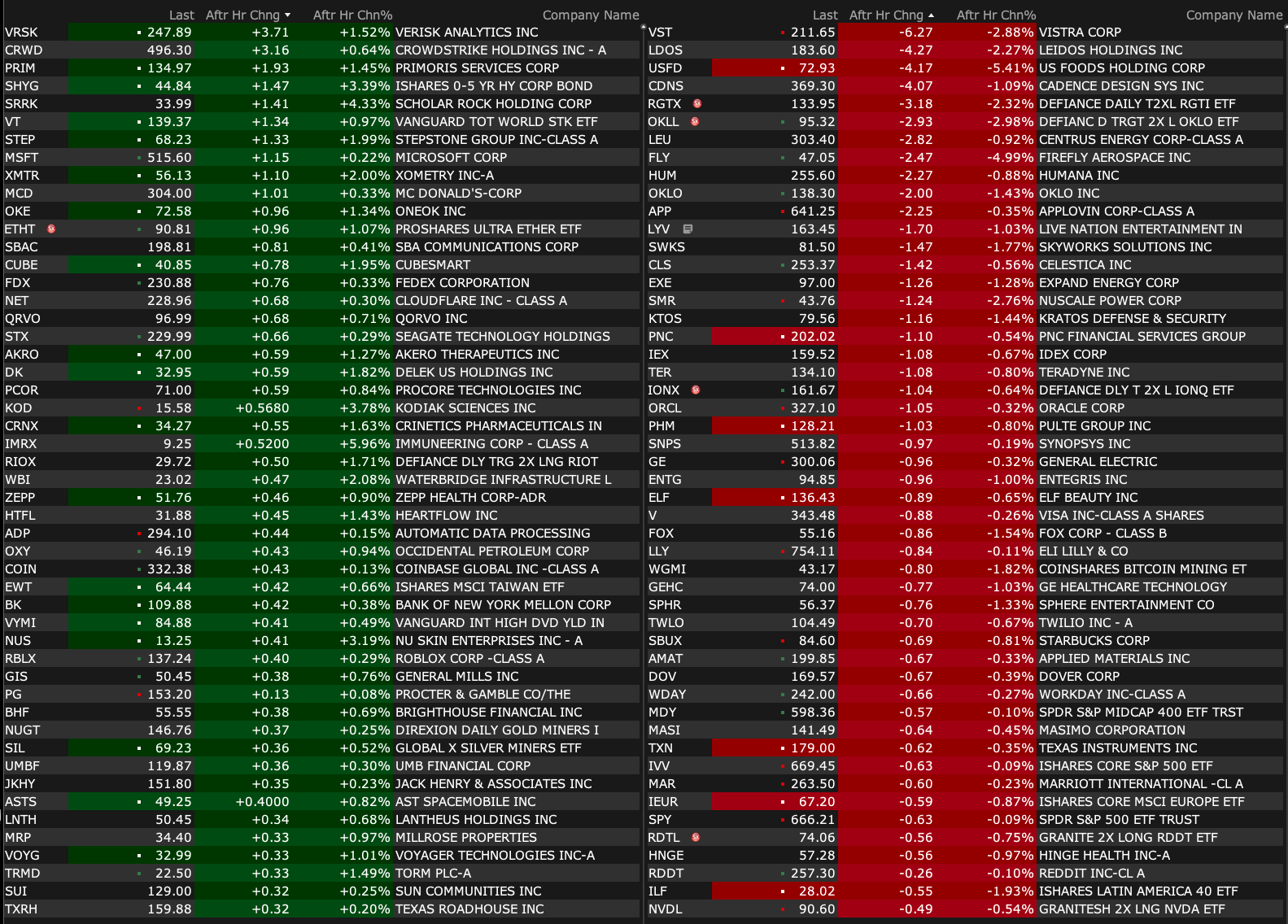

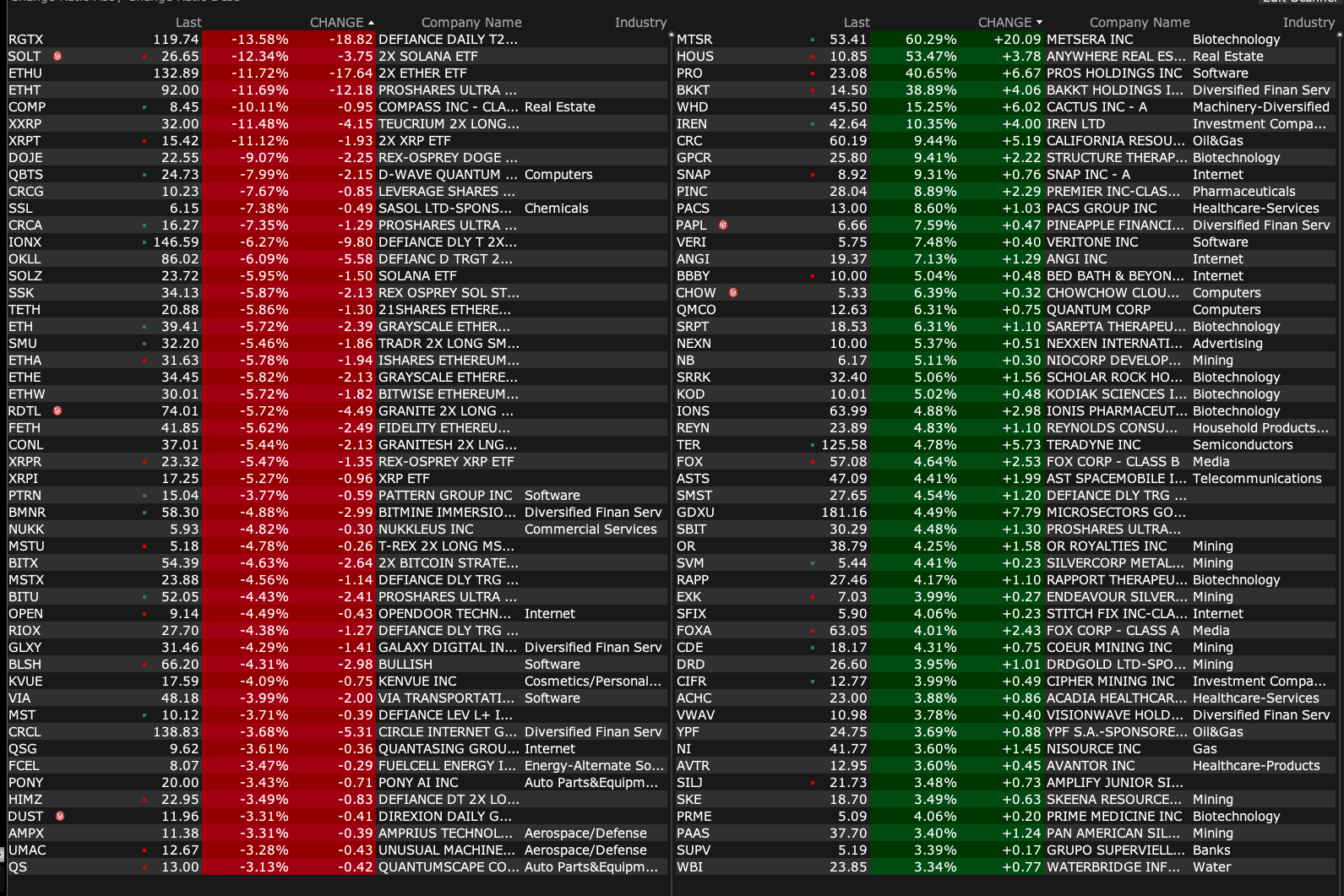

Monday's After-Hours Movers

As of 4:20 p.m.

