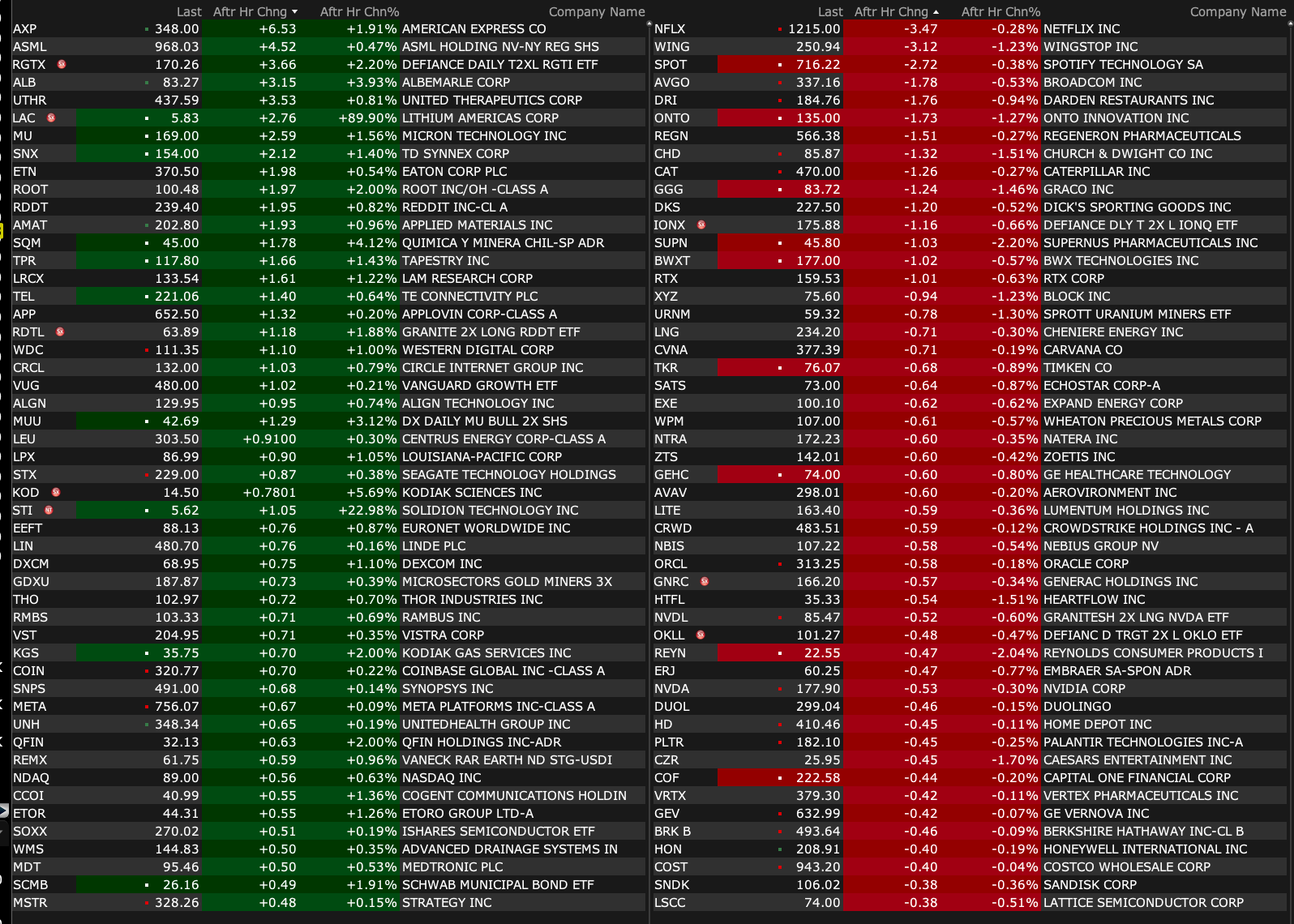

Tuesday's After-Hours Movers

As of 4:23 p.m.:

BY Doug Kass · Sep 23, 2025, 4:45 PM EDT

As of 4:23 p.m.:

BY Doug Kass · Sep 23, 2025, 4:45 PM EDT

BY Doug Kass · Sep 23, 2025, 4:27 PM EDT

BY Doug Kass · Sep 23, 2025, 3:35 PM EDT

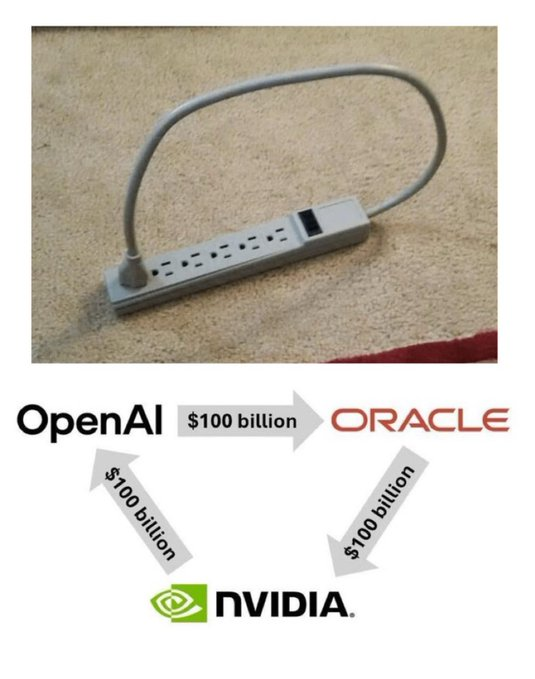

I will take, "Things That Happen At The Top for $1,000, Alex":

