This is a story of a well-regarded multi-billion-dollar healthcare hedge fund, BVF (Biotechnology Value Fund), founded in 1993, which had a near 35% holding (19.7 million shares) in MoonLake Immunotherapeutics (MLTX) .

BVF led a Series A financing of MoonLake in 2021.

Yesterday, MoonLake shares fell by nearly 90% after reporting disappointing results for its Phase 3 VELA-1 and VELA-2 trials of sonelokimab in patients with moderate-to-severe acne (inversa).

The Biotechnology Value Fund lost in excess of one billion dollars yesterday.

Bottom Line

Not everyone can be Warren Buffett.

There is plenty of downside to concentrated portfolios — no matter how sophisticated an investor may be.

Boockvar on Home Prices, Manufacturing, JOLTS and Consumer Confidence

From Peter Boockvar:

Home price gains slow/Mfr'g still contracting/JOLTS & consumer confidence point to slowdown in hiring

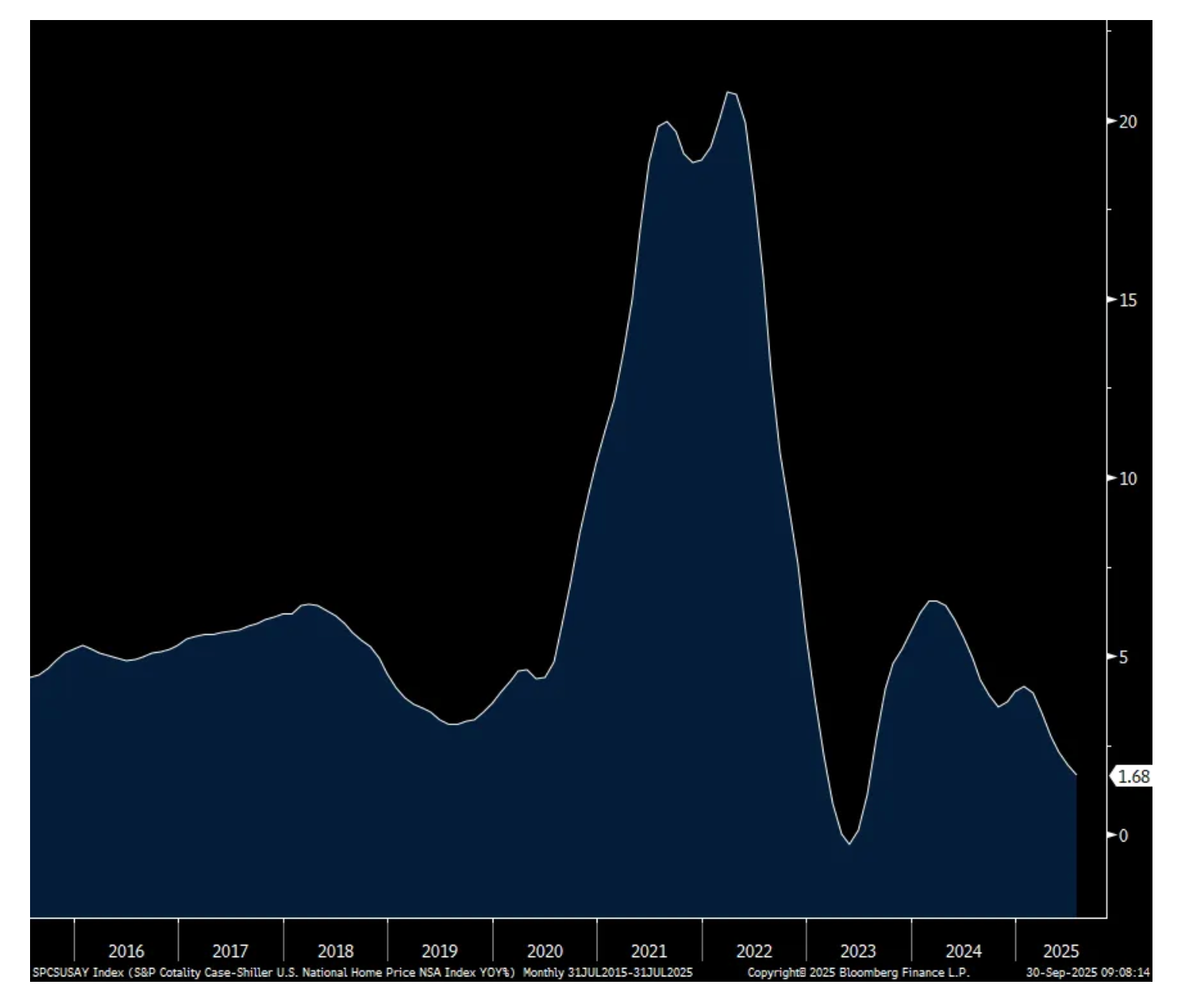

As seen in the somewhat dated July Case-Shiller home price index, price gains continue to moderate y/o/y and are down 5 months in a row m/o/m seasonally adjusted. The y/o/y price increase of 1.7% is the slowest since July 2023, though prices are still up about 50% over the past 5 years.

The overbuilt markets are the ones seeing declines such as in Miami, Tampa, Phoenix and Denver. San Francisco was pretty weak too with home prices down 1.9% in contrast to it being the best rental market in the country right now in terms of rate of price change. Price gains were the best in NY, Chicago, Cleveland and Boston where there has been less supply.

Bottom line, I believe this is a well needed cooling in home price gains so as to thaw out this frozen market. Watching home prices rise like a meme stock is just not a healthy dynamic and why the pace of existing home sales slowed to 30 yr lows. S&P Global said something similar today in this release. “Looking ahead, the housing market appears to be settling into a new, more measured equilibrium. The era of 15-20% annual home price jumps is behind us, and in its place we’re seeing growth rates closer to overall inflation – or even a bit below it. While that means homeowners aren’t gaining wealth at the breakneck pace of the recent past, it also signals a potentially healthier trajectory for housing in the long run. Prices that grow in line with incomes and consumer prices are more sustainable, and they reduce the risk of the kind of affordability crisis and speculative bubbles we’ve seen before.”

Home Price Gain y/o/y

The September Chicago manufacturing PMI remained weak at 40.6 vs 41.5 in August and below the consensus estimate of 43.3. Going back to August 2022, this index was above 50 in just one month and comes the day before the national ISM which is expected tomorrow to print 49 and thus remaining in a modest contraction.

Said in the press release, “The decline was driven by another sharp drop in New Orders, alongside declines in Supplier Deliveries and Employment. These dynamics were partly offset by rises in Production and Order Backlogs.” Prices paid fell a touch, by .4 pts to the lowest since January.

