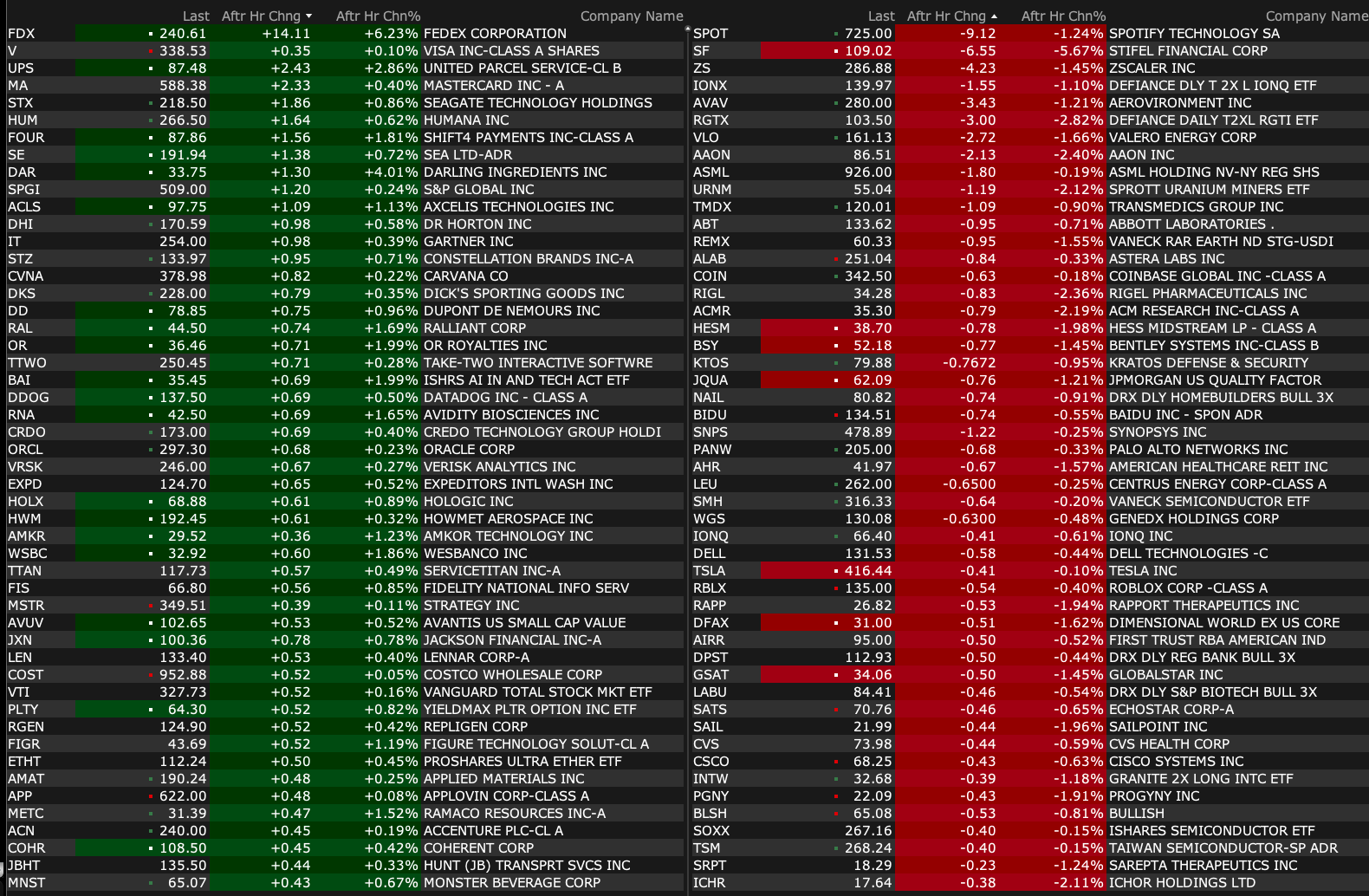

Thursday's After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Sep 18, 2025, 5:15 PM EDT

As of 4:22 p.m.:

BY Doug Kass · Sep 18, 2025, 5:15 PM EDT

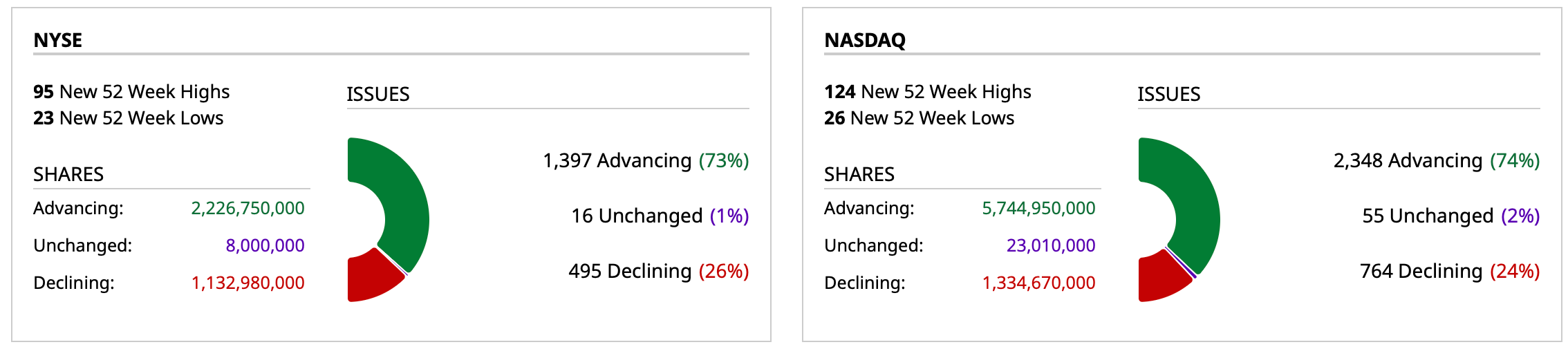

- NYSE volume 8% above its one-month average

- NASDAQ volume 25% above its one-month average

- VIX index: down 0.13% to 15.70

BY Doug Kass · Sep 18, 2025, 5:08 PM EDT

BY Doug Kass · Sep 18, 2025, 3:47 PM EDT

Over the last two days the rate on a fixed-rate mortgage has increased by +24 basis points.

BY Doug Kass · Sep 18, 2025, 3:22 PM EDT

BY Doug Kass · Sep 18, 2025, 2:30 PM EDT

BY Doug Kass · Sep 18, 2025, 1:20 PM EDT

*Heads investors win, tails investors win...

BY Doug Kass · Sep 18, 2025, 12:50 PM EDT

Senator Paul on hemp and cannabis.

BY Doug Kass · Sep 18, 2025, 12:03 PM EDT

Gaztama

Hi Doug, can you share some thoughts behind your PEP position?

Dougie Kass

the concerns with regard to snack vulnerability (from glp1) are well known and seemingly discounted in the current valuation

the elliott mgt recommendations - if incorporated - could buoy secular EPS growth

if pepsico mgt ignores elliott, i would not be surprised if other activists come to elliott's support

in a slow growth global economy, consumer non durables could be benefit of rotation out of cyclical areas

meanwhile, the dividend yield of close to 4% provides some support

more next week

from peter boockvar this morning:

"Within the S&P, the consumer food/product companies are getting really attractive I believe. They've been hammered and now have bond like dividend yields with equity like upside."

BY Doug Kass · Sep 18, 2025, 11:45 AM EDT

BY Doug Kass · Sep 18, 2025, 11:21 AM EDT

No trades today.

BY Doug Kass · Sep 18, 2025, 10:34 AM EDT

Per My Response to the FOMC Decision (below), as a clarifying point, I should have added that the Fed might have at least reduced their forecast for gross domestic product, increased it for unemployment, and potentially lowered it for inflation as well, to make their forecasts consistent with their actions on rates (and forward looking dot plot), particularly since inflation remains elevated.

The result was doublespeak and gobbledygook.

When I am in memory care (which the markets might drive me to!), I think I will be able to produce something more logically coherent.

Frankly, the AI, which after hundreds of billions of dollars of investment still hallucinates like it overdosed on ayahuasca and does not know who the president of the United States is, even when prompted, could do a better job:

Part of the problem is the Fed's lack of competence and judgement.

The other problem is we are in a pickle of significant proportions, which they (for decades) have enabled.

Unfortunately we all have to lie in the bed they made along with the political class.

