RICK Stock Hits the After-Hours Red Light District

Investment short RCI Hospitality (RICK) is in the news after the close (causing the shares to drop by over -$6/share (-20%)) as the New York Attorney General has charged the company and five executives (including the CEO) with conspiracy, bribery and tax fraud.

The business media is filled with the sunshine boys and girls who never met a market they didn't like — rarely reporting negative developments.

Well I have one... the highly touted Winklevoss twins' crypto exchangeGemini Space Station(GEMI) is approaching its $28 per share IPO price — down by $4 (-12%) to $28.55 today.

Doug--have you ever disclosed the methodology behind your short-term S&P oscillator? I'd love to understand what's behind it to better understand its signals and possibly incorporate it into my oscillators. Thanks in advance!

Dougie Kass

S&P Short-Range Oscillator (SRO)combines several market indicators to provide a normalized measure of market sentiment, assisting traders in making informed decisions.

The SRO utilizes two simple moving averages (SMAs) of different lengths: a 5-day SMA and a 10-day SMA. It also incorporates the daily price change and market breadth (the net change of closing prices). The 5-day and 10-day SMAs are calculated based on the closing prices. The daily price change is determined by subtracting the opening price from the closing price. Market breadth is calculated as the difference between the current closing price and the previous closing price.

The raw value of the oscillator, referred to as SRO Raw, is the sum of the daily price change, the 5-day SMA, the 10-day SMA, and the market breadth. This raw value is then normalized using its mean and standard deviation over a 20-day period, ensuring that the oscillator is centered and maintains a consistent scale.

Finally, the normalized value is scaled to fit within the range of -15 to 15.

When interpreting the SRO, a value below -5 indicates that the market is potentially oversold, suggesting it might be a good time to start buying stocks as the market could be poised for a rebound. Conversely, a value above 5 suggests that the market is potentially overbought. In this situation, it may be prudent to hold on to existing positions or consider selling if you have substantial gains.

