Quite the two-handed set of comments from Powell at Jackson Hole.

He learned his economic schooling well.

Two-handed in part because they are in a giant pickle. Too many years of circular fiscal excess aided and abetted by monetary shenanigans. One leading to more of the next, and so on. Which continues. There wouldn’t need to be so much if, but, then, maybe, could be this, could be that, in his full set of comments if the current situation, of our own making, had not become so complex.

I found his comments about the neutral rate to be interesting. Notice in the first sentence that he does not tell you what he thinks the neutral rate is (crafty, but transparent), but he later acknowledges it is now higher. Of course, being two-handed, he uses the word “may” as opposed to “is,” which shouldn’t be too hard. Just a gutless weenie. Of course, none of the bullish equity strategists mentioned that Powell said the neutral rate is now higher, which is a big deal!

My guess as to the neutral rate is that the political party in power would tell you it is 0% while the political party out of power would tell you it is 8%. Might as well just average the two, seems as good a methodology as any.

Our policy rate is now 100 basis points closer to neutral than it was a year ago…

We cannot say for certain where rates will settle out over the longer run, but their neutral level may now be higher than during the 2010s, reflecting changes in productivity, demographics, fiscal policy and other factors that affect the balance between saving and investment.

Boockvar: What Mortgage Rate Can Trigger More Supply?

From Peter Boockvar:

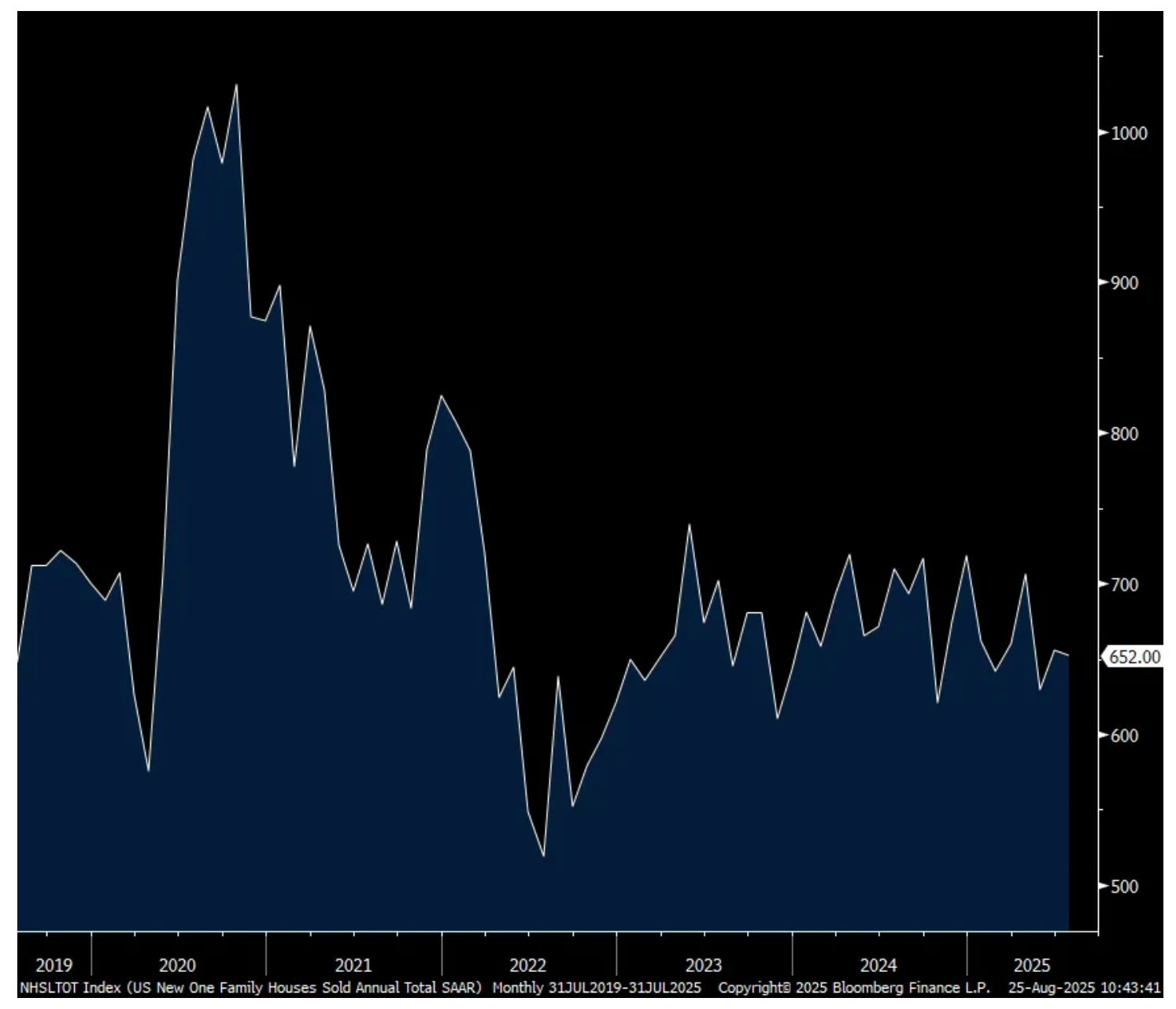

Home sales/What's the mortgage rate that would trigger more existing supply?

July new home sales totaled 652k vs 656k in the month before but that was 22k more than the consensus expected and June was revised up by 29k. Smoothing out this very volatile figure puts the 3 month average at 646k vs the 6 month average of 658k and the 12 month average at 669k. Months’ supply held at 9.2 while the median home price fell 5.9% y/o/y with mix always a big influence.