From yesterday:

Well, I am not surprised, but this is still a new one to me.

With inflation (understated) at well above targeted levels and accelerating, the Fed is cutting rates, and projecting more rate cuts. At the same time as upgrading its growth forecast, lowering its unemployment rate forecast, and increasing its inflation outlook.

Make it make sense?

-- Growth: GDP forecasts raised for 2025, 2026 and 2027.

-- Employment: Unemployment rate forecast for 2025 unch, lowered for 2026 and 2027

-Inflation: PCE forecast for 2025 unch, raised for 2026, unch for 2027, Core PCE forecast for 2025 unch, raised for 2026 and unch for 2027

But the good news is their new projections show inflation finally returning to the 2% target in 2028. This is seven straight years of inflation exceeding targeted levels, and if done on a cumulative basis (area under the curve given the amount of excess inflation), it has exceeded targeted levels by a fair bit.

If the notion was that if inflation was under target for a period of time, it should go over target by a period of time to make up the difference, shouldn’t the same apply in reverse and we should be owed the same amount of under-inflation in return? Clearly, the answer is no, which it should be, because that would be a disaster. The problem is the notion of letting inflation run above targeted levels was also equally stupid.

Lots of IQ, for the most part. No common sense to go along with it as well.

Position: None

By Doug KassSep 17, 2025 3:16 PM ED

BY Doug Kass · Sep 18, 2025, 9:31 AM EDT

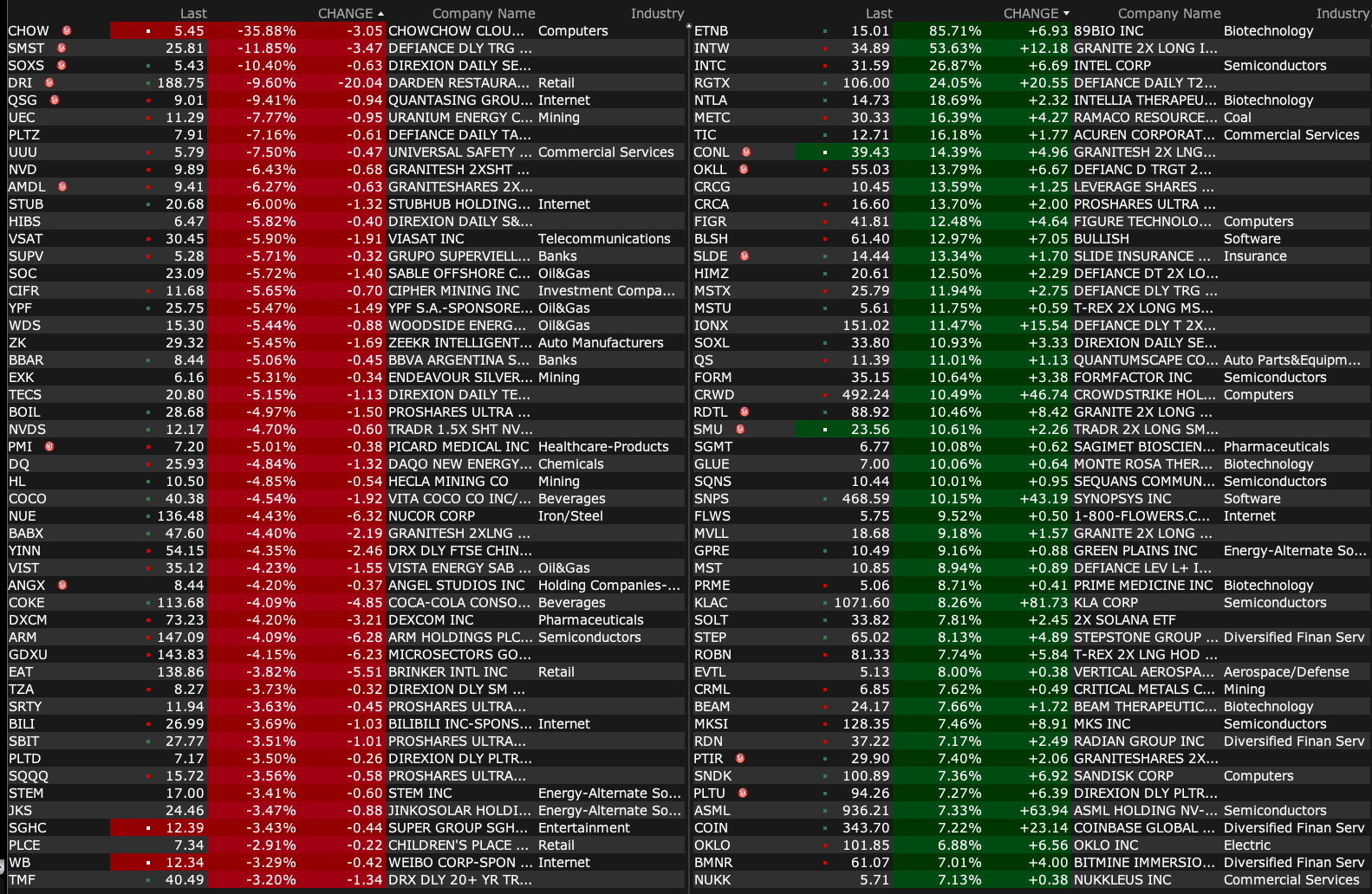

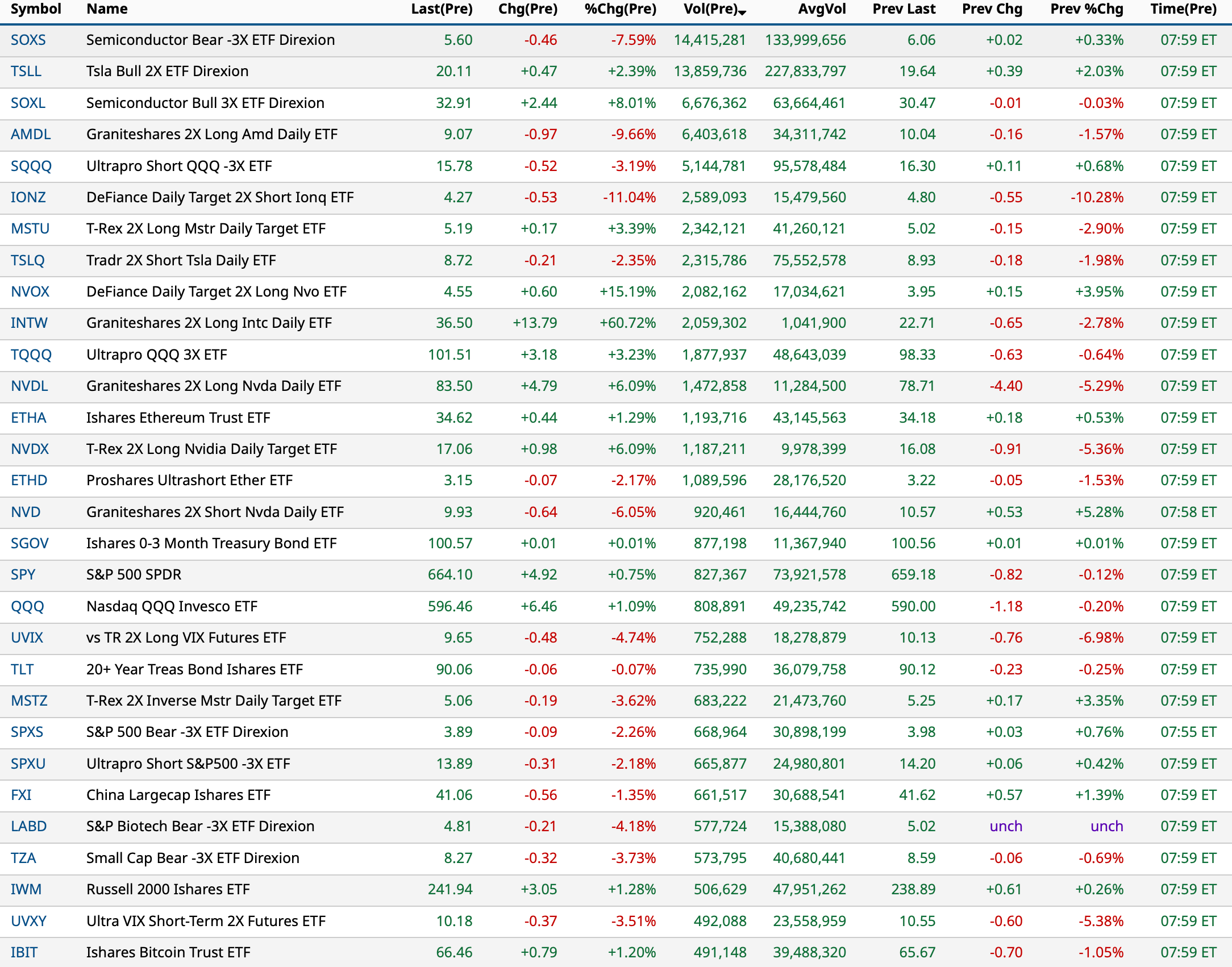

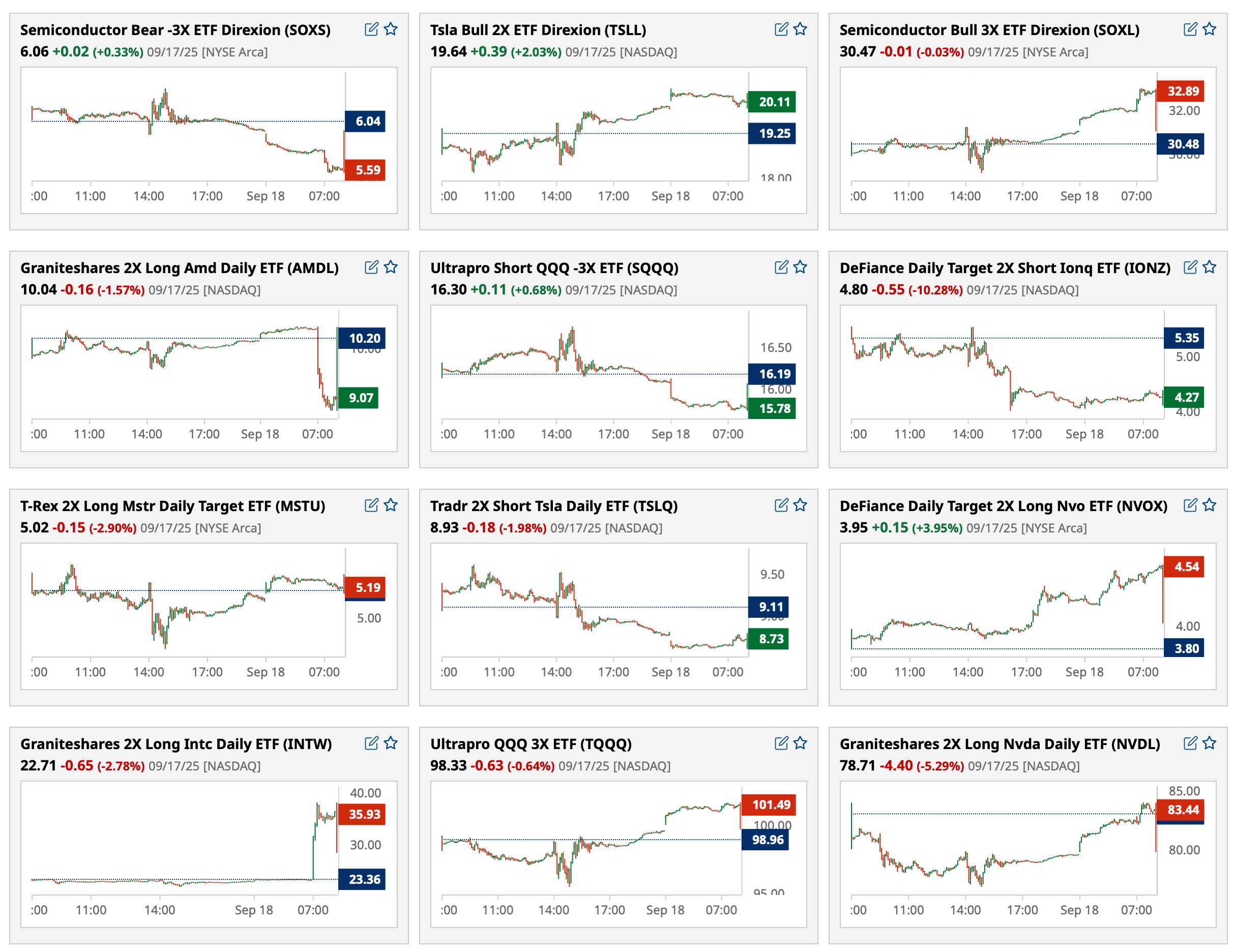

-INTC +29% (NVIDIA and Intel to develop AI infrastructure and personal computing products; NVIDIA to invest $5B in Intel common stock at $23.28/shr)

