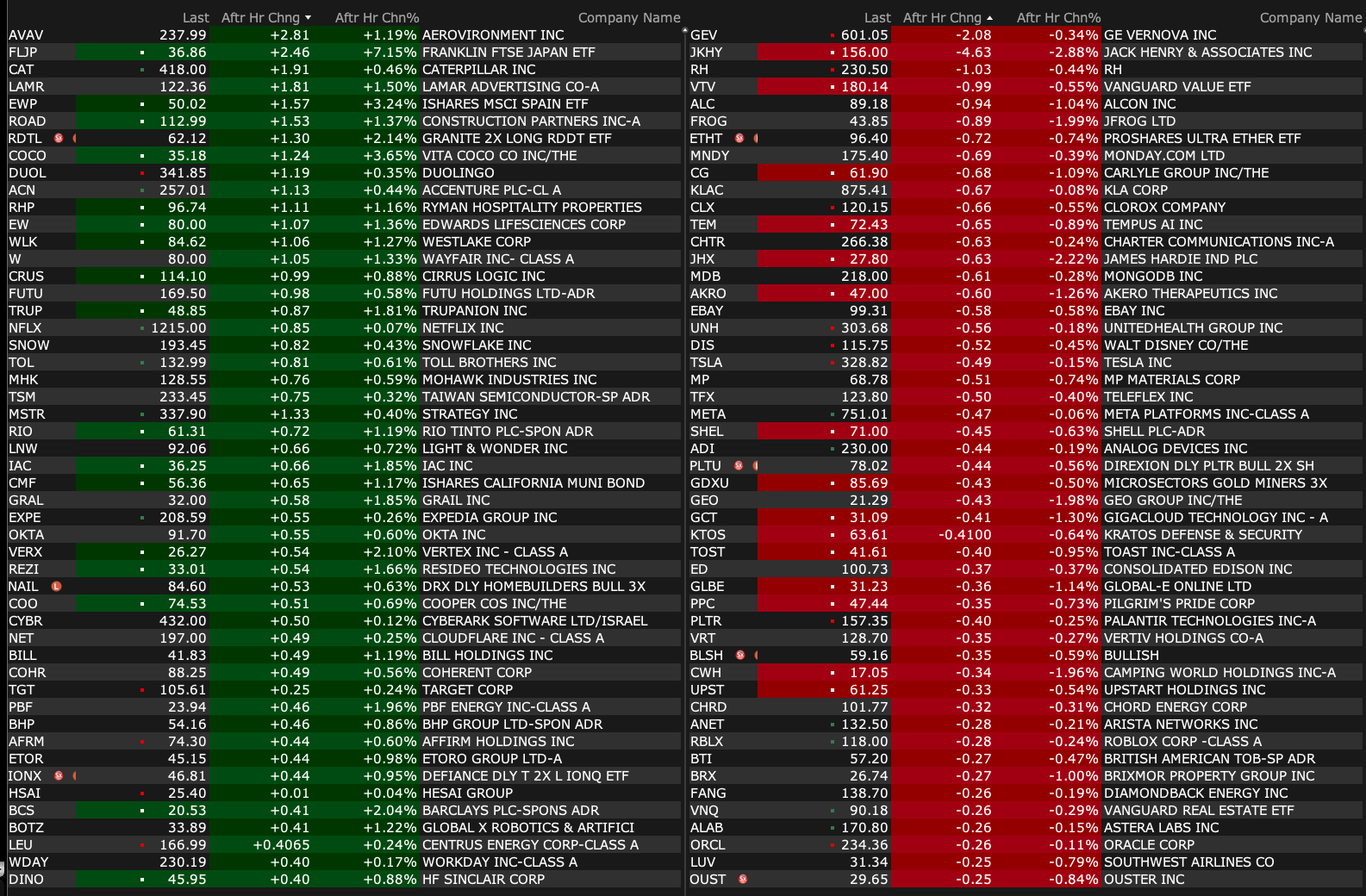

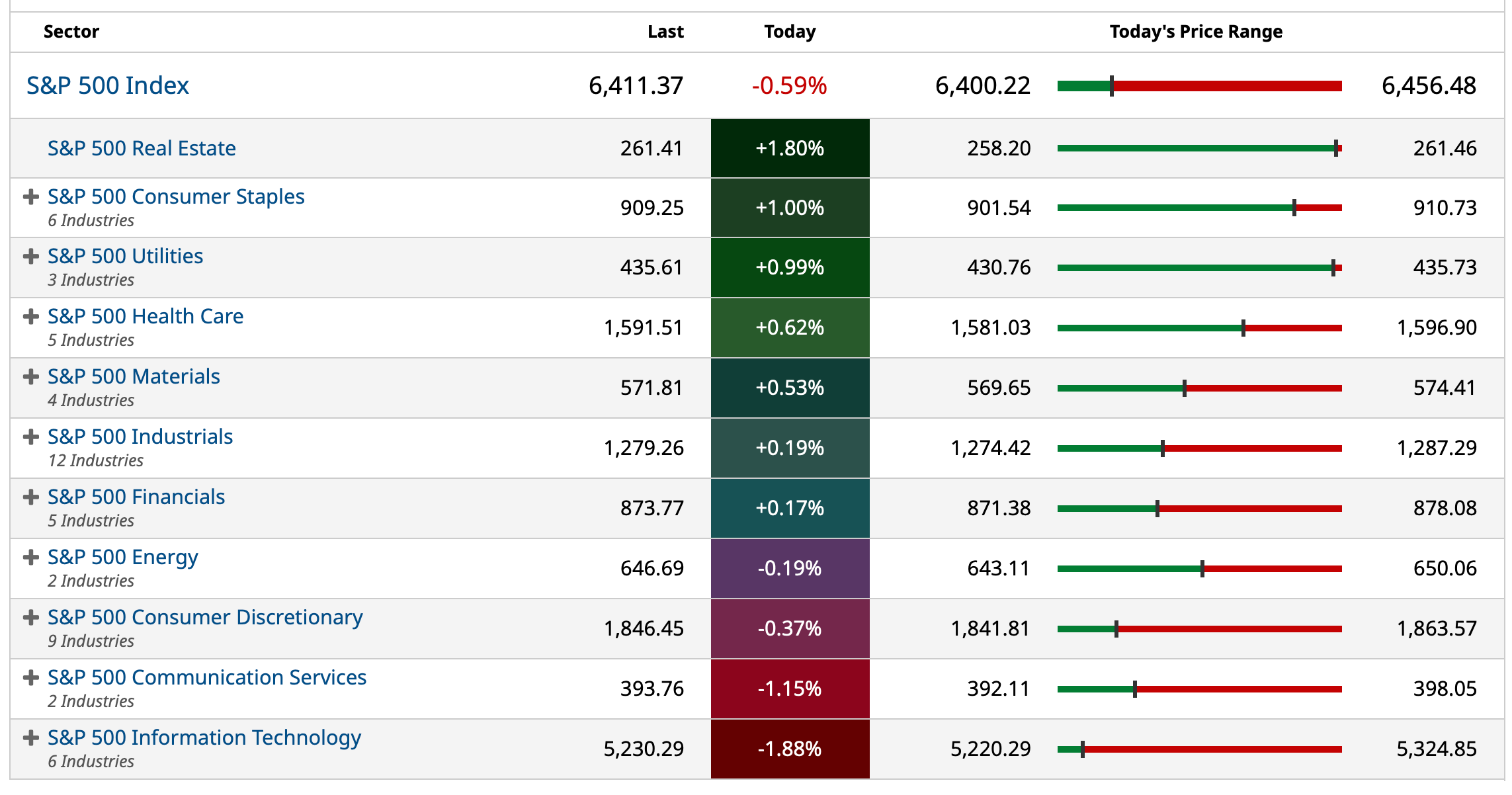

Tuesday's After-Hours Movers

As of 4:20 p.m.:

BY Doug Kass · Aug 19, 2025, 4:45 PM EDT

As of 4:20 p.m.:

BY Doug Kass · Aug 19, 2025, 4:45 PM EDT

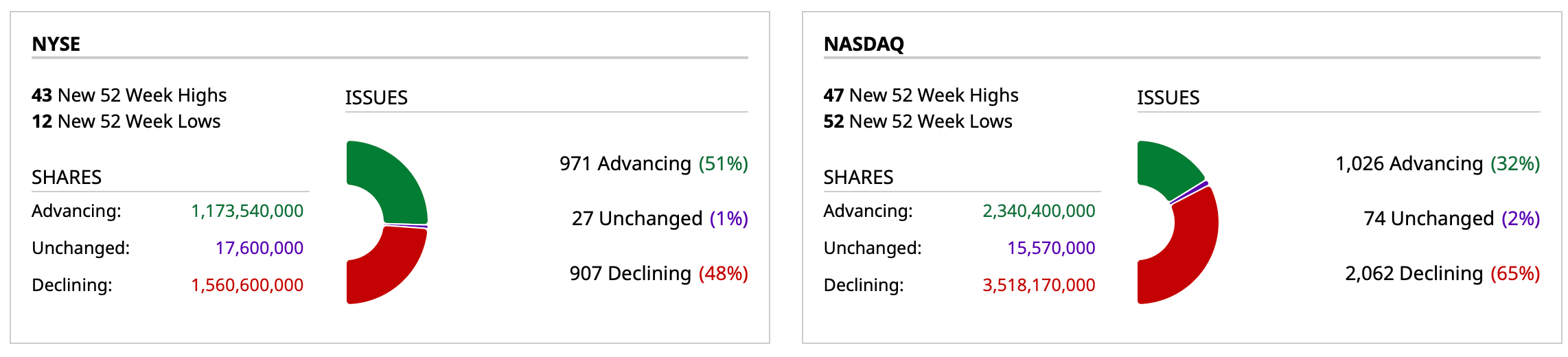

- NYSE volume 16% below its one-month average

- NASDAQ volume 10% below its one-month average;

- VIX index: up 3.87% to 15.57

BY Doug Kass · Aug 19, 2025, 4:40 PM EDT

Thanks for reading my Diary today.