BY Doug Kass · Sep 22, 2025, 4:40 PM EDT

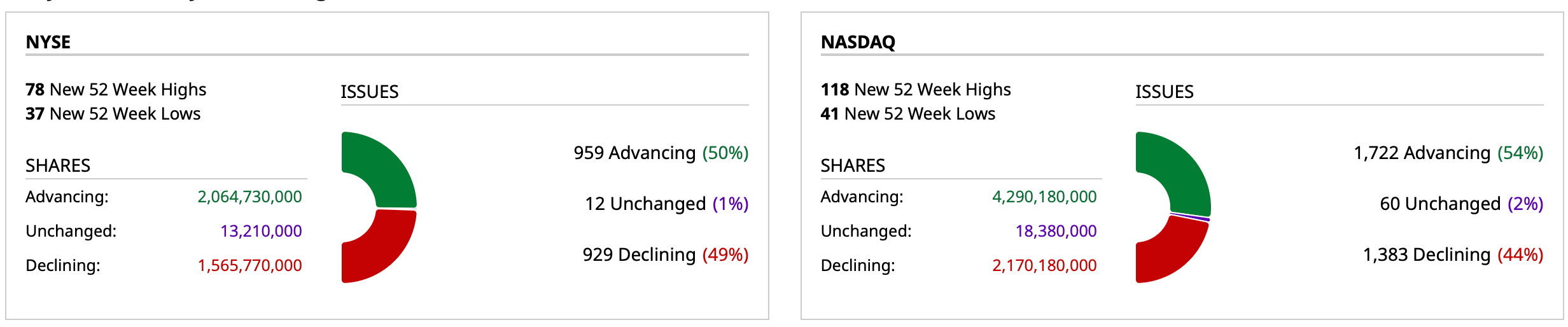

As of 4:20 p.m.