-PDSB +10% (sets Significant Benchmark in Head and Neck Cancer by Achieving Extended Survival in Low PD-L1 Expression (CPS 1–19) Cohort in VERSATILE-002 Trial, Potentially Eliminating Need for Chemotherapy in the Population)

-BLSH +8.3% (earnings, guidance)

-BLBX +7.7% (signed MOU for long-term offtake, giving REalloys access to up to 40% of Araxá Project’s rare earth production in Brazil)

-IMNM +4.0% (Infinimmune announces research collaboration with Immunome)

-GANX +3.8% (begins GT-02287 Phase 1b Extension study in people (21 participants) with Parkinson’s Disease)

-ONDS +2.9% (Unit Apeiro launches NDAA-compliant made-in-the-USA Combat-Proven Fiber-Optic Spools for drones and ground robotics)

-LWAY -24% (Danone to no longer pursue an acquisition of Lifeway)

-KAPA -11% (efficacy data from going Phase 2 clinical trial of ENV105)

-ALMU -7.3% (prices 1.7M shares at $13.00)

-CBRL -7.2% (earnings, guidance)

-DRI -7.0% (earnings, guidance)

-SANG -4.5% (earnings, guidance)

-U -3.5% (weakness attributed to Meta Connect announcement about replacing Unity with its own runtime engine for app development)

-NNDM -2.7% (earnings)

BY Doug Kass · Sep 18, 2025, 9:11 AM EDT

BY Doug Kass · Sep 18, 2025, 8:55 AM EDT

BY Doug Kass · Sep 18, 2025, 8:45 AM EDT

BY Doug Kass · Sep 18, 2025, 8:30 AM EDT

From Peter Boockvar:

A few things stood out to me from Jay Powell's presser yesterday. The two comments that the cut was a 'risk management' move and they are 'meeting to meeting' was the right way to approach this as they balance the difficult and delicate balance of a muted labor market in terms of hiring but still having inflation stuck around 3%. Powell said "There are no risk free paths now." Powell also said of note that outside of one individual, they didn't discuss cutting 50 bps.

What also remains glaring is the asymmetry of how they deal with financial conditions. When credit spreads are wide and we're in a bear market for stocks the Fed is quick to ease. In contrast, Powell yesterday when asked about cutting into a record high in stocks he sort of brushed it off. In a speech in 1955 Fed Chair at the time William McChesney Martin said "The Federal Reserve is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up." The Fed is now adding more alcohol to that bowl and one Fed Governor wants to put grain alcohol in it.

Valuations don't matter until they do but we're now in rarefied air for the S&P 500 with the 2025 P/E ratio at 24.5 and 22x the 2026 calendar year estimate. On a GAAP basis, we are now trading at 29x 2025 earnings estimates. The dividend yield is at just 1.2% currently. Again, doesn't matter though until it does. I do want to argue too that there are cheap stocks out there, just not as many in the highly concentrated S&P 500. Within the S&P, the consumer food/product companies are getting really attractive I believe. They've been hammered and now have bond like dividend yields with equity like upside.

While the 2 yr yield is down about 3 bps vs 1:59pm est yesterday, the 10 yr and 30 yr yields are up by 1 bp. We of course watch the reaction in the long end to see if we get a repeat of the post September 2024 cuts or not. Yields fell going into that, just as they have over the past few months.

In the statement from the Bank of Canada yesterday with their expected 25 bps rate cut they said "With a weaker economy and less upside risk to inflation, governing council judged that a reduction in the policy rate was appropriate to better balance the risks going forward." From here though it wasn't as clear as "the disruptive effects of shifts in trade will continue to add to costs even as they weigh on economic activity." They will be "proceeding carefully" from here they said. Over the past two days the Canadian dollar is basically flat as is the 2 yr yield (down 3 bps yesterday, up 3 bps today).