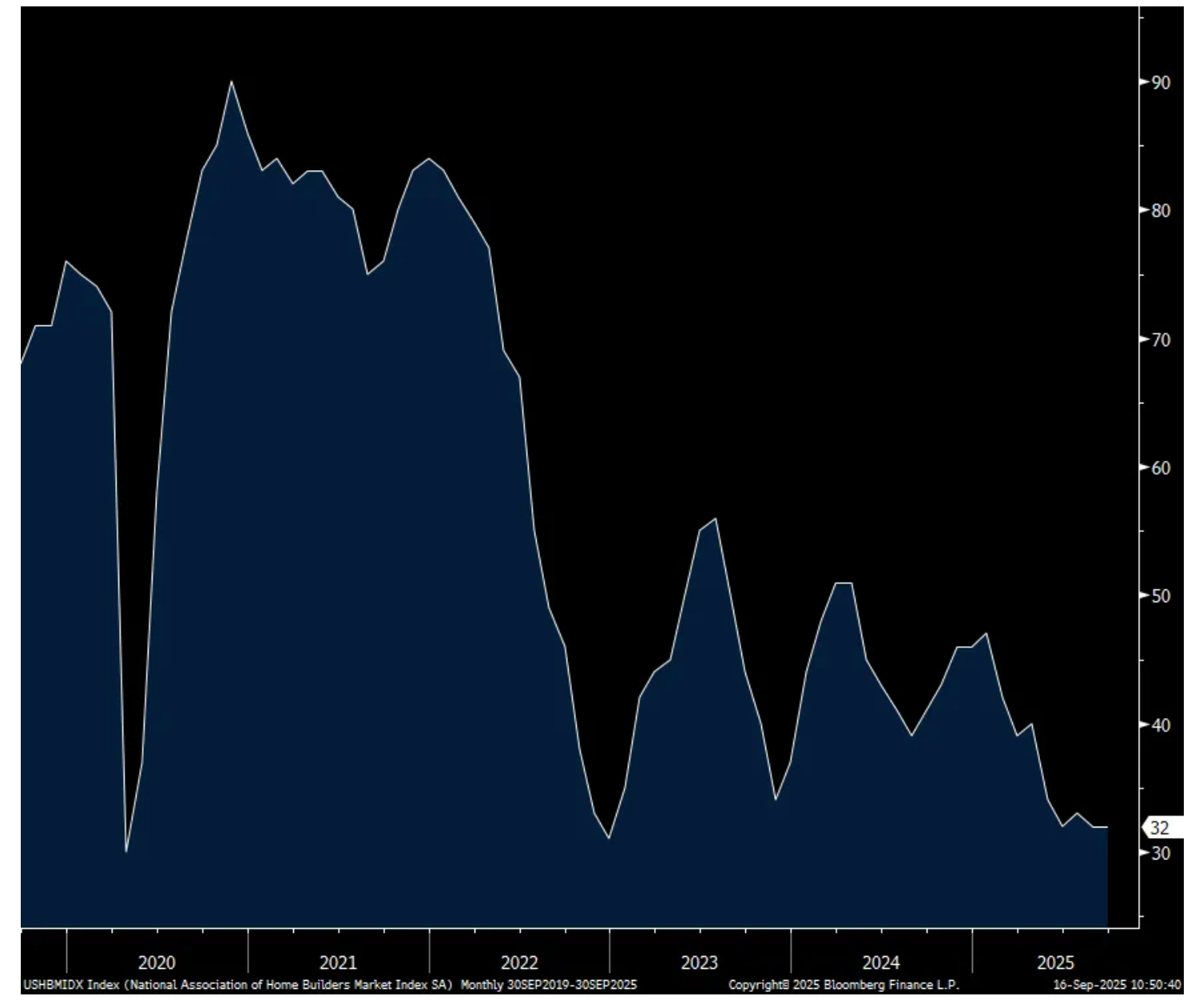

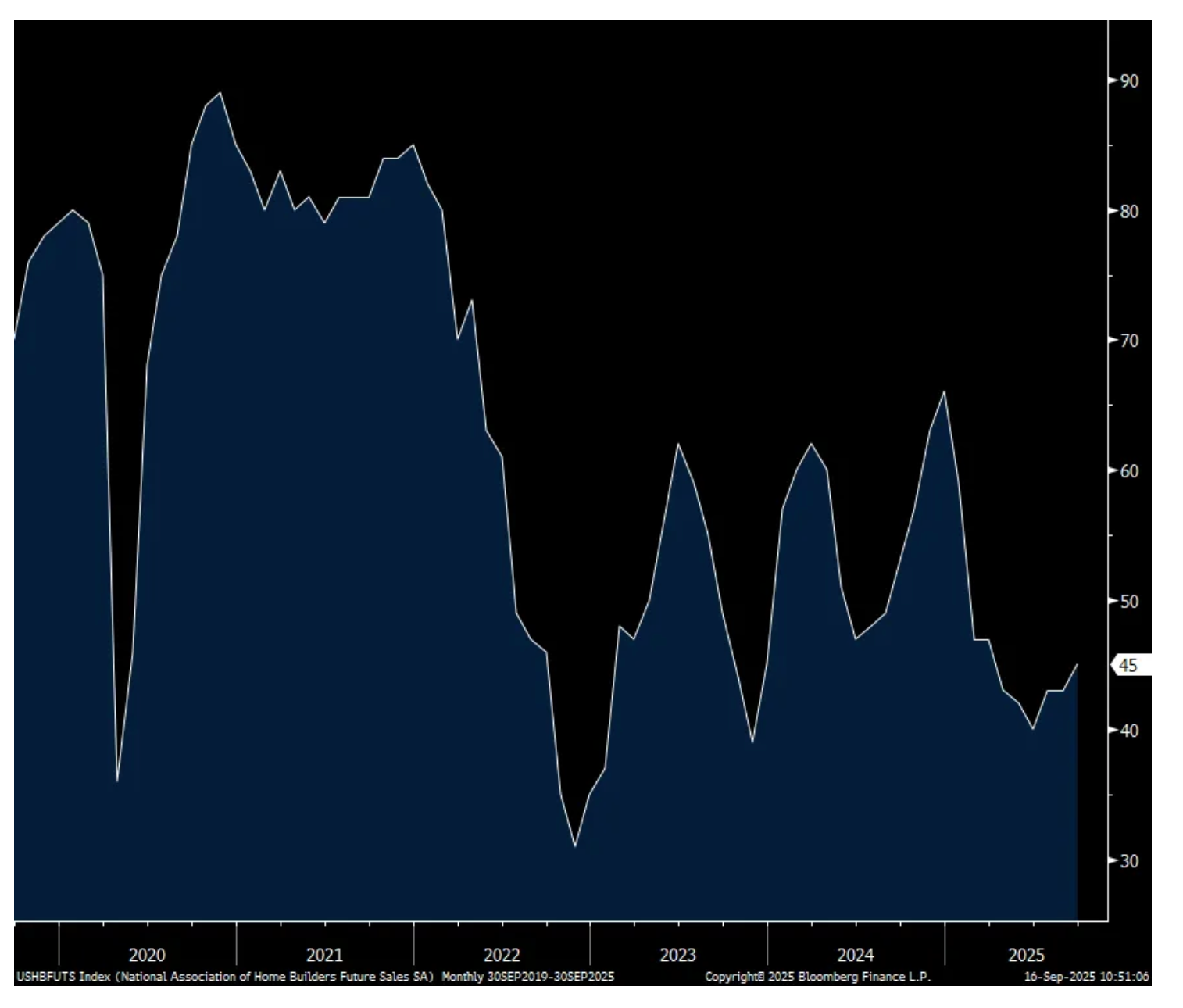

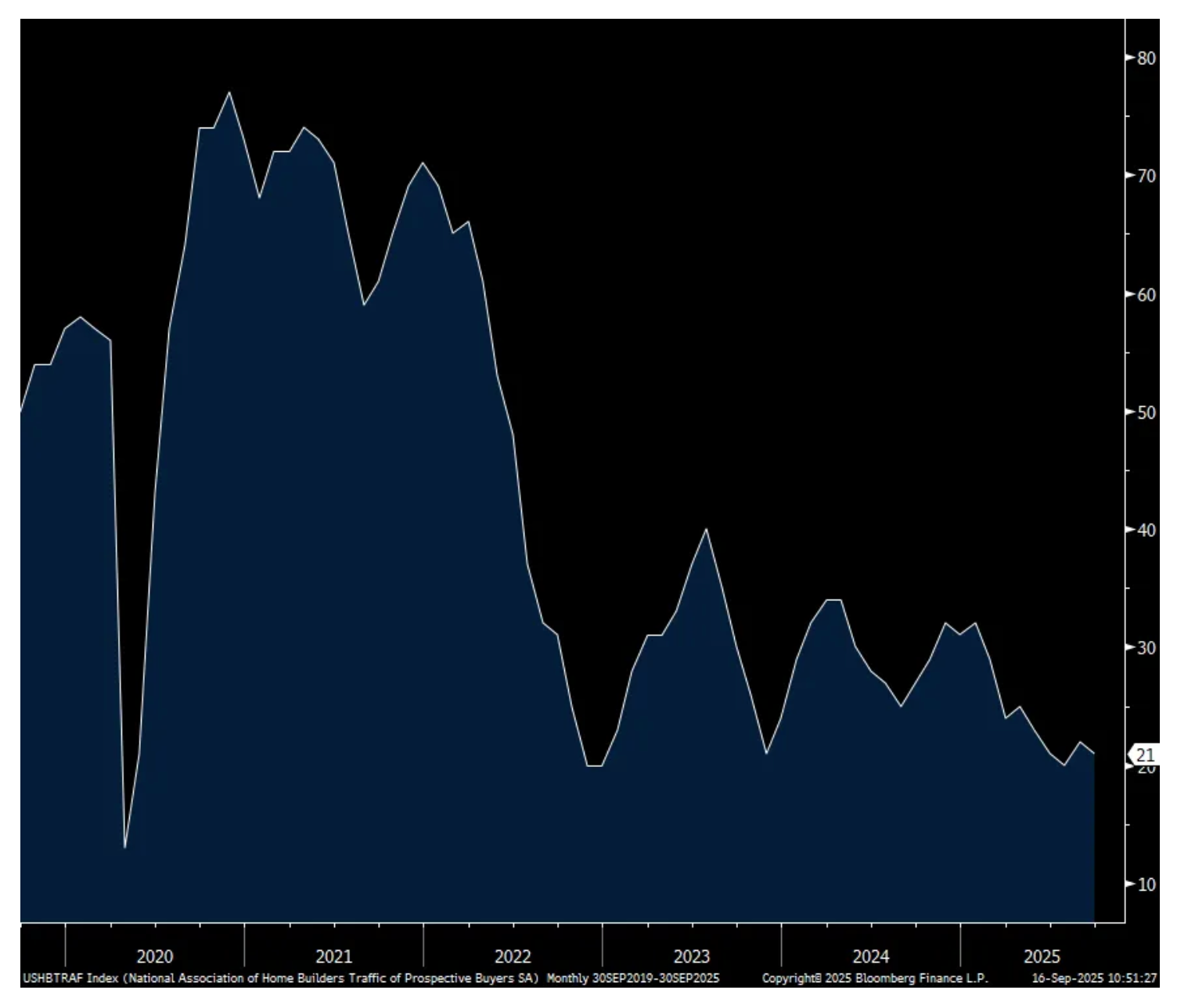

Home builders hopeful that lower rates will help but buyer traffic still punk

The September NAHB home builder sentiment index was flat at just 32 but the Future Expectations component continues to creep higher as builders of course hope that Fed rate cuts will result in lower mortgage rates for a sustainable period of time. This component rose 2 pts to 45, though still below 50. The demand side though remains punk as Prospective Buyers Traffic fell 1 pt to only 21, 29 pts below the breakeven of 50.

The hope of course is lower mortgage rates will stimulate demand but in order to not have higher home prices offset that benefit, we need more supply. Helping to stimulate demand, price discounts and incentives continues. The NAHB said “39% of builders reported cutting prices in September, up from 37% in August and the highest percentage in the post Covid period. Meanwhile, the average price reduction was 5% in September, the same as it’s been every month since last November. The use of sales incentives was 65% in September, essentially unchanged from 66% in August.”

Not mentioned here is the supply side from the existing home market where it seems to be growing in the previously hot markets like Austin, Phoenix and some in Florida while others are more supply constrained as the mortgage lock in effect remains in place and may not be relieved in a notable way unless mortgage rates get below 5%.

