My Nvidia Plan

I plan to maintain my small-sized Nvidia NVDA short (after reviewing the EPS release).

I will short more on strength.

More later.

BY Doug Kass · Aug 27, 2025, 4:45 PM EDT

I plan to maintain my small-sized Nvidia NVDA short (after reviewing the EPS release).

I will short more on strength.

More later.

BY Doug Kass · Aug 27, 2025, 4:45 PM EDT

At 4:26 p.m.:

BY Doug Kass · Aug 27, 2025, 4:35 PM EDT

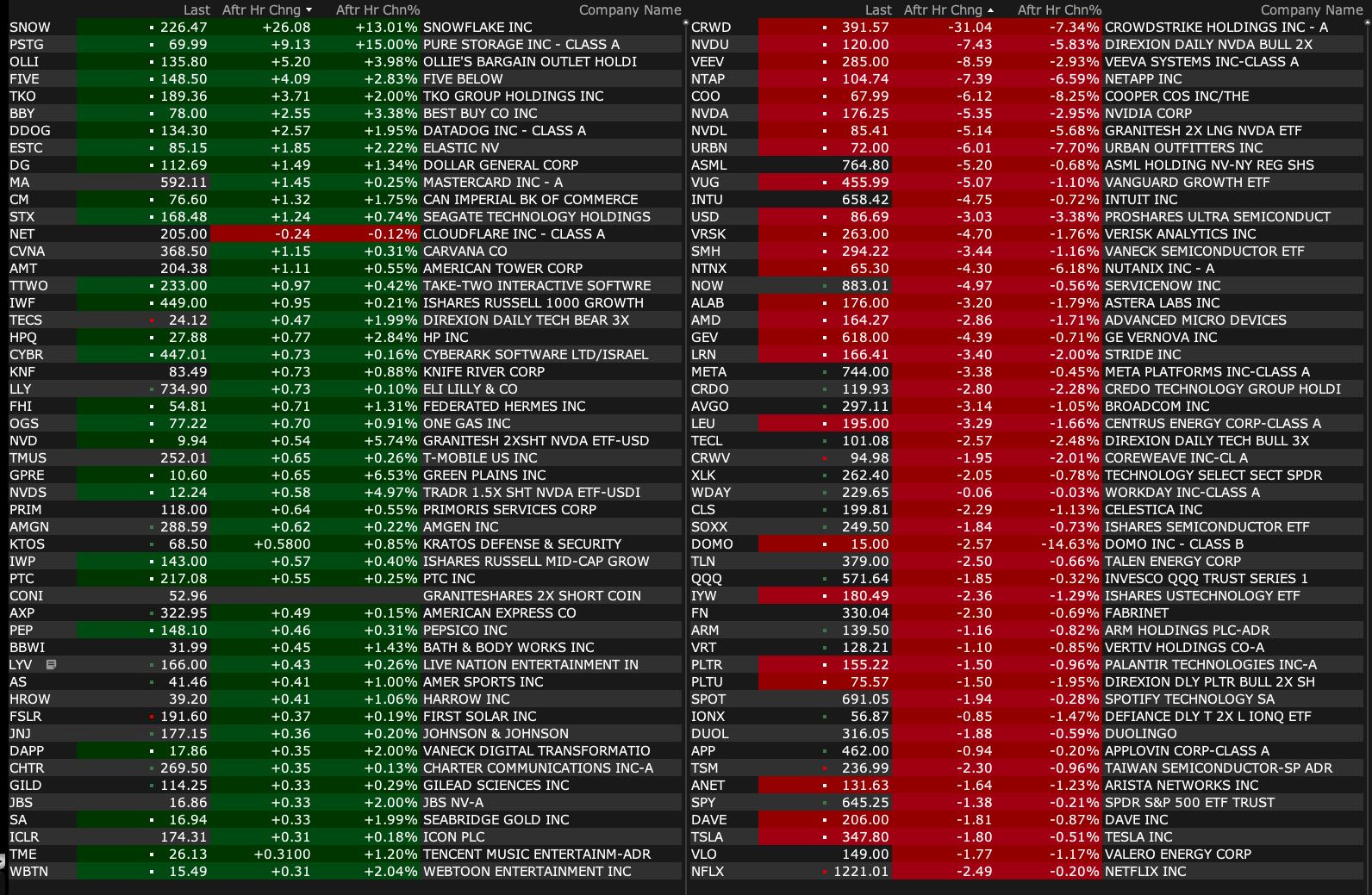

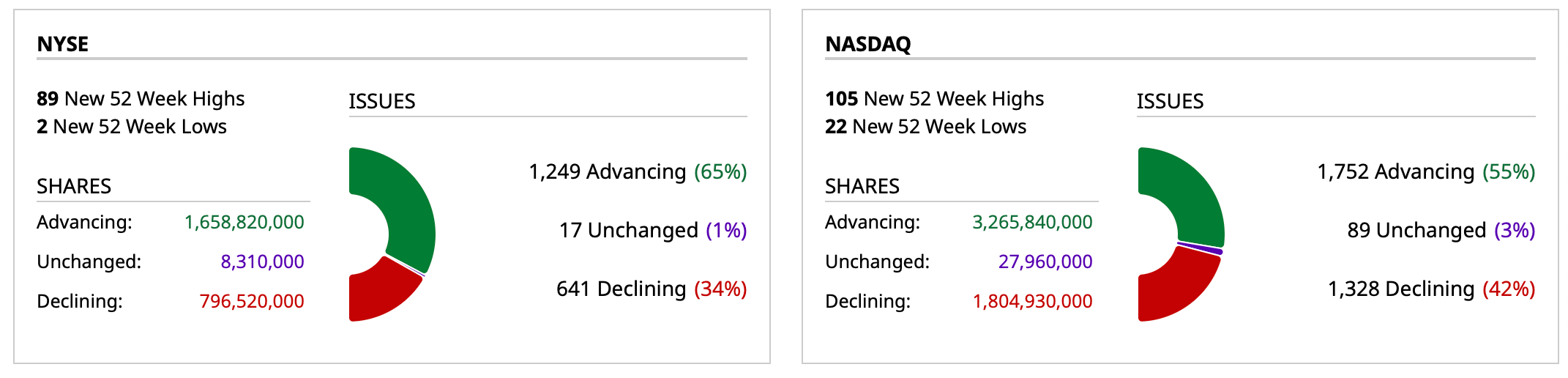

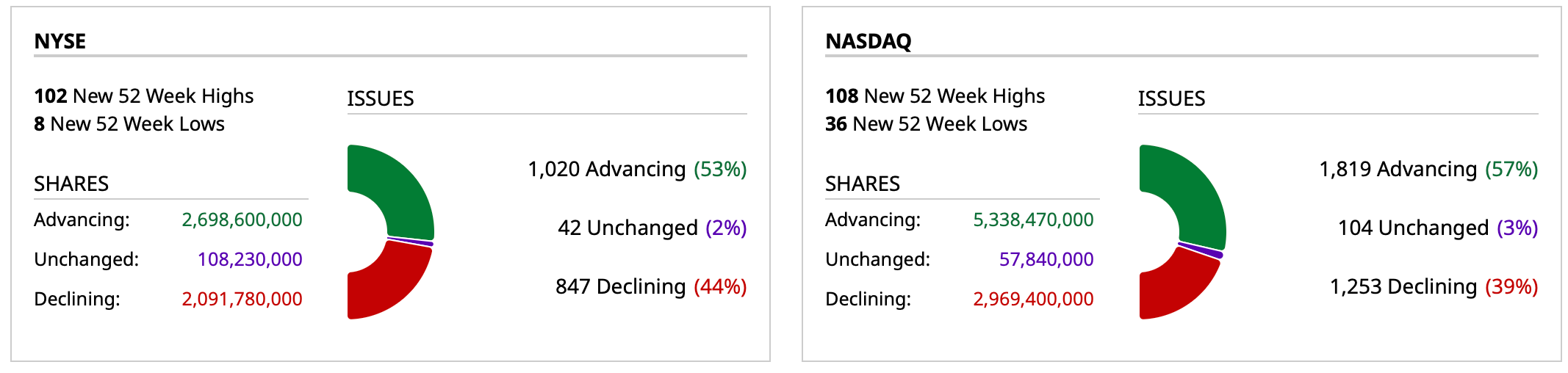

- NYSE volume 19% below its one-month average

- NASDAQ volume 11% below its one-month average

- VIX index: up 1.64% to 14.86

BY Doug Kass · Aug 27, 2025, 4:27 PM EDT

* Part of my short homebuilders thesis...

