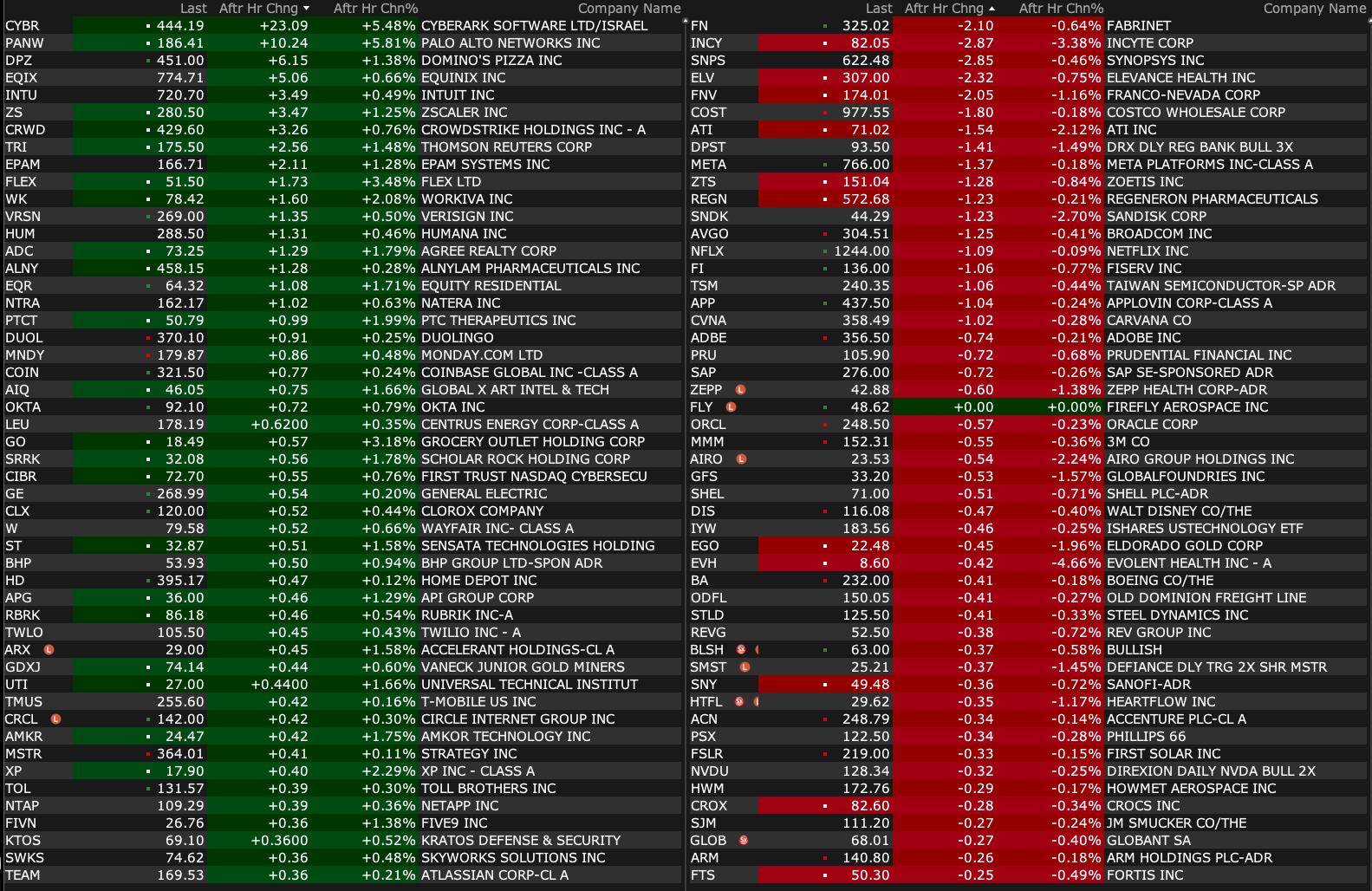

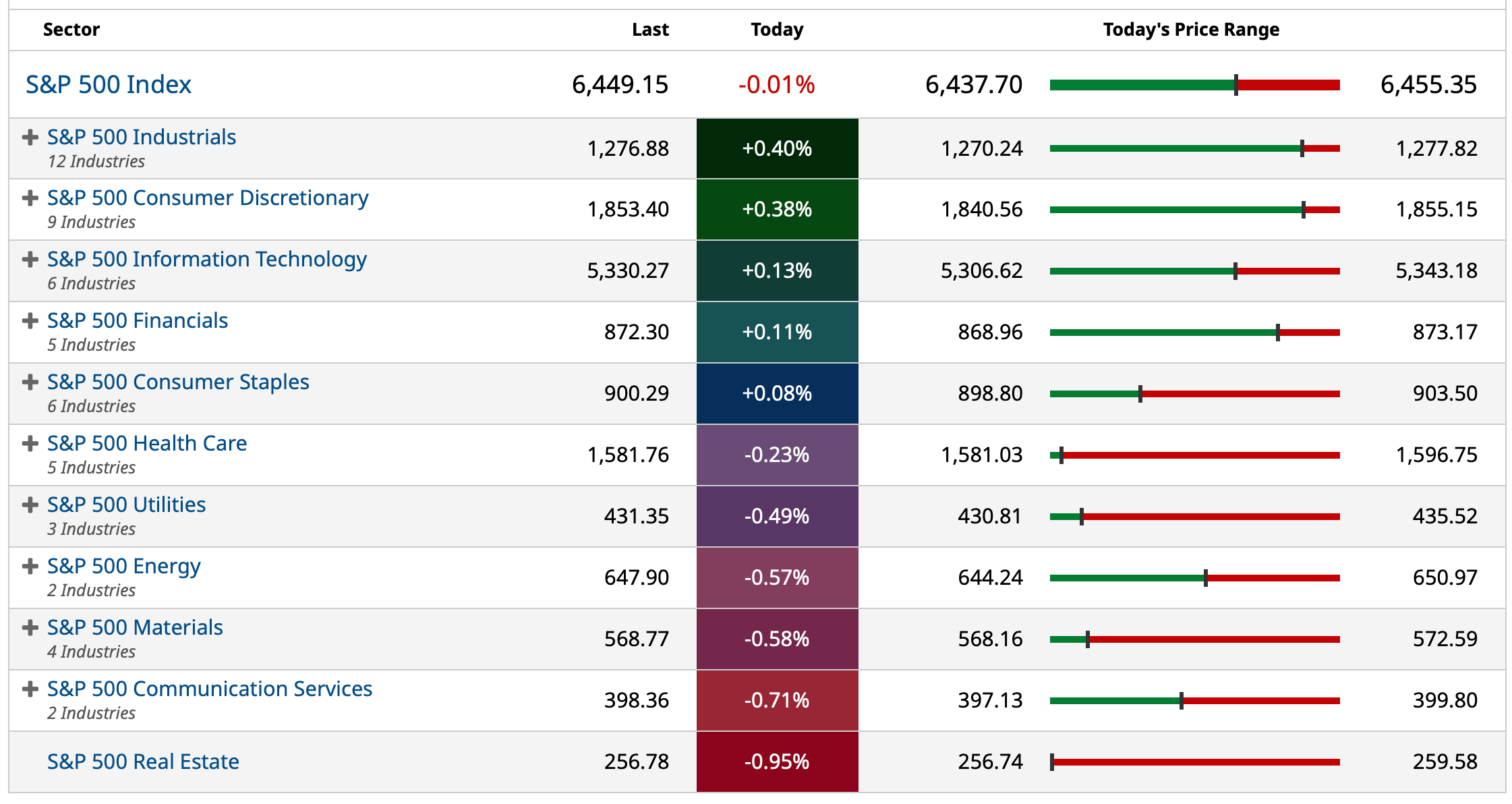

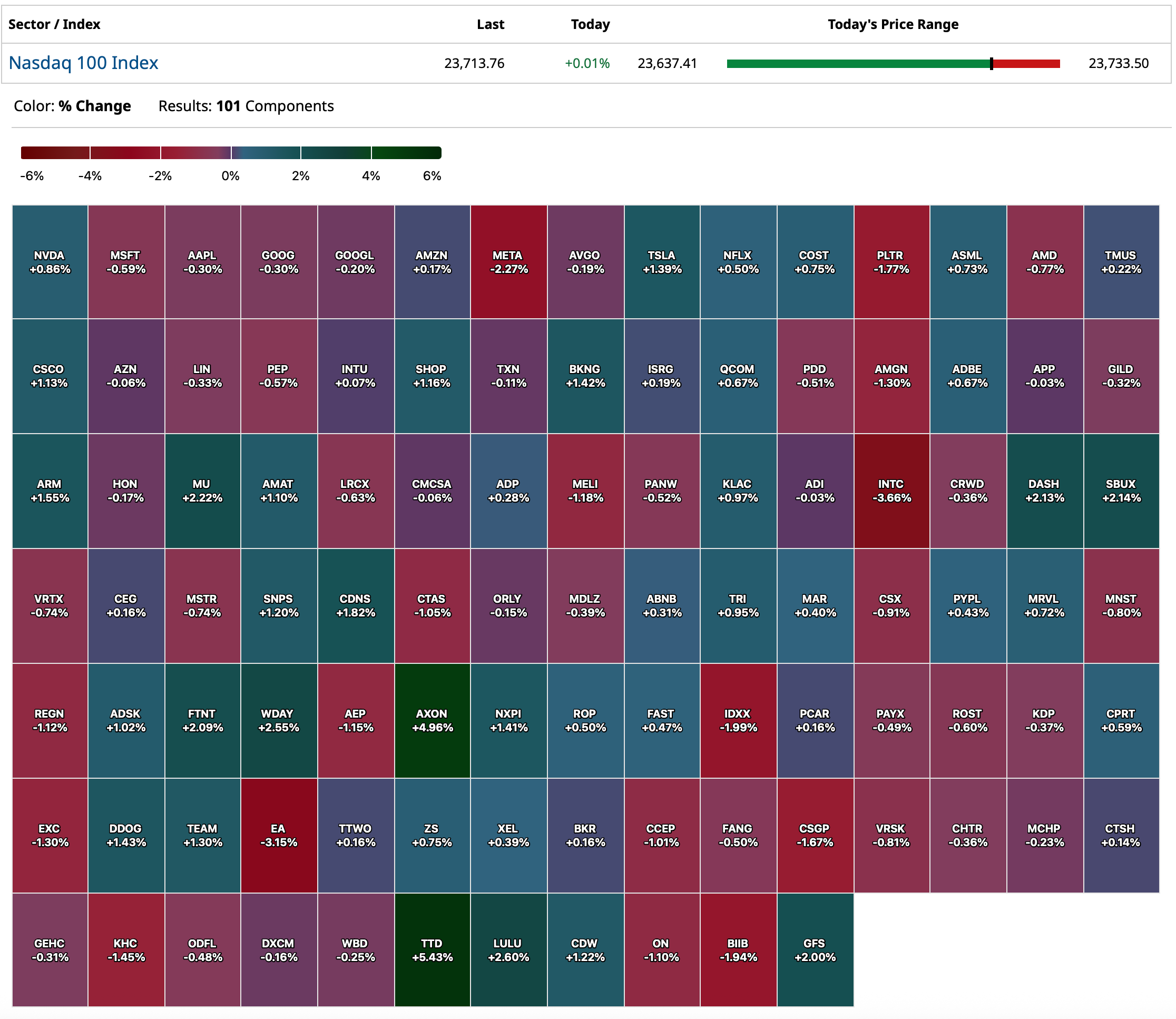

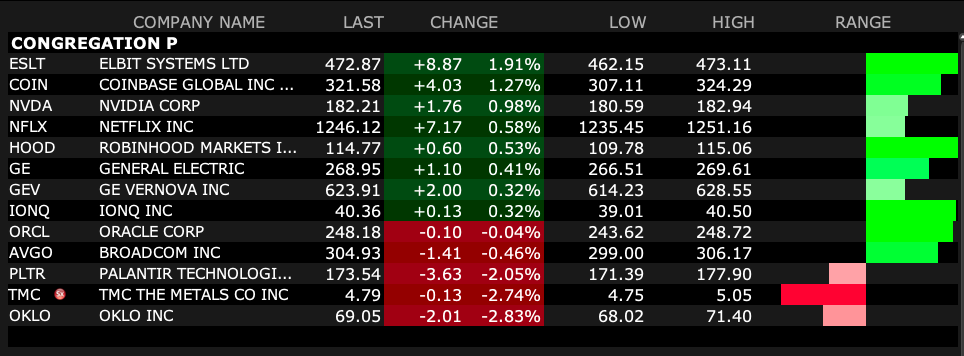

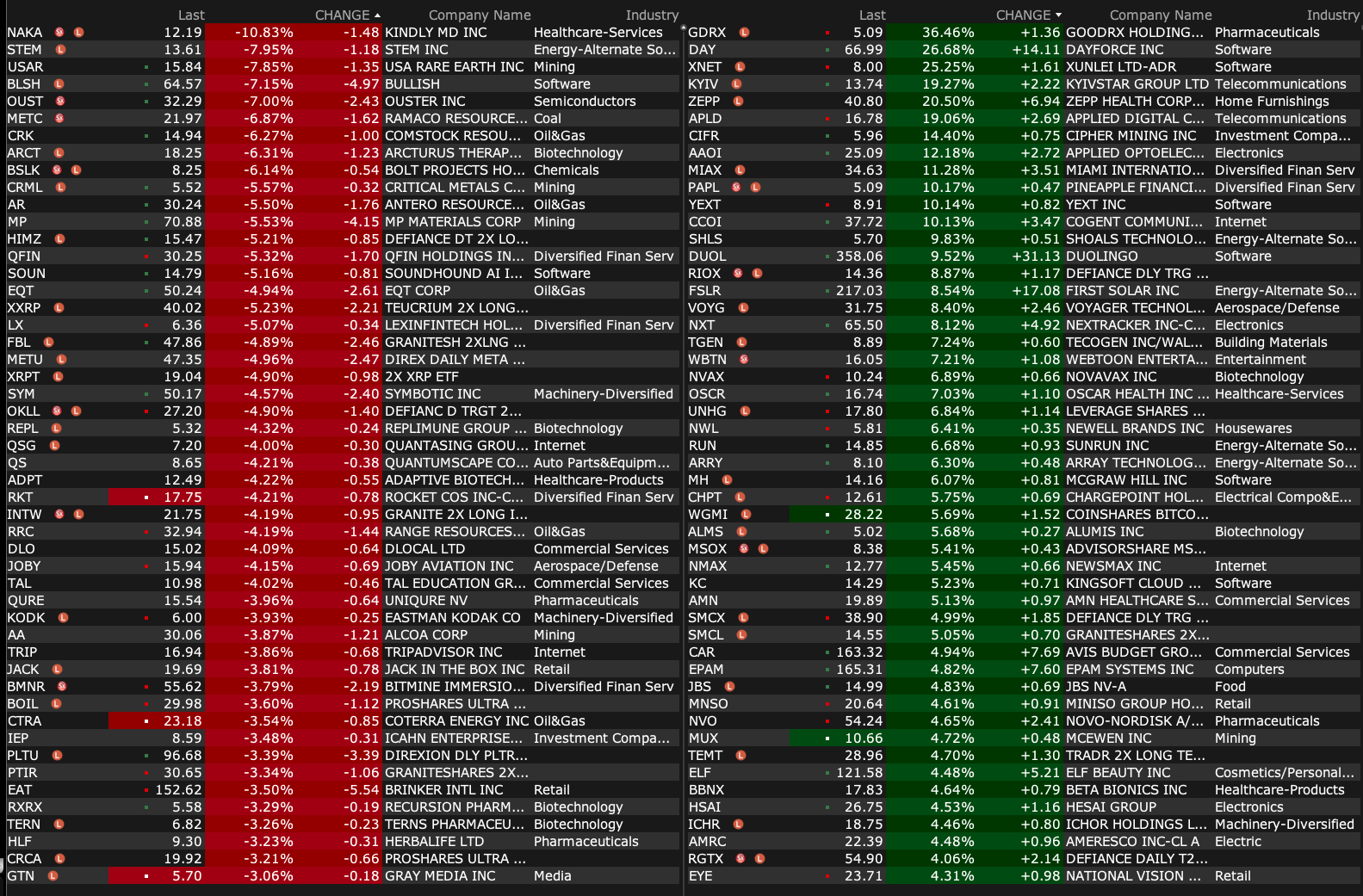

Monday's After-Hours Movers

As of 4:22 p.m.:

BY Doug Kass · Aug 18, 2025, 4:35 PM EDT

As of 4:22 p.m.:

BY Doug Kass · Aug 18, 2025, 4:35 PM EDT

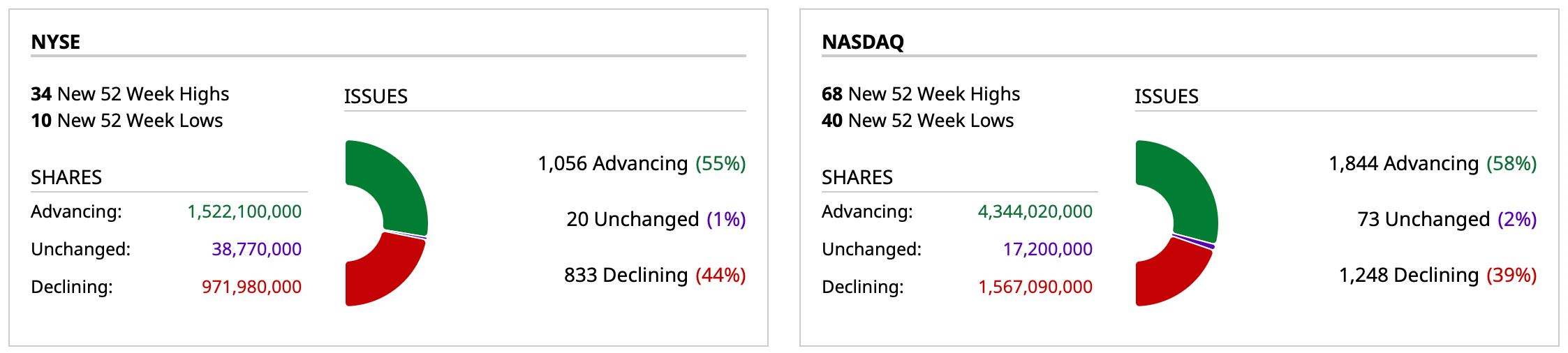

- NYSE volume 22% below its one-month average;

- NASDAQ volume 14% below its one-month average;

- VIX index: down 0.73% to 14.98

BY Doug Kass · Aug 18, 2025, 4:25 PM EDT

At 3:42 PM:

BY Doug Kass · Aug 18, 2025, 3:50 PM EDT

BY Doug Kass · Aug 18, 2025, 3:35 PM EDT

I am planning to shortly convert my short common in the indices to short calls. (In the money for September expiration to take in some premiums.)

BY Doug Kass · Aug 18, 2025, 3:15 PM EDT

With S&P cash now unchanged I am shorting index calls on SPY and QQQ.

BY Doug Kass · Aug 18, 2025, 3:05 PM EDT

WTF, after all the hype, Sam Altman goes on CNBC and says there is no such thing as AGI and compares the AI boom to the dot-com crash while at the same time he is trying to raise money again, this time at a $500 billion valuation. The world is truly upside down. And boy the U.S. government sure can pick em!