I want to highlight that according to the NAHB, historically speaking the housing industry all in, so including everything from builders, to title companies, to repair & remodel, etc… makes up anywhere from 15-18% of US GDP. This sector has essentially been in a recession for the past few years and any relief it can get would obviously be economically noteworthy.

Bernard Baruch was far more eloquent than most of us (me). That being said, generally speaking there is a corollary which in my observation notes that the greater the extreme of greed or fear, the subsequent "correction" will also be more extreme in either/both time and price:

"We must remember that delusions swing between extremes, like pendulums. Delusions of grandeur and unending wealth give place to delusions of unending gloom. One is as unreal as the other."

- Bernard Baruch

Skepticism and doubt have left Wall Street.

To learn from history it is helpful to go back in history.

“Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.”

* I call more BS on the calculation of the CPI ...

I wonder what the guys who cook up the CPI will do next? We have already substituted from steak to ground beef.

Now ground beef is too expensive, will they estimate the price of road kill and just assume the population has increased their consumption of dead racoon and skunk and the expense of hamburgers? Can’t wait until I get the opossum-burger at In-N-Out Burger, might as well get it animal style right?

The Animal Style Burger is a popular "off the menu" item at In-N-Out Burger, known for its rich, tangy flavor profile achieved by adding grilled onions, pickles, extra special sauce, and a mustard-glazed beef patty. It is one of the most iconic variations on In-N-Out's secret menu, with the option to customize other sandwiches like the Double-Double or even a veggie-based Wish Burger with the same style. The burger is also available as fries "animal-style," which include melted cheese, grilled onions, and special sauce on top.

More Tales From Nvidia: CoreWeave and the Dot-Com Comparisons

For all the dot-com bubble comparison talk, this is the closest compare for me. Not much different than bandwidth swaps and mark ups. Just more elegant and complex versions of the same baloney, but baloney is still baloney, no matter how thin you slice it!

Round and round we go, the circles keep getting bigger and bigger….

On September 9, 2025, CoreWeave, Inc. (the “Company”) and NVIDIA Corporation (“NVIDIA”) entered into a new order form (the “Order Form”) under the existing Master Services Agreement (“MSA”) dated as of April 10, 2023, which has an initial value of $6.3 billion, that establishes an arrangement with respect to the sale by the Company of reserved cloud computing capacity to its customers and provides NVIDIA access to any residual unsold cloud computing capacity. Under the terms of agreement, in instances where the Company’s datacenter capacity is not fully utilized by its own customers, NVIDIA is obligated to purchase the residual unsold capacity through April 13, 2032, subject to any termination described below and satisfaction of delivery and availability of service requirements. The Company has determined that the MSA is a material agreement within the meaning of Item 1.01 of Form 8-K because the MSA is no longer immaterial in amount or significance. The MSA will remain in place until either all outstanding orders under the MSA are expired or terminated, or the MSA is otherwise terminated in accordance with its terms. Either party may terminate the MSA (and any order thereunder) (i) upon 30 days’ written notice to the other party of a breach or (ii) if the other party becomes subject to a bankruptcy petition or other insolvency proceeding, receivership, liquidation or assignment for the benefit of creditors and such proceedings are not dismissed within 90 days. The MSA contains customary provisions regarding representations and warranties, indemnification, and limitations on liabilities. In addition to the MSA, NVIDIA supplies the Company with NVIDIA GPUs and is a stockholder of the Company.

* The equity advance continues apace as investors ignore sticky inflation, moderating economic growth, uncontrolled government spending (and a rising deficit and debt load), historically lofty valuations and a possible peaking of the AI trade (which has been a prominent factor in the market's overall advance).

* Nevertheless, in the investment battle of late 2025 I favor Disraeli and Voltaire over Pangloss...

Bottom Line

"Dr. Pangloss, welcome to Wall Street, where it is indeed the best of all possible worlds."

- Randall Forsyth, Barron's (Up and Down Wall Street)

Pangloss, the unfailingly pollyannaish tutor of Candide (the protagonist of Voltaire's novel by the same name) is considered a symbol of foolhardy optimism.

Though in the investment business, as in life, faith moves mountains — with the potentially toxic cocktail of sticky inflation, moderating economic growth, climbing U.S. debt loads, high valuations (in the 98% -tile), a market dependent upon the AI trade and gross speculation (e.g. Opendoor Technologies (OPEN) et al) reminiscent of the late 1990s — I remain cautious (and frustrated) as, for now, Dr. Pangloss is prevailing.

Nonetheless I am reminded of another turn of the phrase from Disraeli:

"What we have learned from history is that we haven't learned from history."

As well as a quote from Voltaire:

"History never repeats itself. Man always does."

Common sense is not so common.

