After-Hours Trading

I am back reshorting Indices in the after hours:

* SPY $642.32

* QQQ $568.02

I covered GOOGL short under $297 for a quick profit.

BY Doug Kass · Sep 2, 2025, 6:41 PM EDT

I am back reshorting Indices in the after hours:

* SPY $642.32

* QQQ $568.02

I covered GOOGL short under $297 for a quick profit.

BY Doug Kass · Sep 2, 2025, 6:41 PM EDT

Dougie Kass

Trading short rental Google $229.02.

Won't be in for long, though.

BY Doug Kass · Sep 2, 2025, 5:28 PM EDT

BY Doug Kass · Sep 2, 2025, 4:27 PM EDT

There is almost $7 billion to buy on the close — this helps to explain some of the rally off of the lows.

BY Doug Kass · Sep 2, 2025, 3:56 PM EDT

Adding to PEP at $150.75.

BY Doug Kass · Sep 2, 2025, 3:27 PM EDT

From "Meet" Bret Jensen:

Bret Jensen

I was worried before dept.

I have been concerned about the CRE space for many quarters now. Then I watched a long video with the founder of BankRegData on how banks are using loan modifications, note on note financing, fly wheels and recent changes to FASB rules to hide their worsening problems with CRE, mortgage, credit card, and various other debt, AKA, an upgraded and modern version of 'Extend & Pretend'. Let's just say I am beyond worried now.

Banks Are Hiding Credit Losses (Here’s How) | Bill Moreland of BankRegData

BY Doug Kass · Sep 2, 2025, 2:55 PM EDT

I'm adding to MSOS at $5.21.

BY Doug Kass · Sep 2, 2025, 2:45 PM EDT

BY Doug Kass · Sep 2, 2025, 12:45 PM EDT

BY Doug Kass · Sep 2, 2025, 12:30 PM EDT

BY Doug Kass · Sep 2, 2025, 12:15 PM EDT

From last week:

BY Doug Kass · Sep 2, 2025, 12:03 PM EDT

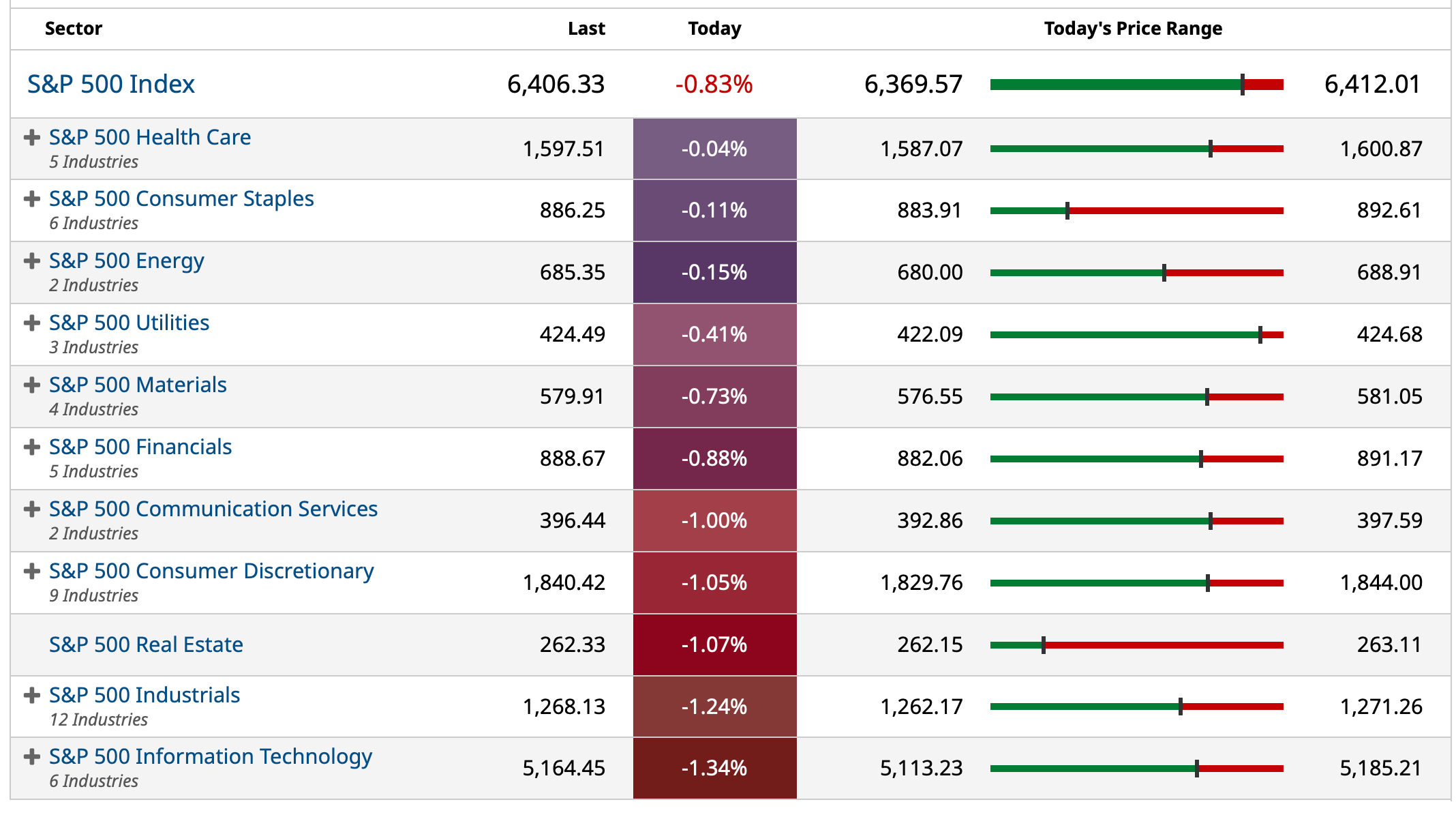

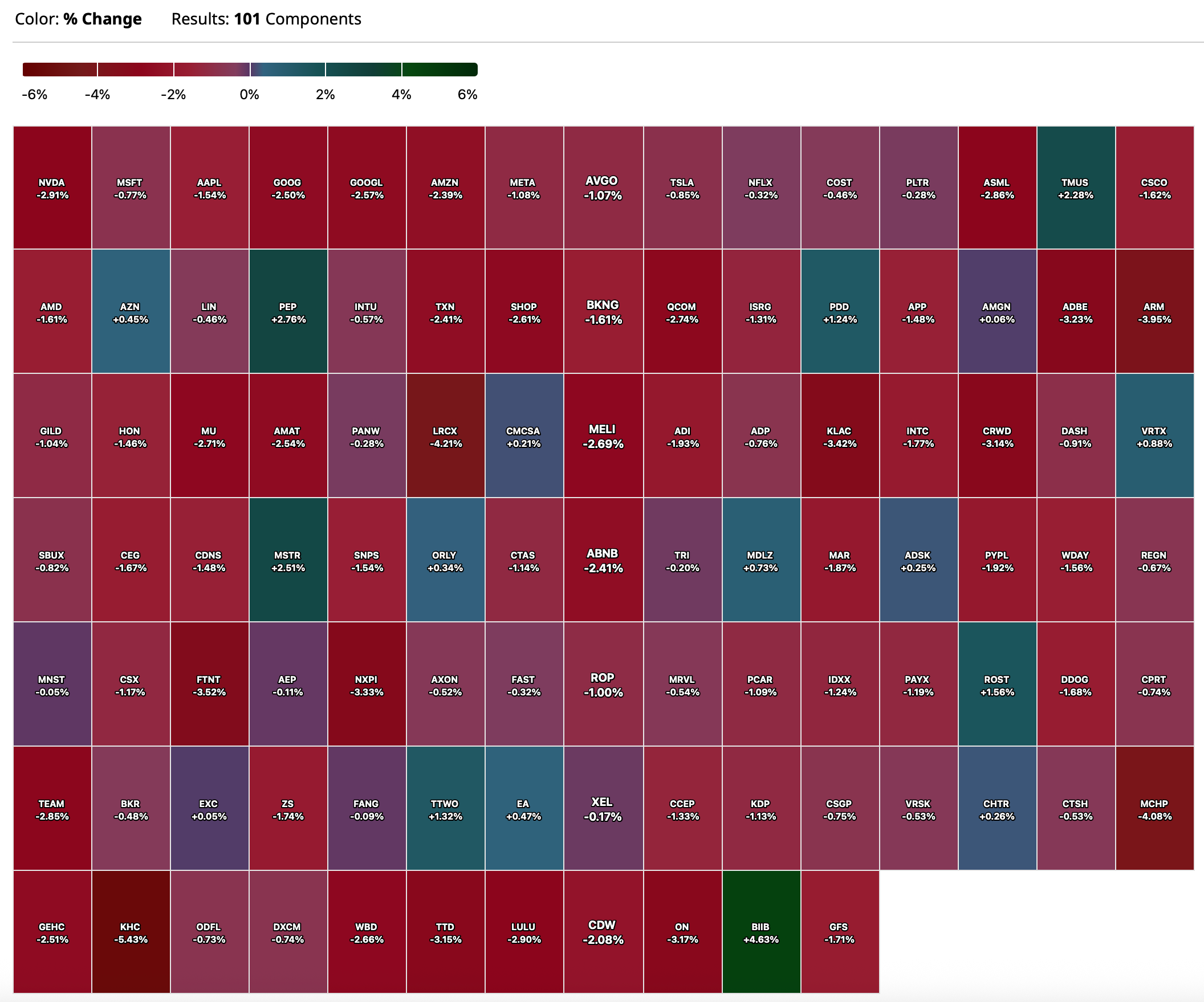

- NYSE volume 16% above its one-month average;

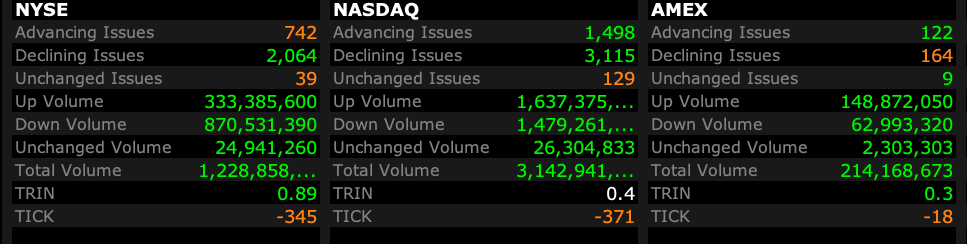

- Nadaq volume flat to its one-month average;

- VIX index: up 15.45% to 18.61

BY Doug Kass · Sep 2, 2025, 11:50 AM EDT

From Peter Boockvar:

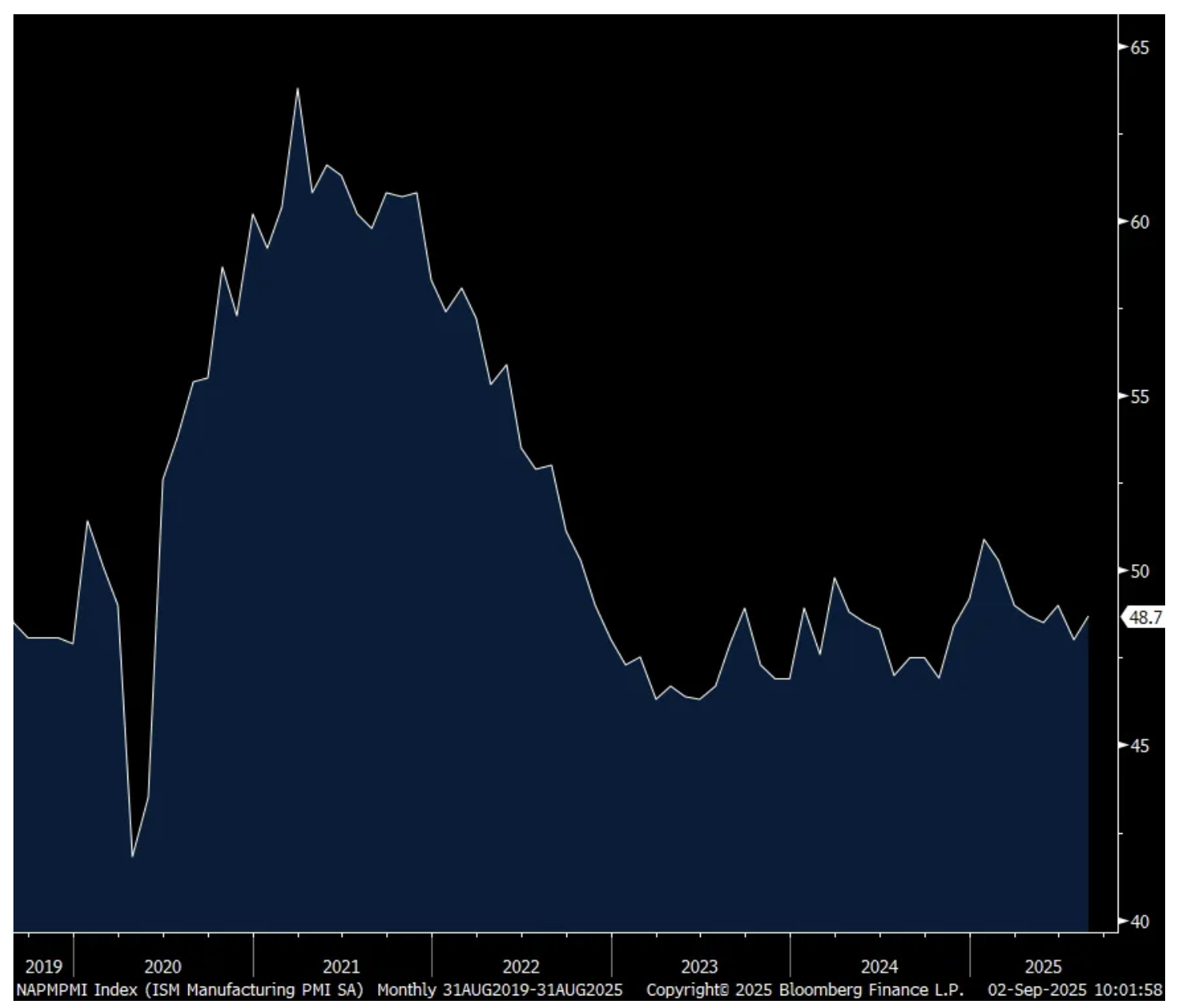

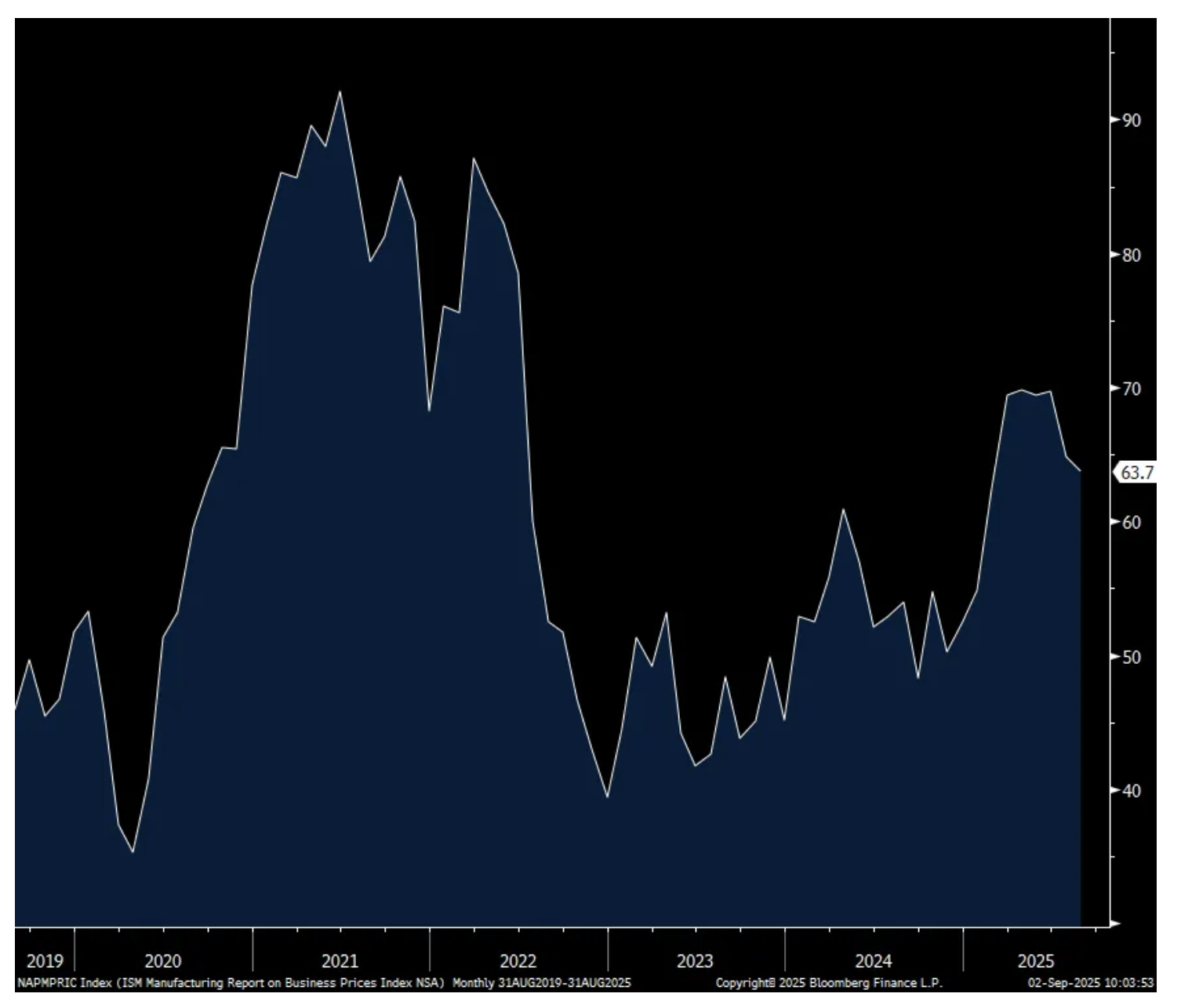

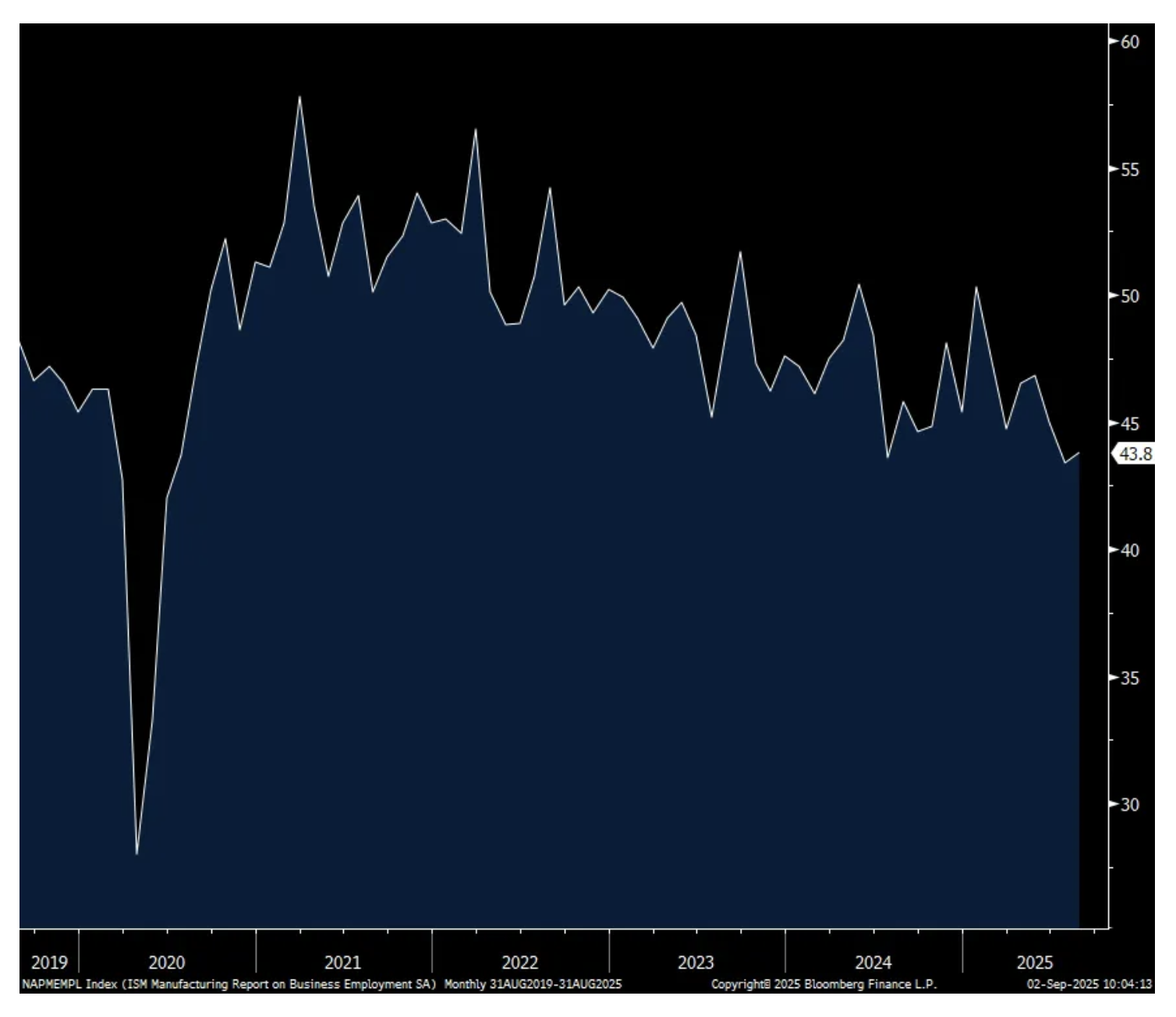

The August ISM manufacturing index rose to 48.7 from 48 but that was just a bit under the estimate of 49 and this index has been below 50 in 32 of the last 34 months. Still hoping that manufacturing is trying to find a bottom saw new orders lift back above 50 at 51.4 from 47.1 and that’s the first time it’s above 50 since January. This while inventories stayed below 50 for the 4th month at 49.4 vs 48.9 in the month before and backlogs fell to 44.7 from 46.8. Customer inventories remain well below 50 at 44.6.

Ahead of the jobs data this week, the employment component was just 43.8, though up a touch from 43.4 in July. Prices paid fell 1.1 pts m/o/m to 63.7, 4 pts below its 6 month average but remaining well above 50. Of the industries asked, 15 paid higher prices vs 16 in July and 15 in June. Supplier deliveries were up 2 pts to back above 50 at 51.3 but unlike in April, May and June where it was around 55, those supply constraints seem to have eased back. Export orders at 47.6 was below 50 for the 6th straight month.

In terms of breadth, it was the same seen in July with 7 industries seeing growth and 10 whose business contracted.

