Friday's After-Hours Movers

As of 4:19 p.m.:

BY Doug Kass · Aug 22, 2025, 4:37 PM EDT

As of 4:19 p.m.:

BY Doug Kass · Aug 22, 2025, 4:37 PM EDT

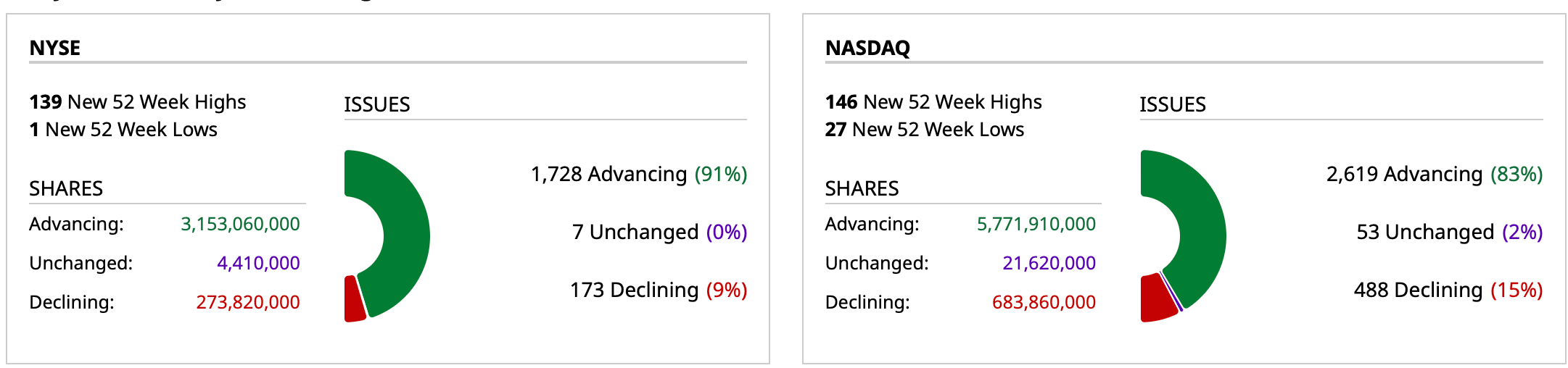

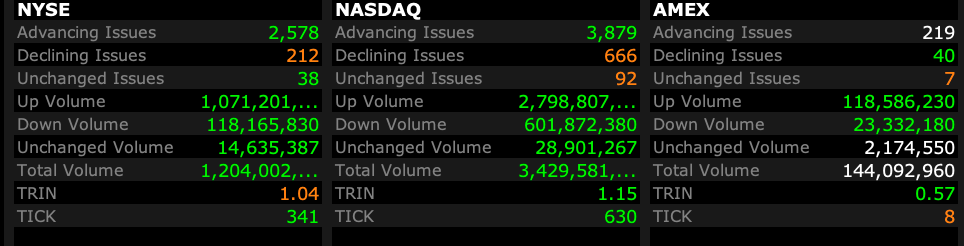

- NYSE volume 11% above its one-month average;

- NASDAQ volume 8% above its one-month average;