Today's economic data and, despite the extraordinary price momentum, there is nothing that derails my cautious outlook which is based on slowing economic growth, prickly inflation and lack of fiscal discipline (that is leading to ever rising deficits).

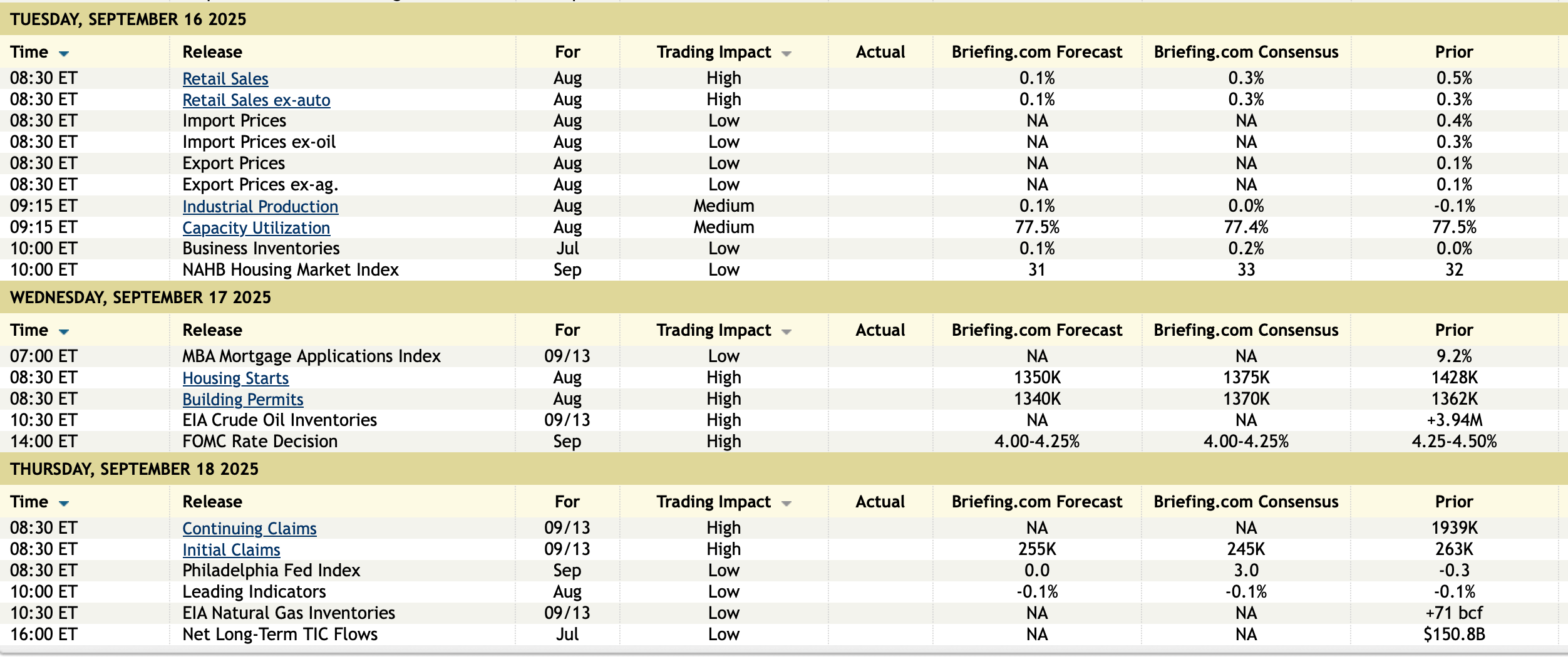

Headline retail sales good but pull forwards and tariff pricing flow thru/Import prices up

Core retail sales in August rose .7% m/o/m, 3 tenths above the estimate and after a .5% rise in July. Above this line item, vehicle sales rose .5% m/o/m while building materials were little changed, up .1% after a drop in the month before of .9%. Versus last year, vehicle sales were up by 3% y/o/y while building materials were lower by 5.7%. To what extent we are seeing pull forward with EV’s ahead of the end of the tax credit we’ll see after they expire.

We just don’t know what impact tariffs are having on auto sales too in particular in terms of pull forwards still and who is eating what. Japanese car companies by the way are done eating them and have announced price increases.

Also, these are nominal figures and thus include any impact from tariff induced price increases.

With back to school, clothing sales were up 1% and up 7.6% y/o/y. Again, sounds great but tariffs are included in the prices. Sporting goods, which have seen sharp price increases since April, saw sales up .8% m/o/m and 4.4% y/o/y. Online retailing was strong, up 2% but tough to say what was pull forward ahead of the elimination of the de minimis tariff threshold with Temu and Shein in particular. Misc store sales were down by 1.1% m/o/m.

Furniture sales fell .3% but after 1.6% jump in July. Electronics sales were up by .3% after rising by 1.2% in July. Eating/drinking at restaurants/bars saw sales rise by .7% m/o/m and by 6.3% y/o/y and continues to be good even though foot traffic in certain things like fast food and fast casual has slowed.