Specifically with new orders, while the component got back into expansion, ISM said “Despite the index’s move into expansion territory, for every positive comment about new orders, there were 2.5 comments expressing concern about near term demand, primarily driven by tariff costs and uncertainty.”

On the labor market, “For every comment on hiring, there were four on reducing head count as companies continued to focus on accelerating staff reductions due to uncertain near to mid-term demand. Layoffs and not filling open positions remain the main head-count management strategies.”

With prices, “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods. Higher prices were reported by 33.5 percent of respondents in August, down from 35.4 percent in July.”

What are respondents saying? A lot about the challenges of dealing with tariffs.

“A 50-percent tariff on imports from Brazil, combined with the U.S. Department of Agriculture’s elimination of the specialty sugar quota, means certified organic cane sugar — and everything made with it — is about to get significantly more expensive.” (Food, Beverage & Tobacco Products)

“Orders across most product lines have decreased. Financial expectations for the rest of 2025 have been reduced. Too much uncertainty for us and our customers regarding tariffs and the U.S./global economy.” (Chemical Products)

“Tariffs continue to be unstable, with suppliers adding surcharges ranging between 2.6 percent to 50 percent.” (Petroleum & Coal Products)

“Tariffs continue to wreak havoc on planning/scheduling activities. New product development costs continue to increase as unexpected tariff increases are announced — for example, 50-percent duties on imports from India, and increases to all countries up from original 10 percent. Our materials/supplies are now rising in price, so our sell pricing is again being reviewed to ensure we keep a sustainable margin. Plans to bring production back into U.S. are impacted by higher material costs, making it more difficult to justify the return.” (Computer & Electronic Products)

“The construction industry, especially home building, is still at a lower level. With new construction at a low level, our new sales are impacted. We are mainly now relying on replacement business. Cost of goods sold is higher due to tariff-impacted goods.” (Machinery)

"Domestic sales remain flat but are down four percent from plan by unit volume [tariff pricing]. Export demand is falling as customers do not accept tariff impacts, which likely will require some production transfers out of the U.S. Supplier deliveries remain consistent with ocean shipping costs dropping significantly. Tariff costs have biggest financial impact but also costs of copper and of steel products." (Fabricated Metal Products)

“The trucking industry continues to contract. Our backlog continues to shrink as customers continue to hold off on buying new equipment. This current environment is much worse than the Great Recession of 2008-09. There is absolutely no activity in the transportation equipment industry. This is 100 percent attributable to current tariff policy and the uncertainty it has created. We are also in stagflation: Prices are up due to material tariffs, but volume is way off.” (Transportation Equipment)

“Very tentative domestic market, with home building and remodeling not very active at all. Inflation, among other factors, is starting to impact consumer buying power, leading to negative signs for our order files. International markets are upended due to the unpredictability of on-again, off-again tariff activity.” (Wood Products)

“We’ve implemented our second price increase. ‘Made in the USA’ has become even more difficult due to tariffs on many components. Total price increases so far: 24 percent; that will only offset tariffs. No influence on margin percentage, which will actually drop. In two rounds of layoffs, we have let go of about 15 percent of our U.S. workforce. These are high-paying and high-skilled roles: engineers, marketing, design teams, finance, IT and operations. The administration wants manufacturing jobs in the U.S., but we are losing higher-skilled and higher-paying roles. With no stability in trade and economics, capital expenditures spending and hiring are frozen. It’s survival.” (Electrical Equipment, Appliances & Components)

“There is still uncertainty in the construction market. Large expansions or investment are hampered by the unknown of costing and the economy. The markets we operate in can be strong short term, but there is an underlying feeling that has you questioning for how long.” (Nonmetallic Mineral Products)

Bottom line, the US manufacturing recession continues on and tariffs threw more mud in its gears. We are due though for improvement and maybe court induced tariff relief could be a catalyst.

ISM Mfr’g

New Orders

Prices Paid

Employment

BY Doug Kass · Sep 2, 2025, 11:30 AM EDT

This is not complicated. Charge the incremental users of the power for the incremental capacity they require, at the generation and distribution level, as opposed to averaging it into the rate base.

Of course, the federal government will come up with the worst possible solution (under the guise of national security or some B.S. of that ilk), and probably subsidize this somehow, and effectively hide it by sticking it on the already bloated balance sheet. This of course makes a bad problem worse, and also leaves the bill with the average person, in a different, but more insidious and worse fashion. Once again, this would be the average person subsidizing the technocrats, who are the last people that need the help, especially from those struggling to put food on the table.

Then, by doing this, it also prevents a common sense, market-based solution from emerging. You know, capitalism.

Doing this also leads to more irrational capital allocation on top of what is already irrational capital allocation.

Unless the users of the incremental power are forced to fully pay for the cost of the incremental power (generation and distribution), the government needs to sit this one out. Otherwise, as usual, it will make a bad problem worse. Any subsidy would fail the "shoe is on the other foot" test and fail it badly. How would they feel about the opposition party funding windmills for example? Oh, we know, because they are cancelling the projects.

From Bloomberg:

(BN) Trump’s Energy Chief Says High Power Bills Are His Top Concern

2025-09-02 14:16:46 GMT

By Ari Natter

(Bloomberg) -- President Donald Trump’s energy chief says

soaring US electricity prices are his biggest concern, remarks

that come as analysts warn utility bills could become a

political liability for Republicans.

“It’s what I worry about most seven days a week,” Energy

Secretary Chris Wright told Fox Business News on Tuesday. “We

want to stop the rise in electricity for Americans and reshore

jobs and opportunity there.”

After decades of flat power demand, surging consumption

from data centers, new manufacturing and the electrification of

the economy is shaking up the US grid. Utility bills are rising

as energy companies rush to generate enough electricity and

build infrastructure to transmit it around the country.....

BY Doug Kass · Sep 2, 2025, 11:15 AM EDT

* From the guy who bought AVGO, AMD and NVDA at the top...

I am reposting this column as it holds true currently:

* Hubris is one of the great renewable resources...

* "What goes around, comes around..."

I have the investing scars on my back, so I have learned (the hard way!) to respect Mr. Market and navigate with the understanding that I am often wrong and always in doubt.

It is for that reason (and that their memories of their mistakes are too often forgotten) that I recoil in reaction to overconfidence in the business media and elsewhere. (This is something I discussed in my Bloomberg interview with Paul and Tom yesterday.)

If a guest or panelist comes across arrogant, it is my view that, especially if he is terribly wrong, he should be open to criticism and reminded of both his arrogance and wrong-footed stance by others. If he is humble, that is another story and criticism should not be immediately levelled at the offender.

In other words, what goes around, comes around...

Smug, condescending and full of hubris is no way to invest, son.

Yesterday the Nasdaq had its second worst day since April 2025.

On Monday , Nvidia's (NVDA) shares suffered their largest fall since April (Broadcom (AVGO) (-$11 yesterday) and Goldman Sachs (GS) (-$10), also previously mentioned and confidentally purchased by the "guy" on CNBC on August 12, also fell dramatically):

While a week or so does not make a potential top, pride goeth before fall...

Let's go to the tapes!

Trade Tracker: Brian Belski buys more Broadcom, Nvidia and AMD

Here is what I wrote only eight days ago on the subject:

* But I will only "criticize by category and praise by individual" (h/t Warren Buffett)

* An appearance on FinTV may have already top ticked the momentum stocks...

"The whole problem with the world is that fools and fanatics are always so certain of themselves and wiser people so full of doubts."

-Bertrand Russell

I am often wrong and always in doubt.

My mantra is that we should not be overly confident as we still have to count the votes!

As I have consistently written over the years, this is too often not the case for uber confident "talking heads" in the business media who are trying to improve their brands, sell a service or gain money management assets.

