Wednesday's After-Hours Movers

As of 4:20 p.m.:

BY Doug Kass · Aug 20, 2025, 4:45 PM EDT

As of 4:20 p.m.:

BY Doug Kass · Aug 20, 2025, 4:45 PM EDT

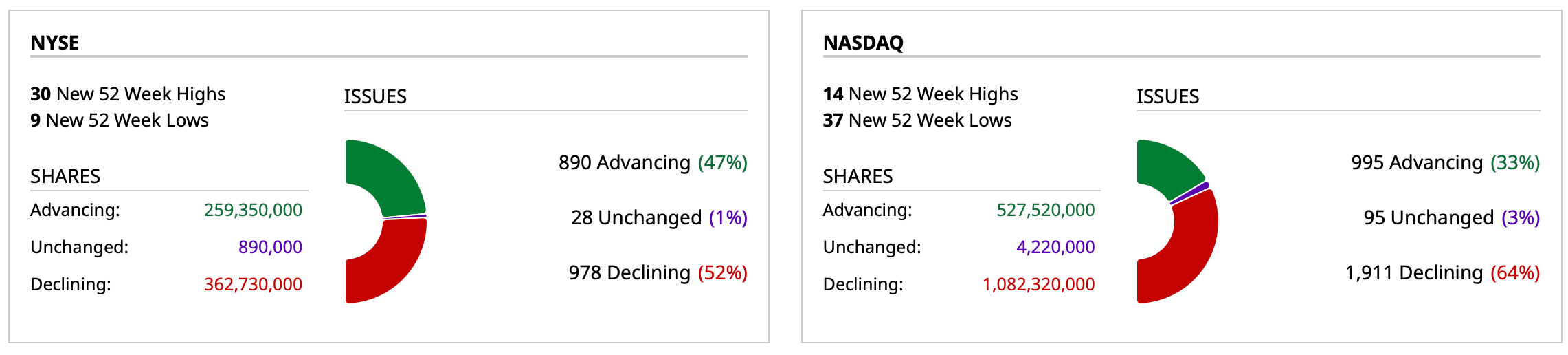

- NYSE volume 9% below its one-month average;

- NASDAQ volume 16% below its one-month average;

- VIX index: up 1.03% to 15.73

BY Doug Kass · Aug 20, 2025, 4:31 PM EDT

I'm back shorting GRNY at $23.13 and JOET at $41.25.

BY Doug Kass · Aug 20, 2025, 3:45 PM EDT

From Peter Boockvar:

'Several' and 'Many' are the key words in the FOMC minutes

‘Several’ and ‘many’ are two of the more important words when the FOMC releases its minutes, especially from their meeting three weeks ago because we know that speaks for the majority, whose word is sometimes used too.

Here were some of the noteworthy lines from the just released minutes that include those words:

In what could be the bottom line for the minutes in terms of how the Fed will be approaching their last three meeting of the year with current information in hand, but which will of course evolve over the next 4 months as new information comes in.

“Participants generally pointed to risks to both sides of the Committee's dual mandate, emphasizing upside risk to inflation and downside risk to employment. A majority of participants judged the upside risk to inflation as the greater of these two risks, while several participants viewed the two risks as roughly balanced, and a couple of participants considered downside risk to employment the more salient risk.”

This one stood out as it doesn’t point to a Fed wanting to goose this further, “Several participants noted concerns about elevated asset valuation pressures.”

“In terms of timing, many participants noted that it could take some time for the full effects of higher tariffs to be felt in consumer goods and services prices. Participants cited several contributors to this likely lag. These included the stockpiling of inventories in anticipation of higher tariffs; slow pass-through of input cost increases into final goods and services prices; gradual updating of contract prices; maintenance of firm–customer relationships; issues related to tariff collection; and still-ongoing trade negotiations.”

“Several participants, drawing on information provided by business contacts or business surveys, expected that many companies would increasingly have to pass through tariff costs to end-customers over time.”

“Several participants emphasized that inflation had exceeded 2 percent for an extended period and that this experience increased the risk of longer-term inflation expectations becoming unanchored in the event of drawn-out effects of higher tariffs on inflation.”