The necessities such as food/beverages saw sales up .3% m/o/m and 2.7% y/o/y. Health/personal care prices fell one tenth after rising by .4% in July.

Bottom line, as said, these are nominal numbers and I just don’t know what was price and what was volume with the above numbers. Also, what was pull forward ahead of the end of de minimis tariff rules and what was not. I’m sure you will read many headlines that the consumer is strong but those comments are in nominal terms, not real and we know directly from a whole slew of retail touching businesses that the consumer is highly bifurcated.

Import prices rose .3% headline m/o/m, well above the estimate of down .2% but partly offset by a 2 tenths downward revision to July. Prices ex food and energy jumped by .5% m/o/m after no change in July but higher by a still modest 1% y/o/y.

Import prices for industrial supplies (up .4% m/o/m), capital goods (up .5%), autos/parts (up .2% after 3 months of declines) and consumer goods (up .7%) all accelerated and something to watch with the weaker dollar and in the debate of who is eating what when it comes to tariffs. While these numbers don’t include tariffs, we can see to what extent importers to us are discounting product or not.

Thus, if the core import figure for August is the beginning of an upward trend, if, they might not be eating much anymore.

Treasury yields are up slightly in response to both figures.

Boockvar on the Fed Drama and Clues from Subprime-Auto-Loan Land

From Peter Boockvar:

Oh to be a fly on that Fed wall

So, do we now assume that new Fed Governor Stephen Miran will vote for a 50 bps cut tomorrow and Lisa Cook will vote for none? Does Waller vote for 50 bps too because he really, really wants the Fed Chair job? I wish we didn’t have to wait so long to get the actual, real minutes (not the laundered ones in three weeks) from this meeting as it will be something.