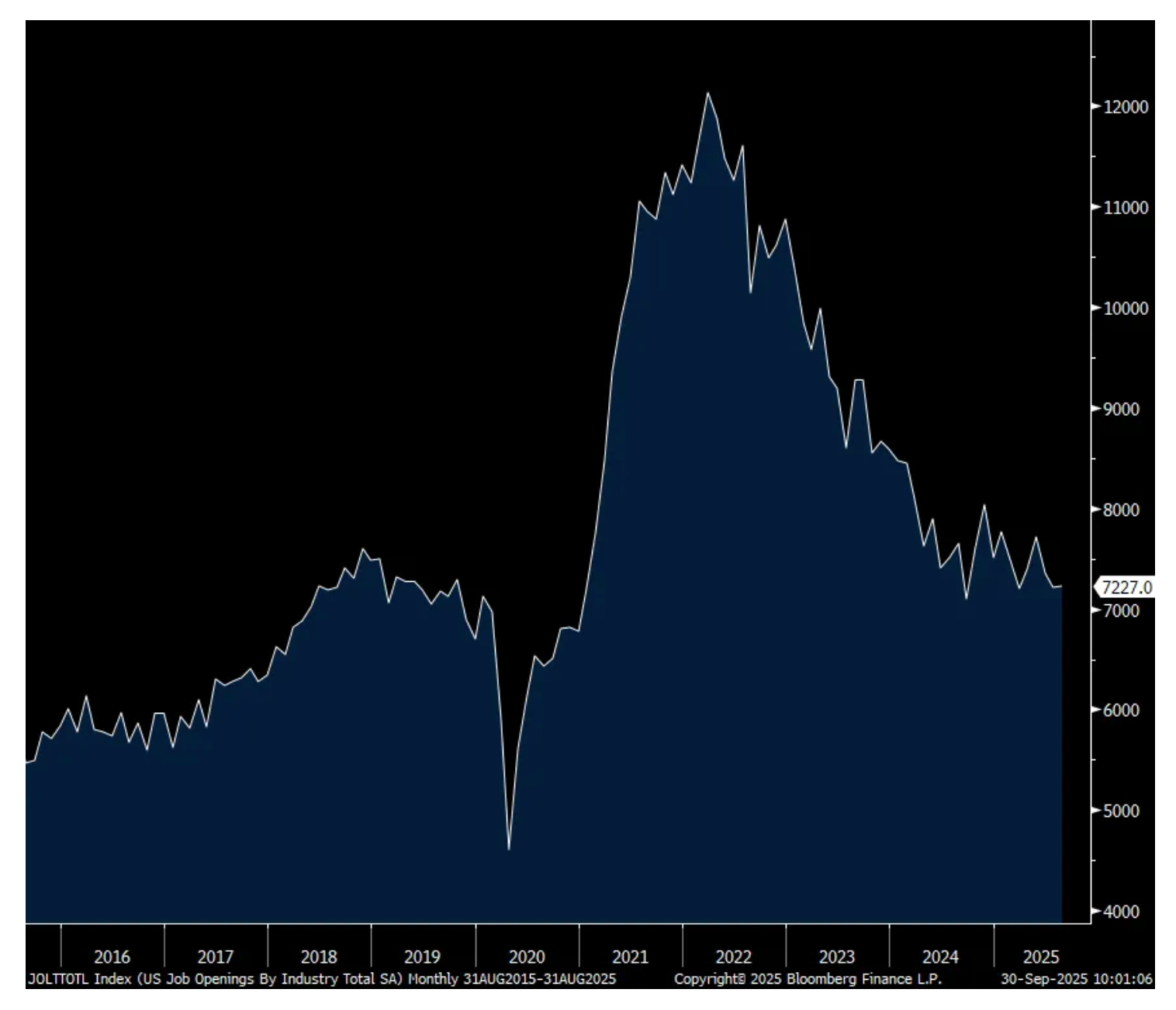

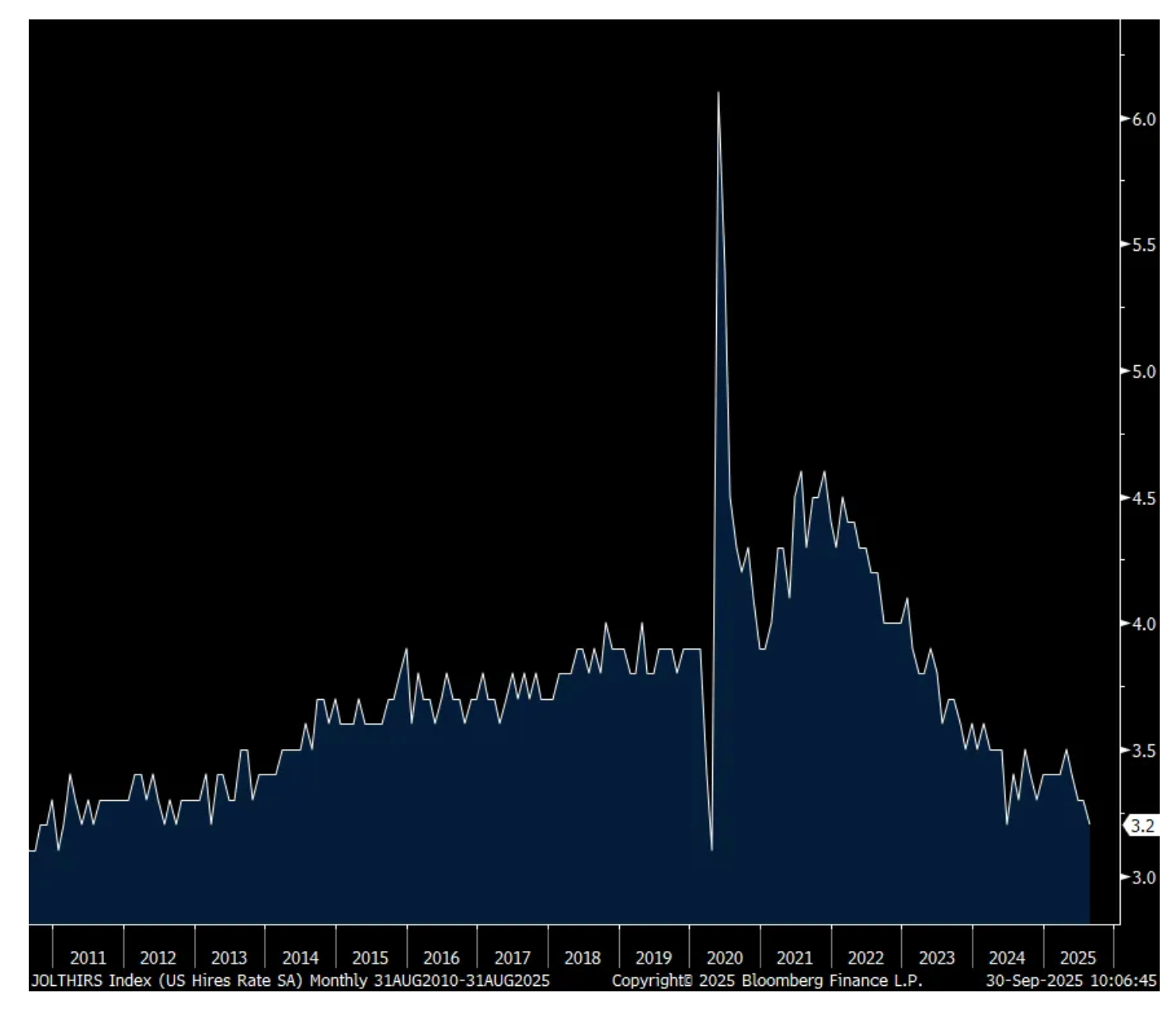

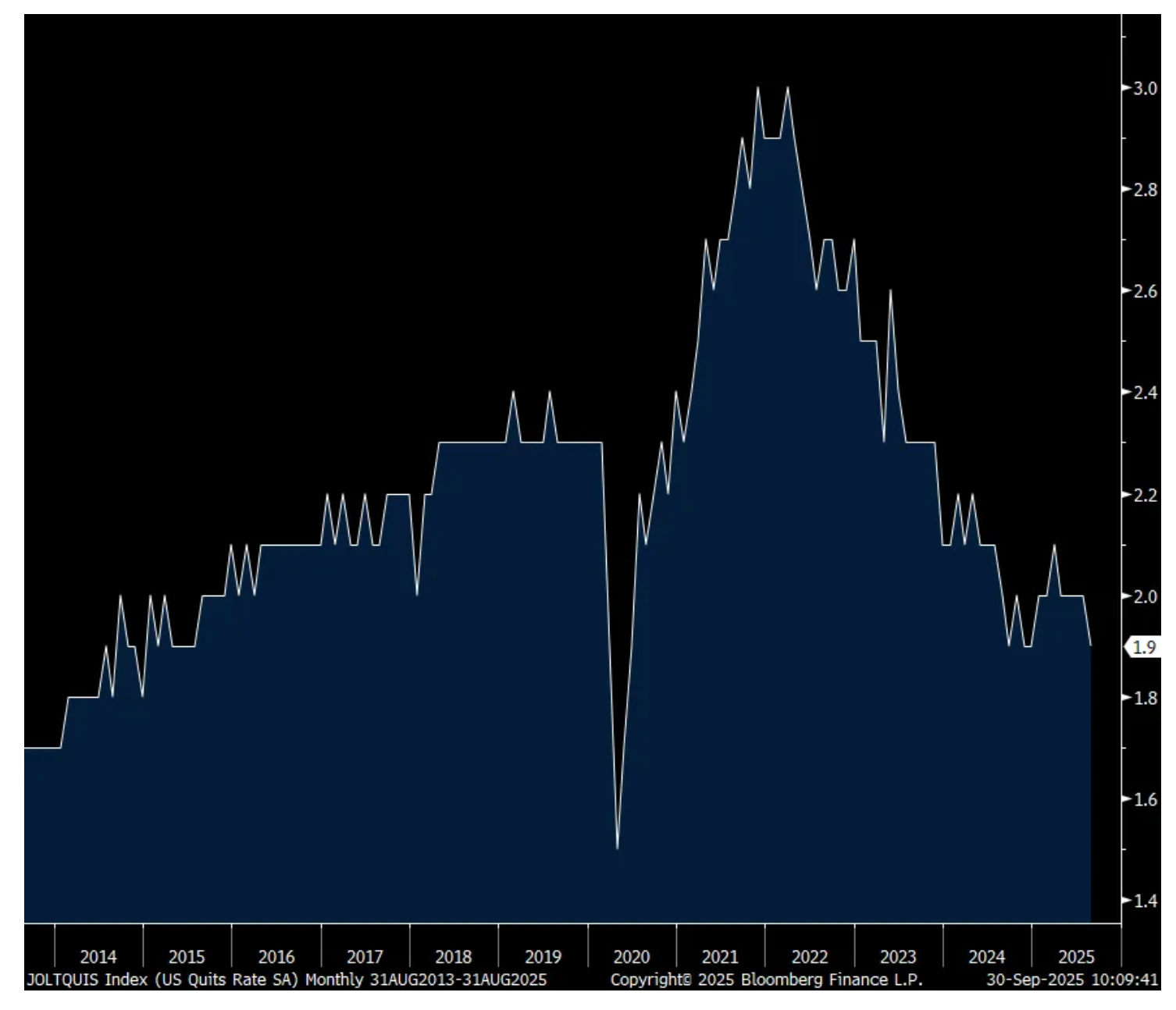

The number of job openings in August totaled 7.227mm which was about as forecasted and little changed with 7.208mm seen in July. Of note, the hiring rate slipped to 3.2% from 3.3% and that matches the lowest level since January 2011 not including Covid. And the quit rate fell to 1.9% from 2% and that matches the lowest since December 2014, also not including Covid.

Bottom line, while job openings are hovering around where they stood in 2019, there is a lot of double counting in the numbers seen now because of the work from home possibilities that didn’t really exist in 2019. And those hiring and quit rates confirm the slowdown in hiring seen in a variety of metrics.