BY Doug Kass · Sep 22, 2025, 4:40 PM EDT

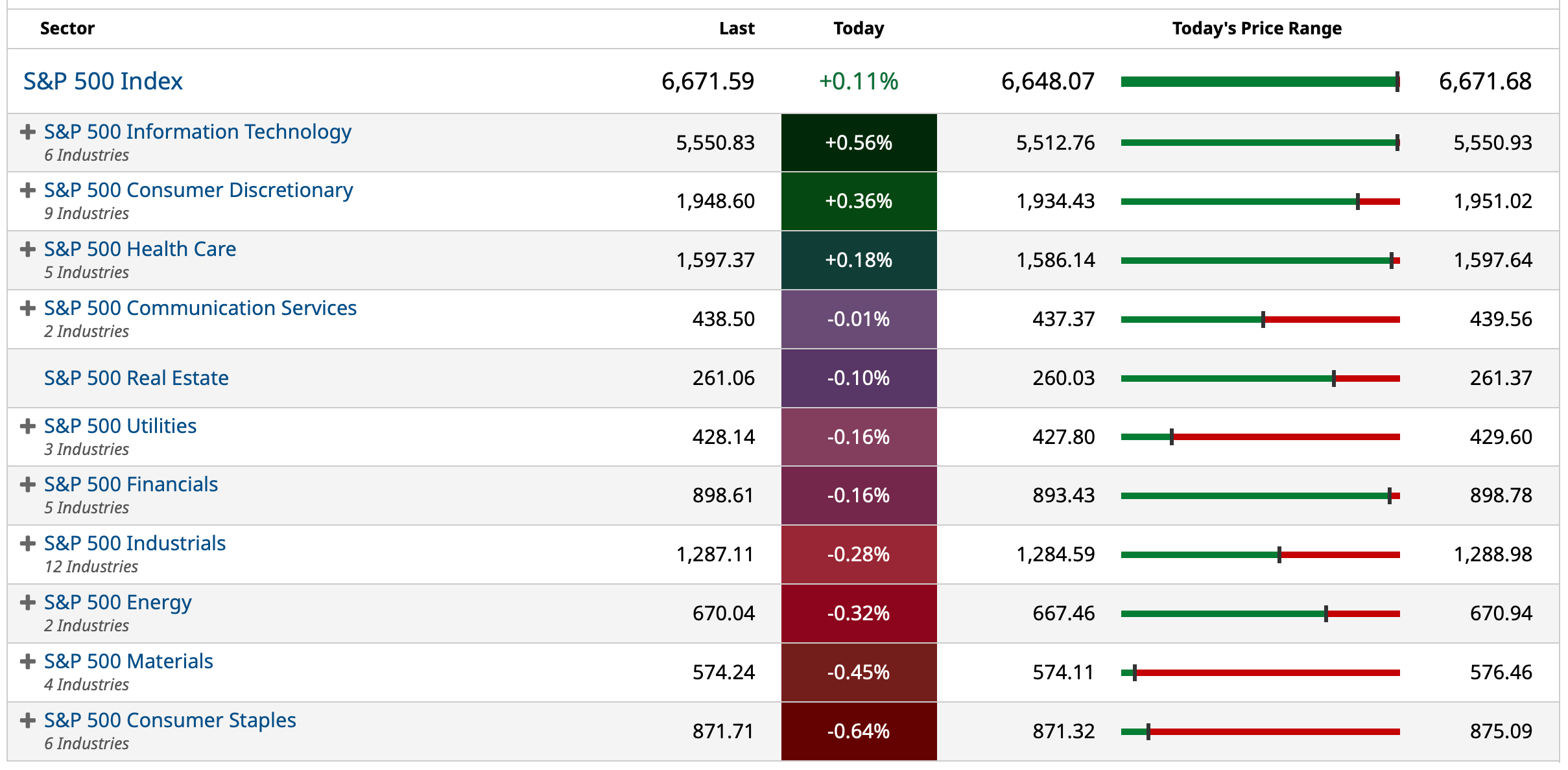

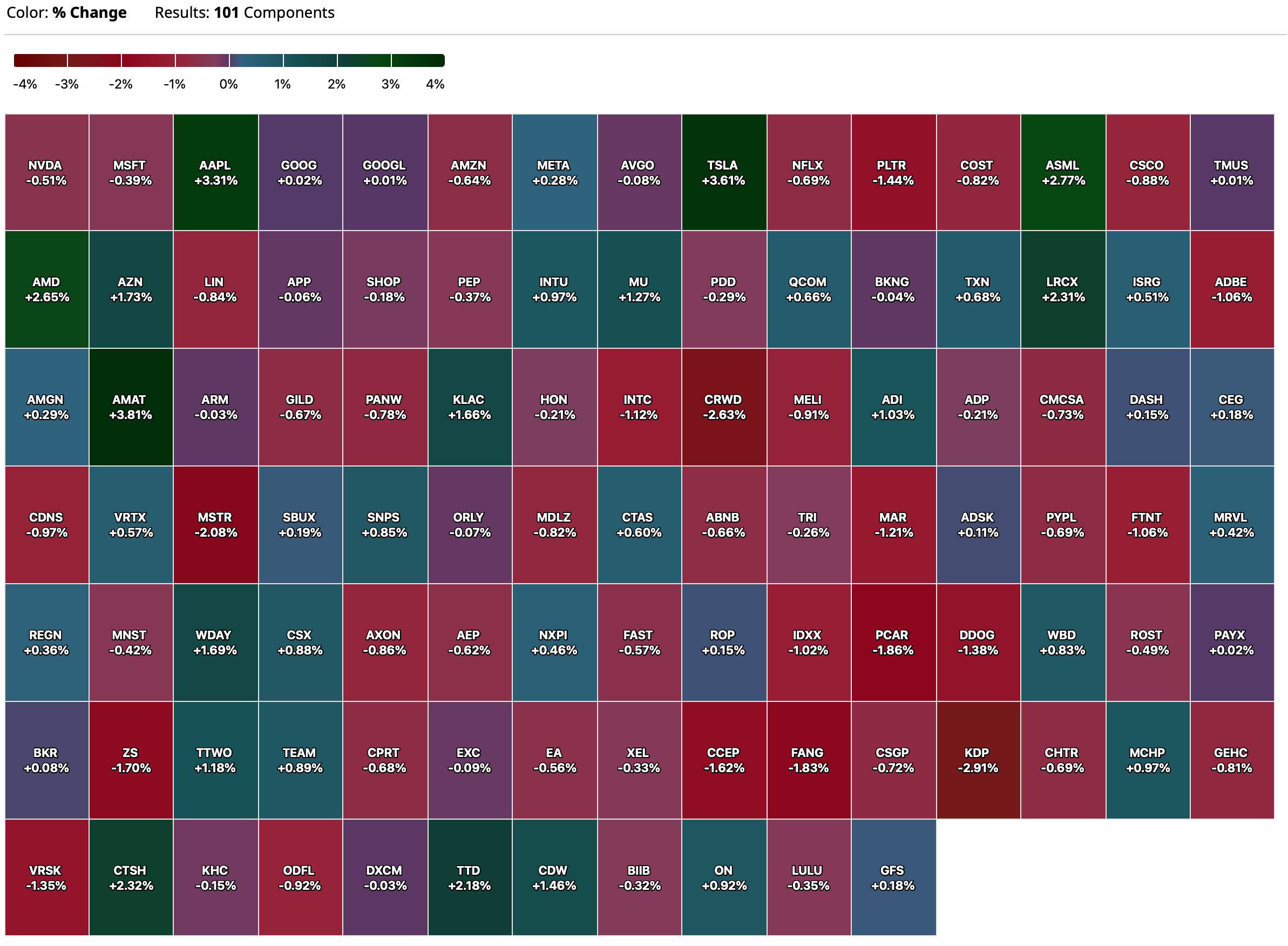

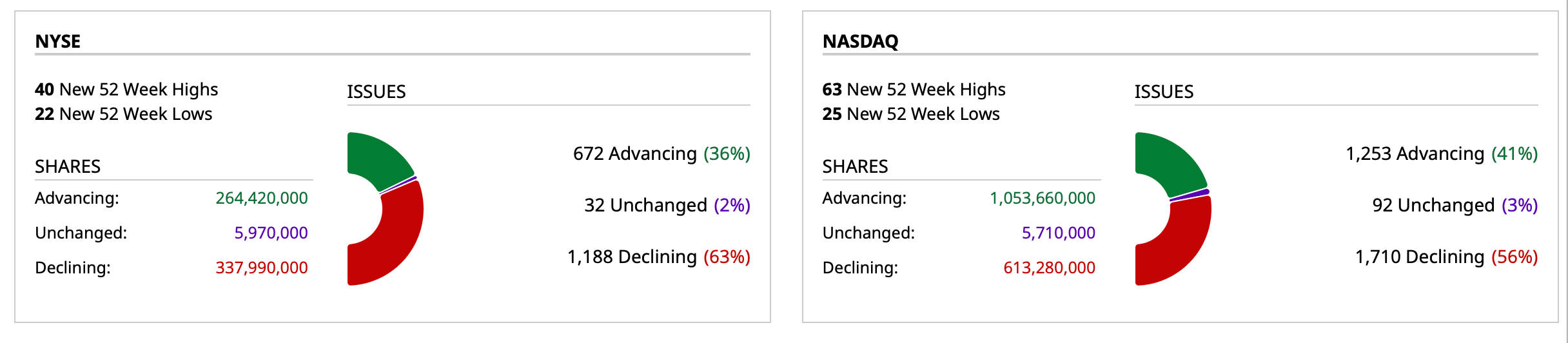

- NYSE volume 18% above its one-month average;

- NASDAQ volume 11% above its one-month average;

