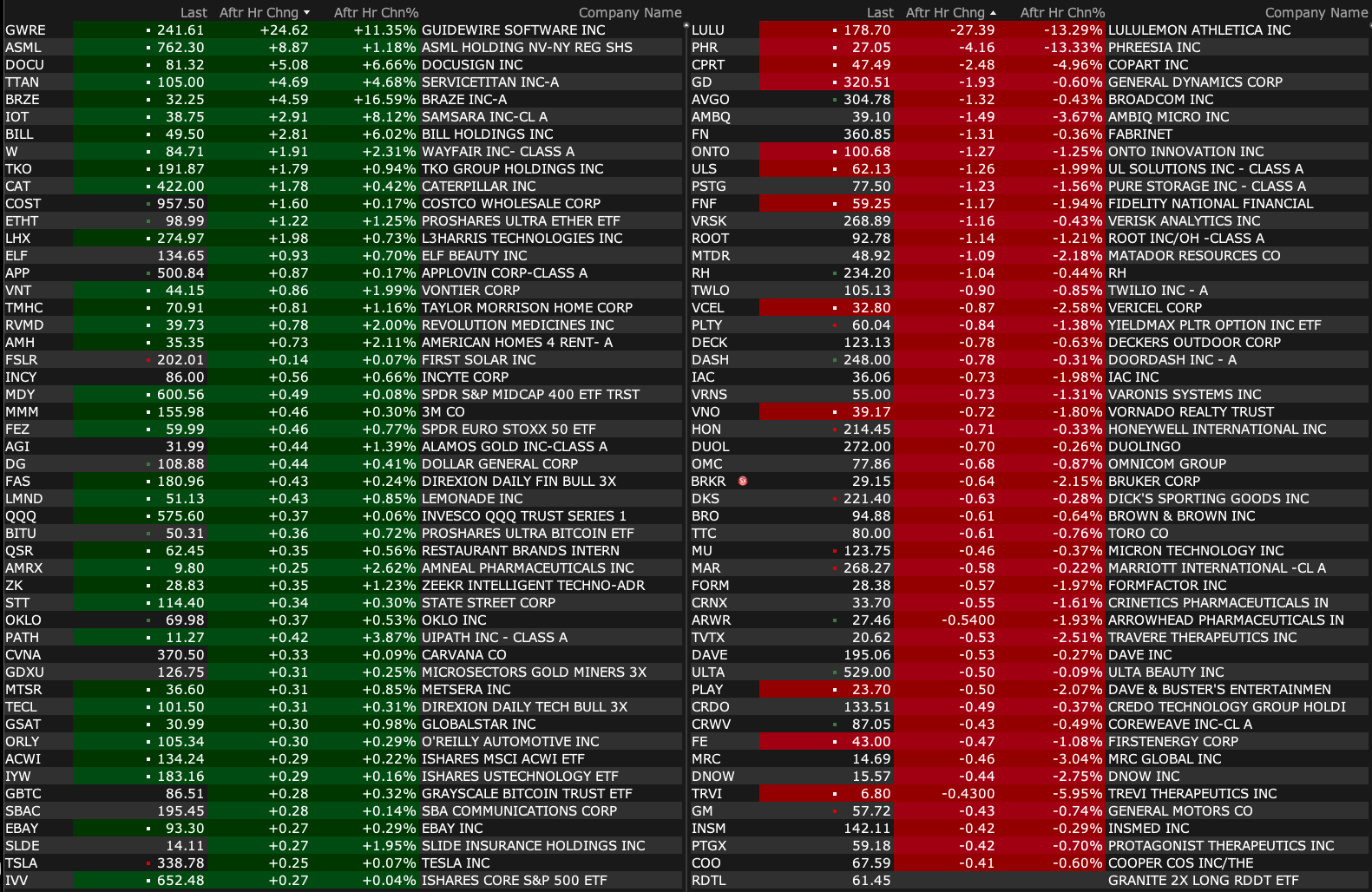

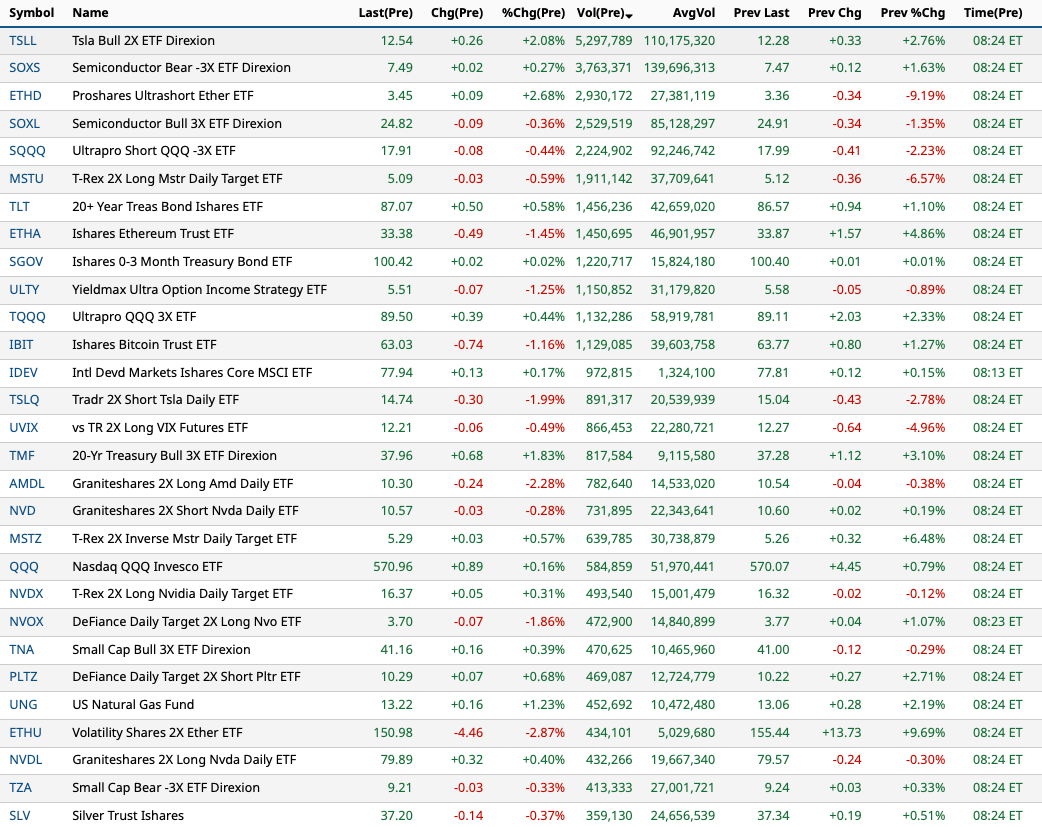

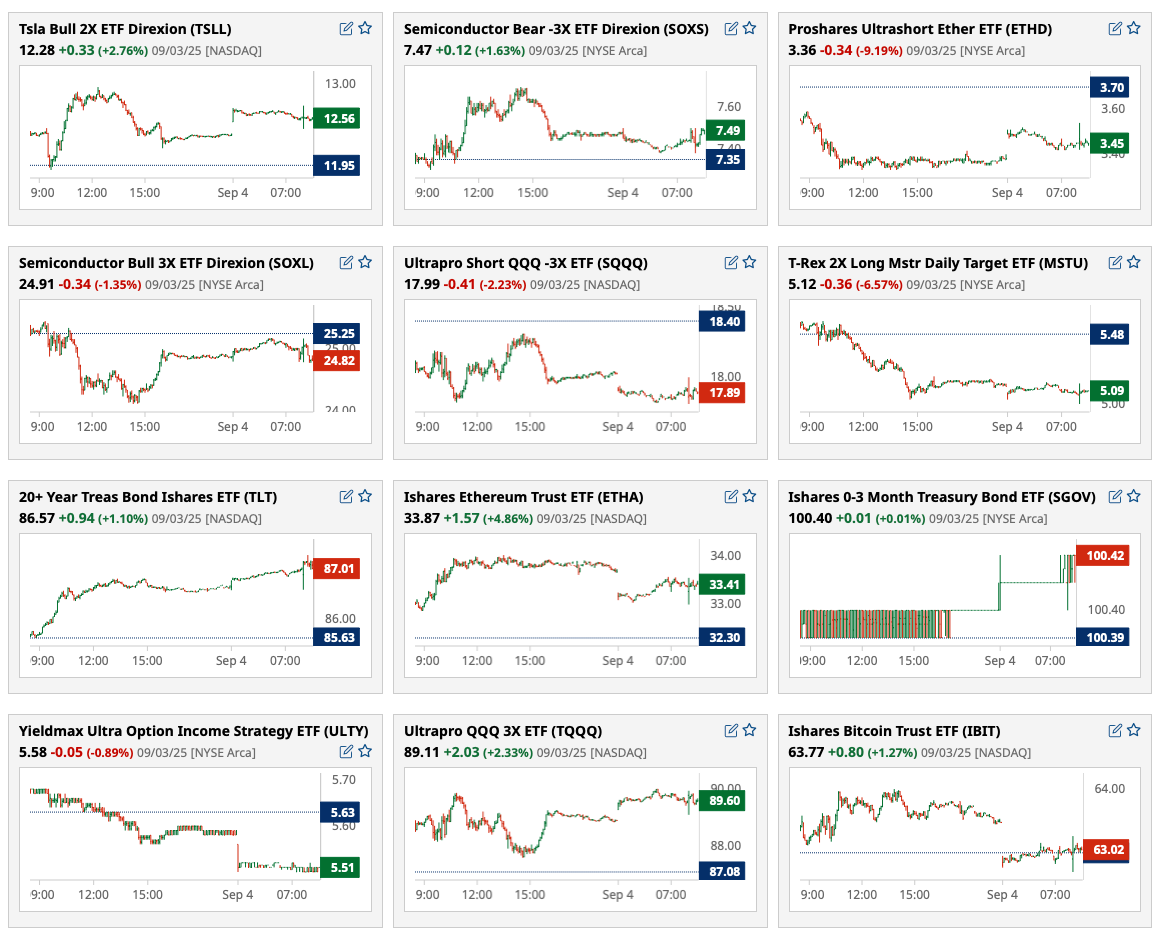

Thursday's After-Hours Movers

At 4:20 p.m.

BY Doug Kass · Sep 4, 2025, 5:00 PM EDT

At 4:20 p.m.

BY Doug Kass · Sep 4, 2025, 5:00 PM EDT

BY Doug Kass · Sep 4, 2025, 4:55 PM EDT

BY Doug Kass · Sep 4, 2025, 3:38 PM EDT

I am taking off some of my AMZN long at $234 now.

BY Doug Kass · Sep 4, 2025, 1:35 PM EDT

Randy

Fed Speak

Fed's Williams Says He Expects Gradual Interest Rate Cuts Over Time If Economy Meets His Forecast; Fed Must Balance Inflation And Job Market Risks Right Now; Monetary Policy Modestly Restrictive, Appropriate For Current Economy; Trade And Immigration Factors Slowing Activity, GDP Will Grow 1.25%-1.50% This Year; Expects Jobless Rate To Rise To About 4.5% Next Year; Sees PCE Inflation At Between 3.00%-3.25% This Year, 2.5% In 2026; Expects Inflation To Get Back To Fed's 2% Target In 2027.

Williams Says Clear Signs Tariffs Are Impacting Prices, Buying Patterns; So Far, Tariffs Don't Seem To Be Pushing Long-term Inflation Rise; Tariffs Likely To Add 1.00%-1.50% To Inflation This Year; Labor Market Cooling To Pre-Pandemic Trends; Labor Market Is Currently In Balance; He Is Monitoring Data To Watch For Contraction In Banking Reserves.

BY Doug Kass · Sep 4, 2025, 1:30 PM EDT

Doing little today.

I am marveling at the continued advance.

BY Doug Kass · Sep 4, 2025, 12:20 PM EDT

More Index shorts:

* SPY $646.05

* QQQ $572.22

BY Doug Kass · Sep 4, 2025, 11:45 AM EDT

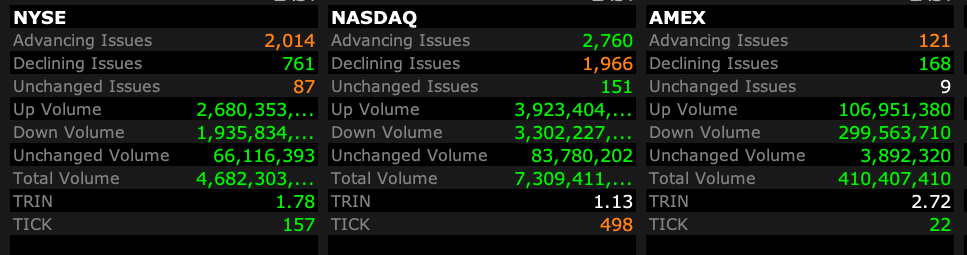

- NYSE volume 4% below its one-month average;

- Nasdaq volume 21% below its one-month average;

