Friday's Closing Market Stats

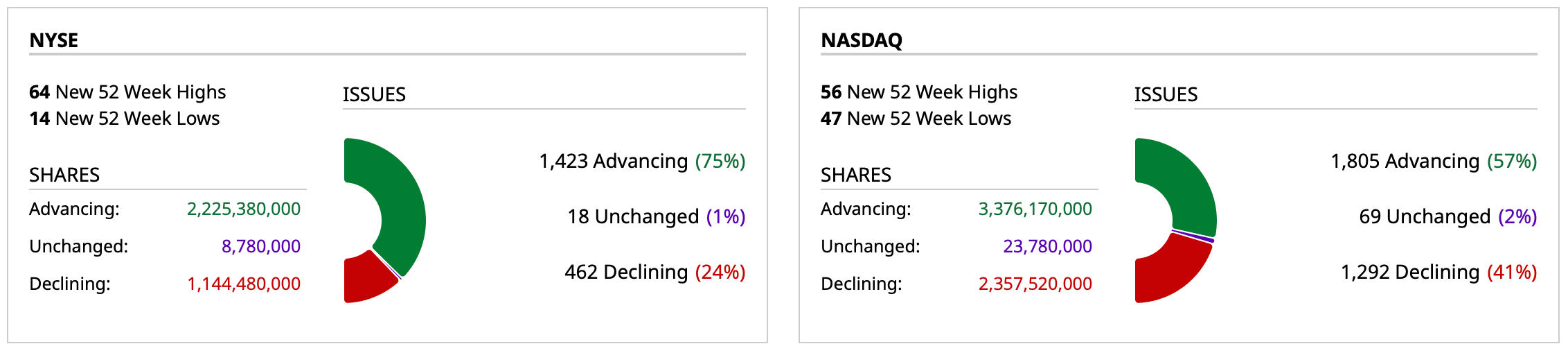

Closing Breadth

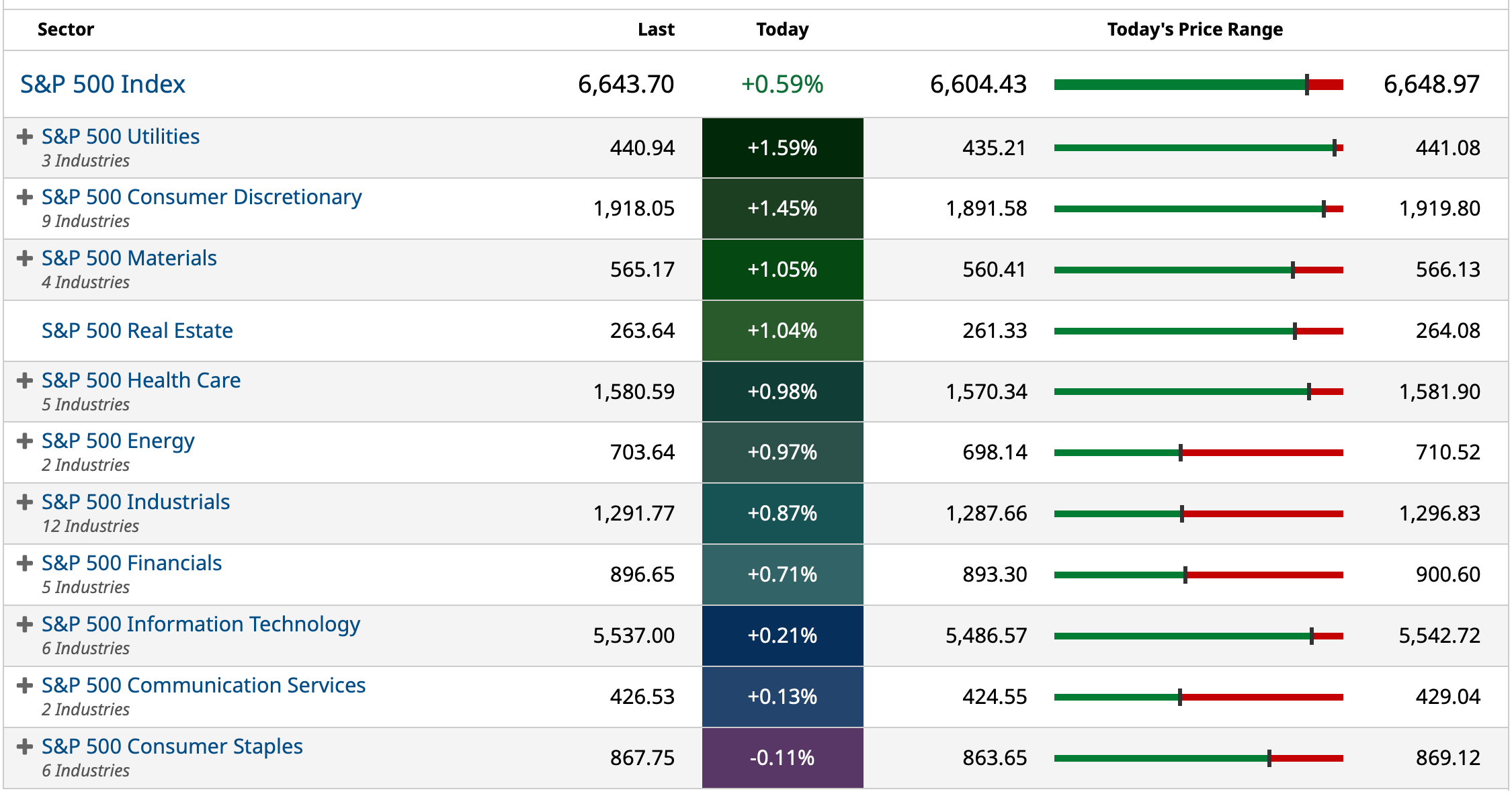

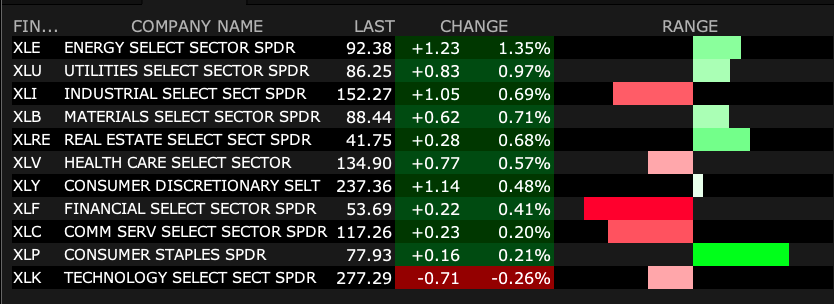

Sectors

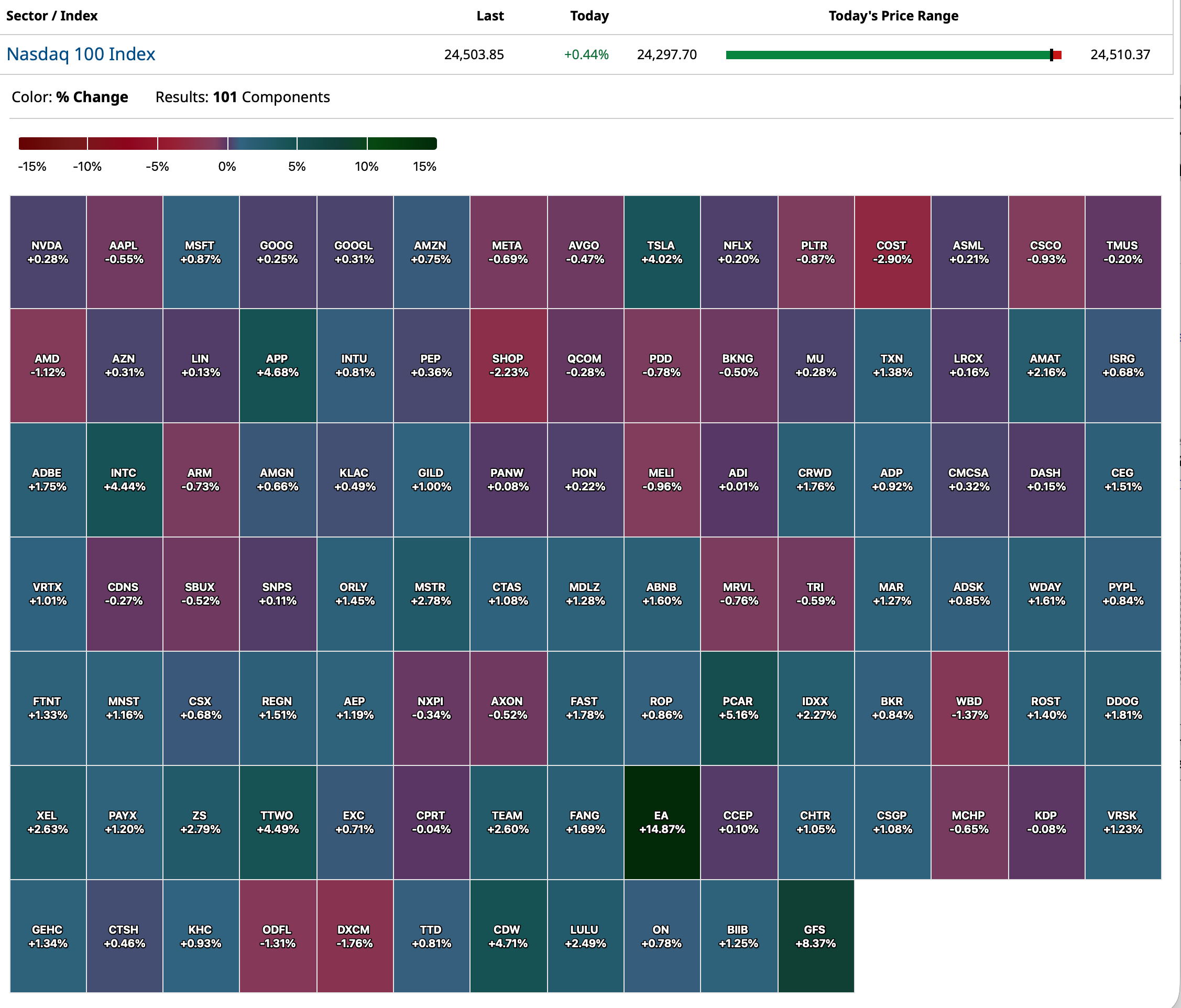

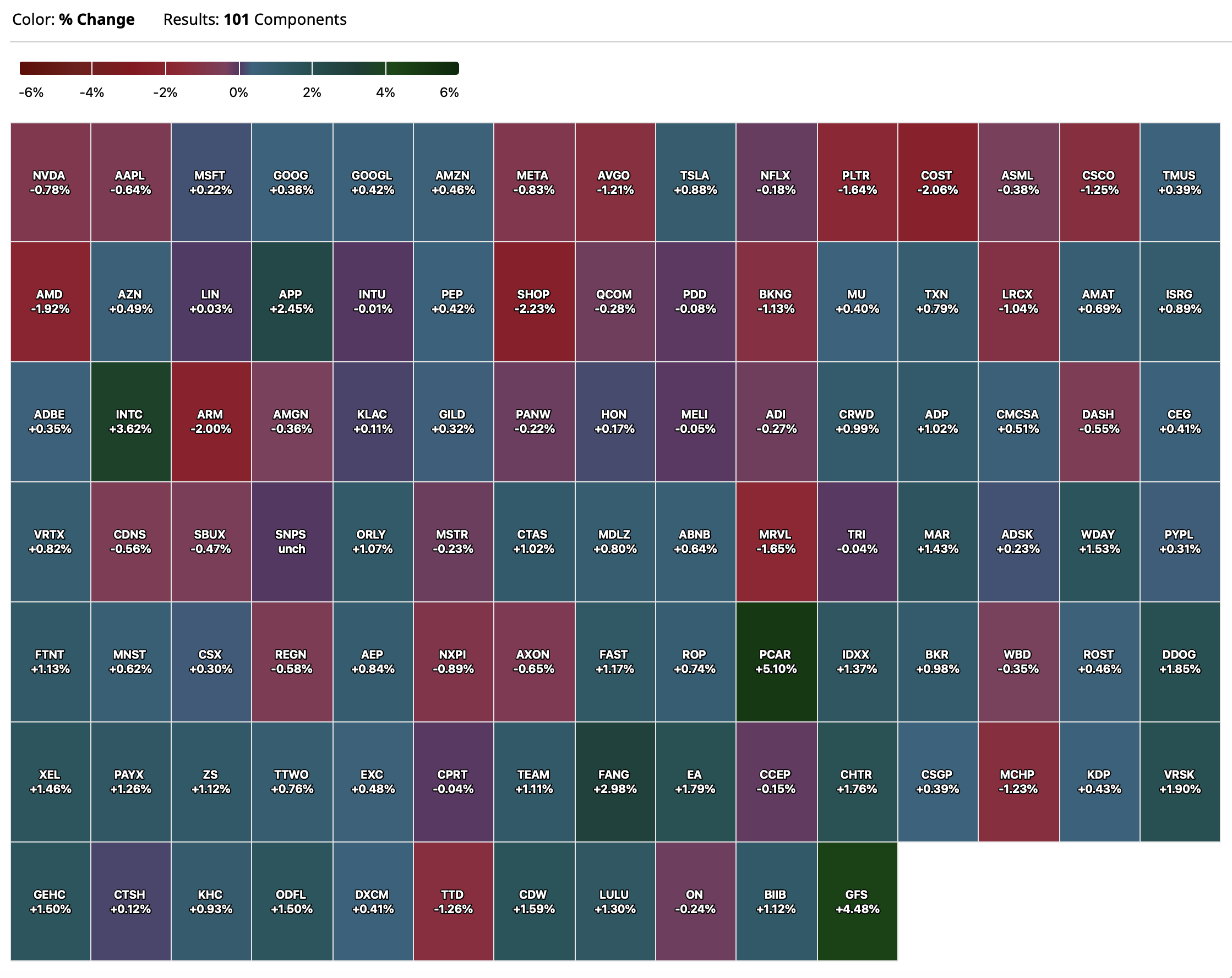

Nasdaq 100 Heat Map

BY Doug Kass · Sep 26, 2025, 4:22 PM EDT

Closing Breadth

Sectors

Nasdaq 100 Heat Map

BY Doug Kass · Sep 26, 2025, 4:22 PM EDT

I am leaving early for the weekend.

A sincere thanks for giving me this platform today, all week, all month, all year and since 1997!

Enjoy the weekend.

Be safe.

BY Doug Kass · Sep 26, 2025, 3:25 PM EDT

Hint: It's sticky!

"Inflation Is in Services despite Powell’s Denials: PCE Price Index for Core Services Accelerated Further. Durable Goods Prices Fell for 2nd Month," Wolf Richter of Wolf Street

BY Doug Kass · Sep 26, 2025, 2:45 PM EDT

I have a research call from 2 p.m. to 3 p.m. today.

Radio silence.

BY Doug Kass · Sep 26, 2025, 2:30 PM EDT

From Peter Boockvar:

Positives

1) Initial jobless claims fell to 218k from 232k and that was 15k below expectations. The 4 week average slipped to 238k from 240k. This smooths out the 264k print two weeks ago which for now ended up being an outlier. Continuing claims were little changed at 1.926mm, though a multi month low.

2) August core durable goods orders rose .6% m/o/m vs the estimate of no change but half was given back by the downward revision of .3% in July. Q3 GDP estimates could be trimmed though as core shipments fell by .3% instead of rising by .3% as forecasted.

3) The August goods trade deficit fell to $85.5b from $102.8b and that was $10b below expectations which could offset the durable good shipment driven trim to GDP.

4) There was big upside to the August new home sales figure where contract signings totaled 800k, well more than the estimate of 650k and compares with 664k in July. Accounting for 105k of the upside m/o/m were sales in the South and the overall sales increase drove months’ supply down to 7.4 from 9.0. Highly influenced by mix and really bounces around month to month, the median home price rose 4.7% sequentially and by 1.9% y/o/y. The 3 month average is now 713k vs the 6 month average of 689k and the 12 month average of 681k.