BY Doug Kass · Sep 23, 2025, 3:00 PM EDT

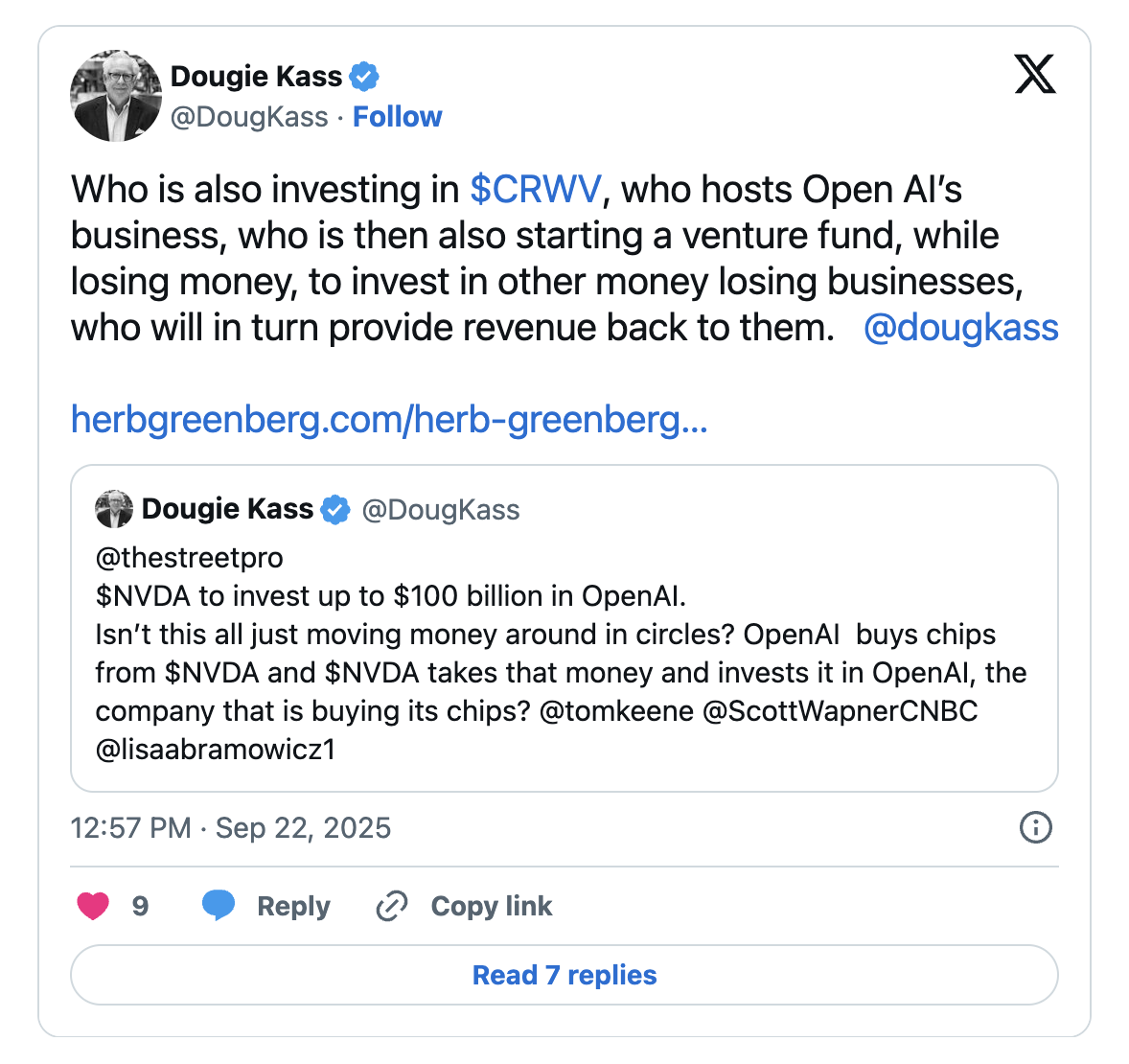

Regarding my point that the AI industry is seemingly self-funding itself in a circular fashion for a reason — it is interesting to link to a study on AI from Bain Consulting below.

The revenue and economics are not there in a natural fashion and the markets do not want to fund this in a natural fashion. So industry participants are funding their own revenue, and financing their own customers, which is a circular relationship.

It is interesting this is legal.

Extend the analogy.

Any large company is not earning much on their massive cash balance. They all have ridiculously high multiples, so buying back stock is not terribly accretive either (it is really just funding stock option exercise and executive comp as well as supporting the stock price, which is also circular). Therefore, every big public company with a big multiple should just found a shell company, that they are the minority investor in, by giving themselves a small ownership share by virtue of ascribing a massive valuation to the shell vehicle, and then having that vehicle turn around and buy services and products from them in return. Do the math on how the public company’s revenue is capitalized, versus what the cash is earning on their own balance sheet. Then in turn, ask yourself how much stock these executives own, and how much they are selling?

AI companies will need $2 trillion in combined annual revenue to fund computing power by 2030, but their revenue is likely to fall $800 billion short, according to Bain & Co.

Bain & Co. estimates that global incremental AI computing requirements could soar to 200 gigawatts by 2030, with the US accounting for half that, and warns that supply chain constraints or insufficient power supply could thwart progress.

An $800 Billion Revenue Shortfall Threatens AI Future, Bain Says

From yesterday:

SEP 22, 2025 1:21 PM EDT

SEP 22, 2025 12:34 PM EDT

BY Doug Kass · Sep 23, 2025, 2:45 PM EDT

Wolf Street on the biggest housing losers (in price terms).

BY Doug Kass · Sep 23, 2025, 2:15 PM EDT

I wanted to take this opportunity to wish Shana Tova to all of my Jewish friends.

And I offer this prayer for the year ahead:

Eternal God, we ask Your blessing for the State of Israel and those who defend it. At this time of ongoing war and loss, give strength to the bereaved and bind up the wounds of the injured. God of peace, grant vision and wisdom to the leaders of the region. God of compassion, help us to hear the cries of the innocents suffering in Israel and in Gaza. God of mercy and strength, inspire the hearts of the captives to keep holding out hope. Please, Eternal source of life, release them, redeem them, bring them home. And let us say, Amen.

BY Doug Kass · Sep 23, 2025, 2:00 PM EDT

From Peter Boockvar:

Powell says nothing new

After having spoken in both a prepared speech and his Q&A last week after the FOMC meeting, Powell in his speech today is not saying anything new.

He again highlighted his challenge, “Near term risks to inflation are tilted to the upside and risks to employment to the downside, a challenging situation. Two-sided risks mean that there is no risk free path.”

For reference, after a tremendous bond rally that took the 2 yr yield to 3.54%, the 10 yr yield to 4.04% and the 30 yr yield to 4.65% at 1:59pm est last Wednesday, we now stand at 3.59%, 4.14% and 4.75% for each of those maturities. I remain bearish on long term sovereign duration around the world and you can’t just analyze US growth, inflation and Fed rate expectations as part of one’s analysis I believe on where rates will go.

BY Doug Kass · Sep 23, 2025, 1:35 PM EDT

From Randorama:

Randy

Fed Speak

Fed Chair Powell Says Downside Risks To Employment Shifted Balance Of Risks, Prompting Last Week's Rate Cut; Rate Cut Was Another Step Toward A More Neutral Policy Stance; Two-Sided Risks Mean There Is No Risk-free Path; Policy Not On Preset Course; Policy Stance Still Modestly Restrictive, Well-positioned To Respond To Potential Developments; Economic Growth Has Moderated, Downside Risks To Employment Have Risen; Inflation Has Risen, Remains Somewhat Elevated

Chair Powell Says Consumer Spending Has Slowed, Businesses Say Uncertainty Weighs On Outlook; Labor Market Less Dynamic, Somewhat Softer; Unusual And Challenging Decline In Both Supply And Demand For Workers; 12-Month PCE Inflation Was Probably 2.7% In August, Core PCE 2.3%, Both Up From Prior Year And Driven By Goods Prices; Goods Price Increases Largely Reflect Tariffs, Not Broader Price Pressures; Reasonable Base Case Is That Tariff-driven Inflation Effects Will Be Relatively Short-lived

Powell Says Disinflation For Services Continues; Most Long-Term Inflation Expectations Consistent With 2% Goal; Tariff Increases Will Likely Show Up As Somewhat Higher Inflation Over Several Quarters; Will Make Sure One-Time Increase In Prices Does Not Become Ongoing Inflation Problem; Public Trust In Economic, Political Institutions Has Been Challenged, Those In Public Service Must Focus Tightly On Critical Missions

BY Doug Kass · Sep 23, 2025, 1:20 PM EDT

Here are today's things:

* Shorted more GS at $822.21.

* Shorted more MS at $163.29.

* Shorted more C at $104.27.

* Added to KVUE at $17.57.

* Added to PEP at $140.31.

BY Doug Kass · Sep 23, 2025, 1:06 PM EDT

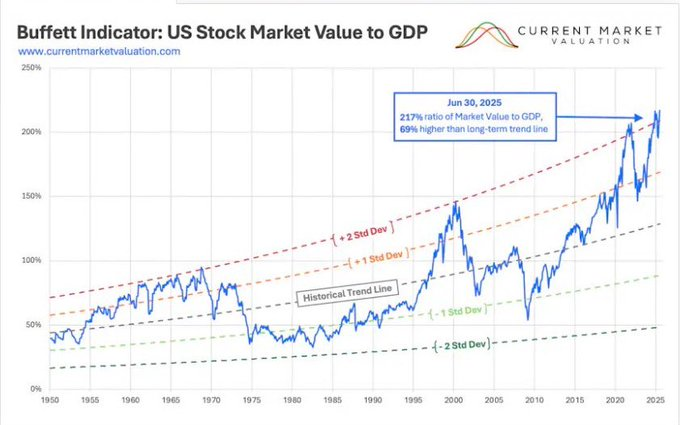

I was (correctly) reprimanded by someone on Twitter, regarding this chart I posted on The Buffett Indicator (about two hours ago):

The tweet was accurate — I mistakenly used the June 30, 2025 S&P price (6000) and not the much higher current price (6685):

So, I understated how overvalued the market is based on this Indicator.

BY Doug Kass · Sep 23, 2025, 12:50 PM EDT

* Not my father's market...

Blackstone BX traded at a high of $189.87 an hour or so ago (up $4/share) — now under $186.00 (and basically flat).

