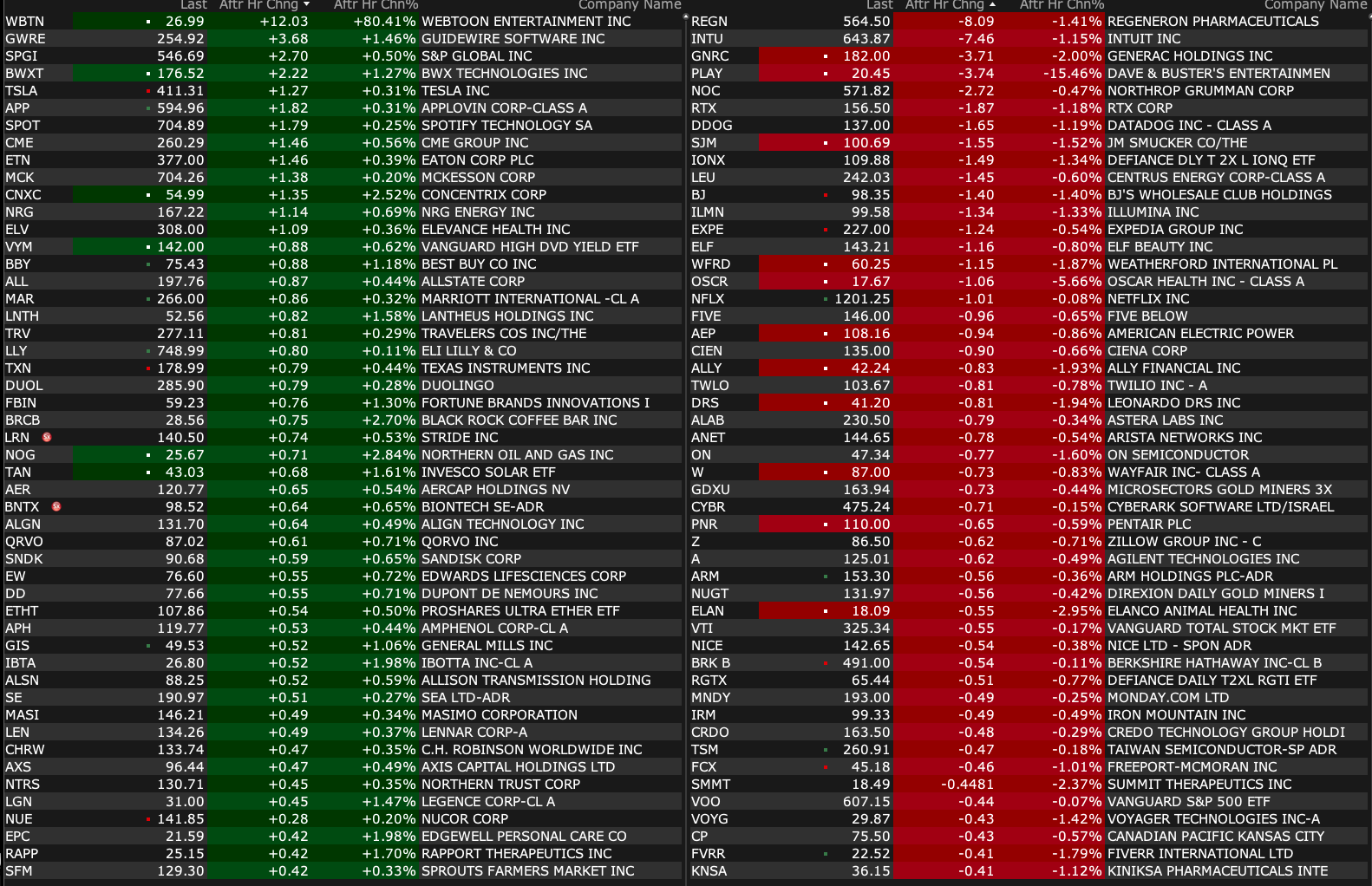

Monday's After-Hours Movers

As of 4:20 p.m.:

BY Doug Kass · Sep 15, 2025, 4:45 PM EDT

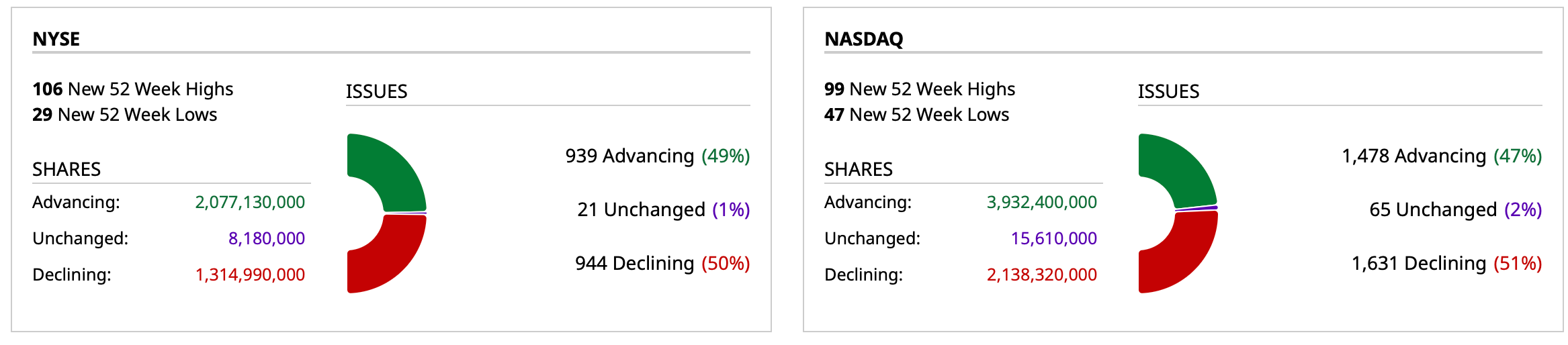

As of 4:20 p.m.:

BY Doug Kass · Sep 15, 2025, 4:45 PM EDT

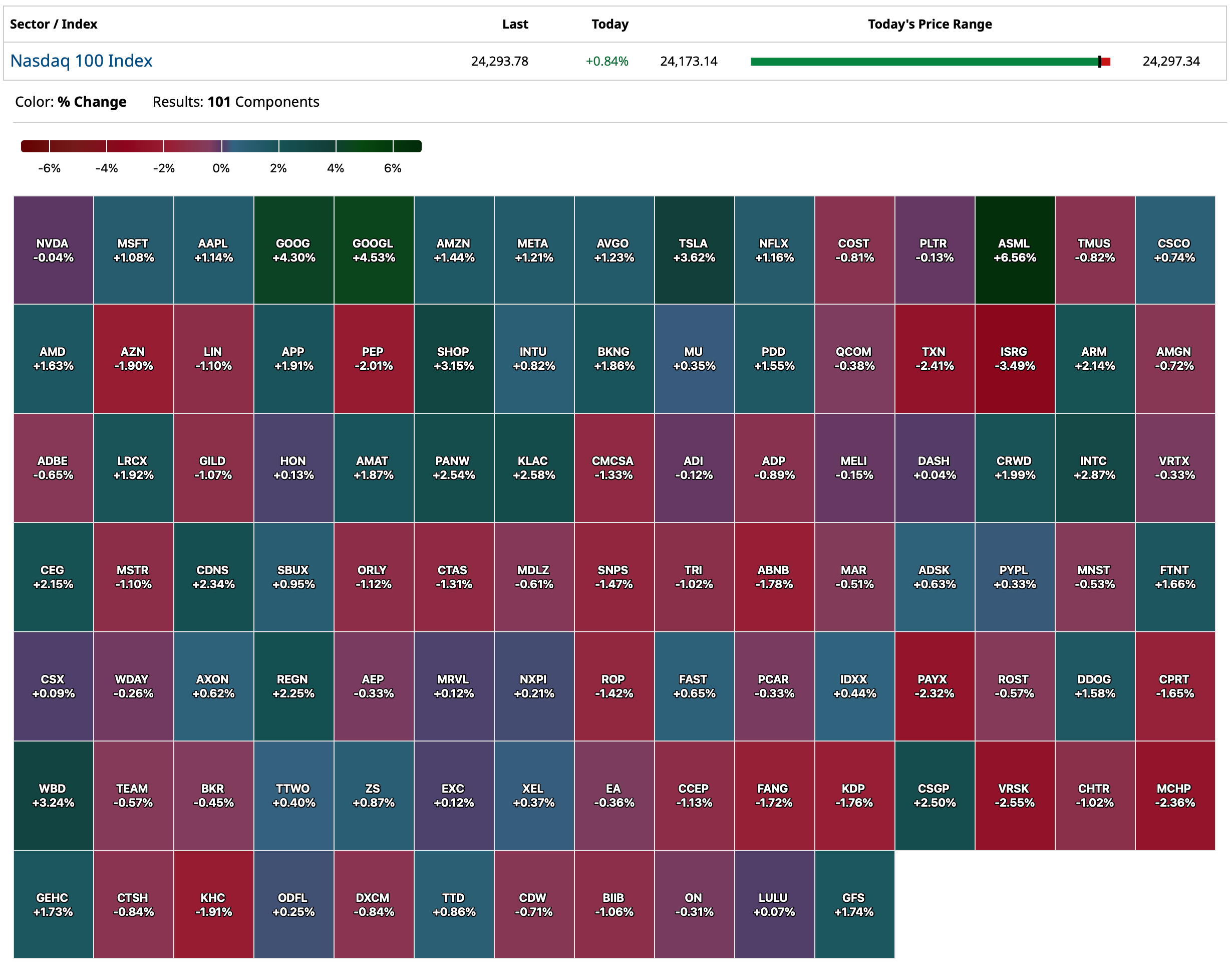

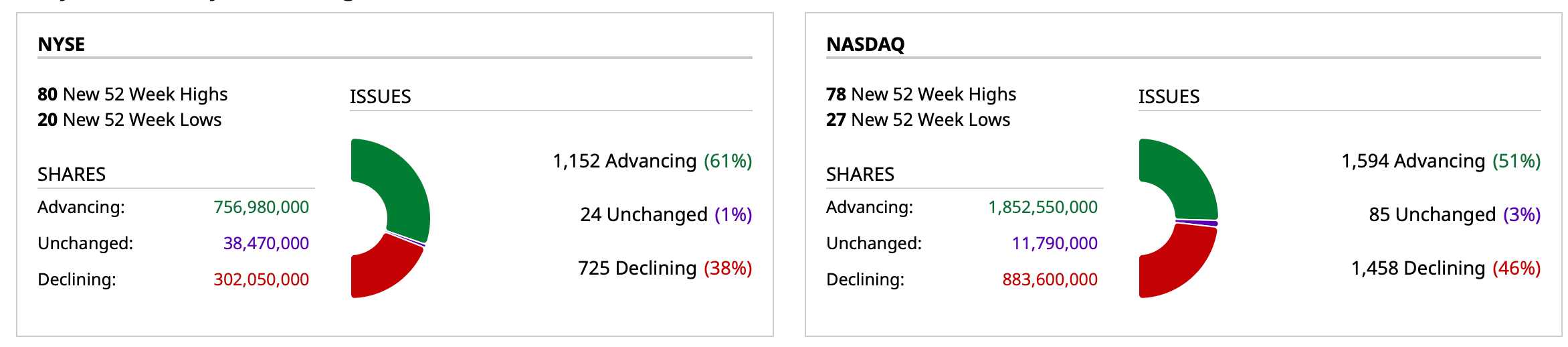

- NYSE volume 8% above its one-month average

- NASDAQ volume 9% above its one-month average

- VIX index: up 6.30% to 15.69

BY Doug Kass · Sep 15, 2025, 4:26 PM EDT

From Peter Boockvar:

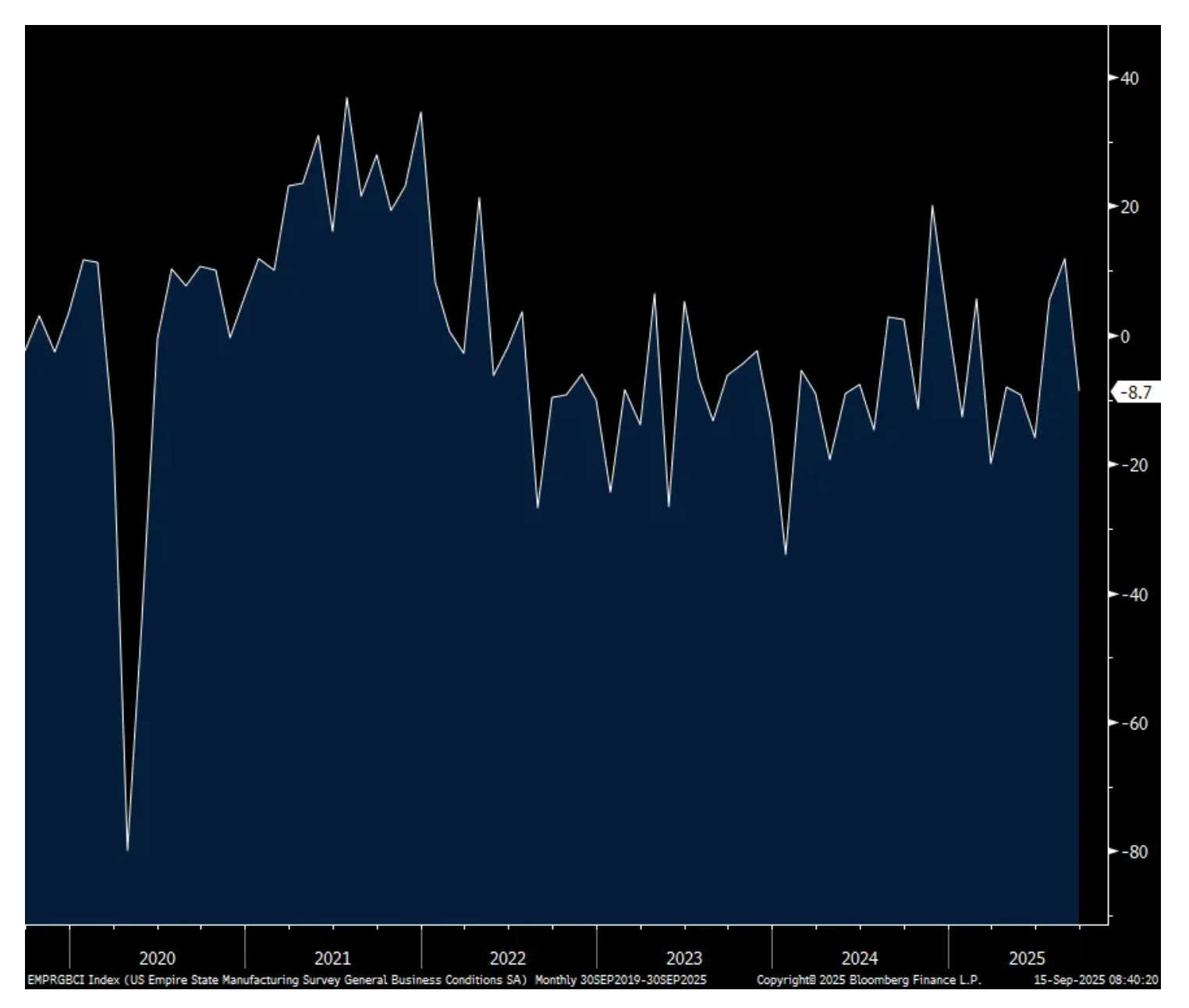

Manufacturing remains a tough sector in September

After two months of positive prints, the September NY manufacturing fell to -8.7. New orders went from +15.4 to -19.6, shipments to -17.3 from +12.2 and backlogs were at -6.9, below zero for a 4th straight month. Inventories too were less than zero at -4.9. Employment declined to -1.2 from +4.4 while the workweek went negative too at -5.1. Prices paid receded to 46.1 from 54.1 but was down a more modest 1.3 pts to 21.6 for those received and both remain elevated.