5) After a nearly 60% spike in refi applications last week, they were flattish this week, up by .8% as the average 30 yr mortgage rate fell by another 5 bps to 6.34%. Purchases were little changed too, up .3% w/o/w after a 2.9% rise in the week before.

6) Positive from a price perspective but not if it’s sending an economic message. The Shanghai to LA container route saw its price for a 40 foot box fall by 10% w/o/w to $2,311, the lowest since January 2024. The trip to NY saw a similar decline and at $3,278 is also at the cheapest rate since January 2024.

7) While very old news, Q2 GDP was revised up to 3.8% growth from the last read of 3.3%. Merging this with the Q1 decline of .5% puts first half GDP growth averaging 1.65% at an annualized pace. An increase in personal spending on services was the main reason for the upgrade along with a smaller than expected drag from the drop in inventories. The other line items were mostly left little changed.

8) From the Richmond Fed and Duke University CFO survey, “The outlook for the US economy among financial decision makers improved somewhat in the third quarter of 2025, as uncertainty declined. However, concerns about the impact of tariffs on prices and business performance continued to weigh on firms.”

9) The August US Architecture Billings Index ticked up 1 pt to 47.2, though remaining below 50 still. With lower rates and with hopes for more, there was a glass half full commentary from them. “While business conditions remained soft at architecture firms nationally, there are signs that the downturn may be bottoming out. Inquiries for new projects have increased four straight months, and billings both at firms with a multifamily or commercial/industrial specialization are beginning to stabilize.”

10) From Costco: Comps grew 6.4% “adjusted for gas deflation and FX” while E-commerce was higher by 13.5%. “Traffic or shopping frequency increased 3.7% worldwide.” Their average ticket was up 2.6% worldwide adjusting for gas and FX.