The Bank of England held rates at 4% as expected and announced the trimming of its sales of longer term Gilts from its balance sheet, also as anticipated and as part of their QT. Their balance sheet will be reduced by 70b pounds in the year beginning in October and that is down from a previous pace of 100b. The vote was 7-2 with those dissenters wanting to cut 25 bps. After a rundown of their economic viewpoints, they said "The timing and pace of future reductions in the restrictiveness of policy will depend on the extent to which underlying disinflationary pressures continue to ease." As there is not much surprise here, gilt yields are little changed as is the pound.

As measured by the Investors Intelligence survey, we are on the cusp of what I consider the danger zone in terms of stock market sentiment from a contrarian stance. I define that as a 40 point spread between Bulls and Bears. Bulls rose to 56.6 from 54.7 while Bears remained at just 17. In today's AAII, the Bulls came out of the woodwork, jumping by 13.7 pts to 41.7 while Bears fell by 7.1 pts to 42.4.

From General Mills:

"We continue to manage through an evolving operating environment in fiscal 2026 with cautious consumer behavior connected to economic uncertainty, global conflicts, and changing food policy regulations. We continue to see consumers seeking value and prioritize their spending on key benefits like protein, bold flavors, and feelings of nostalgia from brands they love."

"if you look at the last year or so, volumes in our category are about flat, which is about 50 bps below what we've seen historically, but not too far behind. And there are a number of factors for that. Probably the most important we believe is that we saw decades worth of inflation in a couple of years. And so consumers are still recovering that as wages have not yet caught up with all that and that inflation. And so, we think that's the biggest driver."

"I mean GLP-1s has a small, we think has had a small impact so far. And consumers seeking value and a stressed consumer maybe a little bit."

And for those on GLP-1, "they want more protein. And there's a reason why Cheerios Protein is off to such a great start, or Progresso Pitmaster, which is high in protein, is off to a really good start. That we introduced Nature Valley Creamy Protein."

From Cracker Barrel and we know had a tumultuous time with the logo change. Its stock is down about 10% pre market:

Comps grew by 5.4% and it was all price as "Pricing for the quarter was 5.4%. We continue to be pleased with the strategic pricing initiative, as flow through results remain favorable."

"Turning to our fiscal '26 outlook. I'll start with an update on traffic trends to date in the first quarter. Traffic for the first half of August was down approximately 1%. Since August 19, the date of the initial logo change, traffic has declined approximately 8%. As similar trends continue for the remainder of the quarter, we anticipate a Q1 traffic decline of approximately 7% to 8%."

"Commodity inflation was approximately 2.3%, driven principally by higher beef, pork, and egg prices, partially offset by lower poultry and produce prices." They saw only modest wage inflation of 1.1%.

Manheim gave us its first half of September wholesale used vehicle pricing and they were little changed from August but up 2.2% from September 2024. They said "Wholesale values are continuing to buck traditional trends as they have for most of 2025, as prices have yet to return to normal depreciation levels. We are continuing to see elevated new and used retail sales trends in the first part of September, and that is keeping retail days' supply relatively tighter, pushing buyers through the doors at Manheim. As we approach the end of September, when tax incentives on EVs end, we are seeing demand trends that are keeping used EV sales strong and values even stronger, even as EVs rise in sales mix at Manheim. The automotive market continues to show resiliency overall, both at the retail and wholesale level, as they are tied so closely to each other."

BY Doug Kass · Sep 18, 2025, 8:17 AM EDT

What Intel INTC taketh today, Taiwan Semiconductor TSM and Advanced Micro Devices AMD may giveth (away).

BY Doug Kass · Sep 18, 2025, 7:58 AM EDT

Break in!

Nvidia NVDA to invest $5 billion in Intel INTC.

Nvidia Invests $5 Billion in Intel With Plans to Co-Design Chips - Bloomberg

BY Doug Kass · Sep 18, 2025, 7:13 AM EDT

From JPMorgan:

US: Futs are higher as investors shake off a hawkish Powell Q&A and refocus on the most dovish Fed statement since 2021, per JPM NLP. Both NDX and RTY are outperforming as the US is poised for an ‘Everything Rally’ alongside a global risk-on tone. The yield curve is bull flattening and USD is flat. Pre-mkt, Mag7 / Semis are bid up with NVDA +2.3%, AVGO +1.9%, TSLA +1.6%, GOOG +1.3%. Large-Caps across all the super-sectors are higher pre-mkt. Today’s macro data focus is on jobless claims where investor will look to confirm last week’s spike was a one-off.

and...