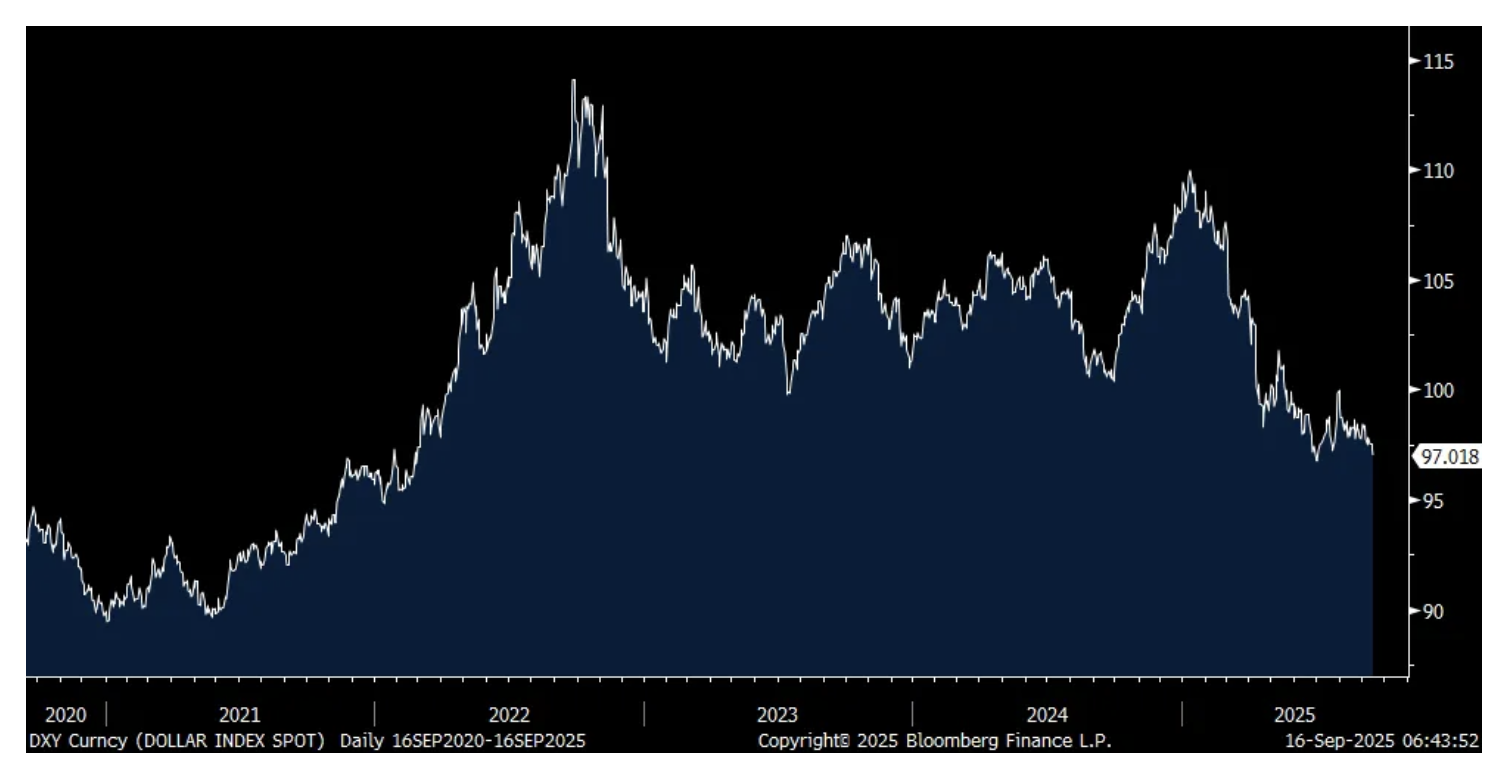

Ahead of the meeting with stocks at the highs and after a rally in Treasuries, the euro/yen heavy US dollar index is just .25 from a 3 ½ yr low and which makes imports even more expensive on top of tariffs that many pay on those imports. About 40% of US imports by the way are raw and intermediate term goods that end up in finished products. Gold in turn is at another record high.

If there is any hint by Jay Powell tomorrow that while he's on board for rate cuts but not by the 100 bps thru the rest of his term that the market is currently pricing in because we're still stuck at 3% inflation instead of 2%, we could get a reversal in the prices of just about everything that has melted up, as so many investors have been trained to just get long when the Fed cuts rates without regard to why they are doing so. Right now, the fed funds futures are pricing in a 100% chance of two cuts this year and a 62% chance of a third.

Also, market participants tend to view interest rate changes very simplistically. Higher rates bad, lower rates good. But, there is so much nuance to that. There is about $7 trillion of money sitting in money market funds that are going to produce less interest income for savers. Pile another $7 trillion of other fixed income that will do the same. Upper income spending has been a main driver of consumer spending and this cohort is about to make less money. On the other hand, anyone borrowing SOFR plus will certainly get relief and we'll soon see how long term Treasuries trade AFTER the fact to see the extent to which home buyers get help too.

DXY

This story I first saw last week can be very isolated or the beginning of something more. I don't know but wanted to bring it up because now the WSJ editorial page got a hold of it and it's worth watching if it ends up being the latter instead of the former. I'm referring to the company Tricolor, a subprime auto lender that filed for Chapter 7 last week. According to the WSJ, "it is liquidating after 18 years in business. The Texas-based firm specialized in lending to car buyers with no credit history or social security number, including undocumented migrants in the Southwest." Fifth Third Bancorp was one of the warehouse lenders to Tricolor and they announced last week they were a "one off" victim of fraud. Tricolor is being accused of fraud by pledging collateral twice to their lenders. If fraud, then this will be a 'one-off', but if a reflection of broader stress in subprime auto lending, then not. The article of that WSJ piece titled "Tricolor and the Subprime Debt Canary...Is the auto lender's surprise bankruptcy an outlier or a harbinger."

Dave & Buster's is down 16% pre-market and said this in their earnings call after missing both top and bottom line expectations and with comps down 3% y/o/y:

"Consumers are looking for value for their money and brands and companies that deliver that prosper even in tough macro environments...one of our priorities is simplifying our marketing message, simplifying our promotions, and making it easy for guests to understand what the real value is."

The rest of the call was very company specific with new management.

Steel Dynamics slightly raised guidance for the current quarter (they will report on Oct 20th) and said "Demand has largely been supported by the commercial, data center, manufacturing, warehouse, and healthcare sectors. Further, the accelerated announcements for meaningful domestic manufacturing investment and onshoring, coupled with the US infrastructure program are expected to positively impact demand for not only steel joist and deck products, but also for flat rolled and long product steel."

The September German ZEW investor confidence index in their economy did rise to 37.3 from 34.7, about 12 pts above expectations. However, the Current Situation weakened to -76.4 from -68.6. ZEW said "There are still considerable risks, as uncertainty about the US tariff policy and Germany's 'autumn of reforms' continues. The outlook has improved in particular for export-oriented sectors, which had recently suffered a strong decline. Among the industries that benefit most are the automotive sector, the chemical and pharmaceutical industry and the metal sector. Nevertheless, the three indicators for these industries continue to be in the negative range." Nothing market moving here though.