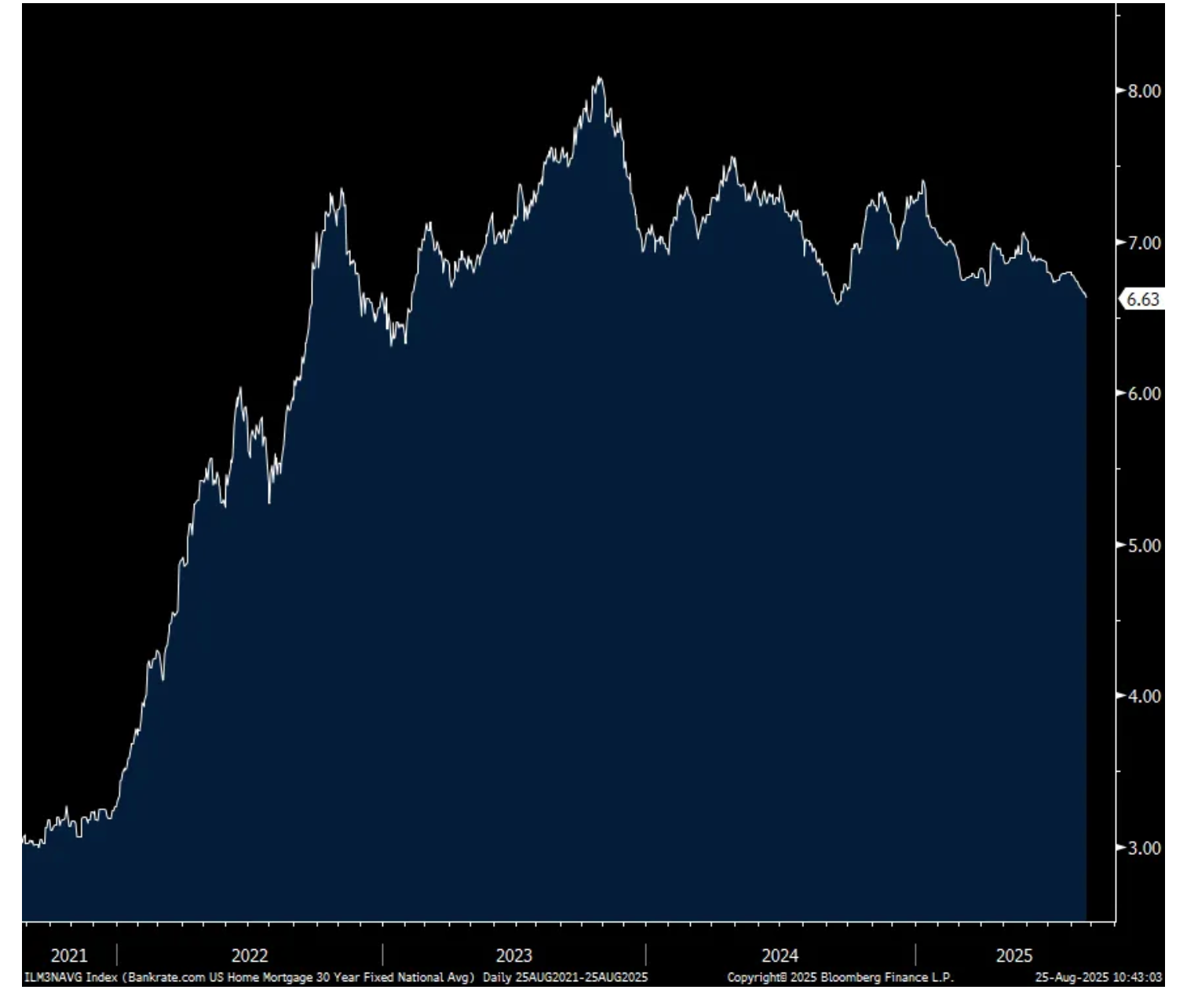

Bottom line, the deceleration over the past year, though modest, certainly reflects the affordability challenges we continue to clearly see. The question of course now is whether the recent decline in the average 30 yr mortgage rate (if it holds which I don’t believe it will) is enough to lift demand that is not offset by higher home prices. The interesting thing though is just maybe the drop in mortgage rates will help the existing home market more so than the new home market as the new home market has already seen the major builders buy down mortgage rates and include other incentives. You can be sure builders can’t wait to stop with the incentives if they can.

With the existing home market, while we tend to focus mostly on the demand side that can be helped by lower mortgage rates, as said here many times the key will be what the supply side response will be. If not enough of the latter, all we’ll see is higher prices that offsets the benefit of lower mortgage rates. However, there is a mortgage rate threshold that maybe triggers those who’ve stayed in their homes enjoying their low mortgage rate that might be incentivized to move, even with the higher rate on a new mortgage relative to the rate on the existing home. I’m not sure though what that rate spread (the one between the new mortgage rate on offer vs the one that would be given up) needs to be in order to encourage more transactions of existing homes.

Coming up now, my favorites — Guy and Dan — talk in an honest and transparent conversation of the important factors (nothing standard or superficial!) that may influence your trading and investing.

Boockvar on What's Next for Powell, AI and Chinese Chips

From Peter Boockvar:

What next?/Big picture with GenAI/BJ's and their growing coupon clippers

What next for Jay Powell? Well, it's now obviously clear what he'll do in three weeks and the October fed funds contract covering the September meeting has the odds at 90% (after initially getting to 100% immediately after his speech) of a 25 bps cut. After that he'll have 5 meetings left and I want to highlight again that while he's been the boss this year, the Fed dot plot has told us that a 1% REAL fed funds rate is what they consider 'neutral.' And I'll say again, the 3% nominal rate only is appropriate in their eyes IF inflation is sustainably at 2% and which instead is about 100 bps above that. Thus, with core PCE expected for July at 2.9% (with core CPI at 3.1%), one or two rate cuts gets us to that 1% REAL rate.

Thus, while Powell is in the seat, getting more cuts than two under his tenure will take another leg down in inflation and/or a much sharper slowdown in the labor market and coincident rise in the unemployment rate. We of course root for the former because rate cuts in response to the latter should not be hoped for and the two recessions over the past 25 years in the early aughts and the GFC did not help stocks under that circumstance. Either way, the market is pricing in a 100% chance of a total of 100 bps of cuts through next April with Powell as Chair (and 100% chance of two this year).

