Wednesday's After-Hours Movers

At 4:24 PM:

BY Doug Kass · Sep 3, 2025, 4:50 PM EDT

At 4:24 PM:

BY Doug Kass · Sep 3, 2025, 4:50 PM EDT

BY Doug Kass · Sep 3, 2025, 4:40 PM EDT

Investment short C3.ai AI spits the bit — misses top and bottom-line and lowers guidance and the CEO steps down.

Here is the press release.

C3 AI Announces Fiscal First Quarter 2026 Financial Results - C3.ai, Inc.

BY Doug Kass · Sep 3, 2025, 4:35 PM EDT

There is no stagflation. Only stagnation.

The Fed’s just-released Beige Book “reported little or no change in economic activity since the prior Beige Book period.” Little or no change which means the economic world is flat. This is a markdown from “Economic activity increased slightly from late May through early July” in the last report six weeks ago. So much for 3%+ second quarter growth, which was principally fueled by a plunge in imports.

On the labor market, how about this? “Eleven Districts described little or no net change in overall employment levels, while one District described a modest decline.” This is another deterioration, at the margin, from “Employment increased very slightly overall” in the previous document. Now how exactly is the new BLS Commissioner going to be able to navigate this reality on Friday without being summarily fired by the President?

How about this little ditty?

“Seven Districts noted that firms were hesitant to hire workers because of weaker demand or uncertainty. Moreover, contacts in two Districts reported an increase in layoffs, while contacts in multiple Districts reported reducing headcounts through attrition—encouraged, at times, by return-to-office policies and facilitated, at times, by greater automation, including new AI tools. In turn, most Districts mentioned an increase in the number of people looking for jobs.”

Nothing too inflationary in that narrative.

Indeed, with respect to inflation, six weeks ago we were told that,“Prices increased across Districts […].” And now “Ten Districts characterized price growth as moderate or modest. The other two Districts described strong input price growth that outpaced moderate or modest selling price growth.”

In addition, “Across Districts, contacts reported flat to declining consumer spending because, for many households, wages were failing to keep up with rising prices. Contacts frequently cited economic uncertainty and tariffs as negative factors […] Contacts observed the following responses to the consumer pullback. Retail and hospitality sectors offered deals and promotions to help price-sensitive consumers stretch their dollars—supporting steady demand from domestic leisure tourists but not offsetting falling demand from international visitors.”

Ergo, companies are having more difficulty than they had thought when it comes to passing on the tariff-induced cost increases:

“While some firms reported passing through their entire cost increases to customers, some firms in nearly all Districts described at least some hesitancy in raising prices, citing customer price sensitivity, lack of pricing power, and fear of losing business.”

The stock market is either unaware or simply doesn’t bother to care, but the fallout will be on profit margins.

Either that, or businesses are being compelled to embark on cost-cutting strategies or offer up incentives/promotional activity — and this is where tariffs actually become disinflationary!

To wit:

“Manufacturing firms reported shifting to local supply chains where feasible and often using automation to cut costs.”

BY Doug Kass · Sep 3, 2025, 3:55 PM EDT

I have a 3:45 PM research call.

Will be returning around 4:30 PM

Radio silence.

BY Doug Kass · Sep 3, 2025, 3:48 PM EDT

BY Doug Kass · Sep 3, 2025, 2:17 PM EDT

I took a small loss in Coca-Cola KO (from yesterday) and I am putting proceeds into PepsiCo PEP.

BY Doug Kass · Sep 3, 2025, 1:45 PM EDT

Moving to large sized on PepsiCo PEP at $147.6.

BY Doug Kass · Sep 3, 2025, 1:28 PM EDT

From this morning (we remain short financials across the board and I am adding to heavily financial (35% weighting)-laden JOET):

Banks, selected financials and private equity shares are disengaged from today's rally.

This is giving me a reason to expand my Index shorts on the current rally off the Tuesday lows.

Position: none.

By Doug Kass Sep 3, 2025 10:37 AM EDT

BY Doug Kass · Sep 3, 2025, 1:00 PM EDT

BY Doug Kass · Sep 3, 2025, 11:54 AM EDT

I bought a slug of MSOS at $4.86 — moving towards but not yet at a large-sized position.