- VIX index: up 4.08% to 16.08

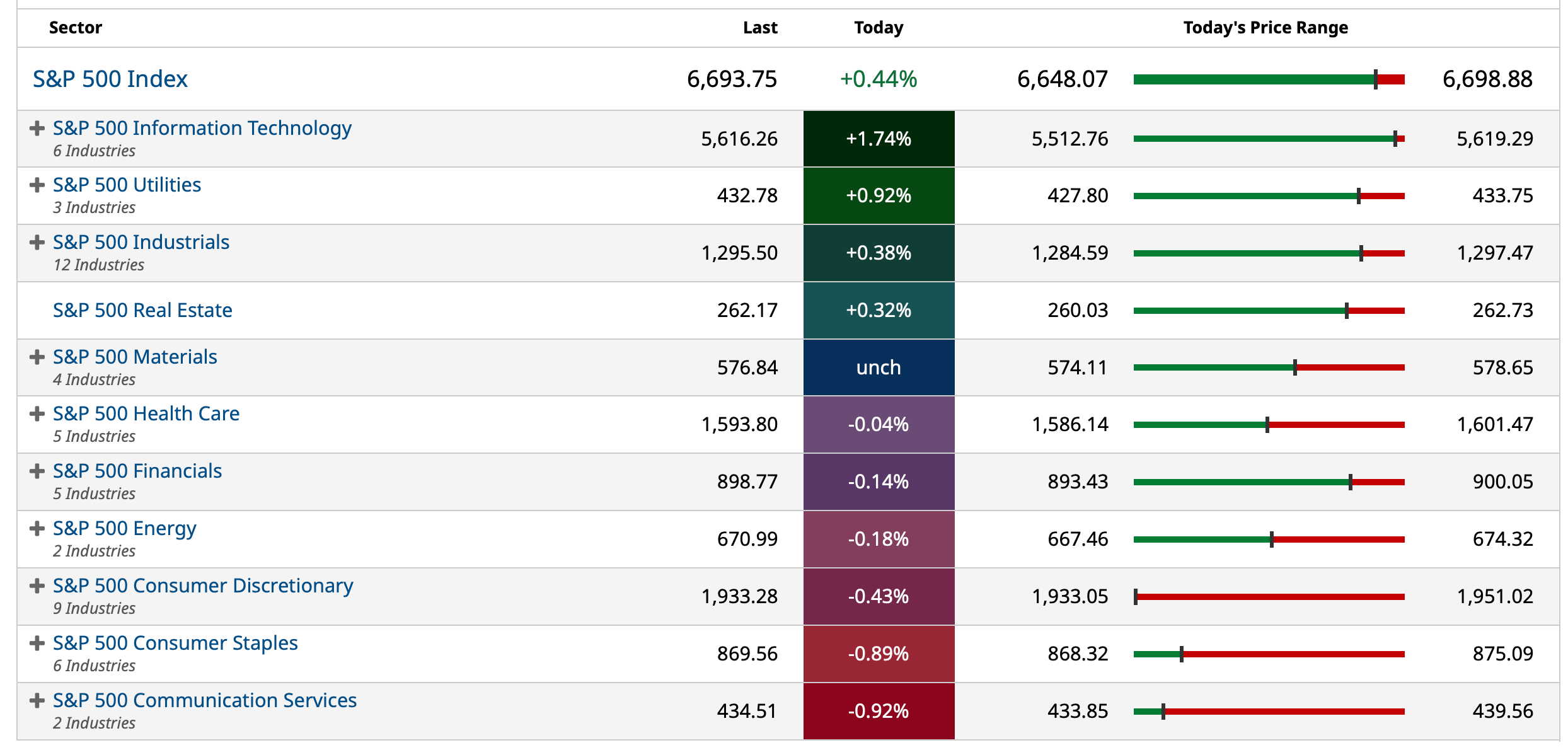

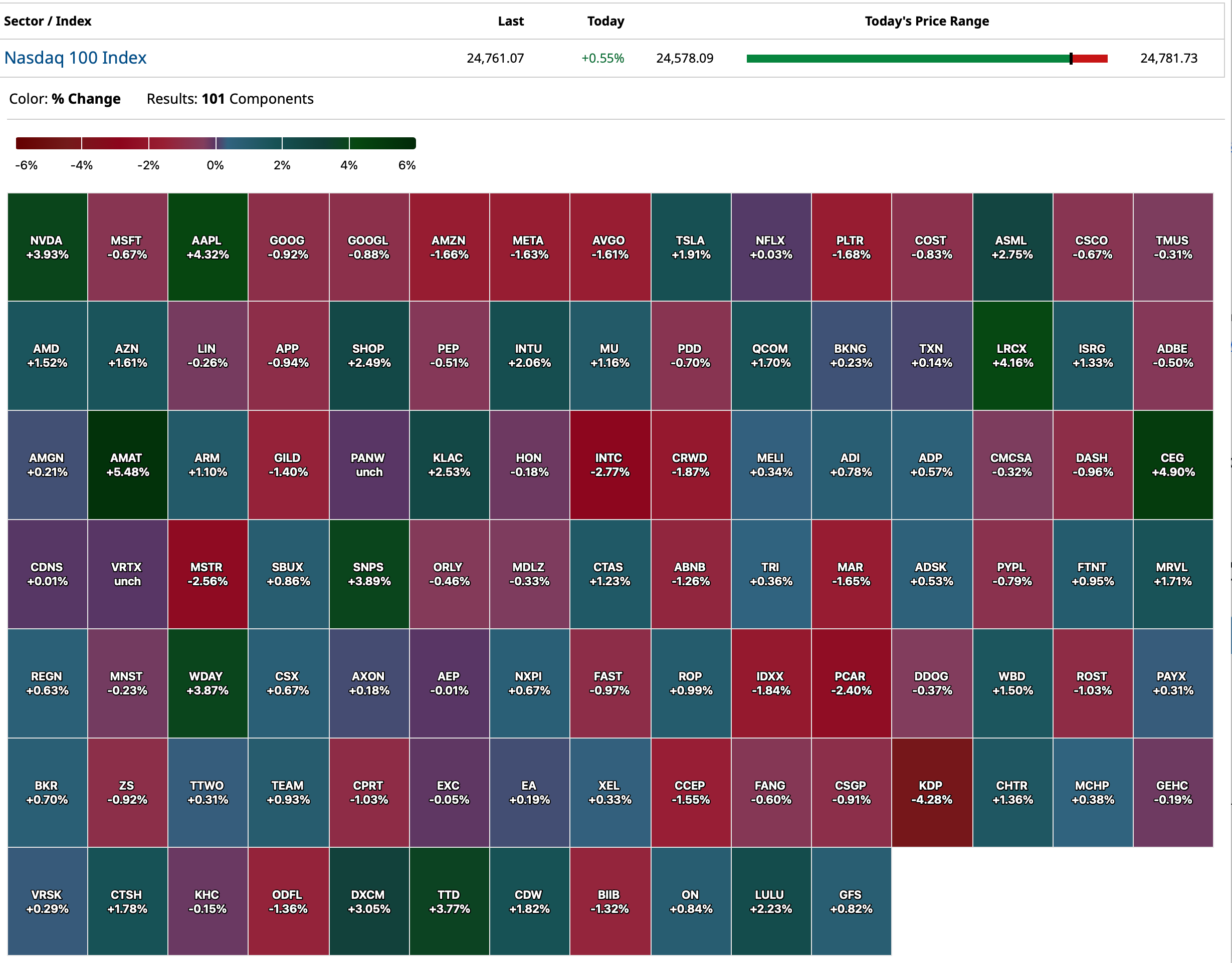

BY Doug Kass · Sep 22, 2025, 4:24 PM EDT

BY Doug Kass · Sep 22, 2025, 3:11 PM EDT

BY Doug Kass · Sep 22, 2025, 2:56 PM EDT

I am shorting more JPMorgan Chase JPM ($113.10):

* Overbought (and high RSI)

* Not the beneficiary of AI

* Trades near 3x tangible book value (something it hasnt done in several decades)

* Jamie Dimon is a seller

BY Doug Kass · Sep 22, 2025, 2:28 PM EDT

BY Doug Kass · Sep 22, 2025, 1:21 PM EDT

BY Doug Kass · Sep 22, 2025, 12:34 PM EDT

I am catching up on some research calls today — both will take about thirty minutes.

At noon, 2 PM and 3 PM.

BY Doug Kass · Sep 22, 2025, 12:09 PM EDT

BY Doug Kass · Sep 22, 2025, 11:10 AM EDT

This morning the homebuilder stocks (down big) are in conflict with the rally in equities.

BY Doug Kass · Sep 22, 2025, 10:45 AM EDT

With S&P cash -3 handles I am adding to index shorts:

* SPY $663.47

* QQQ $599.34

BY Doug Kass · Sep 22, 2025, 10:09 AM EDT

* Added to PEP long at $140.32.

* Added to JPM short at $112.34.

BY Doug Kass · Sep 22, 2025, 9:48 AM EDT

From The Street of Dreams

From JPMorgan:

US: Futs are weaker after SPX / NDX closed at ATHs on Friday. Bond yields flat with USD slightly weaker. Pre-mkt, Mag7 names are lower ex-AAPL, TSLA; NVDA is -88bp dragging Semis lower as we start the week with a slight defensive tone. In cmdtys, precious metals are the upside standouts with Gold +1%, Silver +1.5% with crude flat and Ags mostly weaker. This week’s macro data is not expected to be market-moving but there are 16x Fedspeakers this week including 4 today. Keep an eye on the yield curve where Jay Barry and team like tactical shorts in the 10Y, which may pressure Equities into quarter-end.

and...