BY Doug Kass · Aug 27, 2025, 3:15 PM EDT

Wolf Street howls that the bond market should not be trifled with.

BY Doug Kass · Aug 27, 2025, 3:05 PM EDT

Payme

Are passive funds to blame for market mania? Have they killed off many of those willing to bet on a downturn?

Dougie Kass

passive funds have squelched volatility, exacerbated the momentum and abetted the concentration.

BY Doug Kass · Aug 27, 2025, 2:45 PM EDT

With S&P cash +20 handles I am adding to my index shorts:

* SPY $647.25

* QQQ $574.25

BY Doug Kass · Aug 27, 2025, 2:35 PM EDT

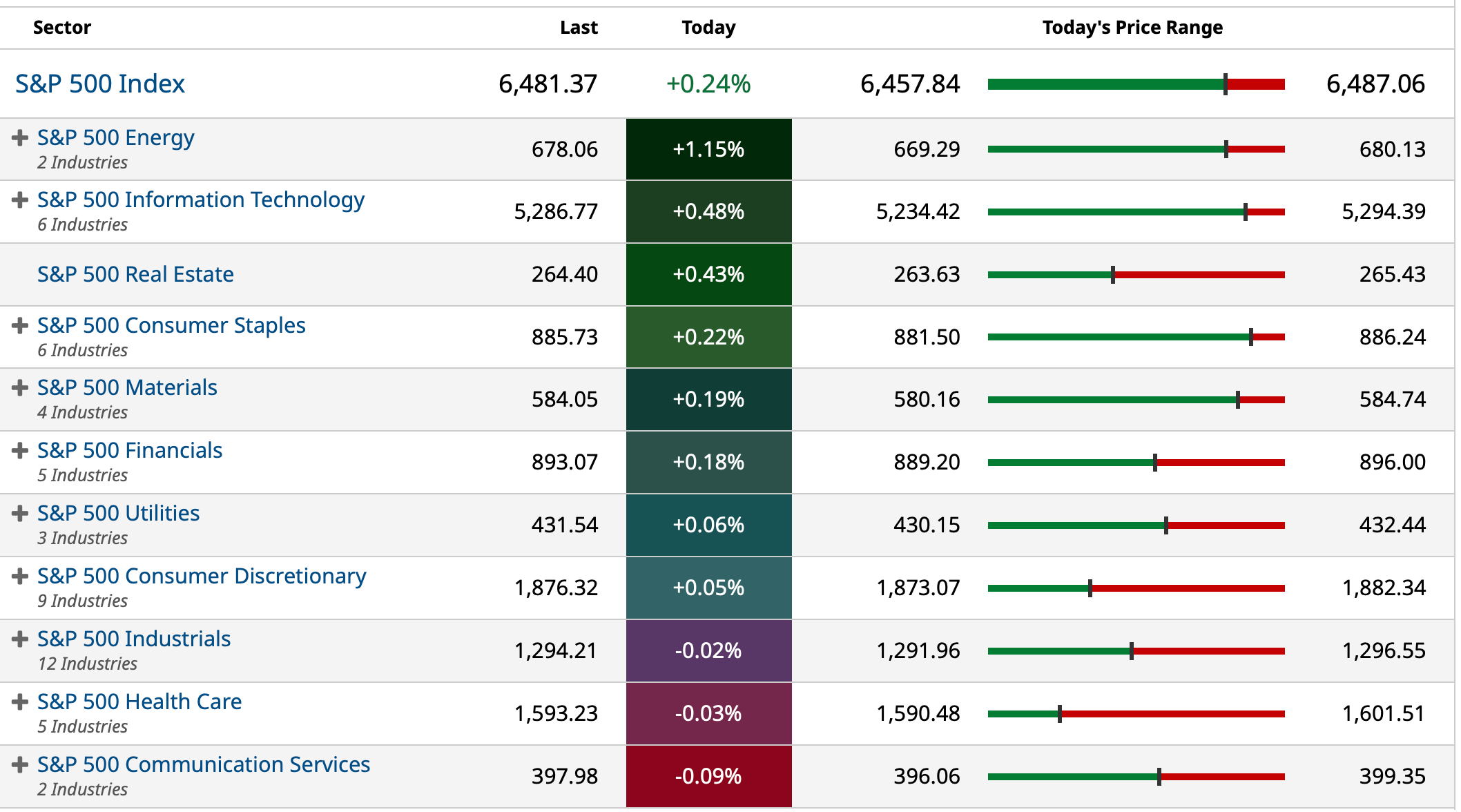

Per my previous point about AI being inflationary over the short term (in More Tales) and not having any impact on the economy otherwise (productivity, etc.) now this on a report from Morgan Stanley:

A new report from a team of Morgan Stanley analysts, led by Stephen Byrd, told clients that "AI impacts may take longer to appear in economic data," with the first real signs not expected until "later this decade and into the next."

Believe me, if there was a real and tangible benefit along the lines of what has been hyped or lead to job losses, it would show up in the numbers, despite the excuses regarding data gathering issues.

If there is not a real and tangible benefit soon (that also delivers a return on invested capital (ROIC) to the suppliers of the technology), investment will not continue at this rate, because they are already spending at 11 (prior rant) and when your CAPEX is 30% of revenue you can’t do more of it.

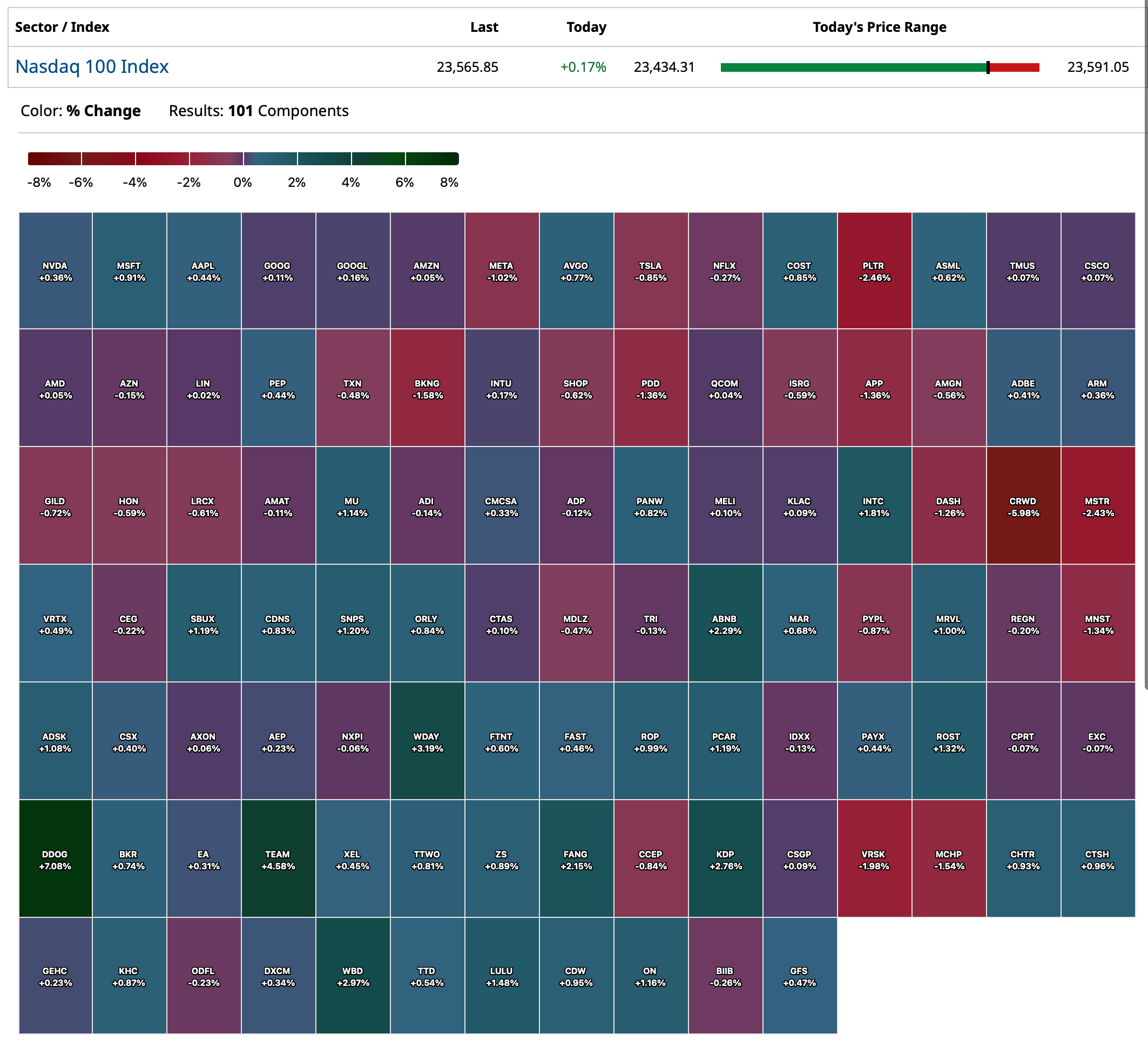

I will go into the Nvidia NVDA EPS report (after the close) very small sized short.

With all the CAPEX previously announced.... if NVDA does not deliver massive upside to numbers and guidance I will be stunned. Stay tuned.

BY Doug Kass · Aug 27, 2025, 1:55 PM EDT

BY Doug Kass · Aug 27, 2025, 1:35 PM EDT

I am adding to my lengthy list of financial shorts with Schwab SCHW ($96.95) now.

BY Doug Kass · Aug 27, 2025, 1:25 PM EDT

BY Doug Kass · Aug 27, 2025, 1:17 PM EDT

TechNova

Unifying the FED under control of the White House, is a trajectory to which we already know the final destination.

