From JPMorgan (good scenario analysis of today's expected Fed cut below):

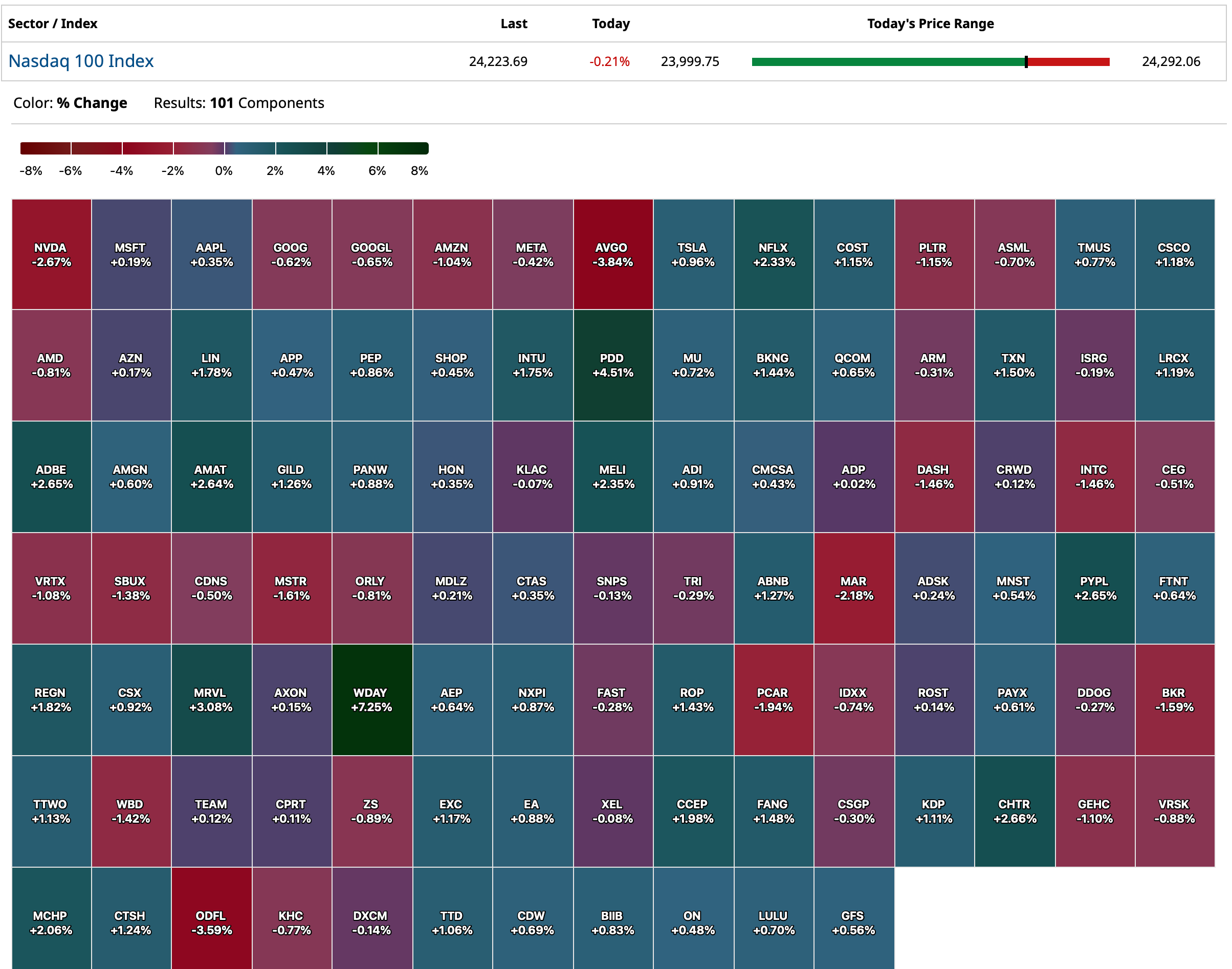

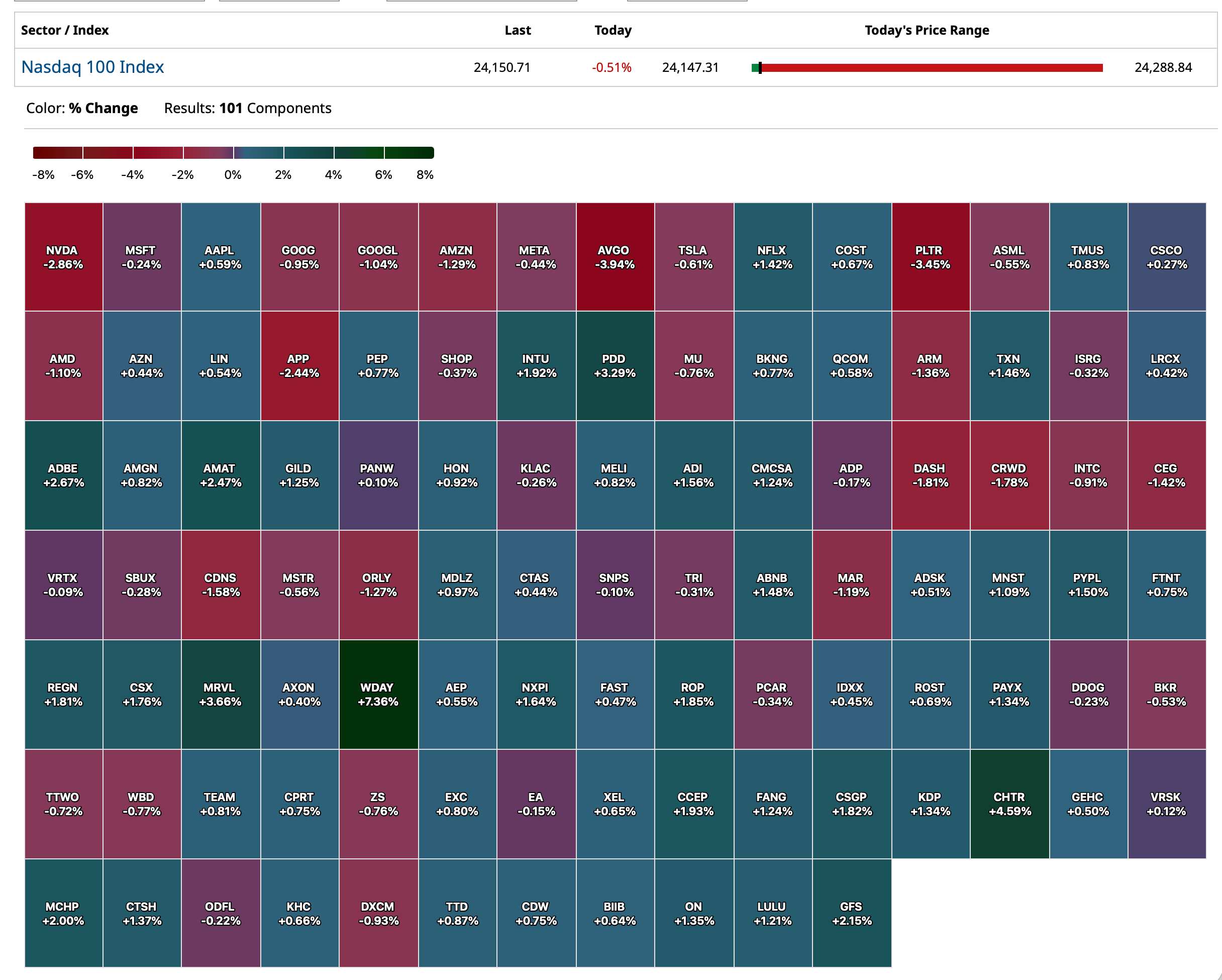

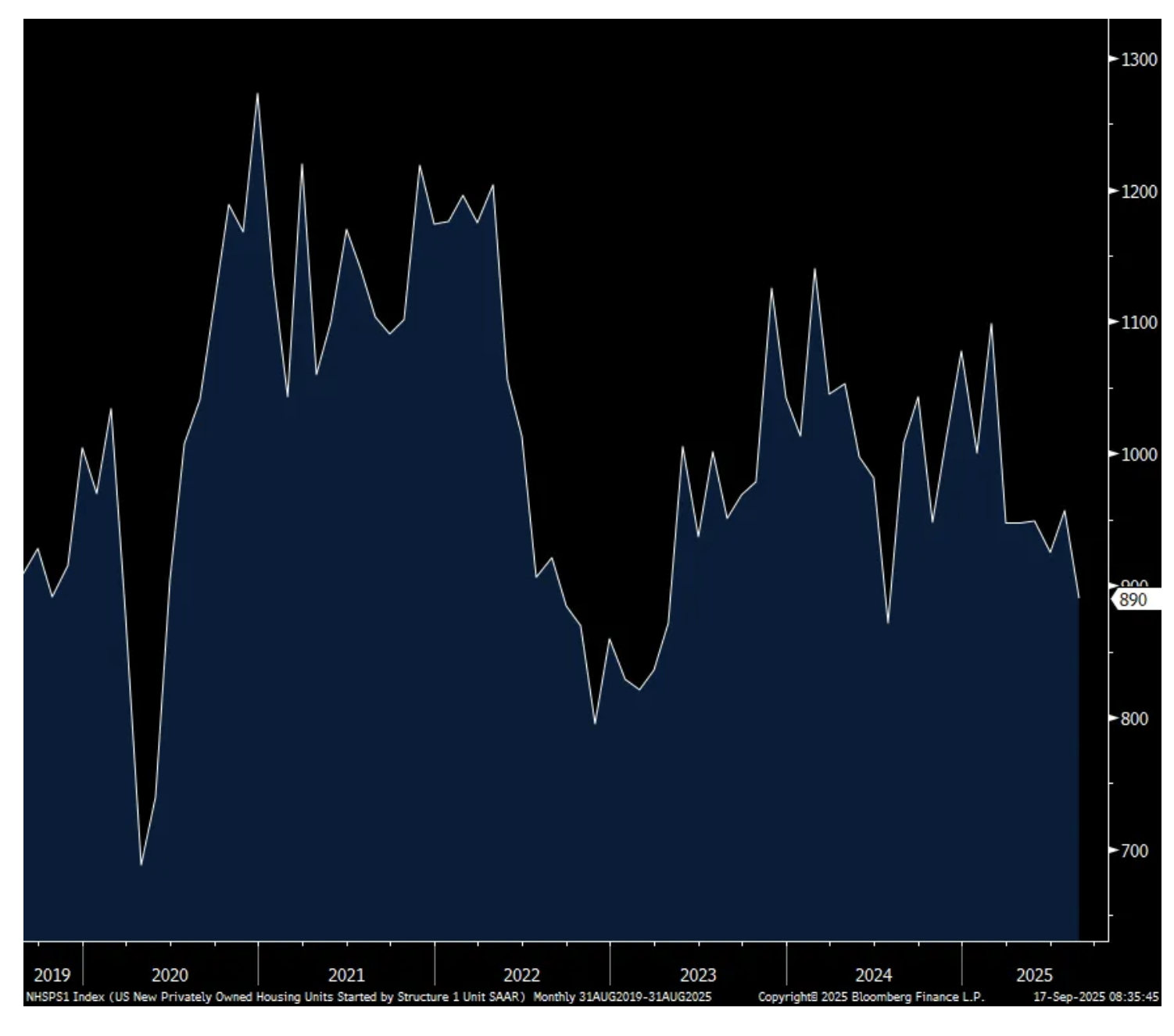

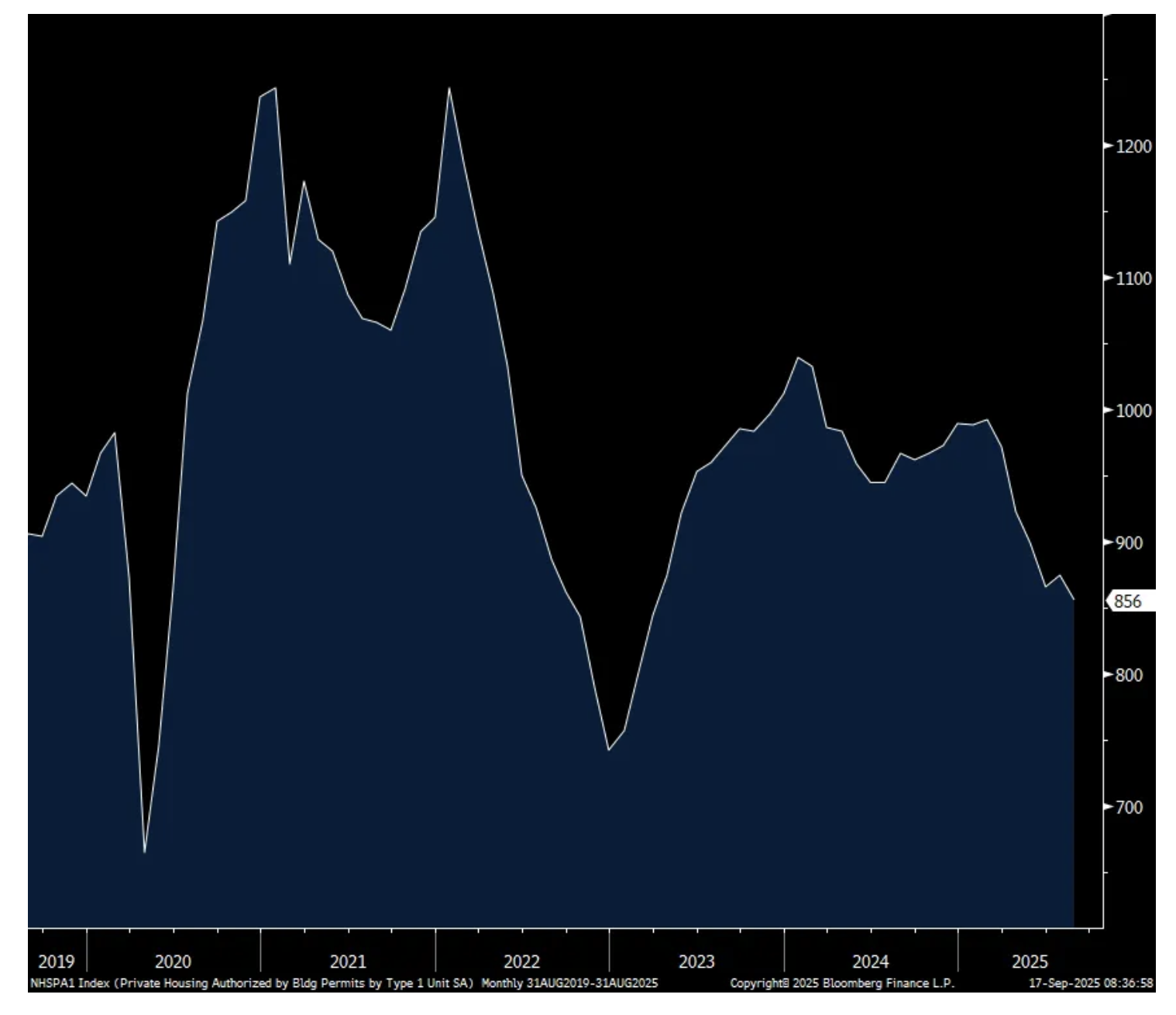

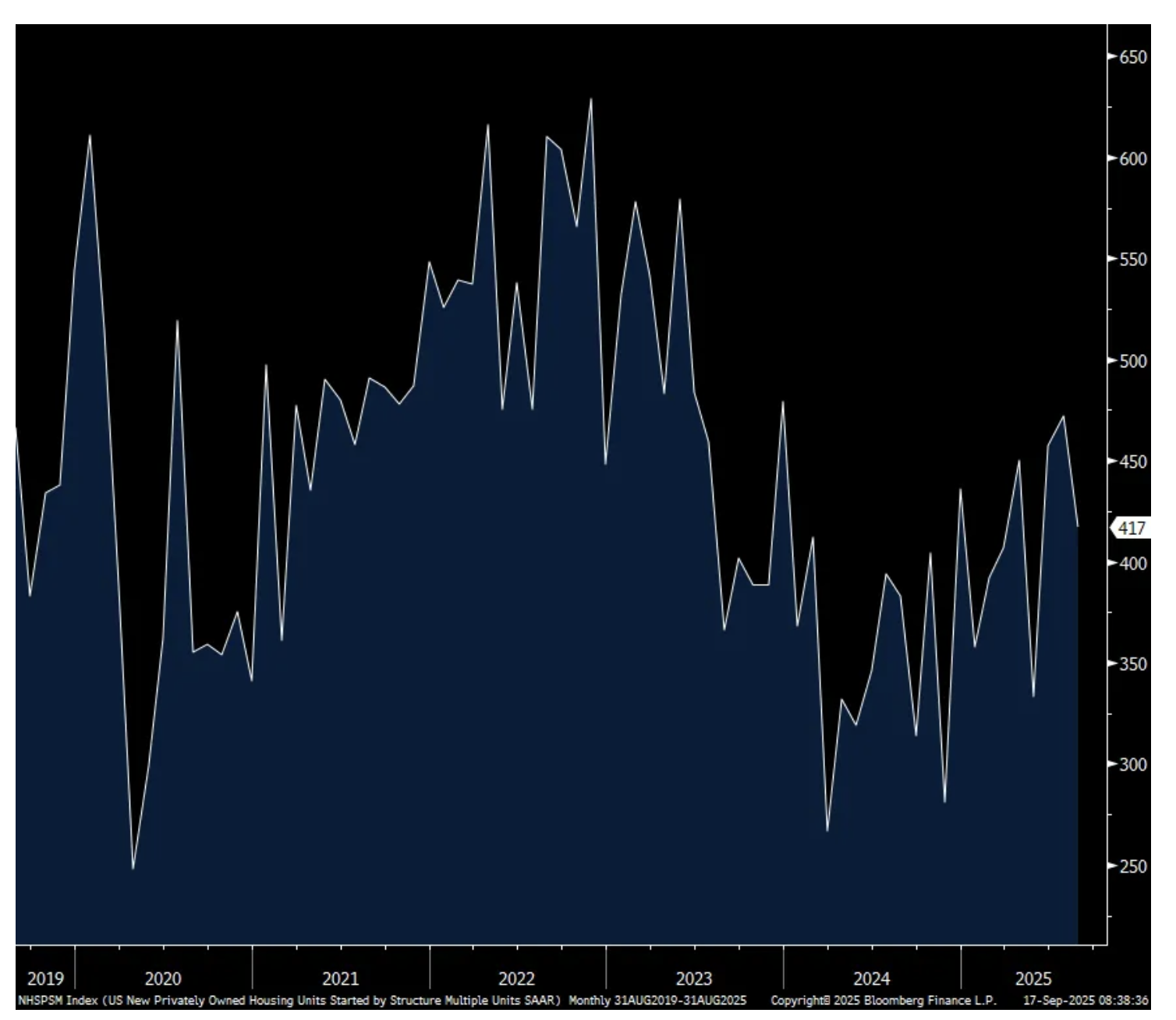

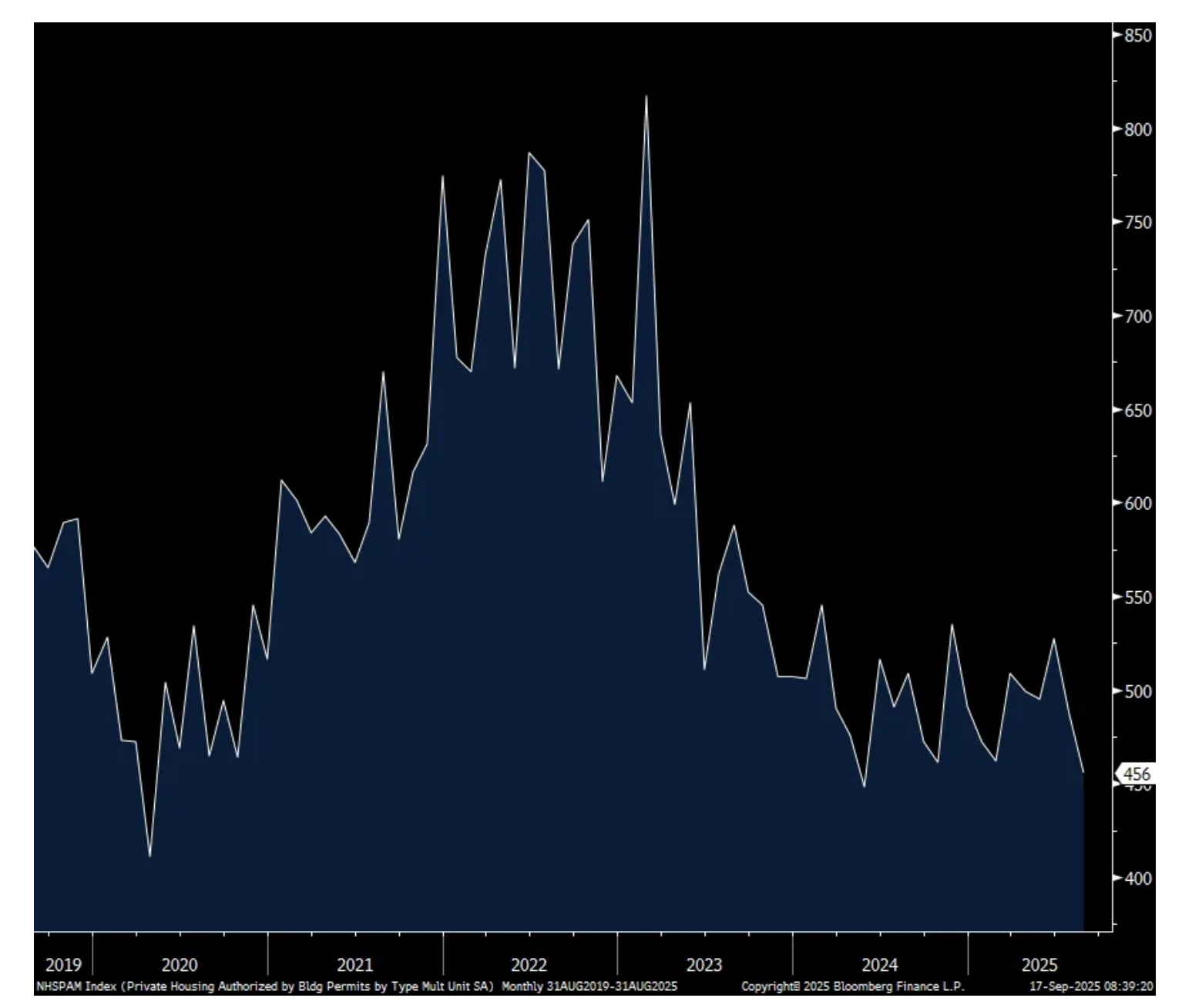