He has also begun questioning whether “artificial general intelligence” remains a useful term, saying it may be losing relevance despite earlier predictions it could arrive in the “reasonably close-ish future.”

“Are we in a phase where investors as a whole are overexcited about AI? My opinion is yes. Is AI the most important thing to happen in a very long time? My opinion is also yes,” he told reporters last week. “When bubbles happen, smart people get overexcited about a kernel of truth.” Altman compared the surge in AI spending to the dot-com boom of the 1990s, when hype drove valuations before the Nasdaq lost nearly 80% of its value.

Investor faith, however, hasn’t wavered. OpenAI is preparing a $6 billion stock sale valuing the firm at roughly $500 billion, just months after raising $40 billion at a $300 billion valuation — the largest private tech round ever.

"When Bubbles Happen...": Sam Altman Says AI Hype Compares To Dot Com Boom Before 2000 Crash

BY Doug Kass · Aug 18, 2025, 2:00 PM EDT

BY Doug Kass · Aug 18, 2025, 1:45 PM EDT

I have a 1 PM research meeting.

Back in about 45 minutes.

Radio silence.

BY Doug Kass · Aug 18, 2025, 1:07 PM EDT

BY Doug Kass · Aug 18, 2025, 12:37 PM EDT

BY Doug Kass · Aug 18, 2025, 12:10 PM EDT

I will be on Bloomberg tomorrow morning with Paul Sweeney and Sir Thomas Keene.

On Thursday afternoon, following the close, I will be doing Dave Rosenberg's podcast.

I have some things to say...

