Thursday's Closing Market Stats

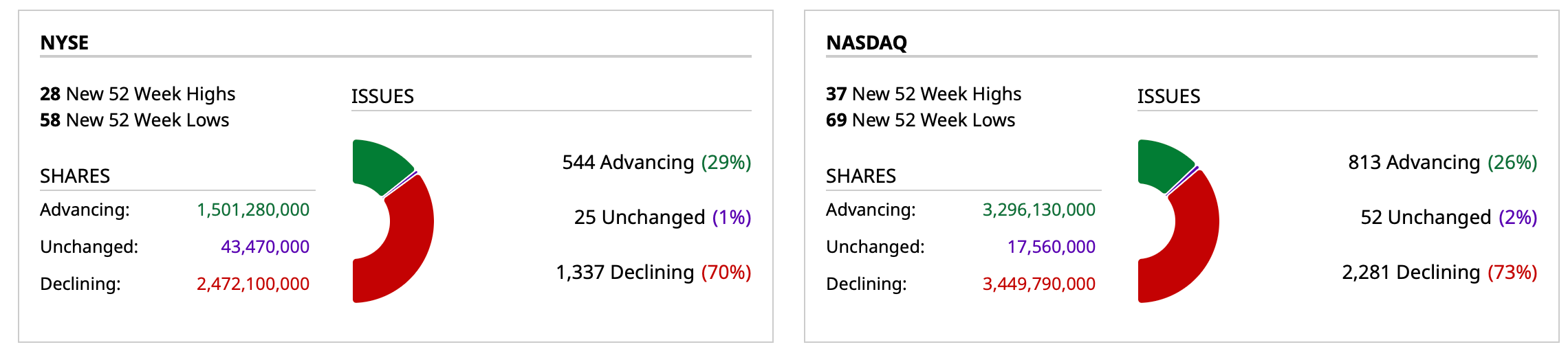

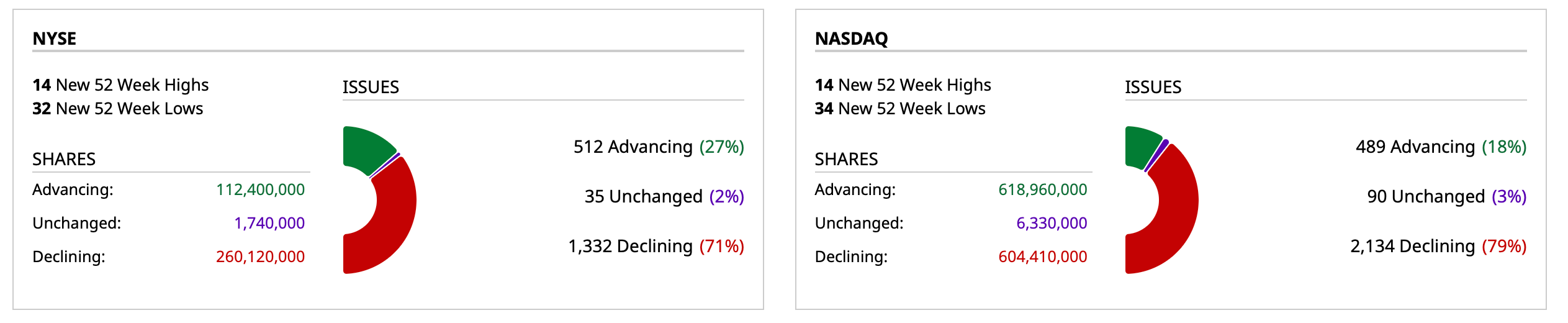

Closing Breadth

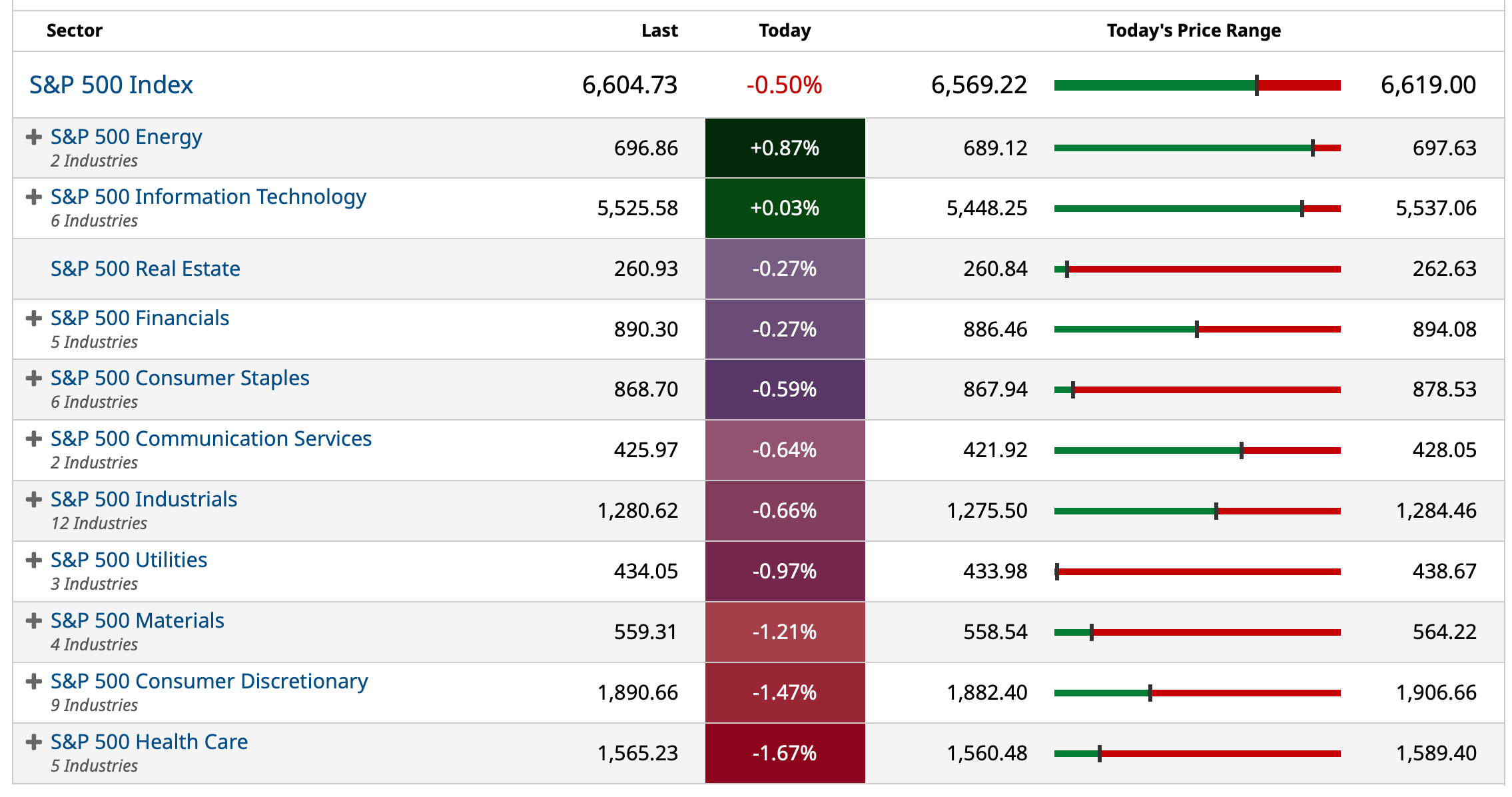

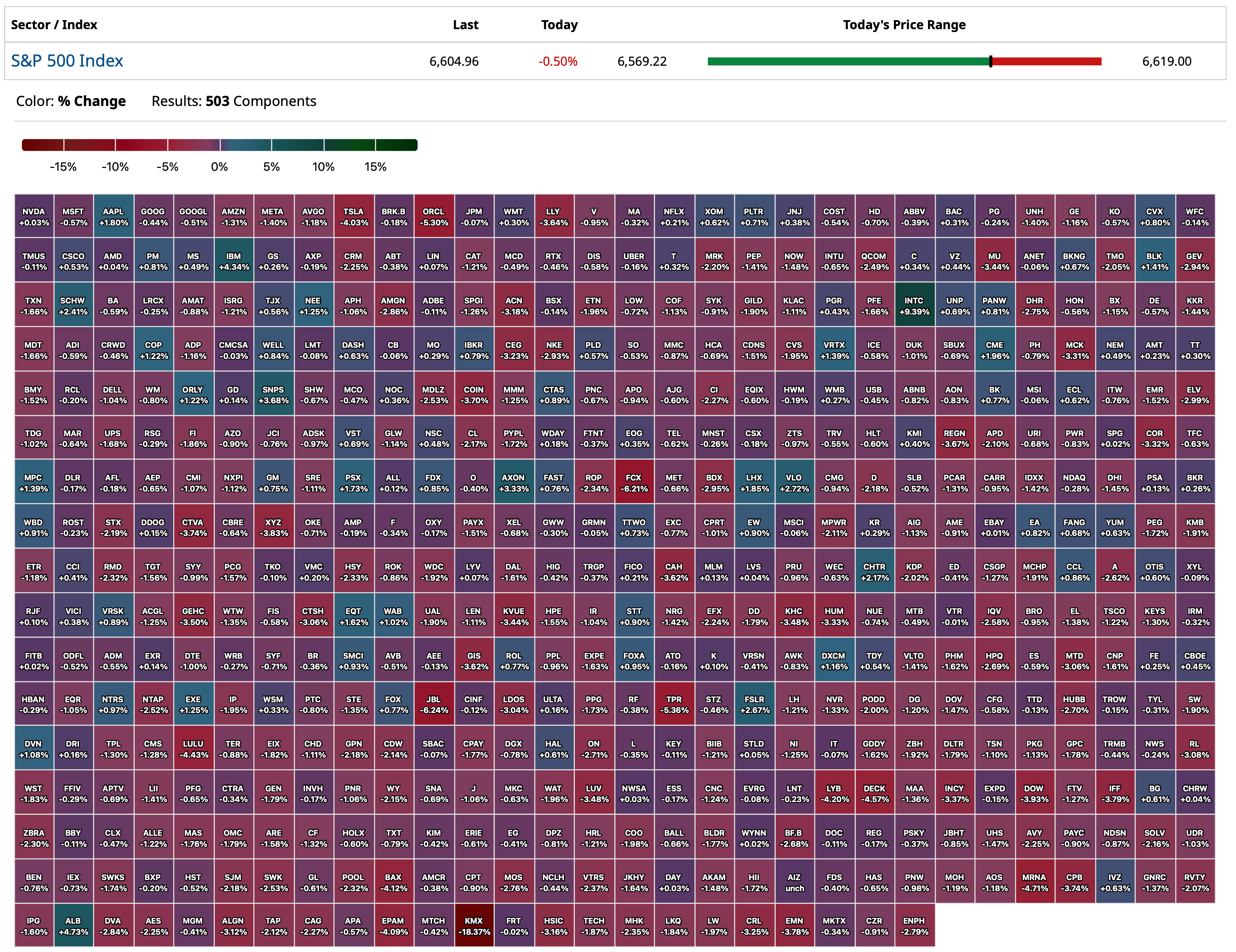