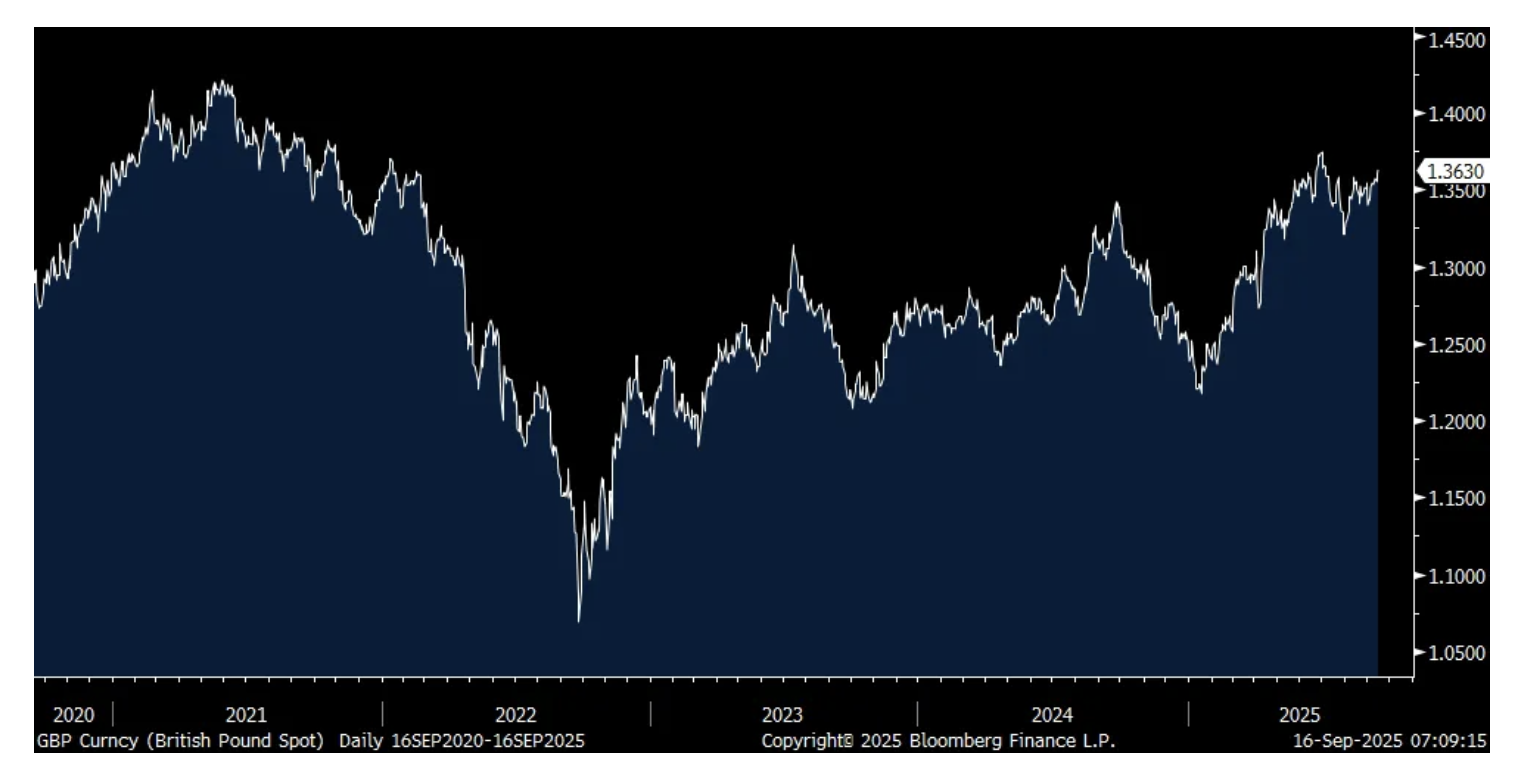

Ahead of the Bank of England meeting on Thursday, payrolls in August fell by 8k but that was 4k less than expected and through July, their unemployment rate held at 4.7% and employment in the three months through July was a bit above expectations. Wage growth continues to run above inflation, higher by 4.8% ex bonuses on a weekly basis, though down from 5% in the month before.

Market expectations for the BoE is that they will leave its base rate unchanged at 4% on Thursday and the pound is trading at its highest level since early July vs the US dollar after the jobs data.

US: Futs are higher, outperforming global counterparts. Bond yields are flat to down 1bp with USD weaker ahead of a widely expected 25bp cut and the resumption of the Fed’s easing cycle which paused in Dec 2024. Both Cook and Miran will be a part of the vote. Pre-mkt, Mag7 is displaying strength across multiple members with add’l TMT support from AVGO (+1.4%) and ORCL (+3.7%). Cyclicals and Semis are poised to lead but with pockets of strength in Defensives (HC, Stpls) also seen. Today’s macro data focus is on Retail Sales where Feroli is below the Street seeing a 0.1% MoM print and 0.3% for the Control Group.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday’s client and internal conversations were focused on whether we see any pullback post-Fed and, if so, what is the magnitude of such a pullback. The majority agreed that a pullback is more likely, and a majority of that cohort see only a 2-3% pullback into quarter-end. Separately, some voiced that until positioning gets stretched, we will not see a pullback, likely pushing timing to early or mid-October with the next support coming from the US 25Q3 earnings season. Everyone agreed that stocks will close the year higher than current levels. Separately, the broadening theme appears to be consensus though none felt comfortable being UW TMT / Mag7, but several expressed a view that China Tech is likely to lead in the very near-term.