I hope my output was helpful.

I am leaving early to go to the beach with my granddaughter.

Enjoy the evening.

Be safe.

BY Doug Kass · Aug 19, 2025, 3:38 PM EDT

BY Doug Kass · Aug 19, 2025, 3:30 PM EDT

Bought back small Paramount Skydance PSKY at $13.16.

BY Doug Kass · Aug 19, 2025, 3:15 PM EDT

BY Doug Kass · Aug 19, 2025, 3:06 PM EDT

With S&P cash -47 handles I have covered my short index calls.

No index positions now.

I will reshort on strength.

BY Doug Kass · Aug 19, 2025, 2:54 PM EDT

* And a lot of other 'relevant' stuff...

Per the excuse making for Sam Altman, a simpler way of saying it, if he really thought we were in inning 1 of a multi-decade Gen AI boom, would he really feel the need to go on TV and try to talk everything down, and make a fool of himself in the process, at the same time he still needs to raise scads of money to keep the doors open based on the rate his own business burns money?

Speaking of burning things, interesting article on power (and water) consumption. All of this, and all the additional capital expense on the newest and greatest chips, for a model that got worse? This makes the business worth more money, why? Next we are going to hear Sam Altman made GPT-5 purposely worse and wasted all of this money to scare away investment in future competition:

https://oilprice.com/Energy/Energy-General/How-Much-Energy-Does-ChatGPTs-Newest-Model-Consume.html

This Substack below on security measures by the ultra-wealthy is somewhat relevant.

The question becomes, why all the bunkers and security measures if AI is about to save the world and utopia is on the way? If there is about to be 10% GDP growth with no inflation and no unemployment, and cancer will be cured, of course the masses will be ecstatic, and there wouldn’t be any need for these security measures. The same guys selling us on AI prosperity are the same guys bunkering themselves from what is to come. I do not mean this in a Terminator version of AI, I mean this in an economic sense, relative to what the country has now become.

I think these guys know it is all baloney, and nothing will be changing for the better because of AI. Things will change, but they will not be better.

The internet was the greatest invention of the last 75 years, alongside waxing and the Toto toilet. Things changed, but is anything really better because of the internet, or are things actually much worse?

As best as I can tell, due to the internet, a very small % of people became relatively much wealthier, and most became relatively much poorer. Social media wrecked the lives of children, and has led to a huge % of kids that are obese and don’t go outside, but instead spend all day on their handset while on Prozac and Adderall. This has now turned into not just kids, but a huge % of the population. Of course, those selling this stuff will not let their own children on it. AI will probably be no different, assuming the tech overlords want their children to be able to think.

One could easily argue the internet also led to the 2000 dot-com bust, which ushered in a new era of easy money, which also led to 2008, and more easy money and monetary experiments, which all led to more fiscal largesse, which the QE helped finance, our bloated budget, and an even greater societal divide. It also helped enable all the offshoring, which happened too quickly, and to too much of a degree, going well beyond the basics of wine and cheese, and leading to a disenfranchised blue collar labor force that has turned into discouraged workers, created corporate cost savings that shifted to the government's balance sheet in the form of entitlements and has led to our bloated budget and entitlement society, and created a massive enemy superpower in China that is also a huge strategic problem because our means of production for nearly everything is now there.

I do not think I am even close to a luddite. How anyone can argue the internet made things better is beyond me. It had the potential to make things better, but it clearly did not. The proof is in the pudding. Things changed, but things are not better. Boy if they could only update these charts: https://www.worldhappiness.report/ed/2019/the-sad-state-of-happiness-in-the-united-states-and-the-role-of-digital-media/

AI will be the same. Things will be different because of it, but most likely, not better, and these guys know it. They just don’t care, but are narcissistic and egomaniacal enough to believe their bunkers and security are the answer. It is pretty stupid frankly. If the world comes to that, who really cares? There will be nothing to spend all the money on.

Guard Towers For The Gilded Class

Different slogans, same result: taller fences around the rich man’s compound.

On a different note, The Financial Times just reported that the nation’s tech titans are spending record sums on personal security. Zuckerberg shelled out $27 million last year to keep himself and his family safe. Elon Musk reportedly travels with 20 bodyguards like some Bond villain or on-stage hip hop performer.

Even Nvidia’s Jensen Huang, the newly minted $153 billion man, had to bump his security budget 60% because people keep mobbing him at conferences—sometimes even in the bathroom (pardon me while I lose my lunch).

You could dismiss this as just another absurd detail from the endless parade of Silicon Valley excess. You know, things like gold-plated panic rooms and CEOs wives pumped full of enough silicon and botox they look like those evil balloons Joker had in the 1980s version of Batman.

But the truth is it’s not just about tech CEOs. It’s a preview of where America is headed. As the wealth gap widens, security for the rich won’t just be a quirky corporate disclosure buried in proxy statements—it’ll be one of the fastest-growing industries in America.

I’m a realist. I get that politics is full of hypocrisy on both sides, and I get that monetary policy is the sacred cow nobody dares touch. Republicans, Democrats—they bicker about culture war scraps, but on money-printing they’re a united front. And that’s the problem: the one thing both parties actually agree on is the very thing that’s quietly driving inequality into the stratosphere.

Both have embraced a de facto version of Modern Monetary Theory—aka the economic cheat code where the Fed can supposedly print infinite dollars with no consequences. It’s magical thinking, the kind usually reserved for children’s video games or, equally as unrealistic, Paul Krugman columns. The result? Every time the Fed steps in with QE, the rich get disproportionately richer, the middle gets squeezed, and the poor get flat-out suffocated.

Democrats, of course, claim to be the party of equity—no longer satisfied with equality of opportunity, they’ve graduated to demanding equality of outcome. But their policies betray them. Endless federal spending, limitless taxation, and a willful ignorance of fiscal discipline all conspire to supercharge exactly the thing they say they want to fix: inequality.

If equity is the goal, monetary sugar highs are not the way to get there.

Democrats don't care about the deficits as Republicans pretend to care about deficits. The later chainsawing government budgets like teenagers at a lumberjack cosplay—until, of course, it’s time to pass tax cuts or defense bills, at which point the chainsaw mysteriously runs out of gas. Democrats, meanwhile, run the presses full blast and insist it’s fine because the U.S. dollar is the reserve currency. One side waves the flag of “fiscal responsibility” while quietly piling on its own debt; the other side waves the flag of “equity” while fueling the very inequality they rail against.

Different slogans, same result: taller fences around the rich man’s compound.

Which brings us back to Zuckerberg’s $27 million moat, Musk’s private army, and the bulletproof boardrooms of Bezos. These aren’t just vanity expenditures. They’re a flashing red signal of where the country is heading. If monetary and fiscal policy keep fueling this great divide, it won’t just be tech CEOs hiring phalanxes of ex–Special Forces to guard their mansions. It’ll be bankers, landlords, hedge-funders, crypto bros, influencers, and eventually anyone who happens to be rich enough to flaunt it.

The killing of UnitedHealth’s CEO by Luigi Mangione earlier this year was a horrific tragedy. But sadly, for the disenchanted, it also served as a dogwhistle of sorts.

Think about it: what happens when the bottom 50% sees its quality of life deteriorate year after year, while the top 10% buys new yachts, new estates, and new tits? You don’t need a PhD in sociology to predict the outcome. Human behavior runs on resentment just as much as it runs on survival. When the masses feel brutalized and disenfranchised, society doesn’t become more polite—it becomes more combustible.

To be clear, this isn’t a call to arms or some endorsement of populist rage. To me it just feels like behavioral economics in the raw. The more brutalized and disenfranchised the bottom 50% feel, the more obvious it becomes: if you’re rich in America, you won’t just need a financial adviser—you’ll need a private army. And judging by the $45 million already shelled out in 2024 alone, the rich already know it.

So yes, $27 million for Zuckerberg’s security detail is eye-popping. Musk’s 20-man entourage is absurd. Bezos building a bulletproof bunker in Seattle is darkly comic. But don’t laugh too hard. These aren’t outliers; they’re harbingers.

Welcome to the golden age of widening inequality: gated, armored, and very well-guarded.

Your move, Jerome Powell.

BY Doug Kass · Aug 19, 2025, 1:35 PM EDT

I just made some individual short covers:

* HOOD $108 (-$7)

* PLTR $159.75 (-$14)

* ARKK $74.46 (-$7)

BY Doug Kass · Aug 19, 2025, 1:00 PM EDT

Housekeeping item.

I covered my Home Depot HD short at $406.50 for a small profit.

From earlier:

* After EPS release...

Dougie Kass

Short HD (after EPS release and rally off lows) at $396.20.

Position: Short HD (VS)

By Doug Kass Aug 19, 2025 6:10 AM EDT

BY Doug Kass · Aug 19, 2025, 12:52 PM EDT

With S&P cash -29 handles I am taking my short index call position from medium sized to small sized.

I plan to sell any rally.