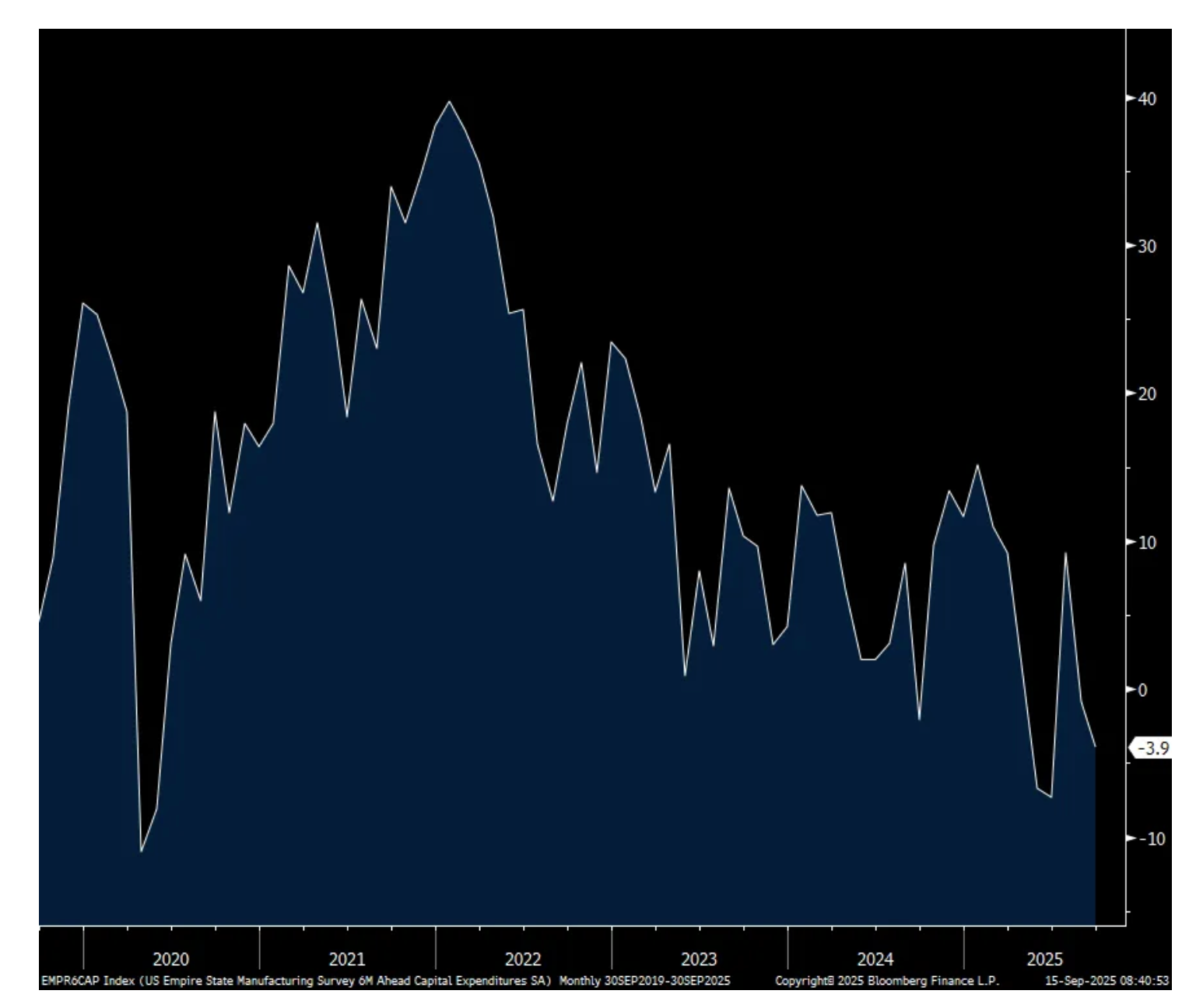

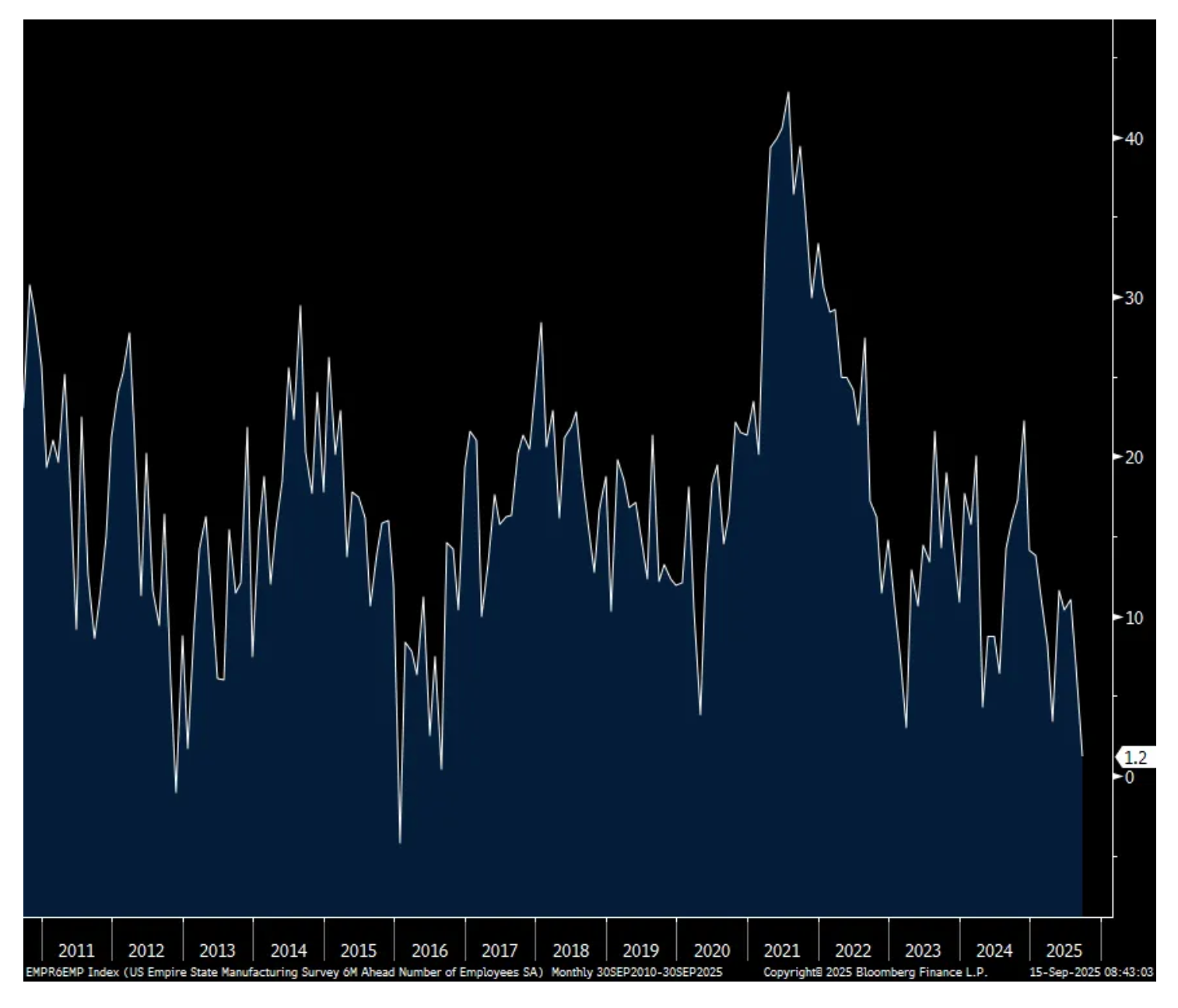

As for the 6 month business outlook, it dipped to 14.8 from 16 and that is a 4 month low. Expectations for employment fell to the weakest since 2016. On prices, they fell for those paid but rose to a 5 month high for expectations for prices received as tariff pass throughs continue. Capital spending plans were negative for a 2nd month at -3.9.