BY Doug Kass · Sep 3, 2025, 11:39 AM EDT

BY Doug Kass · Sep 3, 2025, 11:30 AM EDT

From Peter Boockvar

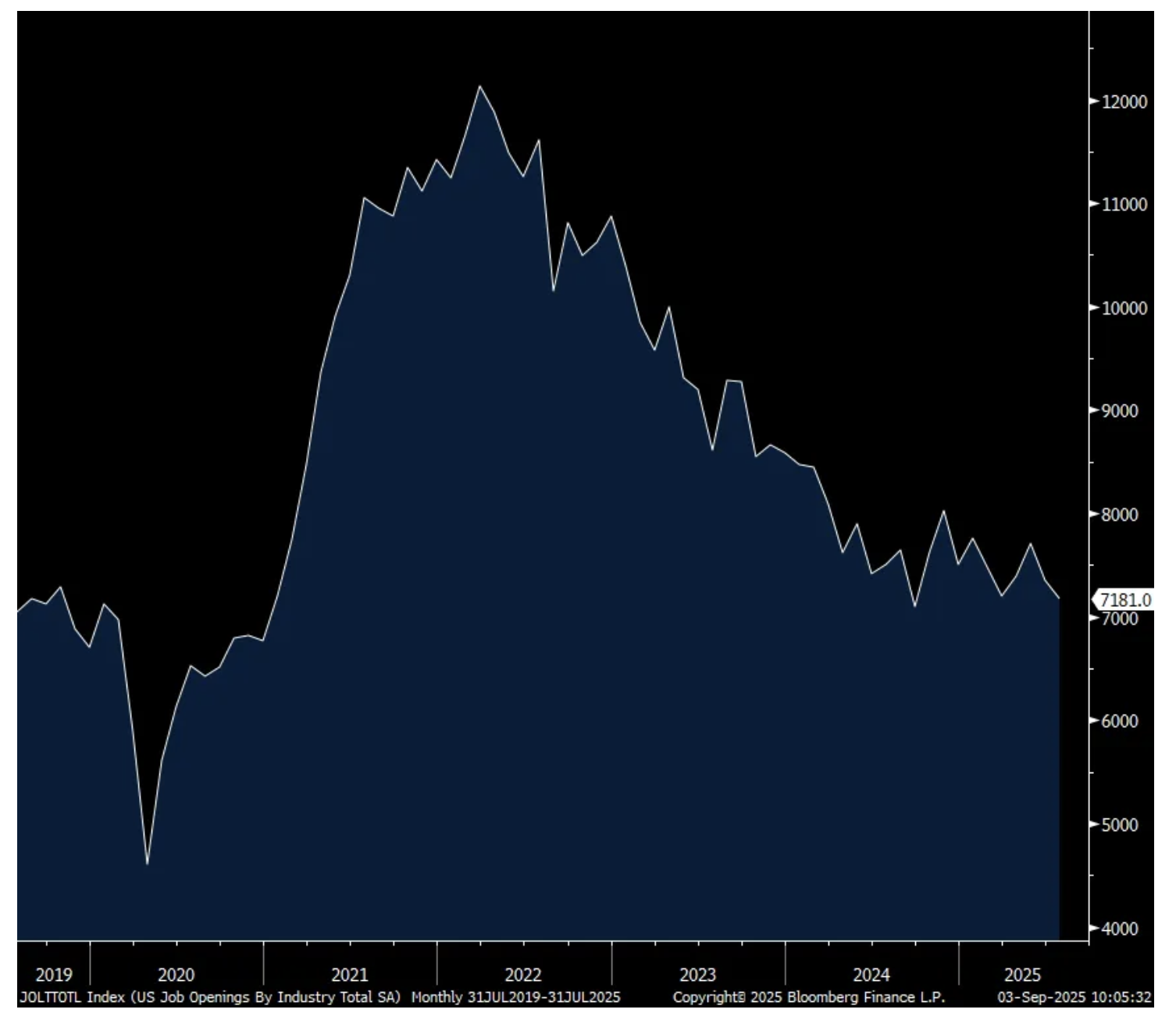

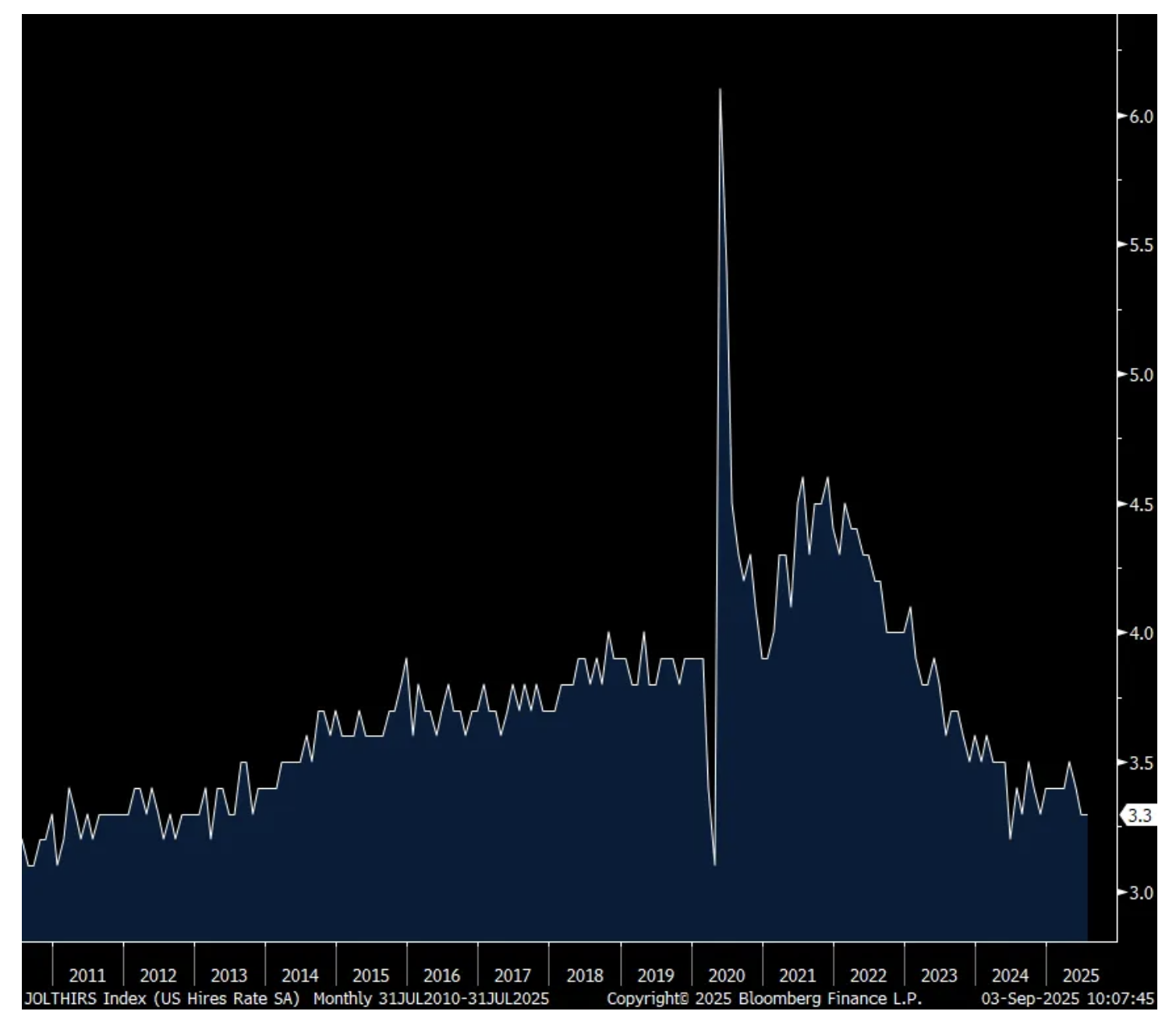

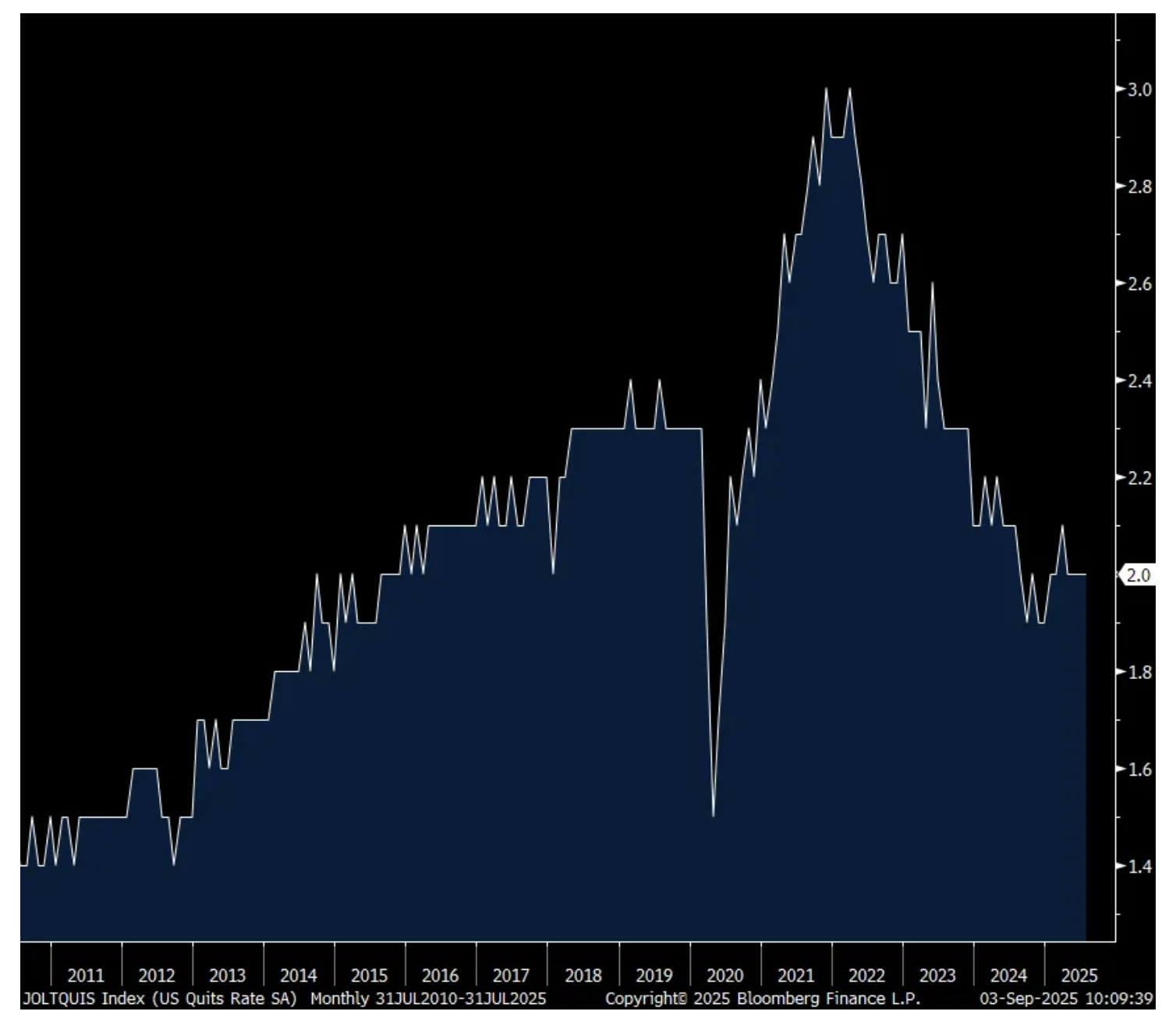

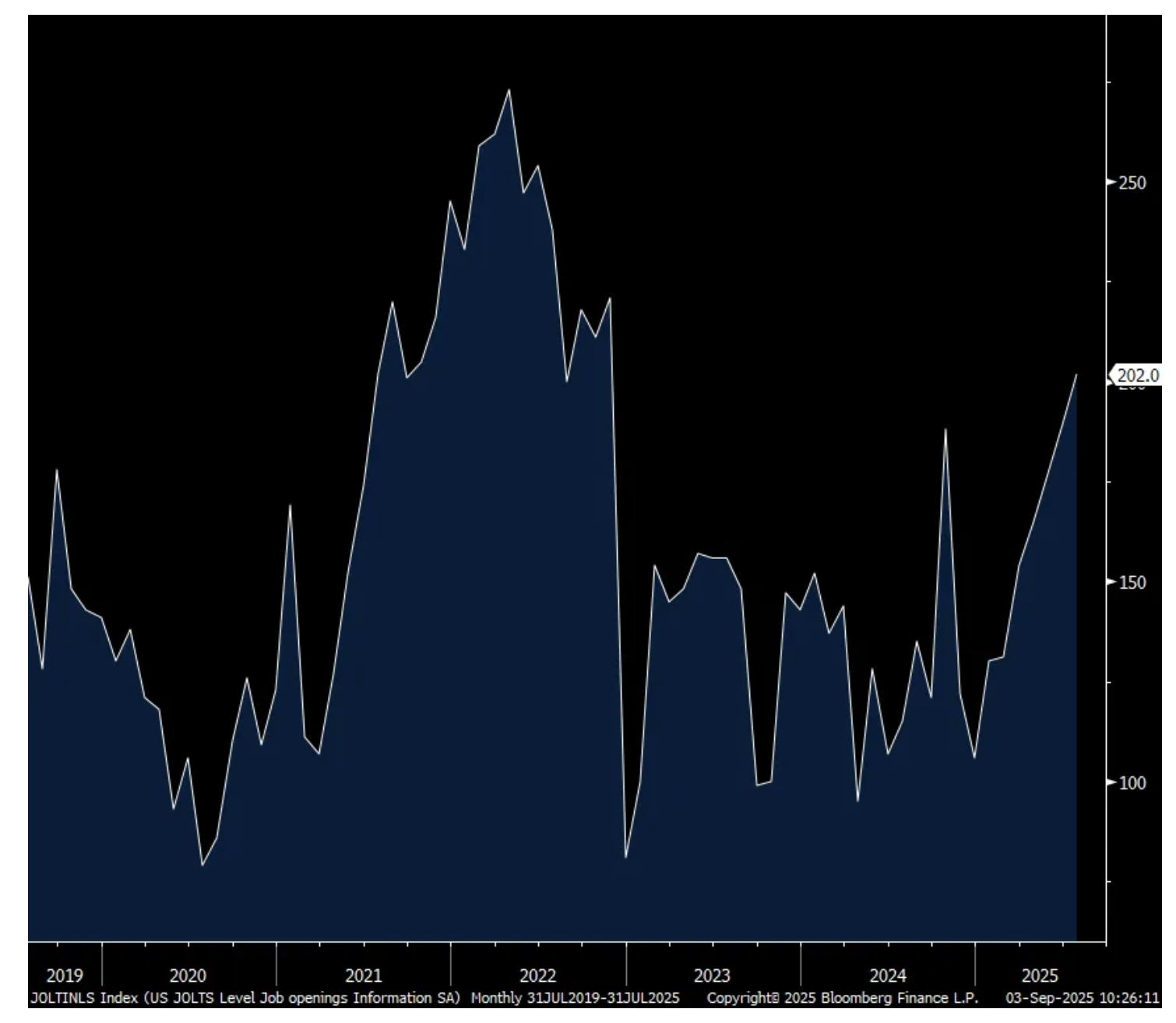

In July, there were 7.181mm job openings in the US economy (with double/triple counting taking place) and that is a reduction from the 7.437mm seen in June and 200k below expectations. That’s also the least since September 2024. The hiring