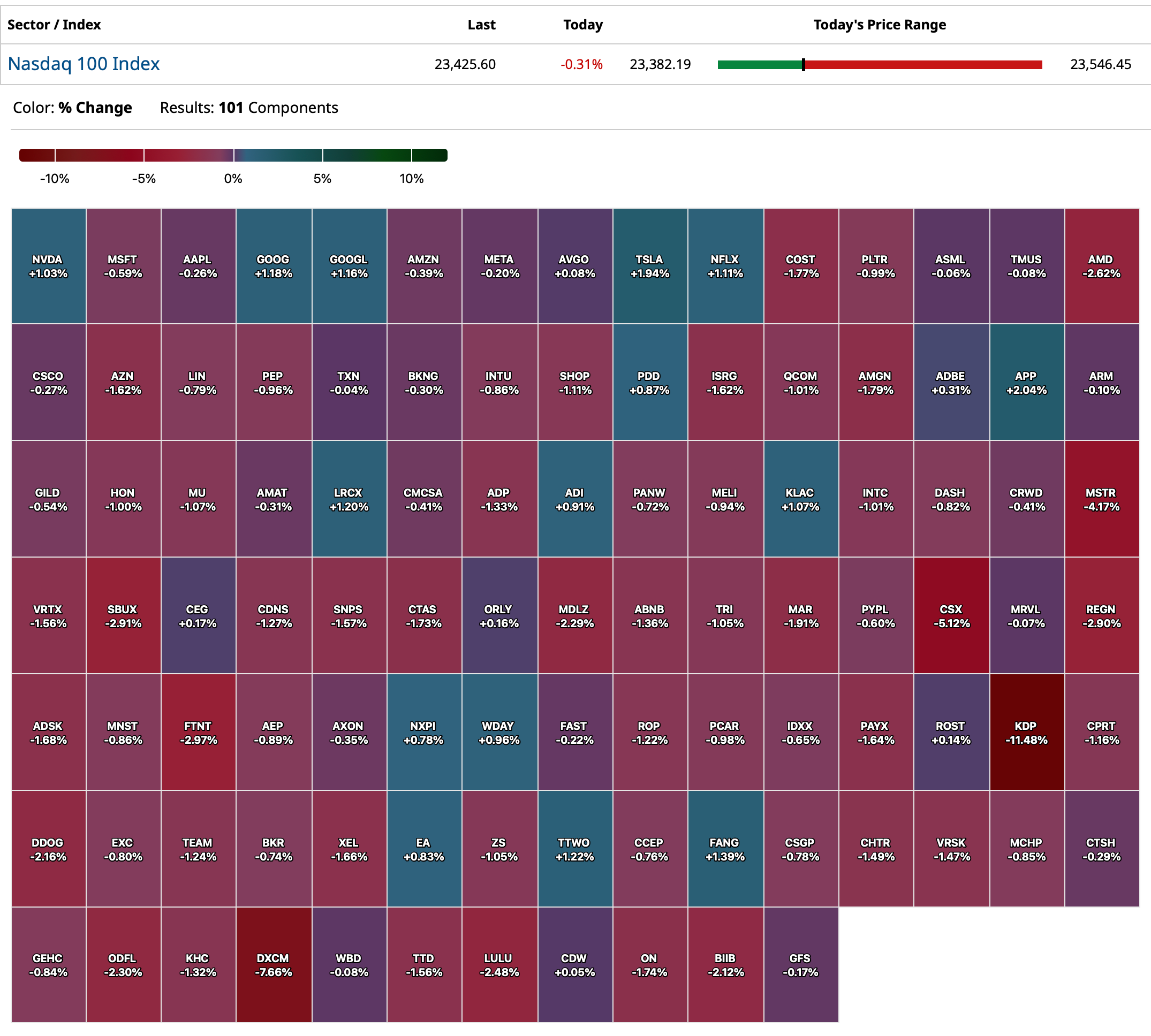

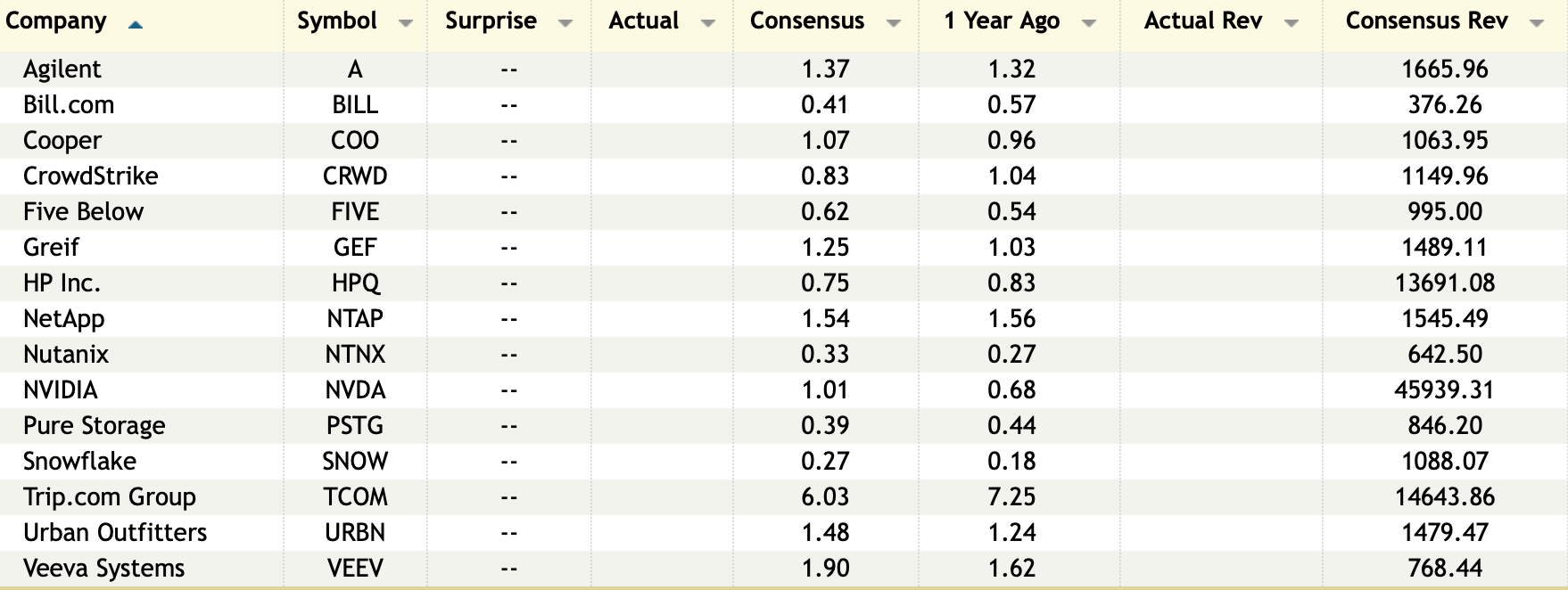

As we gear up from Nvidia's earnings because not only does the stock make up 8% of the S&P 500, a figure not seen for any one stock going back at least 45 years, but also what it means for the entire massive AI capital spending ecosystem which has been the main driver of economic growth over the past two years, outside of upper income spending and government largess. I want to make a point though as we think about Gen AI globally in the coming years because I don't think there is enough appreciation of the intensity of Chinese competition that American companies are going to experience.

We've already lit a fire under China by incentivizing them to build out their own semiconductor industry where in the coming years they will not need our chips at all. Cutting them off has been an epic fail but great for them as they are far more advanced technologically than they would have been otherwise. And, they are a huge competitor now in the creation of Gen AI models and many more than just DeepSeek (Moonshot Kimi, Qwen from Alibaba, MiniMax to name a few). Imagine being that shoestring start up in Singapore and you need access to a reliable, cheap GenAI model, who are you going to go to? The cheapest one most likely, assuming many models are pretty similar which they will be as the software becomes commoditized, and China will be able to provide that.

As an example of the new reality, in the Weekend FT, I read this headline, "Chinese semiconductor shares surge after DeepSeek boosts domestic chips." In it, "Cambricon Technologies led a rally of Chinese chipmakers yesterday after artificial intelligence start-up DeepSeek unveiled an updated model that would be compatible with domestically made semiconductors."

My point here is that US tech became a global, dominant powerhouse with high market share around the world, outside of China blocking Google, Facebook, Instagram, and Twitter (X). With semi's and with GenAI software, that is not going to be the case in coming years as China will be a tough rival.

This is what BJ Wholesale said of note on Friday in their earnings call as the stock fell 8.5% in a big up tape:

"Our perishables (like dairy, meat and fresh produce), grocery, and sundries division led our Q2 performance with healthy 3% comp growth and a two year stack that held steady with Q1." General merchandise comp sales fell 2.2% y/o/y.

"certain higher ticket discretionary categories in general merchandise, such as recreation and lawn and garden, experienced double digit declines in comp sales." On the flip side, "our apparel business grew comp in the low single digits despite the weather headwinds."

Bottom line from them, "As we step out of the discrete quarterly results and evaluate the state of our membership base more broadly, we did see members across all income levels turn a bit more cautious during the quarter, driven by the uncertain macro environment."

"I think we're seeing overall a pretty resilient consumer in the face of everything going on with the tariffs and the news cycle and the resulting inflation that's come through. As a side note, the inflation that's come through wasn't all that much yet in the quarter. It was about 1 point of inflation, very similar to what you've heard from our competitors that have reported this week. But I do think you're seeing a consumer that is really frustrated by the whole thing. And when we look at the economic cohorts that we talked to you all about, the high, medium and low segments, all of them look like they're a little bit concerned about what they're seeing out there and what they're hearing."

"Although total spending increased in each of those cohorts and on a per-member basis within each of those cohorts, you could definitely see behaviors that indicate that they're on the lookout for value. Their propensity to use coupons or to react to deals is a bit higher. Certainly looking at private label, a little bit more than they have in the past, which may be good for us in the long term, but it certainly could be an indication of consumer stress out there."