That said, I am increasingly convinced that my observations in "Watching In Amazement" will prove insightful:

Aug 12, 2025 2:43 PM EDT

I had CNBC's "Halftime Report" on today and I listened to a panelist (praise by individual, criticize by category — so no names!) who confidently added (AVGO) , (NVDA) and (GS) to his portfolio this afternoon.

Please look at the price charts of those companies before you read further!

While I recognize that my market view has been half baked for quite a while and having been mentored at Putnam by one of the great momentum traders in history ("The Chief") — I simply can't fathom the downside versus upside (and the absence of a margin of safety) in these buys.

While my general concerns continue to be realized — most notably: slowing economic growth, prickly inflation (seen in this morning's CPI report) and ever higher valuations — this has obviously not translated into a lower market.

Every day it grows clearer that momentum is a force unto itself.

It is terribly frustrating as I try to operate within the framework of a market that is disinterested in negatives and is continuing to be bought on every dip.

Despite that frustration I will not chase under any condition and compromise my investment process.

I will buy value (as I recently did with (UNH) and (PSKY) but I will never abandon the notion of risk/reward.

By Doug Kass Aug 15, 2025 11:30 AM EDT

Position: Long PSKY (VS), UNH (VS)

Aug 20, 2025 7:30 AM EDT

BY Doug Kass · Sep 2, 2025, 10:51 AM EDT

From Peter Boockvar:

Here were the most relevant comments from the Federal Appeals Court upholding the previous decision with regards to the use of the International Emergency Economic Powers Act:

"in each statute delegating tariff power to the President, Congress has provided specific substantive limitations and procedural guidelines to be followed in imposing any such tariffs. It seems unlikely that Congress intended, in enacting IEEPA, to depart from its past practice and grant the President unlimited authority to impose tariffs. The statute neither mentions tariffs (or any of its synonyms) nor has procedural safeguards that contain clear limits on the President's power to impose tariffs."

"Taken together, these other statutes indicate that whenever Congress intends to delegate to the President the authority to impose tariffs, it does so explicitly, either by using unequivocal terms like tariff and duty, or via an overall structure which makes clear that Congress is referring to tariffs. This is no surprise, as the core Congressional power to impose taxes such as tariffs is vested exclusively in the legislative branch by the Constitution; when Congress delegates this power in the first instance, it does so clearly and unambiguously."

Finally of note, "Upon declaring an emergency under IEEPA, a President may, in relevant part, 'investigate, block during the pendency of an investigation, regulate, direct and compel, nullify, void, prevent or prohibit' the 'importation or exportation of...any property in which any foreign country or a national thereof has any interest.' 'Regulate' must be read in the context of these other verbs, none of which involve monetary actions or suggest the power to tax or impose tariffs."

And the bottom line, "we discern no clear congressional authorization by IEEPA for tariffs of the magnitude of the Reciprocal Tariffs and Trafficking Tariffs. Reading the phrase 'regulate...importation' to include imposing these tariffs is a 'wafer thin reed on which to rest such sweeping power'...Given these considerations, we conclude Congress, in enacting IEEPA, did not give the President wide-ranging authority to impose tariffs of the nature of the Trafficking and Reciprocal Tariffs simply by the use of the term 'regulate...importation.'"

As the court has allowed the tariffs to continue on until October with the expected appeal to the Supreme Court, we of course wait for that and what other Sections the administration will use to replace the tariffs lost. In the early part of this year I was hoping that the use of tariffs would be strategic and narrowly focused rather than scattershot. Instead, we got the latter but maybe striking down the use of IEEPA will get back to a strategic and narrowly focused approach rather than tariffing things that we will never make in the US and are not of national security purposes like coffee from Brazil to use just one example. Or T-shirts from Bangladesh or sneakers from Vietnam. And I can go on and on.