Dougie Kass

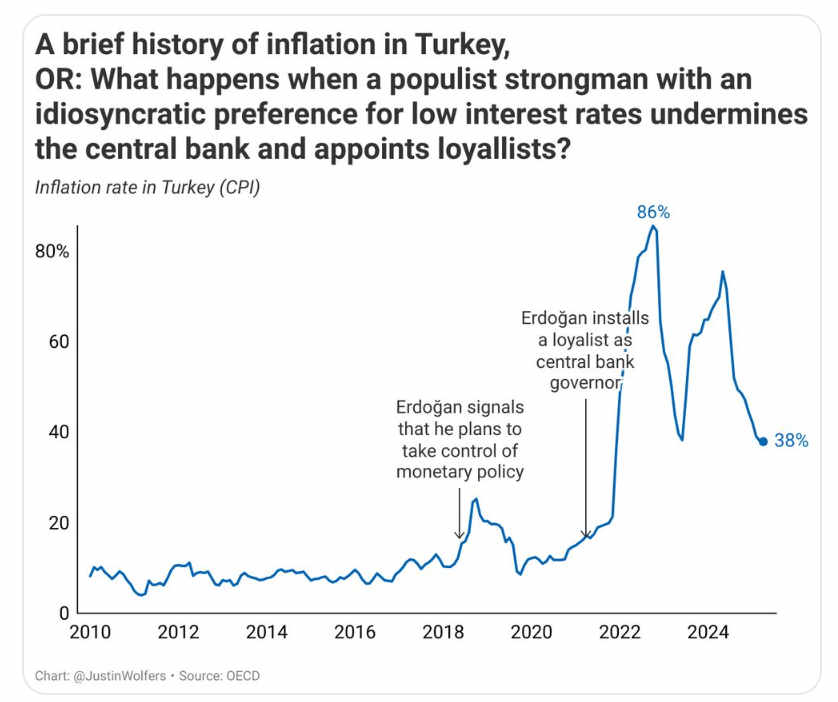

History is clear.

Populist strong men who undermine their central banks and abandon price stability by promoting extremely easy money policy end up in the shit house, economically and currency wise.

Turkey, above, is an example.

Argentina is an even better example. It had the ninth largest country GDP until Eva Peron...

TechNova

So few people are talking about the fact the US Assets benefit from very little risk premium attached to them. Stocks, Bonds and US Dollar.

With every control mechanism, and safeguard we abandon, the RISK to those assets will rise. Which means we will need to start applying a RISK discount to value.

I cannot see why any foreign investors will be willing to RISK placing their money with us. Those assets can be confiscated, annulled, or simply tampered with, with a single directive from the KING.

BY Doug Kass · Aug 27, 2025, 12:15 PM EDT

Here are today's things:

* I added to my index shorts — SPY $645.86 and QQQ $573.35.

* Shorted more GRNY at $23.56.

* Added to GS short at $752.63

* Added to JPM short $300.71.

BY Doug Kass · Aug 27, 2025, 12:02 PM EDT

BY Doug Kass · Aug 27, 2025, 11:25 AM EDT

Coming up at 11 AM MRKT CALL with Carter, Dan and Guy.

Run don't walk to tune in at MRKT Call - Wednesday, August 27th

Rich in content, absent hubris and full transparency... and it's free!

BY Doug Kass · Aug 27, 2025, 11:00 AM EDT

- NYSE volume 22% below its one-month average

- NASDAQ volume 13% below its one-month average

- VIX index: up 1.57% to 14.85

BY Doug Kass · Aug 27, 2025, 10:55 AM EDT

Everyone should watch Rebecca Patterson, who was on CNBC yesterday: A 'significantly politicized' Fed is growing risk, warns Wall Street Veteran Rebecca Patterson

This was part of my homebuilder thesis ...

BY Doug Kass · Aug 27, 2025, 10:30 AM EDT

BY Doug Kass · Aug 27, 2025, 10:10 AM EDT

BY Doug Kass · Aug 27, 2025, 9:55 AM EDT

BY Doug Kass · Aug 27, 2025, 9:45 AM EDT

FED SPEAKERS

8:30 a.m.: Federal Reserve Bank of New York President John Williams (Voter) on CNBC;

11:45 a.m.: FedBank of Richmond President Barkin (Non-Voter) speaks before the Greensboro Chamber of Commerce State of Our CommunityLuncheon 2025, Greensboro, NC (No livestream. Audience Q&A expected. No separate media Q&A)

TREASURY AUCTIONS

11:30: Treasury hosts a $28B 2-Year FRN Auction;

11:30: Treasury hosts a $65B 17-Week Bill Auction;