- VIX index: down 14.34% to 14.22

Breadth

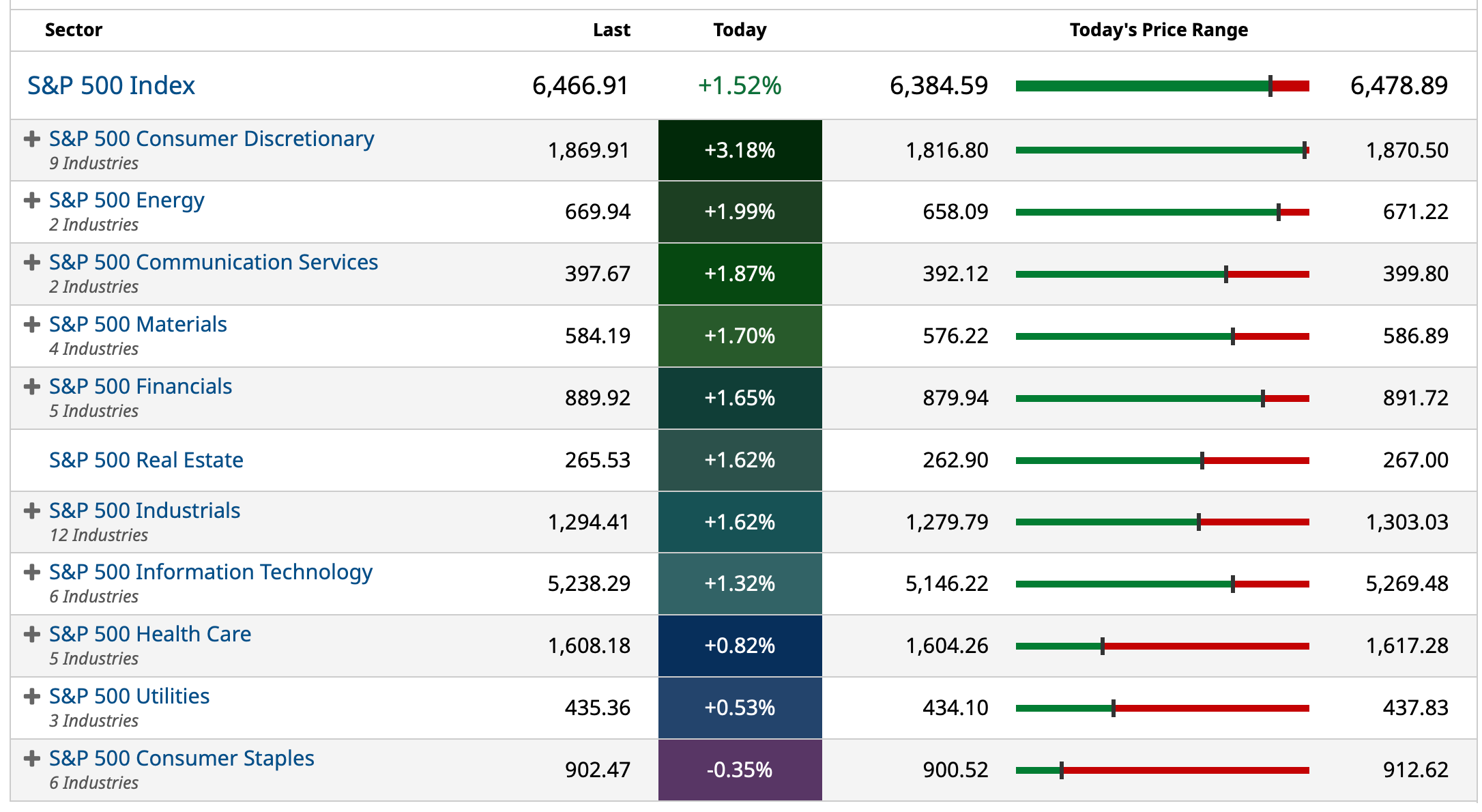

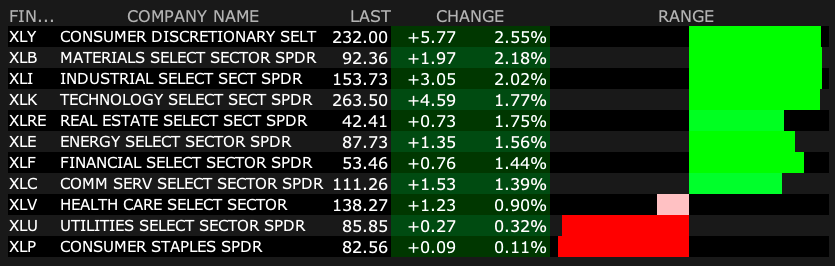

Sectors

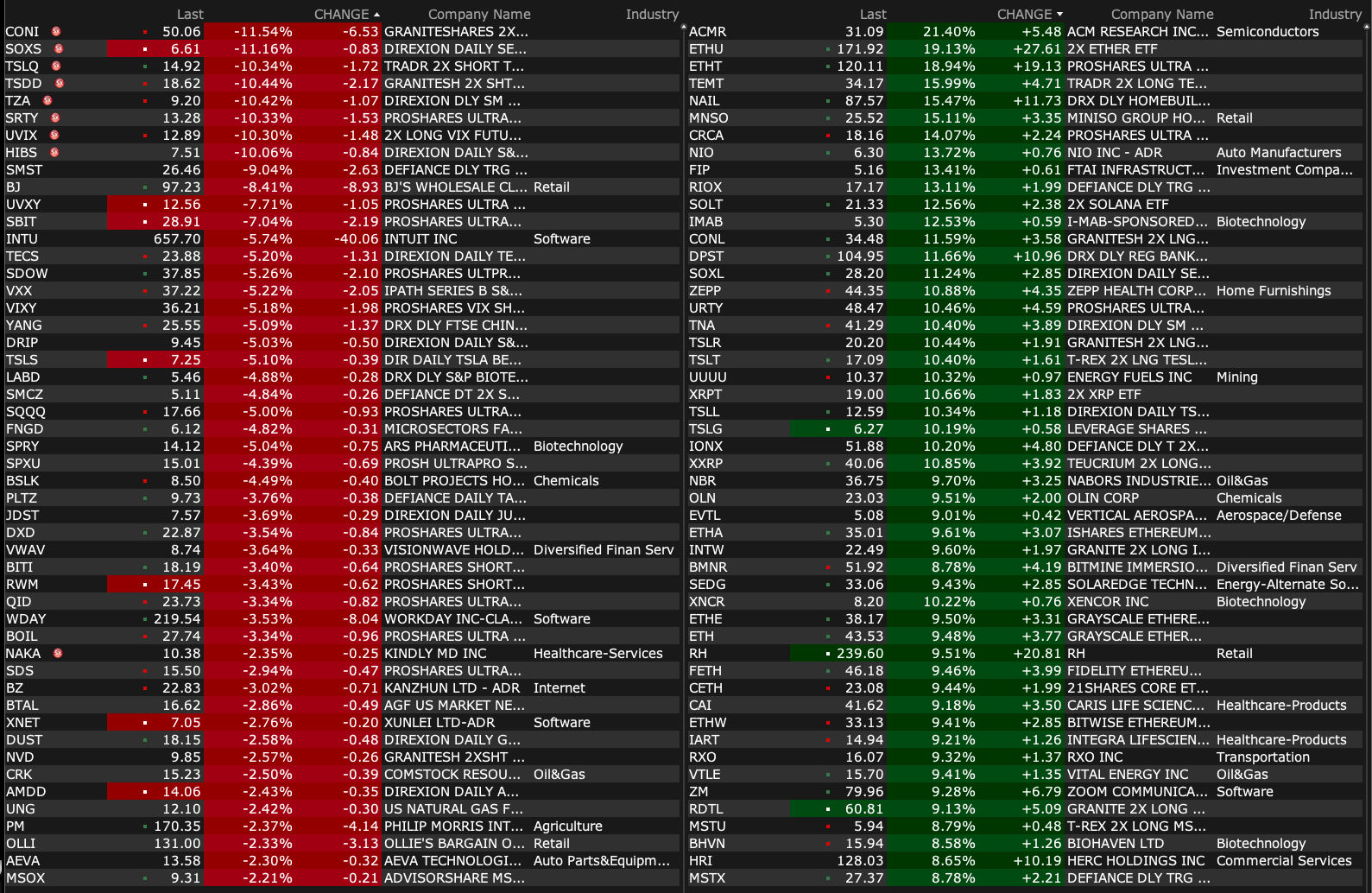

% Movers

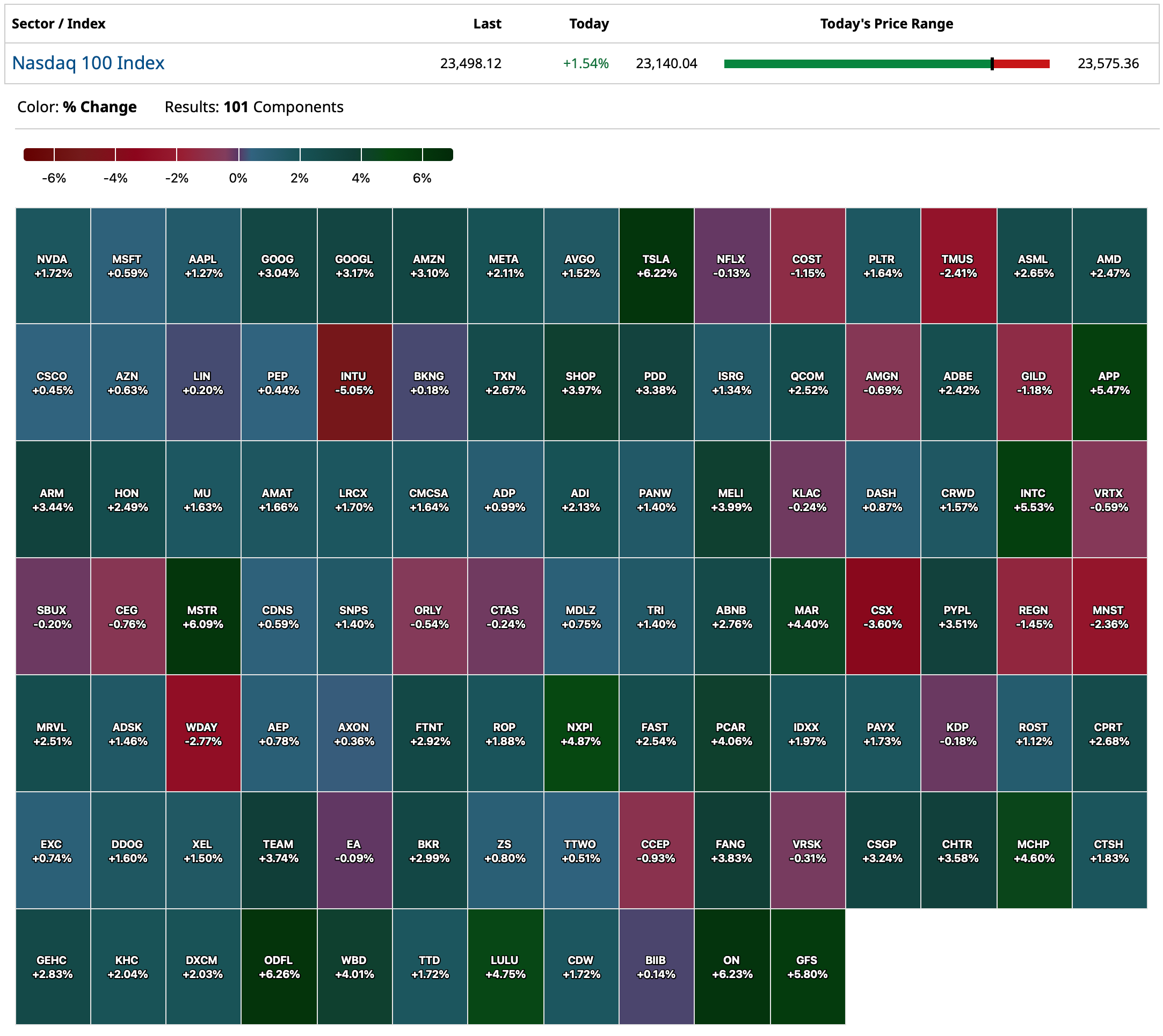

Nasdaq 100 Heat Map

BY Doug Kass · Aug 22, 2025, 4:22 PM EDT

I am calling it a day early to spend some time on the beach with my family.

As always, a sincere thanks for letting me have this platform today, all week and over the last 28 years.

I hope my output provided value to your investing and trading processes.

Enjoy the weekend.

Be safe.

BY Doug Kass · Aug 22, 2025, 3:00 PM EDT

From Peter Boockvar:

Succinct Summation of the Week’s Events

Positives,

1) Agree with him or not, Jay Powell at least gave us certainty for an expected rate cut in September.

2) The August US manufacturing PMI jumped to 53.3 from 49.8. The service sector PMI, which DOES NOT include retail/wholesale trade and construction for some reason and a notable chunk of the service sector, fell a touch m/o/m to 55.4 from 55.7. There was a lift in employment to the highest since January as “Companies largely took on additional staff in response to rising backlogs of work.”

3) Within the Philly manufacturing index the six month business outlook rose to 25 from 21.5 and compares with the half year average of 20.8. A standout positive was the capital spending plans which jumped to 38.4 from 17.1 and about double the six month average.

4) Housing starts in July totaled 1.428mm, above the estimate of 1.297k and June was revised up by 37k to 1.358mm. The main reason for the lift was an increase in multi family starts to 489k from 445k in June and that is the most since May 2023, though jumps around month to month. Single family starts were up 26k m/o/m to 939k but after falling by 36k in the month before and well below the 1mm we saw in January and nearly 1.1mm in February.

5) July existing home sales remained at 30 yr lows but at 4.01mm annualized was a bit above expectations of 3.92mm. Months’ supply was 4.6 vs 4.7 in June and 4.6 in May. Home prices were flat y/o/y while first time buyers made up only 28% of purchases vs 30% in the two prior months and 34% in the one before that. Cash buyers rose to a 5 month high that of course aren’t subject to mortgage rates.

6) From the Dallas Banking Conditions survey: "Loan volume and demand increased in August. Loan volume was driven by a sharp acceleration in residential real estate loans, which had contracted in the prior period. Credit tightening continued, but loan pricing declined, both at a pace slightly faster than in June. Across all loan types, loan performance deteriorated. Bankers reported declining general business activity; however, their outlook is mildly optimistic. Survey respondents expect growth in loan demand and business activity six months from now, with a minor deterioration in loan performance."

7) From Walmart: With Walmart US and whose comps grew 4.6% y/o/y, "Sales and general merchandise were positive in every segment and across categories in the US led by apparel, media and gaming, and automotive." They also saw “strong growth in grocery and health & wellness” and they gained market share too.

8) From Ross Stores: Comps grew 2% and "This improvement was broad based with a positive change in trend in nearly all major merchandise categories and most of the regions across the company. During the second quarter, sales in May were strong and softened in June before rebounding sharply in July. We were pleased to see the improved trend at the end of the quarter, particularly with the early sales performance related to the back-to-school selling season, which bodes well for the third quarter."

9) From Target: "we saw clear indications of progress in our business in the second quarter as traffic and comp trends improved meaningfully from Q1, particularly in our stores...And to be clear, while we were happy to see improvement in Q2, we are far from satisfied with where our business is performing today." Also, "While a lot of the season is still ahead of us, both back-to-school and back-to-college are off to encouraging starts. Guests are responding to our value offerings."