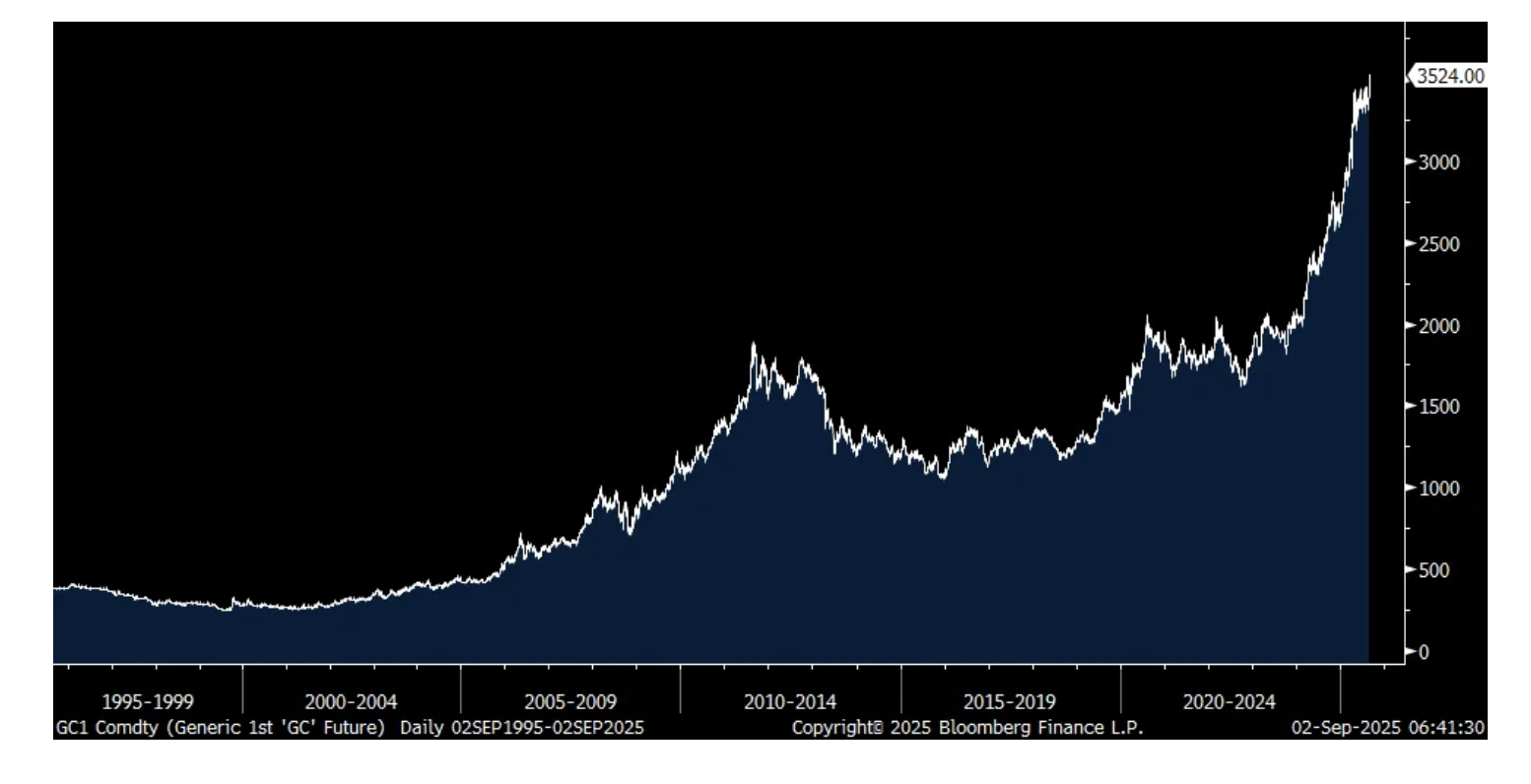

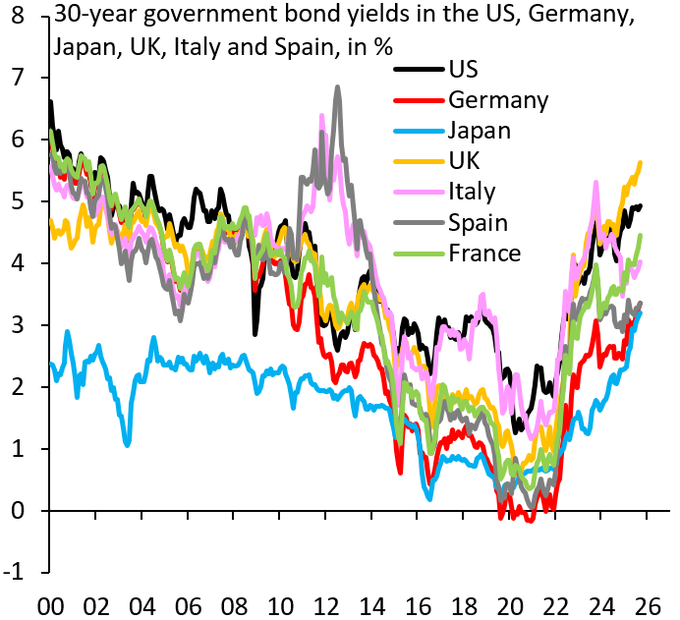

I'll say for the umpteenth time, you must keep your eye on long term bond yields because they are moving higher again and gold continues to be the biggest beneficiary of the push back against excessive debts and deficits as it is at a record high, also taking up silver and platinum. The British pound and yen are also getting hit hard today. Gilt yields are moving higher again but JGB yields are little changed after a better than expected 10 yr auction. Also lifting other European yields was the 2.3% core CPI print in August in the Eurozone which was one tenth above the estimate and holding the July increase. The headline gain at 2.1% was as forecasted but up from 2% in July. The US 30 yr yield is knocking on 5%, again. We remain bearish on long duration bonds and long gold, silver and platinum.

Gold

As part of my constant due diligence on the state of the US economy, I wanted to confirm the strength of the live concert business and went to see Oasis last night at MetLife stadium. I paid the most amount of money I've ever spent for face value tickets at $400 per for my son and I and wanted to see if anyone was going to show up with those prices. And sure enough they did with about 60,000 other people following their previous night's performance in front of the same amount of people. We remain long Live Nation, Madison Square Garden Entertainment and Universal Music Group.

As we market participants look now to the rest of 2025, Oasis sang these lyrics from their great song "The Masterplan":

“I'm not saying right is wrong

It's up to us to make

The best of all the things that come our way

'Cause everything that's been has passed

The answer's in the looking glass

There's four and twenty million doors

On life's endless corridor

Say it loud, and sing it proud

And they

Will dance if they wanna dance

Please, brother, take a chance

You know they're gonna go

Which way they wanna go

All we know is that we don't know

How it's gonna be

Please, brother, let it be

Life on the other hand

Won't make you understand

We're all part of a master plan”

On to some important earnings comments from late last week and I'll do my best to keep each brief since there were a lot. For the retailers, those doing well are providing value, newness and innovation. If you can't, times are tough. With tech, you are either selling into the AI infrastructure buildout or you're not and if you are, the bar is high in terms of expectations.

From Best Buy:

Comps rose 1.6%, "our highest in three years...We grew sales in several product categories, including gaming, computing, mobile phones, wearables, and headphones. This growth was partially offset by declines in the home theater, appliance, tablet, and drone categories."

"For the most part, customer shopping behavior in the first half of the year has not changed materially from the commentary we have shared for the past several quarters. Customers continue to be resilient, but deal focused and attracted to more predictable sales moments, including our Black Friday and July sales event."

"In the current environment, customers continue to be thoughtful about big ticket purchases and are willing to spend on high price point products when they need to or when there is technology innovation."

On tariffs, they only directly import 2% to 3% of what they sell. "So that means, as it relates to tariffs, some vendors are clearly communicating cost trends - cost increases. Some are adjusting promotions, some are planning to potentially increase prices with new product innovations, which always happens in our space, and some are just not increasing them at all, given these are very, very global supply chains."

From Dollar General:

"Same store sales increased 2.8% during the quarter, driven by relatively balanced growth of 1.5% in customer traffic and 1.2% in average basket. The basket growth was driven by an increase in both average unit retail price per item and average items per basket."

"We were excited to see a second consecutive quarter of broad based category growth with positive comps in each of our consumables, seasonal, home, and apparel categories."

"we're pleased to see growth with customers across all income brackets during the quarter. This includes our core customer, who increased spending despite worsening sentiment."

"In addition, we continue to see trade-in growth with middle and higher income customers during the quarter, which we believe is contributing to the nice performance we've seen in our non-consumable categories. Ultimately, customers across all income brackets are coming to Dollar General as they seek value."

And to that value, they "will continue to have at least 2,000 items at $1 or less every day on the shelf."

On tariffs, "With the rates currently in place, we believe we will be able to mitigate the vast majority of the impact on our cost of goods. The proactive approach of our sourcing team, coupled with our relatively low direct import exposure, has positioned us well to serve our customers with a quality assortment at tremendous value. While the landscape remains dynamic, tariffs have begun to result in some price increases, and we will continue to work to minimize them as much as possible."

From Five Below:

Comps grew almost 13% as "delivering extreme value I think has been one of our keys to success this past quarter. And clearly communicating that we've got an amazing assortment, the majority of which is at $5 and below."

"in terms of the customer and tariffs on a go forward basis, we've seen really nice growth in customers, both new as well as retained, and great, nice traffic trends. And so all of that has been very positive, when we have taken those price adjustments and really looked at simplification of pricing, we've been pleased with the elasticity that we've seen in terms of those adjustments."

From Burlington Stores, another value focused retailer:

Comps grew 5% after a 5% growth rate last year. "The trend in Q2 started out slowly with the weather in the Midwest and Northeast in May being cooler than last year, but then our trend picked up in June and July as the weather normalized."

"Traffic was flattish in the quarter. Our comp was driven by a higher transaction size."

"Let me move on to the outlook for the rest of the year. Despite our strong performance in the second quarter, we remain concerned about the external outlook for the back half. We are maintaining our comp guidance of 0% to 2% for Q3 and Q4."

"Our updated full year guidance assumes that we will be able to offset most, but not all of this incremental tariff pressure."

From Williams Sonoma:

Comps grew 3.7% "with all brands again running positive comps...This was our second quarter of accelerated positive comps coming out of 2024, despite continued geopolitical uncertainty and no material improvement in the housing market."

With furniture specifically and the sales gain there, "you're not seeing housing improve. Did we hit the bottom? Could be. But it's really related to the product offer. We can see it completely linked to the newness we're bringing in."

With tariffs, "At our May earnings call, our incremental tariff rate was 14%. As of today's call, it has doubled to 28%" but they outlined a 6 point mitigation plan that includes this, "we are carefully taking select price increases on products with a focus on maintaining competitive pricing."

From Dick's Sporting Goods:

Q2 comps were up 5% "with growth in average ticket and transactions." And, "we continue to gain market share from online only and from omnichannel retailers."

The 5% was "driven by a 4.1% increase in average ticket and a .9% increase in transactions. We saw broad based strength across our key categories."

They lifted guidance and said it "balances our confidence in the outcomes we are driving through our strategic initiatives and our operational strength against the ongoing complex and dynamic macroeconomic environment."

"We are not seeing any signs of slowdown with the consumer. In fact, one of the most exciting things about the quarter that we just delivered is the broad based nature of the growth that we saw...So footwear, apparel, team sports, and golf, all doing really, really well."

From Ulta Beauty:

Comps rose 6.7% with "positive comp growth in both channels and all major categories, continued market share gains during a highly competitive quarter."

"I want touch on what we're seeing across the beauty and consumer landscape. Engagement with beauty and wellness remains healthy. The growth of the US beauty category has been fairly stable, with low single digit growth in mass and mid single digit growth in prestige beauty during the second quarter."

