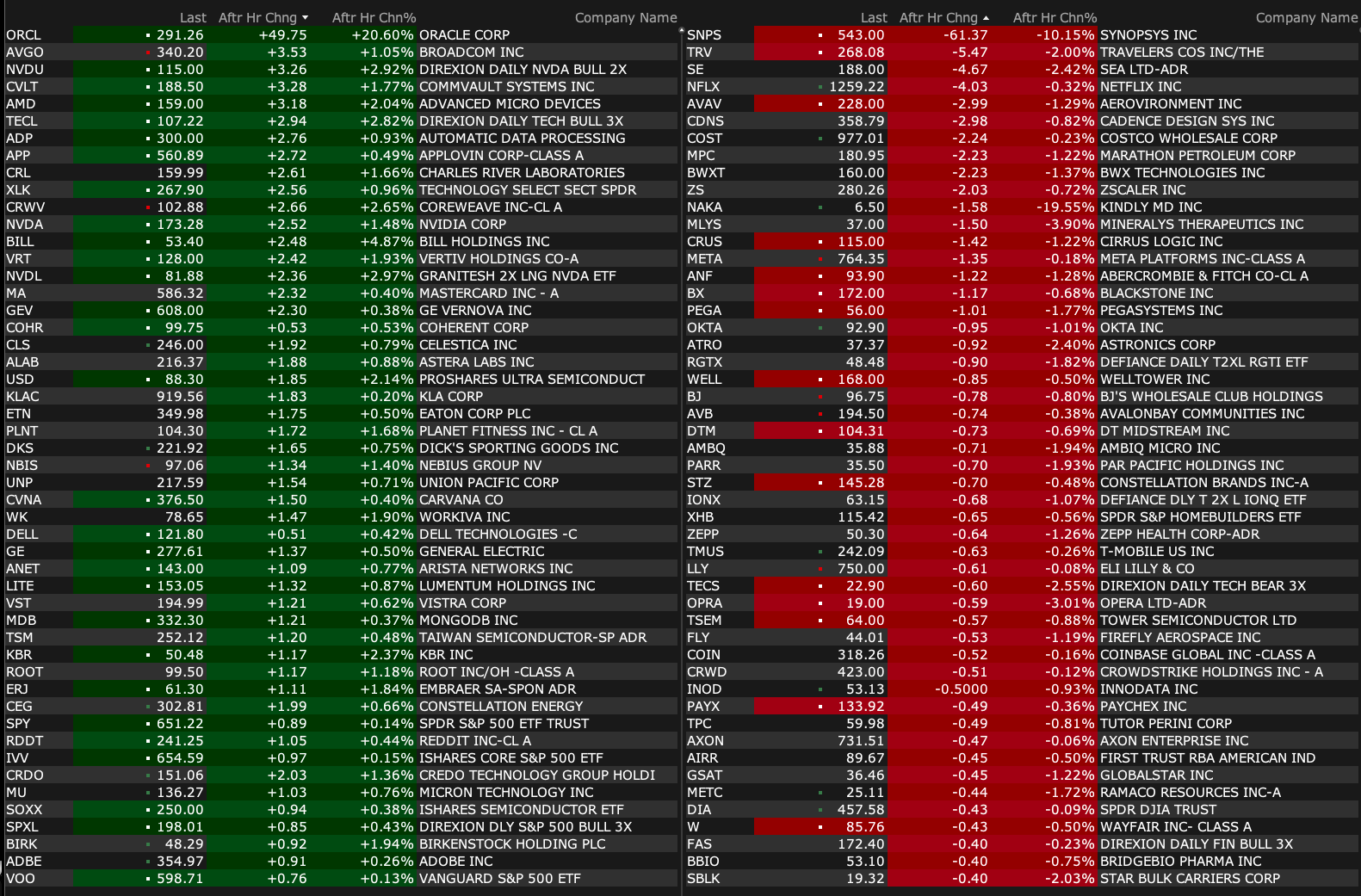

The Oracle ORCL backlog blowout (with Oracle future revenues ultimately still dependent on the availability of chips, companies' access to large sums of debt/capital and the need for a very large increase in power capacity) "could" mark the end of the AI trade.

As well, it should be recognized that the ramp in future revenue projections by Oracle will produce dramatically lower profit margins relative to the company's currently robust margins.

Moreover, those projected ORCL sales will be taken out of the pocket of some other large tech competition.

In the after hours on the shows, the exact opposite view was expressed.