10) From TJX: "Overall, comp sales for the second quarter exceeded our expectations, increasing 4% and were strong across all of our divisions. Customer transactions were up at every division and drove our overall comp sales increase…As we have seen through so many retail and economic environments, consumers were drawn to our excellent values and brands. And going forward, we continue to see market share opportunities across each of our US and international divisions."

11) From Home Depot: "Big ticket comp transactions, or those over $1,000, were positive 2.6% compared to the second quarter of last year. We were pleased with the performance we saw in categories such building materials, lumber, and hardware.”

12) From Toll Brothers: "While affordability pressures and uncertain economic conditions persist, we are pleased with the resilience of our luxury business and more affluent customer base. In this environment, we continue to focus on strategically balancing price and pace in order to maximize profitability and returns."

13) From Workday: They pushed back on AI disrupting the SaaS model. "The interesting thing you hear out there is we hear that AI is eating the software world and unless something has changed from yesterday, I think AI is software and we're leaning heavily into it."

14) From Palo Alto Network: "During Q4, many of the deals our teams had been working on during our fiscal year came to fruition. We saw robust activity across the board. In Q4, our bookings growth turned a corner and was the highest we've seen in 2.5 years. This growth is driven by deals across our platforms and also as a result of strong renewals and upsells across our existing portfolio…Demand for cybersecurity remains strong. Our customers are looking to us to help them secure their cloud and AI transformation journeys. We continue to see GenAI conversations as it becomes imperative for our customers to deploy productivity tools, coding tools, or revamp their customer systems to enable natural language conversations. All these use cases for AI need to be protected."

15) From Viking Holdings: "In terms of the overall booking environment, we are seeing sustained strength in demand; 96% of the 2025 capacity for our core products is already booked, effectively selling out this year. As such, our attention remains on 2026 bookings, where we're seeing a very strong start. As of August 10, 55% of the capacity of our core products for the 2026 season was already sold, which is in line with our book position at the same point last year and at higher rates."

16) Japan's August composite PMI index was up a touch at 51.9 vs 51.6 but the components were mixed with manufacturing up 1 pt to 49.9 while services slipped to 52.7 from 53.6, though still above 50 and resulting in growth. S&P Global said "that growth momentum picked up across the private sector in August, with output rising at the fastest rate in six months. Encouragingly, the upturn was broad based, with a fresh rise in factory production accompanying a further strong increase in services activity."

17) Australia saw a rise in both its manufacturing and services August indices with both holding above 50. S&P Global said, "While domestic factors, including the easing of interest rates, supported better conditions in August, the renewed rise in export business suggested that external conditions have also started to pick up."

18) India continues to see broad strength with manufacturing rising to 59.8 from 59.1 and services at 65.6, up from 60.5 in July.

19) The August Eurozone composite index saw a gain to 51.1 from 50.9 with manufacturing getting back above 50 at 50.5 from 49.8 while services slipped a touch to 50.7 from 51. S&P Global said, "Overall, we've seen a slight acceleration in growth over the past three months. Despite headwinds like US tariffs and general uncertainty, businesses across the Eurozone seem to be coping reasonably well. The EU Single Market is likely playing a helpful role here, especially since most export and tourism revenues are generated within the EU."