- VIX index: down 3.79% to 15.73

BY Doug Kass · Sep 4, 2025, 11:07 AM EDT

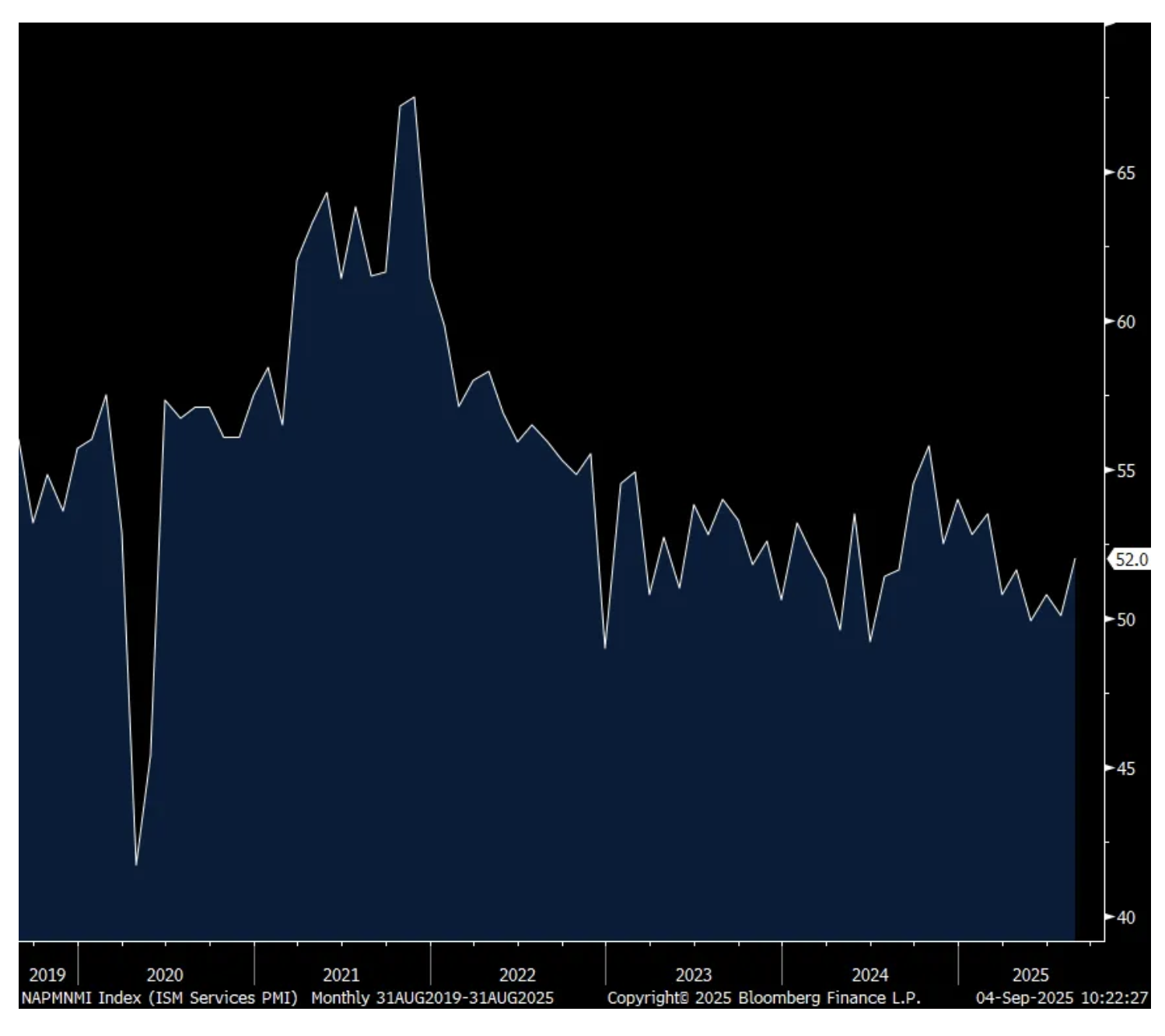

From Peter Boockvar:

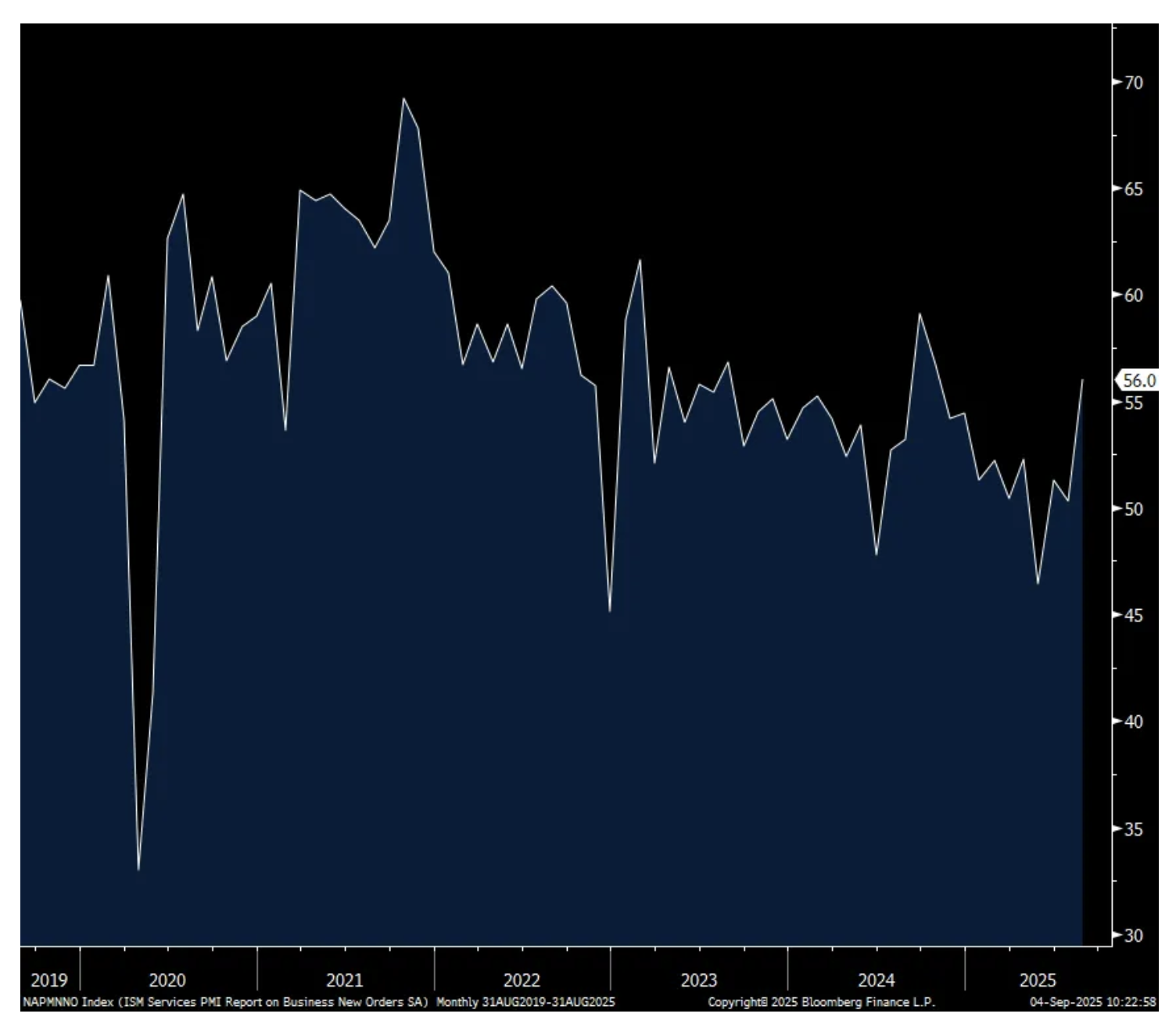

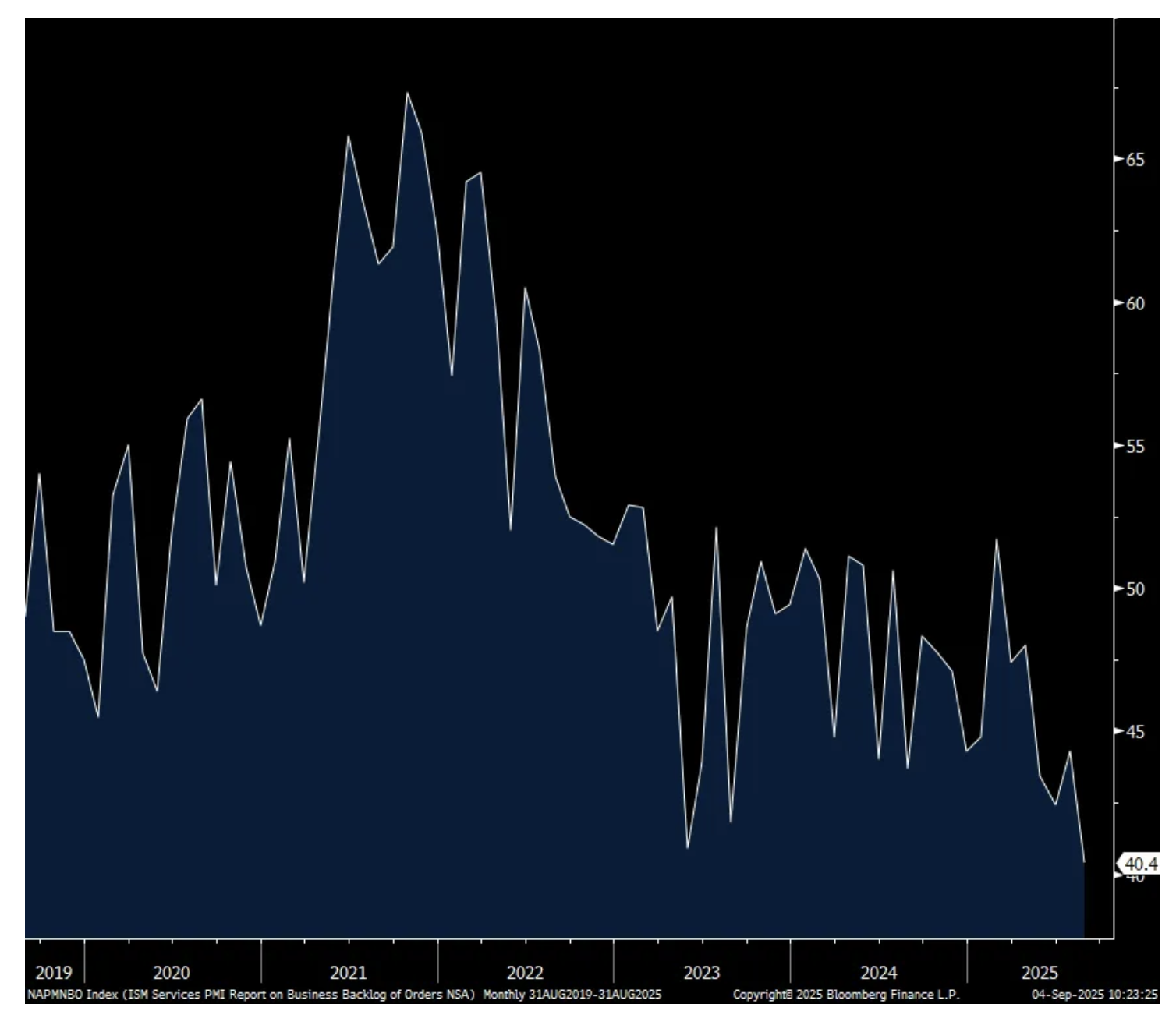

The August ISM services index rose to 52 from 50.1 and that was a bit better than the estimate of 51. The components though were pretty mixed. New orders rose 5.7 pts to 56 but backlogs dropped down to just 40.4 from 44.3. Inventories were up by 1.4 pts to 53.2.

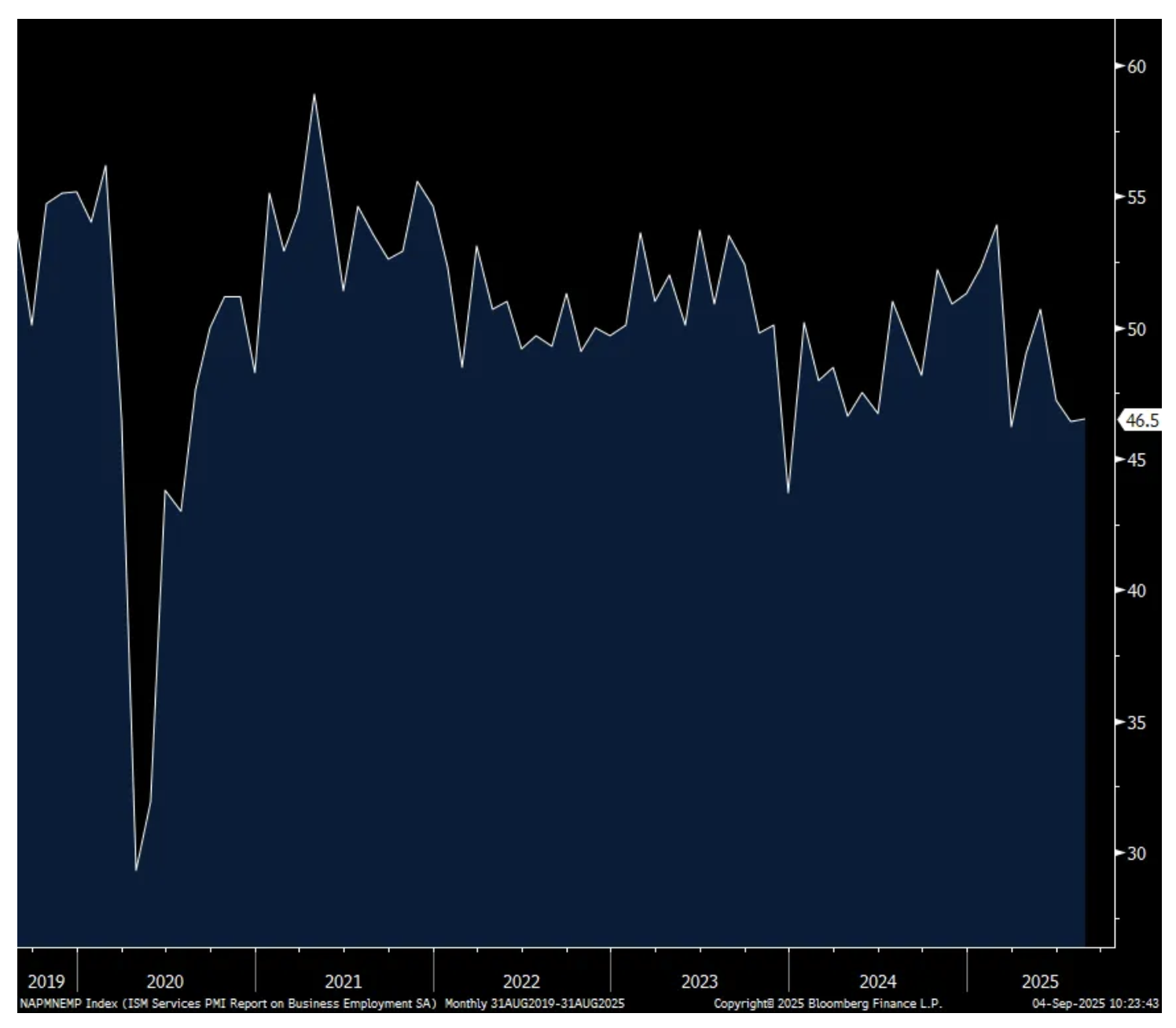

The employment component at 46.5, little changed m/o/m but was below 50 for the 5th month in the past six.

No supply issues with the supplier delivery figure at 50.3 but prices paid remained high at 69.2 vs 69.9 in the month before.

Of the 18 industries surveyed, 12 saw growth vs 11 in July and 10 in June. Four reported a contraction vs 7 in July. Specifically with employment, just 2 said they are increasing payrolls. With prices paid, 16 industries are paying higher prices vs 15 in July and 14 in June. New orders saw 13 industries seeing growth vs 7 in July but only 3 experienced an increase in order backlogs.

Here is some color on the rise in new orders, “Comments from respondents include: ‘Data center construction is driving the increase in order activity’ and ‘Getting merchandise into the US ahead of effective dates of tariff increases.’ “

This sums up the still low level of jobless claims but elevated rate of continuing claims with this respondent comment on the labor market, “Staffing is adequate, but work hours are down due to softer traffic and sales.”

On the elevated level of inventories, one respondent said “We have been making strategic buys of critical components to build a safety stock in response to extended lead times and anticipated price increases in the fourth quarter.” And from here, “As lead times continue to improve, we are reducing our inventory of finished goods and expect to continue doing so.”

The bottom line from ISM, “Commentary once again was led by respondents’ increasing citations of tariff impacts, with some indication that business activity and imports are being driven by an attempt to get ahead of additional price increases while preparing for the holiday peak season.”

My bottom line, I’ll argue again that tariffs are mud in the gears of business and we are hearing it a lot from corporate America with bigger companies much better able to mitigate the impact relative to small and medium sized ones.