Job Openings

Hiring Rate

Quit Rate

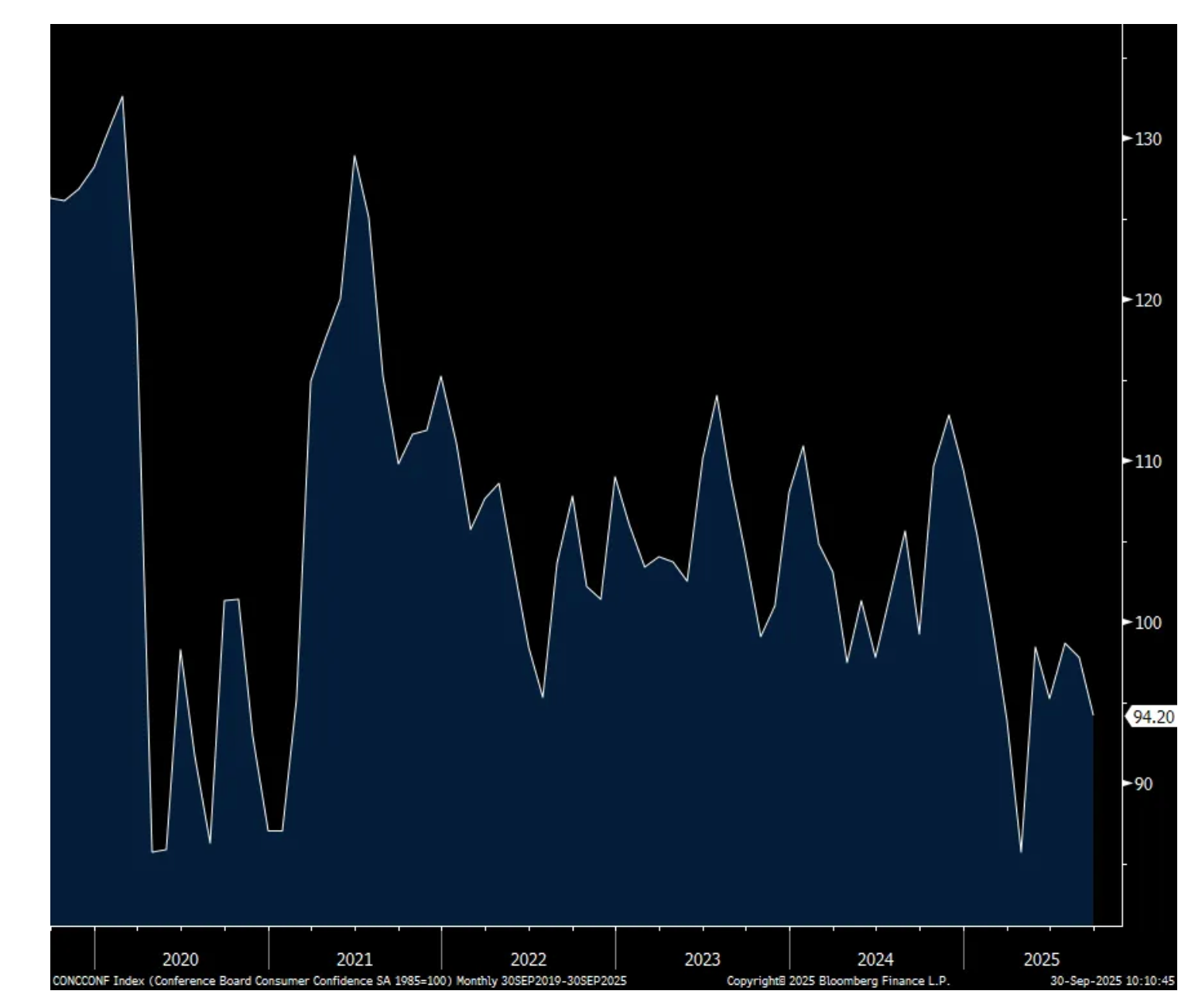

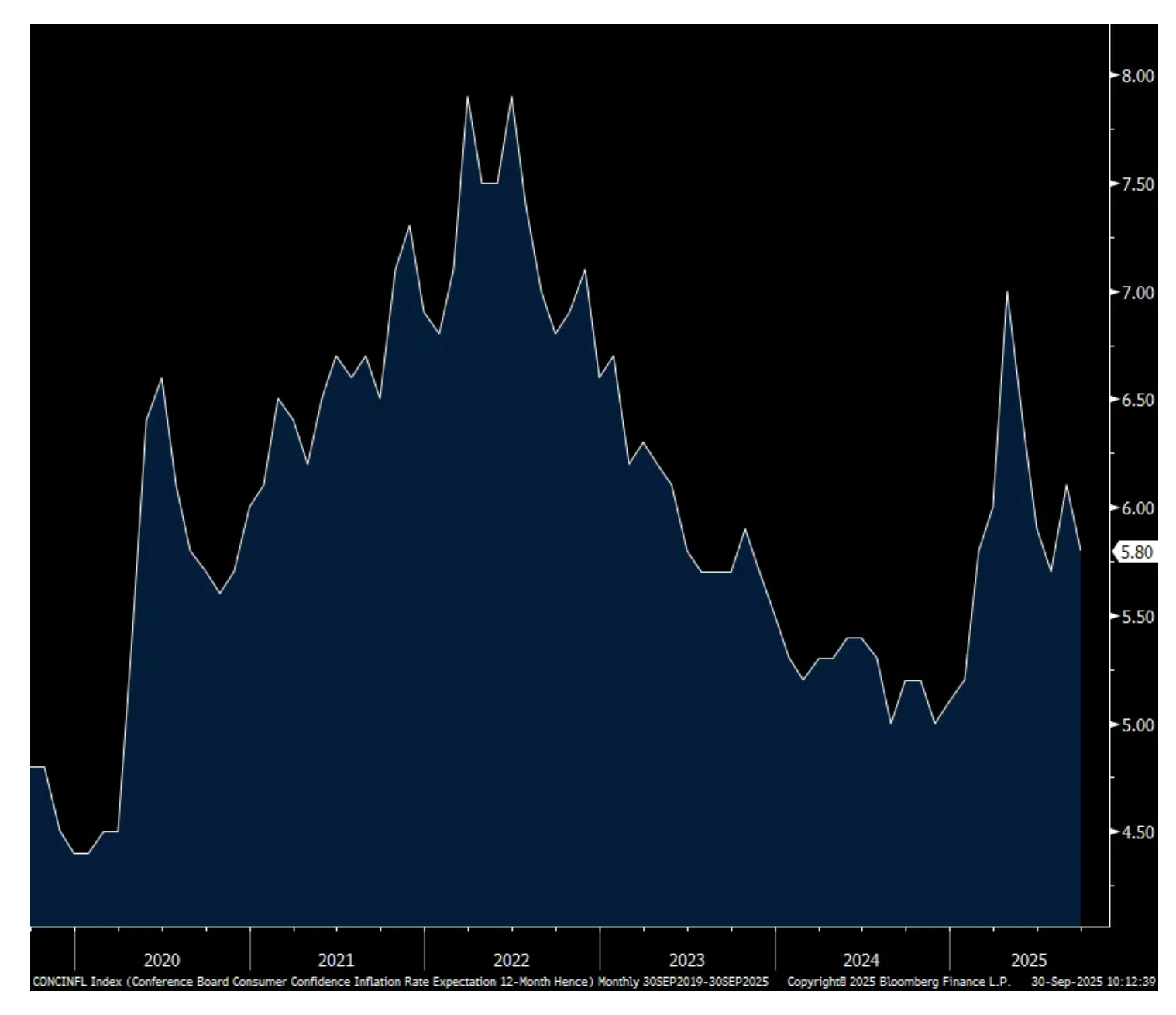

The September consumer confidence index from the Conference Board fell to 94.2 from 97.8 and vs the estimate of 96. That’s a five month low with most of the weakness in the Present Situation component. One year inflation expectations fell to 5.8% from 6.1% in August and vs 5.7% in July.

The answers to the labor market questions deteriorated as those that said jobs were Plentiful fell by 3.3 pts m/o/m to the weakest since February 2021. There was no change to jobs Hard to Get but holding at the highest since February 2021. Those expecting ‘more jobs’ in the coming six months fell to a 3 month low and those expecting an ‘increase’ in income declined by 1.2 pts m/o/m.

The drop in mortgage rates helped to lift buying intentions of a home to a 4 month high, a certain positive within these figures. They did though fall for buying a vehicle by .4 pt after rising by a like amount in August. For major appliances it was a mixed bag.

Demographically, confidence rose for those under 35 but dropped for those older. Income saw “no clear pattern emerging.”

Inflation still matters said the Conference Board as “Consumers’ write-in responses showed that references to prices and inflation rose in September, regaining its top position as the main topic influencing consumes’ views of the economy. References to tariffs declined this month, but remained elevated and continued to be associated with concerns about higher prices.”

And on the slowdown in hiring, “Among consumers’ write-in responses, there was a rise in mentions of jobs and employment to a level unseen since August 2024. The comments were mostly negative, especially when referring to the current situation; there were a few positive comments which mostly conveyed hopes that things would get better.”

Finally, this doesn’t read well, “consumers’ views of their current financial situation recorded the largest one-month drop since we started to collect this data in July 2022.”

Bottom line, I continue to see a very mixed and uneven economy and where one is situated sector wise and income wise are seeing much different economic worlds. The economy is firing on some cylinders and not others.

Rents/Banking/Mfr'g/Cruising/Poor JGB auction/China dominates in EVs

Rents we know are a key component of the inflation stats with them more overweighted in CPI relative to PCE. Apartment List this morning released its National Rent Report covering September and new leases (not renewals) fell .4% m/o/m. “This was the second consecutive m/o/m decline, as we’ve now entered the rental markets off season. It’s likely that we’ll continue to see further modest rent declines through the remainder of the year.” Versus last year, new leases are lower by .8% and compare this with renewals that are up between 2-3% according to the publicly traded apartment REITS.

Also of note, “The national multifamily vacancy rate now sits at 7.1%, a record high for our index (dating back to 2017). We’re past the peak of a multifamily construction surge, but a healthy supply of new units are still hitting the market, and vacancies are still trending up.”