rate was 3.3%, at that level for a 5th straight month and that is just one tenth above the lowest level since 2013 not including Covid. The quit rate was 2% for a 4th straight month. That’s one tenth above the lowest since 2015, also not including Covid.

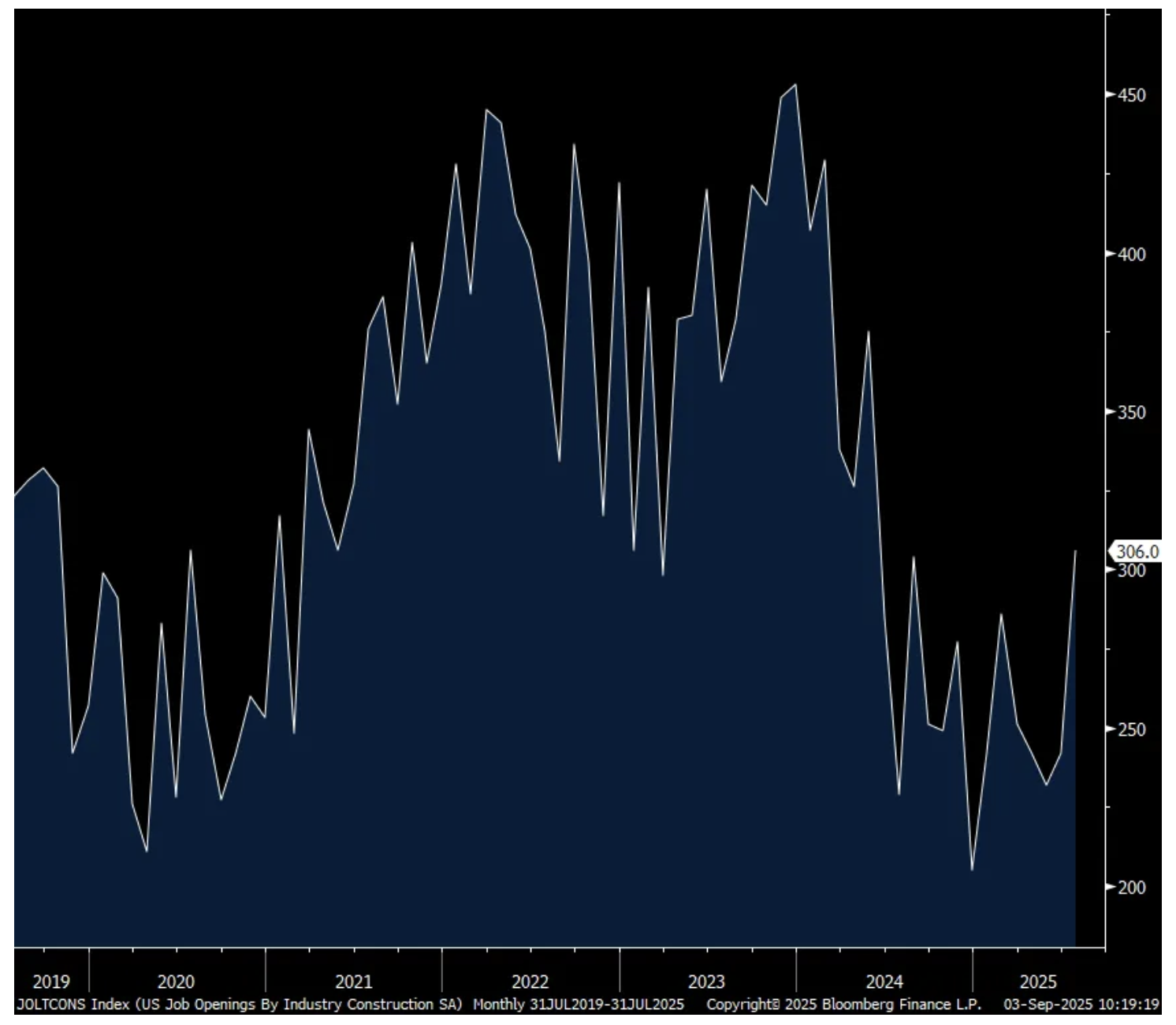

Likely due to the data center buildout, the demand for construction jobs rose to 306k from 242k and that is the most since May 2024. Job openings for ‘information’ were up too, the highest since November 2022.