"Discretionary categories were more impacted than the non-discretionary which, again, was not too much different from the first quarter, but all these are indications of a consumer that's a little bit more choosy with their dollars. And it's what I think we'll see for the remainder of the year until we get through this cycle."

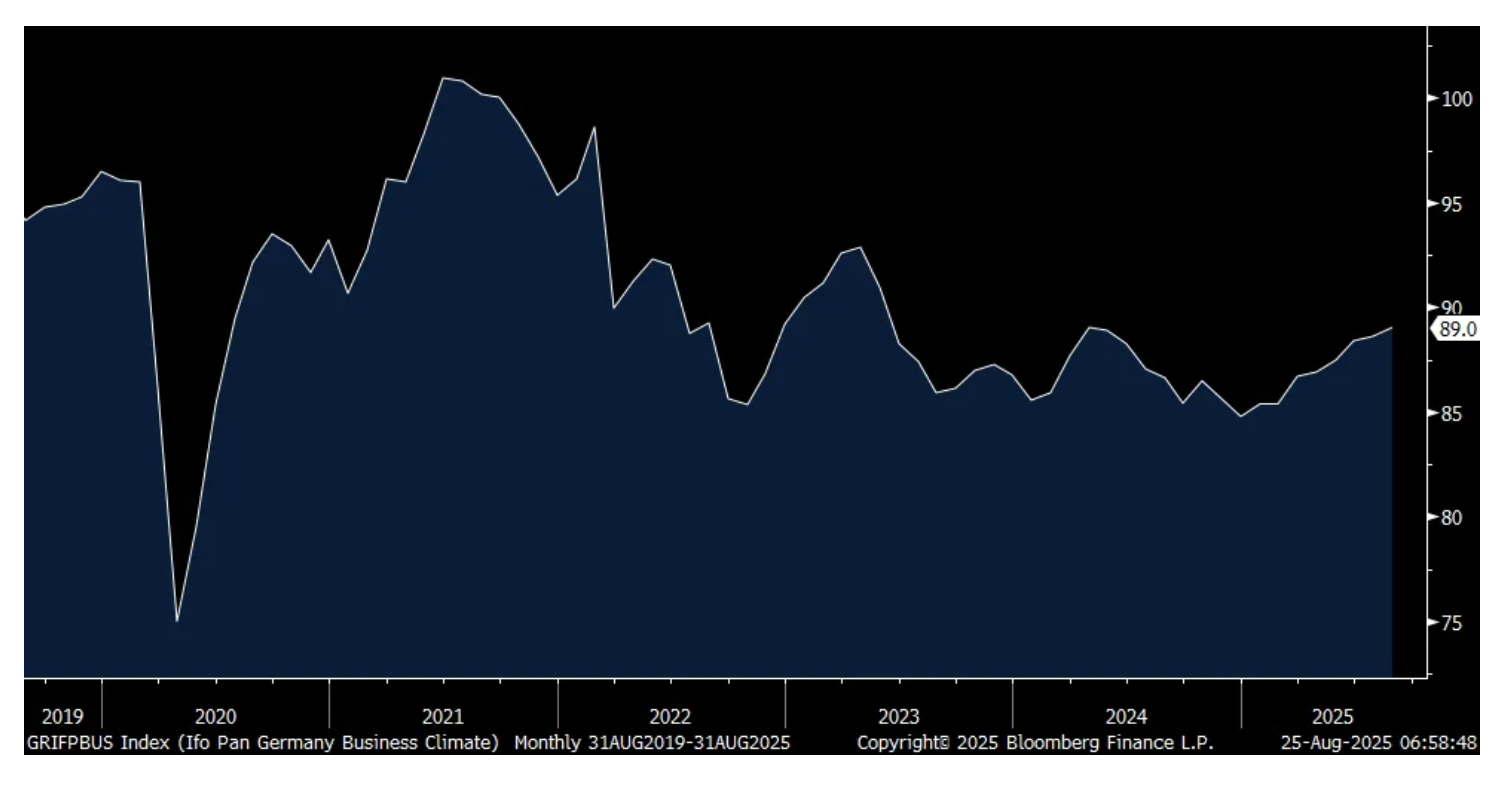

The only noteworthy data point outside the US was the August German IFO business confidence index which rose a touch to 89 from 88.6 and vs the estimate of 88.8 with all of the improvement in the Expectations component as the Current Assessment fell a hair m/o/m. While the index is at the best level since May 2024, IFO said "The German economy's recovery remains weak." Current conditions for both manufacturing and services fell slightly m/o/m though expectations for each improved.