11) From Jabil: “So stepping back, FY ‘25 demonstrated two things at once. Some end markets were choppy...Where automotive and renewables slowed, AI driven demand more than offset.”

12) Tokyo reported September CPI and the core/core rate rose 2.5% y/o/y which was below the estimate of 2.8% but a lot of that had to do with the expansion of those children getting free daycare. Also, there were subsidies given to cover water bills.

13) The Eurozone PMI composite index rose to 51.2 from 51 though was mixed as manufacturing fell back below 50 at 49.5 from 50.7, offset by services which rose to 51.4 from 50.5. S&P Global said, “The outlook for manufacturing is looking a bit cloudy. Production is still growing, but the pace is being dragged down by France, where the government shake-up in early September likely threw a wrench into companies’ production plans. Apart from this, hopes for an acceleration in growth are not justified as new orders have dropped significantly in both Germany and France. In the medium term, higher defense spending could drive up demand for industrial goods.”

14) I think for anyone paying attention and interested in the geopolitical and commercial rivalry between the US and China must listen to alternative views and this is one of them:

Negatives

1) Remaining well above the Fed target, August headline PCE rose .3% while the core rate was higher by .2% m/o/m with both as expected. The y/o/y gains were 2.7% and 2.9% vs 2.6% and 2.9% in the month before respectively. Noteworthy in the inflation stats is the lift in goods prices which are now up .9% y/o/y which is modest but the most since September 2023. This while services inflation remains persistent, up by 3.6% y/o/y and has been between 3.5% and 3.6% for the past six months.

2) Personal income rose .4% m/o/m in August, one tenth above expectations and spending too exceeded the estimate by one tenth with its .6% increase. Combining the two puts the savings rate at 4.6% vs 4.8% in the month before and the lowest since December 2024.