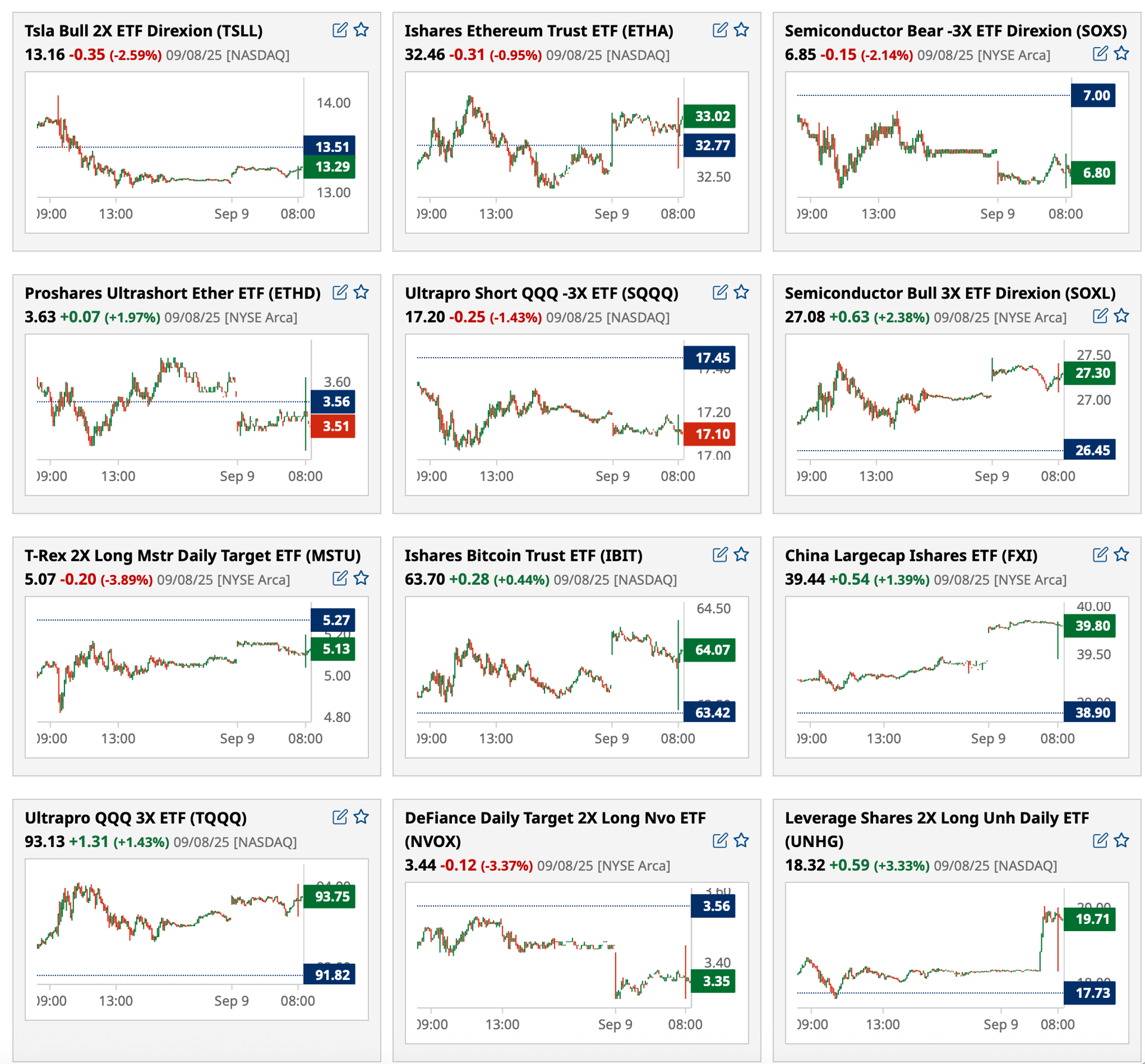

I remain short Apple AAPL. I added to my short yesterday morning. The shares are now -$3 to $234 (investors apparently don't like the iPhone 17 pricing):

Premarket Trading

I added to my very small-sized Tesla (TSLA) short in the premarket ($354.99).

I also added to my very small-sized Apple (AAPL) short in the premarket ($239.59).

"The economy is weakening....that's a big (jobs) revision."

- Jamie Dimon, JPMorgan

In a world dominated by investment products and strategies that worship at the altar of price momentum, I suppose it is not surprising that the economic warnings of JPMorgan's JPM Jamie Dimon — the most powerful banker in the world with the best economic data extant — is being ignored by the markets.

Calling an Audible on Homebuilders — Staying Opportunistic

* I plan to reshort strength...

I have covered my homebuilder shorts (with a plan to reshort strength) — as some constituents are down as much as -$7/share (on average between 3% to 5% lower on the day):

To watch for you while you're sleeping? Well, please don't be surprised when you find me dreaming too; It's just a box of rain, I don't know who put it there. Believe it if you need it, Or leave it if you dare; But it's just a box of rain Or a ribbon for your hair; Such a long, long time to be gone, And a short time to be there.

And as we close in on another anniversary of the World Trade Tragedy of 9/11 I miss Brown Bear (Chuck Zion) more than ever.

I will publish my annual tribute to Chuck and the victims on Thursday morning.

But I just got this great email from another dear friend of Chuck's who I have quoted frequently in the past - Don Gher.

Don's email to me this morning:

As 9/11 approaches, I am thinking about Chuck Zion, aka the Brown Bear, and I know you are, as well.

I thought of one of my favorite stories about his trading acumen. In 1983, I moved to Denver to work for their internal state fund and I was responsible for managing about $1 billion of the Equity portfolio. In my Springfield IL days, I was close to Salomon Brothers when I was managing one of the largest bond funds in the country but had also gotten to know Laszlo Biryini quite well from the Equity side. Laszlo's quant work leading the way, we were able to add Solly to our Equity broker list in Denver.

I had built a 500,000 share position in Texas Instruments with a big profit and it was near my price target. Working with the money flow work from Las, the stock looked toppy, as well. My trader and I put in an order to sell but at a 1/4 point higher. A few minutes later, the trader had me come into her office for a call with our trader in our new Salomon relationship, Chuck Zion. He said he could take the entire stock at the current price, a 1/4 point below the order. I was a little hesitant, then he said, "Donnie, the hardest part of investing is selling. Anyone can buy a stock. But when it comes to selling, you have gotten attached to the stock and drag your feet. You already made the tough decision to sell, don't let a quarter point get in your way."