BY Doug Kass · Aug 19, 2025, 12:44 PM EDT

BY Doug Kass · Aug 19, 2025, 12:17 PM EDT

BY Doug Kass · Aug 19, 2025, 11:45 AM EDT

From Peter Boockvar:

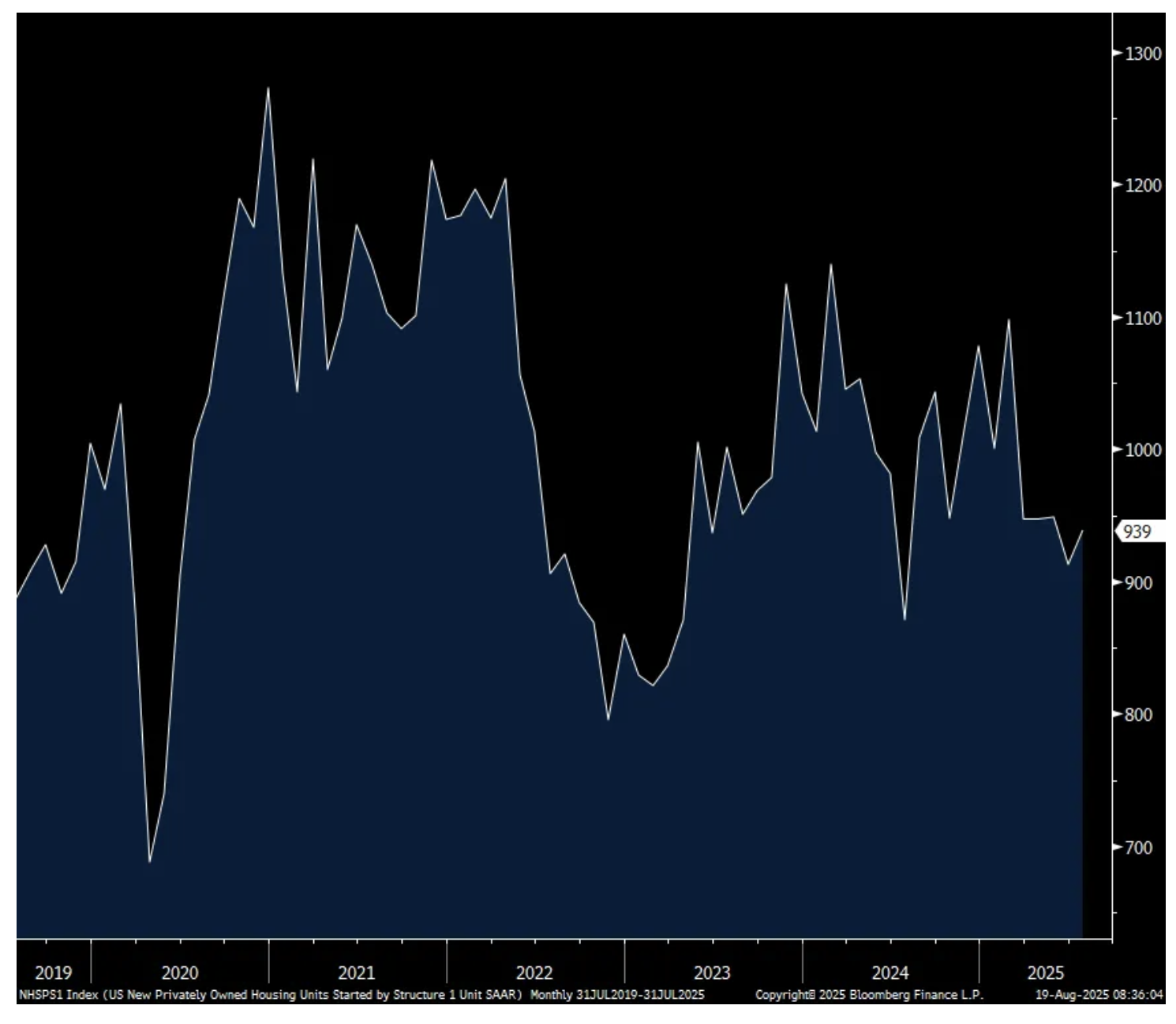

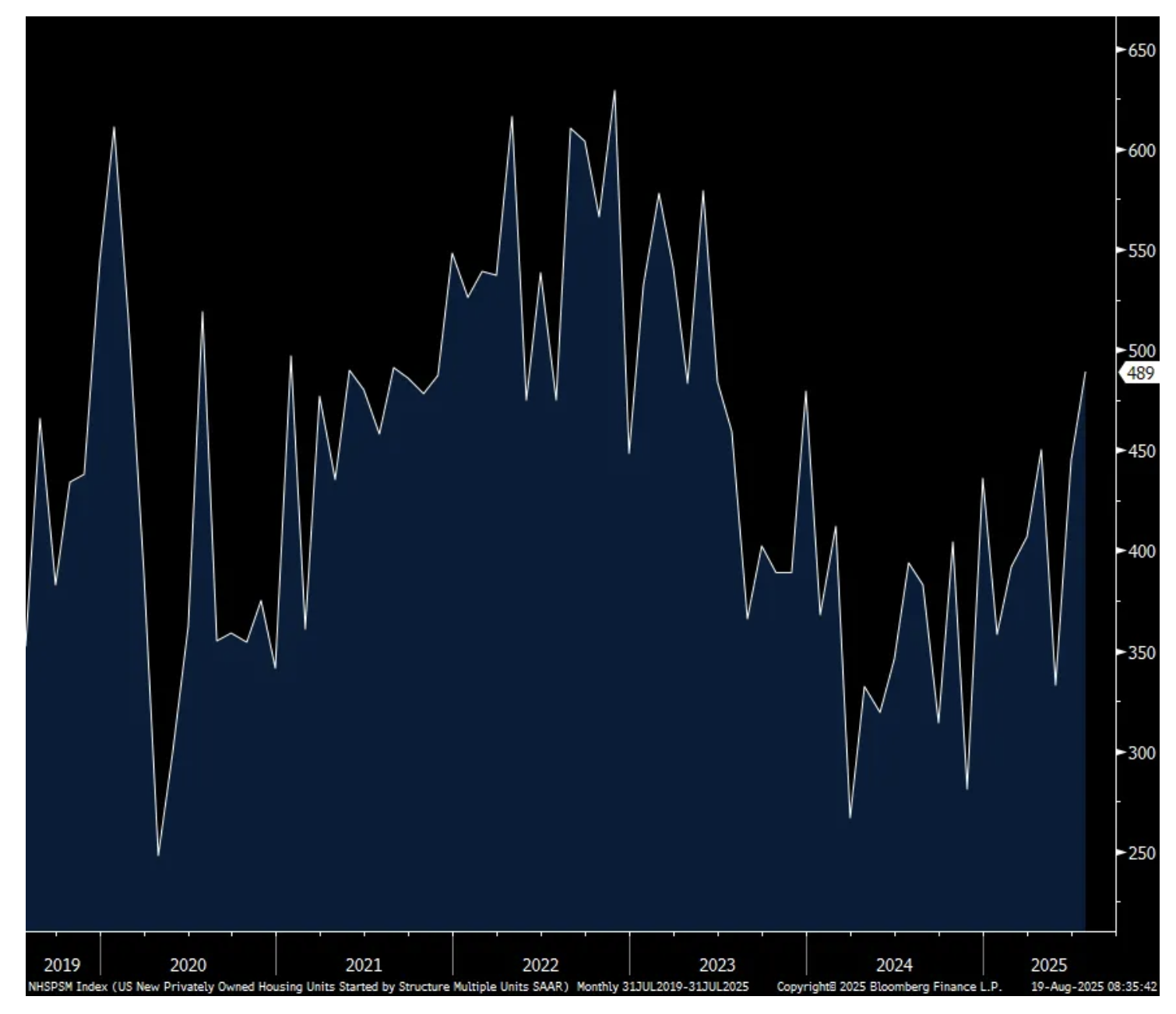

Housing starts in July totaled 1.428mm, above the estimate of 1.297k and June was revised up by 37k to 1.358mm. The main reason for the lift was an increase in multi family starts to 489k from 445k in June and that is the most since May 2023, though jumps around month to month. Single family starts were up 26k m/o/m to 939k but after falling by 36k in the month before and well below the 1mm we saw in January and nearly 1.1mm in February.