Passive investing dominates the investing landscape — and here is another example of how dispassionate, momentum-based strategies and products buy higher.

And, when price and momentum break, they sell lower.

This is not my father's market.

BY Doug Kass · Sep 23, 2025, 12:35 PM EDT

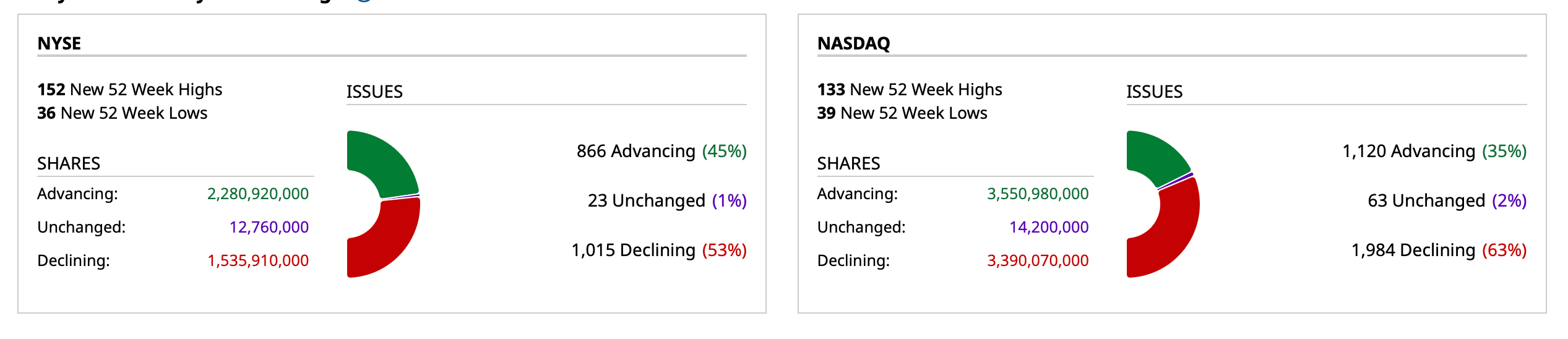

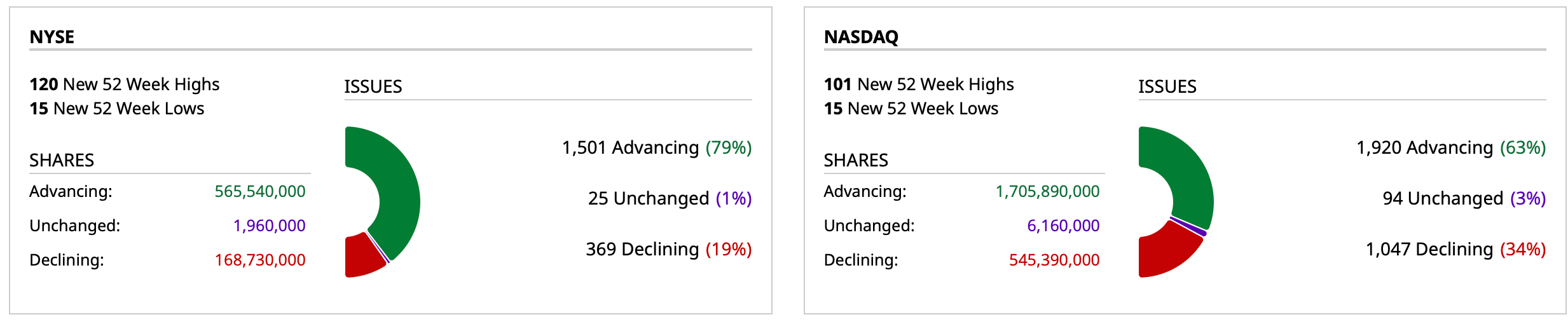

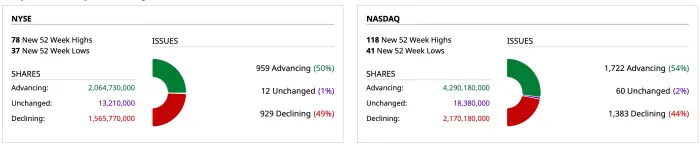

- NYSE volume 5% above its one-month average

- NASDAQ volume 14% above its one-month average

- VIX index: up 0.06% to 16.11

BY Doug Kass · Sep 23, 2025, 11:55 AM EDT

I added to Kenvue KVUE at $17.52.

BY Doug Kass · Sep 23, 2025, 11:41 AM EDT

The Buffett Indicator is now nearly 70% above trendline — and at a record 217%.

To state the obvious, this is not a good launching pad for future investment returns.

BY Doug Kass · Sep 23, 2025, 10:50 AM EDT

This morning from The Divine Ms M:

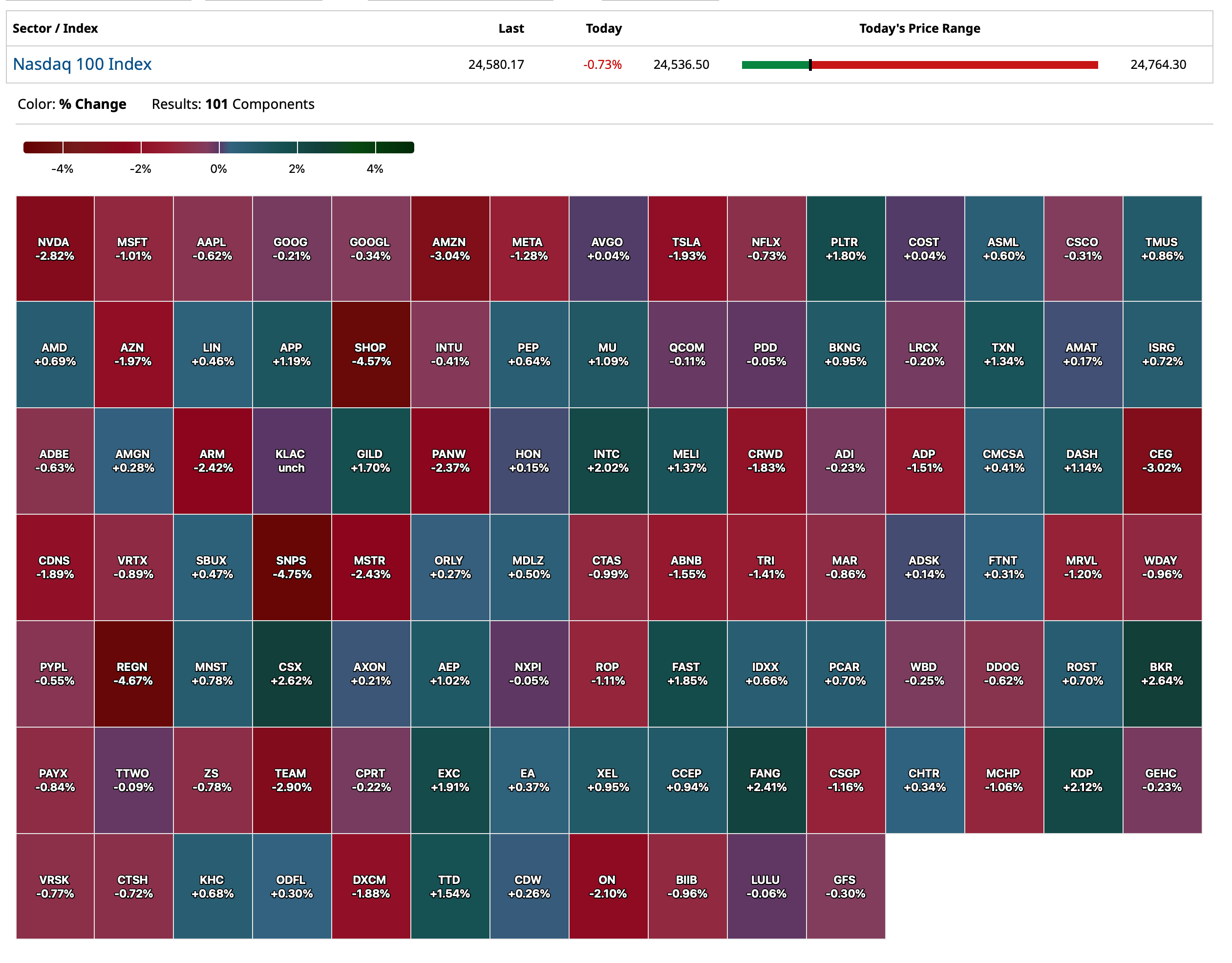

Meta META, Google GOOGL, and Amazon AMZN were all down on Monday. Is a rally in NVDIA NVDA now sucking the life out of them, not just the 493? Amazon has yet to make a higher high than February and now sits smack on an uptrend line. Maybe tomorrow it will get saved and become the stock of the day, but I find it curious no one gets excited over this stock anymore. They must have some AI thing they can talk about!