We sold and a few days later the stock skidded down. Brown Bear was a true legend both as a trader and a person!

All my best,

Don

To all of my friends (some of whom are also subscribers) and who shared a friendship with Chuck over the years, please email me to share memories.

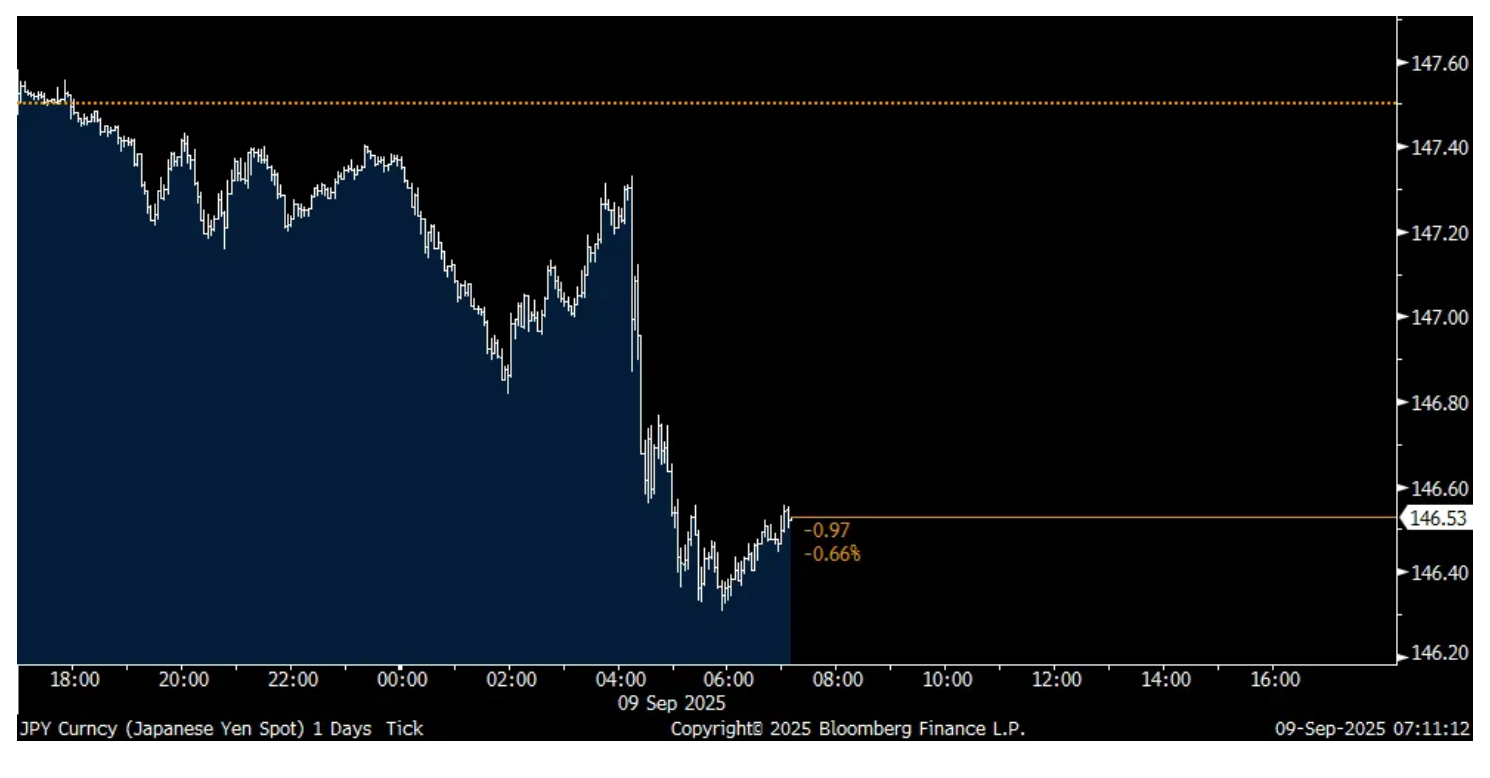

Yes, the Fed is going to cut multiple times but reminded today that the BoJ might hike multiple times

The yen is jumping to the highest level since July 23rd after a story hit Bloomberg at 4:15am est (so after the Japanese market closed) that said "Bank of Japan officials are of the view that it may be possible to raise the benchmark interest rate again this year regardless of domestic political instability, as economic conditions have developed in line with expectations, according to people familiar with the matter."

The story says they will likely keep rates unchanged next week but hiking in October and December are now real possibilities. The story went on to say, "the economy has performed as expected, with steady progress toward the bank's stable inflation target, and the trade deal signed last month removed some potential risks to growth, according to the people."

We'll see how cash JGB's trade tonight but JGB futures are trading lower with yields up and European and US yields are ticking higher too in response after the drop over the past few days. French yields by the way are little changed as President Macron is now looking for another Prime Minister. I still don't think we're out of the woods with respect to long term global sovereign bonds.

On gold, which is at another fresh record high and we remain bullish and long, though could be due for a correction at any moment, its importance as a global reserve asset continues to grow with central bank buying the main driver for 3 years running and more global trade settling in gold for those that don't want to transact in US dollars.