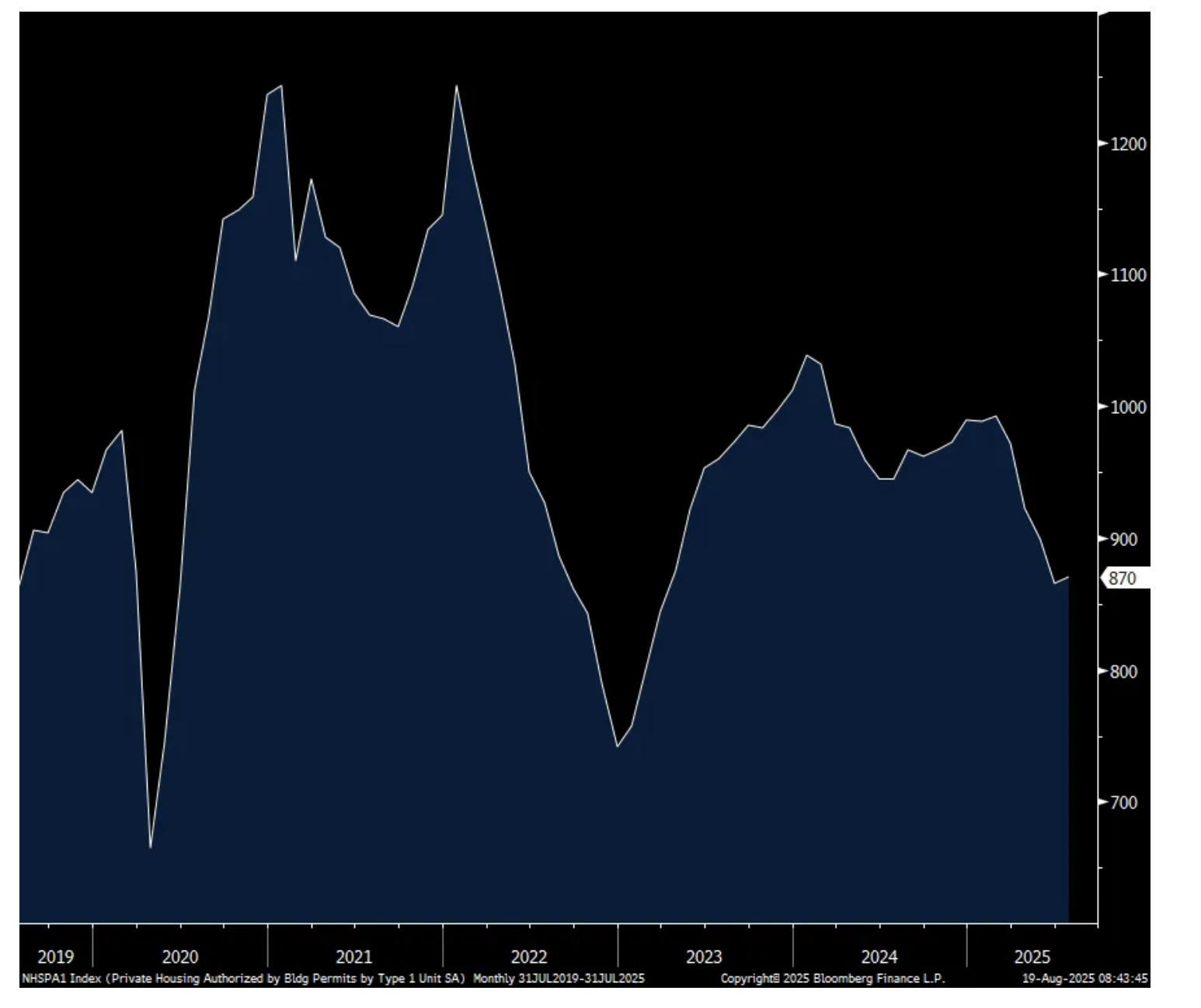

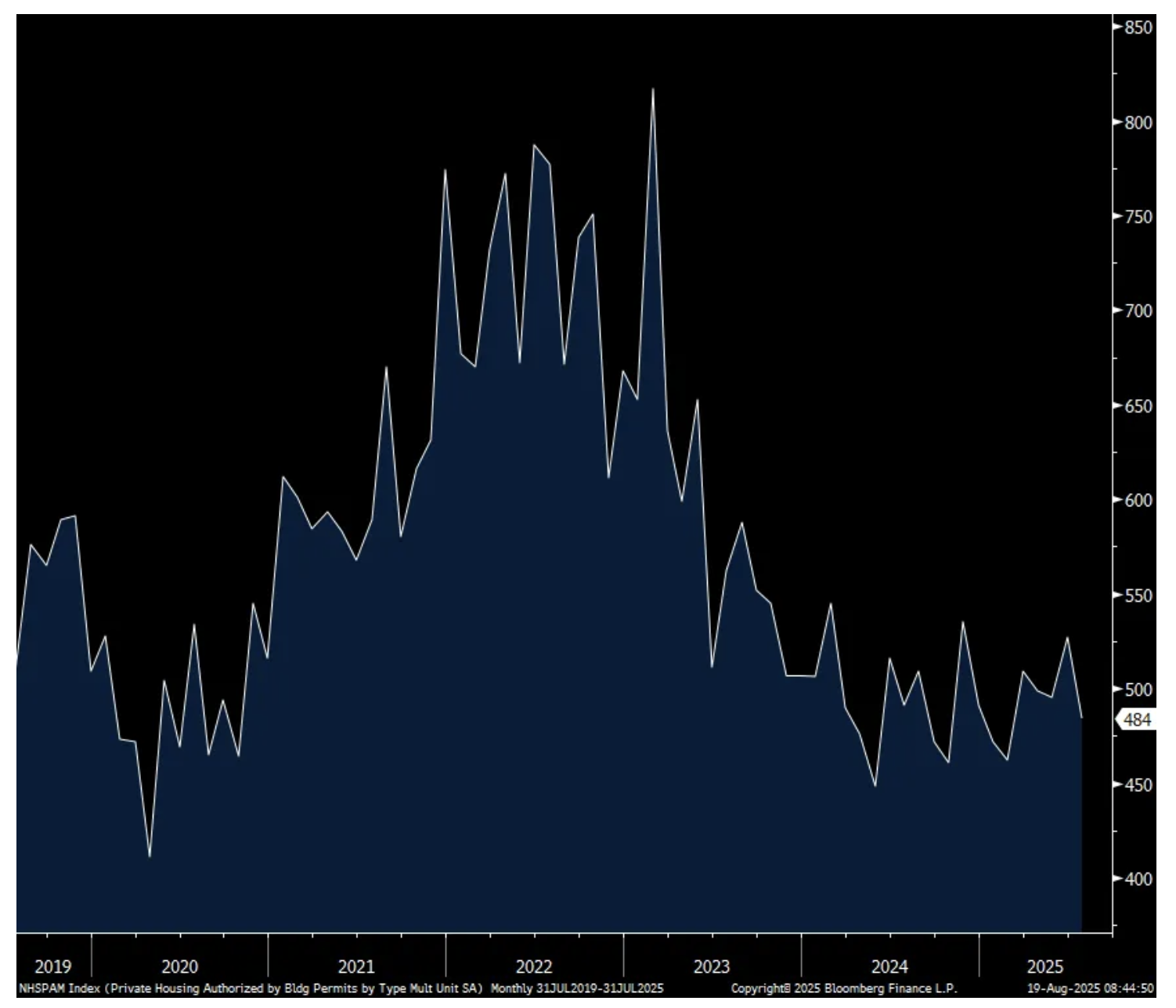

While multi family starts saw a lift, permits for new apartment buildings fell to a 4 month low to 484k, down 43k m/o/m and vs 495k in May with the biggest declines seen in the South and West, exactly where most of the supply has come on line this year. Single family permits were little changed, up 4k after dropping by 33k in June.

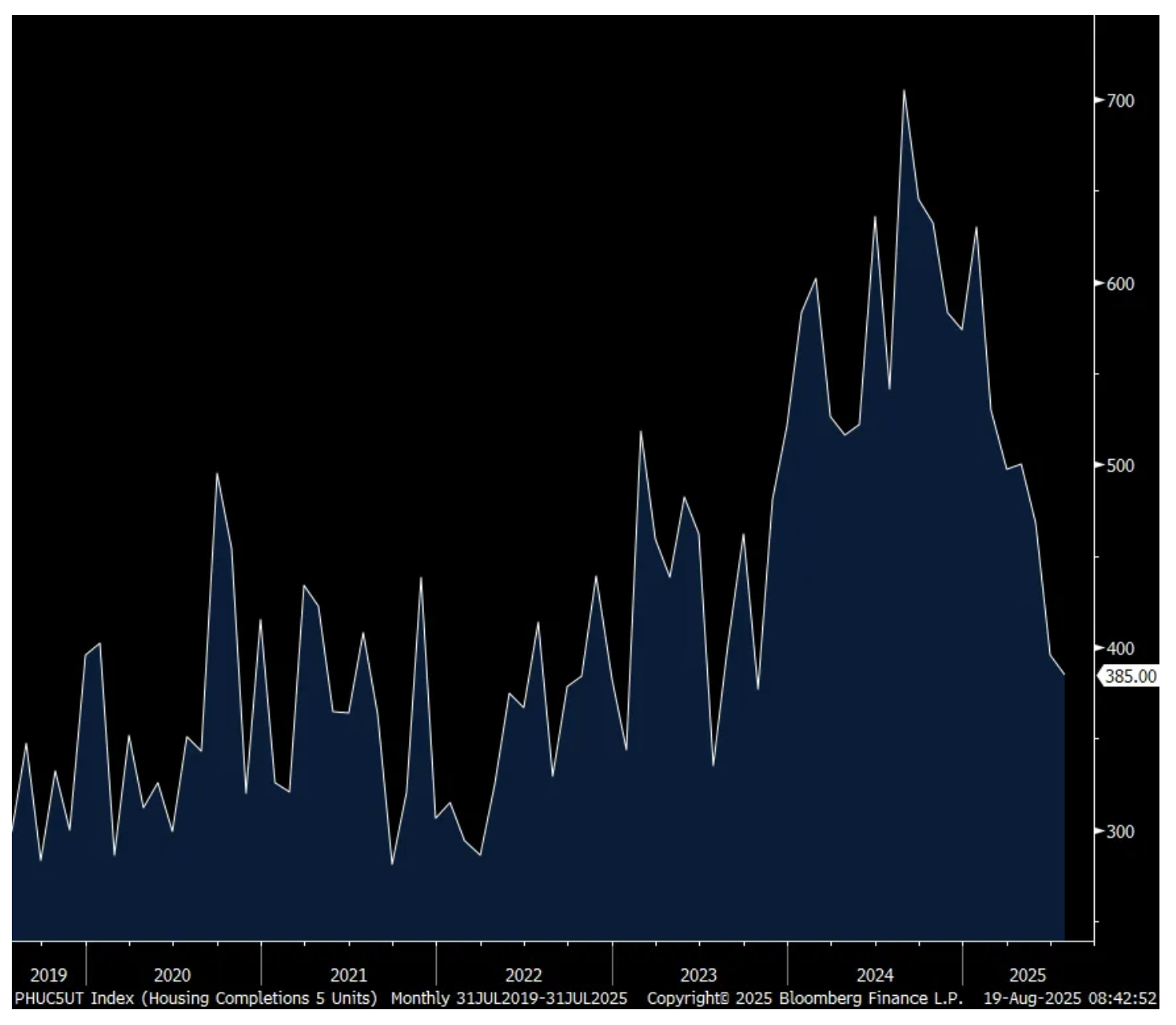

One more thing on multi family, the number of completions fell to just 393k, the least since October 2023 right before a huge spike, down almost half from the 648k it stood at in January so the pick up in starts in this category is in this context. Also, as seen in one of the charts below, the epic multi family supply mostly hitting sunbelt states this year was following the spike in starts that began in 2022 after projects got designed, funded and permitted in 2021 when the cost of capital was about half the level it stands now.

Finally, with the muted pace of starts, it squares with the 32 print seen in yesterday’s NAHB home builder survey index.