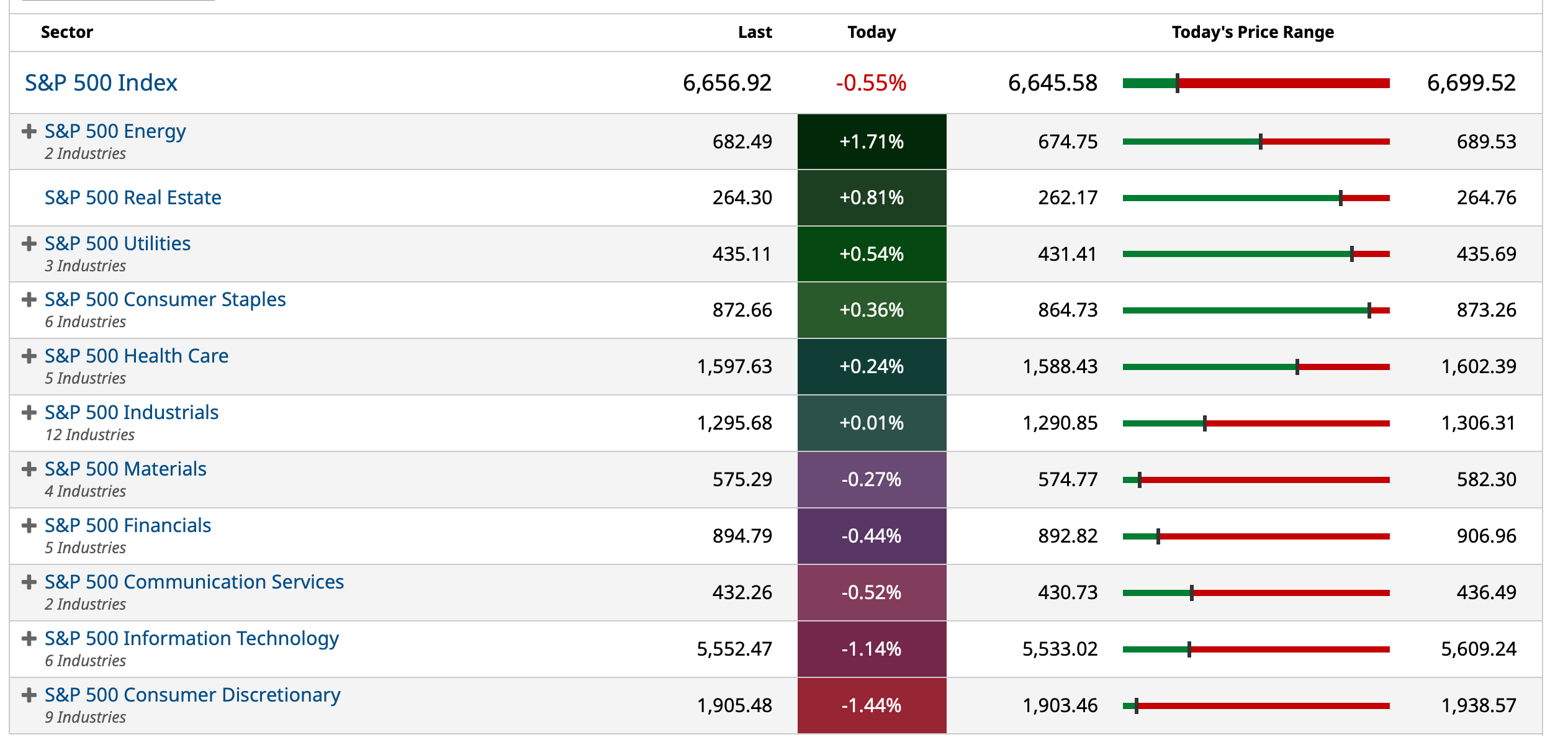

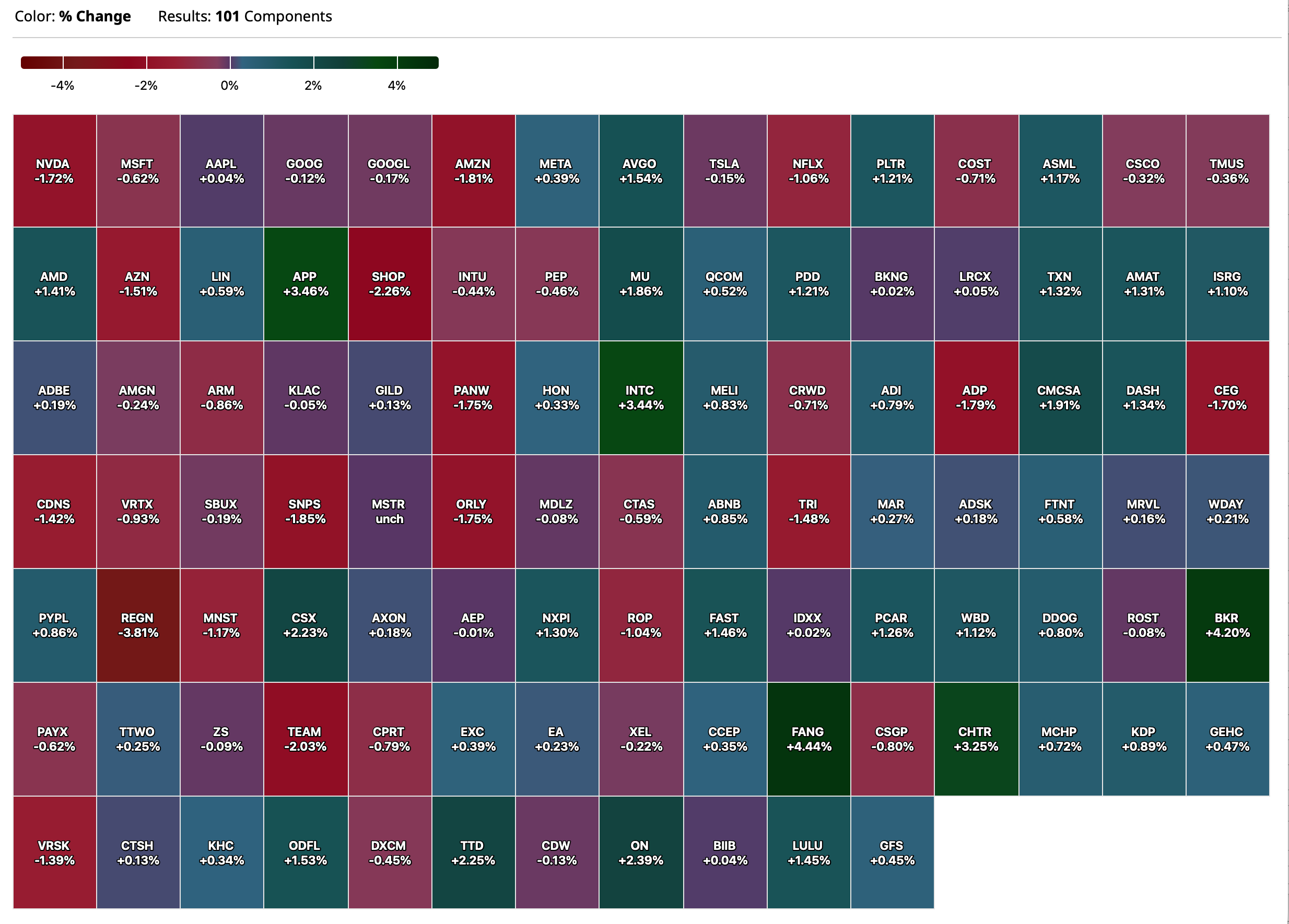

By contrast, NVDA, AAPL and ORCL accounted for 42% of the S&P advance - as overall NYSE market breadth was flat (though Nasdaq breadth was slightly positive):

Strange brew... and hard to dance to (American Bandstand)!