Yen intraday day move on story

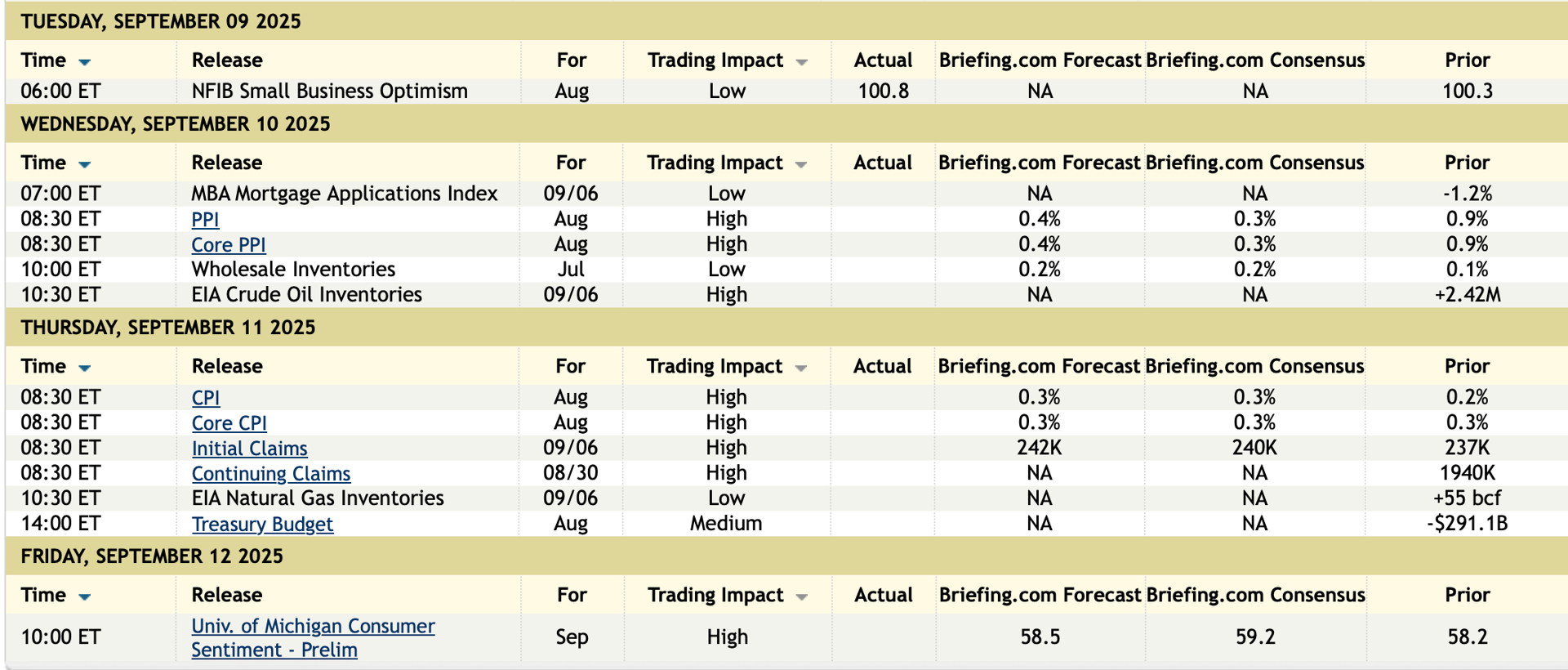

As we await the benchmark payroll revision today for the 12 months through March from the BLS with the possibility of a downward adjustment of about 700,000 jobs, understand that this is where the birth/death model, which estimates job changes each month, is reset to reality and will reflect what actually took place.

Speaking of reality, or lack thereof in government inflation stats, as I read in the Financial Times yesterday, according to Mercer, "The cost of companies' health insurance plan for employees is expected to jump by an average of 6.5% in 2026, the biggest increase in 15 years...For people who buy health insurance on government exchanges, the median increase for 2026 is 18% - more than double last year's 7% rise, according to KFF, a non-profit health policy research group." In the July CPI, health insurance prices were up 4.4%. The PCE for Q2 said overall health care inflation was up by 3% (I don't have health insurance component) and a big chunk is Medicare and Medicaid reimbursement rates, artificially suppressed. Yes, Fed policy has little impact on health insurance prices, outside of the changes in the labor market and thus demand for company provided healthcare, but it still is a major cost of living and we'll see what actually happens next year.