BY Doug Kass · Aug 18, 2025, 11:54 AM EDT

- NYSE volume 21% below its one-month average;

- Nasdaq volume 9% below its one-month average;

- VIX index: up 1.13% to 15.26

BY Doug Kass · Aug 18, 2025, 11:21 AM EDT

I am not a big fan of following hedge fund 13-F filings, as they are old and often outdated - but some like to see what the whales are doing:

Adage:

Top Buys: NVDA, MSFT, AVGO, AMZN, NFLX

Top Sales: AAPL, HES, UNH, MMM, VRTX

AllianceBernstein:

Top Buys: NVDA, MSFT, AVGO, SYK, AMAT

Top Sales: UNH, ZTS, COST, LLY, ANET

Alyeska:

Top Buys: GOOGL, CRWV, JPM, ANET, META

Top Sales: AMZN, CSCO, UAL, MDT, T

Ameriprise:

Top Buys: NVDA, AVGO, GOOGL, GILD, GS

Top Sales: AAPL, UNH, ABBV, CVX, XOM

Anomaly:

Top Buys: MSFT, INTU, GOOGL, FIVE, GIL

Top Sales: RH, AMZN, CNM, DHI, SKX

APG:

Top Buys: LQD, HYG, EGP, ESS, SBRA

Top Sales: ARE, EQR, REXR, DOC, IRT

Appaloosa:

Top Buys: UNH, NVDA, AMZN, TSM, INTC

Top Sales: SPYX p, AAPL p, PDD, BABA, FXI

AQR:

Top Buys: NVDA, AVGO, MNST, RBLX, PNC

Top Sales: AAPL, COP, CMCSA, CNC, JNJ

Balyasny:

Top Buys: QQQ p, MSFT c, BRO, AMZN c, ANET

Top Sales: QQQ c, IVV, SPY, SPY c, VTI

Barrow Hanley:

Top Buys: VRT, COF, ENTG, CCL, MCHP

Top Sales: ELV, UNH, J, CRH, HES

Baupost:

Top Buys: FI, ELV, DG, GOOG, CRH

Top Sales: WTW, EXP, SOLV, CLVT, SGI

Berkshire:

Top Buys: UNH, NUE, LEN, POOL, DHI

Top Sales: AAPL, TMUS, DVA, CHTR

Blackrock:

Top Buys: NVDA, AVGO, NFLX, AMZN, TSLA

Top Sales: PG, V, CVX, MRK, TMO

Blackstone:

Top Buys: TXNM, KMI, TLN, ENB, LNG

Top Sales: EXE, TRGP, SPY p, LOAR, TRP

Bridgewater:

Top Buys: NVDA, MSFT, GOOGL, META, UBER

Top Sales: BABA, SPY, PDD, BIDU, CEG

Brookfield:

Top Buys: BAM, TXNM, CCI, AWK, ENB

Top Sales: SRE, BABA, TRP, DTM, WES

Cal PERS

Top Buys: NVDA, MSFT, VOO, JPHY, AMZN

Top Sales: UNH, BRK.B, MCD, PEP, PG

Cal STRS

Top Buys: NVDA, MSFT AVGO, META, NFLX

Top Sales: UNH, XOM, CVX, DFS, FI

Candlestick:

Top Buys: QQQ p, AMZN, MSFT, AAPL p, SPY p

Top Sales: IWM p, HYG p, DAL c, UBER p, META

Capital International Investors:

Top Buys: MSFT, RBLX, RCL, KLAC, GE

Top Sales: UNH, AAPL, ABBV, DRI, ABT

Capital Research Global Investors:

Top Buys: NVDA, AVGO, SBUX, RCL, ORCL

Top Sales: UNH, GILD, AAPL, GEHC, CRM

Capital World Investors:

Top Buys: NVDA, MSFT, COF, META, NET

Top Sales: UNH, AAPL, DFS, LLY, AMZN

Caxton:

Top Buys: GLD, ELVN, BRK.B, RZLT

Top Sales: CRDF, LXEO, ACET

Cinctive:

Top Buys: FLR, BPMC, CFG, INFA, WMB

Top Sales: BECN, KS, ALGM, IEF, IEF c

Citadel:

Top Buys: MSTR c, NFLX c, NFLX p, QQQ p, COIN c

Top Sales: SPY p, SPY c, QQQ c, SCHW, IWM p

Coatue:

Top Buys: CRWV, ORCL, ARM, AVGO, CVNA

Top Sales: AMZN, META, BABA, TEAM, SMCI

Cohen & Steers:

Top Buys: DLR, SBAC, KRC, HST, KRG

Top Sales: AMT, OHI, AVB, UDR, PSA

Corvex:

Top Buys: WGS, SWX, QSR, AMZN, ORCL

Top Sales: DLTR, KOF, UGI, GOOGL, TSM D1:

Top Buys: CLH, NU, DHI, LPX, CRS

Top Sales: RCL, CP, SNPS, ELV, CRL

Davidson Kempner:

Top Buys: HES, AZEK, BABA debt, BPMC, ANSS

Top Sales: ITCI, BECN, FRPT debt, AKAM debt, IQ debt

D.E. Shaw:

Top Buys: NVDA, MU, NFLX, TMUS, AAPL

Top Sales: GEV, SCHW, INTU, TSM, HOOD

Delta Global:

Top Buys: MSFT, NVDA, PM, TOST, COF

Top Sales: BURL, HD, AXP, TEAM, WMT

Deerfield:

Top Buys: MRK, UTHR, VERA, LEGN, TNDM debt

Top Sales: ACCD debt, ALHC, DVAX, CMRX, NBIX

Discovery:

Top Buys: CLS, COF, QXO, JPM, AMX

Top Sales: DFS, GCAL, GDXJ, GEO, EAT

Driehaus:

Top Buys: CRDO, HDB, ALAB, STNE, CCJ

Top Sales: YUMC, SFM, BRBR, ESTC, CWAN

Elliott:

Top Buys: SPY p, NVDA p, HPE, HYG, SMH p

Top Sales: XLI p, BMRN, IWD p, MTCH, CSCO p

Eminence:

Top Buys: SPY p, CPNG, UNH, TSLA p, GTLB

Top Sales: PRMB, OKTA, ELB, SE, GEHC

Engineers Gate:

Top Buys: SJM, VTR, SBRA, CHD, UDR

Top Sales: PNC, HD, ECL, ABNB, LVS

Exodus Point:

Top Buys: QQQ c, QQQ p, NVDA c, IWM c, IWM p

Top Sales: TLT c, HYG p, SPY c, SPY p, XEL

Fir Tree:

Top Buys: RSP c

Top Sales: SPY

FMR:

Top Buys: MSFT, AVGO, META, GEV, TSM

Top Sales: AAPL, UNH, LLY, XOM, BRK.B

Fred Alger:

Top Buys: NVDA, NBIS, VST, TLN, RBLX

Top Sales: AAPL, GFL, V, APP, NRG

Freestone Grove:

Top Buys: GOOGL, BRO, LHX, ABT, VOO

Top Sales: IVV, HII, UMBF, BA, XOM

Glenview:

Top Buys: AVGO, MSFT, META, ORCL, NXPI

Top Sales: UNH, MCD, SBUX, TGT, MRK

Greenlight:

Top Buys: FLR, GPK, TEVA, CI, WFRD

Top Sales: VTRS, CNR, BHF, DLTR, PTON

HG Vora:

Top Buys: FUN, GVA, IQV, PRKS CLVT

Top Sales: FAF, BYD, MGM, UGI, WSC

Holocene:

Top Buys: IWM, AMZN, MSFT, NVDA, GOOGL

Top Sales: TSLA, CSCO, UNH, AAPL, AZO

Hudson Bay:

Top Buys: QQQ p, TSLA p, MSTR, NFLX c, AMZN p

Top Sales: MSFT p, IWM p, HYG p, AAPL, FE debt

Icahn:

Top Buys: CVI, CTRI, UAN, IEP

Top Sales: DAN, ILMN

Interval Partners:

Top Buys: SPY p, NSC, IWM p, SYY, WCC

Top Sales: SPY c, LUV, JCI, BURL, AMZN

Jana:

Top Buys: WEX, RPD, FRPT, THS

Top Sales: LW, FIS

Jain Global:

Top Buys: SPY p, XLK p, EEM p, XLF p, SPY c

Top Sales: IVV, XLE p, HYG c, HYG p, TLT c

Janus:

Top Buys: NVDA, MSFT, AVGO, CMG, DDOG

Top Sales: GOOG, AAPL, UNH, PGR, LLY

Kerrisdale:

Top Buys: UNH, WDC, ACMR, NE, DAVA

Top Sales: DEO, AMZN, MSFT, CSX, WAB

Land & Buildings:

Top Buys: GLPI, REXR, CSR, DHI, RHP

Top Sales: AIV, EQR, VICI, NHI, ELME

Lone Pine:

Top Buys: VST, UNH, EQT, BN, BKNG

Top Sales: LLY, TOL, INTU, CDNS, ARES

Longaeva:

Top Buys: HUM c, CAI, QXO, BRO, AS

Top Sales: SCHW, ETR, AEP, KKR pr D, ADT

Long Pond:

Top Buys: WH, NSA, IRT, CPT, BRSL

Top Sales: HLT, H, MTH, KRG, PLYA

Mane Global:

Top Buys: MSFT, ROST c, HAS, EAT, AS

Top Sales: PRMB, APP c, DASH, YUMC, CHWY

Marshall Wace:

Top Buys: CRCL, NVDA, AMZN, TMUS, DE

Top Sales: IVV, AAPL, TSLA, DHR, V

SCHW, MNST, META, GFL, DHR

Millennium:

Top Buys: QQQ c, NVDA p, SPY c, APP, MSFT c

Top Sales: IVV, QQQ p, AAPL p, CRH c, BAC

Miller Value:

Top Buys: GCI, JELD, BFH, CNDT, AXL

Top Sales: T, UNFI, TPC

Moore:

Top Buys: QQQ c, SPY c, MSFT, SPY p, NVDA

Top Sales: HYG p, QQQ p, IWM p, IWM, TLT c

Neuberger Berman:

Top Buys: MSFT, NVDA, META, AMZN, JPM

Top Sales: AAPL, BRK.B, KR, ACN, TMUS

NFJ:

Top Buys: GOOGL, PFE, UPS, UNP, OSK

Top Sales: MSCI, MA, UNH, AAPL, RBA

Nuveen:

Top Buys: META, NVDA, MSFT, GOOG, AMZN

Top Sales: CMRE, AAPL, NUGO, UNH, ATEC

Palestra:

Top Buys: PRMB, PGR, AMZN, CPNG, ANSS

Top Sales: FLUT, HSIC, LPX, CVNA, INTU

PAR:

Top Buys: CVNA, UAL, H, BKNG, SABR

Top Sales: UBER, CARG, LTM, CAR, UBER p

Paulson:

Top Buys: PPTA, BHC, JNPR, GOOG

Top Sales: MDGL, ITCI

Pentwater:

Top Buys: CAR p, SPY p, BPMC, SKX. UNH

Top Sales: X, ITCI, X p, BA, SPY

Pershing Square:

Top Buys: AMZN, GOOGL, BN, HTZ, HLT

Top Sales: CP

Pointstate:

Top Buys: PCG c, CX, ILMN c, EWY, XYZ

Top Sales: SPY p, WCC, RSP p, SRE, IWM p

Point72:

Top Buys: NVDA, MSFT, ANET, SNOW, BIIB

Top Sales: DHR, SPOT, SPY c, BKNG, META

Renaissance Technologies:

Top Buys: NVDA, NFLX, AAPL, GEV, UNH

Top Sales: AVGO, GOOGL, META, AMD, WMT

Rokos:

Top Buys: IWM c, QQQ p, MSFT, p, QQQ, IWM

Top Sales: CRM c, AAPL, DFS, GEV c, GOOGL

Ruane Cunniff & Goldfarb:

Top Buys: MSA, TSM, ICLR, AMTM, TECH

Top Sales: UNH, ELV, CACC, BRK.B, LBRDK

Schonfeld:

Top Buys: FBTC, IBIT, IWM c, NVDA, CAT

Top Sales: IVV, QQQ c, SPY, META, EEM

Soros:

Top Buys: QQQ c, SPY p, GPN debt, IWM p, XLP p

Top Sales: AZN, TLT c, SPY, AEP, AAPL p

Squarepoint:

Top Buys: QQQ c, HOOD p, AMZN, PLTR p, SOFT p

Top Sales: MSFT, IWM c, AAPL, QQQ p, IWM p

Starboard Value:

Top Buys: TRIP, IJH, CRM, IWM, BDX

Top Sales: KVUE, GEN, ADSK, HR, RIOT

Steadfast:

Top Buys: FND, POOL, ANSS, GOOGL, UBER

Top Sales: ROST, META, CMG, KR, LAD

Surgocap:

Top Buys: INTU, JCI, HLT, NU, HLT c

Top Sales: UNH, CRS, NOW, MCK, LPLA

Third Point:

Top Buys: NVDA, COF, COOP, VST, META

Top Sales: SPY p, EQT, X, DFS, T

Tiger Global:

Top Buys: AMZN, RDDT, CHYM, NVDA, AVGO

Top Sales: PDD, DASH, WDAY, NOW, TTAN

Tudor:

Top Buys: SPY, QQQ p, QQQ c, META c, BRK.B c

Top Sales: IWM, BA p, HYG p, K, XLE c

Trian:

Top Buys: FERG, WEN

Top Sales: IVZ, UHALB, ALL, UHAL

T. Rowe Associates:

Top Buys: NVDA, MSFT, AVGO, META, GE

Top Sales: AAPL, FI, LLY, TMO, XOM

T. Rowe Investment Management:

Top Buys: AMZN, APH, SBUX, META, HLT

Top Sales: FTV, MRVL, TMO, UNH, WCN

Two Sigma:

Top Buys: IGV, GEV, DUOL, UNH, QQQ

Top Sales: AVGO, SPY, MRVL, AMD, NOW

Valueact:

Top Buys: AMZN, SSD, MDB, COOP, RKT

Top Sales: NSIT, META, EXPE, DIS, RBLX

Vanguard:

Top Buys: NVDA, MSFT, AVGO, META, NFLX

Top Sales: CVX, DFS, FI, WELL, ADBE

Verition:

Top Buys: LQD, QQQ c, HYG p, QQQ p, XRT c

Top Sales: IVV, AMZN p, AMZN, NVDA, NVDA p

Viking Global:

Top Buys: DIS, APD, JPM, MCD, DHR

Top Sales: UNH, INTU, NFLX META, CB

Voya:

Top Buys: MSFT, NVDA, BSX, CAT, DIS

Top Sales: AAPL, CRM, PCG debt, LLY, UNH

Walleye:

Top Buys: QQQ p, MSFT, PLTR, SPY p, T

Top Sales: HYG c, HYG p, TLT c, NVDA p, SPY c

Wellington:

Top Buys: NVDA, MSFT, GOOGL, META, NDAQ

Top Sales: UNH, AAPL, PG, MRK, TMUS

Woodline:

Top Buys: MSFT, ALNY, NVDA, BRO, AJG

Top Sales: LRCX, MET, TRV, EA, ABBV Long AMZN VS UNH VS META VS

BY Doug Kass · Aug 18, 2025, 11:00 AM EDT

* Another lesson to be learned in "The Twilight Zone"

There is a fifth dimension, beyond that which is known to man. It is the middle ground between light and shadow, between science and superstition, and it lies between the pits of his fears and the summit of his knowledge.

This is the dimension of imagination, it is the area we call The Twilight Zone - where investors have seemingly crossed in recent months.

Opening Narration: Suspended in time and space for a moment, your introduction to Miss Janet Tyler, who lives in a very private world of darkness. A universe whose dimensions are the size, thickness, length of the swath of bandages that cover her face. In a moment we will go back into this room, and also in a moment we will look under those bandages. Keeping in mind of course that we are not to be surprised by what we see, because this isn't just a hospital, and this patient 307 is not just a woman. This happens to be the Twilight Zone, and Miss Janet Tyler, with you, is about to enter it.

Plot Summary: Janet Tyler has undergone her eleventh treatment - the maximum number legally allowed by the "State" - in an attempt to look normal. Her head is completely bandaged so that her face is entirely covered, and her face is described as a "pitiful twisted lump of flesh" by the nurses and doctor, lurking in the shadows of the darkened hospital room. The outcome of the procedure cannot be known until the bandages are removed.

Unable to bear the bandages any longer, Janet pleads with the doctor and eventually convinces him to remove them early. As he prepares, the nurse says that she still is uneasy about Janet's appearance. The doctor becomes displeased and questions why Janet or anyone must be judged on their outer beauty. The nurse warns him not to continue in that vein, as it is considered treason.

The doctor removes the bandages and announces that the procedure has failed, her face having undergone no change.

Janet is revealed to be a beautiful woman by contemporary standards while the hospital staff all possess monstrous faces with drooping features, large, thick brows, sunken-in eyes, swollen and twisted lips, and wrinkled noses with pig snout-like nostrils. Distraught by the procedure's failure, Janet tries to escape until a similarly attractive man named Walter Smith arrives to take her to a village of "[her] own kind" where they will not trouble the State.

As he does so, he assures her that while the State's society find her ugly, others will find her beautiful.

Closing Narration: Now the questions that come to mind: "Where is this place and when is it?" "What kind of world where ugliness is the norm and beauty the deviation from that norm?" You want an answer? The answer is it doesn't make any difference, because the old saying happens to be true. Beauty is in the eye of the beholder, in this year or a hundred years hence. On this planet or wherever there is human life – perhaps out amongst the stars – beauty is in the eye of the beholder. Lesson to be learned in the Twilight Zone.

"The Eye of the Beholder" episode (1959) of TheTwilight Zone Source: Wiki

As a child I was a huge fan of Rod Serling's Twilight Zone. I still am. The "Eye of the Beholder" episode reminds me so much of my contrary market view. Its a scary episode; one that I vividly remember as my parents were at our neighbor's house playing Canasta. My two sisters and I were alone. When I saw the faces of the nurses and doctors in the episode, I don't think I was ever so scared. I ran up to my sisters' room and Debbie (my famous artist sister) seemed to be sleeping with one eye open. That was it for me, as I ran crying to get my parents' attention next door....

Cue, The Twilight Zone's opening theme.

What is beauty? Equity bulls see plenty beauty:

1. Equities are in a new secular bull market.

2. The U.S. economy is recession-resistant because we are in a service economy and owing to the likely intermediate-term benefits of AI.

3. Tariffs are a one-off, that they contribute to an ever increasing stacked or cumulative inflation (since Covid) is irrelevant.

4. The (now weakening) U.S. housing market (which has presaged every recession) should be ignored as there will be a Fed put upon the assignment of a new fed chairman.

5. Charts over fundamentals. Balance sheet and income statement analyses are passe. Value investing is dead and so is the need for rigorous securities analysis.

6. Weak market breadth should be ignored - despite lessons from history - as concentrated strength begets strength is an investment landscape populated by passive products and strategies that worship at the altar of price momentum.

7. Every dip is an opportunity because "cash is trash" and there is a record level of cash on the sidelines ($7 trillion) that will dull any market decline and be a powder keg for further market advances as interest rates decline.

8. There are no concerns with regard to a large market drawdown (See Susan Berge's comments earlier).

9. Excesses are permanent in the new investing paradigm, a 24-times price to earni is a reasonable launching pad for future investment returns (though history dictates otherwise).

10. A top-heavy tech market is no problema - though Mag7 companies have morphed from being capital lite to capital intensive (reflecting massive AI capital expenditures).

11. Massive AI investments will result in large return on investment for the hyperscalers, producing significant productivity gains for the U.S. economy.

12. The Administration's "pay for play" is acceptable policy - and so are picking company/industry winners and losers a sound idea.

13. Fundstrat's Tom Lee will inherit the Earth.

By dismissing sticky inflation and slowing global economic growth (among other issues) it seems many investors have indeed crossed over to The Twilight Zone and have raised valuations to scary (98%-tile) levels as expressed in my August column -- which I am reposting in its entirety because of its meaning and possible consequences:

AUG 5, 2025 1:00 PM EDT

There Are No New Eras. Excesses Are Never Permanent.

* From my perch, equities are more overvalued than at any time this year.

* Current valuations are a poor launching pad for future investment returns.

* "Slugflation" likely lies ahead — as domestic economic growth is moderating and inflation is sticky.

* We see numerous cracks in forward-looking global economic fundamentals, an unclear path of U.S. corporate profit.

* Speculation has run amok with the proliferation of 0DTE options, meme stocks, Palantir (100x revenues), dip buying, etc. have led to a suspension of fear, doubt and skepticism.

* Everyone (especially "The Kids Today"), it seems, now worship at the altar of price momentum — a condition previously seen in the Winter of 1999, the Summer of 2007 and in late 2021.

"Lesson #3. There are no new eras—excesses are never permanent."

- Bob Farrell's Rules of Investing

What follows is a summary of some of my recent Daily Diary contributions on TheStreet Pro and selected correspondences with my hedge fund investors at Seabreeze Partners.

God's Plan

Skepticism and doubt have left Wall Street.

To learn from history it is helpful to go back in history.

“Once a bull market gets underway and once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks. In effect, these people superimpose an I-can't-miss-the-party factor on top of the fundamental factors that drive the market. Like Pavlov's dog, these "investors" learn that when the bell rings - in this case, the one that opens the New York Stock Exchange at 9:30 a.m. - they get fed. Through this daily reinforcement, they become convinced that there is a God and that He wants them to get rich.”

- Warren Buffett, “God’s Plan” (November 1999)

The Oracle of Omaha delivered the above quote only a few months before the end of the dot-com boom. Arguably, it may apply to today’s markets.

Buffett’s warnings should have been heeded, as, by March, 2000, the Nasdaq made a seminal top and commenced on a sutherly route that would result in a -80% drawdown in that index.

Twenty eight years ago I wrote an editorial in Barron's, Kids Today — the zeitgeist today is similar to that 26 years ago near the end of the dot-com boom:

"Being over 40 years old has been a liability in the Bull Market of the 1990s. ... I want to be like Sheldon The Kid and the rest of the kids in the 1960s and 1990s — trading in and out and relentless buying all dips, paying 15x revenues for tech stocks, disregarding value and common sense — but I can't."

- Doug Kass, "Kids Today" editorial in Barron's, July 7, 1997

https://drive.google.com/file/d/17y0Fv708jPFHx-LZk2G__y24fxv0lwyl/view

A decade later another vivid illustration of the acceptance of "God's Plan" was made in an infamous quote by Citigroup's former CEO Chuck Prince in July, 2007 — a few months before the Great Financial Crisis, which also led to an unprecedented market decline in percentage terms and in time:

"When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you've got to get up and dance. We're still dancing."

Voltaire said that “History never repeats itself. Man always does.”

I am blinded by a sense of history.

In both the Winter of 1999 and in the Summer of 2007 day traders and speculation ran amok and a rising market was an almost accepted part of the zeitgeist.

Conditions today are clearly much different than in 1999 and 2007 — today's market leaders are healthy/profitable companies with deep moats (and not companies with no or limited futures).