BY Doug Kass · Sep 23, 2025, 10:10 AM EDT

Needham says DIS should consider shutting down ABC:

Needham analyst Laura Martin:

"Jimmy Kimmel is back on ABC. Tactically, we recommend DIS launch simulcasts of all ABC broadcast content on Hulu (in addition to its ABC app), so DIS's viewers can always watch DIS's content on an unregulated platform, in order to preserve revenue. Given DIS's negative share price performance based on recent FCC comments, we argue that DIS should shut down (not sell) ABC because we believe: Value destruction would be low as a percent of DIS's market cap, and 1x only, which Wall Street would add back; Shutting down ABC would unmask DIS's faster revenue growth segments, which would drive valuation multiple expansion and result in 10% more value for DIS shareholders; and, GenAI collapses time frames, thereby making the delays, distractions and headaches of regulation more expensive, so jettisoning regulatory risks is increasingly valuable."

BY Doug Kass · Sep 23, 2025, 9:45 AM EDT

From today's Spencer Jakab's WSJ Market A.M. newsletter:

The polite phrase when giving a stranger holiday greetings these days is “if you celebrate.”

There’s no need to tiptoe around mentioning the great U.S. bull market. It’s something seemingly every American holds in awe: Let us rejoice and be glad in it. But this is a time of year when a bit of religious superstition moves traders of all faith

Among the more famous bits of market timing wisdom is “Sell Rosh Hashanah, Buy Yom Kippur.” The period between the two holiest days on the Jewish calendar, the new year and the day of atonement, is notoriously rocky for stocks. The dates move around according to a complicated lunisolar calendar and fall in September or October. This year’s High Holy Days kick off today and end October 2.

Though not quite dating back to biblical times, the stock-market legend has some history. It supposedly took hold in 1955 when the Dow had its second-largest point drop ever on the eve of Yom Kippur. President Eisenhower had suffered a heart attack.

There are other seasonal patterns—the Santa Claus Rally, the Decennial Cycle, the January Barometer. Many have become less potent the more they’re known.

But “Sell Rosh Hashanah” still has a decent record over the past 25 years. On average, the S&P lost 0.68% between the holidays and gained 0.79% in the following two weeks, based on data from Bespoke Investment Group.

Of course September is a notoriously rocky month anyway, and October has seen plenty of crashes, so the timing of the holidays is inauspicious. Why are those months so bad for stocks, though? Nobody knows.

A more apt question is why investors love seasonal patterns. One is that everyone wants a shortcut. Back when stockbrokers needed clients to be active and pay hefty commissions, they loved them too: Patterns provided one more excuse to dial for dollars.

Even in today’s zero-commission world, shifting in and out of stocks or funds for a week triggers taxes. The money to potentially be saved, meanwhile, is insubstantial.

If you were to actually trade on a seasonal trend, which you really shouldn’t, the one to pick would be “Sell in May and Go Away.” According to “The Stock Traders Almanac,” investing $10,000 in the Dow Jones Industrial Average every November and selling the following April from 1950 through 2023 would have earned you $1,352,316 before dividends. The other six months of those years? A measly $2,910.

That trend had some basis long ago in a primarily agricultural economy. Farmers required capital when planting in the spring and then flooded banks with savings after the harvest.

If you celebrate, there’s a Jewish version of the same pattern: “Buy Yom Kippur, Sell Passover.”

BY Doug Kass · Sep 23, 2025, 9:35 AM EDT

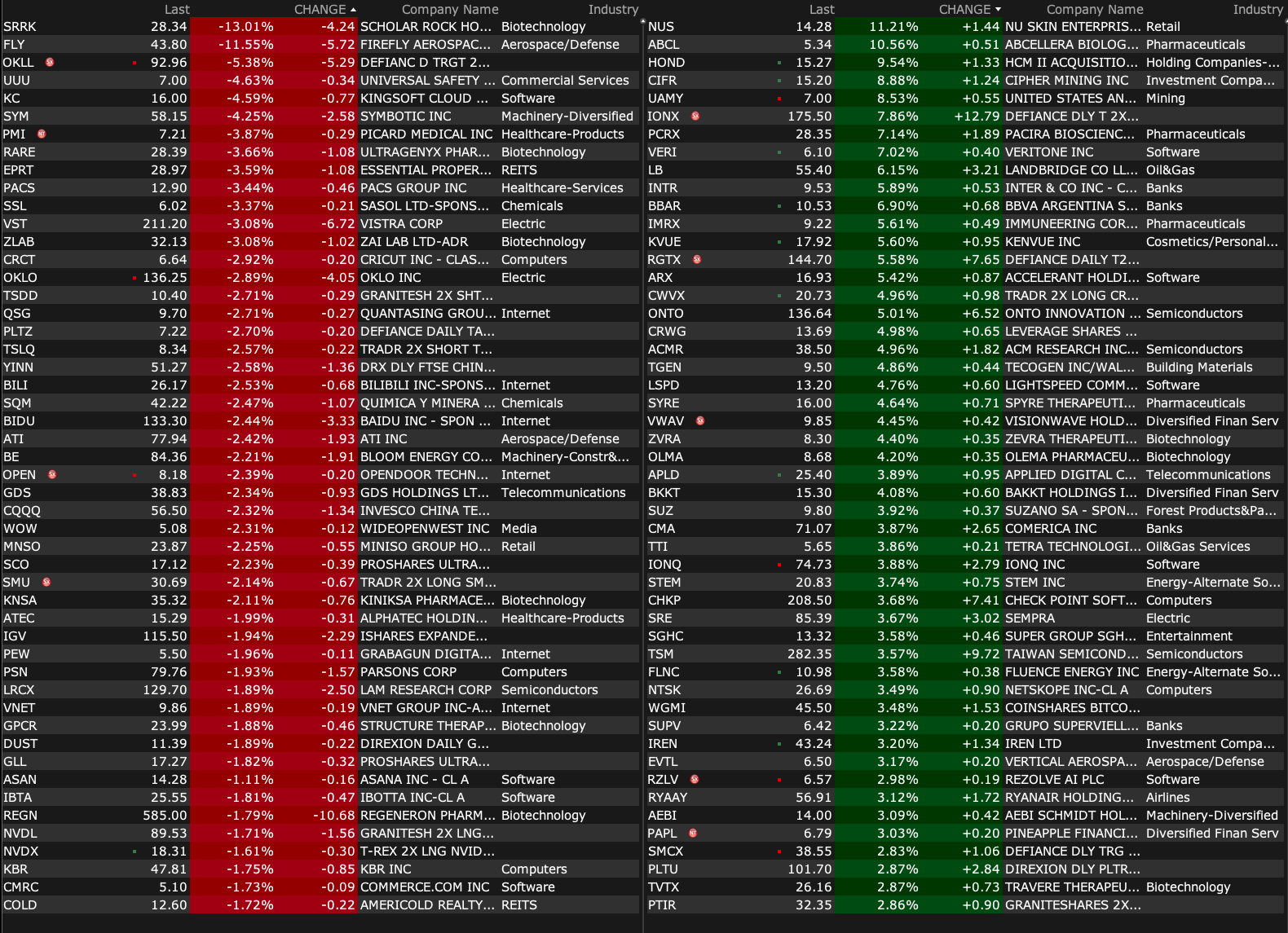

-FLD +29% (launches Bitcoin Credit Card with up to 3.5% rewards, powered by Stripe and Visa)