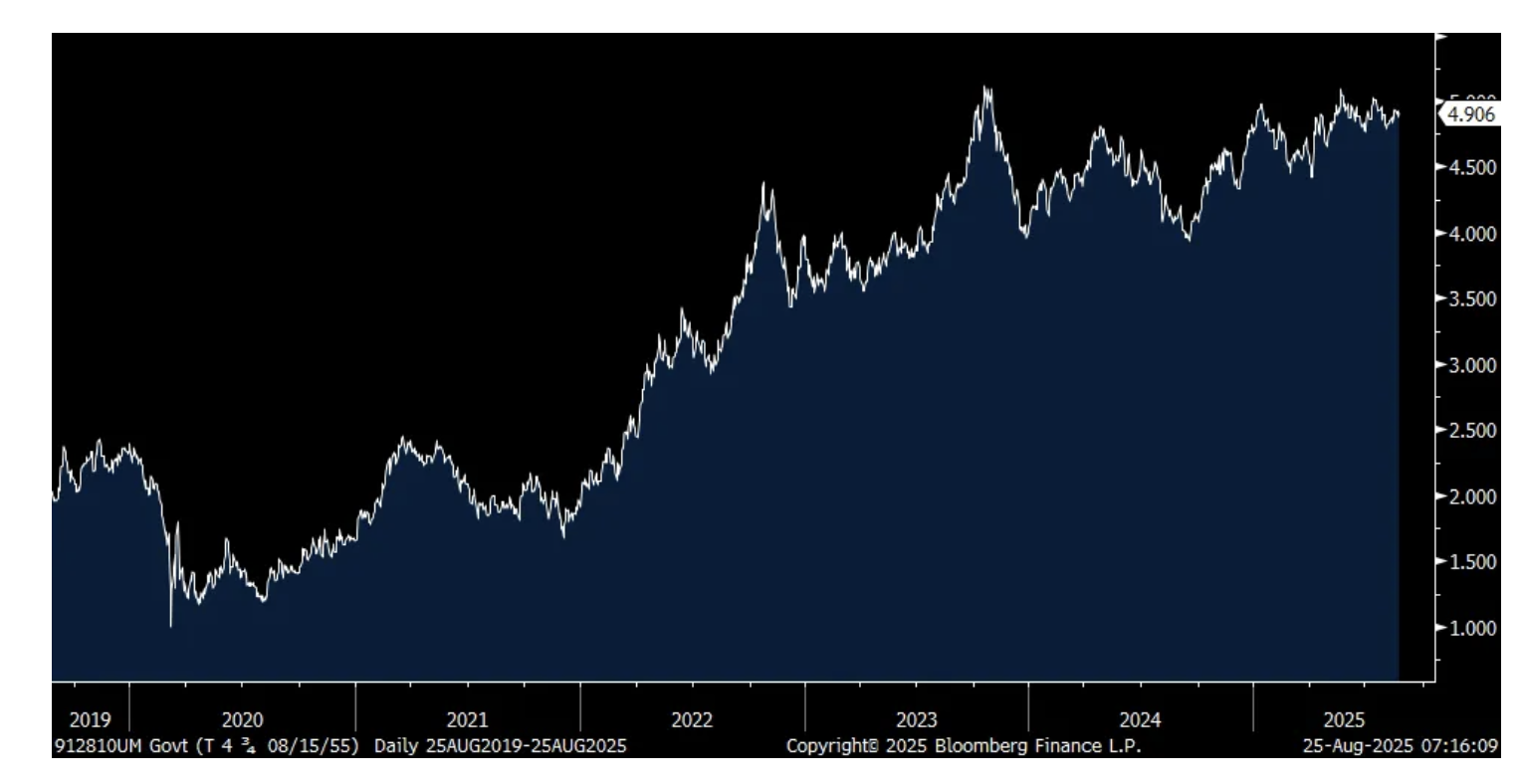

While about as expected, European bond yields are rising across the board by about 5 bps. The French 30 yr yield is at the highest since November 2011. The US 30 yr yield at 4.90% is exactly back to where it was right before Powell's speech hit the tape, up 3 bps this morning.