20) The Reserve Bank of New Zealand and the Indonesian central bank each cut interest rates to 3% and 5% respectively. The former was expected while the latter was not. The Swedish Riksbank held steady with its 2% policy rate, the same rate that the ECB has.

Negatives,

1) Initial jobless claims rose 11k w/o/w to 235k and that was 10k above expectations. That shifts the 4 week average up to 226k from 222k. Continuing claims at 1.972mm is back to a cycle high and the most since November 2021 and up from 1.942mm in the week before.

2) Comments in the US PMI from S&P Global: “Tariffs were reported as the key driver of further cost increases in August. Companies across both manufacturing and service sectors collectively reported the steepest rise in input prices since May and the second-largest increase since January 2023. Rates of increase accelerated in both sectors. While the manufacturing cost rise was especially large, being the second-steepest since August 2022, the service sector increase was the second-highest since June 2023. Average prices charged for goods and services rose at the sharpest rate since August 2022 as firms passed higher costs on to customers. Although goods price inflation cooled slightly for a second month in a row, it remained among the highest seen over the past three years. Service sector price inflation meanwhile was the sharpest since August 2022.”

3) The Philly index was about dead flat at -.3, down from +15.9 in July and below the estimate of +6.5. Of note on inflation, prices paid rose 8 pts to 66.8 and that is the highest since May 2022. Prices received were up 1.3 pts m/o/m to 36.1 and 2 pts above the six month average. The Philly Fed did ask a special question on inflation as “firms were asked to forecast the changes in prices of their own products and for US consumers over the next four quarters. Regarding their own prices over the next year, the firms’ median forecast was for an expected increase of 4.1%, up from 38.5 when this question was last asked in May.”

4) The July Architecture Billings Index fell to 46.2 from 46.8 with 50 being the breakeven. While there was improvement in the 'commercial/industrial' sector, likely helped by data centers and healthcare, declines were seen in 'institutional', 'mixed practice' and 'multi family' residential. The AIA chief economist said, "Business conditions remain challenging for architecture firms nationwide, with billings declining across all regions in July. Client inquiries into new projects continue to build. Still, while commercial and industrial sectors show some signs of stability, the multifamily residential sector still is facing significant headwinds."

5) For the week ended August 15th and with little w/o/w change in mortgage rates after the recent modest drop, purchase applications were flat while refi's fell 3.1% after last week's 23% pop higher.

6) While multi family starts saw a lift, permits for new apartment buildings fell to a 4 month low to 484k, down 43k m/o/m and vs 495k in May with the biggest declines seen in the South and West, exactly where most of the supply has come on line this year. Single family permits were little changed, up 4k after dropping by 33k in June.

7) The August NAHB home builder sentiment index fell 1 point m/o/m to 32 vs the estimate of a 2 point lift. That matches the lowest print since December 2022 and remains well below 50. The Present Situation was down 1 point to 35 while Future Expectations were unchanged at 43, thus closer to 50 on likely hopes that Fed rate cuts could ease the financing burden for buyers. As for Prospective Buyers Traffic, it remained depressed but a bit less at 22, up 2 points m/o/m. From the NAHB, “Elevated mortgage rates, weak buyer traffic and ongoing supply-side challenges continued to act as a drag on building confidence in August, as sentiment levels remain in a holding pattern at a low level.” And what has been the biggest problem in the housing market, “Affordability continues to be the top challenge.” On the supply side, there are still issues too, “Builders are also grappling with supply side headwinds, including ongoing frustrations with regulatory policies connected to developing land and building homes.”

8) The August NY services index was -11.7 vs -9.3 in July.

9) From Walmart: Operating income was up just .4% in constant currency. "This is below what we expected going into the quarter, as we absorbed a headwind of 560 bps for the expenses related to general liability claims in the US." More on this, "This expense pertains to general liability and workers' compensation claims for which we self-insure. While this claim count has decreased y/o/y, the cost to resolve claims has risen, both for us and across the retail industry, and we've increased our accrual to reflect these trends." Also, "As it relates to what we're experiencing with customers and members here in the US, their behavior has been generally consistent. We aren't seeing dramatic shifts. The way things have played out so far, the impact of tariffs has been gradual enough that any behavioral adjustments by the customer have been somewhat muted. But as we replenish inventory at post-tariff price levels, we've continued to see our costs increase each week, which we expect will continue into the third and fourth quarters."

10) From Home Depot: “we continue to see softer engagement in larger discretionary projects where customers typically use financing to fund the renovation project."

11) From La-Z-Boy: Retail comps fell 4% "as lower traffic and consumer demand was partially offset by higher average ticket and design sales."

12) From Workday: Most of their business was strong but they did see weakness in state and local and education business. "On state and local, we did see a little bit of headwind in that market. And I think we'll continue to see that as people are trying to figure out what the funding flow down is going to look like all the way to the state level. On the higher ed side, it's really interesting because higher ed is clearly under pressure, they've lost some federal funding. And if it's a higher ed university that includes a healthcare system, they too are getting a little pullback in funding. So it's something we're keeping our eye on."

13) From Estee Lauder: "While there are early signs of stabilization in mainland China, travel retail conversion continues to be weak and challenges persist in the West, including subdued consumer sentiment in the US and Western Europe." Tariffs are a problem, "Based on current information and net of planned mitigation actions, the Company expects tariff related headwinds to impact fiscal 2026 profitability by approximately $100 million. The company continues to evaluate additional strategies, including further PRGP (profit recovery growth program) initiatives and potential pricing actions."

14) From Coty: "The US, our largest individual market at nearly a quarter of sales, was a major headwind in fiscal year '25 and the top driver for our underperformance. While we've consistently gained share in prestige across most regions, we lost share in the US in both prestige and mass…Our analysis of cosmetics category weakness points to value seeking behavior, some fatigue with innovation as consumers circle back to basics and less frequent usage, particularly with Gen Z migrating to fragrances. US specific factors, like in-store and anti-theft measures, and immigration policy changes, have also contributed to the slowdown."

15) From James Hardie: "Presently, demand in both repair and remodel and new construction in North America are challenging. Uncertainty is a common thread throughout conversations with customer and contractor partners. Homeowners are deferring large ticket remodeling projects like re-siding. And affordability remains the key impediment to improvement in single family new construction, where most recently, homebuilders are moderating their demand expectations and slowing starts to align their home inventory with a decelerating pace of traffic and sales."