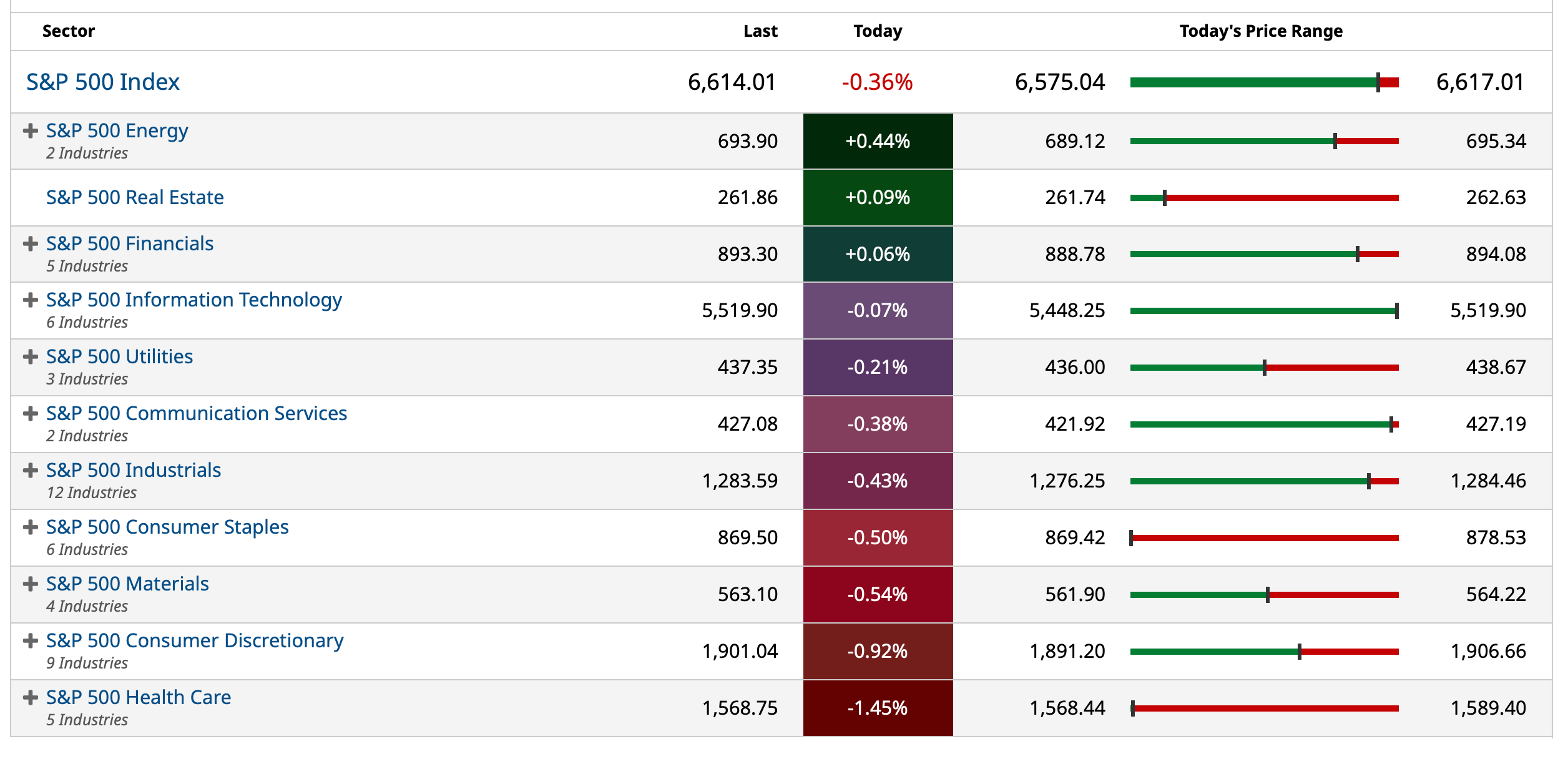

Sectors

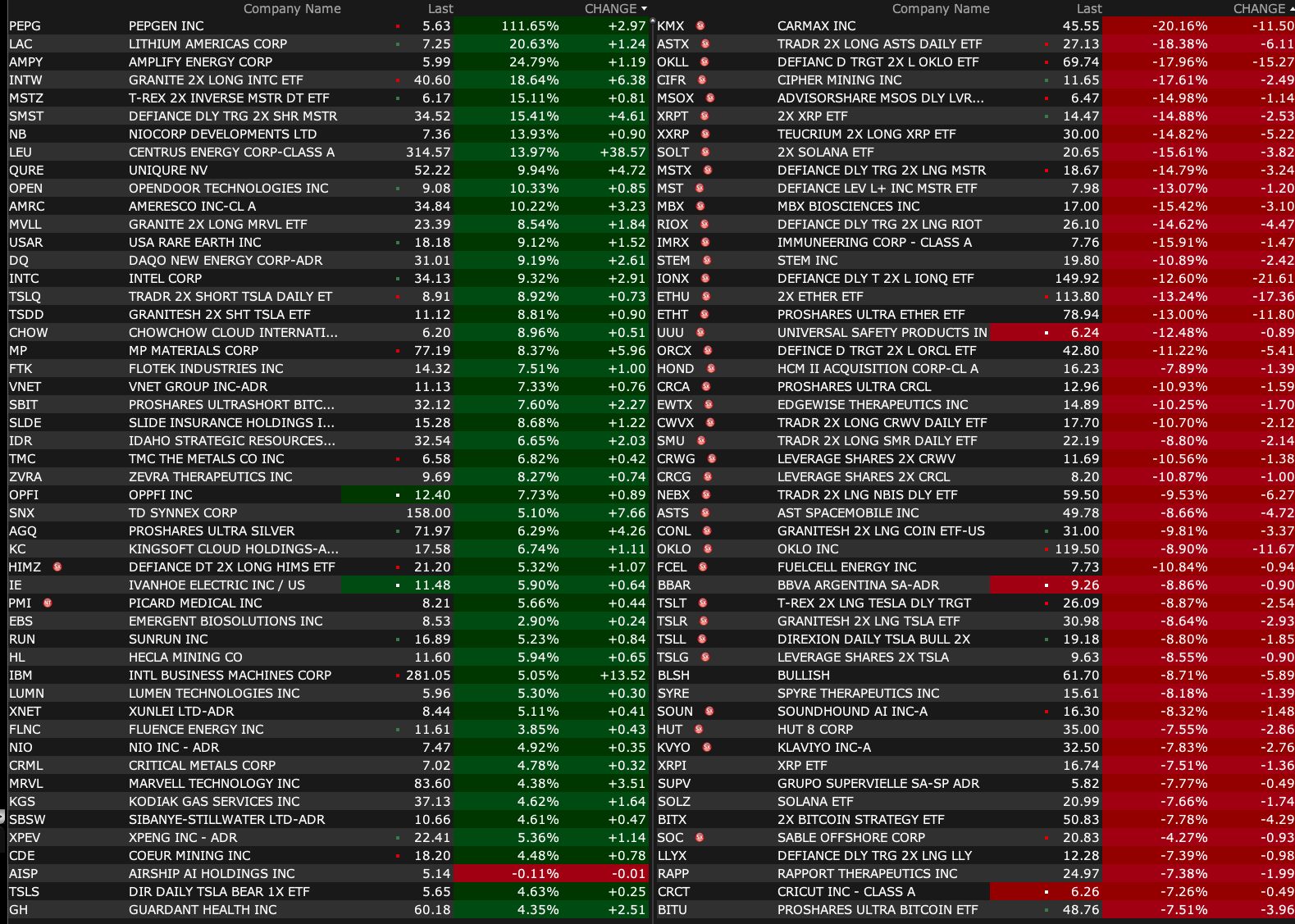

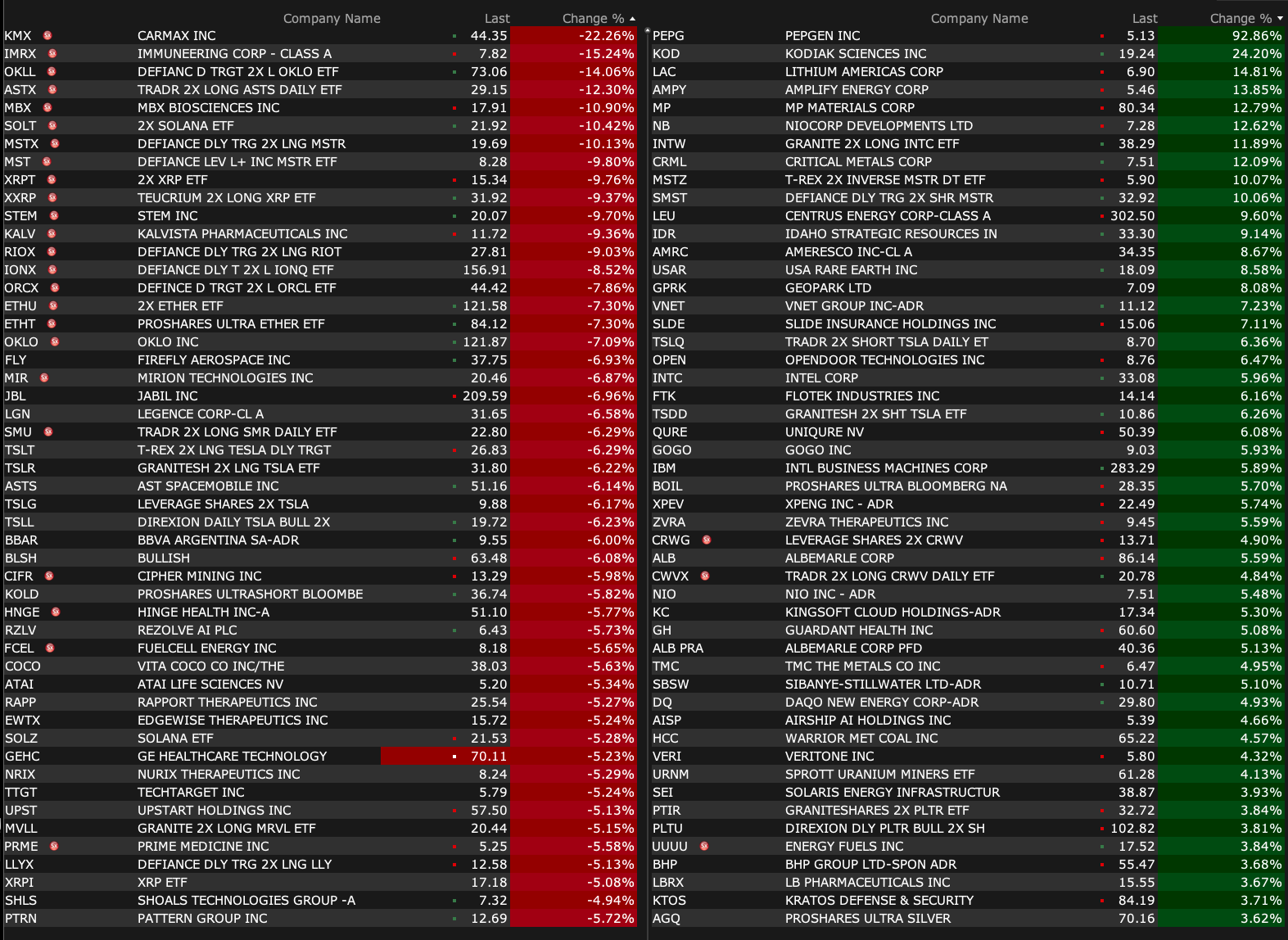

% Movers

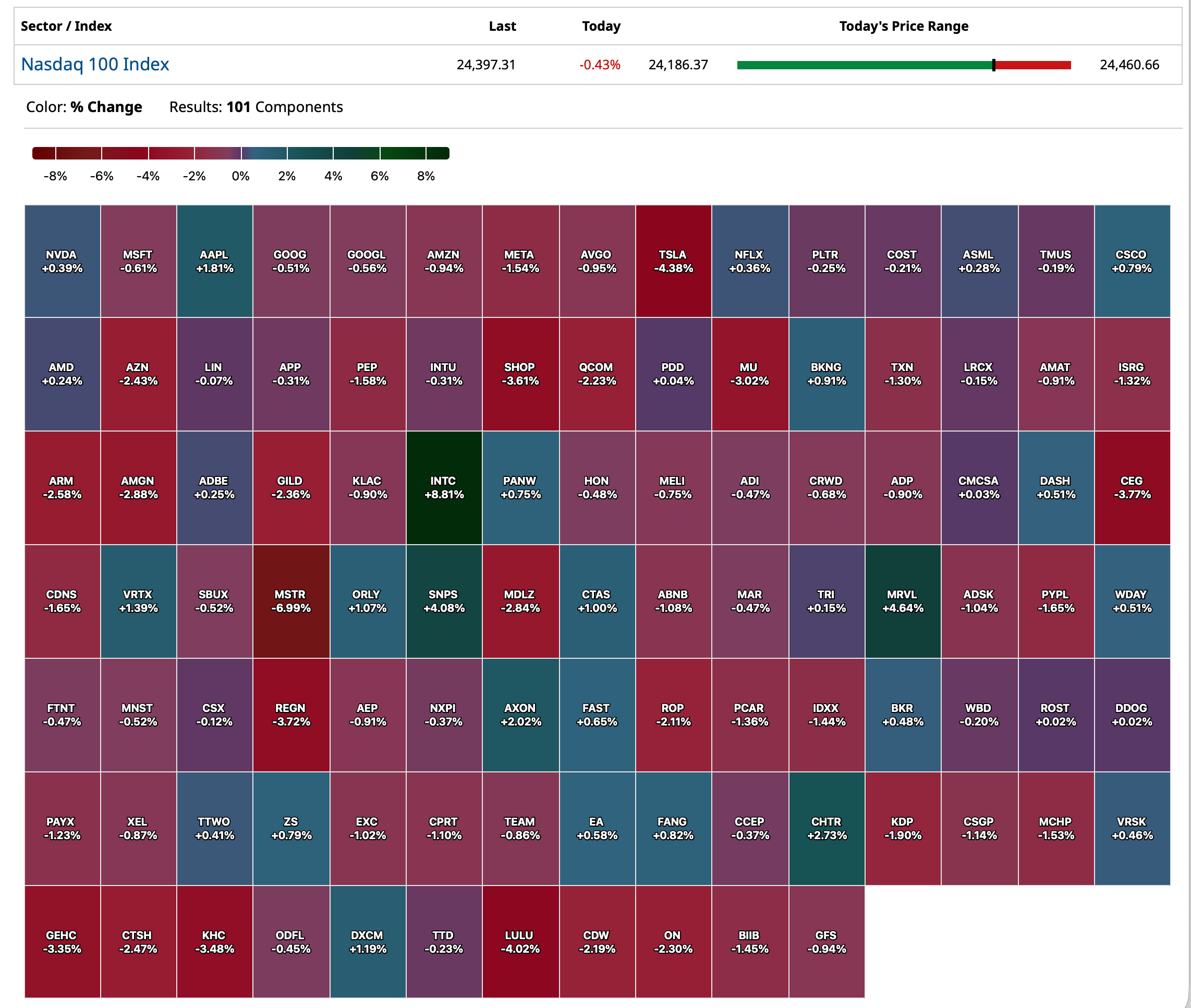