Single Family Starts

Multi Family Starts

Single Family Permits

Multi Family Permits

Multi Family Completions

BY Doug Kass · Aug 19, 2025, 11:30 AM EDT

From JPMorgan:

US: Futs are flat ahead of consumer-sector earnings kicking off today. Pre-mkt, Mag7 names are mostly lower ex-NVDA. Semis are mostly weaker ex-INTC on SoftBank stake and potential US Gov’t stake. Defensives are slightly outgaining Cyclicals pre-mkt. Bond yields are down 1bp from 2s to 30s with front-end outperforming; USD is weaker. Cmdtys are weaker dragged lower by energy despite strength in precious and Ags. BBG flagging a trade escalation from Friday where Trump expanded the metals tariffs to more than 400 consumer goods, including baby gear, and there is no exemption for goods already in transit; the article states this impacting ~$328bn of goods based on 2024 trade levels vs. $191bn before the expansion and is more than 6x levels from 2018. Today’s macro data focus is on housing starts and building permits; XHB has lagged SPX YTD by 138bp but has outperformed the SPX by 912bp over the last month.

· EU/UK: Major markets are all higher, led by France with UK lagging. The region is seeing more than +1z moves in more than two dozen baskets with CAC/SCXP also up 1.2z; Aero/Def plays are down 1.1z to 2.6z which may be related to yesterday’s White House meeting. Value is leading, Momentum is lagging; Cyclicals over Defensives. UKX +0.3%, SX5E +0.7%, SXXP +0.5%, DAX +0.4%. CSI -0.4%, HSI -0.2%, NKY -0.4%, ASX -0.7%, KOSPI -0.8%.

and...

US MKT INTEL – The Sep 11 CPI print feels like pivotal inflection point for markets as we close out the year. While bond markets are pricing ~90% chance of a cut in Sep (55% for Oct; 75% for Dec), this seems to express a view that the Fed will care more about political pressure than the data; from a data perspective, it is unclear that the Fed should be cutting given inflation. Conversations with Equity clients reveal a range of views from zero cuts up to a 50bps cut, discussed in more detail below. We think the base case is for a 25bp cut but we lean closer to zero than to 50bp as typically PPI has a one-month lag to CPI. If that pattern holds, then we will see a material increase in inflation which may push the Fed to the sidelines. Currently, economist Nora Szentivanyi forecasts 0.44% for Core MoM with the following two months printing 0.54% and 0.5%. Our Inflation Trading Desk sees Core MoM at 0.43%, as of Friday.

o 0bp pause – if the combination of NFP and CPI is enough to keep the Fed on the sidelines, the reaction here would likely be a bear flattening of the yield curve with a potential vol shock. In Equities, this would likely push markets to the 5% pullback many have called for, as this would exacerbate September’s negative seasonality. Further, if subsequent macro data (Retail Sales, PCE, Oct NFP) reflects the same trends, then the sell-off could evolve into a technical correction (10%+ down-move). In this scenario a move towards a long in Credit ETFs vs. an Equity short is one way to play. Alternatively, long Defensives vs. short Beta / RTY / Nasdaq would perform well.

o 25bp cut – the base case. Here the bull rally continues and likely broadens due to the increasing earnings power of SPX493. There may be a bias towards Quality but think Tech and Cyclicals perform well in this scenario.

o 50bp cut – this is likely to ignite a global risk-on rally with US Equities reflecting a ‘Dash for Trash’ as we see a material squeeze that could finally create the flush that is generally associated with a consensus bull rally. Look for SMid-Caps and Beta plays to lead. The risk here is that the bond market rebels, seeing 50bps as too much given the inflation increase is in its infancy. Recall, around the last 3 cuts of 2024 (Sep, Nov, and Dec), the 10Y yield increased 114.7bp, from Sep 17, 2024 (day before Sep Fed) to Jan 14, 2025 (52-week and YTD high). This appeared to be the bond market expressing the view that Fed Funds was not restrictive enough as the economy averaged 2.9% real GDP growth over the previous 8 quarters and 2.8% of 24H2. Our colleague Marissa Gitler tells us that there are a number of SOFR options prints reflecting a 50bps cut.

o CLIENT 1 – We think that there are a number of companies who are waiting to increase prices, likely because there is the possibility of lower tariff rate or more exemptions. At this point in time, those companies do not want to hurt customer loyalty by pre-emptively increasing prices if the Effective Tariff Rate declines. That said, when we track buying patterns versus shelf-stocking patterns, typically October / November is when we are most likely to see things like clothing & shoe prices see meaningful increases.

o CLIENT 2 – The timing of the inflation surge is uncertain, but it still feels early to me. I think it [inflation] becomes a bigger issue closer to year-end, if not early 2026.

BY Doug Kass · Aug 19, 2025, 11:10 AM EDT

My Bloomberg interview this morning: Bloomberg Surveillance: Market Risks - Bloomberg

At the 17 minute thirty second mark.

BY Doug Kass · Aug 19, 2025, 10:50 AM EDT

BY Doug Kass · Aug 19, 2025, 10:45 AM EDT

S&P cash is +2 handles, adding to short Index calls.

BY Doug Kass · Aug 19, 2025, 10:22 AM EDT

Reshorted WMT at $102.21.