“Several participants noted that the low and stable unemployment rate reflected a combination of low hiring and low layoffs.”

“a number of participants noted that softness in aggregate demand and economic activity may translate into weaker labor market conditions, as could a potential inability of some importers to withstand higher tariffs.”

“Several participants stated that they expected growth in economic activity to remain low in the second half of this year.”

Bottom line, after hearing from some notable people on tv today talking about a 3% neutral rate that the Fed should be quickly heading towards, I need to remind them and others that a 3% Fed declared neutral rate assumes the rate of inflation is sustainably at 2%, thus giving us a 1% REAL rate. We of course are not at 2%, let alone sustainably. A 1% current real rate would imply a current fed funds rate of 3.75-4%, not far off from where we are now with core PCE and CPI running between 2.7-3.1%.

As for these minutes, while we’ll get a cut next month, it will be of the more hawkish kind with the late October meeting undertaking a fresh view of the data then seen, rather than a committee making any multi meeting declarations right now, outside of a few of its members.

Treasury yields while still down on the day did lift off their lows in response.

BY Doug Kass · Aug 20, 2025, 2:50 PM EDT

BY Doug Kass · Aug 20, 2025, 2:40 PM EDT

Interesting article here on inflation, focusing primarily on the monetary side:

My comments and questions:

* Even though interest rates are not low, financial conditions by many measures remain very easy/accommodative. The growth in money supply, for example.

* If the theoretical intent is to let things run hot, how can the Fed be allowed to set (raise) the inflation target on their own? This effectively makes the Fed more powerful than the Executive Branch. For those that like it now, ask yourself if you would like what was going on if the other political party was in office. This fails the shoe on the other foot test. Also think about where this ultimately leads.

* What is the point of lowering taxes, if you effectively increase them on nearly everyone, in the most insidious way possible? Since when has inflation solved anything for any economy? Again, I ask for those that like this, ask yourself if you would like it if the other political party was in office?

* To the degree the housing market is an issue, price is one of the things limiting affordability and turnover, it is not just rates. They are inter-related. Because rates were too low for too long, prices were driven up to an un-natural point (just like it was for other assets too). Lowering rates to solve for this problem is akin to giving a drug addict more drugs. It is a circular doom loop. Driving up un-naturally high prices also certainly does not solve for the affordability problem. A giant mess has been created by easy money for too long. It seems to be an almost unsolvable problem now.

If we want to try and grow our way out of the mess, fine, do it the old-fashioned way, but not with monetary gimmicks. Set the right incentives with policy and curtail all the crazy spending. If that causes a little pain, so be it. But in this regard, the excess in the financial markets is now also a problem. They have a very circular relationship with the economy more than at any point in the past. A monetary response to this issue, should it arise again, also is a complex problem which will continue to have greater consequences and will once again make a small portion of the population relatively much wealthier and everyone else relatively much poorer, while also continuing to distort the economy and push money into more diseconomic and speculative places.

It is quite a pickle we have made for ourselves. I do not have all the answers, but I would have started on the spending side, a long time ago too. Spending is the most straightforward of all issues and getting that under control leaves a fair bit of leeway to deal with other things.

BY Doug Kass · Aug 20, 2025, 2:22 PM EDT

I'm adding to WMT short at $102.36.

BY Doug Kass · Aug 20, 2025, 1:17 PM EDT

Dougie Kass

I have written 107 MORE TALES FROM NVIDIA

I have published these for a reason = to discuss the risks few are mentioning.

Many here and elsewhere have objected to my critical take in such a leadership sector.

They have observed the strong stock performance and equated it to commericial success.

People are finally coming around to the risks, which are real.

See next post.

BY Doug Kass · Aug 20, 2025, 12:50 PM EDT

BY Doug Kass · Aug 20, 2025, 12:35 PM EDT

From Kuppy:

Global Crossing Is Reborn... - Praetorian Capital

My response to his great column....

Kuppy glossed over one important point.

Although companies will find value to some of AI, they would find no value to any of it if they were forced to pay a price that would enable the system (service and infrastructure providers) to earn a return.