Austin remains the weakest market with rents down 6.5% y/o/y while San Francisco is the best, playing catch up, with rents up 4.9% y/o/y. Generally speaking, the sunbelt states had the most supply over the last few years and they have the weakest markets currently when compared to the coastal regions and two in the Midwest, Chicago and Minneapolis.

As I’ve argued many times, we are sowing the seeds for an eventual uptick in rental growth but that is something more likely to be a 2nd half of 2026 thing. Apartment List finished up by saying, “As construction slows further in the second half of this year and into 2026, rent prices and occupancy should begin to stabilize, and a return to tighter market conditions remains on the horizon. That said, the outlook has been complicated by a continued influx of new units to the market and a weakening macroeconomic outlook, which could lengthen the time that it takes for the market to metabolize the recent growth in the rental stock.”

Out yesterday was the September Banking Conditions Survey from the Dallas Fed and this was their summary:

“Loan volume and demand increased in September. Credit tightening continued, but loan pricing declined. Credit standards and terms eased for residential real estate while tightening continued for the remaining loan types. Overall loan performance deteriorated slightly; however, loan performance for commercial real estate sharply improved. Bankers reported stable general business activity. Bankers’ outlooks are mixed. Survey respondents expect an acceleration in loan demand and increasing business activity six months from now but a moderate deterioration in loan performance.”

This quote from a bank summed up the bifurcated economy we are living in with regards to the haves and the have-nots:

“Outlook continues to be uncertain as we monitor the likelihood of lower short-term rates and future estimates for unemployment and inflation. Borrowers of more modest means are in many cases under financial pressure, while more affluent members seek the benefits of lower rates.”

And more on the mixed picture:

“The uncertainty of the economy seems to be affecting loan demand.”

“The FOMC action in lowering interest rates has definitely created more inquiries about loan interest rates for all types of loans.”

Also out yesterday was the September Dallas manufacturing index which fell to -8.7 from -1.8. I’ll go right to some notable quotes as the internal figures are all over the place and so volatile month to month. The comments point to a still challenged macro environment with continued policy uncertainty and the very first quote below was not encouraging.

“Computer and electronic product manufacturing

I may have to close the company. Orders have stopped coming in, and we do not know why.

Fabricated metal product manufacturing

Orders have been put on hold, and we are not receiving any new [purchase orders] since Aug. 15 on open RFQ’s [requests for quotation].