We closed the week at ATHs for SPX and NDX as RTY sits 77bps below its ATH. The question is what’s next? We think higher and maintain our Tactical Bullish call, thinking that stocks have a shot at hitting 7,000 by year-end. That said, we may see some choppiness along the way, first from a combination of quarter-end rebalancing then around earnings, and finally with the macro releases. We feel any pullback should be bought into year-end. The biggest risks into year-end are (i) exhaustion of the AI theme / general TMT profit-taking; (ii) a spike in hiring (use U.3 and U.6 unemployment as a proxy rather than NFP) that results in accelerated spending; (iii) extended volatility / spike in bond yields potentially from a stronger growth outlook; (iv) an escalation in the trade war.

· MONETIZATION MENU – We like bullish Cyclical plays (esp. Consumer and Financials) to outperform alongside Small-Caps as we see further short covering so our High Short Interest basket (JPTASHTE Index) could be added, too. It makes sense to push TMT holdings to maximum levels. For those looking for laggards, Healthcare could be another profitable long given its earnings prowess, overly negative pricing of news from OBBBA, low positioning, and a potential boost from M&A. The USD weakness makes EM an attractive long, where we have preference for China (esp. China Tech) and Latam. For a tactical hedge, consider VIX calls / call spreads or VXX longs.

· PREVIOUS MENU – is similar to the above but we had suggested reducing a TMT OW to something closer to Neutral. We were wrong on this thinking. While we are aware of the risks from valuation and commentary around AI exhaustion, it feels like the actual spend and ‘AI arms race’ between the US and China will keep this trend in play and among the top performing themes.

BY Doug Kass · Sep 22, 2025, 9:45 AM EDT

-MBX +128% (once-Weekly Canvuparatide Achieved Primary Endpoint in Phase 2 Trial with 63% Responder Rate at 12 Weeks; 79% Responder Rate at 6 Months in Open-Label Extension; Preparation underway to initiate Phase 3 trial in 2026)

-MTSR +62% (Pfizer confirms to acquire Metsera at $47.50/shr for EV of $4.9B plus possible milestone payouts of up to $22.50/shr)

-HOUS +56% (reportedly to be acquired by Compass for $1.6B)

-BKKT +41% (appoints Mike Alfred to Board of Directors)

-PRO +40% (to be acquired by PE firm Thoma Bravo at $23.25/shr cash)

-ODP +33% (to be acquired by Atlas Holdings at $28/shr in cash in ~$1.0B all-cash transaction)

-SMLR +28% (announces Bitcoin treasury merger with Strive, Inc, in all-stock transaction)

-DGNX +22% (momentum)

-IREN +9.7% (targets Q1 2026 AI Cloud ARR $500M)

-PINC +8.5% (to be acquired by Patient Square Capital at $28.25/shr cash)

-SNAP +8.5% (meme trades, TikTok deal peripherals)

-VUZI +7.0% (achieves Waveguide Production Milestones and receives additional $5M Quanta Investment)

-BLNK +6.6% (Hubject teams with Blink Charging to expand intercharge network across N.A.)

-CCO +6.4% (reportedly Activist Anson pushing company to pursue a sale)

-ACTU +6.3% (provides FDA with Updated Clinical Data Package to Support Planned Regulatory Interactions with FDA and EMA over the coming months)

-IMNN +6.2% (presents IMNN-001 Phase 2 Translational Data in Advanced Ovarian Cancer Demonstrating 13-Month OS Extension via Tumor Micro-Environment Shift)

-BBBY +5.1% (announces dividend of warrant to shareholders)

-GDYN +4.0% (Jefferies Initiates GDYN with Buy, price target: $11)

-REYN +3.2% (to be added to S&P600 Index, effective Sept 24th)

-B +2.5% (broker raises price target on Nevada mine)

-EAT +2.4% (Wells Fargo Raised EAT to Overweight from Equal Weight, price target: $175 from $165)

-FLY +2.4% (receives $10M NASA Contract Addendum for Blue Ghost Mission 1 Lunar Data)

-FOX +2.1% (reportedly considering stake in TikTok)

-COMP -12% (confirms to merge with Anywhere Real Estate in $10B all-stock agreement)

-DFDV -4.5% (announces strategic collaboration with ZeroStack in treasury accelerator deal)

-KVUE -4.3% (weakness in anticipation of Trump Administration linking Tylenol to autism)

BY Doug Kass · Sep 22, 2025, 9:26 AM EDT

BY Doug Kass · Sep 22, 2025, 9:10 AM EDT

BY Doug Kass · Sep 22, 2025, 9:00 AM EDT

FED SPEAKERS:

9:45 a.m.: Fed Bank of New York President Williams (Voter) participates virtually in panel before the "Monetary Frameworks: Recent Developments and Outlook – An International Comparative View" event organized by the Bank for International Settlements, European Central Bank and SUERF, NYC (No text. Moderated Q&A expected);

10 a.m.: Fed Bank of St. Louis President Musalem (Voter) speaks on the outlook for the U.S. economy and monetary policy at the Brookings Institution, Washington, DC (In-person with virtual option. Other details TBA);

12 p.m.: Member of the Board of Governors of the Federal Reserve System Stephen Miran (Voter)speaks at the Economic Club of NY;

12 p.m.: Fed Bank of Richmond President Barkin (Non-Voter) speaks virtually on the economy before the Howard County (Maryland) Chamber of Commerce, Richmond, VA;

12 p.m.: Fed Bank of Cleveland President Beth Hammack (Non-Voter) speaks on "The Fed's Role in the Economy and Impact on Everyday Life" before a "Fed Talk" event, Cleveland, OH (No text. Audience Q&A expected)

TREASURY AUCTION:

11:30 a.m.: Treasury hosts an $82B 3 and a $73B 6-Month Bill Auction

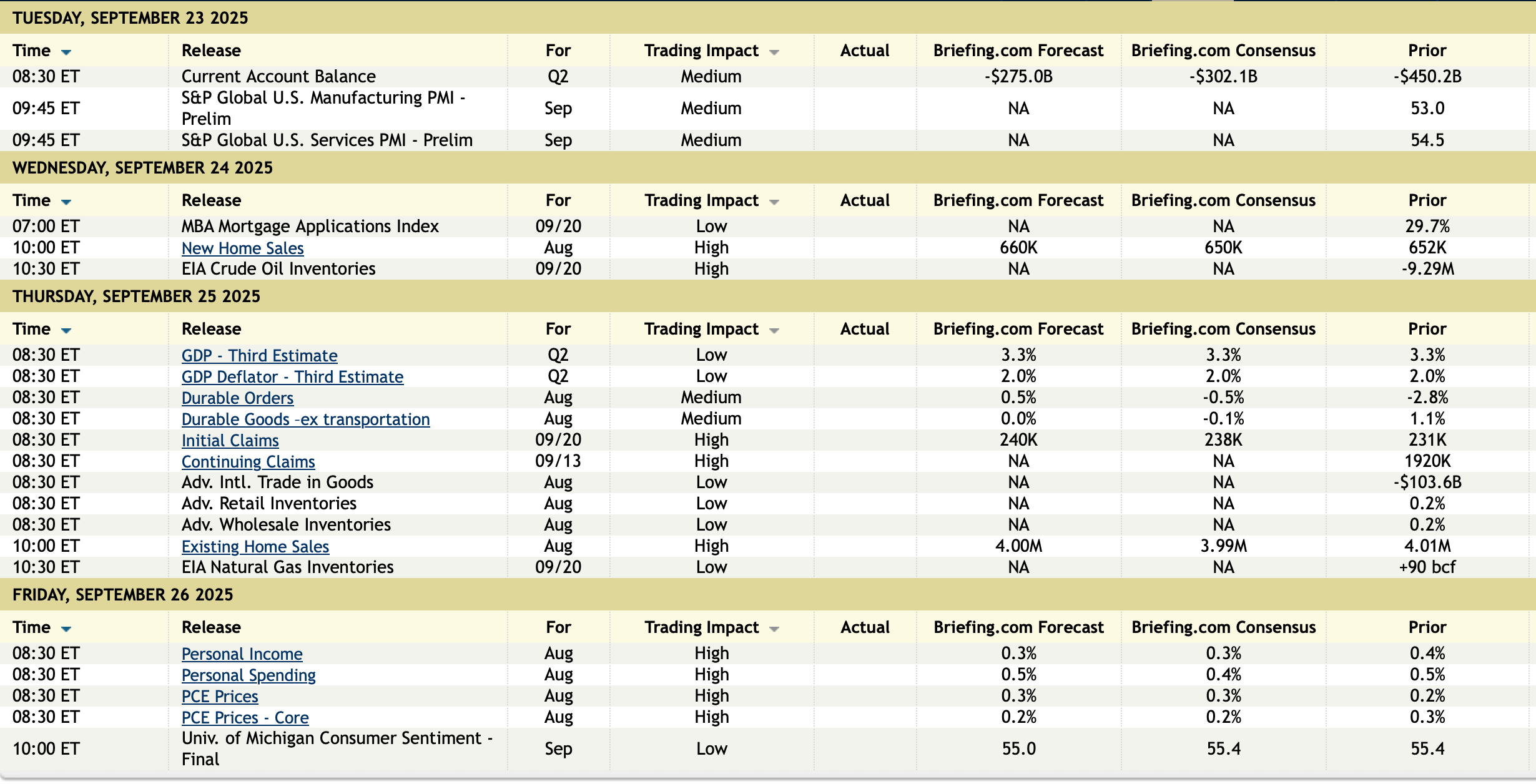

ECONOMIC CALENDAR FOR REMAINDER OF THE WEEK:

BY Doug Kass · Sep 22, 2025, 8:50 AM EDT

From Peter Boockvar:

The S&P 500 bottomed in March 2009 at 666. On Friday we touched 6666. What an amazing, incredible, bizarre, long, strange trip it's been.

If you, like me, always are trying to test conventional wisdom and your own beliefs, especially as a money manager of other people's money, I recommend a read of this, gqg.com/insights/dotcom-on-steroids/ that I read over the weekend.