So the situation is far worse than he lays out.

BY Doug Kass · Aug 20, 2025, 12:20 PM EDT

BY Doug Kass · Aug 20, 2025, 12:05 PM EDT

Wally Deemer responds to my Top Tick missive this morning:

Speaking of "Arrogance": from March 2000 --

Market Strategies and Insights: Current Weekly Report (Substitute NVIDIA for Cisco and Occidental Pete for Sears...)

Your old pal,

Wally

BY Doug Kass · Aug 20, 2025, 11:35 AM EDT

Dougie Kass

Long MSOS ($4.40 average) as I now believe the Administration will likely recommend rescheduling.

I dont know the timing - but I suspect it could be short term.

I conclude this based on:

More to come later.

BY Doug Kass · Aug 20, 2025, 11:25 AM EDT

* MIT report: 95% of generative AI pilots at companies are failing

Well it seems the entire use case for generative artificial intelligence is for kids to cheat on their homework, fail corporate pilots (which the author and researcher tries to put a positive spin on, but really it is just failing) and doing things like writing poor code. The code, by the way, requires substantial debugging efforts on the other side, neutralizing the benefit, and being a net money loser on a full system basis. This is especially true when considering the full cost of using the Gen AI to write code to begin with if you consider the losses of the service and infrastructure providers like CRWV. The other funny thing is it's being used to write job applications, so everyone has the same application now that they send to 2,000 places at the same time, which is then screened by AI, so you have the AI interviewing the AI, which is a circular doom loop. But on the positive side you can make some funny memes with it.

The GenAI Divide: State of AI in Business 2025, a new report published by MIT’s NANDA initiative, reveals that while generative AI holds promise for enterprises, most initiatives to drive rapid revenue growth are falling flat. Despite the rush to integrate powerful new models, about 5% of AI pilot programs achieve rapid revenue acceleration; the vast majority stall, delivering little to no measurable impact on P&L… for 95% of companies in the dataset, generative AI implementation is falling short…

BY Doug Kass · Aug 20, 2025, 11:03 AM EDT

I am long KO, PEP and PG.

For some time I was short consumer non durables... but no more!

BY Doug Kass · Aug 20, 2025, 10:11 AM EDT

11 a.m.: Fed Board Governor Waller (Voter) speaks on "Payments" before the Wyoming Blockchain Symposium 2025;

1 p.m.: Fed Bank of Atlanta President Bostic (Non-Voter) discusses the economic outlook in a moderated conversation beforethe Fintech South 2025 event (Atlanta, GA; No audience Q&A, no media Q&A, no embargoed text, Livestream