3) The September US PMI composite index fell to 53.6 from 54.6 with both components lower m/o/m and after saying that “the monthly profile is one of growth having slowed from its recent peak back in July, and September saw companies also pull back on their hiring” they said “Softening demand conditions are also becoming more widely reported, curbing pricing power. Although tariffs were again cited as a driver of higher input costs across both manufacturing and services, the number of companies able to hike selling prices to pass these costs on to customers has fallen, hinting at squeezed margins but boding well for inflation to moderate.” This also was of note. We assume there was a lot of inventory stocking by importers ahead of tariffs and now “there are also signs that disappointing sales growth has caused inventories to accumulate at an unprecedented rate, which could also further help soften inflation in the coming months. The inventory build-up of course also hints at some downside risks to future production.”

3) More tariffs to come on furniture, trucks, and pharma.

4) From the Q3 Richmond Fed and Duke University CFO survey, “Overall, CFOs projected that tariffs would have a big impact on price growth: On average, price growth would be about 30% lower in 2025 and roughly 25% lower in 2026 without the addition of tariffs, indicating that firms expect to grapple with tariff-related price increases into 2026. Meanwhile, almost a quarter of firms continued to report that they will decrease capital spending in 2025 due to tariffs.”

5) The entire AI tech trade/Infrastructure buildout is in big trouble ahead if Bain is right in their prediction this week. “Two trillion dollars in annual revenue is what’s needed to fund computing power needed to meet anticipated AI demand by 2030. However, even with AI related savings, the world is still $800 billion short to keep pace with demand” they said. For the sake of a lot in markets and the economy, let’s hope GQG is wrong too, https://gqg.com/insights/dotcom-on-steroids/ .

6) Existing home sales in August at 4mm annualized continues to hover around 30 year lows. Prices rose 2% y/o/y which is a needed deceleration as first time buyers made up just 28% of purchases.

7) The September Philly services index remained under zero at -12.3 vs -17.5 in August.

8) The UoM final September consumer confidence index was 55.1 vs 58.2 in August and that is the lowest since May. “Although September’s decline was relatively modest, it was still seen across a broad swath of the population, across groups by age, income, and education, and all five index components. A key exception: sentiment for consumers with larger stock holdings held steady in September, while for those with smaller or no holdings, sentiment decreased.” Also, “Tariffs remain highly salient to consumers and influence their economic expectations; about 60% of consumers provided unprompted comments about tariffs, compared with 65% in May 2025 and 28% in January 2025. With trade policy remaining unsettled, inflation uncertainty is far higher than a year ago, despite plummeting since the spring far more rapidly compared with previous spikes.”

9) From CarMax: “while hard to quantify, we believe there was a pull forward of demand into the first quarter. In the second quarter, we responded by lowering retail margin to drive sell-through, and we intentionally slowed buys to balance our inventory with sales.” Also, they had a $71 million rise in their loan loss provision from their 2022 and 2023 vintages. “Recall, these customers have been the most impacted by the convergence of rapidly increasing vehicle prices and broader inflation. Despite the observed worsening, these vintages still remain highly profitable at an estimated lifetime profit of $1,500 per unit versus $1,800 contemplated at origination.” Their 2024 and 2025 “post contraction vintages continue to be right in line with our original loss expectations.”

10) From Costco: “Turning to inflation. Overall inflation remained in the low to mid-single digit range. Fresh and food and sundries were relatively similar to last quarter...In non-foods, we saw inflation return for the second consecutive quarter, primarily driven by imported items. This inflation drove the $43 million LIFO charge for the quarter.”

11) From AutoZone: “We continue to expect ticket inflation to be up at least 3% for the remainder of the calendar year. We also saw DIY traffic count down 1.9%, which was relatively consistent across the quarter...We continue to see data that confirms we are gaining share.” More on that 3%, it “probably goes up from here. I mean, at the end of the day, we’ve talked for years about this industry being pretty disciplined and rational in pricing, and we’re going to use the pricing lever as we need to, to cover the cost of goods and make sure we stay competitive in the marketplace.” On the consumer with their discretionary spend, “So I’d say it’s probably bottomed out and slowly started to gain some traction. Maybe there’s a little bit of green shoots, but I would say it’s a little early to say. And I still think that the lower end consumer is still under quite a bit of pressure, and this is mostly on the DIY sales floor side of the business.”

12) From Thor Industries: “While there is significant internal excitement around the company specific initiatives that have the potential to drive business results beyond what the broader market would normally support, we are cognizant of the inherent uncertainty surrounding the timing of these dynamics playing out. Additionally, with multiple data points suggesting weakness emerging in the job market, we think it is prudent to plan for another challenging year.”

13) From KB Homes: “While we experienced consistent traffic at our communities, net orders totaled 2,950, a 4% decline.” Also, “Orders have been good, but I wouldn’t say that we’ve seen a big uptick yet or maybe the uptick that we would expect to see from such a change in mortgage rates. And I think to some extent buyers are in maybe a bit of a wait-and-see mode, maybe waiting for rates to come down further, maybe they were waiting around for the actual Fed event expecting that to have some immediate impact on rates.”

14) Japan’s September PMI composite index fell to 51.1 from 52 with manufacturing softening to 48.4 from 49.7 while services were little changed at 53. With manufacturing specifically, S&P Global said the weakness “was linked by some firms to cautious inventory policies among clients amid challenging market conditions.” Also of note, “Cost pressures remain a key concern, and while the rate of input cost inflation has eased since the start of the year, the respective index remains consistent with a sharp rate of inflation overall. This translated into a further solid increase in selling prices as firms looked to ease pressure on their margins.”

15) Australia’s composite index weakened to 52.1 from 55.5 with both components lower. India’s slipped to a still strong 61.9 from 63.2.

16) In Germany, the September IFO business confidence index slipped to 87.7 from 88.9 and that was under the estimate of 89.4 with m/o/m declines in both the Current Assessment and Expectation components. IFO said succinctly, “Prospects for an economic recovery have suffered a setback.” Both manufacturing and services weakened with the latter having “deteriorated noticeably” said IFO. They said with services the weakness was particularly in “the transport and logistics sector” which of course is tied to manufacturing. Trade was down but construction improved.

17) The UK PMI fell to 51 from 53.5 with manufacturing at just 46.2 vs 47 while services dropping to 51 from 53.5. Also, with regards to the outlook for the coming 12 months, “The degree of confidence slipped to its lowest since June, reflecting falling optimism across the service economy. Service providers noted challenging economic conditions, squeezed budgets among clients and heightened business uncertainty. However, manufacturers were the most upbeat since February.”