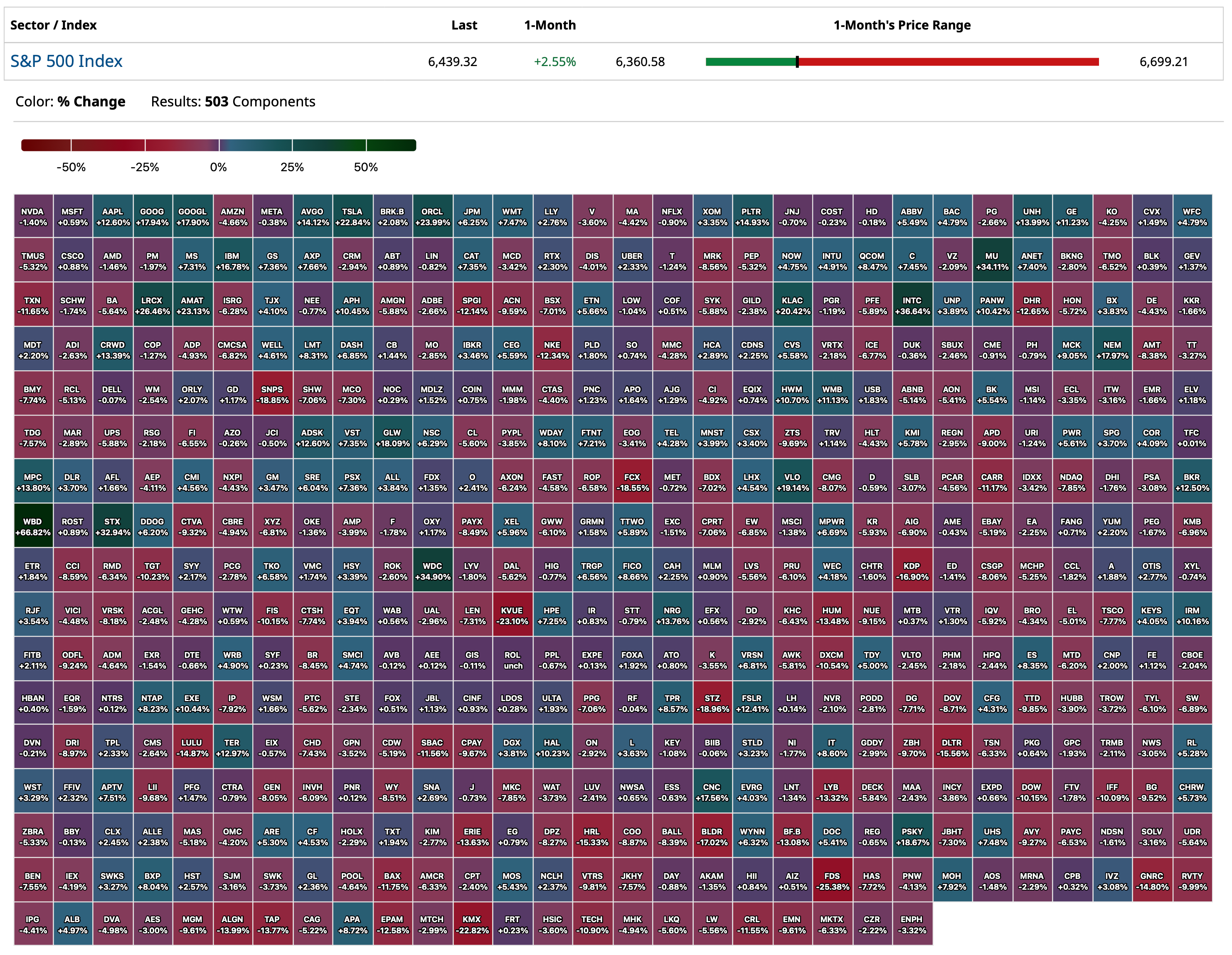

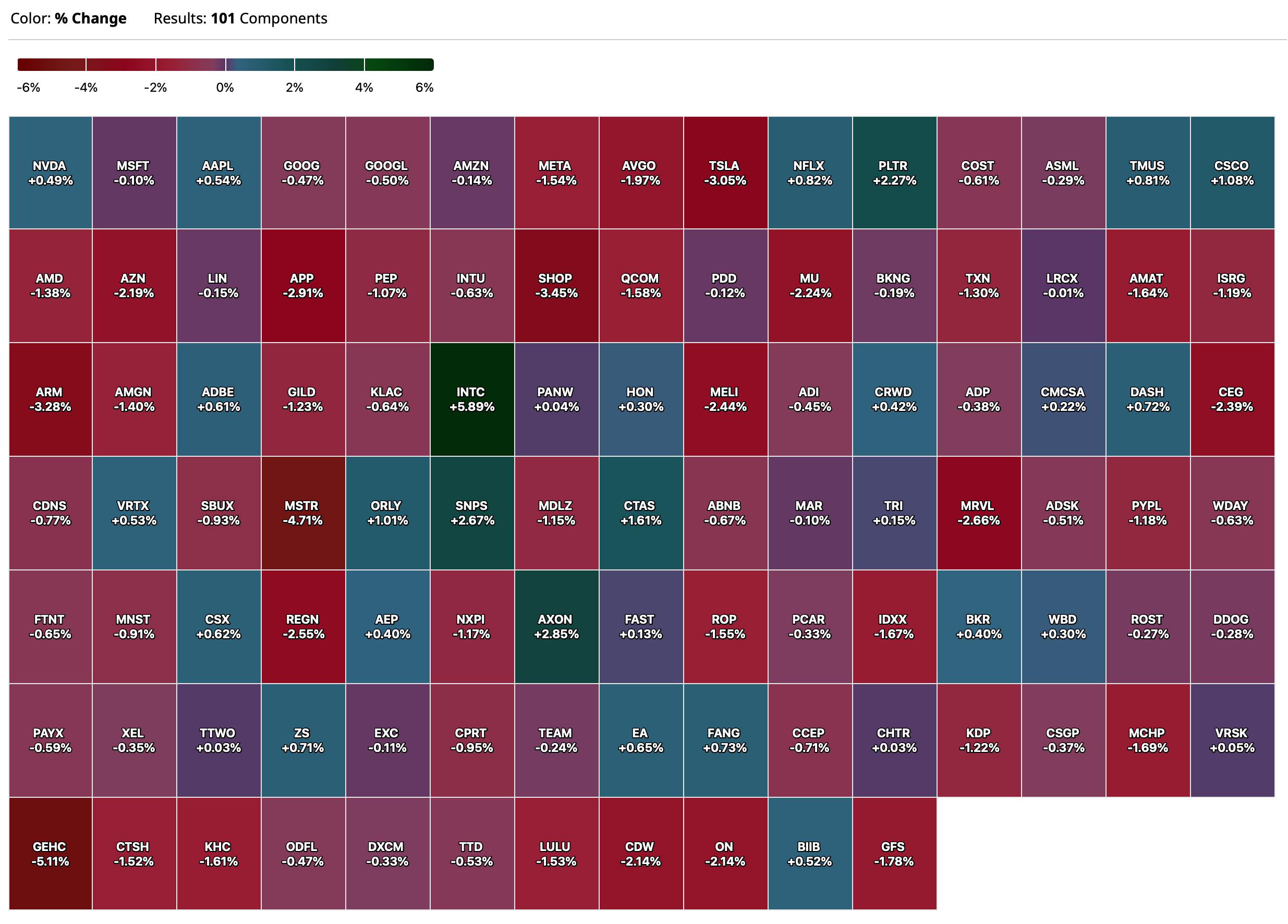

Nasdaq 100 Heat Map

BY Doug Kass · Sep 25, 2025, 4:48 PM EDT

BY Doug Kass · Sep 25, 2025, 4:48 PM EDT

Break in!