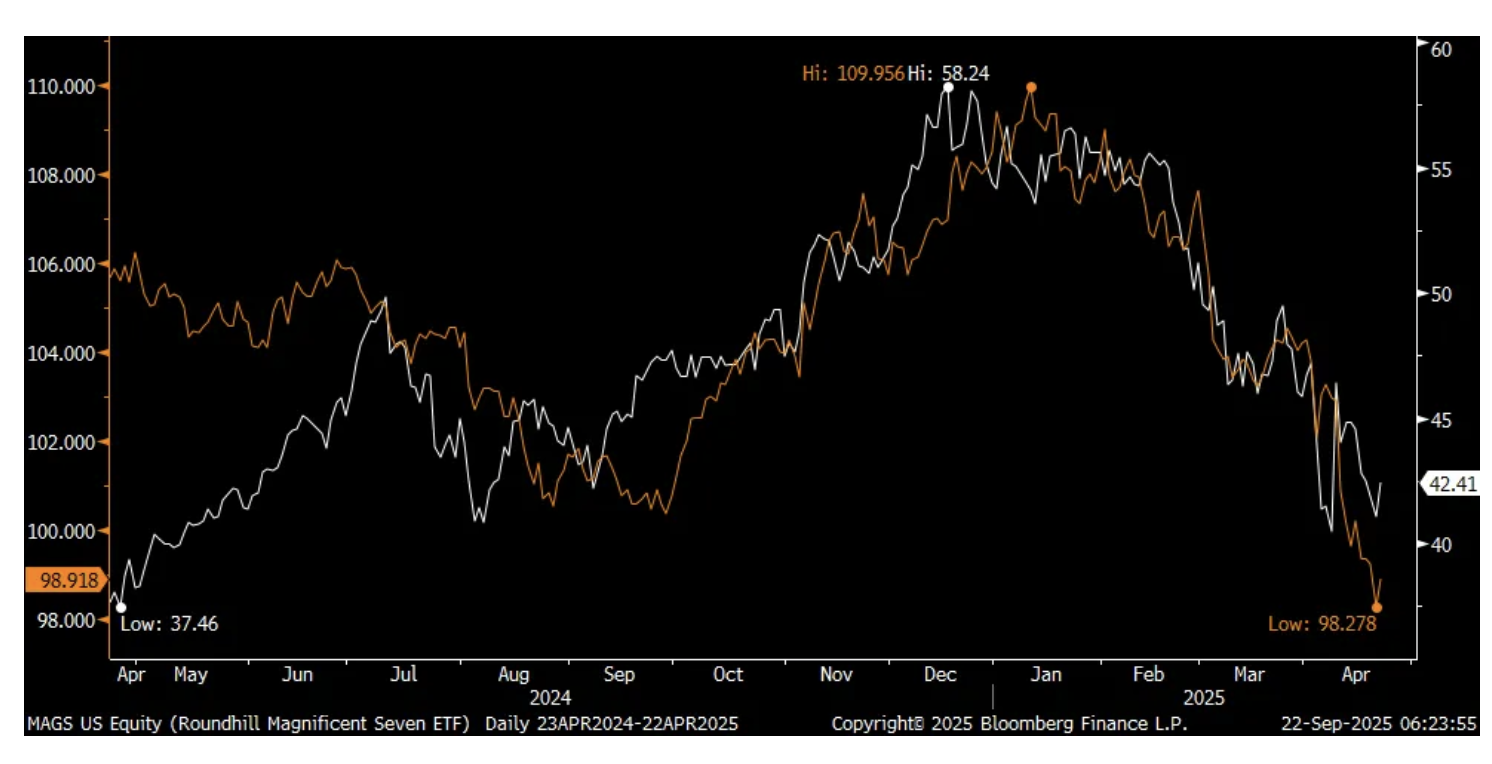

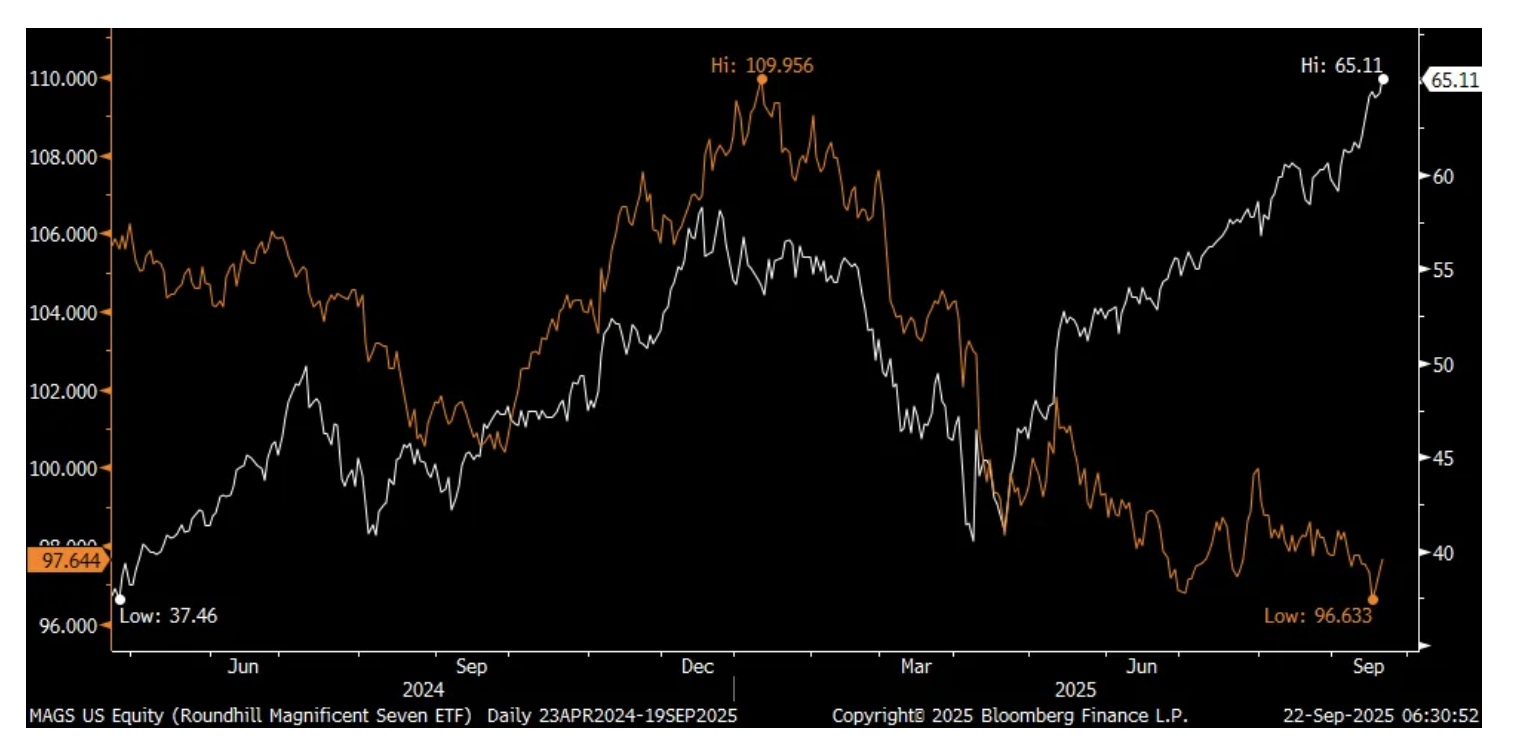

Back in April when the tariff news/noise reached its pinnacle on April 2nd, I included here a chart reflecting how the MAG 7 trade became not just a US domestic based investment love affair, the stocks also became a foreign reserve asset in the 12 months leading into April and there was a tight relationship between the MAG 7 and the US dollar index. The first chart includes that time frame.

The second chart reflects what has happened since as the MAG 7 trade got a second wind but the US dollar still can't get out of its own way. I have one explanation based on what I'm reading. Foreigners continue to hold/buy US big cap tech stocks but now they are hedging their US dollar exposure in a growing, notable way. In the weekend FT article titled "Dollar is taking hit from foreign investors' US fears" it quotes George Saravelos from Deutsche Bank who said "foreign investors are now removing dollar exposure at an unprecedented pace." The piece went on to say "Now hedged flows into US exchange traded funds are outweighing unhedged flows for the first time this decade. This switch is, he said, 'exceptionally stark' in stocks, where more than 80% of inflows are now hedged - an extraordinary run up from the start of the year, when the hedged portion was close to zero. But in bonds, too, the hedged tally is running at about half of the total." I bolded for emphasis.

ft.com/content/ac9e7ee1-ebe5-431a-a315-b833de728ec9

DXY in orange, MAGS etf in white (April 2024-April 2025)

Thru Friday, DXY in orange, MAGS etf in white

Many define the success or failure of tariffs on just whether there is more than a one time impact on inflation and how much money it's raising for the US government without debating the economic growth implications. There are major dislocations still with companies dealing with tariffs and last week 43 industry associations sent a letter to the administration on one piece of the tariffs, "expressing concern on steel, aluminum derivative expansion & inclusions process."

In the letter it said:

"We write to express concern over the Commerce Department's new Section 232 steel and aluminum "Inclusions Process" and the subsequent expansion of 50% tariffs on 407 Harmonized Tariff Schedule (HTS) codes comprising roughly $240 billion of imports. While we support the Administration's objectives of safeguarding national security and promoting American manufacturing, we urge the Department to eliminate further unpredictable expansions, provide comprehensive guidance, ensure a transparent stakeholder consultation process and make targeted determinations with a clear nexus to national security. The recent expansion was implemented without adequate notice and creates significant unintended costs, complexity, and uncertainty for US businesses."

"The sudden expansion of tariffs with limited industry consultation increases costs by generating significant compliance burdens for businesses of all sizes, including those that do not produce steel and aluminum products. Manufacturers account for more than half of all US imports, and these imports are very often products that are not available from domestic sources in sufficient quantities or supplied quickly enough to meet operational timelines. The harm to US employment among downstream producers of items now covered will ultimately be significant, including with respect to those that are key to powering critical industries and the broader US economy."

"In addition to the complex task of determining which types of tariffs apply to specific parts of goods, importers are now responsible for reporting information and value calculations that often extend well beyond Tier 1 suppliers and end manufacturers. This includes determining where the steel was melted and poured, where the aluminum was smelted and cast, the value and weight of the metals in the products, and the percentage of the value those metals represent...Any misstep or delay in reporting risks the imposition of a 50% tariff on the value of the entire product. For aluminum, the inability to trace sourcing results in a 200% tariff on the value of the entire product."

My point in bringing this up is that tariffs and its economic impact are still coursing through the economy and throwing mud in the gears of business activity. The success or failure of them should not be just defined by the inflationary impact or not and how much money the US is raising from them where the money is coming mostly from the US private sector.