We don’t expect anywhere near the declines of 2000-23 or 2007-09. However, we do expect an extended period of substandard to negative returns — an ideal backdrop for a long/short hedge fund, like Seabreeze, that is comfortable with a short book.

Investors face a host of secular headwinds that could be more long lasting than even at prior market peaks — the most important of which are:

* A rising probability of "slugflation" (prickly inflation, disappointing economic growth).

Prickly Inflation: Despite the slowdown in the domestic economy, recent reports suggest a possible reacceleration in the rate of growth of inflation. Tariffs will not help in the time ahead. (See my comment on tariffs later on in today’s commentary)

An acquaintance made some good points to me over the weekend (edited):

To put Fed 2.0% inflation target in proper perspective, to reach 2.0% inflation is not reality.

From 1965 to 2024 inflation averaged 3.9%. The last time inflation was generally low and not due to a crisis of some kind was the sixties. It was 1.6% in 1965 when the economy was booming at 6.5% GDP growth. Then again in 1986 as Fed Chair Volcker was coming to the end of his inflation crushing interest rate program, so not a normal period. In 1998 it was 1.6% when the economy was doing well and there was a trove of new technology being introduced which helped improve productivity. GDP grew at 4.2% real growth. Then from the period of the GFC 2009-2016 it was under 2.0%. But again, that was a very unusual period of financial market meltdown and grave financial crisis when the banks and Wall Street were essentially out of the market. Then in 2002, right after 9-11, so again, not a normal period. If we look for periods comparable to today when inflation was 2.0%, there are almost zero. We must ask where did this 2.0% target for the Fed come from and how did that number become the gospel. Achieving it based on history is not realistic. Perhaps the entire premise the Fed is operating under of needing to reach 2.0% is a fantasy that is unlikely to be achievable so long as the economy is growing. It would only be achievable if there is a deep recession or another financial crisis like 2009. 3.0% is a realistic target and we are there now with PCE at 2.6%, so rates should come down.

Possibly we can have 2.0% inflation someday once AI is much more widespread and productivity is even higher than today and GDP is growing at 4.0%. But we are not there now and with tariffs we are not going there anytime soon.

Many recall the Humphrey-Hawkins Full Employment and Balanced Growth Act of 1978 – a landmark legislation designed to address unemployment and promote economic stability. That bill set the goal for inflation to be at 4% by 1988. The lesson was that Congress cannot set inflation rates just as these rates cannot be legislated today.

Disappointing Economic Growth: All traditional signposts (labor reports, ISMs, etc.) point to a slowing U.S. economy and a challenge to the wrong-sided bullish notions that macro-U.S. data is resilient, S&P EPS growth will be robust and the trade war rhetoric is improving.

I won’t repeat the multiple macroeconomic and company/sector examples of a growing slowdown but I would add something that I have found to be one of the best predictors of growth — Las Vegas tourism. And, on that score, we should also be cautious on a consumer-based economy.

The consumer is spent up, not pent up.

(We have numerous consumer sector shorts in our Seabreeze portfolio).

Representatively, this is from Colgate-Palmolive’s (CL) 3Q2025 EPS release (hat tip Peter Boockvar). Colgate makes things we use every day like toothpaste, deodorant, soap, and shampoo.

"There is a persistently cautious consumer in North America right now. We saw some rebound in April, May. The categories took a little step back in June, which we weren't expecting."

"Many of our markets and categories around the world remained challenging in the second quarter and we expect this to continue through the second half of the year."

"The cost environment is difficult as we're dealing with tariff increases, higher raw and packaging material costs, and less underlying category inflation. This means that our revenue growth management strategies need to drive additional pricing and mix with lower levels of elasticity as we look to improve organic sales growth in the second half of the year."

* The rate of corporate profit growth will markedly decelerate in this year’s second half

* Undisciplined fiscal policy by both parties that will likely lead to a continued and large deficit, adding to our nation's debt load

* Political and geopolitical polarization and competition will probably translate into less political centrism and a reduced concern for deficits — creating structural uncertainties, limited fiscal discipline and imprudence around the globe ... and for the possibility of bond markets to "disanchor"

* Equities are overpriced against interest rates: The equity risk premium is at a two-decade low — typically consistent with a slide in equities. (Given the plethora of uncertainties (many of them adverse), risk premiums should be rising, not falling!) The S&P dividend yield is at a near record low of 1.27% — and the spread between the dividend yield and the 10-year U.S. Treasury note yield has rarely been as wide.

* Valuations that are in the 98%-tile, a poor launching pad for future investment returns: The S&P Index’s trailing P/E multiple now stands at 26x — taking out the 23x peak of late 2021 and similar to the valuation reached in August 2000 (right before a two-year bear market commenced). The current multiple is more than +30% above the long-run norm. This is even more disquieting in that the real risk-free interest rate (at more than two percent) is double the historical average.

Over the last few weeks the markets have been buoyed by, among other factors, the Trump administration's "tariff" agreements which have been viewed by market participants as a big net investment positive.

We strongly are of the view that tariffs represent a bonafide threat to economic growth.

Most recently, the energetic reaction to a series of economically unfriendly tariff announcements and "agreements" are an exclamation point of unbridled and, arguably, poorly analyzed blind political and market enthusiasm. Moreover, the goal posts have been constantly been moved (in attempts to represent tariff policy success).

From John Mauldin ( "Thoughts From The Front Line) over the weekend in "Uncertainties Squared" Uncertainty Squared - Mauldin Economics:

“I know very few bullish investors who think tariffs are good. Mostly, they see tariffs as the “least bad” response to an intolerable situation. They recognize the ill effects but believe the tariff pain will end soon. (More on that below.) In this view, the current confusion and chaos will lead to a new equilibrium that is manageable and maybe even positive. They don’t think it will be bad enough to derail the other bullish factors like AI technology. If that’s what you believe, then it makes sense to take advantage of current bearishness to buy more. I’m not in that group but I understand their thinking. What I don’t see is reason to think the tariffs lead to even a neutral outcome, much less a good one. I’ve gone over the reasons before and won’t repeat them now. (Read this if you’re interested. It is my letter from April 25 and realize how much change there has been since then. Rather astonishing, really.)The best case I can imagine is that tariffs will raise import prices for American consumers enough to show up as higher inflation but not enough to trigger a recession. Because I think even 2% inflation is too high and robs all of us, I don’t see that as a good trade-off. Further, the way all this is being done makes the hoped-for manufacturing revival more difficult in reality than it is in the theory that some political types believe. I would also note that bulls keep moving the goal posts. Stocks rallied back from their April crash because Trump postponed the highest tariff rates for 90 days, during which he was going to negotiate a bunch of great deals with our top trading partners. The 90 days passed with no significant deals. Now we are told higher rates are coming in August, but traders seem to think those rates won’t happen, either. Maybe they’re right. But other governments are planning their retaliatory moves, and this could easily spiral into a broader trade war. Hopefully cooler heads will prevail, and we won’t end up with a repeat of the spiraling Smoot-Hawley tariffs. I get the idea of “seeing through” short-term volatility. My problem is with the “short-term” part. I just don’t see the finish line. I assume one is out there. I don’t think it is near.”

The unjustified bows taken by the current administration were recently outlined in The Financial Times:

“Anyone surprised by this? Thinking equities will keep going up once the great negotiator finishes the most amazing beautiful deals with Europe and others might be in for a rude awakening.

“I just signed the largest trade deal in history, I think maybe the largest deal in history, with Japan,” Trump boasted Tuesday. But a new report from The Financial Times demonstrates that U.S. and Japanese officials don’t see eye to eye on what exactly the countries agreed upon.

According to Trump and his administration, in return for a reduction in tariffs, Japan would invest $550 billion in certain U.S. sectors and give the United States 90% of the profits.

Japanese officials, however, say the profit sharing isn’t so set in stone: A Friday slideshow presentation in Japan’s Cabinet Office, contra the White House, said profit distribution would be “based on the degree of contribution and risk taken by each party,” according to The Financial Times.

The FT also reports conflicting messages between Washington and Tokyo as to whether that $550 billion commitment is, as team Trump sees it, a guarantee or, as Japan’s negotiator Ryosei Akazawa sees it, an upper limit and not “a target or commitment.”

Mireya Solís, a senior fellow at the Brookings Institution, told The Financial Times that the deal contains “nothing inspiring,” and that “both sides made promises that we can’t be sure will be kept” and “there are no guarantees on what the actual level of investments from Japan will be.”

The inconsistent interpretations of the deal could be because it was hastily pulled together over the course of an hour and 10 minutes between Trump and Akazawa on Tuesday, according to the FT, which cited “officials familiar with the U.S.-Japan talks.” And, moreover, “Japanese officials said there was no written agreement with Washington—and no legally binding one would be drawn up.”

Does Trump’s so-called “largest deal in history” even count as a deal at all? Brad Setser, senior fellow at the Council on Foreign Relations,

“Well-nigh two thousand years and not a single new god!”

- Fredrich Nietzsche, The Antichrist (1888)

Another possible threat has emerged — the investing world almost universally believes it has discovered a new god in artificial intelligence and machine learning.