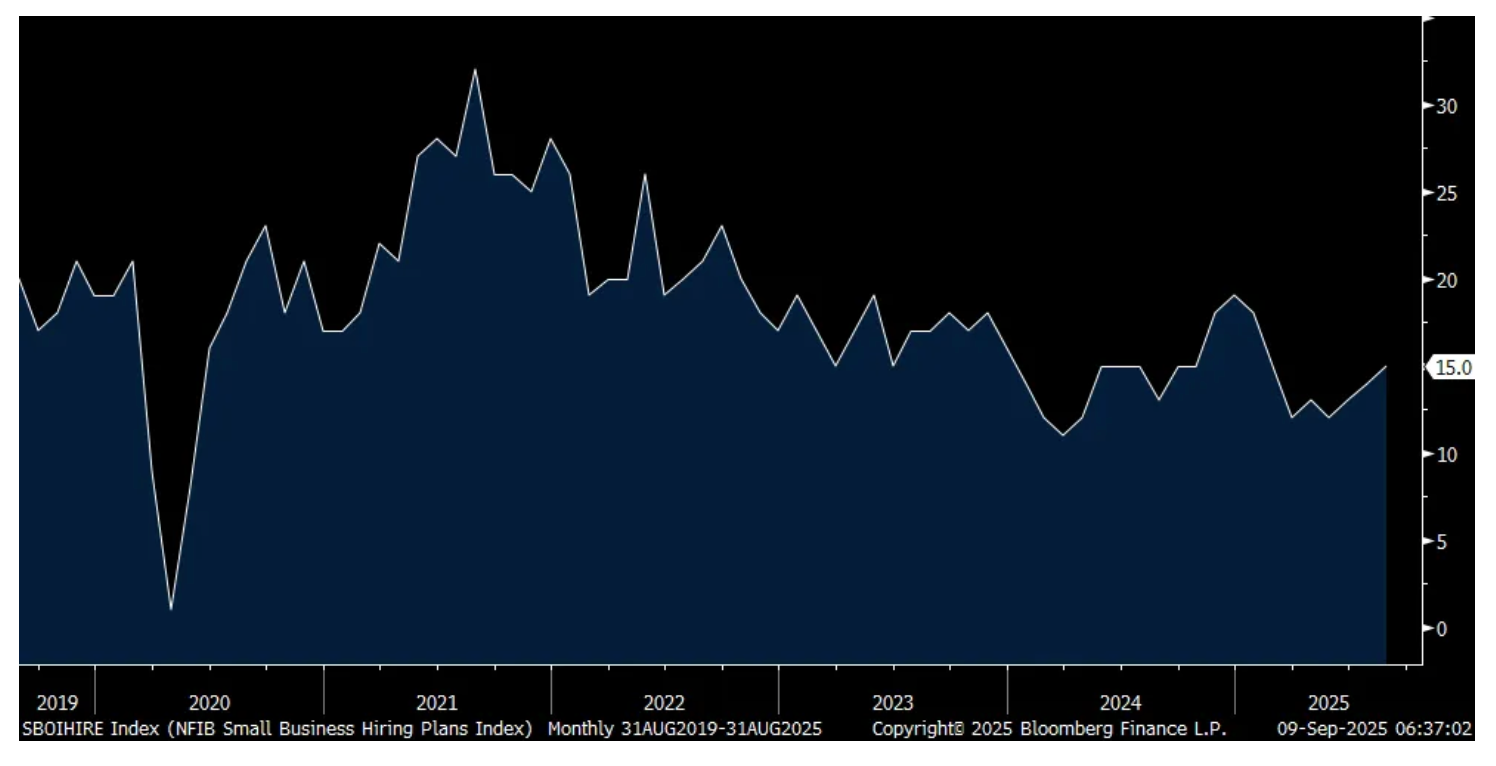

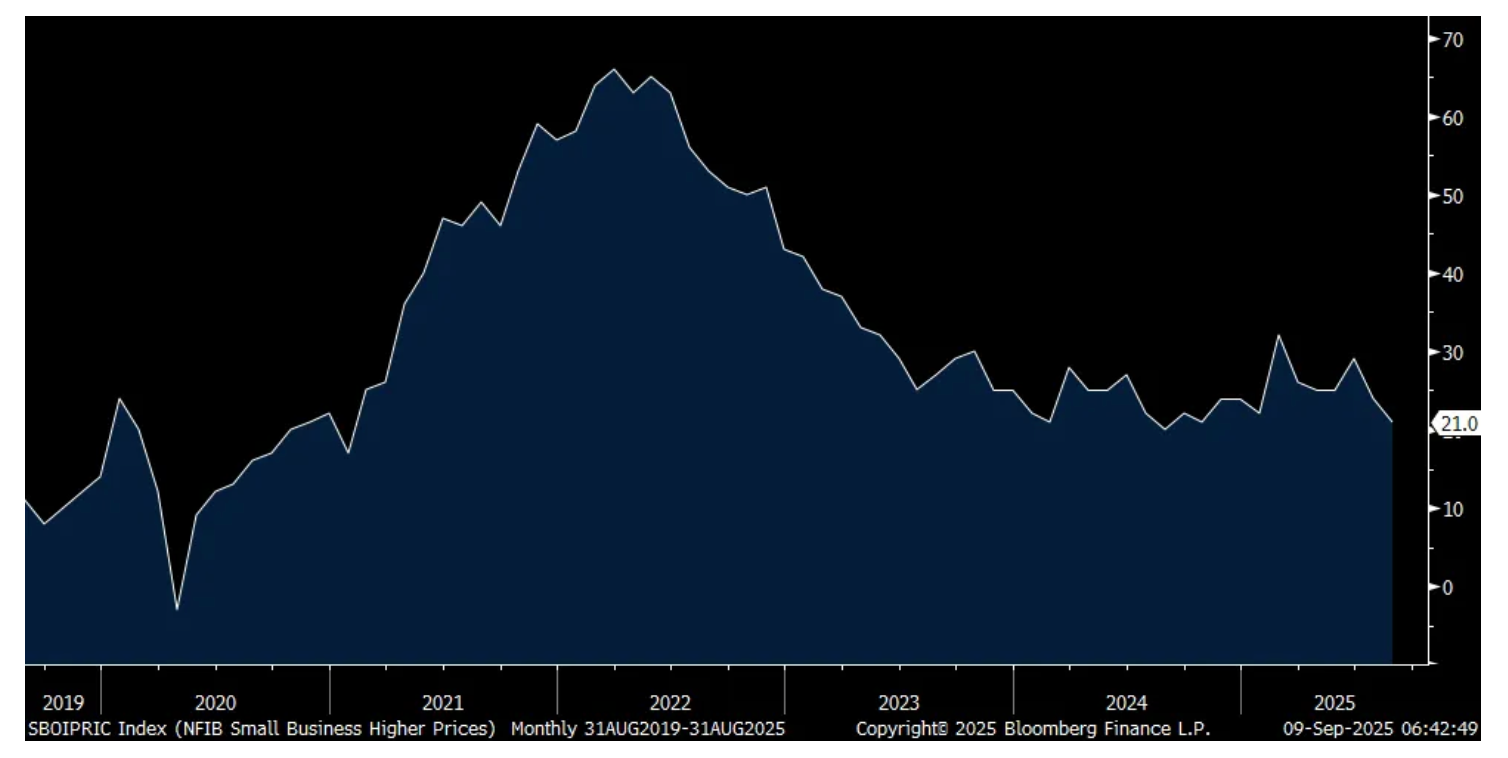

With respect to the business mood of small business, the NFIB Small Business Optimism index for August rose .5 pt m/o/m to 100.8 and that is the highest since January and for comparison it was at 93.7 in October 2024, reached 105.1 in December and was 104.5 in February 2020.

While the labor market has reflected a clear slowdown in hiring in a variety of metrics, Plans to Hire rose 1 pt to 15%, matching the most since January when it was at 18%. Confusing things though is the drop in job openings that are hard to fill which fell to 32%, matching the lowest since July 2020. The NFIB said "The difficulty in filling open positions is particularly acute in the construction, manufacturing, and transportation industries. Nearly half (49%) of small businesses in the construction industry had a job opening they could not fill, down 6 pts from July and 11 pts below last year's level. This suggests a softening in the job market." After falling in July, the two compensation components were higher.

Capital spending plans fell 1 pt after rising by 1 pt in July while there was no change in inventories. After increasing by 14 pts in July, those that Expect Better Economy fell 2 pts as did the Good Time to Expand component after rising by 5 pts last month. Those that Expect Higher Sales doubled to 12%, which was a key reason why the headline number rose m/o/m and there was a 3 pt rise in the earnings component.

Of note too, Higher Selling Prices fell 3 pts to 21%, matching the least since August 2024. But NFIB said it's still above the average of 13% "suggesting continued inflationary pressure." On expectations of Fed rate cuts priced into the forward curve, the average rate paid on a loan fell to 8.1% from 8.7%.

Lastly, "In August, the percent of small business owners reporting labor quality as the single most important problem for their business remained at 21%, continuing to rank as the top problem."

Nothing market moving here but we certainly watch the small business sector closely as they are most sensitive to many challenges that an economy faces, particularly with the cost of capital, tariffs, regulations, taxes, etc... relative to bigger companies.