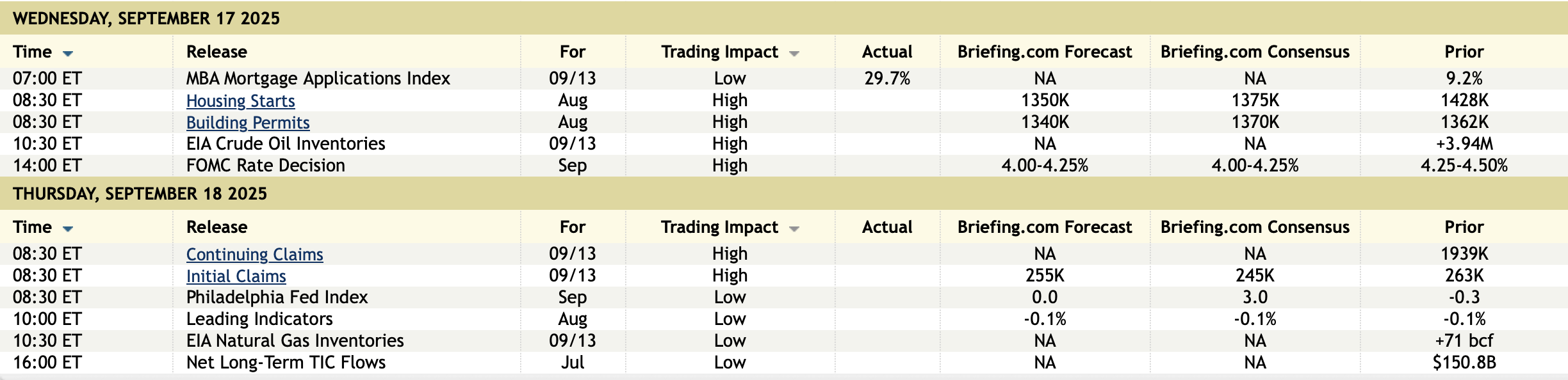

US: Futs are flat into the Fed with the long end of the yield curve moving lower. USD is catching a bid after losing nearly 1% the last two days. Pre-mkt, Mag7 names are mixed with NVDA down 1% on news reports of a ban on their chip sales to China. AMD -1%, AVGO