Bottom line, we’re still not getting help from the manufacturing sector of the US economy with tariffs not making it any easier, especially for those companies that source raw materials and intermediate stage stuff overseas that go into finished products.

NY Mfr’g

Prices Paid

Prices Received

Expectations for Capital Spending

Expectations for Employment

BY Doug Kass · Sep 15, 2025, 12:50 PM EDT

From Peter Boockvar:

Ahead of the Fed rate cut, I still believe in the benefits of positive REAL rates/Silver/France/China

Outside of the expected 25 bps rate cut on Wednesday, I believe the key thing to watch is what the long term REAL rate in the dot plot is. I assume it stays the same at 1%, with a nominal rate of 3% and thus assumes a 2% inflation rate sustainably, long term. It's important because while the Fed is shifting its attention to the labor market, the inflation rate focus should not be ignored and a fed funds rate ABOVE the rate of inflation I believe will always be the better way to conduct monetary policy.

A main critique I've had with the Fed over the past 20 years was their experiment with negative REAL rates that that came in response to the implosion of the tech bubble but then led to the housing bubble and was followed by nominal zero rates and with multiple rounds of QE to deal with the aftermath of that housing/bank downturn. Seven years of zero nominal rates and very negative REAL rates resulted in punk growth post GFC and then after Powell's attempt to at least bring them back to zero, he got spooked in late 2018/early 2019 (in part due to the tariffs then and the manufacturing downturn they caused) and we were back to negative REAL rates and which then followed after Covid and drove an eventual 9% inflation rate in the summer of 2022. By the way, it would have been well into the double digits if home prices instead of rents were used in the CPI calculation.

My point here is that low and stable prices are the foundation of healthy economic growth from which a low unemployment rate comes. Thus, while we're certainly getting some rate cuts this year, I believe we need a more notable decline in the inflation rate to get much more than 2-3 cut if the Fed sticks to the dot plot of forecasting positive REAL rates of 1%, give or take.

While I knew the answer before I even typed it in, for illustration here and to present the case, I typed into Gemini "Why should interest rates be above the rate of inflation?" This is what it told me:

"Interest rates should be above the rate of inflation to preserve the purchasing power of money, encourage saving over spending, and give consumers and businesses confidence in planning for the future by providing a real return on their money. When rates are higher than inflation, savings accounts and investments still grow in real terms, preventing wealth erosion."

With the massive misallocation of capital seen during the negative REAL rate and QE time frame, Gemini also said this, "Positive real interest rates are crucial for investment. Investors are more likely to invest when they can expect a real return on their capital, which drives economic growth and stability."

Also, "When interest rates are predictable and positive in real terms, consumers and businesses can plan their finances with more certainty about the future value of their money."

Moving on. With the price of gold finally exceeding its inflation adjusted January 1980 high, I wanted to highlight that if we inflation adjust the 1980 peak of around $50 for silver, it would be about $200 today. We still own and like silver.

While Fitch downgraded France's sovereign credit rating to A+ from AA-, French oats are rallying with yields down about 2 bps. Fitch said "France's general government debt ratio will continue to rise, reflecting persistent primary fiscal deficits. Fitch projects debt to increase to 121% of GDP in 2027 from 113.2% in 2024, without a clear horizon for debt stabilization in subsequent years...France's rising public indebtedness constrains the capacity to respond to new shocks without further deterioration of public finances." The euro is up too as is the CAC.

The economic data in China for August was softer than expected with retail sales, industrial production, fixed asset investment and property investment. Also, home prices, both new and existing, continued to fall. Notwithstanding all of this, Chinese stocks, particularly those that trade in Hong Kong continue to outperform as they got way to cheap and on the belief that their economy is showing some stabilization broadly and while the residential real estate market is still under pressure, we're already well into the adjustments and there are pockets of improvement.

I'll add more, my friends at the China Beige Book said this a few weeks ago in their August report, "China's Beige Book's August data show clear improvement in economic conditions. Almost all headline indicators improved on-year and on-month, as did nearly every sector. Consumer spending surprised to the upside and even residential realty rebounded this month." It was mixed elsewhere but overall the Chinese economy is hanging in there.

BY Doug Kass · Sep 15, 2025, 12:20 PM EDT

At 11:47:

BY Doug Kass · Sep 15, 2025, 12:00 PM EDT

CHWY is +$1.85 (+5%) today - taking a quick profit from my trading long rental last week.

BY Doug Kass · Sep 15, 2025, 10:53 AM EDT

I am maintaining my short positions in popular stocks - PLTR, NVDA, MSTR and HOOD. Shockingly I have profits in each of these shorts (with a large point gain in Strategy (MSTR).

BY Doug Kass · Sep 15, 2025, 10:47 AM EDT

Here are today's things:

* I added to my very large PEP long at $141.70.

* I added to a medium-sized MSOS at $4.25.

* I added to these very small financial shorts: GS $788.69 MS $158,10 XLF $54.04 and JPM $309.35.

BY Doug Kass · Sep 15, 2025, 10:26 AM EDT

I added to PEP at $141.70.