18) The Swedish Riksbank cut its benchmark rate by 25 bps unexpectedly to 1.75% but said that’s it “for some time to come.” For reference, their August CPI ex fuel was up 2.9%. Rolling the dice with inflation.

BY Doug Kass · Sep 26, 2025, 2:12 PM EDT

* (SPY) $661.38

* (QQQ) $495.29

BY Doug Kass · Sep 26, 2025, 1:59 PM EDT

BY Doug Kass · Sep 26, 2025, 1:08 PM EDT

More Index shorts:

* (SPY) $660.69

* (QQQ) $594.63

BY Doug Kass · Sep 26, 2025, 12:50 PM EDT

Here are today's things:

* I reinitiated index shorts:

(SPY) $660.84

(QQQ) $595.45

* Added to (PEP) $140.01

* Added to (KVUE) $16.30

BY Doug Kass · Sep 26, 2025, 12:36 PM EDT

BY Doug Kass · Sep 26, 2025, 12:10 PM EDT

Wall Street Journal on the AI bubble building spree.

BY Doug Kass · Sep 26, 2025, 11:24 AM EDT

BY Doug Kass · Sep 26, 2025, 11:08 AM EDT

From Peter Boockvar:

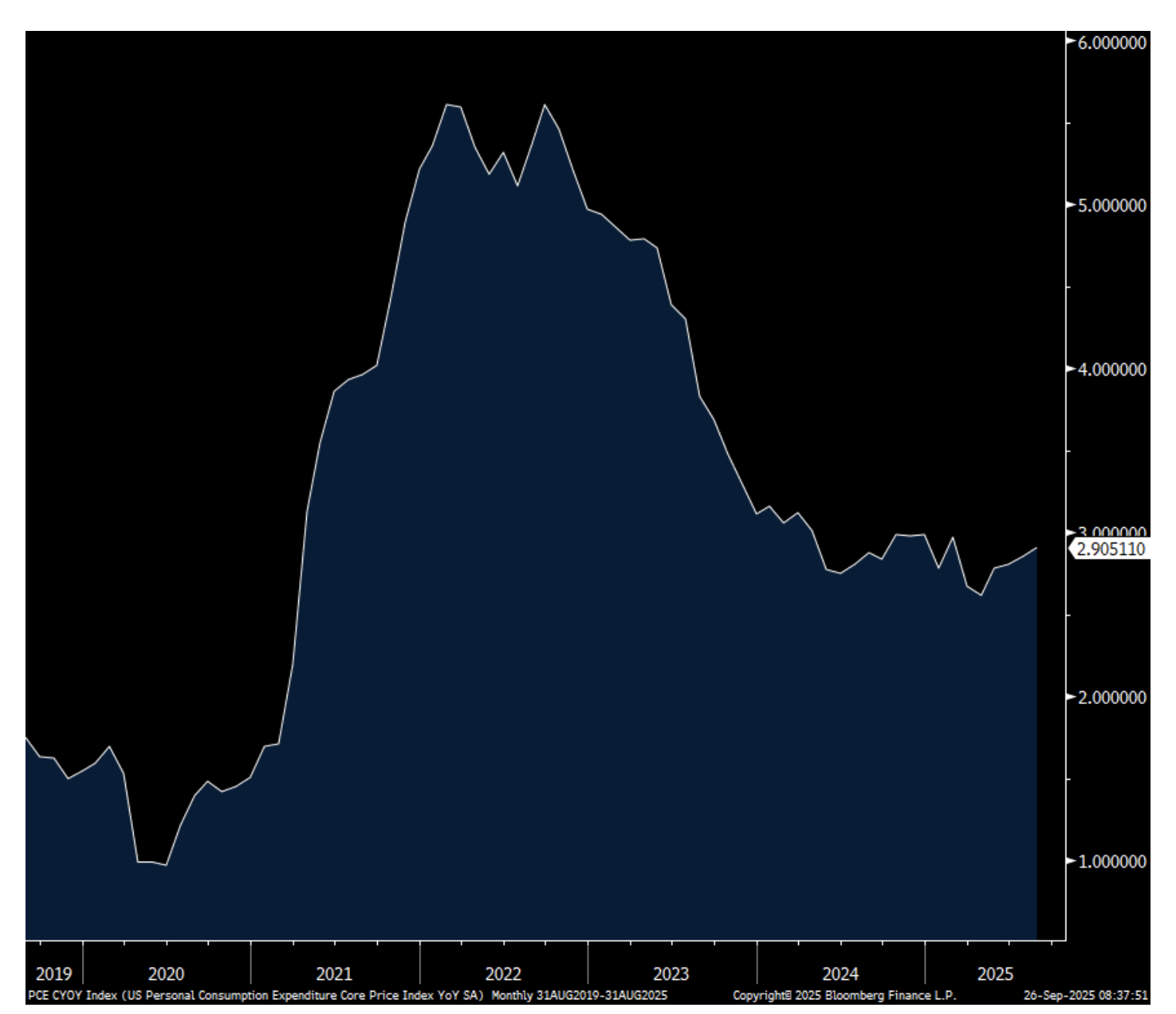

August headline PCE rose .3% while the core rate was higher by .2% m/o/m with both as expected as this data point usually is with most of the inputs already in hand. The y/o/y gains were 2.7% and 2.9% vs 2.6% and 2.9% in the month before respectively. As seen in the chart below, core PCE remains stuck around 3%.

Noteworthy in the inflation stats is the lift in goods prices, which are now up .9% y/o/y. It doesn’t sound like much but it’s the most since September 2023 with the disinflationary period over for now led by higher durable goods prices because of the tariffs. This while services inflation remains persistent, up by 3.6% y/o/y and has been between 3.5% and 3.6% for the past six months. Again, yes, tariffs are a tax and thus are theoretically one time in nature but if it is so disruptive to global supply chains, that will be a multi year process of adjustment which I believe will be the case.