"Our insights suggest consumers continue to prudently manage their day-to-day spending and are watchful of pricing trends in response to tariffs. At the same time, beauty enthusiasts tell us that they're prioritizing their beauty regimens and remain strongly engaged within the category. While we continue to manage the business thoughtfully amid ongoing macroeconomic uncertainty, we believe beauty and wellness offer a unique sense of comfort and escape, which we expect will continue to support the beauty category resilience."

Stepping up to a higher price point, from Malibu Boats:

"Fiscal year 2025 was a challenging period for the marine industry, shaped by a difficult retail environment and heightened tariff uncertainty."

"As we noted in fiscal Q3, we expected dealers to continue trimming inventory. Elevated interest rates, ongoing macroeconomic uncertainty, and the timing of trade policy changes weighed on consumer sentiment, which showed up in the softer industry retail data. Initial market data suggests that fiscal Q4 was the weakest quarter of the year with the broader market down mid-teens percentage points."

As for fiscal '26, "at this point we're kind of seeing more of the same. There's nothing that says there's going to be this wild rise up yet that we're at the beginning of the next up cycle. So we've kind of looked at it and positioned it as more of the same."

From Affirm, where we now the use of Buy Now, Pay Later continues to increase:

"we're feeling very good about the originations we're driving. We feel quite excellent about our ability to get paid back on time. So on the credit side of the equation, continues to perform really well. On the demand for our service, you see the acceleration in GMV and the new record in that sense, off calendar, if you will, is also a reflection of the fact that folks are using Affirm for more and more things."

On to some tech companies.

From Dell:

"We continue to see strong demand for AI servers, building on the exceptional demand observed in Q1...Our pipeline remains multiples of our backlog."

"In traditional servers, revenue grew again...From a demand perspective, international markets grew, but the April weakness we saw in North America continued."

"In storage, revenue was down 3% and demand moderated."

Their Client Solutions Group which includes PCs saw little growth and "We expect moderate growth as the PC refresh continues, driven by an aging installed base and the Windows 10 end-of-life, which is now 48 days away."

From Marvell Technologies:

"Our data center end market continued its strong momentum, growing 69% y/o/y, fueled by robust AI demand. We also saw solid recovery in our enterprise networking and carrier infrastructure end markets."

They did however talk about "lumpiness...particularly with the large hyperscale builds that happen and especially as you ramp them into production." And that's the main reason why the stock got hammered on Friday as they see Q3 data center revenue flat sequentially.

Lastly, here were the PMI's from overseas and they were up across the board m/o/m but with still some key manufacturing indices below 50:

China's manufacturing PMI 49.4 vs 49.3

China's non-manufacturing PMI 50.3 vs 50.1

Japan 49.7 vs 48.9

South Korea 48.3 vs 48

Taiwan 47.4 vs 46.2

Indonesia 51.5 vs 49.2

Thailand 52.7 vs 51.9

India 59.3 vs 59.1

Australia 53 vs 51.3

Malaysia 49.9 vs 49.7

BY Doug Kass · Sep 2, 2025, 10:45 AM EDT

It's a world of laughter,

a world of tears

It's a world of hopes

and a world of fears

There's so much that we share

that it's time we're aware

It's a small world after all

It's a small world after all

It's a small world after all

It's a small world after all

It's a small, small world

- It's A Small World It's A Small World

This New York Times article on Disney underscores my concern about this popular but disappointing company and stock: Opinion | Disney World Is the Happiest Place on Earth, if You Can Afford It.

For some time I have viewed too steady and rapid escalation of theme park admission prices as a threat to consensus earnings per share expectations.

I have found that demand elasticity (read: weakening demand) would follow those admission price hikes over the fullness of time.

I still do.

This keeps me from buying this seemingly cheap stock.

BY Doug Kass · Sep 2, 2025, 10:20 AM EDT

BY Doug Kass · Sep 2, 2025, 10:05 AM EDT

I will take off half $53.17:

I am shorting (XLF) at $54.07.Position: Short XLF (VS)

Short XLF S

Aug 29, 2025 2:13 PM EDT

BY Doug Kass · Sep 2, 2025, 9:54 AM EDT

BY Doug Kass · Sep 2, 2025, 9:45 AM EDT

PLTR (a short), down another six beaners in premarket, appears to be rolling over.

BY Doug Kass · Sep 2, 2025, 9:35 AM EDT

It remains my contention that (with a 35%+ weighting) -- as go hyperscalers and AI chip manufacturers -- so goes the markets. Surprisingly, a critical discussion about AI has been materially absent in the business media dialogue.

It's as if they build them, the herd/consensus believes they will come. (We remain short NVDA at fine prices thank you!).

As I discussed in a recent Bloomberg Market Surveillance interview link (with Paul Sweeney and Tome Keene and a terrific podcast with Rosie to be distributed tomorrow) the search for truth abhors consensus, because when consensus is reached, thinking stops.

For that reason I have written over 100 "More Tales."

Maybe heads should stop nodding about sky high expectations for AI.

As Bob Farrell writes, "excesses are never permanent."

I have approached this series of "More Tales" as a layman and not as a luddite -- trying to use analysis and common sense -- with a dash of skepticism.

Moving forward with my next "Tales":

'The core barrier to scaling is not infrastructure, regulation or talent. It is learning. Most GenAI systems do not retain feedback, adapt to context or improve over time."

From Spinal Tap Meets John Malkovich -- What's so funny about the need for world models by Gary Marcus (August 31) Spinal Tap meets John Malkovich - by Gary Marcus :

It reminds me of a subplot in the novel Catch 22, where Milo Minderbinder has this syndicate business which is profitable, with the exception of his decision to buy all Egyptian cotton in existence, which he cannot unload afterward (except to other entrepreneurs, who sell the cotton back to him, because he simply ordered all Egyptian cotton) and tries to dispose of the cotton by coating it with chocolate and serving it in the mess hall.

This whole round tripping issue also reminds me of the economics of the AI ecosystem too, and all the cotton coated up with chocolate by definition ended up in the toilet after a long period of indigestion!

Post Script: Maybe Gen AI is a job creator after all, and will lead to more demand for labor?

This article: Humans are being hired to make AI slop look less sloppy

BY Doug Kass · Sep 2, 2025, 9:30 AM EDT

-SSKN +77% (IP portfolio holds exclusivity in combination therapies of Its XTRAC Excimer Laser with JAK inhibitors, systemic and biologic drugs)

-UUU +75% (Board declares a special dividend of $1.00/shr)

-UTHR +42% (Tyvaso meets primary endpoint in TETON-2 study, improving lung function in Idiopathic Pulmonary Fibrosis)

-CYTK +26% (late-stage study data shows Company’s drug more effective for heart disease symptoms than standard-of-care)

-HOTH +20% (Cancer Therapeutic HT-KIT surpasses preclinical milestones with potent anti-tumor activity and GLP-validated bioanalytical results, exceeding regulatory standards)

-IONS +17% (Olezarsen significantly reduces triglycerides and acute pancreatitis events in landmark pivotal studies for people with severe hypertriglyceridemia (sHTG); plans to submit sNDA to U.S. FDA by end of year)

-ULCC +16% (Deutsche Bank Raised ULCC to Buy from Hold, price target: $8)

-TIXT +15% (agrees to full ownership of TELUS Digital at $4.50/shr)

-IDYA +13% (to present First Median Overall Survival Data from Phase 2 Trial of the Darovasertib/Crizotinib Combination in Metastatic Uveal Melanoma at the 2025 Society for Melanoma Research Congress)

-INSM +8.0% (Unit Insmed Gene Therapy LLC Receives US FDA Orphan Drug Designation for treatment of Duchenne Muscular Dystrophy)

-LQDA +7.4% (strength in sympathy with UTHR)

-AL +6.3% (to be acquired at $65/shr by Sumitomo, SMBC Aviation Capital, Apollo, and Brookfield)