-UAMY +11% (awarded $245M Sole-Source Five-Year Contract by the U.S. Defense Logistics Agency for the Purchase of Antimony Ingots)

-VERI +7.0% (adds ESPN audio content to NCAA Championship licensing)

-LB +5.9% (announces strategic agreement with NRG to power potential data center in the Delaware Basin, Texas)

-KVUE +5.6% (EMA Notes Use of paracetamol (acetaminophen) during pregnancy unchanged in the EU following Trump Administration linking drug to autism)

-ACMR +5.3% (to replace KLG in the S&P SmallCap 600 Index, effective Sept 26th)

-IONQ +3.8% (achieves Significant Quantum Internet Milestone, Demonstrates Quantum Frequency Conversion to Telecom Wavelengths)

-SRE +3.7% (to sell 45% of Sempra Infrastructure Partners for $10B cash to KKR affiliates)

-TSM +3.6% (3nm process price increase)

-KITT +3.5% (announces Ultra Deepwater Aquanaut Test Results using Subnero Modems)

-BA +2.5% (lands $8B Uzbekistan deal and reportedly nearly large China deal)

-BOXL -27% (prices 1.33M shares at $3.00/shr in $4.0M registered direct offering)

-DGNX -16% (downside momentum)

-SRRK -13% (FDA issues CRL for apitegromab; Resubmission planned after Catalent remediation)

-FLY -11% (earnings, guidance)

-STSS -5.6% (partners with Jupiter Exchange on staking partnership to accelerate Solana adoption)

-KC -4.7% (prices upsized HK$2.8B offering of 338M shares at HK$8.29/shr)

-FLGC -3.8% (enters sales agreement with Revere Securities for up to $2.1M of shares)

-LAC -3.3% (reportedly Trump Administration reviewing DoE loan for Company’s Thacker Pass mine)

-VST -3.0% (Jefferies Cuts VST to Hold from Buy, price target: $230)

-AZO -2.4% (earnings, color)

BY Doug Kass · Sep 23, 2025, 9:20 AM EDT

I am buying KVUE:

BY Doug Kass · Sep 23, 2025, 9:10 AM EDT

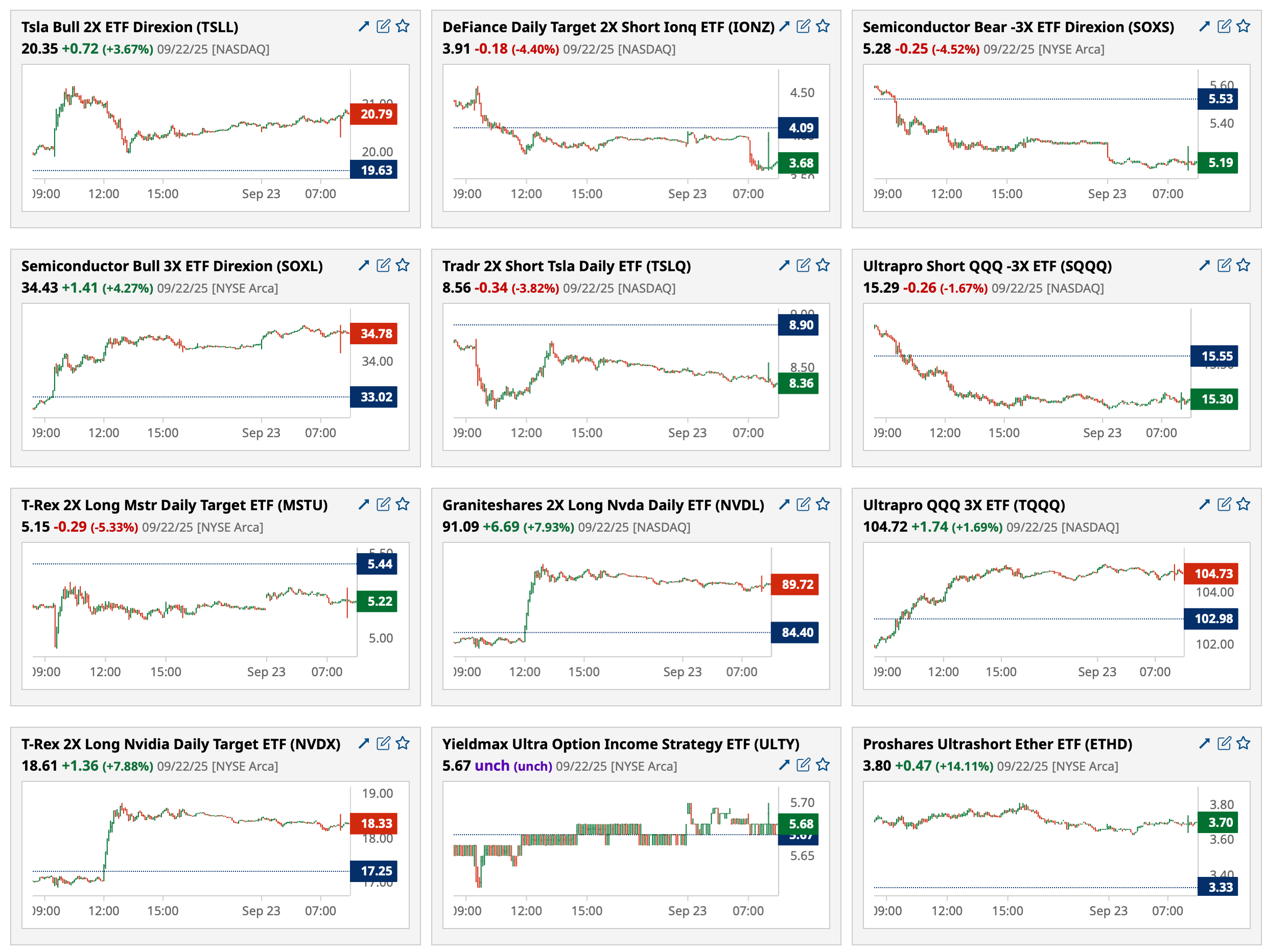

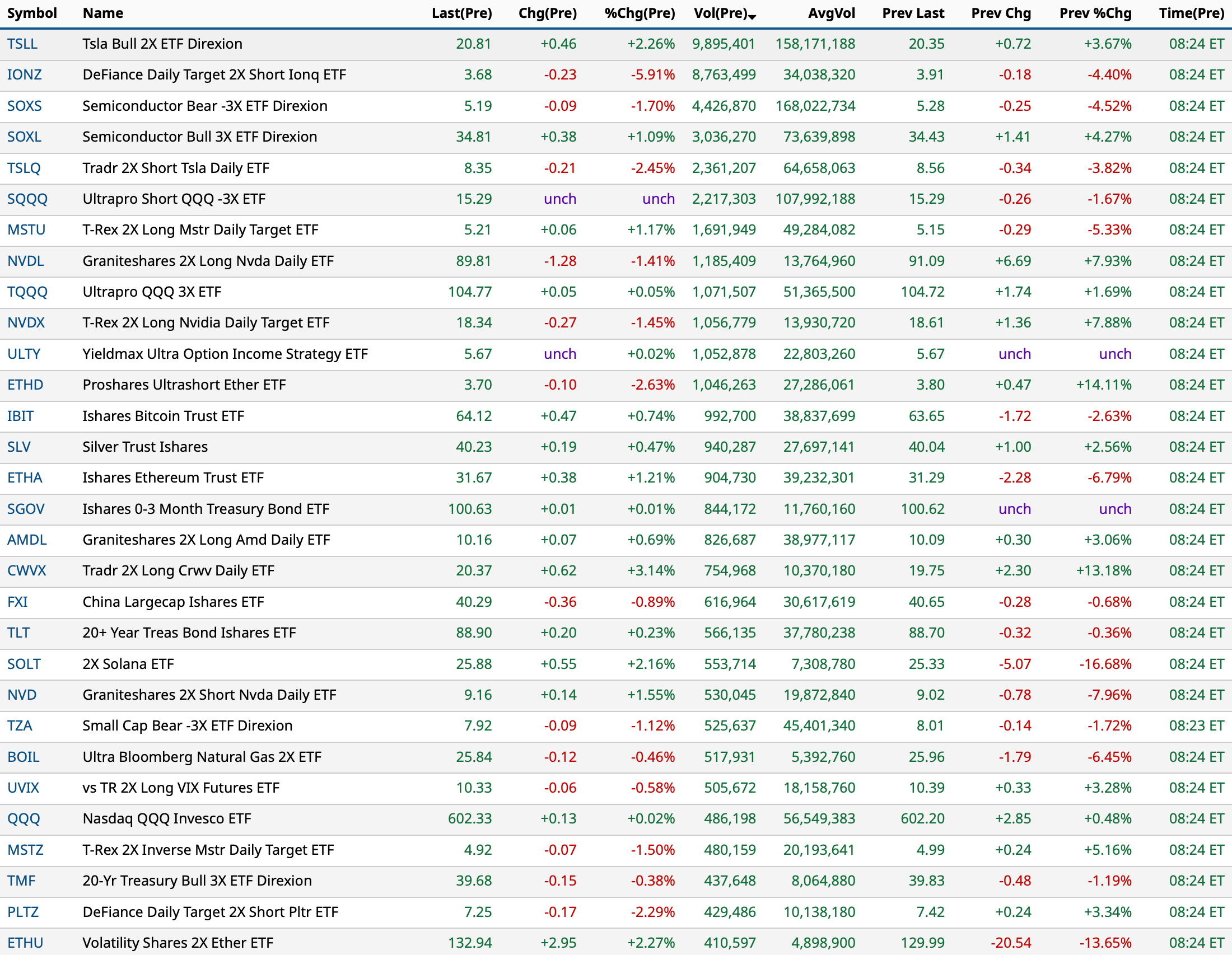

BY Doug Kass · Sep 23, 2025, 9:00 AM EDT

BY Doug Kass · Sep 23, 2025, 8:50 AM EDT

FED SPEAKERS:

8:30 a.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) Television Appearance -- CNBC Squawk Box;

9:00 a.m.: Fed Vice Chair for Supervision Bowman (Voter) speaks on the economic outlook before the 134th Annual Kentucky Bankers Association Convention, Virtual (Text available. Q&A from moderator);

10:00 a.m.: Fed Bank of Atlanta President Bostic (Non-Voter) speaks on the economic outlook before a Macro Musings podcast live recording. (Livestream. No audience Q&A. No media Q&A. No embargoed text);

12:35 p.m.: Fed Chair Powell speaks on the economic outlook before the Greater Providence Chamber of Commerce 2025 Economic Outlook Luncheon, Warwick, RI (Text available. Q&A from moderator. Livestream at vimeo.com;

3:10 p.m.: Fed Bank of Chicago President Goolsbee (Non-Voter) Television Appearance -- ABC News Live (streaming news service)

TREASURY AUCTIONS TODAY:

8:00 a.m.: Fed Treasury Repo Reference Rate;

11:00 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasury hosts an $85B 6-Week Bill Auction;

1:00 p.m.: Treasury hosts a $69B 2-Year Note Auction

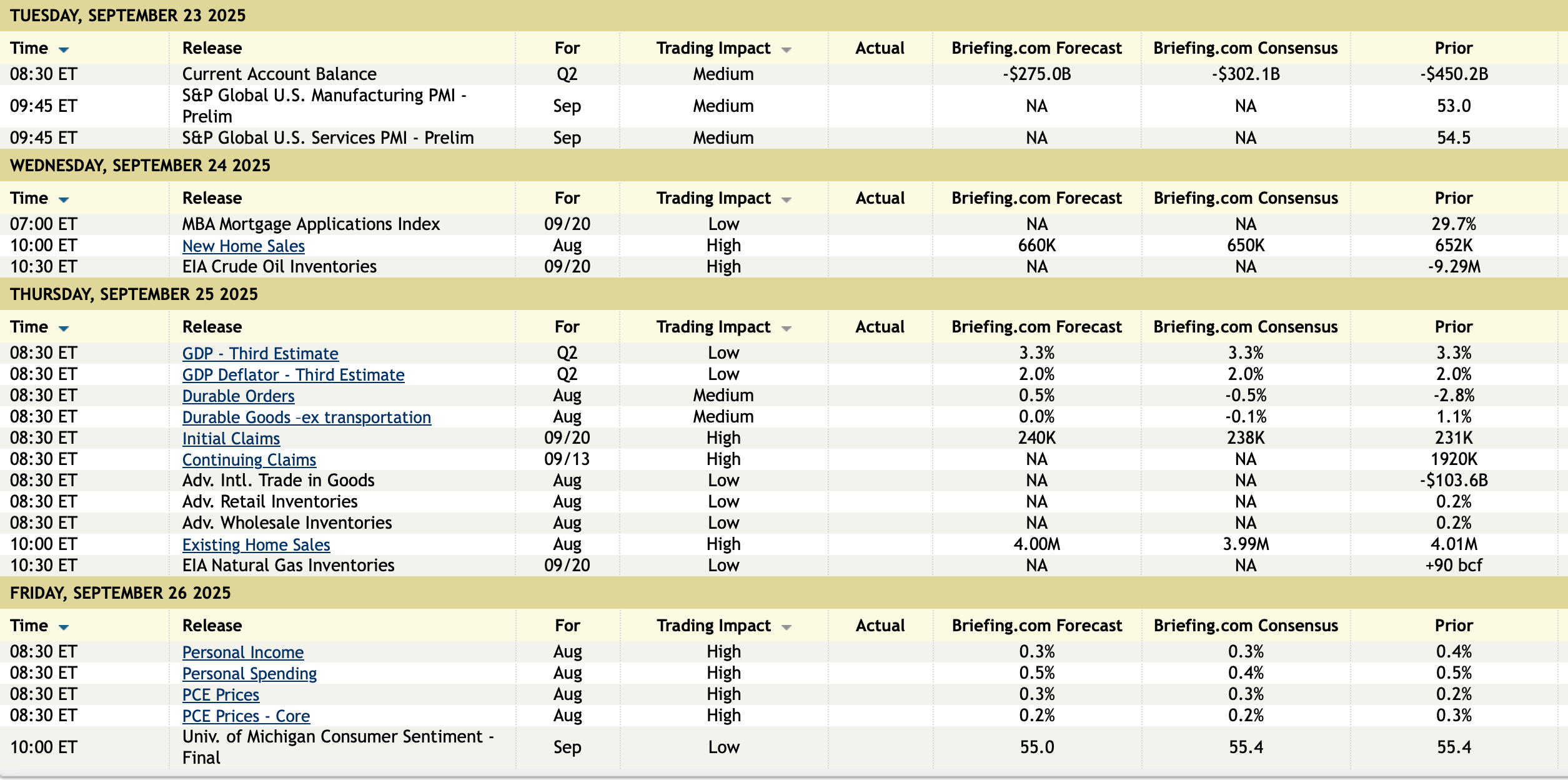

ECONOMIC CALENDAR FOR THE WEEK:

BY Doug Kass · Sep 23, 2025, 8:35 AM EDT

From Peter Boockvar:

Another vendor financing deal in the AI space between Nvidia and Open AI has the names Lucent and Nortel ringing in my ear from the days when they announced similar deals with customers in the late 1990's except the ones being announced now are so much bigger in terms of dollars. With the other massive agreements Open AI is announcing, with the previous $300b one with Oracle, Open AI in a way is now too big to fail for the sake of the GenAI data center buildout. For this whole massive experiment to work without causing large losses, Open AI and its peers now have got to generate huge revenues and profits to pay for all the obligations they are signing up for and at the same time provide a return to its investors.

Bain doesn't think it's going to happen anytime soon. While I haven't seen their actual piece, I saw in a Bloomberg News story this morning that summarizes it and is titled "An $800 Billion Revenue Shortfall Threatens AI Future, Bain says." Bain said "By 2030, AI companies will need $2 trillion in combined annual revenue to fund the computing power needed to meet projected demand in its annual Global Technology Report" released today. "Yet their revenue is likely to fall $800 billion short of that mark as efforts to monetize services like ChatGPT trail the spending requirements for data centers and related infrastructure, Bain predicted."