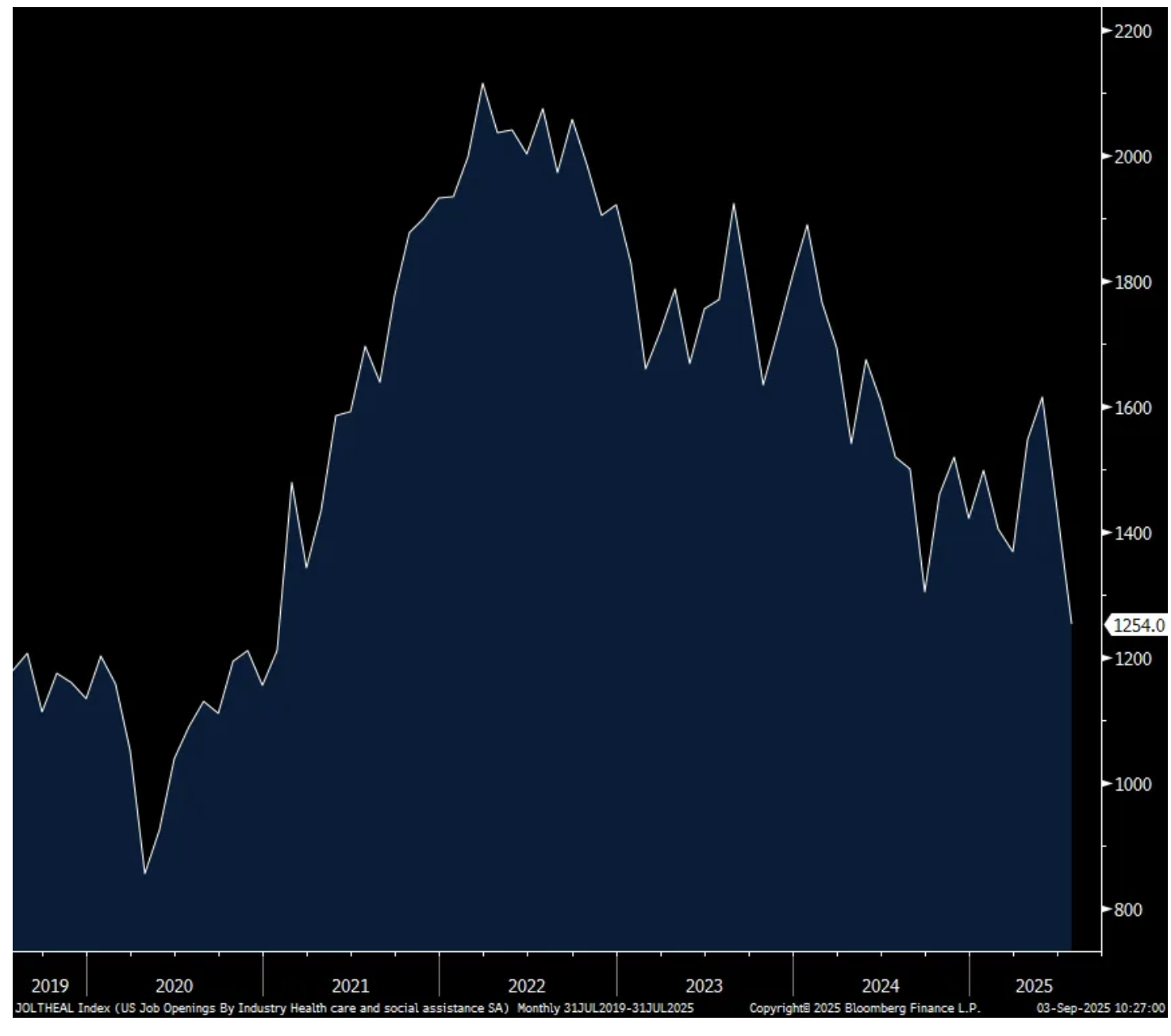

Where most of the job opening decline took place was in health care/social assistance and in the ‘arts, entertainment’ sector. We know that health care/social assistance has been the main area of job gains over the past few years.

Bottom line, while dated this data point does confirm the slowing pace of hirings being seen in a variety of stats in the aggregate but something we’re well aware of and why the Fed is cutting rates by 25 bps in two weeks.

Job Openings

Hiring Rate

Quit Rate

Construction Job Openings

Information Job Openings

Health Care/Social Assistance Job Openings

BY Doug Kass · Sep 3, 2025, 11:12 AM EDT

Banks, selected financials and private equity shares are disengaged from today's rally.

This is giving me a reason to expand my Index shorts on the current rally off the Tuesday lows.

BY Doug Kass · Sep 3, 2025, 10:37 AM EDT

Adding to longs - MSOS $5.08 and PEP $149.95.