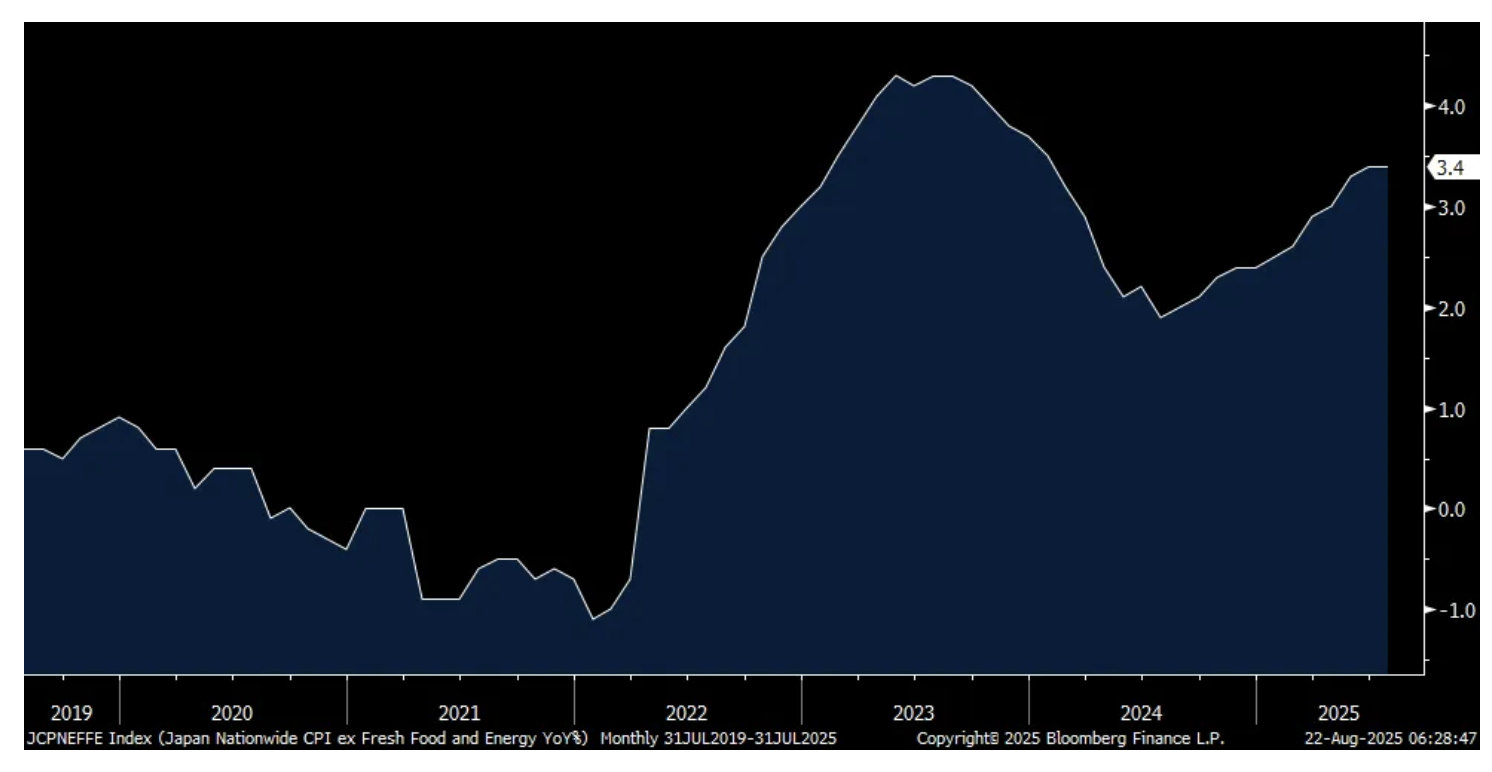

16) Core/core CPI in July for Japan rose 3.4% y/o/y, holding well above their 2% target as they sit there with a .50% overnight rate. While as expected, it's the quickest rate since January 2024 and above 3% for a 4th month.

17) Japanese exports fell 2.6% y/o/y in July, about as expected but with still the tariff challenges. Export declines were seen in autos, auto parts and steel in particular.

18) In the August Eurozone PMI, "Inflationary pressures picked up in August, with both input costs and output prices increasing at faster rates than in July. Input prices rose sharply, and at the steepest pace in five months...The pass through of higher input costs to customers meant that output prices increased again in August. The pace of inflation quickened fractionally and was the fastest in four months."

19) The UK PMI was mixed with manufacturing falling to 47.3 from 48, offset by an almost 2 pt rise in services to 53.6. S&P Global said "It's evident from survey measures of order books, however, that the demand environment remains both uneven and fragile. Companies report concerns over the impact of recent government policy changes, as well as unease emanating from broader geopolitical uncertainty. Goods exports are still falling especially sharply." On cost inflation, "August data also indicated a sharp and accelerated rise in average cost burdens across the private sector economy. The rate of input price inflation was the highest since May, reflecting stronger cost pressures in both the manufacturing and service sectors. Survey respondents once again noted that suppliers had sought to pass on rising National Insurance payments. Some firms also commented on higher food prices and transportation bills. Higher freight costs were partly linked to longer shipping times for items sourced from Asia." On the price pass through, "Prices charged by UK private sector companies increased at a robust pace in August. Service providers signaled the fastest pace of output charge inflation for three months. However, manufacturers indicated the slowest rise in factory gate prices since January, which was attributed to subdued demand and intense competition."

20) Headline CPI in the UK in July rose 3.8% y/o/y both headline and core and both one tenth above expectations. Service price inflation was 5%. The ONS said this was NOT due to greater hotel room demand because of the Oasis concert shows but higher prices for restaurants and hotels were a factor in CPI, along with transportation and food/beverage. Air fares spiked by 30% m/o/m but likely a timing issue around the holiday calendar.

BY Doug Kass · Aug 22, 2025, 2:45 PM EDT

As of 2:15 p.m.:

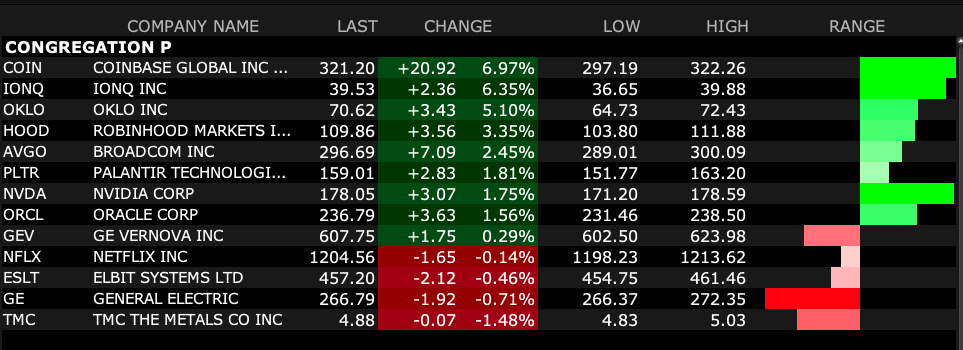

Congregation P

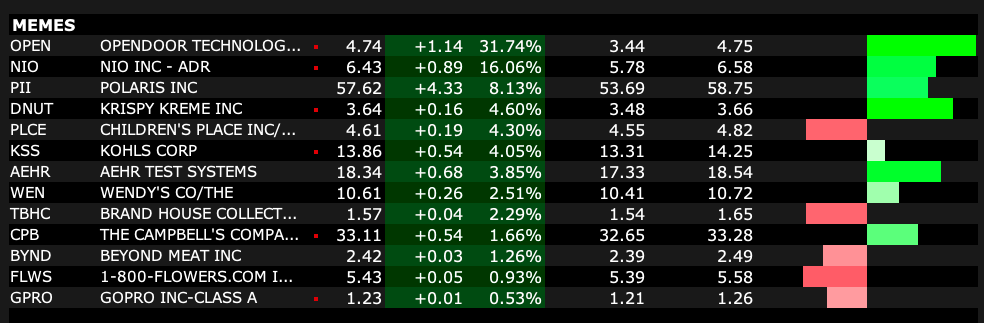

Memes

BY Doug Kass · Aug 22, 2025, 2:25 PM EDT

I shorted more AAPL at $228.05

BY Doug Kass · Aug 22, 2025, 2:09 PM EDT

* GS $753.02

* JPM $296.68

BY Doug Kass · Aug 22, 2025, 2:02 PM EDT

"Powell Makes Room for Rate Cut. Fed Kills 'Average Inflation' Targeting that Caused so Much Damage when Inflation Raged," Wolf Street

BY Doug Kass · Aug 22, 2025, 1:52 PM EDT

From Charlie!