BY Doug Kass · Aug 19, 2025, 10:12 AM EDT

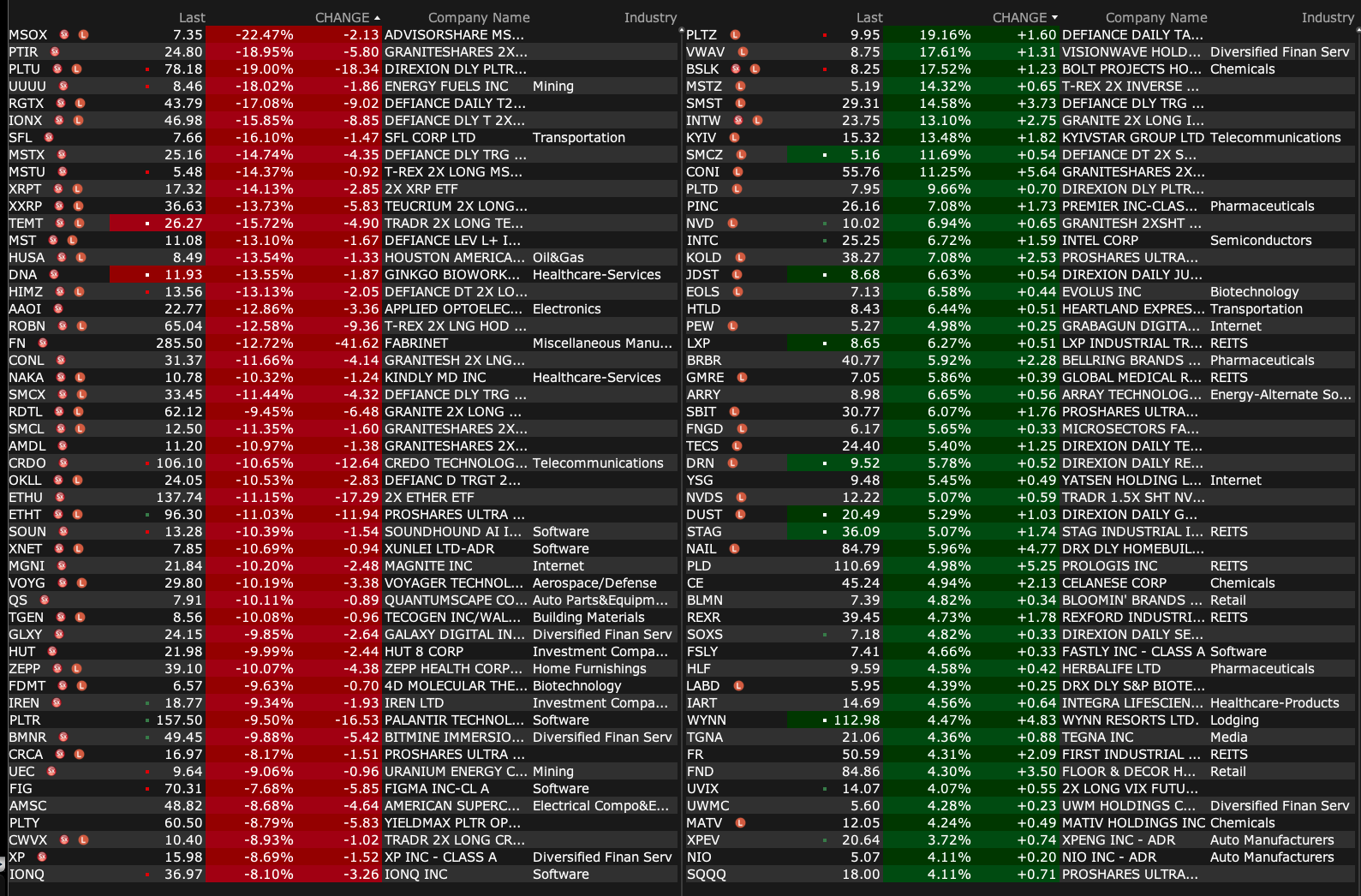

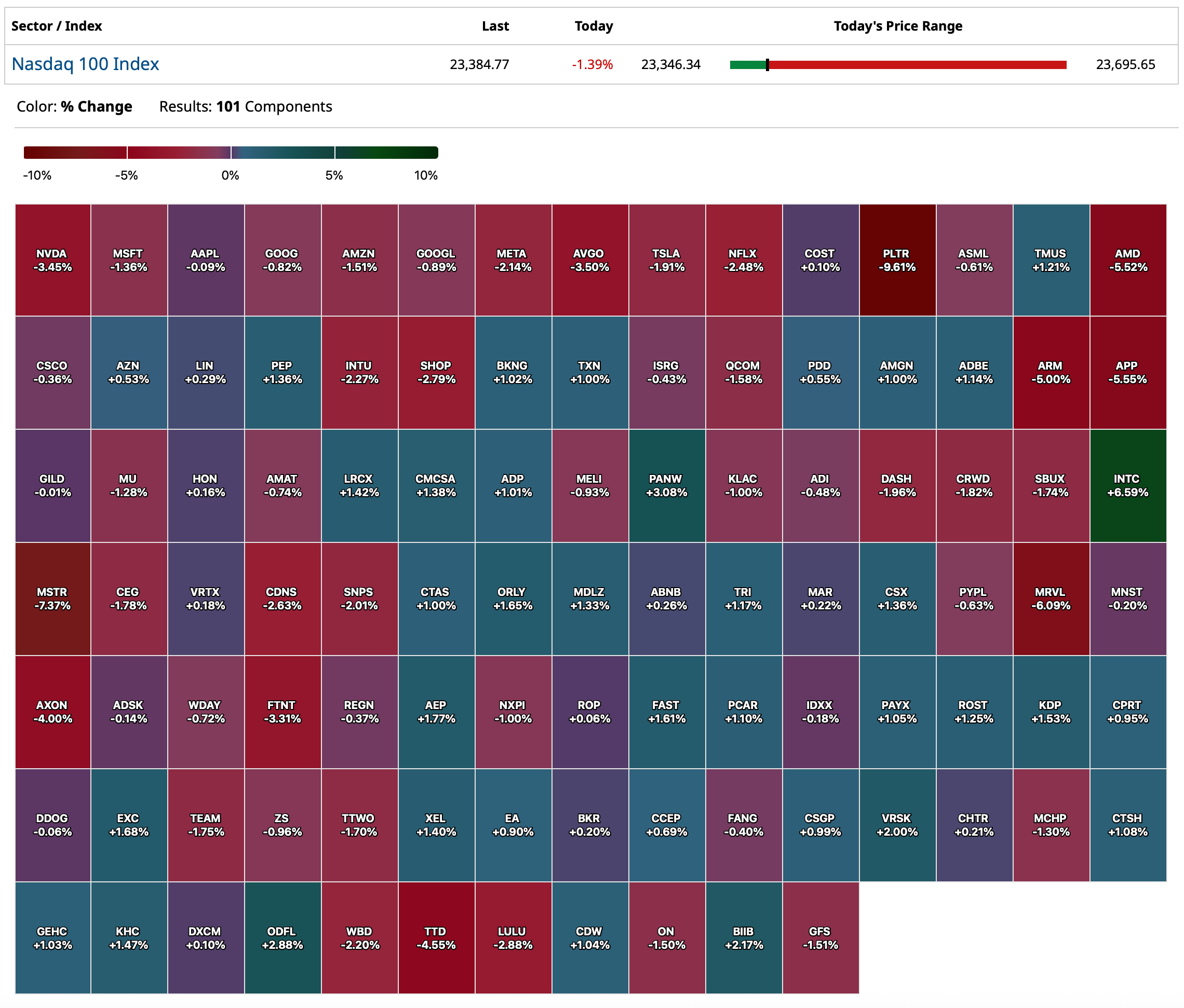

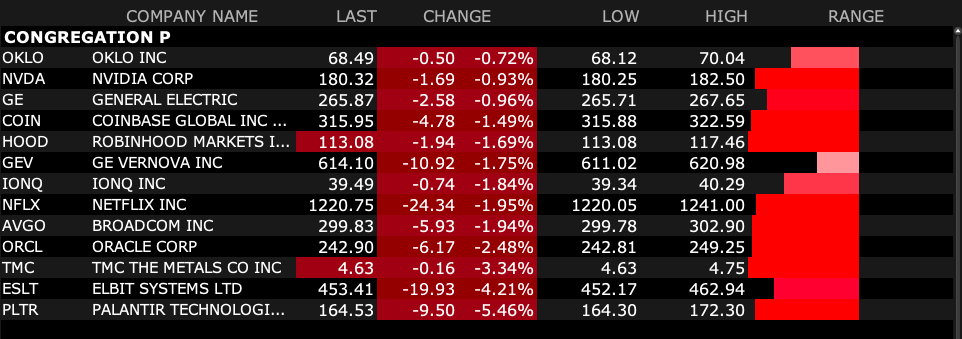

All constituents of "Congregation P" were down as of 9:45 a.m.:

BY Doug Kass · Aug 19, 2025, 10:00 AM EDT

On Friday and Monday I added to some momentum and market leaders - ARKK, NVDA, PLTR etc.

Shorting more GRNY and JOET.

BY Doug Kass · Aug 19, 2025, 9:45 AM EDT

With S&P cash -4 handles I am adding to my short Index calls.

BY Doug Kass · Aug 19, 2025, 9:36 AM EDT

BY Doug Kass · Aug 19, 2025, 9:13 AM EDT

BY Doug Kass · Aug 19, 2025, 9:06 AM EDT

-PLYM +44% (Sixth Street Partners, LLC,to acquire 100% of the outstanding Common Stock and 100% of the common equity interests of Plymouth Industrial Operating Partnership, L.P. for a price per share equal to $24.10)

-IOVA +14% (Amtagvi (lifileucel) receives Health Canada approval for Advanced Melanoma)

-IINN +10% (secures $27M government binding purchase order for ART100 Systems)

-KYIV +7.9% (post-IPO momentum)

-NXST +7.7% (TGNA to be acquired by Nexstar Media Group at $22.00/shr in cash in deal valued at $6.2B)

-BTU +7.6% (confirms termination of Anglo American coal deals due to MAC at Moranbah North Mine following March ignition event)

-FLEX +6.6% (issued warrant to Amazon to purchase up to 3.9M shares at exercise price $51.29/shr)

-PANW +6.1% (earnings, guidance; announces retirement of Nir Zuk, Founder and CTO)

-INTC +5.5% (reportedly Softbank said to have held talks with Intel on buying contract chipmaking business; US potentially taking a stake in Intel would bolster the case for further SoftBank investment)

-TGNA +4.8% (TGNA to be acquired by Nexstar Media Group at $22.00/shr in cash in deal valued at $6.2B)

-DALN +4.7% (Holder MNG raises offer to $18.50/shr from $17.50/shr)

-OPRA +3.8% (earnings, guidance)

-XPEV +3.3% (earnings, guidance)

-VKTX -30% (announces Top-Line Results from Phase 2 VENTURE-Oral Tablet Dosing Trial of VK2735 Tablet Formulation in Patients with Obesity)

-FN -9.8% (earnings, guidance)

-MDT -3.6% (earnings, guidance; adds two new Directors following engagement with large shareholder Elliott)

-AS -2.3% (earnings, guidance)

BY Doug Kass · Aug 19, 2025, 8:52 AM EDT

2:10 p.m.: Federal Reserve Vice Chair for Supervision Michelle Bowman (Voter) speaks on "Fostering New Technology inthe Banking System" before the Wyoming Blockchain Symposium 2025 (Text available. No Q&A. Livestream here)

Treasury Auctions

11:00 a.m.: Treasury Announces a 4 and 8 Week Bill Auction

11:30 a.m.: Treasury hosts a $85B 6-Week Bill Auction

Economic Calendar

BY Doug Kass · Aug 19, 2025, 8:35 AM EDT

My interview on Bloomberg with Paul Sweeney and Tom Keene: Bloomberg Live: Business, Finance, Earnings & Investment News | Watch 7AM - 6PM ET Weekdays