Food manufacturing

Political and interest rate instability are killing us. We are fortunate that our raw ingredients are stable by price and supply chain availability. The non-profit food relief “business” is a train wreck.

We are still concerned over employment and labor issues.

Furniture and related product manufacturing

We are seeing demand decline.

Machinery manufacturing

We see the oil industry slowing and are more hesitant to invest in their business. We believe that the uncertainty of government decisions is affecting their business decisions, which in turn will affect our business.

We should have our best month of the year in September. Orders are strong, plus we are working on some good new projects.

Relief! Rates are easing, finally. Tariffs are of little consequence. Labor is steady. We might even turn a profit by year-end!

Nonmetallic mineral product manufacturing

After careful evaluation of prevailing economic conditions, including the current level of interest rates and unpredictability of tariffs, our company continues to hold and not proceed upon our expansion plans. The cost of financing at existing rates has materially impacted the feasibility of these projects, and we believe it is prudent to delay implementation until interest rates are reduced to more sustainable and affordable levels.. We remain committed to our operations in Texas and to continued long-term growth. However, further expansion (building addition, inventory expansion, capital equipment acquisition) will be contingent upon a more favorable borrowing environment that supports capital investment and job creation.

The interest rates for mortgages are keeping potential new homeowners out of the market. Homebuilders do not want to build up excess inventory, and therefore our business of producing materials for homebuilders has dropped off significantly. In addition, roughly 30 percent of buyers are falling out of the homebuying process due to inability to qualify for mortgages (credit card debt).

Paper manufacturing

We are still neutral on our current status, but incoming orders are trending down when this time of year they should be up. A few tariff surcharges are starting to show up, but not enough to try to pass along. Competition in the packaging industry has prices declining somewhat.

Printing and related support activities

We need interest rates to fall more than a quarter percentage point.

Incoming orders have definitely slowed way down, and all we can attribute it to is the crazy tariff-induced environment we are living in. Instead of Washington, D.C. policies increasing business and making it better, they seem to be adding way too much uncertainty and making things worse. We have continued to be busy because of robust incoming orders earlier in the summer. If things don’t change quickly, we may soon be looking at reducing hours and possibly cutting back on the number of employees, which will be a shame given how hard it is to get good workers up to speed with your manufacturing processes.

Transportation equipment manufacturing

The trucking industry has now reduced its production forecast for 2026 to essentially be flat with 2025. This remains at a depressed level versus industry averages.”

While the stock traded down 4% yesterday because of conservative guidance with regards to yields, Carnival still had a good quarter and said this:

“yields increased 4.6%, all of which was achieved on a same ship basis. Yields were also over a point better than guidance, again due to the strength in both close-in demand and on-board spending. Unit costs beat guidance by 1.5 pts on continued cost discipline.”

“booking trends have continued to improve since our last update, nicely outpacing capacity growth at higher prices and setting a record for bookings made on sailings two years out. And with nearly half of 2026 already on the books at higher prices, we feel pretty good about next year.”

They also saw “a continuation of strong onboard spending.”

“both North America and Europe are at historical record high levels in pricing.” And this should continue as they also said “we don’t really have capacity growth. So when you think about 2026 with no new ships and then one thereafter for the next couple of years, that’s all going to increase demand on a very restrained supply side for our capacity.”

To the data overseas of note, September CPI in France rose 1.1% y/o/y which was 2 tenths below expectations and we’ll see the German figure in a few hours. French yields though are up a touch.

In Germany, the number of unemployed in September rose by 14k people which was 6k more than consensus, partly offset by a 2k person downward revision to August. Their unemployment rate held at 6.3% but that is the most since the summer of 2020 and 2015 before then and we know the challenges their manufacturing sector is facing.

German Unemployment Rate

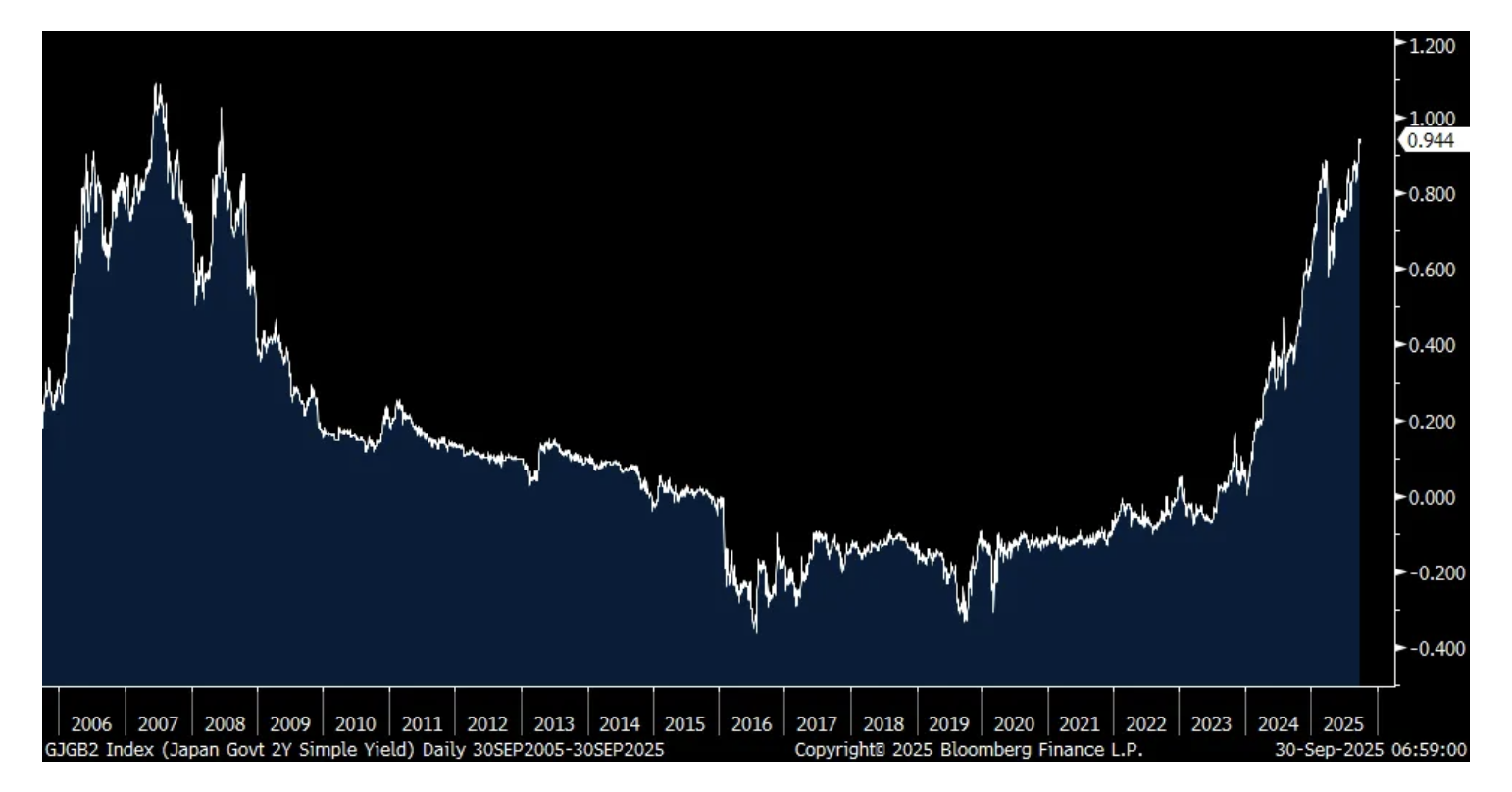

I mentioned yesterday the hawkish comments from a typically dovish BoJ member and that consequence showed up in the 2 yr JGB auction today which saw the weakest bid to cover ratio since 2009 at 2.81 and vs the one year average of 3.79. The 2 yr yield at .944% is at the highest level since 2008 which in turn is helping the yen to rally.