BY Doug Kass · Sep 3, 2025, 9:42 AM EDT

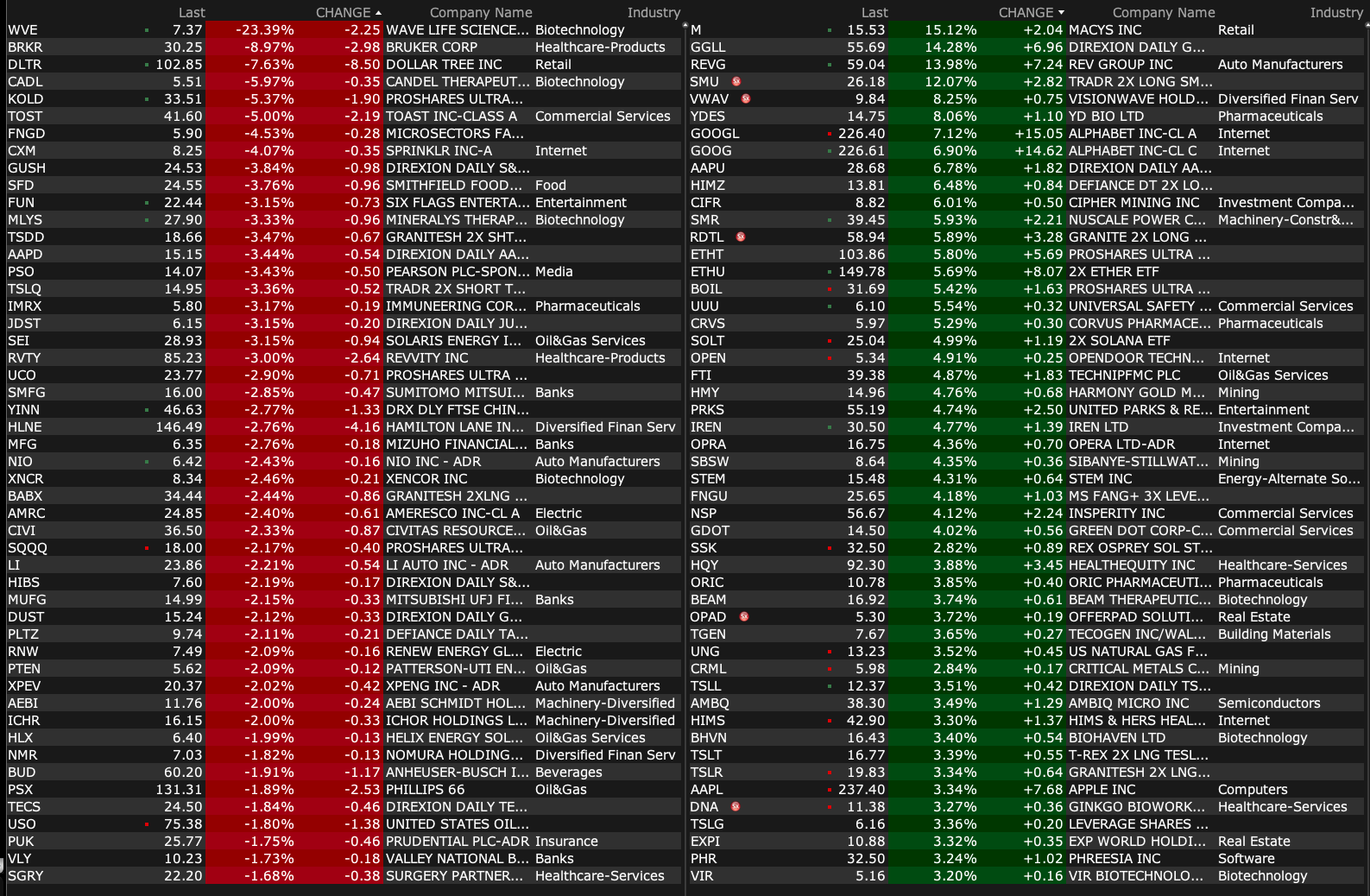

BY Doug Kass · Sep 3, 2025, 9:24 AM EDT

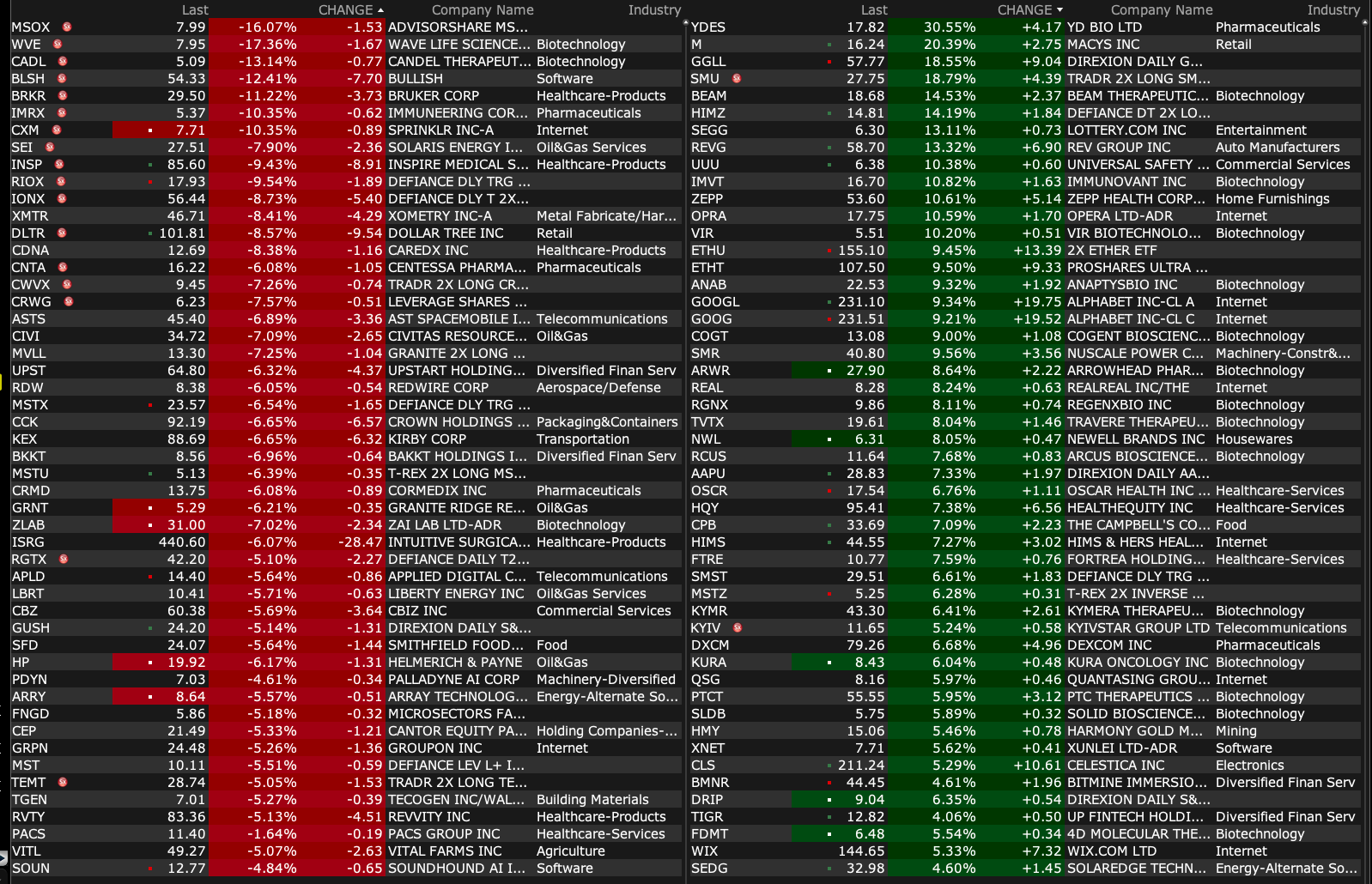

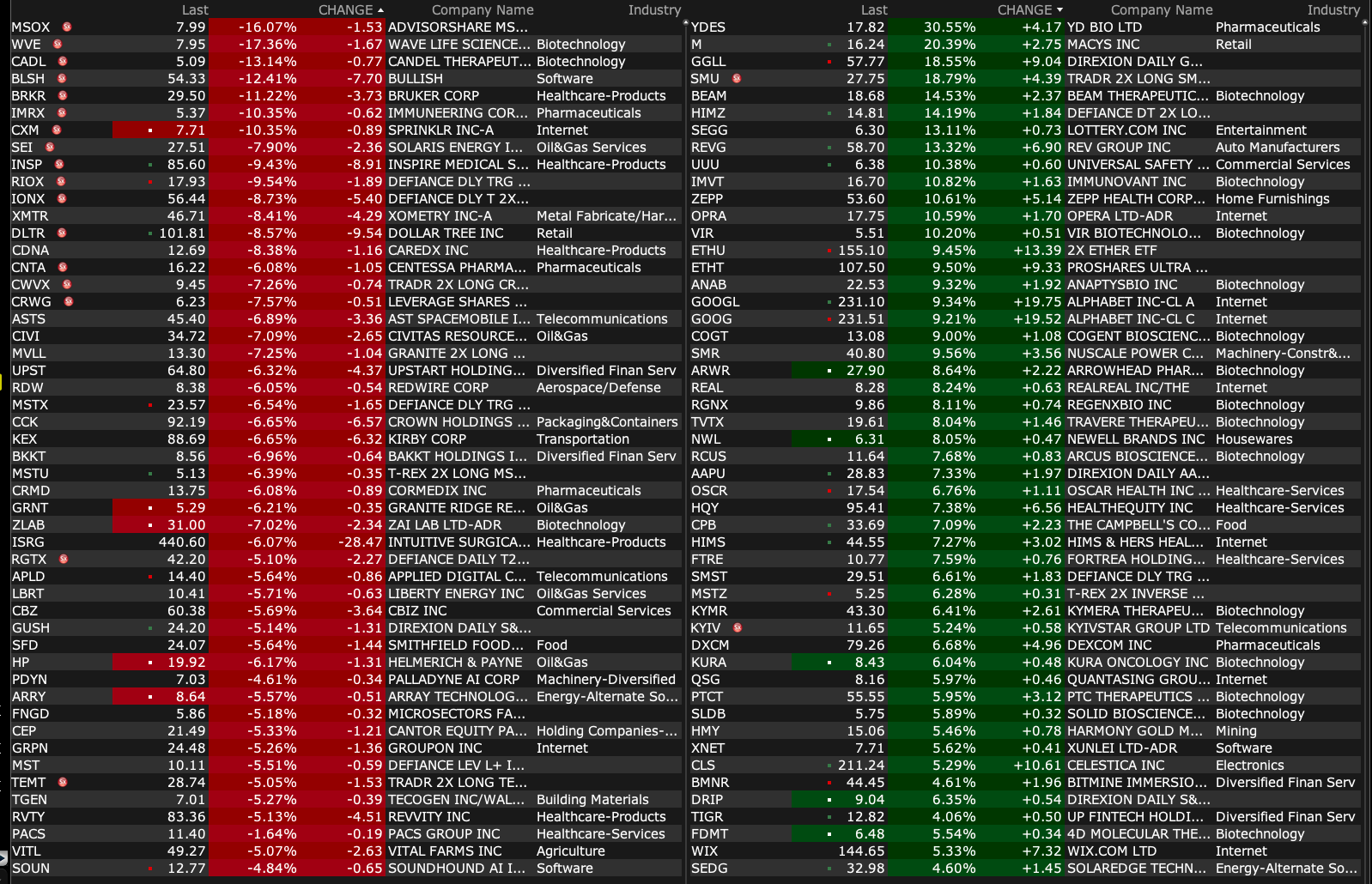

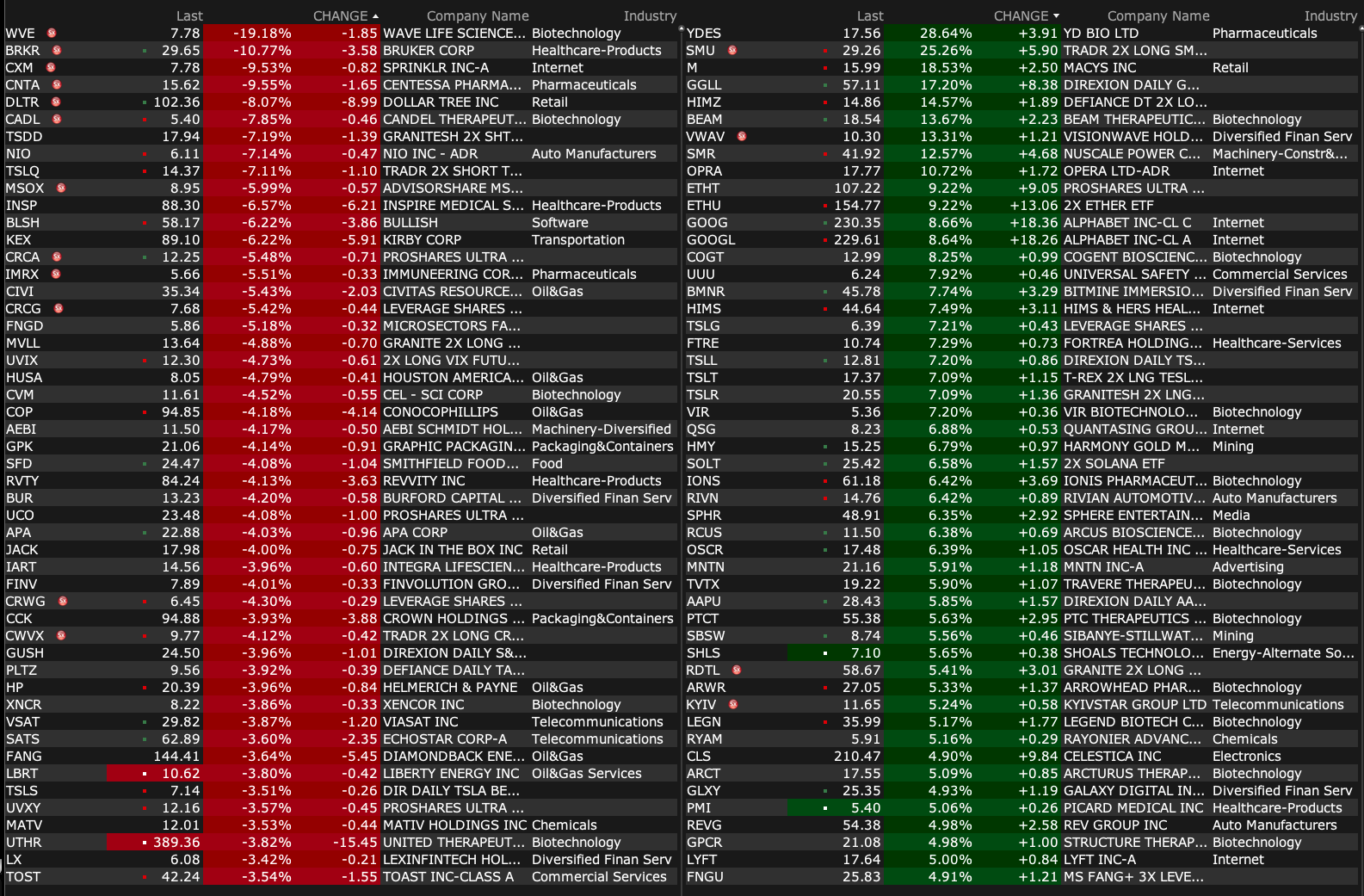

-GEG +29% (earnings)

-SINT +27% (publishes landmark study demonstrating broad-spectrum antiviral activity of Silicon Nitride)

-M +12% (earnings, guidance)

-REVG +7.9% (earnings, guidance)