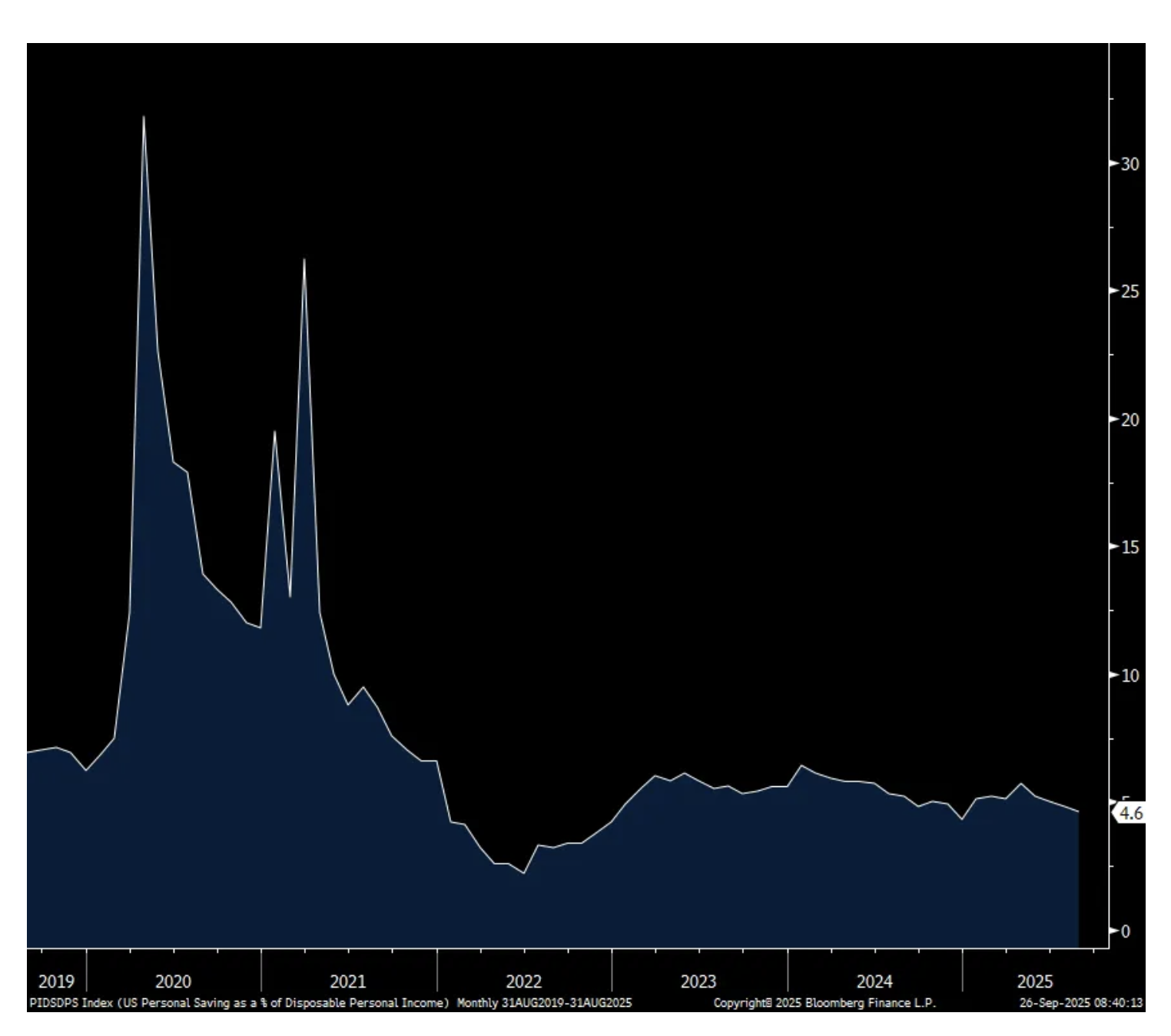

Personal income rose .4% m/o/m, one tenth above expectations and spending too exceeded the estimate by one tenth with its .6% increase. Combining the two puts the savings rate at 4.6% vs 4.8% in the month before and the lowest since December 2024.

Looking specifically at private sector wages/salaries, they rose .3% m/o/m. Spending saw a .8% m/o/m gain in goods and a .5% lift on services. These are all nominal figures.

Bottom line, no surprises in the data and why Treasury yields are about exactly where they were at 8:29am. And core PCE still hanging around the 3% level for now again confirms to me that as long as Jay Powell is Fed Chair, we’re only going to see a rate tweaking cycle rather than a rate cutting cycle. Obviously all is thrown out the window after May 2026 if Stephan Miran’s views are what is followed and whose views expressed this week are some I don’t agree with in terms of his views of where the REAL rate should be. It of course doesn’t matter what I think though because luckily we have the long end of the yield curve to speak out and who has a much bigger voice.

Core PCE y/o/y

Savings Rate

BY Doug Kass · Sep 26, 2025, 10:35 AM EDT

Randy

44 minutes ago

Kenvue (KVUE) upgraded by Rothschild & Co Redburn from Neutral to Buy.

BY Doug Kass · Sep 26, 2025, 10:30 AM EDT

Added to index shorts on the ramp - now small sized from very small sized:

* (SPY) $661.35

* (QQQ) $595.45

BY Doug Kass · Sep 26, 2025, 9:54 AM EDT

From Peter Boockvar:

That new furniture you’ve been looking to buy is about to become more expensive after another slew of tariffs are coming. Transportation of manufactured goods will be as well as the cost of building the actual trucks that drive this stuff around are going up too. Pharma tariffs? Do what Ireland did instead, lower the corporate income tax rate further in the US in order to make us more competitive. Paccar is trading up pre-market while Williams Sonoma and RH are down in response.

Meanwhile, US trade with China continues to shrink if shipping rates are any indication. The Shanghai to LA container route saw its price for a 40 foot box fall by 10% w/o/w to $2,311, the lowest since January 2024. The trip to NY saw a similar decline and at $3,278 is also at the cheapest rate since January 2024.

WCI Shanghai to LA

Here is what CarMax said yesterday in its earnings call where the stock fell 20%:

“During the quarter, we delivered total sales of $6.6 billion, down 6% compared to last year, reflecting lower volume.”

“while hard to quantify, we believe there was a pull forward of demand into the first quarter. In the second quarter, we responded by lowering retail margin to drive sell-through, and we intentionally slowed buys to balance our inventory with sales.”

As I mentioned yesterday from their release they had a $71 million rise in their loan loss provision from their 2022 and 2023 vintages. “Recall, these customers have been the most impacted by the convergence of rapidly increasing vehicle prices and broader inflation. Despite the observed worsening, these vintages still remain highly profitable at an estimated lifetime profit of $1,500 per unit versus $1,800 contemplated at origination.” Their 2024 and 2025 “post contraction vintages continue to be right in line with our original loss expectations.”

They did try to help those people that bought cars in 2022 and 2023 as “we watched that customer begin to struggle and continue to struggle a little bit. We made some adjustments that we thought were very smart for the consumer and smart for us, that has proven to be the case, and that was we adjusted our extension policy in the fall. We saw more payments come in had we otherwise not done that.”

From the retail behemoth Costco where I just bought a tv from:

Comps grew 6.4% “adjusted for gas deflation and FX” while E-commerce was higher by 13.5%. “Traffic or shopping frequency increased 3.7% worldwide.” Their average ticket was up 2.6% worldwide adjusting for gas and FX.