-PEP +4.6% (Elliott confirms investment of $4B in PepsiCo; encouraged PepsiCo's management and Board to embrace change and work toward becoming a faster growing, higher margin and far more valuable company)

-SIG +3.6% (earnings, guidance)

-SAIL +3.3% (Morgan Stanley Raised SAIL to Overweight from Equal Weight, price target: $25)

-NIO +3.2% (earnings, guidance)

-ZYME -15% (to discontinue clinical development of ZW171, a Mesothelin-directed T cell Engager)

-STZ -8.2% (cuts guidance)

-FTFT -6.7% (signs Project Cooperation Agreement with Innovatelab LLC, securing the global exclusive license for the revolutionary 'Vacuum Parcel' technology for ultra-high-speed rail transportation)

-CTOR -4.9% (files $200M mixed shelf)

-ASO -4.3% (guidance)

-LRCX -4.0% (Morgan Stanley Cuts LRCX to Underweight from Equal Weight, price target: $92)

-ELF -3.6% (Deutsche Bank Cuts ELF to Hold from Buy, price target: $128)

-NVDA -2.6% (downside momentum)

-LYFT -2.3% (files to sell $450M in convertible notes due 2030)

BY Doug Kass · Sep 2, 2025, 9:20 AM EDT

I am adding to MSOS at $3.21.

BY Doug Kass · Sep 2, 2025, 9:17 AM EDT

BY Doug Kass · Sep 2, 2025, 8:59 AM EDT

BY Doug Kass · Sep 2, 2025, 8:45 AM EDT

BY Doug Kass · Sep 2, 2025, 8:35 AM EDT

TREASURY AUCTIONS FOR TUESDAY

11:00 a.m.: Treasury Announces a 4 and 8 Week Bill Auction;

11:30 a.m.: Treasury hosts an $82B 3- and a $73B 6-Month Bill Auction;

1:00 p.m.: Treasury hosts a $50B 52-Week Bill Auction;

1:00 p.m.: Treasury hosts an $85B 6-Week Bill Auction

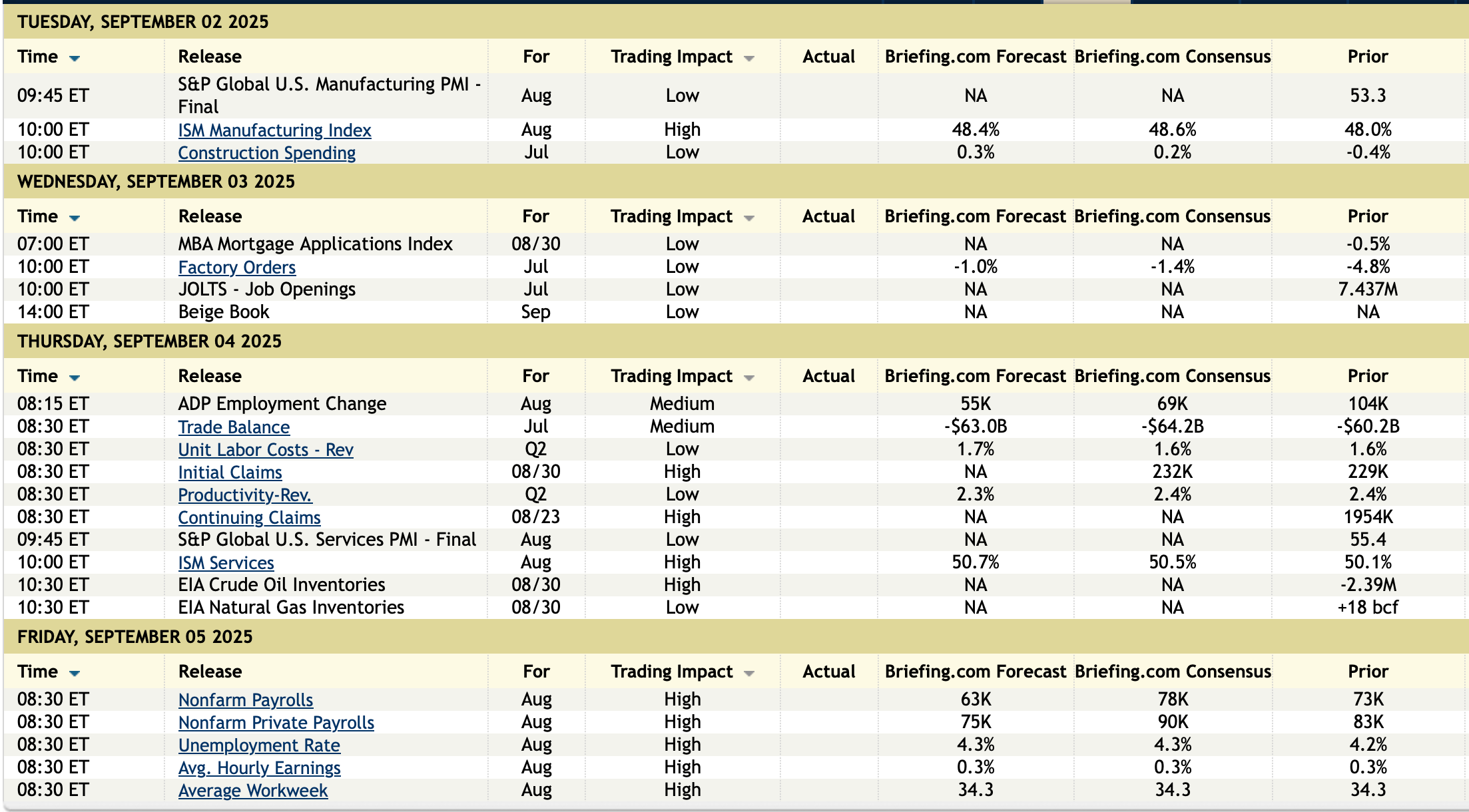

ECONOMIC CALENDAR FOR THE WEEK

BY Doug Kass · Sep 2, 2025, 8:25 AM EDT

I'm buying more Coca-Cola KO in premarket at $69.17 after the PepsiCo PEP news (+$7).

BY Doug Kass · Sep 2, 2025, 8:00 AM EDT

BY Doug Kass · Sep 2, 2025, 7:50 AM EDT

BY Doug Kass · Sep 2, 2025, 7:40 AM EDT

Elliott Management has announced a $4 billion stake in PepsiCo PEP — planning an activist program.

PEP shares are +$7 in premarket trading.

We are long PEP and have recently added.

BY Doug Kass · Sep 2, 2025, 7:35 AM EDT

BY Doug Kass · Sep 2, 2025, 7:30 AM EDT

Bonus - Here are some great links:

Post Labor Day Blues ("Jazzy" Jeff Hirsch)

BY Doug Kass · Sep 2, 2025, 7:15 AM EDT

BY Doug Kass · Sep 2, 2025, 7:05 AM EDT

BY Doug Kass · Sep 2, 2025, 6:55 AM EDT

From Charlie!

BY Doug Kass · Sep 2, 2025, 6:45 AM EDT

BY Doug Kass · Sep 2, 2025, 6:35 AM EDT

BY Doug Kass · Sep 2, 2025, 6:25 AM EDT

BY Doug Kass · Sep 2, 2025, 6:15 AM EDT

Wolf Street howls about office CMBS delinquency rates.

BY Doug Kass · Sep 2, 2025, 6:05 AM EDT

Doomberg on "Drowning Swimmers"

BY Doug Kass · Sep 2, 2025, 5:55 AM EDT

The S&P Short Range Oscillator is at 2.91% vs. 2.63% — moving to a greater overbought.

BY Doug Kass · Sep 2, 2025, 5:45 AM EDT

$NVDA worst day since April. Also closed below its 20dma for the first time in almost four months.