JGB 2 yr Yield

'

In China, its state dominated September manufacturing PMI rose to 49.8 from 49.4 while the non-manufacturing index slipped to 50 from 50.3.

The private sector focused survey from RatingDog saw manufacturing rise to 51.2 from 50.5 while services were little changed at 52.9 vs 53.

With manufactuing RatingDog said “On the demand side, new orders performed well, while new export orders returned to growth for the first time since March 2025. Although new export orders rose only modestly, it was still a relatively positive signal, alleviating some market concerns over the recent weakness in exports.” And “Overall business confidence also strengthened again in September.”

On the services side, “Better market conditions, new product launches and supportive government policies were cited as reasons for the expansion in new work in September...New export orders also expanded in September, driven by rising tourism activity.” Employment on the other hand was soft.

Chinese stocks continued higher and quite a run it’s been. We still own and like the Macau casino stocks along with AIA Group and the big cap tech stocks there.

And to my continued point I’ve been trying to make, the US faces some intense competitive pressure from China in a variety of different manufacturing and tech areas and EVs are a key one. From a Business Insider article citing the CEO of Ford Jim Farley speaking on The Verge’s ‘Decoder’ podcast, he said this:

“The competitive reality is that the Chinese are the 700 pound gorilla in the EV industry. There’s no real competition from Tesla, GM, or Ford with what we’ve seen from China. It is completely dominating the EV landscape globally and more and more outside of China...China’s successful for good reason. It has great innovation at a very low cost.”

I’ll add that ‘innovation’ is something new and should be heeded as they are not just copying their way to success.