"Put These Charts on Your Wall (2025 Edition)," Charlie Bilello's Blog

BY Doug Kass · Aug 22, 2025, 1:30 PM EDT

Kohlberg Kravis KKR $142.65

Blackstone BX $171.69

BY Doug Kass · Aug 22, 2025, 1:13 PM EDT

BY Doug Kass · Aug 22, 2025, 12:30 PM EDT

Here are today's things:

* I reestablished my SPY $644.22 (average) and QQQ $571.71 (average) shorts

* Added to NVDA $178.39 and AAPL $227.51 shorts

* Shorted more GRNY $23.41

* Added to MSOS long at $4.92

BY Doug Kass · Aug 22, 2025, 12:15 PM EDT

Wolf Street howls about housing inventory for sale:

BY Doug Kass · Aug 22, 2025, 12:00 PM EDT

I have moved to medium-sized short in the indices.

S&P cash is now +104 handles:

* SPY $645.95

* QQQ $573.49

BY Doug Kass · Aug 22, 2025, 11:43 AM EDT

BY Doug Kass · Aug 22, 2025, 11:30 AM EDT

Adding to GRNY short at $23.53.

BY Doug Kass · Aug 22, 2025, 11:13 AM EDT

September Almanac, Vital Stats & Strategy Calendar: Bearish Bias Last 75 Years

Portfolio managers back after Labor Day have tended to clean house in September. Since 1950, September has been the worst performing month of the year for DJIA, S&P 500, NASDAQ (since 1971), Russell 1000 and Russell 2000 (since 1979). September was creamed four years straight from 1999-2002 after four solid years from 1995-1998 during the dot.com madness. More recently, DJIA, S&P 500, NASDAQ, Russell 1000 and 2000 have been down seven of the last eleven Septembers and four of the last five. Average losses over the last eleven years range from –1.2% by DJIA to –2.4% from NASDAQ and Russell 2000.

I recommend the entire post: https://www.stocktradersalmanac.com/Alert/20250821_1.aspx

BY Doug Kass · Aug 22, 2025, 11:00 AM EDT

As of 10:42 a.m.:

- NYSE volume 11% above its one-month average;

- NASDAQ volume 5% above its one-month average;

- VIX index: down 11.39% to 14.71

Breadth

Sectors

% Movers

BY Doug Kass · Aug 22, 2025, 10:53 AM EDT

From Peter Boockvar:

This was all Jay Powell needed to say to clinch a September rate cut, “with policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance.” This was just a few sentences after saying this in his, ”In the near term, risks to inflation are tilted to the upside, and risks to employment to the downside—a challenging situation. When our goals are in tension like this, our framework calls for us to balance both sides of our dual mandate.”

And why is he shifting more to the softer labor side vs the tariff risks on inflation? “Overall, while the labor market appears to be in balance, it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers. This unusual situation suggests that downside risks to employment are rising. And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.”

And on tariffs and their influence on inflation, “The effects of tariffs on consumer prices are now clearly visible.” And, “A reasonable base case is that the effects will be relatively short lived—a one-time shift in the price level.” With the caveat though, that “Of course, "one-time" does not mean "all at once." It will continue to take time for tariff increases to work their way through supply chains and distribution networks. Moreover, tariff rates continue to evolve, potentially prolonging the adjustment process.”

And with this risk too, “It is also possible, however, that the upward pressure on prices from tariffs could spur a more lasting inflation dynamic, and that is a risk to be assessed and managed. One possibility is that workers, who see their real incomes decline because of higher prices, demand and get higher wages from employers, setting off adverse wage–price dynamics.”

But, “Given that the labor market is not particularly tight and faces increasing downside risks, that outcome does not seem likely.”

And after all that said, “Of course, we cannot take the stability of inflation expectations for granted. Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem.”

Bottom line, today’s speech could not be more clear that Powell is ready to cut rates on September 17th and the market is now fully priced for it and for a 2nd one by year end. As for one cut at each of the following three meetings. The market is not there yet but at least has priced in a small chance of 12%.

The 2 yr yield fell 8 bps in response to the dovish speech while the 10 yr yield is lower by 5 bps and the 30 yr yield by a more modest 3 bps.

BY Doug Kass · Aug 22, 2025, 10:40 AM EDT

With S&P cash +92 handles:

SPY $644.95

QQQ $572.74

Scaling on strength, will likely move to medium sized.

BY Doug Kass · Aug 22, 2025, 10:39 AM EDT

- Possible that tariffs can spur lasting inflation

- Won’t allow one-time increase to become ongoing problem

-Short-lived tariff price effects a reasonable base case

- Fed faces ‘a challenging situation’

- Shifting balance of risks may warrant adjusting policy

- New framework removes low-rates language, returns to flexible inflation targeting

- Labor-market stability allows us to proceed carefully

BY Doug Kass · Aug 22, 2025, 10:26 AM EDT

Moved to small-sized (from very small) in the indexes:

Additional shorts with S&P cash + 95 handles :

* SPY $644.72

* QQQ $572.74

BY Doug Kass · Aug 22, 2025, 10:24 AM EDT

I am bidding for more consumer staples - PEP PG and KO.

BY Doug Kass · Aug 22, 2025, 10:20 AM EDT

Scaling higher.

SPY $642.67

QQQ $569.53

BY Doug Kass · Aug 22, 2025, 10:15 AM EDT

Back shorting indexes on the ramp higher:

* SPY $639.25

* QQQ $565.99

BY Doug Kass · Aug 22, 2025, 10:03 AM EDT

From Peter Boockvar

It was only about 3 weeks ago since we last heard from Jay Powell and his message was that he was essentially in 'wait and see' mode and since then we got a 3.1% core CPI print for July, a very hot PPI (more than just the higher price of portfolio mgmt fees with core goods up 3.6% at annualized rate this year) and a soft payroll report. With more jobs and inflation data to see before the September meeting, maybe today he just remains in a 'wait and see' type stance.

Or maybe he expresses his bigger worry remains inflation and less so the labor market. Yesterday, the Atlanta Fed released a paper titled "Will Tariffs Touch Off an Inflationary Impulse? Business Execs Think So." I guess this is why non-voting member Raphael Bostic only wants one cut through the remainder of the year. https://www.atlantafed.org/research/publications/policy-hub/2025/08/21/04-will-tariffs-touch-off-inflationary-impulse-business-execs-think-so

The conclusion of the paper, "We find evidence for the potential of tariffs to touch off another bout of high inflation. First, firms that are directly exposed to tariffs have increased their year-ahead price growth expectations sharply (by .7 percentage points). Second, firms that are not directly exposed to tariffs but are operating in industries that are highly exposed to tariffs anticipate a moderately higher trajectory for year-ahead price growth (.3 percentage points). Third, this broadening of overall price pressures - a key feature of the pandemic era inflationary impulse - is only partially offset by lower price increases from tariff-exposed firms that are operating largely in industries not exposed to tariffs."

