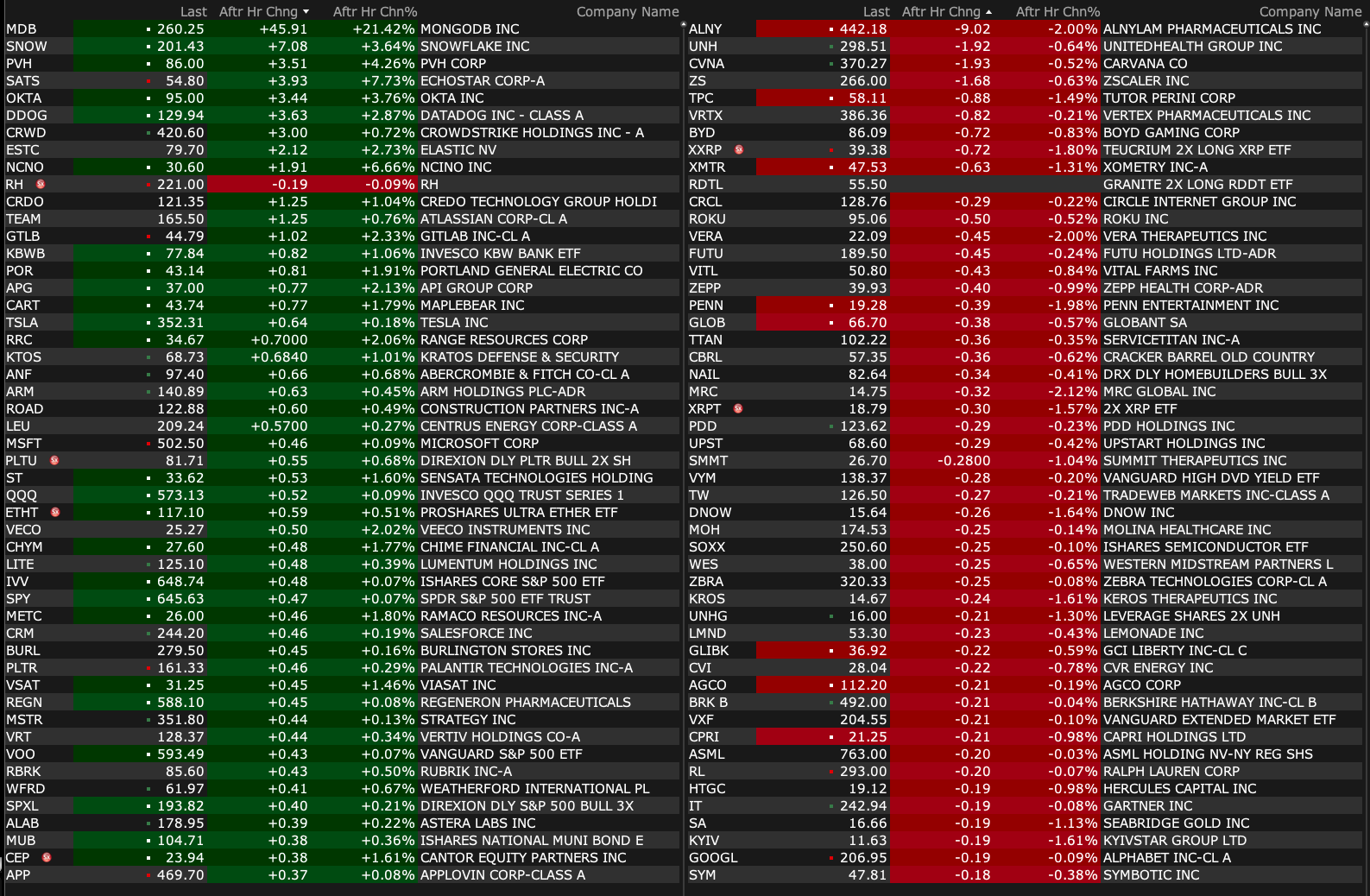

Tuesday's After-Hours Movers

As of 4:18 p.m.:

BY Doug Kass · Aug 26, 2025, 4:45 PM EDT

As of 4:18 p.m.:

BY Doug Kass · Aug 26, 2025, 4:45 PM EDT

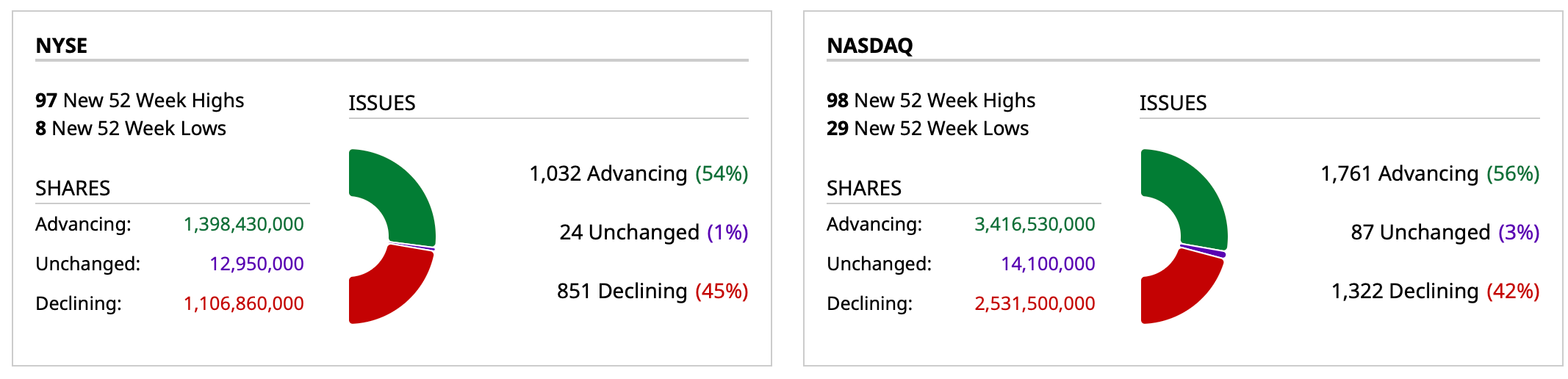

- NYSE volume 23% below its one-month average

- NASDAQ volume 2% below its one-month average

- VIX index: up 0.14% to 14.81

BY Doug Kass · Aug 26, 2025, 4:35 PM EDT

On the ramp I added to my index shorts:

* SPY $644.47

* QQQ $571.99

Still small sized but scaling into medium sized if the rally continues.

BY Doug Kass · Aug 26, 2025, 3:52 PM EDT

As posted days ago I had taken UnitedHealth UNH down to a very small sized position:

BY Doug Kass · Aug 26, 2025, 3:50 PM EDT

BY Doug Kass · Aug 26, 2025, 3:20 PM EDT

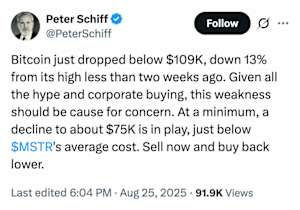

From my pal TechNova:

TechNova

POSTED THIS HERE LAST NIGHT:

BTC : The bottom may be in.

Peter Schiff calling for $75K now.

AT A MINIMUM.

That ...should.. do it.

BY Doug Kass · Aug 26, 2025, 3:00 PM EDT

Here are today's "things":

* ETF shorts:

GRNY $23.37 (add ons)

JOET $41.51 (add ons)

SPY $642.65 (new)

QQQ $570.75 (new)

* Financial shorts (all add ons):

BAC $ 49.96

BX $ 170.16

C $ 95.04

GS $ 739.86

JPM $296.49

KKR $138.90

WFC $81.09

* Homebuilder shorts (all add ons):

DHI $168.76

KBH $63.85

PHM $132.23

TOL $139.26

BY Doug Kass · Aug 26, 2025, 2:30 PM EDT

Good stuff from Rosie this morning:

Revisiting Bob Farrell’s Market Rule #7

Markets are strongest when they are broad and weakest when they narrow to a handful of blue-chip names

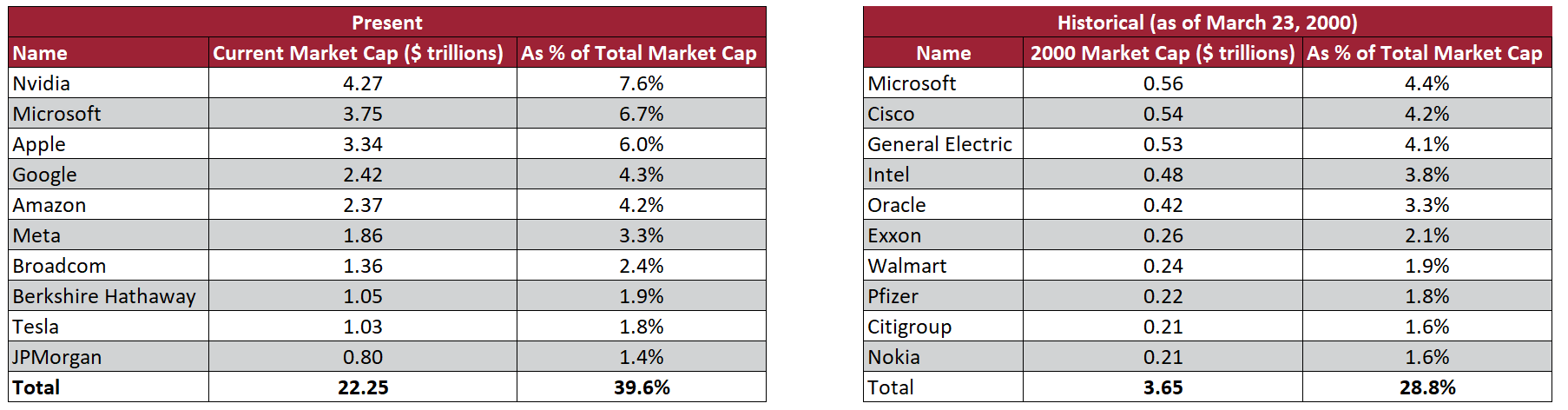

The table below says it all. At the peak of the last tech bubble back in March 2000, the largest stock in the S& 500 was Microsoft with a $560 billion valuation and 4.4% share of the total market cap. Today it is Nvidia, the world’s first $4 trillion company with a market share just below 8% which is unprecedented. The top three companies command over a 20% market share versus 12.5% back in 2000 when all we talked about was an unbalanced backdrop, The top ten today have a 40% market share versus sub-30% a quarter-century ago. The smallest top-ten company today is 43% bigger than the biggest one back at the March 2000 market peak. Eight of the top ten today are in the tech sector either directly or indirectly, compared to five back in the 2000 boom. No big box retailer, no industrial, no energy and now health care. And, as you can see, the only company still in the ranking is Microsoft and the other nine from 2000 are nowhere to be found in today’s list. Ninety percent turnover. Who was saying back then that the tech giants like of Cisco and Intel would no longer be ranking in the top ten? Nvidia had just gone public (not long after Amazon), and nobody know what it was.