With regards to merchandising, “Fresh sales were up high single digits, led by double digit growth in meat...Wagyu and grass fed beef performed well in the quarter, and lower cost proteins like poultry, pork, and ground beef also saw very strong unit growth.”

“In the quarter, gold and jewelry, gift cards, majors (like consume electronics), toys and men’s apparel were all up double digits. While gold was less of a y/o/y tailwind than earlier in the year, as we have now started to lap sales from a year ago, it continues to perform well.”

“Turning to inflation. Overall inflation remained in the low to mid-single digit range. Fresh and food and sundries were relatively similar to last quarter...In non-foods, we saw inflation return for the second consecutive quarter, primarily driven by imported items. This inflation drove the $43 million LIFO charge for the quarter.”

“We continue to work closely with our suppliers to find ways to mitigate the impact of tariffs, including moving the country of production where it makes sense, and consolidating our buying efforts globally to lower the cost of goods across our markets. Additionally, we are changing item assortment where appropriate.” On using the price lever, “And last effect would be we pass on price. And, if we do that, we’re going to be the last one to go up and always the first one to go down on any opportunities we have out there.”

From Jabil, a major contract manufacturing heavy in tech, healthcare, industrial and aerospace and whose stock fell 7% yesterday:

“Health care was in line, while renewable and energy infrastructure and automotive and transportation both exceeded expectations, supported by incentive related demand pull forward and stronger volumes across core programs.”

Their Intelligent Infrastructure business saw gains that “was driven primarily by three factors within cloud and data center.” But this area I think is why the stock fell as margins were light and guidance was as expected.

They saw “softness in consumer driven products. This was partially offset by continued growth in warehouse and retail automation (which includes robotics).”

“So stepping back, FY ‘25 demonstrated two things at once. Some end markets were choppy...Where automotive and renewables slowed, AI driven demand more than offset.”

To the overseas news of note, Tokyo reported September CPI and the core/core rate rose 2.5% y/o/y which was below the estimate of 2.8% but a lot of that had to do with the expansion of those children getting free daycare. Also, there were subsidies given to cover water bills. So yes, the BoJ still thinks underlying inflation is too low while the government keeps handing out money to ease the inflationary pressures on its populace.

Inflation breakevens were unchanged in response and little movement too in the 10 yr JGB yield but 30s and 40s were up about 4 bps. The yen is flattish just under 150 vs the US dollar while the Nikkei fell .9%. We remain positive and long Japanese stocks.

BY Doug Kass · Sep 26, 2025, 9:45 AM EDT

BY Doug Kass · Sep 26, 2025, 9:25 AM EDT

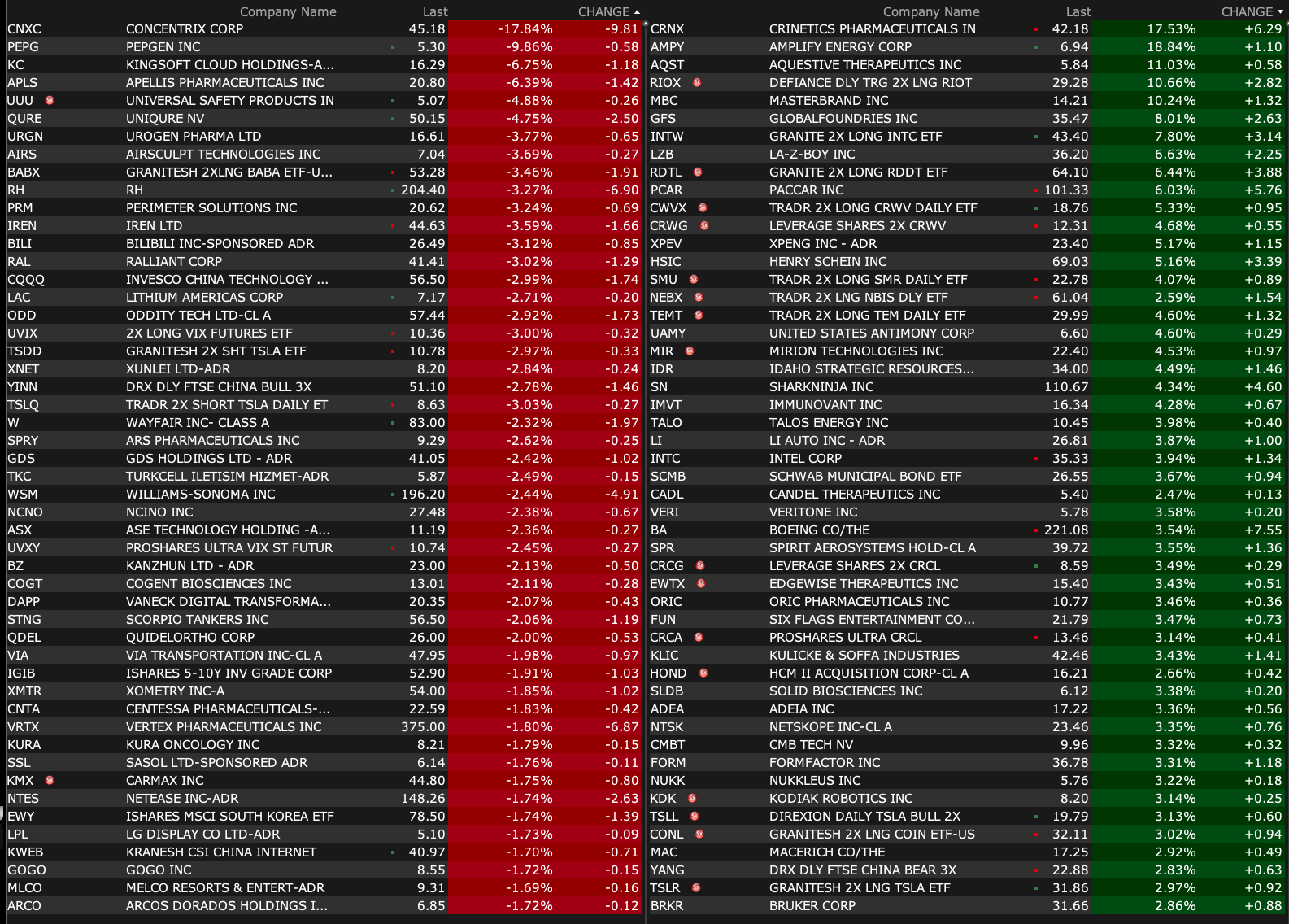

-GUTS +18% (Data from REMAIN-1 Midpoint Cohort Shows Revita Maintained Weight Loss After GLP-1 Discontinuation)

-CRNX +13% (US FDA Approves PALSONIFY (paltusotine) for Treatment of Adults with Acromegaly)

-ONCO +12% (announces Financing Through a $12.9M Private Placement of Series D Preferred Stock and Warrants, Termination of Merger Agreement with Ocuvex, Inc. and Settlement of $8.8M Debt with Veru, Inc.)