flat. Cyclicals are under pressure. The cmdty complex is weaker with notable losses in silver and coffee, each down more than 2.2%. In addition to the Fed today, we also have Housing Starts / Bldg Permits ahead of tmrw’s jobless data.

and...

US MKT INTEL’S FED DAY SCENARIO ANALYSIS [REPOST]

Feroli expects a 25bps rate cut, with 2-3 potential dissenters who would be looking for at least 50bp of cuts, and then 3 consecutive cuts from Oct 2025 – Jan 2026. He thinks the DOTS will show 1x additional cut in FY25, 2x cuts in FY26, and then 1x cut in 2027 to get to 3.00%. At the Press Conference, Powell is likely to the focus on downside risks to employment, given that tariff-induced inflation is expected to be transitory, but Feroli does not expect firm forward guidance. The macro environment has changed since the easing seen in 2024, when Core PCE was falling, from 2.9% to 2.6%; whereas, now inflation is rising, with Core PCE increasing from 2.6% to 2.9%. In 2024, the Fed cut by 50bp at the Sep 18, and then by 25bp at the Nov 7 and Dec 18 meetings. From Sep 17 to Jan 14, the 10Y yield rose by 114.7bp; Jan 14 was the YTD high for the 10Y yield.

· [1.0%] FED HIKES – SPX falls 2% – 4%. The first tail risk with the probability closer to zero than 1%. Given that Core CPI MoM has increased 3 consecutive months, this will give the Fed pause but the CPI print was not hot enough to make this a credible threat. For reference, the 3-month average for Core CPI MoM is .30% or 3.64% annualized which is hot but not enough to hike given tariff policy that may inflect dovishly.