The S&P Short Range Oscillator has moved into oversold for the first time in quite a while (-1.97%).

BY Doug Kass · Sep 25, 2025, 4:40 PM EDT

BY Doug Kass · Sep 25, 2025, 3:32 PM EDT

At $16.32, I have moved to medium-sized long Kenvue (KVUE) .

Five percent yield.

BY Doug Kass · Sep 25, 2025, 2:50 PM EDT

Attys Must Pay $24K For AI Citations In FIFA Antitrust Case

By Lauren Berg

Counsel representing the now-shuttered Puerto Rico Soccer League in its antitrust suit against FIFA must pay more than $24,000 in attorney fees and litigation costs to the soccer federation and other defendants for filing briefs that appeared to contain errors hallucinated by artificial intelligence, a federal judge ruled Tuesday.

They will fix this soon, saving future generations of law firm associates the chore of actually reading cases they cite.

Westlaw Notes Uncopyrightable, AI Company Tells 3rd Circ.

By Elliot Weld

An artificial intelligence-powered legal search engine has asked the Third Circuit to reverse a district court's decision that its use of Westlaw headnotes did not constitute fair use [meaning they cannot use the copywritten materials for free], arguing its utilization of them "radically promoted scientific progress" and increased access to justice.

Of course AI should be entitled to use others’ work for free because, really, who is against scientific progress, access to justice or Mom’s apple pie.

BY Doug Kass · Sep 25, 2025, 2:40 PM EDT

From Peter Boockvar:

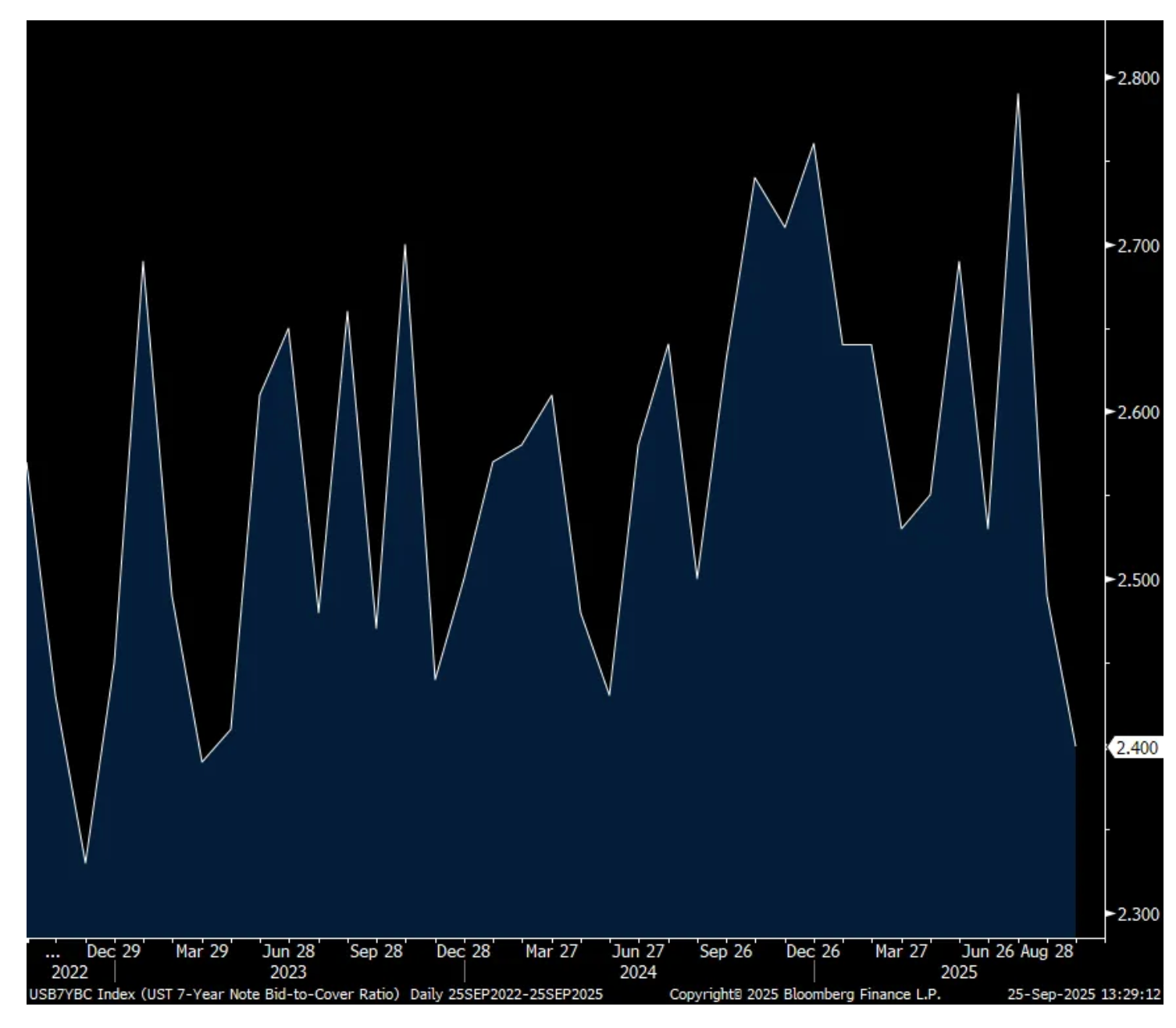

After sell on the Fed rate cut news, poor 7 yr auction

The sell on the Fed rate cut news over the past week was followed by a very poor 7 yr note auction. The yield of 3.953% was just above the when issued of 3.947% but what really stood out was the 2.40 bid to cover ratio which was well below the one year average of 2.64 and the weakest since March 2023. Also, dealers were left with 12% of the auction, the most in 5 months.

Treasury yields didn’t move much in response but are at the highs of the day with the 10 yr yield in particular at a 3 week high. May we live in interesting times.

Bid to Cover

BY Doug Kass · Sep 25, 2025, 2:20 PM EDT

JeffI

“Someone tell Joe Kernen and his guest on @SquawkCNBC (and all the rest of the sunshine boys and girls) that the aggregate S &P EPS revisions higher over the last four months are entirely on the shoulders of Mag7. The other 493 have not undergone much of a revision higher.”

Maybe… Historically the vast majority of returns came from just a small fraction of winners?

“…the top-performing 2.4% of companies account for all of the $75.7 trillion in net global stock market wealth creation during the entire 30-year period. This is to say, a handful of stocks drive the return of the stock market, and more than half of stocks do worse than essentially zero-risk T-bills.

Bessembinder’s findings are consistent with a previous study by the Vanguard Group, “How to Increase the Odds of Owning the Few Stocks that Drive Returns,” published in December 2019 in The Journal of Investing. The authors, Chris Tidmore, Francis M. Kinniry Jr., Giulio Renzi-Ricci, and Edoardo Cilla, found that the median return of stocks in the Russell 3000 Index between January 1987 and December 2017 was just 7%, versus a mean return for the entire benchmark of 387%. The large difference between the median and mean shows that the vast majority of returns came from just a small fraction of winners.”

Dougie Kass

My tweet had nothing to do at all with your case (above) that a small set of companies are typically responsible for overall aggregate market performance over time.

I was directly responding to the CNBC guest (and Joe K) who both opined that the upward S and P EPS revisions for 2025 were broadly higher and encompassed many sectors/industries. They were not as nearly all the revisions were confined to MAG7's contributions.

Estimates for the other 493 S and P members below MAG 7 were virtually unchanged.

You conflate two entirely different issues and create a "Straw Man" to be argumentative.

BY Doug Kass · Sep 25, 2025, 2:00 PM EDT

* We interrupt tonight's radio broadcast...

"Incredible as it may seem, both the observations of science and the evidence of our eyes lead to the inescapable assumption that those strange beings who landed in the Jersey farmlands tonight are the vanguard of an invading army from the planet Mars."

- Orson Welles, War of the Worlds Radio Broadcast

On October 30, 1938 The War of the Worlds (directed and narrated by Orson Welles) was broadcast.

This infamous radio adaptation of H.G. Welles' novel caused widespread panic among listeners who believed that an actual alien invasion was occurring. The broadcast was presented as a a series of news bulletins, which contributed to the confusion and fear among the audience. It is often cited as one of the most significant events in American broadcast history, showcasing the power of radio as a medium for storytelling and information dissemination. (So, I want to emphasize that this event has NOT actually happened yet, so no Orson Welles style misinterpretations please!)

Many (including myself) have predicted that President Trump’s second-term would be filled with unexpected, extreme and controversial policies that go much further than anything in his first term.

The president has already recommended eliminating quarterly reporting — in favor of six months' reporting. I believe that recommendation is put in place by year end. (My view continues to be that in doing so we lose a level of transparency and with it, producing a likely higher cost of capital.)

In a follow up to the change in quarterly reporting, in early 2026, in a move that stuns even his own party, President Trump in an attempt to elevate stock prices further, "rewards" (his words) the country's economy in the hopes of furthering his bull market narrative — by abolishing short-selling in all individual U.S. equities (futures are still allowed to be shorted).

Initially many believe, like the Orson Welles broadcast of The War of the Worlds, that the President's edict is hyperbolic (much like his initial tariff announcements) and that his intention to promote the idea is not real.

But this is not Grovers Mill, New Jersey and it is not Orson Welles' make believe War of the Worlds broadcast — this is President Trump's Washington, D.C.

The president markets his Executive Order by stating "that you either own a stock or you don’t," prompting a very short-lived and violent rally in global markets..

However, very soon after the announcement, his plan backfires as he fails to realize the enormous and leveraged hedges that exist in today's market. Those hedges are forced to be unwound in anticipation of the implementation of the Executive Order to eliminate equity shorts. The decline in stocks quickly accelerate as Citadel, Susquehanna and Goldman Sachs (in particular) grow ever more aggressive in selling out their large hedged books. Market makers and quant strategies hedged books are ruined — their liquidation of their hedges add even more fuel to the avalanche of selling.

Global equities decline by nearly 20% in the ensuing eight weeks. The negative wealth effect and erosion in consumer sentiment are instrumental in generating back-to-back negative quarters of real GDP (a recession).

And now back to dulcet tones of "Stardust" with Ramon Raquello and his orchestra.

BY Doug Kass · Sep 25, 2025, 12:35 PM EDT

BY Doug Kass · Sep 25, 2025, 11:40 AM EDT

As I mentioned earlier, I sold some of my long position in premarket on the gap to $5.