So far this year, the tech sector has been responsible for 54% of the S&P 500’s total return (tip of the at to Howard Silverblatt) – this compares to a 12% contribution from leader Microsoft back in 2000! Tack on the telecom services sector which is tied at the hip (Netflix and Amazon belong -- responsible for another 15% of the market’s total return and we are talking about almost 70% of the return coming from two sectors. Nvidia alone (ahead of Wednesday’s financial results), alone has accounted for 26% of the total return. When you add on the next four gorillas -- Microsoft, Meta, Broadcom, and Palantir – you are talking about a handful of stocks representing 70% of this year’s total S&P 500 return. Never mind two sectors – we are talking about five companies! By way of comparison, the top five companies back at the 2000 market bubble peak accounted for 42% of the S&P 500 return.

While valuations are not as stretched today as was the case back then, the degree of market concentration today is far more troubling. While the market has been broadening out of late on receding recession fears and Fed rate-cutting hopes, the tech giants are simply too big go prevent either a major correction or bear market if Big Tech begins to stumble or see buyer fatigue. A lot is riding on this Wednesday after the bell. The best hedge if you don’t want to start taking chips off the table and raising cash would be to go long the S&P 500 equal-weight index while shorting the cap-weight index. That is a trade I like (as does Doug Kass).

THEN AND NOW – A COMPARISON OF THE TOP TEN STOCKS TODAY VERSUS THE MARCH 2000 BUBBLE PEAK

In late July I approached this from a slightly different viewpoint:

There is a consensus view that many of the Mag 7 companies will be immune to an economic or market downturn.

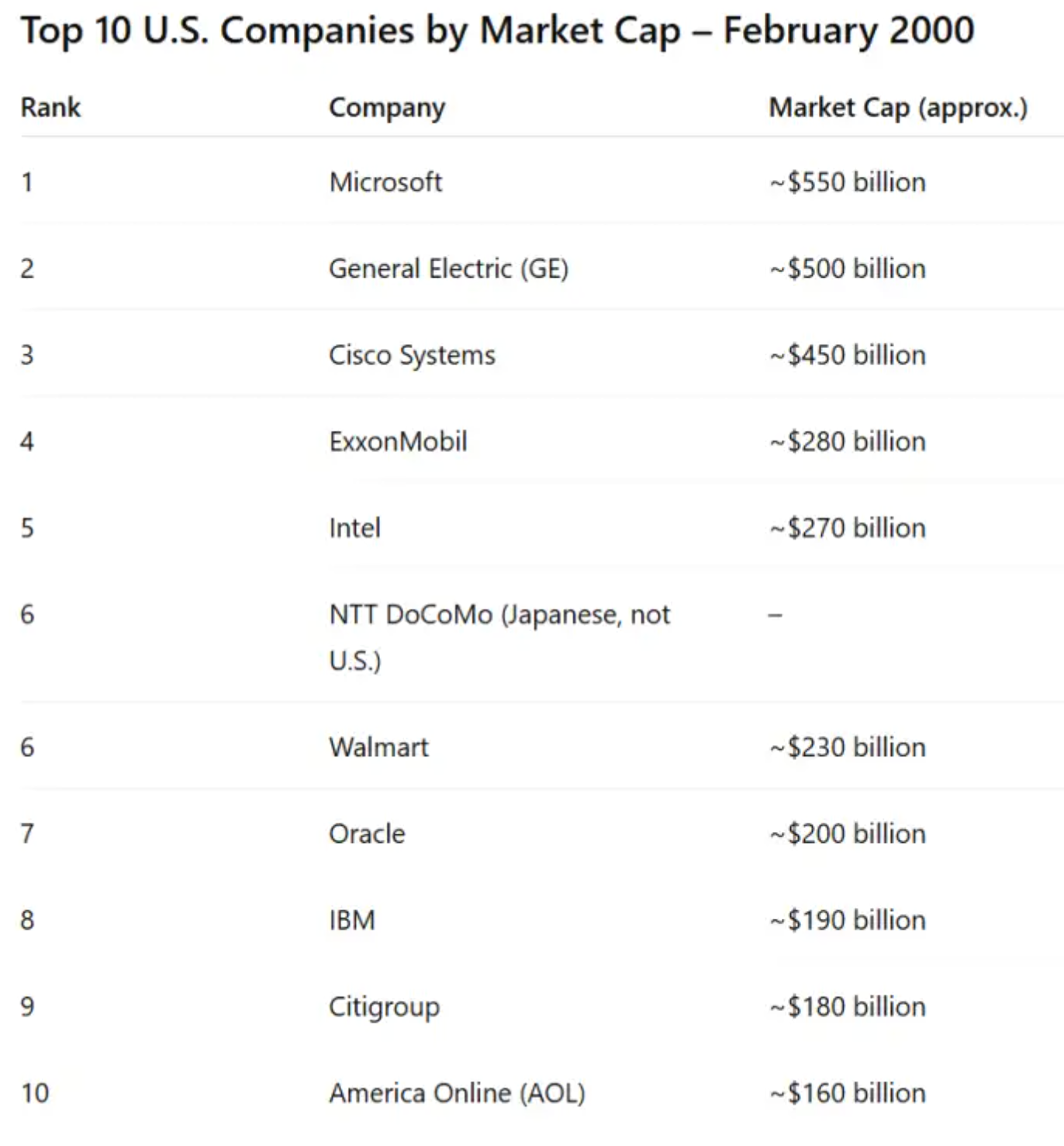

Let me remind everyone that the 10 biggest companies just before the 2000 crash were ALL "real" companies — so even in that regard there's nothing all that different from today:

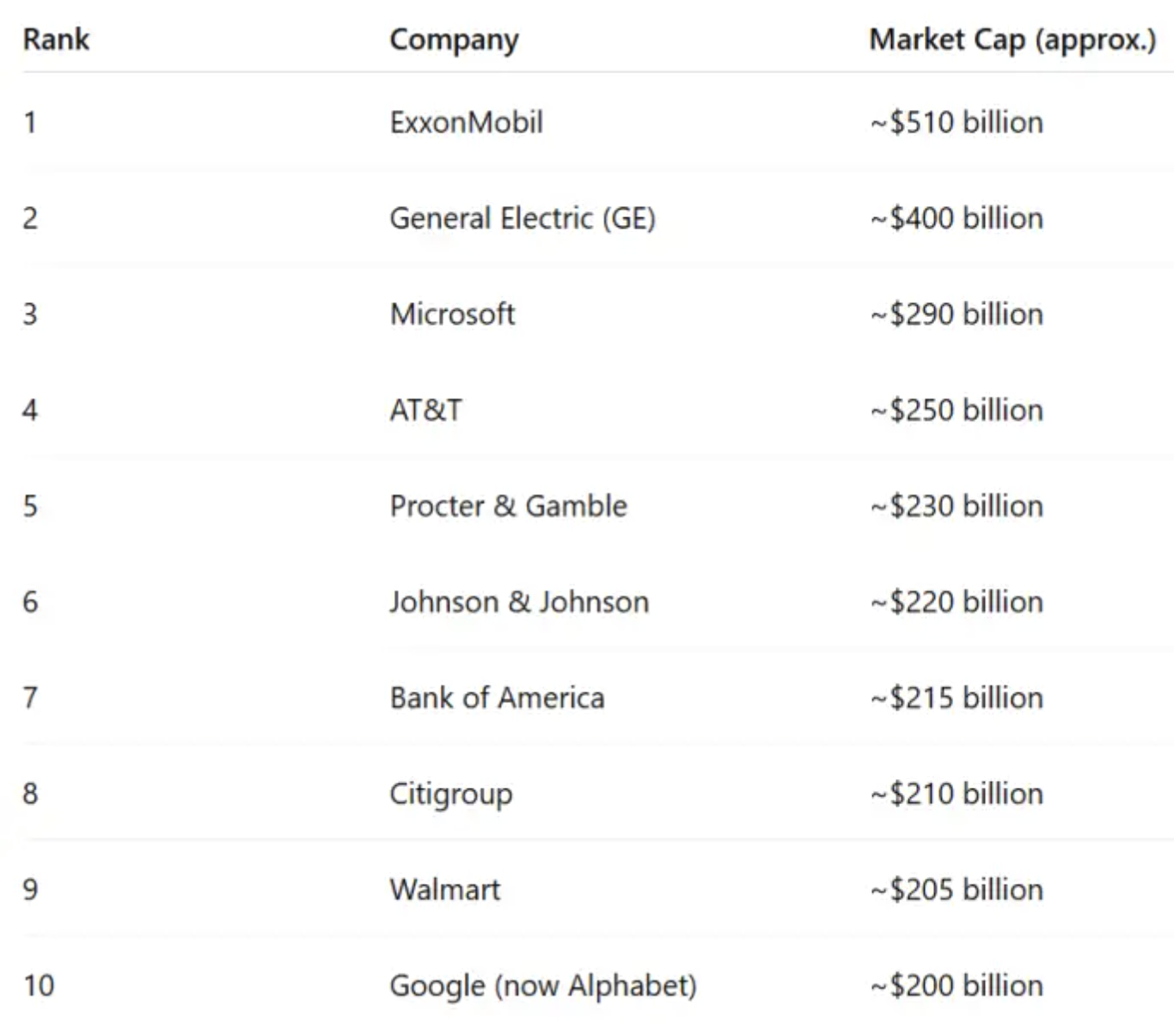

And the same held for September 2007:

BY Doug Kass · Aug 26, 2025, 12:45 PM EDT

BY Doug Kass · Aug 26, 2025, 11:35 AM EDT

From Peter Boockvar:

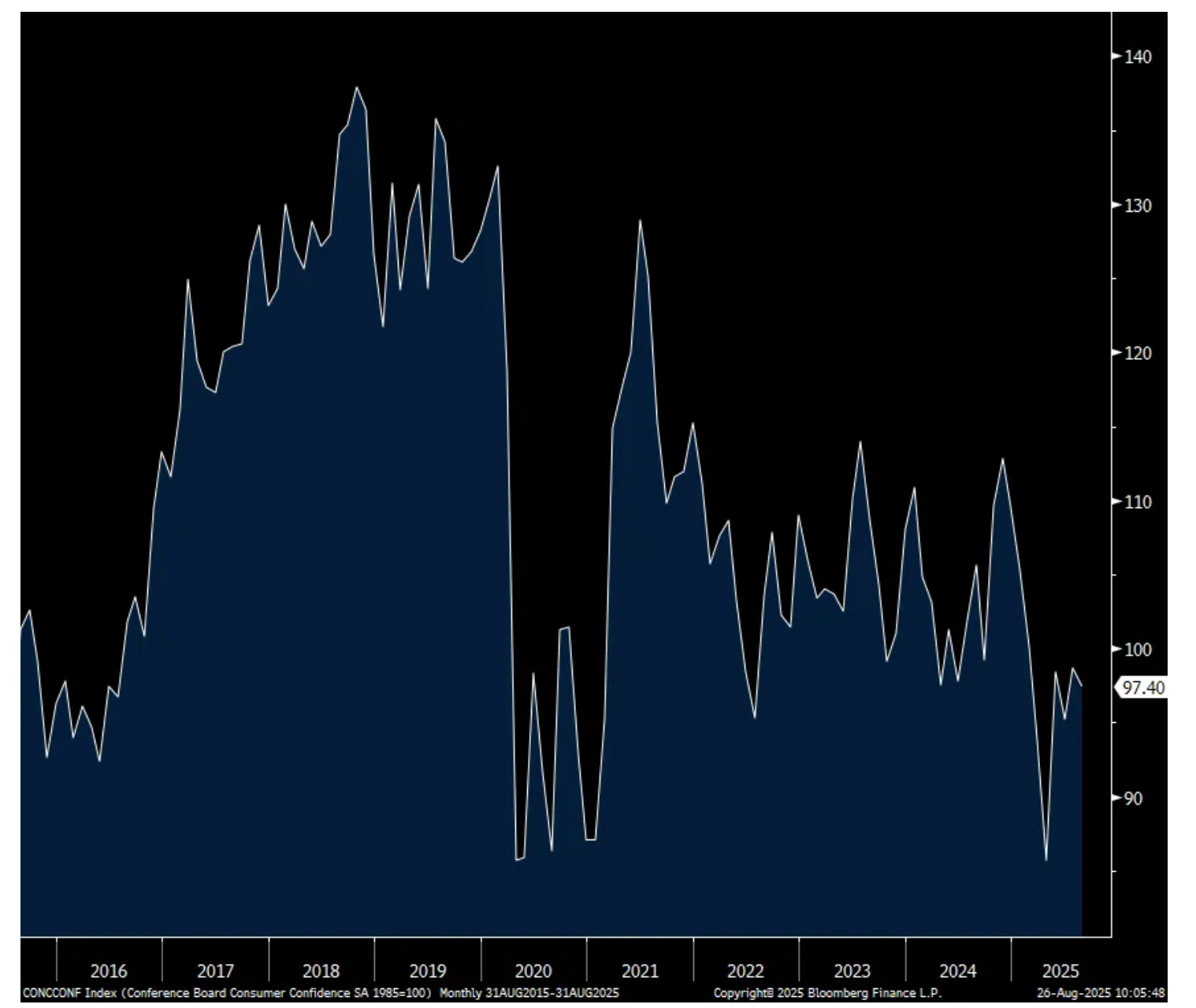

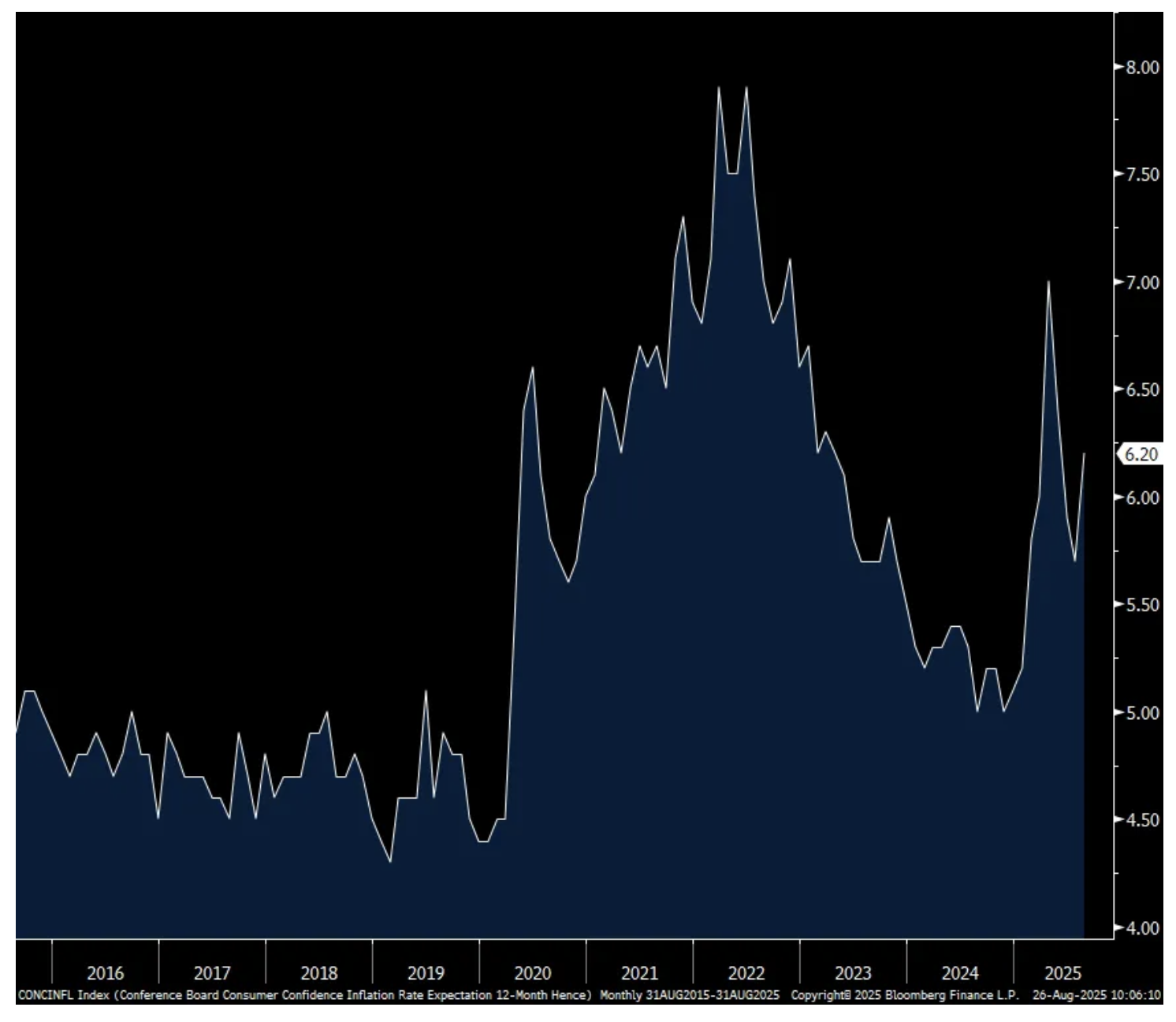

The August consumer confidence index from the Conference Board fell to 97.4 from a revised 98.7 in July (from 97.2 initially) but that was just above the estimate of 96.5. For perspective, this figure has averaged 96.8 year to date. The Present Situation was down slightly while the Expectations component was up a bit. One year inflation expectations did lift to 6.2% from 5.7% in July and 5.9% in June.

On the rise in inflation expectations, the Conference Board said “Consumers’ write-in responses showed that references to tariffs increased somewhat and continued to be associated with concerns about higher prices. Meanwhile, references to high prices and inflation, including food and groceries, rose again in August.”

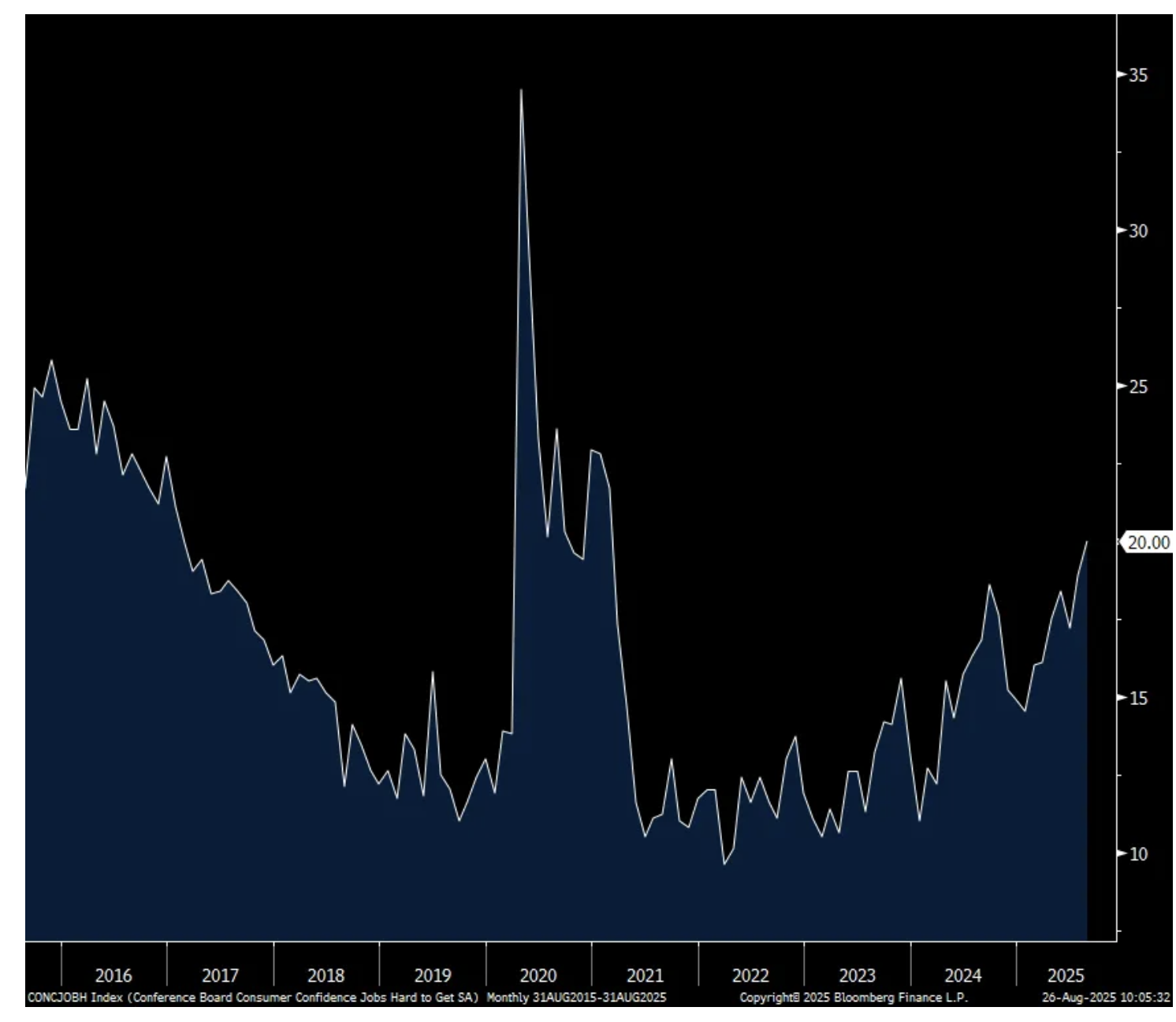

The answers to the Current labor market questions did weaken again with those saying jobs were Plentiful slipping to just off the least since March 2021. Those that see jobs as Hard to Get rose 1.1 pts to 20, the highest since February 2021. As for 6 month Expectations of the labor market, after rising in July, those that see ‘more jobs’ fell by .1 pt m/o/m while those that see ‘fewer jobs’ rose to a 4 month high. Income expectations fell .4 pts after rising by 1.1 pts last month.