"In sum, these results suggest that the possibility of seemingly one-time tariff-related price increases becoming a full fledged inflationary impulse - like the episode we lived through just a few years ago - is elevated."

Agree with this or not, the paper is now out there in Federal Reserve land.

One last thing, this line in the FOMC minutes continues to stick out to me. “Several participants noted concerns about elevated asset valuation pressures.” My bold. The argument by those saying that current monetary policy is restrictive are not including the easy financial conditions we currently have in the discussion as evidenced by drum tight credit spreads and expensive equity valuations that have only been seen a few times in history (but only matter when they do). If we had the reverse with wide spreads and depressed valuations, these same people would be calling for cuts to ease tight financial conditions.

Rate cut odds for the September meeting have slipped to 68% vs more than 90% a few weeks ago. Thru year end, odds of a cut are still 100% but down to 84% for a second vs two being fully priced in just recently.

Meanwhile, the BoJ continues to face pressures to again raise interest rates especially today after core/core CPI in July for Japan rose 3.4% y/o/y, holding well above their 2% target as they sit there with a .50% overnight rate. While as expected, it's the quickest rate since January 2024 and above 3% for a 4th month. JGB yields are higher across their curve in response with the 20 and 30 yr maturity yields rising to record highs. The 10 yr JGB yield at 1.625% is at the highest since July 2008. Something to continue to watch closely with regards to global long rates.

Japan CPI ex food/energy y/o/y

10 yr JGB Yield

From Walmart:

"Growth in transactions and units is helping drive our performance. We grew eCommerce sales by 25% globally." Walmart US and Sam's Club in particular saw 26% gains. "Customers are liking our faster delivery speed."

With Walmart US and whose comps grew 4.6% y/o/y, "Sales and general merchandise were positive in every segment and across categories in the US led by apparel, media and gaming, and automotive." They also gained market share.

However, operating income was up just .4% in constant currency. "This is below what we expected going into the quarter, as we absorbed a headwind of 560 bps for the expenses related to general liability claims in the US." More on this, "This expense pertains to general liability and workers' compensation claims for which we self-insure. While this claim count has decreased y/o/y, the cost to resolve claims has risen, both for us and across the retail industry, and we've increased our accrual to reflect these trends." We certainly live in a pretty litigious society.

"With regard to our US pricing decisions given tariff related cost pressures, we're doing what we said we would do. We're keeping our prices as low as we can for as long as we can."

"As it relates to what we're experiencing with customers and members here in the US, their behavior has been generally consistent. We aren't seeing dramatic shifts. The way things have played out so far, the impact of tariffs has been gradual enough that any behavioral adjustments by the customer have been somewhat muted. But as we replenish inventory at post-tariff price levels, we've continued to see our costs increase each week, which we expect will continue into the third and fourth quarters."

"Not surprisingly, we see more adjustments in middle and lower income households than we do with higher income households. In discretionary categories where item prices have gone up, we see a corresponding moderation in units at the item level as customers switch to other items or, in some cases, categories."

And more on the income breakdown driving the 4.6% Walmart US comp, it came "with upper income households contributing the largest gains...It think that's a response to some of the better brands that we're now offering, including private brands like Bettergoods."

"As always, our customers are aware, smart and value conscious. We have approximately 7,400 price rollbacks across our assortment, which is about 2,000 more than last quarter. Our rollback count in grocery was up 30% in the quarter compared to last year. Back-to-school is usually something of an indicator of how the holidays will go, and we feel good about how it went for us in terms of units and dollars sold and inventory sell-through at both Walmart and Sam's Club."

On Walmart's tariff exposure, "The US is by far our number one market for sourcing. For the less than a third of what we sell in the US that's imported, China, Mexico, Vietnam, India and Canada are our largest markets."

From Ross Stores, another value focused retailer and up 2% pre-market:

Comps grew 2% and "This improvement was broad based with a positive change in trend in nearly all major merchandise categories and most of the regions across the company. During the second quarter, sales in May were strong and softened in June before rebounding sharply in July. We were pleased to see the improved trend at the end of the quarter, particularly with the early sales performance related to the back-to-school selling season, which bodes well for the third quarter."

"In the second quarter, cosmetics was the best merchandise area. By geographic region, the strongest markets were the Southeast and the Midwest."

"While tariffs remain at elevated levels, we feel good about the progress the merchants have made to mitigate the impact on margin. The team has worked tirelessly to execute a multi-pronged approach, including vendor negotiations, diversifying our sourcing mix, and adjusting prices strategically. Additionally, we were able to expand the portion of our business, driven by closeouts, which further mitigated the impact."

"Looking ahead, we are confident that we can continue to offset most of the impact of tariffs, but we do anticipate modest pressure in the third quarter, which we expect will be further mitigated in the fourth quarter."

"From a pricing perspective, we are beginning to see higher prices across the retail industry. With this backdrop, we are focused on maintaining our value proposition relative to traditional retailers, while balancing the opportunity to preserve our merchandise margin...The off-price sector has historically benefited from disruptions within the supply chain and the retail industry. We believe this time will be no different."

From Workday and whose stock is down pre-market:

They pushed back on AI disrupting the SaaS model. "The interesting thing you hear out there is we hear that AI is eating the software world and unless something has changed from yesterday, I think AI is software and we're leaning heavily into it."

Most of their business was strong but they did see weakness in state and local and education business. "On state and local, we did see a little bit of headwind in that market. And I think we'll continue to see that as people are trying to figure out what the funding flow down is going to look like all the way to the state level. On the higher ed side, it's really interesting because higher ed is clearly under pressure, they've lost some federal funding. And if it's a higher ed university that includes a healthcare system, they too are getting a little pullback in funding. So it's something we're keeping our eye on."

Back overseas, there was no change in the August French consumer confidence index at 96, 1 pt below expectations and still below the February 2020 print of 106.

BY Doug Kass · Aug 22, 2025, 10:00 AM EDT

BY Doug Kass · Aug 22, 2025, 9:45 AM EDT

BY Doug Kass · Aug 22, 2025, 9:30 AM EDT

-IXHL +40% (authorizes $20M share repurchase program)

-BHVN +12% (affirms expected troriluzole NDA decision during 4Q25)

-UI +12% (earnings; announces share repurchase, raises dividend)

-ZM +4.4% (earnings, guidance)

-SBET +4.2% (authorizes $1.5B stock buyback program)

-BKE +4.0% (earnings)

-ZONE +3.4% (earnings)

-ROST +3.0% (earnings, guidance)

-ANTE -9.1% (files to sell $180M direct offering of 80.8M shares and warrants at $2.23/unit)

-INTU -6.3% (earnings, guidance)

-WDAY -4.7% (earnings, guidance)

-BJ -2.9% (earnings, guidance)

BY Doug Kass · Aug 22, 2025, 9:25 AM EDT

BY Doug Kass · Aug 22, 2025, 9:15 AM EDT

BY Doug Kass · Aug 22, 2025, 9:05 AM EDT

* 69% of SPX contracts were ODTE options (yesterday)...