BY Doug Kass · Aug 19, 2025, 8:25 AM EDT

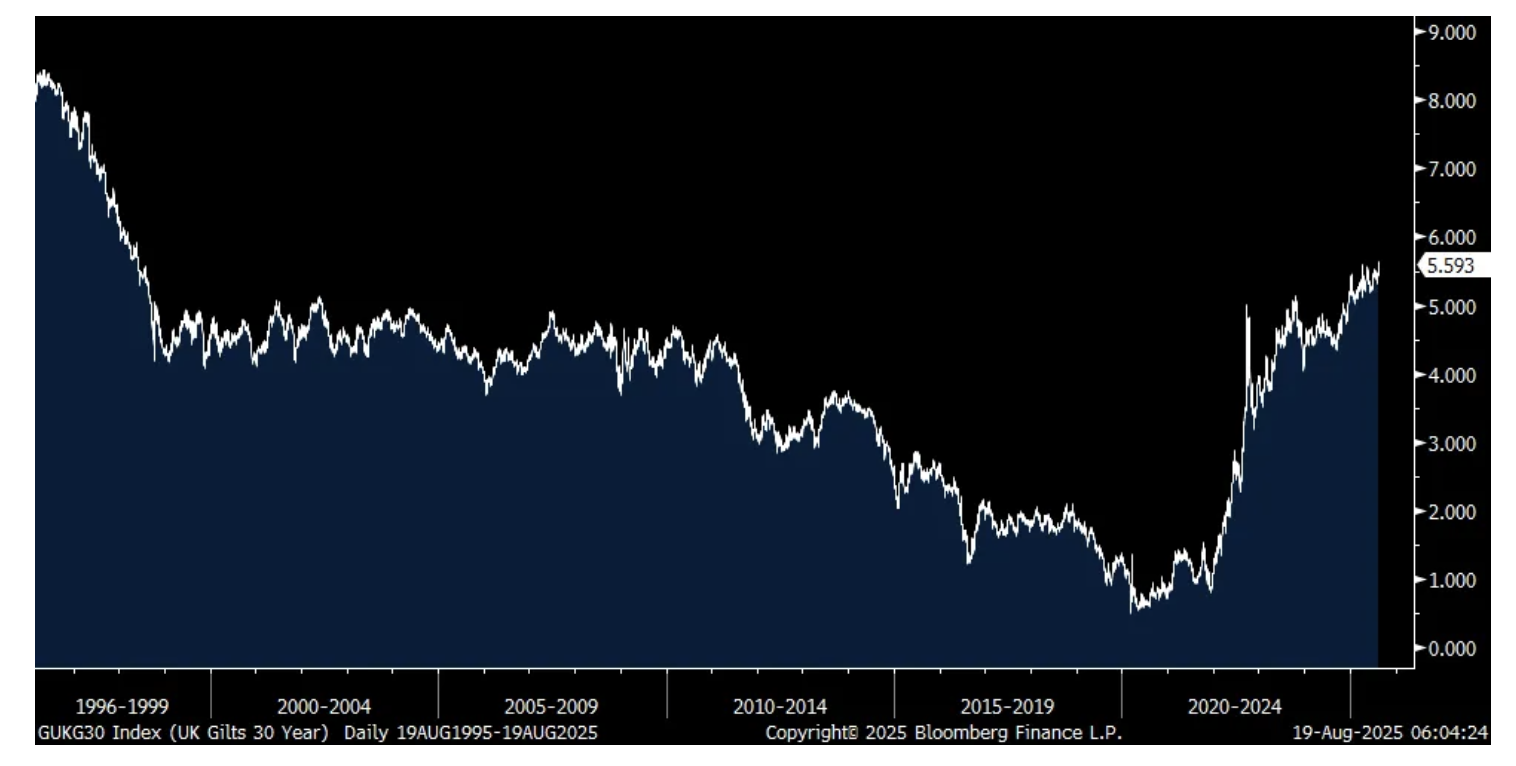

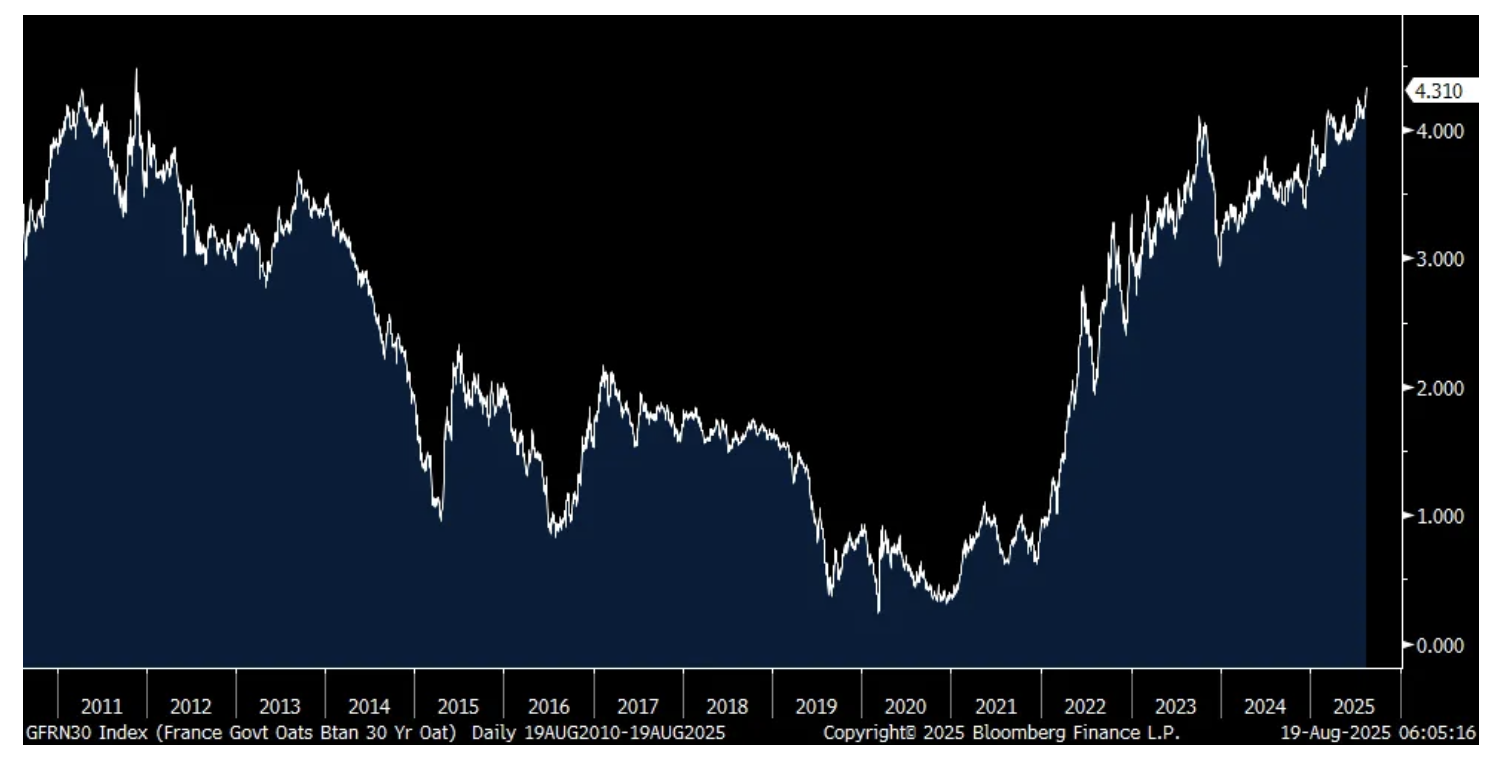

From Peter Boockvar:

Just two weeks after the Bank of England cut its bank rate to 4%, the 30 yr gilt yield yesterday closed at its highest level since 1998, rising by almost 20 bps in three days before backing off a touch today by 2 bps. Even though the ECB has cut its deposit rate by 200 bps over the past year, German and French 30 yr yields today are at 14 yr highs. I raise this for two reasons, the global bear market in bond duration continues and central bank attempts at lowering interest rates have only had an impact on short term rates. The Fed knows how this feels after they've cut 100 bps and we of course all watch to see how the long end trades from here as we are about to get some more cuts.