Spending intentions were mixed. After falling in July by 1.2 pts, plans to buy a vehicle rose by .7 pts. Plans to buy a home held at a 4 month low. For major appliances, spending plans were uneven.

Demographically, confidence was mixed too. For those 55 and older, confidence rose to the highest since February but fell to a 4 month low for those under the age of 35. In between, confidence was little changed m/o/m.

I’ll finish with this, at 97.4, confidence remains well below the February 2020 level of 132.6 because the big lift in the cost of living over the past 5 years has stressed consumers. Wages have done a good job of keeping up but if there is no REAL inflation adjusted progress, people feel left behind, especially for younger people where necessities make up a bigger portion of their spend relative to income.

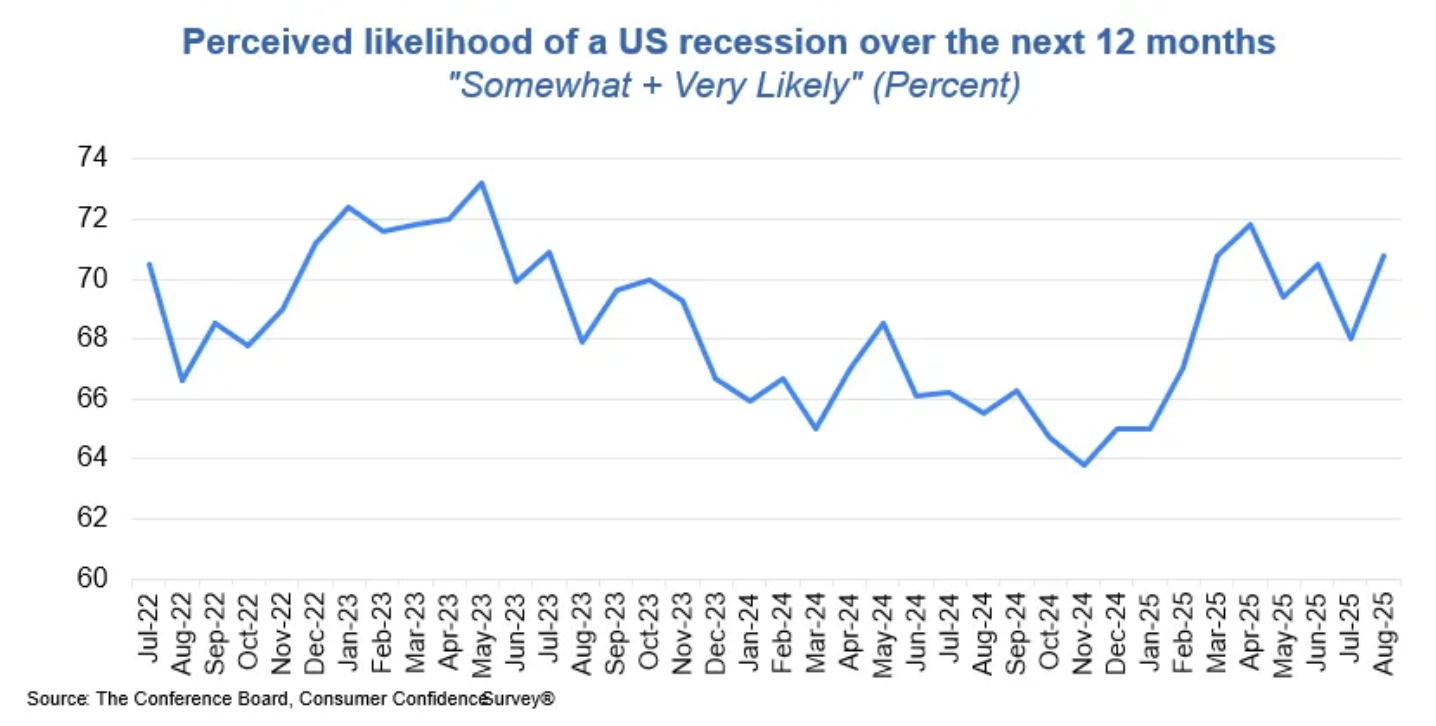

Lastly, below is a chart from the Conference Board on consumer expectations for a recession in the coming year.

Consumer Confidence

One yr Inflation Expectations

Jobs Plentiful

Jobs Hard to Get

The August Richmond manufacturing index came in at -7 vs -20 in July and it’s the 3rd regional survey of 4 reported so far that has been below zero, though not by much with Philly and Dallas.

The Richmond Fed referred to activity as remaining “soft.” While the Philly index saw a big jump in CapEx plans, the Richmond survey reflected the exact opposite with deeply negative figures for CapEx, Equip & Software and Services Expenditures.

Of note on costs, prices paid jumped to 7.2 from 5.7 and that is the highest since February 2023.

Bottom line, US manufacturing is searching for a bottom and I do believe one is here, with some evidence from S&P Global with its PMI. The question though is when does the improvement come and the first sign will be with some inventory building when companies have more clarity on tariffs and end demand.

BY Doug Kass · Aug 26, 2025, 11:00 AM EDT

From Peter Boockvar:

I don’t want to downplay mortgage fraud and the evidence presented seems clear on the surface but we have to be honest that Lisa Cook was likely targeted (I'm sure among others) and then disposed of without due process (even though we don't yet know how this will go from here in terms of cause proven while she was in her Fed seat and whether she ultimately leaves or not) in order to remake the Fed with people who will be most inclined to cut interest rates. I will let the value of the US dollar, gold and 10 and 30 yr Treasuries from here do most of the talking in coming weeks/months/quarters/years on what they think of all of this but I don't think any of us should feel good about what is going on with the attempt to remake the Fed for the sole purpose of having lower interest rates than they would be otherwise.