BY Doug Kass · Sep 15, 2025, 9:56 AM EDT

Dougie Kass

STAFF

7 minutes ago

I will be out of the office addressing my family member's health issue this afternoon so my posts will be less frequent and shorter.

Back to normal activity starting tomorrow morning...

BY Doug Kass · Sep 15, 2025, 9:45 AM EDT

From JPMorgan:

US: Futs are flattish with small caps leading amid a flat yield curve and flat dollar. Mag7 names are mixed with AAPL, AMZN, and GOOG up 90bp – 108bp; NVDA is down 2.9% as China launched an anti-dumping probe into chips with AMD and TXN down more than 2.5%. US / China trade talks enter a second day today. Cmdtys are mixed with Energy up and Ags / Metals down. Today’s macro data focus is Empire Mfg ahead of tmrw’s Retail Sales and Weds’ Fed Mtg.

and...

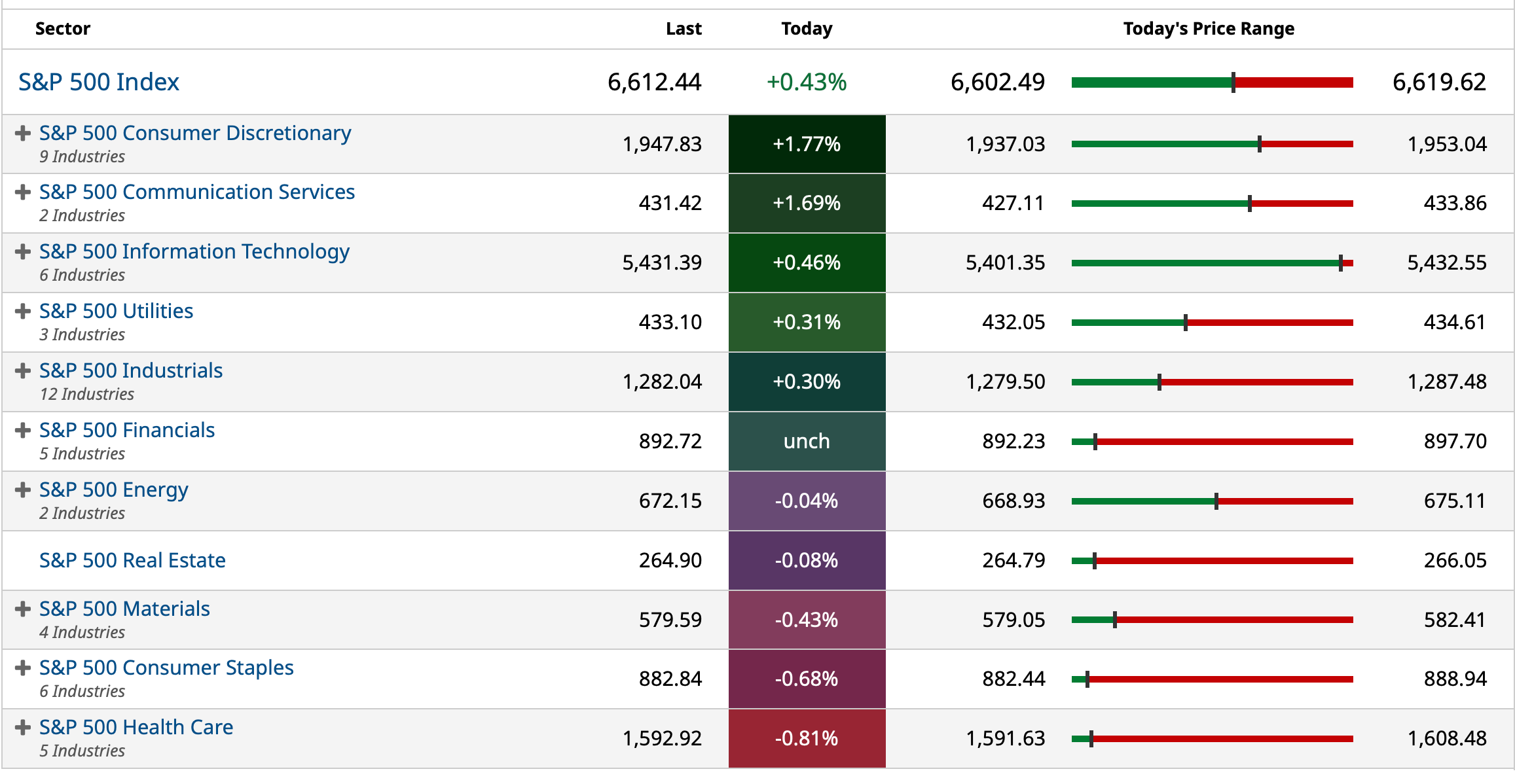

Last week, the SPX added 1.6% setting a new ATH on Thursday with NDX and RTY adding 1.9% and 0.3%, respectively. ORCL earnings helped reignite the AI trade without Quantum Computing (JPG1QTUM Index) and AI Data Centers (JP11DCEN Index) adding 12.9% and 6.6%. Within factors, Momentum L/S led, +7.8%, with Value L/S, the biggest laggard, losing 5.3% as Cyclicals outperformed Defensives by 4.4%. Healthcare had the most sub-sector dispersion, with our top basket adding 7.5% (Medicaid Exposure – JP1BCAID Index) and our bottom basket losing 5.6% (Potential Biotech M&A 2025 – JPBMNA25 Index). Aside from idiosyncratic stories, macro data focused on inflation, which appears to be enough to cement a 25bp cut this week, likely launching an easing cycle that lasts until 2027 as Fed Funds is expected to move to 3%.

As we shift our attention to this week, we are Cautious on stocks into month-end but think any pullback should be bought. As we look toward month-end, Fed Day may act as a “sell-the-news” event as investors take time to consider the macro environment, the Fed future reaction function, potentially stretched positioning, a temporarily weaker corporate buyback bid, waning Retail investor participation, and quarter-end rebalancing. In the Fed Day Scenario Analysis section (click here to skip to that section), we expand on our thinking as well as how we would play the outcomes.