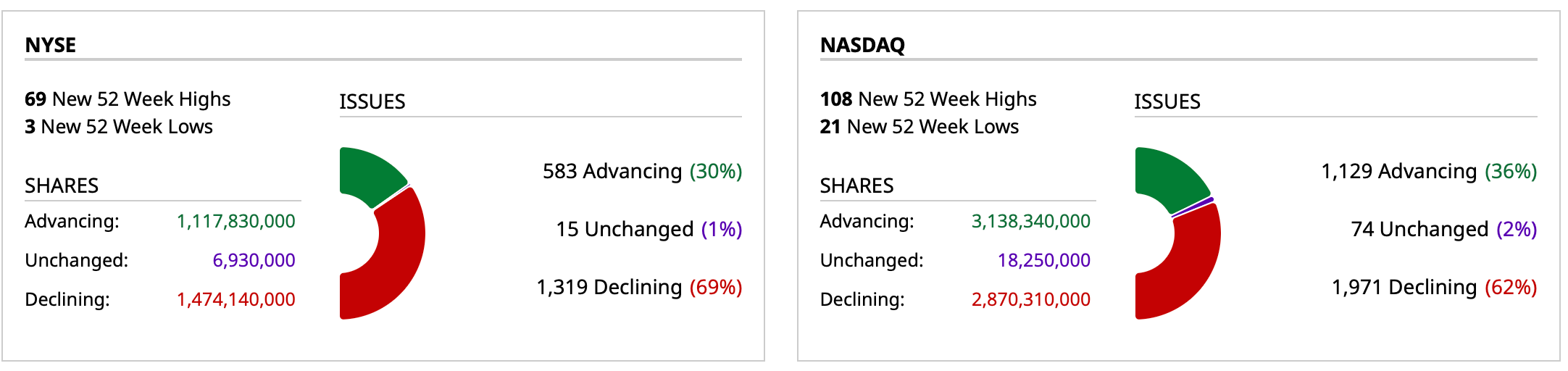

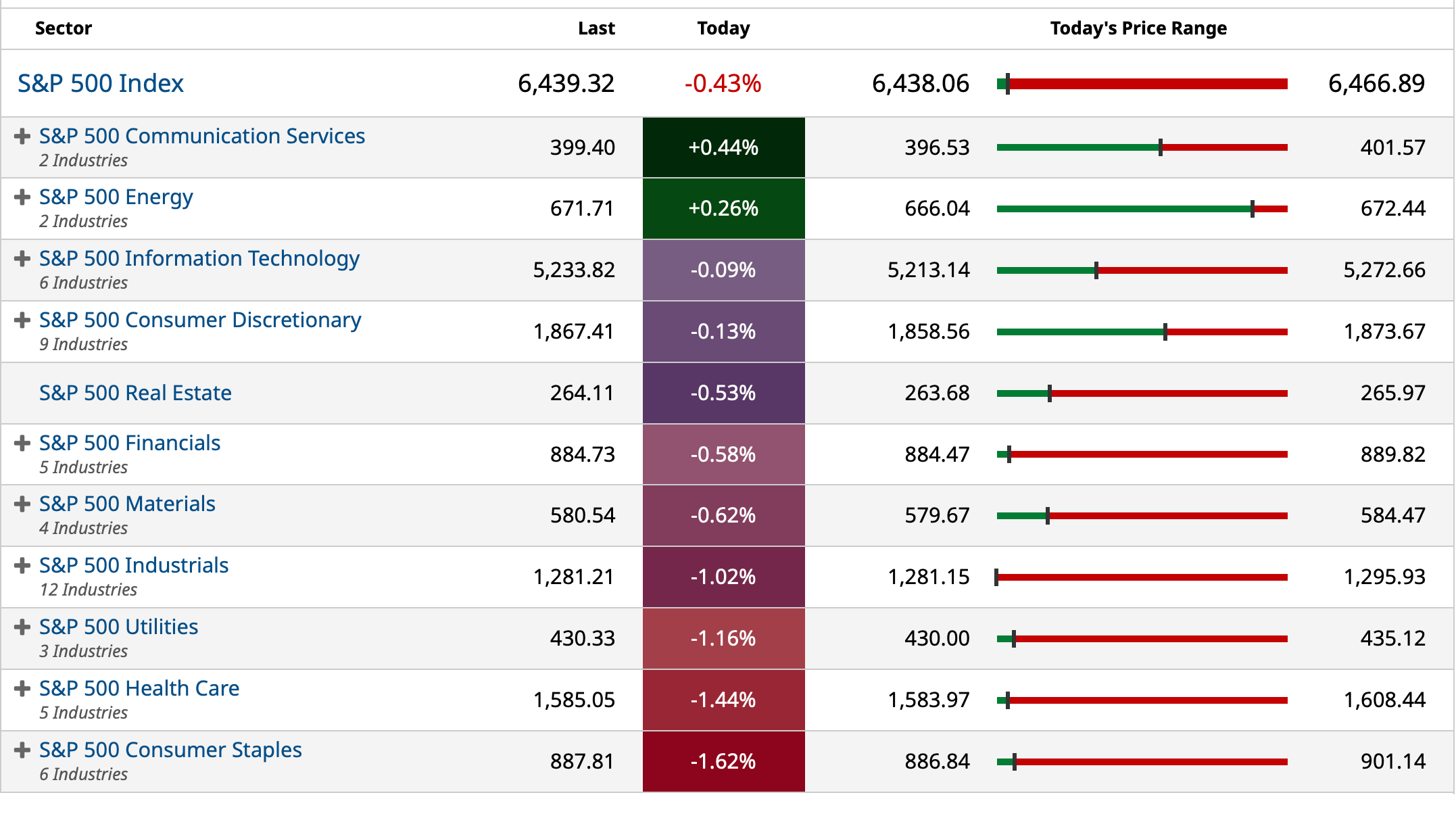

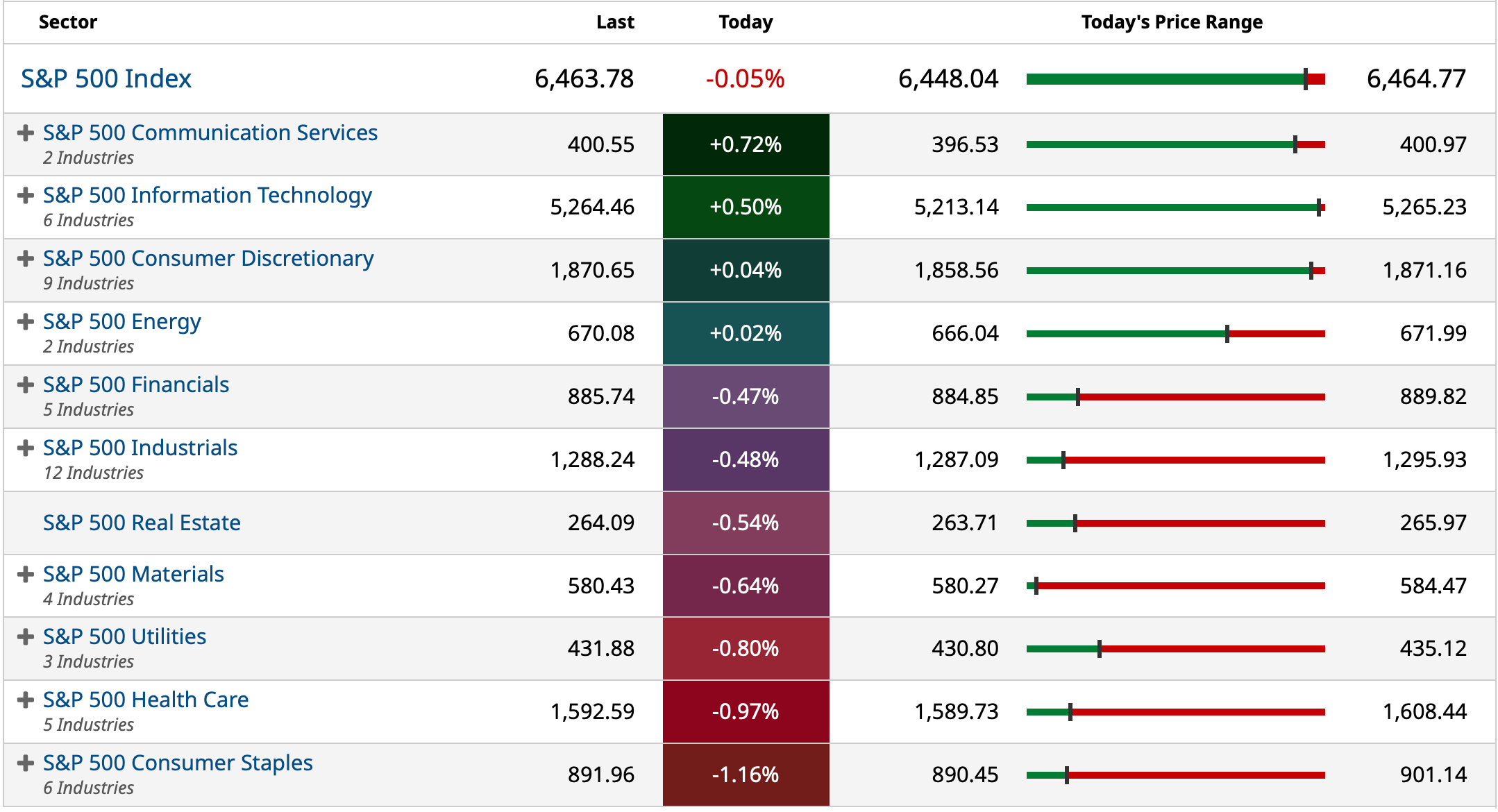

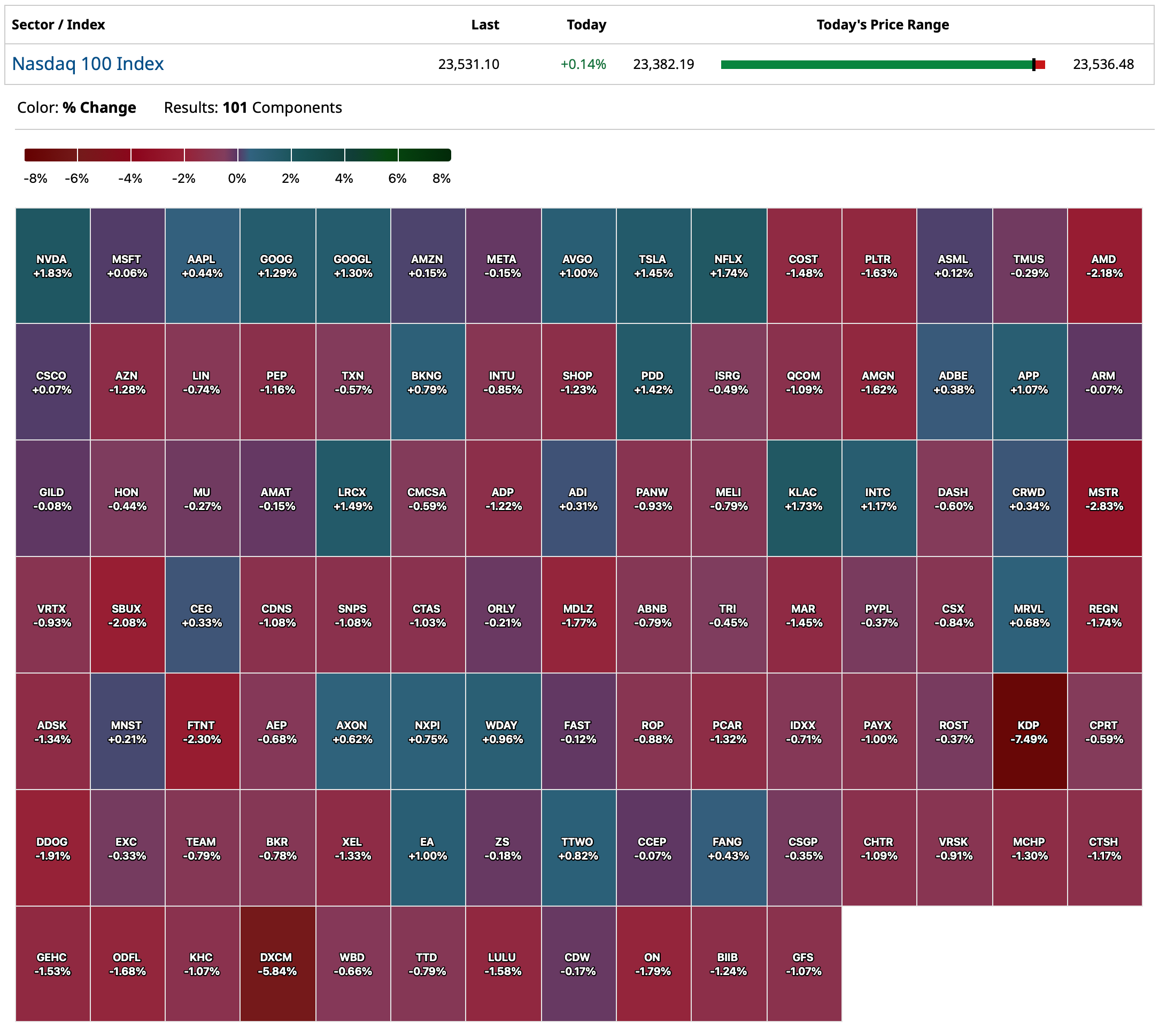

We remain tactically bullish. After 5 consecutive down-days, the SPX stages a rally, gaining its most since May 27, to finish its third consecutive up-week, closing 2pts below an all-time high. Powell’s speech at Jackson Hole confirms a Sept Fed cut, which ignited the rally which also broadened. On Friday 10 of 11 SPX sectors were higher with nearly 85% of the index constituents in the green. As we close out this month, NVDA remains key datapoint as the AI theme has come under pressure, led by a retail investor that flipped to net-short for the first time in two months. Upon returning from Labor Day, the market will focus on NFP which is unlikely to create a headwind as it would take a material uptick in hiring to reduce expectations for a Sept cut, e.g., moving from 73k in the Aug print to something like 175k – 200k in Sep. Currently, BBG survey see Sep printing 85k jobs. At this stage, even a hotter CPI print on Sep 11 seems unlikely to derail optimism surrounding accommodative monetary policy. While September seasonality is negative, on average, it has been a 50/50 proposition of whether it has a gain or loss over the last 15 – 25 years (see chart at the bottom of this section). While we may see a slight pullback, it seems that Bears would need see significant sell-off in Tech, catalyzed by an NVDA earnings miss, for the market to experience a 5% pullback ahead of the Sep 17 Fed meeting.