-DGNX +11% (provides update on acquisition strategy)

-PCAR +6.3% (US Pres Trump: 25% tariff on all big trucks (>10K lbs), effective Oct 1st)

-GFS +6.2% (Trump Admin reportedly considering new plan to dramatically reduce US reliance on overseas produced semiconductors)

-SPRU +5.9% (Wins Competitive Spruce PRO Backup Servicing Agreement Expanding to Puerto Rico, Cementing Status as the Go-To End-to-End Solar Portfolio Servicer)

-INTC +4.6% (reportedly approached TSM regarding manufacturing investments or partnerships)

-LPTH +4.1% (earnings)

-RAPT +3.7% (Leerink Partners Raised RAPT to Outperform from Market Perform, price target: $37)

-MIR +3.6% (prices upside $356M offering of 17.3M A shares at $21.35/shr (prior $350M))

-KNOP +3.5% (earnings, color)

-BA +3.1% (FAA said to lift cap on 737 Max production from 38 to 42 per month; Decision may come as soon as today)

-SPR +3.0% (higher in sympathy with Boeing)

-CNXC -19% (earnings, guidance)

-DRIO -15% (profit taking off recent run up)

-LGCY -13% (earnings, guidance)

-APLS -6.0% (hearing Goldman Sachs Cuts APLS to Sell from Neutral, price target: $18)

-QURE -5.0% (prices upsized ~5.8M shares at $47.50/shr for gross proceeds $300M)

-CLSK -4.4% (JPMorgan Chase and Co Cuts CLSK to Neutral from Overweight, price target: $14)

-RH -3.8% (Trump Admin imposing 50% tariff on all kitchen cabinets, bathroom vanities and associated products)

-W -3.0% (Trump Admin imposing 50% tariff on all kitchen cabinets, bathroom vanities and associated products)

-WSM -2.6% (Trump Admin imposing 50% tariff on all kitchen cabinets, bathroom vanities and associated products)

-DELL -2.3% (Trump Admin could require US tech firms to match chip imports 1:1 with domestic production or face tariffs)

BY Doug Kass · Sep 26, 2025, 9:15 AM EDT

BY Doug Kass · Sep 26, 2025, 9:05 AM EDT

(After an in line inflation release...)

As promised (see below) I am back shorting the indexes after the rise off of yesterday's lows (Thursday afternoon and this morning, in premarket trading):

* (SPY) $660.91

* (QQQ) $596.35

From yesterday:

I have covered the balance of my Index shorts:

* (SPY) $655.75

* (QQQ) $589.17

I plan to reshort strength.

Position: none.

By Doug KassSep 25, 2025 9:57 AM EDT

BY Doug Kass · Sep 26, 2025, 8:49 AM EDT

Fed Speakers Today:

9 a.m.: Federal Reserve Bank of Richmond President Thomas Barkin (Non-Voter) speaks before the Peterson Institute for International Economicsm, Washington, DC (No prepared remarks. No group media interview. Livestream here.);

10 a.m.: Fed Governor Bowman (Voter) participates in "Approach to Monetary Policy Decision-Making" conversation hosted by the Forecasters' Club of New York, The Cornell Club, NYC (Text available. Q&A from moderator and audience. No webcast)

BY Doug Kass · Sep 26, 2025, 8:45 AM EDT

BY Doug Kass · Sep 26, 2025, 8:30 AM EDT

BY Doug Kass · Sep 26, 2025, 7:20 AM EDT

BY Doug Kass · Sep 26, 2025, 7:10 AM EDT

BY Doug Kass · Sep 26, 2025, 7:00 AM EDT

* From those wonderful folks that top ticked cryptocurrencies...

* Fin TV (CNBC's Scott Wapner "They look pretty good" - yesterday) and now technicians are all over Chinese stocks, after an enormous run — caveat emptor!

Bonus — Here are some great links:

BY Doug Kass · Sep 26, 2025, 6:45 AM EDT

* Sound familiar?

I have long been concerned about the hyperscalers morphing from capital light to capital intensive:

From early August:

More Tales From Nvidia: The New Capital-Intensive Commodity Businesses

BY Doug Kass · Sep 26, 2025, 6:35 AM EDT

BY Doug Kass · Sep 26, 2025, 6:25 AM EDT

and...

And another repost from late August on my view of homebuilding equities:

BY Doug Kass · Sep 26, 2025, 6:15 AM EDT

For the reasons mentioned in my series, "More Tales From Nvidia," I continue to be of the view that the announcement of the Nvidia/Oracle contract likely marked the near term peak in the AI trade.

A repost from Sept. 9:

Yesterday I opined that the Oracle (ORCL) "backlog blowout" might mark a possible peak in the AI trade.

Most importantly, one must be aware that all of the quickly depreciated spending on IT infrastructure must generate sufficient revenue and profits to recover the costs.

Remember that Oracle's future revenues are someone else's future capital spending. (According to the conference call three individual companies contributed to much of the company's dramatic rise in backlog.)

We have contended that many of the global AI players collectively are spending much more than they might earn on those expenditures in the face of numerous uncertainties:

Here's my contrary view.

The Oracle (ORCL) backlog blowout (with Oracle future revenues ultimately still dependent on the availability of chips, companies' access to large sums of debt/capital, the need for a very large increase in power capacity, the forecasts assume no recession or price compression) "could" mark the end of the AI trade.

As well, it should be recognized that the ramp in future revenue projections by Oracle will produce dramatically lower profit margins relative to the company's currently robust margins.

Moreover, those projected ORCL sales will be taken out of the pocket of some other large tech competition.

In the after hours on the shows, the exact opposite view was expressed.

(Edited at 7:33 ET)

Position: None

By Doug Kass Sep 9, 2025 7:33 PM EDT

Today someone else agrees:

Here Is The Batshit Insane Chart That Sent Oracle Stock Soaring 25% After Hours | ZeroHedge

Position: None

By Doug Kass Sep 10, 2025 6:20 AM EDT

BY Doug Kass · Sep 26, 2025, 6:05 AM EDT

Wolf Street on the housing crush.

BY Doug Kass · Sep 26, 2025, 5:55 AM EDT

The S&P Short Range Oscillator has moved into oversold for the first time in quite a while (-1.97% vs. 0.82%).

BY Doug Kass · Sep 26, 2025, 5:45 AM EDT