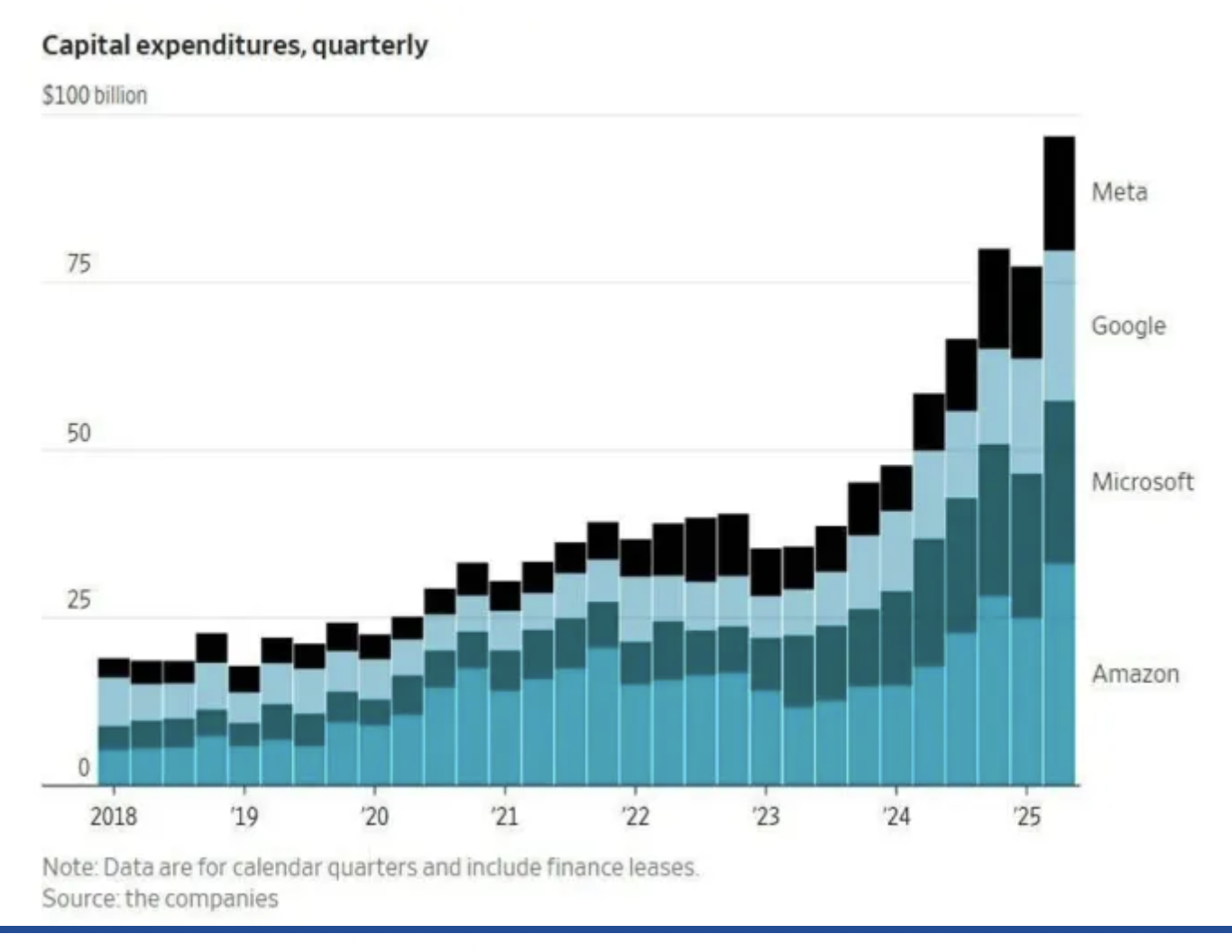

In dollar terms the AI outlays eclipse anything in history — with the four hyperscalers (Google (GOOGL) , Meta (META) , Amazon (AMZN) and Microsoft (MSFT) ) undertaking a spending orgy by committing almost 60% of their 2025 cash flows (approximately $300 billion in 2025) on AI capital spending.

Putting this into perspective, AI infrastructure CAPEX is already 20% higher as a % of GDP than what was spent on telecom and internet infrastructure at the peak of the dot com boom. For Microsoft and Meta, CAPEX is now more than a third of their total sales. Astonishingly and according to Neil Dutta (head of economic research at Renaissance Macro Research), capital spending for AI contributed more to growth in the U.S. economy in the past two quarters than all of consumer spending.

The depreciation schedules being used for this AI spend is somewhere between aggressive and absurd. One company, CoreWeave (CRWV

) , is reporting earnings before capital expenses!

I share the following concerns expressed over the weekend by The Credit Strategist:

“Anyone who questions AI faces the challenge of answering technology experts (genuine and self-proclaimed) who claim superior knowledge of the topic. But the projections on which future AI revenues and profits are based remain highly speculative because they are based on events that have yet to happen; put bluntly, they are based on predictions about the future that is always unknowable. But one characteristic of the future that is knowable is that it is reflexive, meaning human beings and organizations react and adjust to changes rather than remain static. As such, arguments that AI will eliminate jobs without creating new ones or arbitrage away margins without creating new margin opportunities are questionable. Further, it is unlikely that multiple LLM models addressing the same market will all prove successful; more likely, ruthless competition will create a small group of winners and many losers with a great deal of capital consumed in the process.

The quantum of AI spending dwarfs anything previously applied to a specific product or sector in such a concentrated period of time. All of this spending has yet to produce a commensurate amount of revenue or profit but we are still in early days and investors are convinced that it will. Whether the world needs numerous LLMs that perform similar tasks remains to be seen; it’s not clear that these models can meaningfully differentiate themselves despite spending hundreds of billions of dollars attempting to do so. As Fred Hickey writes in The High Tech Strategist (highly recommended): “revenue generation for the LLM builders is limited (they’ve not found killer apps for the masses) and the losses are unlimited. The capex would be destroying their company P&Ls – except for the fact that the chips and equipment costs are spread out over several years via depreciation expensing.” The fight for dominance and first-user advantage will continue to the bitter end. Some are projecting that annual AI spending could increase even further but I suspect it may end up tapering off if it doesn’t generate promised returns before long.”

To summarize, while Mag 7 and AI-related equities have dominated the market’s advance and participants’ attention over the last two years, AI has yet to demonstrate it will save the world. Any change in attitude towards these companies could send markets reeling lower.

S&P 500 Index over past 4 years

We see numerous cracks in forward-looking global economic fundamentals, an unclear path of U.S. corporate profits, coupled with extended valuations (both absolutely and relative to interest rates).

BY Doug Kass · Aug 18, 2025, 10:30 AM EDT

From Peter Boockvar:

I argue again that the best path Jay Powell can take in his speech Friday, and something I recommend too to his colleagues, is to focus on the September meeting only (basically telling us you'll cut as the market expects) and not prognosticate about what you'll do after that because the economic landscape is clear as mud. Non voting member taking Raphael Bostic is taking that same tact, especially after a three day trip visiting households and businesses in meetings in Alabama and Mississippi, regions he covers. "Today, I think my strategic approach would be 'move and wait.' It might be that it will take some time for the economy to evolve after a move that we do, in ways that make clear sort of what the next step would need to be" he said late last week.

According to the Bloomberg News story that covered this trip, it also said "Tariff costs are actually real costs," he said. While many firms have absorbed some of the shock to shield consumers, "they don't think they can do that forever," said Bostic. "And time is getting short."

I agree with the theoretical economic concept that a tax (tariff in this case) is a one time price reset but I'll also argue that it is much more nuanced than that as if supply chains get shifted and tossed around in response to tariffs, the price impact can be multi year.

Here's a great example I read about in the Weekend WSJ on an article about tariffs and inflation. "Barry Roth, who imports used cars from Canada for US dealers, says he imported around 1,000 cars a month on average last year through November. In January, that surged to almost 1,500 as car dealers tried to get ahead of tariffs. Now, as many cars from Canada face 25% levies, he says he is lucky to import 400 vehicles a month."

"But as dealers sell down their expanded inventories, they will either have to pay the tariffs or be left with fewer cars to sell. Either way, he says, prices are likely to rise. 'It's not going to happen tomorrow, it's not going to happen next week, but it will ratchet up,' Roth said."

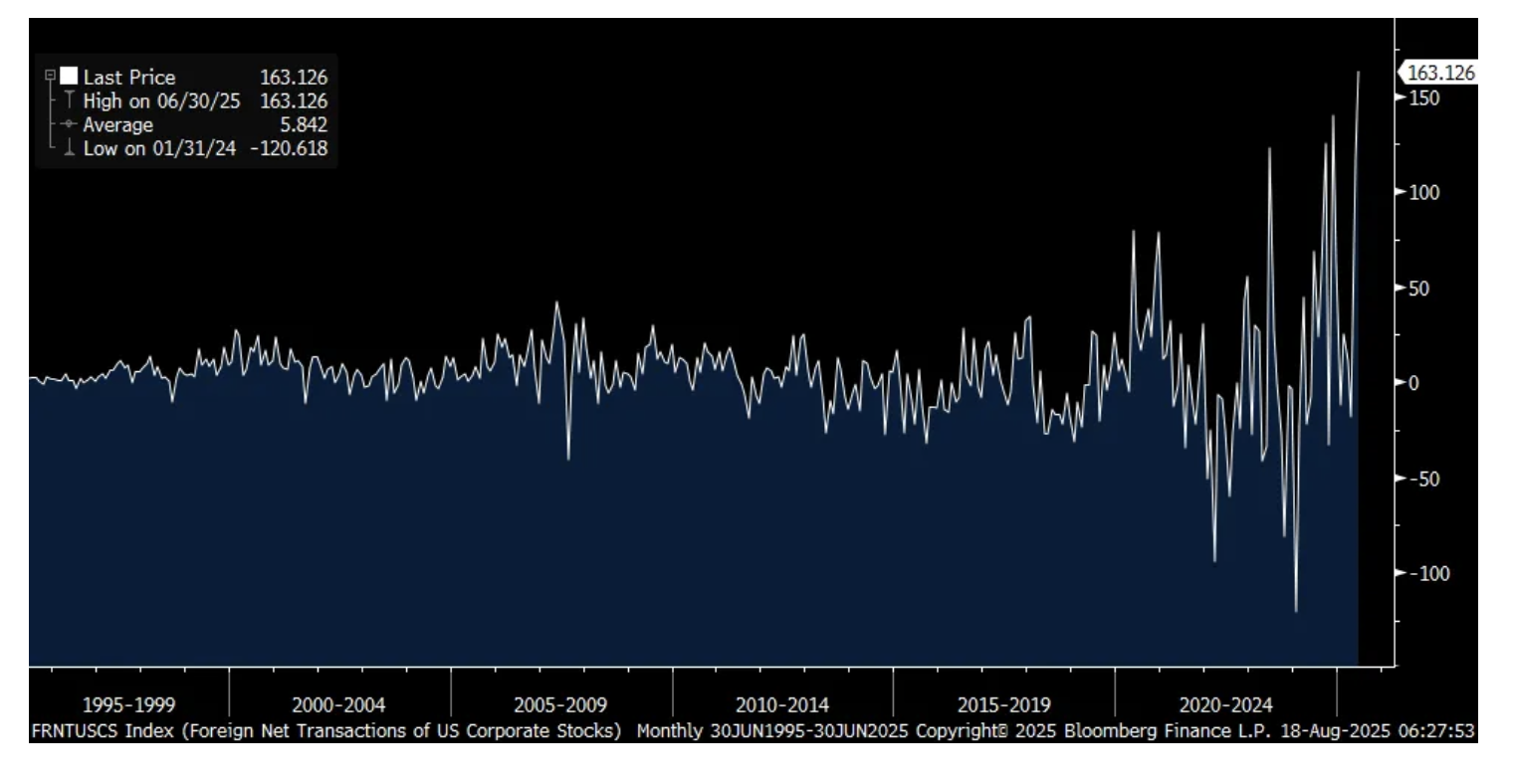

Seen Friday was the June TIC data reflecting foreign purchases of US assets and vice versa. While foreigners sold on net US Treasuries by $5b after a large rebound in May, they gobbled up US equities. In fact, with US stocks, they've never bought this much in any one month, purchasing $163b worth on net. Let's hope they are not a contrarian indicator because they bought a record amount, at the time, in February 2000 and did so again in May 2007. On the other hand, they used pullbacks in 2020 and 2022 to add.