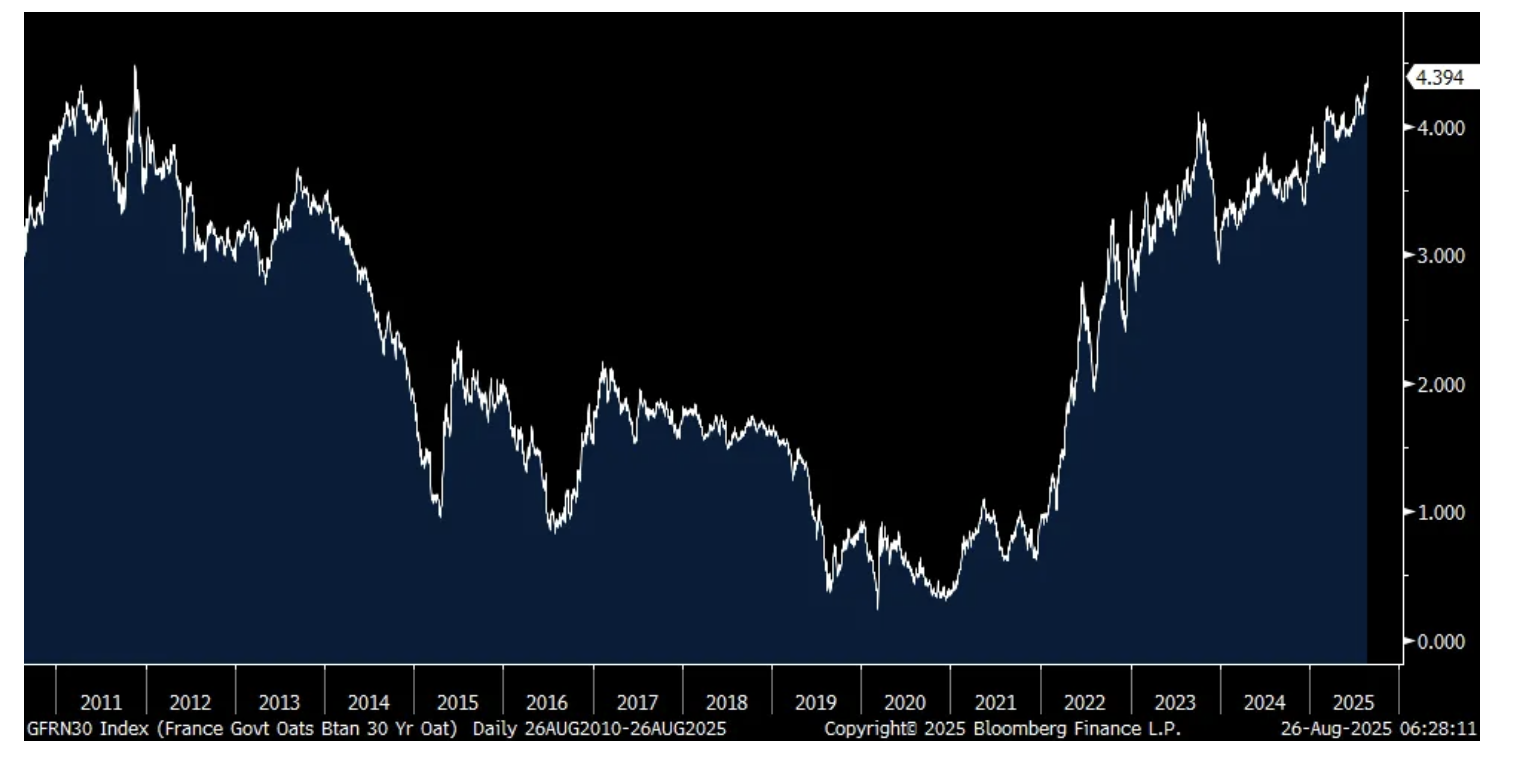

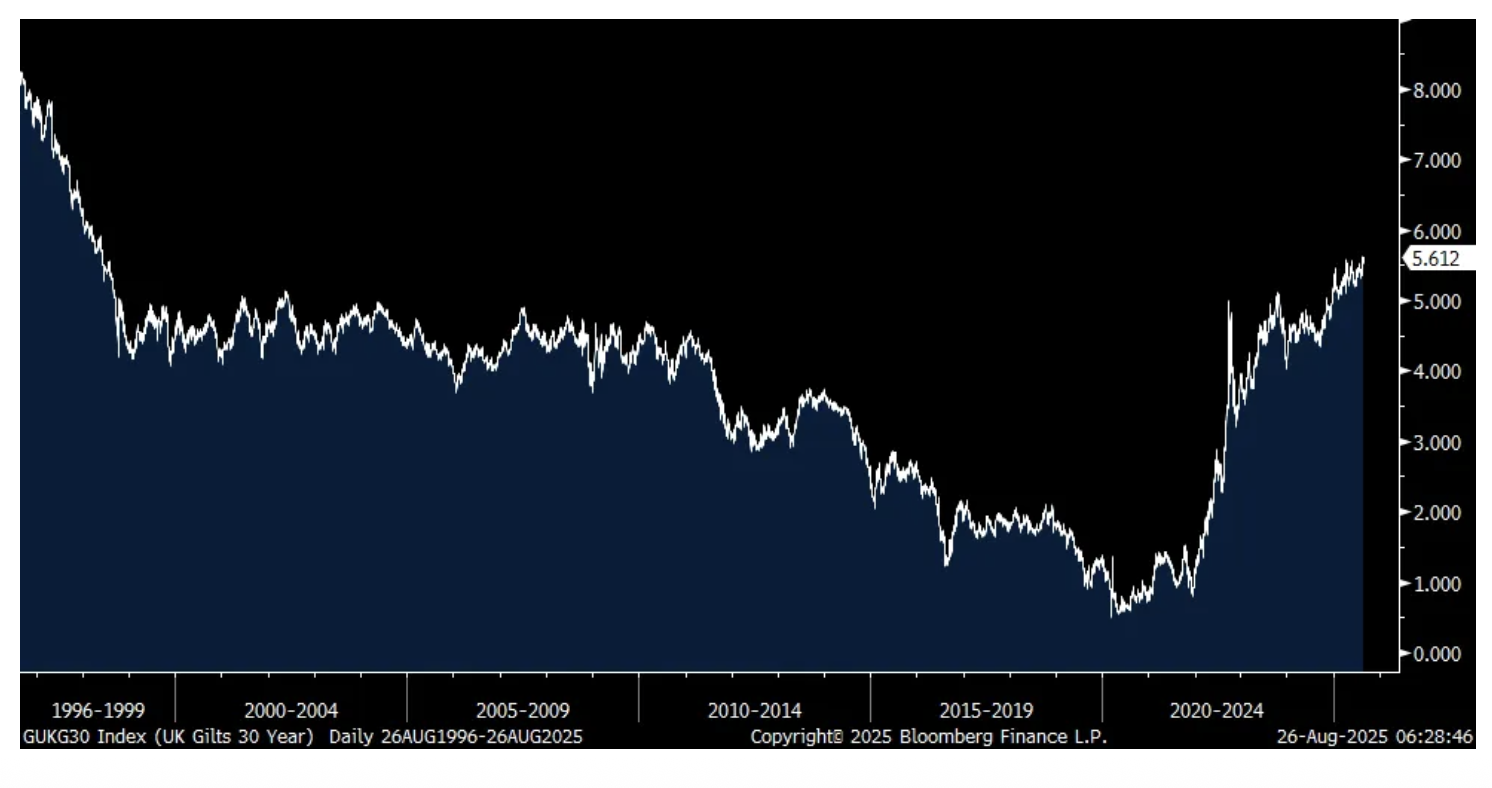

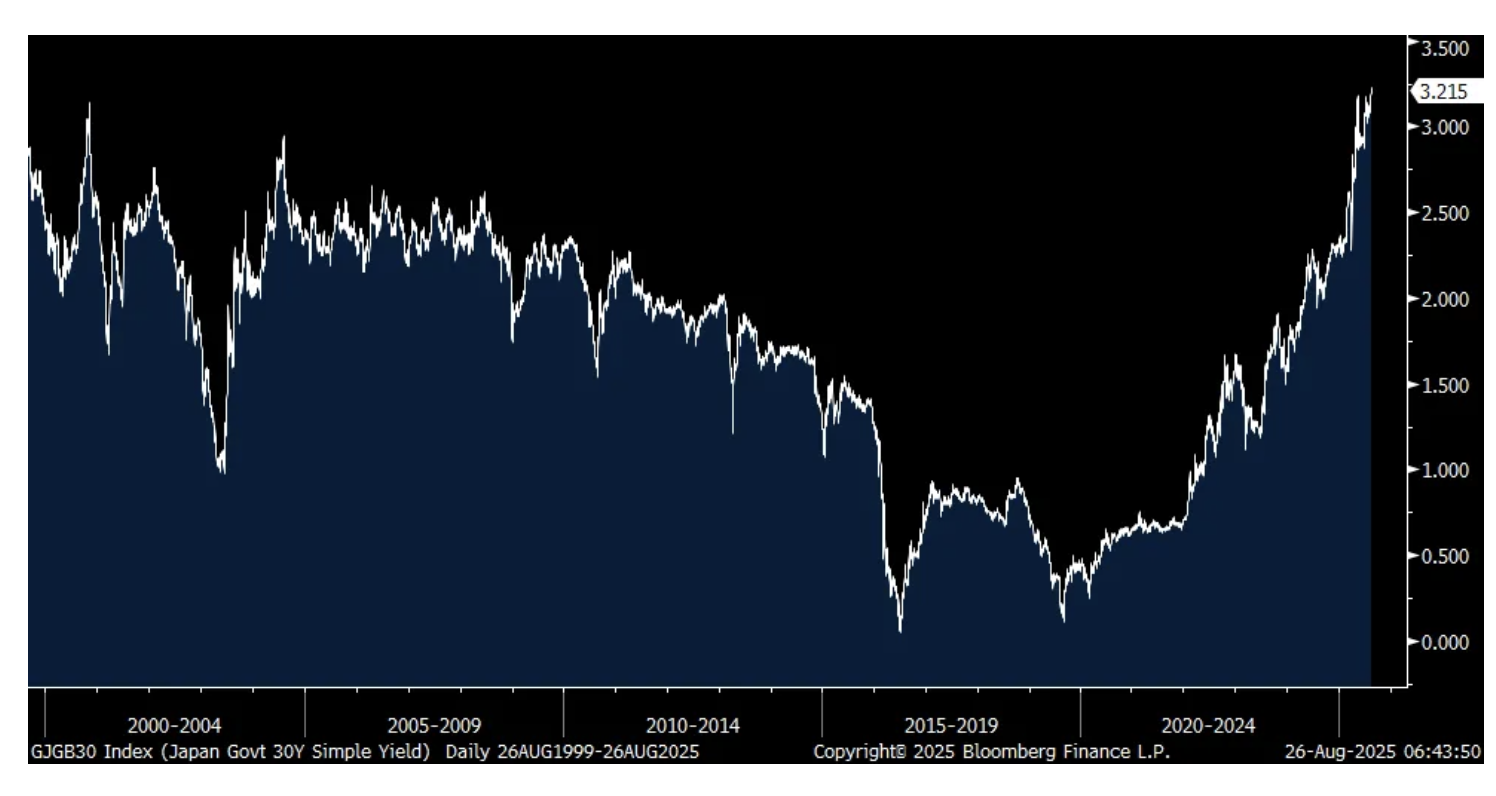

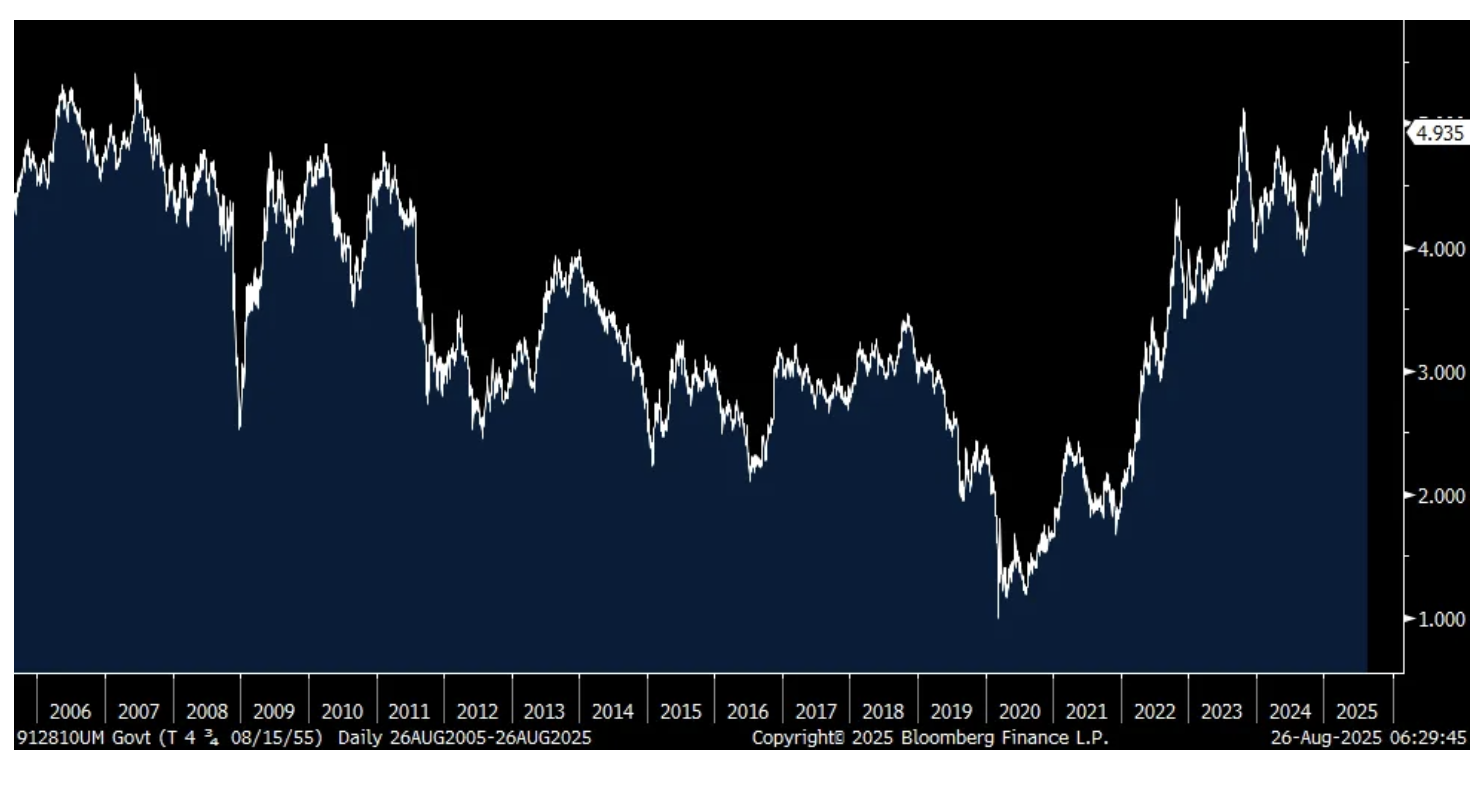

Rising long term rates is now mattering in France as Prime Minister Michel Bayrou has called for a confidence vote that could end his minority government coalition and the French CAC is trading down by 1.5% after a 1.6% decline yesterday. He did so in order to push back against the political opposition to the proposed spending cuts and tax increases that have been laid out to trim France's debts and deficits and whose high levels is what the bond market is most worried about. The French 30 yr yield is flattish today but sitting at a 14 yr high. In sympathy, the UK 30 yr yield is at a 17 yr high, the 30 yr JGB yield closed flat but at its 26 yr high and the US 30 yr Treasury yield is at a one month high at 4.93-.94% and is just 18 bps from an 18 yr high.