· MONETIZATION MENU – We still like MegaCap Tech as a long but think it makes sense to reduce exposure to play a broadening of the rally. Further, we think China Tech plays will continue to close the recent performance gap (Mag7 has outperformed HSTECH by 12% over the last 3 months and KWEB by 6.4%). We think Cyclicals and SMID-caps plays outperform in the very near-term. Rate sensitives (esp. Homebuilders), Consumer-related (esp. Retailers), and High Short Interest (JPTASHTE Index) are likely to perform well as we see the broadening of the rally. Defensives standout as potential short plays. Ex-US, we like EM (China and Latam) over DM as a bearish USD play.

· MACRO DATA – Last week’s data was a mixed bag, but the Flash PMIs give optimism that growth may be accelerating but with increasing pass-through of tariff costs to the consumer. More specifically, PMIs shows business activity expanding at the fastest rate since 2022, across both Mfg and Srvcs. This is increasing labor demand as the we are seeing the largest build-up of uncompleted work since May 2022. Business confidence is improving, confirming information for the Small Business Optimism survey. Tariffs are spiking prices with the highest rise in average selling prices seen in 3 years, comments echoed by WMT. Jobless claims showed a weakening labor force.

· JACKSON HOLE / FED CALL – Powell confirmed the Sept Fed cut as the Committee shifts its focus from balanced risks to being supportive of the labor market. Feroli sees Powell’s comments as confirming the Fed cutting by 25bp in Sep as the bond market reduced its probability from 84% on Monday to 72% on Thursday and then to 81% on Friday.

· RETAIL INVESTOR – retail investor behavior changed during the past week with the Tech selling in early in the week, breaking their 2 month long daily buying streak (+$1bn avg/day) to become net sellers (-$140mm). NVDA earnings could be an important catalyze in rebooting the Retail bid.