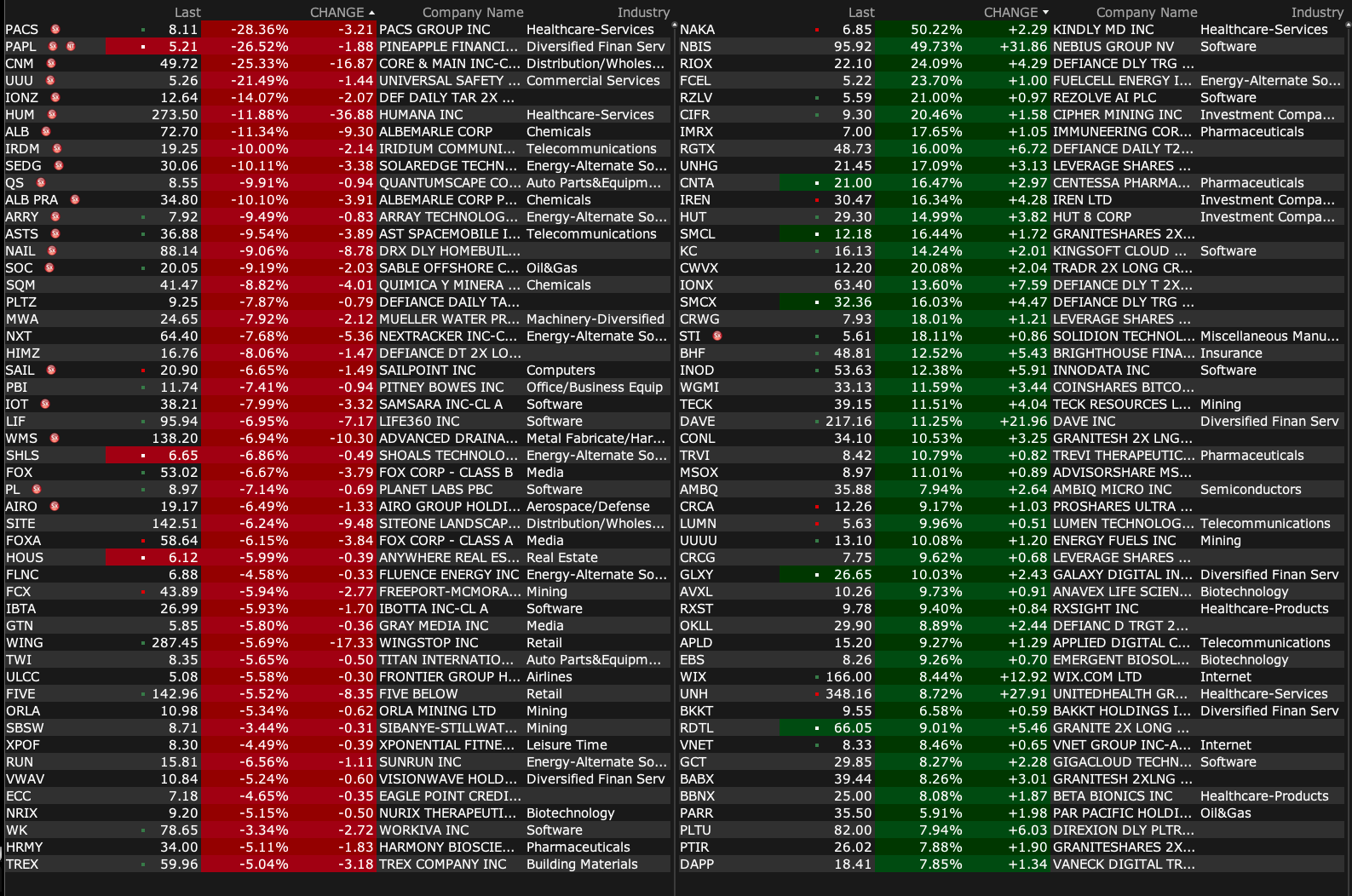

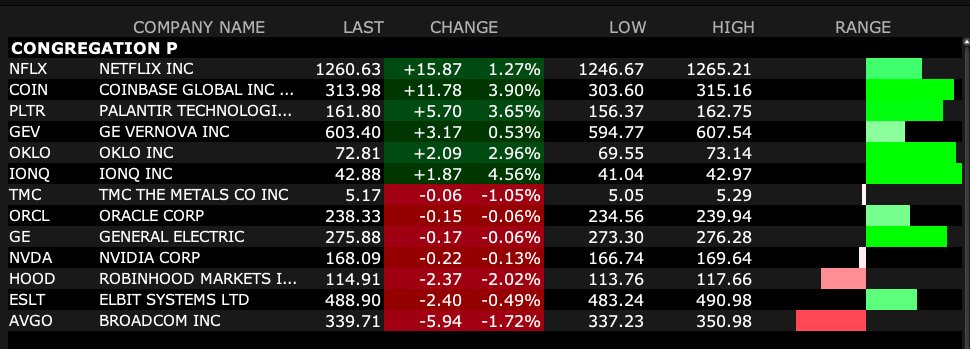

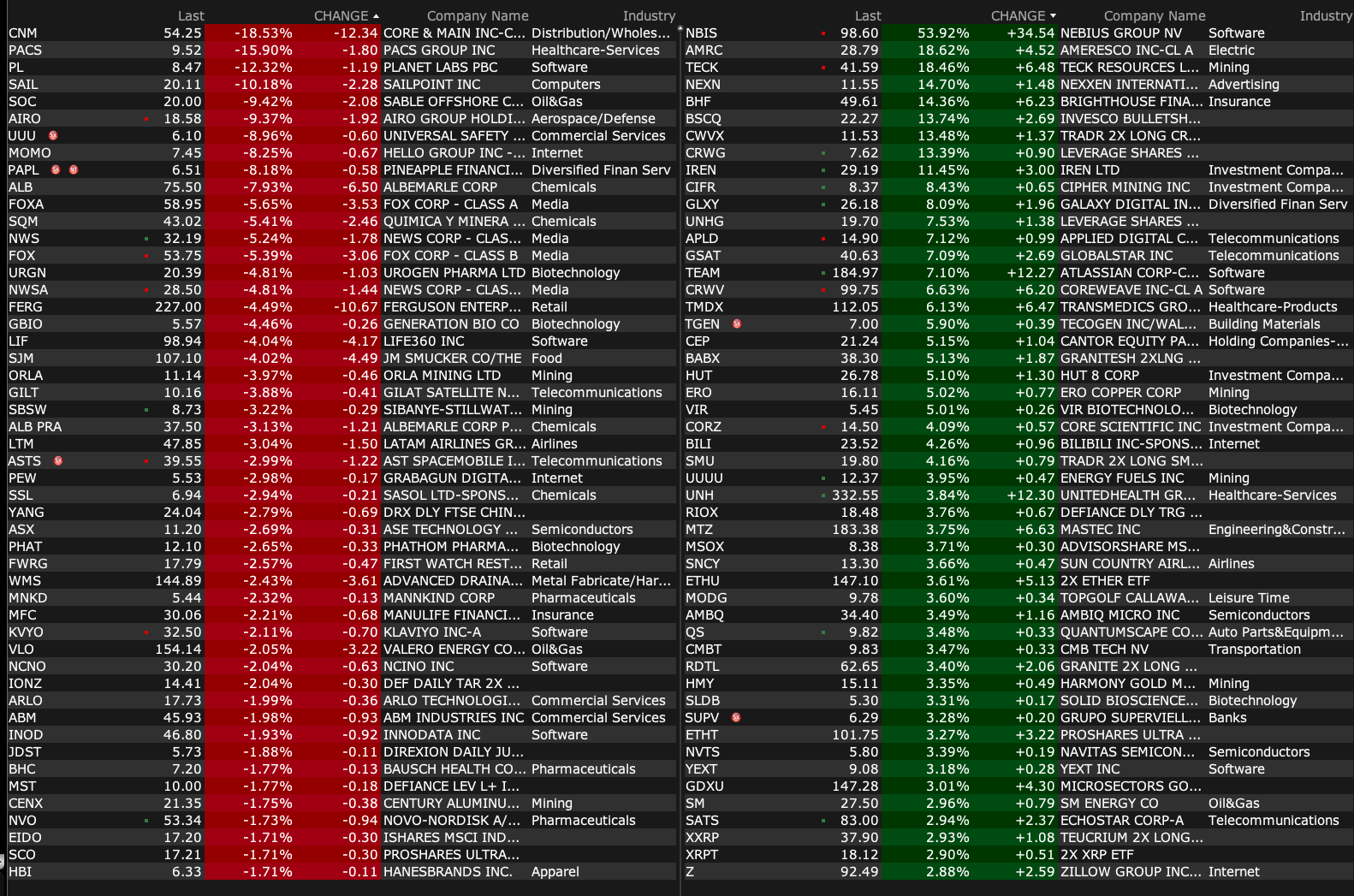

-MMA +150% (Donald Trump, Jr. joins as strategic advisor)

-WOLF +60% (Plan of Reorganization confirmed, clearing path to emerge from restructuring process in the next several weeks)

-TRML +58% (to be acquired by Novartis at $48/shr for EV $1.4B)

-ZONE +57% (earnings)

-NBIS +55% (announces ~$17.4B agreement with Microsoft for AI infrastructure through 2031)

-TECK +18% (Teck and Anglo American confirm to combine through merger of equals valued at ~$53B)

-BHF +12% (Aquarian is in advanced talks regarding raising the funds to finance the acquisition of the co., seeking to raise >$3.0B)

-CRWV +6.8% (higher in sympathy with NBIS; launches CoreWeave Ventures to invest in AI companies)

-KFY +6.4% (earnings, guidance)

-UNH +3.7% (preliminary Centers for Medicare & Medicaid Services (CMS) Medicare Advantage star ratings for Star Year 2026 / Payment Year 2027; ~78% of its membership in 4 star or higher plans)

-DKS +2.2% (CitiGroup Raised DKS to Buy from Neutral, price target: $280)

Downside:

-CNM -18% (earnings, guidance)

-PACS -13% (appoints Mark Hancock Interim CFO, effective immediately)

-PL -12% (files to offer up to $300M in Convertible Senior Notes due 2030)

-SOC -9.4% (reportedly California Governor Newsom to propose additional restrictions on offshore oil in exchange for onshore production)

-SAIL -8.5% (earnings, guidance)

-ALB -7.9% (weakness from easing supply expectations for lithium)

US: Futs are higher led by Tech as the rally appears poised to continue. The yield curve is bear steepening, USD is flat, and cmdtys are pushing higher with broad-based strength across all 3 complex but notable increases in crude, natgas, coffee, and iron. In stocks, Mag7 are seeing a muted bid with AVGO / NVDA leading Semis higher. Both Cyclicals and Defensives have a pre-mkt bid with Materials buoyed by the Anglo / Teck deal. Today’s macro data focus is on the NFP revision with BBG survey seeing a 700k negative revision to payrolls and the NFIB Small Business Optimism where the Hiring sub-index has been a leading indicator for future NFP prints.