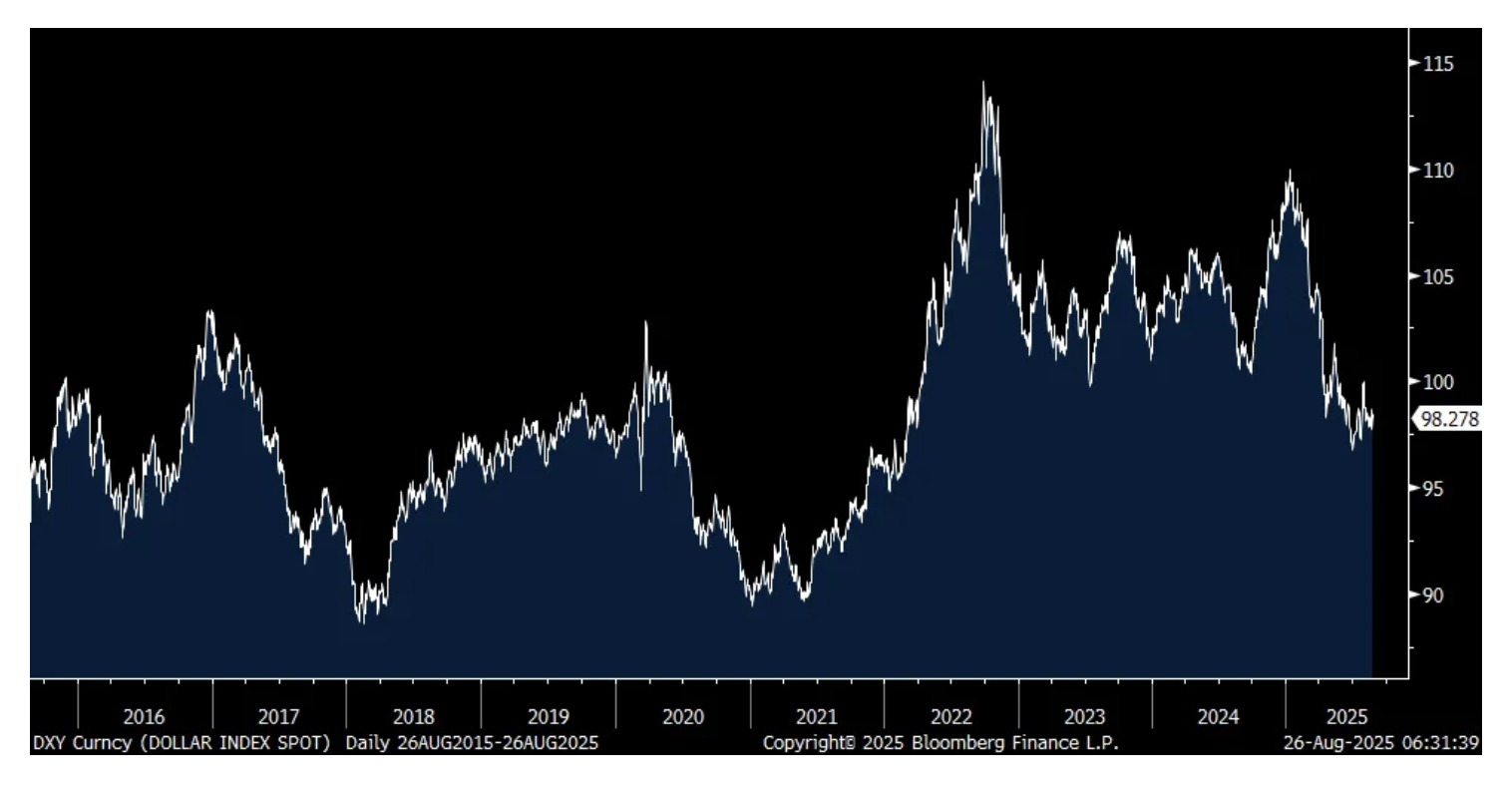

I'll say again, don't ignore what is going on with longer term global bond yields. The euro heavy dollar index by the way is down a touch and still hovering just above the weakest level since early 2022.

French 30 yr Oat Yield

30 yr UK Gilt Yield

30 yr JGB Yield

US 30 yr Yield

DXY

French consumer confidence for August also came out and it fell 1 pt m/o/m to 87, two points below expectations and is at the lowest level since October 2023.

French Consumer Confidence

BY Doug Kass · Aug 26, 2025, 10:25 AM EDT

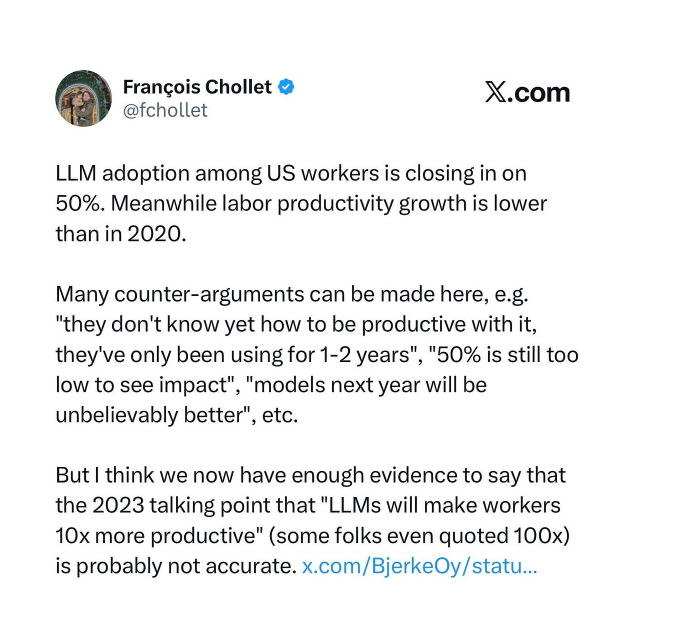

Interesting article below - AI, layoffs, productivity and The Klarna Effect

So far, AI has only been inflationary, and labor productivity growth is slower than in 2020!

After the hundreds of billions already spent on AI, the Consumer Price Index is now running hot (above target) and accelerating, and the Producer Price Index is even worse than the CPI. The services component of our inflation metrics was especially problematic, which is what AI should most directly affect, although in theory it should affect everything based on what we are told (and develop a cure for cancer and 10% GDP growth with no unemployment and no inflation).

Productivity growth seems to have flattened recently (certainly not accelerated), and there is still job and wage growth: fred.stlouisfed.org/series/OPHNFB/

At the same time, electricity prices are spiking fred.stlouisfed.org/series/CUSR0000SEHF01, and stock prices have ripped again, mainly centered around the AI theme. Increasing equity prices equate to loosening financial conditions, which are inflationary.

Therefore, believe it or not, so far, AI has been inflationary.

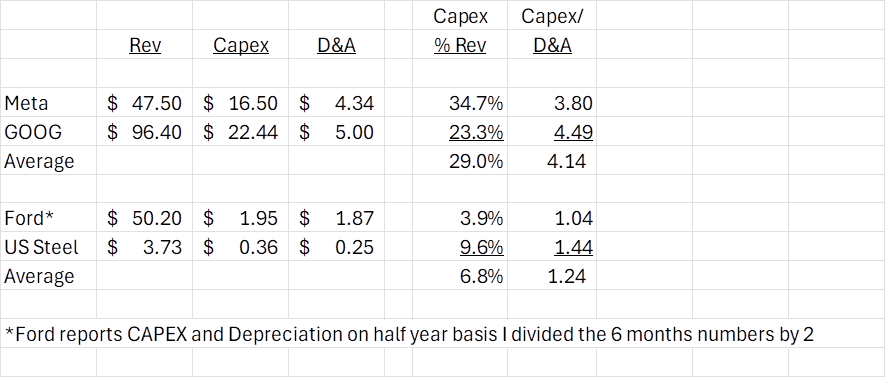

To be clear, none of this is to say NVDA will not have a good quarter and outlook, they will. Clearly, the spending is there, and has re-accelerated over the short term. It was decelerating, but as I explained in my “so bad it is good rant, spending has picked right back up due to the U.S. government's involvement and hype, the reflexive nature of this whole thing with the retail-led rebound in equity prices, and most importantly nothing worked or scaled, so as opposed to pausing and re-evaluating, everyone seems to have doubled down on what is not working (ergo so bad it is good) and is spending even more money on more of what is not working. The fail of GPT-5 is quite ominous in this regard, but over the short term nobody seems to care because people know NVDA is going to show good numbers and have a positive outlook, which is currently being supported by the inflationary CAPEX plans of the hyperscalers. But ultimately, in two or three quarters that trajectory will flatten again, and the rubber is going to finally have to hit the road at some point. CAPEX as % of sales is about as high as it can be, and many many many multiples as a % of sales (~about 4x) of what capital intensive industries like Steel and Auto Manufacturers spend. We have already gone to 11: youtube.com/watch?v=4xgx4k83zzc

I recommend reading Gary Marcus' AI, layoffs, productivity and The Klarna Effect, which I will except here below:

Promises about AI replacing employees often don’t work out — and may not be such a hot idea.

Employers of late are often looking to cut employees. They often use vague talk of AI to license their layoffs, and they often don’t know what the hell they are talking about, at least when it comes to AI.