Foreign Purchases of US Stocks

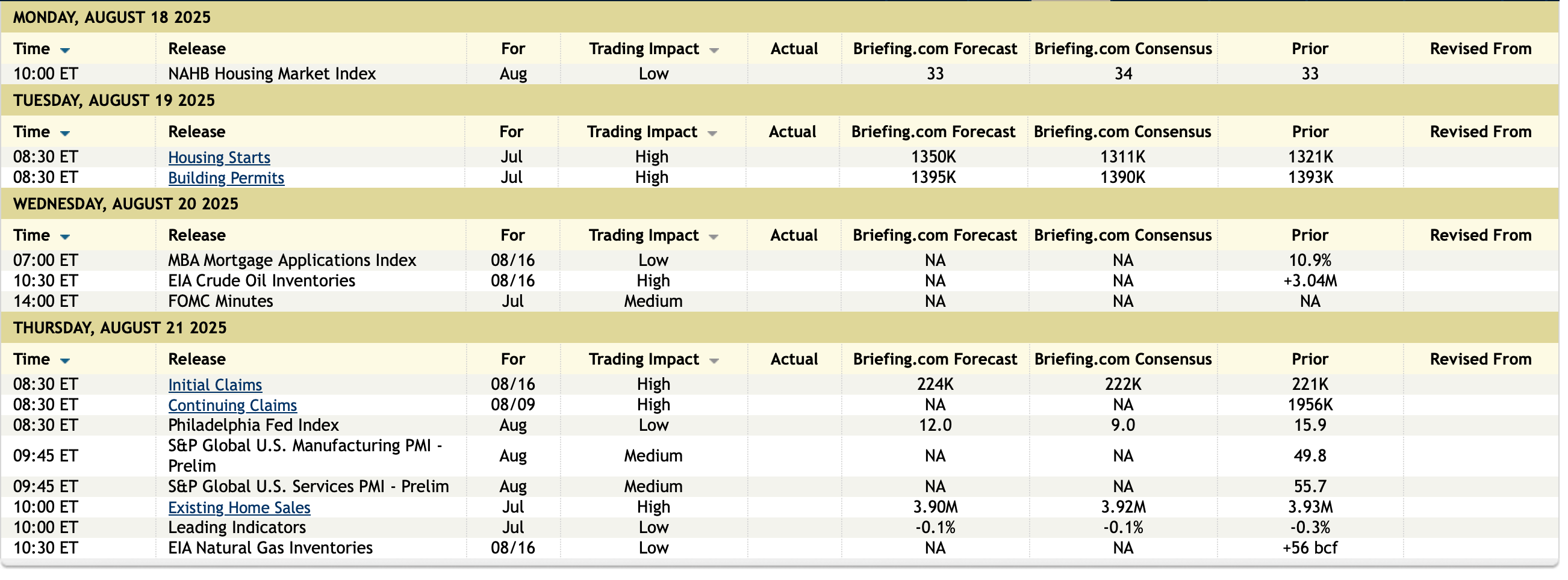

It's quiet otherwise ahead of big retail earnings this week and Mr. Powell on Friday.

BY Doug Kass · Aug 18, 2025, 10:15 AM EDT

As far as circles to square are concerned, how can the PPI show substantial inflation and an acceleration, while the CPI shows that inflation is tame at the same time?

First of all (as I have noted in "Inconceivable!") the CPI was not nearly as tame as the numbers were spun to be.

It is like earnings with these economic stats now, where a number is purposely set at a point where it can be beat. Markets react to the gimmicked beat, as opposed to the quality of the actual number, and what it showed. I reiterate:

“I never thought I would see the day when inflation coming in at 2.7% (and +0.2% month over month) was considered good. Even worse, Core CPI, which is what we are meant to care the most about, was hotter than expected at 3.1% (and +0.3% month over month), and is now accelerating again. Super core was up 3.59% year over year, the hottest since February and also accelerated (up 0.55% month over month). “

At any rate, it is clear what the hot PPI showed. One can infer, more CPI inflation is coming, even with a CPI that is designed not to show it.

This morning's commentary is not about whether or not tariffs are a good or bad idea, it is about what is going to happen. We learned during the period of post-Covid inflation (that still sadly has not ended because all that money is still floating around and the government budget is still through the roof) that corporations have an amazing ability to put price through. There was zero margin compression in the S&P. In fact, many companies had margin expansion during this period.

Talk to any executive at a company that has their supply chain in China or anywhere else that is affected by tariffs. They will tell you they are about to put price through. It has just been time delayed, because they account for their inventory on a FIFO basis. They had low-cost pre-tariff inventory, which they have now sold through. What is coming in at the higher input price is about to be sold through at the higher output price. Just watch. They did it post Covid, they will do it now. Industries are consolidated enough, that this can happen. A huge part of exec compensation is stock based. They can’t have margins go down. It has been proven.

Tick tock, it is coming.

As far as why so much of our production has moved abroad (and why we now have tariffs), it was a huge mistake to move so much production to begin with. Moving everything to China was never cheaper, when measured on a full system basis. The world is not as simple as the David Ricardo wine-and-cheese theory of comparative advantage that we learned about in our first economic class that we were sleeping through.

Some production that went abroad certainly should have and fell in line with this theory. Other production went for different reasons. Many important things went offshore because of favorable tax treatment and the ability to pollute like crazy, which is a massive cost savings, but not part of the wine-and-cheese theory. When something is made in China, it needs to be shipped back here, which costs time and money. Semiconductor manufacturing is all capital and chemicals, there is almost zero labor in the final cost. I have seen it out there, including the noxious chemicals being poured out the back door into the ground. The fact that semiconductor manufacturing is very capital intensive is why a fair bit of it remained in the U.S., and why it is one of the first things to start coming back. Numerous industries went abroad that fall into the bucket of being abroad for reasons other than pure wine and cheese. It has been very one sided in this regard too.

Many things went abroad for corporate accounting reasons, not wine and cheese reasons.

Bigger picture though, which nobody talks about, is the cost shifting. When this happens at such a rapid rate, that the jobs are not replaced, the lower cost of goods that a corporation has are more than offset by the entitlement cost of the unemployed, that end up on the governments balance sheet. The unemployed also often become discouraged workers, who magically disappear from the numbers, and end up out on the streets, the cost of which is also huge on many levels. Many also seem to learn they don’t need to work, because the government (vote buying) will bail them out to some degree, and we have a society that just decays.

Then, we have enabled the creation of an enemy superpower. There is now huge cost to dealing with China and their impact on the world. Our defense budget is a good example. Dealing with the global instability that China helps create is another. Who do you think is buying the Iranian oil and re-supplying them with missiles and other stuff? The cost to all of this is massive, but again, hidden on the governments ever-growing balance sheet.

Further, not everything is about cost. Insurance is a cost, yet we all have health, auto and home insurance. Putting the entirety of certain supply chains abroad in enemy territory is the opposite of having insurance. Stupid. There is a huge policy cost to dealing with this issue too. It really limits our ability to strategically do things that we need to be doing.

Nobody talks about any of this, but at the end of the day all the offshoring has been a disaster. Corporates benefitted from it, but the massive cost just shifted to the government's balance sheet, and society as well, which has become markedly more two tiered. We have created what is basically an enemy superpower, which is costly on many levels. The proof is in the pudding, just look at the state of the country and the government's balance sheet, since all the offshoring began, as well as our standing and influence in the world, which has substantially decayed. Things are markedly worse off on every measure.

Measuring everything by CPI cost alone (also understated) was a disaster. We missed a massive shift of cost from the corporations to what was basically hidden on the government's balance sheet. We have created an enemy superpower, which is also very costly, on many levels.

The full system cost of all of this has been completely ignored, but in this case, it has clearly not worked out as wine and cheese David Ricardo would have predicted.

AI is similar in this regard. Nvidia NVDA, the public company, gets all the benefit.

But the losses are massive, and likely greater than the money Nvidia is making, but they are just hidden in private companies losing money hand over fist (you can tell by the rates at which they need to raise capital and how much they are raising), and also the big public companies that put the expense onto the balance sheet and then depreciate it at an absurdly low rate.

Ergo, if you look at the economics of the whole system, they are not what people think they are, because the substantial costs/losses are hidden. It is the same for the consumers of the product. If it was priced at a point where the service and infrastructure providers were earning an economic return, the math would be quite different for the consumers.

Finally I left out an important point in the initial squaring the circle section (above). If one believes companies will not be passing through supply chain price increases, one should be selling the stonks, because margins are about to take a big digger, and there are going to be substantial earnings downgrades.

But nobody is selling the stonks, because nobody believes price won’t be put through. Therefore, once again for the large portion of the population that are not beneficiaries of equity price appreciation, BOHICA. This one could be a stagflationary BOHICA, although it will never show up in the numbers.

Brief follow up. Interesting short video and text commentary in this tweet. Robots make the robots:

Two big takeaways:

* Notice, no humans anywhere in the factory. Shoes are out there because of wine and cheese, this stuff is not. There is an enormous amount of production that has moved to China that falls into this bucket.

* This happens to be a German company, with its production in China. It has now become wine and cheese for them. Obviously not because of lower cost labor. It is because the entire rest of the supply chain has moved there. What originally was not wine and cheese has now become wine and cheese, because the entire supply chain is there. Therefore, it is cheaper and faster to make things in China, when it really shouldn’t be, because labor is an immaterial part of the BOM for this stuff. A good example is drone manufacturing, where China now has near 100% market share. They shouldn’t. Go Pro, for example, tried, and failed bigly and quickly. Should have been easy for them too, they had all the camera expertise, scale, distribution, and the brand name. But the Chinese competitors had their entire engineering teams in China, and since the supply chain is in China, they could rev new models in about 1/5th of the time it would take Go Pro. Therefore, Go Pro could never keep up and was always a cycle or two behind.

This, in general (well beyond just drones), is now a huge problem to solve for. Not only is it broadly a national security problem, but we handed them a comparative advantage they should not have, by moving the near entirety of the supply chain over there, including the non-labor based components, due to all sorts of short-sighted and accounting based reasons (taxes, etc.) and their ability to operate in ways not considered legal anywhere else (chemical pollution, etc).