BY Doug Kass · Sep 25, 2025, 11:15 AM EDT

BY Doug Kass · Sep 25, 2025, 11:00 AM EDT

From Peter Boockvar:

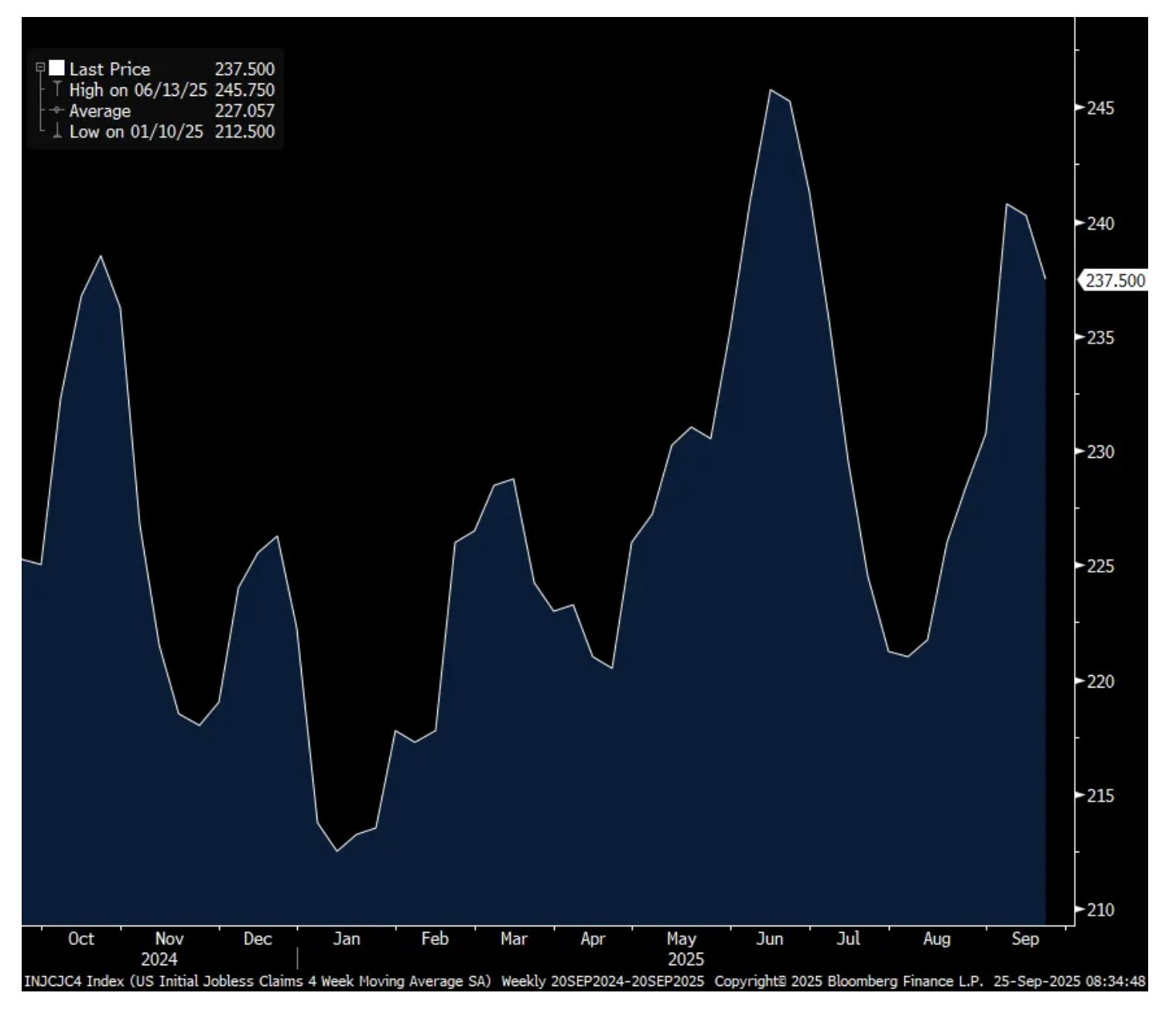

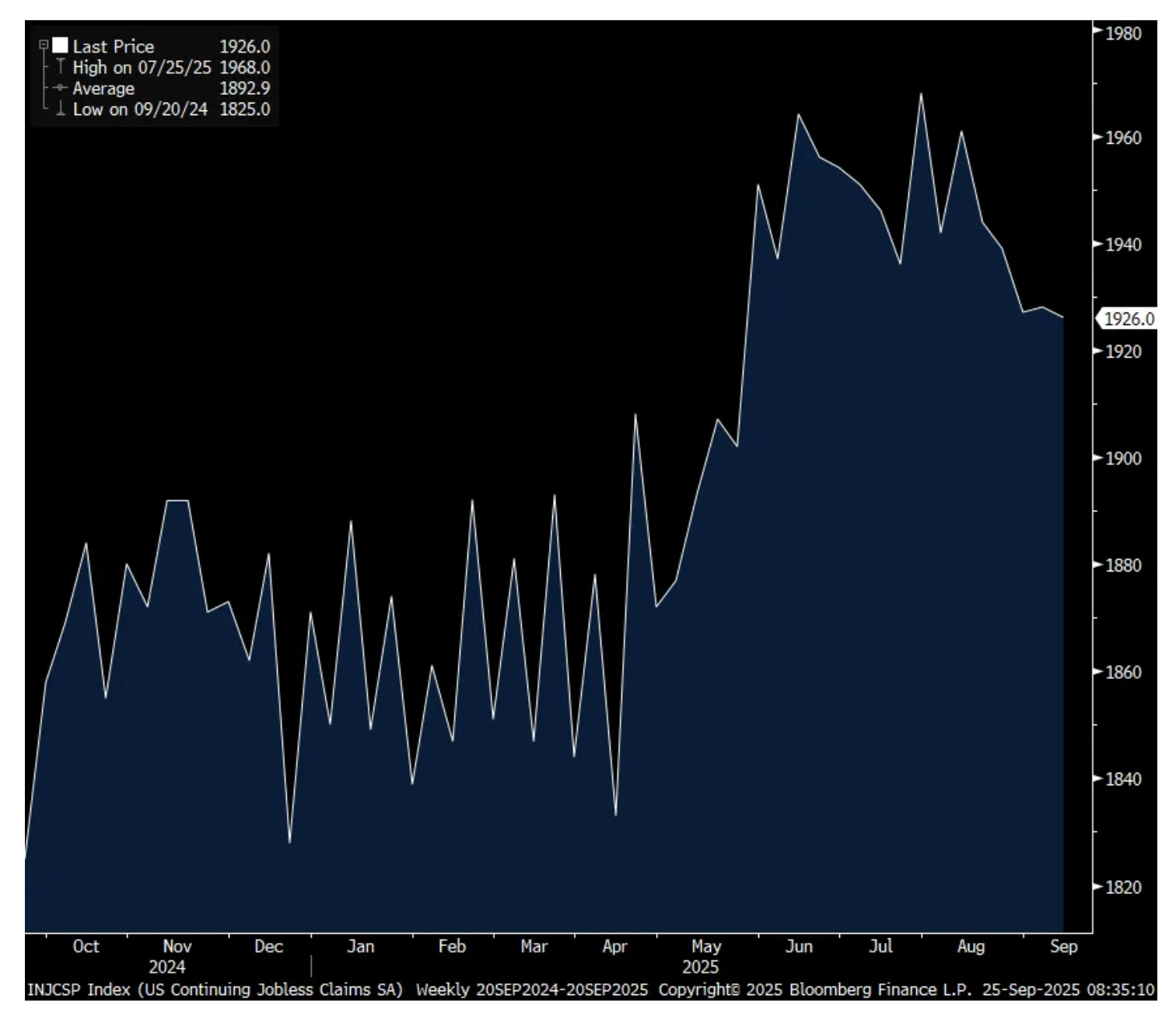

Initial jobless claims fell to 218k from 232k and that was 15k below expectations. The 4 week average slipped to 238k from 240k. This smooths out the 264k print two weeks ago which for now ended up being an outlier. Continuing claims were little changed at 1.926mm.

The bottom line remains very much the same with still a muted pace of firing’s as measured here, though it is above its one year average, at the same time there is a sluggish pace of hiring’s. I can’t say whether the drop in continuing claims is because they are running out or these people are finding new jobs as we’ll need other corroborating information to figure that out.

4 week avg Initial Claims

Continuing Claims

August core durable goods orders rose .6% m/o/m vs the estimate of no change but half was given back by the downward revision of .3% in July. Q3 GDP estimates could be trimmed though as core shipments fell by .3% instead of rising by .3% as forecasted.

While very old news, Q2 GDP was revised up to 3.8% growth from the last read of 3.3%. Merging this with the Q1 decline of .5% puts first half GDP growth averaging 1.65% at an annualized pace. An increase in personal spending on services was the main reason for the upgrade along with a smaller than expected drag from the drop in inventories. The other line items were mostly left little changed.

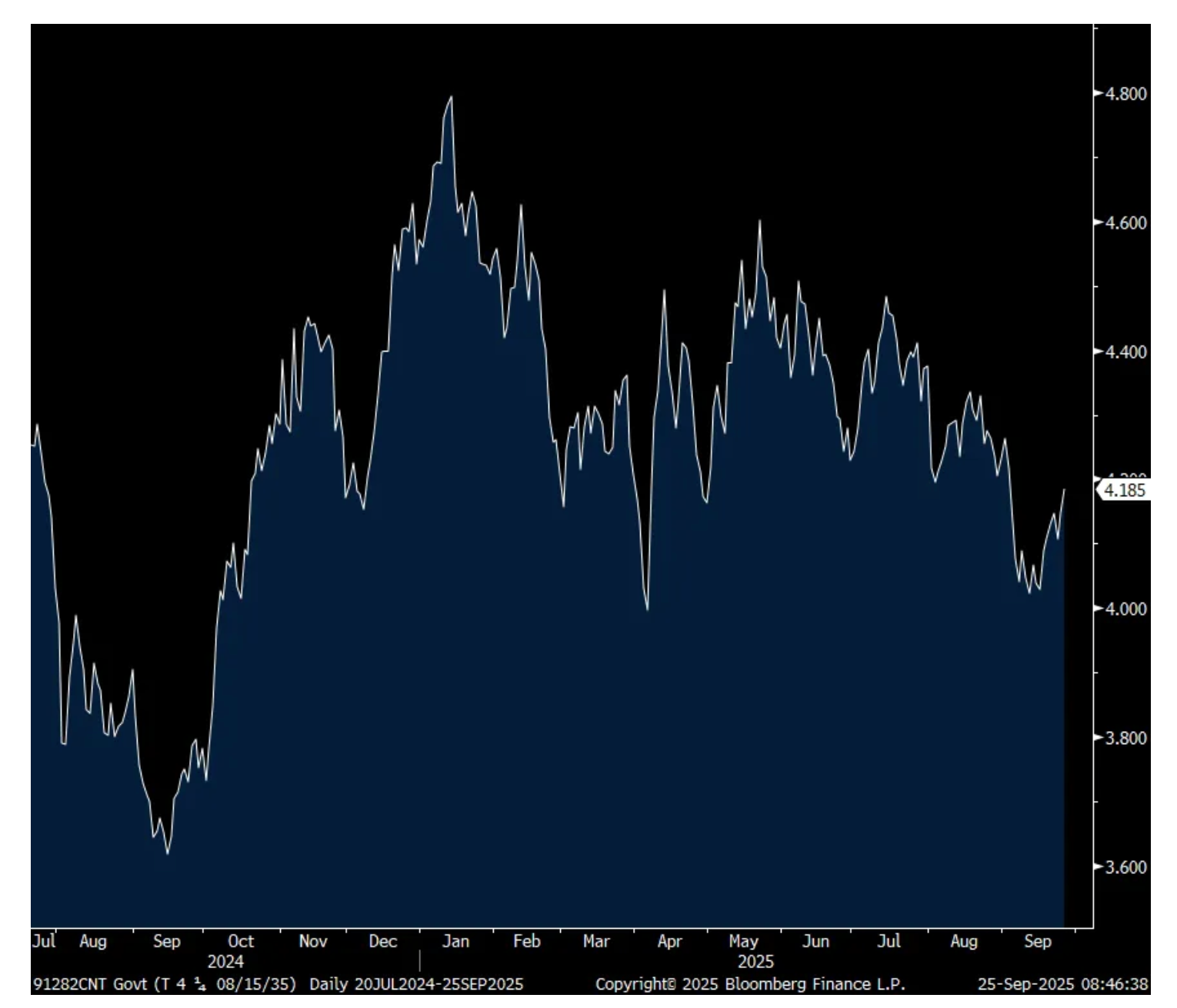

Yields are at the highs of the morning in response. The 2 yr yield at 3.65-.66% compares with 3.54% right before the Fed cuts rates. The 10 yr yield at 4.18-.19% vs 4.04% prior to the cut and the 30 yr yield is now at 4.76%, up 11 bps from 1:59pm est last week. We’ll see where this goes from here but early on, we’re seeing a repeat of the rate reaction to the September 2024 initial Fed rate cut of 50 bps.