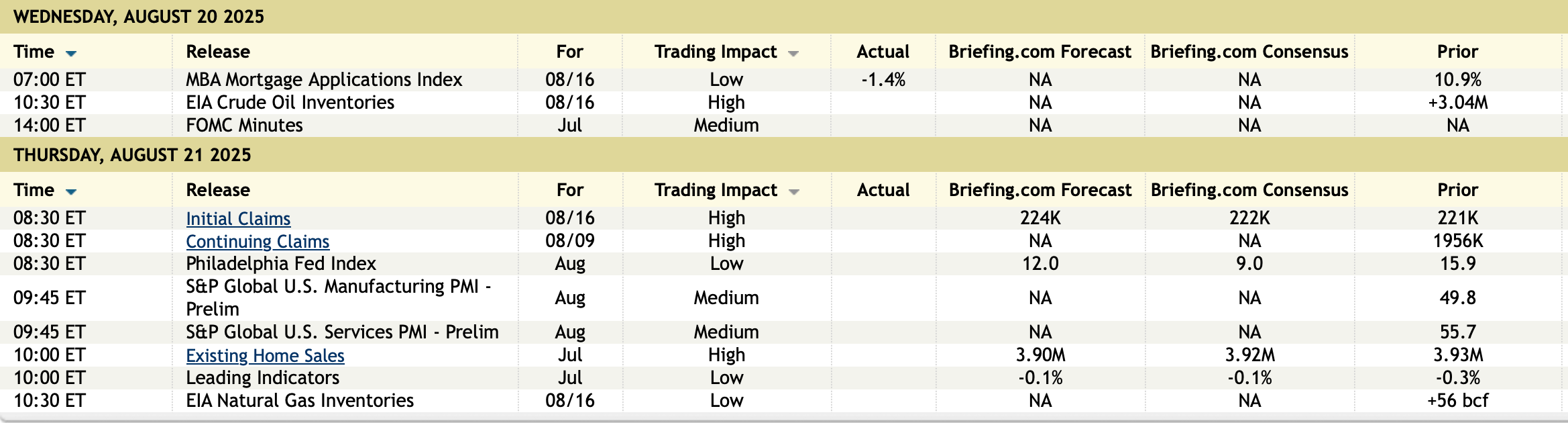

ECONOMIC CALENDAR FOR THE WEEK

BY Doug Kass · Aug 20, 2025, 9:52 AM EDT

BY Doug Kass · Aug 20, 2025, 9:21 AM EDT

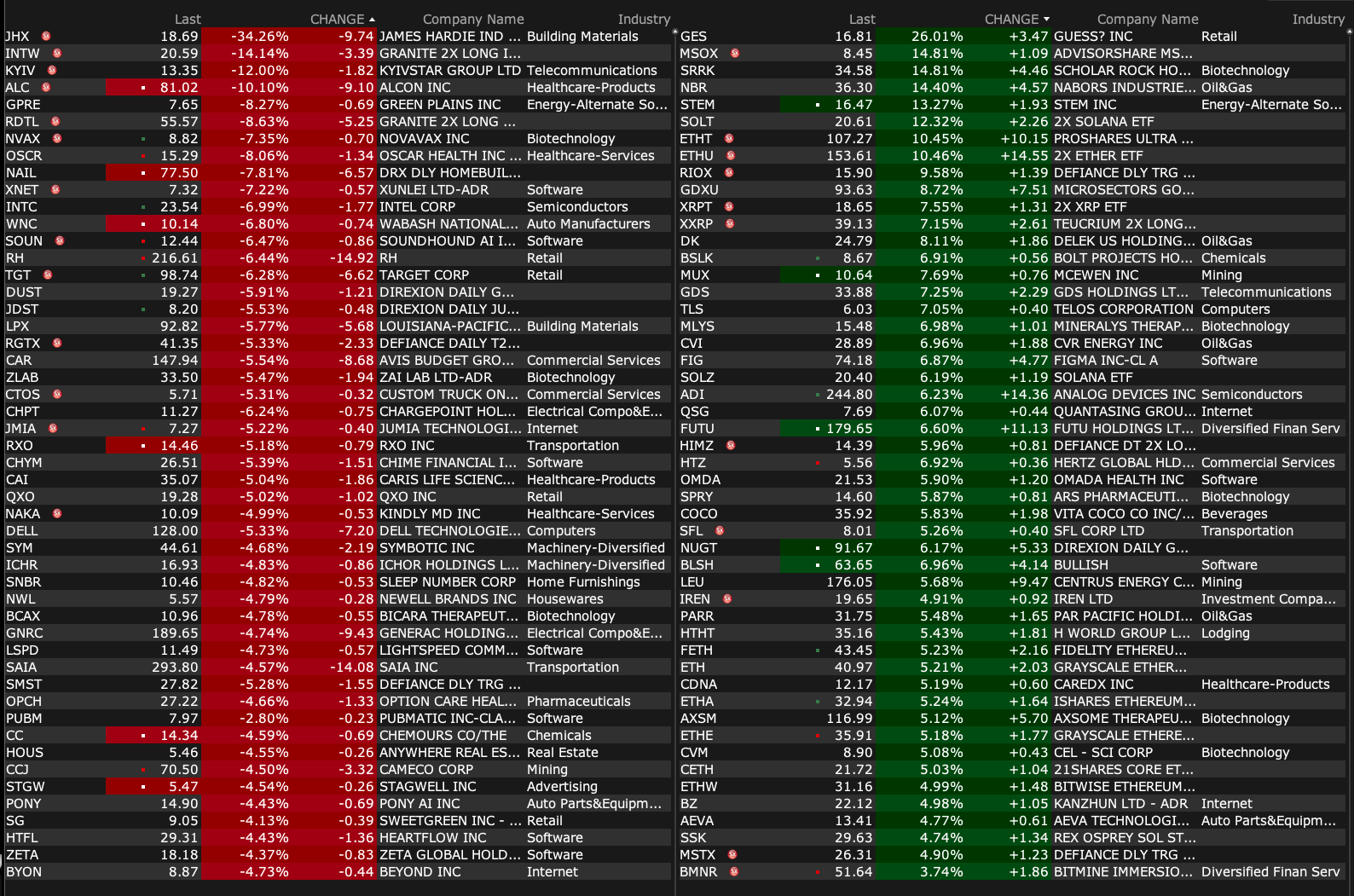

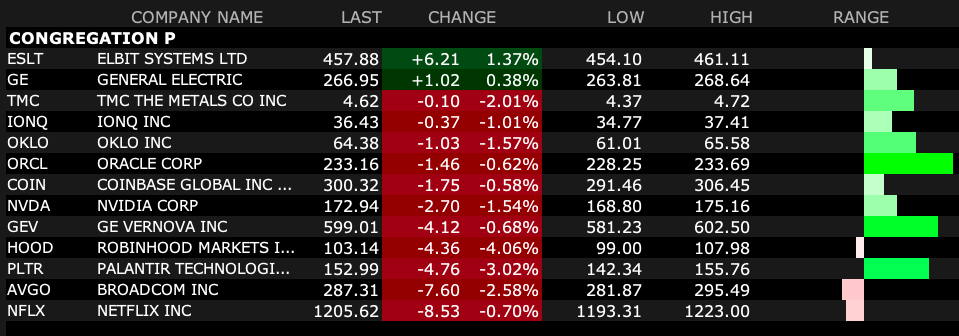

-TIVC +26% (receives IND transfers for Entolimod to advance ARS and cancer programs)

-GES +24% (Co-Founders and Authentic Brands to take company private at $16.75/shr cash for deal value ~$871M)

-RCKT +21% (US FDA lifts clinical hold on Pivotal Phase 2 Trial of RP-A501 for Treatment of Danon Disease)

-FLNT +9.2% (earnings)

-HTZ +8.5% (to sell used vehicles online through Amazon Autos partnership)

-TJX +3.8% (earnings, guidance)

-FUTU +3.7% (earnings)

-ADI +3.3% (earnings, guidance)

-DAY +3.2% (confirms Thoma Bravo takeover discussions)

-LOW +2.9% (earnings, guidance)

-SNOW +2.6% (Tier1 firm Raised SNOW to Buy from Neutral, price target: $240 from $220)

-LZB -21% (earnings, guidance)

-TGT -11% (earnings, guidance; announces CEO change)

-DY -9.1% (earnings, guidance)

-EL -8.6% (earnings, guidance)

-ZIM -5.8% (earnings, guidance)

-MU -5.0% (reportedly Trump Administration considers equity stakes in chip manufacturing companies including Micron)

-CTOS -4.6% (JPMorgan Chase and Co Cuts CTOS to Underweight from Neutral, price target: $5.50)

-CVNA -3.3% (used car retailer weakness following Hertz announcement to sell used vehicles online through Amazon Autos partnership)

-PLTR -3.0% (downside momentum)

BY Doug Kass · Aug 20, 2025, 9:15 AM EDT

BY Doug Kass · Aug 20, 2025, 9:08 AM EDT

From Peter Boockvar:

While Home Depot was a key earnings and housing focus yesterday, along with the housing starts data, I'm going to start with James Hardie, the maker of residential new construction and remodeling products like siding, trim, soffits, PVC decking, railing products, etc... The stock is down 26% pre market and they said this on their earnings calls:

"Presently, demand in both repair and remodel and new construction in North America are challenging. Uncertainty is a common thread throughout conversations with customer and contractor partners. Homeowners are deferring large ticket remodeling projects like re-siding. And affordability remains the key impediment to improvement in single family new construction, where most recently, homebuilders are moderating their demand expectations and slowing starts to align their home inventory with a decelerating pace of traffic and sales."