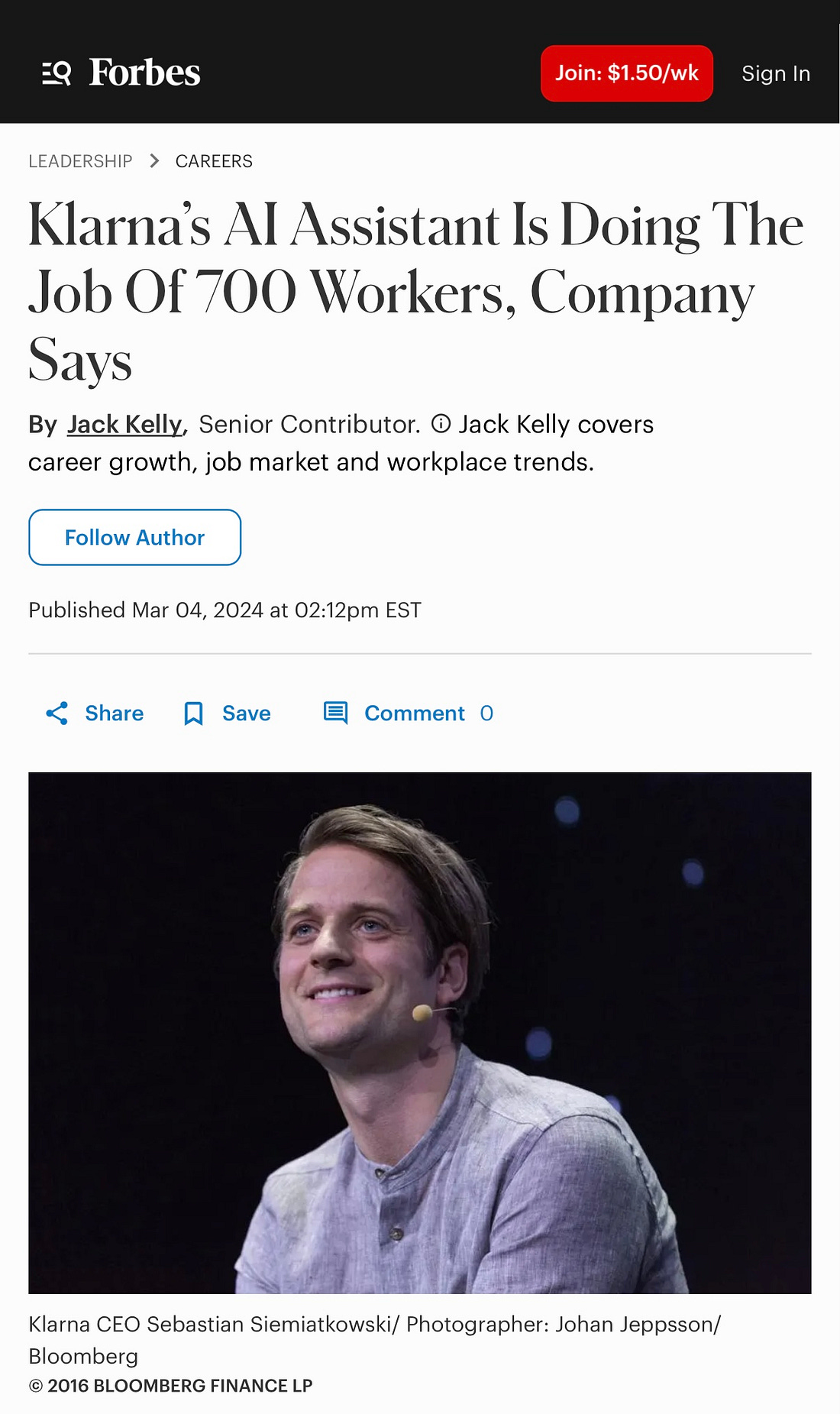

Klarna, in particular, was way ahead of the curve on this one, bragging about AI layoffs long before it was trendy. They were among the first to announce major AI layoffs, hyping them proudly for quite some time, and among the first to realize they had screwed up.

Here they are, crowing about supposed AI efficiencies, thought by some to preening before the market before a possible IPO, in 2024:

And here they are again, walking it all back in February 2025.

They are hardly alone; a person on X for example once told me similar things are happening in China:

I was so amused by Klarna’s turnabout that I decided to dub the whole arc—from premature declaration of AI’s ubiquitous power to the 180 proudly announcing human rehirings—

...

Post Script:

Yeah, not off to a good start on the productivity front. Silicon Valley, powerful as it is, should be wary of ticking off 67 million Americans ... New Jersey residents, whose 13.3% bill increase was the third-highest in the U.S., can perhaps draw some comfort from New York faring worse, where bills surged 14.4%.... After many years of flat electricity demand, PJM now forecasts an imminent jump, and it takes time — as well as spiking price signals — for energy supply to react. The culprit is the AI boom, with PJM serving Virginia’s burgeoning data center alley. Some 64% of those ballooning capacity payments that began hitting bills in June relate to actual and projected datacenter demand, according to Monitoring Analytics’ calculations (also see: this from Bloomberg.)

Add into this, all the operating losses generated by the system (service and infrastructure providers). Eventually they will have to price at a point where it is economic. Therefore, that is a big offset to whatever benefit they offer. Said differently, it is challenging for something that is very very very expensive to begin with (even with the expenses hidden) to be a substantial net offset to inflationary pressure. So far, if anything, it has only been inflationary, per my prior below. Even Jerome Powell at Jackson Hole cited a slowing in productivity growth as something that puts more pressure on inflation. Bottom line, so far, AI has not increased productivity and only put more pressure on the inflationary side of the ledger, not less. We cannot say for certain where rates will settle out over the longer run, but their neutral level may now be higher than during the 2010s, reflecting changes in productivity, demographics, fiscal policy, and other factors that affect the balance between saving and investment.

BY Doug Kass · Aug 26, 2025, 9:55 AM EDT

Shorting more GRNY - my vote against momentum stocks.

Shorting more JOET - my vote against financial stocks (seem to be rolling over today after great gains).

Shorting more financials stocks (see above) and homebuilders (long JOE).

BY Doug Kass · Aug 26, 2025, 9:45 AM EDT

From JPMorgan:

US: Futs are flattish as the yield curve twists steeper with 5Y yield flat, as Trump moves to fire the Fed’s Cook; USD is weaker. Cook says that POTUS has no authority to oust her and that she will not quit; SCOTUS indicated that the Fed Governors could not be fired at-will. Pre-mkt, parts of Mag7 and Semis are higher with Defensive sectors outperforming Cyclicals; large-cap Industrials are in the green. Cmdtys are weaker, dragged by Energy.

and...

JPM MARKET INTEL EQUITY & MACRO NARRATIVEIn the US, the top overnight news is Trump’s move to fire Cook which appears destined to be a long-term legal process, but it is unclear whether “firing for cause” means allegations, despite no indictment, or whether it means a criminal conviction or loss of a civil case. Further, is Cook allowed to stay while the legal process plays out? It seems more likely there the answer is Yes given the Supreme Court’s rulings earlier this year. Also, Pulte also accused Democratic Senator Schiff of similar malfeasance (The Hill; Politico). For now, US markets are not seeing a dramatic reaction, which may be aided by the sell-off seen in EMEA and with the potential for NVDA’s earnings tomorrow to re-ignite the AI theme amid a broader US rally. TRADING DESK COMMENTARY· ILAN BEHAMOU (Equity Derivatives) – Is this the beginning of a “cutting wave” after mission accomplished (inflation on track and full employment amid weakening labor) or just an “insurance cut” to blink at the loosening labor market but also deflect the mounting political pressure coming from all sides? My view is more the latter. Aside from loose market conditions (everything more or less at ATH), I think the Fed cannot afford to be too complacent on inflation this “early” tariff-wise. And without going into the whole BLS debacle, while the latest NFP batch was weak (and revisions even worse), job market slack is not due to a drop in labor supply.o Now, is the “cut” really that important? Well, from a narrative perspective, it’s obviously better to have one than not, but that’s not really the crux of it all. This market was thriving even as the Fed was on its hiking spree, so whether the Fed stops at 25bp or continues will add a bit of vol but won’t change things terribly. Plus, don’t forget that in this AI cycle, investments are made by uber-cash-rich companies that won’t necessarily benefit from 25bp lower in front-end rates. I would actually argue that the current rate policy narrative only exacerbates the Tech to Value rotation as economy-sensitive companies would benefit the most from this situation (it’s not back for QQQ, it’s just better for IWM). What really matters, though, is if the recent Tech wobble has legs. So why was Tech so weak as of late? There again, there isn’t just one reason (this ain’t DeepSeek) but rather a myriad of different perturbations adding up. A couple of bad earnings reactions despite strong results (CRWV, AMAT, CSCO), China’s warning not to use NVDA H20 Chips (some speculating a DeepSeek moment for made-in-China chips is brewing), the underwhelming reviews of the last Chat GPT-5 update (is the LLM hype fatigued?).o We all know that the AI revolution is inevitable but won’t be done in a straight line, so at this moment, it all comes down to will the AI train slow down or continue chugging a while longer? No one can time this perfectly, of course. It took a while between the cable-infra frenzy of CSCO in the 90s before the advent of the internet as we know it in the mid-2000s. Time will tell, but I tend to think that each revolution happens faster than the last and in Tech, at an exponential rate. For what we care, i.e., NVDA earnings on Wednesday night, I think that despite stunning numbers, the risk is that we see the same type of reaction as we’ve seen - albeit with higher beta - with other AI darlings : disappointment. Interestingly enough, from a technical standpoint, you have both short interest near all-time low while momentum long appears still max long.o Going forward (after this week) , a good NVDA outcome would help immediately mend the Tech turbulence otherwise I think that the playbook will be the rebuild of the AI trend for the last quarter. Despite the latest attempt to see the laggards (Value/Cyclicals) try to outperform amid the nearly-confirmed cut , I believe this market’s locomotive won’t be too different than the one that took us where we are. Vol is cheap and year-end upside calls appealing , that’s where I focus my attention for now.

BY Doug Kass · Aug 26, 2025, 9:40 AM EDT

I remain short MSTR, which is (obviously) my proxy for a bitcoin short.

BY Doug Kass · Aug 26, 2025, 9:27 AM EDT

BY Doug Kass · Aug 26, 2025, 9:25 AM EDT

-IVVD +130% (momentum)

-ALLR +83% (announces Granted FDA Fast Track Designation for Stenoparib for the Treatment of Advanced Ovarian Cancer)

-SATS +69% (AT&T to acquire 50Mhz low-mid band spectrum licenses from EchoStar for $23B)

-SER +26% (receives FDA Support for SER-252 Registrational Trial Design in Advanced Parkinson's Disease under 505(b)(2) NDA Pathway)

-PACK +24% (expands existing relationship with Walmart to deploy Autofill systems)

-OPAD +19% (momentum)

-TLRY +12% (recent talk of cannabis reclassification, Jefferies bullish commentary)

-AEHR +8.8% (awarded purchase order from undisclosed supplier of artificial intelligence (AI) processors for a wafer level burn-in (WLBI) application evaluation and correlation program)

-CTRN +8.4% (earnings, guidance)

-DOMO +6.9% (TD Cowen Raised DOMO to Buy from Hold, price target: $21)

-GILT +5.5% (secures $25M contract to enhance digital connectivity in Peru's Cusco Region)

-GOOS +5.3% (Baird Raised GOOS.CA to Outperform from Neutral, price target: C$24)

-KNTK +5.3% (to replace PPBI in the S&P SmallCap 600 Index, effective Sept 2nd)

-LCTX +5.1% (announces research collaboration with William Demant Invest to develop ReSonance (ANP1) for Hearing Loss)

-TLN +5.0% (to replace IBKR in the S&P MidCap 400 Index, effective Aug 28th)

-LEU +4.9% (signs agreement with KHNP and POSCO International for potential investment in American Uranium Enrichment)

-DJT +3.5% (signs definitive agreement for a business combination with Yorkville Acquisition Corp ($YORK) and Crypto.com to establish Trump Media Group CRO Strategy, Inc.)

-VFC +3.4% (Baird Raised VFC to Outperform from Neutral, price target: $20)

-IBKR +3.3% (to replace WBA in the S&P 500 Index, effective Aug 28th)

-LLY +2.3% (announces oral GLP-1 orforglipron successful in third Phase 3 trial, triggering global regulatory submissions this year for treatment of obesity)

-EH -11% (earnings, guidance)

-DQ -5.6% (earnings, guidance)

-NVO -2.0% (weak off LLY GLP-1 trial data)

BY Doug Kass · Aug 26, 2025, 9:15 AM EDT

BY Doug Kass · Aug 26, 2025, 9:05 AM EDT

BY Doug Kass · Aug 26, 2025, 8:55 AM EDT

Shadd Dales and Anthony Varrell on yesterday's Trade to Black podcast provided a good deal of background and current state of the rescheduling process.