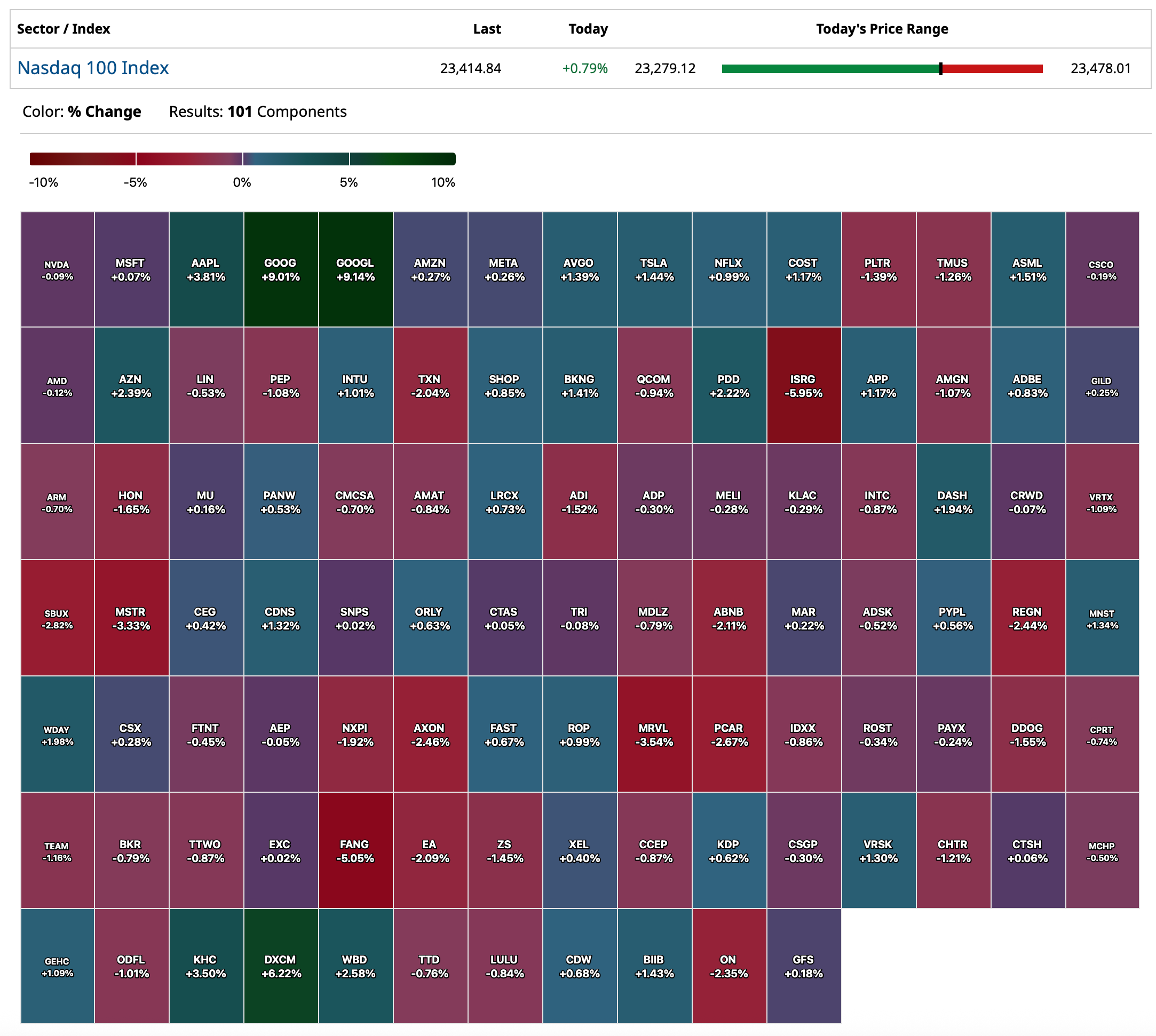

-GOOGL +6.3% (judge rules Company will not have to divest Chrome)

-TECX +4.1% (Oppenheimer initiates TECX with Outperform, price target: $80)

-AAPL +3.6% (higher in sympathy with GOOGL; reportedly iPhone 17 Pro's starting price may increase by $100 compared to the iPhone 16 Pro)

-CPB +2.6% (earnings, guidance)

-UIS +2.6% (Needham Initiates UIS with Buy, price target: $6)

-WVE -19% (trial data for GSK-partnered RNA-editing therapy)