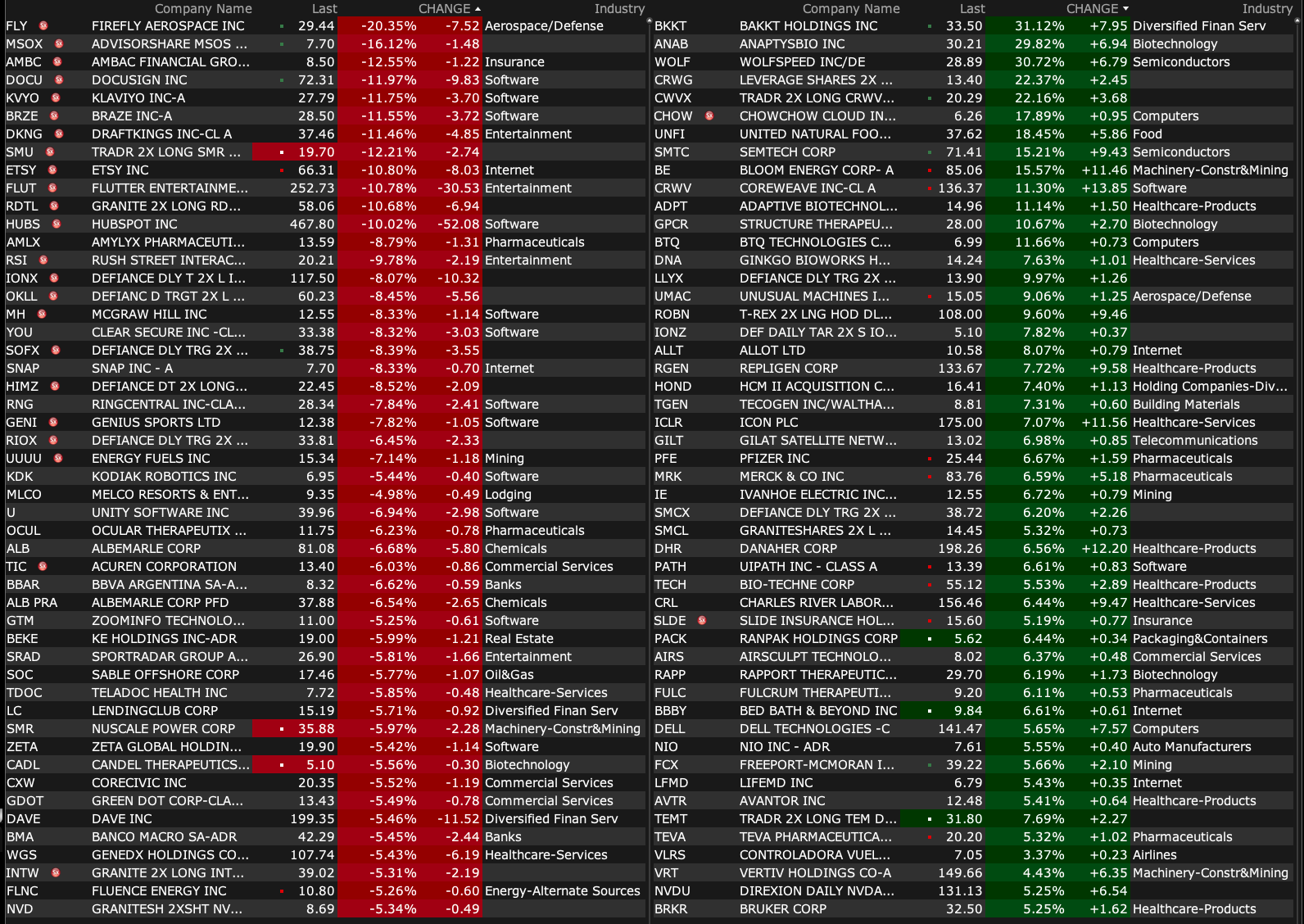

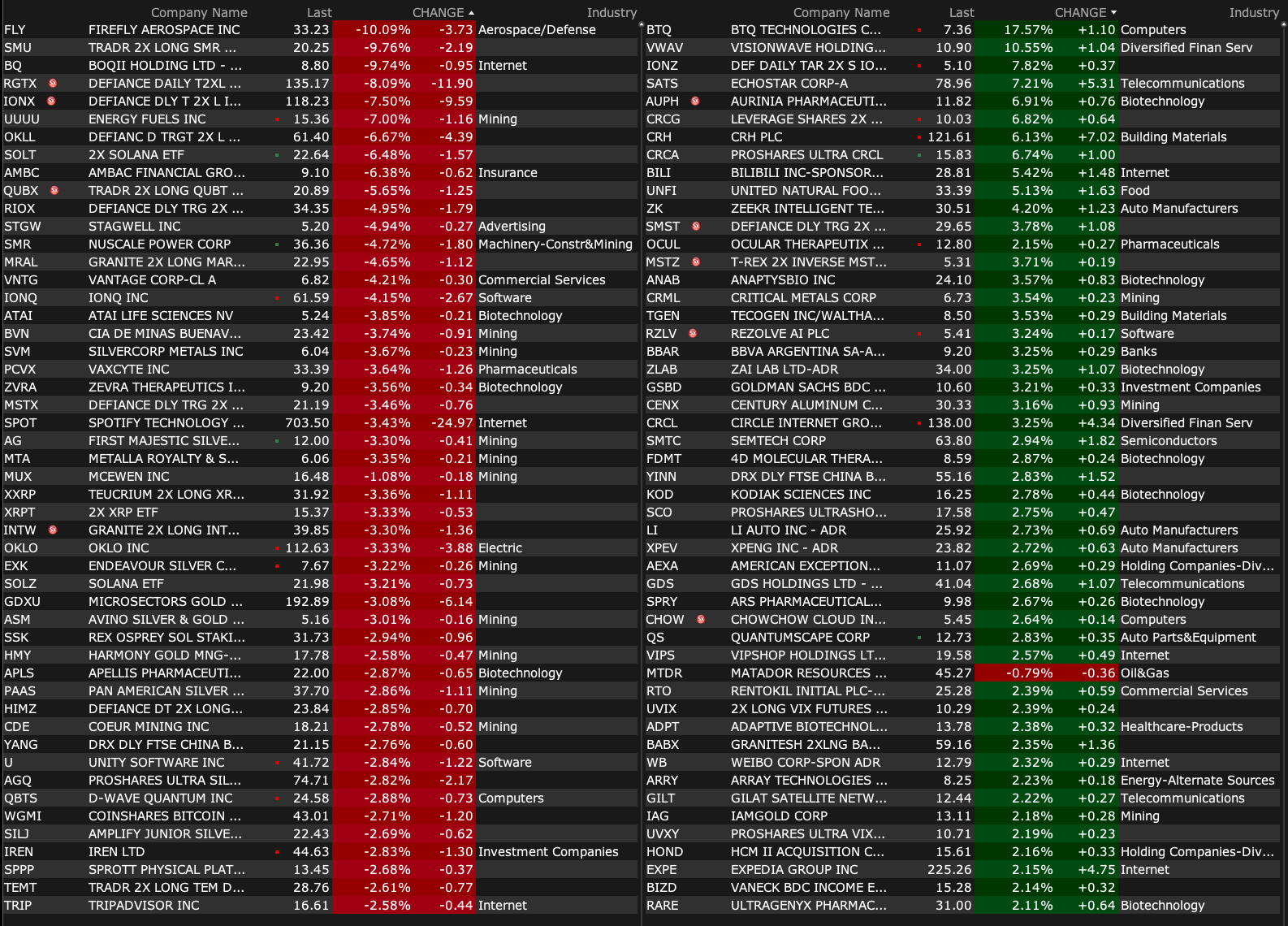

-WOLF +26% (announced the successful completion of its financial restructuring process and emergence from Chapter 11 protection)

-PATH +16% (announces partnerships with Snowflake, Nvidia)

-SLXN +15% (announces Positive New Human Cell Line Data Confirming Pan-KRAS Activity of SIL204, Demonstrating Up to 99.7% Inhibition and First Evidence in Gastric Cancer)

-CRWV +9.2% (said to sign deal with Meta to supply $14.2B worth of compute; Evercore ISI Institutional Equities Initiates CRWV with Outperform, price target: $175)

-AUPH +7.6% (stands behind the favorable benefit/risk profile of LUPKYNIS (voclosporin) by an FDA official)

-SATS +7.3% (Verizon reportedly in talks to acquire AWS-3 wireless spectrum from EchoStar)

-VVOS +7.0% (releases additional clinical data showing marked improvement in pediatric ADHD from use of Vivos DNA device)

-CLRB +6.3% (presented data in Oral Session and Panel Discussions at the American Association for Cancer Research Special Conference on Discovery and Innovation in Pediatric Cancer)

-LW +6.0% (earnings, guidance)

-SMTC +5.4% (Oppenheimer Raised SMTC to Outperform from Perform, price target: $81)

-CELH +4.7% (Morgan Stanley Raised CELH to Overweight from Equal Weight, price target: $70)

-UNFI +4.7% (earnings, guidance)

-UMAC +4.1% (awarded $12.8M order for components supplying Strategic Logix's Rapid Reconfigurable Systems Line)

-FEAM +3.5% (earnings)

-QS +3.0% (QuantumScape and Corning sign agreement to jointly develop ceramic separator manufacturing capabilities for QS solid-state batteries)

-NEOV +2.9% (earnings)

-SSKN +2.8% (receives continued validation for personalized approach with new published study highlighting Xtrac excimer laser treatment combined with a topical drug in psoriasis)

-TAOP +2.7% (to acquire Skyladder Group in all-stock transaction valued at CNY 152M)

-FCX +2.1% (Tier1 firm Raised FCX to Buy from Neutral, price target: $42)

Downside:

-ARTL -21% (announces pricing of $2.0M public offering of 441K shares at $4.40/shr)

-FLY -11% (disclosed first stage of Firefly’s Alpha Flight 7 rocket experienced an event that resulted in a loss of the stage)

-UUUU -6.3% (files to sell $550M of convertible senior notes due 2031)

-IDT -6.0% (earnings, guidance)

-OSS -4.5% (prices 2.5M shares at $5.00/shr in $12.5M registered direct offering)

-SPOT -3.8% (Founder and CEO Daniel Ek to Become Executive Chairman, Appoints Alex Norstrom and Gustav Soderström as Co-CEOs, effective Jan 2026; Goldman Sachs Cuts SPOT to Neutral from Buy, price target: $770)

As you are all aware, during the last week I have begun to build up short positions in (the very popular) financial sector — with emphasis on money center banks.

From my pal Larry McDonald this morning (and I am in agreement for many of the same reasons):

"Personally, I am the MOST bearish on the financials today since Q1 2007. I am long June 2026 puts (in size) on C, BAC, and JPM in my personal account. Why high conviction? C (Citi) equity % above its 200-week moving average is EXTREMELY rare, a strong sell signal. Since 2000, C equity has only been here one week, in January 2008. 1) Mortgage delinquency trends are moving higher, inflation and higher rates have the bottom 60% in real pain. 2) There is a credit crisis developing in (Business Development Companies in private credit) BDCs, and software defaults are rising fast. 3) Auto financing is a complete mess. 4) Buy now, pay later equities are crashing. 5) Student lending is crashing. 6) Month-end - Quarter-end liquidity for the banks is bearish for the next 20 days. Puts are for speculative investors only; this is a hedge vs. my size hard asset positions. Taking some of my (gold, platinum, palladium, and silver) gains and shorting the financials. "

Just wishin' and hopin' and thinkin' and prayin' Plannin' and dreamin' his kisses will start That won't get you into his heart- Dusty Springfield, Just Wishin' and Hopin' NEW * Wishin' And Hopin' - Dusty Springfield {Stereo}