Stretching this out, when the 10 yr yield started its leg down going into the September 2024 rate cut it was at about 4.25% vs 4.19% right now as stated. So, 125 bps of Fed rate cuts has given us 6 bps of relief on the 10 yr. Yes, the 10 yr yield is down from the 2023 peak of 5% but it’s still up from 3.60% on the day the Fed starting its easing process. I remain bearish on long duration sovereign bonds.

10 yr Yield from mid July 2024 thru today

BY Doug Kass · Sep 25, 2025, 10:30 AM EDT

Adding to (PEP) long $141.47 and (KVUE) at $16.61.

BY Doug Kass · Sep 25, 2025, 10:26 AM EDT

From Peter Boockvar:

Forget about what some economist says or what a government stat reveals, the Richmond Fed’s Q3 CFO survey, in collaboration with Duke business school, told us yesterday what CFO’s think about the influence of tariffs on prices. “Overall, CFOs projected that tariffs would have a big impact on price growth: On average, price growth would be about 30% lower in 2025 and roughly 25% lower in 2026 without the addition of tariffs, indicating that firms expect to grapple with tariff-related price increases into 2026. Meanwhile, almost a quarter of firms continued to report that they will decrease capital spending in 2025 due to tariffs.”

As for the overall survey, “The outlook for the US economy among financial decision makers improved somewhat in the third quarter of 2025, as uncertainty declined. However, concerns about the impact of tariffs on prices and business performance continued to weigh on firms.”

(see www.richmondfed.org/)

Another notable survey came out yesterday and this one was from the Dallas Fed and it was their quarterly energy report. While the index increased a touch, it remained below zero at -6.5 vs -8.1 in Q2. With oil prices at around $65, no wonder. Here were some of the relevant comments from those in the industry, either E&P or on the services side and it confirms my bullishness on the energy sector with the mood dour and why we are long oil, natural gas and pipeline companies, among other factors:

“There are a variety of issues affecting our business. First, excess in the global oil market is restraining oil prices near term. Second, there is continued uncertainty from OPEC+ unwinding production cuts. Third, trade and tariff changes and the resulting geopolitical tensions.”

“The administration is pushing for $40 per barrel crude oil, and with tariffs on foreign tubular goods, [input] prices are up, and drilling is going to disappear. The oil industry is once again going to lose valuable employees.”

“The uncertainty from the administration’s policies has put a damper on all investment in the oilpatch. Those who can are running for the exits. Tobin’s q < 1.”

“The U.S. shale business is broken. What was once the world’s most dynamic energy engine has been gutted by political hostility and economic ignorance. The previous administration vilified the industry, buried it in regulation and cheered the flight of capital under the environmental, social and governance banner. Wall Street and pension funds walked away, and even private equity shifted from fueling growth to engineering exits. Now the current administration is finishing the job. Guided by a U.S. Department of Energy that tells them what they want to hear instead of hard facts, they operate with little understanding of shale economics. Instead of supporting domestic production, they’ve effectively aligned with OPEC—using supply tactics to push prices below economic thresholds, kneecapping U.S. producers in the process. The collapse of capital availability has fueled consolidation by the majors, pushing out independents and entrepreneurs who once defined the shale revolution. In their place, a handful of giants now dominate but at the cost of enormous job loss and the destruction of the innovative, risk-taking culture that made the U.S. shale industry great.”

“While crude prices have stabilized in the low-$60s per barrel, the expectation of higher prices is still present. Because of that, a stable price in the low-60s has increased uncertainty due to the expectation of low-60s well into 2026 if not beyond. Costs have been relatively flat and we’re not seeing the efficiency gains that are being reported elsewhere in the Permian. With all of that, our expectation is to manage our lease expirations but not drill unnecessary wells in this price environment.”

“OPEC overproduction is affecting our business. So is weak sanctions on Russia. U.S. production staying flat while non-U.S. and non-OPEC production is growing exacerbating the glut. The administration’s tariffs, particularly on steel and aluminum at fifty percent, are increasing our cost of business.”

“Tariffs continue to increase the cost of production. We are suffering from a combination of increased cost due to tariffs and downward pricing pressure from end users. Global geopolitical issues and U.S. foreign policy uncertainty are creating increased financial challenges for both our U.S. and international business.”

“A vibrant oilfield services sector is critical if and when the U.S. needs to ramp up production. Right now we are bleeding.”

“Tariffs are increasing our supply costs.”

Shifting to surveys on stock market sentiment, we’ve reached what I consider extreme in the Investors Intelligence index where the Bull/Bear spread is now above 40. Bulls rose to 58.5 from 56.6 while Bears held at just 17. The weekly AAII saw no change in Bulls at 41.7 while Bears fell by 3.2 pts to 39.2. I still think the former survey is voting market momentum as sentiment follows price while the retail survey has views on the economy and jobs market that creeps into the mood.

On to some earnings comments.

From Thor Industries, the RV maker:

“While there is significant internal excitement around the company specific initiatives that have the potential to drive business results beyond what the broader market would normally support, we are cognizant of the inherent uncertainty surrounding the timing of these dynamics playing out. Additionally, with multiple data points suggesting weakness emerging in the job market, we think it is prudent to plan for another challenging year.”

From KB Home:

“With respect to current conditions, we are pleased to see stability in demand in June, which continued as our third quarter progressed. We are encouraged by the decline in mortgage interest rates, which should support greater demand for homeownership.”

“Our focus is on offering the most compelling value at a transparent price while limiting the use of incentives. When we discuss with buyers the alternative of the lower sales price we offer, versus a much higher price that can be offset by incentives, buyers recognize that they have a better opportunity for building wealth through equity over time with our home that has the lower starting price point.”

“While we experienced consistent traffic at our communities, net orders totaled 2,950, a 4% decline.”

“In the third quarter, pricing in our communities was as stable as we’ve seen this fiscal year, with 70% of our communities experiencing steady or increased prices and the other 30% price reductions, as we continue to balance pace and price to optimize our assets.”

“In terms of affordability, it has improved compared to the start of our third quarter, driven by the decrease in mortgage interest rates, which have fallen roughly 60 bps. This equates to approximately $30,000 of additional purchasing power at our average sales price, a significant boost for a first time or first time move-up buyer, which comprise about 70% of our homebuyers.”

That said by them, “Orders have been good, but I wouldn’t say that we’ve seen a big uptick yet or maybe the uptick that we would expect to see from such a change in mortgage rates. And I think to some extent buyers are in maybe a bit of a wait-and-see mode, maybe waiting for rates to come down further, maybe they were waiting around for the actual Fed event expecting that to have some immediate impact on rates.” I bolded for emphasis.

From the CarMax earnings release and whose stock is trading down pre-market as they missed both top and bottom line estimates:

They referred to the quarter as a “challenging” one as combined retail and wholesale used vehicle unit sales fell 4.1% y/o/y. Average selling prices for used vehicles fell 1% y/o/y while rising by 1.6% for wholesale vehicles.

This too of note in the Auto Finance business, “This quarter’s provision for loan losses was $142.2 million compared to $112.6 million in the prior year’s second quarter. The provision for loan losses in the 2nd quarter of fiscal 2026 included an increase of $71.3 million in our estimate of lifetime losses on existing loans, primarily due to worsening performance among 2022 and 2023 vintages. Despite the worsening performance, these vintages remain highly profitable. As a result of the previously disclosed tightening of CAF’s underwriting standards, the vintages originated after April 2024 are performing in line with expectations.”

“As of August 31, 2025, the allowance for loan losses of $507.3 million was 3.02% of auto loans held for investment, up from 2.76% as of May 31, 2025.”

The Swiss National Bank spared themselves, and the rest of us, from another trip into negative rates, for now by keeping their policy rate unchanged at zero as expected. President Schlegel of the SNB said “The bar to go into negative territory with interest rates is certainly higher than just a normal rate cut. We are aware that this negative interest rates could be a challenge for many actors in the economy. At the same time if it’s really necessary to fulfill our mandate we are ready to use all the tools that are available - also negative interest rates.”

I’ll argue again that NIRP is poison for any economy and financial system so I hope they don’t go there again. Zero rates are painful enough for lenders and savers.

Gilt yields and in other parts of Europe are higher today and in part why US Treasury yields are at their highest point since the Fed rate cut last week. Auctions of 5s, 9s, 13s and 30 yr gilts this week have all gone poorly. The bid to cover for the 30 yr in particular fell to a 3 year low.

BY Doug Kass · Sep 25, 2025, 10:15 AM EDT

* My mid year Surprise...

BY Doug Kass · Sep 25, 2025, 10:08 AM EDT

I have covered the balance of my Index shorts:

* (SPY) $655.75

* (QQQ) $589.17

I plan to reshort strength.