-DLTR -4.8% (earnings, guidance)

-SFD -4.4% (Holder SFDS UK Holdings Ltd. files to sell 16M shares)

-TOST -4.1% (hearing received Boutique firm downgrade)

-CXM -3.1% (earnings, guidance; CFO to depart)

BY Doug Kass · Sep 3, 2025, 9:10 AM EDT

FED SPEAKERS:

9 a.m.: Fed Bank of St. Louis President Musalem (Voter) participates in moderated conversation on the U.S. economy and monetary policy before the Peterson Institute for International Economics (In person and virtual option. Text anticipated. No media availability);

1:30 p.m.: Fed Bank of Minneapolis President Kashkari (Non-Voter) participates in a fireside chat hosted by the Minnesota Women's Economic Roundtable, MN (Livestream at minneapolisfed.org. Audience Q&A expected. No media Q&A. No prepared/embargoed text)

TREASURY AUCTION

11:30 a.m.: Treasury hosts a $65B 17-Week Bill Auction

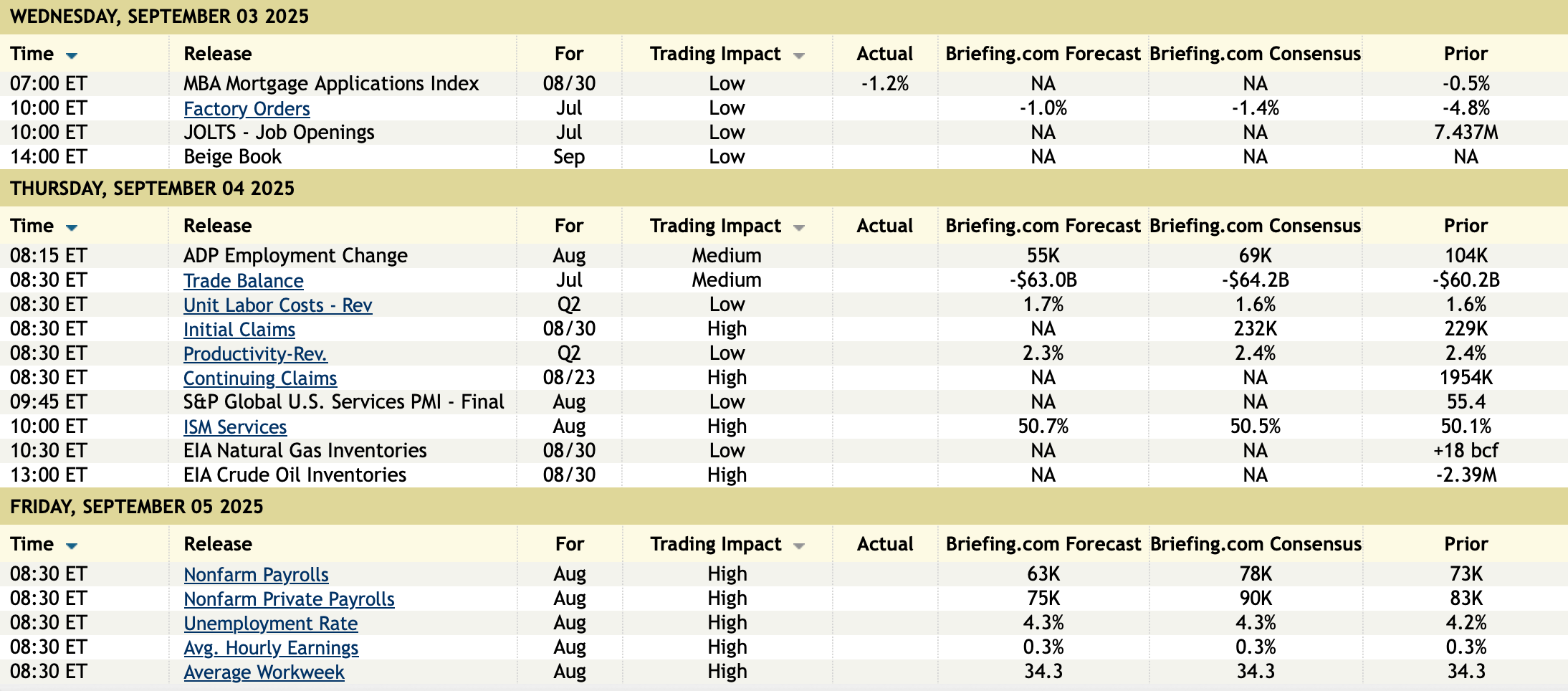

ECONOMIC CALENDAR FOR THE REMAINDER OF THE WEEK

BY Doug Kass · Sep 3, 2025, 9:00 AM EDT

BY Doug Kass · Sep 3, 2025, 8:44 AM EDT

From Peter Boockvar:

I'll start with rents just two weeks before the Fed will cut interest rates and we debate what they'll then do thereafter. Last week the August Apartment List National Rent Report, in case you missed it, said "The national median rent dipped by .2% in August, and now stands at $1,400. This was the first m/o/m decline since January, and marks the beginning of the rental markets off season. It's likely that we'll continue to see further modest rent declines through the remainder of the year."

Versus last year, new rents are down .9%. The vacancy rate is at 7.1% which is the highest since Apartment List started this survey in 2017 and "We're past the peak of a multifamily construction surge, but a healthy supply of new units are still hitting the market, and vacancies are still trending up." I'll add, most of this supply is coming from the sunbelt states with Austin, Texas being the weakest market followed by Denver (not sunbelt but most others are), Phoenix and Tucson. The best rental markets are on the coasts that have seen less supply growth. For example, San Francisco is now the best market with rental rates up 4.7% y/o/y, playing catch up. Overall, "Units are taking an average of 29 days to get leased after being listed, up one day from last month's reading, and down from a high of 37 days in January."

Not in this report but from what I heard from the publicly traded REIT's, renewal rates are running at about 3-4% so the blended rental growth rate is about 1-2%. This is below what the CPI and PCE are telling us but again, keep in mind that CPI and PCE never captured the high growth rates seen in rents at the peak in 2022. Also, while the rate of change in rent growth has clearly slowed, new rents are still up 22% from January 2021 and why consumer confidence levels for many are still at low levels with this being the biggest annual cost for those renting.

The bottom line on where the rental market goes from here, Apartment List said "With construction expected to slow further in the second half of this year and into 2026, conditions are likely to shift, but it will still take time for the market to metabolize the recent growth in the rental stock." I expect rent growth to stabilize in the first half of 2026 and expect rents to start rising again in the back half of 2026.

While the average 30 yr mortgage rate fell another 5 bps w/o/w to 6.64%, purchase applications fell by 3.1% after a 2.2% rise in the week before. While these numbers seasonal adjust, maybe the end of the summer had back-to-school on most minds and also the busy selling season has come to an end. Refi's were up about 1% w/o/w.

On to some calls and what Petco Health & Wellness, a stock we own, said on Thursday in their call is a reminder that the back half of 2025 will be more impactful for some with regards to tariffs. This as the inventory now being sold include the tariffs while the previous inventory sold was procured pre-tariffs. "So, we had almost no tariff impact in Q2 (the quarter just reported). There was some, but let's call it rounding. As we go to Q3, it becomes meaningful and then it becomes even much more meaningful in the fourth quarter."

From Signet Jewelers and whose stock rose 2.7% yesterday in a down tape:

"At the category level, our early efforts to focus on fashion drove a 2% comp growth...We are focused on delivering fashion pieces across key price points to reach more customers, including an expanded assortment of lab growth diamond, or LGD, fashion pieces." LGD pieces by the way now make up 14% of their fashion sales.

"Bridal comps were flat."

Anyone looking for value we know can now go to the lab grown diamond market. "We see our customer willing to spend as long as the assortment is compelling and delivers on their expectations of value...We've tripled our ownership of lab growth diamond fashion below $1,000, have bigger increases below $500, and with particular focus on that $250 to $500 price point."

"We are working with our vendors to land the inventory at the best time to minimize tariffs and maximize holiday availability. We're also working to reduce the impact of tariffs through discussions with suppliers to maximize domestic production, optimize country of origin, and by value engineering pieces that deliver on customer expectations at the right price points."