· FED GOVERNOR COOK – Multiple media outlets are reporting that paperwork filed related to secondary homes was marked as ‘second home’ and not ‘primary’ refuting Pulte’s claims against her (CNBC, RTRS, WSJ). Separately, it is reported that Pulte’s parents claimed two homes as primary residences (CNBC, RTRS); it is unclear if the DOJ will investigate.

· GEOPOLITICS – On Friday, the US urged G7 sanctions on Russian oil, additional there could be secondary sanctions in the form of 50% – 100% tariffs on China and India for purchasing Russian oil. the US is prepared to mirror any tariff on China and India imposed by the EU. The goal is to cripple the Russian economy to end their invasion of Ukraine and curtail any potential expansion beyond Ukraine. Further, the US is telling the G7 to create legal pathways to seize frozen Russian assets to help fund Ukraine’s defense; these frozen assets total ~$300bn. WTI was up as much as 2.6% in the trading session before closing +0.5%.

· RETAIL SALES – Feroli sees Retail Sales printing 0.1% MoM vs. 0.3% survey; 0.5% prior. For Retail Sales ex-Autos 0.4% vs. 0.4% survey; 0.3% prior. For the Control Group, he sees 0.3% vs. 0.4% survey; 0.5% prior. The weaker headline number adds downside risk to 25Q3 consumption. XRT has gained 39.0% since the Apr 8 low vs. SPX +32.1%, a 687 bp outperformance. Our Cyclicals basket (JPAMCYCL Index) is 63.4% in the same time frame, Mag7 +58.6%, and XLY +35.3%.

· TRADE UPDATE – (i) Mexico plans to impose tariffs of as much as 50% on cars and other products made by China and several Asian exporters (e.g., South Korea, India), ahead of renegotiating USMCA; the deal is expected to be approved in the budget plan for 2026. (ii) Last Thursday, Lutnick signaled optimism around reaching trade deals with Taiwan, Switzerland, and India (“… sort it out once they stop buying Russian oil”); he added that South Korea has not yet formally signed the agreement it has reached with the US. (iii) US ambassador-designated to India Sergio Gor said that the US and India are “not that far apart” on tariff issues and indicated an agreement is forthcoming.

BY Doug Kass · Sep 15, 2025, 9:01 AM EDT

* The equity advance continues apace as investors ignore sticky inflation, moderating economic growth, uncontrolled government spending (and a rising deficit and debt load), historically lofty valuations and a possible peaking of the AI trade (which has been a prominent factor in the market's overall advance).

* Nevertheless, in the investment battle of late 2025 I favor Disraeli and Voltaire over Pangloss...

There is intense scrutiny on the employment report and CPI. Both sets of numbers are squishy at best, as well. I am not sure what the employment report tells us anymore and the CPI remains systemically understated.

The set of data that is accurate and might be the most important right now, is completely ignored by the markets and pundits. That is the data on the federal deficit. Here is a writeup on the latest numbers. I thought Secretary Bessent was going to be the adult in the room, but I guess not:

A few observations:

* Is it always appropriate to throw Food and Energy out of the CPI and focus on core? In current times, aren’t food and energy prices a function of fiscal, monetary and regulatory policy, as opposed to uncontrollable external events?

* Since when is the CPI (understated) printing at +2.9% and +0.4% month over month (core +3.1%, supercore +3.52%) considered good? Interesting exercise in mass psychology, if everyone says the number is good, I guess it is good.

* If you looked at the CPI (understated) and employment report, would it be reasonable to say we are in a "stagflationary" or "slugflationary" environment? But again, if nobody says it, apparently not.

* Theoretical question too, although we haven’t seen it yet. I thought the economy could be relatively recession proof (at least with regards to how the data are reported), because we are now a service-based economy. Recessions used to happen in a manufacturing based economy, when too much capacity was put in place. However, in the current economy, all of a sudden, one of the biggest components of growth is

With regard to why Food and Energy is out of the CPI, this article written by Steve Roach in May of 2021 explains the history of how and why it happened. He was working for the Fed in the 70s when it did. Also, interestingly he closes with:

“Today, the federal funds rate is currently more than 2.5 percentage points below the inflation rate. Now, add open-ended quantitative easing – some $120 billion per month injected into frothy financial markets – and the largest fiscal stimulus in post-World War II history. All of this is occurring precisely when a post-pandemic boom is absorbing slack capacity at an unprecedented rate. This policy gambit is in a league of its own. For my money, today’s Fed waxes far too confidently about well-anchored inflation expectations. It also preaches the new gospel of “average inflation targeting,” convinced that it can condone above-target inflation for an unspecified period to compensate for years of coming in below target. My students would love to throw out their worst grade(s) as well!”

Boy did he turn out right, because we know what happened next. So much for transitory inflation, I am still waiting for it to go away!

Also, interestingly (and as noted previously), AI has been nothing but inflationary so far. The obvious impact is on electricity prices. There have been no productivity gains yet, in fact productivity growth has slowed recently. AI as substantially boosted equity prices, which is inflationary. Even odder, it has been inflationary at the same time many of the service and infrastructure providers are selling it at a price that results in massive economic losses for them, to really so far just enable kids to cheat on their homework as roughly 70% of tokens processed seem to be due to the school year.

Interesting upside down world we now obviously live in. Oracle ORCL misses revenue and EPS, puts up a very squishy contract win (subject to numerous factors) and its stock goes up 40% and adds $300 billion of market cap. (We contend that the OpenAI "win" may mark a peak in AI equities, which have been the straw that stirs the market's drink):

and...

Just as hyperscalers morph from capital light to capital intensive — more resembling automobile and steel stocks than technology:

AI Adoption Rate Trending Down for Large Companies

"Dr. Pangloss, welcome to Wall Street, where it is indeed the best of all possible worlds."