"In May, we built into our full year guidance an assumption that end market demand could decline by approximately mid-single digits, driven by expectations for further decline in repair and remodel. Over the course of the summer, single family new construction activity has been weaker than anticipated, and we have adjusted our expectations to account for softer demand."

"Furthermore, we believe it is prudent to plan for more cautious order patterns and defensive inventory positioning at our channel partners, exacerbated by the slower seasonality of new construction into the back half of the calendar year."

This is what Home Depot said of note:

"During the second quarter, our comp average ticket increased 1.4%, and comp transactions decreased .4%. The growth in our comp average ticket primarily reflects a greater mix of higher ticket items, inflation from core commodity categories, including lumber and copper, and modest decrease in promotional activity relative to prior years."

"Big ticket comp transactions, or those over $1,000, were positive 2.6% compared to the second quarter of last year. We were pleased with the performance we saw in categories such building materials, lumber, and hardware. However, we continue to see softer engagement in larger discretionary projects where customers typically use financing to fund the renovation project."

"When we talk generally to our customers, each of our sets of consumers and Pros, the number one reason for deferring the large project is general economic uncertainty. That is larger than prices of projects, of labor availability, all the various things we've talked about in the past. By a wide margin, economic uncertainty is number one." I bolded to highlight.

On the furniture side, La-Z-Boy is down 25% pre market after missing numbers. They said this:

They mentioned that investments "to grow our retail store footprint and expand brand reach, combined with soft industry demand, had a downward impact on our margin performance this quarter."

Retail comps fell 4% "as lower traffic and consumer demand was partially offset by higher average ticket and design sales."

Toll Brothers, a builder that caters to the buyer of $1mm homes on average and where about 25% pay in cash, said this in their press release ahead of their call:

"While affordability pressures and uncertain economic conditions persist, we are pleased with the resilience of our luxury business and more affluent customer base. In this environment, we continue to focus on strategically balancing price and pace in order to maximize profitability and returns."

On the flip side of the economic coin to housing, cruising has certainly been a bright spot. From Viking Holdings who caters to boomers, retirees and empty nesters:

"In terms of the overall booking environment, we are seeing sustained strength in demand; 96% of the 2025 capacity for our core products is already booked, effectively selling out this year. As such, our attention remains on 2026 bookings, where we're seeing a very strong start. As of August 10, 55% of the capacity of our core products for the 2026 season was already sold, which is in line with our book position at the same point last year and at higher rates."

I do want to add that these cruisers are a cohort that does NOT want the Fed to cut interest rates because they are benefiting tremendously from the interest income on their savings.

From Estee Lauder, a stock we own and trading down pre market:

They saw "Ongoing subdued sentiment and lower conversion from Chinese consumers."

In North America, they saw "Ongoing retail softness for some brands as well as pressures from subdued consumer confidence and sentiment in the second half of fiscal 2025, which led to elevated levels of inventory and destocking at certain retailers, along with the timing of shipments compared to the prior year."

Tariffs are a problem, "Based on current information and net of planned mitigation actions, the Company expects tariff related headwinds to impact fiscal 2026 profitability by approximately $100 million. The company continues to evaluate additional strategies, including further PRGP (profit recovery growth program) initiatives and potential pricing actions."

I'm sure trade deficits in skin care, make up, fragrance and hair care are a national emergency that must be dealt with.

For the week ended August 15th and with little w/o/w change in mortgage rates after the recent modest drop, purchase applications were flat while refi's fell 3.1% after last week's 23% pop higher. While mortgage rates have fallen by about 15 bps over the past 3 weeks, purchase applications are just modestly higher as the price of a home is still too high for many first time buyers and mortgage rates are still elevated enough to have the one who has a 4% mortgage to stay put.

Overseas, the Reserve Bank of New Zealand and the Indonesian central bank each cut interest rates to 3% and 5% respectively. The former was expected while the latter was not. The Swedish Riksbank held steady with its 2% policy rate, the same rate that the ECB has.