1:00 p.m.: Treasury hosts a $70B 5-Year Note Auction

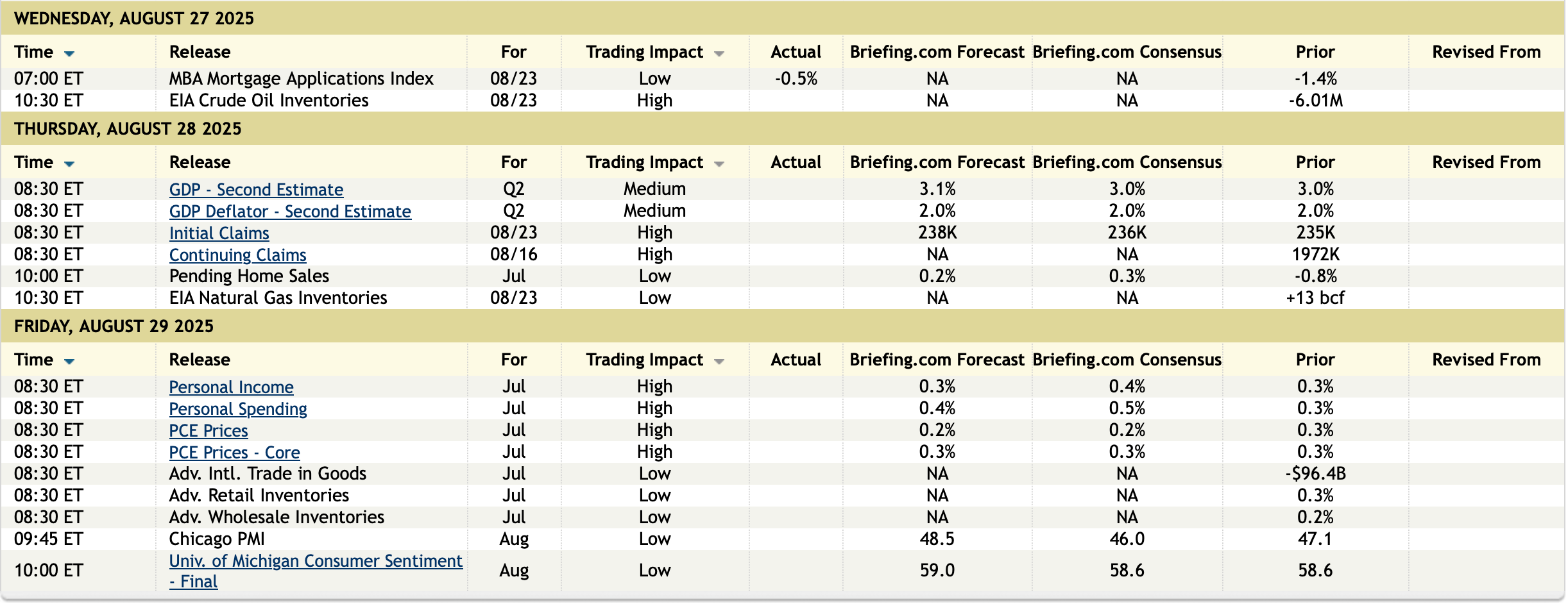

ECONOMIC CALENDAR FOR REMAINDER OF WEEK

BY Doug Kass · Aug 27, 2025, 9:30 AM EDT

BY Doug Kass · Aug 27, 2025, 9:25 AM EDT

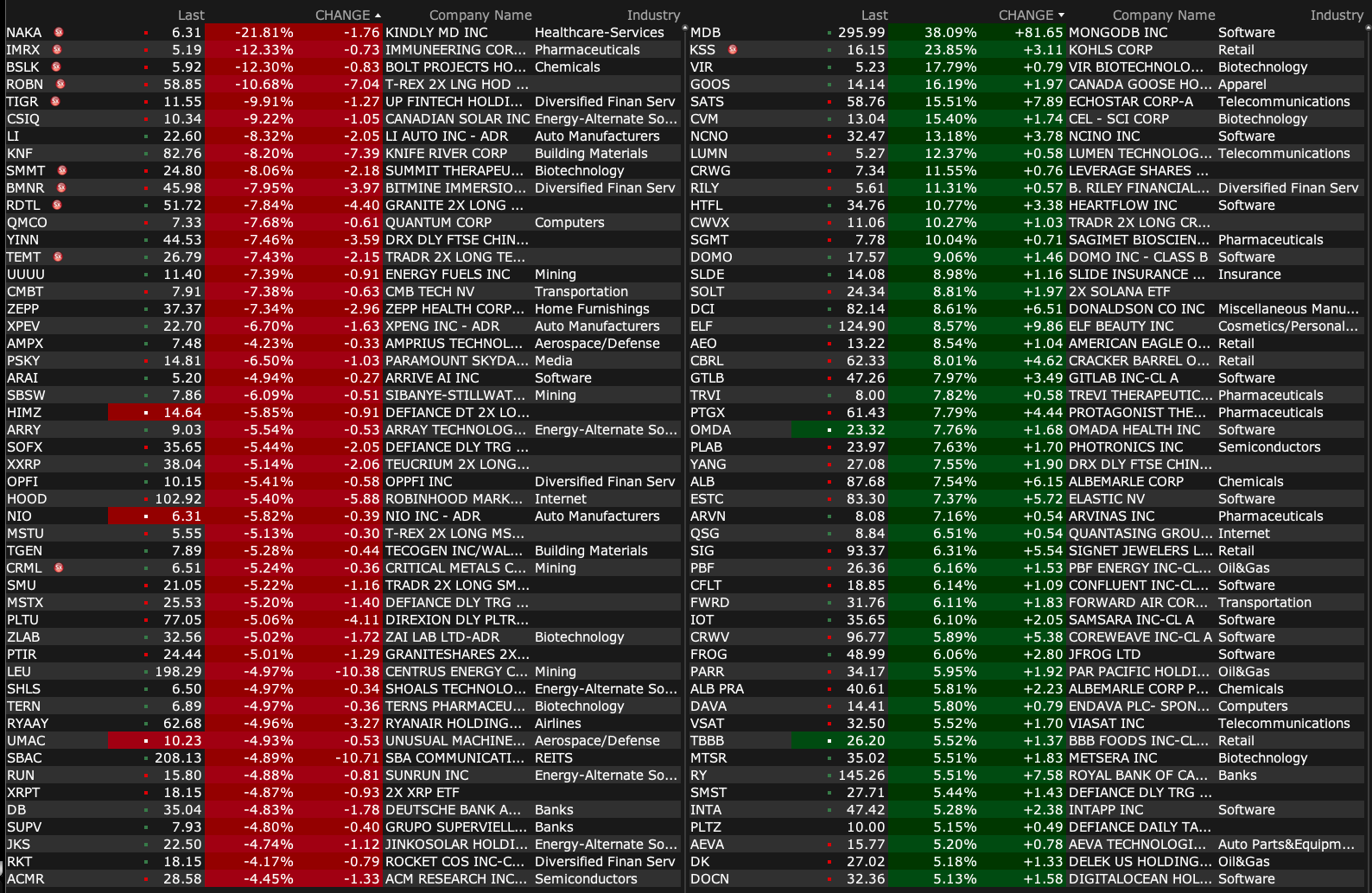

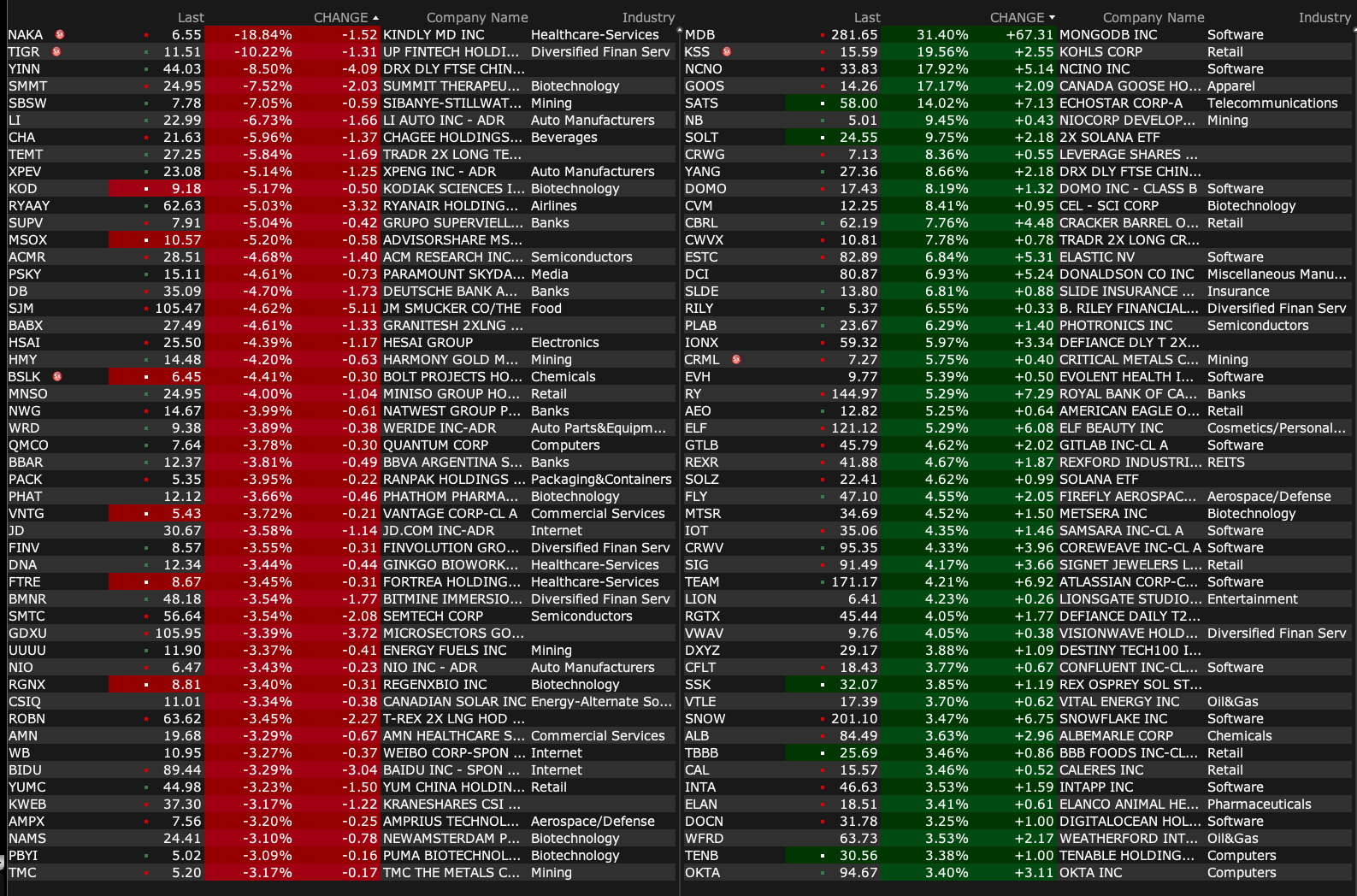

-FLNT +30% (expands data intelligence infrastructure through strategic partnership with Databricks)

-MDB +30% (earnings, guidance)

-KSS +23% (earnings, guidance)

-GOOS +16% (said to receive privatization bids valued at up to $1.35B)

-BHR +13% (entered letter agreement with external advisor Ashford, Inc. regarding potential sale of Company by the Board of Directors for $480M plus fees)

-AHL +12% (confirms to be acquired by Sompo at $37.50/shr in $3.5B cash deal)

-PLAB +8.2% (earnings, guidance)

-BOX +7.5% (earnings, guidance)

-DCI +7.0% (earnings, guidance)

-ELAN +7.0% (to replace SRPT in the S&P MidCap 400 Index)

-NCNO +7.0% (earnings, guidance)

-PVH +6.4% (earnings, guidance)

-GRCE +5.8% (U.S. FDA accepts GTx-104 NDA)

-SNOW +4.9% (higher in sympathy with MDB)

-CBRL +4.7% (decides to not update logo following complaints)

-OKTA +4.3% (earnings, guidance)

-SLDE +4.0% (announces $75M stock repurchase program)

-MNKD +3.7% (to receive $5M upfront payment as UTHR exercised option to develop a second dry powder inhalation therapy)

-QMMM -8.1% (Bear Cave makes cautious comments)

-DNUT -6.4% (JPMorgan Chase and Co Cuts DNUT to Underweight from Neutral)

-ANF -3.0% (earnings, guidance)

-SJM -2.4% (earnings, guidance)

-PYPL -2.3% (reportedly German banks blocking PayPal payments worth in the double-digit billion range)

BY Doug Kass · Aug 27, 2025, 9:15 AM EDT

BY Doug Kass · Aug 27, 2025, 9:05 AM EDT

From JPMorgan:

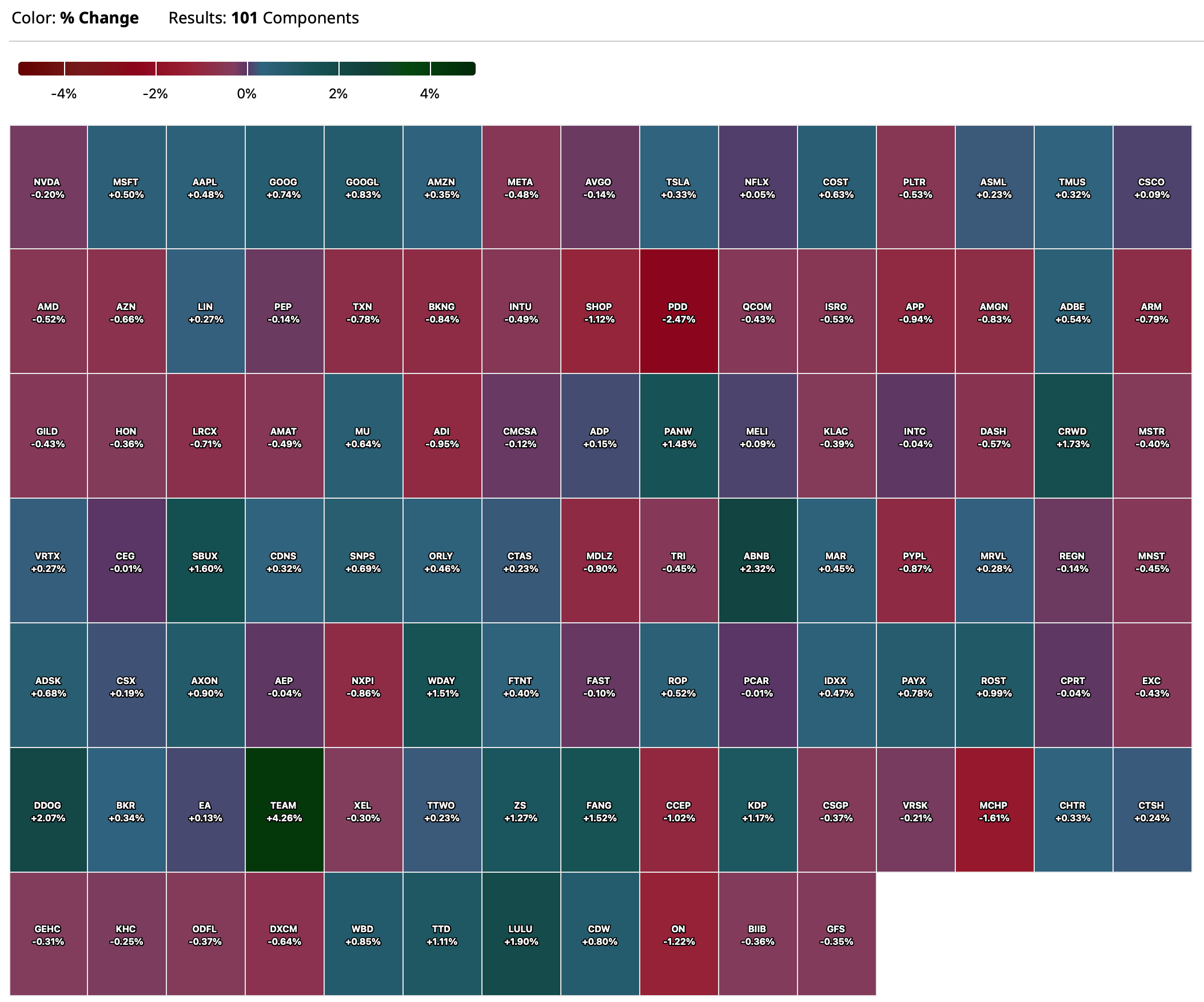

US: Futs are flat with NVDA earnings after the bell. The yield curve is twisting steeper but with a lesser magnitude to yesterday; USD is bid. Pre-mkt, NVDA is +54bp with most of the Mag7 higher and Semis bid up. Cyclicals are mixed (Indu up, Fins down) with Defensives mostly higher. The market’s focus is on NVDA today, with details on the print below. $70bn of 5Y notes will be auctioned later; yesterday’s 2Y auction saw strong demand closing 1.5bp through.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVE

Yesterday, we saw TMT / Large-caps flattish as we await NVDA earnings. Anticipation for the next phase of the easing cycle aided Cyclicals and Small-Caps, with high short interest names seeing covering. Further, the Aero/Def sector had its strongest day since July 23 on Lutnick comments of the US Gov’t potentially taking equity stakes in the sub-sector. Separately, the 2Y bond auction saw strong demand as the curve steepened in reaction to Trump firing Fed Governor Cook, which is now being legally challenged.

Regarding Cook and the standard for meeting a ‘for cause’ dismissal, Bloomberg Intelligence Senior Litigation Analyst Elliott Stein said this yesterday afternoon, “[The allegations are] likely insufficient to meet the ‘for cause’ standard for ousting a Fed governor, though on their face the claims against Cook look more damaging than the cost-overrun ones made against Fed Chair Powell.”

With NVDA, the market needs a solid print to prevent triggering a pullback. It appears that a solid print will also trigger a rotation as some downside fears are assuaged. In that scenario, look for Cyclicals and Small-Caps with USD dictating demand for Int’l / EM Equities.

DELTA-ONE FLOWS & POSITIONING: INFLOWS INTO GROWTH, CORPORATE BONDS, AND VIX ETFS; OUTFLOWS FROM GOLD AND CRYPTO ETFS – Bram’s full note is here

BY Doug Kass · Aug 27, 2025, 8:55 AM EDT

Dougie Kass

STAFF

31 minutes ago

Premarket shorting of the Indices (7:55AM):

SPY $645.86

QQQ $573.35

BY Doug Kass · Aug 27, 2025, 8:45 AM EDT

JPMorgan JPM (trading short rental) downgrades Krispy Kreme DNUT (investment short).

BY Doug Kass · Aug 27, 2025, 8:45 AM EDT

* A more aggressive move to cut interest rates by a politically motivated Fed (lacking independence) will likely backfire and produce higher (not lower) mortgage rates.

* After a spectacular rise in the last four months I am shorting homebuilders.

A 'significantly politicized' Fed is growing risk, warns Wall Street Veteran Rebecca Patterson

Homebuilders' shares have had a big run off of the April lows.

There is a lot of hot (or performance) money in this small-weighted sector based on the perception that the Trump administration (especially after the aggressive legal tact taken towards firing Fed Governor Lisa Cook and the resignation of Adriana Kugler) will easily gain control of the Federal Reserve and cajole Fed members into a path of much easier money.

The consensus belief is that interest rates will then fall and be housing sector stimulative.

As noted by Rebecca Patterson (see above) on CNBC yesterday, this consensus expectation is probably misunderstood and at a material risk.

While I agree that the Trump administration will likely gain majority control of the Fed, I am fearful that Fed rate cuts will stimulate higher yields in the intermediate and longer-term fixed-income markets — triggering higher mortgage rates in the process.

There is historical precedent for this.