And with their earnings guide, it includes the assumption of a "measured consumer environment and being somewhat conservative to what we've seen happen in the business, just knowing the backdrop of the business" as they approach the holidays. "There's a lot of moving parts in the environment right now, but we've seen our customer be resilient. We largely set in what is a planned and emotional purchase, and those drivers are fairly timeless, resilient, and we're seeing customers respond to that in the marketplace."

Constellation Brands updated their guidance ahead of a conference they were speaking at. They said "We continue to navigate a challenging macroeconomic environment that has dampened consumer demand and led to more volatile consumer purchasing behavior since our first quarter of fiscal 2026. Over the last several months, high-end beer buy rates decelerated sequentially, as both trip frequency and spend per trip declined. Notably, high-end beer buy rate declines for Hispanic consumers were more pronounced than general market declines, which has an outsized impact on our Beer Business compared to the broader beer category." Corona and Modelo are two of their key brands.

From Academy Sports & Outdoors and whose stock fell 8% yesterday:

Comps were flat, up .2% but was an improvement from Q1.

"We saw solid results across most of our core categories, such as athletic and outdoor apparel and footwear, sporting goods, hunting, camping and our backyard businesses. One consistent soft spot was seasonal categories such as swim, pools and summer seasonal footwear that got off to a slower start during the first half of the quarter. We attributed this to a cooler and wetter start to the summer." They said as the weather improved, "all these businesses rebounded."

"During our Q1 call, we discussed the customer trade down effect that we first started to see in the back half of last year. Consumers are clearly looking for ways to navigate the current inflationary environment and are seeking out ways to stretch their spending power."

"We continue to see strong double digit growth in foot traffic and share gains from customers in the top two income quintiles, which are households making more than $100,000 a year. We were flattened in traffic share in the middle income consumer whose households make $50,000 to $100,000 a year. And finally, we continue to see traffic erosion in the lower income cohorts that make less than $50,000 a year, but the pace of these declines was less than what we saw in Q1."

Overseas, the China's August RatingDog (no longer Caixin) private sector focused services PMI rose to 53 from 52.6 and that is the best level since May 2024. RatingDog said "the index measuring overall new business saw a significant jump to its highest point since May of last year, while new export business expanded at the quickest pace since February. This was largely driven by more stable domestic demand and a recovery in foreign demand. At the same time, service sector businesses remained optimistic about the future, with overall confidence the joint-highest since March."

I will add that the Macau casino numbers continue to improve month-to-month and we remain long Las Vegas Sands and Melco.

Also out with the August PMIs, Singapore's fell to 51.2 from 52.7 while Hong Kong's rose to 50.7 from 49.2. The Vietnam manufacturing PMI fell 2 pts to 50.4. Japan's final services PMI was 53.1 vs 53.6. Australia's services PMI hit 55.8 from 54.1 and that's the best since April 2022. India's services PMI rose to 62.9 from 60.5 and that is a 15 yr high as India's economy continues to outperform many of its peers.

The service sector continues to outperform manufacturing in Europe, but barely. The final August Eurozone services PMI was 50.5 vs 51 in July and 50.5 in June. While the ECB is comfortable with inflation, S&P Global said, "Inflationary pressures picked up across the euro area service sector. Input cost inflation rose to a three month high, while charges increased at the fastest pace since March."

Overall for the Eurozone, S&P Global said "Riding a bike too slowly can make you tip over. That's the risk facing the Eurozone. Yes, the economy has been growing since the start of the year, but the pace is painfully slow." Also, "Political tensions in France and Spain, uncertainty around the EU-US trade deal, and ongoing troubles in the key automotive sector aren’t helping. On the bright side, increased defense spending across Europe and Germany’s infrastructure program offer hope that the economy might keep moving forward – and avoid falling off the bike."

The UK August services PMI outperformed the continent with its print of 54.2 vs 51.8 in July and that's the best read since April 2024. S&P Global said, "growth prospects for the UK service economy have moved up from the lows seen this spring. Improved sales pipelines, lower borrowing costs and receding fears about US tariffs all helped to boost business optimism. However, many service providers still commented on elevated government policy uncertainty and worries about forthcoming tax raising measures expected in the autumn Budget."

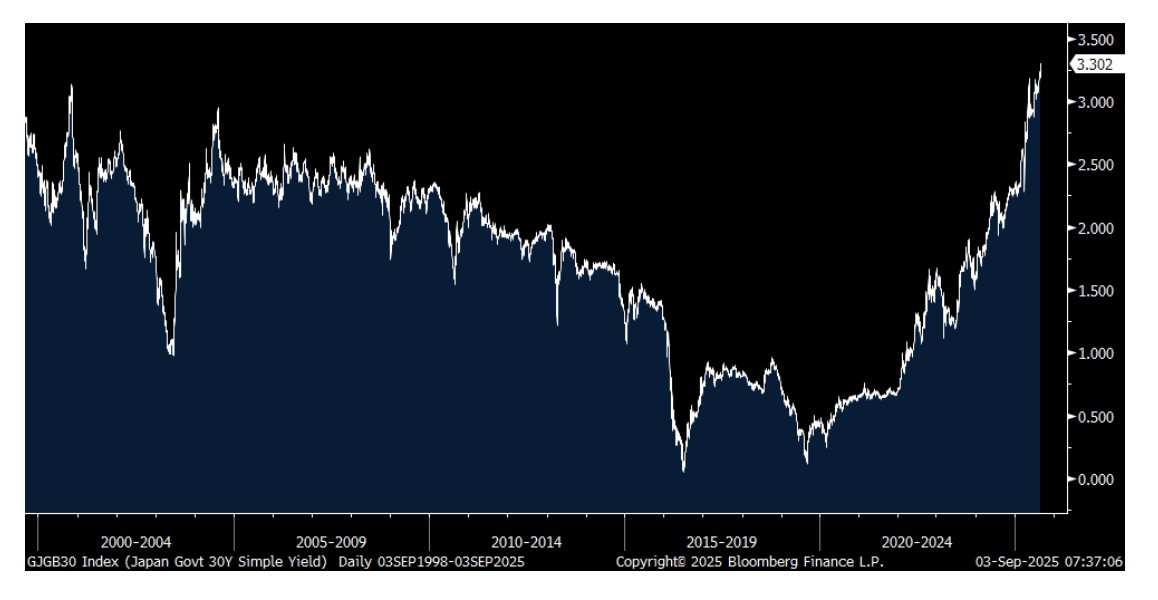

After yesterday's selloff, European sovereign bonds are bouncing a touch while Asian bonds sold off following the Tuesday action elsewhere. Long bonds in Japan in particular continue to jump with the 30 yr yield up 7 bps to a fresh 25 yr high since it was first introduced.

30 yr JGB Yield

BY Doug Kass · Sep 3, 2025, 8:30 AM EDT

A few days ago I had the privilege of being interviewed by David Rosenberg — Macroeconomic Research and Market Insights — in his podcast series.

Rosie is a dear and old friend, which I hope came through in his interview with me.

It is my wish that this blunt and honest hour-long podcast gives you new insights about my investing process, market/economic thoughts and my concerns about the trajectory of profits derived by the adoption of artificial intelligence (which has dominated the market's advance).

Here is the link to Rosie's podcast:

BY Doug Kass · Sep 3, 2025, 7:35 AM EDT

BY Doug Kass · Sep 3, 2025, 6:45 AM EDT

BY Doug Kass · Sep 3, 2025, 6:25 AM EDT

The S&P Short Range Oscillator is at 1.74% vs. 2.91%.

BY Doug Kass · Sep 3, 2025, 6:05 AM EDT

I added to my late-day's short in the indices at around 4:30 AM on Wednesday morning:

* SPY $643.02

* QQQ $569.23

From late yesterday - in case you missed it! (6:40 PM, Tuesday night):

I am back reshorting Indices in the after hours:

* (SPY) $642.32

* (QQQ) $568.02

I covered (GOOGL) short under $297 for a quick profit.

Position: Short SPY (S), QQQ (S)

By Doug Kass Sep 2, 2025 6:41 PM EDT

BY Doug Kass · Sep 3, 2025, 5:55 AM EDT

BY Doug Kass · Sep 3, 2025, 5:45 AM EDT