· [4.0%] FED REMAINS PAUSED – SPX falls 1% – 2%. Another tail-risk and we think that this outcome would have required both a stronger NFP print as well as a hotter CPI print. We effectively received neither and given Powell’s comments at Jackson Hole, this scenario likely does more harm than good.

· [40%] HAWKISH 25BP CUT – SPX is flat to down 50bp. The primary argument now is whether the statement / press conference skewed hawkishly or dovishly. We are in the camp that with inflation increasing at a decreasing rate, plus YoY levels that in a 2% - 3% range are fine for the Fed to cut rates and resume its data-driven approach. Fedspeak points to the labor market being the bigger concern than inflation and with data pointing to hiring inflecting higher (Small Biz survey, Indeed listing, etc.) this could lead to a more hawkish Powell than expected, nullifying some of the stock market appreciation into Fed Day.

· [47.5%] DOVISH 25BP CUT – SPX gains 50bp – 1%. Continuing with the above argument, it is possible that with a transitory view on inflation that the Fed sees the labor market as being far away from having an inflationary impact on the economy and thus has some room to cut, preferring a gradual series of 25bp cuts, as long as inflation remains contained and NFP remains weak.

· [7.5%] 50BP CUT – SPX loses 1.5% to SPX gains 1.5%. The final tail risk and we are aware that this range of outcomes is pretty wide. The negative outcome would be tied to a market expressing a view that the Fed is more concerned about the labor market than it is letting on and that new uncertainty triggers a selling event. The positive outcome is tied to a view that the Fed sees itself as needing to catch up to the economic realities of a labor market on the precipice of rolling over and printing negative NFP.

· WHAT ARE OPTIONS PRICING? These are indicative only, call the desk for live pricing.

o EQUITIES – SPX options are pricing in 88bp move for options that expire on September 17, based upon data as of Sep 12.

o FX – EUR / USD is a 10 vol equating to a 42bp breakeven. USD / JPY is a 15 vol equating to a 63bp breakeven; pricing is as of Sep 11. Tomorrow, the team will update the full list of currencies.

o RATES – The 10Y breakeven is 4.625bp; pricing is as of Sep 12. Tomorrow, the team will update the full list of major Treasuries.

· US MARKET INTELLIGENCE – We see a Dovish Cut as the most likely outcome, producing a positive gain on the day. As we look toward month-end, Fed Day may act as a “sell-the-news” event as investors take time to consider the macro environment, the Fed future reaction function, potentially stretched positioning, a temporarily weaker corporate buyback bid, waning Retail investor participation, and quarter-end rebalancing.

o If this comes to fruition, look for a 3-4% pullback with some key catalysts to support the BULL CASE: (i) PCE on Sep 26 which is already de-risked with today’s CPI print; (ii) NFP on Oct 3 where a higher MoM print will continue to support an increasingly optimistic macro outlook; (iii) CPI on Oct 15 which will guide expectations for the Oct 29 Fed similar to the set-up into Sept Fed. Based upon information we have now, we like the BULL CASE and would use any pullback to add to risk.

o WHAT WOULD WE BUY AFTER A PULLBACK? While we do like the market broadening theme we also like being OW TMT / MegaCap Tech / AI-Theme. We do not see Defensives outperforming but things like (i) Utilities will benefit from a decline in the 10Y yield esp. if it falls to / thru 3.50% and (ii) Healthcare on the combination of strong EPS generation and low positioning plus Biotech should benefit from the anticipated wave of M&A. In international space, we like EM over DM if USD continues to weaken but if US macro data continues to inflect higher there could be squeeze that strengthens the USD, likely benefitting the US, generally, and TMT, specifically.

o WHAT IF A PULLBACK DOES NOT MATERIALIZE? Given a dovish cut, it is possible that this phase of the Bull Rally continues without a pullback despite the aforementioned reasons. If so, it is likely a continuation of the short-covering led rally that we saw on CPI Day, potentially at the expense of TMT; where TMT is positive but underperforms both SPX and RTY.