BY Doug Kass · Sep 25, 2025, 9:57 AM EDT

BY Doug Kass · Sep 25, 2025, 9:45 AM EDT

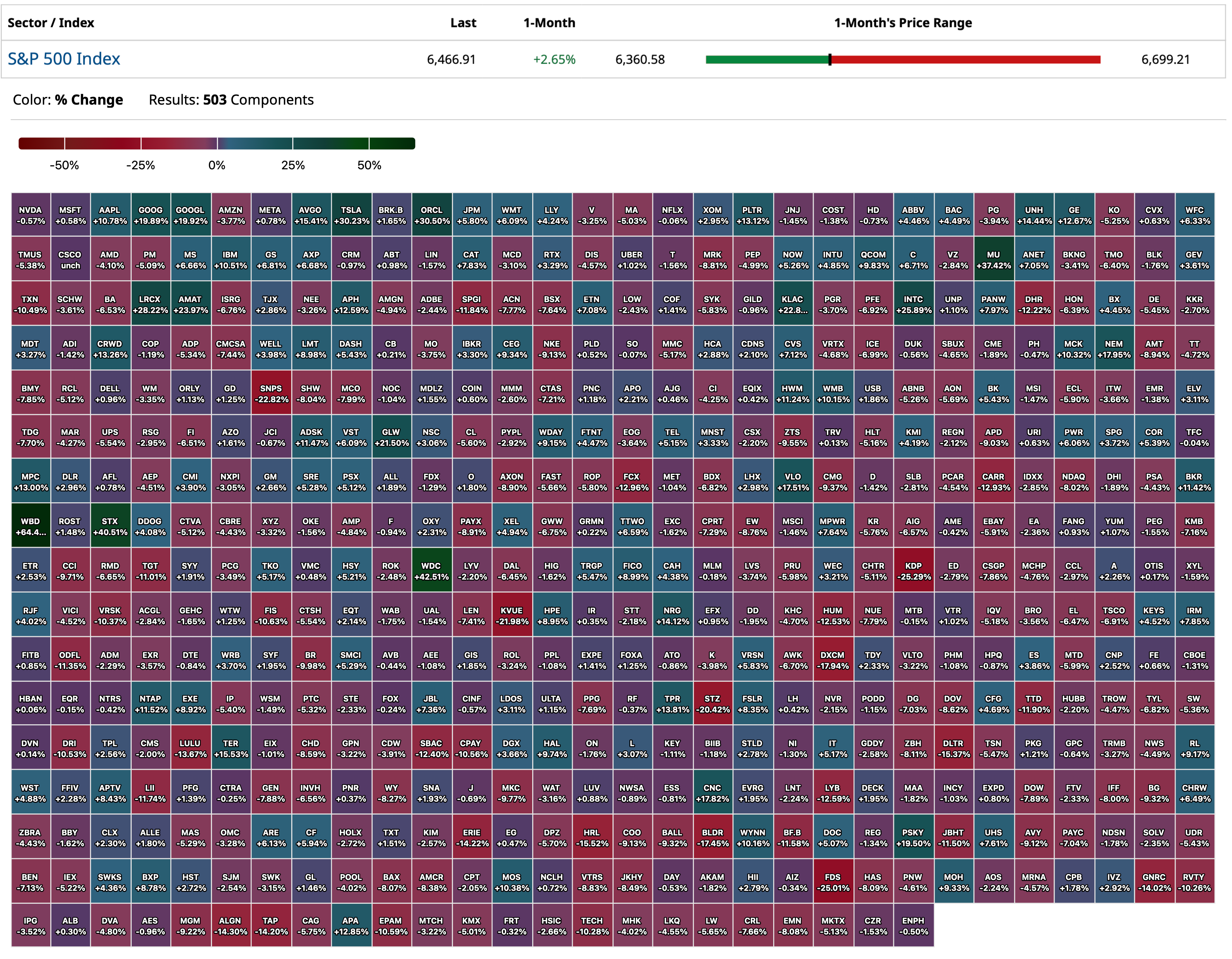

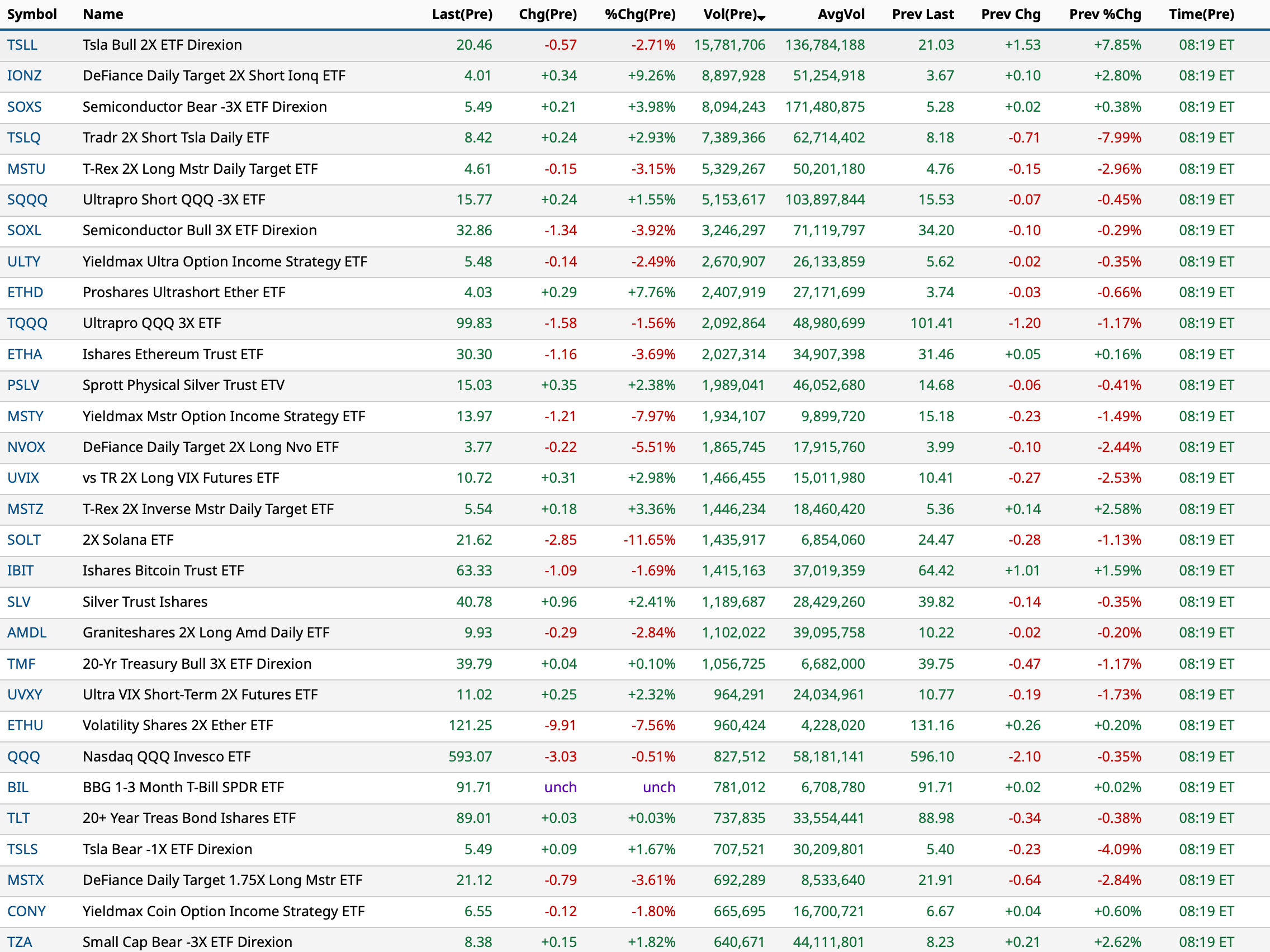

People may be surprised to learn how much red there is over a one-month period’s percent change per name….

BY Doug Kass · Sep 25, 2025, 9:30 AM EDT

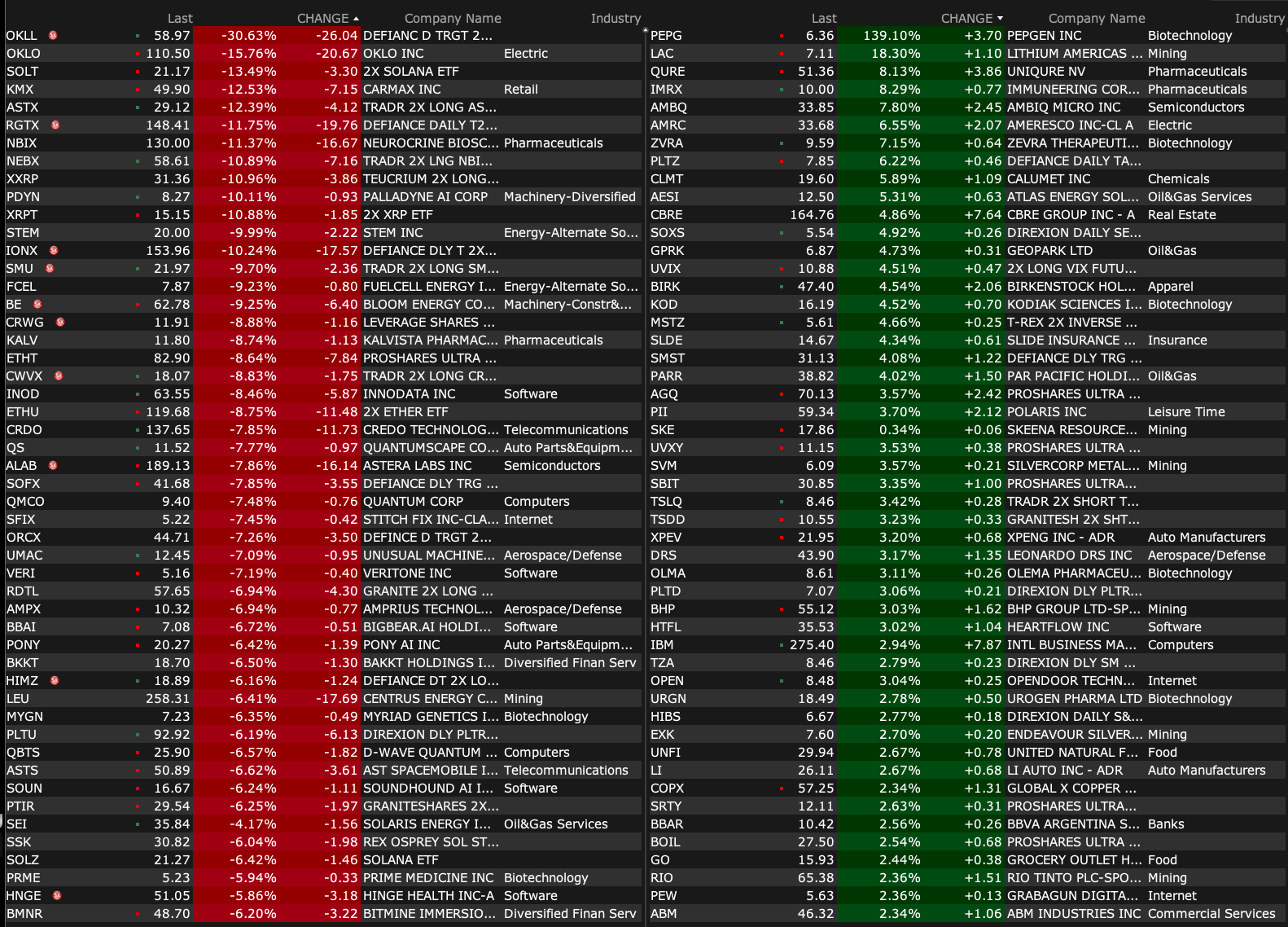

-LUXE +24% (earnings)

-LAC +21% (reportedly US government is considering a stake in company)

-IMRX +11% (prices $175M equity offering and concurrent placement to Sanofi at $9.23/share; the total number of shares is ~21.7M)

-QURE +8.7% (files to sell $200M public offering through Leerink, Stifel)

-CAPR +7.4% (affirms HOPE-3 pivotal trial topline data expected mid-Q4 2025 which will be used to support BLA resubmission)

-BIRK +4.5% (prelim earnings, guidance)

-OPEN +4.4% (Jane Street discloses 5.9% stake)

-BB +3.2% (earnings, guidance)