Here is what ‘Respondents Are Saying’ and not surprisingly tariffs are an issue. I also bolded the word ‘starting’ twice, as I highlighted that Petco and American Eagle said basically that in their earnings calls in that the tariff impact is just about to hit them:

“We are starting to see the impact of tariffs on the cost of imported goods. For our company, this is primarily for goods from Asia and South America. We expect to see the full effect of tariffs in our cost of goods sold by October.” [Accommodation & Food Services]

“Tariffs are starting to become a factor in our pricing to specific markets. We are an importer from Europe. The intention is not to pass on these costs, but it’s getting harder as this goes on.” [Agriculture, Forestry, Fishing & Hunting]

“Tariffs continue to loom, and providers are starting to include references to tariffs when requesting price increases.” [Finance & Insurance]

“While our overall spending approach is to remain cautious while waiting out the effects of the new tariff policies on commodity pricing, we expect fiscal year 2026 to be positive.” [Management of Companies & Support Services]

“Business continues to remain flat.” [Other Services]

“Business growth continues to be strong as companies work to understand costs of expanding U.S. operations.” [Professional, Scientific & Technical Services]

“Locally, prices have and are continuing to rise on goods and services that do not appear to be directly impacted by tariffs.” [Public Administration]

“Our company had the strongest quarter in its history since it became a public company in 2020. Revenue is increasing due to M&A activity and in spite of a slow housing market and increasing tariffs.” [Real Estate, Rental & Leasing]

“It’s all about country specific tariff management. All decision making is currently dominated by tariff considerations.” [Retail Trade]

“Business overall is tightening. Most customers are extremely price conscious.” [Transportation & Warehousing]

ISM Services

New Orders

Backlogs

Employment

Prices Paid

BY Doug Kass · Sep 4, 2025, 10:55 AM EDT

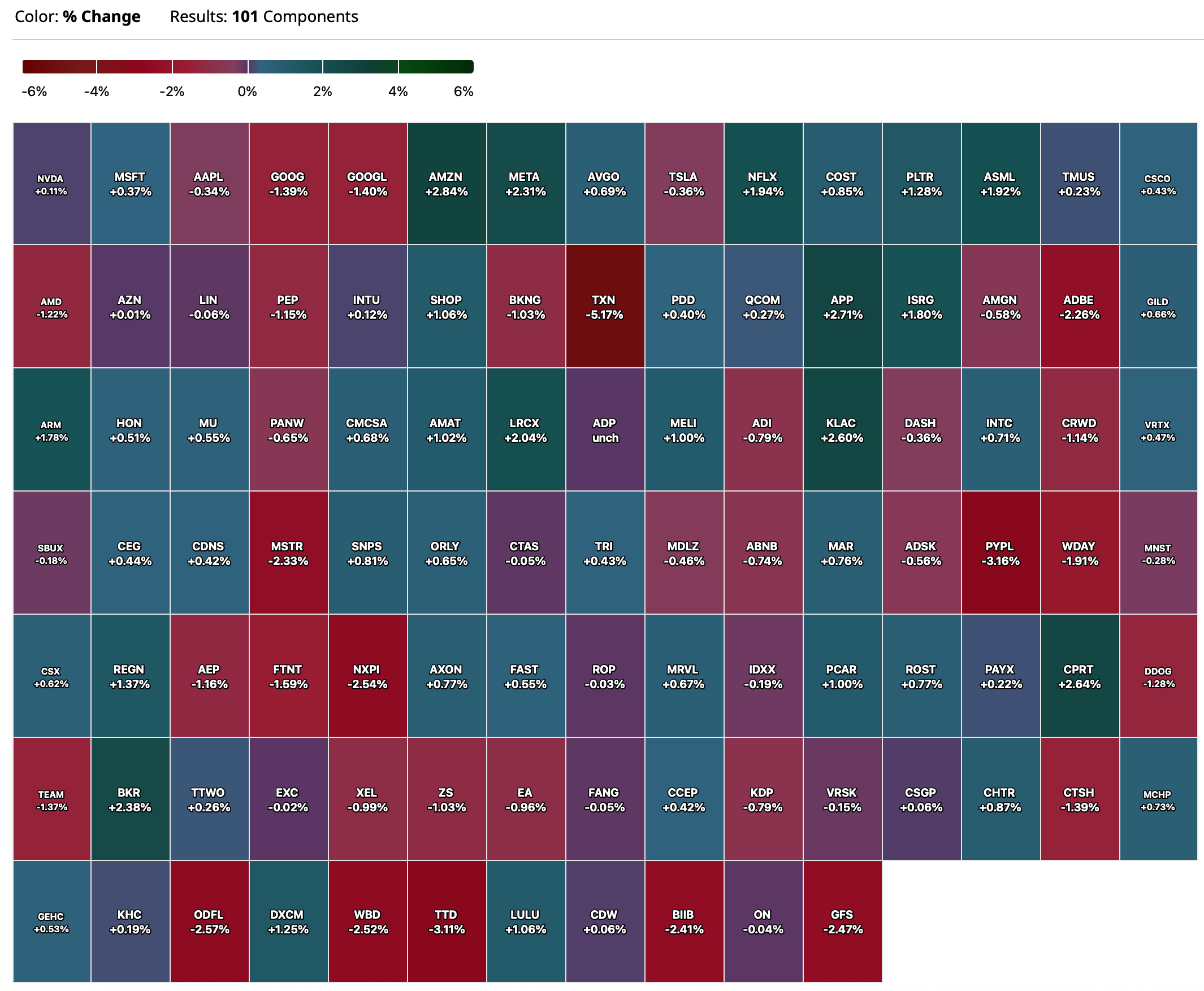

My only MAG7 longs are META and AMZN.

BY Doug Kass · Sep 4, 2025, 10:23 AM EDT

Shorted more GRNY (elder abuse!) at $23.24 and JOET at $41.70

BY Doug Kass · Sep 4, 2025, 10:11 AM EDT

Added to PEP long at $148.

Large sized now .

BY Doug Kass · Sep 4, 2025, 9:59 AM EDT

From JPMorgan:

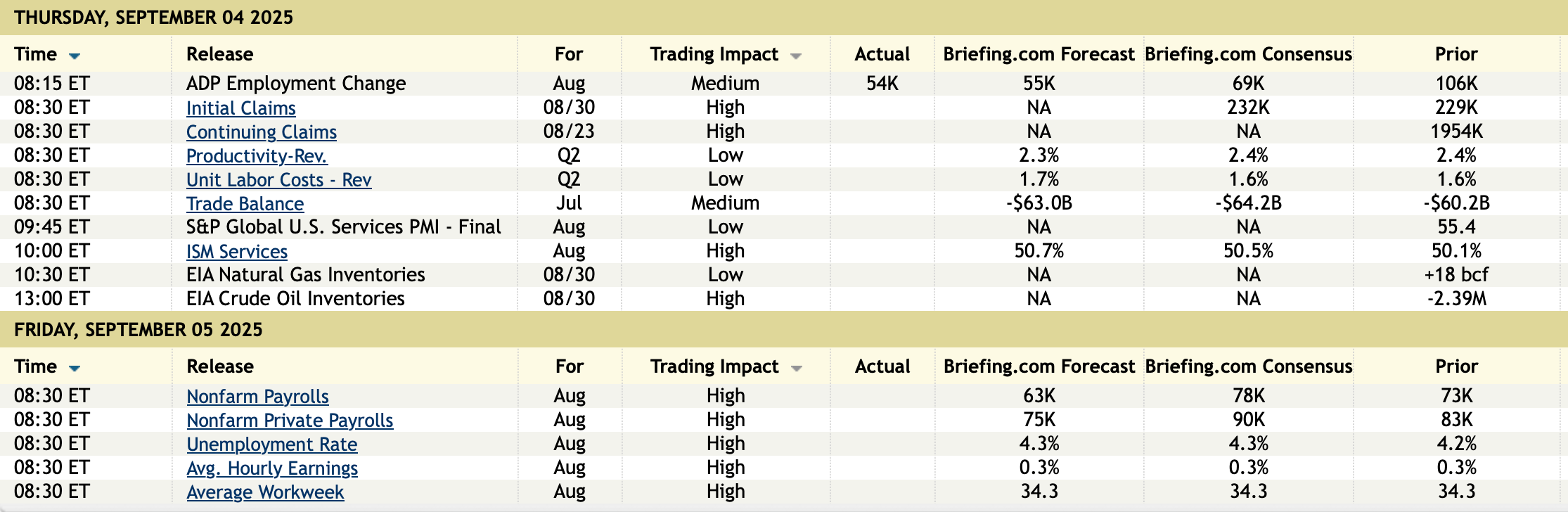

US: Futs are higher. Pre-market, Mag 7 are mostly higher with AMZN and TSLA adding 1.3% and 1.4%, respectively. Bond yields are 1-3bp lower; USD is higher. Commodities are mostly lower; oil -1.2%; gold -0.6%. Overnight, not a lot of major headlines in the US as investors are waiting for the 2x major catalysts this week (Broadcom earnings today amc and NFP tomorrow). We will receive ADP Employment at 8:15am ET and ISM-Srvcs at 10am ET today. Feroli expects ISM-Srvcs to print 51.0 vs. 50.9 survey vs. 50.1 prior.

and...