Generally, mortgage rates are tied to the 10-year Treasury note, which I see as moving higher in the months ahead, exacerbated by too-aggressive Fed easing and stubbornly high inflation (which will be boosted by tariff increases going thru the pipeline):

Already the 2/10 yield curve is at the steepest since April 2025:

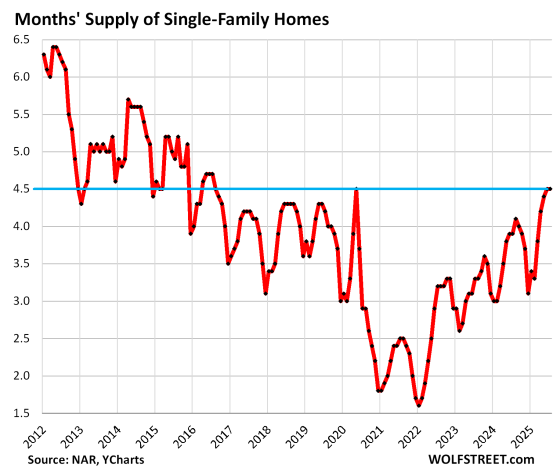

Besides the likelihood of higher, not lower mortgage rates (byproduct of Fed easing), the inventories of unsold homes are moving higher across the country as home prices begin to sputter:

* Average Age of First-Time Home Buyers and How it Changed over the Past 25 Years | Wolf Street

* Inventory of Homes for Sale Balloons in Texas and its Big Metros: Dallas-Fort Worth, Houston, Austin, San Antonio | Wolf Street et

An additional and non-trivial concern is that the recent rise in the CRB Index and building materials which could dampen profit margins.

With the administration's politically motivated gain of control of the Federal Reserve producing a central bank soon to be hell bent on lowering the Fed Funds rate — another error in monetary policy seems to lie ahead as the interest rates (10-year Treasuries) tied to mortgage rates likely rise.

Sticky inflation (causing potential homebuilder profit margin erosion) and a rising glut of unsold homes raise formidable headwinds to homebuilder profitability in the year ahead.

BY Doug Kass · Aug 27, 2025, 7:30 AM EDT

* Another tweet on vanishing volatility...

BY Doug Kass · Aug 27, 2025, 7:20 AM EDT

BY Doug Kass · Aug 27, 2025, 7:10 AM EDT

BY Doug Kass · Aug 27, 2025, 6:50 AM EDT

BY Doug Kass · Aug 27, 2025, 6:10 AM EDT

BY Doug Kass · Aug 27, 2025, 5:55 AM EDT

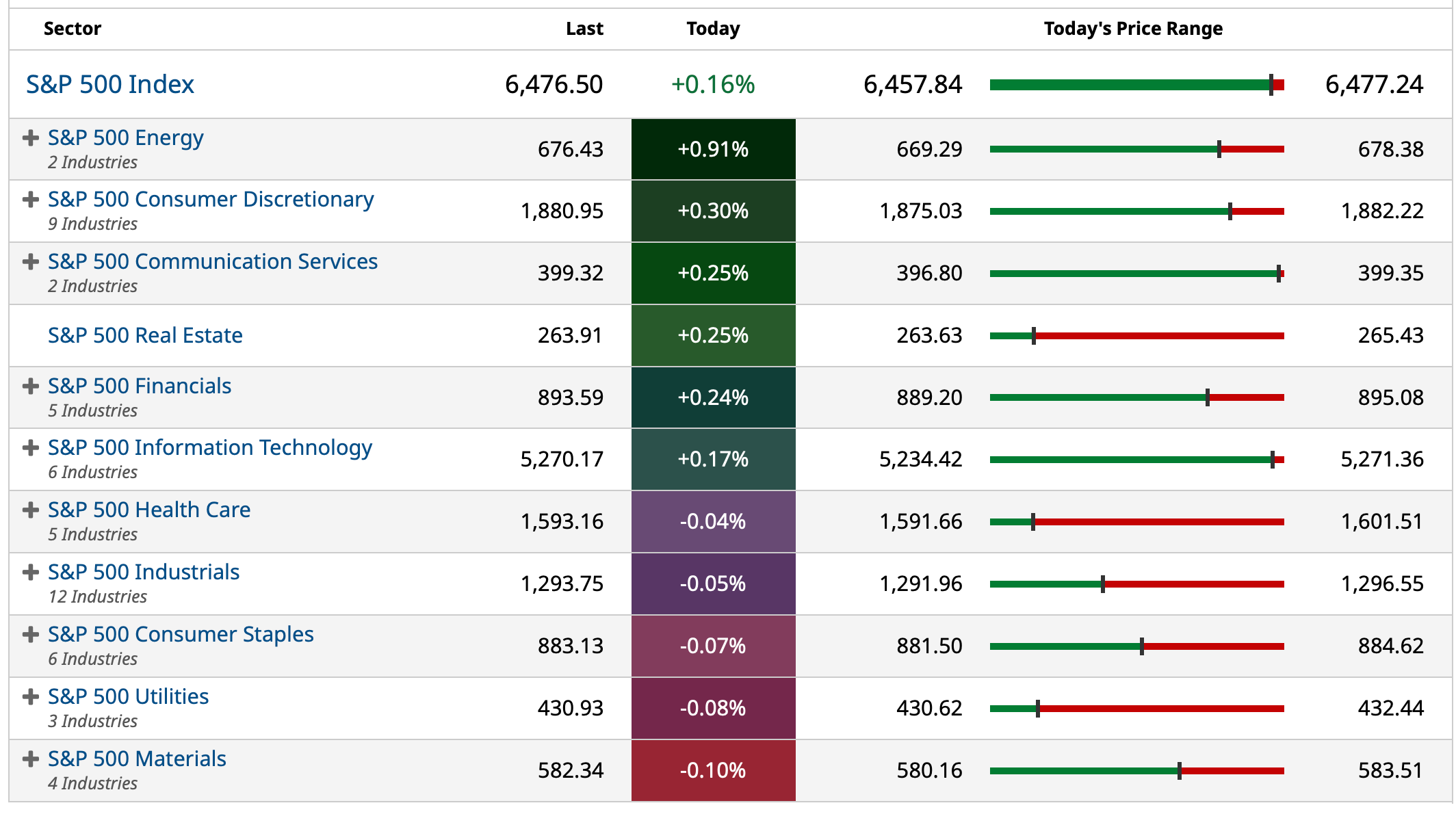

The S&P Short Range Oscillator stands at 2.02% vs. 3.30%.

BY Doug Kass · Aug 27, 2025, 5:45 AM EDT