and...

US MKT INTEL CPI SCENARIO ANALYSIS

Feroli’s CPI preview is here. For CPI he sees Headline MoM printing +0.36% and Core MoM printing +0.31%, both numbers are above the Street. This equates to 2.9% YoY for Headline (up from 2.7% last month) , a seven month high, and 3.1% YoY for Core.

The following scenario analysis is NOT A PRODUCT OF JPM RESEARCH, this is a trading desk view fromJPM US Market Intelligence. This month we focus onCore MoM outcomes and 1-days SPX moves.

· WHAT ARE OPTIONS PRICING? Options that expire on Tuesday are pricing ~92bp move based on Monday’s (Sep 8) closing prices. This is touch lighter than usual when we typically see about a 1.25% implied move.

· US MARKET INTEL – Similar to our NFP analysis, we think the outcomes are skewed positively as we think Powell’s Jackson Hole speech cemented a 25bp cut for September. We do not think there is a credible threat to the print that would force the Fed to remain paused in September. However, we do think a materially hawkish print here adjusts the Fed’s reaction function to October and December meetings. Stated plainly, if we see a spike to inflation in this print then it is likely we see inflation acceleration into year-end and into 2026. That outcome is likely to keep the Fed on the sidelines for Oct / Dec especially if GDP growth metrics continue to move higher. Alternatively, a dovish print will increase expectations for the Fed to cut by 50bp in September, which is a positive tail-risk.

I thought that it was signficant that Mike Tyson was on a lengthy podcast with the Trump administration's Steve Miller's wife discussing the merits of cannabis rescheduling (this tweet was reposted by Elon Musk!):