Stocks rallied 51bp yesterday, entirely driven by the +3.8% and +9.1% move higher in AAPL and GOOG/L post GOOG/L antitrust decision, respectively. However, outside Mag 7, the performance of SPX493 was lagged amid the weak July JOLTS report and Beige Book. Will this rotation back to MegaCap tech continue? NFP this week and CPI next will be the most important macro catalysts to reassess the Fed rhetoric. In addition, AVGO’s earnings after market close could add more positive momentum to MegaCap Tech and the AI-Theme. JPM Tech Spec Sales Josh Meyer flagged that his buyside survey results (below) underline some optimism on the AI semis outlook.

BY Doug Kass · Sep 4, 2025, 9:55 AM EDT

Adding to MSOS and Index shorts on the opening.

BY Doug Kass · Sep 4, 2025, 9:43 AM EDT

TREASURY AUCTIONS

11:00 a.m.: Treasury announces a 3 and 6 month bill auction;

11:30 a.m.: Treasury hosts a $100B 4 and $85B 8 Week Bill Auction

FED SPEAKERS:

12:05 p.m.: Fed Bank of New York President Williams (Voter) gives keynote before an Economic Club of New York Signature Luncheon (Text and moderated Q&A expected. In person with virtual option);

7:00 p.m.: Fed Bank of Chicago President Goolsbee (Voter) participates in moderated Q&A before mHub (Livestream available. Embargoed text TBD. Event information: chicagofed.org/

ECONOMIC CALENDAR:

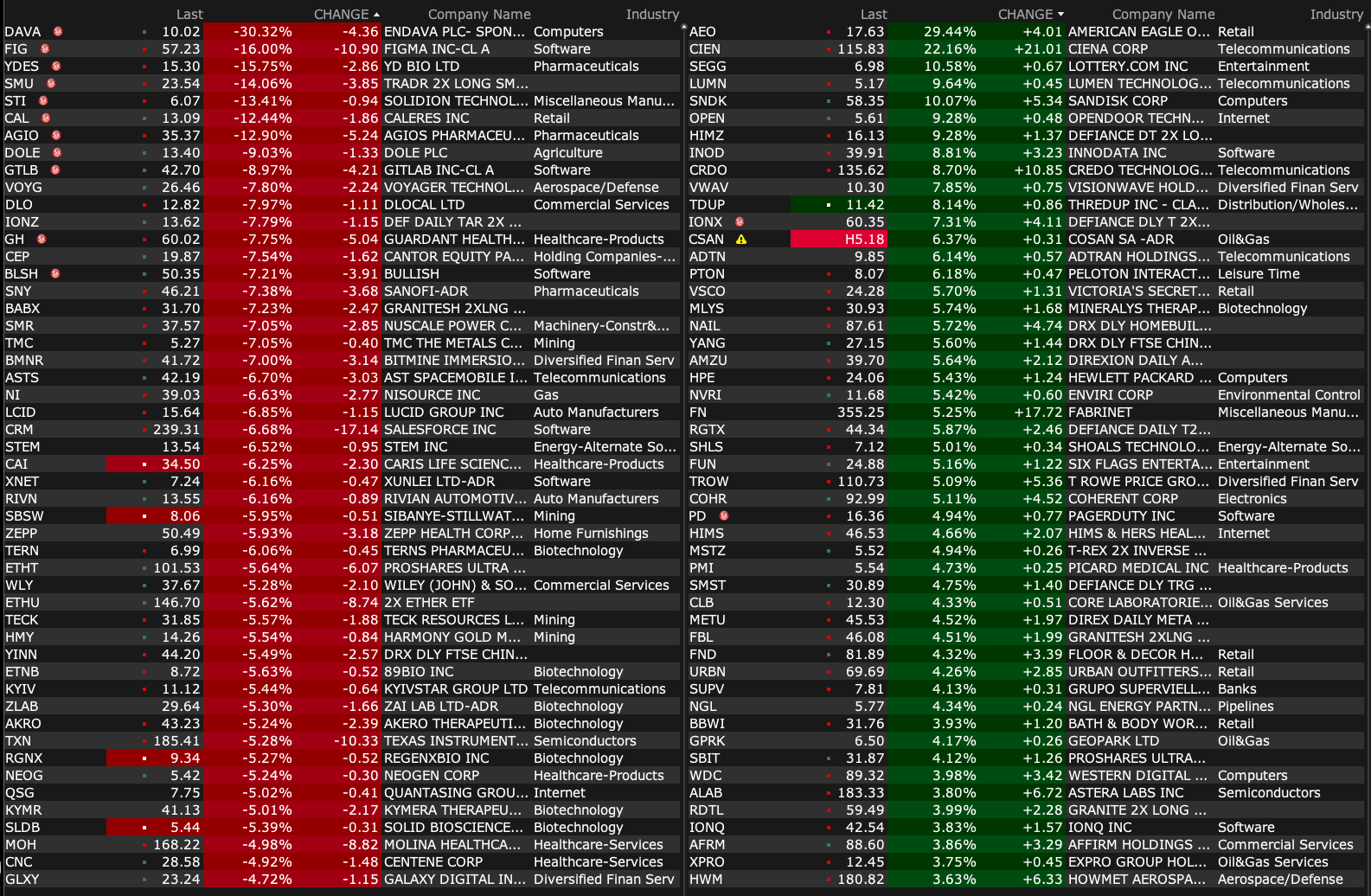

BY Doug Kass · Sep 4, 2025, 9:35 AM EDT

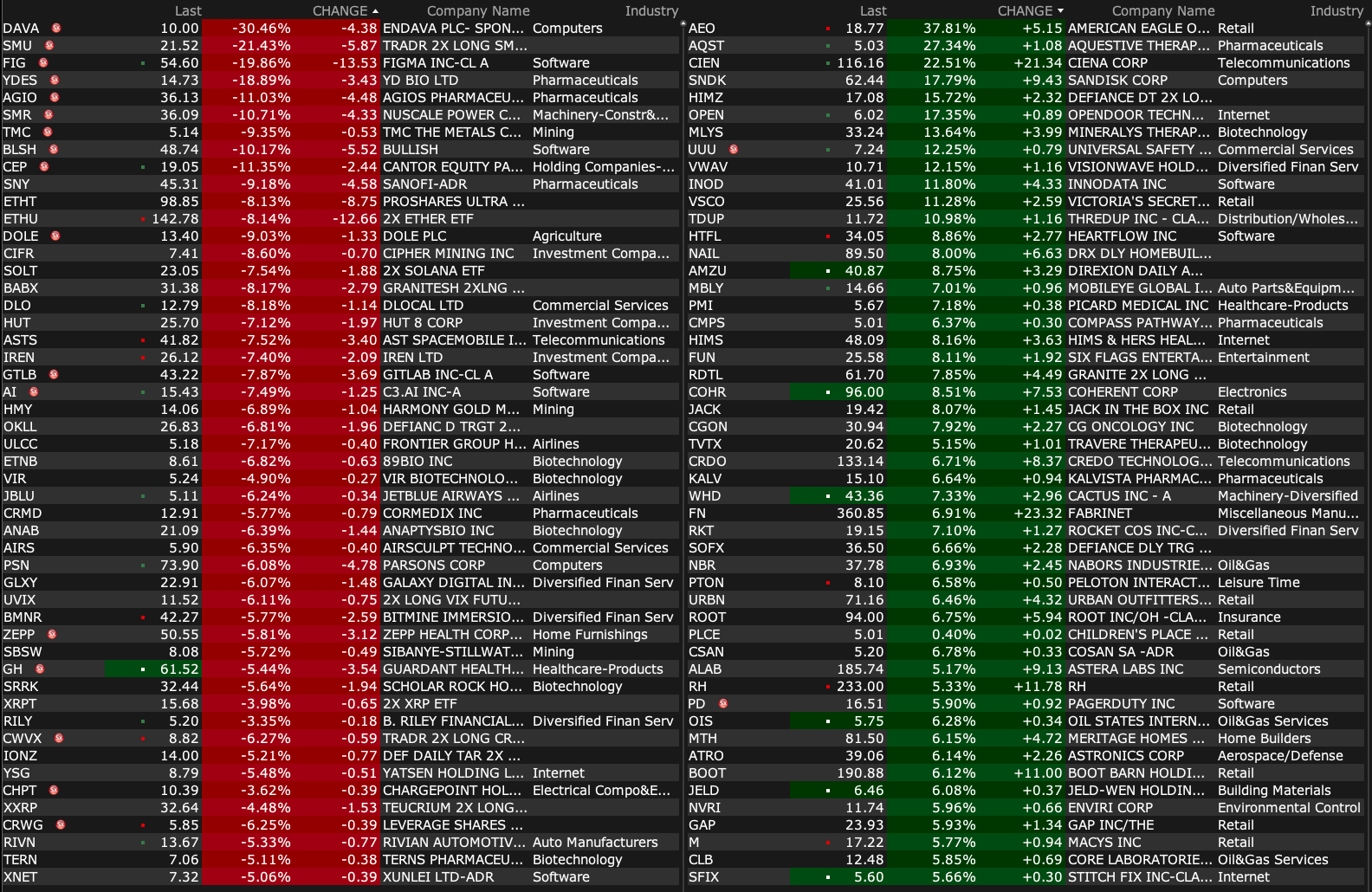

-AEO +23% (earnings, guidance)

-SCVL +15% (earnings, guidance)

-CIEN +14% (earnings, guidance)

-WDH +10% (earnings; raises dividend)

-TROW +7.8% (Goldman Sachs and T. Rowe Price sign strategic collaboration)

-BYRN +6.4% (prelim Q3 revenue)

-AQST +5.1% (FDA confirmed no advisory committee meeting required for Anaphylm)

-HPE +5.1% (earnings, guidance)

-BRC +2.1% (earnings, guidance)

-MCHP +2.1% (Citi conference presentation)

-NEON -77% (announces $15-20M of anticipated proceeds from patent lawsuit settlement; Ladenburg Thalmann Cuts NEON to Neutral from Buy, price target: $6)

-CAL -18% (earnings; to suspend annual guidance)

-AI -15% (earnings, guidance)

-FIG -15% (earnings, guidance)

-DOLE -10% (prices secondary offering of ~11.9M Ordinary Shares at $13.25/shr)

-SNY -8.4% (COAST 1 phase 3 study results)

-PD -3.2% (earnings, guidance)

-DUOL -2.8% (DA Davidson Cuts DUOL to Neutral from Buy, price target: $300)

-GIII -2.3% (earnings, guidance)

BY Doug Kass · Sep 4, 2025, 9:20 AM EDT

BY Doug Kass · Sep 4, 2025, 9:10 AM EDT

BY Doug Kass · Sep 4, 2025, 9:00 AM EDT

From Peter Boockvar:

The US economy can really use more Sydney Sweeney marketing campaigns, Travis Kelce too/Good enough JGB auction

The Fed's Beige Book continues to read like the US economy is barely growing. Yesterday it said, "Most of the twelve Federal Reserve Districts reported little or no change in economic activity since the prior Beige Book period—the four Districts that differed reported modest growth."

Sector wise, "Across Districts, contacts reported flat to declining consumer spending because, for many households, wages were failing to keep up with rising prices. Contacts frequently cited economic uncertainty and tariffs as negative factors. New York reported that "consumers were being squeezed by rising costs of insurance, utilities, and other expenses." Contacts observed the following responses to the consumer pullback. Retail and hospitality sectors offered deals and promotions to help price-sensitive consumers stretch their dollars—supporting steady demand from domestic leisure tourists but not offsetting falling demand from international visitors. The auto sector noted flat to slightly higher sales, while consumer demand increased for parts and services to repair older vehicles. Manufacturing firms reported shifting to local supply chains where feasible and often using automation to cut costs."

The main area of strength right now, outside of upper income consumer spending, "The push to deploy AI partly explains the surge of data center construction—a rare strength in commercial real estate noted by the Philadelphia, Cleveland, and Chicago Districts. Atlanta and Kansas City reported that data centers had increased energy demand in their Districts."

Ahead of ADP today and the BLS report tomorrow, it doesn't sound like there is much hiring going on. "Eleven Districts described little or no net change in overall employment levels, while one District described a modest decline. Seven Districts noted that firms were hesitant to hire workers because of weaker demand or uncertainty. Moreover, contacts in two Districts reported an increase in layoffs, while contacts in multiple Districts reported reducing headcounts through attrition—encouraged, at times, by return-to-office policies and facilitated, at times, by greater automation, including new AI tools. In turn, most Districts mentioned an increase in the number of people looking for jobs."

On the labor supply side, "half of the Districts noted that contacts reported a reduction in the availability of immigrant labor, with New York, Richmond, St. Louis, and San Francisco highlighting its impact on the construction industry."

With respect to cost pressures and the price pass through, "Ten Districts characterized price growth as moderate or modest. The other two Districts described strong input price growth that outpaced moderate or modest selling price growth. Nearly all Districts noted tariff-related price increases, with contacts from many Districts reporting that tariffs were especially impactful on the prices of inputs. Contacts in multiple Districts also reported rising prices for insurance, utilities, and technology services. While some firms reported passing through their entire cost increases to customers, some firms in nearly all Districts described at least some hesitancy in raising prices, citing customer price sensitivity, lack of pricing power, and fear of losing business. In some cases, as highlighted by Cleveland and Minneapolis, firms reported being under pressure to lower prices because of competition, despite facing increased input costs."

And from here on prices, "Most Districts reported that their firms were expecting price increases to continue in the months ahead, with three of those Districts noting that the pace of price increases was expected to rise further."

With regards to what this all means for the Federal Reserve's monetary policy, it reads like the economy needs a rate cut or two but until the rate of inflation falls notably from around 3%, I don't think they have too many to give us right now.

Auto sales in August according to Wards totaled 16.07mm which was about as expected. It compares with 15.13mm in August 2024 and 16.97mm in August 2019. I want to make a point that with respect to the extent tariffs are working their way through the auto supply change, we can't just look at the MSRP because I've heard stories where while the MSRP might be staying the same, which might show up in CPI as 'new car prices unchanged', dealers are getting you in other places. Such as higher financing costs, more expensive warranties, and increases in auto service and repair prices. If you think the dealers are eating the tariffs, only maybe the smaller ones are.