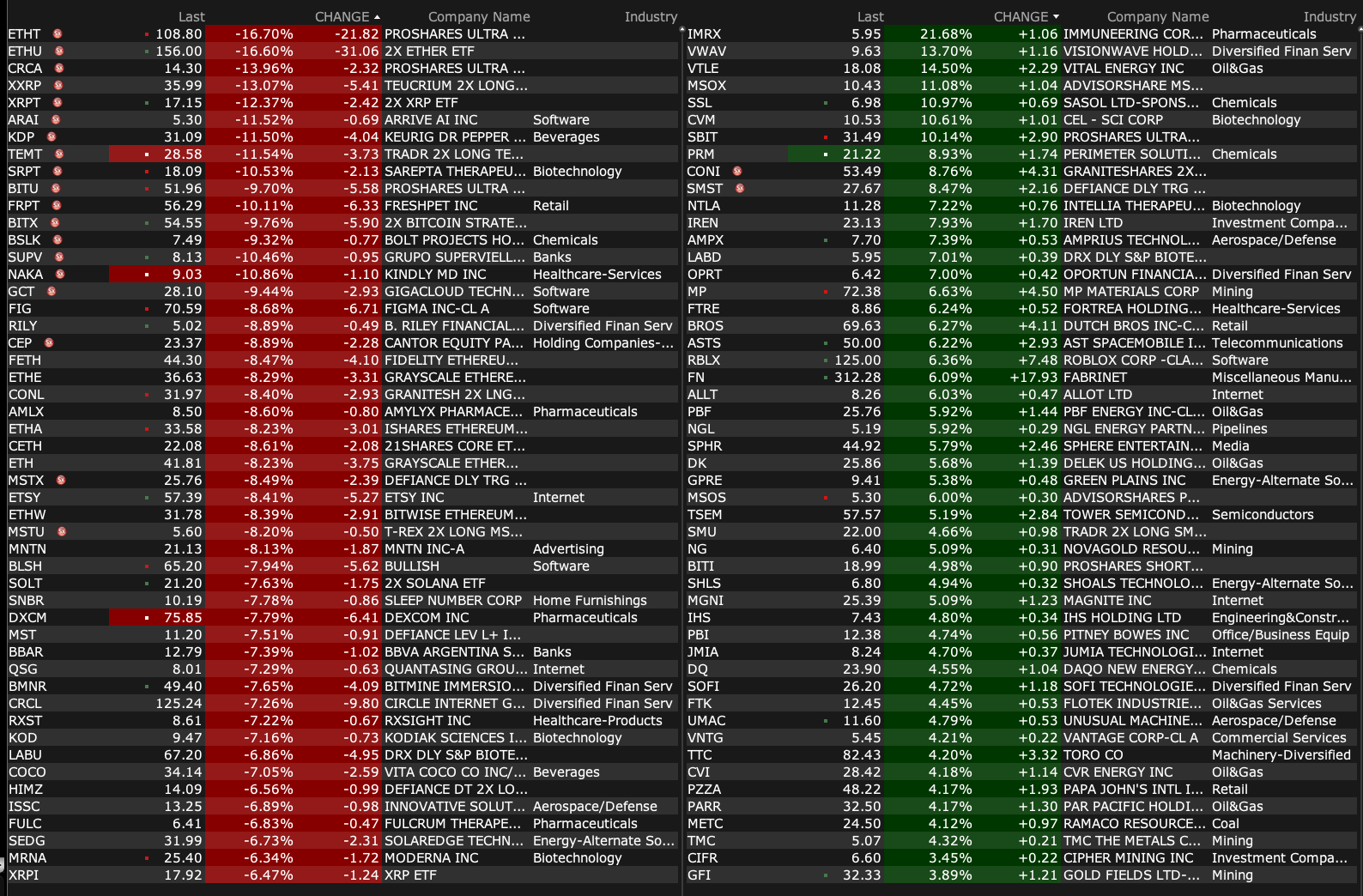

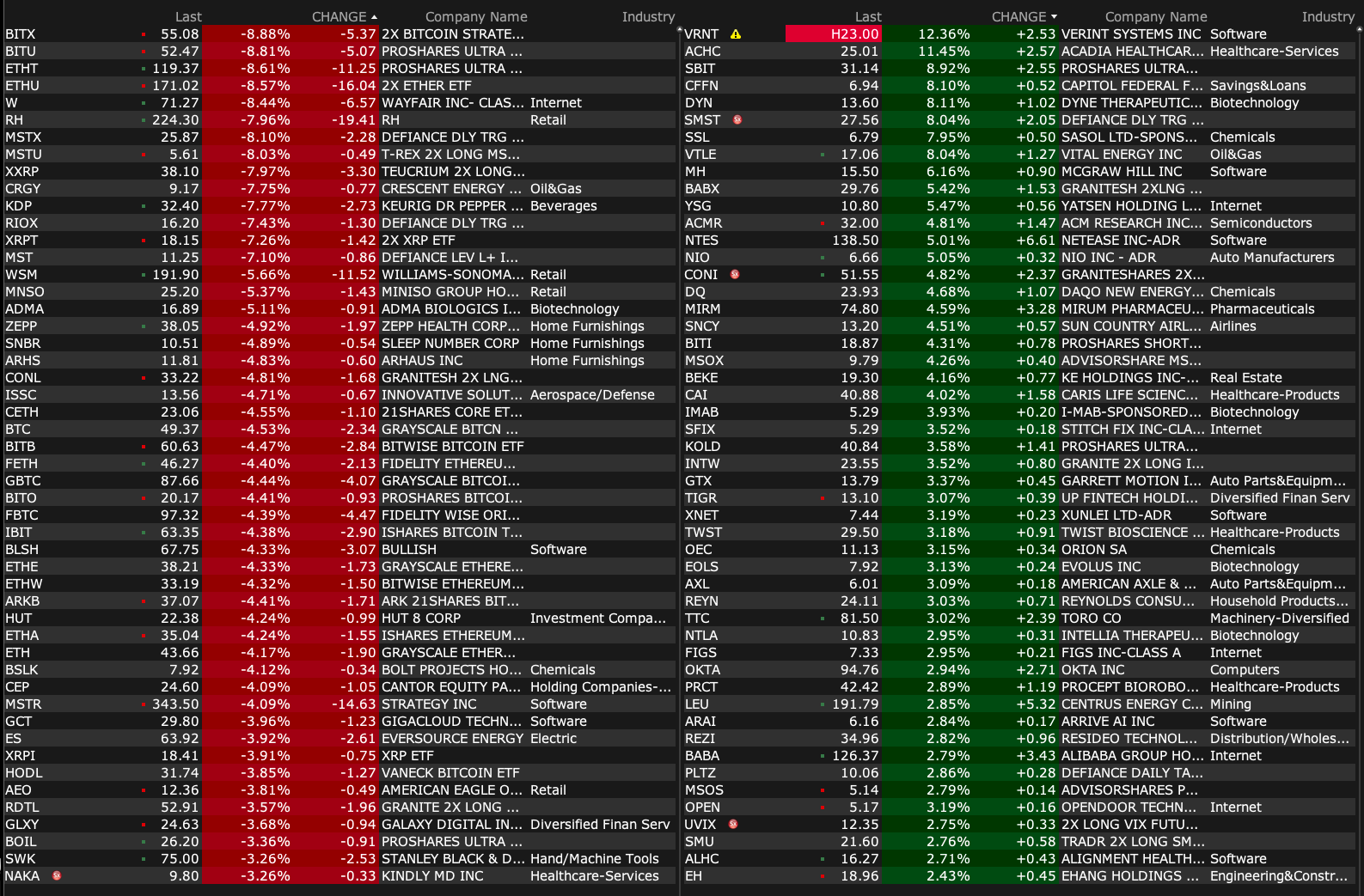

-STSS +46% ($400M private offering announcement at placement of $6.50/shr)

-OPAD +30% (momentum)

-NSSC +15% (earnings)

-SCPH +13% (to be acquired by MannKind at $5.35/shr in cash plus $1.00/shr CVR)

-VRNT +12% (confirms to be acquired by Thoma Bravo at $20.50/shr cash for EV of $2B)

-VTLE +9.3% (Crescent Energy to acquire Vital Energy in all-stock transaction valued at $3.1B)

-OLPX +8.6% (Canaccord Genuity Raised OLPX to Buy from Hold, price target: $2 from $1.50)

-BFRI +8.5% (announces Last-Patient-Out in Phase 2b Study of Ameluz (aminolevulinic acid HCI) Topical Gel, 10% for the Treatment of Moderate to Severe Acne Vulgaris)

-AUUD +6.8% (announces restructuring of engineering team in preparation for business combination)

-DYN +6.1% (Raymond James Raised DYN to Strong Buy from Outperform, price target: $35)

-OKTA +2.9% (Truist Raised OKTA to Buy from Hold, price target: $125)

-EOLS +2.8% (Evolysse Sculpt Injectable Hyaluronic Acid Gel Premarket Approval application submitted to U.S. FDA with approval expected in 2H26)

-FN +2.2% (JPMorgan Chase and Co Raised FN to Overweight from Neutral, price target: $345)

Downside:

-AXGN -14% (US FDA extends PDUFA goal date for Avance Nerve Graft BLA by three months to Dec 5)

-DFDV -12% (announces $125M equity raise of 4.2M shares at $12.50/shr to accelerate Solana treasury growth)

-RH -8.1% (US President Trump claims to do ‘major tariff investigation’ on furniture imports)

-W -8.1% (US President Trump claims to do ‘major tariff investigation’ on furniture imports)

-KDP -7.0% (confirms to acquire JDE Peet's at €31.85/shr in cash in €15.7B deal and subsequently separate into two companies)

-CRGY -5.9% (acquiring VTLE in all-stock transaction valued at $3.1B)

11:30: Treasury hosts a $82B 3 and a $73B 6-Month Bill Auction;

FED SPEAKERS:

3:15 p.m.: Fed Bank of Dallas President Logan (Non-Voter) speaks and participates in panel before the Bank of Mexico Centennial Conference, Mexico City, Mexico (Text available. Moderated Q&A expected);

7:15 p.m.: Fed Bank of New York President Williams (Voter) gives keynote before the Bank of Mexico Centennial Conference, Mexico Ciry, Mexico. (Text and moderated Q&A expected)

Based on my accumulated research input, it is my view that Pres. Trump will shortly (and finally!) give cannabis rescheduling the green light.

According to my contacts, the principal motivating factor is not the rationale presented by leading advocates who the President is close to (e.g. Weldon Angelos, Mike Tyson and industry influencers like Trulieve's TCNNF Kim Rivers and others) but rather the desire to embarrass the Democratic party who were unable to bring to ball over the goal line during the Biden Administration.

The President, I have been told, also wants to gain favor from a specific population (and voting) sector.

Frankly, after all these years I and others will take it anyway we can get it!

I got chai recently by reestablishing my MSOS long. (I also own MSOS calls)