate cut, but the risk to December is if we see hiring resume proxied by unemployment moving lower. This will be complicated by the roll off of self-terminated federal workers under the DOGE program rolling off payrolls over the next month. Beyond the very near-term, the market setup remains favorable with many growth metrics inflecting higher despite a worsening labor market. Earnings are likely to be robust, producing the fourth consecutive double-digit growth quarter. NKE earnings highlight headwinds from tariffs as well as uncertainty over magnitude. That said, realized tariffs are coming in lighter than expected so the market may continue to look through the recent increase in tariff headlines.

BY Doug Kass · Oct 1, 2025, 7:00 AM EDT

BY Doug Kass · Oct 1, 2025, 6:45 AM EDT

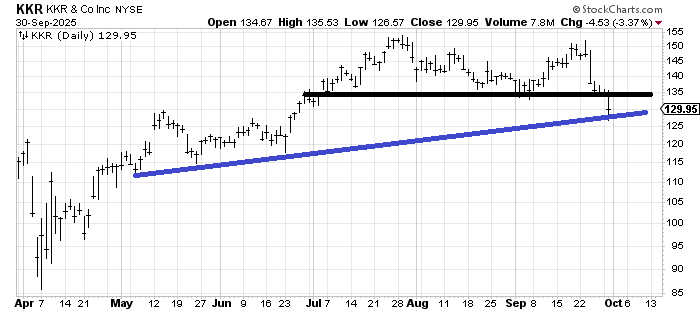

I remain short private equity ( (KKR) and (BX) ) — which have quietly broken down in the last 7-10 trading days.

As an example, KKR traded over $152 on September 23, a week or so later its under $129.

From The Divine Ms M this morning:

Last week I highlighted some of the asset managers like (KKR) and (ARCC) . They had no bounce off those declines, and today they dropped more. Some of the drops were worse than others. KKR is now at support (blue line) but the top it broke from measures to 120.

The good news is last week no one cared about the moves and this week there is a lot of chatter. I don’t have a strong view as to whether stocks like KKR hold here but it ought to be on your radar.

BY Doug Kass · Oct 1, 2025, 6:35 AM EDT

I shorted Nvidia (NVDA) last night at $186.24 .

BY Doug Kass · Oct 1, 2025, 6:25 AM EDT

BY Doug Kass · Oct 1, 2025, 6:15 AM EDT

The S&P Short Range Oscillator stands at -0.45% vs. -0.76%.

That is basically a neutral reading.

BY Doug Kass · Oct 1, 2025, 6:05 AM EDT

Dougie Kass

Two new shorts last night at 6:54 PM:

HOOD $142.48

NVDA $186.24

BY Doug Kass · Oct 1, 2025, 5:55 AM EDT

* At 4:02 AM...

Dougie Kass

4:02 AM Wednesday morning

Covered SPY $660.96 and QQQ $594.85 shorts with S and P futures -52 handles - for a profit.

I will recover on a rally.

From yesterday:

With S&P cash +3 handles I am adding to my index shorts:

* (SPY) $663.90

* (QQQ) $598.62

Position: Short SPY (M), QQQ (M)

By Doug Kass Sep 30, 2025 2:40 PM EDT

BY Doug Kass · Oct 1, 2025, 5:45 AM EDT