Chairman of Bain's global technology practice said "If the current scaling laws hold, AI will increasingly strain supply chains globally." The report dives into other areas of tech like quantum computing, humanoid robots and others too so let's get our hands on this report.

I've argued here that US tech has a competitor now the likes they have never seen and that is China. Putting aside our enabling of it in part because we inhibited their access to our best technology, Bloomberg News also has an interesting piece today titled "Huawei Plans Three-Year Campaign to Overtake Nvidia in AI Chips." It said "Huawei on Thursday took the rare step of publicizing a three-year vision for eroding Nvidia's dominance in the AI boom." Doubt China's capabilities at your own risk.

I bring this all up to again just have us challenge conventional wisdom and as market investors/participants we should always be watching our back.

The great thing about hearing from Fed members in the week after a meeting is we can associate the personalities with their dots. On one end of the dovish/hawkish spectrum, I'm guessing it was non voter member Beth Hammack of the Cleveland Fed that did not want to cut rates as she said "I think that we should be very cautious in removing monetary policy restriction. It worries me that if we remove that restriction from the economy, things could start overheating again." She thinks policy is only "very mildly" restrictive and "I'm really worried about what's going on with inflation" and less so with the labor market.

On the complete other hand, Fed Governor Stephen Miran is all in with his econometric models as he laid out all his computer driven math yesterday and he thinks the fed funds rate right now should be between 2-2.5% which would thus give us a negative real rate. On one hand he criticized the previous actions of a very activist Fed but on the other hand he wants to perform his own activism by voting for three 50 bps cuts in three meetings and then quickly taking it even lower. In such a condensed period of time of wanting to do this, that's some real Fed activism and he's clearly willing to roll the dice that inflation doesn't flare up in response.

I'm of the belief that humility should be a key characteristic of a central banker and similar to a head coach of a football team, each game (or Fed meeting) should be the focus and they should not be looking to the next 'game' six weeks later until we get there. Also, I'm old school but continue to believe, with decades of financial historical evidence in hand, that the best monetary policy is one that is stable itself and has the fed funds rate above the rate of inflation. We can all debate what that REAL rate should be but the further one away is from the arbitrary 2% target, the higher that REAL rate should be. Miran of course disagrees with me on all of this except we both agree that the Fed shouldn't be in the game of credit allocation towards specific industries, like housing via MBS holdings.

In between the two, voting member Alberto Musalem was kind of covering all his bases by saying "Should further signs of labor market weakness emerge, I would support additional reductions in the policy rate, provided the risk of above target inflation persistence has not increased and longer term inflation expectations remain anchored."

Non voting member Raphael Bostic in an interview with the WSJ doesn't want any more rate cuts this year after the one given last week which he was on board with. "I am concerned about the inflation that has been too high for a long time. And so I today would not be moving or in favor of it, but we'll see what happens." On the labor market he "doesn't believe that the labor market is in crisis right now" and "It's an open question about exactly how weak it is." On inflation and the pass through of tariffs, "The full story has not been told in terms of how the change in their cost basis is going to reveal itself into the final goods process."

Moving on to this continued rise in gold, which we remain long and bullish but acknowledging a correction could come at any moment. I mentioned yesterday the stats where foreign investors in US assets are more and more hedging their dollar exposure. It is also reflective that non dollars are what they want and gold is the ultimate non dollar asset. I want to highlight silver again as while we heard about gold reaching its 1980 inflation adjusted peak, silver would have to go to $200 in order to achieve that and is still below its nominal high of about $50. We remain bullish and long too of platinum.

Gold

Some September PMI's are coming out today. Australia's composite index weakened to 52.1 from 55.5 with both components lower. India's slipped to a still strong 61.9 from 63.2.

The Eurozone composite index rose to 51.2 from 51 though was mixed as manufacturing fell back below 50 at 49.5 from 50.7, offset by services which rose to 51.4 from 50.5. S&P Global said, "The outlook for manufacturing is looking a bit cloudy. Production is still growing, but the pace is being dragged down by France, where the government shake-up in early September likely threw a wrench into companies' production plans. Apart from this, hopes for an acceleration in growth are not justified as new orders have dropped significantly in both Germany and France. In the medium term, higher defense spending could drive up demand for industrial goods." Other fiscal spending from Germany could help too.

The UK PMI fell to 51 from 53.5 with manufacturing at just 46.2 vs 47 while services dropping to 51 from 53.5. Also, with regards to the outlook for the coming 12 months, "The degree of confidence slipped to its lowest since June, reflecting falling optimism across the service economy. Service providers noted challenging economic conditions, squeezed budgets among clients and heightened business uncertainty. However, manufacturers were the most upbeat since February."

Finally overseas, the Swedish Riksbank cut its benchmark rate by 25 bps unexpectedly to 1.75% but said that's it "for some time to come." For reference, their August CPI ex fuel was up 2.9%. Rolling the dice with inflation. The Swedish Krona is higher on the stated pause.

BY Doug Kass · Sep 23, 2025, 8:19 AM EDT

From Bramo:

I couldn't agree more!

BY Doug Kass · Sep 23, 2025, 8:05 AM EDT

No all clear, here:

BY Doug Kass · Sep 23, 2025, 7:55 AM EDT

From JPMorgan:

US: Futs are flat with bond yields 1-2bps lower as the yield curve shifts lower; USD is flat. Pre-mkt, Mag7 names are mixed as Semis have a slight bid. BA is +2.3% on a potential order stemming from US / China trade talks. Cmdtys are mixed with crude and precious leading; gold +90bp as China moves to custody gold similar to NY Fed. OECD hikes global growth estimate for FY25 from 2.9% to 3.2% with US growth est. moving from 1.6% to 1.8% and 1.5% for FY26. OECD also predicts that the full impacts from tariffs have yet to be felt. The macro data focus is on Flash PMIs and regional Fed activity measures.

and..

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

This market momentum, in the face of negative seasonality has many clients bulled up and so several conversations yesterday focused on what could derail this bullish run. My favorite response was “an asteroid hitting the earth”. In yesterday’s Morning Briefing, we flagged the biggest risks into year-end are (i) exhaustion of the AI theme / general TMT profit-taking; (ii) a spike in hiring (use U.3 and U.6 unemployment as a proxy rather than NFP) that results in accelerated spending; (iii) extended volatility / spike in bond yields potentially from a stronger growth outlook; (iv) an escalation in the trade war. Let us know your thoughts!

Shifting back to bullish thinking, our colleague Gui Infante tells us, “The market keeps pushing ahead as we remain above the late April upward trend line. Every sale is seen as a buying opportunity. Gold and Silver also doing well. The market seems to be removing negative tail risk scenarios and momentum is the best performing sector. Significant support should be expected around 6500 level for the SPX as we enter the choppy seasonality of late September. Expect a very positive 4Q.”

BY Doug Kass · Sep 23, 2025, 7:45 AM EDT

BY Doug Kass · Sep 23, 2025, 7:35 AM EDT

I initiated a starter position long Kenvue KVUE this morning in the premarket.

Tylenol-maker Kenvue shares bounce, Trump claims face pushback | Reuters

More later.

BY Doug Kass · Sep 23, 2025, 7:25 AM EDT

BY Doug Kass · Sep 23, 2025, 7:10 AM EDT

BY Doug Kass · Sep 23, 2025, 7:00 AM EDT

BY Doug Kass · Sep 23, 2025, 6:45 AM EDT

* Call for...

BY Doug Kass · Sep 23, 2025, 6:35 AM EDT

BY Doug Kass · Sep 23, 2025, 6:25 AM EDT

BY Doug Kass · Sep 23, 2025, 6:15 AM EDT

The S&P Short Range Oscillator is at 1.16% vs. 1.37% — that is close to neutral.

BY Doug Kass · Sep 23, 2025, 6:05 AM EDT

BY Doug Kass · Sep 23, 2025, 5:55 AM EDT

BY Doug Kass · Sep 23, 2025, 5:45 AM EDT