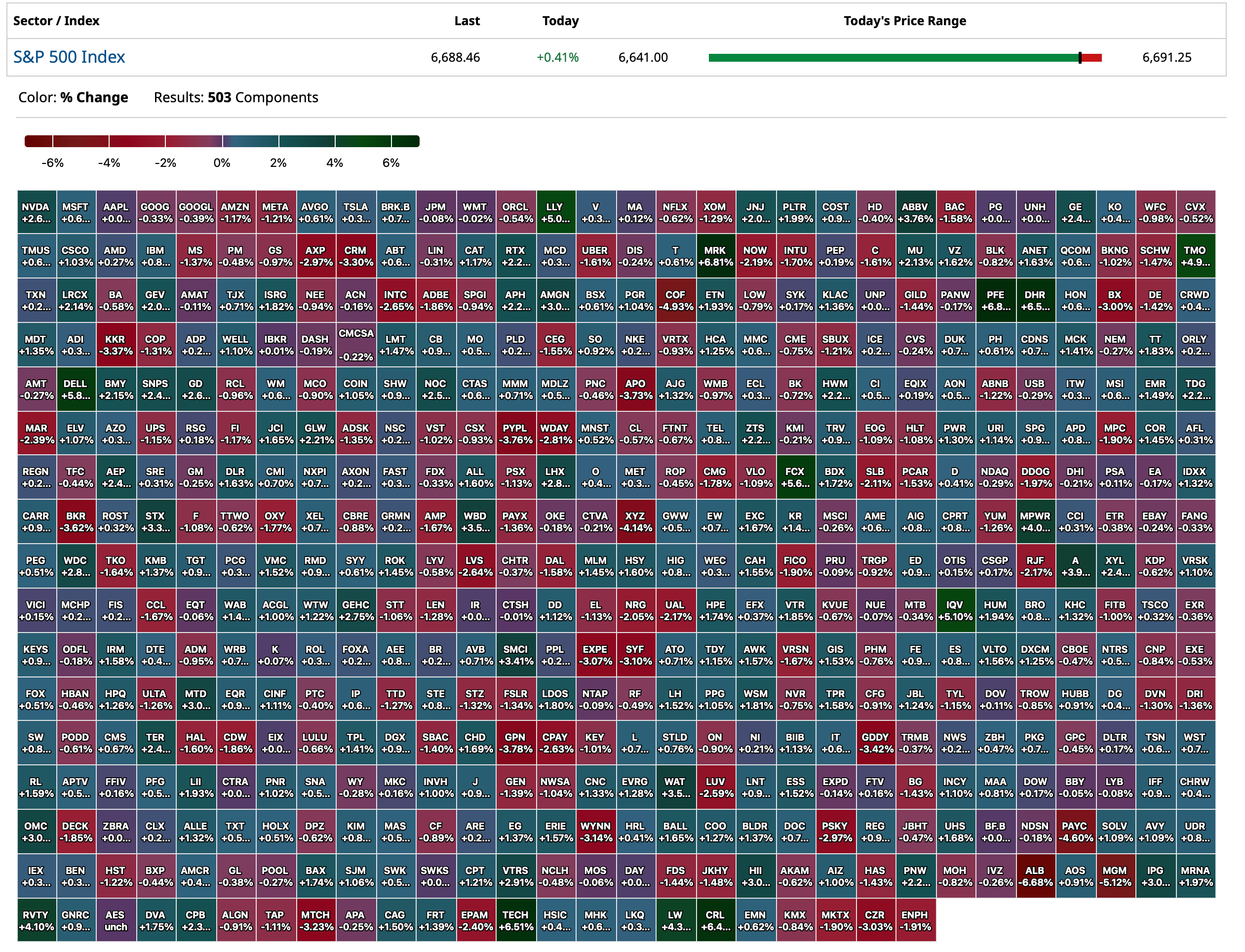

Over the last few days, equities seem to be meandering in a trendless way.

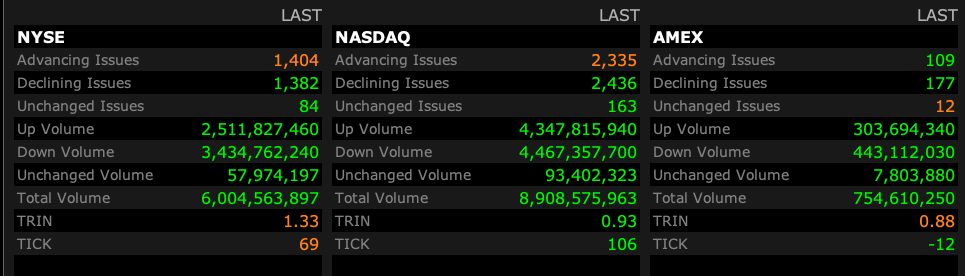

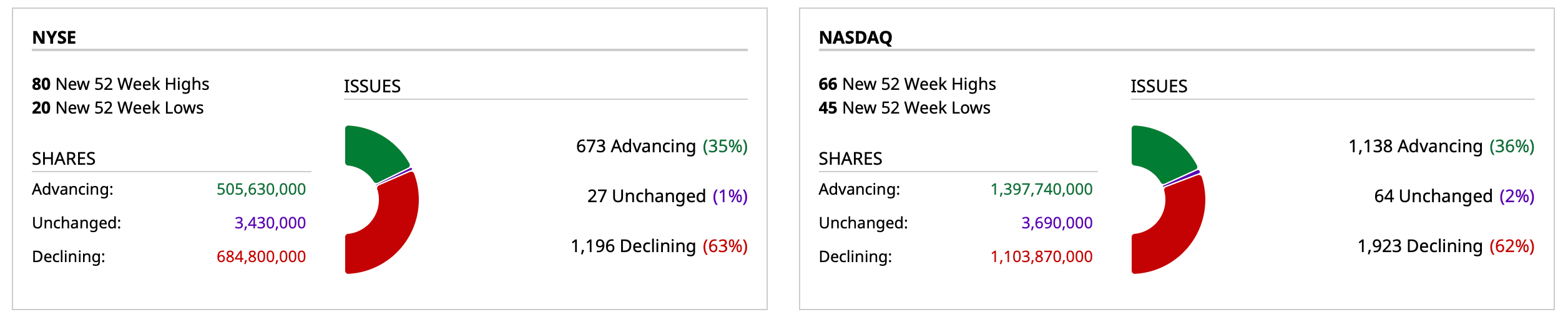

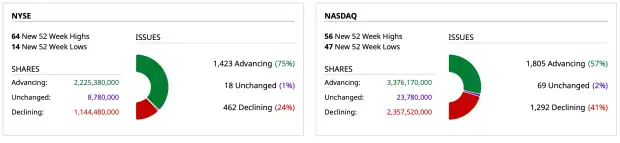

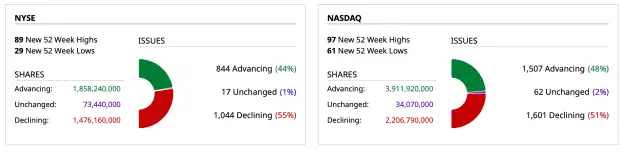

Market breadth on Friday was great:

Market breadth yesterday was wanting:

That said I am planning to significantly raise my net short exposure today and over the balance of the week based on my multiple fundamental (economic, inflation, deficit/debt-load, AI concerns, etc.), sentiment and valuation concerns.

Or maybe I am just wishin' and hopin' that investors will catch on to the threat of "slugflation."

In defending my ursine view I would again add that the "artificial" influence of passive investing (products and strategies that worship at the altar of price momentum) is dirtying up the market's water though the fish could be shortly overcome by the pollution of overvaluation.

US: Futs are lower as we close out the quarter/month, ahead of a likely gov’t shutdown. Bond yields are lower as the curve bull steepens; the USD is weaker, sitting ~1.1% above its 52-wk low. Pre-mkt, Mag7 are all lower with Semis mixed; Defensives seeing outperformance relative to Cyclicals. Within cmdtys, virtual everything is lower ex-natgas; gold / silver down 86 and 196bps, respectively looks like profit-taking / rebalancing with crude lower on potential increased OPEC+ supply. Trump set 10% tariffs on timber and 25% on kitchen cabinets as of Oct 14. Today’s macro data focus is JOLTS, Consumer Confidence, Housing Price Indices, and regional activity indicators. Expect headlines on the shutdown through the day, which we analyze in the succeeding sections but ultimately do not see a material impact on markets.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

With the risk of the government shutdown and subsequent delay of some macro data releases, specifically NFP, the market may put extra emphasis on today’s JOLTS and tomorrow’s ADP prints, in addition to other macro data that points to the Fed maintaining the expected 25bp cut in October. The bond market is pricing in an ~89% chance of a cut in October; we agree with that view with December being at-risk from an accelerating economy that translates into improved hiring. Stated differently, if unemployment (U.3) were to fall to 4.1%, or lower, ahead of the December Fed that may be enough to trigger a pause. That said, the near-term risk is for higher unemployment given the roll off of federal employees who voluntarily accepted the DOGE layoff package, which should show in the October data that prints in November.

· JOLTS – Feroli sees JOLTS openings declining from 7.181mm to 7.050mm MoM, implying a 4.2% job opening rate, the lowest of the cycle. The hiring rate of 3.3% would be near the bottom of the post-COVID range.

· ADP – Feroli sees private sector employment increasing by 54k jobs, down from prior month’s 106k jobs. He notes that the average absolute error between ADP and NFP, over the last 12 months, is 82k; but this narrows to 20k of revised BLS data over the last six months.

· NFP – Feroli sees 50k jobs being added, up from last month’s 22k. Unemployment stays at 4.3%.

· GOV’T SHUTDOWN – this gov’t shutdown is different from a debt ceiling event. Debt ceiling means the gov’t can spend but not issue debt. A gov’t shutdown means the gov’t can issue debt but not spend it. The OBBBA raised the debt ceiling so, most likely, a credit downgrade is off the table.