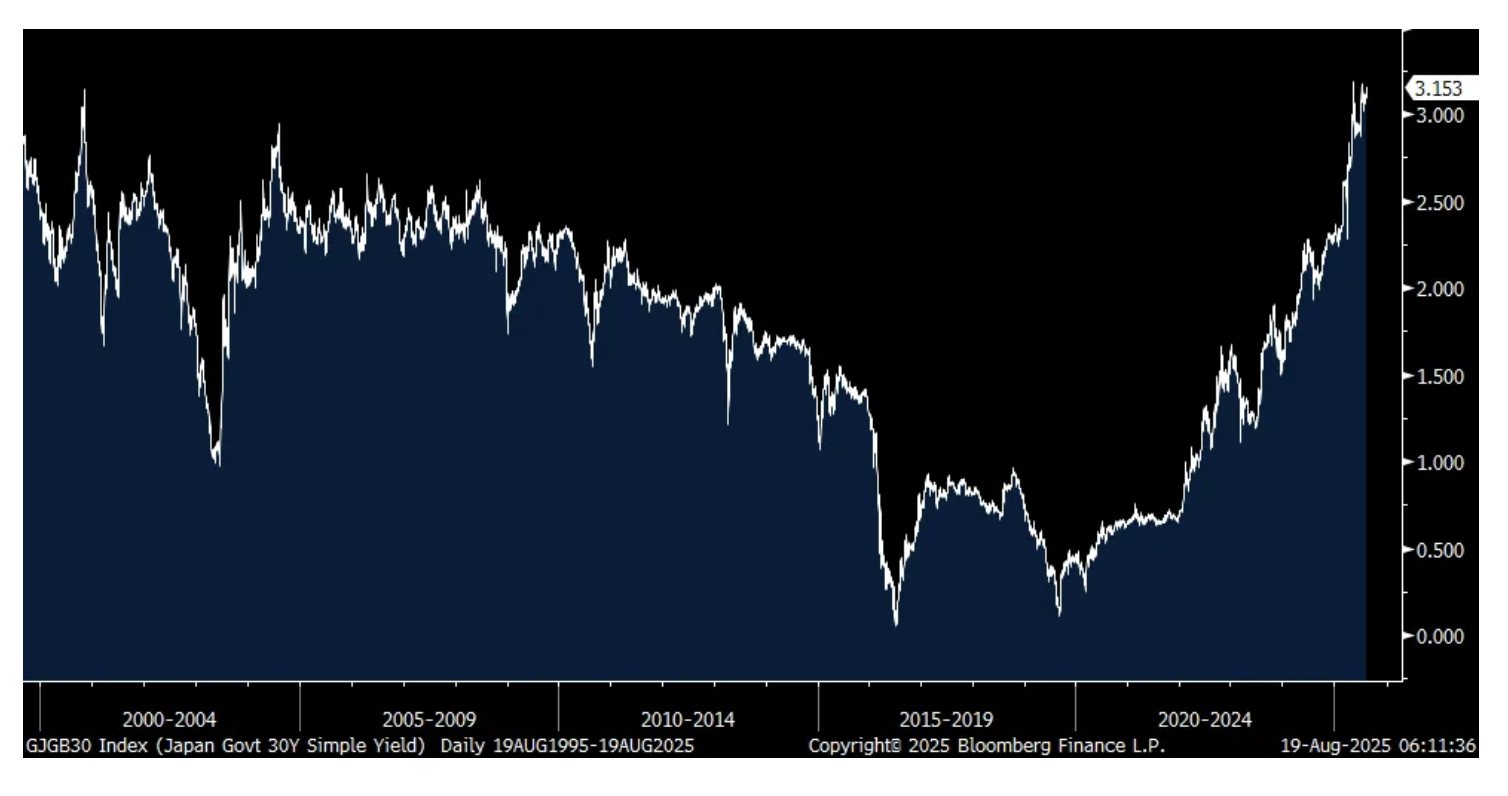

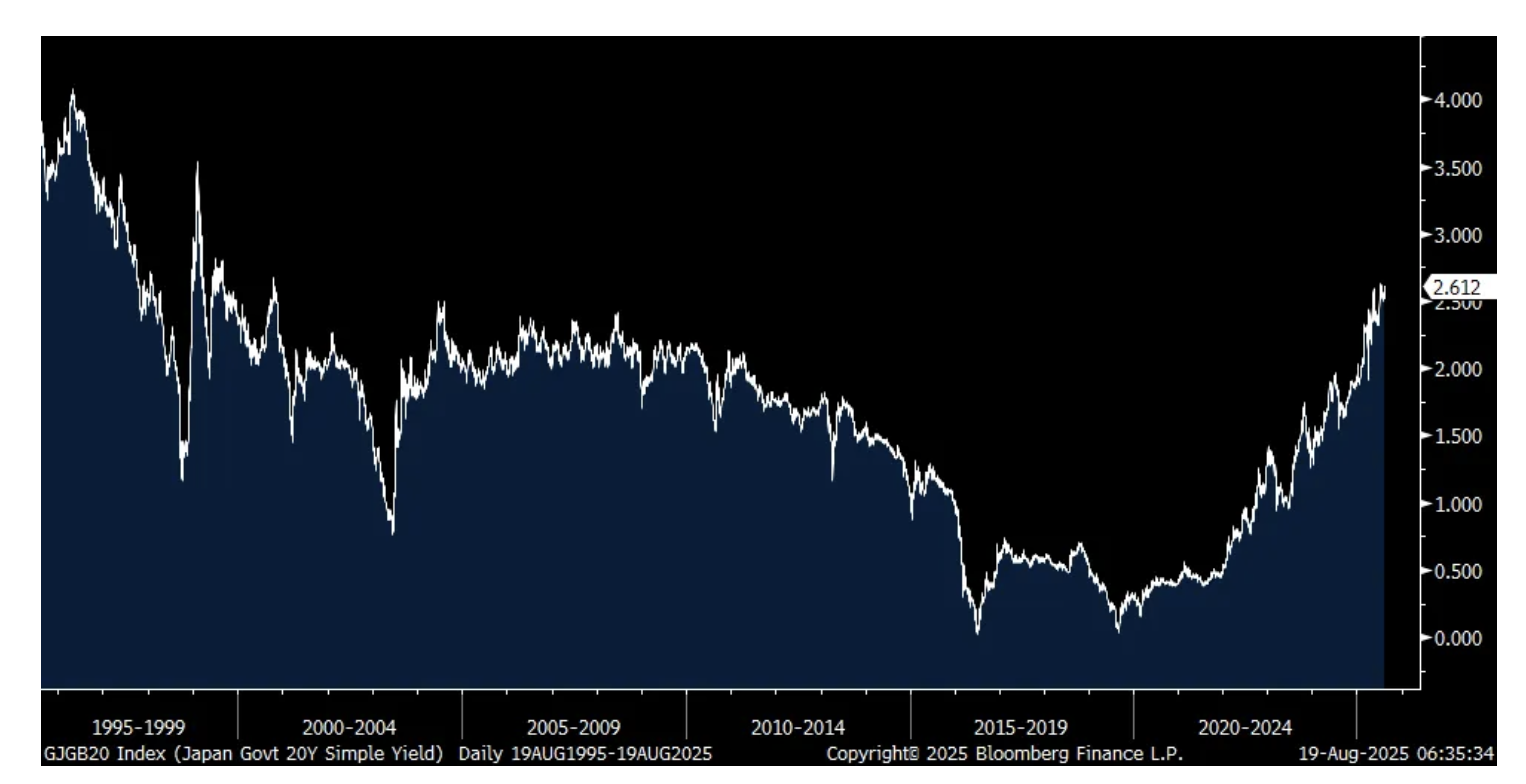

JGB yields, something I continue to encourage people to watch each day, rose too overnight after a mediocre 20 yr bond auction. The 40 yr yield closed up by 5 bps to near a one month high. The 30 yr yield closed within 3 bps of matching a record high since this was first issued in 1999. The 20 yr yield is less than 1 bps from a level last seen in 2000.

30 yr Gilt Yield

30 yr Bund Yield

30 yr JGB Yield

20 yr JGB Yield

Sensitive to the value of one's homes, mortgage rates and consumer confidence, Home Depot's Q2 top and bottom line both slightly missed expectations and comps were a touch light, up 1% vs the estimate of 1.4%.

They cite the reason for the comp miss to FX rates that "negatively impacted total company comparable sales by approximately 40 bps." I'm guessing it's their FX exposure to CAD and MXN and maybe had to do with hedges. We'll listen about this on their call at 9am.

They continue to see green shoots though with their base business. "The momentum that began in the back half of last year continued throughout the first half as customers engaged more broadly in smaller home improvement projects."

Palo Alto Network, the cyber security company, had a good quarter and guidance too:

"During Q4, many of the deals our teams had been working on during our fiscal year came to fruition. We saw robust activity across the board. In Q4, our bookings growth turned a corner and was the highest we've seen in 2.5 years. This growth is driven by deals across our platforms and also as a result of strong renewals and upsells across our existing portfolio."

"Demand for cybersecurity remains strong. Our customers are looking to us to help them secure their cloud and AI transformation journeys. We continue to see GenAI conversations as it becomes imperative for our customers to deploy productivity tools, coding tools, or revamp their customer systems to enable natural language conversations. All these use cases for AI need to be protected."

On the big economic picture, "I don't think the macro is bad. I think macro is fine...I think there's no big step-up or step-down in macro, and we'll see what happens going forward, but I don't see anything different in the market going forward."

More on some macro, the Dallas Fed released yesterday its August Banking Conditions Survey and said this:

"Loan volume and demand increased in August. Loan volume was driven by a sharp acceleration in residential real estate loans, which had contracted in the prior period. Credit tightening continued, but loan pricing declined, both at a pace slightly faster than in June. Across all loan types, loan performance deteriorated. Bankers reported declining general business activity; however, their outlook is mildly optimistic. Survey respondents expect growth in loan demand and business activity six months from now, with a minor deterioration in loan performance." Still sounds like a 1%ish type economy to me. https://www.dallasfed.org/research/surveys/bcs/2025/bcs2505#tab-comments

The survey participant comments were pretty mixed and you can still hear the fragility that's out there.

· Regional business activity is improving, along with loan demand. Business owners are willing to move forward despite uncertainties tied to tariffs, interest rates and other factors.

· The longer that trade policy changes drag on without being finalized, the longer borrowers will pause on capital spending.

· Uncertainty remains in the market; however, rate cuts will have an impact. Current rates are having a negative psychological impact when there is a perceived likelihood of a federal funds rate cut in the third or fourth quarter of this year.

· We believe there are three areas that are affecting loan demand in this environment. One, customers are taking a wait-and-see attitude toward the next rate decrease—by when and how much. They are looking over the horizon and will wait for the decrease. Two, the really smart borrowers loaded up when rates were low, and they are working through their capital spends with the cheaper dollars. They also have a wait-and-see attitude. Three, we are seeing some banks (just a few) alter rates and terms just to get a deal. They are competing with credit unions that are offering unrealistic terms and conditions. Some [offerings] seem to border on safety and soundness—including long terms, low rates and no personal guarantees.

· We are seeing a slowdown across a number of metrics as the year has progressed.

· Borrowers and applicants seem to have increasing concerns regarding the uncertainty of the timing and direction of rate changes.

· We have increased demand from the new development in northeast Louisiana. Logging and agriculture-related businesses are struggling. Rental demand is strong, but new development struggles to generate cash flow due to the rate environment.

· Construction activity has decreased somewhat as a result of a lack of availability of workers due to Immigration and Customs Enforcement raids. Regulatory burden has eased as a result of the change in administration.

· Overall, commercial lending is very slow. We are not seeing commercial investments being made by small business owners. Consumer real estate lending is primarily second-lien home equity loans to customers who have low-interest-rate first-lien loans. Presently, our primary focus is to help meet the needs of the flood victims in our Kerrville and San Angelo markets.

· I expect increased nonperforming loans and repossessions, resulting in significant charge-offs, as a result of overpriced vehicles financed since the pandemic.

BY Doug Kass · Aug 19, 2025, 8:07 AM EDT

The excuse-making for these Sam Altman comments in my prior "Tales" yesterday is quite comical and shows you the degree to which people are drinking the Kool-Aid and are plugged to their eyeballs with investments in the space that they are trying to defend.

The excuse is Sam Altman is trying to discourage investment in the space, so he has less competition. How does that make sense?

* If this stuff is on the cutting edge of what is going to be the future, what does he care? Further, if there is going to be such insatiable demand for all things AI, what is he even worried about? That excuse in and of itself is damning. Sam Altman worried about too much capacity. Hmmmm

* A huge portion of the investment dollars and his competition is coming from public companies. Does he really think Google, Zuckerberg, or Elon Musk give a damn about what he says? Some of the other privates like Anthropic are also joined at the hip with the publics, like Amazon’s relationship with Anthropic.

* OpenAI is raising money hand over fist, it seems like they have to do a round every few months to stay in business. If he is trying to discourage investment in the space, how is OpenAI going to keep the doors open?

* Anyone with a functioning brain cell at this point has already figured out there is no path for Gen AI to turn into AGI anyway, so that part is not even news. I think he just Freudian slipped and was terribly awkward about it. I think even for someone who seems a bit pathological to some, at this point it is quite challenging (especially after GPT-5 just flopped) to say AGI is right around the corner...

I would love to see/hear a more critical assessment of my concerns in the business media — perhaps a bit more than having Dan Ives saying AI is now in the "second inning."

But that's just me!

BY Doug Kass · Aug 19, 2025, 7:30 AM EDT

BY Doug Kass · Aug 19, 2025, 6:55 AM EDT

BY Doug Kass · Aug 19, 2025, 6:45 AM EDT

BY Doug Kass · Aug 19, 2025, 6:30 AM EDT

* After EPS release...

Dougie Kass

Short HD (after EPS release and rally off lows) at $396.20.

BY Doug Kass · Aug 19, 2025, 6:10 AM EDT

* Decelerating EPS growth in back half of 2025...us

BY Doug Kass · Aug 19, 2025, 6:05 AM EDT

When "talking heads" are glib and sarcastic and criticize bears... the end could be nigh:

BY Doug Kass · Aug 19, 2025, 5:55 AM EDT

The S&P Short Range Oscillator stands at 2.23% vs. 3.31% — still overbought.

BY Doug Kass · Aug 19, 2025, 5:45 AM EDT