From Hedgeye's lynx-eyed Keith McCullough:

BY Doug Kass · Aug 22, 2025, 8:55 AM EDT

cjsolus

9 hours ago

Nvidia Corp. has instructed component suppliers including Samsung Electronics Co. and Amkor Technology Inc. to stop production related to the H20 AI chip, the Information reported, citing unidentified sources.

Nvidia issued those orders after Beijing urged local companies to avoid using the H20, the Information said.

BY Doug Kass · Aug 22, 2025, 8:45 AM EDT

Maybe, if I pray every night

You'll come back to me

And maybe, if I cry every day

You'll come back to stay

Oh, maybe (maybe, maybe, maybe)

- The Chantels - Maybe (Dick Clark's Beech-Nut Show Ep #3 March 1st,1958)

The time was 1958. The song was believed to have been recorded in a Manhattan church.

"Maybe" (with virginity personified as an unwanted condition!) is one of my favorite songs of all time.

Lead singer Arlene Smith belts it out with so much energy and expression -- showing the world what the "girl sound" would become.

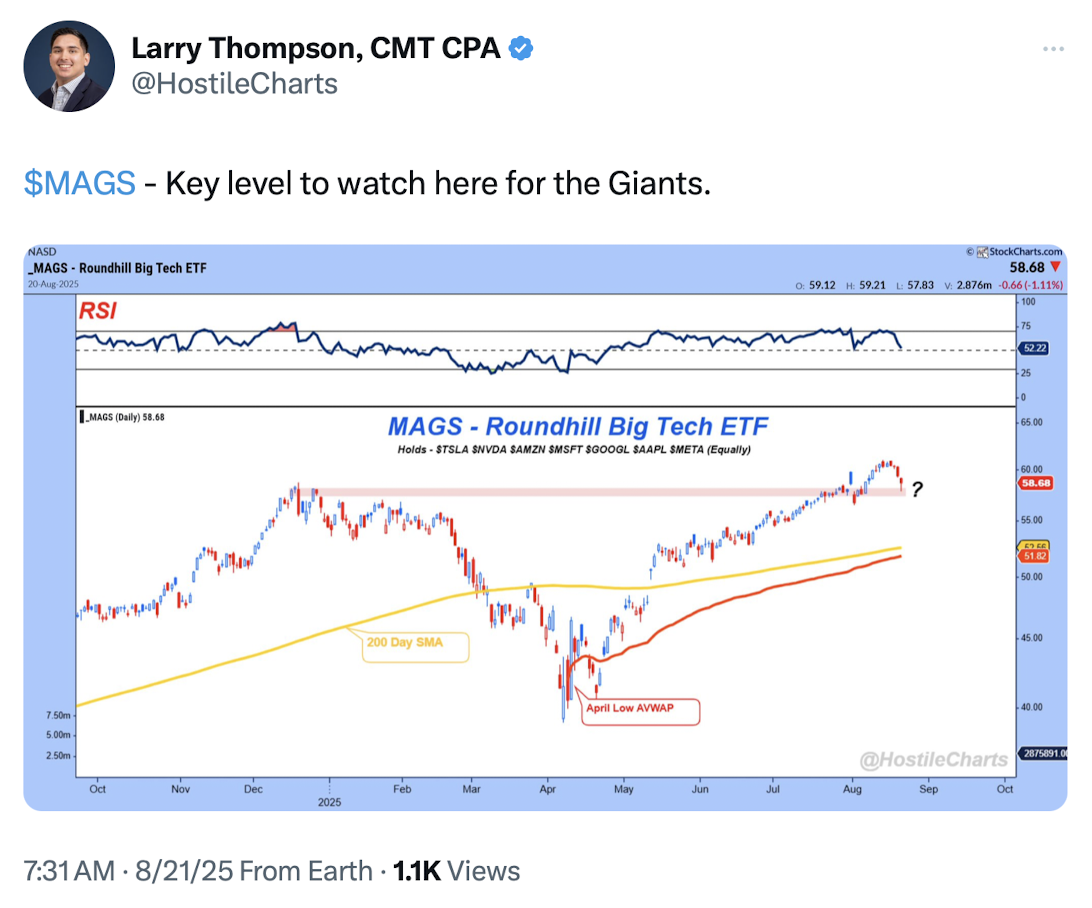

I spent quite a lot of time throwing a skeptical light with regard to AI and the Mag7 on Rosie's podcast yesterday afternoon.

The chart of (the MAG7) seems to be at a critical level:

BY Doug Kass · Aug 22, 2025, 8:35 AM EDT

Bonus - here are some great links:

The Only Two For Tech The Only Two For Tech

Thirty Stocks, One Voice Thirty Stocks, One Voice: Dow at New Highs - TrendLabs

Growth Stumbles, Value Steps Up Growth Stumbles, Value Steps Up 🔄

When Staples Lag, Bulls Rejoice When Staples Lag, Bulls PartyS and P, Bitcoin Latest StockCharts TV Video - by Frank Cappelleri

BY Doug Kass · Aug 22, 2025, 8:20 AM EDT

* There are now some 498 AI unicorns, or private AI companies, valued at $1 billion or more, with a combined value of $2.7 trillion...

* This week we shorted NVDA and PLTR

In yesterday's podcast with Rosie I spent some time on the pitfalls of speculation and the risks associated with AI (and, by inference, the growing vulnerability of MAG7).

The venture side of all the AI speculation is also interesting.

As much as anything else, these are just bets on public market flips in some way shape or form (including being acquired with overvalued paper), as opposed to underlying fundamentals.

Speculation on speculation, for lack of a better term.

Also, another blurb on the underlying dis-economics, and an interesting chart.

Palantir is a curious one too, because not sure how big a business that relies on the government for a lot of its revenue can grow, nor am I sure how the business model scales. But it is indicative of how equities are priced these days, and that pricing provides the umbrella for the venture speculators.

Consider these two factoids and we can clearly see how the bubble talk in AI will continue to resurface every now and then. This "private wealth" situation is much more extreme than in 2000:

1. There are now some 498 AI unicorns, or private AI companies, valued at $1 billion or more, with a combined value of $2.7 trillion, according to CB Insights.

2. How bad are AI startup unit economics? Here’s how the AI startup economy works right now: you, the user, pay an application-layer company $1. That company pays $5 to a foundation model provider, which then pays $7 to a hyperscaler, who finally pays $13 to a GPU maker.

Bloomberg's John Authers with an interesting chart:

Source: Bloomberg/Authers

BY Doug Kass · Aug 22, 2025, 7:30 AM EDT

Adding to AAPL short at $226.20.

Correction: I mistakenly told Rosie that I had no short position in this company in yesterday's podcast. That was incorrect as I have a very small short in this name. I plan to add on any strength.

BY Doug Kass · Aug 22, 2025, 7:21 AM EDT

The S&P Short Range Oscillator is at 1.98% vs. 2.27%.

I currently have no index positions.

BY Doug Kass · Aug 22, 2025, 7:15 AM EDT

BY Doug Kass · Aug 22, 2025, 7:06 AM EDT

BY Doug Kass · Aug 22, 2025, 6:50 AM EDT

BY Doug Kass · Aug 22, 2025, 6:35 AM EDT