Also, as trade flows calm down after the panic rush in April, May and June, Japanese exports fell 2.6% y/o/y in July, about as expected but with still the tariff challenges even with a 'deal.' Export declines were seen in autos, auto parts and steel in particular. The Nikkei took a breather after its recent run, down by 1.5% just as US tech stocks did.

A few weeks after the BoE cut rates on a very split vote to 4%, headline CPI rose 3.8% y/o/y both headline and core and both one tenth above expectations. Service price inflation was 5%. The ONS said this was NOT due to greater hotel room demand because of the Oasis concert shows but higher prices for restaurants and hotels were a factor in CPI, along with transportation and food/beverage. Air fares spiked by 30% m/o/m but likely a timing issue around the holiday calendar.

The UK 10 yr inflation breakeven is little changed in response at 3.02% and this is near the lowest level in 4 1/2 years as investors don't think this inflation can last. Gilt yields are down too after the recent run higher.

UK core CPI y/o/y

BY Doug Kass · Aug 20, 2025, 8:29 AM EDT

* Hubris is one of the great renewable resources...

* "What goes around, comes around..."

I have the investing scars on my back, so I have learned (the hard way!) to respect Mr. Market and navigate with the understanding that I am often wrong and always in doubt.

It is for that reason (and that their memories of their mistakes are too often forgotten) that I recoil in reaction to overconfidence in the business media and elsewhere. (This is something I discussed in my Bloomberg interview with Paul and Tom yesterday.)

If a guest or panelist comes across arrogant, it is my view that, especially if he is terribly wrong, he should be open to criticism and reminded of both his arrogance and wrong-footed stance by others. If he is humble, that is another story and criticism should not be immediately levelled at the offender.

In other words, what goes around, comes around...

Smug, condescending and full of hubris is no way to invest, son.