The FOMC Statement read dovishly with more cuts being forecasted amid stronger growth; however, the Press Conference was hawkish. The markets seemed to focus on Powell’s statement that yesterday’s cut was for “Risk Management” rather than the potential beginning of a new easing cycle (full quote below). Feroli believes this is the beginning of the next phase of easing with an additional 100bp of cuts coming. Regarding the consumer, Powell mentioned that the aggregate Consumer is in good shape, ex-bottom income bracket, and the consumer default rates are not concerning. Overall, yesterday’s meeting was focused on the labor market where the immigration / deportation policy is the primary driver of weakness which may be exacerbated by tariff policy and cumulative inflation. As the Fed looks to 2026, they seem to acknowledge how tricky it is to forecast when government policies may continue to change rapidly.

“I think you could think of this in a way as a risk management cut because if you look at the SEP, actually, the projections for growth have ticked up … Let’s remember, though, the unemployment rate is 4.3 percent. The economy is growing at one and a half percent. So, it’s not a bad economy or anything like that. We’ve seen much more challenging economic times but from a policy standpoint, the stand point of what we’re trying to accomplish, it’s challenging to know what to do. There are, as I mentioned earlier, there are no risk free paths now. It’s not incredibly obvious what to do, so, we have to keep our eye on inflation.” – Jay Powell

Some additional color that we blasted via IB:

· US MKT INTEL ON THE FOMC STATEMENT – This is the dovish cut that we were looking for with the DOTS aligned with the consensus view of 2 more cuts this year. These insurance cuts are supportive of the bull case especially in light of yesterday’s Retail Sales. If the Oct 3 NFP moves higher and Oct 15 CPI stays contained look for Equities to explode higher after what should be a strong 25Q3 earnings period. For those looking for 7k by year-end, this is first part of the formula. Look for the rally to broaden in the US but weaker USD to be supportive of Int’l Eqys especially for EM (we like China and Brazil). The question does remain as to IF or WHEN we see a pullback with the second half of September being the worst two weeks of the year. The press conference has the potential to reverse these gains. Even if we see a pullback, we advise buying the dip and moving toward being maximally long.

· US MKT INTEL ON THE PRESS CONFERENCE – The press conference skews hawkishly. The immigration / deportation policy is hurting the labor market with uncertain outcomes. This concerns the Fed, but monetary policy will not solve this problem. Powell’s comment on this being a ‘risk mgmt’ cut is being viewed as hawkish by markets despite the forecast for 2 more cuts this year. The Press Conference does not change our view that any/all dips should be bought with a low conviction view that markets pullback into month-end/quarter-end.

o ECON DEVELOPMENTS – growth has moderated with GDP ~1.5% in 25H1 vs. 2.5% FY24 reflecting a slowing in consumer spending (retail sales shows it is concentrated in the top two income quintiles). Unemployment ticked up but remains at a low level. Slowing labor supply is the likely culprit for this slowing growth (immigration, deportation, and lower participation rate).

§ Total PCE rose 2.7% over the last 12 months and Core PCE rose 2.9% and these readings are going higher due to Goods but may be offset by Srvcs disinflation. Flags the risk of sticky, tariff-induced inflation.

§ Flags uncertainty from gov’t policy which continues to change.

BY Doug Kass · Sep 18, 2025, 6:40 AM EDT

BY Doug Kass · Sep 18, 2025, 6:30 AM EDT

Doomberg on "Fields of Dreams."

BY Doug Kass · Sep 18, 2025, 6:20 AM EDT

Bonus — Here are some great links:

New All-Time Highs in September Are Bullish

BY Doug Kass · Sep 18, 2025, 6:05 AM EDT

BY Doug Kass · Sep 18, 2025, 5:55 AM EDT

The S&P Short Range Oscillator stands at 3.25% vs. 3.35%.

BY Doug Kass · Sep 18, 2025, 5:45 AM EDT