- Randall Forsyth, Barron's (Up and Down Wall Street)

Pangloss, the unfailingly pollyannish tutor of Candide (the protaganist of Voltaire's novel by the same name) is considered a symbol of foolhardy optimism.

Though in the investment business, as in life, faith moves mountains — with the potentially toxic cocktail of sticky inflation, moderating economic growth, climbing U.S. debt loads, high valuations (in the 98% -tile), a market dependent upon the AI trade and gross speculation (e.g. Opendoor Technologies OPEN et al) reminiscent of the late 1990s — I remain cautious (and frustrated) as, for now, Dr. Pangloss is prevailing.

Nonetheless I am reminded of another turn of the phrase from Disraeli:

"What we have learned from history is that we haven't learned from history."

As well as a quote from Voltaire:

"History never repeats itself. Man always does."

Common sense is not so common.

BY Doug Kass · Sep 15, 2025, 7:40 AM EDT

* Naturally (with strong gains last week), technicians universally loved the chips — that was before the Nvidia news...

Bonus — Here are some great links:

Another Strong Week for Stocks

BY Doug Kass · Sep 15, 2025, 6:20 AM EDT

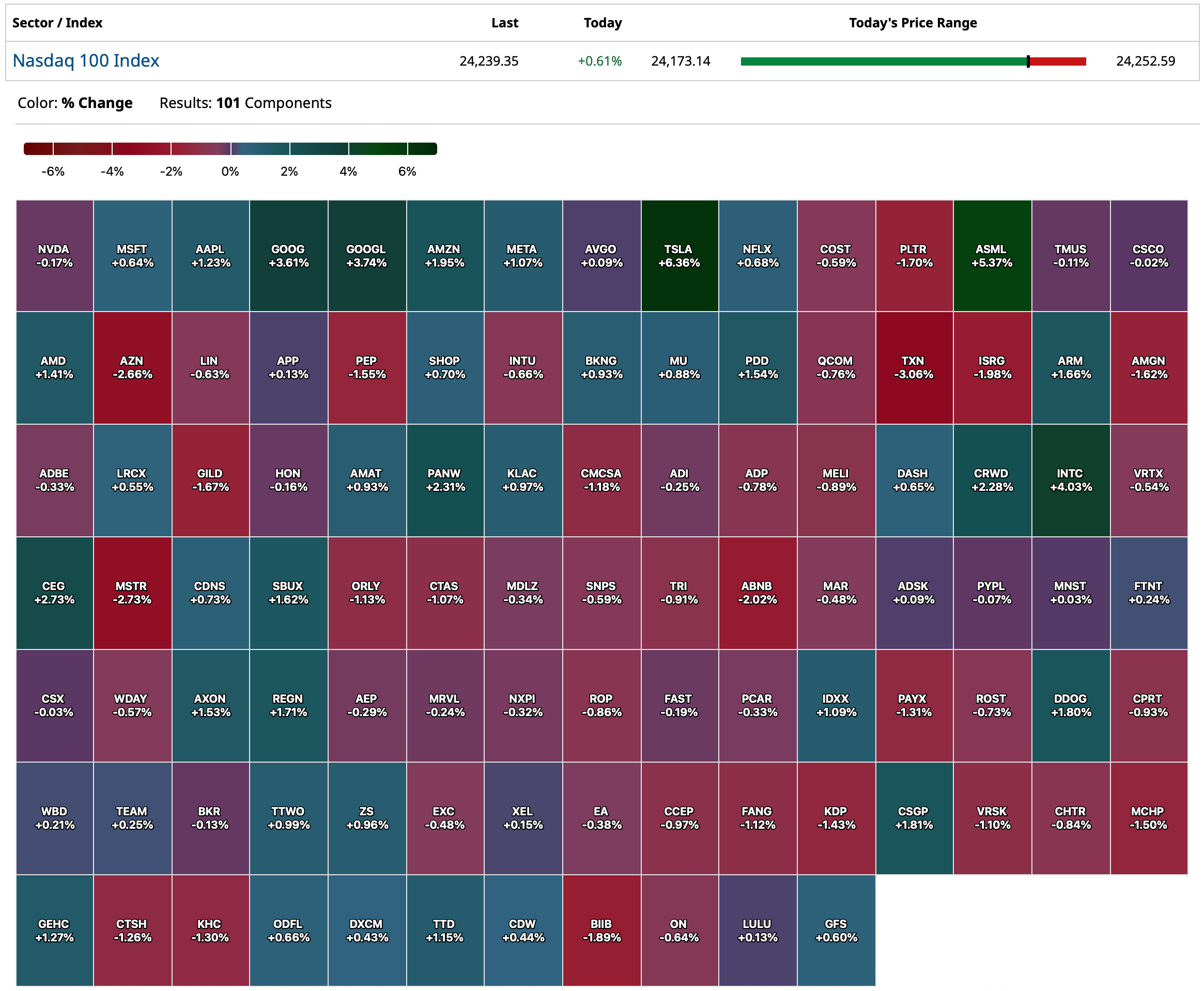

On Nvidia NVDA:

China: Nvidia violated anti-monopoly law, will continue investigation

In premarket trading, NVDA is -$5.50/share.

Late last week I contended that the Oracle ORCL contract announcement with OpenAI may have marked a peak in the AI euphoria.

I still believe so (and remain short of NVDA) and will expand upon this view and my market view this morning.

BY Doug Kass · Sep 15, 2025, 6:10 AM EDT

The S&P Short Range Oscillator stands at 2.39% vs. 3.21% — still overbought.

BY Doug Kass · Sep 15, 2025, 5:55 AM EDT

BY Doug Kass · Sep 15, 2025, 5:45 AM EDT

So far this year, AI capex, which we define as information processing equipment plus software has added more to GDP growth than consumers' spending.