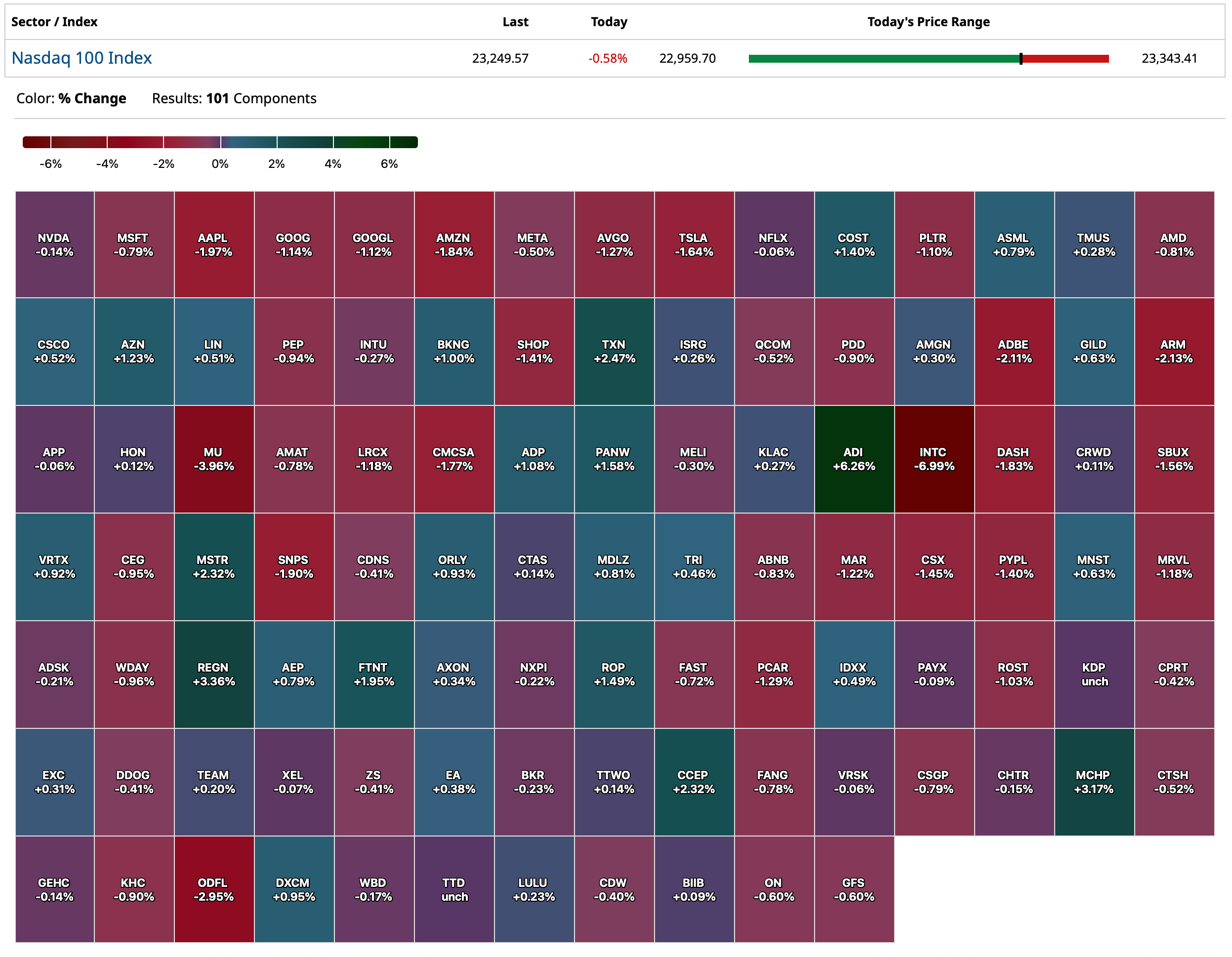

Yesterday the Nasdaq had its second worst day since April 2025.

On Monday , Nvidia's NVDA shares suffered their largest fall since April (Broadcom AVGO (-$11 yesterday) and Goldman Sachs GS (-$10), also previously mentioned and confidentally purchased by the "guy" on CNBC on August 12, also fell dramatically):

While a week or so does not make a potential top, pride goeth before fall...

Let's go to the tapes!

Trade Tracker: Brian Belski buys more Broadcom, Nvidia and AMD

Here is what I wrote only eight days ago on the subject:

* But I will only "criticize by category and praise by individual" (h/t Warren Buffett)

* An appearance on FinTV may have already top ticked the momentum stocks...

"The whole problem with the world is that fools and fanatics are always so certain of themselves and wiser people so full of doubts."

-Bertrand Russell

I am often wrong and always in doubt.

My mantra is that we should not be overly confident as we still have to count the votes!

As I have consistently written over the years, this is too often not the case for uber confident "talking heads" in the business media who are trying to improve their brands, sell a service or gain money management assets.

That said, I am increasingly convinced that my observations in "Watching In Amazement" will prove insightful:

Aug 12, 2025 2:43 PM EDT

I had CNBC's "Halftime Report" on today and I listened to a panelist (praise by individual, criticize by category — so no names!) who confidently added (AVGO) , (NVDA) and (GS) to his portfolio this afternoon.

Please look at the price charts of those companies before you read further!

While I recognize that my market view has been half baked for quite a while and having been mentored at Putnam by one of the great momentum traders in history ("The Chief") — I simply can't fathom the downside versus upside (and the absence of a margin of safety) in these buys.

While my general concerns continue to be realized — most notably: slowing economic growth, prickly inflation (seen in this morning's CPI report) and ever higher valuations — this has obviously not translated into a lower market.

Every day it grows clearer that momentum is a force unto itself.

It is terribly frustrating as I try to operate within the framework of a market that is disinterested in negatives and is continuing to be bought on every dip.

Despite that frustration I will not chase under any condition and compromise my investment process.

I will buy value (as I recently did with (UNH) and (PSKY) but I will never abandon the notion of risk/reward.

By Doug Kass Aug 15, 2025 11:30 AM EDT

BY Doug Kass · Aug 20, 2025, 7:30 AM EDT

Bonus — Here are some great links:

They Say the Consumer Is Broke…

BY Doug Kass · Aug 20, 2025, 6:25 AM EDT

The S&P Short Range Oscillator stands at 2.30% vs. 2.23% — still overbought.

BY Doug Kass · Aug 20, 2025, 5:51 AM EDT