With respect to stock market sentiment, there continues to be a pretty wide divergence between the mood of the individual investor and that of the professional. I say that because the individually focused AAII survey has Bulls at 32.7, down 1.9 pts w/o/w and Bears at 43.4, up 4 pts. On the flip side, the Investors Intelligence survey has the Bull/Bear spread approaching the danger zone of 40. Bulls at 54.9 is up from 51 last week while Bears sit at just 17.6, unchanged on the week. I think the differential is explained by the professional investor that is just focused on market trends and momentum while sentiment on the economy sometimes flows through on the individual side. The CNN Fear/Greed index is smack in the middle of the 'Neutral' camp at 52 vs 65 one week ago. The Citi Panic/Euphoria model is at .48, off its highs but still Euphoric. Last week's NAAIM Exposure index at 92 is pretty bullish. Overall, a mixed bag but with still notable signs of bullish complacency.

If only everyone can get Sydney Sweeney to market their products, Travis Kelce too, the US economy would boom. From American Eagle, up 24% pre market:

"Product initiatives across brands, exciting new marketing campaigns, and greater operational disciplines are all contributing to improved business results." I bolded.

"Second quarter traffic was positive across brands and channels, and I was pleased to see traffic momentum build throughout the second quarter, which continued into August."

"Fueled by the strength of our product lines and the success of our recent marketing campaigns, the iconic fall denim campaign with Sydney Sweeney affirms we are the American jeans brand. We saw record breaking new customer acquisition and brand awareness cutting across age demographics and genders." Travis Kelce helped too with its Tru Kolors brand.

"Sweeney's signature jeans sold out within a week." Between her and Kelce, "we are very pleased with these campaigns. Since the launch, customer counts are up more than 700,000 and the campaigns combined have generated a staggering 40 billion impressions."

As I highlighted yesterday with what Petco Health & Wellness said on Friday about the 2nd half of the year where most of the tariffs will be felt, American Eagle said "With respect to tariffs, we will begin to feel the impact in the second half...We are using all levers to mitigate tariff increases. Early efforts have been successful."

From Dollar Tree who could have used some Sydney Sweeney and Travis Kelce marketing help as its stock fell 8.4% yesterday:

"The timing of the impacts of the tariffs and our mitigation activities played out differently than we originally anticipated with some of the net positive benefits of our mitigation initiatives coming earlier in Q2 and the tariff impact shifting to later in the year."

"The second quarter unfolded against a volatile backdrop for both the consumer and retail industry as the economy continued to adjust to elevated tariffs, persistent cost pressures and a static labor market. In today's environment, customers are seeking value and convenience more than ever and Dollar Tree is uniquely positioned to deliver both."

"Whether it's a mom stretching her grocery budget, a college student outfitting a dorm room or a higher income shopper attracted to an expanded assortment of everyday essentials, our stores are increasingly the destination of choice."

Comps did grow by 6.5% and "was nicely balanced between traffic and ticket and between consumables and discretionary."

"Underscoring growing engagement, the number of shoppers visiting three or more times a month increased by 11% in Q2, a sequential improvement from the 9% growth we saw last quarter. While sales growth was strong across all income cohorts, we continue to see especially strong performance from middle and higher income customers with households earning over $100,000 per year providing a meaningful portion of our Q2 growth." I bolded for emphasis.

From Macy's and whose stock popped by 21%:

Comps were up 1.9% and "Turning to category performance, comparable sales of women's contemporary and career as well as men's tailored clothing outperformed. In addition, fine jewelry and watches, textiles and mattresses continued to experience strong demand." Fragrance also did well.

"Now let's discuss our view on the consumer. Our customer across nameplates has remained resilient through the first half of the year and quarter to date. However, given the uncertainty regarding the impact of tariffs on demand, we believe, it's prudent to continue to incorporate a more choiceful consumer into our guidance for the remainder of the year."

"In addition, reflecting the incremental tariffs that have been announced since our last earnings call, full year guidance now incorporates a 40 bps to 60 bps tariff impact to gross margin. This compares to our prior expectation of 20 bps to 40 bps and equates to roughly $.25 to $.40 of EPS versus our prior expectation of $.10 to $.25."

From Campbell's and whose stock jumped 7.2%:

"As we have seen over the last few quarters, consumers remain cautious and intentional with their spending. They continue to seek value in a variety of ways, such as cooking at home, a behavior that fuels growth in our Meals & Beverages business. Consumers are also increasingly seeking flavor-forward offerings, premium experiences and health and wellness benefits."

If there is one thing I noticed from a variety of calls, snaking is now considered a discretionary product that has been negatively impacted by selective consumer spend. "Pressure on snaking categories remained in the fourth quarter, but we were encouraged that our in-market results improved sequentially, resulting in a 2% consumption decline versus the prior year."

From Salesforce which is down about 6% pre-market because of the worries about how they will be able to play in the new AI world and how monetizable their agentic product Agentforce will be:

"It is early days in the adoption cycle, but we are really confident in our strategy to monetize AI" said the CFO. "I've never been more excited about anything in my entire career" said CEO Marc Benioff.

Shifting gears, Switzerland had true price stability in August as its CPI was unchanged y/o/y. We await to see if the Swiss National Bank will ever experiment with the financially poisonous negative interest rates again.

Japan had a 30 yr JGB auction that was about in line with the one year averages and that led to a rally in JGB's which followed the US Treasury rally yesterday on the heels of the soft JOLTS data and European bonds are rising too with yields lower. A temporary respite after a rough few months.

BY Doug Kass · Sep 4, 2025, 8:55 AM EDT

We remain short RCI (Rick's Cabaret strip clubs!):

BY Doug Kass · Sep 4, 2025, 8:40 AM EDT

Walt Disney: Fine-tuning our DIS EBITDA margins

Needham Analyst Laura Martin added, "We lower our FY4Q25E Op Inc and EBITDA estimates by 6% and 4%, respectively, to reflect comments made on DIS's FY3Q25 earnings call. Specifically, we lower our FY4Q25 EBITA (Op Inc) estimate by 6% to $3.4B, driven by: a) we lower our OI estimate for Content, Sales & Licensing by 10% (to a loss of $110mm vs $100mm profit), reflecting guidance from DIS's FY3Q25 earnings call; b) we cut our FY4Q25 tax rate by 42% to mirror FY3Q25; and c) we raise our expense estimates by 2% (to $21.1B) to be more in line with FY3Q25 levels. We make NO changes to our FY25E rev estimate of $95.6B (up 4.5% y/y) or our Adj EPS estimate of $5.85 (up 17.7% y/y) for FY25E. We also maintain our FY26 estimates of rev of $99.7B (up 4.3% y/y), EBITA of $18.3B (up 5% y/y), and EPS Adj of $6.13 (up 4.8% y/y)."

BY Doug Kass · Sep 4, 2025, 8:30 AM EDT

BY Doug Kass · Sep 4, 2025, 8:19 AM EDT

BY Doug Kass · Sep 4, 2025, 8:10 AM EDT

I will be leaving early today (at about 2 PM) and will be back on Monday morning.

BY Doug Kass · Sep 4, 2025, 8:00 AM EDT

Interesting news between T. Rowe Price TROW and Goldman Sachs GS.

Goldman to Buy $1 Billion of T. Rowe Stock as Firms Team Up - Bloomberg

TROW's shares are trading +7% in premarket trading.

BY Doug Kass · Sep 4, 2025, 7:25 AM EDT

BY Doug Kass · Sep 4, 2025, 6:55 AM EDT

BY Doug Kass · Sep 4, 2025, 6:40 AM EDT

Adding to index shorts (615 AM-kind):

* SPY $645.13

* QQQ $571.92

BY Doug Kass · Sep 4, 2025, 6:30 AM EDT

BY Doug Kass · Sep 4, 2025, 6:20 AM EDT

Last night on Mad Money. Salesforce CEO calls guidance 'appropriately conservative' as stock declines after earnings

BY Doug Kass · Sep 4, 2025, 6:15 AM EDT

The S&P Short Range Oscillator is at 1.53% vs. 1.74%.

BY Doug Kass · Sep 4, 2025, 6:06 AM EDT