-IBM +3.1% (quantum computing partnership yields positive results)

-CIFR +2.2% (signs 168 MW, 10-Year AI Hosting Agreement with Fluidstack; files to sell $800M in 0.00% convertible senior notes due 2031)

-OKLO -15% (weakness in nuclear)

-RIG -15% (prices 125M shares at $3.05/share)

-KMX -13% (earnings)

-CTGO -11% (files to sell stocks and warrants)

-HNGE -9.5% (downside momentum)

-ALAB -6.5% (downside momentum)

-LEU -6.4% (weakness in nuclear)

-CRDO -6.3% (downside momentum)

-NNE -6.1% (weakness in nuclear)

-SFIX -6.0% (earnings, guidance)

-SNX -4.2% (earnings, guidance)

-ACN -3.9% (earnings, guidance)

-JBL -3.9% (earnings, guidance)

-SMR -3.5% (weakness in nuclear)

-ORCL -2.9% (Rothschild & Co Redburn Initiates ORCL with Sell, price target: $175)

-WS -2.8% (earnings)

-FUL -2.1% (earnings, guidance)

BY Doug Kass · Sep 25, 2025, 9:25 AM EDT

BY Doug Kass · Sep 25, 2025, 9:16 AM EDT

BY Doug Kass · Sep 25, 2025, 9:09 AM EDT

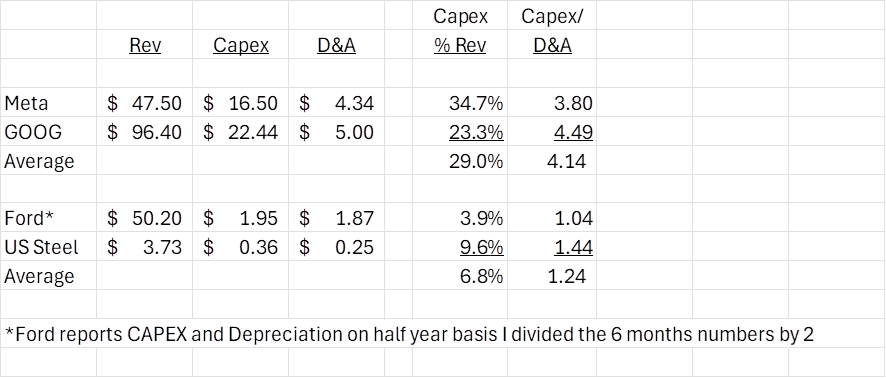

To date, investors have taken as gospel the rationale behind massive AI capital expenditures -- in terms of the increase in potential (and ultimate) customer user sets, what will be the return on invested capital, the ability to fund unprecedented cap ex and the contribution to overall company profits. Few are pointing out how the massive cap spending of hyperscalers (to buy Nvidia (NVDA) chips, etc.) will adversely impact their future earnings. As noted in previous "Tales", Jim Chanos has mocked the depreciation schedules - as I have.

The latest gimmick is for Nvidia to lease out GPUs. Customers don't want to take shorter depreciation marks:

I published the chart below in a previous More Tales From Nvidia in order to quantify the magnitude of the weight of depreciation .

Look at capital expenditure (I compare to two deep cyclicals, F and X to (META) and (GOOGL) ) as a percent of revenue vs. depreciation as a percent of revenue, and the ratio of capex to reported D&A. Capex is running at over 4-times reported D&A:

Finally, look how dependent the domestic economy is on AI spend:

And, as noted in my numerous "More Tales of Nvidia" I am suspicious that the AI capital spending will meet forecasts....

BY Doug Kass · Sep 25, 2025, 8:51 AM EDT

Fed Speakers:

8:20 a.m.: Fed Bank of Chicago President Goolsbee (Voter) participates in a moderated question-and- answer session before Crain's Power Lunch, "The Fed and the Economy: Trends for West Michigan," Grand Rapids, MI (Livestream here. Embargoed text TBD);

9 a.m.: Fed Bank of New York President Williams (Voter) gives welcome remarks before the Fourth Annual International Roles of the U.S. Dollar Conference hosted by the Federal Reserve Bank of New York and the Federal Reserve Board;

9 a.m.: Fed Bank of Kansas City President Schmid (Voter) speaks on "The View from Main Street" (monetary policy, economic and banking outlook) before the Mid-Sized Bank Coalition of America;

10 a.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks on "Supervision and Regulation" before hybrid Financial Markets Quality Conference 2025 (Text TBD. Q&A from moderator and audience. Livestream at youtube.com/live/p5dqovme1UE?);

1 p.m. Fed Board Governor Barr (Voter) participates in "Bank Stress Testing" conversation before the Peterson Institute for International Economics , Washington, DC (Text available. Q&A from moderator and audience);

1:40 p.m.: Fed Bank of Dallas issues text of President Logan's (Non-Voter) remarks before closed Federal Reserve Bank of Richmond Collaboration of Research Economists Week Panel;

3:30 p.m.: Fed Bank of San Francisco President Daly (Non-Voter) participates in conversation before the Federal Reserve Bank of San Francisco 2025 Western Bankers Forum, Salt Lake City, UT (No prepared remarks. No group media interview. Livestream here.)

BY Doug Kass · Sep 25, 2025, 8:29 AM EDT

BY Doug Kass · Sep 25, 2025, 7:45 AM EDT

BY Doug Kass · Sep 25, 2025, 7:30 AM EDT

From JPMorgan:

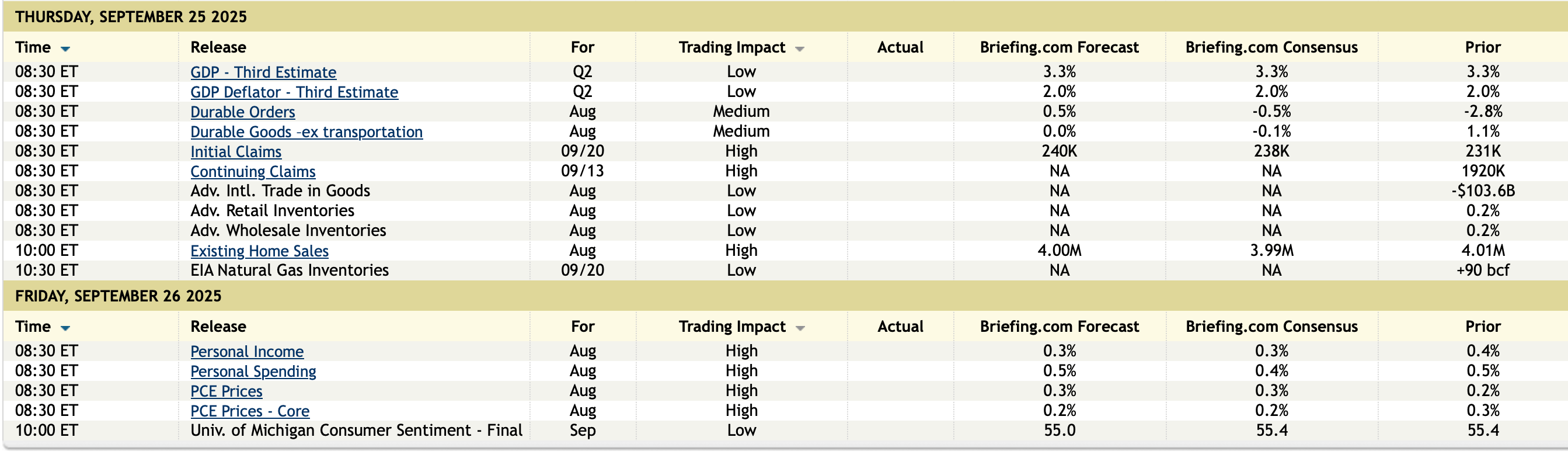

US: Futs are flat after giving up overnight gains with bond yields lower by 1-2bp and a flat USD; yesterday was the best USD performance since Sep 2. Pre-mkt, Mag7 / TMT are weaker ex-INTC who looks for an investment from AAPL. Defensives are leading Cyclicals pre-mkt. Cmdtys are mixed with silver +2% and coffee +1.5% the standouts. US launches a Section 232 (sectoral tariffs) probe on Machinery, Med Devices, and Robotics. Today’s macro data focus is on Q2 GDP data, Durable / Cap Goods, Jobless data, Existing Home Sales, Adv. Goods Net-Exports, and Inventories. While none of these macro releases is expected to be market-moving, they may provide a holistic view of a stable / resilient economy that may be inflecting higher.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

The last two sessions, we have seen the SPX fall later in the session alongside higher bond yields. This has led to client conversations questioning whether we are seeing some later than expected negative seasonality and / or if this an early start on the period-end rebalancing which is thought to see a selling of Equities and a buying of bonds. Given the lighter high touch volumes, it feels a bit like investors are waiting to see if there is a vol spike into month-end with some indicating that they will wait to for volumes to pick up before executing portfolio changes. In some cases, rebalancing’s occur 2-3 days before the period ends which would be Friday / Monday. Could we be setting up for a 1-2% downdraft? Maybe. The SPX has seen two days since May 1 where the index lost at least 1.5%, highlighting the strength of the ‘dip buyers’. In any case, the near-term setup remains bullish, and we would buy any weakness. Also, keep an eye on EM Equities.

BY Doug Kass · Sep 25, 2025, 7:20 AM EDT

BY Doug Kass · Sep 25, 2025, 7:10 AM EDT

BY Doug Kass · Sep 25, 2025, 7:00 AM EDT

BY Doug Kass · Sep 25, 2025, 6:50 AM EDT

BY Doug Kass · Sep 25, 2025, 6:35 AM EDT

BY Doug Kass · Sep 25, 2025, 6:25 AM EDT

That said, in premarket trading, (MSOS) traded over $5/share (on no news) and I have made some sales. (I had purchased stock under $4.40 all week, as documented).

BY Doug Kass · Sep 25, 2025, 6:15 AM EDT

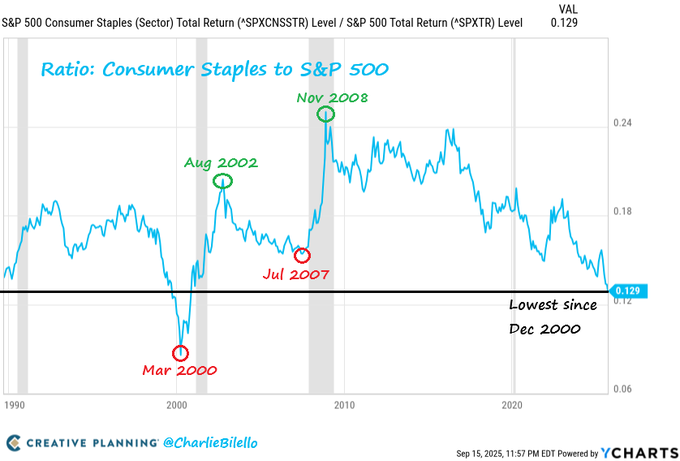

* In terms of opportunities in value we are somewhere between March 2000 and July 2007...

Yesterday I pointed out how inexpensive consumer staples are to the overall market:

Here is another example of that theme:

BY Doug Kass · Sep 25, 2025, 6:05 AM EDT

BY Doug Kass · Sep 25, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at 0.82% vs. 1.35%.

BY Doug Kass · Sep 25, 2025, 5:45 AM EDT