BY Doug Kass · Aug 18, 2025, 9:30 AM EDT

BY Doug Kass · Aug 18, 2025, 9:20 AM EDT

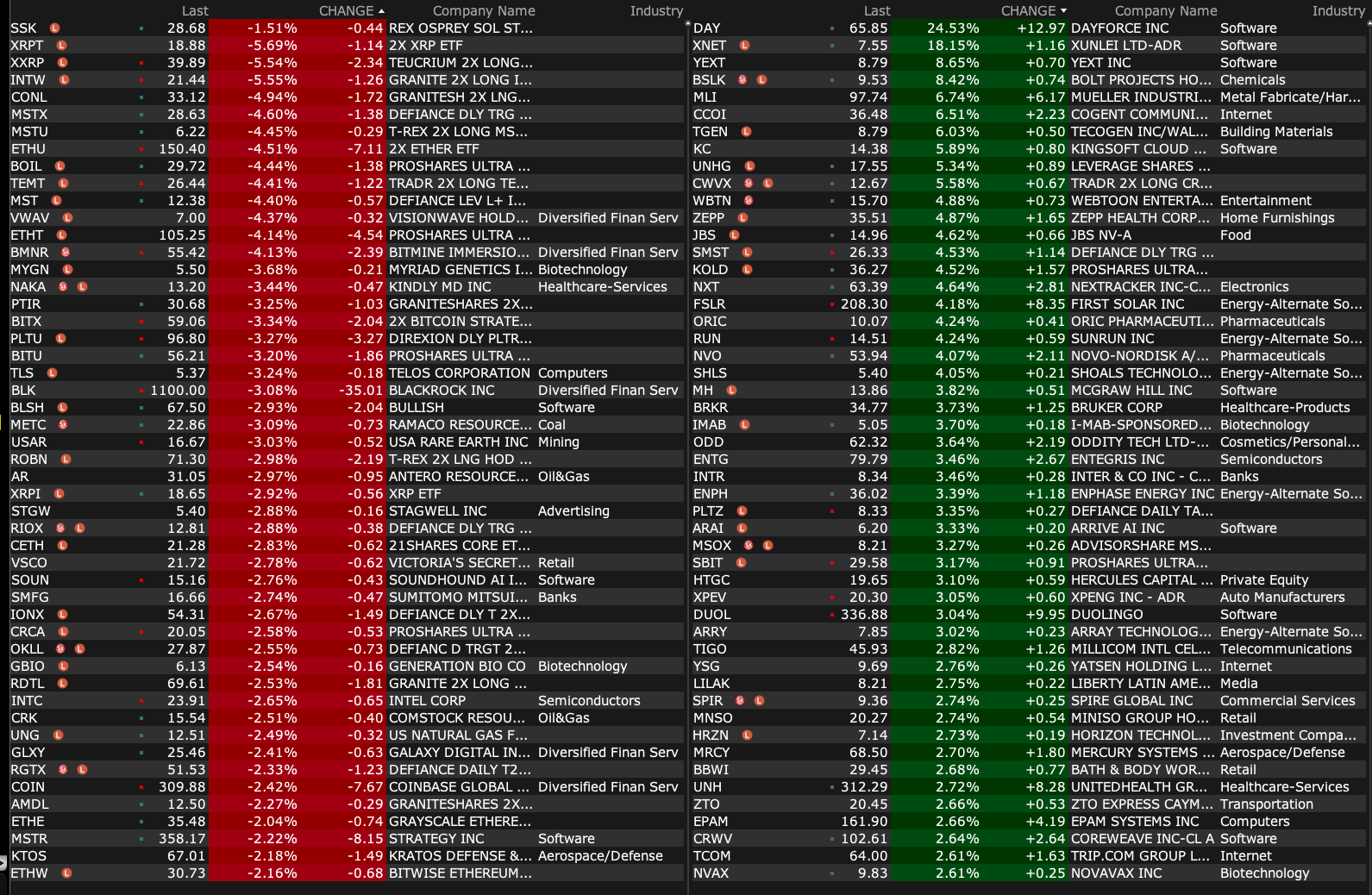

-SNGX +44% (confirms FDA Grants Soligenix Orphan Drug Designation for the Treatment of Behçet's Disease after Reviewing Recent Phase 2 Clinical Study Results)

-BTAI +26% (announces Positive FDA Pre-sNDA Meeting Comments for sNDA Submission for BXCL501 in Agitation Associated with Bipolar Disorders or Schizophrenia)

-DAY +24% (Thoma Bravo said to be in talks to acquire the company; potential terms not disclosed)

-SHCO +16% (agrees to be taken private at $9.00/shr for Implied EV of $2.7B with investor group led by MCR and its Chairman and CEO Tyler Morse; Appoints Neil Thomson as CFO, effective immediately)

-LIXT +11% (reports on new findings published in Scientific Journal Nature that validate ongoing clinical trials with LB-100 and launches new pre-clinical study)

-WULF +11% (Google increases backstop to $3.2B and stake in TeraWulf to 14% from 8% announced last week)

-YEXT +8.7% (CEO Walrath submits proposal to acquire company at $9.00/shr for value $1.1B)

-CUPR +7.1% (reaffirms commitment to shareholders and patients following recent stock market activity; remains on track with its operational and regulatory milestones)

-TNXP +6.7% (momentum following US FDA approval Tonmya (cyclobenzaprine HCl sublingual tablets) for treatment of Fibromyalgia)

-CCOI +6.5% (Wells Fargo Raised CCOI to Overweight from Underweight, price target: $45)

-JBS +4.7% (positive mention in Barron’s)

-RUN +4.4% (RBC Raised RUN to Outperform from Sector Perform, price target: $16)

-NVO +3.7% (Wegovy approved in the US for the treatment of MASH; receives US FDA NDA Supplemental 24 approval for Wegovy)

-ENTG +3.5% (momentum)

-UNH +2.7% (momentum)

-BDRX +2.3% (first patients enrolled into Pivotal Phase 3 Serenta Trial in Familial Adenomatous Polyposis)

-TPIC -54% (downside momentum)

-EMPD -13% (secures $25M credit facility funding share repurchases; discloses BTC holdings)

-NNE -4.2% (hearing Ladenburg Thalmann Cuts NNE to Sell from Buy, price target: $9)

-MDGL -4.0% (weakness following FDA approval of NVO’s Wegovy for MASH)

-VVPR -4.0% (announces Tembo e-LV Subsidiary on Track for Investment from Energi Holdings at EV of $200M via SPAC Transaction)

-BMNR -3.7% (discloses crypto holdings)

BY Doug Kass · Aug 18, 2025, 9:05 AM EDT

BY Doug Kass · Aug 18, 2025, 8:55 AM EDT

BY Doug Kass · Aug 18, 2025, 8:38 AM EDT

11:30 a.m.: Federal Reserve Board of Governors Meeting: Review and determination by the Board of Governors of the advance and discount rates to be charged by the Federal Reserve Banks.

11:30 a.m.: Treasury hosts a $82B 3 and $73B 6-Month Bill Auction

BY Doug Kass · Aug 18, 2025, 8:20 AM EDT

* Susan cites numerous technical divergences that exist today...

“Remember, Susan, let someone else have the first 10% and let someone else have the last 10%. You take the 80% in the middle.”- FG

When I was at Putnam in Boston, Stanley Berge was a revered technical source for Marty Hale and Jerry "The Chief" Jordan. (Merrill Lynch's Bob Farrell and (in-house technician) Wally Deemer were the other notable technical sources used by Putnam's two aggressive growth managers).

When Stan passed on, his daughter Susan ably took over the reins of "The Berge Report."

Susan is bearish and sees the Primary Trend of both the NYSE and Nasdaq as bearish.

Here are some of her more salient and recent (Friday) observations:

NYSE Primary Trend

* One non-technical indicator we follow is the year-to-year percent change in the 4-week moving average of 30-year government bond yields.... When it rises above 15%, as it did last week, it adds a negative point to the NYSE PTI. If there is little or no accumulation of bearish technical evidence at the time this indicator rises above 15%, a bearish ranking has little impact on the level of the NYSE PTI.

* The DJIA tried to make a new closing high on Friday but closed below both its all-time high on 12/4 (45014.04) and its recovery high on 7/23 (45010.29). If it were to close in new high ground in coming days/weeks, the NYSE PTI would likely lose additional points.

* Interestingly, while the DJIA closed up on Friday, nothing else did. The Nasdaq averages, S&P 500 and the NYA all closed down on the day. The breadth was also negative – there were 430 more stocks down than up. This has been the longest period of distribution of stock under cover of strength in the averages since 1976.

* No matter how high some market measures go or how many new highs the S&P 500 makes, underlying technical indicators maintain their negative divergences. They are either making lower highs or actually declining in spite of new highs in some of the averages.

NYSE Intermediate Trend

* Had the DJIA closed in new high ground on Friday, the NYSE ITI would have lost additional points. If the DJIA does manage to close above either its July high or its December 2024 high or both, the NYSE ITI would likely drop to -10. The distribution of stock under cover of strength in the averages is evident not only in breadth-related indicators.

* One indicator we follow is a 30day oscillator based on up and down volume on the NYSE. In late May, it peaked at 16.9. A level above 15 is evidence that the market is very overbought. On Friday, with the DJIA very close to making a new high, this 30day oscillator was .7.

* It is very unlikely that new highs in the DJIA in the near term will be accompanied by a new high in this indicator. What is absolutely amazing is that last September it peaked at 19.0. And yet, here we are. Every other measure of the market except the DJIA has made a series of new highs this year and this indicator hasn’t confirmed a single one.

NASDAQ Primary Trend

* The Nasdaq averages are in a world of their own. While the Nasdaq averages made new highs again last week, they closed down on Thursday and Friday, looking tired. The NDX is up 39.5% and the Nasdaq Composite Index has gained 42.2% in a little more than 4 months. And yet, not once throughout this extraordinary rally has the 200day moving sum of advances-declines on the Nasdaq market risen above zero.

* There isn’t a single indicator we follow related to the Nasdaq market that is making new highs along with the averages. Some remain so weak, like 200day A-D, that they haven’t risen above zero even though the Nasdaq averages made new all-time highs again last week. Breadth-related indicators are lagging. Up vs. down volume indicators are lagging. Momentum indicators are lagging. The number of stocks making new highs is lagging. The number of stocks making new lows is rising.

* Intermediate-term buying momentum has been falling since early July. Intermediate-term selling pressure has been rising for the past four weeks. It’s hard to identify what is holding this market together, much less driving the averages to new all-time highs.

* There is absolutely no fear, or even concern, that the Nasdaq averages might be overbought and over-extended. The 10day TRIN ratio for the Nasdaq market dropped to .69 on Friday, and the 25day moving average of the 10day TRIN dropped to .70.

General Market Comments

* With the market up so much since the April lows, especially the Nasdaq averages, and the lack of concern that the market might go down at some point, it seems to us that capital preservation rather than capital gains should be the focus of investor attention.

* Back in the 1960s and 1970s when classic major bear markets were much more frequent than they have been since 2000, investors were familiar with the idea that not losing money in a bear market was just as important as making money in a bull market. Because classic bear markets have become few and far between, people don’t worry much about them anymore. When I started in this business in 1976, there was man, F.G., who used to poke his head in the door now and then and say, “Remember, Susan, let someone else have the first 10% and let someone else have the last 10%. You take the 80% in the middle.” Wise advice.

* From what we see from a technical viewpoint, the averages are way overbought and way overextended, and the market underneath the averages has already topped out. It is only a matter of time before the averages do the same. When a major bear market begins, we usually do not know why it happens until it is well underway. Hence the old Wall Street saying, “Bad news makes bottoms. Good news makes tops.”

BY Doug Kass · Aug 18, 2025, 6:52 AM EDT

Bonus — Here are some great links:

More Bears Than Bulls at Record Highs

BY Doug Kass · Aug 18, 2025, 6:20 AM EDT

A reminder, late Friday afternoon I began to reshort some high-octane, high-beta names.

Back short (PLTR) , (ARKK) , (HOOD) and (NVDA) .

Position: Short PLTR (VS), NVDA (VS), ARKK (VS), HOOD (VS)

By Doug Kass Aug 15, 2025 3:05 PM EDT

BY Doug Kass · Aug 18, 2025, 6:10 AM EDT

The S&P Short Range Oscillator stands at 3.31% vs. 3.02% — that's overbought.

BY Doug Kass · Aug 18, 2025, 5:55 AM EDT

Add to index shorts:

* SPY $644.65

* QQQ $578.67

BY Doug Kass · Aug 18, 2025, 5:46 AM EDT

If something like this is not "papered" it isn't really a deal. My two cents 3/3 ft.com/content/c1183b…