BY Doug Kass · Sep 22, 2025, 8:29 AM EDT

BY Doug Kass · Sep 22, 2025, 8:12 AM EDT

BY Doug Kass · Sep 22, 2025, 7:55 AM EDT

What goes up must come down

Spinning Wheel got to go 'round

Talkin' 'bout your troubles

It's a cryin' sin

Ride a painted pony

Let the Spinning Wheel spin

- Blood Sweat and Tears, Spinning Wheel

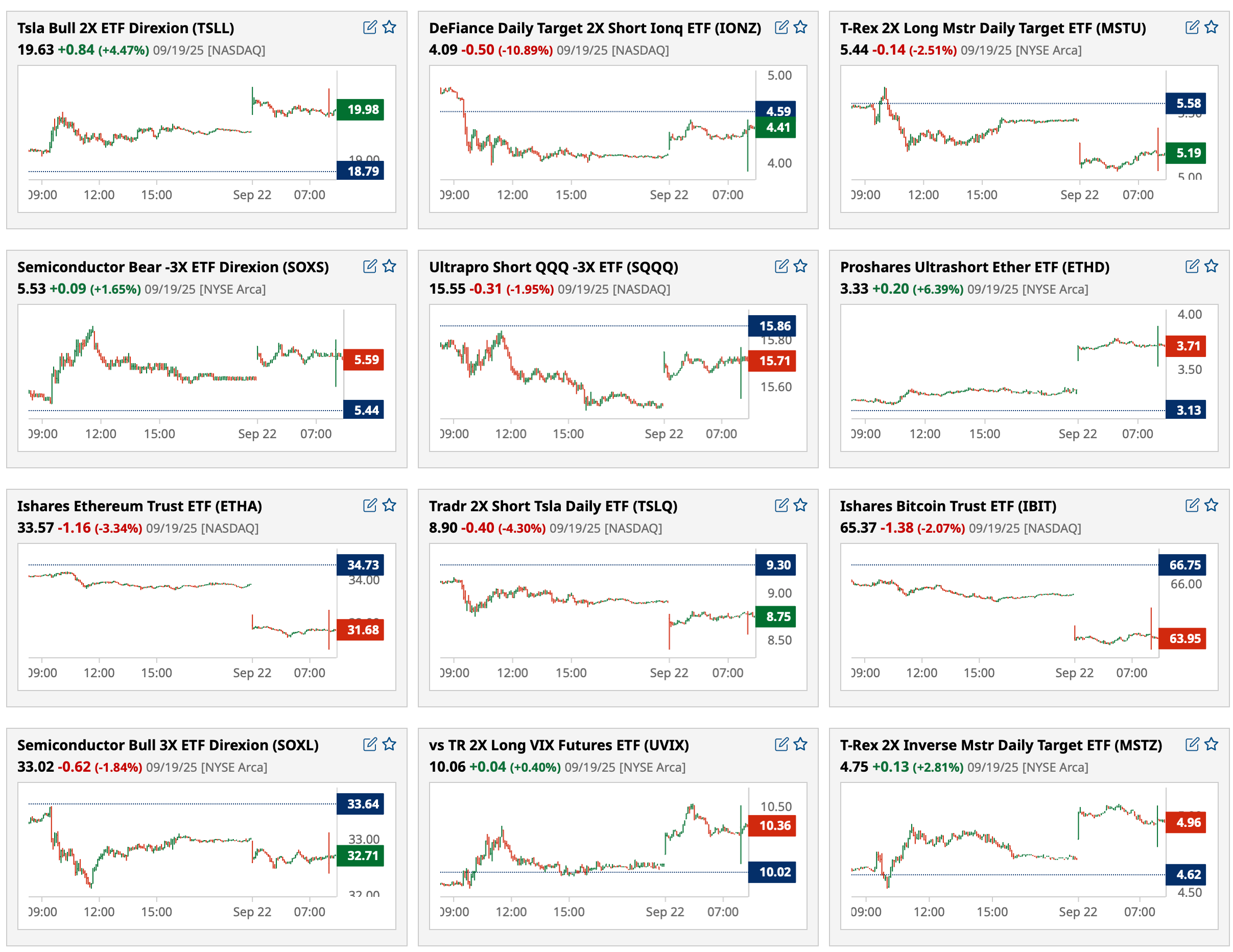

This morning ethereum is -7% (-$310) and bitcoin is down by nearly 3% (-$3,100).

One of my concerns (and potential catalysts for a market correction) is the leveraged crypto currency market — a market that is now favored by memesters, regular traders and investors and the current administration in Washington D.C.

There is an extraordinary amount of leverage in crypto — so much so that a quick price drop could weigh on other asset classes (like equities).

This underappreciated and potential trouble spot has been a continuing refrain from me (in my Diary) when I probe for non-traditional catalysts to a market swoon.

BY Doug Kass · Sep 22, 2025, 7:30 AM EDT

* A boycott of Disney+ and Hulu streaming is now joining the bonafide threats of AI and absurdly high theme park admission prices

* Look for reduced EPS expectations at Disney...and a likely lower share price

Besides ridiculously high theme park admission and lodging costs etc. — which hits the increasingly vulnerable middle class (a deteriorating jobs market nationally and sticky inflation relative to incomes) — Disney DIS now faces another challenge.

Regardless of one's political views, those that argue against the Jimmy Kimmel cancellation have mounted an effort to cancel Disney+ and Hulu streaming memberships and, even, to cancel Disney theme park vacations.

I expect further pressure on Disney's shares in the time ahead and I would not be surprised (in a market correction) that the company's share price tumbles and creates an excellent entry point on the buy side.

But, the time to buy is not yet likely at hand. I would be patient on price with this popular and heavily institutionalized name.

I wrote this column about three weeks ago:

It's a world of laughter,

a world of tears

It's a world of hopes

and a world of fears

There's so much that we share

that it's time we're aware

It's a small world after all

It's a small world after all

It's a small world after all

It's a small world after all

It's a small, small world

- It's A Small World It's A Small World

This New York Times article on Disney underscores my concern about this popular but disappointing company and stock: Opinion | Disney World Is the Happiest Place on Earth, if You Can Afford It.

For some time I have viewed too steady and rapid escalation of theme park admission prices as a threat to consensus earnings per share expectations.

I have found that demand elasticity (read: weakening demand) would follow those admission price hikes over the fullness of time.

I still do.

This keeps me from buying this seemingly cheap stock.

By Doug Kass Sep 2, 2025 10:20 AM EDT

I wrote this article in August:

I recently purchased a very small starter position in Disney (DIS).

In a different era, I would be more aggressive.

But we live in the new (altered) world of artificial intelligence and I am increasingly concerned that AI could disintermediate both Disney's movie and its theme park business. (The latter — admission prices — being priced sky high into a likely consumer slowdown. Come to think of it, the same can be said of Disney's movie admission prices!)

I don't think many are thinking in these terms.

By Doug Kass Aug 11, 2025 1:45 PM EDT

BY Doug Kass · Sep 22, 2025, 7:00 AM EDT

BY Doug Kass · Sep 22, 2025, 6:25 AM EDT

BY Doug Kass · Sep 22, 2025, 6:15 AM EDT

Wolf Street howls about climbing mortgage rates after the Fed rate cut.

I expected this (rising intermediate-to longer-term rates) in my writings in my Diary over the last few months.

Higher interest rates translates into an ever thinner equity risk premium, which, historically, presages lower equity prices.

BY Doug Kass · Sep 22, 2025, 6:05 AM EDT

The S&P Short Range Oscillator has been lowered to 1.37% vs. 2.75%.

BY Doug Kass · Sep 22, 2025, 5:55 AM EDT

* I added to index shorts: SPY at $662.98 and QQQ at $598.51.

* I added to JPM short at $311.74 and WFC short at $84.64.

BY Doug Kass · Sep 22, 2025, 5:45 AM EDT