In this, Shadd and Anthony discuss some of my own views on the issue of rescheduling..

Let's go to the tape.

Trump’s Political Play on Cannabis Rescheduling I TTB Powered by Dutchie

BY Doug Kass · Aug 26, 2025, 8:42 AM EDT

Did I mention that Costco's COST shares fell by -$17 yesterday?

BY Doug Kass · Aug 26, 2025, 7:48 AM EDT

BY Doug Kass · Aug 26, 2025, 7:36 AM EDT

Bonus — Here are some great links:

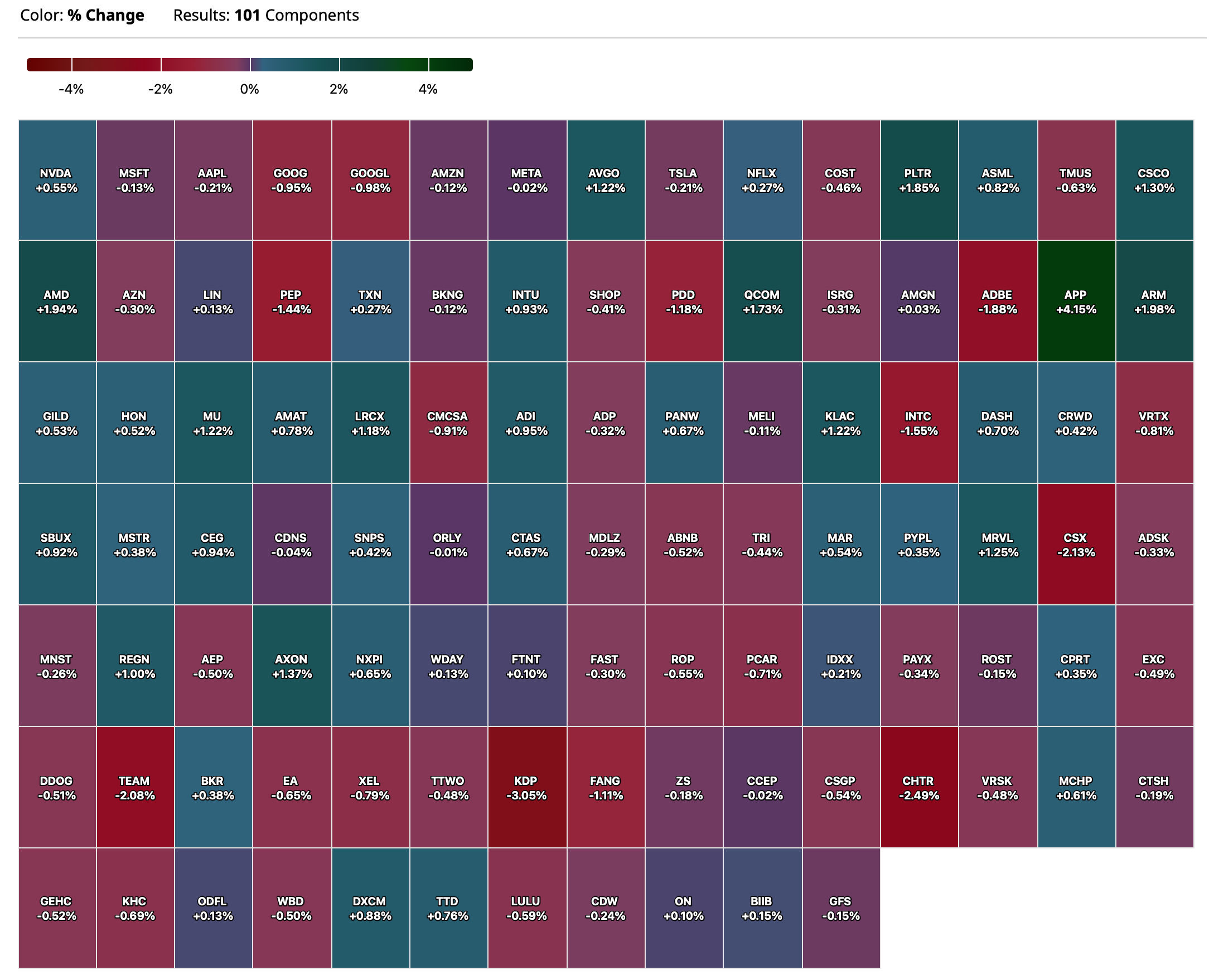

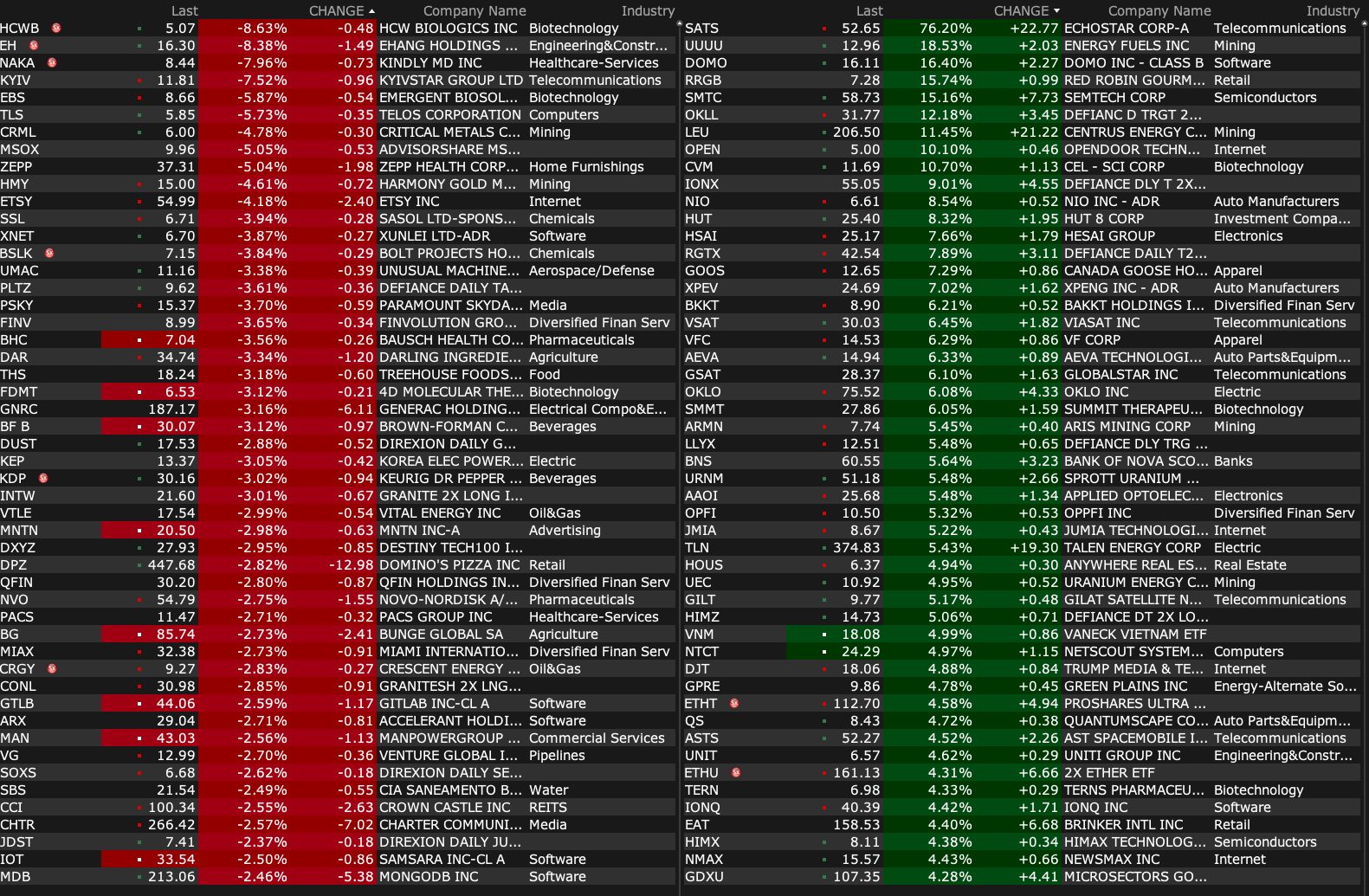

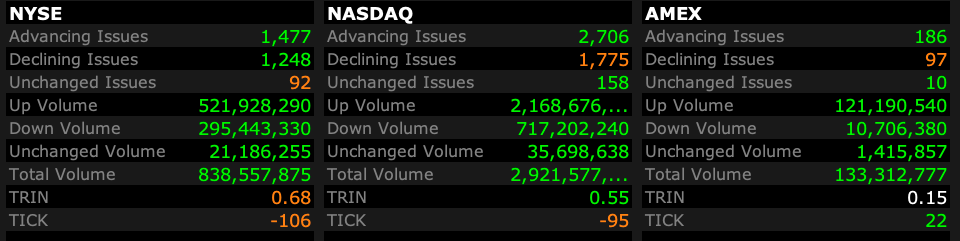

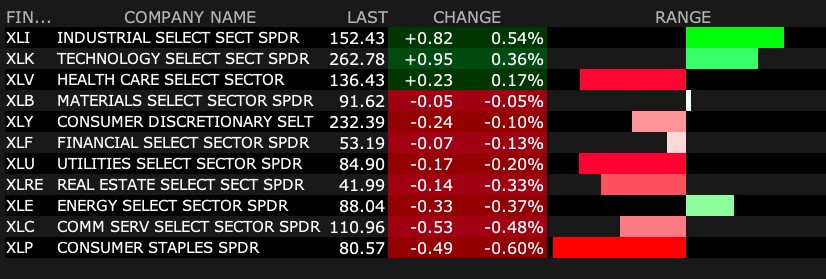

Confirmation Across the Cap Scale

BY Doug Kass · Aug 26, 2025, 6:40 AM EDT

BY Doug Kass · Aug 26, 2025, 6:30 AM EDT

* That was fast!

On a scale I am back reshorting the Indices:

* SPY $642.07

* QQQ $570.07

BY Doug Kass · Aug 26, 2025, 6:20 AM EDT

BY Doug Kass · Aug 26, 2025, 6:10 AM EDT

The S&P Short Range Oscillator remains in overbought at 3.33% vs. 3.85%.

Note: Last night (S&P -23 handles) we covered our index shorts on the Lisa Cook and tariff news. We have no Index positions currently but plan to reshort strength.

BY Doug Kass · Aug 26, 2025, 6:00 AM EDT

Dougie Kass

845 PM

On the Lisa Cook and tariff news I have covered all of my Index shorts:

I most definitely plan to reshort on strength.

Cash register...

BY Doug Kass · Aug 26, 2025, 5:50 AM EDT

Should we call this the Klarna effect?

This is the case in many industries. Last year, many illustrators in China were fired because their bosses thought they be replaced by "AI". However, the results were so bad that they ended up rehiring illustrators.